In‑depth explainer on Berachain, an EVM‑identical Layer 1 using Proof‑of‑Liquidity to align security with DeFi liquidity, covering its architecture, tokenomics, ecosystem, performance, risks, and role in the multichain landscape.

+2 sources across the wider coverage universe

Berachain liquid staking protocol infrared raises funds from Binance Labs in private token round.2024-06

Berachain liquid staking protocol infrared raises funds from Binance Labs in private token round.2024-06 Berachain announces 15.75% BERA airdrop for community, apps, and liquidity providers ahead of token launch.2025-02

Berachain announces 15.75% BERA airdrop for community, apps, and liquidity providers ahead of token launch.2025-02 Bera’s just getting started. Deposit into yBERA, yHONEY, or BOLLAR to max out your BOINTS. Bearn is Yearn on Berachain. Start now!2025-05

Bera’s just getting started. Deposit into yBERA, yHONEY, or BOLLAR to max out your BOINTS. Bearn is Yearn on Berachain. Start now!2025-05 Leaked documents show Berachain gave Brevan Howard’s Nova Digital fund a rare $25M refund right letting the VC reclaim its entire Series B investment a year after the TGE, effectively eliminating downside risk.2025-11

Leaked documents show Berachain gave Brevan Howard’s Nova Digital fund a rare $25M refund right letting the VC reclaim its entire Series B investment a year after the TGE, effectively eliminating downside risk.2025-11 Interview with Berachain co-founder. Evolving from an NFT community to Layer 1 and building a positive flywheel effect.2024-07

Interview with Berachain co-founder. Evolving from an NFT community to Layer 1 and building a positive flywheel effect.2024-07 Berachain sees $1.6B pre-launch liquidity surge, would technically making it the 10th largest chain by TVL.2025-01

Berachain sees $1.6B pre-launch liquidity surge, would technically making it the 10th largest chain by TVL.2025-01

Berachain: An Evergreen Guide to the Proof‑of‑Liquidity Layer 1

Berachain is a high‑performance, EVM‑identical Layer 1 blockchain built around a novel Proof‑of‑Liquidity (PoL) consensus mechanism designed to align network security with on‑chain liquidity and DeFi activity. Since its mainnet launch in early 2025, the chain has become a test case for whether deep incentives, real‑time UX, and purpose‑built DeFi primitives can create a more sustainable liquidity ecosystem than traditional proof‑of‑stake chains, even as it has faced sharp boom‑and‑bust cycles, security‑driven chain halts, and controversy around investor terms and decentralization.

1. Berachain in Context

Any attempt to understand Berachain begins with the broader evolution of smart contract platforms. First‑generation networks like Ethereum established the programmable base for decentralized finance, but their general‑purpose designs left key pieces of the liquidity stack to be solved at the application layer, often through aggressive and short‑lived liquidity mining schemes. Berachain emerges from a different thesis: that a blockchain can be optimized from the ground up for capital efficiency, DeFi throughput, and incentive alignment by integrating liquidity directly into its consensus and reward mechanisms. In other words, instead of viewing DeFi as an emergent use case on a neutral platform, Berachain attempts to make DeFi the organizing principle of the chain’s economics and governance.

At a technical level, Berachain brands itself as an EVM‑identical Layer 1, meaning it aims to replicate the Ethereum Virtual Machine environment so closely that the same bytecode, tooling, and developer workflows can be used without modification. This is a stronger claim than mere EVM compatibility: in principle, contracts deployed on Ethereum or Arbitrum should be portable to Berachain with minimal or no code changes, allowing existing DeFi protocols to extend into the Berachain ecosystem with reduced engineering overhead. For developers and users, that promise is crucial because it lowers switching costs and allows Berachain to plug into the wider Ethereum tooling universe, from wallets to development frameworks.

Where Berachain departs most sharply from incumbent chains is its adoption of Proof‑of‑Liquidity as the core economic coordination mechanism. In conventional proof‑of‑stake systems, staked capital is largely idle apart from securing the network and earning inflationary rewards; liquidity for DeFi venues must be sourced separately and is often rented through short‑term yield incentives. Berachain’s PoL design instead attempts to turn network emissions into “productive liquidity, application growth, and ecosystem value,” as its documentation puts it, by rewarding capital that simultaneously contributes to security and deepens on‑chain liquidity. This is packaged as a way to make emissions less wasteful and to internalize some of the costs that DeFi protocols typically bear alone.

From a narrative standpoint, Berachain has positioned itself at the intersection of three trends: the multichain DeFi explosion, the search for real‑time low‑latency blockchains, and the professionalization of crypto infrastructure backed by large venture and corporate treasuries. The project has raised significant capital from major digital asset investors, cultivated an ecosystem of derivatives, lending, and yield protocols, and pursued partnerships with infrastructure providers and centralized exchanges. At the same time, it has been tested by a steep post‑launch drawdown in token price and total value locked, an emergency chain halt in response to a large Balancer exploit, and scrutiny over investor protections granted to a key venture backer.

This guide situates Berachain within that evolving landscape. It traces the project’s origins and funding story, explains the architecture and mechanics of Proof‑of‑Liquidity, unpacks its tokenomics and native assets, surveys the DeFi ecosystem building on the chain, and analyzes its performance, security posture, and role in the wider multichain environment. Along the way, it integrates recent developments such as the proposal for a 200‑millisecond preconfirmation layer, the network’s handling of cross‑chain security incidents, and the dynamics of “mercenary capital” that have shaped its TVL cycles. The goal is not to promote or dismiss Berachain, but to provide a durable, technically grounded reference for readers tracking its trajectory in the coming years.

Berachain co-founder pushes back against “incomplete and inaccurate” allegations, saying the hit piece relied on disgruntled ex-employees and misrepresented Brevan Howard’s terms, while reaffirming Nova remains one of the project’s largest and most supportive tokenholders.

"- Brevan Howard co-led our Series B a year ago, out of their Abu Dhabi office, via Nova, a new liquid-only vehicle on the same terms as all other investors. Nova had approached Berachain to lead the round some months prior to this. - In contrast to everything implied in this piece, Nova is still one of, if not THE, largest tokenholder in Berachain. They are a liquidity provider, a holder of both LOCKED BERA acquired in the Series B, and liquid BERA purchased on the open markets, and have continued to be supportive through highs and lows. If anything, they have increased their BERA exposure over time, despite running a liquid fund in a harsh alt environment."

Readers click Berachain stories for proof that the Proof-of-Liquidity flywheel is real—but the second-highest engagement cluster is on the exits and side-deals (Brevan Howard refund, TVL collapse) that suggest sophisticated capital never believed in the flywheel at all.↗

2. Origins, Launch, and Funding Story

2.1 From Testnet to Mainnet

Berachain’s journey from concept to mainnet fits into a broader wave of alternative Layer 1s that sought to differentiate not merely on throughput, but on novel economic designs tailored to DeFi. Early public materials emphasized that the chain would marry a Cosmos‑style consensus and networking stack with an EVM‑identical execution environment, effectively combining Ethereum‑like smart contract semantics with Tendermint‑derived finality and cross‑chain potential. During its testnet phases, Berachain’s team used incentive programs and partnerships to attract DeFi builders, signaling that liquidity providers and protocol teams would be first‑class citizens in its PoL‑driven economy rather than peripheral users.

The transition to mainnet crystallized that thesis. On February 6, 2025, Berachain launched its mainnet as an EVM‑compatible Layer 1 blockchain, with public coverage highlighting its focus on enhancing liquidity and user engagement through PoL and a native DeFi stack. The launch positioned Berachain not as a niche sidechain but as a base settlement layer competing for developers with Ethereum mainnet, rollups like Arbitrum, and other general‑purpose L1s. Early messaging framed the chain as a “home for DeFi,” with stablecoins, perps, and credit markets slated as pillar applications.

The mainnet debut also set the stage for Berachain’s initial TVL growth and ecosystem build‑out. Liquidity mining campaigns, airdrop speculation, and partnerships with DeFi protocols helped bootstrap activity, while the project’s close alignment with established crypto funds and infrastructure providers lent it institutional credibility. Yet, as later sections will explore, this rapid acceleration brought its own set of challenges, including intense competition for sticky liquidity and exposure to cross‑chain security incidents that would test the project’s governance and social consensus.

2.2 Fundraising, Backers, and Treasury Design

A core aspect of Berachain’s story is its ability to raise substantial capital from prominent investors and to structure that capital as an on‑chain treasury aligned with the Protocol’s long‑term goals. Public filings and announcements connected to a transaction involving Greenlane Holdings, a NASDAQ‑listed company, reveal that Berachain raised approximately $150 million from a syndicate including Brevan Howard Digital’s Nova fund, Framework Ventures, Polychain Capital, and Samsung Next, among others. The same materials indicate that Greenlane planned to use BERA, Berachain’s native token, as a primary reserve asset in its corporate treasury, effectively tying a traditional company’s balance sheet to the success of the chain.

This fundraising structure underscores how Berachain straddles the line between grassroots crypto network and institutionally backed infrastructure project. On the one hand, the treasury gives it resources to fund ecosystem grants, incentives, and core development well beyond what many fledgling chains can afford. On the other hand, it ties Berachain’s governance and token distribution to the interests of large, sophisticated investors whose risk preferences and time horizons may diverge from those of retail participants. The presence of funds like Polychain and Brevan Howard also signals that professional allocators view PoL and EVM‑identical Cosmos‑based chains as investable experiments in the evolution of DeFi infrastructure.

The treasury’s design is intertwined with Berachain’s tokenomics and PoL emissions, since inflationary rewards, strategic allocations, and liquidity programs all interact with the chain’s ability to secure itself and to retain capital. The BERA token documentation notes a fixed genesis supply of 500 million BERA, with annual inflation of roughly 5% delivered as wrapped BERA (WBERA) via PoL reward emissions, subject to governance decisions. That combination of a large initial float, moderate inflation, and investor allocations subject to cliffs and vesting schedules means that both the treasury and private backers play an outsized role in shaping circulating supply and market dynamics, particularly in the early years after launch.

2.3 Investor Terms and the Nova Digital Refund Controversy

Berachain’s fundraising has not been free of controversy. Investigative reporting by Unchained Crypto, based on leaked documents, revealed that Brevan Howard’s Nova Digital fund negotiated a $25 million refund right in connection with its Series B investment in Berachain. According to those documents, Nova had the option to demand the return of its entire $25 million investment in cash within a year of the token generation event (TGE), effectively eliminating downside risk on that tranche of capital. In a venture context where investors typically accept illiquidity and the possibility of total loss in exchange for upside, such a clause stood out as unusually favorable.

The existence of this refund right raised questions about asymmetry between institutional and retail stakeholders. If one of the largest and most influential backers could exit at par within a year, while public token holders bore full market volatility and drawdown risk, critics argued that the playing field was tilted. It also led to speculation about how much influence Nova and similar funds might have over Berachain’s strategic decisions, particularly during periods of market stress or governance contention. The optics were sensitive enough that Berachain’s co‑founder publicly pushed back against the report in subsequent coverage, characterizing parts of it as incomplete or based on disgruntled former employees, while emphasizing that Nova remained one of the project’s largest and most supportive tokenholders.

Regardless of where one falls in that debate, the episode highlights an important structural reality: Berachain is both a public blockchain and a heavily capitalized startup, and the contracts it signs with early backers can materially affect perceptions of fairness and decentralization. That reality is not unique to Berachain—many L1s and rollups have complex investor protections—but it takes on added significance in a network that markets itself as a new model for aligning incentives among validators, liquidity providers, and DeFi protocols. As we turn to the technical architecture, it is worth keeping in mind that PoL’s promise of coordination exists atop a social and financial substrate shaped by private negotiations.

3. Architecture and Proof‑of‑Liquidity Consensus

3.1 EVM‑Identical Execution on a Modular Base

At the heart of Berachain’s architecture is the claim of being EVM‑identical, rather than merely EVM‑compatible. In practice, this means the chain aims to reproduce Ethereum’s execution environment, including its opcodes, gas semantics, and contract behavior, so that Solidity and Vyper contracts compiled for Ethereum can be deployed on Berachain without modification. This is a stronger form of compatibility than many EVM‑like chains that tweak gas costs, precompiles, or state management in ways that may subtly break assumptions embedded in existing smart contracts. For developers, EVM‑identicality is especially appealing because it reduces the risk of unpredictable behavior when porting audited contracts and allows existing testing suites and infrastructure to be reused.

To deliver this environment, Berachain uses a modular stack where consensus and networking are decoupled from execution. Public materials describe it as an EVM‑identical Layer 1, implying that the base consensus protocol is not Ethereum’s proof‑of‑stake but a different engine, with the EVM sitting as a state machine atop it. In earlier iterations, Berachain’s architecture was described as leveraging a Cosmos SDK‑style framework with a custom EVM implementation, although the specific components may evolve over time. What matters conceptually is that execution is Ethereum‑like while the underlying consensus layer is free to adopt innovations such as Proof‑of‑Liquidity, preconfirmation layers, and chain‑specific governance.

This modularity allows Berachain to experiment in areas where Ethereum is more conservative, such as transaction inclusion times and validator reward structures. Plans for a preconfirmation layer that can deliver transaction inclusion in approximately 200 milliseconds, down from a baseline of around two seconds, are a prime example. Because the EVM execution layer is abstracted from the consensus machinery, Berachain can potentially add fast preconfirmations without breaking contract execution semantics, at least in theory. The challenge, as always, is ensuring that such architectural complexity does not introduce new centralization vectors or attack surfaces.

3.2 What Proof‑of‑Liquidity Aims to Solve

Proof‑of‑Liquidity sits at the center of Berachain’s differentiating thesis. The project’s documentation describes PoL as an economic coordination system that redirects network emission into productive liquidity, application growth, and ecosystem value, rather than into idle stake or short‑term yield‑farming that quickly flees to the next high‑APR venue. The core idea is that the same capital that secures the network should also be the capital that provides liquidity for its DeFi applications, so that emissions do double duty rather than being split between security and liquidity mining.

In conventional proof‑of‑stake systems, validators and delegators lock tokens in staking contracts where they cannot be directly used as liquidity in AMMs, lending protocols, or derivatives venues. DeFi protocols therefore must “rent” liquidity through their own token incentives, often paying high yields to attract capital that will depart as soon as subsidies decline. Under PoL, Berachain attempts to internalize some of that cost by rewarding liquidity provision and protocol engagement within the consensus mechanism itself. Conceptually, a validator that attracts more economically useful liquidity—such as LP positions in core DEX pools—should be rewarded in both governance influence and emissions.

By tying validator weight and reward eligibility to measures of liquidity contribution, PoL aspires to align the incentives of validators, DeFi protocols, and liquidity providers. In an ideal steady state, the chain’s most important applications would enjoy deep, sticky liquidity because that liquidity is not only earning trading fees or lending interest, but also securing the network and capturing a share of inflationary rewards. That, in turn, could make Berachain more attractive for sophisticated DeFi strategies, derivatives, and structured products that rely on low slippage and robust collateral markets.

3.3 How Proof‑of‑Liquidity Works in Practice

While exact implementation details may evolve, a widely discussed conceptual model for Berachain’s PoL involves multiple interlocking tokens and roles. The BERA token serves as the native gas and staking asset, used to pay transaction fees and to participate in validator selection. A separate governance‑oriented token, often referred to as a “Berachain Governance Token” (BGT) in earlier designs, is envisioned as being earned by providing liquidity to certain whitelisted pools or by otherwise contributing to on‑chain economic activity. Liquidity providers receive governance weight over how PoL emissions are directed, creating a feedback loop between app usage, governance, and validator rewards.

In this model, liquidity providers deposit assets into designated pools on native DEXs or other core DeFi protocols. In return, they may receive LP tokens and accrue governance points or tokens that can be used to vote for particular validators or gauge emission rates to specific pools. Validators, for their part, accumulate stake not only from direct BERA delegations but also from the governance influence wielded by liquidity providers who choose to support them. PoL reward emissions, denominated as wrapped BERA (WBERA), are then distributed according to this combined picture of stake and liquidity contribution. The result is a more complex, but potentially more expressive, mapping from economic activity to consensus power.

A simple way to think about this is that Berachain’s consensus attempts to answer two questions simultaneously: who should propose and validate blocks, and which economic activities should be subsidized by inflation? On a pure PoS chain, the first question is determined by token stake, and the second is left to application‑level incentives. On Berachain, PoL tries to blend them so that validators representing more productive liquidity ecosystems receive more rewards, while protocols that can mobilize engaged communities of LPs gain more say over the direction of emissions. This design is reminiscent of “governance‑mining” models seen in DeFi, but applied to the base consensus layer.

3.4 Comparing PoL with Proof‑of‑Stake and Liquidity Mining

To evaluate PoL, it is useful to contrast it with the two dominant paradigms it seeks to improve on: proof‑of‑stake and application‑level liquidity mining. Traditional PoS focuses on capital at stake as the primary input to security: validators with more stake have more to lose from misbehavior and gain more from honest participation. Liquidity mining, by contrast, focuses on capital deployed into specific protocols, rewarding users who contribute to trading pools, lending markets, or yield strategies. Berachain’s PoL effectively says that in a DeFi‑centric chain, capital that is both at stake and deployed in economically relevant ways should sit at the apex of the reward hierarchy.

One potential advantage of this approach is the reduction of “wasteful” emissions. Instead of protocols minting their own tokens to attract liquidity, only to see those tokens crash once incentives dry up, PoL offers a shared emissions pool that can be directed toward whichever combinations of protocols and validators the ecosystem deems most beneficial. This could, in theory, lead to more sustainable APRs and a more measured growth of TVL, since rewards flow to liquidity that the collective governance has deemed strategically important rather than to whichever protocol can raise the most short‑term hype.

However, PoL also inherits and amplifies some of the coordination challenges seen in both PoS and DeFi governance. Concentrated token holders, including funds and core team allocations, may exert significant influence over emission direction, especially in the early stages when community distribution is still maturing. Liquidity providers may also be tempted to engage in rent‑seeking governance behaviors, directing emissions to pools that benefit them personally rather than those that maximize long‑term ecosystem health. In this sense, PoL does not eliminate the tension between private and public incentives; it simply relocates that tension to the base layer.

3.5 Limitations and Open Questions

The true test of PoL is empirical, and Berachain’s first year of mainnet operation has already provided mixed evidence. On the one hand, the chain quickly attracted billions of dollars in TVL at its peak, suggesting that its liquidity‑centric design and ecosystem incentives resonated with sophisticated DeFi users and protocols. On the other hand, that TVL later collapsed from a reported peak of around \$3.35 billion to roughly \$393 million, an 88% decline, alongside a price drawdown of over 90% in the BERA token from its all‑time high. Such volatility suggests that PoL has not yet insulated Berachain from the classic boom‑and‑bust dynamics of liquidity mining, at least in its early stages.

Several open questions arise from this experience. One is whether PoL can produce stickier liquidity once the most speculative capital has churned through, or whether the system will remain dependent on attractive emissions to keep TVL anchored. Another is how governance will evolve as more of the token supply vests and distributes beyond early investors and insiders. The existence of investor protections like Nova Digital’s refund right complicates perceptions of fairness and may influence how smaller stakeholders view their role in PoL governance. A third question concerns security: because PoL intertwines consensus with DeFi positions, systemic shocks such as a large exploit or sudden unwind of collateral could have cascading effects on validator economics.

Ultimately, Proof‑of‑Liquidity should be seen as a bold but still experimental attempt to embed DeFi into the very fabric of a blockchain’s economic design. Its long‑term viability will depend on whether Berachain can calibrate emissions, governance, and validator incentives in ways that weather market cycles, security events, and cross‑chain stresses without frequent recourse to ad‑hoc interventions. The next sections examine how the chain’s tokens, DeFi stack, and performance features interact with that ambition.

4. Native Assets, Tokenomics, and Economic Design

4.1 The BERA Token

The BERA token is the foundational asset of the Berachain ecosystem. According to the project’s official documentation, BERA functions as both the native gas token used to pay for transactions and smart contract execution, and the staking token that validators and delegators lock to secure the network under PoL. Its dual role mirrors the design of many proof‑of‑stake chains, but with the added twist that staking economics are mediated through the PoL apparatus rather than through a pure stake‑weight model. As such, BERA’s value is tied not only to usage demand and speculative interest, but also to its utility as collateral in liquidity provisioning and as a key input to validator selection.

Token supply and issuance are crucial for understanding BERA’s long‑term inflation dynamics. At genesis, Berachain’s documentation reports a total supply of 500 million BERA, distributed across categories such as the community, core contributors, ecosystem development, and investors. On top of that fixed genesis supply, BERA is subject to ongoing inflation of approximately 5% annually, delivered via Proof‑of‑Liquidity reward emissions as WBERA, with parameters subject to on‑chain governance. This means the effective supply of circulating BERA can grow over time, particularly if governance chooses not to taper emissions as the network matures.

Vesting mechanics further shape the token’s supply curve. All allocated categories—such as team, investors, and ecosystem funds—share the same vesting terms: a one‑year cliff during which no tokens unlock, followed by an initial unlock of one‑sixth of the allocation after the cliff, and then linear vesting of the remaining five‑sixths over twenty‑four months. In practice, this means that the second and third years after mainnet launch see substantial increases in circulating supply as locked tokens vest, which can exert selling pressure if market demand does not keep pace. Combined with PoL inflation, these schedules create a complex interplay between dilution, reward yields, and the incentive to hold versus farm and sell.

4.2 Governance and Incentive Tokens

Beyond BERA, Berachain’s economic design relies on governance‑linked incentive tokens that encode participation in the PoL economy. While naming and specifics can change over time, earlier designs outlined a non‑transferable governance token—often discussed as BGT—that would be minted to users who provide liquidity in designated pools or otherwise contribute to network activity. The core concept is that governance power is earned through economically useful behavior, not purchased outright on secondary markets, mitigating some of the plutocratic dynamics common in token voting systems.

These governance tokens serve several functions in the PoL system. First, they can be used to direct reward emissions: holders vote on which validators or liquidity pools should receive a larger share of WBERA issuance, creating a “gauge” system reminiscent of Curve’s veCRV mechanics but applied at the chain level. Second, governance tokens can influence protocol‑level parameters such as whitelisted collateral types, stablecoin risk settings, and credit allocation within Berachain’s native DeFi protocols. Third, they may function as a reputational signal, indicating which wallets and entities have historically contributed to the chain’s liquidity and activity.

However, the mere existence of governance tokens does not guarantee egalitarian outcomes. Concentration risk remains if early liquidity providers, sophisticated funds, or core team‑associated entities accumulate a disproportionate share of governance power by virtue of their capital and information advantages. The challenge for Berachain is to design issuance, lock‑up, and delegation mechanics that encourage broad participation while still rewarding those who provide meaningful, long‑term liquidity rather than short‑term mercenary flows. In this sense, governance tokenomics are as important as BERA’s supply schedule in determining whether PoL achieves its stated coordination goals.

4.3 Stablecoins and HONEY as a “Local Dollar”

Stablecoins are the lifeblood of DeFi, and Berachain has treated them as a first‑class concern from the outset. The project’s blog on “Stablecoins on Berachain” emphasizes the role of a native stable asset, often referred to as HONEY, in providing a resilient unit of account for the chain’s internal economy. HONEY is positioned as a decentralized, over‑collateralized stablecoin backed by on‑chain assets, distinct from centralized fiat‑backed stablecoins such as USDC or USDT that can be frozen or redeemed at the issuer’s discretion. In Berachain’s design, HONEY serves as a “local dollar” that can smooth disruptions when external stablecoins experience stress events.

The blog describes a scenario in which a centralized stablecoin “hiccups”—for example, due to regulatory action, a depeg, or technical issues—and explains how HONEY’s vault architecture can isolate the affected collateral, spread redemptions over time, and keep the broader “dollar economy” on Berachain functioning. Rather than forcing every DeFi protocol on the chain to deal with a suddenly illiquid or impaired stablecoin directly, the design channels that stress into specific vaults and redemption flows, limiting contagion. This is conceptually similar to isolated lending markets or tranching structures that quarantine toxic assets, but applied to the stablecoin layer.

In practice, the success of HONEY hinges on several factors: the quality and liquidity of its collateral, the robustness of its liquidation mechanisms, and user confidence in its peg during volatile conditions. Competition from bridged and native stablecoins complicates this picture, as does the risk of governance capture over risk parameters. Nonetheless, the existence of HONEY as a native, PoL‑aligned stablecoin is an important pillar of Berachain’s economic design, especially when viewed in conjunction with its credit and lending primitives.

4.4 BEND: The Credit Layer of Berachain

To complement PoL and the stablecoin system, Berachain introduced BEND, described as the chain’s “credit layer.” BEND’s purpose is to give the capital stored in the network’s liquidity primitives a productive outlet by enabling lending, borrowing, and leveraged strategies that are tightly integrated with the PoL economy. Rather than leaving LP tokens and HONEY deposits idle or forcing users to move them to third‑party lending markets, BEND provides a native venue where these assets can be used as collateral to access credit.

Public materials explain that BEND “turns the network’s stored liquidity into a credit layer that allows users and builders to lend, borrow, and build on top of the capital already sitting in PoL‑aligned positions.” In concrete terms, this means that LP tokens from core DEX pools, HONEY positions, and possibly other PoL‑recognized assets can be pledged within BEND to obtain loans denominated in stablecoins or other tokens. Builders, in turn, can compose with BEND to create structured products, leveraged yield strategies, or risk‑managed vaults, knowing that the credit system is deeply integrated with Berachain’s consensus incentives.

From a systemic perspective, BEND amplifies both the benefits and the risks of PoL. On the positive side, it increases capital efficiency, allowing the same dollar of collateral to simultaneously back liquidity provision, secure the network, and fuel credit creation. On the negative side, it introduces additional leverage and complexity that can exacerbate shocks during stress events. If a major collateral type within BEND experiences a sharp drawdown or exploit, liquidations could cascade across liquidity pools and validator economics. Designing conservative risk parameters, robust liquidation bots, and circuit breakers becomes essential to preventing feedback loops that could threaten network stability.

4.5 Emissions, Vesting, and Supply Schedules in Market Context

Berachain’s tokenomics cannot be evaluated in isolation from market behavior. The chain’s first year illustrates how supply schedules and emission design interact with speculative cycles and “mercenary capital” dynamics. Despite the presence of cliffs and linear vesting for allocated BERA, public analysis has documented that Berachain’s TVL fell from around \$3.35 billion at peak to roughly \$393 million, an 88% decline, while the BERA token dropped more than 90% from a reported high of about \$2. These figures suggest that even with carefully staged unlocks, a significant portion of early liquidity was short‑term and highly sensitive to changes in incentives and sentiment.

Emissions via PoL also play a dual role. On the one hand, a roughly 5% annual inflation rate, directed toward productive liquidity, can provide attractive real yields that draw in participants and help secure the chain. On the other hand, if those emissions are rapidly farmed and sold, they can exert persistent downward pressure on the token price, especially in the absence of strong organic demand from users and long‑term holders. Governance has the latitude to adjust PoL emissions, but doing so involves trade‑offs between short‑term activity metrics and long‑term dilution.

Investor and team unlocks add another layer of complexity. As vesting cliffs expire and linear unlocks proceed, more BERA becomes available to entities that acquired tokens at low or zero cost. If these holders choose to exit or rebalance, the resulting sell pressure can coincide with declines in PoL yields or TVL, amplifying volatility. The reported refund right for Nova Digital, although specific to one investor and bound by time limits, contributes to a broader perception that some stakeholders may have more protection against downside than others. Over time, the way Berachain manages emissions, buybacks (if any), and treasury deployment will be critical in shaping its market profile.

Leaked documents show Berachain gave Brevan Howard’s Nova Digital fund a rare $25M refund right letting the VC reclaim its entire Series B investment a year after the TGE, effectively eliminating downside risk.

So it's more of a loan with option to aquire tokens if price is/was profitable.. NOt the worst deal for either party I guess. Free loan for Bera, risk free option for Brevan

- 01Proof-of-Liquidity mechanism viability↗

PoL is Berachain's core differentiator—readers wanted to understand whether BGT delegation through DeFi pools creates a durable flywheel or just a structured liquidity bribe.

- 02Bearn/Yearn yield product ecosystem↗

Multiple high-click headlines around yBERA, yHONEY, yBGT, and BOLLAR vaults show readers tracking concrete yield destinations, not just chain-level narratives.

- 03TVL surge versus mercenary capital flight↗

The arc from $1.6B pre-launch surge to $3.26B peak to 50% collapse framed the central question of whether PoL-incentivized liquidity is sticky or purely extractive.

- 04Brevan Howard refund and VC downside protection↗

Leaked documents showing a $25M Series B refund to Nova Digital exposed that insiders negotiated away the risk that retail holders could not—directly undercutting the community airdrop narrative.

- 05BERA airdrop and token launch mechanics↗

The 15.75% community allocation, pre-mainnet OTC price discovery at $8, and 500M total supply gave readers the inputs to calculate their own entry valuation before TGE.

- 06Centralization and network halt risk↗

Validators voting to halt the entire chain after the Balancer exploit raised a concrete governance failure mode that contradicted Berachain's decentralized positioning.

5. DeFi Ecosystem: From Liquidity Hubs to Yield Aggregators

5.1 Core Liquidity Infrastructure

Berachain’s design philosophy assumes that deep, composable liquidity will be both the engine and the beneficiary of its PoL consensus. At the base of this stack are decentralized exchanges and automated market makers that host pools for BERA, HONEY, major stablecoins, and blue‑chip assets bridged from other chains. While specific brand names and pool configurations shift over time, the recurring theme is that these venues are closely tied to PoL gauges and often considered “core” for emissions and governance purposes. This tight coupling between base‑layer incentives and DEX liquidity distinguishes Berachain from ecosystems where AMMs operate more independently of the chain’s security and reward mechanisms.

The connection between core liquidity infrastructure and network security became particularly salient during the Balancer exploit discussed later. Balancer’s V2 pools, or similarly structured sophisticated AMM designs, hosted large amounts of liquidity on multiple chains, including Berachain. When an exploit siphoned approximately \$116 million from Balancer V2 pools across chains, Berachain’s response—coordinating a validator vote to halt the network for an emergency hard fork—highlighted how deeply its DeFi layer is intertwined with its consensus and governance processes. In such an environment, core AMMs are not just applications; they are systemic infrastructure whose failures can trigger chain‑wide interventions.

5.2 Kodiak: Perpetuals, Aggregation, and Cross‑Chain Trading

Among the protocols that have embraced Berachain as a home base, Kodiak Finance stands out for its dual focus on perpetual derivatives and trade aggregation. Documentation describes Kodiak as a platform that offers a “Super Aggregator” called kX, an advanced swap aggregator and API that automatically searches for the best route to execute swaps across available liquidity, whether or not the route uses Kodiak’s own liquidity pools. By routing order flow intelligently, kX aims to improve execution quality for users and integrators while helping to unify fragmented liquidity on Berachain.

Kodiak has also launched a native perpetual exchange on Berachain, with early seasons of its perps product accompanied by trading competitions and reward campaigns targeting the chain’s growing community of derivatives traders. Coverage from social channels notes that “Season 2” of Kodiak Perps concluded with xKDK rewards ready to be claimed by eligible traders, underscoring how the protocol uses token incentives and gamified events to bootstrap activity. Separate media coverage has depicted Berachain as a “native liquidity hub” whose “bears” bring their best traders to perps competitions with tens of thousands of dollars in rewards, reflecting the cultural branding around the chain’s bear motif.

Kodiak’s positioning also illustrates Berachain’s multichain aspirations. Other coverage notes that assets like Solana have become tradable on Berachain via bridges such as Wormhole, with Kodiak providing the trading venue for these wrapped assets. By offering preconfirmation‑friendly perps and deep spot liquidity for bridged tokens, Kodiak sits at the intersection of Berachain’s PoL‑driven liquidity base and its race toward sub‑second transaction inclusion. The protocol’s success depends not only on its own risk management and product design, but also on the security of bridges, the stability of PoL incentives, and the performance characteristics of the underlying chain.

5.3 Bearn and Yearn‑Style Yield Strategies

If Kodiak represents Berachain’s derivatives face, Bearn represents its yield‑optimization and “DeFi blue chip” side. Social posts describe Bearn as a “Yearn on Berachain” product, and other coverage identifies it as a sub‑DAO of Yearn Finance that has chosen Berachain as one of its deployment targets. Bearn offers vaults such as yBERA, yHONEY, and BOLLAR, which are designed to optimize yields by allocating user deposits across lending markets, liquidity pools, and other strategies within the Berachain ecosystem. These vaults often use the ERC‑4626 standard, which standardizes tokenized vaults and improves composability, making them attractive building blocks for other protocols.

One notable example is yHONEY, which has been described in coverage as an ERC‑4626 vault that optimizes HONEY deposits across lending markets on Berachain. Rather than forcing users to constantly move their HONEY between different platforms to chase the best yield, yHONEY automates that process while abstracting away complexity. In this sense, Bearn operates as a meta‑layer that sits atop Berachain’s PoL infrastructure, HONEY stablecoin system, and credit layer, offering curated access to yield opportunities for both retail and institutional users.

The presence of a Yearn‑affiliated product on Berachain is significant for two reasons. First, it signals that established Ethereum‑native DeFi teams are willing to deploy on EVM‑identical alternative Layer 1s when they see compelling economic and technical reasons. Second, it increases the complexity of Berachain’s liquidity topology: as Bearn vaults aggregate positions in BEND, AMMs, and other protocols, they become systemically important actors whose strategies and risk management decisions can influence the health of the broader ecosystem. PoL emissions directed toward pools or markets heavily used by Bearn may have outsized effects on yield dynamics and capital flows.

5.4 Boyco, Incentives, and the Points Meta

Beyond traditional DeFi primitives, Berachain has embraced the contemporary “points meta,” in which users earn non‑transferable points for on‑chain activity that may later translate into token airdrops or governance rights. Boyco is a key piece of this incentive infrastructure. Social announcements from the official Berachain account have highlighted the launch of Boyco claims, a portal where users can connect their wallets to view positions and claim rewards across Berachain protocols. By aggregating and standardizing the distribution of incentives, Boyco reduces friction for users and provides a clearer picture of how different activities translate into rewards.

Boyco’s role becomes evident when viewed alongside campaigns like Bearn’s “BOINTS” program, which encourages users to deposit into yBERA, yHONEY, or BOLLAR to maximize their points accrual. In such campaigns, points function as a bridge between the long‑term governance‑oriented logic of PoL and the short‑term engagement goals of individual protocols. Users may choose strategies not only based on current yield, but also on expected future token drops or governance power, creating an additional axis of competition among protocols for attention and capital.

The proliferation of points programs introduces both opportunities and risks. On the upside, they can distribute future governance rights more broadly than initial token sales, rewarding genuine users rather than pure speculators. On the downside, they can encourage transactional behavior where users farm points across many protocols with little intention of long‑term engagement. For Berachain, which already relies on PoL to channel emissions toward productive liquidity, the challenge is to ensure that points ecosystems like Boyco remain complementary rather than undermining the chain’s efforts to discourage mercenary capital.

5.5 Other Protocols and Composability

Berachain’s DeFi landscape extends beyond Kodiak, Bearn, and Boyco. Coverage has highlighted the deployment of platforms such as Dolomite, whose DOLO token launched with airdrops claimable exclusively on Berachain, underscoring the chain’s appeal as a primary venue rather than just a side deployment. Other pieces have noted activity around credit, margin trading, and structured products that build on BEND, HONEY, and PoL‑aligned liquidity pools, deepening the chain’s roster of composable financial primitives.

Developer‑oriented initiatives also play a role in seeding the ecosystem. Tutorials like “SnekBeraLlama,” which walks through launching a collateralized debt position (CDP) stablecoin on Berachain using Vyper and Curve‑style mechanics, demonstrate that the chain is courting builders who want to launch complex financial instruments with familiar tooling. Such resources lower the barrier to entry for DeFi teams that might otherwise stick to Ethereum or major L2s, while also showcasing how Berachain’s PoL and stablecoin infrastructure can support tailored designs for collateral, redemption, and governance.

Finally, infrastructure and security partnerships such as those with Orochi Network (as cited in newsroom coverage) signal that Berachain is integrating third‑party services for oracles, randomness, or cross‑chain communication. These integrations, together with bridges that bring assets like Solana and SolvBTC into the ecosystem, embed Berachain in the broader multichain DeFi fabric. As later sections will discuss, this connectivity is a double‑edged sword: it expands the universe of assets and strategies available on Berachain but also exposes the chain to risks originating elsewhere.

6. Performance, Latency, and the Preconfirmation Race

6.1 Baseline Throughput and Latency

Performance is a key differentiator among competing Layer 1s, especially for DeFi applications that rely on tight execution and low slippage. Berachain, built with a BFT‑style consensus engine under its EVM execution layer, targets relatively fast block times on the order of a couple of seconds, providing a level of responsiveness comparable to many modern proof‑of‑stake chains. Public discussion around its preconfirmation proposal indicates that the baseline transaction inclusion time prior to preconfirmations was around two seconds, which is already substantially faster than Ethereum’s roughly 12–15 second slot times.

However, in an environment where chains like Solana, Sui, and Monad are pushing for sub‑second block times and extremely low end‑to‑end latency, a two‑second inclusion target may not be sufficient for certain latency‑sensitive DeFi use cases. High‑frequency trading, arbitrage between on‑chain venues, and sophisticated derivatives strategies benefit from faster feedback loops, as do real‑time gaming and certain UX‑heavy consumer dApps. Berachain’s decision to pursue a preconfirmation layer reflects an acknowledgment that latency is an increasingly important competitive dimension in the “real‑time blockchain” race.

6.2 The 200 Millisecond Preconfirmation Proposal

Berachain’s community has discussed and advanced a proposal to introduce a preconfirmation layer capable of slashing transaction inclusion times from around two seconds to approximately 200 milliseconds, without sacrificing the security guarantees of the underlying consensus. Reports from outlets like Cointelegraph and others describe this as a system where a subset of validators or a designated committee can issue rapid preconfirmations that a given transaction will be included in an upcoming block, even though final settlement still occurs on the normal block schedule. The goal is to give users and applications a high‑confidence signal that their transactions are effectively locked‑in long before full finality.

This architecture can be thought of as a two‑tier system. At the base layer, the BFT consensus protocol continues to produce blocks at its normal cadence, ensuring safety and liveness under standard assumptions. Above it, the preconfirmation layer aggregates votes or commitments from participating validators that a transaction will be included, providing a soft but highly reliable form of early confirmation. If designed correctly, the system can provide near‑instant UX for most transactions while falling back to the slower, fully finalized path in adversarial conditions. Berachain’s challenge is to implement this without introducing undue centralization or enabling censorship by a small group of preconfirming validators.

6.3 Trade‑offs and Comparisons with Other Real‑Time Chains

The preconfirmation approach sits within a broader spectrum of performance strategies across blockchains. Some chains opt for extremely short block times and aggressive pipelining at the base layer, trading off state bloat and potential network instability for raw speed. Others, like Ethereum rollups, focus on batching and compression while accepting longer withdrawal times to L1. Berachain’s strategy is to maintain a relatively conservative base consensus while adding a faster, optional UX layer on top, similar in spirit to designs like “soft confirmations” or optimistic pre‑execution.

This design has several advantages. It allows Berachain to preserve core security assumptions while still improving the user experience for the majority of transactions that are not contested or re‑ordered. It also creates a clear separation between hard finality and soft UX guarantees, which can be useful for dApps that need to reason about risk. However, the preconfirmation layer must be carefully engineered to prevent it from becoming a de facto centralization vector. If only a small number of highly resourced validators can reliably participate in preconfirmations, users and protocols may come to rely on them as privileged transaction sequencers, undermining the decentralization goals of the underlying chain.

Compared to rollup‑based ecosystems like Arbitrum, which rely on Ethereum for final settlement, Berachain’s monolithic Layer 1 plus preconfirmation approach offers different trade‑offs. It can potentially deliver lower latency since it does not need to batch and post data to a separate base layer, but it also shoulders more of the burden for data availability and censorship resistance. In the context of DeFi, these trade‑offs matter for cross‑chain arbitrage, liquidation timing, and MEV dynamics, all of which depend on how quickly and predictably transactions can be confirmed.

6.4 Implications for DeFi Protocols and Users

For protocols like Kodiak, which operate perpetual futures markets and high‑frequency trading venues, preconfirmations could be transformative. A perps exchange that can rely on 200‑millisecond preconfirmations for order placement and cancellation will be more attractive to professional market makers and arbitrageurs than one that must wait multiple seconds for inclusion, all else equal. This, in turn, can deepen order books, tighten spreads, and improve execution quality for retail users, feeding back into higher volume and protocol revenue. Similarly, lending platforms and credit primitives like BEND can benefit from faster liquidation triggers and collateral updates, reducing bad debt during rapid market moves.

For everyday users, preconfirmations can make the network feel more responsive, approximating the experience of Web2 applications where actions appear instantaneous. Wallets can display “preconfirmed” status indicators, dApps can proceed with optimistic UI updates, and merchants can accept low‑value payments with greater confidence that they will not be reversed. At the same time, users must be educated about the distinction between soft preconfirmations and hard finality, particularly for large or high‑risk transactions. The system must also be robust against potential griefing or censorship attacks where preconfirmations are selectively withheld or delayed.

In summary, Berachain’s performance strategy, anchored by its proposed preconfirmation layer, is an important component of its pitch to DeFi builders and traders. If successful, it could allow the chain to offer both the composability of an EVM environment and the responsiveness of real‑time chains, reinforcing its branding as a home for sophisticated financial applications. If mismanaged, it could introduce new forms of centralization or complexity that undermine user trust.

7. Security, Governance, and Network Intervention

7.1 Validator Set, Governance, and Social Consensus

Security on Berachain is provided by a set of validators who stake BERA and participate in the PoL‑mediated consensus process, while delegators can stake via validators to share in rewards and contribute to network security. Governance decisions, including parameter changes, PoL emission adjustments, and protocol upgrades, are made through on‑chain proposals that can be voted on by stakeholders according to their governance power, which in turn is influenced by both stake and PoL‑related governance tokens. This structure blends traditional PoS governance with a DeFi‑influenced, liquidity‑weighted approach.

However, like all blockchains, Berachain ultimately relies on social consensus in addition to formal governance mechanisms. When critical events occur—such as large exploits, consensus bugs, or chain halts—validators, core developers, and community members must coordinate off‑chain as well as on‑chain to decide how to respond. The degree to which this coordination is transparent, inclusive, and consistent with publicly stated decentralization values is a key determinant of a network’s legitimacy. Berachain’s handling of the Balancer exploit incident provides a clear example of this interplay between formal governance and social decision‑making.

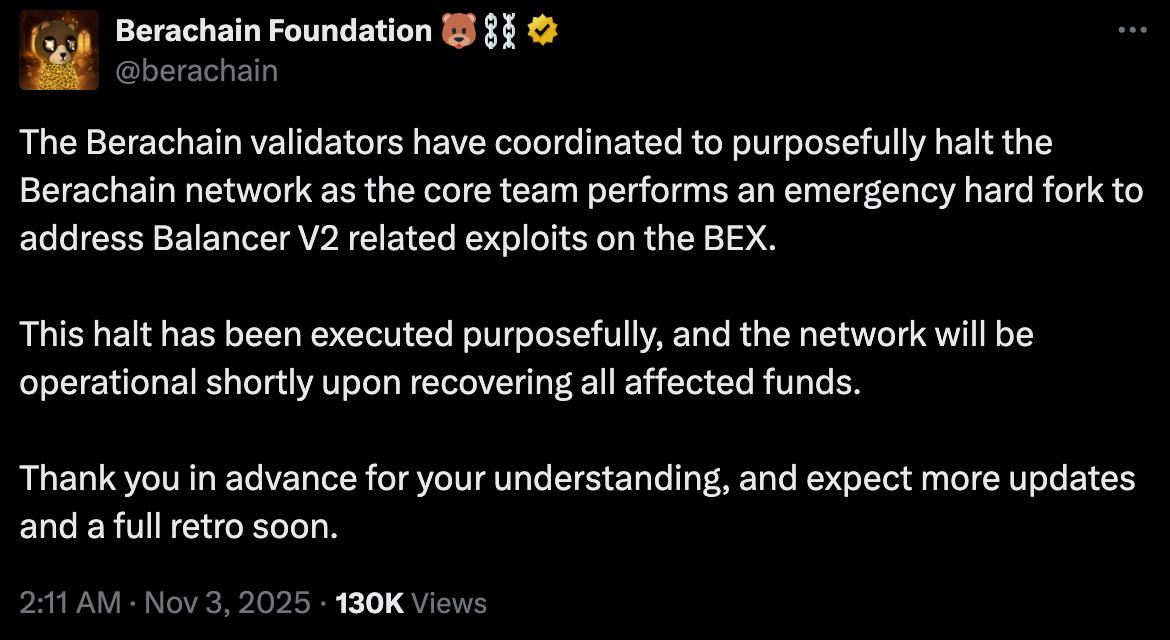

7.2 The Balancer Exploit and Emergency Hard Fork

In late 2025, a major exploit targeted Balancer’s V2 pools, draining approximately \$116 million in liquidity across multiple chains. Because Balancer or Balancer‑style pools formed an important component of Berachain’s DeFi stack, the exploit had direct implications for users and protocols on the chain. In response, the Berachain validator set coordinated to purposefully halt the network while the core team prepared and executed an emergency hard fork intended to address the impact of the exploit. An official statement from the project’s social channels confirmed that validators had agreed to halt block production for this purpose.

This decision sparked immediate debate. On the one hand, supporters argued that halting the chain and performing a hard fork to mitigate exploit damage demonstrated responsible stewardship and a commitment to user protection. Given the interconnectedness of PoL, BEND, and liquidity pools, a cascading failure could have threatened not only DeFi users but also the chain’s consensus economics. On the other hand, critics contended that such a “kill switch” undermined claims of decentralization, revealing that a relatively small set of actors could unilaterally stop the network and modify its state in response to application‑level events. For some, this blurred the line between a public blockchain and a more centrally governed financial infrastructure.

The Balancer incident illustrates the tension at the heart of many modern Layer 1s: the desire to be both user‑friendly and resilient, and the need to reconcile those goals with the ethos of censorship resistance and immutability. Berachain’s choice to prioritize rapid, coordinated intervention over strict non‑interference places it closer to the “pragmatic governance” end of the spectrum. How this choice will affect perceptions among developers, institutional users, and regulators remains an open question, but it highlights the importance of transparent procedures and clear criteria for future interventions.

7.3 Upbit Suspension and Upgrade Coordination

Security and governance also intersect with centralized exchange integrations. When Berachain undergoes upgrades or hard forks, exchanges that list BERA must coordinate closely to avoid issues with deposits, withdrawals, or account balances. In one notable episode, the South Korean exchange Upbit announced an urgent suspension of BERA deposits and withdrawals, citing a Berachain network suspension and subsequent upgrade. The exchange specified that BERA deposit and withdrawal services would be temporarily halted as of a particular date and time while the network upgrade was in progress, with services to resume once stability was confirmed.

Such coordination is standard in the industry, but it carries implications for user experience and perceived reliability. For users whose primary exposure to BERA is via centralized exchanges, repeated or poorly communicated suspensions can create the impression that the underlying network is unstable. At the same time, failing to suspend services during major upgrades or chain halts could lead to serious issues if deposits are sent on a forked or paused chain. Berachain’s ability to maintain clear communication with exchanges like Upbit, and to minimize disruptive downtime, will be a key factor in its broader market integration.

7.4 Cross‑Chain Risk: SolvBTC and Bridged Assets

Modern DeFi ecosystems are deeply interconnected, and Berachain is no exception. One illustration of this is the handling of SolvBTC, a yield‑bearing BTC derivative issued by Solv Protocol that operates on multiple chains. In a recent update, Solv announced the closure of burn‑mint permissions for selected assets and chains—including SolvBTC deployments on Ethereum, BNB Smart Chain, Arbitrum, Avalanche, Base, Solana, XLayer, Monad, Ink, Soneium, Sonic, Berachain, Rootstock, and zkSync—via a shared permissioning infrastructure. This move underscores the complexity and risk of cross‑chain assets whose supply and redemption logic depends on smart contracts deployed across many networks.

For Berachain, participation in ecosystems like SolvBTC brings both benefits and risks. On the benefit side, it allows users to access BTC‑denominated yield products and to use BTC‑backed assets as collateral or liquidity within PoL‑aligned protocols. On the risk side, any issue with SolvBTC’s design, governance, or cross‑chain bridges could spill over into Berachain, affecting collateral values and user positions. The decision to close burn‑mint permissions across multiple chains was framed as a security measure, but it also illustrates how decisions made by external protocols can affect Berachain users without direct recourse to Berachain’s governance mechanisms.

This dynamic extends to other bridged assets, such as wrapped Solana tokens brought in via Wormhole. Each bridge carries its own security model, often based on multi‑sig committees or external validator sets, which may not align with Berachain’s threat assumptions. For a PoL chain where liquidity and collateral are deeply enmeshed with consensus, an exploit in a major bridge could have magnified consequences. As Berachain’s ecosystem grows, its governance and risk management frameworks will need to develop systematic approaches for assessing and responding to cross‑chain risks.

7.5 Decentralization, Interventionism, and Long‑Term Credibility

Taken together, incidents like the Balancer exploit response, exchange suspensions during upgrades, and cross‑chain asset risk paint a nuanced picture of Berachain’s security and governance posture. The network has shown a willingness to intervene decisively in the face of threats, coordinating validator actions and core team efforts to protect users and restore stability. This approach may reassure some participants, particularly those with large capital allocations who value predictable and proactive crisis management.

At the same time, each intervention chips away at the ideal of a neutral, unstoppable ledger. Critics may argue that if a small set of actors can halt the chain or heavily influence remediation outcomes, Berachain is more akin to a consortium or permissioned network than a fully decentralized Layer 1. Proponents would counter that in a world of complex DeFi composability and cross‑chain dependencies, a purely hands‑off stance is no longer tenable, and that transparency and community input around interventions can mitigate centralization concerns.

In the long run, Berachain’s credibility will depend on how it codifies and communicates its intervention norms. Clear frameworks for when and how chain halts, hard forks, or parameter changes can occur—ideally ratified through on‑chain governance and social consensus—will help participants assess the risk profile of building and holding assets on the network. As more capital and regulatory attention flow into PoL and similar designs, the balance between flexibility and immutability will remain a central tension.

After a $116M Balancer exploit rippled across chains, Berachain validators voted to halt the entire network — raising hard questions about whether “decentralization” still means what it used to.

same vibes as that bad SUI hack...lose lose situation

Berachain raises $100M Series B led by Brevan Howard and others

$1.6B pre-launch liquidity via Boyco vaults ahead of mainnet

Mainnet launches February 6; $3.3B TVL at genesis, $7B FDV

BERA community airdrop (15.75% supply) distributed at TGE

Balancer $116M exploit; Berachain validators vote to halt network

Berachain TVL plunges ~50% from peak; mercenary capital rotation confirmed

Leaked docs reveal Brevan Howard received $25M full Series B refund post-TGE

Polychain leads $110M deal to build Berachain treasury; Greenlane adopts BERA as reserve

8. Liquidity Dynamics, TVL, and Mercenary Capital

8.1 The TVL Boom: Initial Liquidity Influx

Like many high‑profile DeFi‑centric chains, Berachain experienced a rapid inflow of capital in the months following its mainnet launch. Generous PoL emissions, ecosystem incentives, and the prospect of future airdrops attracted liquidity providers seeking high yields, while DeFi protocols eager to tap into these flows rushed to deploy on the chain. Blockeden’s “one year later” analysis estimates that Berachain’s total value locked (TVL) reached a peak of around \$3.35 billion, a striking figure for a relatively new Layer 1. This surge reflected not only organic interest in PoL, but also broader market conditions and the cyclical appetite for yield farming.

The early boom period was characterized by intense competition among protocols for emissions and liquidity. AMMs, lending platforms, and structured product protocols all vied for PoL allocation and user attention, often augmenting chain‑level rewards with additional token incentives and points programs. For a time, Berachain looked like a textbook example of how a novel consensus mechanism, combined with targeted ecosystem funding, could push a chain into the top tier of DeFi TVL rankings. However, as with previous cycles on other chains, sustaining that growth turned out to be more challenging than catalyzing it.

8.2 The TVL Bust and BERA Drawdown

The same Blockeden analysis notes that Berachain’s TVL did not remain at its peak for long. Over the subsequent months, TVL reportedly collapsed from \$3.35 billion to approximately \$393 million, an 88% decline. At the same time, the BERA token’s price was said to have crashed more than 90% from its all‑time high of about \$2, illustrating the downside of a heavily incentivized initial growth phase. Separate newsroom coverage has pointed out that, on a shorter time frame, Berachain’s TVL declined by roughly 50% in a single month, underscoring the volatility of liquidity that is heavily influenced by emissions and external market conditions.

Several factors likely contributed to this bust. As PoL and protocol‑level yields normalized, some liquidity providers reallocated capital to other chains or strategies offering better risk‑adjusted returns. Token unlocks and market‑wide drawdowns may have added selling pressure on BERA, dampening price expectations and reducing the appeal of holding rewards rather than selling them. Cross‑chain incidents, such as the Balancer exploit and changes in SolvBTC permissions, may have further shaken confidence or reduced the attractiveness of certain collateral types. The net result was a much smaller, though potentially more “sticky,” base of liquidity compared to the euphoric highs.

8.3 Mercenary Capital and the Limits of Emissions

Berachain’s boom‑and‑bust TVL pattern reinforces a lesson that has recurred across DeFi cycles: mercenary capital is both a powerful bootstrap tool and a persistent challenge. High emissions and generous incentive programs can attract large volumes of capital quickly, but much of that capital is price‑insensitive on the way in and hyper‑sensitive on the way out. When yields compress or alternative opportunities arise, it can exit just as quickly, leaving behind fragmented liquidity and underutilized infrastructure. PoL was in part designed to mitigate this dynamic by embedding liquidity within consensus, but Berachain’s experience suggests that design alone cannot fully overcome market psychology.

In traditional liquidity mining models, protocols often end up in a “subsidy trap,” where they feel compelled to continue high emissions to maintain TVL, even when those emissions are no longer justified by usage or revenue. PoL offers a more coordinated alternative by pooling emissions at the chain level and directing them toward a curated set of productive activities. However, if governance is not sufficiently disciplined, or if governance itself is captured by actors benefiting from high emissions, PoL can replicate some of the same dynamics at a different scale. The 88% TVL drawdown indicates that Berachain is still grappling with how to calibrate rewards to attract durable, not purely speculative, liquidity.

8.4 Toward Stickier Liquidity: Credit, Yield, and Points

Recognizing these challenges, Berachain’s ecosystem has increasingly focused on making liquidity stickier by offering deeper integration, additional utility, and layered incentives. The BEND credit layer allows LP tokens and HONEY positions to serve as collateral, increasing the opportunity cost of withdrawing liquidity since doing so can reduce access to credit and leveraged strategies. Yield aggregators like Bearn streamline complex strategies and build reputational trust around risk‑managed vaults, encouraging users to leave capital deployed over longer horizons. Points and rewards platforms like Boyco provide meta‑incentives that extend beyond immediate yield, tying participation to future governance and token allocations.

Moreover, as the initial speculative fervor subsides, a different class of user may come to the fore: those who prioritize product quality, execution reliability, and risk management over raw APR. For these users, features like preconfirmations, robust security practices, and transparent governance processes carry significant weight. If Berachain can demonstrate that its PoL design, DeFi stack, and performance features create a genuinely superior environment for certain strategies—such as real‑time perps trading or complex credit constructs—it may cultivate a base of liquidity that is more resilient to short‑term emissions changes.

That said, the path from mercenary to sticky liquidity is seldom straightforward. It requires iterative tuning of emissions, careful curating of “core” protocols that receive PoL support, and a willingness to let underperforming or overly extractive strategies starve. It also requires building trust with users and institutional partners who have many options in a crowded multichain landscape. Berachain’s early TVL cycle should thus be viewed as a first pass in a longer‑term experiment in liquidity‑aware consensus.

9. Berachain in the Multichain DeFi Stack

9.1 Relationship with Ethereum, Arbitrum, and EVM Ecosystems

Because Berachain is EVM‑identical, it is best understood not as an isolated ecosystem but as part of the broader Ethereum and EVM family. Contracts originally written and audited for Ethereum mainnet or rollups like Arbitrum can, in principle, be deployed on Berachain with minimal modification, enabling multi‑chain deployments for protocols that want to tap into PoL incentives or Berachain’s real‑time features. This compatibility extends to user‑facing tools: wallets like MetaMask can be configured to interact with Berachain just as they do with Ethereum, and developer frameworks like Hardhat and Foundry can be pointed at a Berachain RPC endpoint with relatively minor configuration changes.

Berachain’s integration into the wider EVM world is further evidenced by cross‑chain assets like SolvBTC, which operate on multiple EVM and non‑EVM chains including Ethereum, BNB Smart Chain, Arbitrum, Avalanche, Base, and Berachain. The ability to move such assets between chains via bridges allows users to arbitrage yields, diversify collateral, and navigate different execution environments while retaining exposure to the same underlying instrument. For Berachain, this means that it competes not only on native token yields but also on how attractive its environment is for hosting shared, cross‑chain DeFi positions.

At the same time, Berachain must differentiate itself from other EVM‑compatible environments if it wants to avoid being just another venue in a crowded field. Its PoL consensus, preconfirmation initiative, and tightly integrated DeFi primitives are the main bets in this regard. Whether these features are compelling enough to draw sustained liquidity away from established hubs like Ethereum mainnet, Arbitrum, and Optimism will depend on both technical execution and the chain’s ability to navigate the risks and controversies discussed earlier.

9.2 Positioning Against Non‑EVM Layer 1s

Beyond the EVM world, Berachain faces competition from non‑EVM Layer 1s like Solana, which have emphasized high throughput and low latency as core differentiators. Berachain’s preconfirmation proposal, aiming for 200‑millisecond inclusion times, can be seen as a response to this competitive pressure, positioning the chain as part of the “real‑time blockchain” race while preserving EVM compatibility. Unlike Solana, which uses a distinct programming model and runtime, Berachain offers a familiar environment for Solidity developers who want near‑real‑time DeFi without adopting a new stack.

However, achieving Solana‑level UX while maintaining the full expressiveness and composability of the EVM is not trivial. The EVM was not originally designed for ultra‑low‑latency, high‑throughput applications, and scaling it reliably requires careful engineering at the consensus, networking, and execution layers. Berachain’s modular approach and use of preconfirmations are attempts to square this circle, but they must be validated under real‑world load. In this sense, Berachain is part of an emerging category of chains that try to marry the EVM ecosystem’s network effects with performance characteristics more commonly associated with bespoke high‑performance L1s.

9.3 Shared Infrastructure, Oracles, and Institutional Backing

Another lens for viewing Berachain’s place in the multichain stack is through its shared infrastructure providers and institutional backers. Newsroom coverage has highlighted the role of venture firms like Dispersion Capital, whose founder has backed infrastructure projects including Helium, Alchemy, Berachain, and 0G as part of a thesis on the importance of core crypto infrastructure. This places Berachain in a portfolio of networks and services that aim to provide the backbone for future decentralized applications, from wireless networks to data layers.

Partnerships with infrastructure providers such as Orochi Network, as mentioned in recent coverage, further embed Berachain in a mesh of oracle, data, and security services that span multiple chains. These partners may provide price feeds, randomness, fraud proofs, or other critical services that both benefit from and contribute to Berachain’s liquidity and activity. As the multichain world matures, chains that can integrate seamlessly with shared infrastructure—while also offering unique features like PoL and preconfirmations—may be better positioned to attract developers who want to build cross‑chain applications without managing bespoke integrations for each network.

9.4 CeFi Touchpoints and Market Access

Centralized exchanges and traditional companies represent another axis of Berachain’s multichain footprint. The decision by Greenlane Holdings to treat BERA as a primary reserve asset in its corporate treasury, as disclosed in its investor communications, suggests that some traditional firms view Berachain as a credible long‑term infrastructure bet. This moves BERA beyond the realm of purely speculative trading and into the domain of treasury management and balance sheet strategy, albeit at an early stage.

At the same time, exchanges like Upbit provide critical liquidity and fiat on‑ramps for BERA, making it accessible to users who may not directly interact with on‑chain DeFi protocols. These CeFi touchpoints are sensitive to network stability, regulatory perceptions, and overall market sentiment. Incidents like chain halts, controversial governance decisions, or high‑profile exploits can influence whether exchanges list, suspend, or delist assets, which in turn affects liquidity and price discovery. Berachain’s integration with CeFi thus requires careful management of operational and reputational risk alongside its technical and economic experiments.

10. Developer and User Experience

10.1 EVM‑Identical Tooling and Developer Ergonomics

For developers, Berachain’s EVM‑identical promise is a central attraction. By ensuring that the chain’s execution environment matches Ethereum’s EVM semantics, Berachain allows teams to reuse existing Solidity and Vyper codebases, testing frameworks, and deployment pipelines with minimal friction. This lowers the barrier to entry compared to non‑EVM chains, where teams must learn new languages and tooling, and compared to EVM‑adjacent chains that introduce subtle incompatibilities. In practical terms, a protocol team can deploy its Ethereum contracts to Berachain, adjust configuration files, and immediately tap into PoL incentives and the chain’s DeFi ecosystem.

This compatibility extends to user‑facing tools. Wallets like MetaMask can support Berachain simply by adding a new network RPC, as is common for other EVM chains. Block explorers, indexing services, and analytics platforms can integrate Berachain with relatively modest engineering effort, leveraging their existing EVM‑oriented code. For developers, this means faster iteration cycles and the ability to test new incentive structures or product ideas on Berachain without abandoning their Ethereum deployments.

10.2 Building DeFi Primitives on a PoL‑Aligned Base

For builders of DeFi primitives, Berachain offers both familiar ingredients and novel levers. On the familiar side, developers can work with standard ERC‑20, ERC‑4626, and other Ethereum token standards, as evidenced by protocols like Bearn that deploy ERC‑4626 vaults such as yHONEY on the chain. They can integrate with AMMs, lending markets, and oracles using well‑understood patterns, and they can use languages like Solidity and Vyper for contract logic.

On the novel side, PoL and the chain’s governance mechanisms allow builders to design protocols that are tightly coupled to base‑layer incentives. A lending protocol might design its collateral and interest models to align with PoL‑recognized LP tokens and stablecoins, maximizing its eligibility for emissions and governance support. An AMM might tailor its pool structures to be designated as “core” infrastructure, ensuring a privileged position in PoL gauges. Tutorials like SnekBeraLlama’s CDP guide show how developers can compose with Berachain’s stablecoin and liquidity primitives to create new forms of credit and leverage that take advantage of PoL’s capital coordination.

However, this tight coupling also means that protocol design on Berachain is sensitive to governance and emissions decisions. A change in PoL allocation or a governance reversal on what counts as productive liquidity can materially affect a protocol’s economics. Builders must therefore monitor governance processes more closely than they might on neutral base layers and may need to actively participate in governance to protect their protocols’ interests.

10.3 Ecosystem Support, Grants, and Capital Access

Berachain’s significant treasury and backing from major funds like Polychain, Framework, and Brevan Howard’s Nova Digital give it substantial resources to support builders. Ecosystem grants, liquidity bootstrapping programs, and co‑marketing initiatives can help early‑stage teams gain traction faster than they might on more mature but less aggressively funded chains. Yearn’s sub‑DAO Bearn choosing to launch on Berachain, and Dolomite making BERA the exclusive venue for claiming DOLO airdrops, reflect the pull of these ecosystem incentives and the potential for Berachain to position itself as a launchpad for new DeFi products.

In addition, infrastructure‑focused investors like Dispersion Capital, which has backed projects such as Helium, Alchemy, Berachain, and 0G, provide a network of relationships and expertise for teams building at the protocol and middleware layers. This ecosystem of capital and support can be especially valuable for complex, capital‑intensive products like derivatives exchanges, credit protocols, and cross‑chain platforms, which require both technical sophistication and significant liquidity to succeed.

10.4 Risks and Considerations for Builders and Users

Despite these advantages, builders and users on Berachain face a non‑trivial risk landscape. Chain‑wide interventions like the Balancer exploit halt demonstrate that protocol‑level failures can trigger network‑level consequences, which may affect assumptions about liveness and immutability. Cross‑chain dependencies introduce additional attack surfaces, as seen in SolvBTC’s decision to close burn‑mint permissions across multiple chains and the general fragility of bridge infrastructure. PoL’s complexity, combined with tokenomics that include significant investor allocations and vesting schedules, adds uncertainty around long‑term emission and governance dynamics.

Users must also weigh the trade‑offs between high yields and smart contract risk. While Berachain hosts sophisticated DeFi protocols and yield strategies, it is still a relatively young ecosystem, and not all contracts have withstood prolonged adversarial scrutiny. The rapid rise and fall of TVL indicates that many participants are opportunistic, which can exacerbate volatility during stress events. As always in DeFi, careful due diligence, diversified exposure, and awareness of protocol dependencies are essential.