Comprehensive explainer on Canton Network, a public privacy-enabled L1 for institutional onchain markets. Covers architecture, Canton Coin economics, repo and Treasuries tokenization, Visa stablecoin pilots, governance, risks, and ETF implications.

+13 sources across the wider coverage universe

HSBC completes tokenised deposit pilot on Canton Network, showcasing interoperable issuance, transfer, and atomic settlement for regulated institutions2026-04

HSBC completes tokenised deposit pilot on Canton Network, showcasing interoperable issuance, transfer, and atomic settlement for regulated institutions2026-04 Alchemy integrates with Canton Network, joining 800+ validators and major financial giants to scale $8T+ tokenized asset ecosystem for institutional blockchain adoption2026-04

Alchemy integrates with Canton Network, joining 800+ validators and major financial giants to scale $8T+ tokenized asset ecosystem for institutional blockchain adoption2026-04 Grayscale says tokenization will reshape capital markets, with Canton leading near-term institutional adoption while Ethereum and Solana compete for long-term dominance2026-05

Grayscale says tokenization will reshape capital markets, with Canton leading near-term institutional adoption while Ethereum and Solana compete for long-term dominance2026-05 Hanwha partners with Digital Asset to explore Canton Network integration, expanding institutional collaboration on shared blockchain infrastructure in South Korea2026-04

Hanwha partners with Digital Asset to explore Canton Network integration, expanding institutional collaboration on shared blockchain infrastructure in South Korea2026-04 ZKsync vs Canton heats up as Matter Labs slams bank-led networks for lacking global rule enforcement, while Digital Asset defends privacy-first design for institutional onchain finance2026-04

ZKsync vs Canton heats up as Matter Labs slams bank-led networks for lacking global rule enforcement, while Digital Asset defends privacy-first design for institutional onchain finance2026-04 Temple partners with Chainlink to power institutional-grade market infrastructure on Canton Network as it expands into new asset classes and trading functionality2026-05

Temple partners with Chainlink to power institutional-grade market infrastructure on Canton Network as it expands into new asset classes and trading functionality2026-05

Canton Network: Privacy-Enabled Infrastructure For Institutional Onchain Markets

Canton Network is a public, permissionless layer‑1 blockchain designed to let financial institutions move real assets, payments, and complex workflows onchain without sacrificing privacy, regulatory compliance, or interoperability. By combining a network-of-networks architecture with granular data controls and an incentive model tied to real usage, Canton positions itself as infrastructure for institutional onchain markets rather than a purely speculative crypto platform.

Defining Canton Network and Its Role in Onchain Finance

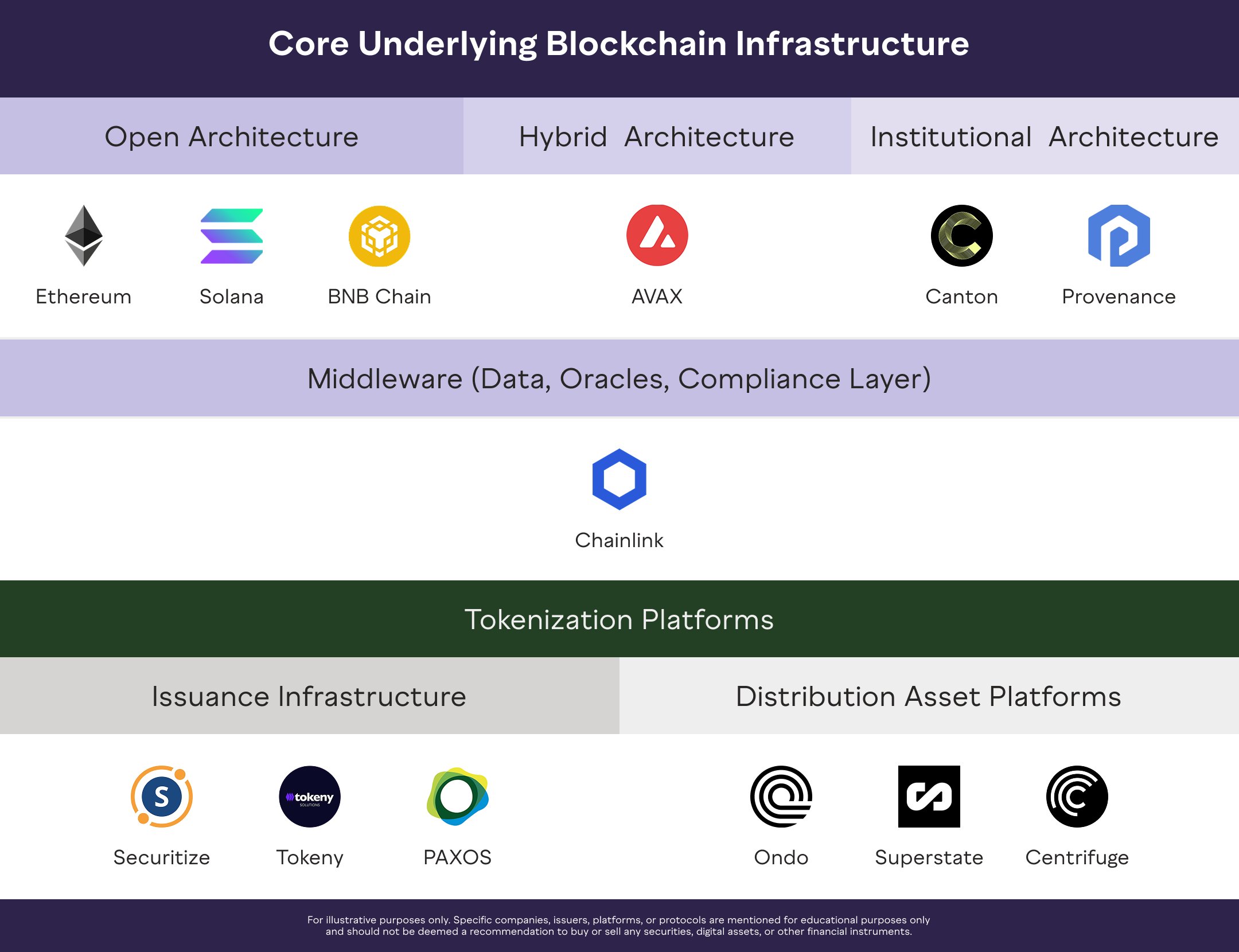

Canton Network is best understood as a general‑purpose blockchain specifically engineered for regulated financial markets, rather than as a retail DeFi chain that institutions might adopt after the fact. At its core, it is a public, permissionless layer‑1 protocol that allows anyone to run validator infrastructure, submit transactions, and build smart contract applications, while giving individual applications the tools to implement permissioned access and strict data controls where needed. The network’s own materials describe Canton as the first privacy‑enabled open blockchain network for institutional finance, capable of connecting multiple applications and markets while preserving confidentiality for each participant. This dual identity—open base layer, institution‑grade privacy at the application layer—is central to understanding how Canton aims to bridge traditional finance and crypto‑native markets.

Unlike monolithic chains such as Ethereum, where every node maintains a copy of a single, globally replicated state, Canton is explicitly designed not to rely on a single global ledger. Instead, it supports interoperable, privacy‑preserving smart contract applications that share data only with the specific parties involved in a given transaction. Messari characterizes this as “configurable privacy with composability,” meaning that while each participant sees only the parts of a transaction they are entitled to access, applications can still interact atomically across the network. In practical terms, this enables use cases such as a repo trade that simultaneously touches a tokenized U.S. Treasury, a cash leg settled in stablecoins, and a collateral management application—executed as a single, all‑or‑nothing transaction—without broadcasting sensitive details to the entire world.

Canton’s positioning within the broader crypto landscape reflects the evolution of enterprise distributed ledger technology into public blockchain infrastructure. For years, banks, market operators, and custodians experimented with private, permissioned DLT platforms that were often siloed and difficult to connect to wider crypto markets. Canton takes the lessons from those experiments—most notably around privacy, settlement finality, and regulatory requirements—and combines them with the openness, shared infrastructure, and native token incentives of public blockchains. This convergence is reflected in the network’s growing ecosystem, which spans tokenized bonds and money market funds, repo and collateral platforms, stablecoin settlement rails, and institutional‑facing payment and deposit networks.

In crypto terminology, Canton is infrastructure for “onchain markets” rather than a single monolithic “onchain market.” Its architecture aims to let regulated institutions bring their existing market structures, risk frameworks, and custody setups onchain with minimal disruption, while still reaping the benefits of programmability and atomic settlement. Institutions can design applications that mirror familiar workflows—such as request‑for‑quote trading, tri‑party collateral arrangements, or multi‑tier custody chains—then execute them through smart contracts on Canton with privacy logic built in. This is a markedly different approach from the typical DeFi pattern of creating entirely new market designs and asking institutions to adapt to them.

OneSwap launches self-custodial Canton browser wallet built for 60-second retail swaps

Promoting from Tsunami auto-feed. Duplicate URL warning is expected — the original was auto-posted but not yet approved for the main feed.

Readers consumed Canton's institutional-adoption headlines as retail trading signals, not infrastructure news — the top clicked angle was a price-divergence framing during a broader crypto selloff, revealing that the Wall Street-blockchain narrative functions primarily as a contrarian catalyst for speculative positioning on CC.↗

Origins, Launch, and Governance

Canton originates from years of development by Digital Asset, a fintech firm that has been building distributed ledger technology for capital markets since the mid‑2010s. Digital Asset initially focused on networks tailored to specific institutions and market infrastructures, working with organizations such as ASX, Broadridge, and major global banks on bespoke distributed ledger deployments. Over time, it became clear that while isolated DLT projects could deliver efficiencies, the bigger opportunity lay in connecting multiple institutions and asset classes on a shared, interoperable network while still preserving confidentiality. Canton represents the culmination of that shift—from fragmented, often closed‑loop DLT environments to an open, public protocol.

The network’s governance reflects this institutional heritage. Canton was initially developed by Digital Asset but has been open‑sourced and is now governed through a decentralized framework centered on what is known as the Global Synchronizer Foundation. According to Digital Asset, the Canton Network is “governed by the Global Synchronizer Foundation with participation from leading global financial institutions,” which collectively steward core protocol decisions, network parameters, and the operation of key infrastructure such as the Global Synchronizer. This governance structure aims to balance decentralization with the need for predictable, risk‑managed decision‑making that regulated institutions can trust.

Canton’s public mainnet went live in 2024, after several years of private deployments and pilots with top‑tier financial institutions. Messari notes that by the time the public network launched, Canton had already “delivered meaningful value through privacy‑preserving deployments, used at scale by institutions,” and that the 2024 mainnet serves as the base layer for more than 150 live or emerging applications. This trajectory is important: Canton did not launch as a speculative network waiting for real‑world adoption; rather, it evolved out of existing institutional use cases and then opened to broader participation once the core technology and operational patterns were proven.

A notable aspect of the launch was the decision to forgo a traditional initial coin offering, premine, or early allocation of the native token, Canton Coin (CC), to founders or venture capital investors. Network representatives emphasize that Canton Coin was introduced without an ICO, pre‑mined supply, or preferential allocation to insiders, and that issuance began only after the Global Synchronizer became operational on the live network. This “fair launch” narrative is reinforced by the network’s economic design, where new CC is minted over time as a function of measurable network participation rather than being distributed upfront based on capital raised.

Governance of the protocol itself is evolving through a proposal system akin to improvement proposals on other blockchains. Canton Improvement Proposals (CIPs) specify changes to core standards and functionality and are debated and approved through the network’s governance channels. CIP‑0112, for example, introduced Token Standard V2, adding privacy‑enhanced batch settlement, prefunded trading features, multi‑tier custody chains, and wallet‑friendly single‑signature authorization. Another proposal, CIP‑0082, created a Protocol Development Fund that receives a share of future token emissions to support ecosystem grants, security audits, and tooling. These CIPs illustrate how Canton’s governance is used to adapt the protocol to emerging institutional needs while maintaining decentralization at the base layer.

Canton’s institutional orientation is underscored by the capital committed to its development. In June 2025, Digital Asset announced a strategic funding round of 135 million dollars led by DRW Venture Capital and Tradeweb Markets, with participation from institutions such as BNP Paribas, Circle Ventures, Citadel Securities, DTCC, Goldman Sachs, Paxos, and others. The stated goal of that round was to accelerate institutional and decentralized finance adoption on Canton, particularly around tokenization of bonds, money market funds, alternative funds, commodities, repos, mortgages, life insurance, and annuities. In June 2026, the company followed with a much larger 355 million dollar raise led by a16z crypto, explicitly aimed at cementing Canton’s role across regulated financial markets, with a focus on tokenization, collateral mobility, settlement, payments, and other regulated workflows. Together, these rounds signal that a significant segment of Wall Street and the crypto venture community views Canton as a serious contender for institutional onchain infrastructure.

Architecture: Synchronizers, Privacy, and Atomic Interoperability

Canton’s architecture is organized around the concept of a “network of networks,” in which multiple applications and subnets can interoperate through shared synchronizers without forming a single, monolithic blockchain. In a conventional public chain, every full node must maintain and process the entire state of the system, which creates scalability limits and makes data from every transaction visible to all participants by default. Canton instead decouples consensus and synchronization from data visibility, allowing applications to share a common settlement fabric while disclosing details only to relevant parties.

At the heart of this design is the synchronizer, a component responsible for ordering and confirming transactions across applications. Each application on Canton connects to one or more synchronizers, to which validator nodes attach in order to participate in consensus. Applications and validators can use multiple synchronizers at once, and synchronizers themselves can be operated by different entities, which enables a modular and resilient network topology. The Global Synchronizer is the primary, publicly available synchronizer for the Canton Network; it allows validators to compose atomic transactions that span multiple applications and subnets, effectively stitching together separate markets into a single interoperable ecosystem.

This architecture enables what Canton describes as “true atomic and privacy‑preserving interoperability” within and across its subnets. Atomicity ensures that complex transactions involving multiple legs and multiple applications either settle in full or not at all, removing settlement risk between independent systems. Privacy is enforced by ensuring that only the parties to a particular contract or transaction see the associated data or state changes, even though the transaction may rely on shared synchronizer infrastructure for ordering and finality. In effect, the synchronizer validates and sequences commitments and proofs about state transitions without requiring visibility into the full underlying business data, which remains partitioned by counterparty and application.

This privacy model is particularly important for financial institutions, which handle highly sensitive information about positions, exposures, and client activity. In a typical public blockchain, these details are at least partially inferable from onchain data, even if addresses are pseudonymous, which is problematic for regulated entities subject to confidentiality and market abuse rules. Canton, by contrast, provides granular access control at the protocol level, allowing applications to enforce that each participant sees only what they are legally or contractually entitled to see. IntellectEU, a technology provider that supports Canton development, highlights that unlike other public blockchains, Canton’s “unique privacy layer and granular access control” align with the needs of regulated institutions that cannot disclose their entire transaction history on a public ledger.

Canton’s smart contract environment is designed for confidential multi‑party workflows rather than simple token transfers. Contracts can encode complex obligations, contingent events, and multi‑step processes—such as collateral substitutions in a repo, waterfall distributions in a fund, or multi‑leg FX swaps—while ensuring that only relevant participants and required regulators have visibility into the details. Because applications can share the same synchronizer, they can also compose their contracts atomically. For example, a repo platform can interact with a collateral management app and a stablecoin settlement rail in one atomic sequence, guaranteeing that cash, securities, and collateral records all update consistently.

Token standards are a key part of this architecture, particularly as the network seeks to represent real‑world assets and complex financial products onchain. CIP‑0112, which introduced Canton Token Standard V2, illustrates how deeply the protocol is tailored to institutional settlement scenarios. The new standard adds privacy‑enhanced batch settlement, allowing multiple transfers or trades to be settled in aggregate without leaking sensitive details to the broader network. It also introduces committed allocations for prefunded trading with iterated settlement, enabling workflows where participants pre‑fund accounts and then trade against those balances with predictable, programmable settlement cycles. Multi‑tier custody chains allow assets to move through layered custodial arrangements, reflecting how securities are actually held and managed in traditional markets. Finally, single‑signature authorization through wallets simplifies user interactions and custody integrations, making Canton assets easier to hold in institutional‑grade wallets while maintaining protocol‑level privacy and control.

From an interoperability standpoint, Canton’s network‑of‑networks approach allows different institutions to maintain substantial autonomy over their own applications and data while still participating in shared markets. An investment bank might operate a collateral management platform, a custodian might run a tokenized securities ledger, and a fintech could provide a stablecoin payments rail, all on separate Canton applications connected to a common synchronizer. When a transaction spans these components, the Global Synchronizer coordinates atomic settlement and ensures that each participant’s local state updates consistently without exposing all underlying data to every node or application. This is a fundamentally different model from cross‑chain bridges or wrapped assets; here, interoperability is achieved natively through the protocol’s synchronization layer.

- 01Price divergence during crypto selloff

Canton's 30% gain while the broader market fell gave retail readers a contrarian trade narrative anchored in institutional credibility, making it the single highest-clicked angle by a wide margin.

- 02DTCC Treasury tokenization pipeline↗

A named DTCC partnership with a concrete 2026 go-live target attached real settlement infrastructure to the Canton story, converting abstract network claims into a trackable institutional milestone.

- 03Wall Street validator accumulation↗

Each successive name — Visa, HSBC, BNP Paribas, Goldman Sachs, Broadridge — functioned as a running legitimacy leaderboard that readers tracked as a proxy for institutional conviction.

- 04Canton Coin treasury strategy and raises↗

Successive nine-figure raises from a16z, DRW, and the Tharimmune treasury vehicle repositioned CC as an institutional balance-sheet asset rather than a utility token, pulling in readers watching capital formation signals.

- 0524/7 weekend on-chain repo settlement↗

A live Saturday Treasury repo trade with no brokers dramatized Canton's always-on settlement rails in a way that made abstract infrastructure claims immediately legible to both TradFi and crypto readers.

- 06Ethereum and Solana competitive framing↗

Tiger Research and Grayscale positioning Canton as a 'most realistic' L1 rival gave crypto-native readers a familiar competitive story to anchor an otherwise opaque institutional-grade network.

Privacy, Compliance, and Institutional Design

Privacy is not a cosmetic feature in Canton; it is the core answer to one of the biggest barriers to institutional blockchain adoption. Financial institutions operate under strict legal obligations to protect client data, trading strategies, and counterparty relationships, and they manage risks related to market abuse, front‑running, and information leakage in tightly controlled ways. Yuval Rooz, co‑founder and CEO of Digital Asset, has argued that traditional financial infrastructure suffers from fragmented data and settlement delays, but that any blockchain‑based replacement must still honor the confidentiality requirements embedded in existing regulations and business practices. Canton is explicitly designed to reconcile these imperatives: it uses blockchain rails to coordinate state across multiple institutions, while its privacy architecture ensures that sensitive information remains compartmentalized.

Canton’s configurable privacy allows each application to define who can see what, down to the level of individual contract fields and transaction details. In a repo transaction, for instance, the borrowing and lending parties, their agents, and relevant custodians need visibility into the collateral, term, rate, and settlement status, whereas other market participants and unrelated nodes do not. The protocol ensures that only these entitled parties receive the relevant state updates and proofs, while the synchronizer validates that the transaction is globally consistent without learning all of its business details. This aligns with how financial institutions already segment data across desks, legal entities, and jurisdictions, and it allows them to bring those patterns onchain without exposing proprietary or client‑sensitive information.

Compliance goes hand‑in‑hand with this privacy model. Canton’s materials emphasize “institutional‑grade compliance,” meaning that while the base layer is permissionless, applications can incorporate know‑your‑customer (KYC), anti‑money laundering (AML), and other regulatory controls as part of their smart contracts and access policies. Market operators can design onchain venues where only whitelisted participants may trade certain assets or access particular workflows, and where transaction data can be selectively disclosed to regulators and auditors without becoming globally visible. This is a crucial distinction from pseudonymous DeFi, where regulatory compliance is often layered on externally, if at all. In the Canton model, compliance features are integral to how institutional applications are built and how they interact with one another.

The recently approved Token Standard V2 under CIP‑0112 underscores Canton’s focus on compliance‑oriented features. Privacy‑enhanced batch settlement allows institutions to net and settle positions in ways that match existing regulatory and operational frameworks, without creating a transparent onchain log of every individual allocation. Committed allocations for prefunded trading with iterated settlement closely mirror how pre‑funded and margin‑based trading operates in traditional markets, but with the added benefit of programmable, verifiable settlement. Multi‑tier custody chains reflect the actual structures found in securities markets, where end investors, sub‑custodians, global custodians, and central securities depositories all play different roles in asset safekeeping and transfer. Finally, the provision for single‑signature wallet authorization helps integrate Canton with mainstream institutional custody solutions while maintaining the privacy guarantees that regulators and clients expect.

IntellectEU, which offers Canton validator and development services, points out that the network’s “unique privacy layer and granular access control” finally aligns public blockchain infrastructure with the needs of regulated institutions. Institutions that previously had to choose between fully public, transparent blockchains and closed, proprietary DLT systems now have an option that combines elements of both: public, shared infrastructure at the consensus and synchronization layer, with tightly controlled, application‑level data visibility. This design not only makes it possible to bring sensitive financial products onchain but also enables cross‑institutional workflows such as syndicated lending, structured products, and complex derivatives that would be impossible to run safely on a fully transparent ledger.

From a markets perspective, Canton’s privacy model aims to reduce risks such as front‑running, information leakage, and reverse‑engineering of trading strategies that have been chronic issues on transparent blockchains. Order sizes, counterparties, and positions can be kept confidential while still being subject to onchain verification and regulatory oversight. This makes it more realistic for institutions to consider moving price‑sensitive activity—such as bond trading, collateral upgrades, or balance‑sheet management—onto a blockchain without broadcasting their internal moves to the entire market. At the same time, the shared infrastructure and atomic settlement guarantee that counterparties can trust the finality and integrity of trades without relying on opaque, off‑chain reconciliations.

Canton Coin and the Burn–Mint Equilibrium

Canton Coin (CC) is the native utility token of the Global Synchronizer and the economic backbone of the Canton Network. Unlike many cryptoassets that launched via ICOs, premines, or large insider allocations, CC was introduced only after the Global Synchronizer went live on the public mainnet, with no pre‑existing supply given to founders, employees, or venture capital investors. Its issuance is entirely tied to live network participation: new CC is minted as a reward when participants operate validator infrastructure, run super validator nodes, or build applications that generate measurable activity on the network. This approach is meant to align token distribution with actual contribution rather than with early access to capital or private deals.

The central design principle behind CC’s economics is what Canton describes as a burn–mint equilibrium model. Instead of relying on fixed issuance schedules disconnected from usage, or on artificially scarce supplies aimed at maximizing speculative value, Canton ties both token creation and destruction to real network activity. On the mint side, the total supply of CC follows a steady, predefined supply curve, which determines how many coins are made available to be claimed over time. These coins are not created automatically; they only enter circulation when participants add measurable utility to the network, such as by operating validator infrastructure, running the decentralized Global Synchronizer, or building and operating applications that attract user activity.

The current phase of the minting curve, which covers roughly 1.5 to 5 years after mainnet launch, allocates the majority of emissions to application providers. According to a breakdown from Zenith, a project that integrates an EVM environment with Canton, application providers currently receive about 62 percent of newly minted CC, validators receive 18 percent, and super validators receive 20 percent. A Protocol Development Fund established under CIP‑0082 receives 5 percent of total emissions, taken pro rata from the other reward categories, to finance ecosystem grants, security audits, and tooling. This distribution is intentionally tilted toward builders of applications that drive real usage, with the goal of shifting value gradually away from pure infrastructure provision and toward products and markets that users actually engage with.

On the burn side of the equilibrium, CC is consumed through transaction fees and other network charges. Canton’s materials emphasize that the value of CC is not based on artificial scarcity but is instead governed by real network utility, with minting and burning adjusting supply to support sustainable growth as global finance moves onchain. While detailed fee mechanics can be complex, coverage from Messari and ecosystem contributors indicates that fees are anchored to fiat terms, often denominated in U.S. dollar equivalents, and paid in CC, with burn parameters adjusting dynamically based on activity and price levels. This means that as the network becomes more heavily used, demand for CC to pay fees increases, and a portion of those tokens is permanently removed from circulation, counterbalancing ongoing emissions.

A crucial aspect of Canton’s narrative is the absence of a premine, founder allocation, or VC distribution. Zenith emphasizes that every CC in existence was minted through active participation in the network after launch, with no special carve‑outs for insiders. This stands in contrast to many layer‑1s where large fractions of the supply are controlled by early backers before public trading begins. However, the resulting distribution is not necessarily egalitarian: because the earliest and most capable participants tend to be large institutions and specialized infrastructure providers, CC ownership has been highly concentrated in practice. A filing related to a proposed Grayscale Canton ETF notes that around 100 wallets hold approximately 89 percent of the current CC supply, highlighting the extent of concentration among early network participants. This dynamic has fueled ongoing debate about centralization risk, particularly as the token becomes more visible in public markets.

The Protocol Development Fund funded with 5 percent of emissions is intended to mitigate some of these concerns by supporting a broader base of developers and ecosystem contributors. Administered through the Canton Foundation, the fund provides grants for building applications, tooling, security infrastructure, and other public goods, with governance and quarterly reporting designed to ensure transparency and accountability. By dedicating a slice of issuance to open‑source and community‑beneficial work, the network aims to grow a more diverse ecosystem of builders who can, over time, claim a meaningful share of new CC emissions through their contributions.

Zenith’s integration with Canton provides a concrete example of how application activity feeds into the burn–mint equilibrium. Every EVM transaction executed on Zenith is represented as Canton activity and routes through the Canton protocol, meaning that Zenith usage consumes synchronizer resources and contributes to CC’s economic flows. Because this activity is accounted for at the Canton level, no value “leaves” the network even though developers and users interact with an EVM environment. Featured applications that generate significant transaction volume can earn CC based on the usage they create, aligning incentives between front‑end products and the underlying infrastructure.

Overall, Canton’s tokenomics are designed less around creating a speculative asset and more around rewarding those who operate the network and build the markets on top of it. The burn–mint equilibrium, the emphasis on application‑driven emissions, and the absence of a premine all reflect an attempt to make CC’s value a function of onchain economic activity rather than purely of narrative or scarcity. Whether this design will produce more stable or sustainable market behavior remains an open question, particularly as CC gains exposure through secondary trading and potential ETF products.

Canton Network public mainnet launch with 45 founding institutional participants including Goldman Sachs and BNY Mellon

Digital Asset raises $135M led by DRW Venture Capital and Tradeweb, with DTCC, BNP Paribas, Citadel Securities, Circle, and Paxos participating

DTCC and Digital Asset partner to tokenize DTC-custodied U.S. Treasury securities on Canton, targeting real-time settlement in 2026

Visa joins Canton Network as first payments Super Validator for privacy-preserving bank settlement

Digital Asset closes $355M funding round led by a16z crypto to accelerate Canton capital markets buildout

- 2026-05milestone

LayerZero deploys on Canton, bridging $8T+ monthly institutional RWA volume to 165+ public chains

- 2026-06regulatory

Lloyds and Archax execute UK's first sterling tokenised deposit Gilt trade on Canton public blockchain infrastructure

Institutional Adoption and Real‑World Asset Tokenization

One of the most distinctive aspects of Canton’s story is the extent of institutional adoption already visible across key segments of capital markets. Messari notes that the network has attracted production and announced deployments from Broadridge, DTCC, and J.P. Morgan across use cases such as repo, collateral, tokenized Treasuries, tokenized bank deposits, and payments infrastructure. This breadth underscores Canton’s ambition to become the connective tissue for onchain representations of traditional financial instruments, often referred to as real‑world assets (RWAs).

Repo markets are among the most advanced Canton use cases. Broadridge’s Distributed Ledger Repo (DLR) platform, described as the world’s largest institutional platform for settling tokenized real assets, runs on Canton and has processed hundreds of billions of dollars in daily transactions. In August of a recent year, Broadridge reported that DLR processed more than 280 billion dollars in average daily repo transactions, totaling about 5.9 trillion dollars for the month. A subsequent update highlighted that Broadridge now processes roughly 340 to 400 billion dollars in repo transactions on Canton every day. Given that Japan’s repo market alone handles approximately 1.5 trillion dollars in daily exposures, these figures suggest that a meaningful slice of global repo activity is already settling on Canton rails.

Canton’s impact on repo is not simply a matter of digitizing existing workflows; it fundamentally changes how collateral and cash can move. Onchain repo enables atomic settlement between cash and collateral, dramatically reducing settlement risk compared to traditional, multi‑step processes. It also allows for near‑instantaneous mobilization of collateral across counterparties and markets, including outside traditional market hours, because the underlying assets and obligations are represented as programmable tokens on a shared network. Recent onchain repo trades have demonstrated how institutions can use Canton to access funding and move collateral in real time, with competitive price discovery through request‑for‑quote workflows and confidential payment flows that mirror existing market structures. For large dealers and buy‑side firms managing trillions in repo exposures, these features translate into tangible balance‑sheet and liquidity benefits.

The partnership between DTCC and Digital Asset to tokenize DTC‑custodied U.S. Treasury securities on Canton is another signal of how deeply the network is embedding itself into core market infrastructure. DTCC announced that it will leverage its ComposerX suite of platforms to enable tokenization of a subset of Treasury securities held at the Depository Trust Company (DTC), with an initial deployment targeted for 2026. The initiative uses Canton as the underlying blockchain, taking advantage of its privacy‑preserving, interoperable architecture to represent Treasuries as onchain assets that can be used in a variety of downstream applications. For example, tokenized Treasuries on Canton can serve as collateral in repo platforms, be used in tokenized funds, or serve as the underlying reference for new indices and structured products.

Canton’s materials also reference broader moves by Wall Street to bring benchmarks onchain, including S&P’s tokenization of a Treasuries index. While details may vary by product, the general pattern is that core reference assets—such as U.S. government securities—are being mirrored as onchain tokens that can plug directly into Canton‑based applications. This allows funds, structured products, and even retail‑facing vehicles to gain exposure to these assets with programmable settlement and composability, without relying on synthetic wrappers or off‑chain representations.

Stablecoin‑based payments and settlement are another pillar of Canton’s institutional adoption story. Visa announced a collaboration with Brale to explore using a U.S. dollar‑backed stablecoin, SBC, for private settlement of institutional payments on the Canton Network. The proof of concept aims to evaluate how privacy‑enabled blockchain infrastructure can support faster, more programmable settlement while helping financial institutions and payment companies maintain strict control over the visibility of sensitive transaction data. Because SBC is natively supported on Canton, the project can test real‑world payment flows where fiat onramps, stablecoins, and recipient institutions all interact on a shared, privacy‑preserving ledger, rather than relying on external bridges or parallel systems. For Visa and its partners, this is an experiment in how to bring existing card and payment ecosystems onto blockchain rails in a way that meets institutional requirements.

Beyond Treasuries, repo, and stablecoins, the Canton ecosystem encompasses a wide variety of tokenized real‑world assets. Digital Asset notes that the network already supports deployments across bonds, money market funds, alternative funds, commodities, repos, mortgages, life insurance, and annuities. These are not merely theoretical experiments; Broadridge’s DLR platform, for instance, settles tokenized collateral and cash in production volumes, and Messari highlights live or emerging applications in areas such as tokenized bank deposits, payments infrastructure, and collateral mobility. Canton’s pitch is that these are native onchain assets, not synthetic wrappers that simply track off‑chain instruments; the underlying ownership and settlement logic lives directly on the network.

Market data and analytics are following suit. Broadridge’s DLR market data has been made available through a Kaiko data application on Canton, bringing institutional‑grade repo analytics onto the same network where the underlying transactions occur. This tight integration of trading, settlement, and data services is characteristic of Canton’s approach: once assets and workflows are represented onchain, multiple services can be built around them—risk management, reporting, analytics—without sacrificing privacy or requiring data duplication across siloed systems.

Taken together, these deployments illustrate why Canton is increasingly framed as “infrastructure for markets” rather than as a standalone trading venue or DeFi ecosystem. Repo, Treasuries, bank deposits, stablecoins, and various fund structures are all being tokenized directly on Canton and integrated into existing institutional workflows. For crypto‑native observers, this represents a different path to real‑world asset adoption: instead of creating crypto‑first products and asking institutions to adapt, Canton starts from institutional realities and uses blockchain to streamline, connect, and extend existing markets.

RedStone charts new oracle waters for Daml, letting Canton apps anchor shared prices while keeping each ledger hidden below the surface

Canton already claims nearly 400 ecosystem participants and trillions in RWAs leveraging the network, so oracle plumbing is not a side quest. If RedStone can make a shared price object usable across Daml apps without letting the oracle see counterparties or balances, you get closer to cross-app repo/collateral workflows without turning Canton into an Ethereum-style public mempool. The weak point shifts from privacy to feed governance: stale NAVs, source disputes, and synchronized liquidation logic matter more when banks are routing tokenized Treasuries, funds, and deposits through the same price surface.

Infrastructure, Validators, and How Institutions Participate

Canton’s operational model revolves around validators, synchronizer operators, and application providers, many of whom are large financial institutions or specialized infrastructure firms. Validators are nodes that connect to one or more synchronizers, participate in consensus, and help order and confirm transactions across the network. Super validators, a subset with enhanced responsibilities, often work closely with the Global Synchronizer Foundation to ensure the robustness and security of the main synchronization layer. Because Canton is permissionless at the protocol level, any entity that meets the technical and economic requirements can, in principle, operate a validator and contribute to the network’s decentralization.

In practice, many institutions choose to work with specialized providers that offer “node‑as‑a‑service” solutions tailored to Canton. The Canton Foundation maintains resources for validators and points to white‑label validator node offerings operated by approved Node‑as‑a‑Service partners. These services handle infrastructure setup, 24/7 operations, and compliance with protocol standards, allowing institutions to focus on building applications or integrating Canton into their existing workflows. IntellectEU, for example, advertises a Validator Node‑as‑a‑Service offering that manages infrastructure, operational monitoring, and adherence to Canton’s privacy and security requirements. This division of labor mirrors patterns seen in other blockchain ecosystems, where professional operators run nodes on behalf of enterprises that may not want to manage the technical complexity themselves.

Running core infrastructure on Canton is not limited to validating transactions. Super validators and synchronizer operators play a central role in the network’s economics and governance. They earn CC rewards for providing critical services such as consensus, transaction ordering, and operation of the Global Synchronizer, which coordinates atomic settlement across applications. Many institutions that apply to become super validators leverage partners for end‑to‑end operational support, from drafting CIPs and monitoring network performance to ensuring compliance with governance and technical standards. This has given rise to a small but growing ecosystem of service providers specializing in Canton infrastructure, which further lowers the barrier to entry for traditional firms.

Developers, meanwhile, interact with Canton through a combination of native smart contract tooling and integrated environments such as Zenith. Zenith provides an EVM‑compatible execution environment whose transactions are represented as Canton activity and routed through the Canton protocol. Every EVM transaction on Zenith consumes synchronizer resources and participates in Canton’s burn–mint equilibrium, ensuring that value and activity are accounted for at the layer‑1 level. This design allows developers familiar with Ethereum tooling and Solidity to build applications that benefit from Canton’s privacy and interoperability features, without needing to learn an entirely new programming paradigm from scratch.

From an institutional perspective, integrating with Canton involves more than just deploying smart contracts. Firms must consider how to map their existing legal entities, account structures, and risk frameworks into onchain representations. For example, a bank that wants to offer onchain repo on Canton might need to define tokenized securities, design collateral management logic, integrate stablecoin or deposit‑based settlement rails, and build interfaces to internal risk and regulatory reporting systems. Node‑as‑a‑service providers and Canton‑focused consultancies often help with this translation, ensuring that onchain behaviors match off‑chain obligations and that applications can scale to production volumes.

The path from pilot to production on Canton typically requires building robust operational infrastructure that institutions can depend on. This includes resilient node setups with redundancy and disaster recovery, continuous monitoring and alerting, detailed logging for audit purposes, and integration with existing security, identity, and compliance systems. Because Canton is designed to carry high‑value, regulated financial transactions, operational standards must match or exceed those of traditional critical market infrastructure. Over time, as more institutions move from pilots to live deployments, best practices around node operations, key management, change control, and incident response are emerging as an important part of the ecosystem.

Approximately 100 wallets hold roughly 89% of Canton Coin supply, creating acute concentration risk for a network marketing itself on institutional trust and broad participation.

DAML-based contracts reduce common EVM attack vectors, but Canton-specific logic handling $6T+ in tokenized RWA carries unquantified tail risk with limited public audit history relative to battle-tested EVM environments.

The permissioned-validator architecture is designed for compliance, but concurrent tokenization of U.S. Treasuries, UK Gilts, and Swiss-custody assets exposes Canton to fragmented and still-evolving cross-jurisdictional securities regulation.

The GlobalSyncFdn has grown to 30+ members including HSBC and BNP Paribas, but founding institutional validators retain outsized influence, creating governance capture risk if large participants align against smaller network members.

Retail depth for CC remains thin despite AMINA's FINMA-regulated custody launch; supply concentration and an institutionally gated validator structure structurally limit open-market liquidity.

CC's outperformance during broader crypto stress reflects speculative positioning on institutional adoption timelines; if DTCC or other flagship deployments slip, the thesis-driven premium unwinds faster than underlying network utility would justify.

Canton in Crypto Markets: Trading, Liquidity, and ETFs

Although Canton is institution‑first in its design, it increasingly intersects with broader crypto markets through its native token and onchain assets. Canton Coin (CC) serves as the medium for paying transaction fees and rewarding infrastructure and application providers, and as such it is a natural candidate for trading on centralized and decentralized exchanges. As the network’s utility grows, secondary markets for CC have attracted the attention of crypto investors looking to gain exposure to institutional onchain infrastructure, rather than only to consumer‑oriented DeFi platforms.

One of the most visible developments on this front is the move by Grayscale to file for a Canton ETF that would hold CC as its underlying asset. According to a report on the filing, the proposed Grayscale Canton ETF would provide investors with exposure to the native token of the Canton Network, allowing them to gain CC exposure through traditional brokerage accounts rather than directly holding tokens. The filing also highlighted that a small number of wallets currently hold a large majority of CC’s supply—around 100 wallets controlling approximately 89 percent—raising questions about liquidity, price discovery, and concentration risk. If approved, such an ETF could increase demand for CC and improve its accessibility, but it would also shine a brighter regulatory and public spotlight on Canton’s economic and governance structures.

Stablecoins and other Canton‑native assets provide additional bridges into the broader crypto ecosystem. The SBC stablecoin used in Visa and Brale’s Canton settlement pilot is one example of a fiat‑backed digital asset whose onchain representation could be integrated with crypto exchanges, custody platforms, and onchain money markets. Stablecoins issued on Canton can, in principle, be listed on centralized exchanges, used as collateral in DeFi protocols, or integrated into cross‑chain liquidity networks, provided that appropriate compliance controls are in place. Coverage of the ecosystem has also noted centralized exchange support for some Canton‑native assets, such as stablecoins used for repo and payment applications, with more assets expected to follow as integration matures.

Canton’s emphasis on native issuance rather than synthetic wrappers is significant for crypto markets. When bonds, equities, or funds are represented as native tokens on Canton, the legal and operational settlement of those instruments occurs directly onchain, rather than being mirrored by off‑chain custodians whose records remain authoritative. This reduces the complexity and risk associated with wrapped assets and makes it easier to reason about ownership and settlement across multiple applications. For crypto investors, it means that exposure to Canton‑based RWAs may more closely track the underlying instruments, with fewer layers of indirection and counterparty risk.

At the same time, Canton’s privacy model complicates some of the transparency assumptions that crypto markets often rely on. Because transaction details and positions are not globally visible, onchain analytics and DeFi‑style composability look different than they do on transparent chains. Liquidity pools, AMMs, and public order books are less central to Canton’s design than request‑for‑quote trading, bilateral or multilateral workflows, and institutionally governed venues. For traders used to monitoring public mempools and onchain order flow, Canton presents a more opaque environment where pricing and activity are often mediated by existing market operators and where data is shared on a need‑to‑know basis.

Nevertheless, as Canton’s token model and onchain assets gain traction, crypto markets are likely to respond with new instruments and strategies. Derivatives on CC, structured products referencing Canton‑based RWAs, and cross‑chain arbitrage strategies that combine Canton assets with those on other blockchains are all foreseeable. The challenge for market participants will be to navigate Canton’s institutional guardrails—KYC, privacy, controlled access—while still harnessing the programmability and composability that define crypto markets more broadly.

Risks, Criticisms, and Open Questions

As Canton’s profile has risen, so have questions and criticisms about its design, governance, and implications for the broader crypto ecosystem. One recurring concern is centralization, both in terms of token ownership and in the operation of critical infrastructure such as the Global Synchronizer. The Grayscale ETF filing’s note that 100 wallets hold nearly 90 percent of CC’s supply underscores how concentrated ownership currently is, likely reflecting the dominance of early institutional participants and infrastructure providers in the minting process. While the absence of a premine or VC allocation is a strong narrative point, it does not guarantee a broad distribution if only a small set of well‑resourced actors can meaningfully contribute to network activity in the early years.

Centralization concerns extend to governance and infrastructure operation. The Global Synchronizer Foundation and associated super validators have substantial influence over transaction ordering, protocol upgrades, and the approval of new CIPs, raising questions about how decentralized decision‑making truly is in practice. Critics argue that a network whose founding and primary operators are deeply embedded in traditional finance and venture capital could end up replicating existing power structures under the guise of decentralization. Supporters counter that the governance model is pragmatic given the regulatory stakes and that over time the set of validators, super validators, and application providers will broaden as more participants join and as CC emissions flow increasingly to builders rather than to infrastructure providers.

Regulatory uncertainty is another risk factor, particularly as Canton touches sensitive areas such as tokenized Treasuries, stablecoins, and payments. While partnerships with DTCC and Visa suggest that the network is operating within frameworks acceptable to key regulators, the broader regulatory environment for tokenization and crypto remains fluid. Questions about how tokenized securities are treated under existing laws, how stablecoin issuers are regulated, and how cross‑border data and capital flows are managed on privacy‑enabled blockchains have not been fully resolved. Canton’s close collaboration with systemically important institutions may help it navigate these uncertainties, but it also exposes the network to shifts in policy and supervisory expectations.

Technical and operational risks must also be considered. Canton’s architecture is more complex than that of traditional monolithic blockchains, involving multiple synchronizers, privacy‑preserving smart contracts, and sophisticated access control logic. This complexity increases the difficulty of auditing systems, verifying security properties, and ensuring that implementations across different institutions are correct and interoperable. Bugs or misconfigurations in privacy logic, token standards, or synchronizer implementations could have far‑reaching consequences, particularly when large volumes of high‑value assets are involved. Operational failures at key validators or synchronizer operators, whether due to technical issues or external attacks, could pose systemic risks to markets that have come to rely on Canton for settlement.

Finally, Canton competes in a crowded landscape of institutional‑focused blockchain and DLT platforms. Other layer‑1 chains, enterprise DLT frameworks, and bank‑run networks all vie to become the primary rails for onchain finance. Canton’s differentiators—configurable privacy with composability, the burn–mint equilibrium, and existing institutional adoption—are significant, but they do not guarantee dominance. The long‑term outcome may not be a single winning chain but a heterogeneous landscape in which Canton is one of several key networks, interconnected through bridges, standards, or shared custody arrangements. The extent to which Canton can maintain its momentum, foster a diverse developer ecosystem, and continue to attract marquee institutional projects will shape its role in that landscape.

Conclusion

Canton Network occupies a distinctive position in the evolution of blockchain infrastructure for finance. It is a public, permissionless layer‑1 protocol whose architecture, privacy model, and governance have been engineered from the outset to meet the needs of regulated institutions. Instead of retrofitting consumer‑oriented DeFi primitives to institutional use, Canton approaches the problem from the opposite direction: it starts with the realities of repo markets, securities settlement, stablecoin payments, and custody chains, and then uses blockchain techniques—atomic settlement, shared infrastructure, programmable contracts—to streamline and connect those workflows.

Technically, Canton’s network‑of‑networks design and use of synchronizers allow it to deliver atomic, cross‑application interoperability without relying on a globally replicated state. Its privacy‑preserving smart contract environment ensures that institutions can keep sensitive data confidential while still benefiting from shared consensus and settlement, addressing one of the central obstacles to institutional blockchain adoption. Token standards like CIP‑0112’s Token Standard V2 embed institutional requirements such as batch settlement, prefunded trading, and multi‑tier custody chains directly into the protocol.

Economically, Canton Coin’s burn–mint equilibrium and utility‑driven issuance model seek to align token value with real network usage rather than with artificial scarcity or speculative hype. The distribution of emissions across infrastructure providers, application builders, and a Protocol Development Fund reflects a deliberate attempt to reward those who make the network useful, while the fair‑launch narrative emphasizes that CC supply is earned through participation. At the same time, concentration of CC among early participants and the central role of the Global Synchronizer Foundation raise valid questions about decentralization that the ecosystem will need to address as it matures.

On the adoption front, Canton’s progress is notable. Broadridge’s DLR platform is settling hundreds of billions of dollars in repo transactions on Canton each day, making it arguably the largest institutional platform for tokenized real assets. DTCC’s decision to tokenize DTC‑custodied U.S. Treasuries on Canton by 2026, along with moves to bring Treasuries benchmarks onchain, signals that core pieces of market infrastructure are beginning to rely on it. Visa’s stablecoin settlement pilot with Brale showcases how Canton’s privacy‑enabled rails can support programmable payments for mainstream financial institutions. The broader ecosystem spans tokenized bonds, funds, commodities, mortgages, insurance products, and bank deposits, with more than 150 applications live or in development according to Messari.

For a crypto news audience, Canton is therefore not just another layer‑1 chain but a case study in how onchain infrastructure can be built around institutional constraints and opportunities. It demonstrates that privacy, compliance, and interoperability can be combined in a public blockchain, and that large financial institutions are increasingly willing to move real assets and core workflows onto such networks when their requirements are met. The network’s success or failure will have implications not only for its own stakeholders but also for the broader trajectory of real‑world asset tokenization and the convergence of traditional finance with crypto‑native markets.

Outlook

Looking ahead, Canton’s trajectory will likely be shaped by several interlocking developments. On the institutional side, the transition of more pilots into full‑scale production—particularly the DTCC Treasury tokenization project and expanded repo, collateral, and payments deployments—will test the network’s ability to operate as systemically important infrastructure. As volumes grow and more asset classes move onchain, the robustness of Canton’s synchronizers, validator set, and privacy mechanisms will come under increasing scrutiny from both market participants and regulators.

On the market side, the evolution of CC as a traded asset and the potential approval of a Canton ETF will influence how crypto investors perceive and engage with the network. If Canton succeeds in anchoring token value to real usage through its burn–mint equilibrium while expanding access via regulated investment products, it could become a template for how institutional‑grade layer‑1s align their token economics with their role in financial markets. At the same time, pressures to decentralize ownership and governance, and to address concentration concerns highlighted in regulatory filings, will intensify.

Finally, Canton’s competition and collaboration with other blockchains will help determine whether institutional onchain finance coalesces around a small number of dominant networks or remains fragmented across many specialized platforms. Canton’s emphasis on native assets, privacy‑preserving interoperability, and institutional partnerships gives it a strong foundation. Whether it can translate that foundation into enduring, broad‑based adoption across global markets is the key question that will define its role in the next phase of onchain finance.

Latest Canton Network news

Sources

- https://www.canton.network

- https://www.tradeweb.com/newsroom/media-center/in-the-news/digital-asset-raises-$135-million-to-accelerate-adoption-of-canton-network/

- https://www.broadridge.com/press-release/2025/billions-in-average-daily-processed-trade-volumes-on-broadridge-dlt-repo-platform

- https://www.canton.network/blog/a-technical-primer

- https://www.youtube.com/watch?v=32IvuhZpjk4

- https://canton.foundation/validators/

- https://www.canton.network/why-canton

- https://x.com/CantonNetwork/status/2064143438216347763

- https://www.canton.network/blog/messari-report-understanding-canton-network

- https://fr.tradingview.com/news/stocktwits:108cd7392094b:0-grayscale-files-for-canton-etf-targeting-a-token-where-100-wallets-hold-89-of-supply/

- https://investor.visa.com/news/news-details/2026/Visa-and-Brale-Explore-Private-Stablecoin-Settlement-for-Institutional-Payments/default.aspx

- https://x.com/CantonNetwork/status/2067000010672156880

- https://x.com/CantonNetwork/status/2068087929298108533

- https://www.intellecteu.com/services/canton-network-support-blockchain-development

- https://blog.digitalasset.com/press-release/digital-asset-355m-funding-canton-capital-markets

- https://zenith.network/resources/blog/understanding-canton-1-canton-coin-economics-burn-mint-equilibrium

- https://x.com/CantonNetwork/status/2065499876138406106

- https://www.dtcc.com/news/2025/december/17/dtcc-and-digital-asset-partner-to-tokenize-dtc-custodied-us-treasury-securities

Community notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…