Deep explainer on crypto markets, from Bitcoin spot and USDC DeFi lending to perpetual futures and prediction markets, covering microstructure, regulation, AI trends, risks, and what growing event-based markets mean for traders.

+74 sources across the wider coverage universe

Coinbase acquires Hyperliquid's USDH deployer, Native Markets, to switch All USDH into USDC2026-05

Coinbase acquires Hyperliquid's USDH deployer, Native Markets, to switch All USDH into USDC2026-05 Leviathan prediction markets expose agent autonomy gap as operator-directed insider trading plays out in real time2026-04

Leviathan prediction markets expose agent autonomy gap as operator-directed insider trading plays out in real time2026-04 Former SEC Chief Economist backs a16z-backed safe harbor, arguing tokenized securities on DeFi can cut costs, enable 24/7 markets, and boost transparency despite regulatory tradeoffs2026-04

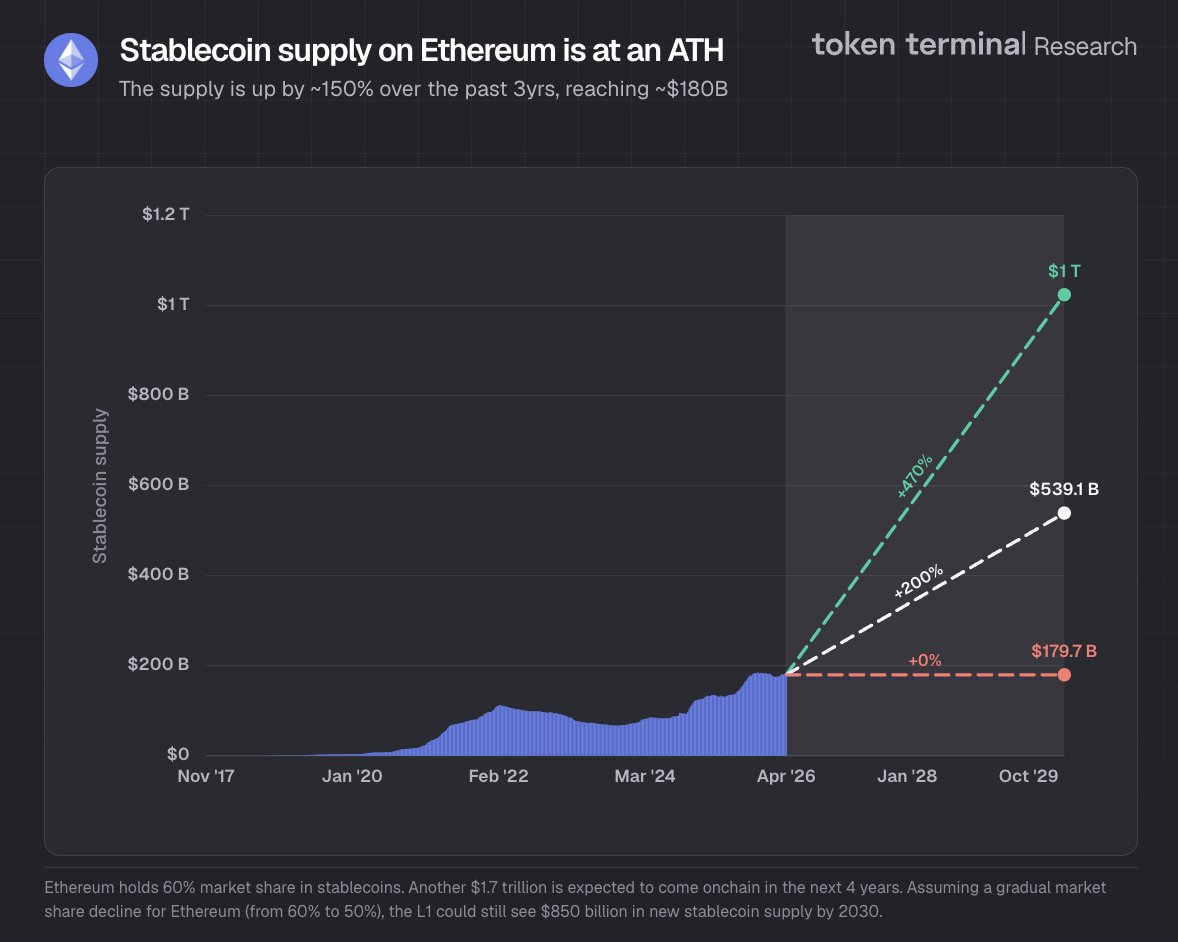

Former SEC Chief Economist backs a16z-backed safe harbor, arguing tokenized securities on DeFi can cut costs, enable 24/7 markets, and boost transparency despite regulatory tradeoffs2026-04 Ethereum stablecoin supply hits $180B ATH with 60% market share, up 150% in three years2026-04

Ethereum stablecoin supply hits $180B ATH with 60% market share, up 150% in three years2026-04 New report breaks down leverage models in prediction markets, highlighting $15M–$50M revenue potential while exposing risks tied to venue architecture, liquidation design, and jump volatility2026-04

New report breaks down leverage models in prediction markets, highlighting $15M–$50M revenue potential while exposing risks tied to venue architecture, liquidation design, and jump volatility2026-04 Aerospace and defense supplier Arxis targets up to $1.06B in US IPO, aiming to capitalize on rising demand for electronic and mechanical components across global defense markets2026-04

Aerospace and defense supplier Arxis targets up to $1.06B in US IPO, aiming to capitalize on rising demand for electronic and mechanical components across global defense markets2026-04

Markets in Crypto: Spot, Derivatives, and Prediction Markets Explained

In finance and crypto, a market is any system that brings together buyers and sellers to determine a price and exchange value. In digital assets, that idea extends from familiar Bitcoin spot markets to onchain lending pools, perpetual futures, and prediction markets where traders wager on everything from elections to AI launches.

Markets are the infrastructure that makes crypto meaningful rather than theoretical, turning blockchains and tokens into tradable, priced assets with real-world consequences. They set the exchange rate between Bitcoin and dollars, the yield on stablecoins like USDC, the funding rates on perpetual futures, and the implied odds that a candidate wins an election or a protocol ships an upgrade on time. As crypto has matured, market design has become more diverse and experimental: centralized exchanges sit alongside automated market makers, tokenized stocks trade on BNB Chain, and event-based contracts on platforms like Kalshi, Polymarket, Coinbase, and Robinhood let users bet directly on future events. At the same time, recent episodes—from the 85% plunge in the MSUSD stablecoin as a Morpho msY/USDC lending market hit full utilization, to turmoil around Strategy’s STRC preferred stock spilling into Bitcoin and broader crypto sentiment—have underscored how fragile liquidity and confidence can be when market structures come under stress. Prediction markets have hit all-time-high volumes, with a16z data showing more than 10 billion dollars traded in a single week and roughly 1.5 billion dollars in open interest, even as they attract fresh scrutiny from regulators and lawmakers. Crypto derivatives and onchain perpetuals are simultaneously moving toward the regulatory mainstream, with the U.S. Commodity Futures Trading Commission (CFTC) chair discussing pathways for onchain platforms like Hyperliquid to come onshore, while large incumbents such as Charles Schwab prepare yes-or-no options on the S&P 500 in partnership with Cboe that resemble prediction market contracts. Against that backdrop, understanding what “markets” are—how spot, derivatives, DeFi lending, and prediction markets actually work, how they fail, and how regulation is evolving—is now core literacy for anyone in crypto, from casual traders to protocol designers.

What Do We Mean by “Markets”?

At the most basic level, a market is a mechanism for price discovery and exchange. In traditional finance that mechanism might be a centralized order book on a stock exchange, a bilateral negotiation between institutions in the bond market, or an auction in a commodity pit. In crypto, it may be an order book on Coinbase, a Uniswap pool on Ethereum, a perpetual futures venue like HTX or Hyperliquid, or an event-based platform such as Kalshi or Polymarket. Despite their different interfaces, all of these venues perform the same core function: they coordinate the beliefs and preferences of many participants into a single observable output, usually a price and a quantity.

Markets exist because individual buyers and sellers do not know in advance who will take the other side of their trade or at what price. A market solves that coordination problem by aggregating orders and enforcing rules for matching and settlement. In an order book, the rule is that the best bid meets the best ask; in an automated market maker, a pricing formula updates the exchange rate between two tokens based on their relative balances; in a prediction market, binary contracts pay one if an event occurs, so the trading price between zero and one reflects the crowd’s implied probability. The structure of a market—the rules for order matching, margining, collateral, and settlement—shapes which participants can enter, what risks they face, and how resilient prices are under stress.

Crypto adds an additional dimension because markets can be embedded directly in smart contracts. Instead of relying on a centralized venue, traders interact with code on a blockchain that holds collateral, enforces trading rules, and settles positions transparently onchain. That is true for automated market makers exchanging USDC for tokens, for DeFi lending pools setting interest rates as utilization rises, and for onchain prediction markets where event contracts are minted, traded, and resolved via oracles. This onchain architecture allows markets to be globally accessible and composable, but it also exposes them to new forms of smart contract risk, oracle manipulation, and liquidity fragmentation across chains.

Finally, “markets” are not only places where prices form; they are also social systems that encode expectations, narratives, and power. When Ray Dalio warns that U.S. equity markets are “highly concentrated in a small group of large AI-related companies” and may deliver negative real returns over the next decade, he is describing how flows and expectations can cluster around particular themes, creating fragility beneath seemingly orderly surface prices. Crypto markets exhibit similar narrative clustering, whether around AI tokens, real-world assets, or the “flippening” of one chain overtaking another in market cap. Understanding markets therefore requires thinking both about microstructure—the plumbing of order books and AMMs—and about human behavior and regulation.

BIS says stablecoins fall short as money, warns of emerging-market risks in annual report

$312B of stablecoin float is already a liquidity layer, and USDT alone is about $185B with roughly $88B of that on Tron. BIS can win the taxonomy fight on singleness, elasticity, and integrity and still lose distribution: EM users are not holding USDT because it is pristine money, they are holding it because local banking rails, FX controls, and weekend settlement are worse. Project Agorá/tokenized deposits have to beat that UX in production, not just clear the central-bank checklist.

Readers click 'markets' content at the intersection of structural power shifts — DeFi protocols eating CEX market share, ETFs bridging TradFi capital into on-chain risk — revealing that the underlying pull is not price speculation but watching incumbents lose control of the plumbing.

Crypto Spot Markets: Where Bitcoin and Tokens Trade

Market cap, price, and volume

Spot markets are where actual assets change hands for immediate delivery. In crypto, spot markets determine the price of Bitcoin, Ether, stablecoins like USDC, and thousands of long-tail tokens. Aggregators such as CoinMarketCap track spot prices, market capitalization, and trading volumes across centralized exchanges and decentralized venues, offering a snapshot of global conditions at any moment. On such dashboards, traders see the combined value of all cryptoassets, the dominance of Bitcoin relative to altcoins, and the liquidity available in different trading pairs.

Market capitalization in crypto is generally calculated as the current price of a token multiplied by its circulating supply. This metric is widely used to compare the relative size of different cryptocurrencies, but it can be misleading when large portions of supply are locked, illiquid, or controlled by insiders. Our own coverage on “how to compare cryptocurrencies using market cap data” has emphasized that traders should pair headline market cap with measures like free float, realized cap, volume, and order book depth. A token can have a nominal multi-billion dollar market cap but trade only a few million dollars per day, meaning prices may move violently when large holders sell.

Volume is another key metric. High daily trading volume suggests a thick market in which orders can be executed with less slippage, while thinly traded tokens may show wide spreads and be vulnerable to manipulation. CoinMarketCap’s aggregate crypto market volume figures help frame how active the ecosystem is on any given day, though traders still need to drill down into individual pairs and venues to assess execution quality. In practice, Bitcoin and major stablecoins like USDC and USDT serve as base assets for many markets, with altcoins quoted against them rather than directly against fiat currencies.

Centralized exchanges and fiat on-ramps

Centralized exchanges, or CEXs, remain the main gateways into crypto spot markets for most users. Platforms like Coinbase, Binance, Kraken, and many regional exchanges provide order books where users can trade crypto against fiat or stablecoins, custody services, and often margin or derivatives products. Coinbase’s decision to launch localized offerings such as its India-focused platform underlines how spot markets expand geographically as regulatory and banking rails improve, creating more direct access from local currencies into Bitcoin, Ether, and stablecoins.

On CEXs, order books collect limit and market orders from buyers and sellers. The exchange’s matching engine executes trades, updates balances, and often interacts with internal or external market makers to keep spreads tight. Because users typically do not control the private keys to their deposited assets, they face counterparty and operational risk if an exchange suffers a hack, insolvency, or regulatory shutdown. At the same time, centralized venues can offer deep liquidity and advanced trading features that are challenging to replicate fully onchain, especially for high-frequency or institutional strategies.

The choice of quote asset on centralized exchanges also shapes market dynamics. Many altcoins trade primarily against USDT or USDC rather than directly against dollars, euros, or rupees, which means their effective fiat price depends on both the token–stablecoin pair and the stablecoin–fiat conversion rate on other markets. When a stablecoin depegs or faces confidence issues, as with the dramatic MSUSD drop described later, its pairs can become dysfunctional, transmitting stress into superficially unrelated markets. For mainstream stablecoins like USDC, maintaining a credible one-to-one peg with the U.S. dollar is therefore essential not only for holders but for the health of the broader trading ecosystem.

Onchain DEXs and USDC-based liquidity

Decentralized exchanges, or DEXs, move the trading venue from a company’s servers to smart contracts on blockchains. Automated market makers (AMMs) like Uniswap, Curve, and PancakeSwap use liquidity pools rather than order books, with pools typically holding two or more tokens in a pre-defined ratio. Prices adjust algorithmically as traders swap tokens, and anyone can add liquidity in exchange for a share of trading fees and sometimes additional incentives.

USDC has become a central asset in many DEX liquidity pools because of its perceived stability and broad integration across DeFi protocols. Onchain markets often quote token prices in USDC, and lending platforms like Morpho, Aave, or Compound use USDC pools as primary sources and sinks of liquidity, with interest rates rising as utilization increases. When a particular market, such as the Morpho msY/USDC pool, reaches 100% utilization—as happened during the MSUSD crisis—it means all deposited USDC is lent out, leaving no immediate liquidity for further withdrawals or loans and signaling acute stress. In that sense, onchain markets reveal in real time how stablecoin liquidity and credit conditions evolve.

DEXs and CEXs are increasingly interconnected. Arbitrageurs move funds between platforms whenever price discrepancies arise, and protocols route trades across multiple DEXs and even bridge to centralized venues to seek best execution. This interplay means that shocks in one type of market, whether onchain or off, can propagate rapidly through the system. For traders and builders, understanding how spot markets function across both centralized and decentralized venues is the foundation for grasping more complex structures like derivatives, lending markets, and prediction markets.

Derivatives, Perpetual Futures, and Leverage

Futures, options, and risk transfer

Derivatives are contracts whose value depends on an underlying asset, index, or event. In crypto markets, the most common derivatives are futures, perpetual futures, and options. Standard futures obligate the buyer and seller to exchange an asset at a predetermined price on a specific future date, while options give the holder the right, but not the obligation, to buy or sell at a given strike price before expiry. These instruments allow traders to hedge price risk, gain leverage, or express views on volatility without holding the underlying asset directly.

Derivatives markets play an outsized role in crypto because they can concentrate liquidity and speculative interest. On some days, global futures and perpetuals volume for Bitcoin and Ether far exceeds spot trading. Derivatives can also be highly leveraged: traders may post a small portion of the notional exposure as margin, amplifying both gains and losses. This leverage can drive rapid price swings when markets move sharply, triggering liquidations that cascade through futures and spot markets alike. As a result, regulators closely scrutinize how derivatives venues manage margin, liquidation, and risk.

Perpetual futures versus spot Bitcoin

Perpetual futures, or “perps,” are a crypto-native innovation that has since attracted attention from traditional derivatives exchanges. Unlike standard futures, perps have no fixed expiry date. Instead, they use a funding rate mechanism that periodically pays from one side of the market (longs or shorts) to the other, incentivizing the perp price to stay close to the underlying spot price. A MetaMask explainer highlights how perpetuals give traders platform-dependent exposure: positions are essentially margin-based contracts held on an exchange or onchain protocol, rather than outright ownership of the underlying Bitcoin or token.

In spot Bitcoin trading, buying BTC on a DEX or CEX transfers the asset to your wallet or account, and you own it outright, subject to counterparty or custody risk. In a Bitcoin perpetual futures contract, by contrast, you hold a synthetic exposure whose payoff mirrors BTC’s price movements without requiring the exchange of the underlying asset. This structure is attractive for traders seeking flexible leverage and for exchanges, which can match long and short interest internally. However, it also means that exposure is entirely dependent on the solvency and risk management of the platform, especially in extreme markets.

The spread between perpetual and spot prices, and the pattern of funding rates, provide important signals. When funding is strongly positive and perps trade at a premium, it suggests over-enthusiasm and crowded longs; when funding is negative and prices trade at a discount, fear and short positioning may dominate. These signals have become standard tools for crypto market analysis, just as futures curves and implied volatilities are in traditional commodities and equity derivatives.

New markets, EVAA perps, and market surface expansion

Derivatives markets constantly expand their “surface” by listing new contracts on more assets, including smaller tokens and real-world assets. Our own coverage noted that HTX launched EVAA/USDT perpetual futures with up to 10x leverage, giving traders direct long and short exposure to EVAA and making the token harder to ignore as its derivatives footprint grows. New listings are not limited to major centralized exchanges: orderbook protocols such as Orderly allow DEX builders to plug into shared liquidity and offer hundreds of perp markets, including on equities like Coinbase and other real-world assets, sometimes with leverage up to 100x.

This proliferation of perp markets reflects both demand for speculative tools and the ease with which new contracts can be created in a software-driven environment. Tokenized stock positions, such as those enabled on Venus Protocol’s BNB Chain deployments, can be used as collateral while maintaining price exposure to underlying equities, blending traditional and crypto markets in a composable way. As more platforms launch tokenized stocks, commodities, and indices, crypto derivatives markets increasingly resemble a parallel financial system with its own idiosyncrasies, such as 24/7 trading and onchain settlement.

Regulators have taken notice. Former CFTC and SEC officials have described commodity and crypto derivatives markets as navigating “stormy seas,” with unresolved questions about whether some perps on assets that resemble securities can legally trade on retail-facing platforms. The ongoing debates around perps offered by CME versus onchain protocols, and the discussions between the CFTC and various venues over how to structure perpetual products, illustrate how market design and legal frameworks remain in flux. Yet the clear demand for derivatives suggests they will remain a central part of crypto’s market infrastructure.

Onchain Markets and DeFi Primitives

Lending, money markets, and utilization

Beyond trading venues, DeFi introduces onchain money markets where users lend and borrow assets through smart contracts. Protocols such as Aave, Compound, and Morpho pool deposits of assets like USDC and allow other users to borrow against collateral, with interest rates set algorithmically based on utilization. When utilization is low, borrowing is cheap and deposit yields are modest; as utilization rises, borrowing becomes more expensive and depositors earn more, encouraging additional liquidity.

The MSUSD episode provides a vivid example of how onchain money markets can amplify stress. According to coverage of the incident, the MSUSD stablecoin fell as much as 85% after an entity called Accountable terminated its verification, triggering a crisis of confidence among holders. At the same time, the Morpho msY/USDC market reportedly reached 100% utilization, meaning every USDC deposited in that pool was lent out, leaving no buffer for further withdrawals or new borrowing. This combination of a collapsing asset and a fully utilized lending market is emblematic of DeFi-specific liquidity spirals: as the value of collateral or borrowed assets falls, borrowers may rush to repay or refinance, while lenders demand higher yield, driving rates even higher.

Money markets also interact with prediction markets and derivatives. Event-based platforms may allow positions to be posted as collateral, while perpetual futures protocols often integrate with lending pools to allow cross-margining. In such intertwined systems, a stress event in one corner—for instance a stablecoin depeg—can propagate quickly through collateral valuations, liquidations, and funding rates. For traders and risk managers, monitoring utilization ratios, collateral composition, and liquidation thresholds across DeFi markets has become as important as watching spot prices.

Stablecoins, USDC, and depeg risk

Stablecoins sit at the center of crypto markets as bridge assets between fiat and onchain ecosystems. Fully backed dollar-pegged coins like USDC and USDT aim to maintain a one-to-one value with the U.S. dollar, providing a relatively stable unit of account for trading, lending, and DeFi yields. Algorithmic or partially collateralized stablecoins such as MSUSD, by contrast, rely on more complex mechanisms or diversified collateral, increasing their sensitivity to market shocks and governance decisions.

The MSUSD collapse illustrates how quickly confidence can evaporate. When the verification relationship with Accountable ended, market participants questioned whether the stablecoin was properly backed, leading to a sharp sell-off that drove its price down as much as 85% from the intended peg. As holders dumped MSUSD for safer assets like USDC, liquidity in MSUSD pairs dried up, spreads widened, and lending markets linked to the asset became stressed. Unlike centralized stablecoins that can sometimes rely on issuer buybacks or emergency redemptions, MSUSD’s onchain mechanisms were not sufficient to preserve parity in the face of panic.

For USDC and similar assets, the challenge is different. They are deeply integrated into CEXs, DEXs, derivatives, and money markets, so any perceived weakness in reserves or redemption processes can have system-wide implications. Episodes where USDC has temporarily traded below one dollar due to banking issues have underscored how tightly crypto market functioning is tied to offchain financial institutions. As more stablecoins emerge—from bank-backed tokens to onchain collateralized coins—markets will continue to test which designs are robust under extreme stress.

Tokenized stocks and real-world assets as collateral

DeFi markets have moved beyond native tokens and stablecoins to incorporate tokenized versions of real-world assets, or RWAs. Venus Protocol’s launch of tokenized stocks as collateral on BNB Chain is a notable example: for the first time on Venus, users can post tokenized stock positions as collateral in its core pool while retaining exposure to the underlying stock price movements. That means a trader might hold a tokenized share of a listed company, use it as collateral to borrow USDC or another stablecoin, and then deploy that liquidity elsewhere in DeFi, all without giving up price exposure to the original equity.

This type of market blurs the line between traditional and crypto finance. On one hand, tokenized RWAs can increase capital efficiency, allowing investors to unlock value from their portfolios without going through traditional margin lending channels. On the other, they raise complex questions about custody, corporate actions, regulatory jurisdiction, and information rights. If a tokenized stock is used in a DeFi protocol that experiences a hack, it is unclear how claims would be resolved between onchain token holders, offchain custodians, and the issuer of the underlying stock.

From a market perspective, tokenized RWAs introduce new collateral types and trading pairs, expanding the opportunity set but also increasing the surface area for contagion. If a tokenized stock market suffers a technical failure, it could constrain collateral availability across lending and derivatives platforms, just as a stablecoin depeg would. Nevertheless, RWA markets represent an important frontier for crypto, one that connects onchain capital formation with offchain economic activity.

- 01DeFi lending parameter stress↗

The Llama Lend / crvUSD governance posts and new market launches drew readers tracking whether on-chain credit markets can self-correct under volatility without blowing up.

- 02DEX eating CEX share

A record 14.22% monthly DEX-to-CEX volume ratio made readers confront that decentralized venues are no longer a rounding error against centralized order books.

- 03Bitcoin ETF systemic contagion

Institutional BTC ETF inflows raised a question readers hadn't had to ask before: what happens to crypto markets when TradFi counterparty risk rides in alongside the capital.

- 04NFT market structural collapse

BAYC floor dropping 90%-plus from its all-time high signaled to readers that the NFT collectibles market wasn't in a cycle — it was in a structural reset.

- 05Macro shock crypto correlation

Jamie Dimon's recession warning and DeepSeek's AI rout dragging BTC and Nasdaq together confirmed readers' suspicion that crypto beta to macro events is no longer deniable.

- 06Liquidation cascade accountability

The Synthetix treasurer liquidation and Mango Markets conviction drew readers who want to know who bears the cost when market structure fails — and whether anyone answers for it.

Prediction Markets: Trading on Events Rather Than Assets

Core design and use cases

Prediction markets are platforms where participants trade contracts whose payoff depends on the outcome of future events, rather than the price of a traditional asset. NerdWallet describes them as online venues where people can bet on events such as elections, financial markets, or sports outcomes, with contracts typically paying a fixed amount if the event occurs and zero if it does not. The trading price of a contract between zero and one dollar reflects the market’s implied probability that the event will happen; for example, a contract trading at 0.65 suggests a 65% implied probability before fees and risk premiums.

These event contracts can be structured in various ways. Some platforms use binary contracts that settle at either zero or one, while others offer range or multi-outcome markets—for instance, contracts tied to the winner of a multi-candidate election. Under the hood, many prediction markets use continuous double auctions, just like stock exchanges, while others experiment with automated market maker designs tailored for probabilities. The key attribute is that prices continuously aggregate dispersed information from traders, leading many researchers and practitioners to view prediction markets as powerful forecasting tools.

Use cases are wide-ranging. Political prediction markets track elections, referenda, and legislative outcomes. Financial event markets might cover whether the Federal Reserve will cut rates at its next meeting, whether Bitcoin will trade above a certain level by year-end, or how inflation prints will come in. Other markets cover sports, entertainment, crypto protocol milestones, regulatory decisions, or even scientific and technological breakthroughs. A popular Instagram explainer notes that these platforms let users trade contracts tied to future events including elections, sports, and government actions, but also highlights that they have been drawn into lawsuits over what kinds of events can be listed.

Major platforms and new entrants

The prediction market landscape spans specialized venues and large, regulated institutions moving into similar territory. Kalshi operates as a federally regulated exchange and prediction market in the United States, where users can buy and sell event contracts on a wide range of economic, political, and other real-world outcomes under CFTC oversight. Polymarket, which describes itself as the world’s largest prediction market, allows users to trade on future events across news, politics, crypto, and other categories, primarily using stablecoins onchain. Coinbase and Robinhood have each launched “prediction market” or event contract products, framing them as regulated ways for customers to trade views on real-world events, from sports to economics.

In addition to these pure-play platforms, large brokers and exchanges are rolling out products that look functionally similar to prediction markets. According to reporting based on Wall Street Journal coverage, Charles Schwab is working with Cboe Global Markets to introduce yes-or-no options tied to the S&P 500 index, allowing customers to wager on whether the index will be above or below specific levels at defined times. A related report notes that these all-or-nothing options mark Schwab’s first move into S&P 500 event-based options, explicitly linking the firm to the fast-growing prediction market–like sector that also includes Coinbase, Robinhood, Polymarket, and Kalshi. These developments blur boundaries between traditional listed options, binary event contracts, and consumer-facing “prediction” products.

The sector’s growth has been rapid. A16z crypto recently highlighted that prediction markets hit a record approximately 10.8 billion dollars in weekly volume and nearly 1.5 billion dollars in open interest, both all-time highs achieved in the same week. That surge reflects not only increased speculative interest but also broader acceptance of prediction markets as legitimate tools for information aggregation and trading, especially as major brands embrace event contracts under regulatory frameworks similar to those governing futures exchanges.

Regulation, insider trading, and integrity

With growth has come scrutiny. The legal status of prediction markets varies widely by jurisdiction, with some regulators treating them as derivatives, others as gambling, and others as unregulated speech unless they involve real money. In the United States, the CFTC has asserted jurisdiction over real-money event contracts on economic indicators and political events, leading to contentious disputes with platforms over whether election markets can be offered to retail users. An Instagram explainer on prediction markets explicitly notes that these platforms have been involved in lawsuits over the types of markets they can list, underscoring the unresolved regulatory classification issue.

Concerns about insider trading have moved to the forefront. Senators introduced the bipartisan Public Integrity in Financial Prediction Markets Act of 2026, which would prohibit certain government officials from using non-public information to trade prediction market contracts on matters related to their official duties. The bill defines “insider information” as any non-public information that a reasonable investor would consider important in making a decision related to a prediction market contract and sets penalties for violations as the greater of 500 dollars or double the profit earned from the transaction. In parallel, a Republican lawmaker in the House, Rep. Bryan Steil, has proposed a provision that would ban congressional lawmakers and their families from betting on prediction markets, reflecting bipartisan unease with officials speculating on the outcomes of policies they influence.

Market integrity concerns are not hypothetical. Our newsroom has reported on a suspected insider who allegedly made approximately 24.25 million dollars by betting on markets using three wallets and funneling profits to Binance, raising questions about whether they acted on privileged information and whether onchain transparency is sufficient to deter such behavior. Regardless of the ultimate facts in that case, it illustrates a core tension: prediction markets thrive on information, but they risk becoming mechanisms for monetizing non-public knowledge in ways that undermine public trust in institutions.

Regulatory leaders also grapple with whether prediction markets serve the public interest. SEC Chair Gary Gensler has reemerged in litigation involving prediction market platforms, as noted in recent coverage, with debates centering on whether certain event contracts constitute unregistered securities offerings. At the same time, proponents argue that prediction markets can improve policy and corporate decision-making by providing real-time, incentive-compatible forecasts. The eventual resolution of these debates will shape how widely prediction markets can operate, what kinds of events they may cover, and how much capital institutional players will commit.

Framework Ventures' Michael Anderson says crypto's next trillion-dollar opportunity is financing AI and robotics, with blockchains evolving into capital markets infrastructure

$31.4B of distributed RWA value is already on-chain per RWA.xyz, but roughly $14.6B of that is U.S. Treasury debt while distributed asset-backed credit is only about $2.2B. Financing robotics and AI pushes crypto into underwriting utilization, hardware depreciation, energy costs, and machine revenue streams, much closer to equipment leasing than vanilla tokenization. If Framework is right, Maple/Centrifuge-style credit markets and DePIN operators start sharing the same primitive: verifiable cash-flow collateral with 24/7 settlement.

Market Microstructure: Liquidity, Spreads, and Order Types

Understanding markets also means understanding microstructure: how orders are matched, how liquidity is provided, and how prices respond to trades of different sizes. In order book markets, bids and asks at various price levels determine the depth of the book. The tightness of the bid–ask spread and the amount of size available near the mid-price are key indicators of liquidity. In crypto, both centralized exchanges and some onchain venues use order books, often supported by professional market makers that quote continuously to earn the spread and fee rebates.

Automated market makers use a different microstructure. In a constant-product AMM, for example, the product of the reserves of two tokens in a pool must remain constant, so large trades cause the price to move along a deterministic curve. This means slippage is a function of trade size relative to pool depth, which can be mitigated by routing across multiple pools or by using more sophisticated formulas like concentrated liquidity. For traders, the practical implication is that large orders in thin pools can move prices significantly, even if broader market sentiment is unchanged.

Microstructure also affects how shocks propagate. In lending markets, utilization is the analogue of order book depth: when all USDC in a pool is lent out, the “book” is empty, and borrowers face sharply higher rates or cannot access liquidity at all. The Morpho msY/USDC market hitting 100% utilization during the MSUSD crisis reveals how quickly liquidity can vanish when many participants try to move in the same direction. In prediction markets, liquidity is often more uneven, with deep markets on major political events and thin markets on obscure topics. Traders must consider both price and depth when inferring probabilities from markets.

Examples from recent coverage show how microstructure issues can bleed across markets. Strategy’s STRC preferred stock trading around 86 dollars, well below its 100 dollar par value and near record lows, signaled distress that affected confidence in related strategies and in the broader risk environment for Bitcoin and crypto assets. When fixed-income-like instruments associated with a strategy or institution fall sharply, it can trigger concerns about solvency, which in turn may lead to de-risking in seemingly unrelated markets. In such situations, thin liquidity and crowded positioning in crypto can exacerbate price moves, regardless of fundamentals.

For onchain prediction markets and derivative platforms, microstructure choices—such as tick size, minimum trade increments, fee tiers, and whether to rely on AMMs or human market makers—are not merely technical details. They shape who participates, how easy it is to manipulate prices, and how resilient markets are during volatility spikes. The design of these systems is therefore a core part of market infrastructure, not a secondary concern.

Risk, Crashes, and Contagion in Crypto Markets

Crypto markets are no strangers to crashes and contagion. Because markets are tightly interconnected, events in one corner often reverberate across others. Stablecoin failures are especially dangerous due to their role as collateral and base assets. The MSUSD plunge is a textbook example: when the stablecoin’s verification was withdrawn, it lost its peg, falling about 85% at one point, and the associated Morpho msY/USDC lending market hit full utilization as borrowers scrambled and lenders sought safety. This feedback loop—loss of confidence, selling pressure, vanishing liquidity, and strained lending pools—is analogous to bank runs in traditional finance.

Derivatives add another transmission channel. Highly leveraged positions on perpetual futures can be liquidated automatically when prices move beyond certain thresholds, leading to forced selling or buying that can accelerate trends. In extreme cases, cascading liquidations can drive prices far below or above levels justified by fundamentals. This dynamic has been seen in Bitcoin and Ether perps during flash crashes, and more recently in altcoin perps where liquidity is thinner and market depth may not absorb large liquidations without large price dislocations.

Cross-asset linkages are also important. The turmoil around Strategy’s STRC preferred stock, trading significantly below par near 86 dollars, raised concerns about the strategy’s stability and the knock-on effects for Bitcoin and other crypto positions associated with it. When investors worry that a major institution or strategy is under stress, they may pre-emptively reduce crypto exposure, especially in correlated or leveraged products. Similarly, when AI-related equities dominate broad equity indices, as Ray Dalio has noted, any reversal in that sector can affect risk appetite in adjacent markets, including AI-themed crypto tokens and futures on AI companies offered by crypto derivatives venues.

The removal of Anthropic and OpenAI perpetuals from Hyperliquid, which had offered investors indirect exposure to these private AI companies, illustrates another dimension of risk. These markets gave traders synthetic access to the performance of major AI players, but they also operated in a regulatory and informational grey zone, with potential concerns around underlying valuation data and the appropriateness of such exposures for retail users. Their delisting underscores that crypto markets are subject not only to price risk but also to “listing risk”: the possibility that an asset or contract will suddenly become untradable as venues respond to legal, reputational, or business pressures.

Prediction markets face analogous risks. Lawsuits or regulatory actions can abruptly shut down popular markets, freeze funds, or force the unwinding of positions. Our coverage of suspected insiders making eight-figure profits on prediction platforms and the growing political focus on insider trading bans shows that legal and reputational risks are rising. When platforms respond by curbing certain markets—such as elections or policy outcomes—liquidity and informational value may suffer, and traders must adapt to a shifting landscape.

- 2022-10exploit

Mango Markets $110M exploit by Avi Eisenberg

- 2024-01regulatory

Spot Bitcoin ETFs approved and launched in the US

- 2024-04regulatory

Avi Eisenberg convicted for Mango Markets manipulation

- 2024-08milestone

Global market rout; Tether mints $1.3B USDT post-Aug-5 bottom

- 2024-11milestone

DEX market share hits record 14.22% of monthly volume vs CEX

- 2024-12milestone

Bitcoin surpasses $106K amid Trump strategic reserve signals

- 2025-01milestone

DeepSeek R1 release triggers AI market rout; BTC falls 6%

- 2025-01launch

Curve ecosystem TVL at $2.36B; Liquity V2 BOLD pools launch with 40%+ yields

Momentum, Narratives, and Market Cycles

Markets are not driven solely by fundamentals; they are also shaped by momentum and narratives. Academic research and practitioner experience have long documented a “momentum effect” in equities, where assets that have outperformed over certain lookback periods tend to continue outperforming for a time. In a recent interview, momentum investor Travis Prentice discussed how various lookback schemes—such as 3-month, 6-month, or 12-month minus 1-month formations—can capture this effect, with his firm and other research suggesting that a 12-minus-1-month window often strikes a strong balance of outperformance. He also emphasized that the momentum premium tends to decay after about 6 to 9 months, after which returns may reverse.

Crypto markets appear to exhibit similar, if more volatile, momentum patterns. When narratives around themes like AI, Layer 2 scaling, or real-world assets take hold, tokens in those sectors can experience sharp runs as traders pile in, often propelled by leverage and social media. Our recent coverage on the “useless flippening” nearing, with market momentum building despite skeptics, captured how traders sometimes rotate into alternative layer-one tokens or niche sectors based on relative performance rather than fundamentals, hoping to front-run a perceived rotation away from entrenched leaders. These dynamics can create self-reinforcing price moves until new information or macro conditions break the trend.

Narratives interact with fundamentals in complex ways. Ray Dalio’s warning that markets are highly concentrated in a small group of AI-related firms and may deliver modest or negative real returns over the next 5–10 years reflects concern that an “AI bubble” might be forming in equities. Crypto has its own AI narratives, with tokens branded as AI-related or linked to AI infrastructure sometimes trading at valuations that assume continued hypergrowth in the sector. If broader equity markets reprice AI risk, it could spill over into crypto AI tokens, prediction markets on AI company valuations, and derivatives linked to AI indices.

Prediction markets can both reflect and challenge prevailing narratives. For example, event contracts on whether a protocol will ship a major upgrade by a certain date, or on whether AI regulation will pass in a given legislative session, can reveal whether market participants think official roadmaps and political rhetoric are credible. When prediction market odds diverge sharply from mainstream commentary, they can serve as an early warning that sentiment is shifting. Conversely, crowded positions in prediction markets may simply mirror hype and groupthink, especially if liquidity is thin or dominated by a small number of players.

Momentum is also present in onchain usage metrics. When a new DeFi protocol launches and quickly accumulates total value locked (TVL) and volume, traders may infer product–market fit and pile into the token, reinforcing the trajectory. But as Travis Prentice noted in the context of equities, momentum without improving fundamentals often fades, and trends can reverse sharply. In crypto, that reversal can be compounded by token unlocks, incentive changes, and shifts in regulatory or security perceptions.

Reading Market Data: Market Cap, Volume, Open Interest, and Odds

For participants in crypto and prediction markets, making sense of data is essential. Spot markets provide prices, market caps, and volumes. Derivatives add open interest, funding rates, implied volatility, and term structure. Prediction markets contribute odds and implied probabilities. Each metric tells part of the story, but none is sufficient on its own.

Market cap and trading volume, as reported by aggregators like CoinMarketCap, are starting points for understanding the relative size and liquidity of tokens. High market cap with low volume may indicate concentrated holdings or lack of organic interest. Conversely, high volume relative to market cap can signal intense speculative churn, perhaps driven by short-term narratives or wash trading. Volume trends over time can show whether interest in a token or sector is growing or fading, independent of price.

Open interest in futures and perpetuals measures the total value of outstanding contracts that have not been closed or delivered. Rapid growth in open interest alongside rising prices may indicate new money entering leveraged positions, potentially setting the stage for either continued momentum or a sharp liquidation event if conditions reverse. Funding rates on perpetuals provide a window into directional bias: persistent positive funding suggests traders are paying a premium to be long, while negative funding indicates shorts are in demand. Combining price, open interest, and funding can help traders distinguish between spot-driven rallies and derivative-fueled squeezes.

In prediction markets, the central metric is the implied probability embedded in contract prices. A binary contract that pays one dollar if an event occurs should, in theory, trade around its expected probability, adjusted for fees and risk. NerdWallet’s calculator tools illustrate how to convert odds and payoff structures into implied probabilities and expected value. However, traders must account for liquidity, platform fees, and potential resolution risk when interpreting these numbers. A 70% pricing in a thin market may not be as reliable as a 60% pricing in a deep, heavily traded market.

For DeFi money markets, utilization, collateral composition, and interest rates are the key variables. High utilization and sharply rising rates, as in the Morpho msY/USDC market during the MSUSD incident, signal strain that may precede forced deleveraging or collateral liquidations. Monitoring these metrics alongside spot prices and stablecoin pegs can provide early warning of systemic stress.

In all cases, data must be contextualized. A16z’s report of prediction markets reaching roughly 10.8 billion dollars in weekly volume and 1.5 billion dollars in open interest is impressive, but traders must ask which events are driving that volume, how concentrated it is across platforms, and what portion is speculative versus hedging. Similarly, a spike in Bitcoin’s trading volume may be bullish or bearish depending on whether it coincides with price gains, derivative liquidations, or regulatory news. Market literacy involves not only reading the numbers but linking them to underlying events, structures, and narratives.

Onchain money laid the foundation for tokenized assets, with Treasuries, money market funds and equities now following stablecoins onto blockchain rails

RWA.xyz has tokenized Treasuries/MMFs around $14.7B distributed value, while tracked stablecoins sit near $296B with ~$6.7T in 30-day transfer volume; the cash leg already dwarfs the asset leg. BUIDL, USYC, USDY and OUSG start changing DeFi market structure once they plug into Aave/Morpho/perps collateral loops with sane liquidation and whitelist handling. Equities are the dangerous leg: Robinhood/OpenAI showed that a token wrapper without issuer consent, redemption rights and shareholder mechanics is synthetic exposure wearing a chain logo.

Regulatory Landscape for Crypto and Prediction Markets

Regulation is increasingly central to how markets operate and evolve. In crypto, the split between securities and commodities frameworks, and between centralized and onchain venues, creates a patchwork of rules. Perpetual futures on Bitcoin may trade under CFTC oversight on U.S. exchanges, while similar products on altcoins could be considered securities and fall under SEC jurisdiction, or be barred altogether from retail venues. Cross-border platforms further complicate matters, as regulators weigh whether and how to police offshore activity that touches domestic users.

The CFTC chair, Mike Selig, recently discussed on a podcast the possibility of bringing onchain derivatives platforms like Hyperliquid into the U.S. regulatory perimeter. He emphasized that blockchain technology and 24/7 trading models are transforming markets and suggested that regulators need to adapt their frameworks to accommodate these innovations while maintaining investor protections. Such remarks hint at a future where decentralized or hybrid venues could obtain some form of regulatory recognition, provided they meet standards for transparency, risk management, and compliance.

Prediction markets sit at a particularly contested intersection of derivatives, gambling, and free speech. The CFTC has approved some event contracts and rejected others, particularly around elections and political control, citing concerns about gaming and public interest. Lawsuits and petitions for review, such as those mentioned in mainstream coverage about prediction markets being in legal battles, illustrate how unsettled the terrain remains. In parallel, the SEC has taken enforcement actions against some platforms for offering what it views as unregistered securities in the form of tokenized event contracts, raising additional barriers to entry.

Legislative initiatives aim to clarify at least one aspect: insider trading by public officials. The Public Integrity in Financial Prediction Markets Act would bar covered individuals from trading contracts on events related to their official duties if they possess non-public information and imposes financial penalties for violations. The House proposal by Rep. Bryan Steil to ban lawmakers and their families from betting on prediction markets pushes in the same direction, reflecting public concern that officials might profit from privileged knowledge or influence over policy outcomes. These efforts mirror earlier bans on stock trading by some government officials and suggest that prediction market participation will be increasingly regulated for those in power.

At the same time, there is pushback against overly restrictive approaches. Advocates argue that allowing regulated, transparent prediction markets could improve policy-making and risk management by providing real-time forecasts on inflation, GDP growth, election outcomes, and regulatory events. Platforms like Kalshi have positioned themselves as compliant venues under CFTC oversight, hoping to demonstrate that event contracts can be integrated into the existing derivatives framework responsibly. The entry of Charles Schwab and Cboe into yes-or-no S&P 500 options likewise shows that mainstream financial firms see value in event-based products when offered under familiar rules.

For crypto more broadly, regulatory clarity around stablecoins, tokenized securities, and onchain derivatives remains a top priority. The future of markets on Coinbase and other U.S. platforms, including spot and prediction markets, will depend on how legislators and regulators resolve questions about token classification, exchange registration, and cross-border activity. In the meantime, markets will continue to evolve in jurisdictional niches, with some innovations launching offshore or onchain before migrating toward regulated environments.

- Smart-contract / protocolHigh

Llama Lend and crvUSD market parameter drift under volatility demonstrated that on-chain lending can silently accumulate bad debt before governance can respond.

The August 2024 market bottom triggered $1.3B in Tether minting in days, illustrating how thin stablecoin liquidity buffers are when correlated sell pressure hits simultaneously.

Perpetual futures open interest on Deribit exceeding $15B in BTC options creates reflexive feedback loops where hedging flows can amplify the very moves they hedge against.

- RegulatoryMedium

EDX Markets filing for an OCC national trust charter and Goldman Sachs signaling conditional market participation indicate regulators are being drawn in — with uncertain perimeter-setting consequences for DeFi.

- CentralizationMedium

Bitcoin ETF concentration among a handful of TradFi custodians reintroduces single-point-of-failure counterparty risk into an asset whose value proposition is the absence of one.

- Slashing / penaltyLow

Weekend market plunges exposing under-collateralized positions — as with the Synthetix treasurer liquidation — remain idiosyncratic rather than systemic slashing events, but the social cost of liquidation has proven high enough to warrant community restitution.

Technology, AI, and the Future of Market Design

Technology is reshaping markets at multiple levels: as an object of investment, as a tool for trading, and as an infrastructure layer for market design. AI sits at the heart of all three. On the investment side, Ray Dalio’s comments about U.S. equity markets being highly concentrated in a few large AI-related companies reflect both investor enthusiasm for AI and concern about overvaluation and systemic risk. Crypto markets mirror this dynamic, with AI-branded tokens and protocols often commanding significant attention and capital, even when their connection to real AI capabilities is tenuous.

On the trading side, AI and machine learning models are increasingly used for signal generation, order execution, and risk management in both centralized and onchain markets. Quantitative strategies may incorporate alternative data, onchain activity, social media sentiment, and prediction market odds into their models. At the same time, AI is being used by regulators and exchanges for surveillance, looking for patterns indicative of manipulation, insider trading, or wash trading. As more market activity moves onchain, the combination of transparent data and AI-driven analytics could make market abuse both more detectable and more subtle, as sophisticated actors attempt to obfuscate their footprints.

AI is also a subject of markets themselves. Hyperliquid’s now-delisted perpetuals on Anthropic and OpenAI are emblematic: they offered traders synthetic exposure to private AI companies that are otherwise inaccessible to public investors. These markets raised questions about how underlying valuations were determined, how closely the perps tracked any reasonable notion of fair value, and whether offering such exposures to retail users was appropriate. Their removal shows how quickly AI-linked markets can appear and disappear, depending on legal assessments and platform strategies.

On the infrastructure side, smart contracts and DAOs enable new forms of market governance. Onchain prediction markets and derivatives protocols can, in theory, be governed by token holders voting on listing policies, fee structures, and oracle choices. This decentralization promises more transparent and participatory market design but also risks capture by whales, coordination failures, and slow responses to crises. However, it also opens the door to markets that would be difficult or impossible to run in traditional frameworks, such as micro-markets on niche events, parameterized insurance contracts, or continuous funding of public goods via market signals.

As AI models improve and become more integrated with onchain data, it is plausible that markets themselves will become partially automated agents, setting spreads, controlling collateral parameters, and even dynamically adjusting listing policies based on risk assessments. For now, human oversight remains central, but the trajectory points toward increasingly algorithmic markets in which AI and smart contracts interact to shape liquidity and price discovery.

Practical Framework for Participating in Markets

For individuals and institutions navigating crypto and prediction markets, a practical framework starts with clarifying objectives and constraints. A long-term holder of Bitcoin seeking exposure to macro trends faces different decisions than a trader speculating on short-term AI narratives or a policymaker using prediction markets to gauge probabilities. Each objective implies a different mix of spot, derivatives, DeFi, and prediction markets and different sensitivities to leverage, counterparty risk, and regulatory uncertainty.

Assessing venue risk is crucial. Centralized exchanges offer convenience and often deep liquidity but entail custodial risk and jurisdictional exposure. Onchain venues provide transparency and self-custody but introduce smart contract and oracle risk. Prediction markets may operate in lightly regulated or contested legal spaces, which can affect the reliability of payouts and the stability of platforms. Platforms like Kalshi, Polymarket, Coinbase, Robinhood, and Schwab’s planned event-based options each sit at different points on this spectrum. Understanding their regulatory status, governance, and track record is as important as evaluating their fee structures or user interfaces.

Thinking in probabilities rather than certainties is especially important for prediction markets and derivatives. Event contract prices provide a starting point for implied probabilities, but traders must adjust for liquidity, platform risk, and personal information or beliefs. Derivatives prices embed expectations about volatility and funding and can be used to infer market-implied scenarios for Bitcoin, AI equities, or stablecoin stability. Combining these market-implied probabilities with fundamental analysis, macro views, and risk tolerance can lead to more robust decisions than anchoring on narratives alone.

Aligning tools with goals also means recognizing when complexity is unnecessary. A user who simply wants long-term exposure to Bitcoin or Ether may not need perpetual futures or complex options strategies. Conversely, a market maker or arbitrageur might rely heavily on derivatives, lending markets, and cross-market prediction signals to manage positions. Overuse of leverage, particularly in volatile tokens or thin prediction markets, is a common path to ruin, as liquidation cascades and rapid repricings can overwhelm even well-reasoned theses. Building positions that can survive adverse scenarios, rather than only the expected case, is a hallmark of sustainable market participation.

Finally, market participants should remain aware of the broader legal and ethical environment. Trading on non-public information about government decisions in prediction markets, or taking advantage of information asymmetries in illiquid DeFi tokens, may be legal in some jurisdictions but still raise ethical concerns and attract future scrutiny. As lawmakers move to ban prediction market bets by public officials and to define insider trading in event markets, the boundaries of acceptable behavior are being redrawn. Market sophistication today must include not just financial acumen but regulatory and ethical awareness.

Outlook

The concept of “markets” in crypto is expanding from simple spot exchanges of Bitcoin for dollars into a sprawling ecosystem of onchain liquidity pools, perpetual futures, lending protocols, tokenized real-world assets, and prediction markets on political, economic, and technological events. Stablecoins like USDC sit at the center of this system, providing the unit of account and collateral that lubricate trading, while innovations such as tokenized stocks on Venus and AI-linked perps on platforms like Hyperliquid illustrate how far the frontier has moved. At the same time, recent shocks—from MSUSD’s 85% plunge and Morpho’s msY/USDC utilization spike to STRC’s preferred stock turmoil and the delisting of AI perpetuals—show that market design, liquidity, and governance are still fragile.

Prediction markets are likely to continue growing in volume and influence, especially as regulated platforms like Kalshi and major brokers such as Charles Schwab normalize event-based contracts alongside Coinbase and Robinhood’s offerings. The sector’s record weekly volumes and rising open interest, as documented by a16z, suggest that both retail and institutional participants see value in trading probabilities, not just prices. However, legal battles, insider trading concerns, and legislative efforts such as the Public Integrity in Financial Prediction Markets Act and congressional betting bans will shape which events can be marketed and who is allowed to trade them.

Onchain markets face a parallel regulatory evolution. The CFTC’s willingness to discuss pathways for bringing platforms like Hyperliquid onshore, and the broader debates over CME versus onchain perps, indicate that decentralized derivatives and DeFi money markets may eventually attain more formal recognition, provided they adapt to risk and compliance expectations. AI will play an increasingly central role, both as an investment theme and as a tool for trading and surveillance, even as voices like Ray Dalio warn of concentration risk and potential bubbles. For market participants, the challenge is to harness the informational and compositional power of these markets—spot, derivatives, DeFi, and prediction—while respecting their limits and fragilities.

In the coming years, the most successful crypto and prediction markets will likely be those that integrate robust onchain transparency with sound governance, prudent leverage, and clear regulatory footing. As markets move closer to the core of policymaking and everyday decision-making, the line between trading, forecasting, and governance will blur. For today’s crypto audience, developing a nuanced understanding of markets—not just prices—is the best preparation for that future.

Latest Markets news

BIS says stablecoins fall short as money, warns of emerging-market risks in annual reportFramework Ventures' Michael Anderson says crypto's next trillion-dollar opportunity is financing AI and robotics, with blockchains evolving into capital markets infrastructureOnchain money laid the foundation for tokenized assets, with Treasuries, money market funds and equities now following stablecoins onto blockchain rails Binance founder CZ says crypto's 50% slide stems from AI capital rotation, geopolitical tensions and the industry's recurring four-year market cycle

Binance founder CZ says crypto's 50% slide stems from AI capital rotation, geopolitical tensions and the industry's recurring four-year market cycle Maxine Waters pushes DOL to withdraw 401(k) rule that could add crypto and private-market assets

Maxine Waters pushes DOL to withdraw 401(k) rule that could add crypto and private-market assets DraftKings launches proprietary prediction markets exchange DKeX as annualized consumer volume tops $3.4B, intensifying competition with Polymarket and Kalshi

DraftKings launches proprietary prediction markets exchange DKeX as annualized consumer volume tops $3.4B, intensifying competition with Polymarket and KalshiSources

- https://coinmarketcap.com

- https://kalshi.com

- https://www.facebook.com/CoinMarketCap/posts/latest-charles-schwab-is-working-with-cboe-global-markets-to-roll-out-all-or-not/1430143249143064/

- https://x.com/WuBlockchain/status/2068044895915225447

- https://pricepredictions.com/news/msusd-drops-85-percent-mainstreet-finance-morpho-100-utilization-june-2026-qyhl2i43

- https://www.youtube.com/watch?v=WZ7mmTrSgxI

- https://www.facebook.com/vnzabbar/posts/breaking-strc-is-now-trading-near-its-record-low-zone-around-86-far-below-its-10/1572500064444020/

- https://www.curtis.senate.gov/press-releases/curtis-slotkin-young-schiff-lead-bipartisan-bill-to-stop-insider-trading-from-government-officials-on-prediction-markets/

- https://a16zcrypto.com/posts/tags/prediction-markets

- https://polymarket.com

- https://robinhood.com/us/en/prediction-markets/

- https://www.coinbase.com/predictions

- https://x.com/WuBlockchain/status/2068102593658990635

- https://www.gurufocus.com/news/8924462/charles-schwab-schw-launches-new-yesorno-options-tied-to-sp-500?mobile=true

- https://www.facebook.com/cnbc/posts/republican-house-member-rep-bryan-steil-on-thursday-is-set-to-introduce-a-provis/1401689635165759/

- https://www.thestreet.com/crypto/markets/hyperliquid-loses-anthropic-openai-markets

- https://metamask.io/news/perpetual-futures-vs-spot-bitcoin

- https://www.nerdwallet.com/investing/learn/what-are-prediction-markets

- https://www.instagram.com/reel/DXhOsQYB-GU/

- https://www.youtube.com/watch?v=puiJC9YVax0

Community notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…