In‑depth explainer on crypto’s technology, markets, regulation and risks, covering Bitcoin cycles, DeFi, stablecoins, Coinbase, AI’s impact, US and EU policy and how investors can approach digital assets in a volatile, evolving landscape.

+83 sources across the wider coverage universe

FBI reports Americans lost $11.4B to crypto fraud in 2025, up 22%, as AI-powered scams hit $893M2026-04

FBI reports Americans lost $11.4B to crypto fraud in 2025, up 22%, as AI-powered scams hit $893M2026-04 Circle launches managed USDC settlement for banks, abstracts all crypto complexity across 20+ chains2026-04

Circle launches managed USDC settlement for banks, abstracts all crypto complexity across 20+ chains2026-04 DefiLlama integrates LlamaAI alerts into Telegram, enabling customizable daily notifications for onchain trends and DeFi news2026-04

DefiLlama integrates LlamaAI alerts into Telegram, enabling customizable daily notifications for onchain trends and DeFi news2026-04 U.S. Treasury extends cyber threat alerts to crypto firms, closing gap with traditional finance2026-04

U.S. Treasury extends cyber threat alerts to crypto firms, closing gap with traditional finance2026-04 DOJ launches victim compensation for $4B OneCoin crypto pyramid scheme via asset forfeiture2026-04

DOJ launches victim compensation for $4B OneCoin crypto pyramid scheme via asset forfeiture2026-04 Beyond the sky: The story of how Jeff built Hyperliquid, a blockchain and crypto trading exchange, into the most profitable startup per employee on earth.2026-04

Beyond the sky: The story of how Jeff built Hyperliquid, a blockchain and crypto trading exchange, into the most profitable startup per employee on earth.2026-04

Crypto: A Comprehensive Guide to Digital Assets, Markets and Regulation

Digital assets commonly grouped under the label “crypto” are programmable tokens that move on public or permissioned blockchains, enabling peer‑to‑peer transactions, new forms of finance and novel digital organizations without relying on traditional intermediaries such as banks. At the same time, these assets remain highly volatile, largely unregulated in many jurisdictions and deeply contested as money, investment and technology, which makes understanding their mechanisms, risks and evolving regulatory treatment essential for anyone engaging with the ecosystem.

What Crypto Is And Why It Matters

Cryptocurrencies are best understood as entries in a distributed database rather than as physical coins or notes: they are digital tokens tracked on an online ledger that multiple participants maintain collectively through cryptography and consensus rules. Unlike national currencies such as the US dollar or the euro, which derive part of their value from being legal tender backed by a sovereign government, most crypto assets have no legislated or intrinsic value and are worth only what users and investors are willing to pay in the market at any given time. This market‑based valuation, combined with 24/7 trading on global platforms, has led to extreme price swings that far exceed those in most traditional asset classes, with Bitcoin’s price, for example, moving from around 30,000 US dollars in mid‑2021 to nearly 70,000 by late 2021 before falling back to roughly 35,000 in early 2022. Despite this volatility, interest and activity in crypto markets have expanded substantially, drawing in retail investors, hedge funds, corporates and, increasingly, pension funds and other institutional allocators that see potential diversification benefits or asymmetric upside.

From a technological perspective, the importance of crypto lies in its ability to enable peer‑to‑peer transactions without requiring users to know or trust one another or to rely on a central clearing entity. Bitcoin’s original design showed that it was possible to combine cryptographic signatures, economic incentives and a shared ledger (the blockchain) so that a decentralized network could maintain consensus about who owns what, even in the face of malicious actors. Over time, this basic architecture has been generalized into programmable platforms such as Ethereum, enabling smart contracts that can automatically execute financial agreements, governance rules and digital media ownership rights, which has given rise to the broader field of decentralized finance (DeFi) and non‑fungible tokens (NFTs). Crypto’s proponents view these innovations as the foundation of a more open, efficient and inclusive financial system, while critics point to speculative excess, environmental costs and illicit finance risks as reasons for caution or outright restriction.

From Digital Tokens To Crypto Ecosystems

The first generation of cryptocurrencies, epitomized by Bitcoin, focused primarily on creating a scarce digital bearer asset that could be transmitted electronically without intermediaries and without double spending. Bitcoin’s pseudonymous creator, Satoshi Nakamoto, intentionally withdrew from public view after launching the protocol, and that ongoing anonymity has become part of the cultural narrative: the absence of a central figure reinforces the ethos that the system should be decentralized, resistant to control and judged on its code rather than its founder’s authority. Early adopters tended to be cypherpunks, libertarians and technologists motivated by a desire for censorship‑resistant money and distrustful of central banks, but the user base has since widened to include traders, institutional investors, corporates and, in some jurisdictions, everyday users seeking an alternative to unstable local currencies.

As the space matured, it evolved from a relatively simple universe of “coins” into a complex ecosystem of platforms, protocols and application‑specific tokens. Smart‑contract platforms such as Ethereum, Solana and others enable developers to deploy decentralized applications that replicate lending, derivatives trading, asset management and even entire exchanges on‑chain, using tokens both as native currencies for paying transaction fees and as governance or incentive instruments for participants. The DeFi sector has introduced mechanisms such as liquidity pools and automated market makers, which change how markets organize trading and liquidity provision, while tokenized real‑world assets aim to bring traditional financial instruments, commodities and even invoices on‑chain for more efficient settlement and fractional ownership. This proliferation of use cases has also led to a proliferation of risks: sophisticated smart contracts introduce new attack surfaces, and complex tokenomics can obscure the distinction between genuine utility and pure speculation, making rigorous due‑diligence and regulatory scrutiny increasingly important.

Crypto Versus Traditional Money And Payment Systems

A recurring question in public debate is whether cryptocurrencies qualify as “money” in the economic sense of serving as a medium of exchange, a unit of account and a store of value. Central banks such as the Reserve Bank of Australia have generally concluded that, at present, most crypto assets do not meet these criteria: only a small fraction of holders use them regularly for payments, price quotes remain overwhelmingly in fiat currencies, and severe price volatility undermines their reliability as a store of purchasing power. By contrast, sovereign currencies gain part of their value from legal tender status and the backing of a central bank with monetary policy tools, which helps anchor expectations and reduces the likelihood that their value collapses to zero in normal circumstances. In crypto, where value depends more directly on collective beliefs about future demand and technical robustness, even leading assets such as Bitcoin could, in theory, experience extreme price declines if confidence erodes or a critical vulnerability emerges, although many advocates argue that growing network effects and institutional adoption reduce this risk over time.

From a payments perspective, crypto networks demonstrate both potential and limitations. On the one hand, they allow cross‑border transfers without relying on correspondent banking networks and can, in principle, offer faster settlement and programmable conditions, which is why stablecoins have become increasingly popular for trading and remittances. On the other hand, transaction fees and throughput constraints have often limited the practicality of using major public blockchains for everyday retail payments; for instance, Bitcoin transaction fees have at times reached median levels around 20 US dollars, making small purchases uneconomical, and confirmation times can be slow during periods of congestion. These frictions have spurred the development of scaling solutions such as payment channels and rollups, as well as the exploration of central bank digital currencies (CBDCs), which could provide digital forms of sovereign money with some of the programmability of crypto but under public oversight. Thus, rather than directly replacing existing payment systems in the near term, crypto is more realistically seen as a complementary layer and experimental laboratory for new financial primitives that may influence both private and public money in the long run.

Binance founder CZ backs efforts to make the U.S. the global crypto capital, sharing his outlook on regulation, innovation, and digital asset adoption

$312B in stablecoin float and roughly $88B USDT on Tron put the U.S. crypto-capital pitch inside the dollar-rail fight. GENIUS gives issuers a federal wrapper; CLARITY/market-structure rules decide whether liquidity routes through regulated U.S. venues or keeps living in offshore settlement. CZ backing Washington after Binance's $4.3B settlement reads like an admission that compliance distribution is becoming the moat CEXs used to get from raw volume.

Leviathan readers click crypto stories hardest when political or legal power is actively redrawing the rules — not for price action alone, but for the moment a regulator retreats, a tax break lands, or a fraudster gets caught, because those events reset who controls the financial upside.↗

Bitcoin And The Foundations Of The Market

Bitcoin remains the anchor of the crypto ecosystem by virtue of its first‑mover advantage, dominant brand recognition and role as the primary reference asset for market sentiment and index construction. Its protocol encodes a fixed maximum supply of just under 21 million coins, with new bitcoins introduced at a steadily declining rate through block rewards that are cut in half roughly every four years, a process known as “halving.” As of early 2020s data, around 89 percent of all possible bitcoins are already in circulation, meaning that future supply growth is increasingly limited and long‑term scarcity is built into the monetary policy of the system. This predictable and capped issuance schedule has fueled narratives comparing Bitcoin to digital gold, arguing that it can act as a hedge against inflation and currency debasement, even though empirical evidence on its performance as a safe haven remains mixed and constrained by its relatively short history.

Bitcoin’s price history has been characterized by repeated boom‑and‑bust cycles, in which parabolic rallies during bull markets have been followed by drawdowns exceeding 70 or 80 percent during subsequent bear markets. In terms of volatility, quantitative analyses suggest that Bitcoin has exhibited roughly four times the price volatility of gold over recent years, underlining that, at least for now, it is too unstable to function as a reliable store of value for risk‑averse investors or short‑term liabilities. At the same time, this volatility is precisely what attracts traders and some longer‑term investors, who see in it the possibility of outsized gains relative to traditional assets, particularly if they believe in a thesis of eventual widespread adoption or digital scarcity premiums. The reality that Bitcoin can behave both as a high‑beta risk asset correlated with broader equity markets and as an idiosyncratic asset influenced by protocol‑specific events such as halvings complicates portfolio construction and risk management, requiring careful scenario analysis rather than simplistic assumptions.

Bitcoin’s Design, Scarcity And The “Digital Gold” Narrative

Bitcoin’s design rests on a combination of cryptography, economic incentives and distributed consensus that allow participants to agree on the history of transactions without a central authority. Miners expend computing power and electricity to solve computational puzzles, proposing blocks of transactions and earning rewards in newly minted bitcoins plus transaction fees, which aligns their incentives with the security of the network as long as the value of the rewards exceeds the cost of attack. The issuance schedule halves the block reward approximately every four years, which not only slows the rate of new supply but also tends to force less efficient miners off the network, sometimes triggering episodes of “miner capitulation” where hash rate temporarily declines before stabilizing again. This mechanical reduction in supply growth over time is one reason why some analysts and institutions have come to describe Bitcoin as “digital gold”: like gold, its supply is scarce and relatively inelastic to price in the short term, even though the analogy is imperfect because gold has both industrial uses and a multi‑millennia track record as money, which Bitcoin lacks.

The “digital gold” narrative has important implications for investment behavior and market structure. If investors treat Bitcoin primarily as a long‑term store of value or macro hedge, they may be more inclined to hold it through cycles, reduce trading frequency and integrate it into diversified portfolios alongside commodities and equities, which could dampen volatility over time. In practice, however, data suggest that a significant share of Bitcoin holdings are used for investment and speculation rather than transactional use, and relatively small net flows from large holders or institutions can materially move the price because of limited float and fragmented liquidity. Moreover, Bitcoin’s environmental footprint has become a central point of critique: estimates in early 2020s placed its electricity consumption roughly on par with that of a mid‑sized country such as Pakistan, raising questions about sustainability, particularly if mining remains heavily dependent on fossil fuels. These environmental concerns have driven policy debates, influenced corporate treasury decisions and pushed some miners toward renewables or alternative revenue streams such as providing computing power for artificial intelligence workloads, thereby linking Bitcoin’s future to broader energy and technology transitions.

A helpful way to contextualize Bitcoin’s role is to compare it to gold and fiat currency across key attributes.

| Attribute | Bitcoin | Gold | Fiat currency (e.g., USD) |

|---|---|---|---|

| Issuance | Fixed cap near 21 million; declining new supply | Physical supply grows slowly via mining | Central bank determines supply |

| Volatility | Very high; ~4x gold’s volatility in 2025 | Moderate; historically volatile but more stable | Typically lower vs. BTC and gold |

| Backing / value source | Network effects, scarcity narrative, speculation | Industrial use, jewelry, historical monetary role | Legal tender status, taxation, policy support |

| Use in payments | Limited, mostly investment and transfers | Very limited in retail commerce | Widely accepted for goods, services, taxes |

| Environmental footprint | High electricity use; concerns about emissions | Environmental costs from mining and refining | Primarily indirect (banking, cash handling) |

This comparison illustrates why some institutions tentatively frame Bitcoin as a speculative store‑of‑value candidate rather than as money, and why regulators and central banks scrutinize it through lenses of consumer protection, financial stability and climate policy rather than simply as another payment technology.

Halvings, Market Cycles And “Crypto Seasons”

One distinctive feature of Bitcoin’s monetary policy is the programmed halving of issuance approximately every four years, which has coincided historically with pronounced market cycles. Analysts at traditional brokerages and digital‑asset firms have popularized a framework that likens these cycles to four “seasons”: a post‑halving “summer” of strong price appreciation up to a new all‑time high, a subsequent “autumn” of distribution and elevated volatility, a “winter” bear market marked by deep drawdowns and capitulation, and a “spring” recovery period leading into the next halving. Historical data suggest that summer phases have tended to last around five months on average, while winters have extended for roughly thirteen months and have sometimes produced drawdowns comparable to those experienced by US equities during the Great Depression, although the limited number of cycles and changing market structure mean such patterns must be treated cautiously. The latest halving occurred in April 2024, and by late 2025 Bitcoin had reached a new peak before entering what many observers interpret as another winter, with the price down about 50 percent from that peak by early 2026 and sentiment indicators such as fear‑and‑greed indexes showing extreme fear.

These cyclical dynamics shape behavior across the crypto ecosystem, influencing miners’ profitability, DeFi activity, altcoin performance and institutional appetite for exposure. During bull markets, retail inflows, venture capital funding and token launches proliferate, often driving valuations of more speculative projects to levels that are difficult to justify on fundamentals, while in bear markets funding dries up, less robust projects fail and market participants refocus on risk management and regulatory compliance. E*Trade’s analysis of past cycles notes that investors seeking to manage risk during downturns may adopt approaches such as “HODLing” through volatility, reallocating toward more defensive segments like stablecoins or infrastructure protocols, or trimming overall crypto exposure to maintain portfolio risk within tolerable bounds, but it also emphasizes that past cycles are not a guarantee of future patterns and that exogenous shocks such as new regulation, severe software bugs or coordinated government action could disrupt expected seasonal dynamics. Recent market stress linked to Strategy Inc.’s STRC preferred stock, which has declined to all‑time lows due to concerns about the company’s debt and dividend obligations rather than Bitcoin’s price, underscores that even ostensibly Bitcoin‑linked equities can exhibit idiosyncratic risks unrelated to the underlying asset, complicating the use of proxy securities for cyclical positioning. In this environment, unprepared investors who extrapolate past bull runs without accounting for leverage, corporate financing structures and regulatory developments may face particularly harsh outcomes in the next downturn, a theme that has featured prominently in recent market commentary.

Key Types Of Crypto Assets

Although Bitcoin often dominates headlines, the crypto asset universe now spans a wide spectrum of tokens with differing economic functions, governance models and risk profiles. A basic taxonomy distinguishes between native cryptocurrencies such as Bitcoin and Ether that secure underlying blockchains, application‑level tokens that confer rights or incentives within specific protocols, and asset‑backed tokens such as stablecoins and tokenized securities that map directly to off‑chain claims. Each category raises different questions for investors and regulators: base‑layer coins implicate issues of monetary design and network security, application tokens raise concerns about whether they constitute securities or commodities under national laws, and asset‑backed tokens sit at the intersection of traditional financial regulation and new technological rails. Understanding these distinctions is crucial for assessing both potential return drivers and the legal protections that may or may not apply to token holders in various jurisdictions.

Within this broad landscape, innovation has been particularly intense in two areas: programmable smart‑contract platforms that underpin DeFi and stablecoins that provide price‑stable units of account for trading and payments. Smart‑contract platforms enable entire financial applications to operate on‑chain, with tokens used for governance, fee payment and rewarding early adopters, while stablecoins serve as a kind of “crypto cash,” letting traders move quickly in and out of volatile assets without going through fiat on‑ramps and facilitating cross‑border transfers without traditional banking infrastructure. A third area of rapid development involves tokenization of real‑world assets, where tokens represent claims on bonds, funds, real estate or even invoices, and can be integrated into DeFi protocols for on‑chain borrowing and lending, blurring the boundary between “crypto‑native” and traditional finance. These innovations expand the design space but also increase systemic complexity, as interdependencies between protocols, custodians and off‑chain institutions become denser and harder to map.

Payment Coins, Smart‑Contract Platforms And DeFi Tokens

Payment‑oriented coins such as Bitcoin, Litecoin or certain privacy coins were initially positioned as alternatives to card networks and bank transfers, promising lower fees and censorship resistance. In practice, as discussed earlier, high volatility and periodic congestion have limited their use in everyday retail payments, and much of their activity now reflects investment, trading and long‑distance transfers rather than routine purchases. Meanwhile, platforms like Ethereum have shifted the center of gravity toward programmable money, where the base asset (Ether, in Ethereum’s case) functions both as a store of value and as “gas” used to pay for computation and storage on the network. Deutsche Bank analysts have described Ethereum as a kind of “digital silver” relative to Bitcoin’s “digital gold,” reflecting its broader utility within DeFi and NFT ecosystems even as it shares many of the same speculative and regulatory challenges as Bitcoin.

DeFi tokens, which include governance tokens for decentralized exchanges, lending protocols and derivatives platforms, represent claims not on traditional company equity but on participation rights within on‑chain systems. For example, automated market maker protocols issue governance tokens that allow holders to vote on fee parameters, incentive programs and treasury allocations, and in some cases these tokens also entitle holders to a share of protocol revenues, blurring the line between utility and investment contract. The BankingHub analysis of liquidity pools and AMMs emphasizes that these systems have become a core part of crypto trading infrastructure, enabling decentralized exchanges to offer liquidity in the absence of centralized market makers and order books, and have attracted billions of dollars in capital seeking yield through liquidity provision. However, DeFi tokens tend to be highly volatile, sensitive to both underlying protocol usage and broader risk sentiment, and in many jurisdictions they sit in a grey area of securities law, which is why legislative initiatives such as the US Digital Asset Market Clarity Act and the Responsible Financial Innovation Act aim to define when such tokens should be treated as securities versus commodities.

Stablecoins, Tokenized Assets And Hybrid Instruments

Stablecoins are digital tokens designed to maintain a stable value relative to a reference asset, most commonly the US dollar, and constitute a distinct category because they seek to minimize price volatility rather than maximize upside. According to Brookings, stablecoins in circulation have collectively surpassed 250 billion dollars in market value, with roughly 99 percent pegged to the US dollar and the remainder linked to other fiat currencies or commodities such as gold. The dominant designs today are fiat‑backed stablecoins, where issuers hold reserves in cash and high‑quality liquid assets such as Treasury bills or bank deposits and promise to redeem tokens at par, and algorithmic or hybrid designs that try to maintain a peg through code‑based adjustments in supply and demand, sometimes with partial collateral. Fiat‑backed stablecoins constitute the overwhelming majority of supply, accounting for around 87 percent, whereas algorithmic stablecoins represent less than 0.2 percent, reflecting the market’s preference for transparent reserves after high‑profile failures.

The uses of stablecoins span trading, payments and hedging against local currency instability. Traders employ them as a convenient base asset for moving quickly between different crypto tokens without relying on fiat gateways, while businesses and individuals in countries with capital controls or inflationary currencies may hold dollar‑pegged stablecoins as a way to preserve value and remit funds internationally. At the same time, the sector’s rapid growth poses new forms of risk: if issuers’ reserves are inadequate or illiquid, a wave of redemptions could trigger a loss of confidence and a “breaking of the buck,” as seen in the algorithmic TerraUSD collapse in May 2022 that wiped out more than 45 billion dollars in value within a week and shook faith even in fully reserved tokens. During that episode, the largest fiat‑backed stablecoin briefly traded at a discount on secondary markets, falling as low as 94 cents despite continuing to honor par redemptions, which underscored that secondary market pricing can diverge from fundamental backing under stress. These events have motivated regulatory responses such as the US GENIUS Act, which mandates one‑to‑one reserve backing in specified high‑quality assets, monthly reserve disclosures, redemption at fixed monetary value and registration under federal or state regimes depending on issuance scale, while prohibiting interest payments on payment stablecoins. They have also accelerated interest in tokenized money market funds and other tokenized real‑world assets, as institutions explore on‑chain representations of fixed‑income instruments within clear regulatory frameworks.

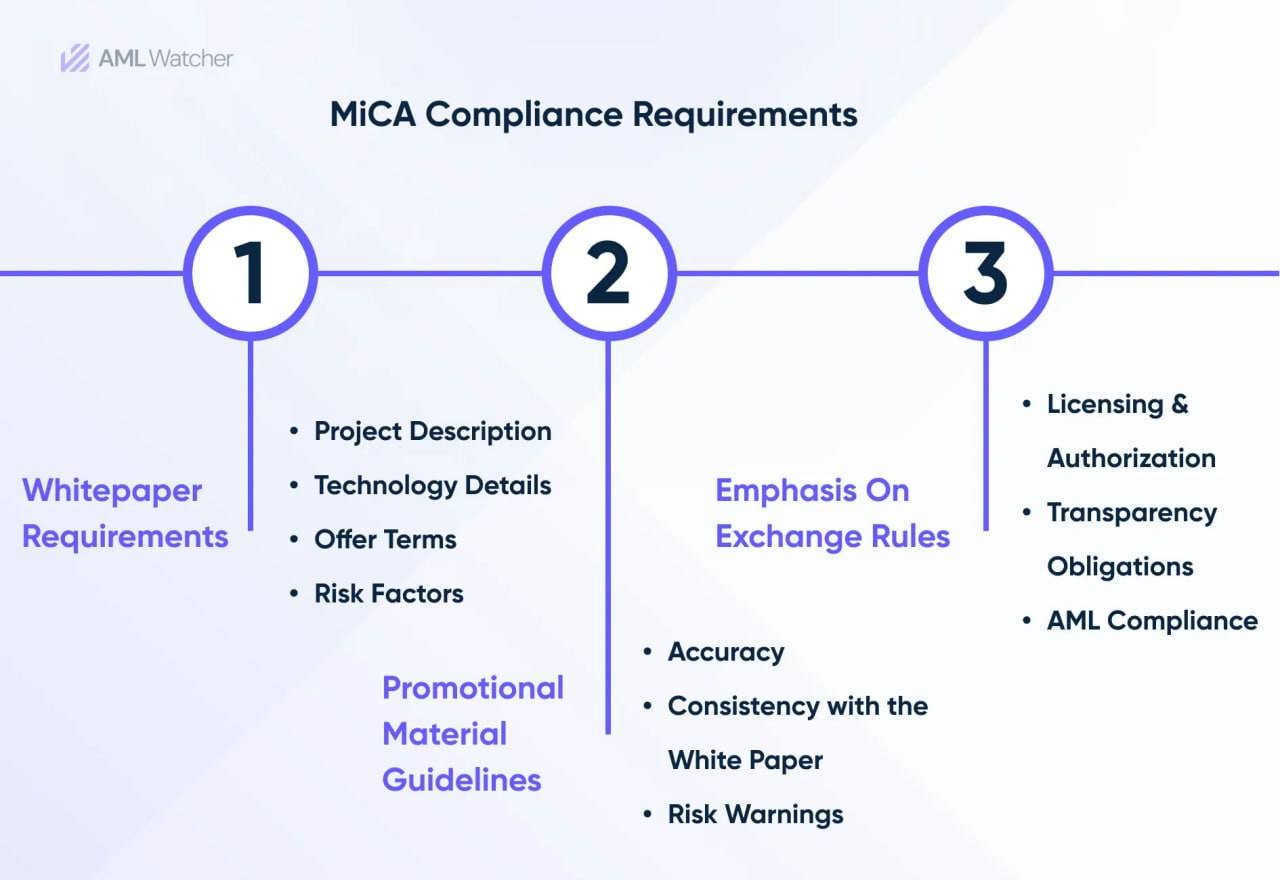

Hybrid assets, including tokenized treasuries, tokenized bank deposits and RWAs integrated into DeFi, aim to bridge on‑chain liquidity with off‑chain cash flows. Analyses of DeFi infrastructure note the emergence of platforms like Orca that provide liquidity not only for purely crypto‑native assets but also for hybrid and traditional financial assets brought on‑chain, suggesting a future in which decentralized exchanges could serve as venues for a broad spectrum of tokenized instruments. This hybridization raises novel questions about jurisdiction, disclosure obligations and investor protection, as tokens that look technologically similar may encode very different legal rights and risk exposures depending on whether they represent equity, debt, fund units or mere governance privileges. As regulators in Europe, the US and elsewhere refine frameworks such as MiCA and consider potential “MiCA 2.0” expansions to cover DeFi and new stablecoin designs, market participants are closely watching how hybrid assets will be classified and supervised, since this will shape whether traditional institutions feel comfortable allocating capital to on‑chain liquidity pools and tokenized portfolios.

SBI's $289M acquisition of Bitbank signals a new phase of consolidation in Japan's crypto industry as regulation pushes exchanges toward scale and institutional strength

1.1T yen in custody across 2.9M accounts gives SBI a distribution moat before Japan moves crypto under FIEA, cuts gains tax to 20%, and clears a path for spot BTC ETFs. Paying roughly 8x revenue for a loss-making venue only pencils if the licensed seat, Bitbank alt liquidity, and Japan Digital Asset Trust custody become rails for SBI's RLUSD/Visa/stablecoin-payments stack. If half of Japan's 27 registered exchanges disappear, the winners won't just collect fees; they'll decide which tokens get compliant JPY liquidity.

- 01US regulatory pivot↗

Trump-era SEC deregulation and zero-capital-gains proposals placed readers directly in the path of policy that could reprice their holdings overnight.

- 02retail mainstream integration

The Uniswap-Robinhood deal — the single most-clicked headline — signals that readers are acutely watching which on-ramps bring the next wave of buyers in.

- 03market crash liquidations↗

Back-to-back headlines on $272M and $600M wipeouts tapped reader anxiety about leveraged exposure during macro-driven sell-offs.

- 04crypto fraud accountability

Stories about the Denver pastor fleeing, pig-butchering operations, Do Kwon's prison wallet, and SBF's profane messages all drew strong clicks around the human cost of enforcement failures.

- 05wallet and infrastructure security

Fireblocks zero-days and Mac-targeting malware hit readers who custody their own assets and fear silent fund loss before patches arrive.

- 06global tax and stablecoin regulation↗

UAE VAT exemption, MiCA transaction caps, and IMF anti-crypto bailout clauses showed readers that jurisdictional arbitrage is real and consequential.

How Crypto Markets And Infrastructure Work

Crypto markets differ from traditional financial markets in several important respects, starting with their around‑the‑clock operation and global access via the internet rather than domestic trading hours and national exchanges. Trading occurs on centralized exchanges, where an intermediary maintains custody and operates order books, and on decentralized exchanges (DEXs) that rely on smart contracts and liquidity pools instead of central order matching. Over the past decade, unregulated decentralized platforms have grown to represent up to a quarter of total crypto trading volume, according to estimates cited by BankingHub, highlighting that a meaningful share of price discovery now occurs in DeFi environments even as most fiat on‑ and off‑ramps remain concentrated in centralized exchanges. This mixed market structure can complicate transparency and supervision, as regulators and investors must track liquidity and risk across both custodial and non‑custodial venues, some of which may operate partially or fully outside traditional regulatory perimeters.

Supporting this trading activity is a layered infrastructure of wallets, custodians, analytics providers and oracles. Non‑custodial wallets give users direct control of private keys and, therefore, of their crypto assets, while custodial services, including exchanges and specialized custodians, hold assets on clients’ behalf and provide interfaces for trading, staking or lending. Blockchain analytics firms track flows across addresses and exchanges, helping law enforcement and compliance teams identify illicit funds and comply with anti‑money‑laundering (AML) rules, while oracle networks feed off‑chain data—such as prices, interest rates or weather information—into smart contracts, enabling more complex decentralized applications. The growth of such ancillary services underscores that, although crypto aspires to decentralize finance, a rich ecosystem of intermediaries and infrastructure providers has risen around base protocols, and their behavior and resilience can significantly influence user experiences and systemic risk.

Exchanges, Wallets And Coinbase’s Role

Centralized exchanges (CEXs) remain the primary entry point for most retail and institutional participants, offering familiar interfaces, fiat on‑ramps and a wide menu of tokens for trading. Among these, Coinbase has emerged as one of the most prominent, operating as a publicly listed US company subject to securities‑market disclosure obligations and positioning itself as a compliant gateway that works with regulators and law enforcement. The company’s international expansion illustrates both the opportunities and challenges of bringing crypto services to large emerging markets: Coinbase has secured registration in India, launched an offering that enables local customers to deposit and withdraw Indian rupees directly, and provides access to spot and perpetual futures trading through its platform, reflecting a belief that India represents a significant growth market for digital assets despite regulatory complexity. At the same time, Coinbase’s experience with a major cloud outage in October 2025, when a widespread failure in an Amazon Web Services region caused around three hours and seventeen minutes of degraded performance for users, illustrates the operational dependencies and single points of failure that can still affect centralized platforms even when the underlying blockchains remain online.

Wallet choice is another fundamental decision for crypto users, and it connects to broader questions of trust, security and usability. Non‑custodial wallets give users sovereignty over their funds by requiring them to manage private keys or seed phrases, but this also means that lost credentials typically cannot be recovered, making human error a leading cause of irreversible asset loss. Custodial wallets and exchange accounts, by contrast, allow password recovery and may offer insurance or fraud monitoring, but they concentrate risk and require users to trust that the provider will remain solvent and secure, as the history of exchange hacks and failures such as Mt. Gox has amply demonstrated. Institutional investors, including funds and corporate treasuries, often rely on specialized custodians that employ multi‑party computation, hardware security modules and insurance layers to mitigate key‑management risks, and regulators increasingly require such arrangements as a condition for licensing and investor protection. Debates over the appropriate balance between self‑custody and regulated custody also intersect with policy questions around financial inclusion and recovery: for example, families saving crypto for their children may prefer robust, insured custodial solutions that allow inheritance planning, whereas cypherpunk users may favor self‑sovereign setups despite higher operational risk.

DeFi Market Structure: Liquidity Pools, AMMs And On‑Chain Liquidity

Decentralized exchanges and lending protocols rely on liquidity pools and automated market makers (AMMs) instead of centralized order books, fundamentally reshaping how liquidity is provided and priced. A liquidity pool is essentially a smart‑contract‑controlled reserve of two or more tokens, where liquidity providers deposit assets and receive pool tokens representing their share; users trade against the pool at algorithmically determined rates rather than against specific counterparties, and prices adjust as the relative balances in the pool change. AMM algorithms, such as the constant‑product formula popularized by early DEXs, allow continuous pricing without needing a central order book, enabling markets even for long‑tail tokens that might not attract professional market makers on centralized venues. This design reduces barriers to listing and can foster innovation, but it also introduces new phenomena such as impermanent loss, where liquidity providers may end up with fewer assets than if they had simply held their tokens, especially when prices move sharply in one direction.

The BankingHub analysis identifies several categories of risk associated with liquidity pools and AMMs, including price volatility, cyberattacks and regulatory ambiguity. Impermanent loss is exacerbated when one asset in a pool experiences large price swings, which is common in crypto markets, and can erode the returns of liquidity providers even if they receive trading fees, particularly in volatile DeFi sectors. Smart contracts controlling pools may harbor bugs or vulnerabilities that hackers can exploit to drain funds, and history has seen numerous exploits involving flash‑loan‑enabled manipulation of oracles or pool balances, leading to significant user losses. Regulatory frameworks have not yet fully caught up with these innovations: in many jurisdictions, it remains unclear how to classify AMM operators, liquidity providers or token holders for purposes of securities law, AML obligations or consumer protection, creating uncertainty for both regulated financial institutions that might wish to participate and for DeFi developers themselves. Nevertheless, hybrid models are emerging in which regulated institutions partner with DeFi project teams or use white‑label solutions to build compliant trading venues that combine centralized and decentralized components, signaling a gradual convergence between traditional capital markets and on‑chain liquidity mechanisms.

Investing In Crypto: Use Cases, Strategies And Risk

Crypto’s investment appeal stems from several interlocking narratives: the possibility of outsized returns in a nascent asset class, the idea of digital scarcity as a hedge against monetary expansion, and the promise of participating in the growth of new financial and computing infrastructures. Empirical evidence indicates that a substantial fraction of crypto activity is indeed speculative: central‑bank analyses note that the fascination with cryptocurrencies has been driven more by expectations of profit than by usage as everyday payment instruments, and Deutsche Bank research estimates that around two‑thirds of Bitcoin holdings are used for investment and speculation rather than transactional purposes. For many investors, especially younger cohorts, crypto also embodies a cultural and ideological dimension, linked to distrust of legacy institutions and enthusiasm for open‑source technology, which can influence risk tolerance and time horizons in ways that differ from traditional portfolio theory. As crypto has matured, however, institutional investors and family offices have increasingly approached it through more conventional lenses of diversification, risk budgeting and scenario analysis, sometimes using exchange‑traded products or managed accounts rather than holding tokens directly.

The range of investment strategies in crypto spans from long‑term “buy and hold” approaches focused on assets like Bitcoin and Ether to active trading, yield farming, arbitrage and venture‑style investments in early‑stage tokens or protocol equity. Long‑term holders may dollar‑cost average into positions and ignore short‑term volatility, believing that network effects and adoption will drive appreciation over multi‑year horizons, while traders exploit intra‑day moves and cross‑exchange price discrepancies in highly liquid markets. DeFi introduces additional dimensions, such as earning yields by providing liquidity, staking tokens to secure proof‑of‑stake networks, or depositing stablecoins into lending protocols, but these activities come with smart‑contract, governance and liquidity risks that can be difficult to quantify. In recent years, public‑company treasury strategies that accumulate large Bitcoin positions—for example, Strategy Inc.’s multi‑billion‑dollar holdings financed partly through debt and equity issuance—have attracted attention as a corporate form of crypto investment, but the turmoil around the firm’s STRC perpetual preferred stock highlights that such strategies embed complex interactions between crypto prices, capital structure and cash‑flow coverage.

Speculation, Saving And Long‑Term Allocations

A key question for both individuals and institutions is whether crypto should be treated primarily as a speculative trading asset or as a long‑term savings vehicle. The concept of “HODLing,” or holding crypto through extreme volatility without selling, has become a cultural meme, and E*Trade’s analysis of Bitcoin cycles notes that some investors adopt “hold on for dear life” strategies in anticipation of post‑halving bull markets. Such approaches may be appropriate only for those with high risk tolerance and long horizons, as past cycles have involved peak‑to‑trough drawdowns near 80 percent and multi‑year recovery times, and there is no guarantee that future cycles will replicate historical patterns. Families considering strategies such as saving crypto for their children’s future must weigh the potential upside against the possibility that technological, regulatory or competitive developments could significantly impair the value of current leading assets over a decade or more, and should consider diversifying across asset classes and maintaining prudent position sizes relative to overall net worth.

Institutional allocators, including pension funds and insurers, generally approach crypto with more conservative sizing and stricter governance. A notable recent example is a Japanese corporate pension fund, reported to be planning to allocate around 1 percent of its assets to crypto starting in fiscal year 2026, signaling cautious interest in digital assets as part of diversified portfolios while remaining aware of regulatory and reputational concerns. Such small allocations can still be meaningful if crypto appreciates strongly, while limiting downside impact if the asset class underperforms or experiences structural setbacks. Similarly, corporate treasuries holding Bitcoin on balance sheet may frame it as a long‑term reserve asset or strategic bet on digital scarcity, but the experience of Strategy Inc., whose STRC preferred stock has fallen below par amid worries about debt and fixed dividend obligations, demonstrates that financing structures and market perceptions of cash‑flow coverage are critical: even if Bitcoin’s price rises, a company with strained cash flows or high leverage may struggle to service obligations, putting equity and preferred holders at risk. These examples underscore that crypto exposure can be implemented at many levels of the capital stack—from direct token holdings to public‑company equities and structured products—and that each carries distinct risk characteristics that investors must evaluate.

Risk Management, Security Threats And Crime

Crypto investing presents a dense array of risks that extend beyond price volatility, encompassing technical, operational, legal and even physical threats. Technical risks include smart‑contract vulnerabilities, protocol bugs and consensus failures, any of which can lead to loss of funds or chain splits; operational risks arise from exchange hacks, phishing attacks, key mismanagement and cloud outages; and legal risks involve evolving regulatory classifications that could affect token liquidity or impose retroactive compliance obligations. High‑profile incidents such as the 2011 Mt. Gox breach, where a hacker briefly crashed Bitcoin’s price on the exchange from 17 dollars to one cent using a stolen auditor password and the platform later rolled back trades amid chaos, illustrate how centralized infrastructure weaknesses can impact market integrity even when core protocols remain intact. More recent incidents of exchange insolvencies, DeFi hacks and oracle manipulations reinforce the importance of counterparty diligence and diversification of custody arrangements, especially for larger holders and institutions.

Illicit finance and associated law‑enforcement responses form another crucial dimension of crypto risk. Stablecoins and other crypto assets have been used for money laundering, sanctions evasion and financing of criminal enterprises, taking advantage of pseudonymous addresses and cross‑border transferability. Brookings cites Chainalysis estimates that between 25 and 32 billion dollars in stablecoins were received by illicit actors in 2024, representing roughly 12 to 16 percent of the sector’s year‑end market capitalization, a non‑trivial share that has drawn intense scrutiny from regulators and policymakers. Additional Chainalysis data reported in media indicate that in Brazil, around 80 percent of illicit crypto flowing into exchanges has been routed through just five addresses, driven by cartel activity, Chinese‑language networks and Russian sanctions evasion, illustrating how forensic analytics can identify concentration points even in decentralized systems. Beyond financial crime, the rise of crypto has been accompanied by physical‑security incidents, including kidnappings and armed robberies targeting individuals known to hold large crypto balances, as well as cybercrime such as malware disguised as harmless files—for example, “anime girl wallpaper” downloads that covertly install crypto‑stealing payloads. These threats have prompted law‑enforcement crackdowns and public vows from officials, including high‑profile statements by FBI leadership about intensifying efforts against crypto‑related fraud, and have led major platforms like Meta to cooperate in freezing illicit funds and assisting investigations.

Investors seeking to manage these risks need to adopt a holistic approach that integrates cybersecurity best practices, diversified custody, careful selection of counterparties and attention to regulatory developments. Basic measures include using hardware wallets or secure custodial solutions, enabling multi‑factor authentication, segmenting devices for crypto activity and remaining vigilant about phishing and social‑engineering attempts. For larger portfolios, institutional‑grade custody with robust internal controls, insurance and independent audits may be appropriate, along with policies for access control, transaction approval and incident response. On the legal side, investors should be aware of their jurisdiction’s tax treatment of crypto, reporting requirements and any restrictions on particular tokens or services, and should recognize that regulatory shifts—for example, reclassifying a token as a security—can have material implications for liquidity and compliance costs. Ultimately, while high potential returns attract capital to crypto, risk management remains central to long‑term survival in a market that continues to experience both innovation and periodic crises.

Framework Ventures' Michael Anderson says crypto's next trillion-dollar opportunity is financing AI and robotics, with blockchains evolving into capital markets infrastructure

$31.4B of distributed RWA value is already on-chain per RWA.xyz, but roughly $14.6B of that is U.S. Treasury debt while distributed asset-backed credit is only about $2.2B. Financing robotics and AI pushes crypto into underwriting utilization, hardware depreciation, energy costs, and machine revenue streams, much closer to equipment leasing than vanilla tokenization. If Framework is right, Maple/Centrifuge-style credit markets and DePIN operators start sharing the same primitive: verifiable cash-flow collateral with 24/7 settlement.

- 2023-Q3milestone

Tokenized T-bills hit $665M in on-chain RWA assets

- 2023-11regulatory

Sam Bankman-Fried convicted on all seven counts of fraud and conspiracy

- 2024-08milestone

BTC drops below $50K; crypto market sheds $600M in leveraged positions in 24h

EU MiCA stablecoin provisions fully enforced, imposing transaction volume caps

Trump administration directs SEC to pull back crypto enforcement, reassigning 50+ lawyers

- 2025-03regulatory

UAE exempts all crypto transactions from VAT

- 2025-06launch

Uniswap partners with Robinhood to enable in-app crypto trading with $10 USDC promotion

Regulation, Policy And Compliance

As crypto’s market capitalization and interconnectedness with traditional finance have grown, regulators worldwide have intensified efforts to create coherent frameworks that address consumer protection, market integrity, financial stability and national‑security concerns. Central banks and financial supervisors initially viewed crypto as a niche phenomenon, but rising retail participation, institutional exposure and the emergence of systemic‑scale infrastructures such as stablecoins have elevated the perceived stakes. Regulatory responses have varied by jurisdiction, from outright bans on certain activities to licensing regimes for exchanges and custodians, and from enforcement‑led approaches that apply existing securities and commodities laws to efforts to enact bespoke digital‑asset legislation. Across these approaches, several common themes emerge: the desire to prevent money laundering and terrorist financing, the need to clarify whether and when tokens are securities or commodities, and the aim of mitigating risks from run‑prone stablecoins and leverage‑driven DeFi products.

At the same time, policymakers must navigate trade‑offs between fostering innovation and safeguarding financial systems. Overly restrictive rules may push activity offshore or into unregulated shadows, while under‑regulation can leave consumers exposed to fraud and systemic vulnerabilities. Global standard‑setting bodies such as the Financial Stability Board, the Basel Committee on Banking Supervision and the Financial Action Task Force have issued guidance on prudential treatment of crypto exposures, travel‑rule obligations for virtual‑asset service providers and risk management for stablecoins, but implementation remains uneven across countries. In major markets such as the United States and the European Union, legislative and regulatory initiatives in 2023–2025 have significantly reshaped the landscape, including the EU’s Markets in Crypto‑Assets Regulation (MiCA), the US GENIUS Act on stablecoins and proposed US acts such as the Digital Asset Market Clarity Act and Responsible Financial Innovation Act.

United States: SEC, CFTC, Congress And The Trump‑Era Debate

In the United States, regulatory authority over crypto has been divided primarily between the Securities and Exchange Commission (SEC), which oversees securities markets, and the Commodity Futures Trading Commission (CFTC), which regulates derivatives and commodity spot‑market fraud, along with banking regulators that supervise stablecoin‑related activities. Historically, the SEC has applied the Howey test to determine whether particular tokens constitute investment contracts and therefore securities, bringing enforcement actions against issuers and platforms it believes have conducted unregistered offerings or operated unregistered exchanges. Industry participants have criticized this “regulation by enforcement” approach and have pushed for clearer legislative definitions distinguishing securities from so‑called “digital commodities.” In response, Congress has debated several bills, most notably the Digital Asset Market Clarity Act (often dubbed the CLARITY Act) and the Responsible Financial Innovation Act (RFIA), which propose alternative frameworks for classifying and regulating digital assets.

According to legal analyses, the CLARITY Act, passed by the House of Representatives in July 2025 by a bipartisan vote, would establish a market‑structure framework that defines a “digital commodity” as a digital asset intrinsically linked to a blockchain system whose value is derived from the use of that system, while treating tokens as securities when they function as part of an investment contract conferring rights in the issuer’s profits or assets. Under this bill, digital assets are presumed to be securities by default until they are demonstrated to be part of a “mature” decentralized blockchain system; issuers bear the burden of filing a notice with the SEC and substantiating that the asset meets decentralization criteria, after which it would become a digital commodity upon SEC approval or by default after 60 days if the SEC does not act. The RFIA discussion draft, led in the Senate by members including the Banking Committee chair and crypto‑friendly lawmakers, would create an alternative classification regime that gives the SEC broader authority to define “ancillary assets” that are not securities and to require more extensive disclosures when issuers self‑certify decentralization, potentially allowing the SEC to retain greater oversight. As of mid‑2020s, the ultimate fate of the CLARITY Act in the Senate remains uncertain, and the interplay between it and RFIA is a focal point of industry lobbying and political debate.

The GENIUS Act, enacted in July 2025, specifically targets stablecoins, requiring issuers to back payment stablecoins one‑to‑one with permitted reserves such as cash, Treasuries and certain money‑market instruments, to provide monthly disclosures on reserve composition, and to comply with federal anti‑money‑laundering obligations, while banning the payment of interest on such stablecoins. The Comptroller of the Currency within the Treasury is designated as the federal regulator for non‑bank stablecoin issuers, whereas bank subsidiaries issuing stablecoins fall under their existing prudential regulators, and smaller issuers may opt for state‑level oversight if their outstanding tokens remain below a ten‑billion‑dollar threshold. Notably, the law excludes “non‑payment stablecoins,” including most algorithmic designs, from its scope, leaving them under state regulation, and leaves open questions about tax treatment, standards for foreign stablecoins marketed in the US and conflicts‑of‑interest policies for issuers—issues that regulators must clarify by 2026. Policy debates have been further complicated by the growing involvement of prominent political families, including the Trump family, in crypto businesses, raising concerns about potential conflicts of interest as federal agencies craft rules affecting enterprises in which politically connected individuals have stakes. Against this backdrop, agencies such as the SEC have continued enforcement actions against exchanges, lending platforms and token issuers, even as major US‑based firms like Coinbase seek to position themselves as compliant actors and expand globally in anticipation of clearer, more durable rules.

Europe, Asia And Global Standard‑Setting

The European Union has moved toward a relatively comprehensive approach to crypto regulation through MiCA and a broader AML package. MiCA, adopted in 2023, sets requirements for issuers of asset‑referenced tokens and e‑money tokens, including obligations regarding reserve composition, governance, disclosure and redemption rights, and notably prohibits charging fees for token redemption and paying interest on stablecoins, aligning with policymakers’ view that stablecoins used for payments should resemble narrow‑banking instruments rather than deposit substitutes. In parallel, the EU has overhauled its anti‑money‑laundering framework through a package that includes the creation of a new Anti‑Money‑Laundering Agency (AMLA) in Frankfurt, which will directly supervise high‑risk financial entities and coordinate national regulators, and a regulation extending “travel rule” information requirements to certain crypto transfers. Under Regulation (EU) 2023/1113, information accompanying transfers of funds and certain crypto assets must be collected and transmitted, with the European Banking Authority tasked with issuing guidelines on restrictive measures by December 2024, while broader AML regulations and directives will expand obliged entities, impose stricter transparency and ban cash transactions above 10,000 euros starting in 2027, alongside tighter rules for crypto‑asset transfers above 1,000 euros. These measures signal a clear intent to bring crypto firmly within the financial‑crime‑prevention architecture, potentially increasing compliance costs but also enhancing legitimacy for regulated actors.

In Asia and emerging markets, regulatory approaches are diverse but increasingly convergent in recognizing the need for licensing of exchanges and clear rules for stablecoins and tokenized assets. India, for instance, has oscillated between restrictive stances and more pragmatic engagement, imposing high taxes on crypto trading while allowing regulated entities to operate within certain parameters. Coinbase’s launch of direct Indian rupee rails and product offerings in India illustrates corporate efforts to navigate this evolving landscape and to tap into a large, tech‑savvy population, even as legal and tax uncertainties persist. Japan, by contrast, has long maintained a licensing regime for exchanges and has recently seen its corporate pension sector test the waters of crypto investment, with a national SME pension fund reportedly planning a modest 1 percent allocation by fiscal year 2026, indicating a cautious but notable shift toward institutional acceptance. At a global level, TRM Labs’ review of 2025 crypto policy developments across 30 jurisdictions, representing over 70 percent of global crypto exposure, highlights trends toward more harmonized AML standards, increased focus on stablecoin reserve transparency and emerging discussions about how to regulate DeFi and non‑custodial services without stifling innovation.

Law‑enforcement and compliance practices are also evolving in response to crypto‑enabled illicit activities. The new EU AMLA and national financial intelligence units are expected to leverage blockchain analytics to more quickly identify suspicious patterns and link addresses to real‑world entities, while in the US and elsewhere, high‑profile crackdowns on frauds, kidnappings and laundering schemes underscore growing investigative capacity and inter‑agency coordination. For market participants, this trajectory means that compliance with travel‑rule obligations, KYC standards and suspicious‑activity reporting is becoming indispensable for operating at scale, and that even DeFi projects and non‑custodial services may face pressure to incorporate compliance‑enabling features or interfaces as regulators grapple with appropriate models of oversight.

AI, Automation And The Future Of Crypto

The intersection of artificial intelligence and crypto is emerging as a significant theme, with implications for security, infrastructure economics and the organization of digital labor. On the security front, AI‑powered tools are being deployed to analyze smart‑contract code, identify vulnerabilities and suggest fixes at a speed and scale that traditional manual audits cannot match, potentially raising the baseline of code quality and reducing some categories of exploits. Developers and auditors can use machine‑learning models to scan large repositories of contracts, learn patterns associated with known vulnerabilities and flag risky constructs before deployment, which is particularly valuable in DeFi, where bugs can immediately expose hundreds of millions of dollars to theft. At the same time, adversaries can harness AI to automate phishing, generate polymorphic malware, discover novel attack vectors and even manipulate social‑media narratives around tokens and protocols, creating an arms race in which both defenders and attackers benefit from more powerful tools. This dynamic heightens systemic risk because vulnerabilities can be exploited faster and more efficiently, and because socially engineered attacks against key individuals, including developers and large holders, may become more convincing and harder to detect.

Beyond security, AI is reshaping the economics and strategic choices of crypto infrastructure providers, particularly miners and data‑center operators. Bitcoin miners run energy‑intensive hardware that is optimized for hashing, and their profitability fluctuates with Bitcoin’s price, block rewards (which halve every four years) and electricity costs. As halving events reduce block subsidies and competition pushes older hardware to the brink of unprofitability, some mining firms are repurposing or expanding their data‑center capabilities to provide compute for AI workloads, which may offer more stable revenue streams, especially given the surging demand for training and inference resources. Industry reports note that miners are “doubling down” on AI by leasing capacity to AI companies or building out new infrastructure, while tokenized real‑world asset markets, including tokenized treasuries and credit, have grown to tens of billions of dollars, indicating a broader convergence between digital‑asset markets and other forms of digitized capital and computation. These shifts suggest that the future of Bitcoin mining and other proof‑of‑work systems will increasingly be intertwined with the broader data‑center and AI economy, with implications for energy policy, geographic distribution of hash power and potential centralization risks.

AI As A Security Tool And Attack Vector

AI’s role in crypto security is multifaceted and evolving. On the defensive side, AI‑driven static and dynamic analysis tools can automate large portions of code review for smart contracts, identifying common pitfalls such as reentrancy, integer overflows and access‑control flaws, and can learn from past exploit patterns to detect more subtle vulnerabilities that might escape rule‑based scanners. These tools lower the cost and increase the speed of audits, enabling more projects, including smaller teams with limited budgets, to obtain at least baseline security assessments before deploying contracts that will hold user funds, which could reduce the frequency of certain classes of DeFi hacks. Additionally, AI can assist in real‑time monitoring of on‑chain activity, flagging anomalous transactions, suspicious patterns of fund movement or unusual interactions with protocols that may indicate exploitation in progress, thereby giving teams and exchanges more time to activate emergency controls such as pausing contracts or freezing withdrawals.

On the offensive side, AI can enhance attackers’ capabilities in several ways. Generative models can produce highly personalized phishing emails, messages or deepfake audio and video that convincingly impersonate known figures in the crypto space, tricking users into revealing private keys, signing malicious transactions or installing malware. Machine‑learning algorithms can also analyze vast numbers of smart contracts to identify those with exploitable vulnerabilities, prioritize targets based on potential yield and even autonomously craft exploit transactions or flash‑loan strategies to drain funds at scale. As defenses improve, attackers can adapt quickly, training models on new detection patterns and devising ways to bypass heuristics used by exchanges and analytics firms, similar to the ongoing cat‑and‑mouse game in traditional cybersecurity but with the added complication that on‑chain exploits often settle irreversibly and rapidly. This dynamic raises the prospect of more sudden, large‑scale failures in DeFi if systemic vulnerabilities are discovered and exploited simultaneously across multiple protocols, and it underscores the need for robust, well‑resourced security practices, including formal verification, responsible disclosure processes and contingency mechanisms.

Mining, Data Centers And “Liquid Machine Labor”

The relationship between AI and crypto is also playing out in debates about the future of work and organizational forms. Some theorists have proposed a “liquid machine labor” thesis, in which AI agents and robots, coordinated via crypto‑based protocols and decentralized autonomous organizations (DAOs), could perform tasks and receive or distribute crypto payments without traditional employment structures, effectively dissolving some aspects of the firm into open networks. While such scenarios remain speculative, elements of this vision can already be seen in autonomous market‑making robots, algorithmic trading bots and on‑chain task marketplaces where contributors perform micro‑tasks in exchange for tokens. As AI systems become more capable, they may increasingly participate in on‑chain economic activity, whether by optimizing liquidity provision, dynamically rebalancing portfolios or negotiating resource allocation in decentralized compute markets, raising complex questions about liability, regulation and the definition of legal personhood.

Bitcoin miners and other infrastructure operators stand at a particularly interesting nexus of these trends. Faced with rising energy costs, environmental scrutiny and declining per‑block rewards after halvings, miners have incentives to diversify revenue streams, and the burgeoning demand for AI computation offers a natural adjacency: both activities require substantial power and specialized hardware, and both benefit from cheap electricity and favorable regulatory environments. Reports of miners “doubling down on AI” by dedicating part of their capacity to AI workloads suggest a future in which mining farms function as hybrid facilities, shifting resources between securing blockchains and training models depending on relative profitability. This evolution could affect Bitcoin’s security assumptions if significant hash power migrates toward multi‑purpose hardware that is more mobile and potentially more sensitive to external economic shocks, and it reinforces the interconnectedness of seemingly distinct digital infrastructures. For policymakers, the convergence of AI, crypto and tokenized real‑world assets complicates regulatory silos, as activities that once fell squarely under financial regulation now intersect with data‑protection, competition and industrial policy, making interdisciplinary approaches increasingly necessary.

The US is mid-pivot from aggressive enforcement to deregulation while the EU enforces MiCA stablecoin caps and the IMF embeds anti-crypto clauses in sovereign bailouts, creating simultaneous liberalization and restriction across major markets.

Leveraged positions remain the primary amplifier of volatility: a single macro equity downturn wiped $600M in positions and triggered $272M in liquidations within 24-hour windows.

- Fraud / ScamHigh

Pig-butchering operations have scaled to a billion-dollar global industry, fake market makers drew SEC charges, and high-profile fraudsters (Do Kwon, SBF, Denver pastor) continue to evade or delay accountability.

- Security / WalletHigh

Fireblocks disclosed multiple zero-day vulnerabilities across major wallet implementations simultaneously, and Cthulhu malware specifically targeted MetaMask, Coinbase Wallet, and Binance on macOS.

SEC subpoenas of early-stage VC firms and the Binance complaint over market structure definitions expose how concentrated capital and gatekeepers still shape which projects survive regulatory cycles.

Liquidity pool design and automated market-making remain functional but exposure to cascading liquidations during correlated sell-offs means protocol-level risk is latent rather than dormant.

Outlook

Crypto has evolved from a fringe experiment into a complex, globally relevant ecosystem encompassing monetary experiments, programmable finance, tokenized assets and emerging intersections with AI and automation. Its core technologies—blockchains, smart contracts and cryptographic tokens—enable new forms of coordination and value transfer, but they also introduce novel risks and amplify familiar ones, from leverage‑driven booms and busts to fraud, cybercrime and regulatory arbitrage. Over the coming years, key drivers of the industry’s trajectory will include the maturation of regulatory frameworks such as the US GENIUS Act and CLARITY Act, the EU’s MiCA and AML package and potential “MiCA 2.0” refinements for DeFi and stablecoins; the degree to which institutional investors, including pension funds and corporates, integrate crypto into diversified portfolios; and the pace at which AI‑enhanced security tools can outpace AI‑enabled attacks.

At the market level, Bitcoin’s halving‑driven cycles will likely continue to shape sentiment and capital flows, but they will do so against a backdrop of increasing macro and regulatory interdependence, where events like corporate balance‑sheet stress at Bitcoin‑heavy firms (as seen in Strategy Inc.’s STRC preferred stock turmoil) or law‑enforcement crackdowns on illicit flows can have outsized impact. Exchanges such as Coinbase and hybrid DeFi venues that support both crypto‑native and tokenized traditional assets will remain crucial points of contact between on‑chain and off‑chain finance, and their success or failure in managing operational risk, compliance obligations and product innovation will influence mainstream perceptions of the sector. For investors and users, the central challenge is to balance enthusiasm for the transformative potential of crypto with sober assessment of its uncertainties: saving some exposure for long‑term goals, including intergenerational wealth, may be sensible for those who fully understand the risks and can afford volatility, but over‑leveraged bets or uncritical faith in historical patterns could prove costly in what may be an increasingly brutal competitive and regulatory landscape.

Latest Crypto news

Binance founder CZ backs efforts to make the U.S. the global crypto capital, sharing his outlook on regulation, innovation, and digital asset adoptionSBI's $289M acquisition of Bitbank signals a new phase of consolidation in Japan's crypto industry as regulation pushes exchanges toward scale and institutional strengthFramework Ventures' Michael Anderson says crypto's next trillion-dollar opportunity is financing AI and robotics, with blockchains evolving into capital markets infrastructure Husher’s no-kyc crypto swap raises regulatory concerns despite 2-second settlement promise

Husher’s no-kyc crypto swap raises regulatory concerns despite 2-second settlement promise Binance founder CZ says crypto's 50% slide stems from AI capital rotation, geopolitical tensions and the industry's recurring four-year market cycle

Binance founder CZ says crypto's 50% slide stems from AI capital rotation, geopolitical tensions and the industry's recurring four-year market cycle EU MiCA licenses near 230 before July 1 deadline as smaller crypto firms face shutdown pressure

EU MiCA licenses near 230 before July 1 deadline as smaller crypto firms face shutdown pressureSources

- https://cryptorank.io/news/feed/50dd4-strc-decline-strategy-financial-structure-analysts

- https://ground.news/article/strategy-stock-is-under-pressure-whats-happening-today_835b07

- https://www.crowdfundinsider.com/2026/06/286778-bitcoin-and-crypto-markets-face-significant-challenges-amid-strategys-preferred-stock-strc-turmoil/

- https://www.rba.gov.au/education/resources/explainers/cryptocurrencies.html

- https://www.db.com/what-next/digital-disruption/dossier-payments/i-could-potentially-see-bitcoin-to-become-the-21st-century-gold?language_id=1

- https://us.etrade.com/knowledge/library/cryptocurrency/cryptocurrency-seasons

- https://x.com/WuBlockchain/status/2068562870653337772

- https://www.facebook.com/loveofhistoryy/posts/this-video-revisits-one-of-the-most-puzzling-moments-in-modern-tech-history-the-/856152283885392/

- https://x.com/CoinDesk/status/2068383627566813511

- https://x.com/Ellaweb_3/status/2068582069433704574

- https://www.coinbase.com/blog/coinbase-secures-registration-in-india

- https://bitcoinfoundation.org/news/bitcoin/bitcoin-vs-gold-which-is-the-better-store-of-value/

- https://www.brookings.edu/articles/what-are-stablecoins-and-how-are-they-regulated/

- https://www.bankinghub.eu/innovation-digital/liquidity-pools-automated-market-making

- https://www.trmlabs.com/reports-and-whitepapers/global-crypto-policy-review-outlook-2025-26?scLang=en

- https://www.akingump.com/en/insights/alerts/crypto-clarity-the-politics-policy-and-implications-of-digital-assets-regulatory-framework-legislation-in-the-119th-congress

- https://www.dlapiper.com/insights/publications/global-anti-corruption-perspective/new-eu-anti-money-laundering-rules-what-to-know

- https://www.coinbase.com/blog/coinbase-launches-in-india-with-direct-inr-rails

- https://fr.tradingview.com/news/cointelegraph:ebd64841a094b:0-crypto-biz-is-ai-the-exit-strategy-for-miners/

Community notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…