Deep dive on Franklin Templeton’s crypto strategy, covering its Benji onchain money market fund, multi-chain tokenization, bitcoin and Solana ETFs, dividend-to-bitcoin DRIP products, and key partnerships with Kraken, MoonPay, Avalanche, Aptos, and tZERO.

+18 sources across the wider coverage universe

Franklin Templeton Digital Assets warns AI could pressure private credit and DeFi ecosystems, with insights from Roger Bayston on shifting financial conditions2026-04

Franklin Templeton Digital Assets warns AI could pressure private credit and DeFi ecosystems, with insights from Roger Bayston on shifting financial conditions2026-04 Unlocking RWA potential: Sandy Kaul's insights from Franklin Templeton2026-04

Unlocking RWA potential: Sandy Kaul's insights from Franklin Templeton2026-04 Scrypt partners with Franklin Templeton to bring tokenized treasuries to Swiss-regulated infrastructure2026-06

Scrypt partners with Franklin Templeton to bring tokenized treasuries to Swiss-regulated infrastructure2026-06 Franklin Templeton doubles down on crypto adoption, saying digital assets are here to stay as it pushes traditional finance further onchain through its Benji platform2026-05

Franklin Templeton doubles down on crypto adoption, saying digital assets are here to stay as it pushes traditional finance further onchain through its Benji platform2026-05 Franklin Templeton CEO Jenny Johnson says Wall Street's resistance to blockchain stems from economics, arguing crypto and tokenization threaten many of traditional finance's most profitable business models2026-06

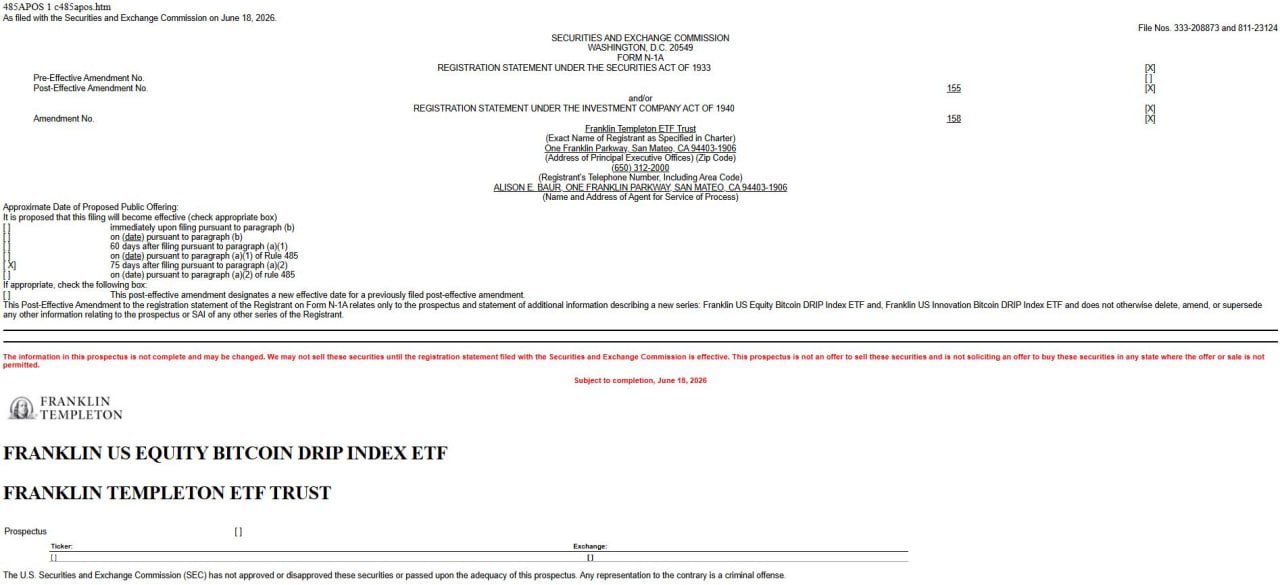

Franklin Templeton CEO Jenny Johnson says Wall Street's resistance to blockchain stems from economics, arguing crypto and tokenization threaten many of traditional finance's most profitable business models2026-06 Franklin Templeton files two Bitcoin DRIP ETFs that reinvest equity dividends into BTC2026-06

Franklin Templeton files two Bitcoin DRIP ETFs that reinvest equity dividends into BTC2026-06

Franklin Templeton in the Crypto Era: Onchain Funds, Bitcoin ETFs, and Tokenization

Franklin Templeton is a global asset manager with more than a trillion dollars under management that has become one of the most aggressive traditional finance firms pushing money market funds, ETFs, and other investment products onto public blockchains. For a crypto audience, it now functions less as a distant mutual-fund brand and more as a central player in real‑world asset tokenization, onchain treasuries, and new ETF structures that route conventional cash flows into bitcoin and other digital assets.

Franklin Templeton: From Legacy Asset Manager to Digital Asset Pioneer

Franklin Templeton is historically known as a diversified asset manager offering mutual funds, ETFs, and institutional mandates across fixed income, equities, alternatives, and multi‑asset strategies. Founded in 1947, the firm has built a global footprint with operations in more than 35 countries and clients in over 150 markets, managing roughly between 1.5 and 1.7 trillion dollars in assets in recent years depending on market conditions. This scale matters in the crypto context because it means Franklin is not a niche digital‑asset startup, but a systemically relevant institution whose decisions influence how pensions, banks, and wealth managers perceive blockchain technology. When a manager of this size embraces tokenization or launches crypto‑linked ETFs, it signals that digital assets have moved from the fringes to the core of institutional asset allocation debates.

The firm’s transition into digital assets has been deliberate rather than opportunistic. Franklin Templeton began building formal “digital asset expertise” around 2018, well before the most recent cycles of tokenization and spot bitcoin ETF approvals. Internally, it has positioned digital assets as both an investment theme and a technology stack, combining tokenomics research, data science, and technical engineering to design products that can operate directly on public blockchains. This approach differentiates Franklin from managers who simply buy bitcoin or use private ledgers; its flagship experiments are designed to use public chains as the authoritative record for regulated investment products. In doing so, the firm has taken on additional regulatory, operational, and reputational risk, but has also secured first‑mover advantages in tokenized funds and onchain infrastructure.

The cultural shift within Franklin Templeton has been articulated publicly by its leadership. Chief executive Jenny Johnson has argued that blockchain technology and digital assets threaten some of Wall Street’s most profitable legacy business models, which explains why many incumbents are slow to embrace the technology. In her telling, Franklin’s strategy is to get ahead of this disruption rather than resist it, by embedding blockchain into fund administration, settlement, and collateral management workflows. That posture is reflected in the firm’s willingness to experiment with public chains like Stellar, Polygon, Avalanche, Arbitrum, and Aptos as infrastructure for regulated products, rather than confining tokenization to closed, bank‑owned consortia. For crypto‑native observers, this makes Franklin one of the most interesting case studies of how large TradFi institutions might actually integrate with open networks rather than simply wrapping them in traditional rails.

Aptos Labs says BlackRock, Franklin Templeton, and Apollo tokenized funds are live on Aptos

Promoting from Tsunami auto-feed. Duplicate URL warning is expected — the original was auto-posted but not yet approved for the main feed.

Readers click Franklin Templeton stories as a real-time map of where institutional on-chain infrastructure is actually deploying — the FOBXX multi-chain expansion and collateral-integration headlines consistently outperform ETF-filing stories, revealing that the signal readers want is 'where is the institutional money landing on-chain,' not 'what has been filed with the SEC.'↗

Building Franklin Templeton Digital Assets

Franklin Templeton’s digital initiatives are now organized under dedicated business and product lines often described collectively as Franklin Templeton Digital Assets. The firm describes itself in multiple public communications as a “pioneer in digital asset investing and blockchain innovation,” emphasizing that it combines tokenomics research, quantitative data analysis, and technical development to create investable products that function safely on public blockchains. Unlike some competitors who confine digital efforts to marketing or thematic equity funds, Franklin’s digital unit is directly responsible for designing tokenized funds, onchain infrastructure features, and partnerships with crypto‑native firms. This orientation positions digital assets not as a marginal product silo, but as a technology strategy that touches fund administration, distribution, and capital markets activity across the organization.

A key milestone in formalizing this strategy was Franklin’s agreement to acquire Liquid Strategies, a business spun out from digital asset firm CoinFund, and to launch a new platform branded Franklin Crypto. The acquisition, announced in 2026, is framed as a way to accelerate Franklin’s push into tokenized strategies and actively managed digital asset products, complementing its existing expertise in money markets and fixed income. By absorbing a crypto‑native team, Franklin gains portfolio managers and technologists who can design strategies optimized for onchain liquidity, DeFi integrations, and 24/7 markets, rather than simply grafting legacy approaches onto new rails. The Franklin Crypto unit is presented by the firm as a bridge between traditional asset management discipline and the experimental, fast‑moving world of decentralized finance.

Research and risk analysis are another core pillar of the digital assets platform. Franklin’s digital assets materials explicitly note that competitive pressures and evolving market dynamics could make it difficult for digital asset funds to gather sufficient assets or achieve commercial success. They also highlight that tokenized products carry risks related to custody, transfer, smart contracts, and the reliability of onchain infrastructure—risks that do not exist in the same form for conventional securities held through central depositories. At the same time, the firm has begun publishing insights on how emerging technologies like artificial intelligence interact with digital assets, including potential impacts on private credit and DeFi ecosystems. For crypto professionals, this combination of product‑driven experimentation and sober risk disclosure is significant, because it shows that large managers can acknowledge both the promise and the fragility of early tokenization markets.

Finally, Franklin Templeton has framed tokenization as part of a structural shift in financial market infrastructure rather than a short‑term bet on cryptocurrency prices. Its public materials consistently emphasize programmable settlement, always‑on collateral, and the ability to embed compliance and yield logic directly in tokens as key reasons to move funds onchain. That framing aligns with the way many policymakers and international organizations discuss tokenization: less as a speculative phenomenon and more as a technological re‑platforming of securities issuance and trading. For crypto markets, this matters because it suggests that large flows into tokenized treasuries and real‑world assets may persist even in periods when pure crypto‑asset prices are under pressure, anchoring a more durable institutional presence onchain.

The Benji Platform and the Franklin OnChain U.S. Government Money Fund

Design and investment profile of FOBXX

The centerpiece of Franklin Templeton’s onchain strategy is the Franklin OnChain U.S. Government Money Fund, trading under the ticker FOBXX and commonly known by its token brand “Benji.” Launched in 2021, this vehicle is widely cited as the world’s first U.S.‑registered mutual fund to use a public blockchain as its primary or official system of record for processing transactions and recording share ownership. In economic terms, FOBXX is a conservative money market fund that invests at least 99.5 percent of its assets in U.S. government securities, cash, and repurchase agreements fully collateralized by U.S. government securities or cash. That means the underlying portfolio consists of short‑dated Treasury bills, government agency securities, and overnight repos, aligning it with traditional cash‑management products used by corporations and institutions for principal preservation and modest yield. For crypto users, the importance of FOBXX lies not in its asset mix, but in the fact that the fund’s shares are natively represented as tokens on public blockchains, allowing them to circulate and be pledged as collateral much like stablecoins.

From a regulatory perspective, FOBXX is a registered U.S. mutual fund advised by Franklin Templeton’s fixed income team, subject to the standard rules governing money market funds. The firm’s disclosures emphasize that although the fund invests in U.S. government obligations, its shares are neither insured nor guaranteed by the U.S. government, and investors can lose money. They also highlight additional risks that arise because share ownership and transfer are recorded on a blockchain, including potential issues with issuance, redemption, custody, and record keeping if the underlying network or smart contracts malfunction. These caveats are important to contrast BENJI with stablecoins that advertise a fixed redemption value but may not be subject to mutual fund regulation or the same degree of portfolio transparency. In practice, however, the economic behavior of FOBXX tokens is closely tied to stable dollar value, as the fund seeks to maintain a stable NAV while passing through yield from its short‑term government holdings.

BENJI tokens: mechanics, usage, and collateralization

Operationally, investors access FOBXX through the Benji Investments mobile application and related interfaces, which allow them to buy fund shares that are represented as tokens compliant with blockchain standards. Each BENJI token corresponds to a share in the underlying money market fund, with the blockchain serving as the record of share ownership and transfers instead of or alongside traditional transfer agent systems. Initially launched on the Stellar blockchain, the tokens can be transferred peer‑to‑peer, enabling secondary market activity among whitelisted investors without requiring each transfer to pass through legacy fund administration rails. Jenny Johnson has emphasized that these tokens are increasingly used as collateral within digital asset markets, with some hedge funds and stablecoin issuers preferring BENJI because it offers regulated exposure to U.S. Treasuries while remaining compatible with crypto‑native workflows and 24/7 settlement.

The use of BENJI tokens as collateral reflects a broader shift in how onchain capital markets are structured. Traditional collateral such as Treasury bills or tri‑party repo usually circulates via bank custodians and clearing systems that operate during business hours and rely on batch settlement cycles. By contrast, a token representing a mutual fund share can be pledged, rehypothecated, or transferred instantly onchain, while still conferring legal claims on a pool of regulated government securities managed by a familiar asset manager. As Johnson has noted, some participants “like the idea that they get yield on their collateral,” meaning they can post BENJI tokens to a counterparty or protocol while continuing to earn the underlying money market yield rather than holding idle cash. This design aligns closely with DeFi concepts of composable collateral and interest‑bearing tokens, but implemented within the regulatory framework of U.S. mutual funds rather than unconstrained smart contracts.

Franklin’s communications also highlight that BENJI tokens are being integrated into broader digital asset infrastructure. Social media commentary from market participants points out that money market funds tokenized by major asset managers—including Franklin’s BENJI and BlackRock’s BUIDL—have collectively surpassed 15 billion dollars in value, with specialized platforms such as Prime turning them into “always‑on collateral” for institutional transactions. While that figure aggregates multiple managers, it underscores how tokenized cash equivalents are becoming a significant asset class in their own right, with BENJI among the foundational components. For crypto traders and protocols, this means that a growing share of onchain liquidity will be backed by regulated government securities rather than purely synthetic or algorithmic stablecoins, potentially changing the risk profile of DeFi collateral markets.

Multi‑chain expansion: from Stellar to Avalanche, Polygon, Arbitrum, and Aptos

Franklin Templeton has not kept BENJI confined to a single blockchain. The firm’s journey began in 2019 when it tokenized shares of a money market fund on Stellar, using that network’s capabilities for inexpensive, fast settlement and built‑in asset issuance primitives. Over time, the OnChain U.S. Government Money Fund expanded beyond Stellar to additional public chains, including Avalanche, Arbitrum, and Polygon, reflecting both investor demand and Franklin’s belief in a multi‑chain future for tokenized securities. In 2024, the firm also leveraged its Benji Technology Platform to launch what it describes as the first fully tokenized UCITS fund in Luxembourg on Stellar, demonstrating that the same infrastructure could be extended to European regulated products. This multi‑jurisdiction, multi‑chain strategy indicates a willingness to treat public blockchains as interchangeable execution layers, with regulatory compliance handled at the fund and investor‑onboarding level rather than the chain level itself.

A particularly notable expansion was onto the Aptos blockchain, where Franklin Templeton’s Nasdaq‑listed On‑Chain U.S. Government Money Fund (FOBXX) now circulates alongside similar tokenized funds from BlackRock and other managers. CoinMarketCap’s coverage describes FOBXX as the first and only U.S.‑registered fund that uses public blockchains as its primary platform for processing and recording transactions and share ownership—a status it maintains even as it broadens to new chains. tZERO, a tokenization and trading infrastructure provider, has explicitly cited Franklin’s roughly 400 million dollar onchain money fund on Aptos, alongside BlackRock’s approximately 500 million dollar fund, as a key reason for integrating Aptos as a leading execution layer for real‑world assets. This illustrates a feedback loop in which Franklin’s tokenized fund not only benefits from but also helps catalyze the development of institutional‑grade RWA infrastructure across multiple chains.

For a crypto audience, the multi‑chain deployment of BENJI tokens carries several implications. It demonstrates that regulated asset managers are not betting on a single “winner chain,” but are instead building abstractions that can route tokenized assets to whichever networks offer the best combination of security, liquidity, and ecosystem integrations at a given time. It also underscores the importance of interoperability standards and cross‑chain bridges that can safely move tokenized fund shares between environments without fragmenting liquidity or undermining regulatory controls. As more chains compete to host RWAs and tokenized funds, Franklin’s approach offers a template for how to manage these deployments while preserving a coherent investor experience anchored in the Benji Platform.

Intraday yield and programmable finance on the Benji Platform

Beyond simply tokenizing fund shares, Franklin has used the Benji Technology Platform as a laboratory for new features that exploit the programmability of onchain assets. In 2025, the firm announced a patent‑pending “Intraday Yield” capability, which allows the proportional calculation and distribution of yield down to the second when a tokenized security is transferred. In practical terms, this means that if an investor holds a tokenized fund share for only part of a day, then transfers it to another investor, the system can accurately allocate that day’s accrued yield between the two holders based on their precise holding periods. Such granular pro‑rata calculations would be extremely cumbersome in traditional fund administration systems, but can be automated with smart contracts and integrated ledger logic on a blockchain.

Franklin highlights that this intraday yield feature is available both for its own tokenized funds and as a white‑label technology for banks and asset managers that wish to tokenize their own securities using the Benji Platform. This positions Benji not merely as a single‑fund wrapper, but as a broader infrastructure layer for tokenized capital markets, where yield‑bearing instruments can be issued, transferred, and integrated into applications with fine‑grained control over income distribution. For DeFi developers and institutional users alike, such functionality opens up possibilities for designing more complex lending, repo, and structured products in which yield is continuously and transparently allocated to token holders as they move collateral around the system.

In the context of stablecoin and RWA markets, intraday yield also hints at how tokenized treasuries may compete with or complement stablecoins as a store of value and medium of exchange. If an institution can hold BENJI tokens for a few hours, use them as collateral, and still receive the appropriate share of daily yield, the opportunity cost of moving out of risk‑free assets and into non‑yielding stablecoins becomes more visible. In practice, this might accelerate the integration of tokenized money market funds into stablecoin settlement flows and DeFi protocols, particularly as more on‑ and off‑ramps connect these regulated tokens to traditional and crypto‑native liquidity rails.

Distribution partnerships: MoonPay, DigiFT, and institutional channels

To scale its tokenized products, Franklin Templeton has pursued partnerships with platforms that can bridge between stablecoins, institutional treasuries, and regulated investors. A prominent example is the 2026 partnership with MoonPay, where Franklin connected the Benji Technology Platform with MoonPay Trade’s institutional infrastructure. The stated goal of this collaboration is to support stablecoin and digital asset market participants by allowing them to move seamlessly between onchain liquidity and tokenized money market funds, effectively turning stablecoin balances into yield‑bearing government exposure via BENJI. In functional terms, the partnership creates a pipeline through which institutions can swap stablecoins or other digital assets into Benji‑linked products and back, using MoonPay’s compliance and settlement rails as the interface layer.

Franklin has also extended Benji distribution through DigiFT, a regulated platform that offers blockchain‑integrated record‑keeping and tokenized securities services. Social media posts from the firm note that Benji’s blockchain record‑keeping system will be made available to accredited and institutional investors via DigiFT’s platform, further broadening the investor base and the venues in which BENJI tokens can circulate. Together with other white‑label and B2B offerings, these partnerships reflect Franklin’s view that tokenized funds must integrate with existing institutional workflows in order to achieve scale, rather than relying solely on direct retail apps.

For crypto‑native participants, these moves are significant because they embed tokenized funds into the broader digital asset stack. Stablecoin issuers, centralized exchanges, market‑makers, and DeFi protocols can all interact with BENJI through familiar intermediaries like MoonPay or through institutional marketplaces that understand both securities regulation and onchain settlement. Over time, this could shift a portion of the “cash leg” of crypto transactions from bank accounts and centralized stablecoins toward tokenized money market funds, particularly for treasurers and funds that are sensitive to counterparty risk and regulatory clarity.

- 01FOBXX multi-chain rollout↗

Each new chain deployment (Stellar, Polygon, Arbitrum, Aptos, Hong Kong) signals which L1/L2 ecosystems are winning institutional validation, making every announcement a proxy vote on chain viability.

- 02SEC ETF delay watch↗

Readers track each SEC postponement on XRP, Solana, and ETH-staking ETFs as a leading indicator of regulatory posture toward altcoin products from the most credentialed filer in the space.

- 03CEO institutional credibility signals↗

Jenny Johnson personally holding Uniswap and SushiSwap tokens, and expressing surprise at TradFi's ignorance of Bitcoin's scale, reads as insider confirmation that crypto adoption inside legacy finance is more advanced than publicly acknowledged.

- 04AI sector predictions and token moves

A $1.5T asset manager publishing bullish AI-agent research triggered 30–90% token surges, making FT's research notes a market-moving catalyst readers monitor for early positioning.

- 05Tokenized MMF as collateral rails↗

Headlines about FOBXX tokens nearing approval as derivatives collateral and the Binance institutional collateral program signal that tokenized Treasuries are becoming live DeFi infrastructure, not just a tokenization experiment.

- 06DeFi ecosystem investments and research

FT's participation in Ethena's $100M ENA raise and its published EigenLayer deep-dive position the firm as an active DeFi participant whose conviction reads are actionable signals for retail.

Onchain Ecosystem Collaborations: Avalanche, Kraken, and tZERO

Franklin Templeton’s tokenization agenda is reinforced by a network of collaborations with blockchain platforms and crypto‑native firms that specialize in trading, custody, and infrastructure. These partnerships are crucial because they extend Franklin’s reach beyond its own distribution channels and integrate its products into broader onchain ecosystems where liquidity and usage can grow organically. From a crypto perspective, they also signal which networks and service providers Franklin considers credible counterparties for institutional‑grade tokenization.

One major initiative is the Avalanche Payments Collective, a consortium launched on the Avalanche network that includes Franklin Templeton alongside VanEck, Anchorage Digital, Paxos, and other companies spanning stablecoins, settlement, treasury infrastructure, foreign exchange, custody, and card issuance. The Collective’s aim is to build a comprehensive payments and settlement stack on Avalanche, leveraging its scalability and subnetwork architecture to support institutional use cases. Franklin’s participation indicates that it sees value not only in issuing tokenized funds on Avalanche, but also in contributing to the design of the broader payments infrastructure that might use these funds as collateral or transactional media. For Avalanche, having a traditional manager of Franklin’s stature in the founding group enhances its credibility in the competitive RWA and payment‑rail landscape.

Perhaps the most consequential partnership from a capital‑markets standpoint is Franklin’s collaboration with Payward, the parent company of crypto exchange Kraken. The two firms announced a strategic program to “bring traditional financial products onchain and expand their utility across digital asset markets,” pairing Franklin’s asset management and tokenization expertise with Kraken’s trading, custody, and onchain infrastructure. Central to this collaboration is Kraken’s xStocks framework, which has processed over 30 billion dollars in volume and is designed to support tokenized equities and other real‑world assets. Franklin and Kraken plan to explore the launch of new actively managed, yield‑focused products onchain, as well as to provide direct access to institutional crypto liquidity via Kraken’s over‑the‑counter and prime brokerage services.

This partnership illustrates how tokenized funds could be integrated into exchange environments that already host spot crypto trading, derivatives, and staking. For example, a tokenized Treasury fund or credit strategy managed by Franklin could be listed and traded alongside bitcoin and ether on Kraken‑linked venues, with Kraken acting as the primary liquidity provider and custodian. Institutional clients could then allocate to these products within the same operational and risk framework they use for digital assets, but with the additional comfort of Franklin’s asset management pedigree and regulated fund structures. For DeFi builders, the collaboration also suggests potential future integrations between Kraken‑linked onchain products and smart‑contract protocols, especially if tokenized funds are issued in formats compatible with DeFi standards.

Franklin Templeton’s presence in the tZERO and Aptos ecosystem rounds out its network of onchain collaborations. tZERO, which positions itself as an institutional‑grade tokenization and trading platform, has integrated the Aptos blockchain as one of its key execution layers for real‑world assets. In its announcement, tZERO explicitly points to the presence of major tokenized funds from BlackRock and Franklin Templeton on Aptos—including Franklin’s roughly 400 million dollar OnChain U.S. Government Money Fund—as evidence that the chain is becoming a hub for institutional RWAs. By deploying BENJI on Aptos and aligning with tZERO’s infrastructure, Franklin gains access to a growing pipeline of tokenized asset issuance and secondary trading venues that cater to regulated investors while still leveraging public‑chain characteristics.

Taken together, these collaborations show that Franklin’s onchain strategy is not confined to a single ecosystem or counterparty. Instead, the firm is pursuing a multi‑platform approach, engaging with Avalanche for payments, Kraken for trading and distribution, and Aptos plus tZERO for tokenization infrastructure, among others. For crypto markets, this means that Franklin’s products are likely to appear in multiple environments—from DeFi‑adjacent infrastructure on Avalanche and Aptos to centralized exchange rails at Kraken—rather than being isolated in a proprietary walled garden. The result is a more interconnected RWA landscape in which tokenized funds and crypto‑native assets can circulate within the same liquidity networks.

Scrypt partners with Franklin Templeton to bring tokenized treasuries to Swiss-regulated infrastructure

FOBXX is a 1940 Act money-market fund with $813.5M net assets and a 3.54% 7-day effective yield, so SCRYPT is plugging regulated cash yield into the same stack it uses for crypto settlement. The useful test is operational: can a Swiss desk treat BENJI like collateral at 2 a.m. without breaking custody, whitelisting, or compliance controls? If yes, tokenized T-bills move from passive RWA TVL into repo, margin, and OTC settlement workflows.

Spot Crypto ETFs and Single‑Asset ETPs: Bitcoin and Solana

While Benji represents Franklin Templeton’s deepest integration with onchain infrastructure, the firm has also been active in developing exchange‑traded products that give traditional investors exposure to crypto assets through brokerage accounts. These vehicles follow the now‑familiar pattern of spot crypto ETFs and exchange‑traded products, but with some innovations specific to Franklin’s lineup and broader strategy. For many retail and institutional investors, these funds remain the most accessible way to gain regulated exposure to bitcoin or major altcoins without directly holding private keys.

The Franklin Bitcoin ETF, trading under the ticker EZBC, is a spot bitcoin exchange‑traded product offered as a series of the Franklin Templeton Digital Holdings Trust. The trust is a Delaware statutory trust formed in 2023, reflecting the relatively recent emergence of spot bitcoin ETFs in mainstream investment channels. EZBC is designed to reflect the performance of the price of bitcoin, but Franklin is explicit that the ETF is not a direct investment in bitcoin; rather, it is an exchange‑traded product that invests in bitcoin and holds it in custody on behalf of shareholders. Coinbase serves as the custodian, and the product is registered under the Securities Act of 1933, positioning it squarely within U.S. securities regulation. For investors, EZBC offers the operational familiarity of an ETF—tradable on exchanges, held in brokerage accounts, and subject to standard ETF disclosure requirements—while abstracting away the complexities of self‑custody, wallets, and private keys.

Franklin has extended this single‑asset ETF approach beyond bitcoin to Solana, a high‑throughput Layer 1 blockchain that has become a significant part of the crypto ecosystem. The Franklin Solana ETF, using the ticker SOEZ, seeks to reflect generally the performance of the price of Solana and to capture staking rewards by staking as much of the fund’s SOL holdings as practicable. The fund’s documentation notes that staking rewards, received in the form of additional SOL tokens, may be treated as income for fund purposes, thereby potentially enhancing the yield profile relative to a non‑staking exposure. As with EZBC, SOEZ is not framed as a direct investment in SOL, but rather as an exchange‑traded product that invests in SOL and is registered under the Securities Act of 1933, with Coinbase again serving as custodian. This structure gives investors access to Solana’s price and staking economics without requiring them to interact directly with Solana’s onchain staking mechanisms or validator infrastructure.

For a crypto audience, the existence of staking‑enabled ETFs like SOEZ raises important questions about centralization, protocol governance, and competition with native staking solutions. On the one hand, institutional investors gain an easy way to participate in Solana’s staking yields through a regulated product, potentially increasing total stake and network security. On the other hand, consolidating large amounts of stake under a small number of custodians and asset managers could concentrate voting power and influence over the network, especially if ETF sponsors or their delegates align with a few validators. These dynamics are not unique to Franklin, but its decision to include staking within the ETF wrapper signals that staking rewards are becoming a standard feature in institutional crypto offerings, rather than a niche DeFi activity.

Relative to holding crypto directly, these ETFs offer clear trade‑offs. Investors benefit from regulated structures, familiar tax reporting, and the ability to trade alongside other securities in the same accounts they use for equities and bonds. At the same time, they surrender direct control over the underlying assets, cannot easily use ETF shares in DeFi, and accept additional layers of management fees and operational risk associated with the ETF sponsor and custodian. For many institutions constrained by mandates or operational risk policies, ETF exposure may be the only viable path to bitcoin or Solana; for crypto‑native users, the more interesting impact is how these funds may drive demand for the underlying assets and how the associated holdings are managed in onchain environments.

FOBXX launched on Stellar via Benji — first US-registered tokenized money market fund

Franklin Templeton files for spot Bitcoin ETF (EZBC)

- 2024-02regulatory

Franklin Templeton files for spot Ethereum ETF

FOBXX expands to Polygon blockchain

Benji platform adds patent-pending intraday yield feature

- 2025-09regulatory

MAS grants approval for Franklin OnChain US Dollar Short-Term Money Market Fund in Singapore

Franklin Templeton acquires CoinFund liquid strategies spinoff and launches Franklin Crypto unit

FOBXX launches on Arbitrum, extending on-chain MMF to Ethereum Layer 2

Turning Dividends into Bitcoin: The Bitcoin DRIP ETFs

Franklin Templeton’s most novel ETF initiative to date is a pair of funds that automatically funnel equity dividends into bitcoin exposure, effectively transforming traditional cash flows into a systematic strategy for accumulating digital gold. These “Bitcoin DRIP” ETFs represent a hybrid of conventional dividend reinvestment plans and crypto allocation strategies, and they have generated significant attention as a possible template for future crypto‑linked income products.

The firm has filed with the U.S. Securities and Exchange Commission to launch two exchange‑traded funds: the Franklin US Equity Bitcoin DRIP Index ETF and the Franklin US Innovation Bitcoin DRIP Index ETF. According to filings and public coverage, the effective date for these funds could be as early as September 1, 2026, subject to regulatory approval. Both funds are designed around the concept of a dividend reinvestment plan (DRIP), a long‑standing mechanism where corporate dividends are automatically reinvested into additional shares of the same stock or fund. Franklin’s twist is to redirect those dividend flows into bitcoin‑linked instruments instead of more equity, creating what one analysis describes as an “automatic, low‑maintenance 5 percent bitcoin feed funded entirely by equity dividends.”

Structurally, each DRIP ETF maintains a baseline allocation of roughly 95 percent to U.S. large‑cap equities and 5 percent to bitcoin exposure. The Franklin US Equity Bitcoin DRIP Index ETF tracks the VettaFi US Large‑Cap 500 Bitcoin DRIP Index, which covers approximately 498 securities with market capitalizations ranging from about 7.5 billion to 4.9 trillion dollars, offering broad exposure to the U.S. large‑cap equity market. The Franklin US Innovation Bitcoin DRIP Index ETF, by contrast, tracks a VettaFi innovation‑focused variant concentrated on growth companies, presumably with heavier weights in sectors such as technology and healthcare. In both cases, the equity sleeve functions similarly to a traditional index ETF, while the bitcoin sleeve is built from dividends generated by those equities and held in bitcoin‑linked instruments.

The mechanics of the bitcoin allocation are carefully constrained. Rather than holding bitcoin directly in the ETF, the funds gain exposure via a mix of spot bitcoin exchange‑traded products, futures contracts, options, and, in some cases, a wholly owned subsidiary in the Cayman Islands that can hold bitcoin or bitcoin derivatives. Dividends generated by the underlying stock portfolios flow into this bitcoin sleeve rather than being paid out to investors or reinvested into equities, causing the bitcoin allocation to grow over time if not rebalanced. However, to manage risk, the index methodology includes quarterly rebalancing rules that trim bitcoin allocations above 5 percent back to 4.5 percent, and a hard cap that limits bitcoin exposure to no more than 20 percent of the portfolio between rebalancing periods. These constraints aim to provide a disciplined exposure path: investors gradually accumulate bitcoin from dividends but are insulated from excessive concentration if bitcoin appreciates sharply.

For different types of investors, these DRIP ETFs can fill distinct roles. Income‑oriented equity holders who are curious about bitcoin but reluctant to allocate principal can use the funds to convert a portion of their dividend income into bitcoin exposure without changing their core equity holdings. Growth investors may view the innovation‑focused DRIP ETF as a way to pair high‑beta equities with a structurally increasing bitcoin sleeve, effectively betting on both technological equities and digital gold as secular beneficiaries of macro and technological change. Institutions subject to allocation caps on alternative assets could potentially treat the bitcoin component as part of an equity strategy, though this would depend on regulatory and internal governance classifications. In each case, the product design lowers the behavioral barrier to bitcoin exposure by automating allocation and linking it to familiar dividend flows.

From a market structure perspective, the Bitcoin DRIP ETFs continue a pattern in which Franklin Templeton uses conventional wrappers to smuggle crypto exposure into mainstream portfolios. Just as BENJI embeds tokenization and public blockchains into a regulated money market fund, the DRIP ETFs embed bitcoin accumulation into broad equity index strategies via dividend routing. If adopted at scale, such products could drive steady, programmatic demand for bitcoin that is somewhat decoupled from short‑term sentiment, as dividends are paid regardless of crypto market cycles. They also illustrate how the ETF ecosystem can be used to construct increasingly sophisticated cross‑asset strategies that treat bitcoin not as a stand‑alone speculative asset but as a component of diversified portfolio construction.

Franklin Templeton in the RWA and Tokenization Race

Franklin Templeton’s initiatives place it squarely in the vanguard of the real‑world asset tokenization race, where large asset managers compete to bring traditional securities onchain in scalable, regulated formats. In this landscape, Franklin competes and collaborates with peers like BlackRock, Fidelity, and Janus Henderson, all of which have launched or are exploring tokenized money market funds and treasury strategies. The headline numbers illustrate the stakes: social and industry commentary suggests that money market funds tokenized by leading asset managers—including Franklin’s BENJI, BlackRock’s BUIDL, and vehicles from others—have collectively surpassed 15 billion dollars in value. At the same time, broader estimates of onchain RWAs, including treasuries and commodities, have reached tens of billions of dollars, with the latest spikes driven heavily by institutional tokenized U.S. Treasuries issued on Ethereum and other major chains.

Within this environment, Franklin’s BENJI fund is notable not only for being first but also for its breadth of deployment. BlackRock’s BUIDL tokenized fund, for example, has quickly grown on Ethereum and other chains and has become a reference point for institutional treasuries onchain. Yet Franklin’s earlier moves on Stellar and its multi‑chain presence on Avalanche, Polygon, Arbitrum, and Aptos give it a distinct footprint that emphasizes interoperability and experimentation with varied blockchain architectures. tZERO’s decision to integrate Aptos, citing the presence of Franklin’s roughly 400 million dollar money fund alongside BlackRock’s 500 million dollar product, underscores how multiple asset managers can coexist and even reinforce each other’s case for RWAs on a given chain. In effect, Franklin and BlackRock together create a critical mass of tokenized funds that attract infrastructure providers, trading platforms, and institutional users, making each product more valuable by virtue of the ecosystem forming around it.

A simplified comparison highlights the different emphases of major tokenized treasury funds, based on public information:

| Aspect | Franklin OnChain U.S. Government Money Fund (FOBXX / BENJI) | BlackRock BUIDL (tokenized fund) |

|---|---|---|

| Sponsor | Franklin Templeton, via Franklin Fixed Income and Benji Platform | BlackRock, via its digital asset and cash management units |

| Asset type | U.S. government securities, cash, and repos, at least 99.5% of assets | Tokenized money market or short‑term U.S. Treasuries as reported by market data |

| Registration | U.S.‑registered mutual fund using public blockchain as system of record | Tokenized fund structure under BlackRock’s regulatory regime |

| Blockchain presence | Stellar, Avalanche, Arbitrum, Polygon, Aptos | Ethereum and other public chains as reported in RWA coverage |

The table is necessarily high‑level, but it shows how Franklin emphasizes public‑chain record‑keeping and multi‑chain presence, while BlackRock’s BUIDL has so far focused on Ethereum‑based issuance and scaling via large inflows. For crypto markets, the key takeaway is that multiple blue‑chip managers are validating the same underlying thesis: that tokenized treasuries and money market funds can function as a new type of base asset in onchain finance, analogous to the role of T‑bills and repos in traditional markets.

Franklin’s role in this race is reinforced by its continuous expansion of the Benji Platform and related tokenization capabilities. The introduction of intraday yield and white‑label tokenization services suggests that Franklin aims not merely to tokenize its own funds but also to enable others to bring their securities onto public blockchains using its infrastructure. The firm’s partnership with MoonPay, for example, positions Benji as a component of a larger stablecoin‑to‑yield ecosystem, while collaborations with Kraken and tZERO target trading and distribution across both centralized and decentralized venues. For DeFi protocols and RWA platforms, Franklin’s presence offers both an opportunity and a challenge: integrating BENJI can attract institutional liquidity and regulatory credibility, but also requires compliance with the fund’s investor eligibility and transfer restrictions.

Cap App Partners with Franklin Templeton to Accept BENJI Deposits

BENJI moving from a parked tokenized Treasury position into Cap deposit collateral is the kind of plumbing RWAs need: Franklin gets distribution, Cap gets a cleaner funding asset than reflexive crypto collateral. BUIDL’s rise showed tokenized funds accrue network effects once venues treat them as usable balance-sheet inventory. Cap’s spread is the fragile part: BENJI holders start with 1940 Act money fund exposure, then layer on Cap’s underwriting, whitelist rules, and redemption timing.

The SEC has issued multiple consecutive delays on Franklin Templeton's XRP ETF, Solana ETF, and ETH-staking ETF applications, keeping the firm's most commercially significant pending products in limbo with no committed approval timeline.

FOBXX runs simultaneously on Stellar, Polygon, Arbitrum, Aptos, and other networks; each additional chain deployment multiplies smart-contract surface area and cross-chain bridge dependencies for a fund holding US government securities.

Franklin Templeton retains full custodial and administrative control over FOBXX share records; the blockchain layer is a settlement rail, not a governance mechanism, meaning the fund's operation is as centralized as any traditional money market fund.

FOBXX holds short-term US Treasuries and is structured as a money market fund; liquidity risk is low under normal conditions, though redemption pressure during a broad risk-off event could stress on-chain settlement throughput.

Franklin Templeton's strategic investments in Ethena (ENA token sale) and its acquisition of CoinFund's liquid strategies arm introduce direct exposure to DeFi protocol performance and the credit quality of synthetic stablecoin collateral.

CEO Jenny Johnson's personal holdings of Uniswap and SushiSwap tokens and the firm's aggressive multi-chain and AI research posture have so far reinforced rather than damaged institutional credibility, but a high-profile protocol failure in an FT-backed ecosystem would create outsized reputational exposure.

Risks, Regulation, and Business Model Tensions

Despite the momentum around tokenization and crypto‑linked ETFs, Franklin Templeton is explicit about the risks associated with its digital asset initiatives. The firm’s digital assets disclosures caution that competitive pressures may inhibit the ability of its funds to gather substantial assets or achieve commercial viability, underscoring that early tokenization experiments may not automatically translate into profitable, scalable businesses. They also emphasize that all investments involve risk, including loss of principal, and highlight that funds like the OnChain U.S. Government Money Fund, while investing in U.S. government obligations, are neither insured nor guaranteed by the U.S. government. These statements are particularly relevant in the context of tokenized treasuries, where some investors may mistakenly infer a stablecoin‑like guarantee from the presence of government securities in the underlying portfolio.

Operational and technology risks are another focal point of Franklin’s risk messaging. The firm notes that there are specific risks associated with the issuance, redemption, transfer, custody, and record‑keeping of shares whose ownership is maintained and recorded primarily on a blockchain. Potential issues include network outages, smart contract vulnerabilities, key management failures, and incompatibilities between blockchain records and traditional legal documentation of fund ownership. While Franklin has designed its systems to mitigate these risks, and maintains conventional oversight and custodial arrangements where appropriate, the residual risk cannot be entirely eliminated as long as public blockchains remain the core infrastructure. For institutions considering onchain exposure via Franklin products, these risk disclosures provide a roadmap of the points in the operational chain that require careful due diligence.

There are also deeper tensions between tokenization and legacy business models. As Jenny Johnson has noted, blockchain and digital assets threaten many of the most profitable functions in traditional finance, including custody, settlement, and payment processing, which often rely on intermediaries extracting fees from inefficient, batch‑settled systems. By contrast, tokenization promises to streamline or even disintermediate some of these functions through programmable smart contracts and 24/7 settlement, potentially compressing margins for intermediaries who fail to adapt. Franklin’s strategy of embracing onchain funds and digital asset partnerships can thus be seen as a hedge against this disruption, positioning the firm to capture value in a world where tokenized securities and DeFi‑style protocols play a larger role in asset management and capital markets.

Regulatory uncertainty remains a structural challenge. While products like FOBXX, EZBC, SOEZ, and the proposed Bitcoin DRIP ETFs operate within U.S. securities law and related frameworks, the broader treatment of tokenized securities, onchain money funds, and crypto‑linked derivatives is still evolving. Questions persist about cross‑border distribution, secondary trading on decentralized venues, and the application of investor‑protection rules to token transfers executed via smart contracts. Franklin’s approach—anchoring products in existing mutual fund and ETF regulations while experimenting with blockchain as the record‑keeping and settlement layer—minimizes some of these risks but does not eliminate them. For DeFi protocols seeking to integrate BENJI or other Franklin products, the regulatory line between compliant tokenization and unregistered securities activity remains a central concern.

Finally, Franklin Templeton faces competitive and reputational risks as it navigates the digital asset landscape. Its disclosures acknowledge that other asset managers and fintech firms are entering the tokenization and crypto ETF space, potentially eroding Franklin’s first‑mover advantages. At the same time, aligning too closely with crypto markets exposes the firm to volatility, regulatory controversies, and technology failures that could impact its broader brand as a conservative, long‑term asset manager. Balancing innovation with prudence is thus an ongoing challenge: Franklin must move quickly enough to remain a leader in tokenization and crypto‑linked products, while maintaining the risk controls and governance standards demanded by its institutional clients and regulators.

Conclusion

For the crypto and DeFi community, Franklin Templeton has evolved from a conventional mutual fund sponsor into a key architect of onchain real‑world asset markets and crypto‑linked investment products. Through the Benji Platform and the Franklin OnChain U.S. Government Money Fund, the firm has demonstrated that a U.S.‑registered mutual fund can use public blockchains as its system of record, circulate as tokens across multiple chains, and function as yield‑bearing collateral in digital asset ecosystems. Its innovations around intraday yield, multi‑chain deployment, and institutional distribution via partners like MoonPay, DigiFT, Kraken, and tZERO show how tokenized funds can be woven into both traditional and crypto‑native workflows.

Parallel to this onchain experimentation, Franklin has launched and proposed a range of ETFs and exchange‑traded products that bring crypto exposure into mainstream portfolios. The Franklin Bitcoin ETF (EZBC) and Franklin Solana ETF (SOEZ) give investors regulated, custodied access to bitcoin and Solana, with SOEZ adding staking rewards into the ETF wrapper. The proposed Bitcoin DRIP ETFs take this one step further by automatically channeling corporate dividends from large‑cap equity portfolios into bitcoin exposure, offering a novel mechanism for long‑term bitcoin accumulation funded by traditional income streams. Combined, these products reveal a consistent design philosophy: use familiar wrappers—mutual funds, ETFs, and money market funds—to introduce blockchain technology and digital assets into the heart of institutional allocation and capital markets infrastructure.

Franklin Templeton’s activities also highlight both the promise and the limits of tokenization. On the positive side, tokenized funds like BENJI can deliver 24/7 settlement, programmable yield, and composable collateral, while remaining anchored in regulated portfolios of government securities. Partnerships across Avalanche, Aptos, Kraken, MoonPay, and tZERO illustrate that tokenized RWAs can plug into diverse ecosystems, from payments collectives to centralized exchanges and institutional tokenization platforms. On the cautionary side, Franklin’s own risk disclosures underscore that tokenization introduces new operational, technology, and regulatory risks, and that competitive pressures may challenge the commercial viability of some digital asset funds.

In the broader RWA race, Franklin Templeton stands alongside BlackRock and other major managers as a principal driver of tokenized treasury and money market adoption. Its early move with BENJI, combined with its research and partnerships, has helped legitimize tokenization as a core pillar of future financial infrastructure rather than a passing trend. For crypto builders, Franklin represents both an opportunity and a constraint: its products can bring deep pools of regulated capital onchain, but they also come with the compliance requirements and centralized governance that characterize traditional finance. How DeFi protocols, onchain infrastructure providers, and competing asset managers respond to this blend of innovation and conservatism will shape the next phase of the crypto–TradFi convergence.

Outlook

Looking ahead, Franklin Templeton is likely to continue expanding its footprint across both tokenized funds and crypto‑linked ETFs, deepening its integration with multiple public blockchains and institutional distribution partners. Growth in tokenized treasuries and money market funds—where BENJI already plays a leading role alongside BlackRock’s BUIDL and others—should further entrench tokenized RWAs as a core component of onchain liquidity and collateral markets. As intraday yield, programmable income distribution, and multi‑chain issuance mature, the Benji Platform may evolve into a broader infrastructure layer that other issuers and banks use to bring their own securities onchain.

Regulatory developments and competitive dynamics will heavily influence the pace and shape of this evolution. Approvals or rejections of products like the Bitcoin DRIP ETFs will signal regulators’ appetite for more complex cross‑asset crypto strategies embedded in traditional wrappers. Meanwhile, the success of partnerships with Kraken, MoonPay, Avalanche, Aptos, and tZERO will determine how deeply Franklin’s tokenized funds permeate trading, settlement, and payment flows in both centralized and decentralized contexts. For crypto participants, Franklin Templeton is likely to remain a bellwether: its decisions on where and how to deploy tokenized products will be watched closely as an indicator of institutional confidence in specific chains, protocols, and digital asset structures, and as a guide to how the next generation of onchain capital markets might be built.

Latest Franklin Templeton news

Sources

- https://coinfomania.com/a-bold-step-for-etfs-franklin-templeton-files-for-bitcoin-linked-funds/

- https://bitcoinmagazine.com/news/franklin-templeton-files-two-etfs-bitcoin

- https://www.franklintempleton.com/investments/asset-class/digital-assets

- https://www.franklintempleton.com/investments/options/exchange-traded-funds/products/39639/SINGLCLASS/franklin-bitcoin-etf/EZBC

- https://digitalassets.franklintempleton.com/benji/

- https://www.franklintempleton.com/investments/options/exchange-traded-funds/products/47315/SINGLCLASS/franklin-solana-etf/SOEZ

- https://x.com/avax/status/2067593945241223376

- https://blog.kraken.com/news/payward-and-franklin-templeton-tokenized-assets

- https://coinmarketcap.com/academy/article/wall-street-titan-franklin-templeton-adds-aptos-to-digital-fund-network

- https://www.franklintempleton.com/press-releases/news-room/2026/franklin-templeton-agrees-to-acquire-liquid-strategies-from-coinfund-spinoff-launches-franklin-crypto

- https://www.franklintempleton.com/press-releases/news-room/2026/franklin-templeton-and-moonpay-partner-to-expand-institutional-access-to-tokenized-money-market-funds

- https://www.franklintempleton.com/investments/options/money-market-funds/products/29386/SINGLCLASS/franklin-on-chain-u-s-government-money-fund/FOBXX

- https://www.franklintempletonme.com/press-releases/news-room/2025/franklin-templeton-launches-patent-pending-intraday-yield-feature-on-benji-technology-platform

- https://x.com/bouncebit/status/2060509334128164901

- https://www.youtube.com/watch?v=yN-rSqe5eoM

- https://www.franklintempleton.com/press-releases/news-room/2026/franklin-templeton-stellar-development-foundation-mark-five-years-of-benji-the-first-u.s.-registered-tokenized-money-market-fund

- https://www.instagram.com/p/DYkW6mVAaBx/

- https://www.franklintempleton.com/about-us/franklin-templeton-digital-assets

- https://tzero.com/news/tzero-expands-institutional-grade-tokenization-infrastructure-adding-aptos-as-a-key-ecosystem

- https://www.investmentnews.com/etfs/franklin-templeton-touts-first-clo-etf/266881

Community notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…