In‑depth explainer on tokenization for crypto markets: how real‑world assets move onchain, tokenomics design, stablecoins, SEC and Fed views, leading RWA case studies (Ondo, Maple, Centrifuge), and the risks and outlook for a multi‑trillion‑dollar tokenized future.

+26 sources across the wider coverage universe

Former SEC Chief Economist backs a16z-backed safe harbor, arguing tokenized securities on DeFi can cut costs, enable 24/7 markets, and boost transparency despite regulatory tradeoffs2026-04

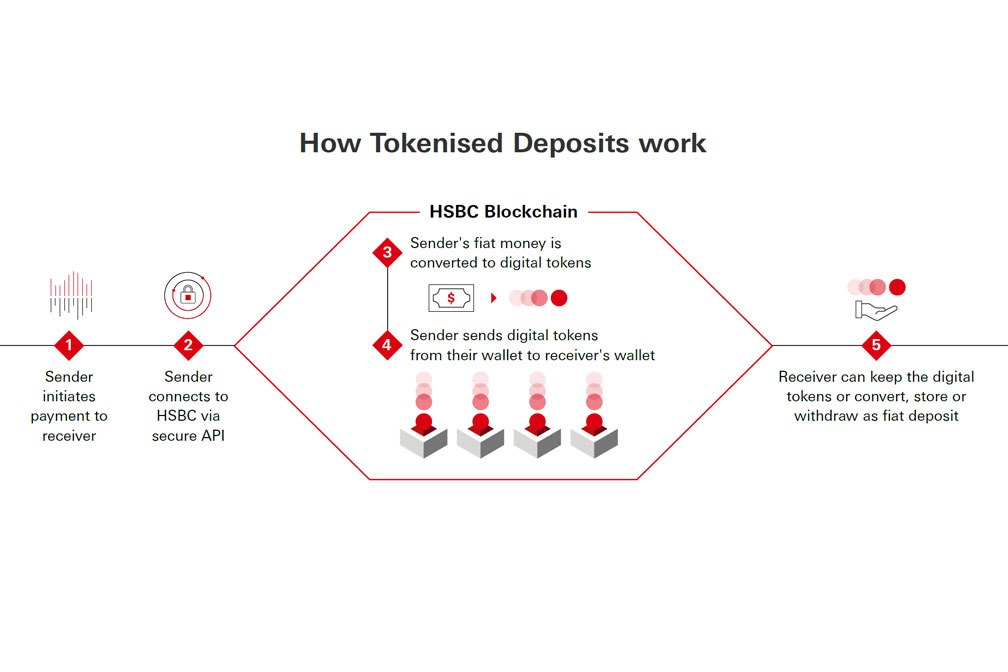

Former SEC Chief Economist backs a16z-backed safe harbor, arguing tokenized securities on DeFi can cut costs, enable 24/7 markets, and boost transparency despite regulatory tradeoffs2026-04 HSBC completes tokenised deposit pilot on Canton Network, showcasing interoperable issuance, transfer, and atomic settlement for regulated institutions2026-04

HSBC completes tokenised deposit pilot on Canton Network, showcasing interoperable issuance, transfer, and atomic settlement for regulated institutions2026-04 HSBC unfurls tokenized deposit service in United States waters, linking global liquidity across key financial markets.2026-04

HSBC unfurls tokenized deposit service in United States waters, linking global liquidity across key financial markets.2026-04 Benchmark says just 0.01% of NYSE’s $44T market could significantly scale Securitize, highlighting massive upside for tokenized assets as institutional adoption grows2026-04

Benchmark says just 0.01% of NYSE’s $44T market could significantly scale Securitize, highlighting massive upside for tokenized assets as institutional adoption grows2026-04 Morgan Stanley eyes tokenization and crypto tax strategies beyond Bitcoin, as exec Amy Oldenburg signals expansion into tokenized funds and digital asset services2026-04

Morgan Stanley eyes tokenization and crypto tax strategies beyond Bitcoin, as exec Amy Oldenburg signals expansion into tokenized funds and digital asset services2026-04 Continental Stock Transfer & Trust taps Securitize as preferred tokenization provider for issuer clients2026-06

Continental Stock Transfer & Trust taps Securitize as preferred tokenization provider for issuer clients2026-06

Tokenization: Bridging Real‑World Assets and Crypto Markets

Turning real‑world assets into blockchain tokens is emerging as one of the most consequential shifts at the intersection of traditional finance and crypto. In its simplest form, tokenization creates a cryptographic representation of ownership or economic rights in an underlying asset and allows those rights to move, settle, and compose on blockchain rails. This is already reshaping how treasuries, private credit, real estate, equities, and even sports rights are issued and traded, with banks, exchanges, and DeFi protocols all building toward a tokenized market structure. Citi estimates that tokenized securities could grow from low double‑digit billions of dollars today to around 5.5 trillion dollars by 2030 in its base case, with bullish scenarios reaching over 8 trillion dollars, underscoring the scale of the structural change underway. At the same time, regulators such as the Federal Reserve and the SEC are warning that tokenization may alter redemption dynamics, liquidity, and risk transmission in ways that can both strengthen and destabilize the financial system, depending on how designs and safeguards evolve. For crypto market participants, tokenization is no longer a fringe experiment: it is increasingly the mechanism by which real‑world yield, institutional capital, and traditional market structure are being brought onchain.

What Tokenization Means in a Crypto Context

In a broad technological sense, tokenization is the process of creating a digital proxy for something of value so that it can be stored, transferred, or processed more safely or efficiently. In payments and data security, this has long referred to replacing sensitive information such as card numbers with non‑sensitive tokens to reduce fraud and compliance overhead. In crypto and Web3, however, the term has come to mean something more ambitious: issuing blockchain‑based tokens that represent legally or economically enforceable rights to real‑world assets or cash flows, and enabling those tokens to trade, settle, and interact with smart contracts across networks. The key difference is that tokenization in this onchain sense is not just a data protection technique but a full stack re‑architecture of how ownership, settlement, and market infrastructure are implemented.

Asset tokenization can be thought of as the onchain cousin of securitization and fund structuring. Instead of bundling loans into a traditional security and listing it on a legacy exchange, a sponsor might place the underlying assets in a legal wrapper such as a trust or special purpose vehicle (SPV) and then issue blockchain tokens that represent claims on that wrapper. Those tokens can mirror equity, debt, fund interests, or deposit‑like claims, depending on the structure, and can be designed to pay yield, embed governance rights, or simply track price exposure. Compared with a spreadsheet‑based or database‑based ledger, the blockchain ledger adds programmability and composability: tokens can be integrated into lending protocols, automated strategies, and stablecoin‑settled trading venues without building new bilateral integrations for each counterpart.

Real‑world asset tokenization (RWA) is the term of art for these designs when they are backed by offchain instruments such as U.S. Treasuries, private credit, real estate, commodities, or equity securities. Stablecoins are perhaps the earliest and most widely adopted example of tokenization at scale, representing tokenized claims on bank deposits or money market instruments, though the market now extends to tokenized funds, credit pools, and even tokenized stocks and exchange‑traded funds (ETFs). Protocols such as Ondo Finance have launched tokenized Treasury products and, more recently, tokenized exposures to U.S. stocks and ETFs that trade on regulated digital asset venues, illustrating how tokenization is leaching into the core of capital markets rather than remaining a niche crypto product. Maple Finance, Centrifuge, and other credit‑focused platforms use tokenization to package private credit and other yield‑bearing assets for onchain investors, emphasizing that “the yield layer underneath has to be real” as more capital moves onchain.

Just as important as the asset side is the regulatory and systemic dimension. Because tokenized instruments can share many features of traditional securities or bank liabilities, agencies such as the SEC and the Federal Reserve are scrutinizing how tokenization interacts with existing investor protections, liquidity frameworks, and prudential rules. The SEC has reportedly explored an “innovation exemption” that could allow third parties to create tokenized stock claims without issuer permission, raising questions about synthetic exposures, market integrity, and contagion between DeFi and public equity markets. In parallel, Federal Reserve officials have warned that tokenized shares in funds or deposit‑like liabilities could alter redemption incentives and run dynamics, potentially amplifying or dampening financial instability depending on design choices. For crypto builders and investors, understanding tokenization is therefore not only a matter of new product design but also of regulatory navigation and macro‑financial awareness.

Continental Stock Transfer & Trust taps Securitize as preferred tokenization provider for issuer clients

Securitize says Continental Stock Transfer & Trust has selected it as preferred tokenization provider, giving the transfer agent's issuer base a path into blockchain-based securities issuance. Continental says it serves 1,800 issuers, 220 global clients, and 2.8M shareholders while handling 60% of U.S. IPOs, so this is another chunk of stock-transfer plumbing moving toward tokenized cap tables. The release is thin on rollout mechanics, but the signal is clear: tokenized securities are being pushed through incumbent transfer-agent channels, not just crypto-native wrappers.

Readers consistently chose the sovereign and central-bank angle over startup deals, revealing that the defining question about tokenization is not whether the technology works but whether monetary authorities will absorb or resist it — governments and regulators occupy 6 of the top 10 clicked stories.↗

How Asset Tokenization Works End‑to‑End

Onboarding Real‑World Assets and Legal Structuring

The starting point for any tokenization project is asset sourcing and legal structuring. McKinsey divides this into a first step of identifying the asset to be tokenized and determining how it will be treated under applicable regulatory regimes, including whether it is a security or a commodity and which jurisdiction’s rules apply. Tokenizing a money market fund, for example, raises different legal questions than tokenizing a carbon credit, a real estate asset, or a private loan portfolio, because the underlying rights, investor protections, and disclosure requirements differ. The sponsor must select an appropriate legal wrapper, which might be a fund, an SPV, a trust, or a direct issuance structure, and ensure that the token is clearly defined as representing a specific claim on that wrapper in offering documents and contracts.

A recent systems‑level taxonomy of RWA tokenization distinguishes between different ways that tokens can be linked to offchain assets, such as direct legal ownership, contractual claims, or synthetic references using derivatives. In a “full title” model, the token might represent a direct pro‑rata ownership interest in the underlying asset held by a custodian on behalf of token holders. In other structures, the token represents a claim on the equity or debt of an issuing entity that itself owns the asset, similar to fund shares, which may offer more flexibility but can add layers of counterparty and governance risk. Regulatory compliance often requires that token holders be restricted to certain investor categories (for example, accredited or institutional investors) or that holding periods and transferability be constrained, which has direct implications for token design and protocol integration.

The need to translate legal rights into programmable logic is one of the core complexities of tokenization. Contracts must spell out how and when tokens can be redeemed for underlying assets or cash proceeds, how defaults and restructuring are handled, and how obligations toward regulators, auditors, and tax authorities will be met. At the same time, onchain smart contracts must encode issuance limits, transfer restrictions, and role‑based permissions that reflect those offchain obligations. If this mapping is incomplete or ambiguous, token holders may mis‑price risk or assume enforceability that does not exist, which is one of the concerns regulators have raised in speeches and consultation papers.

Digital Issuance, Token Standards, and Custody

Once the legal and asset‑side structure is in place, the next stage is digital issuance and custody. McKinsey describes this as moving any physical counterpart of the asset into a secure, neutral facility or into the custody of a trusted intermediary, and then issuing a digital token on a chosen blockchain network that represents the asset. This stage involves selecting token standards (such as fungible ERC‑20‑like formats for funds and credit pools or non‑fungible ERC‑721‑like formats for specific assets), configuring token metadata, and setting up onchain controls for minting, burning, and freezing where necessary for compliance. Issuers must also choose between public, permissionless blockchains; permissioned or consortium chains; or enterprise ledgers operated by market infrastructures, each of which offers trade‑offs in terms of openness, scalability, regulatory comfort, and composability with DeFi.

Custody in tokenization has a dual character: the underlying asset is usually held by a regulated custodian, trustee, or depository, while the token itself may be held either in self‑custody wallets or by digital asset custodians and broker‑dealers on behalf of clients. Market infrastructures such as Clearstream and DTCC are experimenting with expanding their existing custody services to include tokenized versions of securities held in their depositories, which can then be traded or settled on blockchain rails while relying on traditional custody and settlement frameworks. For example, Clearstream has partnered with Ondo Finance and 360X, a digital asset venue backed by Deutsche Börse, to make tokenized stocks and ETFs available on a regulated trading venue while maintaining underlying custody within established systems. DTCC, in partnership with the Stellar Development Foundation, plans to create tokenized versions of assets held in its central depository, effectively giving existing assets a parallel life in tokenized form without abandoning the current post‑trade infrastructure.

The emergence of “asset tokenization studios” and platforms reflects a push to compress the issuance process. Some networks are building open‑source, enterprise‑oriented tooling that aims to let institutions launch compliant tokenized assets, including RWAs and stablecoins, in minutes rather than months by automating much of the smart contract deployment, permissioning logic, and integration with KYC/AML systems. These issuance layers sit alongside specialized RWA platforms like Centrifuge, which Coinbase has selected as a preferred tokenization infrastructure partner as it brings private credit and fixed income exposures onto its Base layer‑2 network. The result is a technology stack where legal structuring, issuance contracts, and custody integration increasingly resemble modular, reusable components rather than bespoke projects.

Distribution, Settlement, and Secondary Trading

After issuance, token distribution and secondary market trading determine whether a tokenized asset achieves meaningful liquidity and adoption. McKinsey’s third step emphasizes that investors need a digital wallet to receive and hold the token, and that a secondary trading venue may be built to facilitate transfers. In practice, tokenized assets can trade across a spectrum of venues, from fully regulated exchanges and alternative trading systems (ATSs) to permissioned platforms, centralized crypto exchanges, and decentralized exchanges (DEXs) and automated market makers (AMMs). Each venue model carries different implications for investor protection, transparency, and regulatory oversight, which has been a focal point of policy debate as tokenized stocks and funds gain traction.

One of the most frequently cited benefits of tokenization is instant or near‑instant settlement. The New York Stock Exchange has announced a project to build a platform for trading tokenized securities that, subject to regulatory approvals, would enable 24/7 trading and instant settlement using blockchain infrastructure, with stablecoins as a funding currency. Similarly, Ondo’s tokenized U.S. stocks and ETFs, available on the 360X venue, are designed to settle onchain within minutes, reducing counterparty risk and capital trapped in long settlement cycles. These models promise to replace the traditional T+2 or T+1 settlement cycles and complex clearing and netting processes with delivery‑versus‑payment (DvP) onchain, where the transfer of tokens and stablecoins occurs atomically in a single transaction.

Stablecoins and tokenized cash instruments are therefore integral to distribution and trading. Payment giants and large banks are experimenting with deposit tokens and onchain stablecoin payment routes that can be used as settlement assets for tokenized securities, credit, and other RWAs, helping to close the loop between the traditional banking system and onchain markets. Coinbase CEO Brian Armstrong has argued that RWA tokenization, 24/7 global trading, and stablecoin payments are among the core upgrades still needed for the financial system, positioning tokenized asset rails and fiat‑linked tokens as complementary components of a modern market stack. However, the degree to which these benefits are realized depends heavily on how interoperable tokenized assets are across venues, how market makers provide liquidity, and whether regulators permit direct retail access or constrain tokenized securities to institutional channels.

Oracles, Data Reconciliation, and Compliance

The final phase in McKinsey’s four‑step framework is asset servicing and data reconciliation, which persists throughout the life of a tokenized asset. This includes regulatory, tax, and accounting reporting; corporate actions such as interest payments, redemptions, or votes; and continuous reconciliation between onchain token balances and offchain records at custodians and registrars. Because tokenization explicitly links a blockchain representation to an offchain reality, this reconciliation layer is critical: if the mapping breaks down, a token may no longer reliably represent the asset it claims to track, undermining market trust.

Oracles and verification systems are central to this linkage. Technical guides such as Chainlink’s RWA tutorials illustrate how smart contracts can use oracle networks to fetch offchain data, such as portfolio balances or price feeds, and then decide whether to mint, redeem, or adjust token supplies based on that information. In a tokenized credit pool, for instance, an oracle might be used to update the net asset value (NAV) and trigger yield distributions; in a tokenized stock product, it might verify that a custodian continues to hold sufficient underlying shares to back outstanding tokens. Emerging “audit‑proof chain” designs aim to go further by publishing cryptographic attestations, proofs of reserve, or zero‑knowledge proofs that allow investors and regulators to verify that onchain supplies are fully backed while preserving confidentiality over granular holdings and counterparties.

Compliance and identity are the other half of this servicing layer. Many RWA tokens are issued under exemptions or regimes that require know‑your‑customer (KYC) checks, limits on which investors can hold the tokens, and obligations to suspend or reverse transfers under certain conditions. These requirements are often implemented through whitelists, role‑based permissions, and transfer‑restriction logic in the token smart contract, sometimes coupled with offchain KYC providers and onchain attestation standards. A growing set of privacy‑preserving identity and data‑sharing tools, including zero‑knowledge databases and selective‑disclosure credential systems, is being developed to allow tokenized markets to meet regulatory requirements while keeping commercially sensitive data concealed from competitors and the public. Industry voices have highlighted that as tokenization moves from experiment to market infrastructure, the bottleneck is shifting from issuance toward verification and privacy: tokenized assets must be verifiably backed and compliant without replicating the opacity and data silos of legacy finance.

Tokenization, Tokenomics, and Market Design

Economic Rights Embedded in Tokens

Tokenomics, broadly understood, refers to the economic design of a token: its supply schedule, demand drivers, distribution, and the rights or utilities it confers on holders. In the context of tokenization, tokenomics is not only about speculative crypto‑native tokens but about how economic rights attached to RWAs are sliced, packaged, and distributed across token holders. A tokenized Treasury fund, for example, typically entitles holders to pro‑rata exposure to the underlying short‑term government bonds and to periodic yield distributions in stablecoins or reinvested shares. A tokenized private credit pool might confer a combination of senior and junior tranches, each with different risk‑return profiles and loss‑absorbing capacities, encoded through separate token classes. Governance tokens in RWA protocols can layer additional rights, such as voting on underwriting standards, fee levels, or reserve policies, complicating the tokenomic picture.

Empirical work on tokenomics in crypto markets has shown that token functions such as medium‑of‑exchange, utility, governance, and claims on cash flows correlate with price behavior and adoption. Tokenized RWAs introduce new function types, such as “claim on offchain collateral,” “claim on fund NAV,” or “deposit receipt,” which must be reconciled with securities and banking law as well as with DeFi norms. The taxonomy of RWA tokenization suggests that distinguishing between “fund tokens,” “note tokens,” and “claim tokens” is crucial, because they embed different rights to redemption, recourse, and seniority relative to other creditors. From a market design perspective, clear tokenomics reduces legal uncertainty and mispricing, while ambiguous or convoluted structures risk obscuring who ultimately bears default or liquidity risk.

One central tension is between fungibility and specificity. Highly fungible tokens, similar to ERC‑20s, facilitate deep pools of liquidity and integration with DeFi protocols but may abstract away important information about the underlying assets, such as concentration risk or idiosyncratic covenants. More granular, non‑fungible or semi‑fungible tokens can better reflect specific claims, such as individual real estate parcels or loans, but fragment liquidity and complicate pricing. Designers therefore face choices about how much heterogeneity to absorb into the token structure and how much to manage offchain through documentation and disclosure.

Liquidity, Pricing, and Market Microstructure

Tokenized assets promise to transform market microstructure by enabling around‑the‑clock trading, fractional ownership, and near‑instant settlement, but these benefits are not automatic. Lessons from ETFs are often invoked as an analogy: ETFs turned mutual fund exposures into highly liquid, intraday‑traded instruments and now represent tens of trillions of dollars globally, and some commentators argue tokenization could echo that boom by making a wide range of assets tradeable and composable in digital form. However, ETF liquidity depends heavily on authorized participants, arbitrage mechanisms, and robust underlying markets; tokenized assets must develop comparable market‑making and arbitrage ecosystems to avoid large discounts or premiums.

The table below summarizes some structural differences between traditional ETFs and tokenized fund‑like products.

| Feature | Traditional ETF | Tokenized Fund / RWA Product |

|---|---|---|

| Trading Hours | Exchange hours only | Potentially 24/7 on blockchain venues |

| Settlement | Typically T+1 or T+2 via clearinghouses | Near‑instant onchain DvP settlement |

| Access | Broader in public markets but often geographically limited | Potentially global, but often restricted via onchain whitelists |

| Composability | Limited programmability, mainly via brokerage infrastructure | Programmable, composable with DeFi protocols and smart contracts |

| Collateral Use | Margin collateral in traditional finance | Onchain collateral for lending, derivatives, structured products |

While tokenization can theoretically enhance liquidity, it can also create liquidity illusions if the underlying assets are themselves illiquid. Private credit, real estate, or sports revenue shares may not be easily sold or valued offchain, even if the corresponding tokens trade frequently onchain, leading to episodes where onchain prices decouple from realizable values. This risk is magnified when DeFi protocols allow leveraged positions against tokenized assets, because forced liquidations or oracle failures can propagate volatility between the tokenized layer and the offchain asset pool. The SEC’s concern about synthetic or wrapped tokenization without issuer consent partly reflects this dynamic: tokens created by third parties on the back of custodial holdings can trade and be leveraged independently of any direct relationship with the underlying issuer, potentially amplifying dislocations.

Price discovery for tokenized assets also depends on the quality of oracles and the transparency of underlying valuations. For tokenized Treasuries and major equities, reference prices are widely available from established markets, which can be fed into oracles and cross‑checked by market participants. For more esoteric RWAs, such as private loans, real estate, or sports IP, valuations are often model‑based, infrequent, and subject to significant uncertainty, making oracle design and disclosure practices critically important. This is one reason why industry discussions increasingly focus on data verification gaps in tokenization services and on the need for richer, more frequent attestations and audits to support market integrity.

Yield Stacks and “Real Yield” Narratives

One of the main attractions of RWA tokenization for crypto investors is access to “real yield” sourced from traditional financial instruments rather than from protocol inflation or short‑lived incentive schemes. Maple Finance captures this shift in its observation that as tokenization brings more capital onchain, “the yield layer underneath has to be real,” distinguishing sustainable credit and Treasury yields from “incentive yield burns” that dominated prior DeFi cycles. Tokenized Treasury products typically pass through yields from short‑term government bonds, which are capped by prevailing interest rates and fund expenses, while tokenized credit pools offer higher but riskier returns based on loan performance. Protocols can take these base yields and stack them with additional incentives or fees, but doing so introduces complexity and potential misalignment between perceived and actual risk.

Citi’s analysis of tokenized markets notes that the convergence of RWA yields and DeFi infrastructure opens up new carry and basis strategies but also demands more sophisticated risk management and credit analysis. Investors can, for instance, borrow stablecoins, deposit them into a tokenized Treasury fund to earn the risk‑free rate, and then re‑deploy the resulting tokenized shares as collateral to lever that exposure, or they can provide liquidity in AMMs that pair RWA tokens with stablecoins, effectively earning trading fees on top of base yields. These yield stacks can be productive when built on transparent, well‑understood assets, but they can quickly become fragile if the base layer is opaque or if redemption rights are poorly defined.

The empirical tokenomics literature underscores that token design can materially affect market outcomes by shaping expectations about dilution, cash flow rights, and governance. In tokenized credit protocols, for example, junior tranche tokens may absorb first losses in exchange for higher yields, while senior tokens earn lower yields but sit higher in the capital stack. If this hierarchy is not clearly encoded and communicated, investors may misjudge their exposure. Moreover, the interaction between RWA tokens and native governance tokens creates multi‑layered incentive structures: governance token holders may vote on risk parameters or reserve ratios that directly affect the safety and yield of RWA tokens, raising questions about conflicts of interest and alignment between protocol insiders and external investors.

- 01Central bank sandbox experiments↗

HKMA Project Ensemble, BIS G20 report, UK Regulated Liability Network, and Project Agorá collectively drew the most clicks, signaling readers track how monetary authorities are testing tokenization before committing to it.

- 02BlackRock tokenization dominance↗

BlackRock's BUIDL fund appearing as a reserve asset for Ethena/Securitize, Larry Fink's ETH ETF backing, and the MD of Digital Assets hire created a narrative that one firm is setting the industry's onchain standard.

- 03Wall Street infrastructure onchain↗

DTCC, NYSE, JPMorgan, and Chainlink pilot stories showed readers that legacy settlement rails — not just startups — are actively rebuilding on-chain, making tokenization feel inevitable rather than speculative.

- 04RWA platform funding race↗

Fundraises by Superstate, Homium, and Ondo alongside Libre's institutional launch signaled a competitive sprint to own the tokenized-fund and tokenized-credit infrastructure layer.

- 05DeFi leverage and stability risks↗

The BIS borrower-behavior study, the Federal Reserve's risk discussion, and the RealT 'slumlording' investigation showed readers are actively stress-testing whether tokenized credit repeats TradFi leverage pathologies on faster rails.

- 06Equity tokenization vs. SEC↗

Robinhood's call for startup-equity tokenization and the SEC advisory subcommittee's rejection of a blanket exemption framed a live regulatory standoff that readers followed as a bellwether for broader U.S. market access.

Real‑World Asset Tokenization: From Concept to Core Infrastructure

Market Size, Momentum, and Projections

The RWA tokenization market has moved from experimental pilots to a meaningful, though still small, segment of global finance. Citi estimates that tokenized digital securities and RWAs could grow from roughly 17 billion dollars today to about 5.5 trillion dollars by 2030 in its base‑case scenario, with a range of 2.7 to 8.2 trillion dollars depending on adoption and regulatory paths. The World Economic Forum similarly highlights tokenization as a next‑generation infrastructure layer for financial markets, emphasizing that tokenized bonds, funds, and other instruments are already being tested or deployed by major banks and market infrastructures. Industry trackers suggest that tens of billions of dollars in private credit, U.S. Treasuries, commodities, and other RWAs are already represented on public blockchains, with more in permissioned pilots, underscoring that this is no longer a marginal use case for crypto infrastructure.

Recent industry developments reinforce this trajectory. Coinbase’s strategic investment in Centrifuge, which it has named its preferred tokenization partner, signals that large crypto exchanges view RWA tokenization as a core pillar of their onchain finance offerings, especially on layer‑2 networks like Base. Protocols such as Ondo have grown tokenized Treasury products into some of the most widely held fixed‑income instruments onchain and have expanded into tokenized U.S. stocks and ETFs, with total value locked reportedly surpassing the billion‑dollar mark in some tokenized equity products. At the same time, traditional market infrastructures like DTCC and Clearstream are integrating tokenization into their services, planning to issue tokenized versions of assets already held in custody and to support blockchain‑based settlement flows.

This momentum has led some commentators to describe a “tokenization takeover” of financial plumbing, where tokenized representations of deposits, funds, and securities become standard rails for transferring and pledging value, even if end‑users are not always aware that tokens are involved. The analogy to the ETF boom is instructive: just as ETFs became a default wrapper for equity and bond exposure over two decades, tokenized wrappers may gradually become standard for issuing and managing a wide range of assets, with onchain markets handling intraday liquidity and settlement while traditional systems handle regulation and long‑term custody. However, whether tokenization reaches multi‑trillion‑dollar scale will depend heavily on regulatory clarity, interoperability between platforms, and the ability of tokenized markets to handle stress events without triggering systemic instability.

Key Asset Classes: Treasuries, Credit, Real Estate, Equities, Commodities, and Sports

Short‑term government debt has been one of the earliest and most popular targets for RWA tokenization. Tokenized Treasury funds such as Ondo’s OUSG and similar products offer onchain investors access to U.S. Treasury yields, with tokens representing interests in funds or SPVs that hold underlying government securities. These products benefit from deep underlying markets, transparent pricing, and relatively low credit risk, making them attractive as collateral in DeFi protocols and as yield‑bearing alternatives to holding idle stablecoins. They also raise questions about how tokenized shares in funds interact with existing regulations for money market funds and collective investment schemes, particularly regarding liquidity fees, gates, and redemption terms.

Private credit is another major frontier, with platforms like Maple Finance and Centrifuge creating tokenized pools of loans to businesses, fintechs, and other borrowers. These pools typically issue senior and junior tranche tokens, with the former marketed as relatively low‑risk, lower‑yield instruments and the latter absorbing first losses in exchange for higher yields. By tokenizing credit exposures, these platforms aim to tap global crypto liquidity for real‑world lending, potentially increasing capital access for borrowers while offering crypto investors a way to earn yields uncoupled from purely crypto‑native cycles. However, they also import credit risk, underwriting risk, and potential default cycles into DeFi, reinforcing regulators’ concerns about cross‑market contagion.

Real estate tokenization spans a spectrum from fractionalized ownership of individual properties to shares in tokenized real estate funds and mortgage‑backed instruments. Tokenization promises to lower investment minimums, broaden the investor base, and enable more fluid secondary markets for traditionally illiquid assets such as commercial buildings or rental portfolios. Yet the legal complexity of property rights, local regulations, and tenant relationships makes robust structuring and governance critical. Coinbase’s Armstrong has highlighted real estate as one sector where tokenization could streamline trading and ownership transfers, connecting global capital with local assets via onchain rails.

Equities and funds have recently become focal points for tokenization. Ondo’s tokenized exposures to U.S. stocks and ETFs, which now trade on the 360X regulated digital asset venue, are one example of how equity claims can be wrapped in tokens while staying within existing regulatory perimeters. The NYSE’s announced platform for tokenized securities aims to allow companies to issue digital tokens representing their securities and to list them for 24/7 trading and instant settlement, potentially upending the traditional exchange model if regulators approve and issuers participate. At the same time, the SEC’s exploration of an innovation exemption for tokenized stocks raises the prospect that third parties could create tokenized claims on public shares without issuer involvement, by buying and custodializing the shares and issuing onchain claims, a model that has triggered intense debate over permission, investor protection, and systemic risk.

Commodities and sports illustrate how tokenization can reach beyond traditional financial instruments. Commodities such as gold and oil are increasingly represented by tokens backed by warehouse receipts or custodied inventories, giving crypto‑native investors exposure to macro hedges and diversification assets via familiar onchain rails. Meanwhile, sports franchises and leagues represent a “500‑billion‑plus” ownership economy built on stadium equity, media rights, and brand IP, much of which is currently inaccessible to fans and smaller investors. Private equity’s growing involvement in sports, with more than 74 North American professional teams having some level of private equity ownership, underlines the appetite for financializing sports assets. Tokenization offers potential pathways for fan‑aligned ownership or revenue sharing instruments, though these raise complex regulatory questions around securities law, consumer protection, and league governance.

Case Studies: Ondo, Maple, Centrifuge, and Market Infrastructures

Ondo Finance is often cited as a leading example of RWA tokenization in practice. The protocol launched one of the first and most widely held tokenized Treasury products, offering tokens such as OUSG that represent interests in funds holding short‑duration U.S. government securities. These tokens are issued under regulatory frameworks that restrict them to qualified investors in many jurisdictions, but they can be held and transacted onchain, integrated into DeFi protocols, and used as collateral. Building on this foundation, Ondo has developed Ondo Global Markets, which provides tokenized exposures to U.S. stocks and ETFs and has partnered with Clearstream and 360X to list these instruments on a regulated digital asset venue, enabling near‑instant settlement and bridging between traditional and onchain markets. Ondo executives have argued that tokenization is moving from experiment to core market infrastructure and that privacy and verification will be critical bottlenecks as tokenized markets scale.

Maple Finance represents a different angle, focusing on institutional‑grade credit markets. Maple operates pools of loans to vetted borrowers, funded by tokenized senior and junior tranche instruments that offer yields tied to loan performance. As Maple notes, tokenization is bringing more capital onchain, but the “yield layer underneath has to be real,” emphasizing that sustainable returns must come from underlying credit spreads and Treasury yields rather than from unsustainable incentive emissions. Maple’s design, which combines offchain underwriting with onchain pool management and tokenization, illustrates both the potential and the risk of RWA credit: capital can flow quickly into new lending markets, but defaults, fraud, or macro downturns can transmit shocks into DeFi investor portfolios.

Centrifuge sits at the intersection of crypto platforms and traditional institutions. As Coinbase’s preferred tokenization partner, Centrifuge works to bring private credit, trade finance, and other fixed‑income exposures onto Base and other networks, using tokenization to lower capital costs and broaden investor access. Coinbase’s investment in Centrifuge underscores a strategic bet that RWA tokenization will be core to its long‑term onchain finance business, complementing its stablecoin and exchange offerings. Other infrastructures, such as tZERO’s addition of Aptos support to scale tokenization and trading of digital securities, and Tether’s memorandum of understanding with Dubai Multi Commodities Centre (DMCC) to advance blockchain education and tokenization initiatives, signal broader industry efforts to embed tokenization into regional hubs and multi‑chain ecosystems.

Market infrastructures like DTCC and Clearstream, meanwhile, are extending tokenization into the heart of existing capital markets. DTCC’s integration with the Stellar network is designed to enable tokenized versions of assets already held in its depository, effectively allowing broker‑dealers and custodians to manage tokenized exposures while relying on the same central counterparty and settlement frameworks that support traditional securities. Clearstream’s collaboration with Ondo and 360X, as noted earlier, brings tokenized stocks and ETFs into a regulated trading venue backed by Deutsche Börse, potentially easing institutional adoption by keeping custody and regulation within familiar bounds. These experiments suggest that tokenization is not only about new crypto‑native assets but about upgrading the rails of existing market infrastructure.

Tokenized Public Markets: Stocks, ETFs, and the SEC Debate

The tokenization of public equities and ETFs sits at the center of some of the most contentious debates about the future of capital markets. On one side, regulated initiatives such as NYSE’s tokenized securities platform and Clearstream’s 360X venue envision issuer‑sanctioned tokenized shares and funds that trade on blockchain rails but remain within the traditional securities regulatory perimeter. These models aim to deliver benefits such as 24/7 trading, instant settlement, and composability with other digital instruments while preserving issuer control, disclosure requirements, and investor protections. On the other side, proposals for SEC innovation exemptions could allow third parties to issue tokenized claims on public stocks without issuer permission, as long as investor protections are deemed equivalent, a move that has sparked concern among some market participants.

A widely discussed scenario involves a third party buying shares of a public company such as Apple, custoding them, and then issuing blockchain tokens that represent claims on those shares, potentially tradable on DEXs without KYC or traditional oversight. These “wrapped” or synthetic tokens could be traded 24/7 worldwide, used as collateral in DeFi lending markets, and repackaged into structured products, even though the issuer has no direct relationship with token holders and owes them no duties beyond those owed to all shareholders. Critics argue that this could turn every public company into a potential locus of DeFi‑driven speculative cycles, with no clear mechanisms to protect token holders if the wrapper issuer defaults or mismanages custody. Proponents counter that similar structures already exist in traditional finance (for example, depositary receipts and total return swaps) and that tokenization could democratize access to global equities.

Regulators such as Fed Governor Cook have emphasized that tokenization can alter the incentives of investors to redeem assets with issuers, which may either stabilize or destabilize markets depending on how redemption rights and liquidity management are designed. For tokenized funds and deposit‑like instruments, features such as intraday liquidity, 24/7 redemption, and global reach could make runs faster and more severe in stress scenarios, especially if token holders are leveraged or if secondary market liquidity evaporates. These concerns are shaping proposals such as the CLARITY Act, which aims to set guardrails around tokenized securities and clarify the roles and responsibilities of issuers, intermediaries, and token sponsors. As tokenized stock and ETF products surpass milestones like one billion dollars in total value and become integrated with DeFi, the stakes of these regulatory decisions will only grow.

Stablecoins and the Role of Onchain Money in Tokenized Markets

Stablecoins are the monetary backbone of tokenized markets, serving as the primary settlement asset, collateral, and unit of account for many RWA tokens and trading venues. Most stablecoins represent tokenized claims on bank deposits or short‑term securities, effectively making them an early and large‑scale form of tokenization in their own right. They enable atomic settlement between tokenized assets and cash‑equivalents onchain, support margining and collateralization in DeFi protocols, and provide a bridge between fiat payment systems and onchain financial markets. As tokenized Treasuries, credit, and equities grow, stablecoins become even more central, because they are the asset that ties together issuers, investors, and trading infrastructure across jurisdictions.

Banks and payment giants are increasingly exploring tokenized deposits and stablecoin payment routes as part of this ecosystem. Reports highlight that large banks are charting deposit networks where tokenized representations of deposits can be transferred across permissioned networks or public chains, potentially coexisting with or complementing private stablecoins. Payment companies are piloting stablecoin‑based cross‑border payment flows, reducing reliance on correspondent banking and legacy messaging systems. These developments blur the line between deposit tokens, stablecoins, and tokenized money market instruments, raising important regulatory questions about which entities can issue tokenized money, how reserves are managed, and how such instruments should be supervised for liquidity and credit risk.

Coinbase CEO Brian Armstrong has repeatedly argued that RWA tokenization and stablecoin payments are among the key upgrades required for the financial system, alongside 24/7 global trading and AI‑driven financial services. In Armstrong’s view, tokenizing assets such as real estate, stocks, bonds, and funds, and enabling them to trade and settle in stablecoins around the clock, will streamline capital formation and make markets more accessible. This vision assumes a world where stablecoins are widely accepted as settlement assets by both traditional and crypto‑native intermediaries, necessitating regulatory frameworks that recognize stablecoins as core infrastructure rather than peripheral crypto products.

At the same time, central banks and regulators are wary of the systemic implications of widespread stablecoin and tokenized deposit usage. Fed officials have noted that tokenization might change the incentives of investors to redeem their assets, potentially affecting the stability of money market funds, banks, and other liquidity transformation vehicles. If tokenized cash instruments promise instant redemption onchain but rely on underlying reserves that may be less liquid in stress scenarios, they could face run dynamics analogous to, or faster than, those seen in past crises. Balancing the efficiency gains from onchain settlement with the need for robust liquidity management and prudential oversight is therefore a central policy challenge in the era of tokenized money.

DTCC acquires Securrency to accelerate tokenization buildout

BlackRock launches BUIDL tokenized treasury fund on Ethereum

HKMA opens Project Ensemble Sandbox for asset tokenization

BIS delivers G20 Brasil report on tokenization and central bank roles

- 2025-01launch

Nomura Laser Digital's Libre protocol launches on Polygon for institutional fund tokenization

- 2025-04milestone

Project Agorá reaches 40+ central banks and financial firms for cross-border tokenization

DTCC expands digital asset initiatives via Stellar network integration

NYSE announces development of tokenized securities trading platform

Regulatory Landscape: SEC, Systemic Risk, and Global Experiments

U.S. Securities Law, the SEC, and Innovation Exemptions

In the United States, tokenization sits at the intersection of securities law, banking regulation, and emerging digital asset rules. If a token represents a share in a fund, a bond, a note, or equity securities, it is generally treated as a security and must comply with the Securities Act, Exchange Act, and related regulations, regardless of its onchain format. The SEC has taken the position that many tokenized instruments fall squarely within its jurisdiction, requiring registration or reliance on exemptions such as Regulation D or Regulation S, and has brought enforcement actions against token offerings that it views as unregistered securities. For tokenized public stocks issued by third parties, questions revolve around whether such issuers are effectively offering depositary receipts or other securities requiring registration and how existing issuer disclosure requirements apply when the issuer is not directly involved.

Reports that the SEC is considering an “innovation exemption” that would allow permissionless tokenization of stocks by third parties have generated intense debate. Under such a regime, an intermediary could buy and custody a block of shares in a public company, then issue blockchain tokens representing claims on those shares without needing explicit permission from the issuer, provided that existing investor protections are maintained through custodian regulation and disclosure. Supporters argue that this would mirror existing structures such as depositary receipts and open the door to more flexible, 24/7, global access to U.S. equities, while opponents warn that it could lead to fragmented liquidity, opaque leverage, and heightened systemic risk if tokenized shares are heavily used in DeFi.

The CLARITY Act and other legislative proposals aim to bring more certainty to tokenized securities by defining when and how digital representations of assets fall under securities law, what disclosures are required, and how intermediaries must be supervised. Industry participants argue that clear, technology‑neutral rules would facilitate responsible tokenization by giving issuers, exchanges, and custodians a stable framework within which to innovate, while regulators emphasize the need to ensure that the core objectives of investor protection, fair markets, and systemic stability are preserved. The outcome of these debates will shape whether the U.S. becomes a leading jurisdiction for tokenized capital markets or cedes that role to other regions.

Prudential Regulation and Systemic Risk Concerns

Beyond securities law, prudential regulators and central banks are concerned with how tokenization might reshape systemic risk. In a notable speech, Federal Reserve Governor Lisa Cook underscored that tokenization could alter investors’ incentives to redeem assets with issuers and change the dynamics of runs on funds or deposit‑like instruments. For example, if shares in a money market fund or claims on bank deposits are tokenized and trade onchain with instant settlement, investors may be able to exit much more rapidly in response to stress, potentially overwhelming liquidity management tools designed for slower, more predictable redemption flows. Conversely, tokenization could enable more granular liquidity and redemption controls, such as smart‑contract‑enforced gates or dynamic fees, that adjust in real time to market conditions.

Tokenized deposits and tokenized shares in money market funds sit at the heart of this debate. On the one hand, they can improve transparency, enable automated compliance and risk management, and integrate more seamlessly with onchain collateral and payment systems. On the other hand, they could amplify contagion if failures in tokenized markets trigger runs on underlying banking or fund infrastructures, especially if DeFi leverage is built on top of tokenized claims. Cook warns that tokenization might thus entail both benefits and risks for financial stability and calls for careful monitoring, robust regulatory frameworks, and possibly new prudential tools tailored to tokenized instruments.

Cross‑border issues further complicate prudential oversight. Tokenized claims on assets in one jurisdiction can be traded and rehypothecated across global DeFi markets, potentially exposing investors and regulators in other jurisdictions to risks they do not fully understand. Harmonizing standards for custody, reserve management, disclosures, and redemption rights across jurisdictions is therefore a major challenge, particularly as more banks, exchanges, and asset managers launch tokenized products. The interplay between global stablecoins, tokenized RWAs, and domestic monetary and macroprudential policies is likely to remain a key focus of central banks in the coming years.

Data Protection, Privacy, and Verification

As tokenized markets mature, privacy and data protection have emerged as critical themes. Tokenization requires detailed information about underlying assets, investors, and transaction flows to be available for verification, compliance, and risk management, but exposing this data broadly on public ledgers can compromise confidentiality, competitive advantage, and personal privacy. Industry voices have emphasized that tokenized markets need strong verification mechanisms and robust privacy controls: it must be possible for counterparties, auditors, and regulators to verify that tokenized assets are fully backed, properly managed, and compliant while preserving the confidentiality of sensitive data.

Zero‑knowledge proofs, secure multiparty computation, and privacy‑preserving databases are being explored as tools to reconcile these demands. For example, a zero‑knowledge database application might allow an issuer to prove that total onchain token supply does not exceed offchain assets held in custody, or that all token holders have passed KYC checks, without revealing granular position data or customer identities publicly. Industry projects claim that such tools can accelerate tokenization workflows by orders of magnitude while maintaining rigorous data protection and compliance, aligning with policy expectations under privacy laws and bank secrecy frameworks. At the same time, regulators and auditors need to develop expertise in evaluating cryptographic proofs and integrating them into supervisory processes, which is a non‑trivial institutional challenge.

Data verification gaps in tokenization services remain a concern. If tokenized assets rely on infrequent or unaudited reports from custodians or issuers, investors may be exposed to misrepresentation or fraud, as seen in historical scandals involving offchain assets and reserve claims. Efforts to build “audit‑proof chain lifecycles” for RWA tokens aim to standardize and automate the publication of proofs of reserve, asset composition, and risk metrics, making it easier for investors and regulators to assess tokenized products in near‑real time. The success of these efforts will be central to the credibility of tokenized markets as they scale.

Global Policy Experiments and Jurisdictional Competition

Around the world, jurisdictions are experimenting with different approaches to tokenization. Some, like the European Union with its Markets in Crypto‑Assets (MiCA) framework and pilot regimes for tokenized securities, are developing comprehensive regulatory structures that recognize tokenized instruments and infrastructures within existing financial law. Others, such as Dubai through its DMCC and virtual asset regimes, are positioning themselves as hubs for tokenization and blockchain innovation, as illustrated by initiatives like Tether’s memorandum of understanding with DMCC to advance blockchain education and tokenization projects in the region. These efforts often aim to attract issuers, exchanges, and infrastructure providers by offering clear, supportive rules while maintaining anti‑money‑laundering and investor‑protection standards.

Asian financial centers such as Singapore and Hong Kong are also pushing forward with tokenization pilots in areas like tokenized green bonds, fund units, and deposit tokens, often emphasizing institutional use cases and permissioned or regulated networks. Their regulatory strategies typically focus on integrating tokenization into existing securities and payment frameworks rather than creating entirely new regimes, which can ease institutional adoption while limiting permissionless experimentation. In contrast, more restrictive jurisdictions may slow or limit tokenization of certain assets, especially where concerns about capital flight, speculative bubbles, or regulatory arbitrage are paramount.

This jurisdictional competition is likely to shape where tokenized capital markets evolve most rapidly. Issuers and platforms may gravitate toward countries that offer clear, predictable frameworks for tokenized securities and stablecoins, while global DeFi protocols will continue to operate across borders, raising complex questions about cross‑border supervision and enforcement. For crypto market participants, understanding the regulatory map is as important as understanding the technology stack, especially when dealing with tokenized instruments that have legal and economic ties to specific jurisdictions and regulatory regimes.

Technical Architectures: Public Chains, Permissioned Ledgers, and Oracles

Public Blockchains and DeFi Composability

Public, permissionless blockchains such as Ethereum and its layer‑2 networks, alongside platforms like Solana and Aptos, provide the backbone for many tokenization projects aimed at crypto‑native users. Their key advantages are global accessibility, 24/7 availability, and composability: once a token is live on a public chain, it can in principle integrate with a wide range of DeFi protocols, wallets, and infrastructure without bespoke bilateral arrangements. This composability enables use cases such as using tokenized Treasuries as collateral in lending protocols, pairing RWA tokens with stablecoins in AMMs, and incorporating tokenized credit exposures into yield aggregation strategies.

However, public chains also present challenges for regulated institutions. The open nature of these networks makes it harder to enforce transfer restrictions, KYC requirements, and jurisdictional limits, although token standards with embedded whitelists and transfer‑restriction logic can mitigate this to some degree. Scalability, transaction costs, and privacy are ongoing concerns, particularly for high‑volume institutional workflows. Nonetheless, major players are leaning into public‑chain tokenization: Coinbase’s Base network is being used as a venue for RWA tokenization via partners like Centrifuge, while protocols like Maple operate on Ethereum to connect institutional borrowers and crypto lenders. tZERO’s addition of Aptos support for tokenization and trading of digital securities reflects a multi‑chain strategy where public networks support regulated and semi‑regulated tokenized instruments.

The convergence of TradFi and DeFi is particularly evident in these architectures. LMAX Group’s CEO, for instance, has noted that the lines between traditional finance and crypto are disappearing as institutions prepare for a tokenized future and that “tokenization tomorrow is the derivative of yesterday,” suggesting a continuity between derivatives innovation and tokenized exposures. As more banks, asset managers, and exchanges deploy tokenized products on public chains, the distinction between “crypto markets” and “traditional markets” may erode, replaced by a spectrum of onchain instruments with varying degrees of regulation and institutional involvement.

Permissioned Ledgers and Market Infrastructure Platforms

Permissioned or consortium ledgers offer an alternative architecture better suited to heavily regulated, institutional contexts. In these setups, access to the ledger is restricted to known participants such as banks, broker‑dealers, custodians, and clearinghouses, and governance is managed by a consortium or a central operator. Tokenization on such ledgers enables many of the same benefits as public‑chain tokenization—such as programmable settlement, instant DvP, and automation of corporate actions—while offering more control over participant identity, data visibility, and compliance.

DTCC’s collaboration with the Stellar Development Foundation exemplifies this approach. DTCC plans to issue tokenized representations of assets held in its depository on Stellar, leveraging blockchain features while keeping custody and systemic risk management within its established infrastructure. Similarly, the NYSE’s tokenized securities platform and Clearstream’s 360X venue are designed as regulated trading environments where tokenized securities can be issued, traded, and settled, often using a mix of permissioned and public components. These models may appeal to issuers and institutional investors that are comfortable with existing governance structures and regulatory oversight but want the efficiency and programmability benefits of tokenization.

Trade‑offs between public and permissioned architectures hinge on openness versus control. Public chains maximize composability and innovation but pose challenges for regulatory compliance and data confidentiality; permissioned ledgers offer tighter control and easier integration with existing systems but may limit interoperability and innovation. Hybrid models—where permissioned networks interoperate with public chains via bridges, wrapped assets, or standardized APIs—are likely to proliferate, especially as tokenized assets are used both in institutional contexts and in DeFi.

Oracles, Attestations, and Proof‑of‑Reserve

Oracles and attestation mechanisms are the connective tissue between tokenized assets and their offchain underpinnings. Chainlink’s RWA tutorials illustrate in detail how smart contracts can interact with offchain data feeds to validate minting and redemption operations, check portfolio balances, and update token states. For example, an RWA minting contract might require a Chainlink Functions call to a custodian or data provider to confirm that new collateral has been deposited before allowing new tokens to be minted, and similarly, redemptions might be contingent on verifying that sufficient collateral is available to honor the claim. Mapping between request IDs, responses, and token states, as shown in such tutorials, underscores the complexity of building reliable tokenized systems that depend on offchain data integrity.

Proof‑of‑reserve mechanisms add another layer, enabling issuers to publish cryptographic attestations that onchain token supplies match or do not exceed offchain reserves. In some designs, auditors or custodians sign messages attesting to reserve levels, which are then verified by smart contracts; in more advanced setups, zero‑knowledge proofs can demonstrate reserve sufficiency without exposing detailed balance sheets. RWA audit lifecycles are being redesigned around these tools, with the goal of making reserve verification more continuous, automated, and tamper‑resistant than traditional quarterly audits.

Despite progress, gaps remain. DTCC’s tokenization initiatives and similar projects face challenges in ensuring that data about underlying assets, settlement statuses, and corporate actions is consistently and accurately mirrored onchain. If oracles fail, are manipulated, or rely on delayed or inaccurate data, tokenized assets can become misaligned with their underlying, creating arbitrage opportunities, mispricing, and potential losses for investors. As tokenized markets grow, the robustness of oracle and attestation frameworks will be as important as the solidity of the smart contracts that manage token logic.

Sandbox regimes in Hong Kong, the EU, and the UK operate on divergent rules, while the SEC's incremental reform stance leaves U.S. equity tokenization in a legal gray zone.

Tokenized RWA platforms rely on smart contracts to enforce legal ownership rights that courts have not uniformly recognized, creating execution risk if on-chain state diverges from off-chain legal record.

Secondary market depth for tokenized funds and real-estate instruments remains thin; the BIS borrower study found DeFi leverage ratios can amplify exit pressure when redemptions spike.

Platforms like Libeara, Libre, and BUIDL depend on single licensed issuers and custodians, concentrating counterparty risk even though the settlement layer is decentralized.

The BIS G20 report warned that programmable tokenized money could complicate central banks' ability to manage monetary conditions if large volumes shift outside traditional reserve channels.

Tokenized Treasuries and investment-grade fund shares carry modest mark-to-market risk; higher risk concentrates in illiquid RWA classes such as real-estate and private credit where on-chain price discovery is immature.

Convergence of TradFi, DeFi, and AI Around Tokenization

Institutional Adoption and the “One Industry” Thesis

Institutional engagement with tokenization has broadened from tentative pilots to more ambitious infrastructure projects. Banks are building tokenized deposit networks; asset managers are experimenting with tokenized funds; and exchanges are designing platforms for tokenized securities, as seen in initiatives by NYSE, DTCC, and Clearstream. Crypto‑native institutions, including major centralized exchanges and DeFi protocols, are simultaneously expanding into RWA tokenization, with Coinbase, Ondo, Maple, and Centrifuge among those positioning tokenization as a core pillar of their growth strategies. This convergence has prompted industry leaders to suggest that “Wall Street and crypto should just be one industry,” reflecting a belief that the divide between traditional and onchain finance will diminish as both adopt tokenized infrastructure.

LMAX Group’s CEO has argued that tokenization is the next iteration of financial innovation, akin to past waves of derivatives and electronic trading, and that the lines between TradFi and crypto are increasingly blurry as institutions prepare for a tokenized future. This perspective is echoed in events like The Convergence Summit, where themes such as “TradFi × DeFi tokenization” and “AI × blockchain” dominate discussions, highlighting the intersecting trajectories of institutional finance, decentralized protocols, and advanced analytics. With an estimated 30‑plus billion dollars of real‑world assets already onchain and trillions more projected, tokenization is becoming a neutral meeting ground where institutions and crypto‑native players collaborate, compete, and co‑evolve.

The implications for market structure are profound. If banks, exchanges, and asset managers adopt tokenization as a standard issuance and settlement mechanism, DeFi protocols may become routes for distributing and leveraging tokenized exposures rather than separate “shadow” markets. Conversely, if DeFi continues to innovate faster than traditional institutions, it may set de facto standards for token design, collateral usage, and risk management that influence institutional practices. Either way, tokenization is at the heart of the dialogue about how “Wall Street” and crypto converge.

AI, Data, and Tokenized Markets

Artificial intelligence is tightly intertwined with tokenization in industry narratives. Analysts and practitioners note that tokenized markets generate rich, machine‑readable data about asset flows, investor behavior, and protocol states, which can be mined by AI systems for trading, risk management, and compliance insights. Citi’s report, for instance, discusses how AI could analyze tokenized asset markets to detect anomalies, optimize liquidity provision, and model systemic risk in real time, leveraging the granularity and transparency of onchain data. Ondo executives and others have suggested that the combination of tokenization and AI could echo or even exceed the ETF boom by enabling highly customized, algorithmically managed portfolios built from tokenized building blocks.

At the same time, AI introduces its own risks and regulatory challenges. Algorithmic trading and portfolio management in tokenized markets can exacerbate volatility, produce opaque feedback loops, and generate herding behavior, particularly if many actors rely on similar models trained on the same data. The integration of AI into compliance workflows—such as transaction monitoring, KYC, and risk scoring of tokenized assets—raises questions about bias, explainability, and accountability. Regulators may need to consider how traditional model risk management and algorithmic trading rules apply in a world where AI systems autonomously interact with tokenized assets and DeFi protocols.

Despite these challenges, the synergies between tokenization and AI are likely to deepen. Tokenized markets offer structured data that are well suited to machine learning, while AI offers tools for navigating the complexity and scale of onchain financial ecosystems. For crypto market participants, this convergence means that understanding tokenization is increasingly inseparable from understanding the role of AI in analyzing and acting upon tokenized markets.

Sports, Media, and the Fan Ownership Economy

Beyond core financial instruments, tokenization is poised to transform sectors such as sports and media, where intangible assets—brand, IP, fan loyalty—are central to value. The sports industry, heading toward a trillion‑dollar valuation, has already seen significant private equity investment, with more than 74 North American professional teams having some level of private equity ownership. This reflects the attractiveness of stable media revenues, global fan bases, and scarce franchise slots. Yet for fans, access to ownership or revenue sharing remains limited, often confined to high‑net‑worth individuals and institutions.

Tokenization offers new possibilities for fan‑aligned ownership and engagement. Teams or leagues could issue tokens representing fractional interests in future revenues, specific game‑day experiences, or intellectual property, allowing fans to participate more directly in the economic upside of the franchises they support. Unlike simple “fan tokens” that confer only voting rights in trivial polls or access to merchandise, security‑like tokens backed by real revenue streams would more closely align with the core economics of sports assets, though they would also fall under securities regulation and league governance rules. The challenge is to design structures that are both legally sound and aligned with fan interests, avoiding exploitative or overly speculative models.

Media and entertainment rights present similar opportunities. Tokenizing revenue streams from streaming deals, music catalogs, or film royalties could open new funding channels for creators and give investors exposure to diversified media portfolios. However, the complexity of licensing, contractual hierarchies, and cross‑border IP enforcement means that robust legal structuring is essential. In all these sectors, tokenization is less about speculative trading of “coins” and more about reconfiguring how ownership and participation are structured, distributed, and governed.

Risks, Challenges, and Open Questions

Legal, Governance, and Counterparty Risks

Despite its promise, tokenization introduces or amplifies several categories of risk. Legal risk arises when the relationship between tokens and underlying assets is ambiguous or inadequately documented. If a token purports to represent a claim on an asset but the legal documentation does not clearly establish that claim or its priority relative to other creditors, token holders may discover in a default scenario that they have weaker rights than expected. Jurisdictional conflicts can exacerbate this uncertainty, especially when tokens trade globally but the underlying assets and issuers are subject to local law that may not recognize or enforce token‑based claims.

Governance risk is particularly salient in RWA protocols, where decisions about underwriting standards, reserve management, and redemption policies are often made by governance token holders or foundation entities. Conflicts of interest can arise between tokenized asset holders seeking safety and predictable returns and governance token holders seeking higher fees or more aggressive growth. Without robust governance frameworks, including clear fiduciary duties, transparency, and checks and balances, tokenized systems may be vulnerable to governance attacks, rent extraction, or mismanagement.

Counterparty risk remains at the core of many tokenized structures. Custodians, trustees, and SPVs holding underlying assets can fail, mismanage funds, or be subject to fraud, even if the onchain token logic is flawless. Synthetic tokenization models, where tokens are backed by an intermediary’s balance sheet rather than segregated collateral, introduce additional credit risk akin to unsecured exposure to that intermediary. While some of these risks are familiar from traditional finance, tokenization can obscure them behind the veneer of smart contracts and onchain activity, potentially leading investors to underestimate counterparty exposure.

Liquidity Illusions, Leverage, and DeFi Feedback Loops

Tokenization’s promise of enhanced liquidity and 24/7 trading can sometimes mask underlying illiquidity and fragility. Illiquid assets such as private loans, real estate, or niche funds may be tokenized and traded frequently onchain, creating an impression of liquidity that may evaporate when investors attempt to redeem tokens for underlying assets. In stress scenarios, redemption gates, long settlement times for underlying asset sales, or outright defaults can lead to sharp discounts in token prices and, if leverage is involved, cascading liquidations.

The integration of tokenized assets into DeFi lending and derivatives markets amplifies these dynamics. If tokenized stocks, bonds, or credit exposures are heavily used as collateral, price drops or doubts about backing can trigger margin calls and liquidations that further depress prices, similar to the dynamics observed in previous DeFi and stablecoin crises. The SEC’s concern that unauthorized tokenization could turn public companies into potential “Terra‑Luna‑like” contagion nodes reflects the fear that misaligned incentives, leverage, and complex interconnections could destabilize not only tokenized markets but also underlying equity markets.

Maple Finance’s emphasis on the need for “real” underlying yields, as opposed to purely incentive‑driven returns, points toward one mitigant: aligning tokenized products with robust, transparent, and sustainable cash flows. However, even with real yields, leverage and opacity can generate systemic risk if not monitored and constrained. Designing risk limits, collateral haircuts, and circuit breakers that take into account the specific properties of tokenized assets is therefore a key challenge for both DeFi protocol designers and regulators.

Operational, Cyber, and Smart Contract Risks

Tokenization also exposes participants to operational and technological risks. Smart contract vulnerabilities can lead to loss or theft of tokenized assets, as seen in numerous DeFi exploits over the past years, and RWA protocols are not immune simply because their underlying assets are offchain. Bugs in minting, burning, or transfer logic can disrupt redemption processes or create discrepancies between onchain and offchain records. Upgrade mechanisms, if not properly governed, can be exploited by insiders or attackers to change contract behavior in ways that harm token holders.

Oracles and data feeds, as already noted, are another vector of risk. Manipulated or malfunctioning price feeds can trigger incorrect liquidations, misprice tokenized assets, or allow minting of unbacked tokens, particularly in thinly traded or illiquid markets. The complexity of integrating multiple data sources, custodians, and legal entities into a coherent tokenization system increases the attack surface and the likelihood of operational errors.

Post‑quantum cryptography concerns add a longer‑term layer of risk. Some analysts have warned that advances in quantum computing could eventually threaten the cryptographic primitives underpinning blockchains, potentially compromising keys and signatures used to control tokenized assets. While this is not an immediate threat, responsible tokenization initiatives must consider upgrade paths to quantum‑resistant cryptography and the challenges of rotating keys and contracts for large, distributed token holder bases.

Social, Distributional, and Ethical Implications

Finally, tokenization raises social and ethical questions about who benefits from increased financialization and access. Proponents argue that tokenization can democratize access to assets such as real estate, credit, and equities by lowering minimum investment sizes, enabling fractional ownership, and reducing geographic barriers. Critics worry that it may instead facilitate further concentration of ownership and control in the hands of large institutions and crypto‑savvy investors, while exposing retail investors to complex and poorly understood risks.

The possibility of tokenizing everything—from housing and education to personal data and social relationships—has sparked debates about commodification and the boundaries of market logic. In sports and culture, for example, tokenization could enhance fan participation and creator funding but could also encourage speculative behavior and financialize intimate aspects of fandom and community. Designing tokenized systems that respect human dignity, avoid exploitative structures, and align with broader social goals is an important but often overlooked dimension of the tokenization conversation.

How Builders and Institutions Can Approach Tokenization

Deciding What to Tokenize and Why

For builders and institutions, the first strategic decision is not how to tokenize but what and why. Tokenization should be applied where it offers clear advantages over existing structures, such as improved settlement efficiency, broader access, better liquidity, or enhanced composability with other financial tools. Assets that are already liquid, easily tradeable, and well served by existing infrastructures may benefit less from tokenization than those that are illiquid, fragmented, or cumbersome to transact. Money market funds, U.S. Treasuries, and blue‑chip equities are attractive because they combine deep underlying liquidity with high demand for onchain exposure, but their tokenization also raises complex regulatory and prudential questions.

Designers must also consider whether they are targeting crypto‑native investors, institutional clients, or both. Crypto‑native investors may value permissionless access, composability, and integration with DeFi protocols, whereas institutional clients may prioritize robust compliance, data privacy, and integration with existing middle‑ and back‑office systems. These preferences influence choices of network (public versus permissioned), token standards, and governance structures. Tokenization projects that lack a clear value proposition or target audience risk becoming purely speculative instruments without sustainable demand.

The taxonomy of RWA tokenization provides a useful framework for thinking about asset selection and design. It encourages issuers to classify tokens according to legal claim type (equity, debt, fund share), economic rights (principal, interest, voting), and technical properties (fungibility, transferability, upgradability). Using such frameworks early in the design process can help anticipate regulatory requirements, investor expectations, and integration needs.

Structuring Tokenomics and Governance for RWA Protocols