Deep dive explainer on real-world assets (RWAs) in crypto: how tokenization works, key market segments, RWA stablecoins and yield, institutional adoption, DeFi use cases, and the legal, market, and technical risks shaping onchain capital markets.

+2 sources across the wider coverage universe

DigiShares integrates Aptos to expand RWA infrastructure, leveraging sub-second finality and Move-based security to deliver scalable, institutional-grade asset tokenization globally2026-04

DigiShares integrates Aptos to expand RWA infrastructure, leveraging sub-second finality and Move-based security to deliver scalable, institutional-grade asset tokenization globally2026-04 IXS selects BitGo to secure Bitcoin collateral for institutional yield products, enabling BTC-backed liquidity and RWA exposure through regulated, bankruptcy-remote infrastructure2026-04

IXS selects BitGo to secure Bitcoin collateral for institutional yield products, enabling BTC-backed liquidity and RWA exposure through regulated, bankruptcy-remote infrastructure2026-04 IPOR Labs proposes utility-based pricing model for RWA liquidity in DeFi, helping investors decide between instant sale or delayed redemption using risk-adjusted certainty equivalents2026-04

IPOR Labs proposes utility-based pricing model for RWA liquidity in DeFi, helping investors decide between instant sale or delayed redemption using risk-adjusted certainty equivalents2026-04 DeFi sees $840M+ in tokenized asset deposits, marking growth of RWAs from theory to execution as advisors explore new risk and yield opportunities2026-04

DeFi sees $840M+ in tokenized asset deposits, marking growth of RWAs from theory to execution as advisors explore new risk and yield opportunities2026-04 Alchemy brings Stellar ecosystem to its platform, enabling builders to scale RWA platforms, cross-border payments, and financial apps with enterprise integrations2026-04

Alchemy brings Stellar ecosystem to its platform, enabling builders to scale RWA platforms, cross-border payments, and financial apps with enterprise integrations2026-04 Unlocking RWA potential: Sandy Kaul's insights from Franklin Templeton2026-04

Unlocking RWA potential: Sandy Kaul's insights from Franklin Templeton2026-04

Real-World Assets (RWAs) in Crypto: An Evergreen Guide

Tokenizing offchain assets on public blockchains is emerging as one of the most consequential trends in crypto, turning everything from U.S. Treasuries and stocks to reinsurance risk and private credit into programmable, composable building blocks. By understanding how real-world assets (RWAs) work onchain—legally, technically, and economically—crypto users can better navigate the growing universe of tokenized yield, trading, and capital markets opportunities while staying clear-eyed about the risks.

1. Introduction: Why Real-World Assets Matter Onchain

The core appeal of RWAs is simple: they promise to connect the trillions of dollars locked in traditional finance with the speed, transparency, and composability of blockchain systems. In traditional markets, access to high-quality yield, diversified credit exposures, or institutional-grade fund products is often gated by geography, minimum ticket sizes, intermediaries, and limited trading hours. Tokenization reframes these constraints as engineering problems. If an asset’s ownership, cash flows, and legal claims can be represented as tokens, then those tokens can move 24/7, be integrated into smart contracts, and be combined in novel ways with stablecoins, derivatives, and DeFi protocols.

This trend is no longer theoretical. The market capitalization of tokenized RWAs is widely reported in the tens of billions of dollars, with Ethereum alone estimated to host the majority of this value. Within that, tokenized U.S. Treasuries and money-market-like products account for a rapidly growing slice; analytics from RWA-focused data providers show over 15 billion dollars in tokenized U.S. government debt instruments alone, spanning bills, notes, bonds, and Treasury-focused funds. At the same time, other blockchains—particularly Solana—have become active venues for tokenized stocks, reinsurance securities, and structured credit funds, as seen in offerings like Exodus and Ondo’s tokenized equities platform and tokenized CLO and reinsurance products.

For a crypto-native audience, RWAs are not just another narrative. They are changing how onchain markets source collateral, generate yield, and attract institutional liquidity. RWA-backed stablecoins promise yield-bearing “cash” instruments. Tokenized Treasuries have become a de facto risk-free rate inside DeFi. Perpetual futures on tokenized equities and ETFs allow traders to express views on macro, tech earnings, or sector rotation without leaving an onchain environment. At the same time, the RWA boom raises deep questions about legal enforceability, regulatory boundaries, oracle and governance risk, and what “decentralization” really means when the underlying collateral sits in traditional custodians.

The goal of this explainer is to provide a durable, evergreen framework for understanding RWAs. It covers definitions and taxonomies, the lifecycle of tokenization, the state of RWA markets across chains, the design of RWA stablecoins and yield products, the dynamics of institutional adoption, and the main risk vectors to monitor. Throughout, it connects these concepts to real examples in today’s markets so that readers can map current headlines to underlying structures and long-run trends.

South Korea's biggest banks, fintechs and internet giants are racing to build stablecoin and RWA infrastructure ahead of regulatory clarity, reshaping Asia's blockchain landscape

RWA.xyz has stablecoins at about $295.6B, with USDT and USDC still around $271B of that, so a KRW coin is fighting dollar network effects before it fights other Korean issuers. The Bank of Korea's bank-only preference is the chokepoint: deposit-token wrappers inside KB/Shinhan/Hana rails would be clean but boring, while a license path for Kakao, Naver Pay, Toss, Upbit/Bithumb-style distribution could turn Korea's retail liquidity premium into actual settlement collateral. Watch whether these assets get DeFi-grade portability and RWA redemption hooks, or just another permissioned wallet balance with a blockchain logo.

Readers click RWA hardest when institutional branding (BlackRock, Ondo, Ethena) attaches a concrete yield number to the product — but their second-tier engagement on governance fights, oracle gaps, and 80%-APY red flags reveals they are simultaneously testing whether the TradFi wrapper actually changes the underlying risk or just the marketing copy.↗

2. Defining Real-World Assets and Tokenization

2.1 From Physical Assets to Blockchain Tokens

In crypto, “real-world assets” usually refers to digital tokens issued on a blockchain that represent claims on offchain assets or cash flows. These might be traditional financial instruments—such as fiat currencies, commodities, equities, corporate or sovereign bonds—or non-financial assets such as real estate, invoices, intellectual property, or insurance-linked securities. The unifying idea is that the token is not purely native to the blockchain like ETH or SOL; instead, it references an external asset and is structured so that tokenholders have some form of economic and often legal claim to that underlying exposure.

Tokenization is the process of converting the ownership rights, or at least certain rights, associated with these assets into digital tokens. In practice, this involves both legal structuring offchain and technical implementation onchain. On the legal side, issuers may form special-purpose vehicles (SPVs), trusts, or regulated funds that hold the underlying assets on behalf of tokenholders and define their rights in offering documents and contracts. On the technical side, smart contracts encode the token’s supply, transfer rules, and interfaces with other protocols. The goal is to create a digital representation that can be programmatically transferred, used as collateral, fractionally owned, and integrated into DeFi while preserving a verifiable relationship with the assets held offchain.

From an economic perspective, RWAs typically fall into two broad buckets. Some are tokenized forms of existing instruments, such as shares in a bond fund or units of a money market vehicle. Others are new structures that use traditional instruments as collateral but issue tokens with novel payoff profiles or governance features. For instance, a token might represent a tranche of a collateralized loan obligation (CLO) that bundles multiple credit exposures, or it might represent a participation in a reinsurance program that passes through insurance premiums and losses. In both cases, the token serves as an access point to risk and return streams that would otherwise remain in opaque or restricted markets.

Chainlink’s educational materials highlight that RWAs can encompass cash, commodities, equities, bonds, credit, artwork, and intellectual property, among other categories. Huma Finance, a protocol focused on income-backed RWAs, emphasizes that tokenization is essentially about digitizing ownership rights and making them programmable and interoperable across the blockchain ecosystem. Academic work has started to formalize these ideas, proposing taxonomies that classify tokenized RWAs by the nature of the claim, the degree of decentralization in control, and how value is transferred between onchain and offchain environments.

2.2 RWAs versus Native Crypto and Synthetic Exposure

It is important to distinguish RWAs from both native crypto assets and synthetic instruments. Native assets such as ETH, BTC, or SOL exist only onchain and are secured by the consensus rules of their networks. Their value arises from network effects, utility, monetary narratives, and speculation, but there is no offchain collateral backing them. RWAs, by contrast, are explicitly backed by external assets held in custody, like U.S. Treasuries, real estate, or corporate equity. The economic risk and return of an RWA token is tied to the performance and legal status of those assets and the entities that administer them.

Synthetic exposure, such as a synthetic stock or a mirrored asset, may track the price of an offchain asset without being legally or economically backed by that asset. For example, a DeFi protocol might build perpetual futures on a stock index using crypto collateral and oracle price feeds. Traders get exposure to the index’s price movements but have no claim on the underlying stocks themselves. RWAs aim to be more than synthetics; their tokenholders generally have contractual rights to income, redemption, or liquidation proceeds from specific asset pools, subject to regulatory structures and offering documents.

The distinction matters for both risk and regulation. Synthetic assets depend primarily on the solvency and risk management of the protocol that issues them. RWAs depend on a chain of trust that includes custodians, trustees, servicers, and auditors in the traditional financial system, plus the smart contracts and oracles that mirror that chain onchain. When evaluating RWAs, crypto users therefore have to think not just like DeFi natives reading contract audits, but also like fixed-income or structured finance analysts reviewing disclosures and legal frameworks.

2.3 A Taxonomy of Tokenized RWAs

Academic work has started to systematize the diverse landscape of RWA projects. A recent taxonomy of RWA tokenization on blockchains proposes analyzing tokenized assets across three planes: the legal layer (what rights are encoded in law), the economic layer (what cash flows and risks the token represents), and the technical layer (how those rights and flows are implemented in code and infrastructure). This approach is helpful for cutting through marketing language and understanding what a token actually is.

At the legal layer, tokenized RWAs can range from simple depositary receipts—digitally representing shares or fund units held at a custodian—to more complex structures in which tokens represent limited partnership interests, profit-sharing rights, or claims on securitized pools. Some tokens are issued under securities regulations, with KYC and accreditation checks. Others seek to rely on exemptions or novel legal constructs, raising questions about enforceability in edge cases. The degree of “onchain-ness” at this layer can be measured by how directly tokenholder rights are articulated and whether they are recognized across jurisdictions.

At the economic layer, RWAs can be classified by the underlying asset class (sovereign debt, corporate credit, real estate, commodities, equities, insurance-linked securities) and the structure of risk transfer. For example, a token might correspond to a senior note in a pool of loans, absorbing minimal credit risk but also receiving lower yield, or it might be an equity tranche that takes first loss but earns higher returns if the portfolio performs. Yield-bearing stablecoins backed by Treasuries fall at one end of the spectrum; complex structured products like CLO tranches or reinsurance-linked securities sit at the other.

At the technical layer, the taxonomy covers aspects such as token standards (fungible versus non-fungible, ERC‑20 versus bespoke standards), permissioning (open versus whitelisted transfers), oracle design (how offchain data about reserves and valuations is brought onchain), and cross-chain interoperability. Some issuers rely on public blockchains only; others use permissioned networks or hybrid architectures. Chainlink, for example, describes RWA tokenization flows that rely on decentralized oracle networks for real-time reserve verification and cross-chain messaging for bridging tokenized assets across ecosystems. Hedera, a hashgraph-based network, presents its infrastructure as a one-stop platform for tokenizing both digital and real-world assets at scale, with predictable fees and compliance features integrated into its token service.

This layered taxonomy underscores that “RWA” is not a single monolithic category. Instead, it is a spectrum of designs that trade off decentralization, regulatory certainty, liquidity, and capital efficiency. For crypto participants, the challenge is to read past the acronym and understand where a given token sits along each of these dimensions.

3. The Tokenization Lifecycle: How RWAs Go Onchain

3.1 Asset Selection and Legal Structuring

Any RWA project begins offchain with asset selection. Issuers must decide which asset class to target, how to source it, and which investors to serve. Popular starting points include highly liquid, low-credit-risk instruments such as U.S. Treasuries, money market fund shares, and investment-grade bonds, which lend themselves well to tokenized cash management products. Other projects focus on higher-yielding but less liquid asset classes such as private credit, trade finance, or real estate, hoping to attract investors willing to trade liquidity for yield.

Once a target asset class is chosen, structuring becomes a legal and regulatory exercise. Issuers often create SPVs or dedicated funds to hold the underlying assets. These vehicles can be domiciled in jurisdictions with favorable securities and fund regulations, and they issue claims—shares, notes, partnership interests—that correspond to the assets they hold. The RWA tokens are then designed to represent those claims, either directly or via additional layers. Legal documentation specifies redemption rights, priority in liquidation, distribution of income, and the obligations of custodians and trustees. For stablecoin-like RWAs backed by Treasuries or money market instruments, documents also define how reserves are invested, what happens in stress scenarios, and how quickly tokens can be redeemed for fiat.

Regulatory compliance is deeply intertwined with structuring. Depending on the jurisdiction and the nature of the assets and investors, issuers may need to register securities, rely on exemptions, or restrict offerings to accredited or institutional investors. Many tokenized securities today are limited to qualified investors, even if the tokens themselves live on public chains. On the other hand, fiat-redeemable stablecoins such as USDC are structured under payments and money-transmission frameworks, with cash and cash-equivalent reserves held at regulated financial institutions and subject to specific disclosure regimes. The RWA label, in other words, covers both securities-like and money-like instruments, each with distinct legal architectures.

3.2 Token Design, Standards, and Tokenomics

Onchain, the RWA manifests as one or more smart contracts that define the token’s behavior. Basic design choices include whether the token is fungible or non-fungible, the token standard used (such as ERC‑20 or ERC‑721 on Ethereum), and whether transferability is permissioned. Fungible tokens are common for exposures that resemble shares or fund units, where each unit is interchangeable. Non-fungible tokens may be used for unique assets, such as specific real estate parcels or individual invoices.

Tokenomics for RWAs differ from purely native DeFi tokens. For tokens that represent direct claims on underlying assets—such as tokenized Treasuries or RWA stablecoins—the supply is generally intended to expand or contract in line with deposits and redemptions. Fees are often charged as management or spread fees at the fund level, rather than via inflationary token issuance. Governance tokens may sit alongside these RWA tokens, accruing value through protocol fees, voting rights, or profit-sharing arrangements, but the RWA itself is typically designed to behave more like a traditional instrument than like a speculative governance token.

Some protocols integrate RWAs into more complex token-economic systems. For instance, onchain asset managers might issue vault tokens that represent shares in a diversified portfolio of RWAs and DeFi strategies, with performance fees paid in a governance token. Collateralized lending platforms such as Maple Finance create pools where institutional borrowers take loans backed by RWAs or their cash flows, and lenders receive interest-bearing tokens that represent their shares of the pool. In such designs, the line between pure RWA exposure and protocol-native risk becomes blurred. Users must understand both the quality of underlying assets and the protocol’s risk-sharing mechanisms.

A particularly important design axis is how yield is handled. For RWA-backed products that invest in yield-bearing instruments like Treasuries, the yield may be reflected in the token’s price (for example, by allowing it to appreciate relative to a stable reference) or in its quantity (by increasing balances through rebasing or reward distributions). Each approach has different implications for how the token interacts with DeFi protocols and how taxable events are recognized in various jurisdictions. Yield-sharing arrangements also define how much of the underlying real-world yield flows to tokenholders versus being retained by the issuer or protocol, a key factor in evaluating whether an RWA product offers fair value.

3.3 Blockchain Selection, Oracles, and Cross-Chain Interoperability

Issuers must also choose which blockchain to use and how to connect onchain tokens to offchain data. Public networks such as Ethereum, Solana, and emerging L1s and L2s offer composability with DeFi ecosystems, while permissioned or enterprise-focused networks may offer finer-grained control over compliance and privacy. Hedera, for example, positions itself as an enterprise-ready network for tokenizing real-world and digital assets, emphasizing predictable fees, built-in compliance features, and an “asset tokenization studio” that lets issuers launch regulated tokens, including RWAs and stablecoins, in minutes.

Oracle infrastructure is another pillar of the tokenization lifecycle. Most RWAs require reliable feeds about the status and value of underlying assets, whether that is the total amount of Treasuries and cash held in reserve, the mark-to-market price of a portfolio, or the occurrence of real-world events such as defaults or insurance losses. Chainlink describes patterns in which decentralized oracle networks connect RWA tokens to offchain data providers and custodians, enabling proof-of-reserves feeds that periodically or continuously attest to the backing of the tokens. Its Proof of Reserve product is designed to verify that collateral balances held by custodians match or exceed the supply of tokens, enhancing transparency and reducing reliance on opaque attestations.

Cross-chain interoperability is increasingly important as RWA activity expands beyond a single chain. Chainlink’s Cross-Chain Interoperability Protocol (CCIP), for example, is marketed as a way to make tokenized RWAs available on multiple blockchains by enabling secure cross-chain messaging and token transfers. In practice, issuers may deploy canonical RWA tokens on one chain and use bridging mechanisms to create representations on others, or they may issue native tokens on multiple chains backed by a shared offchain asset pool. Each approach introduces its own trust and risk assumptions. For investors, understanding which token is legally and economically “primary”, and how cross-chain representations are managed, is crucial.

3.4 The Audit and Proof-of-Reserves Chain

Because RWAs rely on offchain assets, ongoing assurance about backing and operations is essential. This has given rise to what can be thought of as an “audit chain” parallel to the blockchain itself. Traditional auditors and administrators review custodial statements, portfolio holdings, and cash flows, issuing periodic reports. Meanwhile, onchain proof-of-reserve systems aim to bring a cryptographically verifiable version of those assurances into the DeFi environment.

Chainlink’s Proof of Reserve feeds are a leading example. They periodically query data from custodians or trusted data providers—such as the total face value of U.S. Treasuries held in a specific account or the net asset value of a fund—and publish those values to smart contracts onchain. DeFi protocols can then set risk controls that reference these feeds, such as halting minting if reserves fall below a threshold or pausing certain operations if a discrepancy is detected. This creates an automated circuit breaker layer that complements human oversight and regulatory supervision.

Beyond proof-of-reserves, some projects are exploring richer “audit-proof” lifecycles in which every step of the tokenization process—from asset acquisition and valuation to interest payments and redemptions—is tied into verifiable data trails. These may link accounting systems, custody platforms, oracles, and protocol smart contracts in near real time. The vision is a world where investors can query not just the existence of reserves, but also their composition, maturity profile, and exposure to various risks, using onchain analytics and open data. While this vision is not fully realized, the direction is clear: RWAs are pushing both traditional audit practices and blockchain transparency tools toward deeper integration.

- 01institutional yield product launches↗

The top headline by a wide margin — MANTRA + Ondo's USDY vault — shows readers are drawn to any product that pairs a named TradFi yield instrument with an accessible DeFi interface, especially when a recognizable issuer backstops the rate.

- 02TradFi giants tokenizing assets

BlackRock's $500M fund, Deutsche Bank's report, Securitize funding, and the Robinhood SEC proposal collectively signal that readers track institutional entry as a legitimacy signal — each new TradFi name is treated as a milestone for the whole sector.

- 03RWA looping and carry-trade leverage↗

Headlines about RWA collateral driving ~30% of Ethereum lending and Drift's RWA margin on Solana pulled readers who recognized that RWA is quietly becoming the fuel for leveraged DeFi strategies, not just a passive yield sleeve.

- 04governance battles over RWA integration

Marc Zeller's public fight against the Horizon RWA proposal and Ethena's reserve overhaul debate attracted readers who understand that the real contest is which protocol captures the RWA yield flywheel — and who gets to set the terms.

- 05offchain oracle and data integrity risk↗

The headline about private credit's systemic data gap — offchain inputs driving onchain logic — alongside MakerDAO's new RWA oracle via M^0 revealed readers are tracking the single weakest link in the RWA stack: the trust boundary between the real world and the chain.

- 06fake RWA yield red flags↗

Anzen's 80% APY 'RWA stablecoin' and the RealT 'slumlording' investigation showed readers are actively pattern-matching against past DeFi blowups — high advertised yields on RWA wrappers trigger the same skepticism as algorithmic stablecoin promises.

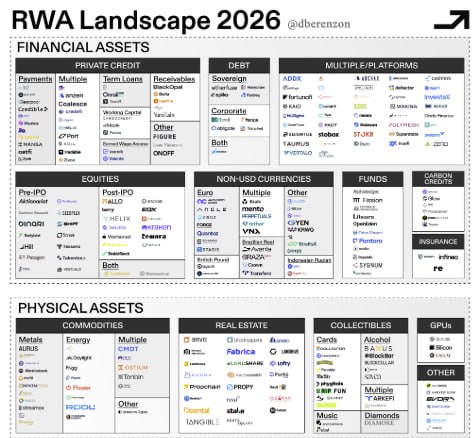

4. The RWA Market Landscape

4.1 Measuring the Market: Size and Chain Distribution

Quantifying the RWA market is challenging because definitions vary and the space is evolving quickly. However, multiple data providers and commentators suggest that the total value of tokenized RWAs—excluding purely fiat-backed stablecoins—has climbed into the tens of billions of dollars. Social data and analytics indicate that roughly 43 billion dollars of value is already locked in RWA-related assets onchain, with Ethereum controlling close to 58 percent of that market. While the exact figures fluctuate with prices and inflows, the key point is that RWAs have grown from an experiment into a material segment of the crypto economy.

RWA-focused analytics platforms such as RWA.xyz aggregate data across issuers, asset types, and blockchains, giving a granular view of the ecosystem. Their dashboards track tokenized Treasuries, corporate bonds, real estate, private credit, and more, along with metrics such as total value, yield, and chain distribution. A dedicated dashboard for tokenized U.S. Treasuries, for example, shows more than 15 billion dollars in tokenized U.S. government debt instruments across multiple providers and chains, highlighting the scale of onchain fixed-income adoption. These data sources provide crucial context for understanding where growth is concentrated and how different asset classes are being adopted.

The market is not evenly distributed across chains. Ethereum remains the primary settlement layer for many institutional-grade tokenization efforts, leveraging its security, tooling, and established DeFi ecosystem. However, other chains are gaining significant traction, especially for high-throughput use cases and retail-oriented platforms. Solana, for instance, has seen notable growth in USDC circulation and RWA-related activity, partly driven by tokenized stocks and ETFs, tokenized CLO funds, and reinsurance-linked securities deployed on its high-performance infrastructure. Networks like Hedera position themselves as enterprise rails for tokenization, while newer L1s and L2s such as Aptos and Mantle are actively courting RWA builders with grants and dedicated research programs.

As the market matures, the analytic stack around RWAs is also becoming more sophisticated. In addition to RWA.xyz, general-purpose analytics platforms like Token Terminal have launched redesigned dashboards focused on stablecoin and RWA issuers, giving investors deeper insight into product mixes, chain footprints, and market share. Combined with protocol-level disclosures and proof-of-reserve feeds, this data-rich environment is gradually making RWA markets more legible to crypto-native investors who are used to real-time transparency in DeFi.

4.2 Tokenized Treasuries and Fixed Income

Tokenized fixed income is one of the most mature and straightforward RWA segments. In these products, issuers acquire U.S. Treasuries or Treasury-focused money market funds and issue tokens that represent fractional interests in the underlying instruments. The appeal is clear: investors get access to short-duration, high-credit-quality yield instruments via wallets and smart contracts, without needing brokerage accounts or traditional fund platforms.

RWA.xyz’s treasuries dashboard illustrates the breadth of this space, listing multiple issuers and products that collectively account for over 15 billion dollars in tokenized U.S. government debt. Some tokens are structured as fund shares; others resemble tokenized notes or depositary receipts. The tokens may be redeemable for fiat, stablecoins, or other onchain assets depending on the issuer’s infrastructure. Yield is typically passed through in the form of appreciation in token price or periodic distributions, reflecting the coupons and reinvestment returns on the underlying Treasuries.

This segment also intersects strongly with stablecoins. Transak, for example, highlights “RWA stablecoins” as tokens backed by productive, yield-generating offchain assets such as U.S. Treasuries, gold, or money market funds, rather than by fiat deposits alone. These instruments bridge traditional interest-bearing assets and onchain programmability, effectively importing the risk-free rate into DeFi. Protocols and DAOs can park treasury assets in tokenized Treasury products, using them as collateral in lending protocols or as yield-generating reserves for their stablecoins and governance tokens. In many ways, tokenized fixed income has become the backbone of “onchain cash management.”

At the same time, tokenized fixed income raises nuanced questions about duration risk, liquidity, and redemption mechanics. If interest rates rise, the mark-to-market value of longer-duration Treasuries falls; if investors treat tokenized Treasuries as stable cash equivalents without understanding this, they may be surprised by price volatility. Similarly, if token liquidity is thin on certain chains or venues, exiting positions quickly in stress scenarios may be difficult. Investors therefore need to grasp not just the blockchain layer, but also the underlying bond math and fund structures.

4.3 Tokenized Equities, ETFs, and Perpetual Markets

Beyond fixed income, equities and ETFs are increasingly being tokenized and traded onchain. One model uses fully backed spot tokens that represent fractional shares in underlying stocks or funds held by a licensed custodian. Users can buy and sell these tokens, sometimes with rights to redeem for the underlying or for cash. Exodus and Ondo, for instance, have launched a tokenized trading platform on Solana that offers access to over 200 tokenized stocks, ETFs, and RWAs via a self-custodial wallet interface. Exodus was among the first publicly traded companies to tokenize its own stock, setting an early precedent for equity tokenization.

Another model focuses on derivatives. Orderly Network, an orderbook-based trading infrastructure, has emerged as a leading venue for RWA-related perpetual futures. It supports more than 30 RWA markets, a figure that exceeds many other perp DEXs, and has been actively listing new single-name equity perps. Recent additions include tokens referencing companies such as Apple, Amazon, Microsoft, Samsung, and others, allowing traders to go long or short these names entirely onchain. In prior coverage, Orderly-linked venues have also listed perps on names like Coinbase and other public companies, giving DeFi users ways to bet on exchange stocks or specific sectors without leaving crypto.

These perpetual markets do not necessarily confer legal ownership of the underlying equities; instead, they provide synthetic exposure via funding-rate-based derivatives, collateralized by crypto assets. Yet they are part of the broader RWA story, because they are enabled by the same infrastructure improvements—reliable price oracles, compliant custody models, and growing comfort with linking TradFi reference assets to onchain instruments. They also showcase how RWAs can reshape trading: a crypto user can now express a view on an Apple–Intel hardware announcement by trading an AAPL or INTC perp on a DeFi venue, or hedge exposure to tech stocks alongside ETH and BTC in a unified, 24/7 portfolio.

Equity and ETF tokenization is still early and faces significant regulatory complexity, particularly around investor protections and market integrity. However, the trajectory is clear. As more platforms like Exodus/Ondo, Enso-integrated wallets, and Aptos-based orderbook projects bring traditional equities onchain, the distinction between “crypto markets” and “equity markets” is likely to become increasingly blurred. For crypto-native traders, this means RWAs could eventually make onchain venues competitive with traditional brokerages in product breadth while retaining the programmability and composability of DeFi.

4.4 Private Credit, CLOs, and Onchain Asset Managers

Private credit and structured credit products are another fast-growing RWA vertical. Maple Finance, for example, offers onchain asset management and permissioned lending markets tailored to sophisticated allocators. Its platform enables the creation of lending pools that provide secured loans to institutions, often backed by real-world collateral or operating cash flows. Investors deposit into these pools and receive interest-bearing tokens that track their share of principal and interest, effectively turning private credit strategies into programmable DeFi instruments.

More recently, tokenized CLOs have begun to appear on public chains. Ethena Labs has announced plans to deploy 250 million dollars into a tokenized AAA-rated CLO fund arranged by Securitize and expanded on Solana, signaling substantial institutional participation in structured credit RWAs. CLO structures bundle pools of leveraged loans and tranche them by risk, with the AAA tranches sitting at the top of the waterfall and absorbing losses only after more junior tranches are wiped out. Tokenizing such instruments allows onchain investors to access institutional-grade credit exposures that were previously confined to specialized funds and large allocators.

These developments illustrate both the promise and the complexity of RWA-based private credit. On one hand, tokenization can democratize access, enhance transparency, and potentially improve liquidity for traditionally illiquid instruments. On the other, the risks—ranging from borrower defaults to servicing failures and structuring errors—are nontrivial and often hard for retail investors to evaluate. The interplay between protocol-level governance and traditional credit risk management becomes crucial: a well-designed DeFi front end cannot compensate for poor underwriting or opaque loan documentation.

The growth of onchain asset managers and RWA platforms is increasingly supported by specialized data infrastructure. Inveniam Capital Partners, for example, is a data infrastructure company that has deepened its RWA bet by planning to acquire Mantra, a layer‑1 blockchain focused on tokenized real-world assets and digital private market infrastructure. This kind of vertical integration—combining data, valuation tools, and a dedicated chain—reflects demand for better reporting, pricing, and compliance capabilities as institutional allocators engage with tokenized private markets. The result is a crowded but increasingly sophisticated landscape of RWA credit platforms, chain-native asset managers, and institutional partners.

4.5 Novel Segments: Real Estate, Reinsurance, and Beyond

While fixed income, equities, and private credit get much of the attention, RWAs extend into more niche but potentially high-impact segments. Real estate tokenization has been a longstanding theme, though it remains fragmented and often localized due to regulatory and operational complexity. More recently, insurance-linked securities and reinsurance risk have emerged as promising candidates for tokenization. SurancePlus, a subsidiary of Oxbridge Re, has launched tokenized securities on Solana that give accredited investors direct exposure to a named reinsurance program associated with HCI Group’s Fortex Re program. These tokens allow investors to participate in reinsurance returns, effectively taking on insurance risk in exchange for premium income.

Tokenized reinsurance RWAs highlight how blockchain can open access to risk pools that were historically available only to specialized institutional investors or via niche funds. They also illustrate the importance of oracles for non-price events: payouts often depend on the occurrence and severity of insured events such as hurricanes or natural disasters, which must be verified and reflected onchain. For crypto-native investors, such products offer diversification away from traditional equity and credit cycles, but they also demand a strong understanding of event risk and modeling uncertainty.

Other emerging RWA categories include tokenized carbon credits, intellectual property royalties, invoice factoring, and even exotic exposures like litigation finance. While not all of these have reached scale, the pattern is consistent: wherever there is a cash flow that can be contractually defined and tied to real-world events, there is potential for tokenization. The limiting factors are legal enforceability, regulatory appetite, and investor demand, not technical capability. With L1s like Hedera emphasizing tokenization use cases and platforms like RWA.xyz cataloging new launches, the long tail of RWAs is likely to keep expanding.

To summarize the current RWA landscape, it is useful to visualize major segments and examples:

| Segment | Typical Underlying Assets | Example Onchain Implementations / Themes |

|---|---|---|

| Cash & Short-Term Debt | U.S. Treasuries, money market funds, commercial paper | Tokenized Treasuries, RWA stablecoins with Treasury backing |

| Stablecoins | Cash, cash equivalents, short-term government debt | USDC reserves, RWA-backed stablecoins earning real-world yield |

| Equities & ETFs | Public company shares, index funds | Tokenized stocks and ETFs on Solana; equity perps on Orderly and other DEXs |

| Private & Structured Credit | Private loans, leveraged loans, CLO tranches | Maple Finance lending pools; tokenized AAA CLO fund on Solana |

| Real Estate | Residential and commercial property | Fractional property tokens (various early-stage platforms) |

| Insurance & Reinsurance | Catastrophe bonds, reinsurance programs | Tokenized reinsurance risk via SurancePlus on Solana |

| Other RWAs | Commodities, carbon credits, IP, invoices, royalties | Emerging pilots and niche platforms across Ethereum, Solana, and enterprise chains |

This table is not exhaustive, but it underscores how RWAs are beginning to cover the full spectrum of traditional financial and real-economy assets.

KDDI and Securitize Japan sign pact to explore RWA tokenization for 30M-plus customer base

KDDI and Securitize Japan signed a June 22, 2026 basic agreement to explore blockchain-based financial services, including Securitize-powered RWA tokenization and new tokenized investment products. The distribution angle is the story: KDDI brings 30M-plus customers, au Jibun Bank and au PAY touchpoints, and a Coincheck wallet push, while Securitize brings its Japan security-token platform and $4B-plus global RWA AUM.

5. RWA Stablecoins, Yield, and Capital Markets Design

5.1 From Fiat-Backed to RWA-Backed Stablecoins

Stablecoins were the earliest and most impactful form of tokenized offchain assets, though they are not always labeled as RWAs. Fiat-backed stablecoins such as USDC are digital tokens redeemable at par for fiat currency, backed by reserves consisting of cash and cash-equivalent assets held by regulated financial institutions. Circle, the issuer of USDC, describes the token as a “digital dollar” backed 100 percent by highly liquid cash and cash-equivalent assets and redeemable one-to-one for U.S. dollars. In practice, this means that a substantial portion of USDC reserves resides in short-dated U.S. Treasuries and similar instruments, even if users primarily experience USDC as a cash-like medium of exchange.

RWA stablecoins, as discussed by Transak and others, go a step further by explicitly structuring the backing to include productive, yield-generating assets such as U.S. Treasuries, gold, or money market funds. Instead of simply holding cash deposits, these stablecoins hold portfolios that earn interest in the traditional economy. The token then represents a verifiable claim on that portfolio, governed by legal and regulatory frameworks that define custody, redemption, and yield-sharing mechanisms. In essence, RWA stablecoins transform the base layer of DeFi “cash” into an interest-bearing asset class.

The difference between fiat-backed and RWA-backed stablecoins can be understood along two axes: transparency and yield distribution. Fiat-backed stablecoins like USDC have moved toward increasing transparency via regular attestations and detailed reserve reports, but they typically do not pass through yield to tokenholders; instead, the issuer earns the spread between reserve returns and operating costs. RWA stablecoins, by contrast, are frequently marketed as yield-sharing instruments that explicitly promise tokenholders some portion of the underlying portfolio’s returns, subject to fees and risk sharing. This design has profound implications for how stablecoins function in DeFi and how they are treated under securities and investment laws.

5.2 USDC and the Role of Cash-Equivalent Reserves

USDC is a useful reference point because it sits at the intersection of traditional finance, stablecoins, and RWAs. Circle’s disclosures emphasize that USDC is backed by cash and cash-equivalent assets, including U.S. Treasuries and similar high-quality instruments, held in segregated accounts and managed by regulated financial institutions. This reserve model is designed to support 1:1 redemption, maintain liquidity under stress, and satisfy regulatory requirements, while also allowing Circle to earn interest income on the underlying assets.

In practice, this makes USDC a hybrid of RWA exposure and digital cash. On one level, USDC behaves as a stable, onchain dollar used for trading, payments, and DeFi liquidity. On another level, USDC represents indirect exposure to a portfolio of short-term U.S. government debt and cash, albeit without a direct claim to the underlying assets beyond the redemption promise. When USDC supply grows, demand for these underlying RWAs grows; when it shrinks, reserves are unwound, feeding back into traditional money markets.

On chains like Solana, USDC has become a foundational asset for RWA ecosystems, enabling dollar-denominated pricing and liquidity for tokenized Treasuries, stocks, CLOs, and reinsurance products. The growth of USDC mints and onchain RWA products is mutually reinforcing: as more RWA strategies offer yield relative to stablecoins, users are incentivized to hold and deploy USDC; as USDC supply expands, more capital is available to flow into RWA issuers and protocols. This dynamic positions large fiat-backed stablecoins as key intermediaries in the RWA economy, even when they themselves are not structured as explicit RWA yield tokens.

5.3 Yield Generation and Distribution

Yield is the main attraction of many RWA products. By tokenizing assets that earn interest or other income in traditional markets—such as Treasuries, corporate bonds, private loans, or reinsurance premiums—protocols can offer onchain instruments that provide “real yield” funded by offchain economic activity. This stands in contrast to earlier DeFi cycles in which much of the advertised yield came from liquidity mining or token emissions, effectively reshuffling existing value rather than tapping new sources.

Transak emphasizes that RWA stablecoins represent productive assets from the traditional economy and therefore bring regulated yield and institutional-grade transparency onchain. Tokenholders effectively gain access to returns generated by the underlying portfolio, subject to management fees and risk provisions, while benefiting from the programmability and liquidity of blockchain-based tokens. In practice, this might mean a stablecoin that gradually appreciates against a reference unit, a tokenized fund share whose net asset value accrues yield daily, or a rebasing token whose balances increase as interest is earned.

More complex RWA yield strategies combine multiple layers. A DAO treasury might allocate a portion of its reserves into tokenized Treasury products, receive yield-bearing tokens in return, and then deposit those tokens into DeFi protocols that accept them as collateral. Platforms like Pendle have built fixed- and variable-rate markets around yield-bearing tokens, including those backed by RWAs, allowing users to separate and trade interest-rate exposure over time. Other protocols introduce pre-mint mechanisms or structured products that front-load access to RWA-backed yield before native staking or redemption mechanisms are live, as seen in experimental “pre-mint” offerings built around RWA strategies in recent coverage.

Yield distribution models also intersect with tokenomics for protocol governance tokens. For example, if an RWA platform earns a spread between gross portfolio yield and net yield paid to tokenholders, that spread can be allocated to a treasury, used for buybacks, or distributed as rewards to governance token stakers. Over time, this could turn governance tokens into pseudo-equity claims on RWA businesses, an idea that has attracted attention from both DeFi investors and traditional institutions. Standard Chartered’s research, for instance, has cited the growing adoption of tokenized RWAs and DeFi as a factor that could benefit protocols like Uniswap, highlighting how fee-generating RWA activity may accrue value to core DeFi infrastructure.

5.4 How RWAs Reshape DeFi Tokenomics

The integration of RWAs into DeFi is altering tokenomics design in several ways. First, RWAs provide a robust baseline yield that protocols can tap into without relying on unsustainable emissions. Instead of paying users to provide liquidity with governance tokens, protocols can direct underlying capital into RWA strategies and share the resulting real-world yield. This can make liquidity provisioning more self-sustaining and reduce sell pressure on governance tokens.

Second, RWAs introduce new collateral types and risk profiles into lending and derivatives markets. Tokenized Treasuries, for instance, can serve as relatively low-risk collateral, enabling borrowers to leverage their positions while still earning underlying yield. Private credit RWAs allow protocols to lend against real-world cash flows, potentially generating higher returns but also exposing users to credit and liquidity risk. These dynamics require careful calibration of interest rates, loan-to-value ratios, and liquidation mechanisms, all of which feed back into protocol tokenomics by dictating protocol revenue and default risk.

Third, RWAs may push DeFi toward more explicit and regulated revenue-sharing models. If a protocol is intermediating securities-like RWAs or earning fees on regulated products, regulators may scrutinize how governance tokens are marketed and whether they confer rights similar to equity or profit-sharing claims. This could lead to more conservative tokenomics—fewer wild emissions, more emphasis on real cash flows, and clearer separation between utility and investment characteristics. At the same time, it could make DeFi projects more legible to traditional investors who are accustomed to evaluating businesses based on earnings and cash flow multiples.

Finally, RWAs and stablecoins are accelerating multi-chain and cross-ecosystem liquidity dynamics. As RWA issuers expand onto multiple chains, they must decide where to concentrate liquidity and how to manage cross-chain representations. DeFi protocols that serve as primary liquidity venues for RWA tokens may benefit from fee flows and network effects; their tokens, in turn, may correlate with the growth of RWA volumes. This creates a feedback loop where tokenomics, RWA adoption, and cross-chain infrastructure all reinforce each other.

- 2023-08launch

Tron launches stUSDT, a yield-bearing RWA-backed stablecoin

CoinGecko Q3 report: tokenized T-bills reach $665M on-chain

- 2023-10launch

Frax launches SFRAX, surpasses $20M supply at ~10% APY

- 2024-03launch

BlackRock launches BUIDL tokenized money market fund on Ethereum

- 2024-08milestone

BlackRock leads $47M funding round for Securitize tokenization platform

RWA TVL surpasses $10B per DeFiLlama; government securities dominate

- 2025-04regulatory

Robinhood files 42-page SEC proposal for federal RWA token legal framework

Ethena deploys $250M into Securitize tokenized AAA CLO fund on Solana

6. Institutional Adoption and Infrastructure

6.1 Banks, Asset Managers, and Regulated Issuers

One of the defining features of the current RWA cycle is the depth of institutional participation. Major banks, asset managers, and regulated financial institutions have moved from pilot projects to live tokenized offerings. Standard Chartered, for example, has published research forecasting that as RWAs and DeFi adoption grow, protocols central to onchain liquidity and price discovery could see substantial increases in value, with Uniswap cited as a key beneficiary. This kind of analysis reflects a view that tokenization is not just a side experiment, but a structural change in how capital markets will operate.

On the asset-management side, firms like Securitize have been instrumental in structuring tokenized funds across multiple asset classes, including CLOs and other credit exposures. Ethena Labs’ decision to deploy 250 million dollars into a Securitize-managed tokenized AAA CLO fund on Solana underscores how institutional-scale capital is beginning to flow into tokenized structured products. Centralized exchanges such as Bybit have rolled out RWA Earn products featuring tokenized bond funds from established managers like PIMCO and CMBI, making institutional-grade fixed income accessible via exchange interfaces to eligible users.

Traditional market infrastructure is also adapting. Custodians and trustees are developing support for tokenized securities models. Transfer agents are exploring onchain registries. Inveniam’s planned acquisition of Mantra, a blockchain designed for tokenized RWAs and digital private markets, is emblematic of this convergence: a data and valuation infrastructure company fusing with a base-layer chain to serve the end-to-end needs of institutional tokenization. As these initiatives scale, the distinction between “crypto-native” and “traditionally regulated” issuers is likely to blur, with hybrid entities operating across both domains.

6.2 Protocol and Middleware Infrastructure

Beneath the surface of headline-grabbing tokenized funds and stock listings lies a growing stack of infrastructure providers. Oracle networks like Chainlink play a key role in connecting offchain data to onchain contracts, providing price feeds, reserve attestations, and cross-chain messaging for RWAs. Their Proof of Reserve and CCIP products are pitched specifically at RWA implementations, promising real-time transparency and cross-chain liquidity without sacrificing security. For RWA issuers, this infrastructure reduces the need to build bespoke data pipelines and lowers the barrier to multi-chain expansion.

Enterprise and public blockchains are positioning themselves as tokenization hubs. Hedera offers an “asset tokenization studio” designed to let developers and enterprises launch regulated assets, stablecoins, and other tokens with built-in compliance controls, predictable fees, and scalable throughput. Its marketing emphasizes that tokenization should not take months of bespoke development and legal negotiation, but can instead be standardized and accelerated using reusable frameworks. Other chains, such as Aptos, are highlighting full-stack infrastructure for capital markets, including orderbook DEXs, equity perps, and RWA issuance by regulated institutions, signaling a strategy focused on marrying high-performance execution with real-world assets.

Middleware protocols like Fluid, which traces roots back to Instadapp, are emerging as generalized infrastructure for onchain financial products. They provide toolkits to launch lending markets, DEXs, and liquidity solutions for stablecoins and RWAs, serving both institutions and DeFi protocols. Grants and research programs from ecosystems such as Mantle and Stacks, which invite builders exploring RWAs, onchain equities, and new financial primitives, reflect a broader recognition that tokenization is now a core DeFi theme rather than a niche.

6.3 Centralized Exchanges and RWA Earn Products

Centralized exchanges (CEXs) have also become distribution channels for RWAs, often targeting users who value the simplicity of exchange interfaces but want access to tokenized institutional products. Bybit’s RWA Earn offerings, which feature tokenized bond funds from established managers, provide one example of how exchanges can package RWAs into savings-style products. Users subscribe using crypto or stablecoins and receive yield-pooling tokens or account credits that reflect exposure to underlying bond portfolios, abstracting away the complexities of custody and legal structuring.

CEX involvement in RWAs can be viewed as a bridge between pure DeFi and traditional brokerage. On the one hand, exchanges may custody tokenized securities in omnibus accounts and offer users synthetic balances, similar to how they handle spot crypto. On the other, some exchanges integrate directly with onchain protocols, using RWA tokens as underlying building blocks for structured products. As regulatory clarity improves, it is plausible that exchanges will expand their RWA offerings to include tokenized equities, ETFs, real estate funds, and more, all accessible to users via familiar Earn and trading interfaces.

For crypto users, the key trade-off is control versus convenience. Self-custodial platforms like Exodus/Ondo and decentralized venues like Orderly-powered DEXs allow users to hold RWA exposures in their own wallets and integrate them into broader DeFi strategies. CEX-based RWA products, while convenient, reintroduce counterparty risk. As the RWA ecosystem grows, users will likely see an expanding menu of options along this spectrum, from fully self-custodied onchain exposure to curated RWA baskets and yield products offered by centralized platforms.

7. Using RWAs as a Crypto Participant

7.1 Onchain Cash Management and Stable Yield

One of the most practical ways crypto users and DAOs are engaging with RWAs is through onchain cash management. Instead of leaving idle stablecoin balances in wallets or zero-yield accounts, treasuries can allocate a portion to tokenized Treasury funds or RWA-backed stablecoins that earn a baseline yield. This approach mirrors traditional corporate treasury practices, where excess cash is parked in short-term instruments, but brings the process entirely onchain.

For example, a DAO might hold USDC as its core treasury asset due to its liquidity and acceptance in DeFi, but allocate a slice of that USDC into tokenized Treasury products that issue yield-bearing tokens in return. These tokens can be integrated into DeFi strategies, used as collateral, or simply held to accrue yield. Because many tokenized Treasury products operate on multiple chains, treasuries can choose the ecosystem that best fits their governance and activity profiles, be it Ethereum for deep DeFi integration or Solana for high throughput and low fees.

RWA-backed stablecoins offer an even more streamlined experience. Instead of manually managing allocations to tokenized funds, users can hold a single token that represents a claim on an actively managed portfolio of short-term RWAs and distributes yield automatically. For DeFi protocols, accepting such tokens as collateral or base assets can simplify liquidity provisioning while enhancing capital efficiency. The trade-off, however, is that users must trust the issuer’s investment and risk-management practices, and may face more complex tax or regulatory treatment due to the yield-bearing nature of the stablecoin.

7.2 RWAs as Collateral in DeFi

As RWAs proliferate, they are increasingly accepted as collateral in DeFi lending and derivatives protocols. Tokenized Treasuries, for instance, are attractive collateral candidates because of their relatively stable value, predictable income, and low credit risk. Protocols can allow users to post RWA tokens to borrow stablecoins or other assets, enabling leveraged strategies or liquidity provisioning. Because the underlying Treasuries continue to earn interest, these positions can offset some borrowing costs or be structured to achieve yield-enhancing carry trades.

Private credit RWAs, such as Maple Finance pool tokens, present a different collateral profile. They typically offer higher yields but also carry higher credit and liquidity risk. If accepted as collateral, they may be subject to lower loan-to-value ratios and more conservative risk parameters. The integration of such tokens into DeFi lending requires robust oracles, clear redemption mechanics, and well-understood loss waterfall structures, all of which link back to the offchain legal and economic layers.

The use of RWA tokens as collateral also opens up new protocol designs. For example, a decentralized stablecoin could be partially backed by tokenized Treasuries, effectively mirroring the reserve model of centralized issuers but with onchain transparency and community governance over allocation mix and risk limits. Similarly, derivatives protocols can build structured products or options strategies on top of RWA collateral, combining onchain leverage with offchain yield. These possibilities illustrate how RWAs are becoming core building blocks in DeFi’s evolving collateral hierarchy.

7.3 Trading and Hedging with RWA Perpetuals and Spot Tokens

For active traders, RWAs create new ways to express macro and micro views without leaving crypto rails. Tokenized equities and ETFs, whether held spot or via perps, allow traders to take positions on specific companies, sectors, or indices in a self-custodial environment. Platforms like Exodus Markets, powered by Ondo, offer direct trading of more than 200 tokenized stocks, ETFs, and RWAs on Solana, combining the familiarity of traditional tickers with the user experience of a crypto wallet. Meanwhile, DEX infrastructure like Orderly supports dozens of RWA markets in perp format and continues to add new listings, including major tech names and other liquid equities.

These markets enable sophisticated strategies. A trader could hedge a portfolio of tech-focused crypto assets by shorting a basket of tech stocks via perps, or could combine positions in ETH and AAPL perps to structure a relative-value trade around macro announcements. They could also express views on exchange business models by trading COIN-like exposures via tokenized equities or perps on RWA-focused DEXs. Because these instruments are onchain, they can be integrated into automated strategies, used as components in structured products, or even embedded in NFT-based financial games.

Beyond equities, RWA-based derivatives may emerge around commodities, interest rates, and credit indices. For example, tokenized reinsurance risk securities could be paired with parametric derivatives that pay out based on weather or catastrophe indices, allowing more granular hedging and speculation. Tokenized CLO tranches could be combined with interest-rate swaps or options to build synthetic leveraged credit strategies. While these products are still nascent, the combination of RWA tokenization and DeFi composability significantly expands the design space for onchain trading and hedging.

7.4 Data, Analytics, and Research

Given the complexity of RWAs, data and analytics play a pivotal role in making the ecosystem investable. Platforms such as RWA.xyz aggregate information on tokenized assets across issuers, tracking metrics like total value, yield, asset composition, and chain distribution. This helps users compare different RWA products, monitor growth, and identify concentration risks. For example, an investor could use RWA.xyz to see which tokenized Treasury products have the largest market share on Ethereum versus Solana, or which private credit pools have the highest yields and default histories.

More general analytics providers like Token Terminal have introduced dedicated dashboards for stablecoin and RWA issuers, offering insights into revenue, user activity, and protocol fundamentals. Combined with onchain proof-of-reserve feeds, block explorers, and governance forums, this creates a multi-layered information environment reminiscent of both DeFi analytics and traditional fund research. For serious participants, analyzing RWAs increasingly means synthesizing legal documents, offchain financial statements, and onchain activity metrics.

Research incentives are also emerging. Ecosystems such as Mantle have launched research challenges with prizes for analysts and builders exploring RWAs, tokenized equities, AI agents, and other onchain finance trends, recognizing that high-quality research and critique are vital for healthy market development. As the RWA space scales, one can expect an expanding body of white papers, rating methodologies, and risk frameworks tailored specifically to tokenized assets, bridging the gap between credit analysts, DeFi researchers, and data scientists.

Black Lake, Nuva Labs tokenize $25M mortgage-loan pool on Provenance ahead of NUVA RWA vault

Black Lake Digital Markets and Nuva Labs completed a $25 million onchain mint and transfer of institutional mortgage loans on Provenance, with the tranche expected to seed a dedicated NUVA.finance vault next month. Each loan is minted as an NFT with data kept in a permissioned DataRoom, while a policy-hash attestation lets investors verify pool eligibility and compliance without touching borrower data. The bet is that mortgage credit can become usable DeFi collateral without dragging the whole $13 trillion U.S. mortgage market’s paperwork mess onchain.

Core tokenization contracts are relatively simple, but composability risk is rising as RWA collateral is increasingly used in looping strategies and leveraged DeFi vaults that chain multiple protocol dependencies.

Almost all tokenized RWA depends on a single off-chain custodian or issuer (e.g., Ondo, Securitize, BlackRock) to maintain the legal claim and enforce redemption — the on-chain token is only as decentralized as that counterparty's operations.

- RegulatoryHigh

Ondo's request for the SEC to pause Nasdaq's tokenized securities plan and Robinhood's 42-page federal framework proposal both illustrate that tokenized securities exist in unresolved legal territory where a single ruling could redefine the entire asset class.

Tokenized Treasuries have a growing secondary market, but private credit RWA (Maple, Florence Finance, Centrifuge) retains thin on-chain liquidity and long lock-up periods that become acute during credit stress events.

Private credit valuations and real estate appraisals are fed on-chain by centralized price reporters with no cryptographic attestation, meaning a single corrupted or manipulated data input can silently misvault collateral across multiple protocols.

RWA looping now represents roughly 30% of Ethereum lending activity; a correlated drawdown in tokenized Treasury prices or a major issuer redemption pause would cascade into forced liquidations across DeFi lending markets simultaneously.

8. Risks, Regulation, and Open Questions

8.1 Legal Enforceability and Counterparty Risk

The most fundamental risk in RWAs is legal enforceability: does holding a token truly entitle the holder to the economic rights it purports to represent, and how is that enforced in practice? Unlike native crypto assets, RWA tokens rely on offchain legal constructs such as SPVs, trusts, fund agreements, and custodial relationships. If these constructs are poorly designed or tested, tokenholders may find themselves with weaker rights than expected, especially in bankruptcy or regulatory intervention scenarios.

The taxonomy literature emphasizes that legal structures can range from direct tokenization of existing securities to more complex wrappers. For example, a token might represent a share in a regulated fund, or it might be a contractual claim on a profit-sharing arrangement governed by bespoke agreements. The degree to which tokenholder rights are recognized by courts, and the ease with which investors can enforce claims across borders, varies widely. Issuer domiciles, choice-of-law clauses, and regulatory registrations all influence this risk.

Counterparty risk extends beyond issuers to custodians, administrators, and service providers. If a custodian holding U.S. Treasuries for a tokenized fund fails, mismanages assets, or becomes entangled in legal disputes, the chain of claims from tokens to underlying assets can break. While proof-of-reserve feeds can attest to the existence of assets at a point in time, they do not eliminate the underlying legal and operational risk. Investors must therefore treat RWAs as layered exposures, combining blockchain-level smart-contract risk with traditional counterparty and legal risks.

8.2 Market, Liquidity, and Interest-Rate Risk

RWAs inherit the market risks of their underlying assets. Tokenized Treasuries are exposed to interest-rate risk: when rates rise, bond prices fall; when rates fall, bond prices rise. If users treat tokenized Treasuries purely as stable cash equivalents, they may be surprised by mark-to-market volatility, especially for longer-duration portfolios. RWA stablecoins that pass through yield may face similar dynamics if their backing includes duration risk.

Liquidity risk is particularly important for private credit, real estate, and structured products. Secondary markets for tokenized loans, private credit pools, or CLO tranches may be thin or fragmented, making it difficult to exit positions quickly without price impact. Redemption mechanisms often involve notice periods, gates, or discretionary controls by issuers, reflecting the illiquidity of underlying assets. During periods of stress, these mechanisms may be triggered, limiting investor flexibility precisely when it is most needed.

In addition, DeFi integration can amplify market risk. If RWA tokens are widely used as collateral in lending protocols, price declines or loss of confidence can trigger cascading liquidations and liquidity crunches. The interplay between onchain leverage and offchain asset performance creates complex feedback loops similar to those observed in traditional securitization and repo markets. Risk controls such as conservative loan-to-value ratios, dynamic interest rates, and oracle-based thresholds are essential, but they cannot fully eliminate systemic risk.

8.3 Smart-Contract, Oracle, and Governance Risk

RWAs may be backed by traditional assets, but their onchain representations are still subject to the full spectrum of smart-contract and governance risks. Bugs in token contracts, vault implementations, or DeFi integrations can lead to loss of funds or mis-accounting. Governance failures, such as poorly designed upgrade processes or treasury management decisions, can introduce additional risk layers. Even when the underlying assets are safe in custody, onchain mismanagement can impair tokenholder value.

Oracle risk is especially salient for RWAs. Price feeds for tokenized assets must be accurate and resilient against manipulation. Reserve feeds must correctly reflect the composition and value of backing assets. Inaccurate or delayed oracle data can trigger false liquidations, misprice derivatives, or allow arbitrageurs to exploit discrepancies between onchain and offchain valuations. Designing oracle systems that balance decentralization, security, and timeliness is a nontrivial challenge, particularly for illiquid or bespoke RWAs.

Governance risk intersects with both legal and technical layers. Many RWA protocols have multisig-controlled contracts, centralized admin keys, or discretionary powers to pause redemptions, change parameters, or allocate reserves. While these powers may be necessary to comply with regulations or handle emergencies, they also create trust assumptions that differ from fully permissionless DeFi. Over time, projects may experiment with more decentralized governance models, including community-elected oversight committees or onchain representatives, but regulatory constraints will likely limit how far this can go for certain asset types.

8.4 Regulatory Trajectories and Jurisdictional Differences

Regulation is the moving target that will define much of the RWA landscape over the next decade. Different jurisdictions are adopting divergent approaches to tokenized securities, stablecoins, and DeFi more broadly. Some regulators see tokenization as an opportunity to modernize market infrastructure, improve transparency, and enhance investor protections; others focus on potential risks and seek to apply existing securities and banking regulations to RWA projects.

Tokenized securities—such as equity tokens, bond tokens, and fund shares—are generally treated as securities under most regulatory frameworks, regardless of whether they are issued on blockchains. This implies registration, disclosure, and investor-protection requirements, or reliance on private-placement exemptions. As a result, many RWA tokens are restricted to accredited or institutional investors or are offered only via regulated platforms with KYC/AML controls. This tension between open DeFi and securities regulation is a central challenge for mass adoption of RWAs among retail users.

Stablecoins occupy a separate but overlapping regulatory domain. Fiat-backed stablecoins like USDC are increasingly subject to dedicated stablecoin legislation and oversight, focusing on reserve quality, redemption rights, and systemic risk implications. RWA-backed stablecoins that invest in yield-bearing assets may fall under both payments and investment-product regulations, raising questions about who is allowed to hold them, how they can be marketed, and what disclosures are required. These questions are far from settled and will likely differ across regions.

Jurisdictional fragmentation adds complexity for global protocols. An RWA issuer might be fully compliant in one jurisdiction but face restrictions or bans in others. Multi-jurisdictional offerings may require complex legal structures and compliance programs, increasing costs and slowing innovation. On the other hand, regulatory clarity in key hubs can catalyze growth by giving institutions confidence to participate. The balance between innovation and protection will shape which RWA models become dominant and which remain niche.

To help frame these issues, it is useful to think about risk and due diligence along several dimensions:

| Risk Dimension | Key Questions for Users and DAOs |

|---|---|

| Legal & Counterparty | What rights does the token confer? Who holds the underlying assets and under what legal structure? |

| Market & Liquidity | How volatile are the underlying assets? How deep are secondary markets and what are redemption terms? |

| Smart-Contract & Oracle | Are contracts audited and upgradable? How are prices and reserves fed onchain and who controls oracles? |

| Governance & Regulation | Who can change parameters or pause the system? What jurisdictions regulate the issuer and the token? |

While this table simplifies a complex reality, it provides a starting point for evaluating RWA products beyond headline yields or narratives.

9. Conclusion

Real-world assets represent one of the most significant bridges between traditional finance and crypto-native systems. By tokenizing claims on cash, bonds, equities, credit portfolios, reinsurance programs, and other real-economy exposures, RWA projects are importing trillions of dollars of potential collateral and yield sources into onchain environments. This transformation is already visible in the tens of billions of dollars locked in tokenized Treasuries, tokenized bond funds, tokenized equities and ETFs, and emerging segments like tokenized CLOs and reinsurance risk.

For crypto users and DeFi protocols, RWAs expand the design space of financial products. They allow DAOs to implement sophisticated cash management strategies with tokenized Treasuries and RWA-backed stablecoins, traders to access global equities and bond markets via self-custodial wallets and perp DEXs, and institutions to launch regulated funds and private-market vehicles directly on public blockchains. They also offer the promise of more sustainable “real yield” in DeFi, rooted in offchain economic activity rather than purely reflexive token incentives.

At the same time, RWAs reintroduce many of the risks that decentralization was meant to mitigate. Legal enforceability, counterparty reliability, market and liquidity risk, smart-contract and oracle vulnerabilities, and regulatory uncertainty all sit at the heart of the RWA value proposition. Tokenholders are no longer dealing purely with code and consensus, but with complex hybrids of legal contracts, custodial arrangements, and programmable infrastructure. Navigating this environment requires both traditional financial literacy and DeFi-native risk awareness.

The RWA narrative today is neither pure hype nor a settled reality. It is an active experiment at global scale, involving some of the world’s largest financial institutions, emerging onchain asset managers, L1 and L2 ecosystems, and millions of crypto users. Its success or failure will shape not only how capital flows between TradFi and DeFi, but also how regulators, auditors, and technologists rethink the infrastructure of capital markets themselves.

Outlook

Looking ahead, the RWA space is likely to move through several overlapping phases. In the near term, growth will probably continue to concentrate in tokenized cash and fixed-income instruments, especially U.S. Treasuries and high-quality bond funds, as investors seek to monetize the global risk-free rate onchain and protocols compete to integrate RWA-backed collateral. The emergence of robust RWA stablecoins will further blur the line between money and yield-bearing assets in DeFi, as more users treat yield-bearing stablecoins as their default unit of account.

At the same time, the breadth of tokenized asset classes will expand. Tokenized equities, ETFs, private credit portfolios, CLO tranches, reinsurance risk, and real estate will likely see more experimentation, particularly on high-throughput chains like Solana and enterprise-focused networks like Hedera. Grants, hackathons, and research challenges from ecosystems such as Mantle, Aptos, and Stacks suggest that tokenization will remain a core area of innovation across L1s and L2s, spawning new primitives in onchain capital markets.

Institutional adoption is poised to deepen as banks, asset managers, and custodians move beyond pilots into scaled offerings. Strategic moves like Inveniam’s planned acquisition of Mantra, Ethena’s large allocation to tokenized CLOs on Solana, and the expansion of tokenized bond and equity products on exchanges and wallet-based platforms all point to a feedback loop in which institutional infrastructure and onchain demand reinforce each other. As regulatory frameworks for stablecoins and tokenized securities mature, especially in key jurisdictions, more conservative capital may enter the RWA arena.

The main constraints will be legal and regulatory clarity, as well as market discipline. Jurisdictional inconsistencies, evolving securities-law interpretations, and prudential concerns around stablecoins and DeFi will influence which RWA models achieve global scale and which remain confined to specific niches. Meanwhile, market participants will need to learn from inevitable failures—whether due to poor underwriting, opaque structures, or governance missteps—and build more resilient, transparent, and investor-friendly RWA platforms.

For crypto-native users, the most pragmatic approach is to treat RWAs neither as a risk-free bridge to TradFi nor as an inherently compromised deviation from decentralization, but as a powerful new category of programmable financial primitives. By combining careful due diligence on offchain legal and economic structures with the analytical tools and risk frameworks honed in DeFi, investors and builders can participate in the RWA wave while helping steer it toward a more robust, transparent, and inclusive onchain financial system.

Latest Real World Assets news

South Korea's biggest banks, fintechs and internet giants are racing to build stablecoin and RWA infrastructure ahead of regulatory clarity, reshaping Asia's blockchain landscapeKDDI and Securitize Japan sign pact to explore RWA tokenization for 30M-plus customer baseBlack Lake, Nuva Labs tokenize $25M mortgage-loan pool on Provenance ahead of NUVA RWA vault Ethra Ship’s new maritime RWA protocol tests investor appetite in a volatile and opaque shipping market

Ethra Ship’s new maritime RWA protocol tests investor appetite in a volatile and opaque shipping market Real‑world assets (RWAs) are the inevitable evolution of stablecoins: tokenization proved viable at scale, creating on‑chain dollar liquidity that now seeks yield, broader use cases, and deeper financial markets

Real‑world assets (RWAs) are the inevitable evolution of stablecoins: tokenization proved viable at scale, creating on‑chain dollar liquidity that now seeks yield, broader use cases, and deeper financial markets Vobile launches RWA program for creative IP rights, expanding monetization for content creators. Rightsholders can now realize value from their IP through digital asset infrastructure.

Vobile launches RWA program for creative IP rights, expanding monetization for content creators. Rightsholders can now realize value from their IP through digital asset infrastructure.Sources

- https://chain.link/education-hub/real-world-assets-rwas-explained

- https://app.rwa.xyz

- https://blog.huma.finance/what-is-rwa-tokenization-how-real-world-assets-are-shaping-the-future-of-finance

- https://x.com/onchainsummit

- https://arxiv.org/html/2606.08534v1

- https://transak.com/blog/what-are-rwa-stablecoins