In‑depth explainer on Ondo Finance, covering its tokenized Treasuries and money market funds, Ondo Global Markets for stocks/ETFs, Ondo Chain RWA infrastructure, key partnerships, risks, and how it bridges TradFi and DeFi.

+9 sources across the wider coverage universe

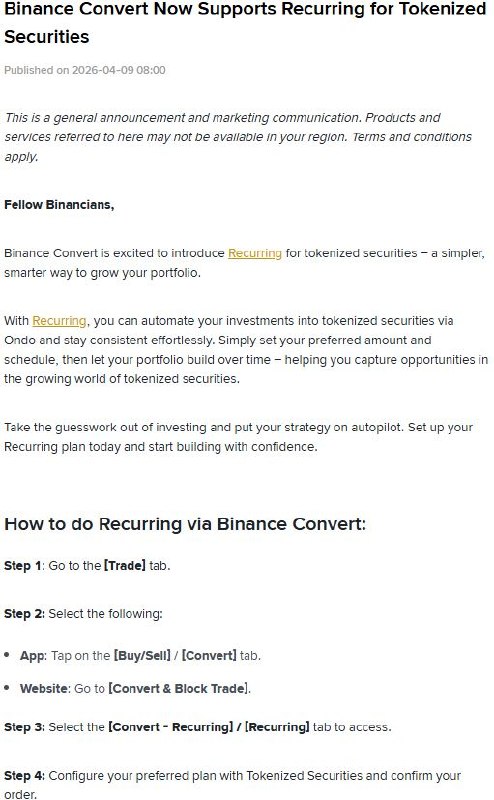

Binance Convert adds recurring buys for Ondo tokenized securities across app and web2026-04

Binance Convert adds recurring buys for Ondo tokenized securities across app and web2026-04 Ondo Finance requests SEC no-action letter to record tokenized securities on Ethereum2026-04

Ondo Finance requests SEC no-action letter to record tokenized securities on Ethereum2026-04 Ondo partners with Deutsche Börse's Clearstream and 360X to bridge tokenized and traditional securities markets2026-04

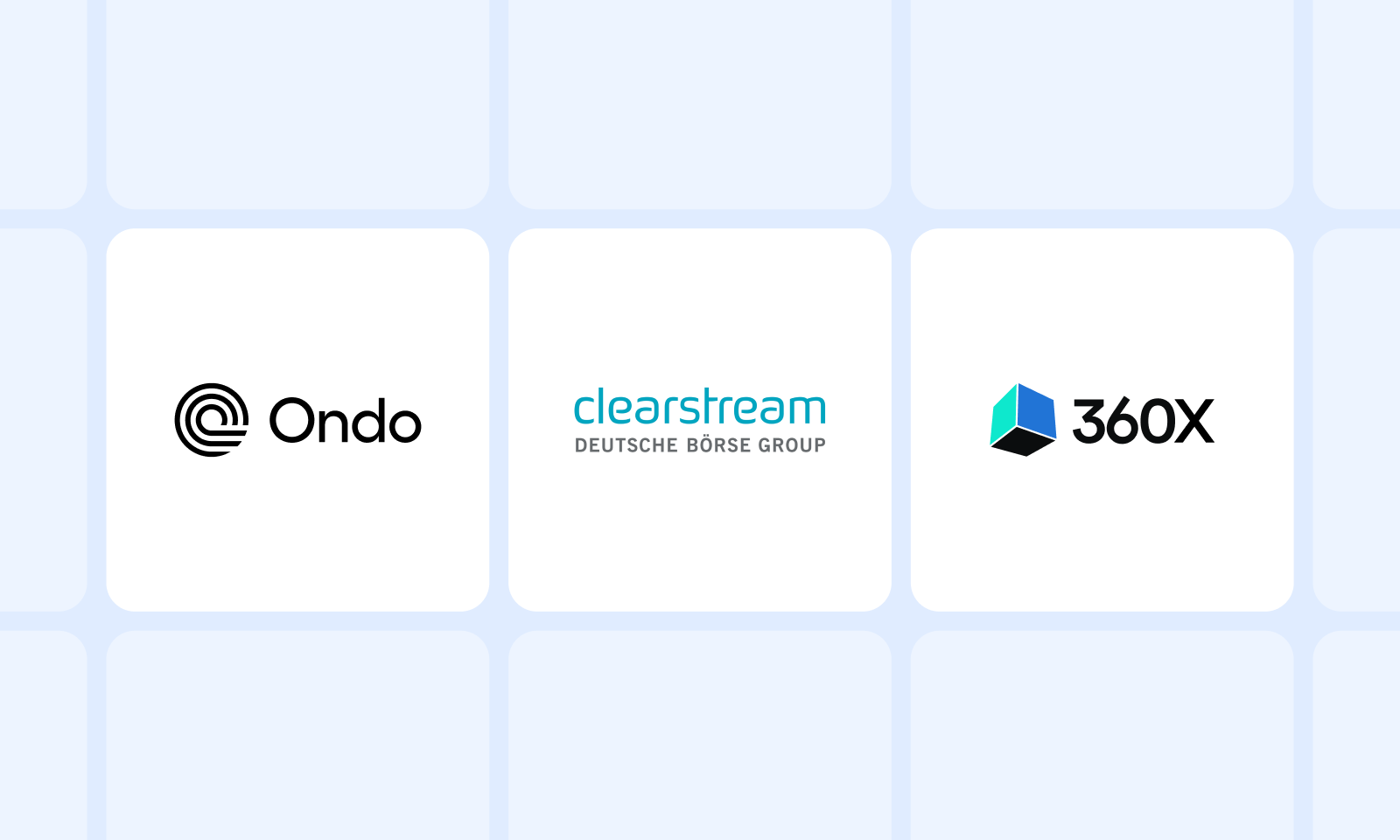

Ondo partners with Deutsche Börse's Clearstream and 360X to bridge tokenized and traditional securities markets2026-04 Ondo, Clearstream, and 360X launch 10 tokenized US stocks on regulated European market infrastructure2026-04

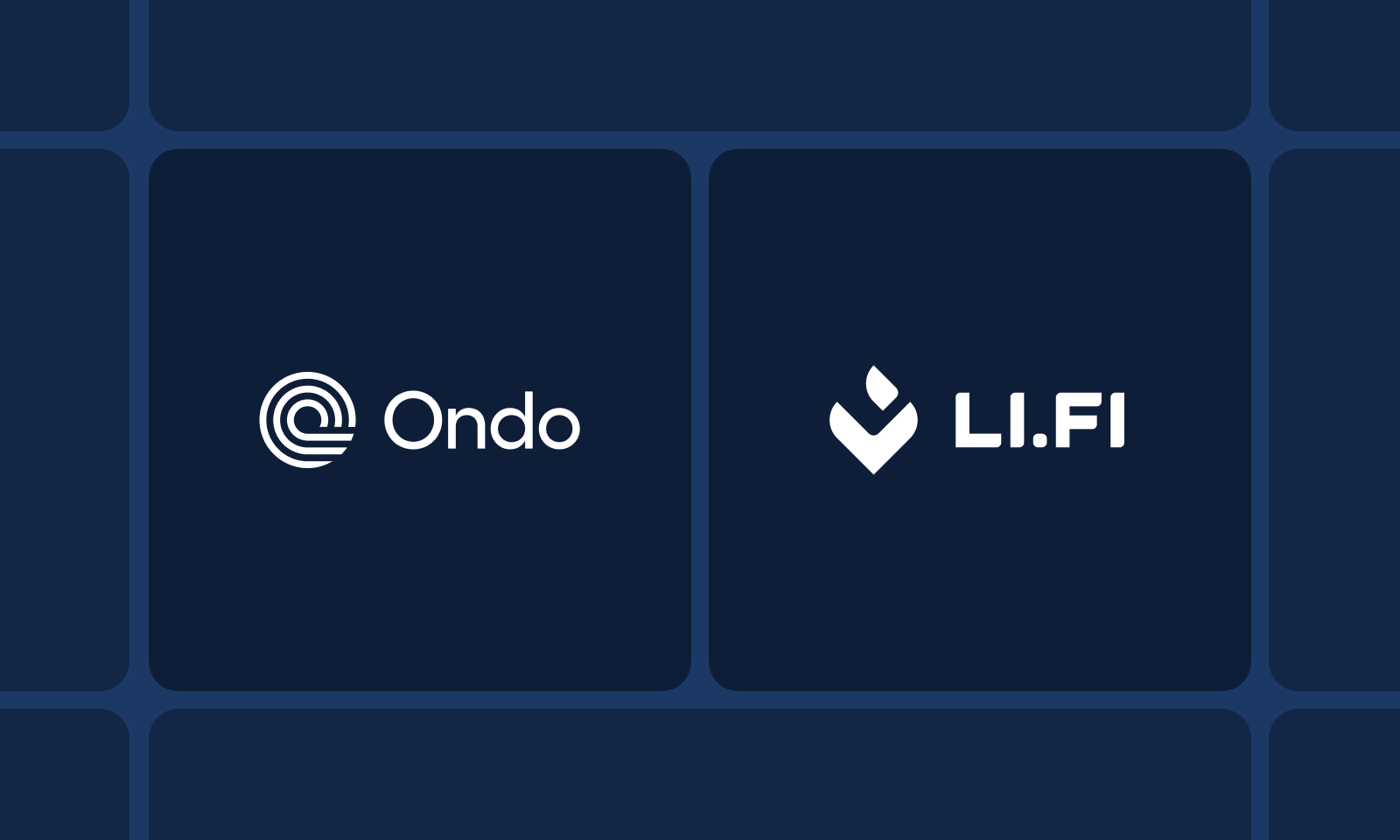

Ondo, Clearstream, and 360X launch 10 tokenized US stocks on regulated European market infrastructure2026-04 Ondo tokenized stocks and ETFs go live on LI.FI with gasless access across 1,000+ wallets and apps2026-06

Ondo tokenized stocks and ETFs go live on LI.FI with gasless access across 1,000+ wallets and apps2026-06 Ondo launches tokenized equity perps with 20x leverage for traders abroad on June 92026-06

Ondo launches tokenized equity perps with 20x leverage for traders abroad on June 92026-06

Ondo Finance: A Comprehensive Guide To The RWA Tokenization Leader

A leading real‑world asset tokenization platform, Ondo Finance issues on‑chain funds, tokenized stocks and ETFs, and a purpose‑built blockchain to connect traditional markets with crypto rails. In practice, it aims to do for Treasuries and equities what stablecoins did for dollars, turning legacy assets into programmable building blocks for DeFi and global capital markets.

Ondo sits at the intersection of traditional finance and decentralized finance, with a product suite that spans tokenized U.S. Treasuries and money market funds, yield‑style dollar products, and a rapidly expanding marketplace for tokenized stocks and ETFs. Its offerings are designed to be institutionally compliant while still composable across public blockchains, allowing investors to access familiar instruments such as U.S. government debt or S&P 500 exposure through tokens held in crypto wallets. The platform has also launched Ondo Chain, a layer‑1 blockchain optimized for real‑world assets with authorized validators and integrated proof‑of‑reserve infrastructure, and has become one of the largest RWA platforms globally by total value locked alongside BlackRock’s BUIDL and Franklin Templeton’s BENJI tokenized funds. Recent partnerships with players such as Mirae Asset Global Investments, J.P. Morgan’s Kinexys, Exodus, Ledger, and Chainlink underscore how Ondo is being woven into both institutional and retail crypto workflows, from cross‑chain settlement of tokenized Treasuries to self‑custodial trading of tokenized stocks on Solana. At the same time, the project has navigated major leadership changes following the unexpected death of its founder, Nathan Allman, with former McKinsey partner Ian De Bode stepping in as CEO and reiterating the ambition to become “the world’s most trusted platform for intelligently managed, on‑chain investment portfolios.”

1. Origins, Vision, and the RWA Context

1.1 From DeFi experiments to institutional‑grade tokenization

Ondo Finance emerged during the broader DeFi boom as developers began to explore how tokenization could extend beyond purely crypto‑native instruments into the realm of bonds, cash equivalents, and other real‑world assets. From its early stages, Ondo differentiated itself by explicitly targeting institutional‑grade standards for custody, compliance, and portfolio construction, rather than treating tokenization as a purely retail or experimental product. The team framed its mission as building platforms, assets, and infrastructure that bring traditional financial markets on‑chain, effectively using blockchain as a new settlement and composability layer rather than trying to replace the underlying securities markets themselves.

This approach led Ondo to focus on regulated fund structures and partnerships with established asset managers from the outset. OUSG, one of Ondo’s flagship products, was launched as exposure to short‑term U.S. Treasuries wrapped in a 3(c)(7) fund structure, available only to qualified purchasers and offered under Regulation D’s Rule 506(c) exemption under U.S. securities law. Rather than buying individual Treasuries directly, OUSG invests in U.S. Treasury and government money market funds managed by firms such as BlackRock, Franklin Templeton, WisdomTree, and Fidelity, with tokens representing an interest in the underlying fund vehicle. This design signaled that Ondo’s strategy was not to bypass regulation but to embed tokenization within existing legal frameworks.

The vision resonated as macro conditions shifted and yields on U.S. Treasuries and money market funds rose, driving interest in on‑chain “risk‑free rate” exposure from both institutions and crypto‑native investors. Ondo capitalized on this trend by positioning itself as a specialist in tokenized fixed income and cash‑equivalent products, building the technology rails and asset management capabilities needed to meet institutional compliance while still delivering the composability that DeFi users expect. Over time, this focus expanded into tokenized equities and ETFs, with Ondo Global Markets growing into one of the dominant tokenized stocks platforms by market share, and eventually into a bespoke blockchain, Ondo Chain, designed to host and interconnect these real‑world asset tokens at scale.

1.2 Real‑world assets and the next phase of crypto markets

The rise of Ondo Finance is part of a broader structural shift in crypto markets towards real‑world assets (RWAs), a category that includes tokenized bonds, Treasuries, money market funds, real estate, equities, and other traditional financial instruments. RWAs are essentially off‑chain assets represented on a blockchain via tokens, with legal structures and custodial arrangements that tie those tokens to the underlying claims. Proponents argue that tokenization can unlock liquidity, reduce transaction and settlement costs, and make markets more globally accessible by allowing investors to hold and trade exposure in a purely digital, wallet‑native form.

Several macro and technological factors underpin this trend. Rising interest rates have made yield‑bearing traditional assets like short‑term U.S. Treasuries newly attractive to crypto participants who previously focused on DeFi yields and speculative altcoins, while regulatory scrutiny of unregistered yield products has made regulated RWA structures more appealing. At the same time, stablecoins have demonstrated that tokenized fiat money can operate at large scale as plumbing for trading, payments, and on‑chain credit markets, offering a template for how other asset classes might migrate onto blockchains. As consultants such as McKinsey have argued, tokenized cash and stablecoins are becoming foundational to next‑generation payment infrastructure, particularly for cross‑border commerce and on‑chain settlement.

Ondo’s leadership explicitly situates their strategy within this macro narrative. John Hoffman, a former Invesco and Grayscale executive who joined Ondo as head of portfolio products, has argued that tokenization could track the explosive growth of the ETF industry, which climbed into the tens of trillions of dollars over several decades. In his view, the convergence of blockchain infrastructure and artificial intelligence could become one of the dominant forces shaping capital markets over the coming decade, and Ondo’s goal is to become the most trusted platform for intelligently managed, on‑chain portfolios that use tokenization as a core primitive. This emphasis on “portfolio products” underscores that Ondo is not merely interested in creating isolated tokens, but in assembling structured strategies and index‑like offerings that can be rebalanced, risk‑managed, and integrated with DeFi protocols.

1.3 Scale and position among RWA platforms

By mid‑2026, Ondo Finance had become one of the largest RWA platforms in the world, with total value locked measured in the multiple billions of dollars. Reporting from industry outlets describes Ondo as a roughly 3.5 billion dollar tokenized RWA platform as of late May 2026, placing it alongside BlackRock’s BUIDL tokenized money market fund and Franklin Templeton’s BENJI suite as one of the “big three” in the sector. Subsequent data cited in RWA‑focused analysis notes that Ondo’s TVL has continued to climb, surpassing approximately 3.77 billion dollars as part of a broader institutional push into on‑chain Treasuries and money market products.

On the equities side, Ondo Global Markets has built a particularly strong position, reportedly holding more than 70% market share among tokenized equity issuers according to data aggregators such as RWA.xyz. The platform crossed the one‑billion‑dollar TVL mark for tokenized stocks in under eight months from launch, with cumulative trading volume reaching tens of billions of dollars and steadily rising as new assets and venues were added. The breadth of available assets has grown from an initial focus on U.S. stocks and ETFs to hundreds of tokenized securities spanning multiple sectors and geographies, including AI, robotics, space, defense technology, lithium and battery technology, and other thematic exposures.

Ondo’s growth has been reinforced by its multi‑chain strategy and distribution partnerships. Tokens are natively issued on networks including Ethereum, Solana, and BNB Chain, and are made accessible through wallets and platforms such as MetaMask, Binance, Bitget, Blockchain.com, and Exodus’s self‑custodial app. This has allowed both retail and professional traders to access tokenized equities through familiar interfaces while maintaining self‑custody of their holdings. At the same time, Ondo’s work with J.P. Morgan’s Kinexys, Chainlink, and other institutional players has highlighted its role in more experimental cross‑chain settlement and tokenized collateral workflows, positioning the platform as a bridge between bank payment rails and public crypto infrastructure.

Ondo tokenized stocks and ETFs go live on LI.FI with gasless access across 1,000+ wallets and apps

Promoting from Tsunami auto-feed. Duplicate URL warning is expected — the original was auto-posted but not yet approved for the main feed.

Readers click Ondo stories most when a named incumbent — a bank, exchange, or DeFi blue-chip — adopts its infrastructure, revealing that the real story is institutional legitimacy transfer to on-chain rails, not Ondo's own product launches.↗

2. Core Building Blocks: Ondo’s Product Stack

2.1 OUSG: Tokenized short‑term U.S. Treasuries

OUSG is Ondo’s flagship tokenized U.S. Treasury product, designed to give qualified investors on‑chain exposure to short‑term Treasuries and related cash instruments. The token represents interests in a 3(c)(7) fund and is offered under Rule 506(c) of the U.S. Securities Act, which restricts participation to qualified purchasers and requires appropriate onboarding and accreditation. Investors can subscribe using either traditional fiat via wire transfer or supported stablecoins such as USDC, with Ondo enabling 24/7 mints and redemptions in stablecoin terms even though the underlying fund operates on conventional business‑day cycles.

The underlying OUSG portfolio is invested in funds issued by leading asset managers, primarily focused on U.S. government securities and high‑quality liquidity vehicles. As of the most recent disclosures, a significant majority of the portfolio is allocated to BlackRock’s USD Institutional Digital Liquidity Fund (BUIDL), with the remainder held in BlackRock’s FedFund (TFDXX), bank deposits, and USDC for liquidity management. The portfolio may in the future include other U.S. Treasury funds or direct holdings of Treasuries themselves, providing flexibility to adapt to market conditions while maintaining a conservative risk profile. Because the underlying assets accrue interest, the value of OUSG appreciates over time rather than maintaining a fixed one‑dollar peg, making it function more like a tokenized fund share than a stablecoin.

A key design choice for OUSG is its focus on instant, blockchain‑native user experience while still respecting the operational constraints of legacy markets. Ondo offers “instant” mint and redemption options for amounts above a relatively modest threshold—currently set at 5,000 dollars for both investments and redemptions—allowing investors to swap between OUSG and stablecoins such as USDC at any time of day. For larger or non‑instant transactions, the minimums are higher, with investments and redemptions in the range of tens of thousands to hundreds of thousands of dollars reflecting the institutionally oriented nature of the product. This dual‑track system lets OUSG function as a relatively liquid on‑chain asset for smaller flows while preserving operational efficiency for larger, more traditional capital allocations.

OUSG is thus best understood as an institutional‑grade, tokenized short‑duration bond fund accessible via blockchain, rather than as a retail savings product. It exemplifies Ondo’s broader approach: marry existing fund structures and regulated custodianship with a token wrapper that can interoperate with DeFi protocols, serve as collateral, and integrate into cross‑chain settlement workflows.

2.2 OMMF: Tokenized U.S. government money market funds

Building on the experience with OUSG, Ondo launched OMMF, a tokenized U.S. government money market fund designed specifically to behave more like a stablecoin in terms of price while still delivering yield. OMMF accepts both fiat and stablecoin subscriptions and redemptions and is intended to be compatible with 24/7 on‑chain financial infrastructure, including over‑the‑counter trading, lending, and settlement workflows. Unlike OUSG, which accrues value in the token price, OMMF is minted and redeemed at precisely one dollar on any business day, with interest distributed daily to holders in the form of new OMMF tokens.

The design of OMMF seeks to harness the cash‑like properties of government money market funds while making them more functional as on‑chain cash equivalents. Because the token’s price is intended to remain stable at one dollar, OMMF can be used as a settlement asset in institutional contexts where price volatility is unacceptable, such as margining, collateral management, or overnight cash management. At the same time, the fact that holders earn yield via automatic distributions makes OMMF a more capital‑efficient alternative to conventional stablecoins or non‑interest‑bearing bank balances, which generally do not pass through underlying money market yields to end users.

For liquidity purposes, OMMF holds a small portion of its assets in on‑chain stablecoin reserves, allowing for instant subscriptions and redemptions around the clock, while maintaining the majority of its portfolio in U.S. government money market funds that invest almost entirely in U.S. government securities. This conservative asset mix aims to keep credit and liquidity risk low, aligning the product with institutional risk appetites and regulatory expectations. Ondo also envisions OMMF being used as collateral in on‑chain lending protocols such as Flux Finance, as well as in OTC trading workflows where counterparties denominate exposures in dollars or stablecoins but prefer to hold yield‑bearing, low‑risk instruments in between settlements.

In effect, OMMF is positioned as a bridge between stablecoins like USDC and traditional cash management products, using tokenization to repackage U.S. government money market funds into a programmable, composable, and yield‑bearing settlement asset. For sophisticated crypto users, it offers an alternative to parking funds in stablecoins or centralized exchanges, while institutions can view it as a way to extend their existing cash dashboards into the on‑chain environment without sacrificing risk controls.

2.3 USDY and other yield‑bearing dollar products

Although not exhaustively detailed in the available documents, Ondo’s broader product lineup includes USDY, often described as a yield‑bearing stablecoin‑style asset that offers on‑chain exposure to U.S. dollar yields through a token wrapper. In coverage that situates Ondo among the largest RWA platforms, USDY is listed alongside OUSG and Ondo Global Markets as a key component of the company’s offering, suggesting that it is central to Ondo’s strategy of bringing dollar‑linked, income‑generating products on‑chain.

The emergence of products like USDY reflects a broader industry trend where token issuers aim to combine the familiarity and unit‑of‑account role of stablecoins with the yield associated with short‑term Treasuries or money market funds. In practice, this typically involves holding a portfolio of dollar‑denominated securities and cash equivalents while promising users either a slowly appreciating token price or periodic interest payouts, subject to varying degrees of regulatory oversight. By layering this on top of existing stablecoin usage—where USDC, USDT, and others already serve as base pairs for trading and DeFi activity—projects like Ondo are effectively trying to move more of the traditional money market stack into programmable form.

From a market structure perspective, such yield‑bearing dollar products can be particularly attractive in an environment where traditional bank deposits may offer relatively low yields compared to instrumentalized money market funds, especially outside the United States. They also introduce new questions around regulatory classification, disclosure, and systemic risk, especially if they begin to be used as collateral or settlement assets in large, interconnected DeFi protocols. Ondo’s emphasis on institutional‑grade structures, transparent underlying holdings, and partnerships with established asset managers suggests that it is positioning itself on the conservative, regulated end of this spectrum, though the regulatory landscape for yield‑bearing tokenized cash remains in flux across jurisdictions.

2.4 Summary of key products

The breadth of Ondo’s product stack can be summarized by comparing the main instruments in terms of their underlying assets, risk profile, and intended use cases. While the details evolve over time, a high‑level snapshot is informative:

| Product | Type | Underlying assets | Target users / eligibility | Primary chains / uses |

|---|---|---|---|---|

| OUSG | Tokenized U.S. Treasuries fund | U.S. Treasury and government MMFs (e.g., BlackRock BUIDL) | Qualified purchasers via 3(c)(7) fund, Rule 506(c) | On‑chain yield, collateral, RWA exposure |

| OMMF | Tokenized U.S. gov’t MMF, $1 token | U.S. government‑only money market funds + small stablecoin | Institutions and crypto users needing cash‑like collateral | Settlement, collateral, cash management |

| USDY | Yield‑bearing dollar‑linked token | Short‑duration dollar assets (Treasuries/MMFs; structure varies) | Global investors seeking yield‑bearing USD exposure | DeFi yield, treasury, savings‑style allocations |

| Ondo Global Markets | Tokenized stocks and ETFs | Publicly traded equities and ETFs, fully custodied | Global traders and investors, subject to regional restrictions | Trading, perps collateral, DeFi composability |

| Ondo Perps | Tokenized equity perpetual futures | Synthetic exposure to stocks/ETFs derived from reference markets | Non‑U.S. traders seeking leveraged equity exposure | Leveraged trading, hedging |

Data derived from Ondo product documentation and public coverage.

This table highlights how Ondo uses tokenization both for relatively low‑risk, income‑generating products tied to U.S. government securities and for higher‑beta trading and investment products tied to stocks and ETFs. Across all of these, the common theme is the attempt to make traditional instruments behave more like native on‑chain assets: transferable 24/7, composable with DeFi, and accessible through standard crypto wallets.

3. Ondo Global Markets: Tokenized Stocks and ETFs

3.1 How tokenized equities work in Ondo’s model

Ondo Global Markets is a platform for tokenizing public securities—primarily stocks and ETFs—into freely transferable tokens that can be used in DeFi and traded around the clock. In this model, a regulated broker‑dealer or custodian holds the underlying securities off‑chain, while Ondo issues tokens on blockchains such as Ethereum, Solana, and BNB Chain that are designed to mirror the economic exposure of those securities, including price movements and, where applicable, dividends. Each token is fully backed by the underlying security, and Ondo’s documentation emphasizes that tokens track the total return of the asset, with income distributions reflected on‑chain.

At the time of recent reporting, Ondo Global Markets offered more than 260 tokenized U.S. stocks and ETFs, with that number rising rapidly as new listings were added and as the platform expanded into additional thematic sectors. Subsequent updates on social platforms indicated that Ondo had surpassed 430 tokenized stocks and ETFs across Ethereum, Solana, and BNB Chain, with particularly strong representation in high‑demand themes like AI, robotics, quantum computing, defense technology, critical materials, data‑center energy, and active strategies from asset managers such as BlackRock. These tokens can be held in standard crypto wallets and are accessible via centralized and decentralized venues including Binance, Bitget, MetaMask, Blockchain.com, and various DeFi protocols.

One important nuance is that, in most cases, tokenized equities on Ondo Global Markets do not grant shareholders’ legal or voting rights in the underlying corporation directly, but instead provide economic exposure to price and income. This is a common structure across the tokenized equity sector, where issuers emphasize that token holders receive the financial benefits of ownership but not necessarily the governance rights associated with registered shareholding. As reporting on Exodus Markets—a self‑custodial wallet that integrated Ondo’s tokenized stocks—has clarified, these tokens “convey economic exposure rather than shareholder rights,” a distinction that issuers highlight to differentiate these products from direct ownership of the underlying securities. Ondo is, however, working to progressively bridge this gap by partnering with infrastructure providers such as Broadridge to bring proxy‑voting and similar shareholder functions to tokenized stocks, at least for certain structures.

3.2 Partnerships and distribution: Exodus, Ledger, and Mirae Asset

A major component of Ondo Global Markets’ growth has been its distribution strategy, which relies on partnerships with both crypto‑native and traditional financial institutions. On the crypto side, one of the most notable collaborations is with Exodus, a publicly traded self‑custodial wallet provider. Exodus and Ondo jointly launched Exodus Markets, a feature within the Exodus app that allows customers in supported regions to buy and sell more than 200 tokenized stocks, ETFs, and real‑world assets directly on Solana via a simple, one‑tap interface. Users can, for example, purchase tokenized shares of Exodus itself (EXOD) alongside hundreds of other tokenized assets, while maintaining control of their private keys.

Exodus Markets relies on a Solana‑based settlement asset called XO Cash (XO), which is used as the medium of exchange when buying or selling Ondo tokenized stocks on the network. The entire setup is fully self‑custodial, meaning users hold their own keys and interact with tokenized equities as they would with any other Solana token, without relying on a centralized broker or exchange to custody their assets. This is emblematic of the broader shift toward integrating tokenized equities into wallet‑centric, DeFi‑compatible environments rather than siloed brokerage platforms. It also reflects Solana’s growing dominance in tokenized equity trading volumes, as high‑throughput, low‑cost blockchains become preferred venues for these assets.

Another distribution channel is hardware wallets. Ondo announced support from Ledger, one of the most widely used hardware wallets in the crypto ecosystem, enabling in‑app swaps for Ondo tokenized stocks directly within the Ledger Live interface. This integration allows users who prioritize secure, offline key storage to trade tokenized stocks and ETFs without moving assets off their hardware wallet environment, further blurring the line between traditional securities investment and self‑custodied crypto asset management. For Ondo, partnerships like this expand the addressable market for tokenized equities and reinforce the narrative that these tokens are first‑class citizens in the broader crypto asset universe.

On the traditional finance side, Ondo has entered into a memorandum of understanding with Mirae Asset Global Investments, one of Asia’s largest asset managers, to tokenize Mirae’s Global X ETF lineup through Ondo Global Markets. Global X, the ETF arm of Mirae, offers widely held thematic funds across categories such as AI and technology, robotics and AI, space innovation, silver miners, blockchain, defense technology, lithium and battery tech, and covered call strategies on indices like the S&P 500 and NASDAQ 100. Under the partnership, Ondo provides the tokenization infrastructure and distribution layer, while Mirae remains the asset manager of the underlying ETFs, starting with U.S.‑listed funds and expanding over time to ETFs listed in Europe, Hong Kong, Japan, Canada, and Australia.

This collaboration underscores a key aspect of Ondo’s strategy: it does not seek to manage all underlying assets itself but instead to serve as a tokenization and distribution layer for established asset managers. By aligning with firms like Mirae and BlackRock, Ondo taps into existing product lineups and AUM while contributing blockchain expertise, on‑chain distribution, and DeFi integration. It also strengthens Ondo’s presence in Asian markets and among investors seeking thematic ETF exposure in on‑chain form.

3.3 Tokenized SpaceX exposure and the “IPO on‑chain” moment

One of the most closely watched developments in Ondo Global Markets has been its effort to offer tokenized exposure to large initial public offerings (IPOs) on day one. Marketing materials and social media coverage have highlighted plans to tokenize shares of SpaceX—expected to be one of the largest IPOs in history—on day one through an instrument dubbed SPCXon, accessible across leading blockchains such as Solana. Promotional content emphasizes that tokenized SpaceX shares would be available via a simple Solana wallet such as Phantom or Solflare, effectively opening a mega‑IPO to a global, on‑chain audience in real time.

Reporting from the broader tokenized equity ecosystem has noted that tokenized stocks are increasingly being listed on chains like BNB Chain and Solana within minutes of major events, sometimes achieving significant trading volumes within the first hour. In the case of SPCXon on BNB Chain, for instance, early coverage described tens of thousands of trades and over one million dollars in volume within the first hour after launch, marking what some have called the largest IPO being made globally accessible via tokenization at record speed and with high execution quality. While specific numbers vary across venues and time, the overarching narrative is that Ondo and its peers are enabling a new pattern: rather than IPOs being gated by geographic and brokerage boundaries, tokenized instruments can offer near‑real‑time exposure to new listings via public blockchains.

Such tokenized IPO exposure is, however, subject to complex legal and regulatory considerations. Structures can vary from fully collateralized tokens backed one‑to‑one by IPO shares held with a regulated custodian to more synthetic exposures that track prices via derivatives or internal market‑making arrangements. Ondo’s emphasis on fully backed tokens and regulated custody for its stock tokens suggests that, for flagship products like SPCXon, it will favor conservative structures that map as closely as possible to underlying share ownership while still being compatible with on‑chain trading and DeFi integrations. For investors, this raises important questions about what exactly they own, what rights they have, and which jurisdictions govern disputes—a theme explored further in the discussion of risk and regulation below.

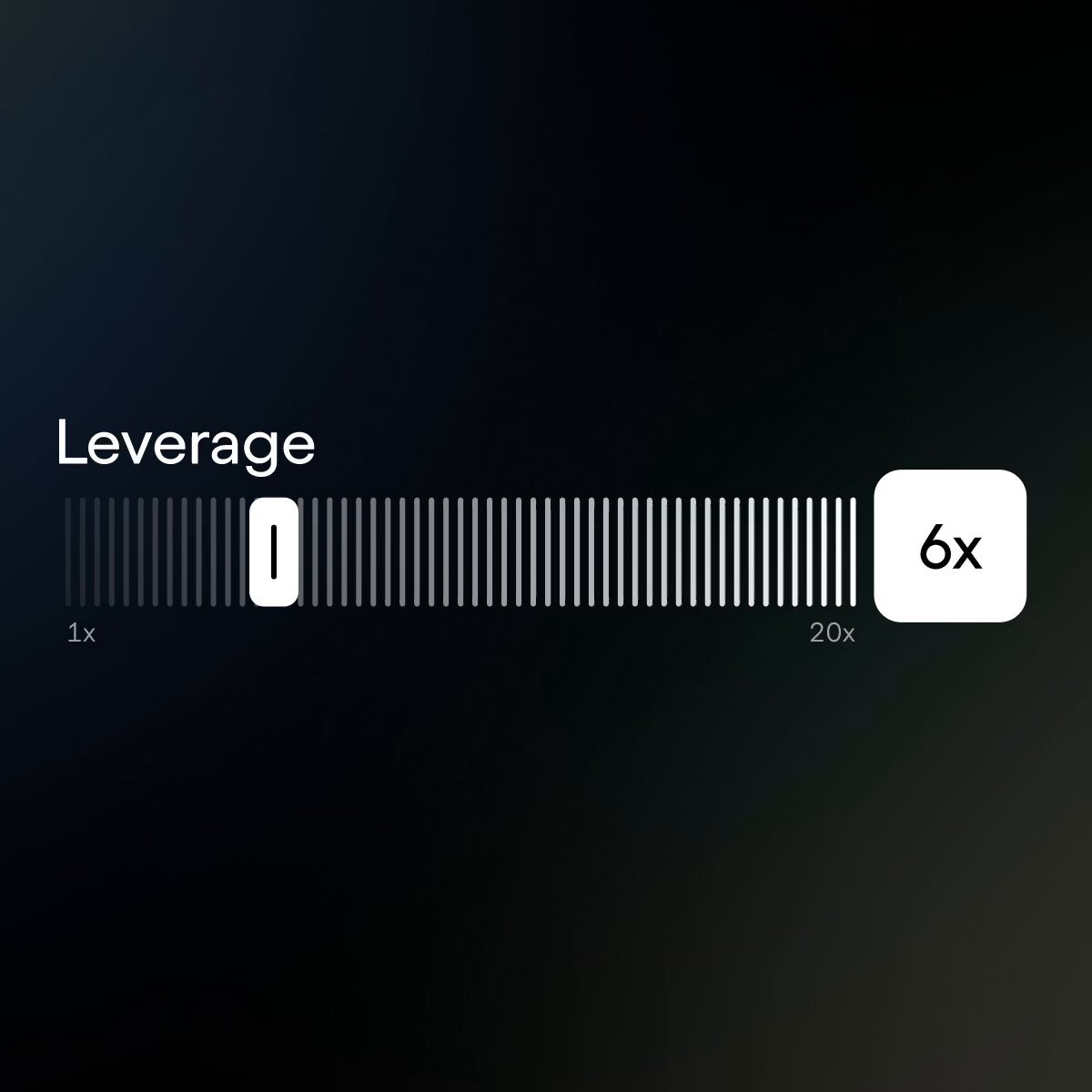

3.4 Ondo Perps: Leveraged equity trading on‑chain

In addition to spot tokenized stocks and ETFs, Ondo has moved into derivatives via the launch of Ondo Perps, a platform for trading perpetual futures on tokenized equities. Perpetual futures, or “perps,” are derivative contracts without a set expiry date whose price is kept in line with the underlying asset through funding payments between long and short positions. Ondo Perps is designed to let users outside the United States trade leading U.S. stocks and ETFs with leverage of up to twenty times, fully on‑chain.

Under this model, traders can open leveraged long or short positions on tokenized versions of assets like Tesla, Nvidia, or ETFs tracking indices such as the S&P 500, with the ability to open, manage, and close positions at any time of day. A distinctive feature of Ondo Perps is its collateral model: traders can post their tokenized stock holdings themselves as margin, rather than needing to convert everything into stablecoins or other base assets. For example, someone holding tokenized Tesla shares on Ondo Global Markets could use those shares as collateral to open a leveraged position on Nvidia, thereby unlocking additional capital efficiency without moving funds off‑platform.

Ondo Perps is explicitly not available to users in the United States, reflecting the fact that perpetual futures on equities are not permitted for U.S. retail traders under current regulations. Access restrictions, geofencing, and compliance measures are therefore integral to the product’s rollout. Nonetheless, the launch of equity perps underscores the broader thesis behind Ondo Global Markets: once equities and ETFs are tokenized and fully integrated into DeFi infrastructure, they can be used not only for spot investment but also as the basis for a rich derivatives ecosystem, including leverage, hedging, and structured products.

For the market as a whole, this blurring of boundaries between traditional securities and DeFi‑style derivatives raises new opportunities and regulatory questions. It could, for instance, make it much easier for global traders to hedge exposure to U.S. tech stocks or to express thematic views via leveraged baskets. At the same time, regulators may scrutinize these products closely, particularly with respect to investor protection, market integrity, and the cross‑border provision of derivatives to retail users.

- 01USDY/OUSG yield adoption↗

The MANTRA savings vault story dominated by 2.6x because it showed a live DeFi product paying real yield through Ondo's tokenized treasury wrapper — proof the mechanism works at scale.

- 02TradFi giants on-chain via Ondo↗

JPMorgan settling a transaction on a public ledger using Ondo infrastructure made abstract institutional tokenization suddenly concrete and credible.

- 03SEC regulatory positioning↗

Readers tracked Ondo's direct SEC lobbying and its objection to Nasdaq's tokenized-securities plan as a window into which rules will govern the entire RWA sector.

- 04Multi-chain USDY expansion↗

Each new chain integration (Cosmos, Solana, Polygon, Ethereum, Mantle, Arbitrum) signals growing liquidity reach for a yield product that competes with stablecoins.

- 05Tokenized equity access↗

The Global Listing and MEXC partnerships gave retail crypto users day-one access to US IPOs and defense/energy stocks, collapsing the barrier between brokerage and DeFi wallets.

- 06Ondo Chain L1 infrastructure bet↗

Announcing a proprietary Layer 1 raised the strategic stakes — readers wanted to know whether Ondo was building a product or positioning to own the settlement layer for all institutional RWAs.

4. Ondo Chain and RWA Infrastructure

4.1 Design goals and architecture of Ondo Chain

Ondo Chain is a layer‑1 blockchain specifically designed for real‑world asset tokenization and institutional use cases. It was launched in early 2025 as a blockchain infrastructure layer that combines aspects of public and permissioned networks, with the goal of providing a secure, compliant environment for RWA tokens while still enabling interoperability with other chains. Where general‑purpose blockchains like Ethereum are designed for maximal openness and decentralization, Ondo Chain explicitly optimizes for regulatory alignment, institutional trust, and secure integration with off‑chain asset custodians.

A central design feature of Ondo Chain is its network of authorized validators. Unlike typical public chains where anyone can become a validator by staking tokens, Ondo Chain restricts validation rights to pre‑approved entities, typically regulated financial institutions. This limited validator set is intended to reduce certain risks that worry institutional participants—such as front‑running, malicious reorgs, or validator collusion—by concentrating block production in known, legally accountable entities. It also facilitates compliance with know‑your‑customer (KYC), anti‑money‑laundering (AML), and sanctions regimes, as validators can be required to adhere to specific policies or respond to regulatory inquiries.

Another distinctive component is its RWA‑backed staking or “wagering” mechanism, where validators can stake tokenized real‑world assets or other low‑risk assets to secure the network. This approach aims to align the network’s economic security with the value of tokenized RWAs themselves while reducing dependence on volatile crypto‑native tokens. From an institutional perspective, it also makes the staking process more familiar, as it resembles collateralization using regulated assets rather than speculative tokens.

Ondo Chain also features integrated omnichain bridging functionality, enabling assets to move seamlessly between Ondo Chain and other compatible networks without relying heavily on external, often vulnerable bridge protocols. Built‑in oracles and proof‑of‑reserve systems provide ongoing verification of off‑chain asset prices and reserve levels, using consensus mechanisms to ensure data integrity. These components are particularly important for RWA tokens, where the primary risk lies not only in on‑chain contract security but also in the linkage between tokens and underlying assets held by custodians or fund vehicles.

4.2 Cross‑chain settlement with J.P. Morgan Kinexys and Chainlink

One of the most notable demonstrations of Ondo Chain’s potential role in institutional finance came through a collaboration with J.P. Morgan’s Kinexys and Chainlink. Kinexys is J.P. Morgan’s blockchain business unit focused on digital payments, and it operates a permissioned blockchain network for payment settlement known as Kinexys Digital Payments. In a joint test, Kinexys, Chainlink, and Ondo Finance executed a cross‑chain delivery‑versus‑payment (DvP) transaction that settled tokenized U.S. Treasuries against U.S. dollar deposits at J.P. Morgan in real time.

The structure of the test was as follows: Kinexys Digital Payments handled the payment leg, enabling the secure settlement of USD deposits within its permissioned network, while the asset leg utilized Ondo Chain’s testnet, representing tokenized U.S. Treasuries (in this case, OUSG tokens). Chainlink’s Cross‑Chain Interoperability Protocol (CCIP) orchestrated the transaction across the different blockchain networks, coordinating messages and ensuring that the asset and payment transfers were synchronized to achieve true DvP settlement.

This experiment demonstrated the feasibility of fully on‑chain, cross‑chain settlement of tokenized assets and fiat value across networks operated by both banks and public blockchain ecosystems. For Ondo, it was a proof‑of‑concept that its tokenized Treasuries and RWA infrastructure could interface with Tier‑1 bank payment rails and institutional blockchain platforms, potentially paving the way for more scalable and seamless digital payments in the broader digital asset ecosystem. When combined with other developments—such as near‑instant, roughly five‑second settlement of tokenized fund shares highlighted in coverage of Ondo’s integration with BlackRock’s BUIDL fund—these tests suggest a future where tokenized cash, Treasuries, and bank deposits can settle against each other in near real time across multiple networks.

From a strategic perspective, collaborating with J.P. Morgan and Chainlink positions Ondo not just as a token issuer but as a critical component in the plumbing of next‑generation capital markets, tying together public DeFi, permissioned bank chains, and cross‑chain messaging layers. It also illustrates how Ondo Chain’s design—combining authorized validators, proof‑of‑reserve systems, and omnichain interoperability—can appeal to regulated institutions that require high assurances around settlement finality, data integrity, and regulatory compliance.

4.3 Ondo Chain’s role in the RWA ecosystem

Ondo Chain is one element within a multi‑chain strategy rather than an exclusive home for all Ondo assets. Many of the company’s products, including Ondo Global Markets’ tokenized stocks and ETFs, live primarily on general‑purpose networks like Solana, Ethereum, and BNB Chain, where liquidity and user activity are highest. Solana, in particular, has captured a large share of tokenized equity trading volume thanks to its high throughput and low transaction costs, and is a focal point for competition among platforms like Backpack, Ondo, xStocks, and PreStocks over issues such as holder rights, legal structures, and regulatory compliance.

Within this landscape, Ondo Chain can be viewed as a specialized hub for certain RWA workflows that require stricter validation controls, integrated proof‑of‑reserve systems, or direct links to institutional payment networks. For example, tokenized Treasuries or money market fund tokens might be native to Ondo Chain, with bridged representations on other networks for trading and DeFi integrations. Similarly, complex portfolio products or tokenized securities that require specific compliance features could be issued on Ondo Chain while still interoperating with Ethereum, Solana, or other ecosystems via built‑in bridges and CCIP‑style messaging layers.

The existence of a purpose‑built RWA chain also allows Ondo to experiment with novel mechanisms, such as RWA‑backed staking, that might be difficult to implement on external networks due to governance constraints or compatibility issues. It gives the company control over protocol parameters such as validator onboarding, block times, and fee structures, which can be tuned to institutional preferences. At the same time, the multi‑chain reality means that Ondo must carefully manage fragmentation, liquidity, and user experience across networks—a challenge that many tokenization platforms face as they seek to balance the benefits of specialized infrastructure with the gravitational pull of established L1 and L2 ecosystems.

4.4 ONDO token economics and unlock events

Ondo Chain is secured and governed, in part, via the ONDO token, which serves as the native asset of the network. While detailed tokenomics are beyond the scope of the available documents, ONDO is described as playing a key role in the ecosystem, with large allocations earmarked for ecosystem growth and protocol development. On January 17, 2025, Ondo released more than 1.9 billion previously restricted ONDO tokens, worth approximately 2.4 billion dollars at the time, significantly increasing the circulating supply.

According to coverage, around 40% of the unlocked tokens were designated for ecosystem growth—such as incentives, partnerships, or grants—and 42% for protocol development, highlighting the project’s intention to fuel long‑term expansion rather than concentrating ownership solely among early insiders. Token unlock events of this magnitude can sometimes exert downward pressure on price due to increased supply, but in Ondo’s case, previous unlocks had reportedly been followed by significant price increases, illustrating how market perception and fundamental growth can outweigh purely mechanical dilution effects.

The use of ONDO as a native token for a real‑world asset chain also raises interesting design considerations. On one hand, linking the value of the token to the success of the RWA ecosystem creates direct economic incentives for token‑holders to support adoption and usage. On the other, over‑reliance on a volatile native token for security can be problematic for institutional users who prefer low‑risk, predictable collateral. Ondo’s approach—allowing RWA‑backed staking and positioning ONDO alongside tokenized Treasuries and similar assets—suggests an attempt to blend crypto‑native and RWA‑based security mechanisms, potentially smoothing volatility and aligning the network’s value with the underlying tokenized asset base.

5. Market Structure, Competition, and Risks

5.1 Positioning among tokenization and RWA competitors

Ondo Finance operates in a crowded and rapidly evolving field of tokenization and RWA platforms, but several features distinguish its positioning. First, its dual focus on both fixed‑income style products (Treasuries, money market funds, yield‑bearing dollar tokens) and tokenized equities/ETFs gives it a broad footprint across major traditional asset classes. Second, its willingness to build dedicated infrastructure—Ondo Chain—while still issuing assets on popular networks like Solana, Ethereum, and BNB Chain positions it as both an issuer and an infrastructure provider.

In the tokenized Treasuries and money market segment, Ondo competes with products like BlackRock’s BUIDL fund and Franklin Templeton’s BENJI suite. BUIDL is a tokenized USD institutional digital liquidity fund managed by BlackRock, while BENJI represents Franklin Templeton’s tokenized U.S. registered money market funds. Crypto RWA briefings have highlighted how these three platforms—Ondo, BlackRock BUIDL, and Franklin BENJI—collectively anchor a large share of the tokenized cash and government debt market, with each offering somewhat different regulatory and operational characteristics. Ondo distinguishes itself by being natively crypto‑native, with deeper DeFi integrations and an independent chain, whereas BUIDL and BENJI are rooted more squarely in traditional asset management firms experimenting with blockchain as an additional distribution channel.

In tokenized equities, Ondo Global Markets competes with platforms like Backed, Matrixdock, xStocks, PreStocks, and others. The competitive frontier in this segment revolves around the number and quality of tokenized assets available, the legal structure and rights granted to token holders, the quality of custody arrangements, and the breadth of DeFi and exchange integrations. Ondo’s relatively high market share, extensive asset lineup (hundreds of stocks and ETFs), and integration into major wallets and exchanges give it an edge, but competition remains fierce, particularly on Solana where multiple issuers are scrambling for both trading volume and institutional acceptance.

5.2 Legal structure, shareholder rights, and jurisdiction

A recurring theme in tokenized equities is the distinction between economic exposure and legal ownership. As documented in the Exodus Markets launch, tokenized assets offered through Ondo do not typically grant direct shareholder rights in the underlying securities, such as voting or direct participation in corporate actions. Instead, they convey economic exposure to price movements and dividend distributions, with the underlying shares held by a regulated broker‑dealer or custodian that legally owns the securities on behalf of the structure.

This separation is partly a pragmatic response to jurisdictional complexities: enabling full legal shareholder rights for a globally distributed set of token holders would require navigating securities laws in multiple countries, corporate registries, and transfer agent requirements. It is also a risk management choice, as issuers seek to avoid inadvertently offering regulated brokerage services or unregistered securities in certain markets. The trade‑off is that token holders must trust the issuer, custodian, and legal structure to pass through economic benefits fairly, without possessing the same direct governance rights as traditional shareholders.

Ondo has signaled an intention to narrow this gap by partnering with voter‑services firms such as Broadridge to enable proxy voting and similar mechanisms for tokenized stocks. The exact implementation details and legal ramifications will vary by jurisdiction and security, but this approach could allow token holders in certain structures to vote on corporate matters via on‑chain or app‑based interfaces, with votes aggregated and submitted to issuers through conventional channels. If successful, such experiments could point toward a future where shareholder democracy is mediated by tokenization infrastructure while still respecting existing corporate governance frameworks.

5.3 Regulatory risk and cross‑border considerations

Regulatory risk is perhaps the single most important factor for any RWA platform, and Ondo is no exception. Its products implicate securities, derivatives, stablecoin‑like instruments, and payment systems, all of which fall under complex and sometimes conflicting regulations across jurisdictions. The company’s decision to structure OUSG as a 3(c)(7) fund offered under Regulation D with qualified purchaser limits is one way of managing U.S. securities law risk, but it also limits the pool of eligible investors. Similarly, OMMF’s structure as a tokenized money market fund that always redeems at one dollar requires careful adherence to regulations governing money market funds and mutual fund distribution.

On the derivatives side, Ondo Perps is explicitly restricted to non‑U.S. users, reflecting the prohibitions on perpetual equity futures for U.S. retail. This geofencing is necessary but not sufficient: platforms must also ensure that marketing, onboarding, and ongoing operations do not inadvertently create regulatory exposure in restricted territories. At the same time, regulators in other regions may interpret tokenized perps differently, potentially classifying them as complex derivatives that require local licenses or investor protection measures. Ondo’s institutional positioning, risk disclosures, and KYC/AML practices will be crucial in managing these cross‑border dynamics.

Tokenized equities add another layer of complexity, especially where tokens trade on public blockchains accessible worldwide. Questions arise around whether these tokens constitute de facto depositary receipts, synthetic derivatives, or a novel category of digital asset; whether KYC is required at the wallet level or only at the platform level; and how to handle secondary trading across jurisdictions with different securities regimes. Ondo’s use of regulated custodians and stress on economic exposure rather than direct shareholder rights can mitigate some of these concerns but does not eliminate them. Future regulatory guidance—whether from the U.S. SEC, European regulators, Asian securities commissions, or self‑regulatory bodies—will play a large role in determining how such platforms scale and which investor segments they can serve.

5.4 Counterparty, custody, and smart‑contract risk

Ondo’s model reduces certain types of risk compared to uncollateralized or opaque DeFi protocols by relying on fully backed tokens, regulated custodians, and transparent fund structures. However, it introduces or retains other risks that investors should understand. Counterparty risk remains significant: token holders must trust that the custodian indeed holds the underlying assets, that legal claims are enforceable, and that the issuer will honor redemption rights. Proof‑of‑reserve systems, third‑party attestations, and on‑chain disclosures can reduce but not eliminate this risk.

Custody risk is also central, particularly for tokenized equities and ETFs where the link between tokens and underlying securities is mediated by broker‑dealers and custodians. Issues such as segregation of customer assets, rehypothecation limits, and insolvency protections will determine how secure token holders’ claims are in extreme scenarios. For money market funds and Treasuries, systemic risks—such as a sudden freeze in short‑term funding markets—could affect liquidity and pricing, though U.S. government securities remain among the lowest‑risk instruments globally.

On‑chain, smart contract vulnerabilities could potentially lead to mis‑pricing, frozen redemptions, or loss of funds if not carefully audited and monitored. Ondo mitigates some of this by leveraging established blockchains and emphasizing security, but the use of bridging, cross‑chain messaging, and complex token interactions inevitably increases the attack surface. Experiences from other DeFi protocols show that even well‑audited systems can be exploited under certain conditions, so users must weigh these technical risks alongside the more familiar financial and legal ones.

5.5 Market volatility and liquidity dynamics

Tokenization changes the venue and mechanics of trading but does not eliminate underlying market volatility. Tokenized Treasuries may experience price fluctuations as interest rates change, while tokenized stocks and ETFs will reflect the same underlying equity risk as their off‑chain counterparts. However, the on‑chain manifestation of these assets introduces additional liquidity dynamics. For instance, the ability to trade 24/7 can lead to price discovery outside traditional market hours, potentially amplifying reactions to news or macro events as global traders respond before conventional exchanges open.

Liquidity in tokenized markets is often uneven, with certain assets attracting deep liquidity pools and market‑maker support while others remain thinly traded. Early metrics have shown rapid accumulation of volume in specific products like SPCXon or AI‑themed ETFs, especially on high‑throughput chains like Solana and BNB Chain, where transaction costs are low and DeFi integration is extensive. In some cases, decentralized exchange aggregators such as 1inch have routed the vast majority of swap volume for specific tokenized stocks, indicating that on‑chain liquidity is consolidating around a handful of venues and routing protocols. For users, this can mean efficient execution for popular names but slippage and wide spreads for niche assets.

OUSG tokenized short-term Treasury product launches

USDY yield-bearing stablecoin alternative launches

JPMorgan Kinexys settles transaction on public ledger with Chainlink and Ondo

Ondo Chain Layer 1 blockchain for institutional RWAs announced

Ondo meets SEC Crypto Task Force to discuss tokenizing US securities

Ondo launches tokenized equity perpetuals with 20x leverage

Ondo acquires Oasis Pro licensed broker-dealer and ATS operator

Founder and CEO Nathan Allman dies; Ian De Bode named CEO

6. Governance, Leadership, and Community Incentives

6.1 Founder legacy and leadership transition

Ondo’s trajectory has been shaped by its founder, Nathan Allman, who played a central role in conceptualizing and building the platform’s RWA‑centric strategy. In late May 2026, Ondo announced that Allman had passed away unexpectedly, a development that was widely reported across the crypto and RWA sectors. The company described the loss as profound and highlighted Allman’s role in articulating a vision for bridging traditional and decentralized finance through institutional‑grade tokenization.

In the wake of Allman’s passing, longtime president and former McKinsey digital‑assets partner Ian De Bode stepped into the CEO role with immediate effect. De Bode had already been deeply involved in Ondo’s strategic direction and operations, and commentators framed the transition as a real‑world stress test of the often‑repeated claim that “founder risk in DeFi is a meme.” In this case, the sudden leadership change occurred just as Ondo’s platform had surpassed roughly 3.5 billion dollars in TVL and as the RWA sector was coalescing around a small number of large players, including BlackRock and Franklin Templeton.

In public communications following the transition, De Bode and the Ondo team emphasized continuity of vision and a commitment to honoring Allman’s legacy while scaling the platform responsibly. Letters to the community described the path forward, reaffirming Ondo’s mission to build trusted on‑chain investment products and infrastructure and highlighting the strength of its existing partnerships and product pipeline. The episode underscores the importance of robust governance, succession planning, and institutionalization in DeFi‑adjacent projects, particularly as they handle billions in real‑world assets and interact with traditional financial institutions.

6.2 Strategic hires and organizational maturation

Beyond leadership changes at the top, Ondo has continued to professionalize its organization through strategic hires from traditional finance. The recruitment of John Hoffman, a former executive at Invesco and Grayscale, as head of portfolio products is one example. Hoffman’s background in ETFs and digital asset products aligns with Ondo’s focus on building not just individual tokens but coherent, intelligently managed on‑chain portfolios that could mirror or extend the ETF model into the tokenized realm.

Such hires indicate that Ondo aims to compete not only as a crypto protocol but also as a full‑fledged asset manager and infrastructure provider capable of working with institutional clients, regulators, and distribution partners. They also reflect a broader industry pattern: as tokenization matures, successful platforms increasingly resemble hybrid organizations, combining software development, financial engineering, regulatory expertise, and product marketing under one roof.

6.3 Ondo Points and community engagement

To incentivize user engagement and bootstrap ecosystems around its products, Ondo has introduced Ondo Points, a rewards system used to recognize community members and increase awareness of products in the Ondo ecosystem. Community documentation describes Ondo Points as accruing through participation in various campaigns, product usage, and possibly other activities, with points later becoming claimable through dedicated portals.

As of early 2026, Ondo announced that claims were open for Ondo Points earned before April 1, 2026, inviting eligible wallets that had participated in early campaigns to claim their rewards. While the exact conversion or utility of Ondo Points can evolve—ranging from governance influence to fee discounts or future token allocations—the basic mechanism echoes that of other DeFi and Web3 projects that have used points as pre‑token or parallel reward systems to align user behavior with platform growth. For a tokenization platform that depends on both institutional and retail adoption, such incentives can help drive liquidity, experimentation, and brand loyalty, particularly in new product lines such as tokenized perps or portfolio strategies.

The existence of Ondo Points also highlights the dual nature of the Ondo ecosystem: on one side, highly regulated RWA products aimed at institutions; on the other, more experimental, crypto‑native mechanisms for community engagement and distribution. Balancing these two faces—compliance‑heavy institutional finance and community‑driven DeFi culture—will remain a central challenge and differentiator for Ondo as it grows.

7. Conclusion

Ondo Finance occupies a distinctive position at the frontier of real‑world asset tokenization, combining a broad product suite, institutional partnerships, and dedicated infrastructure to bring traditional securities on‑chain. Its core offerings—OUSG, OMMF, USDY, and related tokenized Treasury and money market products—provide on‑chain exposure to low‑risk, yield‑bearing instruments, offering alternatives to both bank deposits and non‑interest‑bearing stablecoins. By wrapping these assets in tokens that can be minted and redeemed around the clock using stablecoins such as USDC, Ondo has created a bridge between the risk‑free rate and DeFi‑style composability, enabling new forms of collateral, settlement, and portfolio construction.

At the same time, Ondo Global Markets has turned tokenized stocks and ETFs into a major growth driver, with hundreds of tokenized securities listed across Ethereum, Solana, and BNB Chain, and integrations with wallets and platforms like Exodus, Ledger, Binance, and others. The platform’s focus on fully backed tokens, regulated custodianship, and evolving shareholder‑rights functionality positions it as a leading contender in the race to “do for stocks what stablecoins did for dollars,” making equities behave as programmable on‑chain primitives. The introduction of Ondo Perps further extends this into derivatives, allowing non‑U.S. traders to access leveraged perpetual futures on tokenized equities, while planned day‑one tokenized exposures to major IPOs such as SpaceX underscore the ambition to make global capital markets accessible via crypto wallets from the earliest moments of trading.

Underpinning these products is Ondo Chain, a purpose‑built RWA blockchain that blends authorized validators, RWA‑backed staking, omnichain bridging, and integrated proof‑of‑reserve systems to offer a compliant, institution‑friendly environment for tokenized assets. Collaborations with J.P. Morgan’s Kinexys and Chainlink, notably the cross‑chain DvP settlement of tokenized Treasuries against bank deposits, underline Ondo’s potential role in the plumbing of next‑generation financial infrastructure, where tokenized cash, Treasuries, and equities settle across multiple networks in near real time.

Ondo’s evolution has not been without challenges, including the sudden death of founder Nathan Allman and the need to manage complex regulatory, legal, and technical risks. The leadership transition to Ian De Bode, the recruitment of seasoned asset‑management professionals, and the ongoing expansion of product lines suggest that the organization is moving toward greater institutional maturity. At the same time, community‑oriented initiatives like Ondo Points signal a continued commitment to crypto‑native engagement and distribution models. As the RWA and tokenization sector matures and consolidates, Ondo’s ability to navigate regulation, secure institutional partnerships, and maintain on‑chain composability will determine whether it can sustain its early lead and help define how trillions of dollars of traditional assets migrate onto blockchains.

Ondo operates at the intersection of securities law and DeFi; its SEC meeting, objection to Nasdaq's tokenization plan, and acquisition of licensed broker-dealer Oasis Pro all confirm that regulatory posture is existential, not peripheral.

OUSG and USDY yields are mechanically tied to US Treasury rates; a Fed rate-cutting cycle directly compresses the yield advantage that drives Ondo's entire value proposition against stablecoins.

Tokenized assets require permissioned whitelists, institutional custodians (e.g. Copper MPC custody), and off-chain redemption rails — the on-chain wrapper is decentralized but the underlying asset control is not.

Holders of OUSG and USDY bear indirect exposure to the custodians and fund managers holding the underlying Treasuries; a failure at that layer would not be recoverable on-chain.

Cross-chain USDY fungibility via LayerZero and Cosmos IBC multiplies the attack surface across bridge contracts operating on different security models simultaneously.

OUSG's 24/7 conversion to PayPal USD and deep integrations across Compound, Drift, and MANTRA suggest improving secondary market depth, though thin on-chain order books remain a risk during stress.

Outlook

Looking ahead, Ondo Finance sits at the confluence of several powerful trends: the institutionalization of crypto, the tokenization of traditional securities, and the integration of AI‑driven portfolio management with on‑chain infrastructure. If the analogy to the ETF boom holds, the addressable market for tokenized Treasuries, money market funds, and thematic equity portfolios could reach into the tens of trillions of dollars over the coming decades, with platforms like Ondo providing the rails through which those assets are issued, traded, and managed on‑chain.

In the near term, the most significant catalysts for Ondo will likely include regulatory clarity around tokenized securities and yield‑bearing dollar products, expanded partnerships with asset managers and banks, and the continued growth of tokenized equity trading on high‑throughput chains like Solana and BNB Chain. Successful execution of day‑one tokenized IPO exposures, broader rollout of voting rights and corporate‑action support for tokenized stocks, and deeper integration of OUSG and OMMF into DeFi lending and derivatives protocols would all further entrench Ondo’s role in crypto markets.

At the same time, risks remain substantial. Regulatory pushback, custody failures, smart‑contract exploits, or major market dislocations in government debt or equity markets could all test the resilience of tokenized RWA platforms. Competition from both crypto‑native rivals and traditional asset managers launching their own tokenized products will also intensify. For now, however, Ondo Finance represents one of the clearest examples of how real‑world assets can be brought on‑chain at institutional scale, providing a case study for how crypto markets may evolve from speculative trading venues into core components of the global financial system.

Latest Ondo Finance news

Sources

- https://ondo.finance

- https://x.com/OndoFinance

- https://ondo.finance/ousg

- https://www.marketsmedia.com/ondo-partners-with-mirae-asset-to-tokenize-global-x-etfs/

- https://www.jpmorgan.com/payments/newsroom/kinexys-chainlink-ondo-tokenized-asset-test

- https://www.thestreet.com/crypto/innovation/ondo-is-bringing-leveraged-stock-trading-on-chain

- https://support.exodus.com/support/en/articles/15173689-getting-started-with-exodus-markets

- https://ondo.finance/blog/ledger-wallet-supports-tokenized-stocks

- https://ondo.foundation/points/campaigns

- https://x.com/OndoFinance/status/2059054473775894797

- https://x.com/OndoFinance/status/2067242920856477819

- https://blog.bitso.com/blog/ondo-chain-rwa

- https://ondo.finance/blog/tokenizing-money-market-funds

- https://www.facebook.com/cryptosrus/posts/dan-tapiero-crypto-is-going-to-50-trillion-20t-bitcoin-1m-per-btc-eth-sol-and-ot/1638023368329492/

- https://unchainedcrypto.com/exodus-and-ondo-launch-exodus-markets-with-more-than-200-tokenized-stocks-and-etfs-on-solana/

- https://www.instagram.com/reel/DZerJIGTMuU/

- https://financefeeds.com/ian-de-bode-ondo-3-5b-rwa-platform-after-allman-death/

- https://news.futunn.com/en/post/74551732/tokenization-mirrors-the-20-trillion-etf-boom-as-blockchain-and

- https://podcasts.apple.com/es/podcast/blackrock-buidl-ondos-5-second-settlement-securitizes/id1884049332?i=1000770972368&l=ca

- https://www.mckinsey.com/industries/financial-services/our-insights/the-stable-door-opens-how-tokenized-cash-enables-next-gen-payments

Community notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…