Stablecoins explained: how fiat-backed, crypto-collateralized, and hybrid designs work, why payments and yield are the key battlegrounds, and what GENIUS Act regulation means for USDC and the broader market.

+33 sources across the wider coverage universe

Fed's reliance on third-party data highlights stablecoin oversight gaps2026-04

Fed's reliance on third-party data highlights stablecoin oversight gaps2026-04 IMF calls Tether's Bitcoin reserves a vulnerability, warns stablecoins susceptible to runs2026-04

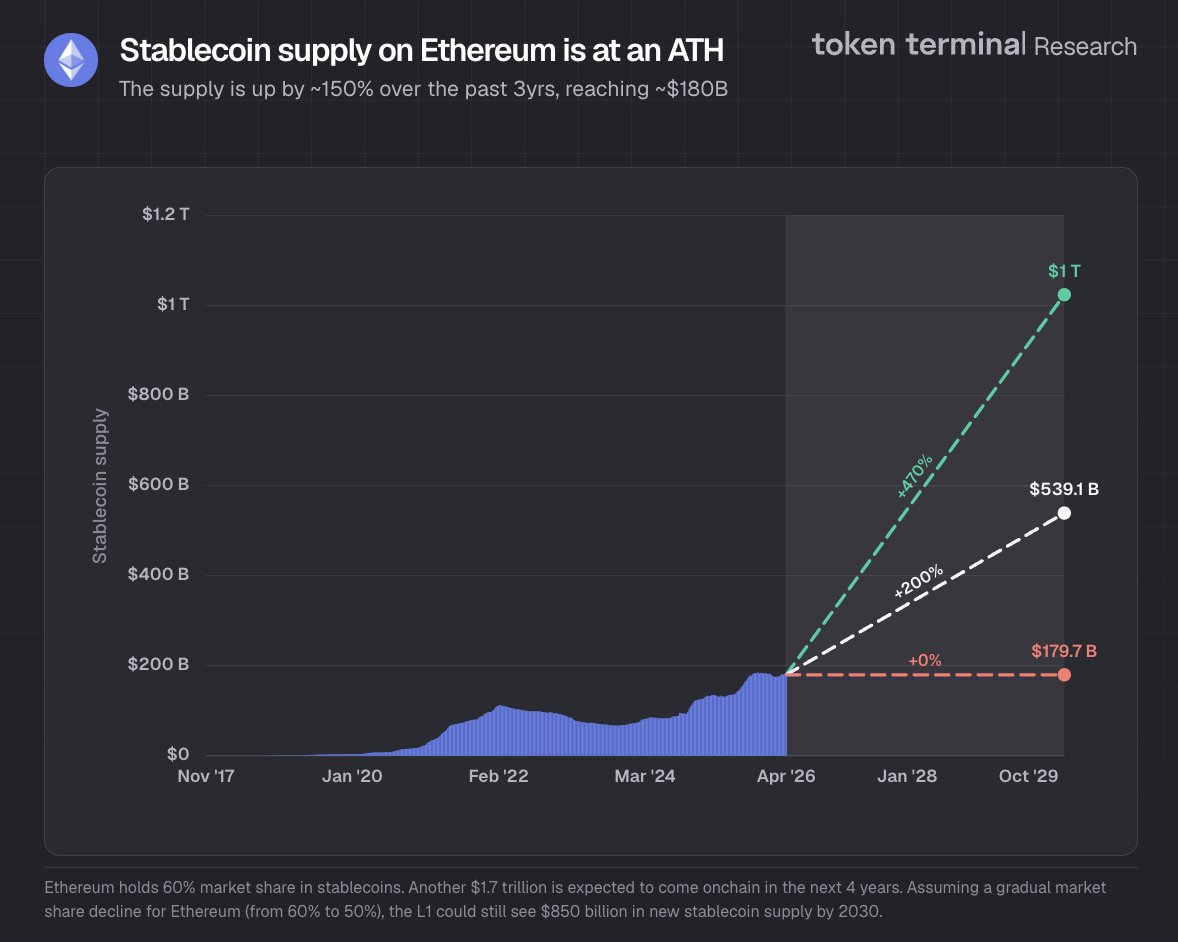

IMF calls Tether's Bitcoin reserves a vulnerability, warns stablecoins susceptible to runs2026-04 Ethereum stablecoin supply hits $180B ATH with 60% market share, up 150% in three years2026-04

Ethereum stablecoin supply hits $180B ATH with 60% market share, up 150% in three years2026-04 Crypto card usage surges to $600M monthly volume, tripling YoY as stablecoins power everyday payments and reduce reliance on traditional off-ramps2026-04

Crypto card usage surges to $600M monthly volume, tripling YoY as stablecoins power everyday payments and reduce reliance on traditional off-ramps2026-04 MoneyGram partners with NALA to enable stablecoin-powered cross-border payouts, settling in digital dollars and delivering local currencies2026-04

MoneyGram partners with NALA to enable stablecoin-powered cross-border payouts, settling in digital dollars and delivering local currencies2026-04 Tether poaches JPMorgan exec to bolster US stablecoin expansion2026-04

Tether poaches JPMorgan exec to bolster US stablecoin expansion2026-04

Dollar-pegged tokens and their equivalents that keep a fixed value on blockchain networks, stablecoins have evolved from a niche trading tool into core infrastructure for global payments, decentralized finance, and sovereign-currency alternatives.

What a Stablecoin Is — and How It Holds Its Peg

A stablecoin is a cryptographic token whose value is designed to track a reference asset — almost always the U.S. dollar, though Swedish krona, euro, and other currency variants exist. Unlike bitcoin or ether, whose prices float freely, stablecoins achieve price stability through one of three mechanisms:

Fiat-backed reserves. The issuer holds cash, Treasury bills, or money-market instruments worth at least one dollar for every token in circulation. Tether (USDT) and Circle's USDC are the dominant examples. Circle publishes weekly reserve attestations; USDC's reserves are held primarily in short-duration U.S. Treasuries and cash held at regulated financial institutions, which is why Fidelity recently launched a GENIUS Act-aligned money market fund specifically designed as a reserve vehicle for stablecoin issuers.

Crypto-collateralized designs. Protocols like MakerDAO's DAI hold excess collateral in other crypto assets to absorb volatility. Because the collateral itself can fall in price, these systems are typically overcollateralized — a $1 DAI might be backed by $1.50 in ETH — and rely on liquidation mechanisms when collateral ratios deteriorate.

Algorithmic or hybrid approaches. These attempt to maintain the peg through code-driven supply expansion or contraction, sometimes backed by a volatile secondary token. The catastrophic collapse of TerraUSD in 2022 demonstrated the systemic risk of poorly designed algorithmic models, setting back the category significantly. Ethereum co-founder Vitalik Buterin has more recently proposed an options-based design that would leverage ETH upside buyers to create stability without debt, liquidations, or funding rates — an approach that has reignited academic debate but has yet to see production adoption at scale.

BIS says stablecoins fall short as money, warns of emerging-market risks in annual report

$312B of stablecoin float is already a liquidity layer, and USDT alone is about $185B with roughly $88B of that on Tron. BIS can win the taxonomy fight on singleness, elasticity, and integrity and still lose distribution: EM users are not holding USDT because it is pristine money, they are holding it because local banking rails, FX controls, and weekend settlement are worse. Project Agorá/tokenized deposits have to beat that UX in production, not just clear the central-bank checklist.

Readers click stablecoin stories not for yield mechanics but for power consolidation — who controls the reserve (BlackRock, Paxos, regulators), who gets frozen out, and which sovereign currency wins the dollar-vs-euro-vs-DeFi war.

The Reserve Yield Question

Fiat-backed stablecoins generate significant revenue because their issuers earn interest on the reserves backing each token — yet, historically, retail holders earned nothing. A 2024 BIS Bulletin (No. 125) formalized what practitioners already understood: centralized exchanges pay stablecoin holders using either reserve returns (yield that tracks policy interest rates) or activity-based income from their own trading operations. Reserve-based yields move predictably with central bank rates; activity-based yields are volatile and opaque.

This bifurcation matters for macro-financial stability. If stablecoins become effective substitutes for bank deposits, their reserve portfolios become a meaningful channel through which Federal Reserve rate decisions transmit into crypto markets. Conversely, if exchanges are funding stablecoin yields through risky proprietary trading, a sharp drawdown could force rapid redemptions — a dynamic regulators are watching closely.

Coinbase has moved aggressively here. Its partnership with Circle gives Coinbase a revenue share on USDC reserves, a relationship that became a material line item as rates rose post-2022. The model illustrates how the stablecoin yield question is not just a product feature but a structural business question: who captures the carry, and under what disclosure obligations?

- 01BlackRock reserve capture

Three separate headlines about BUIDL backing Frax and Ethena drove readers to track whether TradFi is quietly taking control of DeFi stablecoin collateral.

- 02Regulatory fragmentation TradFi risk

ESRB and FSB warnings about systemic risk from stablecoin-TradFi integration drew the single highest click count, signaling readers watch macro prudential threat as a top-tier story.

- 03Euro stablecoin sovereignty

ECB, Société Générale, Keyrock, Coinbase EURC, and non-USD de-dollarization pieces clustered together, revealing readers tracking whether Europe can field a credible dollar alternative.

- 04Centralized freeze and censorship risk

The $2 billion frozen headline and Huione illicit stablecoin expose readers' concern that permissioned stablecoins are a surveillance and seizure vector.

- 05DeFi stablecoin mechanism design

Frax v3 leaks, Curve crvUSD peg data, f(x) Protocol sPOSITIONs, and the Inverse Finance Monolith proposal show readers actively tracking novel collateral and leverage architectures.

- 06Stablecoin issuer consolidation exits

Binance terminating BUSD, FlowBank bankruptcy hitting Anchored Coins customers, and Paxos Singapore approval together signal readers watching who survives the issuer shakeout.

Stablecoins as Payment Rails

The most consequential near-term use case is payments. On-chain stablecoin volume crossed $390 billion according to recent industry data — a figure that rivals some mid-sized national payment networks. The appeal for cross-border transfers is straightforward: settlement in seconds rather than days, no correspondent banking fees, and 24/7 availability.

Several recent launches underscore how quickly institutional players are moving onto stablecoin rails:

- MoneyGram launched MGUSD on the Stellar network, allowing remittance recipients to hold and spend digital dollars — though the product comes with the same caveats as any custodial stablecoin, including freeze risk and limits on redemption.

- Zelle, the P2P payments brand operated by the largest U.S. banks, announced Zelle USD for international payments, a striking signal that traditional financial infrastructure is treating stablecoins as a viable rails extension rather than a competitive threat.

- Shinhan Card scaled Solana-based stablecoin rails across a customer base of 28 million South Koreans, one of the largest deployments of stablecoin payments infrastructure outside the United States.

- AllUnity launched SEKAU, a fully reserved Swedish krona stablecoin, across Ethereum, Solana, Base, Tempo, and Polygon — illustrating the multi-chain, multi-currency direction the market is heading.

Integrating stablecoins into a payment product, however, is not simply a matter of accepting USDC at checkout. Compliance infrastructure — sanctions screening, anti-money-laundering controls, transaction monitoring — must be built before or alongside any stablecoin payment flow. Tempo's Jevgenijs Kazanins has argued publicly that banks cannot scale stablecoin payments without rigorous sanctions screening and fund-freeze capabilities, a position that's gaining ground as regulatory scrutiny intensifies. Solutions such as WalletConnect Pay now offer pre-settlement sanctions screening, indicating the compliance tooling layer is maturing rapidly.

Onchain money laid the foundation for tokenized assets, with Treasuries, money market funds and equities now following stablecoins onto blockchain rails

RWA.xyz has tokenized Treasuries/MMFs around $14.7B distributed value, while tracked stablecoins sit near $296B with ~$6.7T in 30-day transfer volume; the cash leg already dwarfs the asset leg. BUIDL, USYC, USDY and OUSG start changing DeFi market structure once they plug into Aave/Morpho/perps collateral loops with sane liquidation and whitelist handling. Equities are the dangerous leg: Robinhood/OpenAI showed that a token wrapper without issuer consent, redemption rights and shareholder mechanics is synthetic exposure wearing a chain logo.

- 2023-08milestone

Binance terminates BUSD support alongside Paxos

- 2024-01governance

Frax v3 details leaked by Sam Kazemian

- 2024-06exploit

FlowBank bankruptcy triggers Anchored Coins customer losses

- 2024-11launch

Ethena Labs unveils USDtb backed by BlackRock BUIDL

- 2025-01governance

Vote to onboard BUIDL as Frax USD backing asset goes live

- 2025-06regulatory

Paxos gains Singapore MAS approval for stablecoin issuance

- 2025-08regulatory

Coinbase enables euro-to-EURC 1:1 conversions under MiCA

- 2025-09milestone

Ethereum stablecoin volume reaches record $1.46 trillion

The Regulatory Landscape: GENIUS Act and Beyond

The United States passed the GENIUS Act in mid-2025, establishing the first federal framework for payment stablecoins. Five U.S. agencies — including the Federal Reserve and FinCEN — have since jointly proposed customer identification requirements for stablecoin issuers modeled on existing bank rules. The proposal would require issuers to verify the identity of holders at onboarding, bringing stablecoin customer due diligence broadly in line with the Bank Secrecy Act.

In Europe, MiCA (Markets in Crypto-Assets) created a licensing framework for electronic money tokens and asset-referenced tokens, but the crypto industry is already lobbying for a MiCA 2.0 that would address gaps around DeFi composability and cross-border stablecoin flows that the original regulation did not anticipate.

In Australia, OSL secured an Australian Financial Services Licence (AFSL) specifically authorizing wholesale stablecoin payments, custody, and OTC trading — a sign that regulated stablecoin infrastructure is being built jurisdiction by jurisdiction, rather than waiting for a single global standard.

The compliance argument is increasingly straightforward: stablecoin compliance infrastructure cannot wait for full regulatory clarity. Issuers that build AML and KYC controls now will be better positioned when rules solidify, while those that defer risk being locked out of regulated payment corridors entirely.

- CentralizationHigh

Over $2 billion in stablecoin balances have been frozen by issuers, and BlackRock's BUIDL is being adopted as reserve collateral across multiple DeFi stablecoins, concentrating systemic dependency on a single TradFi actor.

- RegulatoryHigh

ESRB flagged stablecoin-TradFi integration as a rising financial stability risk, the ECB is pushing a digital euro as a defensive response to dollar-backed crypto dominance, and the FSB issued cross-border supervisory guidance for global stablecoin arrangements.

- LiquidityMedium

Ethereum stablecoin volume hit $1.46 trillion but DAI's dominance is partly attributable to wash trading and high transfer frequency, making true organic liquidity depth difficult to assess.

- Smart-contractMedium

Novel mechanism designs like f(x) Protocol sPOSITIONs with fixed leverage and liquidation brakes introduce untested on-chain logic, while Curve crvUSD's tight peg data suggests its AMM-based design is holding but remains unproven at scale.

- MarketMedium

Non-USD stablecoins are shifting from speculative instruments to operational necessity in Europe and LATAM, but competitive dynamics remain uncertain as dollar-backed incumbents (USDT, USDC) dominate volumes.

- CounterpartyMedium

FlowBank's bankruptcy caused potential losses for Anchored Coins customers, and Huione's illicit marketplace launching its own stablecoin demonstrates that counterparty provenance risk extends into criminally-operated issuers.

Non-Dollar Stablecoins and Emerging Use Cases

The narrative that stablecoins are inherently "dollar instruments" is eroding. AllUnity's SEKAU (Swedish krona) joins a growing list of non-dollar stablecoins targeting regional treasury management, FX hedging, and local payment ecosystems. The euro-backed EURC from Circle and various pound-denominated experiments reflect demand from multinational firms that need to settle in local currencies without touching traditional correspondent banking.

Beyond currency pegging, stablecoin primitives are finding novel applications:

Tokenized deposit hybrids. Custodia Bank and Vantage are testing a token that toggles between a bank deposit and a stablecoin on Ethereum — maintaining FDIC-adjacent protection when the holder wants it, and on-chain composability when they don't. This architecture could become the template for how chartered banks enter the stablecoin market without abandoning deposit insurance frameworks.

Real-world asset financing. USDAI is using stablecoins to fund GPU loans for non-crypto AI cloud infrastructure, addressing a genuine financing gap in the AI buildout where traditional lenders lack the speed and flexibility operators require. This represents a maturation of the "RWA" (real-world asset) thesis: stablecoins as working capital, not just trading instruments.

DeFi capital layers. Protocol designers increasingly distinguish between stablecoins optimized for DeFi composability (where programmability and permissionlessness matter most) and those designed for institutional use (where regulated custody, clean yield structures, and AML compliance are non-negotiable). Products like USDf and fUSD are being explicitly positioned to serve both audiences without conflating them.

South Korea's biggest banks, fintechs and internet giants are racing to build stablecoin and RWA infrastructure ahead of regulatory clarity, reshaping Asia's blockchain landscape

RWA.xyz has stablecoins at about $295.6B, with USDT and USDC still around $271B of that, so a KRW coin is fighting dollar network effects before it fights other Korean issuers. The Bank of Korea's bank-only preference is the chokepoint: deposit-token wrappers inside KB/Shinhan/Hana rails would be clean but boring, while a license path for Kakao, Naver Pay, Toss, Upbit/Bithumb-style distribution could turn Korea's retail liquidity premium into actual settlement collateral. Watch whether these assets get DeFi-grade portability and RWA redemption hooks, or just another permissioned wallet balance with a blockchain logo.

Market Structure and Concentration Risk

USDT and USDC together account for the substantial majority of all stablecoin market capitalization, creating concentration risk that regulators and protocol designers have flagged repeatedly. Tether's reserve disclosures have historically been less granular than Circle's, though both have maintained their pegs through periods of significant market stress.

Token Terminal's redesigned stablecoin dashboards — tracking product mix, market share, and chain distribution by issuer — reflect growing investor demand for granular visibility into how stablecoin supply is distributed across chains and custody relationships. The fragmentation of stablecoin supply across Ethereum, Solana, Base, Tron, and other networks complicates both risk assessment and regulatory oversight.

FV Bank's launch of a unified fintech platform for stablecoins, payments, and programmable finance signals another trend: the convergence of banking services and stablecoin infrastructure into single products rather than parallel stacks that require bridging.

Outlook

Stablecoins are no longer a crypto-native instrument being considered for mainstream use; they are mainstream payment infrastructure being formalized into regulatory frameworks. The coming years will be defined by several parallel contests: fiat-backed versus crypto-collateralized models, U.S. dollar dominance versus multi-currency expansion, and compliance-first issuers versus permissionless protocol designs.

Yield distribution — who earns the reserve carry and under what rules — will likely become a central regulatory and competitive battleground as stablecoins approach deposit-like scale. The institutions entering the space in 2025 and 2026, from Zelle to Fidelity to Shinhan Card, suggest that the answer will look more like regulated financial products than the bearer instruments early stablecoin pioneers envisioned. What remains to be determined is how much of the original permissionless architecture survives contact with that regulatory reality.

Latest Stablecoins news

BIS says stablecoins fall short as money, warns of emerging-market risks in annual reportOnchain money laid the foundation for tokenized assets, with Treasuries, money market funds and equities now following stablecoins onto blockchain railsSouth Korea's biggest banks, fintechs and internet giants are racing to build stablecoin and RWA infrastructure ahead of regulatory clarity, reshaping Asia's blockchain landscape Arc launches open-source stablecoin FX app on testnet, pitching a flagship multi-currency hub for global stablecoin finance

Arc launches open-source stablecoin FX app on testnet, pitching a flagship multi-currency hub for global stablecoin finance How Paypal Is Racing To Keep Its Lead In Stablecoins With PYUSD

How Paypal Is Racing To Keep Its Lead In Stablecoins With PYUSD BitGo cuts nearly 15% of workforce to refocus on stablecoins, settlement, and AI infra

BitGo cuts nearly 15% of workforce to refocus on stablecoins, settlement, and AI infraCommunity notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…