USDT (Tether) is the world's largest stablecoin by market cap, pegged 1:1 to the US dollar and used as the primary trading and settlement currency across crypto exchanges and DeFi protocols globally.

+26 sources across the wider coverage universe

TON taps Swiss-licensed SCRYPT to open institutional USDT rails for banks and fintechs2026-04

TON taps Swiss-licensed SCRYPT to open institutional USDT rails for banks and fintechs2026-04 Bank of AI goes live on TRON, building financial plumbing for autonomous agents atop $86B in USDT liquidity2026-04

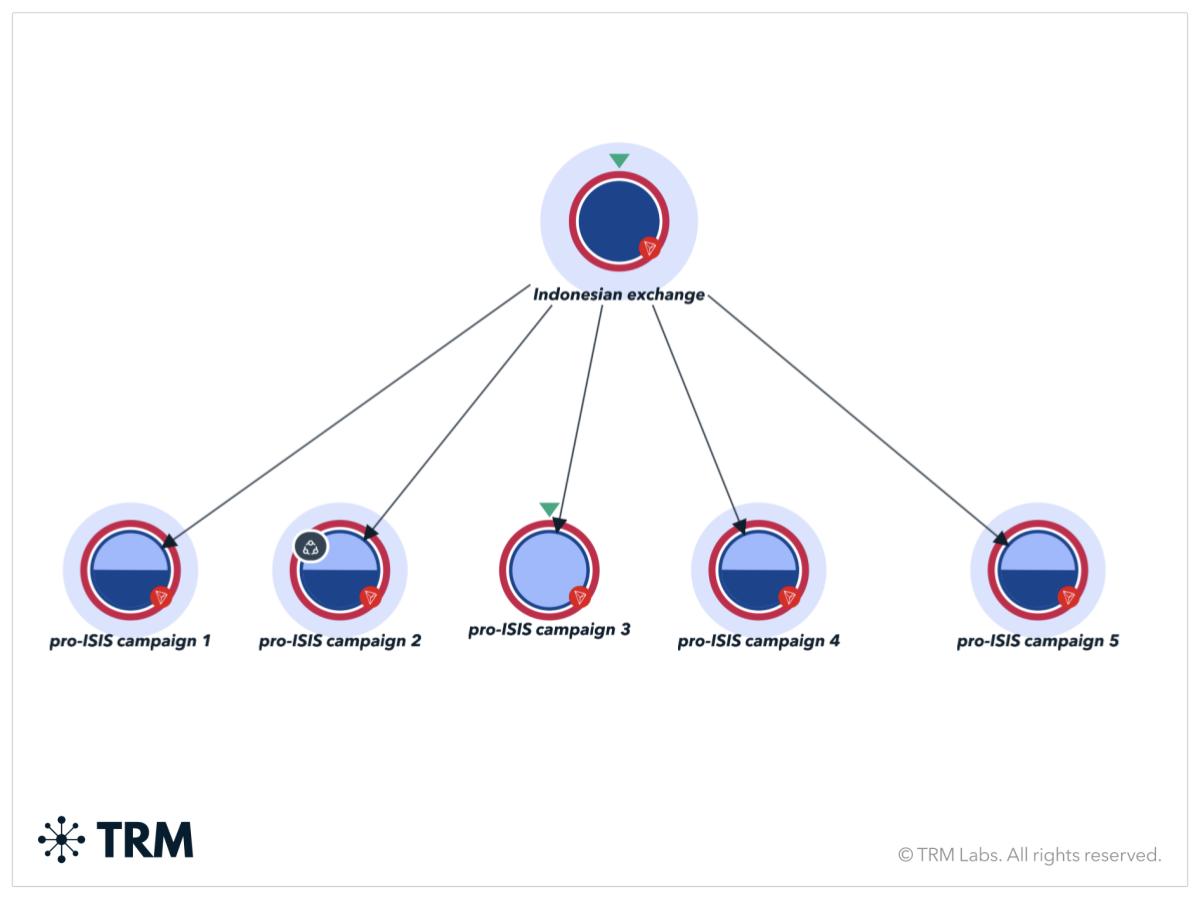

Bank of AI goes live on TRON, building financial plumbing for autonomous agents atop $86B in USDT liquidity2026-04 Indonesia convicts 3 terrorism financiers after onchain USDT trails linked funds to ISIS-affiliated networks2026-04

Indonesia convicts 3 terrorism financiers after onchain USDT trails linked funds to ISIS-affiliated networks2026-04 Spark seeds Uniswap v4 with $150M in USDS-PYUSD and USDS-USDT liquidity for stablecoin FX layer2026-06

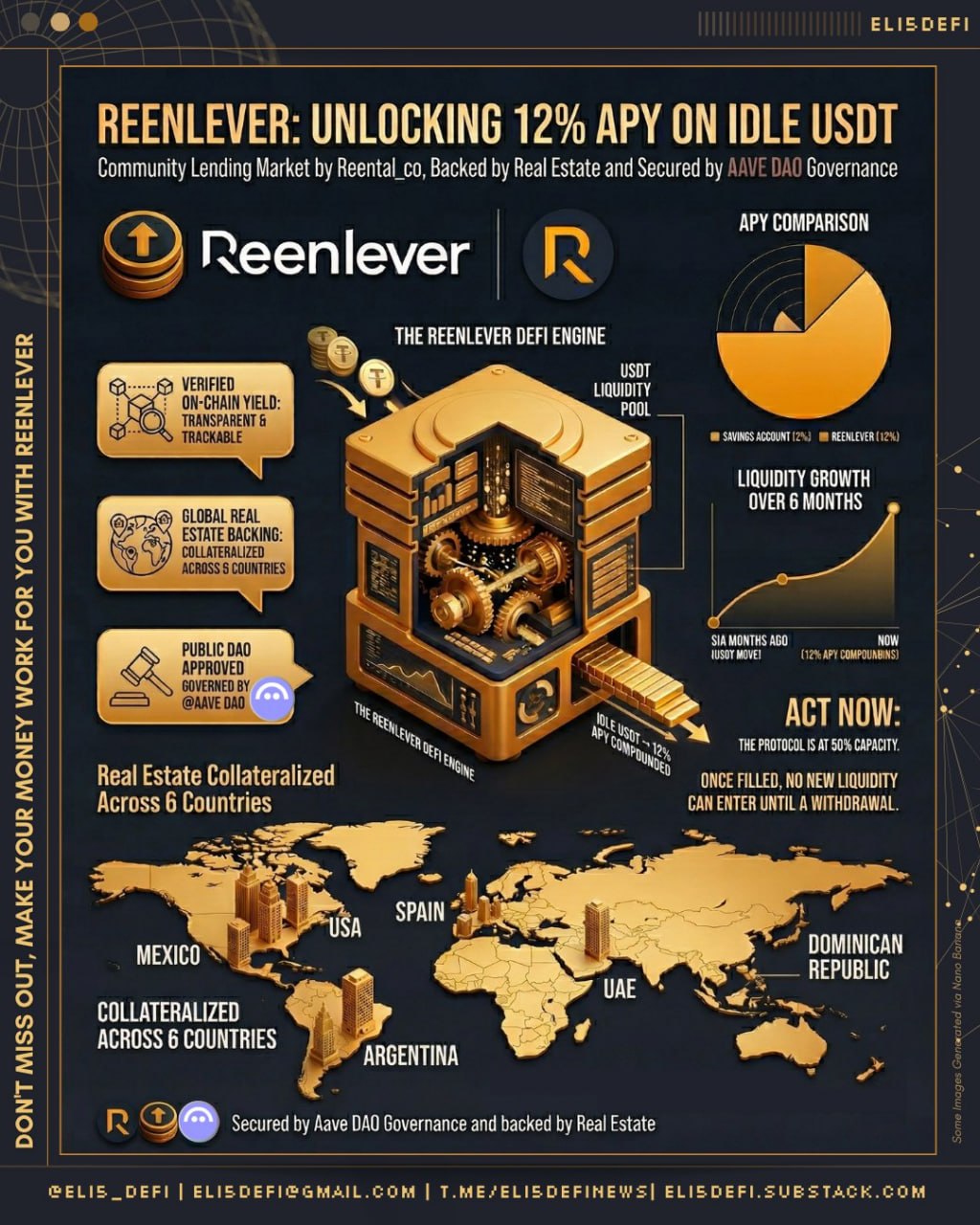

Spark seeds Uniswap v4 with $150M in USDS-PYUSD and USDS-USDT liquidity for stablecoin FX layer2026-06 Real estate company Reental's community lending market, Reenlever generates 12% APY on idle USDT.2026-04

Real estate company Reental's community lending market, Reenlever generates 12% APY on idle USDT.2026-04 Peter Thiel-backed Ramp launches zero-fee USDT↔USD conversions across its platform, expanding support for Ethereum, Solana and Plasma as stablecoin payments gain traction2026-04

Peter Thiel-backed Ramp launches zero-fee USDT↔USD conversions across its platform, expanding support for Ethereum, Solana and Plasma as stablecoin payments gain traction2026-04

Tether (USDT) is a fiat-collateralized stablecoin pegged 1:1 to the US dollar, designed to move value across blockchain networks without exposing holders to cryptocurrency price volatility.

What USDT Is and How It Works

At its simplest, USDT is a digital token whose value is meant to always equal one US dollar. Tether Limited — the Hong Kong-based company that issues it — claims to hold reserves of cash, cash equivalents, and other assets sufficient to back every token in circulation. When a user deposits dollars with Tether, new USDT is minted; when they redeem, tokens are burned and dollars are returned. This mechanism is called fiat collateralization, as opposed to algorithmic or crypto-collateralized designs used by other stablecoins.

USDT runs on more than a dozen blockchains, including Ethereum (as an ERC-20 token), Tron (TRC-20), BNB Chain, Solana, Avalanche, Ton, and Aptos, among others. Multi-chain deployment is a deliberate infrastructure choice: it lets traders move liquidity wherever transaction fees are lowest or settlement is fastest. A temporary suspension of USDT withdrawals on the Aptos network — noted in recent exchange bulletins — illustrates the kind of chain-specific maintenance events users encounter in a multi-chain world.

Spark seeds Uniswap v4 with $150M in USDS-PYUSD and USDS-USDT liquidity for stablecoin FX layer

Spark deployed about $150 million into two Ethereum Uniswap v4 pools, pairing USDS with PYUSD and USDT as the first phase of its Stablecoin FX Layer. The initial rollout uses standard v4 pools, with Spark planning a later Shared Liquidity Layer and DualPool hook after separate security review. The pitch is simple: stablecoin issuers get shared onchain liquidity instead of each rebuilding market makers, inventory, and venues from scratch.

Readers click USDT stories not for stablecoin mechanics but for two opposing forces: Tether aggressively expanding its rails into every chain and corridor while regulators, sanctions enforcers, and competitors simultaneously chip away at its legitimacy — the tension between ubiquity and untrustworthiness is the real story.

The Origins: From Realcoin to Market Dominance

Tether launched in 2014 under the name Realcoin before rebranding. It was built on the Omni Layer protocol atop Bitcoin, making it one of the earliest token issuances on BTC. The project's early history is inseparable from Bitfinex, the cryptocurrency exchange that shared ownership with Tether Limited under the iFinex corporate umbrella. That relationship attracted regulatory scrutiny: in 2021, the New York Attorney General's office settled with both companies after finding that Tether had temporarily used Bitfinex's funds to cover an $850 million shortfall, requiring $18.5 million in penalties and a prohibition on serving New York customers. Tether admitted no wrongdoing but agreed to regular reporting of its reserve composition.

Despite the controversy, the product found product-market fit at a scale no one predicted. USDT became the default unit of account across centralized and decentralized trading venues — the "dollar of crypto."

Reserve Composition and Transparency Debates

Tether's reserve disclosures have evolved substantially over the years, driven partly by regulatory pressure and partly by competitive pressure from rival stablecoins. Tether now publishes quarterly attestations (not full audits) from the Italian accounting firm BDO, showing that the majority of reserves are held in US Treasury bills.

As of early 2025 reporting, Tether held over 80% of reserves in cash and cash equivalents, primarily short-term T-bills, making it one of the world's larger holders of US government debt. Smaller portions are allocated to secured loans (which attracted criticism), precious metals, and bitcoin. Tether has also introduced Tether Gold (XAUt), a separate token backed by physical gold, which platforms like Ledn have recently accepted as collateral for USDT and US dollar-pegged loans — part of a broader trend in which tokenized commodities are approaching 17% of relevant market share.

Critics argue that quarterly attestations fall short of the full annual audits that traditional financial institutions provide, and that the secured-loan portfolio introduces counterparty risk. Tether maintains that its disclosed holdings exceed total USDT in circulation, creating an "overcollateralization" buffer.

- 01Cross-chain USDT rail expansion

Wormhole's native 7-network transfer (999 clicks), USDT0 omnichain unification, TON integration, and Rabby gas abstraction show readers tracking Tether's infrastructure land-grab as the defining liquidity story.

- 02Tether minting as market signal

The $1.3B post-Aug-5 mint and the EOS/Algorand deprecation read together as readers using Tether's supply decisions as a real-time sentiment indicator for crypto market cycles.

- 03Sanctions and illicit-finance exposure

The $20B Garantex investigation and the T3 unit's $100M Tron freeze (including North Korea-linked funds) pulled readers tracking how USDT's permissionless reach becomes a liability under law enforcement scrutiny.

- 04Reserve audit transparency deficit

Tether's talks with a Big Four firm over $140B in issued USDT drew readers who see the long-delayed audit as the single unresolved systemic risk underneath the entire stablecoin ecosystem.

- 05Regulatory delisting pressure

Crypto.com's MiCA-driven USDT delisting in Europe and the Philippines regulator-triggered 7% discount dump show readers watching geographic fragmentation of USDT access as a concrete regulatory outcome.

- 06Stablecoin market structure shifts

XRP overtaking USDT in market cap, RLUSD entering the arena, and DAI's $960B volume lead (adjusted for wash trading) signal readers tracking whether USDT's dominance is structurally durable or already eroding.

USDT as Trading Infrastructure

More than any other single asset, USDT functions as the connective tissue of crypto markets. Virtually every centralized exchange — Binance, Bybit, KuCoin, HTX, Upbit, Bithumb — denominates most of its trading pairs in USDT. When South Korea's Upbit added nine new tokens including PEAQ, LIT, and MORPHO in June 2026, it opened BTC and USDT markets simultaneously, reflecting the standard dual-quote model most exchanges use. Similarly, HTX's launch of EVAA/USDT perpetual futures with up to 10x leverage shows how USDT is the default settlement currency for derivatives exposure as well.

This infrastructure role means USDT supply acts as a rough proxy for capital entering or leaving crypto markets. When USDT market cap grows, it often signals fresh fiat is being on-ramped; when it shrinks, it can indicate redemptions or migration to other stablecoins.

Perpetual futures denominated in USDT — sometimes called "USDT-margined" or "linear" perps, as opposed to coin-margined "inverse" contracts — have become the dominant derivatives format. Bybit's Global Assets Trading Fest, featuring $202,000 USDT in prizes across TradFi and crypto markets, and prize pools of 20,000 USDT on KuCoin for new token launches, illustrate how USDT-denominated incentives have become standard marketing currency in the industry.

USDT vs. USDC: The Stablecoin Rivalry

The most significant competitor to USDT is USD Coin (USDC), issued by Circle, a US-based company. The two stablecoins account for the overwhelming majority of the stablecoin market, but they serve somewhat different audiences.

USDC has positioned itself around regulatory compliance and transparency. Circle maintains full attestations through major accounting firms and has proactively sought US money-transmitter licenses. USDC is the preferred stablecoin in many DeFi protocols, institutional integrations, and US-regulated contexts.

USDT dominates on centralized exchanges and in emerging markets, particularly in Asia and Latin America, where it functions as a dollarization tool for people with limited access to traditional banking. Tether processes more daily on-chain transfer volume than USDC across most metrics.

The two tokens occasionally compete for liquidity in DeFi pools. A recent Curve Finance update funded a new pool seeded with MIM, USDT, and USDC — a common pattern in which protocols balance liquidity across both stablecoins to minimize slippage and reduce single-issuer risk.

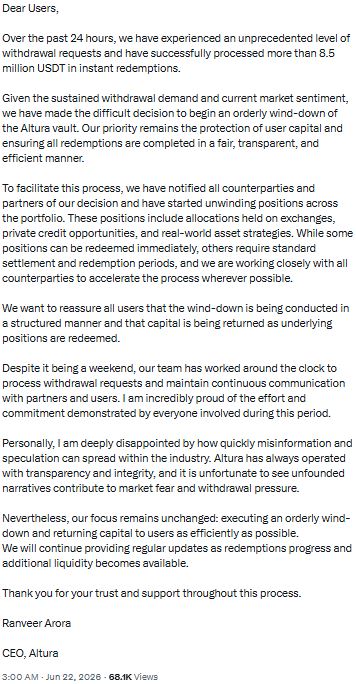

Altura’s vault loses $8.5 million to USDT redemptions, forcing an orderly wind-down on Hyperliquid

$8.5M of redemptions against Altura's own recent $38M AUM claim is a ~22% one-day bank run, and it came right after the team said it had already processed $5M while denying any Mainstreet/MSY exposure. The weak spot is the maturity stack: HyperEVM stablecoin deposits with 72-hour/instant-with-fee withdrawal UX backed by exchange balances, private credit, and RWA legs. Solvent can still mean illiquid in DeFi when every depositor sees the same exit door, so future RWA vaults need live liquidity buckets, counterparty exposure, and redemption queue data on the front page.

- 2022-11milestone

Stablecoin market cap hits $140B record high amid USDC and USDT resurgence

- 2024-08milestone

Tether mints $1.3B USDT following Aug 5 market bottom

- 2024-09milestone

Tether reports 330M on-chain USDT wallets by Q3 2024, record 36.25M new users

- 2024-10launch

USDT and XAUT launch on Telegram's TON blockchain, reaching 900M user base

- 2024-11regulatory

T3 Financial Crime Unit freezes $100M in USDT on Tron, including North Korea-linked funds

- 2024-12regulatory

U.S. and UK open investigation into $20B USDT flows through sanctioned Russian exchange Garantex

- 2025-01regulatory

Crypto.com delists USDT and nine tokens in Europe under MiCA compliance deadline

- 2025-02launch

Tether introduces USDT0, unifying USDT liquidity across all chains via omnichain architecture

Regulatory and Legal Risks

Tether operates in a complex regulatory environment. In the United States, the company does not hold a banking license and direct retail access for US persons is limited. The European Union's Markets in Crypto-Assets (MiCA) regulation, which took effect in stages through 2024, imposes reserve, audit, and volume requirements on stablecoin issuers. As of mid-2025, USDT was not listed on major European exchanges under MiCA-compliant terms, pushing Tether to explore regulatory engagement rather than retreat from European markets.

In South Korea, authorities have demonstrated enforcement interest in USDT-related crime: police arrested 23 individuals in an $11 million USDT money-laundering case, illustrating how the pseudonymous nature of blockchain transfers can attract illicit use even as exchanges themselves implement increasingly robust KYC/AML programs.

Anti-money-laundering compliance has become a more active area for Tether. The company has cooperated with law enforcement requests to freeze USDT addresses linked to sanctioned entities and illicit activity — a capability built into the ERC-20 contract via a blocklist function. By 2024, Tether had frozen hundreds of millions of dollars in USDT across multiple jurisdictions.

Yield, Earning, and DeFi Integration

Holding USDT itself pays no yield — Tether retains the interest earned on its T-bill reserves. But the ecosystem around USDT has built extensive yield-generating infrastructure. Binance Earn has offered promotional rates on USDT Simple Earn, including limited campaigns at 35% APR, though sustained rates are typically in the 3–8% range depending on market conditions.

DeFi lending protocols like Aave, Compound, and their forks allow users to lend USDT to borrowers or use it as collateral. Curve Finance's stablecoin pools generate fee income from arbitrageurs keeping prices in peg. The yield available on USDT is inversely correlated with broader crypto risk appetite: in bull markets, demand for borrowed USDT rises (traders want leverage), pushing rates up; in bear markets, rates compress.

- CentralizationHigh

A single private issuer (Tether) unilaterally controls minting, redemption, blacklisting, and chain support — as demonstrated by the simultaneous deprecation of EOS and Algorand without governance vote.

- RegulatoryHigh

Active U.S./UK sanctions investigations tied to the $20B Garantex corridor, MiCA-forced European delistings, and a Chinese underground banking crackdown collectively show USDT at the center of multi-jurisdiction enforcement actions.

- Reserve / CounterpartyHigh

With over $140B USDT issued and no completed Big Four audit, reserve backing remains unverified by an independent attestor, creating a systemic trust gap that competitors are actively exploiting.

- Smart-Contract / BridgeMedium

USDT's expansion across 7+ chains via Wormhole and omnichain USDT0 multiplies bridge attack surface; the $50M loss swapping USDT for AAVE illustrates that multi-hop DeFi routes introduce non-obvious execution risk.

- LiquidityMedium

The sharpest monthly supply drop since the FTX collapse in February 2024 and Poloniex's withdrawal from stUSDT show that redemption pressure and protocol-level exits can rapidly compress circulating supply.

- Market / CompetitionMedium

RLUSD pending NYDFS approval, DAI leading raw on-chain volume, and XRP briefly overtaking USDT in market cap indicate that USDT's dominance is under structural challenge from multiple regulated and decentralized alternatives.

USDT Market Capitalization and Supply Dynamics

USDT's market capitalization crossed $100 billion in 2023 and has continued to grow, making Tether one of the most systemically significant entities in crypto by any measure. The minting and burning process is highly responsive to market demand: in periods of high crypto trading activity, new USDT is minted rapidly; during downturns, net redemptions reduce supply.

Tether's profitability — driven by the spread between near-zero cost of issuance and T-bill yields — became conspicuous when interest rates rose in 2022–2023. The company reported billions in quarterly profit, a fact that both validated the business model and raised questions about why users receive none of it.

Security Considerations for USDT Holders

USDT is not risk-free. The primary risks are:

- Issuer risk: If Tether Limited became insolvent or its reserves were proven to be insufficient, USDT could lose its peg permanently. This is sometimes called de-pegging risk.

- Smart contract risk: Bugs in the token contract on any given chain could expose funds to theft or freezing.

- Regulatory risk: Government action could restrict USDT use or force redemption programs.

- Blacklist risk: Tether can freeze specific addresses; users whose addresses are flagged lose access to their USDT balance on-chain.

- Bridge risk: Moving USDT across chains via third-party bridges introduces additional smart contract exposure.

The 2022 collapse of TerraUSD (UST), an algorithmic stablecoin with no fiat backing, reinforced market preference for fiat-collateralized models like USDT and USDC, even as questions about Tether's reserve practices persisted.

Outlook

USDT's dominance in crypto trading infrastructure appears durable for the medium term. Its network effects — universally quoted on every major exchange, the default settlement currency for perpetual futures, deeply embedded in DeFi liquidity pools — create switching costs that competitors have struggled to overcome despite years of effort.

The outstanding questions are regulatory. MiCA compliance remains unresolved for European markets. US stablecoin legislation, if enacted, could require Tether to either seek a banking or payment license or exit the US market more formally. Tether has signaled intent to engage with regulation rather than flee it, and its recent investments in transparency reporting suggest an awareness that the era of operating in regulatory grey zones is narrowing.

The broader stablecoin market — of which USDT commands roughly half — is growing as institutional adoption of blockchain settlement infrastructure expands. Competition from USDC, PayPal's PYUSD, and potential central bank digital currencies will pressure Tether's market share over the long term. For now, USDT remains the closest thing the crypto industry has to a universal currency.

Latest USDT news

Community notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…