Deep dive explainer on TRX, the native token of Tron, covering its role in stablecoin rails, staking and DeFi, institutional adoption, governance, risks, and how Tron’s low‑cost DPoS network competes with Ethereum in the stablecoin era.

+6 sources across the wider coverage universe

TRON’s Justin Sun launches TRX Earn on Telegram with boosted yields up to 13.61% APY, combining base rewards and a limited 60-day bonus for new users2026-04

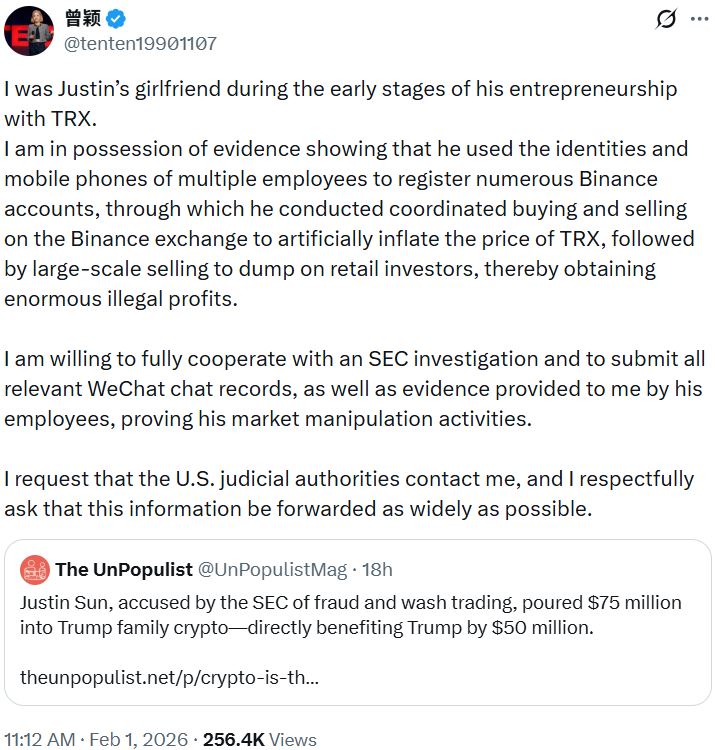

TRON’s Justin Sun launches TRX Earn on Telegram with boosted yields up to 13.61% APY, combining base rewards and a limited 60-day bonus for new users2026-04 Lady claiming to be Justin Sun's girlfriend during the early stages of his entrepreneurship with TRX, request that the U.S. judicial authorities contact her. She expressed willingness to fully cooperate with an SEC investigation and to submit all relevant WeChat chat records, as well as evidence provided by his employees, proving his market manipulation activities.2026-02

Lady claiming to be Justin Sun's girlfriend during the early stages of his entrepreneurship with TRX, request that the U.S. judicial authorities contact her. She expressed willingness to fully cooperate with an SEC investigation and to submit all relevant WeChat chat records, as well as evidence provided by his employees, proving his market manipulation activities.2026-02 Anchorage Digital brings Tron inside regulatory perimeter with institutional TRX custody and staking2026-03

Anchorage Digital brings Tron inside regulatory perimeter with institutional TRX custody and staking2026-03 Justin Sun says gas-free transfers of stablecoins coming to Tron this year2024-07

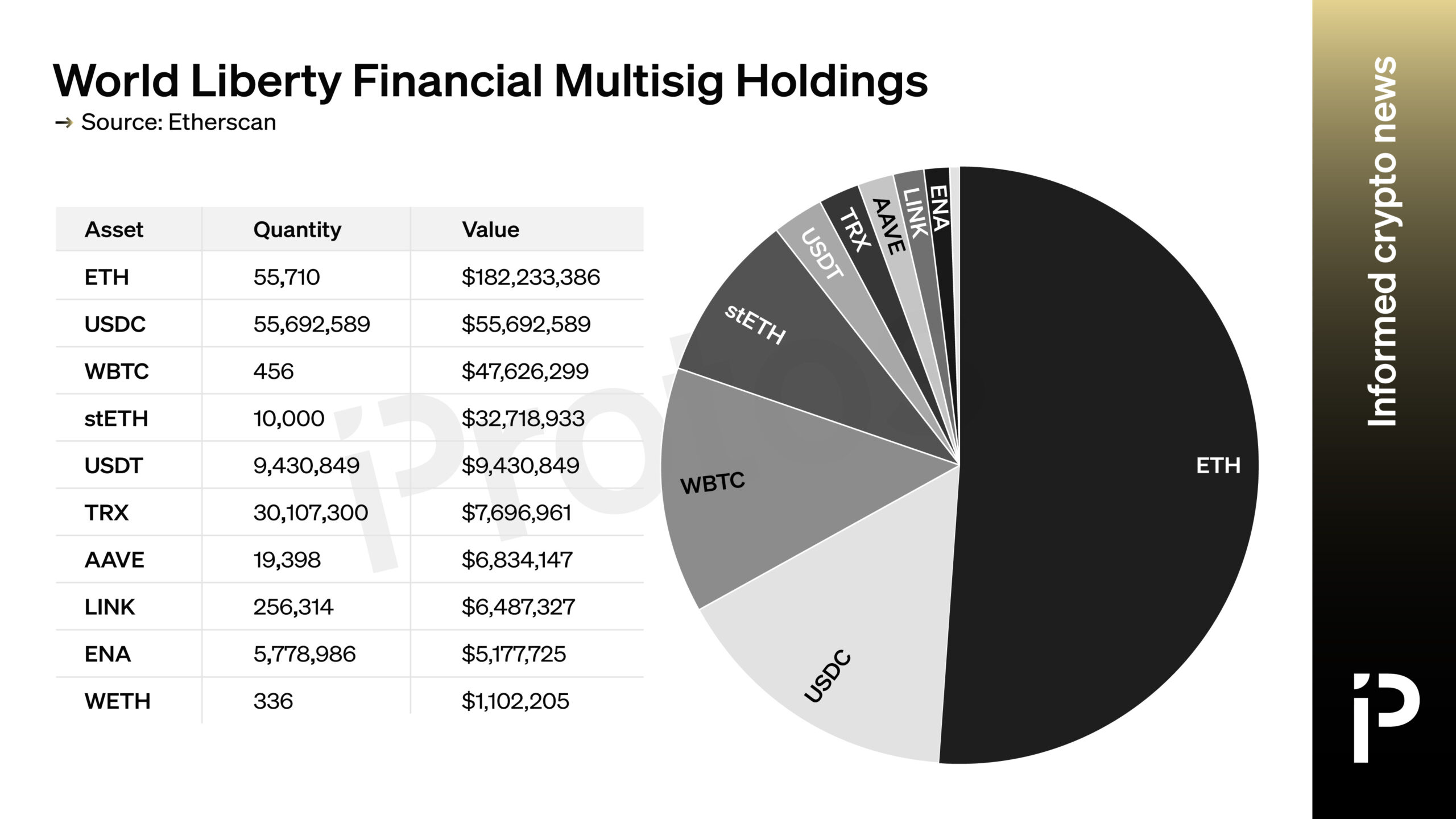

Justin Sun says gas-free transfers of stablecoins coming to Tron this year2024-07 Trump backed World Liberty Financial to acquire TRX for treasury2025-01

Trump backed World Liberty Financial to acquire TRX for treasury2025-01 World Liberty Financial has been diversifying its holdings, acquiring assets including Justin Sun-affiliated TRX and WBTC.2025-01

World Liberty Financial has been diversifying its holdings, acquiring assets including Justin Sun-affiliated TRX and WBTC.2025-01

TRX: An Evergreen Guide to Tron's Native Token and Stablecoin Engine

As the native token of the Tron blockchain, TRX underpins one of the most widely used smart‑contract networks for stablecoin transfers, payments, and DeFi applications, particularly around USDT and other dollar‑pegged assets. Built on a delegated proof‑of‑stake architecture and a resource model that makes most transfers effectively free, TRX functions simultaneously as gas token, staking asset, governance tool, and key collateral inside a rapidly evolving on‑chain financial system.

TRX today sits at the intersection of three large themes in crypto: the rise of low‑cost settlement layers for stablecoins, the institutionalization of digital asset infrastructure, and intensifying regulatory scrutiny around centralized actors. Tron’s network has emerged as a dominant venue for USDT, with tens of billions of dollars in circulating Tether on TRC‑20 rails and a broader stablecoin market cap near ninety billion dollars. At the same time, new listings on compliant exchanges such as Binance.US and regulated custody support from Anchorage Digital are pulling TRX and TRC‑20 assets further inside the traditional financial perimeter, even as on‑chain governance experiments, DeFi incentives, and algorithmic stablecoins like USDD introduce meaningful risk. This explainer traces how TRX works, what it does inside the Tron ecosystem, why stablecoins matter so much to its value proposition, and how emerging institutional and regulatory dynamics could shape its long‑term trajectory.

What Is TRX?

TRX, sometimes referred to by its long form Tronix, is the native cryptocurrency of the Tron blockchain, a decentralized proof‑of‑stake network with smart contract functionality and its own virtual machine for running dApps. The Tron project was founded by entrepreneur Justin Sun in 2014, with the Tron Foundation established in Singapore in 2017 to oversee development and steward the ecosystem. From its earliest marketing, Tron positioned itself as an open‑source infrastructure for digital entertainment and content distribution, designed to let creators publish and monetize work without relying on centralized platforms or intermediaries. TRX, in that original vision, would serve both as a medium of exchange within this content economy and as the core token used to secure and operate the underlying network.

Over time, the focus of Tron’s usage has shifted from pure content distribution toward a broader role as a high‑throughput public blockchain for payments, stablecoins, and decentralized finance. Tron supports smart contracts and token standards such as TRC‑20, enabling developers to issue fungible tokens, including major stablecoins like Tether’s USDT, on its rails. TRX is the asset that users consume or lock up to obtain the network resources—bandwidth and energy—required to submit transactions and interact with these token contracts. In addition, the token is central to Tron’s delegated proof‑of‑stake (DPoS) governance system, where holders can stake TRX to vote for so‑called Super Representatives (SRs) who produce blocks and validate the chain. Taken together, these roles make TRX analogous to ETH on Ethereum: it is simultaneously a utility token, a staking asset, and a governance instrument embedded in nearly every economic action on Tron.

Tron’s native token has also become deeply intertwined with the rise of dollar‑denominated stablecoins. The network has evolved into one of the most important settlement layers for USDT, and to a lesser extent USDC and the algorithmic stablecoin USDD, with TRX acting as the unit users need to pay for transaction resources when moving those dollar assets. Much of TRX’s demand is therefore now indirectly tied to stablecoin activity, whether through users topping up small balances to cover fees, DeFi protocols using TRX as collateral alongside stablecoins, or staking products that blend TRX yields with stablecoin‑denominated incentives. As the stablecoin market grows and competition among base layers intensifies, the relationship between TRX and these dollar tokens has become central to understanding the project’s long‑term prospects.

TRON’s Justin Sun launches TRX Earn on Telegram with boosted yields up to 13.61% APY, combining base rewards and a limited 60-day bonus for new users

13.61% APY on TRX when base staking yields sit around 3-4% — that ~10% delta is pure user acquisition subsidy that burns off after 60 days. Sun's running three parallel demand sinks right now: Telegram Earn, the Canary Capital staked TRX ETF filing (advertising 4.5% yield), and the sTRX→USDD dual-profit loop. All designed to lock up circulating supply while TRX price action stays flat despite growing network activity. Convenient timing too — this drops weeks after the $10M SEC settlement cleared Rainberry's regulatory overhang.

Readers click TRX for the paradox of simultaneous institutional embrace and regulatory abandonment — Trump's World Liberty Financial buys in while Circle exits, Binance drops TRC20 USDC, and the SEC labels TRX a security, revealing Tron as crypto's most politically charged stablecoin settlement layer rather than a DeFi platform.↗

Origins, Leadership, and Governance

The Tron ecosystem is closely associated with its founder, Justin Sun, a Chinese‑born Kittitian entrepreneur who has become one of the most prominent billionaires in crypto. Sun founded Tron in 2014 and has remained the project’s public face, overseeing its rapid expansion into smart contracts, DeFi, and stablecoins, including the launch of the USDD algorithmic stablecoin under the TRON DAO Reserve. According to biographical reporting, he has accumulated substantial wealth from his crypto ventures, with Forbes estimating his net worth in the multi‑billion‑dollar range by 2026, underscoring how closely his personal brand and capital base are bound up with Tron’s trajectory. While Tron emphasizes decentralized governance through its DAO and Super Representative structure, Sun’s influence—both perceived and actual—remains an important factor in how markets and regulators view TRX.

Institutionally, Tron has gone through a governance evolution. In its early years, the TRON Foundation, a non‑profit entity based in Singapore, oversaw protocol development and ecosystem funding. In subsequent years, governance has increasingly been framed as community‑driven under the TRON DAO, a decentralized autonomous organization that Sun describes as steering the network’s direction. Official communications around events like exchange listings and partnerships now typically emphasize the DAO, as in the announcement of TRX’s listing on Binance.US, which described TRON DAO as “the community‑governed DAO dedicated to accelerating the decentralization of the internet through blockchain technology and decentralized applications.” In practice, this means protocol changes are proposed and voted on through on‑chain governance processes that require TRX staking and voting power, even as core development remains tightly coordinated.

Sun’s leadership has sometimes attracted controversy, and more recently it has intersected with growing regulatory scrutiny. In the project’s early years, critics accused Tron of borrowing heavily from other open‑source codebases without adequate attribution, and Sun’s aggressive marketing tactics have occasionally drawn skepticism in the wider industry. More recently, according to claims that have surfaced in connection with U.S. regulatory interest, a woman identifying herself as Sun’s girlfriend during the early days of TRX has publicly offered to cooperate with U.S. judicial authorities, including the SEC, and to provide chat records and internal employee evidence she says demonstrate market manipulation around TRX. These allegations have not yet been adjudicated in court, but they illustrate the degree to which Tron’s founder remains under the regulatory microscope and how potential enforcement actions could impact TRX’s reputational and legal environment. For holders and users, understanding this founder‑driven dynamic is essential, because it differentiates Tron from more diffuse, less personality‑centric projects.

At the same time, Tron Inc.—the corporate arm associated with the project—continues to publish financials that speak to the ecosystem’s economic viability. Recent reports indicate that Tron Inc. recorded net income of over twelve million dollars in the third quarter of 2025, suggesting that the combination of network‑related revenue, ecosystem services, and possibly corporate holdings of TRX and other assets is generating meaningful cash flow. While these corporate results are distinct from the on‑chain economics of TRX itself, they point to a broader picture in which the Tron ecosystem functions not only as a decentralized network but also as a business with operating income, partnerships, and strategic investments. The interplay between the DAO narrative and this corporate reality will continue to shape perceptions of TRX in both crypto‑native and institutional circles.

How the Tron Network Works

Delegated Proof‑of‑Stake and Super Representatives

At the core of Tron’s architecture is a delegated proof‑of‑stake (DPoS) consensus mechanism, which differs in important ways from both traditional proof‑of‑work systems like Bitcoin and the proof‑of‑stake design now used by Ethereum. In DPoS, token holders do not typically run their own validating nodes directly; instead, they vote with staked tokens—TRX in Tron’s case—to elect a limited set of validator nodes known as Super Representatives (SRs). These SRs are responsible for packaging transactions into blocks, proposing them to the network, and reaching consensus on the canonical chain, earning block rewards and a share of transaction fees in return. The number of SRs is intentionally small relative to the total number of token holders, which allows the network to achieve relatively high throughput and low latency compared with most proof‑of‑work systems.

The Tron developer documentation emphasizes that DPoS is designed to balance decentralization with performance by making validator selection a fluid, token‑weighted voting process. TRX holders can delegate their voting power to preferred SR candidates and can redelegate at any time, theoretically enabling the community to remove underperforming or malicious SRs. In practice, however, DPoS systems often exhibit significant concentration of voting power among large holders, exchanges, and ecosystem funds, raising perennial questions about how decentralized the validator set actually is. While the documentation stresses that SR selection is based on the number of votes received and that many nodes can theoretically compete, the fact that only a small group ultimately produces blocks means that network governance can be influenced by a limited number of actors with large TRX stakes.

Compared with Ethereum’s proof‑of‑stake design, in which tens or hundreds of thousands of validators attest to blocks and finalize the chain, Tron’s SR model prioritizes performance and cost over maximal decentralization. Public comparisons note that Tron offers high throughput and low transaction fees, with average transaction costs reported as significantly lower than on Ethereum. This design choice has been crucial to Tron’s positioning as a low‑cost settlement layer for stablecoins and high‑frequency transfers, but it also means that the network’s security and censorship resistance are more reliant on a relatively small set of elected validators and on the broader political and regulatory environment in which those validators operate. For TRX holders, staking thus entails not only financial considerations but also a view about how this governance trade‑off will be perceived over time.

Resource Model: Bandwidth, Energy, and Fees

One of Tron’s distinctive features is its resource model, which abstracts transaction costs into two main resource types: bandwidth and energy. Bandwidth can be thought of as the resource consumed by the raw data size of a transaction, while energy is consumed by the computational work performed by smart contracts. According to Tron’s developer documentation, each externally owned account on the network receives a daily allocation of free bandwidth—600 units per day—allowing users to perform a certain number of basic transactions, such as simple token transfers, at no cost. Beyond this free allotment, users can acquire additional bandwidth by freezing or staking TRX, or they can pay for it directly, with the unit price of bandwidth currently set at 1,000 sun, where sun is the smallest denomination of TRX.

Energy operates similarly but is more focused on smart‑contract interactions. When a contract executes, it consumes energy, and users must ensure they have sufficient resources to cover this consumption through staked TRX or by paying fees. This dual resource model allows Tron to keep most routine transfers extremely cheap or effectively free for users who maintain even modest TRX stakes, while shifting more of the cost burden to complex contract interactions in DeFi and dApp ecosystems. From a design perspective, this aligns incentives: casual users can interact with stablecoins and simple transfers at trivial cost, while DeFi protocols and power users, who consume more network resources, are encouraged to stake TRX or to bear higher fees.

The result of this resource model is a user experience quite different from Ethereum’s traditional gas mechanism. On Ethereum, every transaction consumes gas, and users must hold ETH to pay for it, with transaction costs fluctuating widely depending on network congestion. On Tron, bandwidth makes everyday token transfers—including USDT stablecoin transfers—predictably low cost, which is one reason Tron has become so prominent for cross‑border payments and remittances. In an interview, Justin Sun has highlighted these characteristics as key to Tron’s ambition to serve as a global settlement layer for issuers and developers worldwide, particularly in the stablecoin space. For TRX, this resource model creates steady baseline demand, since users and applications must either stake or spend TRX to secure the bandwidth and energy required by their activity.

Smart Contracts and TRC‑20 Tokens

Tron supports smart contracts via its own virtual machine, enabling developers to build decentralized applications (dApps) and issue tokens using standards analogous to Ethereum’s ERC‑20. The most relevant of these for the broader crypto economy is the TRC‑20 standard, which defines a fungible token interface that has been widely adopted by stablecoin issuers and DeFi protocols on Tron. Tether’s USDT, for example, is issued as a TRC‑20 token on Tron, enabling users to send and receive dollar‑pegged balances at high speed and low cost; similarly, the USDD algorithmic stablecoin is available on Tron alongside other networks. TRC‑20 tokens leverage the same resource model as native TRX transfers, so users must maintain TRX balances to pay for the bandwidth and energy required to interact with them.

The proliferation of TRC‑20 tokens has transformed Tron from a niche content‑distribution platform into a full‑fledged DeFi and stablecoin ecosystem. Major DeFi protocols such as JustLend DAO, which offers lending, borrowing, and interest‑bearing deposits, are built around TRC‑20 assets, including TRX‑denominated cTokens and stablecoins like USDT and USDD. Decentralized exchanges (DEXs) such as SunSwap enable users to trade between TRC‑20 tokens and native TRX, providing liquidity and price discovery for the entire Tron token economy. The recent launch of SunSwap V4, for instance, has explicitly focused on reducing friction in these interactions by allowing users to trade directly between native TRX and TRC‑20 assets without having to wrap TRX into a separate token first. This tight integration between TRX and TRC‑20 tokens makes TRX an indispensable part of the transaction graph for almost all economic activity on Tron.

From a developer’s standpoint, Tron’s smart‑contract platform offers a familiar environment, with tooling and languages inspired by Ethereum’s ecosystem but optimized for Tron’s performance characteristics. The low fees and predictable resource model make it attractive for applications that require high transaction throughput or serve users in regions where on‑chain fees are particularly sensitive. For TRX holders, this means the token’s demand profile is closely linked not only to end‑user adoption but also to the success of TRC‑20‑based applications and stablecoins that rely on Tron’s infrastructure.

TRX Tokenomics, Staking, and Governance

Staking, TRON Stake 2.0, and Yield

TRX’s role in Tron’s staking system is central to both network security and token economics. In the delegated proof‑of‑stake model, TRX holders can stake their tokens to gain voting power and allocate that power to Super Representative candidates, who in turn share a portion of their rewards with voters. Staking also locks TRX into the network’s resource economy, generating bandwidth and energy that can be used directly by the staker or leased out indirectly via DeFi markets. With the introduction of TRON Stake 2.0, the network has sought to make staking more flexible, reducing frictions around lock‑ups and redemptions while maintaining security guarantees.

One concrete example of how this plays out for users is the SafePal x XYSwap integration, which brings native TRX staking directly into the SafePal wallet ecosystem. According to SafePal, users can stake TRX through its interface with no formal lock‑up period and an estimated annual percentage yield around ten percent, although this rate floats with real‑time supply and demand in the energy rental market and with Super Representative voting reward rates. The staking process leverages TRON Stake 2.0 under the hood and involves a fifteen‑day unstaking cooldown—fourteen days enforced by the protocol and an additional one‑day buffer—during which funds cannot be fully withdrawn. SafePal emphasizes the non‑custodial nature of this staking, particularly when used with its hardware wallets, where private keys remain offline and staking transactions are signed securely on device.

The yields offered by such staking products are composed of multiple streams. First, staked TRX generates voting power, which aggregates into SR rewards distributed back to voters by SRs as part of their incentive schemes. Second, staked TRX produces energy, which can be rented out in markets where DeFi protocols and high‑volume users pay to obtain discounted network resources instead of burning TRX directly. SafePal describes how both income streams—SR voting rewards and energy rental income—are pooled and distributed back to stakers as compounding TRX rewards, producing the headline APY. This dual‑source yield model underscores how deeply staking ties TRX to the broader economic life of the network: staking is not only about consensus security but also about owning a share of the resource economy that powers stablecoin transfers and DeFi.

Beyond wallet‑based staking, the Tron ecosystem has seen the emergence of staking derivatives and yield strategies that wrap staked TRX into liquid tokens. Products like sTRX and staked‑TRX vaults allow users to maintain exposure to TRX staking yields while using derivative tokens as collateral in DeFi protocols or to mint stablecoins such as USDD. For example, recent campaigns have advertised the ability to mint USDD using sTRX and TRX vaults with a low stability fee—around 0.5 percent—and additional reward pools in USDD, creating leveraged exposure to both TRX and stablecoin yields. While such structures can enhance capital efficiency, they also introduce additional smart‑contract and liquidation risks, which users must weigh against the incremental returns.

Governance and On‑Chain Proposals

In Tron’s governance model, TRX is not only a staking asset but also the core instrument of on‑chain voting and protocol change. Holders who stake TRX receive voting rights that can be used to elect Super Representatives and to participate in governance proposals affecting the protocol and major DeFi platforms. This governance layer is visible in systems like JustLend DAO, Tron’s first official lending platform, where key parameters—such as which assets are listed, collateral factors, and reward schedules—are governed through DAO proposals and votes. TRX holders, either directly or through their chosen SRs and delegates, thus exert influence over the evolution of lending markets that are central to Tron’s DeFi economy.

Recent governance initiatives illustrate how this process works in practice. One example is the proposal to add a new “U” stablecoin market to JustLend DAO, introducing the U token as both a supply and borrow asset and integrating a U/TRX price oracle and support for corresponding jTokens in the protocol’s smart contracts. Such a change involves multiple moving parts: oracle integration to ensure reliable pricing, risk assessment to determine appropriate collateral parameters, and smart contract upgrades to handle the new asset. TRX‑based governance serves as the mechanism through which the community can approve or reject these changes, reflecting its priorities around market diversity, liquidity, and risk management. For TRX holders, active governance participation offers a way to shape the direction of DeFi on Tron and to protect the value of their staked capital.

Governance also extends to the infrastructure layer. Oracle providers like WINkLink introduce new price feeds—such as the KGST/TRX pair—through processes that involve both technical deployment and community validation. The addition of a KGST/TRX feed, for instance, enables broader DeFi adoption of the KGST token by ensuring that its value relative to TRX can be reliably referenced by lending protocols and DEXs. Here again, TRX plays a dual role: as a governance asset helping to approve these integrations and as the quote asset in the oracle pairs that underpin them. This multi‑layered involvement underscores TRX’s position not merely as a passive investment token but as an active governance and infrastructure instrument in the Tron ecosystem.

TRX and the Energy Rental Market

An increasingly important dimension of TRX tokenomics is the energy rental market, through which network resource demand and TRX staking yields intersect. Because staked TRX generates energy, which is required to run smart contracts, a secondary market has emerged where protocols and high‑usage entities rent energy from TRX stakers rather than staking TRX themselves. This arrangement can be economically efficient: protocols that need large amounts of energy for a limited time do not have to permanently lock capital in TRX, while long‑term TRX holders can monetize their stake by leasing out the energy it generates. The yields described in products like SafePal’s TRX staking—where energy rental forms a significant part of the return—are thus directly linked to the intensity of DeFi and stablecoin usage on Tron.

The introduction of SunSwap V4 is relevant in this context because it aims to radically reduce the energy footprint of trading by optimizing gas usage and eliminating the need to wrap TRX into a separate token before providing liquidity or trading. Commentators have noted that V4’s fee optimizations and redesign of the cost structure result in near‑zero transaction costs for many trades and up to a ninety‑nine percent reduction in energy consumption for certain operations, compared with earlier versions. For TRX holders, this means that while the efficiency gains may reduce the per‑transaction resource demand, they can simultaneously increase overall transaction volume, potentially expanding the market for energy rental. The interplay between protocol‑level efficiency improvements and resource‑market pricing is an important, if technical, factor in TRX’s long‑term economic design.

Lady claiming to be Justin Sun's girlfriend during the early stages of his entrepreneurship with TRX, request that the U.S. judicial authorities contact her. She expressed willingness to fully cooperate with an SEC investigation and to submit all relevant WeChat chat records, as well as evidence provided by his employees, proving his market manipulation activities.

Justin Sun just keeps jumping from oil to fire

- 01Trump-WLF TRX acquisition↗

Political capital entering TRX via World Liberty Financial created the clearest signal that Tron's regulatory fate is now entangled with U.S. election politics, drawing readers who track power-aligned crypto bets.

- 02Stablecoin infrastructure exits↗

Circle ending USDC on Tron and Binance dropping TRC20 USDC support signaled that major stablecoin issuers are quietly distancing themselves from Tron's compliance exposure, a slow-moving but consequential withdrawal.

- 03Illicit finance crackdowns

The T3 Financial Crime Unit freezing $100M, U.S. Treasury sanctioning Tron wallets tied to Houthi financing, and a Tether laundering loophole report made Tron the most visible on-chain compliance battleground.

- 04SEC securities classification↗

TRX appearing on the SEC's 48-token securities list alongside the halted investigation into Justin Sun made Tron's legal status the most-read regulatory subplot tied to a single founder.

- 05Gas-free stablecoin transfers

Justin Sun's announced fee elimination for stablecoin transfers directly attacks Ethereum's cost advantage and signals competitive repositioning of Tron as a frictionless USDT rail.

- 06USDD stability and DAO collapse↗

The TRON DAO Reserve shutting down and USDD 2.0 launching with a 20% APY promise echoed Terra/LUNA alarm patterns, attracting readers who track algorithmic stablecoin systemic risk.

TRX at the Heart of Tron’s Stablecoin Machine

Tron as a Stablecoin Settlement Layer

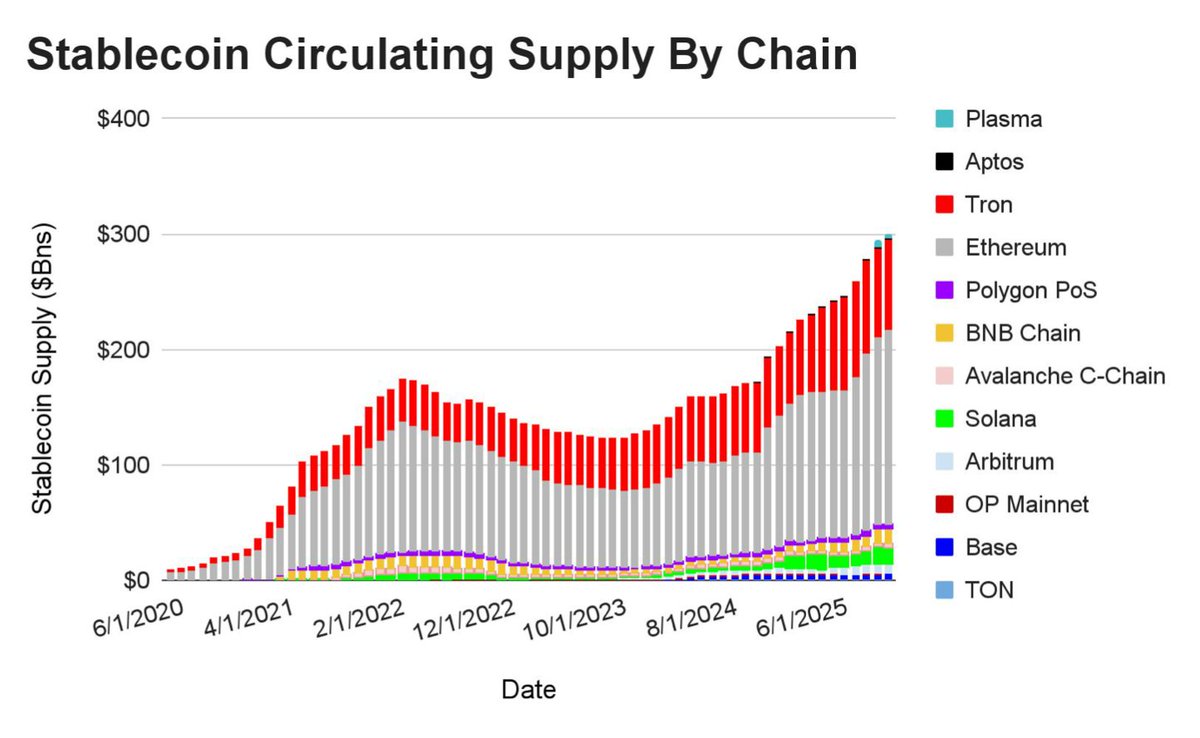

Tron’s rise to prominence in crypto has been driven less by its original content‑distribution ambitions and more by its unexpected emergence as a global stablecoin settlement layer. By 2025, Tron’s on‑chain metrics showed strong growth in transaction volume, active addresses, and network revenue, with stablecoin activity playing a central role. Research from crypto analytics firms indicates that the supply of USDT on Tron surged by more than forty percent in the first half of 2025, reaching approximately 81.2 billion dollars and reinforcing the network’s dominance in stablecoin infrastructure. Parallel data from DeFi analytics platforms show that the total stablecoin market cap on Tron approached nearly 90 billion dollars, with USDT accounting for over ninety‑seven percent of that supply. These figures underscore how deeply intertwined Tron has become with Tether’s dollar‑pegged token and with the broader stablecoin economy.

This growth has had tangible effects on the comparative landscape between Tron and other smart‑contract platforms, particularly Ethereum. Where Ethereum once dominated USDT issuance, Tron has, according to recent coverage, flipped Ethereum in USDT dominance, meaning that a larger share of all circulating USDT now exists on Tron’s TRC‑20 rails than on Ethereum’s ERC‑20 contracts. The exact ratio can fluctuate, but the reported surge in Tron‑based USDT supply and the concentration of nearly ninety billion dollars in stablecoins on Tron suggest that this flip in dominance is structurally meaningful. For markets, the shift implies that liquidity, especially for USDT‑denominated trading and cross‑border transfers, increasingly routes through Tron’s network, which in turn supports demand for TRX as the gas and resource token needed to move those stablecoins.

Justin Sun himself has repeatedly framed this trajectory as part of a larger strategic vision. In a widely watched interview, he noted that Tron’s stablecoin ecosystem had surpassed 83 billion dollars in value and argued that Tron had become one of the best blockchains for stablecoin payments and remittances, citing its low fees and fast transaction finality. He also articulated an ambition for Tron to become a global settlement layer for “every issuer in the world,” positioning the network as foundational infrastructure for tokenized dollars and other assets. Whether or not that vision is fully realized, the current data around USDT and other stablecoins clearly shows that TRX’s value proposition is tightly linked to Tron’s role as a dominant stablecoin rail.

USDT, USDC, USDD, and Beyond

Within Tron’s stablecoin universe, three tokens stand out: USDT, USDC, and USDD. USDT, issued by Tether, is by far the largest, especially on Tron, where it commands nearly the entire stablecoin market cap. Its appeal lies in the combination of Tether’s extensive exchange integrations and Tron’s low transaction costs, making USDT on Tron the preferred rail for many centralized exchanges, OTC desks, and retail users transferring funds across borders. USDT transactions on Tron consume bandwidth and, for contract interactions, energy, thus requiring small amounts of TRX even when the primary asset being moved is dollars. This dynamic cements TRX’s position as the “fuel” behind a vast global network of dollar transfers, even if many end users hold relatively small TRX balances purely to cover fees.

USDC, issued by Circle, has had a comparatively smaller presence on Tron but is becoming more relevant in cross‑chain liquidity strategies. Recent developments have seen TRX/USDC trading pairs launched on decentralized exchanges operating on other networks, such as Aerodrome on Base, with cross‑chain bridges facilitating TRX liquidity between Tron and Ethereum‑aligned ecosystems. These TRX/USDC pairs aim to deepen liquidity, allow traders to move between TRX exposure and a regulated stablecoin like USDC, and link Tron’s native economy with the rest of the multi‑chain world. However, they also introduce cross‑chain risks, as bridging mechanisms become potential points of failure or exploitation, and as TRX’s price dynamics become more tightly coupled to conditions on other chains. For users and institutions evaluating TRX, understanding how these cross‑chain markets work—and what security assumptions they involve—is increasingly important.

The third major stablecoin in Tron’s orbit is USDD, a decentralized USD‑pegged token introduced by Justin Sun and the TRON DAO Reserve. Unlike fully collateralized stablecoins, USDD began as an algorithmic stablecoin, with mechanisms intended to maintain its peg through on‑chain incentives and, over time, through a reserve of assets managed by the DAO. It is pegged one‑to‑one to the U.S. dollar and exists not only on Tron but also on other chains such as Ethereum, BNB Chain, and NEAR. As of August 2023, USDD’s circulating supply was around 737 million tokens, with a market price very close to one dollar, though its peg stability has at times been questioned in the market. Incentive programs like sUSDD campaigns, which offer hundreds of thousands of USDD in rewards and TRX airdrops for participants, have sought to deepen liquidity and strengthen the stablecoin’s usage, but they also signal that maintaining confidence in algorithmic or partially collateralized designs requires ongoing incentives.

Risk Management and the T3 Financial Crime Unit

The concentration of stablecoin activity on Tron has also drawn attention from regulators and compliance professionals, pushing the ecosystem toward more robust risk management and law‑enforcement cooperation. A prominent example is the T3 Financial Crime Unit, a joint initiative between Tether, Tron, and blockchain analytics firm TRM Labs. According to recent coverage, this unit has already frozen over 300 million dollars’ worth of illicit crypto assets across more than twenty jurisdictions, assisting global authorities in cases of fraud, money laundering, and other financial crimes. The collaboration involves monitoring suspicious activity on Tron’s stablecoin rails, using analytics tools to trace funds, and leveraging Tether’s and Tron’s ability to freeze or blacklist addresses at the token‑contract level when required by law enforcement.

These actions highlight a core tension in Tron’s positioning. On the one hand, the ability to freeze assets and cooperate quickly with enforcement agencies makes Tron‑based stablecoins more acceptable to regulated institutions and governments, potentially supporting the long‑term adoption of USDT and similar assets on the network. On the other hand, such powers raise concerns about censorship resistance and the degree of centralization in stablecoin contracts and in Tron’s governance. For TRX holders and users committed to a decentralized ethos, the knowledge that stablecoin balances can be frozen at the contract level may weaken the perception of Tron as a permissionless system, even as it strengthens its compliance credentials. The T3 initiative thus exemplifies the hybrid nature of Tron’s stablecoin machine: part public blockchain, part regulated financial infrastructure.

TRX in the Tron DeFi Stack

Lending, Borrowing, and JustLend DAO

Beyond stablecoin transfers, TRX plays a crucial role in Tron’s DeFi lending and borrowing markets, most notably on JustLend DAO, the network’s first official lending platform. JustLend enables users to deposit assets such as TRX, USDT, USDD, and other TRC‑20 tokens to earn interest, while borrowers can post collateral and take out loans in supported assets, all governed by smart contracts. TRX is both a core collateral asset and, in many cases, a reward token for liquidity mining programs, meaning that users can earn TRX by supplying or borrowing certain assets during promotional periods. This deepens TRX’s integration into DeFi strategies, as users balance the opportunity cost of staking TRX for governance and resource generation against the potential yields from deploying it in lending pools.

Governance proposals like the aforementioned addition of a U market on JustLend illustrate how TRX’s governance and DeFi roles intersect. Introducing a new stablecoin or token as a collateral and borrow asset involves careful calibration of interest rate models, collateral factors, and liquidation mechanics—all of which affect systemic risk. TRX holders, via governance, effectively vote on the risk profile of the lending platform, which in turn can influence the perceived safety and attractiveness of Tron’s DeFi ecosystem. For instance, adding thinly traded or experimental stablecoins as collateral without sufficient safeguards could increase the risk of undercollateralized positions and cascading liquidations, impacting both TRX and stablecoin markets on Tron.

Promotional programs like Supply Mining activity for assets such as wrapped BTC (WBTC), where users who supply WBTC to JustLend earn both supply interest and additional TRX rewards, also shape TRX’s demand and distribution. These campaigns typically run for defined periods and distribute TRX based on users’ contribution to liquidity, effectively using TRX emissions to bootstrap deeper markets in non‑native assets. While such strategies can be effective in accelerating growth, they also introduce questions about long‑term sustainability: once mining rewards taper off, will the underlying markets remain attractive on their own merits, or will liquidity migrate elsewhere? For TRX, the pattern of such campaigns influences its distribution among DeFi‑native users and its perceived role as a reward token in addition to its structural utility.

SunSwap V4 and DEX‑Driven Liquidity

Decentralized exchanges are another pillar of Tron’s DeFi stack, and SunSwap stands as the flagship DEX on the network. The launch of SunSwap V4 has been framed as a major upgrade that “revolutionizes” TRON DeFi by redesigning the cost structure and dramatically reducing friction for TRX users. One of the key improvements is the elimination of the need to wrap TRX into a synthetic token (such as WTRX) before trading or providing liquidity; V4 allows direct pairing between native TRX and TRC‑20 assets, simplifying user workflows and reducing the number of contract interactions per trade. This not only improves usability but also reduces energy consumption and transaction costs, with some observers highlighting near‑zero transaction costs enabled by aggressive fee optimization and energy efficiency improvements that cut costs by up to ninety‑nine percent for certain operations.

These design changes have important implications for liquidity and market structure. By making it easier and cheaper to use TRX directly in trading pairs, SunSwap V4 encourages deeper TRX‑denominated pools, which can improve price discovery and reduce slippage for traders entering or exiting TRX positions. It also strengthens TRX’s role as a base asset in the Tron DeFi ecosystem, analogous to how ETH serves as a reference asset across many Ethereum DEXs. The inclusion of TRX pairs with major stablecoins like USDT and USDC, along with cross‑chain integrations, means that TRX sits at the center of on‑chain liquidity routing on Tron and beyond. For TRX holders, the vibrancy of these markets affects both the asset’s day‑to‑day volatility and its attractiveness to traders and arbitrageurs.

Yield Products, TRX Earn, and sUSDD Incentives

The combination of staking rewards, DeFi incentives, and stablecoin yields has given rise to an array of yield products centered on TRX. In addition to non‑custodial staking in wallets like SafePal, new distribution channels have emerged, including TRX Earn on Telegram, a product launched under Justin Sun’s direction. TRX Earn offers boosted yields—reported at up to around 13.6 percent APY—by combining base staking rewards with limited‑time promotional bonuses for new users over sixty‑day periods. These offerings are marketed as a way for retail users to access TRX yield from within familiar messaging environments, lowering the barrier to participation but also concentrating custody and counterparty risk, depending on how deposits are managed under the hood.

On the stablecoin side, protocols have introduced sUSDD and similar derivative tokens that represent staked or vaulted positions in USDD, often paired with TRX incentives. Campaigns offering hundreds of thousands of USDD and additional TRX airdrops to users who mint or hold sUSDD aim to deepen liquidity and bolster confidence in the algorithmic stablecoin, especially amid broader market concerns about stablecoin design and peg integrity. The presence of such high‑yield incentives, however, is a double‑edged sword: they can attract capital in the short term but may also signal that organic, incentive‑free demand is insufficient to sustain the peg without ongoing subsidies.

These dynamics underscore a broader theme in Tron DeFi: TRX often functions as the incentive currency used to kick‑start or reinforce liquidity and usage of both native and third‑party tokens. While this can be effective in building network effects, it also means that TRX’s supply distribution and inflation profile are partly shaped by these programs. Investors and users must therefore consider not only the headline APY figures but also the long‑term sustainability of the yields, the sources of reward funding, and the smart‑contract and custodial risks embedded in each product.

Institutional and Enterprise Adoption

Exchange Listings and Compliant Market Access

A key milestone in TRX’s journey from retail‑focused token to institutionally relevant asset has been its listing on regulated exchanges, particularly in the United States. In April 2026, TRON DAO announced that TRX would be listed on Binance.US, a U.S.‑licensed digital asset platform, with trading pairs including TRX/USD and TRX/USDT. According to the announcement, the listing was framed as strengthening TRX’s availability within compliant U.S. market infrastructure, supporting enhanced liquidity and broader accessibility across established digital asset markets. For TRX, such listings are more than symbolic; they open the door for U.S.‑based retail and institutional investors who are restricted to trading on regulated venues.

The addition of TRX/USD pairs is particularly important because it allows direct pricing and settlement in dollars, reducing reliance on stablecoin intermediaries for price discovery. Combined with deep TRX/USDT markets on global exchanges, this expands the range of hedging and arbitrage strategies available to traders and market makers. The presence of TRX on compliant platforms also facilitates integration into structured products and brokerage platforms that require assets to be traded on regulated exchanges, further weaving TRX into the fabric of the broader financial system. However, it simultaneously subjects TRX to more intense regulatory scrutiny and compliance obligations, especially in light of ongoing questions about token classification and founder behavior.

Anchorage Digital and Regulated Custody

Perhaps even more significant for TRX’s institutional profile is its integration into regulated custody and banking infrastructure. Anchorage Digital, the first federally chartered crypto bank in the United States, has announced support for the Tron blockchain, including custody for TRX and TRC‑20 assets. Anchorage describes itself as providing secure, institutional‑grade custody, trading, staking, and governance participation for digital assets, and the decision to add Tron means that U.S. institutions can now hold TRX and TRC‑20 stablecoins like USDT on a regulated platform subject to bank‑level oversight. According to Anchorage’s announcement, the integration allows institutions to custody TRX both on Anchorage’s main platform and in Porto, its self‑custody wallet solution, with plans to support staking and other on‑chain activities.

Coverage of this move has emphasized that Anchorage’s support brings Tron inside the U.S. regulatory perimeter, giving institutions a compliant way to access one of the largest and most widely used networks in crypto. For TRX, this legitimizes the asset in the eyes of conservative institutional allocators who might otherwise avoid assets lacking bank‑level custody solutions. It also opens the door to TRX being included in institutional portfolios, customer offerings from fintech platforms, and potentially in tokenized products that rely on regulated custodians to hold underlying assets. At the same time, Anchorage’s involvement further entwines Tron’s future with the evolving stance of U.S. regulators toward stablecoins, DeFi, and non‑Bitcoin digital assets.

Beyond Anchorage, Tron has announced expanded enterprise access through integrations with other crypto, stablecoin, and tokenized asset infrastructure providers, giving corporations and financial institutions in select jurisdictions access to TRX and TRC‑20 USDT. Some coverage has praised these integrations as a way to bring cheap, high‑throughput stablecoin rails to enterprises, while more critical analyses have warned that opening TRX and TRC‑20 USDT to enterprise flows also exposes companies to network‑specific risks, including smart‑contract vulnerabilities, potential regulatory actions against Tron, and the concentration of stablecoin risk on a single chain. The debate reflects a broader tension between the desire for efficient digital‑dollar rails and the need for robust, diversified infrastructure that can withstand shocks.

Grayscale Watchlist and Investment Products

Another indicator of TRX’s growing institutional relevance is its inclusion on Grayscale’s “Assets Under Consideration” watchlist for Q1 2026. Grayscale, one of the largest digital asset managers, periodically publishes lists of altcoins it is evaluating for potential inclusion in future investment products, such as publicly traded trusts or ETF‑like vehicles. The Q1 2026 list included thirty‑six altcoins, among them TRX, TON, ENA, HYPE, and others, signaling that TRX is on Grayscale’s radar as a candidate for structured investment vehicles. While being on the watchlist does not guarantee that a product will be launched, it indicates that the asset meets certain thresholds of liquidity, security, and market interest that Grayscale considers necessary.

If Grayscale or similar asset managers were to launch TRX‑linked products, it could have several effects. On the one hand, such vehicles would make TRX exposure accessible to a wider range of investors, including those constrained to holding securities rather than native tokens. On the other hand, they could introduce new sources of demand that are insensitive to on‑chain usage, potentially decoupling TRX’s market price from fundamentals like network activity and stablecoin volume in the short term. Moreover, the structuring of such products would likely involve close engagement with regulators, whose view of TRX’s legal status and of Tron’s governance and compliance practices would influence approvals. Thus, inclusion on Grayscale’s watchlist is both a validation of TRX’s market maturity and a reminder that its future is increasingly bound up with mainstream financial regulation.

Anchorage Digital brings Tron inside regulatory perimeter with institutional TRX custody and staking

Big win for Tron. So sad it just never reflects on TRX price

SEC identifies TRX as unregistered security in 48-token list

- 2023-11milestone

Tether, Tron, and TRM Labs launch T3 Financial Crime Unit

- 2024-03regulatory

U.S. Treasury sanctions Tron wallets tied to Houthi financing

Circle discontinues USDC support on Tron network

World Liberty Financial acquires TRX for treasury holdings

Tron plans public listing as U.S. halts Justin Sun investigation

Anchorage Digital adds institutional TRX custody and staking

Tron reports $916M revenue and $81B USDT supply for H1 2025

Comparing TRX and Ethereum in the Stablecoin Era

A recurring theme in analysis of Tron is its comparison with Ethereum, the dominant generalized smart‑contract platform. Tron and Ethereum share certain characteristics—they both support Turing‑complete smart contracts, fungible token standards, and DeFi applications—but their design choices have led to distinct niches in the crypto economy. According to performance comparisons, Tron emphasizes high throughput and low transaction fees, with average fees significantly lower than Ethereum’s, a factor that has contributed to its appeal for stablecoin transfers and micro‑transactions. Ethereum, by contrast, has prioritized decentralization and security, running a far larger and more distributed validator set at the cost of higher base‑layer fees, which are partly mitigated by rollups and Layer‑2 solutions.

In the stablecoin arena, these differences have had concrete consequences. Ethereum remains home to large supplies of USDC and substantial USDT, as well as many other stablecoins, but Tron has emerged as the primary chain for USDT transfers by supply, with tens of billions of dollars of USDT circulating on its TRC‑20 contracts. This dominance is not merely a function of supply; it reflects the preferences of exchanges, OTC desks, and users who value low fees and fast confirmation times for dollar transfers, particularly in emerging markets where stablecoin remittances and P2P trading are common. The fact that stablecoin supply across networks has reached record levels—reported at around 300 billion dollars, up seventy‑five percent year‑on‑year, with Ethereum, Tron, and BNB Chain leading and USDT and USDC accounting for eighty‑five percent of the market—highlights how both networks are integral to the digital‑dollar system.

From a developer ecosystem perspective, Ethereum still hosts a broader and more diverse set of DeFi, NFT, and application infrastructure, with a large open‑source community and extensive tooling. Tron’s ecosystem is more focused on payments, high‑velocity transfers, and targeted DeFi use cases such as lending, DEXs, and yield strategies tied closely to TRX and stablecoins. Tron’s DPoS governance and resource model yield a user experience closer to that of centralized fintech apps, whereas Ethereum’s model, especially when combined with rollups, offers a more modular but sometimes more complex stack. For TRX, this means that its fate is more tightly bound to stablecoin and payment use cases than, say, the NFT or on‑chain gaming sectors that feature prominently on Ethereum.

The comparison also extends to risk profiles. Ethereum’s heavy decentralization and established regulatory narratives (including the widespread view that ETH is sufficiently decentralized) may make it more resilient to certain kinds of regulatory and governance shocks. Tron, by contrast, faces greater scrutiny over centralization—both in its SR set and in the prominence of Justin Sun—and over the degree of control that Tether and Tron entities have over stablecoin balances through blacklisting mechanisms. For users deciding whether to hold or use TRX versus ETH, the question is not simply one of fees and throughput but also of comfort with these differing governance and regulatory trade‑offs.

Economics and Sustainability of the Tron Ecosystem

The long‑term viability of TRX depends on whether Tron’s economic model can sustain network security, incentivize validators and stakers, and maintain a robust ecosystem of applications and stablecoin flows. Tron generates on‑chain revenue through transaction fees and resource consumption, particularly energy used by smart‑contract interactions in DeFi, and this revenue is distributed to Super Representatives and, indirectly, to TRX stakers. As stablecoin and DeFi activity grow—evidenced by the near‑record levels of on‑chain activity reported in the first half of 2025—this revenue base expands, supporting the economic case for staking TRX and for running SR infrastructure. In this sense, TRX functions as a claim on the future cash flows of the network’s resource economy, though unlike a traditional equity, it does not convey formal ownership of the corporate entities associated with Tron.

The profitability of Tron Inc., with reported net income of over twelve million dollars in a recent quarter, suggests that the broader Tron ecosystem is generating not only on‑chain fees but also off‑chain revenue from services, partnerships, and holdings. While detailed financial statements are not fully transparent in public reporting, this profitability indicates that Tron has resources to fund continued development, marketing, and incentive programs such as liquidity mining and sUSDD campaigns. For TRX holders, this corporate strength can be a double‑edged sword: on one hand, it means the ecosystem has staying power and can invest in growth; on the other hand, it raises questions about how value accrues between corporate entities, the DAO treasury, and TRX token holders, especially in the absence of formal revenue‑sharing mechanisms.

A key question for TRX’s economics is the sustainability of incentives. Programs that distribute TRX to users of JustLend, SunSwap, and stablecoin vaults can jump‑start adoption but may also contribute to token inflation if not carefully calibrated. Without transparent and predictable issuance and burn schedules, it is difficult for investors to model long‑term supply dynamics and to assess whether staking yields are primarily funded by genuine economic activity (fees and resource demand) or by subsidized emissions. The fact that some staking products advertise double‑digit APYs, combining SR rewards, energy rental income, and promotional bonuses, underscores the need for users to differentiate between sustainable and unsustainable components of yield.

In the stablecoin context, Tron’s heavy reliance on USDT is both a strength and a risk. As long as USDT remains widely used and perceived as reliable, Tron’s position as a primary USDT rail supports demand for TRX and reinforces the network’s relevance. However, any serious disruption to USDT—whether regulatory, operational, or market‑driven—could disproportionately impact Tron relative to other networks with more diversified stablecoin ecosystems. Similarly, the success or failure of USDD as an algorithmic stablecoin will influence perceptions of Tron’s appetite for risk and its ability to manage complex monetary mechanisms. The aggressive incentives around sUSDD and related products suggest that this experiment is still in a formative phase, and the memory of past algorithmic stablecoin failures in crypto markets means that confidence must be earned rather than assumed.

Risks, Controversies, and Considerations

No evaluation of TRX is complete without a candid look at the risks and controversies surrounding Tron. On the technical side, the DPoS consensus model’s reliance on a relatively small set of Super Representatives introduces potential centralization and governance risks. If a handful of SRs were to collude or be compromised, they could disrupt the network, censor transactions, or manipulate governance votes. While token‑holder voting and the ability to rotate SRs mitigate this risk in theory, in practice, concentration of voting power among large stakeholders and centralized platforms can make change slow and politically complex.

Regulatory and legal risks are also prominent. The close association between Justin Sun and Tron means that any regulatory action against Sun could have direct and indirect consequences for TRX. The recent public claims by a woman identifying as Sun’s early‑stage girlfriend—offering to provide chat records and employee testimony to U.S. authorities in an SEC investigation into alleged market manipulation in TRX’s early history—highlight the possibility of enforcement actions that could affect the token’s status or market access. Even absent specific charges, the broader environment of U.S. regulation—where agencies have at times alleged that various tokens are unregistered securities—creates uncertainty for projects with centralized leadership and fundraising histories. Listings on platforms like Binance.US and custody support from Anchorage Digital suggest that TRX has passed certain internal legal and compliance reviews, but they do not immunize it from future regulatory developments.

The stablecoin‑centric nature of Tron’s economy also introduces concentrations of risk. A large share of network activity, fees, and DeFi usage is tied to USDT flows, making Tron highly exposed to Tether’s operational and regulatory fortunes. While initiatives like the T3 Financial Crime Unit help demonstrate compliance and law‑enforcement cooperation, they also confirm that Tron’s stablecoin ecosystem is actively monitored and subject to address freezing and other interventions. This may be positive from an AML and sanctions perspective but can be disconcerting for users who expect censorship resistance and financial sovereignty from public blockchains. Moreover, algorithmic and partially collateralized stablecoins like USDD carry inherent design risks, as market stress can reveal weaknesses in peg‑maintenance mechanisms that are not apparent during normal conditions.

DeFi on Tron shares many of the smart‑contract and oracle risks seen elsewhere in crypto. Lending protocols like JustLend rely on accurate price feeds from oracles such as WINkLink; if those feeds were manipulated or suffered outages, they could trigger improper liquidations or allow undercollateralized borrowing. DEXs like SunSwap, even with cost‑optimized V4 designs, are exposed to issues such as impermanent loss, front‑running, and potential contract bugs. The energy rental and staking‑derivative markets introduce additional layers of complexity, as users may be exposed to cascading failure if a major protocol is hacked or a wrapped token depegs. For TRX holders who engage with these systems, prudent risk management requires assessing not just yields but also underlying technical and counterparty structures.

Finally, market volatility and liquidity risks remain intrinsic to TRX as a crypto asset. Even with deep TRX/USDT and emerging TRX/USDC markets, TRX’s price can move sharply in response to macro conditions, regulatory news, or events within the Tron ecosystem. Cross‑chain integrations, such as TRX pairs on Base or other networks, can propagate volatility across ecosystems and expose TRX holders to bridge‑related risks. For institutions and individuals alike, these factors underscore the importance of viewing TRX not simply as a utility token within Tron but as a speculative asset whose value is contingent on a complex interplay of technical, economic, and regulatory forces.

Justin Sun exerts outsized influence over protocol direction; the TRON DAO Reserve shutdown eliminated the primary decentralized governance layer, concentrating decisions at the founder level.

TRX is listed among 48 tokens the SEC identified as unregistered securities, the U.S. Treasury has sanctioned Tron-routed wallets, and Justin Sun faced a multi-year SEC enforcement action before it was halted.

- Illicit Finance ExposureHigh

T3 FCU froze $100M in illegal USDT on Tron including North Korea-linked funds, a separate AMLBot report tied $78M in losses to a Tether laundering loophole active on Tron since 2017.

A disclosed bug put approximately $500M of assets at risk on the Tron network, and Tron was one of three chains drained in the CoinEx hack, indicating meaningful infrastructure vulnerability.

Circle and Binance exiting TRC20 USDC reduces stablecoin route diversity, though USDT supply on Tron exceeded $81B in H1 2025, keeping overall settlement liquidity deep.

Institutional custody added by Anchorage Digital and political backing via World Liberty Financial provide price support, but SEC securities designation and stablecoin issuer exits create persistent regulatory overhang.

How TRX Is Used in Practice

In practical terms, most users encounter TRX in a handful of recurring roles that illustrate its multi‑faceted nature within Tron’s economy. First, TRX serves as the gas token for moving stablecoins and other tokens. A user sending USDT on Tron typically needs only a small amount of TRX to cover bandwidth and energy; once funded, they can perform numerous transfers at negligible cost thanks to the 600 units of free daily bandwidth per account and the low unit price of additional bandwidth. This is particularly attractive for cross‑border remittances and P2P trading, where users value predictably low fees.

Second, TRX functions as a staking and yield asset. Users who wish to earn returns on their holdings can stake TRX directly through Tron wallets or via third‑party platforms like SafePal, participating in TRON Stake 2.0 and earning yields from SR voting rewards and energy rental markets. More sophisticated users might deposit TRX into JustLend pools, supply TRX as collateral to borrow stablecoins, or use staking derivatives like sTRX in combination with stablecoin vaults to pursue leveraged strategies. Each of these approaches involves trade‑offs between yield, liquidity, and risk, but they all rest on TRX as the foundational asset.

Third, for developers and DeFi participants, TRX operates as collateral and governance capital. Protocols may require TRX deposits for participation in governance, for seeding liquidity pools, or for accessing premium services, such as discounted energy rentals. TRX votes help determine which Super Representatives secure the network and which proposals are adopted in governing DAOs like JustLend, meaning that holding TRX can also be a way to influence the rules and direction of Tron’s financial infrastructure. This governance dimension is subtle but important: it shapes everything from interest rate curves in lending markets to the listing of new assets and the adoption of upgrades like SunSwap V4.

From the perspective of enterprises and institutions, TRX is increasingly part of stablecoin and digital asset infrastructure. Companies integrating with Tron’s rails may hold TRX to pay for transaction resources, to support on‑chain operations, or to stake through regulated custodians like Anchorage Digital as part of treasury management strategies. As integrations with enterprise‑grade infrastructure providers expand, TRX may also be used behind the scenes in payment flows that are abstracted away from end users but crucial to the functioning of tokenized dollar and asset systems. This institutional uptake adds another layer to TRX’s demand profile beyond retail speculation and DeFi activity.

Outlook

TRX stands at a pivotal point where its fate is tied to broader trends in stablecoins, on‑chain finance, and crypto regulation. On the positive side, Tron’s demonstrable strength as a stablecoin settlement layer, evidenced by tens of billions of dollars in USDT supply and an overall stablecoin market cap nearing ninety billion dollars on the network, gives TRX a concrete, utilitarian role that is relatively rare among altcoins. The network’s low fees, high throughput, and resource model are well‑suited to payments and remittances, and recent developments—from SunSwap V4’s cost optimizations to expanding institutional support from Anchorage Digital and Binance.US—reinforce its position as infrastructure rather than mere speculation.

At the same time, TRX faces material challenges and uncertainties. Its heavy reliance on USDT and the Tether‑Tron nexus concentrates risk, while algorithmic experiments like USDD add another layer of complexity and potential fragility. Regulatory scrutiny of Justin Sun and of token projects more broadly, coupled with the evolving stance of U.S. and global regulators toward stablecoins and DeFi, means that TRX’s legal and market access landscape could change rapidly. The DPoS governance model and centralized points of control, such as stablecoin contract freeze functions, will be judged not only by crypto‑native standards of decentralization but also by policymakers deciding how deeply to integrate such systems into the regulated financial system.

For now, TRX remains a core asset in one of the busiest corners of crypto. Its long‑term trajectory will hinge on whether Tron can continue to balance performance, compliance, and decentralization; whether it can sustain its lead in stablecoin infrastructure amid competition from Ethereum rollups and other chains; and whether it can manage governance and regulatory risks tied to its founder and centralized components. For a crypto news audience and market participants, TRX is thus best understood not as an isolated token but as a gateway into the complex, evolving story of how public blockchains are becoming the pipes of a global, programmable dollar system—and how that system is being contested, regulated, and rebuilt in real time.

Latest TRX news

TRON’s Justin Sun launches TRX Earn on Telegram with boosted yields up to 13.61% APY, combining base rewards and a limited 60-day bonus for new usersLady claiming to be Justin Sun's girlfriend during the early stages of his entrepreneurship with TRX, request that the U.S. judicial authorities contact her. She expressed willingness to fully cooperate with an SEC investigation and to submit all relevant WeChat chat records, as well as evidence provided by his employees, proving his market manipulation activities.Anchorage Digital brings Tron inside regulatory perimeter with institutional TRX custody and staking Tron Inc. has reported their 2025 Q3 results, recording a net income of $12.17M.

Tron Inc. has reported their 2025 Q3 results, recording a net income of $12.17M. Stablecoin supply hits a record $300B, up 75% YoY, driven by Ethereum, Tron, and BNB Chain. USDT and USDC dominate with 85% share, while new entrants like $CASH and GAIB AI surge.

Stablecoin supply hits a record $300B, up 75% YoY, driven by Ethereum, Tron, and BNB Chain. USDT and USDC dominate with 85% share, while new entrants like $CASH and GAIB AI surge. Tether, TRON, and TRM Labs’ T3 Financial Crime Unit has frozen over $300 million in illicit crypto across 23 jurisdictions, aiding global law enforcement in major fraud and money laundering cases.

Tether, TRON, and TRM Labs’ T3 Financial Crime Unit has frozen over $300 million in illicit crypto across 23 jurisdictions, aiding global law enforcement in major fraud and money laundering cases.Sources

- https://www.youtube.com/watch?v=ZwSrORDoCeE

- https://en.wikipedia.org/wiki/Tron_(blockchain)

- https://developers.tron.network/docs/concensus

- https://developers.tron.network/docs/resource-model

- https://en.wikipedia.org/wiki/Justin_Sun

- https://cryptorank.io/insights/research/tron-h-1-2025

- https://defillama.com/stablecoins/tron

- https://atomicwallet.io/academy/articles/what-is-usdd

- https://x.com/skinnydefi/status/2062645616271040923

- https://justlend.org

- https://chainspect.app/compare/tron-vs-ethereum

- https://www.youtube.com/watch?v=zo_cUsrLfJ0&vl=en-US

- https://www.safepal.com/en/blog/stake-trx-safepal-xyswap-earn-10apy

- https://www.newsfilecorp.com/release/293167/TRX-Listing-Launches-on-Binance.US-Advancing-U.S.-Market-Access-to-TRON

- https://www.anchorage.com

- https://x.com/Arielessayshelp/status/2053880533180940354

- https://www.anchorage.com/insights/anchorage-digital-adds-support-for-tron-with-institutional-custody-and-staking-infrastructure

- https://www.tradingview.com/news/coinpedia:a7b3c09ac094b:0-anchorage-digital-adds-tron-custody-opens-institutional-trx-access/

- https://www.tradingview.com/news/coinpedia:5efc64681094b:0-grayscale-releases-36-altcoin-watchlist-for-q1-2026/

Community notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…