In-depth explainer on RISE in crypto, covering RISE Chain (Ethereum L2), RISE Launchpad on Solana, and Rise payroll, with context on Bitcoin, Ethereum, DeFi, stablecoins, macro rates, and institutional adoption.

+46 sources across the wider coverage universe

Hyperfinancialisation: On the rise and ouroboric nature of gambling and financialisation. This piece was written as an accompaniment to long degeneracy.2025-12

Hyperfinancialisation: On the rise and ouroboric nature of gambling and financialisation. This piece was written as an accompaniment to long degeneracy.2025-12 "Yearn saved my life" - a new article by Sam from RISE2026-02

"Yearn saved my life" - a new article by Sam from RISE2026-02 RISE Launchpad launches on Solana with permissionless token launches featuring built-in floor price protection and instant borrowing to cap downside risk while capturing unlimited upside potential2026-04

RISE Launchpad launches on Solana with permissionless token launches featuring built-in floor price protection and instant borrowing to cap downside risk while capturing unlimited upside potential2026-04 The rise of US Bitcoin ETFs sparks concerns about systemic risks within the financial system. The level of risk hinges on the degree of market adoption.2024-01

The rise of US Bitcoin ETFs sparks concerns about systemic risks within the financial system. The level of risk hinges on the degree of market adoption.2024-01- Michael Saylor warns against rampant deepfake videos featuring Bitcoin scams, removing 80 daily. The MicroStrategy executive chairman is taking action against the alarming rise of AI-generated videos that falsely promote Bitcoin doubling schemes.2024-01

The Stable Summit at ETHDenver kicks off with a talk by @CurveCap on "The Rise of Yield Bearing Stablecoins"2025-02

The Stable Summit at ETHDenver kicks off with a talk by @CurveCap on "The Rise of Yield Bearing Stablecoins"2025-02

Understanding RISE in Crypto: Chain, Launchpad, and Payroll Infrastructure

Several distinct projects now share the RISE brand in crypto, spanning an Ethereum Layer 2 chain, a Solana token-launch platform, and a Web3 payroll provider, each targeting different layers of the emerging digital-asset stack. Taken together, these initiatives offer a useful lens on how high-speed blockchains, permissionless token markets, and stablecoin-based payroll rails are reshaping the way capital, labor, and data move across the Bitcoin, Ethereum, and broader DeFi ecosystem.

Defining “RISE” in a Crowded Crypto Landscape

The first challenge in explaining RISE is conceptual rather than technical: there is no single “RISE protocol.” Instead, the term refers to multiple unrelated or loosely related projects that happen to share the same name, and which sit at very different points in the crypto value chain. For a reader approaching this as an evergreen reference, disambiguation is critical, because the risks, opportunities, and user interactions differ dramatically depending on whether the discussion concerns an Ethereum Layer 2 network, a Solana-based launchpad, or a crypto payroll platform.

The most structurally important of these projects for the DeFi infrastructure stack is RISE Chain, an Ethereum Layer 2 network built to deliver extremely high throughput and low-latency execution for professional-grade financial applications. RISE Chain is fully compatible with the Ethereum Virtual Machine (EVM), uses a hybrid security model that combines optimistic rollups with zero-knowledge fraud proofs, and aims to support order-book trading and derivatives at speeds typically associated with centralized exchanges. Its design foregrounds market microstructure and MEV-aware execution, positioning the chain as a specialized venue for high-frequency trading, on-chain order books, and complex DeFi strategies that are bottlenecked on latency on other networks.

The second major usage of the RISE brand is RISE Launchpad on Solana, a permissionless token-launch platform that emphasizes a protocol-enforced floor price and instant borrowing against launched tokens to cap downside risk while preserving upside exposure. RISE Launchpad positions itself at the intersection of retail speculation, memecoins, and structured risk management, introducing design features intended to address the “complete rug” dynamics that have characterized many earlier token launches. In doing so, it draws directly on the Solana ecosystem’s strengths in low-cost, high-throughput DeFi and its growing suite of lending and collateralization primitives.

A third pillar is Rise, a Web3 payroll and workforce solution provider that helps teams pay contributors and employees globally in local currencies, stablecoins, or other cryptocurrencies. This Rise platform integrates with major DeFi protocols such as Uniswap to support on-chain treasury management and payouts, and offers no-code connections to existing tools, positioning it as a bridge between the fiat payroll world and crypto-native treasuries. In parallel, the Alpine Formula 1 team has launched RISE+, a fan engagement platform with games, a Race Hub, XP-based rewards, and exclusive content, showing how the RISE label is also being used in non-financial, entertainment-heavy contexts around attention and fandom rather than core finance.

Across these incarnations, the RISE projects collectively intersect with broader themes that have dominated recent crypto coverage: the rise of Bitcoin as an ETF-fueled macro asset, the central role of stablecoins in global payments and de-dollarization debates, the evolving Ethereum Layer 2 landscape, the growth of DeFi lending relative to liquid staking, and a still-tense macro backdrop of shifting interest rates and tightening bank credit. By situating RISE Chain, RISE Launchpad, and Rise payroll within that wider context, it becomes easier to see them not as isolated brands, but as concrete examples of how infrastructure, speculation, and everyday financial rails are being rebuilt in parallel.

Hyperfinancialisation: On the rise and ouroboric nature of gambling and financialisation. This piece was written as an accompaniment to long degeneracy.

"In a hyperfinancialised economy, financial activities like speculative trading overshadow productive services which contribute more widely to society, while household wealth and inequality become increasingly tied to asset prices. to put it simply, wealth is no longer directly correlated to hard work and is disconnected from the means of production. this leads to more capital being channeled into speculative activities"

Readers clicked macro 'rise of X' systemic-risk stories at 5–8× the rate of RISE-project-specific news, revealing that the audience evaluates any new 'RISE' entrant through the lens of whether the ecosystem it enters — L2s, launchpads, restaking — is itself durable or the next fragility vector.↗

RISE Chain: High-Speed Ethereum Layer 2 for Markets

Architecture and Performance Claims

RISE Chain is explicitly engineered as a high-performance Ethereum Layer 2 network that optimizes for throughput, latency, and market-centric execution rather than general-purpose smart-contract compute or maximal composability. It advertises a continuous block pipeline and so-called secured shred preconfirmations that together enable sub-millisecond to low-millisecond transaction latencies and tens of thousands of transactions per second, far above what is typical on Ethereum mainnet and competitive with other performance-oriented L2s and alternative L1s. The project’s own materials describe target latency around one millisecond and throughput above fifty thousand transactions per second, while independent coverage has cited a capability of more than one hundred thousand transactions per second in benchmark scenarios.

From a security standpoint, RISE Chain adopts a hybrid rollup architecture that blends optimistic rollups with zero-knowledge fraud proofs, which is conceptually distinct from L2s that rely solely on optimistic or solely on zk-rollup constructions. In an optimistic rollup, transactions are assumed to be valid unless challenged during a dispute window, while in a zero-knowledge scheme validity proofs are generated up front; combining these approaches is intended to balance the cost and latency profile of optimistic systems with the stronger guarantees and censorship resistance of zk-based verification. All of this is anchored into Ethereum’s consensus, meaning that RISE Chain ultimately inherits security from Ethereum as its settlement layer, an alignment that Galaxy has emphasized in its discussion of backing RISE as an Ethereum-aligned scaling solution.

A distinctive feature of RISE Chain is its continuous block pipeline and interrupt-driven processing model, which are designed to minimize batching delays and keep block production and execution as close to real-time as possible. In a traditional rollup, transactions are batched and posted to Ethereum in discrete intervals, which can introduce latency even when the rollup itself is fast; RISE’s continuous approach aims to smooth this flow, reducing jitter and bringing performance characteristics closer to centralized matching engines that market makers and quant funds are accustomed to. Secured shred preconfirmations further allow participants to obtain cryptographic assurances about their transaction’s eventual inclusion and ordering before the full batch is finalized, which is crucial for high-frequency traders managing intra-second risk.

Crucially, RISE Chain maintains full EVM compatibility, meaning that existing Solidity contracts and Ethereum developer tooling can be used with minimal changes. This is not trivial for a chain that diverges architecturally from Ethereum’s traditional execution model, and it signals an intent to plug into established DeFi codebases, auditors, and hard-won security patterns rather than asking teams to re-write contracts for a bespoke virtual machine. That compatibility lowers the switching cost for projects considering deployment on RISE Chain, and it enables multi-chain DeFi protocols to treat RISE as an additional venue with familiar semantics rather than a wholly foreign environment.

Order Books, Perpetuals, and Market Microstructure

Where many earlier Ethereum L2s emphasized generalized scalability and broad smart-contract support, RISE Chain is explicit about being “designed for markets, not retrofitted for them.” Its native MarketCore infrastructure offers on-chain order books with shared liquidity across applications, enabling different protocols to plug into a common matching layer rather than fragmenting liquidity across isolated DEX instances. Every smart contract on RISE can interact with the order book in a single transaction, which is particularly important for complex operations such as margining, hedging, and multi-leg strategies that need tight coupling between different positions.

This architecture directly targets use cases that have historically struggled on Ethereum and many L2s due to latency and gas constraints, including perpetual futures, options, and other derivatives that require continuous re-pricing and risk monitoring. On a slow or congested chain, liquidations can lag price moves, or arbitrage can be too costly, leading to unstable markets and poor capital efficiency; by driving execution into the low-millisecond range, RISE aims to reduce slippage, tighten spreads, and make on-chain books behave more like professional centralized venues. That ambition aligns with broader trends seen in perpetual DEXs such as Hyperliquid, which has dramatically grown its trading volume and open interest, underscoring trader appetite for high-throughput, derivatives-focused platforms.

The ability to combine shared order books with custom smart contracts also opens up new design space for structured products, cross-market arbitrage, and MEV-aware strategies that act across multiple venues. For example, a protocol could implement a vault that algorithmically provides liquidity at the best bids and offers across several order-book pairs, hedges its exposure on external venues, and manages its risk parameters in response to volatility spikes, all within a single transaction pipeline on RISE. This style of programmable market-making is conceptually similar to some of the more sophisticated strategies implemented around Uniswap v3’s concentrated liquidity, but transplanted into an order-book-centric environment with different microstructure and latency assumptions.

At the same time, such design choices bring their own risks. A chain optimized for high-frequency markets can become a magnet for adversarial bots, latency arbitrage, and sophisticated MEV extraction strategies that exploit any asymmetry in access to preconfirmations or block-building. The use of secured shred preconfirmations, hybrid fraud proofs, and EVM compatibility can mitigate some of these issues, but they also introduce new technical complexity and potential attack surfaces that must be carefully audited and monitored as usage grows. For users and projects considering RISE Chain, understanding how order flow is routed, who controls block production, and how MEV is shared or mitigated will be as important as reading the smart contracts themselves.

Dune Analytics Integration and Data Transparency

One of the notable choices in RISE Chain’s go-to-market strategy is its deep integration with Dune Analytics, which provides a public, queryable interface to the chain’s on-chain data from day one. Dune has become a de facto standard for on-chain analytics across Ethereum and other ecosystems, giving researchers, traders, and journalists the ability to write SQL-like queries against blockchain data and publish dashboards that track everything from protocol revenues to user retention cohorts. By making RISE’s transactions, blocks, and market interactions fully accessible through Dune, the chain positions itself as radically transparent, a key property for a network that wants to host high-stakes financial activity.

This integration matters at several levels. For traders and quants, real-time access to order-book data, depth metrics, and execution quality across venues on RISE can inform algorithmic strategies and risk management frameworks, bringing the analytics standards of traditional finance into on-chain markets. For DeFi researchers and protocol teams, Dune dashboards can be used to monitor liquidity fragmentation, user concentration, and protocol-level revenue, helping them adjust incentive programs or fee structures in response to evolving behavior. For regulators and compliance teams in institutions that eventually interface with RISE-based protocols, the ability to audit flows via public analytics can be an important part of due diligence.

The Dune integration also dovetails with a broader trend of growing interest in Ethereum data and analytics as retail participation returns. Search trends around “Etherium” (misspelled) have spiked in the past, historically associated with waves of retail inflows and increased volatility in ETH and related tokens. As Bitcoin and Ethereum re-approach or surpass prior highs, and as ETF-driven flows and stablecoin issuance expand, the ability to analyze not just price but on-chain behavior becomes more critical to understanding market structure. RISE, by making its data easily accessible from launch, lowers the barrier for both professional and amateur analysts to scrutinize its markets, which in turn can foster a healthier culture of critique and transparency.

Positioning within Ethereum and DeFi

RISE Chain enters an Ethereum ecosystem that is already dense with scaling solutions, including generalized optimistic rollups, zk-rollups, and application-specific L2s. Galaxy, which has publicly backed RISE, frames it as a “new kind of L2” delivering high throughput and fast finality while remaining aligned with Ethereum’s decentralization ethos. That alignment is meaningful for investors and developers who see Ethereum as the canonical settlement layer for programmable money and who want L2 scalability without sacrificing the security and composability benefits of the Ethereum base layer. In this sense, RISE aims to complement rather than replace incumbent L2s, differentiating through ultra-low latency and market-centric design rather than raw TVL or user count.

This positioning intersects with the broader rise of Ethereum-centric platforms as key profit centers in the crypto industry. Bernstein’s decision to rate Coinbase as an outperform stock with a notably high price target was explicitly linked to Coinbase’s emergence as a pivotal Ethereum player, benefiting from the Base L2, ETH staking, and stablecoin growth on Ethereum. In that landscape, RISE is part of a second wave of Ethereum-aligned scaling projects that emphasize specialized functionality and institutional-grade performance, much as Base emphasizes integration with Coinbase’s user base and compliance stack.

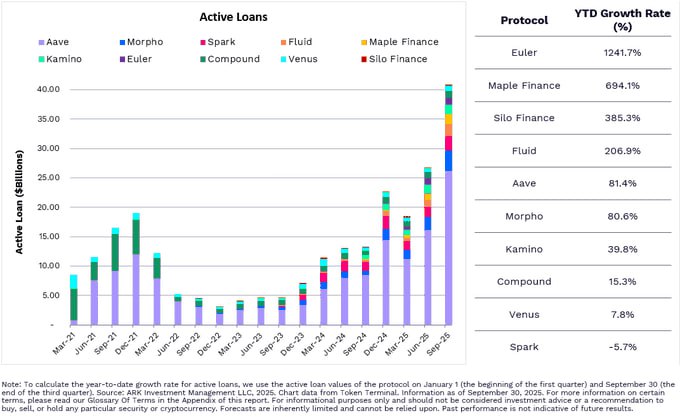

At the same time, DeFi itself is undergoing a sectoral rotation. While liquid staking previously dominated, recent data have highlighted DeFi lending as the top sector by deposits, with tens of billions of dollars in on-chain loans across platforms led by Aave and its peers. Some analyses have noted that, despite overall market recovery, traditional DeFi categories such as lending, liquid staking, and spot DEXs have seen more modest growth or even contraction in volumes, as users gravitate toward derivatives venues, restaking, and newer primitives. RISE’s focus on high-frequency markets positions it directly within this shift toward more leveraged, derivative-intensive strategies, and its success will likely depend on whether those flows continue to migrate on-chain in search of better execution and capital efficiency.

Funding, Governance, and Crypto VC Interest

RISE Chain has attracted backing from Galaxy Ventures, the venture arm of Galaxy, which invests in “cutting-edge founders, technologies, and business models” across crypto software infrastructure and financialized applications. Galaxy’s public commentary on RISE emphasizes its potential to scale Ethereum with “infinite speed and decentralization” in a manner that remains philosophically aligned with Ethereum’s core values. This endorsement is notable in a venture capital climate where aggregate crypto VC funding has declined, even as some firms, including Galaxy itself, remain publicly optimistic about the long-term trajectory of infrastructure investments.

The decision by a prominent institutional investor to support a performance-optimized L2 speaks to a broader thesis: that the next phase of DeFi will require not only more secure and compliant primitives, but also infrastructure capable of matching or exceeding the latency and throughput of traditional financial systems. This is the same thesis animating projects around on-chain treasuries, digital asset treasury companies (sometimes dubbed DATCOs), and tokenized real-world assets, where large enterprises and financial institutions experiment with bringing loans, bonds, and other instruments on-chain. Recent moves by Societe Generale’s SG Forge to bring parts of its loan book on-chain using MiCA-compliant stablecoins via Morpho underscore this trend toward DeFi as backbone infrastructure for global finance, rather than a purely retail trading playground.

In such a world, governance and risk management structures become more salient. While RISE Chain is still early in its lifecycle, questions about who controls upgrades, sequencer operations, fee markets, and MEV capture will frame institutional comfort levels. For crypto-native users, the more immediate question is whether RISE’s governance will be credibly neutral and responsive, or whether it will re-centralize key chokepoints in the name of performance. The experience of other L2s suggests that paths from highly centralized to progressively decentralized governance are possible, but they require real commitment and transparent roadmaps rather than purely rhetorical alignment with Ethereum’s decentralization ethos.

RISE Launchpad on Solana: Floor Prices, Borrowing, and Speculation

Solana DeFi and the Launchpad Context

RISE Launchpad operates not on Ethereum but on Solana, an alternative high-performance Layer 1 that has become a leading DeFi ecosystem with billions in total value locked and a fast-growing user base. Solana’s architecture, with its high throughput and low transaction fees, has made it particularly attractive for trading-heavy applications, memecoins, and interactive consumer experiences where per-transaction costs on Ethereum would be prohibitive. Within this ecosystem, lending protocols such as Kamino, MarginFi, Solend, Jupiter Lend, and Drift illustrate the richness of Solana’s DeFi stack, offering everything from cross-margin lending to integrated swap-and-lend functionality.

In this setting, token launchpads and IDO platforms have proliferated, often serving as the entry point for new retail participants who are drawn to Solana’s memecoin culture and rapid-fire trading environment. Traditional launchpads typically allow teams or communities to list tokens, raise liquidity, and bootstrap markets, but they often provide limited structural protection against rug pulls, liquidity drains, or complete price collapses. As a result, token launches can exhibit extremely skewed payoff distributions, with a small number of outsized winners and a long tail of near-total losses, reinforcing the perception of memecoin trading as a form of gambling rather than investment.

RISE Launchpad positions itself as an attempt to engineer better downside protection into this process, using protocol-level mechanisms to enforce a floor price for each launched token and enabling instant borrowing against that floor. This model draws conceptually on developments in structured DeFi products and collateralized lending, but imports those ideas into the memecoin and launchpad context. The premise is that, by guaranteeing that a token’s price cannot fall below a certain level determined by its protocol reserves or liquidity structure, RISE can limit the extent of catastrophic losses while still allowing for potentially unbounded upside if speculative demand surges.

This approach intersects with Solana’s DeFi primitives because the enforceable floor price can serve as a form of collateral; if the protocol can credibly guarantee that tokens can always be redeemed or sold back at the floor, holders can borrow against that minimum value at some loan-to-value ratio without taking full exposure to spot market volatility. In practice, the risk still depends heavily on how the floor is implemented, which reserves back it, and how those reserves are managed across market cycles. However, the conceptual link between launchpads and lending is a notable evolution from earlier eras where token launches and borrowing were distinct phases in a project’s lifecycle.

Mechanism Design: Floor Prices and Instant Borrowing

The core notion behind RISE Launchpad is a protocol-enforced, non-decreasing floor price for launched tokens. Social media commentary has emphasized that tokens launched through RISE have a permanent floor price that can only move upward over time, with some designs targeting the floor as a fixed proportion of the token’s historical all-time high. While the exact implementation can vary, one broad design pattern is to route a portion of primary issuance or trading fees into a reserve pool that stands ready to buy back tokens at the floor price, ensuring that the market cannot clear below this level without depleting the reserve.

On top of this floor, RISE introduces instant borrowing functionality, allowing token holders to borrow against the guaranteed value of their holdings, effectively collateralizing the floor while retaining exposure to any upside above it. Compared with traditional lending protocols where collateral is valued at volatile spot prices with conservative loan-to-value ratios, this structure aims to simplify risk assessment: as long as the protocol’s reserve mechanism remains solvent and the floor remains credible, the collateral value used in borrowing decisions may be more stable than the market price. This is conceptually similar to how over-collateralized stablecoin systems use crypto collateral to back a more stable asset, but here the “stable” component is a minimum price level for an otherwise volatile token.

This structure has several implications for both issuers and traders. For issuers, the existence of a floor can make token launches more palatable to users who are wary of total loss scenarios, potentially expanding the pool of participants who are willing to engage with new tokens. For traders, being able to borrow against the floor creates opportunities for leveraged strategies, such as borrowing stablecoins to fund additional purchases of the token or to diversify into other assets, while knowing that at least some portion of their collateral’s value is structurally protected. However, it also introduces the risk of reflexivity: if the floor’s credibility comes into question, or if reserve management is misjudged, the sudden evaporation of perceived safety can trigger cascades of deleveraging and panic selling.

The integration of borrowing into the launchpad model must also be understood in the context of Solana’s broader lending ecosystem. On Solana, lending and borrowing are governed by smart contracts where users supply assets to lending pools and earn interest, while borrowers pledge collateral and face potential liquidation if collateral value falls relative to debt. Interest rates in these protocols are dynamic, adjusting based on supply and demand rather than being fixed. RISE’s instant-borrowing feature can be thought of as a specialized lending product built around newly launched tokens, potentially interfacing with or complementing existing Solana lending protocols by creating a pipeline from launch to collateralization.

Memecoins, Hyperfinancialisation, and Risk Culture

The RISE Launchpad emerges amid what many commentators have described as a cycle of hyperfinancialisation within crypto, where gambling-like behavior and complex financial engineering increasingly intertwine. Essays such as “Hyperfinancialisation: On the rise and ouroboric nature of gambling and financialisation” have connected the dots between memecoins, perpetual futures, restaking derivatives, and NFT speculation, arguing that the crypto ecosystem has become a self-referential machine that financializes ever-smaller slices of attention and culture. RISE Launchpad, with its combination of memecoin-friendly branding and structured downside protection, sits squarely within this discourse.

On the one hand, protocol-enforced floors and integrated borrowing can be framed as an attempt to civilize degenerate behavior, placing guardrails around speculative activity so that participants are less likely to be completely wiped out by a single ill-timed token purchase. On the other hand, by lowering the perceived risk of participation and making leverage more accessible at the point of token issuance, such designs can amplify speculative fervor and feed into the very ouroboric dynamics critics highlight. The experience of ConstitutionDAO and the subsequent rise of memecoins has shown how quickly narratives and social momentum can transform financial experiments into cultural phenomena, for better or worse.

This tension plays out in a macro environment where interest rates, risk appetite, and retail participation are all in flux. FedWatch indicators have at times shown notable increases in the probability of rate cuts, which traditionally supports risk assets by lowering discount rates on future cash flows and encouraging yield-seeking behavior. At the same time, central banks such as the ECB have warned banks to brace for potential rises in bad loans amid stress in small business and real-estate sectors, pointing to underlying fragilities in the real economy. Against this backdrop, the crypto market has seen Bitcoin extend rallies to new record highs above certain psychological levels, driven in part by inflows into spot ETFs, while Ethereum has benefited from surging interest in its ecosystem and from stablecoin growth.

In such cycles, search data showing a spike in misspelled “Etherium” queries have historically been interpreted as an indicator of returning retail traders, often preceding increased volatility and froth. RISE Launchpad, built on Solana, is likely to be a beneficiary of similar waves of speculative inflows when retail enthusiasm peaks. The question for a long-term observer is whether its mechanism design can channel that energy into more sustainable token economies, or whether it will simply add another layer of leverage and complexity to the existing memecoin landscape.

"Yearn saved my life" - a new article by Sam from RISE

TL;DR: Sam recounts how a critical vulnerability in an early Yearn-based vault nearly put $50M at risk, and how the Yearn team stepped in calmly and decisively to secure user funds, shaping his long-term approach to onchain security. That experience underpins RISE’s decision to partner with Yearn today, entrusting them with curating portfolio margin markets, managing AutoYield vaults, and overseeing RLP looping—because Yearn consistently prioritizes security, principled risk management, and long-term sustainability over short-term yield.

- 01ETF systemic risk concentration

The top headline framed Bitcoin ETF adoption not as triumph but as new institutional fragility, pulling readers who track whether TradFi on-ramps create rather than absorb systemic risk.

- 02EigenLayer displacing Lido

The $2.5bn Lido outflow story cast restaking protocols as existential competition, attracting readers tracking which staking layer survives the LRT wave — a dynamic directly relevant to any new L2 seeking TVL.

- 03Yield-bearing stablecoin proliferation

The ETHDenver yield-stablecoin talk paired with the NY Fed warning drew readers debating whether the category is durable infrastructure or the next fragility vector before it reaches scale.

- 04RISE Chain L2 Galaxy backing↗

Galaxy Ventures' public investment in RISE Chain attracted readers weighing whether institutional conviction in a high-speed Ethereum L2 is a signal or a narrative play in a saturated market.

- 05RISE Launchpad floor-price mechanics↗

The Solana launchpad's built-in floor price protection and instant borrowing drew readers already skeptical of token-launch sustainability after the points-vs-airdrop debate peaked.

- 06Points and airdrop sustainability doubt

The 40-billion-points story crystallized reader anxiety that tokenomic incentive layers — including those backing new launchpads like RISE — are structurally unsustainable for retail participants.

Rise Works: Crypto Payroll and Web3 Workforce Rails

Product Overview and Integrations

While RISE Chain and RISE Launchpad operate primarily at the trading and speculation layers of crypto, Rise as a payroll and workforce solution tackles a more quotidian but foundational problem: how to pay people around the world using crypto. Rise offers global payroll services that allow organizations to streamline payments to both contractors and full-time employees in multiple forms, including local fiat currencies, stablecoins, and other cryptocurrencies. This multi-currency flexibility is particularly valuable for crypto-native teams whose treasuries are denominated in digital assets but whose contributors live in jurisdictions with different currencies and regulatory regimes.

The platform emphasizes no-code integration with existing tools, lowering the barrier for small teams and DAOs that may lack dedicated finance or engineering staff. It also provides built-in integrations with DeFi protocols such as Uniswap, enabling on-chain treasury rebalancing and payouts without requiring teams to manually interact with DEX interfaces for every transaction. In effect, Rise acts as a middleware layer between on-chain treasury management and off-chain human resources processes, handling the complexity of currency conversion, payment routing, and compliance while allowing organizations to preserve crypto-native funding and compensation models.

This functionality has become more relevant as stablecoins and tokenized treasuries have grown in prominence. ARK’s reporting in its DeFi Quarterly has highlighted the rise of digital asset treasuries and tokenization as key trends, while Galaxy’s research on digital asset treasury companies (DATCOs) has explored how corporates and public companies are using capital markets to accumulate crypto. In this landscape, a payroll platform that can pay out in stablecoins denominated in dollars or other currencies becomes a natural extension of treasury strategy, especially when combined with on-chain investments and yield generation.

Why Crypto Payroll Matters in a Stablecoin World

The importance of crypto payroll cannot be separated from the rise of stablecoins as global money-like instruments. Dollar-based stablecoins have seen rapid adoption across emerging markets, often outcompeting local currencies in terms of perceived stability and integration with global commerce. In Africa, for example, initiatives aimed at de-dollarization and regional currency blocs have struggled to gain traction in part because dollar stablecoins remain attractive and convenient for users and businesses, undermining purely policy-driven efforts to move away from the dollar. At the same time, MiCA-compliant euro stablecoins and other regulated fiat-backed tokens are beginning to provide alternatives within Europe and other regions.

For remote-first, globally distributed crypto teams, paying salaries and contractor fees in stablecoins offers concrete advantages. It can reduce friction and settlement times compared with traditional cross-border bank transfers, minimize conversion costs, and allow contributors to hold or convert into whatever assets they prefer, including Bitcoin, ETH, or local fiat. Platforms like Rise serve as coordination tools that abstract away much of the complexity, providing a single interface where a DAO or startup can schedule payments, manage payouts, and track obligations while the underlying system handles on-chain and off-chain interactions.

This also intersects with the trend of on-chain corporate treasuries. As more companies hold digital assets directly, whether as a strategic reserve or as operating capital, they face the question of how to transform those holdings into payroll without repeatedly exiting into fiat via centralized exchanges. Using a crypto payroll solution that can draw on DeFi liquidity, swap into stablecoins, and distribute funds directly to users’ wallets closes this loop. The experience of firms like Societe Generale’s SG Forge, which has moved parts of its loan book on-chain using MiCA-compliant stablecoins and integrated with DeFi protocols such as Morpho, suggests a future where large institutions and smaller Web3-native teams share a common settlement substrate, even if their governance and compliance frameworks differ.

Compliance, FX, and Treasury Risk

The move toward crypto payroll raises regulatory and risk management questions that platforms like Rise must navigate carefully. Paying employees in crypto can trigger different tax treatment depending on jurisdiction, and withholding obligations may vary widely. Moreover, payroll flows are a key focus area for anti-money-laundering and sanctions enforcement: platforms need robust KYC processes and transaction monitoring to ensure that they are not facilitating illicit payments, especially as cryptocrime continues to evolve. Recent reporting has highlighted how crypto crime is increasingly moving offline, with physical attacks and coercion targeting individuals known to hold substantial digital assets, underscoring that security concerns extend beyond smart-contract vulnerabilities.

Currency risk is another major consideration. While paying in Bitcoin or ETH might appeal to some contributors, the volatility of these assets can make them poor units of account for salaries, and sharp drawdowns can create financial hardship for employees who have bills denominated in fiat. Stablecoins mitigate this to some extent but introduce counterparty and regulatory risk: if a stablecoin issuer faces legal action, banking problems, or chain-specific sanctions, payroll flows could be disrupted. Platforms like Rise must therefore design systems that can switch between different stablecoins or payout channels as needed, maintaining continuity of payroll even as the regulatory environment shifts.

Interest-rate dynamics also play a role. In a world where on-chain yields from DeFi lending, restaking, or tokenized treasuries compete with off-chain cash rates, treasury managers must decide how much to keep in fully liquid, non-yielding stablecoins versus riskier on-chain instruments. If central banks such as the Federal Reserve are expected to cut rates, DeFi yields may regain relative attractiveness, potentially incentivizing treasuries to keep more capital on-chain, some of which might be routed through payroll solutions. Conversely, if bank deposit rates or short-term government yields remain high, the opportunity cost of idle stablecoin balances increases. Crypto payroll providers, in this context, are not just payment processors but integral parts of an organization’s broader treasury strategy.

Data, Culture, and the Broader “RISE” Narrative

RISE+, Fandom, and Attention Markets

Beyond finance-specific infrastructure, the RISE brand also surfaces in projects like RISE+, a fan hub for the Alpine Formula One team that offers games, XP-based rewards, competitions, and exclusive race-week content. RISE+ recently launched a new Race Hub with additional games and engagement mechanics, further blurring the lines between fan engagement, gaming, and loyalty programs. While not itself a DeFi or crypto-trading platform, RISE+ exemplifies how digital attention and participation are being structured in ways that are increasingly compatible with tokenized or financialized overlays, even when those overlays are not yet present.

The rise of AI shopping agents and AI influencers adds another layer to this story, as brands and creators explore how algorithmic agents can mediate consumer choices, content discovery, and fan interactions. In such a world, platforms like RISE+ can be seen as proto-environments where engagement metrics, reputational scores, and attention spans could eventually be tied into token incentives, NFTs, or other forms of digital property. From the perspective of a crypto observer, the key point is that “RISE” is not only about blockchains and DeFi; it is also a signpost in the ongoing convergence of entertainment, identity, and financialization.

Storytelling and Personal Narratives

Within the RISE ecosystem, storytelling plays a significant role in shaping culture and expectations. Articles such as “Yearn saved my life,” authored by a contributor associated with RISE, highlight the deeply personal impact that DeFi protocols and yield strategies can have on individuals. Yearn Finance, one of the earlier yield-aggregation protocols on Ethereum, became emblematic of a cohort of DeFi users who used on-chain strategies to escape traditional financial constraints, pay off debts, or fund life changes. By publishing such narratives, RISE-affiliated voices contribute to a broader mythology around DeFi as not just a technical or speculative enterprise, but a transformative one at the individual level.

At the same time, reflective pieces on hyperfinancialisation and the degeneracy of crypto markets serve as counterweights to purely celebratory narratives. They ask whether the same tools that help some people achieve financial freedom are also fueling excessive gambling, short-termism, and social harm, particularly when leveraged by retail traders who do not fully grasp the risks. These debates mirror larger conversations in finance about responsible innovation, consumer protection, and the line between speculation and exploitation. For projects under the RISE umbrella, engaging with these questions is part of maintaining credibility in a maturing ecosystem.

Research, Analytics, and Institutionalization

The integration of RISE Chain with Dune Analytics, the publication of DeFi research by firms like ARK and Galaxy, and the move of institutions such as Societe Generale into on-chain lending and stablecoins all point toward a deepening institutionalization of DeFi data and analysis. ARK’s DeFi Quarterly, with its focus on stablecoins, tokenization, and digital asset treasuries, provides a framework for understanding where capital is flowing and which primitives are gaining traction. Galaxy’s work on DATCOs and its decision to invest in RISE Chain further underscore how institutional players are not only analyzing but also shaping the infrastructure they study.

For users of RISE platforms, this means that activity on these networks is likely to be scrutinized and modeled in increasingly sophisticated ways, from VaR models for high-frequency trading strategies on RISE Chain to credit-risk assessments for floor-price borrowing on RISE Launchpad. It also means that the data exhaust from these systems becomes part of the broader informational substrate that traders, regulators, and even AI-driven agents will use to make decisions. As AI becomes more integrated into trading and portfolio management, the availability of rich, structured on-chain data via platforms like Dune could make RISE’s markets particularly attractive for machine-driven strategies.

Risk, Security, and Cryptocrime

No discussion of RISE would be complete without acknowledging risks and security challenges. The concentration of high-frequency trading activity on a single L2 raises questions about systemic risk: a bug in the rollup’s state transition function, a failure in the preconfirmation logic, or a governance attack could have outsized impact on markets built atop RISE Chain. Smart contracts interacting with MarketCore order books add complexity in both code and execution paths, increasing the surface area for exploits or unexpected interactions. Similarly, the solvency of the floor-price reserves on RISE Launchpad is a point of potential failure; if the reserves are mismanaged, exploited, or depleted in a stress event, the promise of a permanent, non-decreasing floor could be broken, leading to loss of confidence.

Beyond protocol-level risks, the broader evolution of cryptocrime adds a human dimension. Cybersecurity reporting has documented how, as on-chain surveillance and compliance measures improve, some criminals have shifted toward offline attacks, including kidnappings, coercion, and other physical threats targeting crypto holders and key personnel. For teams building and using RISE platforms, security practices must therefore encompass both technical controls and personal safety, especially in contexts like payroll where identifiable individuals receive regular payments. As stablecoins and crypto payments gain mainstream traction, the stakes for both digital and physical security will only increase.

RISE Launchpad launches on Solana with permissionless token launches featuring built-in floor price protection and instant borrowing to cap downside risk while capturing unlimited upside potential

Floor-backed bonding curves aren't new — Tuna did zero-loss exits with 60-min lockups back in December — but bolting a lending layer on top changes the game theory entirely. Instead of panic-redeeming at floor and draining the reserve pool, holders borrow against their floor collateral and stay exposed to upside, which in theory reduces cascading sell pressure at the exact moment it matters most. Smart mechanism design, but the second-order question nobody's asking: if a token trends toward floor and most holders have already borrowed against it, who's left to absorb the bad debt when those loans go underwater? With only ~13k followers at launch, the real stress test hasn't happened yet — floor protection is easy to promise when inflows exceed redemptions.

RISE Amid Macro Cycles: Bitcoin, Ethereum, Stablecoins, and Rates

Interest Rates, Credit Conditions, and DeFi Yields

The evolution of RISE projects cannot be separated from the broader macro environment, particularly interest rates and credit conditions. When market-implied probabilities, such as those tracked by FedWatch, point to rising odds of rate cuts by central banks, risk assets including Bitcoin, ETH, and DeFi tokens often see renewed inflows, as lower discount rates and search-for-yield dynamics support valuations. Conversely, when central banks raise rates aggressively or signal prolonged tightness, risk assets tend to suffer, and DeFi yields must compete with attractive off-chain alternatives in money markets and short-term bonds.

At the same time, traditional banks have been warned by authorities such as the ECB to prepare for a potential rise in non-performing loans amid stress in small business and commercial real estate sectors. This combination of tighter bank credit and the search for alternative yield sources is part of what drives interest in DeFi lending, tokenized treasuries, and on-chain credit. RISE Chain’s focus on financial applications positions it as a potential venue for interest-rate derivatives, credit products, and structured DeFi instruments that benefit from low latency and transparent settlement. RISE Launchpad’s borrowing features tap into the same demand for leverage and yield, but in a more speculative, memecoin-inflected domain.

For stablecoin-centric payroll platforms, interest rates shape the opportunity cost of holding idle balances. If DeFi lending on Ethereum, Solana, or RISE-based protocols offers competitive yields, treasuries may be more willing to keep working capital on-chain, ready to be deployed for payroll or other operational needs. Conversely, if off-chain yields dominate, on-chain capital may be concentrated in only the highest-conviction strategies, with more conservative organizations preferring to keep payroll funds in traditional bank accounts. The behavior of DATCOs and other corporate treasuries will likely be driven by these relative yield considerations, alongside regulatory and operational constraints.

Bitcoin, Ethereum, and Retail Cycles

Bitcoin and Ethereum remain the gravitational centers of the crypto universe, and their cycles influence the fortunes of projects like RISE, even when those projects are technologically distinct. In periods when Bitcoin extends rallies to new all-time highs, supported by inflows into ETFs and growing institutional adoption, liquidity and risk appetite generally spill over into altcoins, DeFi tokens, and speculative platforms such as Solana launchpads. Ethereum’s own performance, boosted by ecosystem growth, stablecoin expansion, and scaling breakthroughs, further shapes the willingness of developers and users to experiment with new L2s like RISE Chain.

Retail participation is a key amplifier in these cycles. Spikes in Google searches for terms like “Etherium” have historically coincided with retail inflows, aggressive leverage-taking, and higher volatility in ETH and related assets. Similar patterns can be seen when memecoin seasons erupt on Solana, with trading volumes and token launches exploding as retail traders chase quick gains, only to shrink sharply when the cycle turns. RISE Launchpad is explicitly positioned to capture this energy, offering a more structured environment for token launches that might appeal to both degenerate traders and slightly more risk-conscious participants.

For RISE Chain, the timing of its mainnet launch and ecosystem growth relative to Ethereum’s broader cycle will matter. If it can attract liquidity, builders, and market-makers during a period of rising ETH prices and renewed interest in DeFi, it may benefit from a positive feedback loop of TVL growth, volume, and developer mindshare. If, however, it launches into a bear phase or is overshadowed by larger L2s with deeper integrations into platforms like Coinbase’s Base, it may need to rely more heavily on niche use cases and differentiated performance characteristics to gain traction.

Stablecoins, De-dollarization, and Global Finance

Stablecoins are the connective tissue between the various RISE projects and the broader financial system. Dollar-based stablecoins remain dominant, serving as the primary quote and settlement asset in most DeFi markets and as a de facto dollar proxy in many emerging economies. At the same time, experiments in de-dollarization, such as regional currency blocs in Africa or initiatives by BRICS countries to reduce reliance on the US dollar, have faced headwinds, in part because stablecoins deepen dollar penetration even where local policymakers seek alternatives. This dynamic complicates narratives about the dollar’s imminent collapse, even as critics warn of long-term risks from debt accumulation and geopolitical shifts.

Within Europe and other regulated jurisdictions, MiCA-style frameworks are enabling regulated stablecoins that can be used by institutions like Societe Generale’s SG Forge to bring loan books and other assets on-chain via protocols such as Morpho. These developments point toward a future where on-chain finance is not only about crypto-native tokens but also about tokenized representations of traditional financial instruments. RISE Chain, with its focus on financial applications, could be a natural home for such tokenized assets, particularly if its performance characteristics and Ethereum alignment appeal to institutions. Crypto payroll platforms like Rise, meanwhile, can leverage both dollar and non-dollar stablecoins to support workers in diverse regulatory and economic environments, allowing organizations to adapt to local expectations while maintaining a unified on-chain treasury.

For RISE Launchpad, stablecoins serve as both the source of demand for new tokens and the asset against which borrowing occurs. If a launched token’s floor price is denominated in stablecoins, then the solvency and trustworthiness of those stablecoins become embedded in the risk profile of the entire system. Users must understand not only the contract-level guarantees around floors and reserves, but also the underlying stability of the stablecoins themselves, including their regulatory treatment, reserve composition, and operational resilience.

DeFi Lending, Liquid Staking, and New Primitives

Recent data have highlighted that DeFi lending has eclipsed liquid staking as the top sector by deposits, with platforms such as Aave driving a large share of on-chain lending activity. This shift reflects a maturation of DeFi where borrowing and lending, rather than staking derivatives alone, are seen as the core primitives around which more complex strategies are built. On Solana, lending protocols like Solend, MarginFi, Kamino, Jupiter Lend, and Drift provide analogous functionality, allowing users to deposit assets, earn interest, and borrow against collateral in a permissionless way. Loan-to-value ratios govern how much users can borrow, and falling collateral values can trigger liquidations, reinforcing the need for careful risk management.

RISE Launchpad’s integration of instant borrowing into the token launch process is a natural extension of this lending-centric paradigm, albeit one targeted at more speculative activity. RISE Chain, meanwhile, can host its own suite of lending and derivatives protocols, potentially leveraging its order-book infrastructure to create more sophisticated credit markets and fixed-income products. For example, interest-rate derivatives, yield-tokenization schemes, and on-chain repo markets could all benefit from a high-performance execution environment aligned with Ethereum’s security model.

The interplay between RISE platforms and existing DeFi categories will likely shape their long-term relevance. If lending, stablecoins, and tokenized real-world assets continue to dominate DeFi, RISE will need to demonstrate that it is more than a niche venue for high-frequency traders or memecoin speculators. Its success will depend on whether it can host products that matter to institutional treasuries, DATCOs, and mainstream users, including those who interact with crypto primarily through Bitcoin ETFs, regulated stablecoins, or embedded finance applications rather than through native wallets and DEXs.

How Users and Builders Might Engage with RISE

Traders and DeFi Power Users

For traders and DeFi power users, RISE Chain offers a potential venue for low-latency, order-book-centric strategies anchored to Ethereum’s security and composability. Users familiar with Ethereum L2s would typically bridge assets to RISE, interact with compatible wallets, and trade on protocols that leverage MarketCore’s shared order books. The availability of rich analytics via Dune means that sophisticated participants can monitor execution quality, liquidity conditions, and protocol behavior in near real time, aiding in both alpha generation and risk management. However, the complexity of the infrastructure and the rapid pace of high-frequency markets mean that retail users should approach with caution, fully understanding the risks of derivatives, leverage, and MEV.

On Solana, RISE Launchpad will attract users interested in participating in token launches with structural downside protections. Traders may choose to purchase tokens with protocol-enforced floors, borrow against their holdings, or construct strategies that exploit the interaction between floor mechanics and market sentiment. To do so responsibly, they must understand the specifics of floor implementation, reserve backing, and liquidation rules, as well as the broader risks of memecoin cycles and liquidity dries-ups. Users familiar with Solana lending protocols and DeFi primitives will be at an advantage in navigating these opportunities and pitfalls.

Builders and Project Teams

For builders, RISE Chain provides a canvas for market-centric DeFi protocols, from order-book DEXs and perpetual futures exchanges to structured-product platforms and institutional trading venues. EVM compatibility lowers the barrier for teams that already have Ethereum-based codebases, while Dune integration facilitates transparent reporting and analytics from day one. Developers need to pay close attention to latency assumptions, execution guarantees, and MEV considerations, ensuring that their protocols behave correctly under the high-throughput conditions that RISE is designed to support. For DAOs and DeFi teams, deploying on RISE can be a way to reach more sophisticated traders, but it may also require revisiting tokenomics, fee models, and governance to reflect a more professional user base.

On Solana, projects can use RISE Launchpad as a distribution and price-discovery mechanism for new tokens, particularly those that want to offer some form of built-in downside protection or collateralization utility. Integration with existing Solana DeFi protocols for additional lending, staking, or liquidity mining can extend the usefulness of launched tokens beyond speculative trading. Teams must design carefully around the interplay between floor-price promises, reserve management, and community expectations to avoid creating perverse incentives or unsustainable dynamics.

For organizations managing teams and contributors, Rise’s payroll solution can serve as a backbone for crypto-native compensation, enabling them to pay salaries, grants, or bounties in stablecoins or other digital assets while maintaining compliance and operational efficiency. Integrations with DeFi protocols like Uniswap can help automate treasury rebalancing and reduce friction in moving between volatile treasury assets and stable payroll currencies. Builders must still engage with local tax and regulatory regimes, but platforms like Rise can help standardize processes and reduce operational overhead.

Institutions, Treasuries, and DATCOs

Institutional actors, including corporates experimenting with digital asset treasuries, banks exploring on-chain lending, and funds allocating to DeFi strategies, will evaluate RISE platforms through a different lens. They will prioritize security, governance, compliance, and data transparency. For RISE Chain to attract such participants, it must demonstrate robust security practices, a credible path toward decentralized governance over time, and clear relationships with Ethereum’s legal and regulatory perimeter. Its partnership with Galaxy and integration with Dune are positive signals, but institutional adoption will hinge on the chain’s track record and on the maturity of the protocols built atop it.

Institutional treasuries may find Rise’s payroll tools attractive as part of a broader shift toward on-chain treasury management, where stablecoins and tokenized assets play a growing role in liquidity and yield strategies. The experience of SG Forge and similar initiatives shows that large institutions are willing to transact on DeFi rails when regulatory frameworks like MiCA provide clarity. DATCOs and other corporates that hold Bitcoin, ETH, and stablecoins on their balance sheets may use crypto payroll as a way to operationalize these holdings in everyday business operations, rather than treating them solely as speculative or reserve assets.

RISE Chain is a newly live Ethereum L2 with minimal mainnet history; its parallel execution and throughput claims have not been stress-tested under adversarial or high-congestion conditions.

RISE Launchpad's floor price protection relies on instant borrowing mechanisms that are untested at scale — a model structurally similar to collateral loops that triggered liquidity spirals in prior DeFi cycles.

Galaxy Ventures' prominent backing concentrates early governance narrative and institutional signaling with a single large backer, creating key-person dependency for adoption momentum.

- RegulatoryMedium

Reader engagement with NY Fed stablecoin warnings and the encryption/privacy crackdown stories reflects that RISE Chain's DeFi integrations inherit a rising regulatory exposure that is not project-specific but sector-wide.

RISE Chain enters a crowded Ethereum L2 landscape; the Lido displacement story in reader clicks illustrates how rapidly market share migrates away from established protocols when a newer primitive gains narrative momentum.

Outlook

Across its different incarnations as an Ethereum Layer 2, a Solana launchpad, and a Web3 payroll provider, RISE functions as a microcosm of crypto’s broader trajectory: high-performance infrastructure for professional markets, experimental mechanisms for structuring speculative risk, and practical tools for integrating stablecoins and digital assets into real-world workflows. Whether the RISE brand ultimately becomes synonymous with a single flagship protocol or remains a constellation of related projects, its evolution will be shaped by the same forces driving the rest of the industry: macro cycles in rates and liquidity, the institutionalization of DeFi, the rise of stablecoins as global settlement media, and ongoing tensions between innovation, speculation, and consumer protection. For a crypto news audience, the key is to treat each RISE project on its own merits, understand the specific risks and design choices involved, and situate them within the larger narratives of Bitcoin, Ethereum, DeFi, and the steadily rising tide of digital asset adoption.

Latest RISE news

Hyperfinancialisation: On the rise and ouroboric nature of gambling and financialisation. This piece was written as an accompaniment to long degeneracy."Yearn saved my life" - a new article by Sam from RISERISE Launchpad launches on Solana with permissionless token launches featuring built-in floor price protection and instant borrowing to cap downside risk while capturing unlimited upside potential FedWatch shows a 69.4% rise in the probability of the Federal Reserve cutting interest rates by 25 basis points in December.

FedWatch shows a 69.4% rise in the probability of the Federal Reserve cutting interest rates by 25 basis points in December. ARK Releases *The DeFi Quarterly* Report for Q3 2025, Highlighting Stablecoins, RWAs, Tokenization, and the Rise of Digital Asset Treasuries

ARK Releases *The DeFi Quarterly* Report for Q3 2025, Highlighting Stablecoins, RWAs, Tokenization, and the Rise of Digital Asset Treasuries Societe Generale’s SG Forge brings its loan book onchain with MiCA-compliant stablecoins via Morpho, signaling DeFi’s rise as the backbone of global finance.

Societe Generale’s SG Forge brings its loan book onchain with MiCA-compliant stablecoins via Morpho, signaling DeFi’s rise as the backbone of global finance.Sources

- https://www.riseworks.io

- https://www.crowdfundinsider.com/2026/05/277744-ethereum-l2-rise-now-live-on-mainnet-on-dune-analytics/

- https://www.alpinef1.com/news/2026-rise-updates

- https://x.com/alchemistaster/status/2047267827527135539

- https://ventures.galaxy.com/portfolio

- https://www.galaxy.com/insights/perspectives/backing-rise-chain-scaling-ethereum-with-infinite-speed-and-decentralization

- https://www.riseworks.io/integration-type/defi-protocols

- https://risechain.com

- https://www.okx.com/en-us/learn/solana-lending-protocols

- https://www.bitget.com/price/rise-launchpad/what-is

- https://www.alpinef1.com/partners

- https://www.youtube.com/watch?v=qw9QcsVGBNQ

- https://x.com/wallstengine/status/1937842233086271585

- https://blog.valr.com/blog/africas-de-dollarization-push-meets-reality-dollar-resilience-stablecoin-rise-shape-future

- https://cybersecurityventures.com/cryptocrime/

- https://blockchain.news/flashnews/etherium-google-search-trend-spike-signals-incoming-retail-demand-for-ethereum-crypto-market-impact-analysis

Community notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…