Comprehensive explainer on Ethereum’s architecture, smart contracts, scaling roadmap, governance, competition with Bitcoin/Solana, ETFs, and key risks, positioning ETH as a programmable global settlement and coordination layer for crypto and tokenized assets.

+53 sources across the wider coverage universe

Attacker mints 1B DOT on Ethereum via Hyperbridge gateway exploit, profits $237K2026-04

Attacker mints 1B DOT on Ethereum via Hyperbridge gateway exploit, profits $237K2026-04 Suspected Thorchain exploit drains $7.4M+ across Bitcoin, Ethereum, BSC, and Base2026-05

Suspected Thorchain exploit drains $7.4M+ across Bitcoin, Ethereum, BSC, and Base2026-05 Ethereum’s Pectra upgrade powers Lido’s consolidation mechanism, letting validators transfer balances directly and stay productive while migrating into stVaults2026-04

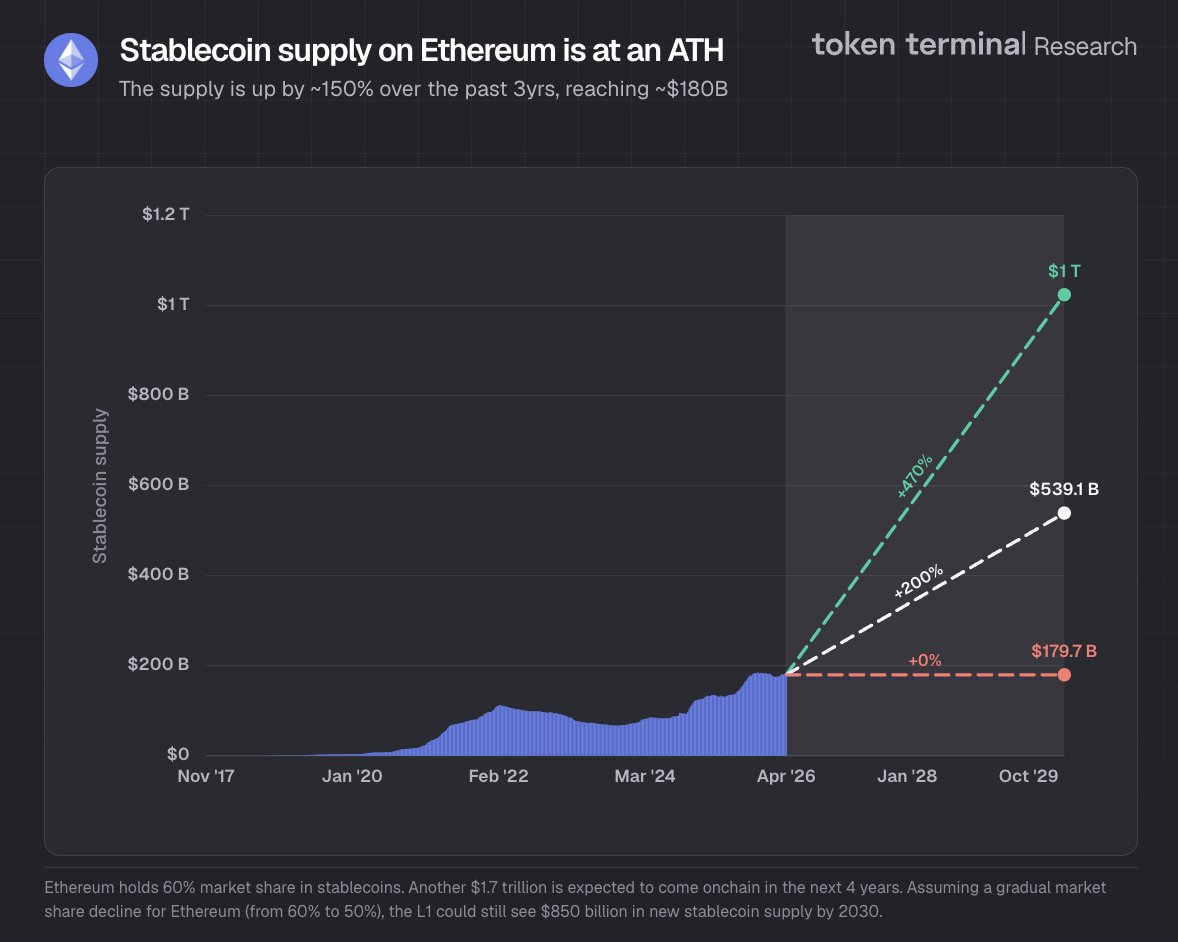

Ethereum’s Pectra upgrade powers Lido’s consolidation mechanism, letting validators transfer balances directly and stay productive while migrating into stVaults2026-04 Ethereum stablecoin supply hits $180B ATH with 60% market share, up 150% in three years2026-04

Ethereum stablecoin supply hits $180B ATH with 60% market share, up 150% in three years2026-04 Ethereum researchers propose “Block-in-Blobs” (EIP-8142) to shift execution data into blobs, reducing validator load while preserving availability in next-gen network scaling push2026-04

Ethereum researchers propose “Block-in-Blobs” (EIP-8142) to shift execution data into blobs, reducing validator load while preserving availability in next-gen network scaling push2026-04 Morpho launches Agents beta, enabling AI systems to read, simulate, and execute lending actions across Ethereum and Base with machine-native interfaces for onchain finance2026-04

Morpho launches Agents beta, enabling AI systems to read, simulate, and execute lending actions across Ethereum and Base with machine-native interfaces for onchain finance2026-04

A programmable public blockchain for decentralized applications, Ethereum combines smart contracts with a native asset, ETH, to provide a general‑purpose settlement layer for crypto finance, digital assets, and emerging on‑chain infrastructure. Rather than focusing on everyday payments, the network is increasingly positioned as shared rails for tokenized assets, identity, coordination, and computation.

What Is Ethereum?

Ethereum is an open, permissionless blockchain that allows anyone with an internet connection to deploy code, issue tokens, and transact using a native cryptocurrency, ETH. Conceptually, it extends the idea introduced by Bitcoin—tamper‑resistant shared ledgers secured by cryptography—by adding a fully programmable virtual machine capable of running arbitrary applications, or smart contracts. Where Bitcoin was designed primarily as a scarce digital asset and transaction network, Ethereum was conceived as a general‑purpose “world computer” on which many different kinds of applications could run.

The idea for Ethereum was first articulated by Vitalik Buterin in a 2013 whitepaper that argued existing blockchains were too limited in expressiveness and that a Turing‑complete scripting environment would enable far richer decentralized applications. In 2014, a group of co‑founders formalized development efforts and conducted a crowdsale of ether to bootstrap funding, with the Ethereum Foundation created as a non‑profit to steward early research and protocol development. The mainnet went live in 2015, marking the launch of a new platform on which developers could deploy smart contracts and issue native tokens without needing permission from any intermediary.

From the outset, Ethereum distinguished itself through its flexibility. The platform’s core innovation is the Ethereum Virtual Machine (EVM), a decentralized runtime environment that executes smart contract bytecode identically on every full node. Instead of hard‑coding a narrow set of operations, Ethereum exposes a low‑level instruction set and a global state, allowing developers to encode arbitrary logic in higher‑level languages like Solidity and then compile to EVM bytecode. This design underpins the network’s evolution from a niche experimental system into the dominant platform for decentralized finance (DeFi), non‑fungible tokens (NFTs), decentralized autonomous organizations (DAOs), and an expanding range of tokenized real‑world assets.

ETH, the native asset, serves intertwined roles in this ecosystem. It is used to pay transaction fees (gas) to compensate validators for including and executing transactions, and it functions as the staked collateral securing the proof‑of‑stake consensus mechanism. ETH also acts as default collateral across DeFi lending protocols, derivatives exchanges, and liquidity pools. Over time, this has shifted ETH’s narrative from purely “utility token” toward a hybrid of digital commodity, productive staking asset, and collateral backbone for on‑chain markets. In parallel, the network’s design and governance have evolved through major upgrades, including the transition from proof‑of‑work to proof‑of‑stake in “The Merge,” which aligned Ethereum’s security model more closely with its on‑chain capital markets.

Ethereum’s history can also be read as a sequence of experiments in what it means to be a global, neutral settlement layer. Early years were dominated by token launches and ICOs, followed by DeFi “money Lego” composability, NFT culture, and today a growing focus on institutional tokenization, layer‑2 scaling, and account abstraction. Each wave has pushed the platform’s infrastructure, economics, and governance in new directions, and the current trajectory stresses Ethereum less as a payments network and more as a programmable coordination fabric for increasingly complex digital economies.

Ethereum's rollup-centric roadmap failed to hide blockchain complexity, forcing users through bridges and fragmented chains while ETH captured little value

$0.0015 median L2 fees are great product work and terrible monetary-premium fuel. Dencun turned Ethereum DA into a cheap wholesale input; Base, Arbitrum and OP can monetize sequencer ordering, app distribution and MEV while L1 burn sits near 74 ETH/day. Chain abstraction may hide the bridge click, but it does not remove the inventory tax: USDC, WETH, perps collateral and LP depth still get split across domains until shared sequencing or synchronous composability makes liquidity feel single-chain again.

Readers click Ethereum through a competitive horse-race frame — clicks cluster on ETH losing ground to Solana on DEX volume and Bitcoin on NFT sales while simultaneously chasing institutional ETF inflow milestones, revealing that the dominant reader question is 'which chain is winning' rather than how Ethereum's technology actually works.

How Ethereum Works: Architecture and Core Concepts

At its core, Ethereum is a distributed state machine maintained by thousands of nodes that agree on a canonical sequence of blocks, each containing transactions that mutate shared state. The state is composed primarily of accounts and their associated data. There are two main types of accounts: externally owned accounts (EOAs) controlled by private keys, and contract accounts controlled by code. Smart contracts are, in Ethereum’s own documentation, essentially programs that run on the blockchain: collections of functions (code) and state (data) residing at specific addresses on the Ethereum network. They are considered a type of Ethereum account, which means they can hold balances and be targets of transactions just like user accounts.

Crucially, smart contracts are not controlled by a person who can arbitrarily change their behavior. Once deployed, their logic is fixed unless they were explicitly designed to be upgradeable through proxy patterns or governance systems. A contract is deployed via a transaction that publishes its bytecode to the chain; after that, any user or contract can interact with it by sending transactions that call its functions. The Ethereum Foundation’s developer documentation emphasizes that smart contracts can define rules similar to legal contracts and then automatically enforce those rules through code, with interactions being effectively irreversible and contracts not deletable by default. This “code as law” property makes Ethereum a powerful platform for trust minimization but also amplifies the consequences of bugs and design errors.

The Ethereum Virtual Machine is the deterministic execution environment where this contract logic runs. Every node that validates a block re‑executes the transactions in that block and checks that the resulting state transitions are correct. To keep computation bounded and mitigate denial‑of‑service attacks, Ethereum uses a gas model in which every EVM operation has an associated gas cost. Users specify a gas limit and fee for each transaction; if execution runs out of gas, it reverts, but the gas already consumed is still paid to validators. This creates an economic throttle on the complexity of on‑chain programs and ties network security to ETH, since gas is paid in ETH.

On the consensus side, Ethereum now operates under a proof‑of‑stake (PoS) design. Validators stake ETH into the protocol and, in return, receive the right to propose and attest to blocks. Misbehavior, such as attempting to finalize conflicting blocks, can result in slashing of staked funds. PoS dramatically reduces the energy consumption associated with block production and, in principle, allows economic security to scale with the value staked rather than the hash power of specialized hardware. It also more tightly integrates the ETH asset into protocol security: staking yields, liquidity staking derivatives (LSDs), and restaking protocols all interact with the base layer’s incentive structure.

Ethereum’s account model further shapes its functionality. Unlike Bitcoin’s UTXO model, which tracks individual coins, Ethereum tracks balances and contract storage directly at account addresses. This makes it straightforward for contracts to maintain internal mappings of balances (for example, token ledgers) and is the foundation for fungible token standards such as ERC‑20 and non‑fungible standards like ERC‑721. It also influences how gas is charged for state growth, since every additional storage slot written by a contract increases the global state that nodes must maintain.

These architectural choices have trade‑offs. The EVM’s flexibility enables rapid innovation but also leads to complex security considerations. The account model simplifies token design but makes privacy more challenging, since a single address’s full activity is easily traceable. Proof‑of‑stake makes ETH economically central but opens new attack surfaces around social coordination and validator concentration. Ethereum’s roadmap and ecosystem are, in effect, attempts to address these trade‑offs while preserving the core property that any developer can deploy globally accessible software without permission.

Ethereum as a Global Settlement and Coordination Layer

The most compelling narrative in Ethereum’s current phase is less about peer‑to‑peer payments and more about becoming a global settlement and coordination layer. Rather than directly competing with credit card networks at the point of sale, Ethereum aims to sit underneath a stack of applications, rollups, and institutions, providing neutral, programmable rails on which financial assets, identity primitives, and coordination mechanisms can be built.

This thesis is increasingly articulated by builders and investors who see Ethereum as replaying the rise of the open internet. In a recent interview, Etherealize co‑founder Vivek Raman argued that tokenization—bringing traditional financial assets and infrastructure on‑chain—is Ethereum’s clearest product‑market fit. He emphasized that the most consequential use case is to move the financial sector and asset infrastructure onto Ethereum, not just consumer gaming or speculative applications. Raman and others draw analogies between permissionless blockchains and open‑source software like Linux, contending that, over time, open infrastructure tends to outcompete vertically integrated corporate stacks because it is more composable, auditable, and resistant to single‑firm capture.

Ethereum’s role as a settlement layer becomes tangible when looking at tokenization and on‑chain representations of real‑world assets. Stablecoins are the leading edge of this movement. Recent launches include SEKAU, a fully reserved Swedish krona‑backed stablecoin issued by AllUnity, which debuted simultaneously on five blockchains: Ethereum, Solana, Base, Tempo, and Polygon. According to the issuer, SEKAU is fully backed by reserves and initially available via a business mint account, enabling fully onboarded institutional clients to mint and redeem the stablecoin without fees on the platform. That SEKAU launched natively on multiple chains from day one—and that Ethereum is among the first deployment targets—underscores how the network functions as one of several base settlement layers for fiat‑linked assets, cross‑chain bridges, and institutional payment flows.

A parallel development is the emergence of tokenized bank deposits and regulated stablecoins that blur the line between commercial bank money and on‑chain tokens. Custodia Bank and Vantage Bank, for instance, announced a platform for US community and regional banks to access tokenized deposits via Custodia’s bank‑grade blockchain infrastructure and the Interlace platform from Infinant. On this system, tokens can circulate across banks and switch between representing a tokenized deposit and a compliant stablecoin, depending on regulatory requirements. While not every such initiative is explicitly on Ethereum, many are built using Ethereum‑compatible technology, reinforcing the idea that the network’s standards and tooling form a baseline for regulated on‑chain financial infrastructure.

Decentralized finance further illustrates Ethereum’s settlement‑layer role. Protocols like Uniswap, Aave, and MakerDAO rely on Ethereum to enforce the rules that govern lending, swaps, and collateralization. Uniswap’s own research shows that its API is now the primary routing engine for MetaMask swaps on Ethereum mainnet, winning 52.4% of routing decisions, with the highest reliability and lowest failure rates among providers. This kind of dominance in swap routing suggests that, at the application layer, a small number of robust protocols are aggregating liquidity and routing intelligence on top of Ethereum, even as the underlying chain remains a neutral settlement engine for the actual state transitions.

Beyond finance, Ethereum also hosts NFTs, gaming assets, DAOs, and identity systems that require global coordination. These applications rely on Ethereum not merely as a ledger but as a rule‑enforcing engine that can coordinate behavior among pseudonymous actors. For example, a DAO may encode its governance rules in a smart contract, with voting power linked to token holdings and execution of decisions entirely on‑chain. Similarly, identity projects seek to build attestations and reputation layers on Ethereum that AI agents and humans alike could reference when interacting in permissionless environments. The common thread is that Ethereum’s smart contracts define and enforce shared reality for a wide range of actors who do not need to trust one another individually.

Account abstraction is an important enabler of this settlement‑layer vision. By allowing smart contracts themselves to serve as user accounts, Ethereum can support programmable wallets that include built‑in recovery, spending controls, and multi‑party authorization—features essential for mainstream users and institutions. The EIP‑4337 standard, which introduces a separate transaction flow based on UserOperation objects bundled by validators and executed through an EntryPoint contract, has already led to large‑scale deployment of smart contract wallets. According to Ethereum’s own roadmap documentation, EIP‑4337 went live on mainnet in March 2023 and has since enabled the creation of over 26 million smart accounts and processed more than 170 million UserOperations, illustrating the demand for more flexible account logic. Such abstractions help Ethereum serve as a more user‑friendly substrate for complex transactions without sacrificing its core neutrality.

- 01ETH vs Solana DEX competition

Solana overtaking Ethereum on DEX volume during the memecoin presale frenzy crystallized 'ETH killer' competitive anxiety that draws consistent reader attention to chain-vs-chain metrics.

- 02Spot ETH ETF institutional flows

ARK's SEC filing, BlackRock ETHA crossing $1B in net inflows, and DRW's disclosed Grayscale ETH Trust holdings let readers track whether institutions are selecting ETH as their designated crypto allocation.

- 03Gas fees and L2 scaling trade-offs↗

Gas hitting multi-year lows because of L2 migration and multi-month highs during ERC-404 frenzy simultaneously frames whether Ethereum's fee market is healing or fragmenting.

- 04Vitalik's technical roadmap signals

Proposals like replacing the EVM with RISC-V function as forward guidance from ETH's de facto figurehead, attracting readers who treat Vitalik's public statements as investable signals.

- 05Stablecoin dominance and DeFi yield risk

Ethereum stablecoin volume hitting a $1.46 trillion record paired with Ethena downplaying USDe collateral risk highlights ETH's role as DeFi's settlement layer and the systemic exposure embedded in that position.

- 06MEV and dark forest persistence↗

Coverage of Ethereum's 'dark forest' surviving UX improvements signals readers' concern that sophisticated extractors continue to disadvantage ordinary users despite years of protocol upgrades.

Smart Contracts, Wallets, and Account Abstraction

Understanding Ethereum as infrastructure requires a closer look at smart contracts and the way users interact with them. A smart contract on Ethereum is, in essence, a set of functions and persistent state stored at a specific address on the blockchain. Like any Ethereum account, a contract can hold a balance and receive transactions, but its behavior is fully determined by its code rather than by a private key holder. When a user or another contract sends a transaction to a contract’s address, the EVM loads the contract’s bytecode and executes it, potentially reading and updating storage, emitting events, and transferring ETH or tokens.

The Ethereum Foundation’s documentation highlights several critical properties of these contracts. First, once deployed, a contract’s code is extremely difficult to change, especially if it was not designed with upgrade hooks, and it cannot generally be deleted. Second, transactions interacting with contracts are irreversible once included in a block, meaning that any bug or misconfiguration baked into a contract can have permanent consequences. Third, because smart contracts are just programs, they can encode arbitrary rules for how funds should move—replicating features of financial contracts, registry systems, or organizational bylaws—with the guarantee that these rules will be enforced exactly as written whenever the contract is invoked. This is both the power and the hazard of Ethereum: it automates enforcement but offers no safety net when logic is flawed.

Users typically interface with smart contracts through wallets such as MetaMask, Coinbase Wallet, or institutional custody systems. Historically, most users have relied on EOAs controlled by private keys. This model is simple but brittle: lose the key and the funds are gone; expose the key and an attacker can drain the account. It also limits what an account can do, since EOAs cannot include built‑in logic like social recovery, custom spending policies, or batched transactions. Account abstraction addresses these limitations by allowing accounts to be controlled by smart contract code rather than directly by a private key.

Ethereum’s roadmap for account abstraction has two major paths. The first, EIP‑4337, avoids modifying the core protocol by introducing a parallel transaction flow. Instead of sending traditional transactions, users sign UserOperation objects that are collected by specialized nodes called bundlers and then submitted to the chain via an EntryPoint contract. This design allows wallet developers to implement features like gas abstraction, session keys, and custom validation logic, since the EntryPoint contract calls into the smart account to verify signatures and gas payment rules. The Ethereum.org documentation notes that EIP‑4337 has already been widely adopted, catalyzing millions of smart contract accounts and hundreds of millions of UserOperations.

The second path, EIP‑7702, is slated to be part of the Pectra upgrade and will modify the native account model by allowing EOAs to temporarily act as smart contracts. In this design, a traditional address can be associated with contract code for the duration of a transaction, enabling programmable validation logic while preserving backward compatibility with existing applications. Combined, EIP‑4337 and EIP‑7702 represent an attempt to bake smarter accounts into both the protocol and an auxiliary transaction system, although this raises questions about fragmentation and complexity, as multiple parallel standards for transaction flows and wallet behavior emerge.

Layer‑2 networks are evolving in parallel. Base, Coinbase’s Ethereum L2, has announced a forthcoming Cobalt upgrade after its Beryl release that is expected to introduce native account abstraction at the rollup level. This would allow Base to support smart contract wallets more deeply in its protocol architecture, aligning the L2’s user experience with Ethereum’s L1 account abstraction roadmap. In this sense, both mainnet and L2s are converging on a world where “wallet” is itself a flexible smart contract with custom policies and hooks for institutions, DAOs, and complex applications.

Smart contracts also introduce new security paradigms. The same automation that ensures tamper‑resistant execution can be exploited through logical traps and adversarial contract interactions. A stark example is the recent hack of the well‑known MEV bot jaredfromsubway.eth on Ethereum, which reportedly lost more than $7.5 million in assets. According to security firm Blockaid, the attacker deployed controlled smart contracts designed to trick the bot’s automated execution system into approving malicious tokens, after which the attacker used those approvals to withdraw the bot’s funds. This incident illustrates the asymmetric risk faced by automated agents and protocols that interact with unvetted contracts in a permissionless environment: the very openness that enables composability also opens the door to sophisticated exploit techniques.

MEV (maximal extractable value) bots like JaredFromSubway operate by monitoring the mempool for profitable opportunities—such as arbitrage, liquidations, and sandwich trades—and then submitting carefully crafted transaction bundles to capture that value. While they provide liquidity and price alignment in some cases, their operations also raise concerns about fairness, user experience, and systemic complexity. The hack underscores that not only end‑users but also automated agents and professional actors can be exploited if they do not fully verify counterparties’ contract logic. It highlights why formal verification, auditing, permission lists, and better wallet UX are critical as Ethereum matures into a settlement layer hosting increasingly valuable assets.

Account abstraction may mitigate some user‑facing risks by enabling more sophisticated validation and policy logic at the wallet layer. For example, a smart wallet could be programmed to refuse approvals to contracts that do not meet certain audit or reputation thresholds, or to cap exposure to newly deployed tokens. Yet abstraction also increases surface area: multiple transaction flows (native and EIP‑4337), complex gas sponsorship arrangements, and cross‑chain operations all create more paths where bugs or misconfigurations can lead to loss. This tension—between flexibility and safety—is central to Ethereum’s evolution as programmable infrastructure.

Base pushes Beryl upgrade by one day as B20 registry requires additional setup, while new hard fork cuts Ethereum withdrawal delays from 7 days to 5

Block 47,806,542 is the ugly backdrop: Base just had an invalid-block stall that left some ecosystem nodes needing restarts, then had to coordinate a fork that adds native token precompiles and changes exit economics. B20 has hard activation plumbing, with the factory at 0xB20f000000000000000000000000000000000000 and the Activation Registry at 0x8453000000000000000000000000000000000001, so a sloppy registry flip would be a bad place to discover issuer or policy wiring is incomplete. The 7d to 5d withdrawal cut is useful for fast-bridge LP inventory turnover, but the higher bar is Base proving it can ship appchain-style primitives without every upgrade reminding users there is still one very visible operator in the loop.

Scaling Ethereum: Rollups, Proto‑Danksharding, and L2 Innovation

Ethereum’s ambitions as a global settlement layer collide with hard constraints on throughput and cost. The base chain can only process a limited number of transactions per second, and block space is scarce. During periods of high demand, gas prices rise sharply, making everyday use prohibitive for many users. To reconcile decentralization with scalability, Ethereum has adopted a rollup‑centric roadmap that moves most user activity off‑chain (or onto L2s) while using the L1 primarily for security and data availability.

Rollups batch many transactions and execute them off‑chain, then post compressed transaction data and proofs back to Ethereum. The dominant cost for rollups is not computation but data availability—publishing enough data to L1 so that the state of the rollup can be reconstructed if needed. Proto‑Danksharding, introduced via EIP‑4844, is a major step in reducing these costs. Instead of forcing rollups to use the same calldata mechanism as ordinary transactions, EIP‑4844 adds a new concept called data blobs that can be attached to blocks. These blobs are not accessible to the EVM and are automatically deleted after a fixed period, specified as 4096 epochs, corresponding to roughly 18 days. By making this data ephemeral and separate from execution, Ethereum can offer rollups cheaper bandwidth for posting their compressed transaction data.

This change was shipped to mainnet as part of the Cancun‑Deneb (“Dencun”) upgrade, which went live in March 2024. Dencun’s deployment marked a turning point, as it concretely lowered L2 fees and signaled that Ethereum’s scaling roadmap would progress through iterative data availability enhancements rather than massive on‑chain throughput increases alone. Users saw substantially cheaper transactions on leading rollups after Dencun, reinforcing the idea that the primary user experience for many will be at the L2 level, with Ethereum L1 faded into the background as a settlement and data layer.

Full Danksharding is the long‑term culmination of this roadmap. While Proto‑Danksharding introduces a limited number of blobs per block—six at the time of writing—full Danksharding is expected to expand this dramatically to 64 blobs per block. This expansion would yield a massive increase in data availability capacity, enabling Ethereum to support hundreds of rollups and potentially achieve an aggregate throughput of over 100,000 transactions per second across the ecosystem. The core idea is that Ethereum itself does not need to execute every transaction; it simply needs to ensure that the data underpinning rollup state transitions is available and that fraudulent behavior can be detected and penalized.

In parallel with the data availability roadmap, Ethereum continues to pursue execution‑layer improvements. The Glamsterdam hard fork, billed as the most significant network upgrade since The Merge, targets a substantial throughput increase and fee reduction on the base chain. According to technical analyses, the upgrade aims to push Ethereum’s throughput toward approximately 10,000 transactions per second while reducing gas fees by roughly 78%, with testnet validation ongoing ahead of mainnet activation. While the precise realized performance will depend on implementation and usage patterns, Glamsterdam represents a major effort to enhance L1 scalability and UX even as rollups remain central to the long‑term architecture.

Layer‑2 networks themselves are evolving quickly. Base, Coinbase’s Ethereum L2, illustrates how rollups can innovate on token standards and node software. The Beryl upgrade on Base, scheduled for mainnet activation on June 25, introduces a new B20 token standard designed specifically for the rollup environment. Unlike traditional ERC‑20 tokens, where all logic resides in smart contracts, B20 embeds token logic directly into the node software. This approach allows tokens to operate more efficiently, with faster execution and lower gas consumption, by leveraging native code paths. B20 is fully compatible with the existing ERC‑20 format, meaning that new tokens created using the B20 standard should be supported by current wallets and exchanges that understand ERC‑20.

The Beryl upgrade’s design goals are to reduce token creation costs, lower state storage overhead, and decrease L2 gas usage, thereby encouraging more token launches and usage on Base. The new standard is expected to benefit DeFi, gaming, and meme‑coin activity on the network by making tokens cheaper and more performant to deploy and interact with. Initially, developers will be offered two templates under B20: one tailored for stablecoins and one for generic assets. Over time, B20 is expected to support paying transaction fees directly in token units, allowing users to transact without holding ETH, and the standard is projected to help double the network’s throughput.

Beryl also introduces other infrastructure improvements. It reduces the withdrawal time from Base to Ethereum from seven days to five days by transitioning to a Multiproofs proof system, shortening the waiting period associated with rollup exits. On the node side, the upgrade integrates Reth V2, a new implementation that reduces disk space requirements and speeds up block processing, making it easier and cheaper for operators to run nodes. Earlier, Base announced the integration of zero‑knowledge proofs from Succinct Labs to enhance security and accelerate transaction finalization, further aligning the rollup’s trust model and UX with Ethereum’s broader ZK‑centric scaling trajectory.

Tying these strands together, Ethereum’s scaling strategy is less about a single “silver bullet” and more about a layered approach. The base chain focuses on security, consensus, and data availability, bolstered by upgrades like Proto‑Danksharding and Glamsterdam. Rollups handle execution and user interactions, experimenting with novel token standards like B20, integrating ZK proofs, and narrowing withdrawal windows. Over time, full Danksharding is expected to provide ample data capacity for a vast rollup ecosystem, while L1 execution improvements keep mainnet usable for high‑value transactions and system‑critical operations. This architecture reinforces Ethereum’s role as settlement infrastructure, with most end‑users interacting through L2s and applications built on top.

- 2023-09launch

Holesky testnet launches for enhanced smart contract testing

- 2024-02milestone

ERC-404 experimental token standard frenzy spikes ETH gas to 8-month high

- 2024-05regulatory

SEC approves spot Ethereum ETFs

- 2024-07launch

Spot ETH ETFs begin trading; BlackRock ETHA launches

- 2025-04governance

Vitalik proposes replacing EVM with RISC-V to simplify execution layer

Coinbase Base activates Beryl upgrade with new B20 token standard

Governance, the Ethereum Foundation, and Funding

Ethereum’s technical roadmap operates within a distinctive governance structure. Unlike corporate blockchain ventures, Ethereum is not controlled by a single company or foundation. Its evolution is the product of a loose coalition of core developers, client teams, researchers, application builders, and ETH holders who coordinate through open processes such as Ethereum Improvement Proposals (EIPs), AllCoreDevs calls, and social consensus. Within this ecosystem, the Ethereum Foundation (EF) plays a prominent but not exclusive role.

The EF is a non‑profit organization that funded much of Ethereum’s early research and development and continues to support client implementations, research teams, and grants to ecosystem projects. It employs researchers and engineers, holds a significant treasury, and often coordinates major upgrades. Vitalik Buterin, one of Ethereum’s co‑founders, has long been associated with the EF, although he does not unilaterally control the protocol. Instead, his influence is informal, rooted in technical leadership and community trust rather than direct economic or legal authority.

In recent years, the EF’s internal dynamics have become a topic of wider interest as personnel changes and funding debates have surfaced. Reports indicate that in 2026 alone, eight senior researchers and leaders announced their departure from the Ethereum Foundation, with five of those resignations occurring in May. Names cited include Carl Beek, Julian Ma, Barnabé Monnot, Tim Beiko, Trent Van Epps, Alex Stokes, and other long‑time contributors in research and operations roles. On its face, such concentrated turnover in a single year may suggest turbulence within the organization, especially given that several of these individuals held prominent public roles in protocol R&D and coordination.

However, closer analysis suggests that the EF remains a sizable and well‑resourced entity. Coverage notes that despite these high‑profile exits, the foundation still employs a large research and operations staff, controls a multi‑billion‑dollar treasury, and continues to fund grants across the Ethereum ecosystem. Rather than signaling institutional collapse, the turnover seems more aligned with a structural reorganization under a 2025 mandate that redefined priorities and roles. From this perspective, EF leadership changes are better understood as a governance story—reflecting evolving views on how to steward a maturing public good—than as an immediate threat to protocol continuity.

The more pressing concern, voiced by some former insiders, relates to funding for core development. Trent Van Epps, a former Ethereum Foundation contributor, has publicly warned that Ethereum’s core development ecosystem could face a “slow‑burning funding crisis” within a three‑ to nine‑month window. He cites EF spending reductions and the scheduled expiration of the Client Incentive Program, a mechanism used to support client teams, as potential stressors. Van Epps estimates that core development requires on the order of $30 million annually and argues that new funding mechanisms may be necessary to sustain the diversity and quality of client implementations and research efforts.

These warnings highlight a structural tension. Ethereum, as a multi‑hundred‑billion‑dollar public network, depends on robust, independent client teams and researchers to maintain and improve its protocol. Yet these teams often rely on a combination of foundation grants, philanthropic funding, and, increasingly, ecosystem‑level initiatives such as protocol‑funded pools or contributions from large stakeholders. If EF resources are reallocated or reduced, and if alternative funding streams are not sufficiently developed, there is a risk that critical infrastructure becomes under‑resourced relative to the value it secures.

At the same time, the decentralized nature of Ethereum’s governance means that no single institution’s retrenchment automatically imperils the protocol. Client teams can and do raise funds from venture investors, community grants, and other sources. Large ecosystem participants—liquid staking protocols, rollups, centralized exchanges—have incentives to support the underlying infrastructure on which their businesses rely. Governance experiments, such as protocol‑level funding mechanisms or client diversity incentives embedded in the consensus layer, are being explored in the broader community, though they raise their own design and capture concerns.

What is clear is that Ethereum’s governance story is becoming more complex and visible. Foundation leadership changes, warnings about funding crunches, and the growing influence of large corporate and institutional stakeholders (from exchanges to ETF issuers) mean that “who pays for and steers core development?” is no longer a niche concern. It is a central question for a network positioning itself as neutral global infrastructure. Maintaining a balance between distributed decision‑making, sustainable funding, and technical coherence will be one of Ethereum’s core governance challenges in the coming decade.

Ethereum, Bitcoin, Solana, and the Multichain Landscape

Ethereum does not exist in a vacuum. It cohabits an ecosystem with Bitcoin, Solana, and numerous other layer‑1 and layer‑2 networks that together form a heterogeneous, partially interoperable crypto landscape. Understanding Ethereum’s place within this environment requires comparing its design choices and narratives with those of its peers.

Bitcoin remains the benchmark asset in crypto, with the longest track record, the largest market capitalization, and a design laser‑focused on being hard money and censorship‑resistant value transfer. Its scripting language is deliberately constrained, limiting complex logic in favor of security and simplicity. Ethereum, by contrast, embraced Turing‑complete programmability, accepting increased complexity and attack surface in exchange for flexibility. Where Bitcoin orbits the narrative of “digital gold,” Ethereum has gravitated toward “programmable settlement layer” and “internet of value” metaphors.

Solana represents yet another design point, prioritizing high throughput and low latency via a tightly integrated, high‑performance architecture. Critics have often questioned its decentralization, pointing to higher hardware requirements and past outages. However, recent analyses argue that Solana’s decentralization metrics, such as stake distribution and validator control, are stronger than many critics acknowledge and in some respects compare favorably to Ethereum, even if Ethereum has far more validators by raw count. One widely cited comparison notes that Ethereum has roughly one million validators versus Solana’s roughly 740, which on a simple count basis makes Ethereum appear orders of magnitude more decentralized. Yet decentralization is multidimensional: concentrated stakes, correlated clients, and social governance structures all shape effective control.

To frame these differences, it can be helpful to summarize some key attributes:

| Network | Primary goal | Smart contracts | Consensus | Typical role in portfolios |

|---|---|---|---|---|

| Bitcoin | Hard money, censorship‑resistant value | Limited scripts | Proof‑of‑work | Store of value, macro hedge, base collateral |

| Ethereum | Programmable settlement & dApp platform | Full EVM | Proof‑of‑stake | Smart‑contract platform, DeFi/NFT/RWA backbone |

| Solana | High‑throughput, low‑latency applications | Full runtime | Proof‑of‑stake–based | Performance‑oriented DeFi, consumer apps |

This table is necessarily simplified, but it illustrates how Ethereum has staked out the middle ground: more programmable and general‑purpose than Bitcoin, but with a stronger emphasis on credible neutrality and composability than many newer chains that optimize for raw performance.

On the market structure side, Ethereum increasingly shares the institutional spotlight with Bitcoin and, to a lesser extent, Solana. Spot Bitcoin ETFs in major markets have become significant vehicles for exposure, channeling traditional capital into BTC without requiring direct custody. Ethereum is following a similar path. Morgan Stanley, for example, has filed for Ethereum and Solana ETFs with a management fee of approximately 0.14%, undercutting some incumbents like Grayscale and Franklin Templeton. In an amended S‑1 filing for a spot Ethereum ETF, Morgan Stanley proposed integrating staking directly into the trust, retaining around 95% of staking rewards inside the vehicle while charging the same 0.14% fee. Such products blur the line between passive exposure and active participation in protocol security, raising questions about how large institutional stakers will influence Ethereum’s validator set and governance.

Price dynamics also differ across networks but are often correlated during broader risk‑on or risk‑off cycles. Ethereum, for instance, has seen episodes of significant volatility, including a recent period in which it traded in the $1,650 to $1,700 support zone below its 100‑day simple moving average after declining more than 45% from prior highs. Technical analyses identified this range as a key support area, with $1,600 acting as a floor that had held through multiple tests. Similar drawdowns and recoveries have been observed in Bitcoin and other major assets, especially around macro events like central bank decisions, underscoring that Ethereum is embedded in a wider market regime where liquidity, rates, and risk sentiment matter as much as protocol fundamentals.

Cross‑chain assets further tie these ecosystems together. The SEKAU Swedish krona stablecoin launched simultaneously on Ethereum and Solana, among other networks, positioning itself as a bridge between different blockchain communities. Users can hold SEK exposure on whichever chain best suits their needs, while the issuer manages reserves and minting/redemption processes across chains. Many other stablecoins, restaking tokens, and DeFi assets now exist in multi‑chain forms or are bridged across L1s and L2s, creating a mesh of dependencies where issues on one chain can propagate to others via liquidity pools and derivatives.

For Ethereum, this multichain context is both a competitive pressure and a validation. Competing smart‑contract platforms force Ethereum to innovate on UX, scalability, and governance. At the same time, Ethereum’s standards (ERC‑20, ERC‑721, EIP‑1559), tooling (EVM, Solidity), and liquidity depth have become de facto norms that other chains emulate or interface with. Even when applications migrate or expand to alternatives like Solana, they often retain Ethereum compatibility or maintain bridges back to Ethereum‑secured rollups. In this sense, Ethereum’s success is increasingly measured not only by on‑chain metrics but by how indispensable it remains as part of the broader crypto stack.

Book of Eth defends Ethereum Foundation's five-year record, citing The Merge, Dencun, public goods funding and scaling upgrades amid growing criticism

$0.0015 median L2 fees by March 2026 is an insane scaling win, and also the source of the current ETH-holder anger: Dencun made Ethereum usable while compressing the burn that made the asset story easy. EF’s five-year record looks much better if the KPI is protocol durability and public-goods throughput; it looks messier if the KPI is value capture from Base, Arbitrum, OP and the rest of the rollup stack. The next credibility test is whether blob demand and sequencing economics route enough surplus back to ETH before users decide “Ethereum won” just means everyone else got cheaper blockspace.

Sophisticated MEV actors continue exploiting less experienced participants despite protocol-level democratization efforts, with the 'dark forest' dynamic persisting across successive upgrade cycles.

Coinbase's Base sequencer routes fees directly to Coinbase exchange rather than the Base ecosystem, illustrating how L2 economic capture concentrates revenue among a small set of dominant operators.

- RegulatoryLow

Spot ETH ETF approvals and filings from BlackRock, ARK, and institutional holders signal a regulatory environment that has materially de-risked Ethereum as a mainstream asset class.

- Competitive marketHigh

Solana overtook Ethereum on DEX volume during the memecoin cycle, Bitcoin surpassed ETH in monthly NFT sales, and Monad raised $225M explicitly to rival Ethereum's L1 position.

- Liquidity / stablecoin systemicMedium

Ethereum's $1.46 trillion stablecoin volume record creates deep liquidity but concentrates systemic risk in DAI and USDe collateral structures, with Ethena explicitly downplaying leverage-backed USDe exposure.

Core developers published a report on a network finality issue and are evaluating EVM replacement with RISC-V, indicating active protocol risk management rather than deferred technical debt.

ETH as an Asset: Staking, Fees, and Market Narratives

ETH occupies a unique position as both the fuel that powers Ethereum and a macro asset traded on global markets. Every transaction, contract deployment, and storage operation requires gas, which is paid in ETH. This gives ETH intrinsic utility: anyone who wishes to use Ethereum must either hold ETH or rely on someone who does to sponsor their transaction fees. EIP‑1559 added a base fee mechanism that is burned rather than paid to validators, tying ETH’s supply dynamics to network usage and shaping narratives about ETH as “ultrasound money” when burn outpaces issuance.

Staking has transformed ETH into a yield‑bearing asset. Under proof‑of‑stake, validators deposit ETH into the protocol to participate in block production and consensus. In return, they earn rewards funded by new ETH issuance and transaction fees. This has spawned a rich ecosystem of staking services, from solo stakers running hardware at home to custodial offerings and liquid staking tokens that represent claims on staked ETH. Restaking protocols go further, allowing staked ETH or its derivatives to be pledged to secure additional networks or services, layering new yield streams and risks atop the base protocol.

From a market perspective, ETH trades as a high‑beta, growth‑linked asset whose value reflects expectations about Ethereum’s future role in global infrastructure. Technical and on‑chain indicators inform these expectations. Recent analyses highlighted a period where ETH defended a key support zone between $1,650 and $1,700, even as it traded below a 100‑day simple moving average anchored around $2,108 after a drawdown of more than 45% from earlier highs. This zone was seen as a pivotal level for bulls and bears, with $1,600 acting as a de facto floor that had held several tests. While such levels are transient, they illustrate how traders interpret Ethereum’s price action in light of macro conditions, protocol upgrades (such as Glamsterdam), and ETF developments.

ETFs, in particular, are reshaping ETH’s investor base. Morgan Stanley’s proposed spot Ethereum ETF with integrated staking is notable, as it effectively institutionalizes the staking yield within a regulated product, albeit capturing most of that yield for the fund rather than passing it through fully to holders. When combined with low‑fee ETF offerings for both Ethereum and Solana, this signals that large asset managers view staking rewards as a component of total return for investors, while also positioning themselves as significant intermediaries in protocol‑level participation. At the same time, spot Bitcoin ETFs have already demonstrated how such vehicles can influence flows, with days of net inflows or outflows coinciding with notable price moves, a pattern likely to repeat for ETH once ETF markets fully mature.

Within DeFi, ETH is ubiquitous as collateral, liquidity, and unit of account. Lending protocols allow users to borrow stablecoins or other assets against ETH, often using liquid staking tokens as collateral, thereby linking traditional DeFi leverage cycles to Ethereum’s security model. Derivatives platforms list perpetual futures and options on ETH, providing hedging instruments and amplifying speculative flows. ETH also remains the base asset for many liquidity pools on decentralized exchanges, where it is paired with stablecoins and long‑tail tokens, making it central to on‑chain price discovery.

The search for yield on ETH also motivates risk‑taking behaviors that can backfire. The JaredFromSubway MEV bot’s $7.5 million loss is a case in point: in pursuit of MEV returns, the bot’s automation interacted with adversarial contracts that exploited its approval logic. Such episodes remind market participants that yield in crypto is seldom risk‑free; it is often compensation for smart contract, counterparty, or strategy risk. As Ethereum evolves into more institutional and retail portfolios via staking products and ETFs, articulating these underlying risks—and how they interplay with the ETH asset—is critical for informed participation.

Risks, Security Threats, and Open Questions

For all its promise, Ethereum faces a range of risks that could shape its trajectory as a settlement layer and asset. Some are technical, others economic or governance‑related, and many are intertwined with broader developments in cryptography and regulation.

Smart contract risk is foundational. Code running on Ethereum is immutable in practice, and mistakes can have irreversible consequences. The MEV bot hack involving jaredfromsubway.eth demonstrates how attackers can use controlled smart contracts to trick automated systems into granting token approvals that are then exploited to drain funds. In that case, according to Blockaid’s analysis, the attacker deployed contracts specifically designed to deceive the bot’s execution logic, causing it to interact with malicious tokens and inadvertently grant them permissions. This kind of exploit does not rely on low‑level protocol flaws but on higher‑level assumptions about how other actors will behave in a permissionless environment. It underscores that composability—any contract can call any other—also means that contracts must treat counterparties as potentially adversarial by default.

Cross‑chain bridges and multi‑network deployments add additional risk surfaces. Many assets today exist simultaneously on dozens of chains via wrapped representations. When providers sunset bridging functionality, as has happened with some restaked ETH derivatives, users can be left navigating manual burn‑and‑redeem processes with on‑chain fee payments and off‑chain coordination. Errors in these workflows, or bugs in bridge contracts, can lead to stuck or lost funds. While such events are not intrinsic failures of Ethereum itself, they highlight the complexity of the ecosystem that now surrounds the base chain and the importance of clear standards, audits, and sunset procedures for bridging services.

Governance and funding risks also loom. The potential “slow‑burning funding crisis” flagged by Trent Van Epps illustrates a scenario where the value secured by Ethereum grows faster than the resources allocated to its core development. In such a world, client diversity could degrade, new protocol features could be delayed, and critical security work might suffer from understaffing. At the same time, over‑reliance on a few large funders—whether the EF, major DeFi protocols, or corporate stakeholders—could shift influence away from smaller contributors and tilt the governance balance. The recent exodus of several EF researchers, while not an immediate existential threat, serves as a reminder that institutions and individuals are not permanent; Ethereum’s resilience depends on continually renewing its contributor base and funding models.

Competition from alternative chains is a different kind of risk. Solana, for example, has been presented in some analyses as more decentralized than critics claim when considering metrics like stake distribution, native staking participation, and validator control, even though Ethereum has roughly one million validators to Solana’s hundreds. If alternative platforms can offer high throughput, good developer tooling, improving decentralization metrics, and compelling economic incentives, they can siphon away applications and liquidity that might otherwise have settled on Ethereum. This is especially true for consumer‑facing apps and high‑frequency trading venues for which latency and fees are paramount.

Regulatory uncertainty is another major variable. Stablecoin issuers, tokenization platforms, and DeFi protocols built on Ethereum must navigate evolving rules around securities, money transmission, and consumer protection. Bank‑led tokenization experiments, like the Custodia‑Vantage tokenized deposit platform, reflect a trend toward regulated entities using blockchain rails for settlement, but they also raise questions about how much of Ethereum’s future activity will be fully permissionless versus gated by KYC and compliance layers. ETF developments add a further layer of regulatory oversight, as issuers must work with securities regulators to structure products that may involve staking, lending, or other forms of on‑chain participation.

Quantum computing represents a more distant but conceptually important threat. Cryptocurrencies rely on asymmetric cryptography—public/private key pairs—for security, transaction signing, and ownership proofs. A recent whitepaper from BlackRock examined the implications of quantum computing for blockchains, emphasizing that cryptocurrencies depend critically on cryptographic primitives that could, in theory, be weakened by sufficiently powerful quantum computers. The paper discusses how algorithms like Shor’s could break widely used public‑key schemes, potentially undermining security for systems like Bitcoin and Ethereum if they do not transition to quantum‑resistant methods in time. While practical, large‑scale quantum attacks remain speculative, the fact that major asset managers are modeling these scenarios signals that quantum risk is no longer a purely academic topic.

Ethereum’s roadmap itself contains open questions. Account abstraction is proceeding along multiple tracks—native changes via EIP‑7702, parallel transaction flows via EIP‑4337, and L2‑native implementations like Base’s planned Cobalt upgrade. This diversity fosters experimentation but risks fragmentation if standards diverge or if user experience differs significantly across layers. Scaling via rollups and Danksharding promises immense capacity, but it also creates dependencies on off‑chain sequencing infrastructure and complex fraud or validity proofs. If rollups become highly concentrated or subject to regulatory capture, Ethereum’s neutrality as a settlement layer could be challenged, even if the base protocol remains permissionless.

MEV and transaction ordering pose further long‑term challenges. As more value flows through Ethereum, the incentives to engage in complex order‑flow strategies, including sandwiching, back‑running, and priority gas auctions, will likely grow. MEVbots like JaredFromSubway demonstrate how profitable and sophisticated such strategies can become, as well as how vulnerable they are to manipulation when adversaries understand their behavior. Designing mempool rules, proposer‑builder separation mechanisms, and MEV‑aware wallets that improve fairness without sacrificing efficiency or decentralization is an active area of research.

In sum, Ethereum’s risk profile is less about a single catastrophic failure and more about a constellation of technical, economic, and governance tensions that must be managed over time. The network’s resilience will depend on how well it adapts to these pressures while preserving the properties that make it valuable: credible neutrality, composability, and open access.

Conclusion

Ethereum has evolved from a bold idea about a “world computer” into a sprawling, multi‑layered ecosystem that anchors much of today’s crypto and on‑chain finance. Its core innovation—bringing general‑purpose programmability to a decentralized ledger—has enabled smart contracts, tokens, DAOs, and a host of applications that use code to enforce rules rather than intermediaries. The EVM, the account model, and proof‑of‑stake consensus together define a platform where developers can deploy autonomous software that interacts with a global pool of liquidity and users.

Over the past decade, Ethereum’s role has shifted from serving as a venue for ICOs and early DeFi experiments to functioning as a settlement and coordination layer for increasingly institutional and multi‑chain activity. Stablecoins like SEKAU, tokenized deposit platforms, and DeFi protocols such as Uniswap treat Ethereum as infrastructure on which to build higher‑level services. Account abstraction efforts through EIP‑4337 and upcoming EIP‑7702 seek to make this infrastructure more accessible and secure for everyday users and organizations, while rollup‑centric scaling via Proto‑Danksharding and layer‑2 networks like Base aim to expand capacity without sacrificing decentralization.

At the same time, Ethereum’s maturation brings new challenges. Governance and funding questions are moving from the background to the foreground as the Ethereum Foundation reorganizes and former insiders warn of potential funding gaps for core development. Competition from chains like Bitcoin and Solana, along with the growing influence of ETFs and institutional staking, complicate the network’s economic and political landscape. Security incidents such as the JaredFromSubway MEV bot hack highlight the risks of composability in a permissionless environment. And long‑term threats like quantum computing underscore that Ethereum’s cryptographic foundations cannot be taken for granted.

Yet these challenges also reflect Ethereum’s success. As more value and attention concentrate on the network, the stakes of its technical choices and governance decisions rise. The path forward will require careful balancing: between experimentation and standardization in account abstraction; between L1 minimalism and the desire for richer base‑layer features; between open participation and the influence of large institutional actors. For investors, builders, and policymakers, understanding Ethereum now means understanding not just a single chain, but a layered system of protocols, organizations, and markets that together constitute one of the most ambitious public digital infrastructure projects of the 21st century.

Outlook

Looking ahead, Ethereum’s trajectory seems poised to deepen its role as shared settlement and coordination infrastructure rather than as a retail payments network. The continued rollout of Proto‑Danksharding, the eventual arrival of full Danksharding, and execution‑layer upgrades like Glamsterdam should expand capacity and lower costs for rollups and users, reinforcing the L2‑centric architecture. On those L2s, innovations such as Base’s B20 token standard and ZK‑proof integrations hint at a future where most user activity is fast, cheap, and abstracted away from the complexities of the base chain.

At the same time, account abstraction is likely to redefine the user experience. As smart contract wallets become the default, features like social recovery, spending limits, and gas abstraction could make Ethereum applications feel more like traditional fintech apps while preserving self‑custody for those who want it. Institutional adoption through tokenization platforms, bank experiments, and ETFs will probably continue, bringing more capital and scrutiny to the network. How Ethereum’s community navigates the resulting governance pressures—ensuring that core development remains sufficiently funded and independent—will be critical for maintaining credible neutrality.

Ultimately, Ethereum’s long‑term success will be measured less by day‑to‑day price movements and more by whether it can sustain a vibrant, composable, and secure ecosystem of applications that treat it as indispensable infrastructure. If the analogy to the early internet and open‑source software holds, the story of Ethereum is still in its early chapters. The network’s evolution over the next decade—through technical upgrades, new applications, and shifting market structures—will determine whether it fulfills its ambition to serve as the world’s programmable settlement layer alongside, rather than instead of, systems like Bitcoin and emerging high‑performance chains.

Latest Ethereum news

Ethereum's rollup-centric roadmap failed to hide blockchain complexity, forcing users through bridges and fragmented chains while ETH captured little valueBase pushes Beryl upgrade by one day as B20 registry requires additional setup, while new hard fork cuts Ethereum withdrawal delays from 7 days to 5Book of Eth defends Ethereum Foundation's five-year record, citing The Merge, Dencun, public goods funding and scaling upgrades amid growing criticism Uniswap lets teams launch CCA token auctions from web app on Ethereum, Base, Arbitrum, and Unichain

Uniswap lets teams launch CCA token auctions from web app on Ethereum, Base, Arbitrum, and Unichain Standard Chartered sees Aave outperforming Bitcoin and Ethereum through 2030, citing V4 upgrades, GHO growth, token buybacks and a 37x expansion in DeFi assets

Standard Chartered sees Aave outperforming Bitcoin and Ethereum through 2030, citing V4 upgrades, GHO growth, token buybacks and a 37x expansion in DeFi assets Propeller introduces Turbine, a new RFQ venue for large trades on Ethereum

Propeller introduces Turbine, a new RFQ venue for large trades on EthereumSources

- https://ethereum.org/developers/docs/smart-contracts/

- https://ethereum.org/roadmap/danksharding/

- https://www.youtube.com/watch?v=JJ-8BZ8SLFY

- https://forklog.com/en/mev-bot-jaredfromsubway-eth-loses-over-7-5-million-in-hack/

- https://x.com/BSCNews/status/2067813370322129268

- https://phemex.com/blogs/ethereum-foundation-researchers-quitting-2026

- https://x.com/crowdfundinside/status/2068381429248200739

- https://x.com/blckchaindaily/status/2068028728534331631

- https://khabarpu.com/b.htm?u=AllUnity-debuts-SEKAU%2C-a-fully-reserved-Swedish-krona-stablecoin_Y29pbnRlbGVncmFwaC5jb20vbmV3cy9hbGx1bml0eS1kZWJ1dC1mdWxseS1yZXNlcnZlZC1zd2VkaXNoLWtyb25hLXN0YWJsZWNvaW4tc2VrYXU%2FdXRtX3NvdXJjZT1yc3MmYW1wO3V0bV9tZWRpdW09cnNzJmFtcDt1dG1fY2FtcGFpZ249cnNz_Q29pbnRlbGVncmFwaA%3D%3D

- https://intellectia.ai/news/crypto/allunity-launches-first-swedish-kronabacked-stablecoin-sekau

- https://allunity.com/news/allunity-launches-the-first-fully-reserved-swedish-krona-backed-stablecoin-sekau

- https://www.prnewswire.com/news-releases/vantage-bank-and-custodia-announce-launch-of-tokenized-deposits-for-us-banks-302592931.html

- https://x.com/Uniswap/status/2067614470118003078

- https://x.com/leviathan_news/status/2068129543995658486/photo/1

- https://www.blackrock.com/us/individual/literature/whitepaper/quantum-whitepaper.pdf

- https://ethereum.org/roadmap/account-abstraction/

- https://financefeeds.com/ethereums-1695-defense-faces-a-high-stakes-moment/

- https://cryptorank.io/news/feed/3c342-coinbase-s-base-targets-june-25-for-beryl-upgrade-and-new-b20-token-standard

- https://forklog.com/en/base-to-activate-beryl-upgrade-on-june-25/

Community notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…