ETH is Ethereum's native token, serving as gas, staking collateral, and DeFi base asset. This explainer covers supply mechanics, staking yield, ETF developments, whale activity, and long-term outlook.

+69 sources across the wider coverage universe

Tom Lee’s Bitmine uplists to NYSE, revealing 4.8M ETH holdings and expanding share buyback program to $4B in a major crypto-linked corporate treasury move2026-04

Tom Lee’s Bitmine uplists to NYSE, revealing 4.8M ETH holdings and expanding share buyback program to $4B in a major crypto-linked corporate treasury move2026-04 Ether.fi commits $3B in ETH to ETHGas in exclusive three-year preconfirmation deal2026-04

Ether.fi commits $3B in ETH to ETHGas in exclusive three-year preconfirmation deal2026-04 SharpLink resumes ETH buys with $7.85M purchase as ether sinks to 2026 low ahead of Russell inclusion2026-06

SharpLink resumes ETH buys with $7.85M purchase as ether sinks to 2026 low ahead of Russell inclusion2026-06 Charles Schwab launches direct BTC/ETH trading via new Schwab Crypto arm to rival Robinhood at 0.75% fee.2026-04

Charles Schwab launches direct BTC/ETH trading via new Schwab Crypto arm to rival Robinhood at 0.75% fee.2026-04 Ethereum Foundation's ETH Rangers identifies ~100 DPRK IT workers across 53 projects, recovers $5.8M in closing report2026-04

Ethereum Foundation's ETH Rangers identifies ~100 DPRK IT workers across 53 projects, recovers $5.8M in closing report2026-04 KyberSwap exploiter sends another 2,000 ETH to Tornado Cash as laundering total hits $40M2026-06

KyberSwap exploiter sends another 2,000 ETH to Tornado Cash as laundering total hits $40M2026-06

Ethereum's native token, ETH, functions simultaneously as the fuel for one of the world's largest programmable blockchains, a yield-bearing staking asset, and an increasingly contested store of value.

What ETH Actually Is

ETH is the native currency of the Ethereum network, the second-largest blockchain by market capitalization after Bitcoin. Unlike BTC, which was designed primarily as peer-to-peer digital cash, ETH was architected from the outset as a utility token — the mandatory fee medium ("gas") for every computation, smart contract execution, and asset transfer on the network.

That original design has compounded into something more complex. ETH is now simultaneously:

- Gas: the unit of account for transaction fees on Ethereum mainnet and its Layer 2 rollup ecosystem

- Staking collateral: validators must lock 32 ETH per validator node to participate in consensus and earn protocol rewards

- Collateral in DeFi: the most widely accepted asset in lending markets, stablecoin systems, and derivatives protocols

- A monetary asset: subject to supply mechanics that make it, under most network conditions, deflationary

Understanding ETH requires holding all four of these functions at once. Analysts who reduce it to "just a tech coin" miss the staking yield story; those who focus only on yield miss the macro sensitivity that ties it to Federal Reserve rate expectations and risk appetite broadly.

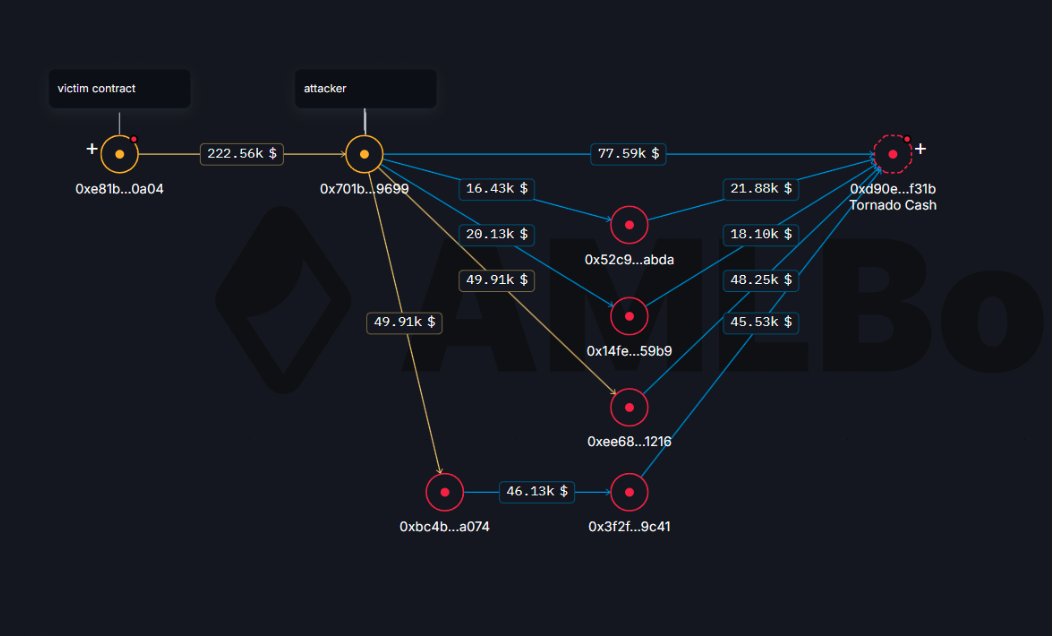

DLMC exploiter routes 37 ETH through Tornado Cash after $222.5K BNB Chain oracle attack

AMLBot says the DLMC attacker exploited the protocol on BNB Chain for about $222.5K via price/oracle manipulation, then swapped and bridged the proceeds to Ethereum through Li.Fi and Mayan Swift. The funds were split into 37 ETH of Tornado Cash deposits across 10 ETH and 1 ETH notes, making the trail harder to follow. It is a smaller exploit by dollar size, but the laundering path is the story: BNB Chain drain, bridge hop, Ethereum mixer.

ETH readers are tracking an identity war in real time — the same asset is simultaneously being positioned as institutional reserve collateral (ETFs, Maker positions), yield infrastructure (restaking vaults, LSD), and speculative leverage vehicle, and readers click hardest when those roles visibly collide or contradict each other.

The Supply Mechanic: EIP-1559 and the Merge

Before September 2022, Ethereum ran on proof-of-work, issuing roughly 13,000 ETH per day to miners. The Merge replaced that with proof-of-stake, cutting new issuance by approximately 90%. Combined with EIP-1559 — introduced in August 2021 — which burns a base fee on every transaction, the net supply of ETH has been close to flat or deflationary in high-activity environments.

The burn rate tracks directly with network usage. During periods of heavy DeFi activity, NFT minting, or mempool congestion from arbitrage bots, more ETH is destroyed than issued. When the network is quiet, issuance outpaces burns and supply grows marginally. This dynamic makes ETH's monetary policy endogenous to demand in a way Bitcoin's fixed-schedule halvings are not.

This matters for long-term holders. The total circulating supply of ETH has oscillated near 120 million tokens since the Merge, compared to Bitcoin's hard cap of 21 million. The argument that ETH is "ultrasound money" rests on the burn mechanism sustaining net deflation during bull-market conditions — a claim that requires active network demand to hold.

Staking: Yield, Liquidity, and Risk

Any holder of 32 ETH can run a validator directly; those with less can participate through liquid staking protocols like Lido (which issues stETH) or institutional vaults such as those brought by Luganodes to Lido V3. Staked ETH currently yields approximately 3–4% annually in ETH-denominated terms, paid by the protocol from new issuance and priority fees.

Liquid staking tokens like stETH and wstETH have become foundational DeFi primitives. SparkLend, for instance, holds more wstETH as collateral than any other venue in decentralized finance. Platforms like Coinbase allow users to borrow up to $1 million in USDC against staked ETH without unstaking — a product that illustrates how yield-bearing ETH collateral is increasingly replacing idle, unproductive BTC as DeFi's preferred base layer asset.

There is a risk dimension to understand here. Liquid staking tokens appear to diversify across validators, but in a systemic stress scenario — a major slashing event, an Ethereum protocol bug, or a simultaneous validator exit rush — they share the same underlying ETH exit path. SparkLend has explicitly acknowledged this: it does not treat LSTs as a diversified basket in its risk models. Holders of wstETH-denominated positions should be aware that correlation to ETH price and ETH protocol risk is near-total.

Restaking, pioneered by EigenLayer, extends ETH's security to external protocols by allowing validators to re-pledge already-staked ETH. This amplifies yield potential but also stacks slashing risk. The ecosystem is still early and the long-run risk profiles are not fully established.

Ethereum's rollup-centric roadmap failed to hide blockchain complexity, forcing users through bridges and fragmented chains while ETH captured little value

$0.0015 median L2 fees are great product work and terrible monetary-premium fuel. Dencun turned Ethereum DA into a cheap wholesale input; Base, Arbitrum and OP can monetize sequencer ordering, app distribution and MEV while L1 burn sits near 74 ETH/day. Chain abstraction may hide the bridge click, but it does not remove the inventory tax: USDC, WETH, perps collateral and LP depth still get split across domains until shared sequencing or synchronous composability makes liquidity feel single-chain again.

- 01ETH ETF institutional flows

Readers followed the entire arc from SEC delay suspense through BlackRock ETHA crossing $1B, treating ETF inflow data as a real-time sentiment gauge for institutional conviction.

- 02DeFi liquidation cascade risk

A live Maker mega-position facing liquidation, combined with $300M wiped in 24 hours, turned abstract protocol risk into a spectator sport with real stakes.

- 03Restaking and LSD landscape

The proliferation of LRT vaults and liquid staking options created a mapping problem readers wanted solved — who offers what yield and at what structural risk.

- 04ETH monetary identity debate

Headlines arguing ETH was never meant to be money and that Ethena structurally suppresses ETH price exposed a foundational narrative tension that provoked strong reader curiosity.

- 05ETH strategic reserve accumulation

On-chain tracking of entities treating ETH as a treasury reserve asset reframed ETH as a macro instrument rather than just a gas token, attracting readers interested in the BTC/ETH reserve race.

- 06Custody exploit accountability

High-ETH exploits at Stake.com and the Bybit wallet incident drew clicks not for the technical mechanics but for the real-time crisis response and who bore the loss.

ETH as Institutional and Macro Asset

The 2024 approval of spot Bitcoin ETFs in the United States changed the landscape for ETH as well. Spot Ethereum ETFs launched in the US in mid-2024, providing regulated exposure to ETH for institutional and retail investors who cannot or will not hold the asset directly. Morgan Stanley has filed amendments for both ETH and SOL ETFs, with fee disclosures described as among the lowest in the market — a sign that institutional competition for ETH exposure products is intensifying.

This matters because institutional flows behave differently from on-chain accumulation. When the Federal Reserve has indicated hawkish monetary policy — projecting fewer rate cuts or higher-for-longer rates — risk assets including BTC, ETH, SOL, and XRP have sold off together. ETH is not immune to macro; its beta to risk sentiment is substantial.

Analyst price targets vary widely. Standard Chartered's Geoffrey Kendrick has maintained a $4,000 year-end ETH target, citing structural demand from staking and ETFs. Against that, some technical analysts have pointed to bearish signals in ETH futures positioning and flagged the possibility of a selling wave if ETH fails to convincingly break above key resistance levels. Options data from mid-June 2026 showed 138,000 ETH contracts expiring with a put-call ratio of 1.03 and a maximum pain point of $1,725 — a modestly bearish skew.

Whale Activity and On-Chain Signals

On-chain data offers a real-time window into large-holder sentiment that equity markets cannot replicate. Recent months have seen notable divergence: some institutional-scale wallets are accumulating aggressively, while others are borrowing ETH from Aave to sell short.

K3 Capital withdrew approximately 10,000 ETH ($16.92M) from Binance in a short window — exchange outflows typically signal accumulation intent, since self-custody is less convenient for immediate selling. Separately, addresses linked to Chun Wang, co-founder of F2Pool, withdrew 7,650 ETH and 124 WBTC from Binance in a similar timeframe, building exposure across both major assets. On the other side, a separate whale borrowed 44,389 ETH from Aave — a protocol that requires overcollateralization — apparently to sell, representing a structurally bearish position that requires ETH to fall for the trade to profit.

Binance's 43rd Proof of Reserves report (June 2026 snapshot) showed user ETH holdings rising alongside BTC holdings, suggesting that the exchange's customer base has been net buyers over the preceding months despite price pressure.

This divergence between accumulating whales and short-sellers borrowing to sell is not unusual at inflection points. On-chain data cannot tell you who is right, but it can tell you that both conviction and contra-bets are being made at scale.

SharpLink resumes ETH buys with $7.85M purchase as ether sinks to 2026 low ahead of Russell inclusion

SharpLink bought 5,000 ETH from FalconX, worth $7.85M, its first ETH purchase since Oct. 26 as ether hit a 2026 low at $1,537. The company now holds 876,285 ETH and equivalents, while Bitmine still dwarfs it with 5.67M ETH after adding another 52,203 ETH last week. The buy lands just before SharpLink’s expected Russell 2000 and Russell 3000 inclusion, which could put passive-flow pressure behind a bruised ETH treasury trade.

- 2023-09exploit

Stake.com exploited for 6,000 ETH

- 2023-07governance

Celsius court approval to convert altcoins to BTC and ETH

- 2024-05regulatory

SEC signals surprise openness to spot ETH ETF approval

- 2024-07milestone

Spot Ethereum ETFs launch in the United States

- 2024-11milestone

BlackRock ETHA surpasses $1B in net inflows

- 2025-02exploit

Bybit ETH wallet incident — CEO Ben Zhou livestream response

- 2025-03milestone

Vitalik deposits 1,900 ETH into Aave amid DeFi pressure

ETH's Role in the Broader Ecosystem

Ethereum's stated long-run vision has evolved beyond payments. Supporters increasingly frame ETH as securing a shared settlement layer for identity systems, AI agent coordination, tokenized real-world assets, and multi-party agreements. On this view, payments are simply the first application that bootstrapped adoption; the endgame is something more like a global state machine underpinning institutional and automated activity.

Critics note that this vision depends on Ethereum retaining its dominance against competitors — Solana, Avalanche, and various Layer 2 networks — all of whom compete for developers and users. Ethereum's own Layer 2 ecosystem (Arbitrum, Optimism, Base, and others) processes more transactions than mainnet, which compresses mainnet fee burns and can blunt ETH's deflationary mechanics.

There are also institutional concerns about protocol sustainability. A former Ethereum insider has warned publicly of a potential funding crunch for core protocol development, noting that the mechanisms by which Ethereum funds foundational research and client diversity are under pressure. This is structurally different from Bitcoin, where the protocol is intentionally static; Ethereum's roadmap is ongoing and requires continued developer resources.

Security incidents also remind the market of smart contract risk. The June 2024 anniversary of the DAO hack — in which 3.6 million ETH was drained via a reentrancy exploit in 2016, triggering the hard fork that split Ethereum Classic from Ethereum — serves as a historical benchmark. More recently, the MEV bot jaredfromsubway.eth was itself exploited for $7.7M, with the attacker converting proceeds to ETH. Sophisticated actors operate across the network at multiple levels; the ecosystem's security posture is only as strong as the weakest deployed contract.

Vitalik Buterin has continued proposing novel financial primitives built on ETH. A recent option-based stablecoin proposal would leverage ETH upside buyers to back stable value without debt positions, liquidations, or funding rates — reigniting debate about whether DeFi can produce robust stablecoins without relying on USDC or overcollateralized models like DAI.

USDC, Stablecoins, and ETH's Relationship

USDC, the dollar-pegged stablecoin issued by Circle, is the dominant stable medium on Ethereum. It settles on Ethereum mainnet and on most major Layer 2 networks denominated in ETH-gas. This creates a structural codependency: USDC demand drives Ethereum transactions, which burns ETH and increases staker rewards. Conversely, if USDC migrated primarily to a competing chain, it would meaningfully reduce Ethereum's fee revenue.

The relationship also runs through lending: USDC is borrowed against ETH collateral constantly at scale, across Aave, Compound, SparkLend, and others. This creates a synthetic ETH leverage position across the entire DeFi ecosystem — when ETH prices fall sharply, collateral ratios compress and liquidations can amplify selling.

- Smart Contract / ProtocolHigh

Cascading liquidations ($300M in 24h) and a single Maker mega-position threatening systemic impact demonstrate that DeFi leverage on ETH collateral can destabilize multiple protocols simultaneously.

- LiquidityHigh

Overlapping LRT vaults, restaking recursion, and large concentrated positions mean exit liquidity can evaporate rapidly during volatility, as seen in the f(x) protocol rebalancing stress event.

- RegulatoryMedium

Spot ETH ETF approval unlocked institutional capital but SEC continued delaying multi-asset index ETFs including ETH, leaving the regulatory perimeter around ETH's securities classification unresolved.

- CentralizationMedium

Restaking concentration through a small set of LRT vault operators and institutional custodians (Grayscale, BlackRock) creates correlated failure points across a nominally decentralized staking layer.

- Market / Price SuppressionMedium

Structural arguments that Ethena's synthetic dollar model mechanically suppresses ETH spot price suggest that ETH's largest DeFi yield primitive may be working against ETH price appreciation.

- Custody / ExploitMedium

High-value ETH wallet exploits at centralized venues (Bybit, Stake.com) show that ETH's deep liquidity makes it the primary target asset in large-scale custodial breaches.

Outlook

ETH occupies a structurally unique position in the digital asset landscape: it is simultaneously a commodity (gas), a bond-like instrument (staking yield), collateral, and an equity-adjacent bet on Ethereum's adoption curve. None of those analogies is exact, which is why it resists clean categorization and attracts both fundamental bulls and tactical shorts.

Near-term, ETH faces resistance from macro headwinds, positioning skepticism in derivatives markets, and genuine questions about whether its price can close the gap with its own ecosystem's growth metrics. Longer term, the ETF approval pathway, institutional staking products, and the buildout of Ethereum's rollup-centric scaling plan represent potential demand drivers that are structural rather than speculative.

The most important single variable is network usage — because ETH's supply mechanics mean that without fee burns, the deflationary thesis weakens. What happens to that usage as AI-native applications, tokenized securities, and prediction markets come online on Ethereum infrastructure will determine whether the "global settlement layer" thesis is narrative or reality.

Latest ETH news

DLMC exploiter routes 37 ETH through Tornado Cash after $222.5K BNB Chain oracle attackEthereum's rollup-centric roadmap failed to hide blockchain complexity, forcing users through bridges and fragmented chains while ETH captured little valueSharpLink resumes ETH buys with $7.85M purchase as ether sinks to 2026 low ahead of Russell inclusionKyberSwap exploiter sends another 2,000 ETH to Tornado Cash as laundering total hits $40M Raoul Pal says Ethereum is crypto's equivalent of Microsoft's operating system, arguing ETH remains the financial sector's preferred settlement and application layer

Raoul Pal says Ethereum is crypto's equivalent of Microsoft's operating system, arguing ETH remains the financial sector's preferred settlement and application layer Ethereum's value lies in credible neutrality, not speed, as Logarithmic Rex argues ETH remains crypto's only trustless coordination layer despite years of weak price action

Ethereum's value lies in credible neutrality, not speed, as Logarithmic Rex argues ETH remains crypto's only trustless coordination layer despite years of weak price actionCommunity notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…