In-depth explainer on yield-bearing crypto assets, covering how stablecoins, bitcoin, gold tokens and tokenized funds generate onchain yield, key mechanisms like RWAs and DeFi lending, and the regulatory and risk trade-offs shaping this new money layer.

- x.com29

- blockworks.co2

- thedefiant.io1

- franklintempleton.com1

- comp.xyz1

- news.curve.finance1

- thecryptohodl.com1

+6 sources across the wider coverage universe

Mitsui launches yield-bearing Zipangcoin on OP Mainnet, backed by physical gold, silver, and platinum2026-04

Mitsui launches yield-bearing Zipangcoin on OP Mainnet, backed by physical gold, silver, and platinum2026-04 Reflect unveils a permissionless framework for yield-bearing stablecoins on Solana, replacing custodial allocators with transparent onchain risk models and automated capital deployment2026-06

Reflect unveils a permissionless framework for yield-bearing stablecoins on Solana, replacing custodial allocators with transparent onchain risk models and automated capital deployment2026-06 Aave brings yield-bearing mUSD spending to MetaMask Card via Mastercard2026-05

Aave brings yield-bearing mUSD spending to MetaMask Card via Mastercard2026-05 Bybit introduces yield-bearing gold product on tokenized gold. Two XAUT savings products are offered: flexible staking with returns of up to 11% APR, and fixed-term savings with up to 12% APR.2026-03

Bybit introduces yield-bearing gold product on tokenized gold. Two XAUT savings products are offered: flexible staking with returns of up to 11% APR, and fixed-term savings with up to 12% APR.2026-03 Convex recaps the history of Resupply ($RSUP) and its $reUSD stablecoin backed by yield-bearing positions in Curve Lend and Fraxlend2026-05

Convex recaps the history of Resupply ($RSUP) and its $reUSD stablecoin backed by yield-bearing positions in Curve Lend and Fraxlend2026-05 Tassat and Lynq leverage Avalanche to rebuild financial rails with real-time settlement and yield-bearing assets, targeting institutional adoption of onchain infrastructure2026-04

Tassat and Lynq leverage Avalanche to rebuild financial rails with real-time settlement and yield-bearing assets, targeting institutional adoption of onchain infrastructure2026-04

Understanding Yield-Bearing Crypto Assets

Crypto assets that automatically pass through income from their underlying collateral are increasingly described as yield-bearing, turning what used to be idle balances into productive capital. In practice, this means tokens that maintain price stability or blue-chip exposure while continuously accruing yield from sources like U.S. Treasuries, money market funds, decentralized lending, derivatives strategies, or tokenized gold.

From Idle Tokens to Productive Capital: What “Yield-Bearing” Means

The term yield-bearing describes any crypto asset whose design makes the accrual and distribution of income a native property of the token itself, rather than an optional add-on via separate lending, staking, or farming positions. In a yield-bearing design, holding the token is sufficient to earn the underlying yield, without having to lock funds in a protocol, choose a strategy manually, or roll over expiring positions. For example, yield-bearing stablecoins are structured so that interest from collateral such as U.S. Treasury bills, money-market instruments, or overcollateralized DeFi lending markets flows automatically to token holders. Yield-bearing instruments differ from traditional “rewards programs” or centralized exchange promotions, which may pay discretionary bonuses on top of a non-yielding stablecoin; in yield-bearing tokens, the right to income is engineered into the asset itself and is typically enforceable onchain.

This shift is particularly stark when contrasted with first-generation stablecoins like USDC or USDT, where issuers invest reserves in safe, interest-bearing assets but retain virtually all of that income for themselves. In the classic model, users get price stability and liquidity, but their dollars remain effectively “idle” even though reserves are earning yields in the background. Yield-bearing stablecoins invert this arrangement by explicitly sharing the reserve income with token holders, transforming the medium of exchange into a productive asset and aligning incentives between issuers and users. More broadly, yield-bearing design is now being applied to bitcoin, tokenized funds, and commodity-backed tokens such as gold, as platforms race to integrate passive yield into every corner of onchain finance.

From a user’s perspective, the core promise of yield-bearing assets is simplicity: one instrument combines price exposure, stability, and yield accrual. A yield-bearing stablecoin aims to track one U.S. dollar while growing in effective value over time, either by increasing the token balance in your wallet or by making each token redeemable for slightly more collateral than before. Yield-bearing gold products seek to marry gold’s price exposure with regular income, something conventional bullion and most gold ETFs do not provide. Bitcoin “vaults” and soon, potentially, yield-bearing bitcoin ETFs, attempt to preserve BTC price exposure while routing coins through lending or other yield strategies on behalf of holders. In all of these cases, yield-bearing tokens move markets beyond the old binary of “hold a coin” versus “lock it somewhere else to earn yield” and toward a unified, composable asset.

Regulators and policymakers, however, increasingly see yield-bearing designs as a double-edged sword. The BIS, for instance, has noted that yield-bearing products built on top of payment stablecoins can amplify familiar risks around reserve quality, liquidity, and runs, especially when yield is generated through re-lending, derivatives, or complex DeFi strategies. Higher advertised returns can draw in more users and more leverage, while obscuring the underlying risk transfer from issuers or platforms to token holders. Whether yield-bearing assets ultimately look more like bank deposits, money-market fund shares, securities, or entirely new categories of financial instrument remains a live regulatory question in many jurisdictions.

Reap integrates Circle’s USYC tokenised fund to bring yield-bearing treasury management to globally operating businesses

USYC’s public terms still carry the TradFi shape: non-US person gate, $100k minimum, USDC subscriptions/redemptions, and instant liquidity only up to capacity. Reap’s edge is distribution into corporate cards and cross-border payout flows, where idle balances already sit on stablecoin rails instead of in a treasury desk’s separate RWA account. CFO-grade controls, redemption assumptions, and securities eligibility become the bottleneck once tokenized T-bills are treated as working capital.

Readers click yield-bearing content most when a TradFi giant (BlackRock, Franklin Templeton, Circle) legitimizes the mechanic — nearly 2× more than any pure-DeFi angle — revealing that the real story is whether on-chain yield can legally and structurally replace bank deposits, not how the yield is generated.↗

Core Mechanisms Behind Yield-Bearing Crypto Assets

Although “yield-bearing” is a marketing-friendly umbrella term, the mechanics that generate and distribute yield vary significantly. Understanding those mechanics is critical to evaluating both the opportunity and the risk profile of any given product. At a high level, the yield in crypto comes either from offchain real-world assets (RWAs) such as Treasuries or money-market funds, or from onchain protocol activity like lending, staking, or derivatives funding. A single token can combine several of these sources, and often wraps an existing stablecoin like USDC inside a more complex structure that captures yield while preserving fungibility and composability.

Collateral and Revenue Sources

Offchain RWA collateral is the dominant source of stable, dollar-like yield in the current cycle. In these designs, a stablecoin issuer or tokenized fund platform takes in onchain dollars, deploys them into short-duration U.S. Treasuries, repurchase agreements, or regulated money-market instruments, and then passes part of the interest income back to token holders. OpenEden’s USDO, for example, is described as a regulated yield-bearing stablecoin pegged 1:1 to the U.S. dollar and fully backed by tokenized U.S. Treasury bills via its TBILL tokens. Because TBILL itself represents ownership in short-term Treasuries, the yield from those government securities is transmitted through to USDO holders, turning onchain dollars into what is essentially a tokenized slice of the T-bill market with continuous proof of reserves.

Tokenized money-market funds form a closely related category, often targeting institutional investors rather than general-purpose stablecoin use. WisdomTree’s WTGXX Treasury Money Market Digital Fund, for instance, is a registered mutual fund whose shares have been tokenized and granted SEC exemptive relief to trade 24/7 with instant settlement under a dealer-principal model. While WTGXX is not branded as a stablecoin, it behaves economically like a yield-bearing cash equivalent: it invests in high-quality short-term instruments, accrues yield at the fund level, and now benefits from blockchain-native settlement without leaving the regulatory perimeter. Similarly, Fidelity International’s tokenized FILQ fund uses Chainlink-based onchain NAV to bring regulated, yield-bearing liquidity into 24/7 digital markets, showing how large asset managers are extending traditional products into crypto rails.

Onchain collateral is the second major source of yield, particularly for DeFi-native tokens. Here, protocols generate revenue through overcollateralized lending, liquid staking derivatives, or derivatives funding and basis trades, and encode that revenue into the token’s economics. Lending protocols such as Aave issue interest-bearing receipt tokens (“aTokens”) that automatically grow in line with borrower interest; these have become the building blocks for more user-facing yield-bearing assets. Aave’s integration with the MetaMask Card and Mastercard illustrates this well: users deposit mUSD into Aave, receive a yield-bearing mUSD receipt token in their wallet, and can then spend directly from that balance, which continues to accrue interest up to the moment of point-of-sale conversion. In this model, yield arises from borrowers paying interest on loans, while users experience it as a continuously growing balance associated with their everyday spending money.

More complex onchain strategies involve derivatives funding rates, futures basis trades, and re-hypothecation of collateral across protocols. Some yield-bearing stablecoins and vaults direct capital into these strategies, seeking to harvest funding spreads while hedging price exposure. The BIS warns that such products, where yield may come from re-lending to margin pools, derivatives collateral, or leveraged DeFi positions, can exacerbate traditional stablecoin risks by adding layers of market and counterparty risk on top of redemption and reserve concerns. Bitcoin-focused products such as Kraken’s Bitcoin Vault allocate BTC to decentralized lending markets to generate yield, introducing borrowers, smart contracts, and liquidity conditions as new risk vectors for what might otherwise be a simple “hold BTC in cold storage” strategy.

Distribution Models: Rebasing versus Accumulation

Once yield is generated, the next design choice is how to deliver it to token holders. In crypto, two patterns dominate: rebasing and accumulating (or reward-bearing) models. In a rebasing design, the token’s unit price stays anchored at the target (often 1 USD), while the protocol periodically increases the number of tokens in each holder’s wallet. If the underlying collateral has earned a 5% return over a given period, a holder of 100 tokens might see her balance become approximately 105 tokens, even though each unit still trades around one dollar. This mechanism gives a user experience similar to bank interest payments while preserving the intuitive “one token equals one dollar” unit of account for accounting and pricing.

By contrast, accumulating or reward-bearing models keep the token balance constant but make each token redeemable for a slightly larger share of the underlying collateral over time. A yield-bearing stablecoin might be minted at a 1:1 exchange rate with USDC, but after a year of yield accrual each token could be redeemable for, say, 1.05 USDC, reflecting the net interest earned. In practice, this means the token’s effective price in secondary markets drifts upward relative to the base stablecoin or underlying asset, even if it continues to be colloquially described as “dollar-pegged.” Accumulating designs are common for wrapper tokens around Treasuries and money market funds, because they more closely resemble traditional mutual fund or ETF shares that increase in NAV rather than paying out discrete interest coupons.

From a DeFi composability standpoint, each approach has trade-offs. Rebasing tokens can be awkward for protocols that assume token balances are static, especially in smart contracts that do not expect balances to change outside of explicit transfers. Accumulating tokens avoid that technical friction but undermine the naive assumption that “1 unit equals 1 dollar,” which can create confusion in pricing, accounting, and risk management. Yield-bearing instruments like R2USD, a stablecoin issued by R2 Protocol that aims to maintain a 1:1 peg to the U.S. dollar while generating onchain yield, highlight the challenge of combining a simple user mental model with the reality of fluctuating collateral and dynamic yields.

Wrappers, Native Designs, and Token Structures

Another key design axis is whether a yield-bearing product is a wrapper around an existing base asset or a native token whose own issuance and redemption rules encode the yield. Many yield-bearing stablecoins operate as wrappers around well-known assets such as USDC, USDT, or tokenized T-bills. In these structures, users deposit the base asset into a protocol and receive a new token that represents a claim on both the principal and accrued yield. For example, many protocols create interest-bearing versions of USDC by depositing it in lending markets and minting a derivative token that tracks both principal and interest, similar to Aave’s aUSDC. R2USD, which is designed as a yield-bearing stablecoin backed by tokenized Treasuries and other onchain assets, can be seen as a step further, where the wrapper itself functions as a full-fledged stablecoin with its own peg and redemption mechanics.

Native yield-bearing designs bake yield into the primary token issuance process. USDO is presented as a stablecoin that is natively yield-bearing because it is overcollateralized by TBILL tokens; users mint USDO directly against Treasury exposure rather than first holding a non-yielding dollar coin. Permissionless frameworks like Reflect go even further, enabling developers to launch new yield-bearing stablecoins that route liquidity to onchain strategies via transparent risk models and automated capital deployment, without relying on a single custodial allocator. Here, the token’s minting, risk management, and yield distribution are tightly interwoven, and the project looks less like a wrapper around USDC and more like a new kind of programmatic money-market instrument.

Tokenized fund shares such as WTGXX or FILQ represent yet another structure. These are explicitly investment products governed by securities law, where each token is legally a share of a regulated fund that holds specific underlying assets. Yield-bearing gold or commodity tokens like Mitsui’s Zipangcoin, which is backed by physical gold, silver, and platinum and described as a yield-bearing instrument, fall into a similar category of tokenized commodities with built-in return streams. The common thread across wrappers, native stablecoins, and tokenized funds is the attempt to expose onchain users to income-generating assets while preserving the programmability, composability, and 24/7 settlement characteristics of crypto infrastructure.

Major Categories of Yield-Bearing Assets

Yield-bearing design is spreading across the crypto asset spectrum, from dollar-pegged stablecoins to bitcoin and gold, and onward to tokenized funds and DeFi-native positions. While the underlying mechanics overlap, each category serves distinct user needs and is subject to different risk and regulatory considerations.

Yield-Bearing Stablecoins

Yield-bearing stablecoins are arguably the most important building block in this new landscape because they directly challenge the status quo of non-interest-bearing stablecoins like USDC. Conceptually, they aim to perform the same core functions—acting as a stable unit of account, medium of exchange, and store of value—while distributing a share of the underlying yield back to holders. In practice, this requires careful collateral management, peg maintenance, and risk controls to ensure that stability is not sacrificed for yield. Chainlink’s analysis frames yield-bearing stablecoins as a “fundamental shift in how digital money operates,” turning the stablecoin itself into a revenue-sharing instrument backed by RWAs or onchain protocol revenues.

USDO exemplifies a RWA-backed implementation: it is pegged 1:1 to the U.S. dollar, fully collateralized by tokenized U.S. Treasuries, and offers native Treasury yield plus onchain proof of reserves. Because USDO is backed by TBILL tokens that represent actual Treasury holdings, reserve transparency is easier to audit onchain, and USDO holders can be confident that their stablecoins are effectively tokenized slices of a T-bill portfolio. The asset’s use as settlement currency in institutional OTC trades, such as a transaction between Galaxy Digital and DeFiance Capital, showcases how yield-bearing stablecoins are beginning to penetrate institutional markets that value both yield and real-time settlement.

R2USD offers a contrasting, more DeFi-centric approach. It is described as a yield-bearing stablecoin issued by R2 Protocol that maintains a 1:1 USD peg while generating sustainable onchain yield from its portfolio of collateralized positions. Rather than relying solely on Treasuries, R2USD may use a diversified set of onchain assets and strategies, subject to smart contract and market risks but also enabling potentially higher returns and more native composability within DeFi ecosystems. Reflect’s permissionless system for creating yield-bearing stablecoins further generalizes this design space by allowing developers to design tokens that allocate funds across onchain strategies according to transparent, algorithmic risk models, eliminating the need for an opaque centralized allocator.

On high-throughput chains like Solana, an expanding array of stablecoin designs—including yield-bearing variants—are emerging as the backbone of DeFi activity. As Solana’s stablecoin landscape grows in volume and diversity, yield-bearing designs are increasingly seen as the future “base layer” money for onchain economies, enabling protocols, treasuries, and users to keep their working capital in productive form. New entrants such as savUSD, Avant’s yield-bearing stablecoin being brought to the Movement network, similarly illustrate how every new ecosystem now tends to launch with some form of native yield-bearing dollar, rather than replicating the non-interest-bearing models of the previous cycle.

Yield-Bearing Bitcoin

Bitcoin has traditionally been framed as “digital gold”: a non-yielding, scarce asset that is held for long-term appreciation or as a macro hedge. In the current market, however, platforms are racing to transform BTC into yield-bearing infrastructure by routing it into lending markets, rehypothecation chains, or derivatives strategies. Kraken’s Bitcoin Vault is a notable example: it allows users to allocate BTC from their Kraken accounts to decentralized lending markets via an embedded non-custodial wallet, with rewards accruing automatically and compounding into the vault balance. Users retain the ability to withdraw BTC at any time, subject to a short deallocation waiting period, while earning a variable APY determined by borrowing demand in underlying markets.

This onchain lending-based yield bears resemblance to yield-bearing stablecoin structures that rely on DeFi lending protocols rather than Treasuries. As with those products, however, it introduces counterparty and protocol risks that do not exist when BTC is simply held in cold storage. Market dislocations, smart contract bugs, or liquidity crunches in DeFi can affect both the continuity of yield and the safety of principal. Kraken’s Bitcoin Vault mitigates some of this through an embedded non-custodial architecture and clear disclosure of variable earning rates and performance fees, but ultimately users are exposed to the health of the lending markets that their BTC is allocated to.

At the institutional level, the prospect of a yield-bearing bitcoin ETF illustrates another direction. BlackRock’s filing of a Form 8-A for a yield-bearing bitcoin ETF, with analysts expecting launch soon, signals interest in packaging BTC exposure with income within a regulated fund wrapper. While details of the underlying yield strategies will matter enormously, the concept suggests BTC could be transformed into a yield-bearing asset in brokerage and retirement accounts much as it is being transformed in DeFi vaults. The key difference is that yield-bearing ETFs will be subject to securities regulation, disclosure, and traditional custody frameworks, whereas onchain yield-bearing BTC positions often rely on smart contracts and composable DeFi risk.

Yield-Bearing Gold and Commodities

Gold and other commodities have historically been non-yielding, with investors relying on price appreciation or, in the case of miners, equity dividends instead of coupon-like income. Crypto tokenization is changing that by allowing gold-backed tokens to be plugged into yield-generating strategies or designed as inherently yield-bearing instruments. Bybit’s XAUT Earn product, for example, allows holders of Tether Gold (XAUT)—a token backed by physical gold—to earn interest through flexible or fixed-term savings products. This model effectively layers a yield-bearing savings program on top of a gold-pegged token, merging exposure to the gold price with onchain income generation, something that is uncommon in both traditional bullion and many digital gold products.

Lista’s slisXAUE token represents a DeFi-native variant, marketed as a yield-bearing gold token powered by Xaue Protocol’s gold yield strategies. In this structure, users deposit XAUt and receive slisXAUE in return, earning yield denominated in gold while retaining the ability to redeem back into the underlying token, subject to business-day settlement timelines. Here, yield presumably comes from strategies such as lending XAUt to borrowers or using it as collateral in derivatives markets, again introducing financial risks that traditional “vaulted gold” investors may not be accustomed to. The difference is that the yield-bearing property is encoded in the slisXAUE token itself, which represents a claim on both the gold and the accrued yield.

Mitsui & Co. Digital Commodities’ Zipangcoin extends the concept to a basket of commodities. Issued on OP Mainnet, Zipangcoin (ZPG) is backed by physical gold, silver, and platinum and described as a yield-bearing instrument distributed through regulated exchanges in Japan, such as GMO Coin. Investors thus gain exposure to a diversified basket of precious metals through a regulated digital instrument that also offers some form of yield, positioning ZPG as a hybrid between a commodity-backed stablecoin and an income-generating fund share. As tokenized commodities proliferate, similar yield-bearing structures are likely to emerge for energy, industrial metals, and even carbon credits, blending real-world commodity markets with onchain yield infrastructure.

Tokenized Money Market Funds and Treasuries

While yield-bearing stablecoins aim to behave like dollars, tokenized money market funds and T-bill tokens explicitly present themselves as investment products. They pull the low-volatility yield that treasurers and institutions have long sought in traditional markets directly onto blockchain rails. WisdomTree’s WTGXX Treasury Money Market Digital Fund is emblematic of this category. The fund invests in traditional money market instruments but issues tokenized shares that now, thanks to SEC exemptive relief, can trade and instantly settle 24/7 via a dealer-principal liquidity model. This combination of regulated fund structure, continuous trading, and instant settlement is a major milestone in blending TradFi oversight with crypto-native settlement.

Similarly, Fidelity International’s FILQ tokenized fund uses Chainlink-powered onchain NAV to bring regulated, yield-bearing fund shares into the 24/7 digital asset ecosystem. Rather than creating a new stablecoin, FILQ represents a traditional fund share whose value floats with underlying fixed-income assets, while benefiting from blockchain-based transparency and composability. On the more DeFi-native side, tokens like TBILL, which back OpenEden’s USDO, and other Treasury-backed RWA tokens serve as building blocks both for stablecoins and for direct treasury exposure onchain.

JTRSY, a token associated with Centrifuge’s real-world asset platform, illustrates an important emerging frontier: redemption infrastructure. JTRSY is yield-bearing, instantly redeemable, and usable as a reserve asset; with the Basin integration, holders can convert JTRSY to USDC instantly, 24/7, mirroring the redemption experience of best-in-class stablecoins. Observers have emphasized that the most underrated piece of tokenized fund infrastructure is exit liquidity: yield-bearing assets remain underutilized as long as redemptions run on traditional timeframes, often limited to business hours and multi-day settlement. By coupling onchain yield with instant, programmatic exit routes, tokens like JTRSY and WTGXX are redefining what “cash equivalent” means in a digital context.

DeFi-Native Yield-Bearing Tokens

Beyond RWAs and traditional assets, DeFi continues to invent new classes of yield-bearing tokens rooted entirely in onchain activity. Aave’s aTokens are a canonical example: when users deposit assets such as mUSD or USDC into Aave, they receive aTokens that represent their deposit plus accrued interest, with balances updating in real time as borrowers pay interest to the pool. These aTokens are not merely receipts but fully composable building blocks that can be used as collateral, integrated into wallets, and, in the case of the MetaMask Card, spent directly at point of sale, all while continuing to accrue yield until the moment of use.

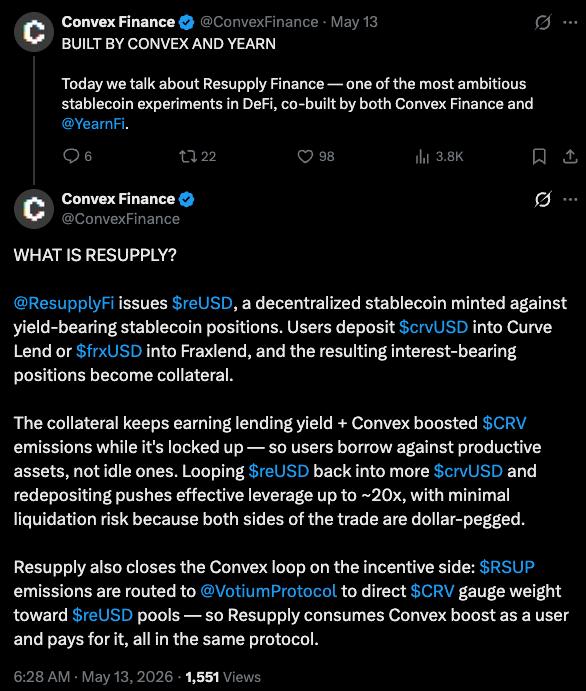

Similar patterns appear in lending markets, restaking and liquid staking protocols, and structured product platforms that issue derivative tokens representing exposure to particular yield strategies. Protocols like Venus and others experiment with vaults that allow users to deposit one yield-bearing token (such as a staked ETH variant) and borrow against it, stacking yield layers into increasingly complex configurations. Stablecoins like reUSD, backed by yield-bearing positions in Curve Lend or Fraxlend, reflect an ongoing trend of using yield-bearing collateral as the backing for new stablecoins, turning yield-bearing DeFi positions themselves into monetary building blocks.

These DeFi-native yield-bearing tokens tend to sit at the riskier end of the spectrum, as their yield is often sourced from leveraged trading, liquidity provision, and volatile funding rates rather than government securities. On the other hand, they showcase the full composability of onchain finance: tokens can represent claims on claims on claims, each layer adding or transforming yield potential. For sophisticated users and protocols, these tokens provide granular tools for yield management; for less experienced users, they underscore the importance of understanding not just that a token is “yield-bearing,” but how, where, and at what risk that yield is generated.

- 01TradFi giants entering yield stablecoins↗

BlackRock BUIDL partnering with Elixir/Curve for deUSD (748 clicks) and Franklin Templeton enabling peer-to-peer BENJI transfers signaled institutional validation that dwarfed every other angle.

- 02Banks lobbying against on-chain yield↗

The regulatory fight over whether yield-bearing stablecoins legally compete with bank deposits framed the entire category as a systemic threat to incumbents, making the stakes concrete for readers.

- 03Funding-rate slump crushing basis yields↗

The collapse of basis-trade profits eroding USDe and peer yields gave readers a real-money mechanism explaining why high advertised APYs are unstable, not just theoretical risk.

- 04Tokenized RWA treasury backing↗

Projects like R2 Protocol (Binance Alpha) and USD.AI tying stablecoin yield to tokenized T-bills positioned RWA backing as the 'safe' alternative to funding-rate-dependent yield, drawing readers comparing durability.

- 05Yield-bearing beyond stablecoins↗

Bybit's tokenized gold savings products, Lombard's yield-bearing LBTC, and GammaSwap's gETH showed readers the mechanic expanding to BTC and commodities, broadening the category's relevance.

- 06Protocol standards and vault mechanics↗

EIP-7540's async vault improvements and Pendle's principal/yield token splitting attracted readers who wanted the infrastructure layer — how composability and yield stripping actually work under the hood.

Use Cases: Why Yield-Bearing Matters

The spread of yield-bearing designs is not just a technical curiosity; it is reshaping how individuals, protocols, and institutions think about cash management, payments, collateral, and savings. As stablecoin yields increasingly mirror or exceed traditional money market rates, and as tokenized funds and commodities layer income on top of familiar exposures, the opportunity cost of holding non-yielding assets is becoming more obvious. Stablecoins charted the first course for onchain dollars; yield-bearing assets now promise to turn what used to be idle digital cash into an always-on source of income.

Onchain Treasury and Cash Management

For DAOs, protocols, and crypto-native businesses, stablecoin holdings have long been the default form of treasury cash. Yet these balances, often dominated by USDC or USDT, typically earned no yield unless actively deployed into lending or liquidity provision strategies. Yield-bearing stablecoins and tokenized T-bill products change that calculus by making passive treasury holdings productive by default. A protocol can hold USDO, R2USD, or a tokenized money market fund in its multisig wallet, maintaining instant liquidity for operational needs while earning Treasury or DeFi yields in the background.

Institutional interest in this model is growing. Initiatives like Tassat and Lynq’s use of Avalanche to rebuild financial rails with real-time settlement and yield-bearing assets illustrate how traditional financial players see tokenized cash equivalents as a way to modernize enterprise payment and treasury systems. Similarly, Kaia’s strategic push to integrate tokenized Treasuries like TBILL and yield-bearing stablecoins like USDO into its core RWA infrastructure aims to provide institutional-grade, yield-bearing base assets for the entire ecosystem. For corporate treasurers, the prospect of holding tokenized, yield-bearing money market exposures with instant settlement and programmable liquidity is increasingly compelling compared with traditional bank accounts or sweep programs.

On Solana, the Solana Foundation’s institutional workshop on building a permissioned, yield-bearing money market fund token highlights a parallel trajectory. Institutions often require permissioned access, KYC controls, and regulatory comfort that generic DeFi protocols do not provide. By enabling permissioned, yield-bearing tokens that nonetheless settle and interoperate on public chains like Solana, the industry is exploring hybrid models that bring real-world funds onchain without sacrificing compliance. Over time, onchain treasuries may come to resemble portfolios of yield-bearing stablecoins, tokenized funds, and DeFi positions, managed via smart contracts with granular risk and duration controls.

Payments, Settlement, and Commerce

Yield-bearing assets are also beginning to reshape payments and settlement, especially where instant settlement and 24/7 markets are crucial. Aave’s integration with the MetaMask Card and Mastercard is perhaps the clearest example at the retail level. Users can hold yield-bearing mUSD or yield-bearing USDC in their MetaMask wallet; when they make a purchase with the MetaMask Card, the required amount of the asset is converted to fiat at the point of sale, while the remaining balance continues to earn interest in Aave until the moment they tap the card. This design allows consumers to treat their spending money as an income-generating asset without sacrificing day-to-day liquidity.

At the institutional level, yield-bearing stablecoins are emerging as settlement currencies in large OTC trades and structured products. USDO’s use as settlement currency in an OTC transaction between Galaxy Digital and DeFiance Capital illustrates how institutional counterparties can agree on a yield-bearing token as the unit of settlement, combining the familiar “USD” mental model with Treasury yield and onchain settlement. Platforms like Tassat and Lynq, which leverage Avalanche to build real-time settlement rails for financial institutions using yield-bearing assets, further underline this trend of upgrading legacy payment systems with tokenized, interest-bearing cash equivalents.

Tokenized payroll offers another emerging use case. Plume’s pilot with Toku and WisdomTree, converting employee wages into yield-bearing WTGXX shares, suggests a future in which salaries are paid not in bank deposits or static stablecoins, but in tokenized money market fund shares that begin accruing yield from the moment they are issued. If widely adopted, such models could materially alter household cash management, effectively turning paychecks into 24/7 yield-bearing money by default.

Trading, Collateral, and Leverage

In trading and DeFi markets, yield-bearing assets are increasingly used as collateral, margin, and base currency for structured products. Yield-bearing stablecoins and tokenized fund shares can serve as collateral in lending protocols, allowing users to borrow against them while retaining yield, which can partially offset borrowing costs. This dynamic is already visible in DeFi designs where users deposit interest-bearing tokens, borrow another asset, and deploy that capital into additional strategies, effectively leveraging their yield streams.

The availability of yield-bearing collateral also influences derivatives pricing and leverage. For instance, strategies that harvest perpetual futures funding or futures basis spreads often depend on having a base asset that accrues a “risk-free” yield in the background. Holding a yield-bearing stablecoin or T-bill token while shorting a futures contract allows traders to lock in a spread between the futures basis and the underlying yield, creating market-neutral income streams that amplify the perceived attractiveness of yield-bearing base assets. Conversely, as more traders use yield-bearing stablecoins as margin, the overall demand for such instruments can deepen liquidity and tighten spreads in both spot and derivatives markets.

However, using yield-bearing assets as collateral also raises questions about rehypothecation and systemic risk. When the same tokenized T-bill or yield-bearing stablecoin serves as collateral across multiple protocols, the promised yield rests on a web of interlocking obligations. Stress in one part of the system can propagate quickly, especially if redemptions are gated or subject to business-day settlement, while DeFi markets expect instant liquidity. JTRSY’s move to enable instant conversion to USDC via Basin, and WTGXX’s 24/7 dealer-principal liquidity model, can be seen as responses to this challenge, aiming to reconcile institutional-grade yield-bearing assets with onchain expectations of always-on redemption.

Savings and Wealth Management

For retail users, yield-bearing assets are reframing basic questions of savings and wealth management. Instead of choosing between a stablecoin that pays nothing and a lending protocol that requires active management, users can increasingly opt into stablecoins, tokenized funds, or gold tokens that automatically accrue yield in the background. Yield-bearing stablecoins like USDO or R2USD give savers a way to hold “dollars” onchain while earning passive income, without having to become DeFi power users. Similarly, tokenized funds like FILQ and WTGXX open the door to regulated fixed-income exposures delivered through crypto-native channels such as wallets, exchanges, and DeFi aggregators.

Gold and commodity investors face an analogous shift. Products like XAUT Earn and slisXAUE allow users to keep wealth in gold-linked tokens while simultaneously earning interest, blurring the line between “store of value” and “income-generating asset.” For long-term savers who historically saw gold as inert, the prospect of gold-denominated yield-bearing tokens is a significant conceptual change. However, it also demands a new level of diligence: understanding whether the yield arises from relatively conservative lending, more aggressive derivatives strategies, or some combination thereof.

As wealth management moves onchain, advisors and platforms will need to educate clients not just about diversification across assets, but diversification across sources of yield. Treasury-backed stablecoins, money market funds, DeFi lending, and derivatives-based strategies carry very different risk-return profiles, even if all are marketed as “yield-bearing.” The challenge—and opportunity—is to construct onchain portfolios that balance these dimensions in a way that aligns with clients’ risk tolerance and regulatory constraints.

Risks, Regulation, and Design Trade-offs

The proliferation of yield-bearing assets raises profound questions about financial stability, investor protection, and the future regulatory perimeter. Yield does not appear out of nowhere: it is compensation for taking risk, whether credit, duration, liquidity, smart contract, or leverage risk. Evaluating yield-bearing tokens therefore requires careful scrutiny of their design, operations, and legal structures, beyond headline APY figures or marketing narratives.

Smart Contract and Protocol Risk

For assets whose yield is sourced from DeFi protocols, smart contract risk is paramount. Bugs, exploits, or governance failures can lead to partial or total loss of collateral, disrupting both yield and principal. When a yield-bearing stablecoin relies on overcollateralized lending markets or staking derivatives, as described in analyses by Chainlink and 1inch, the safety of the token hinges on the integrity of those underlying protocols. The more composable the system—where a yield-bearing stablecoin is backed by yield-bearing DeFi positions, which themselves depend on other protocols—the more points of failure exist.

Protocol risk also includes oracle failures, liquidation mechanisms, and governance capture. For tokenized funds that use onchain NAV, like FILQ, inaccuracies or lags in NAV updates can create arbitrage opportunities or mispricing, especially in volatile markets. For RWA-backed stablecoins like USDO or R2USD, reliance on tokenized representations of Treasuries or other assets introduces dependencies on custody, tokenization platforms, and legal enforceability. Users must trust not only the DeFi smart contracts but also that offchain legal agreements will be honored in adverse scenarios.

Market, Liquidity, and Redemption Risk

Yield-bearing assets with offchain collateral face classic money-market risks: duration mismatch, liquidity constraints, and run risk. The BIS notes that yield-bearing products built on payment stablecoins can add layers of liquidity and market risk, especially when reserves are re-lent or invested in less liquid instruments to chase higher yields. If many users simultaneously seek redemption, issuers may be forced to liquidate assets under pressure, potentially at a loss, threatening the stability of the token’s peg.

Redemption design is thus a central trade-off. Kraken’s Bitcoin Vault offers BTC withdrawals but requires a deallocation period of several days, reflecting the need to unwind positions in decentralized lending markets without incurring penalties or slippage. Yield-bearing gold tokens like slisXAUE promise redemption of XAUt within business-day timelines, aligning with the operational constraints of physical gold custody and settlement. JTRSY and WTGXX have pushed toward instant, 24/7 redemption or liquidity, but these mechanisms depend on the robustness of dealer-principal models or liquidity provisioning arrangements that may be stress-tested only in times of crisis.

DeFi-native yield-bearing tokens introduce additional liquidity risks. If a yield-bearing stablecoin is backed by positions in protocols like Curve Lend or Fraxlend, the ability to maintain a 1:1 peg under stress depends heavily on secondary market liquidity, oracle performance, and the health of those lending markets. Users must ask not only “What is the yield?” but “Under what market conditions can I exit at or near par, and through what mechanisms?”

Counterparty, Custodial, and Legal Risk

Many yield-bearing assets, especially those backed by RWAs, rely on custodians, trustees, or centralized issuers. OpenEden’s USDO is marketed as fully collateralized by tokenized Treasuries with an emphasis on customer and asset protection and on-chain transparency, but users still rely on the integrity and solvency of the TBILL issuer and the custodial chain behind those tokens. Zipangcoin’s backing by physical gold, silver, and platinum requires trust in Mitsui and its custodial partners, as well as confidence in Japanese regulatory oversight. Bybit’s XAUT Earn product depends on both Tether’s physical gold backing for XAUT and Bybit’s solvency and risk management for the yield layer.

Legal risk is equally salient for tokenized funds and yield-bearing stablecoins. WTGXX and FILQ operate under explicit regulatory frameworks, with exemptions and approvals tailored to their tokenized nature. Their tokens represent fund shares, subject to securities law, disclosure obligations, and investor protections. In contrast, many yield-bearing stablecoins and DeFi-native yield tokens operate in murkier regulatory territory, where the classification of the token—as a payment instrument, money market fund, security, or something else—is unresolved. This ambiguity can lead to enforcement actions, forced restructurings, or sudden loss of market access, particularly in jurisdictions with aggressive securities regulators.

Regulatory Treatment of Yield-Bearing Stablecoins and Tokenized Funds

Regulators globally are grappling with how to categorize and oversee yield-bearing stablecoins and related products. The BIS’s analysis of stablecoin-related yields warns that yield-bearing products offered by cryptoasset service providers, especially when using reserve-backed payment stablecoins as a base, can amplify existing stablecoin risks. In some cases, platforms advertise high yields funded by re-lending stablecoins to borrowers, margin pools, or DeFi protocols, while users may not fully grasp that they are underwriting credit and liquidity risk in addition to price stability risk.

The regulatory response so far has been fragmented. Some jurisdictions are moving toward explicit stablecoin legislation that distinguishes between payment stablecoins and investment-like tokens, with stricter rules for those offering yield. Tokenized funds like WTGXX have navigated this landscape by working within existing mutual fund frameworks and obtaining targeted exemptive relief to allow 24/7 trading and instant settlement while maintaining traditional fund oversight. Yield-bearing bitcoin ETFs, if approved, would similarly be integrated into familiar securities regimes, with prospectus-level disclosures of strategies and risks.

Going forward, regulators are likely to scrutinize three aspects in particular: the nature and quality of underlying assets; the mechanisms of yield generation (including leverage and derivatives); and the clarity of disclosures to investors. Products that share yield from high-quality short-term government securities, with robust proof of reserves and redemption rights, may be viewed more favorably than those that obscure speculative strategies behind attractive APY figures. At the same time, the line between a yield-bearing stablecoin and a tokenized money market fund may blur, forcing regulators to decide whether to treat some “stablecoins” as de facto investment funds subject to fund regulation.

Systemic and Macro Considerations

Beyond individual products, the rise of yield-bearing stablecoins and tokenized funds has potential systemic implications. As more capital migrates from bank deposits to tokenized T-bill funds and yield-bearing stablecoins, traditional banks could face competitive pressure for retail and corporate cash balances, especially if tokenized products offer higher yields, instant settlement, and superior transparency. This dynamic resembles the growth of money market funds in the 1970s and 1980s, which reshaped short-term funding markets and prompted regulatory responses to mitigate run risk.

Onchain, the concentration of stablecoin reserves in short-term government debt and repo markets means that crypto money increasingly sits on top of traditional sovereign debt markets. While this can strengthen channels of monetary policy transmission, it also raises questions about spillovers: if a large yield-bearing stablecoin or tokenized fund were to experience a run, forced liquidation of Treasuries could, in theory, propagate stress into traditional markets. Conversely, sharp moves in Treasury yields or liquidity conditions could affect the stability and attractiveness of stablecoin yields, feeding back into DeFi and crypto asset prices.

Finally, as yield-bearing assets become the default form of onchain money, they influence how protocols and users think about “risk-free rate” benchmarks. The yield on a major RWA-backed stablecoin or tokenized money market fund could become DeFi’s reference rate, shaping lending rates, discount factors, and valuation models across the ecosystem. This knitting together of TradFi yield curves and DeFi pricing is a powerful step toward an integrated global financial system, but it also means that shocks in one domain can more easily propagate to the other.

- 2021-01launch

Franklin Templeton launches BENJI on Stellar blockchain

- 2023-08milestone

Pendle Finance surpasses $125M TVL splitting yield tokens

- 2024-03launch

BlackRock launches BUIDL tokenized fund on Ethereum

- 2024-09governance

EIP-7540 proposed for async yield-bearing vault standard

- 2025-02milestone

Stable Summit at ETHDenver highlights yield-bearing stablecoin rise

- 2025-03launch

BlackRock BUIDL enables deUSD minting via Elixir/Curve partnership

Galaxy Digital and DeFiance Capital settle OTC trade in USDO

Yield-bearing stablecoins record $1B+ outflows, largest since UST collapse

Design Patterns and Emerging Infrastructure

Under the surface of individual products, a set of shared design patterns and infrastructure components is emerging to support the yield-bearing future. These include permissionless frameworks for creating yield-bearing stablecoins, permissioned platforms for institutions, oracle and proof-of-reserves systems for RWAs, and cross-chain settlement and interoperability layers.

Permissionless versus Permissioned Yield-Bearing Architectures

Reflect’s launch of a permissionless system for yield-bearing stablecoins on Solana illustrates the permissionless end of the spectrum. Instead of relying on a custodial operator to allocate reserves, Reflect uses transparent onchain risk models and automated capital deployment to route funds into yield strategies. This approach fits the ethos of DeFi: anyone can deploy a new yield-bearing stablecoin, and risk-management logic is open-source and auditable. However, it also means users must bear smart contract and governance risk, and regulatory classification may be uncertain.

On the other end are permissioned systems designed specifically for institutions. The Solana Institutional Workshop on building a permissioned, yield-bearing money market fund token with Solana’s developer platform speaks directly to this audience. In such designs, only whitelisted institutions can hold or transact the token; KYC and AML checks are enforced at the asset level; and the underlying fund must comply with securities regulations. Yield-bearing tokens issued in this manner function less like DeFi stablecoins and more like modernized fund shares, but they still benefit from 24/7 settlement, programmable compliance, and automated interest accrual.

Between these poles lie hybrid architectures, where base tokens are permissioned but derivatives or wrappers can circulate more freely, or where permissionless usage is allowed up to certain size or risk thresholds. Kaia’s KIP initiative, which aims to bring sustainable capital and institutional-grade yield-bearing products into its ecosystem using TBILL and USDO as core RWA infrastructure, exemplifies how ecosystems can blend institutional-quality assets with permissionless DeFi interfaces.

Data, Oracles, and Proof of Reserves

Data infrastructure is crucial in making yield-bearing assets trustworthy. For RWA-backed tokens and tokenized funds, onchain NAV and proof-of-reserves systems provide transparency into backing and performance. Chainlink’s collaboration with Fidelity International on FILQ, where onchain NAV enables regulated yield-bearing liquidity in 24/7 markets, is one prominent example. Reliable oracles allow tokens like FILQ to integrate with DeFi protocols as collateral or trading pairs, because downstream protocols can trust that the token’s price reflects current NAV.

Proof-of-reserves mechanisms, whether implemented by Chainlink or other providers, similarly underpin trust in stablecoins like USDO and emerging designs like USDu, which has been highlighted for offering full onchain proof of reserves as a yield-bearing stablecoin. In these systems, reserve data from custodians or banks is periodically attested and published onchain, enabling both users and smart contracts to verify that tokens in circulation are fully backed. As more stablecoins and tokenized funds adopt real-time or near-real-time proof-of-reserves, transparency will become a key differentiator between competing yield-bearing offerings.

Analytics platforms such as RWA.xyz complement these primitives by aggregating and visualizing data about yield-bearing RWA tokens, including metrics like assets under management, yields, and collateral composition. The R2USD page on RWA.xyz, for example, describes R2USD as a yield-bearing stablecoin designed to maintain a 1:1 peg while generating sustainable onchain yield, situating it within a broader taxonomy of RWA-backed stablecoins and funds. Such tools help investors and protocols compare products and understand how different yield-bearing designs fit into their risk frameworks.

Interoperability across Chains and TradFi

Finally, interoperability is a defining challenge for yield-bearing assets. Users increasingly expect to move stablecoins, tokenized funds, and yield-bearing tokens across chains and platforms without friction, while institutions aim to integrate these assets into existing payment, settlement, and custody systems. Avalanche’s collaboration with Tassat and Lynq to build real-time settlement rails powered by yield-bearing assets shows how L1 blockchains can serve as neutral infrastructure for institutional flows. On Optimism, Zipangcoin represents the extension of a regulated, yield-bearing commodity token from a domestic Japanese context to a global, EVM-compatible environment.

On Solana, the expanding stablecoin ecosystem and institutional tokenization initiatives highlight a different path: a highly performant L1 designed to host both permissionless DeFi and permissioned yield-bearing fund tokens. On Movement and other newer chains, yield-bearing stablecoins like savUSD are being positioned as core building blocks from day one, ensuring that onchain economies use yield-bearing dollars as their default unit of account. Cross-chain bridges, messaging protocols, and standardized token formats will play a key role in allowing these assets to be used seamlessly across ecosystems.

Interoperability also extends back into TradFi. MetaMask’s partnership with Mastercard and Aave’s yield-bearing mUSD shows how crypto-native tokens can plug into existing card networks, enabling users to spend yield-bearing assets at millions of merchant locations. Plume’s tokenized payroll pilot with WisdomTree and Toku connects employer payroll systems to yield-bearing WTGXX shares, translating traditional HR and payroll operations into onchain flows. As these integrations deepen, the boundary between “crypto” and “traditional finance” will blur further, with yield-bearing tokens serving as the connective tissue.

Conclusion

Yield-bearing assets represent a major evolution in the design of digital money and investment instruments. By embedding the right to income directly into tokens—whether stablecoins, bitcoin wrappers, gold tokens, or tokenized funds—crypto markets are transforming what it means to hold cash, commodities, or blue-chip exposures onchain. Early stablecoins showed that dollars could move at internet speed; yield-bearing stablecoins and tokenized T-bill funds now show that dollars can earn money-market yields while retaining instant, programmable liquidity. DeFi-native yield-bearing tokens push this logic further, encoding lending, staking, and derivatives revenues directly into composable assets that protocols and users can coordinate around.

At the same time, the rise of yield-bearing designs raises complex questions about risk, regulation, and systemic stability. Yield is never free: it is compensation for bearing credit, duration, liquidity, or protocol risk. Products like USDO, R2USD, WTGXX, Zipangcoin, XAUT Earn, Kraken’s Bitcoin Vault, and Aave’s yield-bearing mUSD each embody different trade-offs between transparency, liquidity, and regulatory oversight. The BIS and other authorities have already cautioned that yield-bearing stablecoins and related products can amplify traditional stablecoin risks if their structures are opaque or overly reliant on re-lending and leverage. For users and institutions alike, the essential task is to look beyond headline APYs to the concrete mechanisms of yield generation, redemption, and risk management.

Despite these challenges, the direction of travel is clear. Capital is migrating from idle balances to yield-bearing assets, from opaque offchain vehicles to tokenized funds with onchain NAV and proof of reserves, and from monolithic custodial platforms to a spectrum of permissionless and permissioned architectures. Whether in the form of yield-bearing stablecoins that serve as onchain base money, tokenized Treasury funds used for payroll and treasury management, or gold tokens that finally combine bullion with income, yield-bearing crypto assets are poised to become a foundational layer of the next-generation financial system.

Yield-bearing tokens are typically composable wrappers (ERC-4626 vaults, Pendle PT/YT splits) stacked on top of base collateral protocols — a vulnerability at any layer cascades to all holders.

US legislators face active bank lobbying to classify yield-bearing stablecoins as unregistered securities or deposit-taking instruments, meaning the entire category's legality in the world's largest capital market remains unresolved.

Yield-bearing stablecoins suffered over $1B in outflows in a single episode — the largest since the UST collapse — demonstrating that yield-seekers exit rapidly when rates compress, creating reflexive liquidity spirals.

Funding-rate-dependent yields (USDe and peers) are structurally cyclical: a slump in perpetual funding rates directly cuts the APY that attracted deposits, creating correlated outflow pressure across the entire category simultaneously.

RWA-backed yield (T-bills, tokenized gold) requires trusted custodians and off-chain asset servicers; institutional issuers like BlackRock and Franklin Templeton introduce counterparty and redemption-gate risk absent from native DeFi yield.

Synthetic yield-bearing dollars backed by derivatives (deUSD, USDe) carry basis risk; if the underlying hedge unwinds faster than the protocol can rebalance, the peg breaks before liquidations clear.

Outlook

Over the coming years, yield-bearing will likely shift from a differentiating feature to a default expectation for many categories of onchain assets. As more stablecoin issuers feel competitive pressure from RWA-backed yield-bearing challengers, the gap between what reserves earn and what users receive may narrow. Tokenized money market funds like WTGXX and institutional products like FILQ will expand the menu of regulated, yield-bearing options, while permissionless frameworks such as Reflect and ecosystem-specific initiatives like savUSD on Movement will continue to innovate at the DeFi edge.

Regulatory clarity will be crucial in determining which models achieve scale. Clear distinctions between payment stablecoins, money market-like tokens, and tokenized funds, along with robust rules on disclosure and reserve quality, could unlock broader institutional adoption while protecting retail users. Interoperability across chains and integration with existing payment and settlement networks will further entrench yield-bearing assets at the heart of both crypto and traditional financial flows. For now, the key for market participants is to embrace the opportunities of yield-bearing design while remaining clear-eyed about its risks, building portfolios and products that harness onchain yield without losing sight of the underlying economic realities that generate it.

Latest Yield-Bearing news

Sources

- https://chain.link/article/yield-bearing-stablecoins-explained

- https://www.bis.org/fsi/fsibriefs27.htm

- https://1inch.com/blog/post/what-are-yield-bearing-stablecoins

- https://x.com/TheBlockCo/status/2065307883013652757

- https://support.kraken.com/articles/bitcoin-vault

- https://x.com/BlockworksAdv/article/2062939673652011060

- https://openeden.com/news/openeden-launches-usdo-new-regulated-stablecoin/

- https://openeden.com/news/usdo-settlement-currency-otc-trade-galaxy-digital-defiance-capital/

- https://x.com/chainlink/status/2054532287660765692?lang=en

- https://aave.com/blog/aave-metamask-mastercard

- https://www.prnewswire.com/apac/news-releases/bybit-introduces-yield-bearing-gold-product-offering-apr-on-tokenized-gold-302718722.html

- https://x.com/lista_dao/status/2064982553858068500

- https://www.optimism.io/blog/mitsui-co.-digital-commodities-launches-zipangcoin-on-op-mainnet

- https://app.rwa.xyz/assets/$R2USD

- https://www.helius.dev/blog/solanas-stablecoin-landscape

- https://x.com/centrifuge/status/2061823926867833272

- https://ir.wisdomtree.com/news-events/press-releases/detail/777/wisdomtree-to-launch-247-trading-and-instant-settlement

- https://x.com/SolanaFndn/status/2067016860147548613

Community notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…