Deep explainer on USD Coin (USDC), covering its design, reserves, regulation, multi-chain deployment, DeFi and payment use cases, and key risks, to help crypto readers understand how this dollar stablecoin underpins modern crypto markets.

+27 sources across the wider coverage universe

Circle launches managed USDC settlement for banks, abstracts all crypto complexity across 20+ chains2026-04

Circle launches managed USDC settlement for banks, abstracts all crypto complexity across 20+ chains2026-04 Coinbase acquires Hyperliquid's USDH deployer, Native Markets, to switch All USDH into USDC2026-05

Coinbase acquires Hyperliquid's USDH deployer, Native Markets, to switch All USDH into USDC2026-05 Coinbase adds usage-based pricing to x402 for AI agents as weekly transactions crater 99% from peak2026-04

Coinbase adds usage-based pricing to x402 for AI agents as weekly transactions crater 99% from peak2026-04 Trump-backed World Liberty Financial dismisses liquidation fears over its Dolomite borrowing position, insisting its collateralized loans remain safe despite rising scrutiny2026-04

Trump-backed World Liberty Financial dismisses liquidation fears over its Dolomite borrowing position, insisting its collateralized loans remain safe despite rising scrutiny2026-04 Crypto card usage surges to $600M monthly volume, tripling YoY as stablecoins power everyday payments and reduce reliance on traditional off-ramps2026-04

Crypto card usage surges to $600M monthly volume, tripling YoY as stablecoins power everyday payments and reduce reliance on traditional off-ramps2026-04 MoonPay partners WalletConnect and Ingenico to enable stablecoin payments at retail, using Virtual Accounts for instant fiat settlement at checkout without merchants holding crypto2026-04

MoonPay partners WalletConnect and Ingenico to enable stablecoin payments at retail, using Virtual Accounts for instant fiat settlement at checkout without merchants holding crypto2026-04

USDC Stablecoin: An Evergreen Explainer for Crypto Markets

A dollar-pegged stablecoin issued by Circle, USD Coin (USDC) is designed to track the value of the U.S. dollar on public blockchains, backed by fully reserved fiat assets and short-term U.S. government obligations. It has become one of the core pieces of plumbing in crypto markets, powering trading, DeFi, and increasingly, payments and cross-border finance.

What Is USDC?

USDC sits at the intersection of traditional money and public blockchain infrastructure. It is a digital token that aims to represent a claim on one U.S. dollar held in a reserve of cash and cash-equivalent assets, enabling near-instant settlement across crypto networks while preserving a familiar unit of account. In contrast to volatile cryptocurrencies like bitcoin or ether, USDC belongs to the class of stablecoins, which are designed to minimize price fluctuations by pegging their value to a reference asset such as a fiat currency or commodity. Because USDC is meant to be redeemable 1:1 for U.S. dollars, it functions as a kind of digital cash legible to both crypto-native users and institutions more comfortable with dollar exposure. Importantly, USDC is not a central bank digital currency (CBDC); it is issued by a private company and operates within existing regulatory and banking frameworks rather than being a direct liability of a central bank.

In practice, USDC has evolved into a foundational settlement asset across multiple blockchains and platforms. It is widely used as a quote currency in trading pairs, as collateral in DeFi lending markets, as a base asset for on-chain derivatives, and as a medium for cross-border remittances and business-to-business payments. For many institutions and fintechs, USDC offers a way to access the programmability of public blockchains while maintaining balance sheet exposure in dollars rather than volatile crypto assets. The token’s design, reserve structure, and regulatory posture are therefore central to assessing its role and risks in the broader digital asset ecosystem.

Stablecoins and USDC’s Place in the Landscape

Stablecoins can be grouped into broad categories based on how they attempt to maintain their peg. Fiat-backed stablecoins, like USDC, are backed by off-chain reserves in bank accounts or money market instruments that match or exceed the value of tokens in circulation. Crypto-collateralized stablecoins, like DAI, rely on overcollateralized positions in other cryptocurrencies managed by on-chain protocols, while algorithmic stablecoins have historically attempted to stabilize their price via supply-adjustment rules and related token incentives rather than fully matched reserves. The significant collapses and depegs of algorithmic and partially collateralized stablecoins over the past cycle have sharpened regulatory and market focus on fully reserved, fiat-backed models.

Within this spectrum, USDC has positioned itself as a payment stablecoin: a token explicitly designed for payments, settlements, and low-volatility treasury management, rather than as a speculative vehicle. Circle emphasizes that USDC is backed 100% by cash and short-term U.S. Treasuries or equivalent government obligations, all held in segregated accounts and managed under a regulated money market fund structure for most of the reserve. This makes USDC structurally distinct from unbacked crypto assets, and also from stablecoins backed by a mix of commercial paper or more opaque instruments. Market participants have, in turn, tended to view USDC as one of the more transparent and institutionally oriented dollar stablecoins, even as it remains exposed to conventional financial system risks such as bank failures and sovereign debt markets.

USDC’s prominence has also been reinforced by its deep integration into regulated platforms and infrastructure. Circle describes itself as one of the most widely regulated and licensed stablecoin issuers globally, with USDC and its euro-pegged counterpart EURC issued through regulated entities subject to financial supervision. Major exchanges, trading venues, custodians, and fintech apps treat USDC as a base asset for client balances and on-chain operations, and developers now build directly against Circle APIs and SDKs to embed USDC flows into applications and AI agents. In this sense, USDC is not just a token; it is a gateway between traditional finance, crypto markets, and emerging programmable money use cases.

Origins: Circle, Coinbase, and the CENTRE Consortium

USDC was launched in 2018 as a joint initiative of Circle and Coinbase, two U.S.-based companies that had already established themselves as major players in crypto trading, custody, and brokerage services. The project initially operated under the CENTRE Consortium, a joint venture created by the two firms to define technical and governance standards for fiat tokens on blockchains. CENTRE was imagined as a neutral standards body that could, over time, admit new members and issuers, while maintaining a common specification for compliant dollar tokens, of which USDC was the first implementation.

Circle Internet Financial (often simply “Circle”) has always been the primary issuer and operator behind USDC, even during the CENTRE era. Coinbase served as a strategic partner, distribution channel, and co-governor, integrating USDC into its exchange, wallet, and custody products and helping promote USDC as a compliant alternative to other stablecoins for U.S. and European customers. Over time, governance evolved, with Circle assuming more direct stewardship of USDC’s issuance and governance while maintaining close commercial and technical ties with Coinbase. Coinbase continues to be one of the largest platforms for USDC trading, offering USDC-denominated pairs and incentives such as USDC rewards on balances in certain jurisdictions.

From the outset, USDC’s architecture was designed to be multi-chain and programmable. The initial token launched on Ethereum as an ERC‑20 asset, but the specification anticipated deployment to additional smart contract platforms and later to non-EVM architectures. Circle’s approach was to issue native USDC on each supported chain, backed by the same unified reserve, rather than relying solely on third-party bridging or wrapped representations. This multi-chain strategy, combined with a regulated reserve structure, positioned USDC as a candidate for both institutional adoption and deep integration into DeFi protocols across ecosystems.

How USDC Works: Issuance, Redemption, and the Dollar Peg

At its core, USDC is a tokenized representation of dollars held in off-chain reserves. Customers who have passed Circle’s KYC and compliance checks can deposit U.S. dollars with Circle or approved partners; Circle then mints an equivalent amount of USDC on the requested blockchain and credits it to the customer’s address. When a customer redeems, Circle burns the corresponding USDC tokens and wires out fiat dollars, keeping the total supply of USDC in circulation matched to the value of reserve assets, net of any operational timing differences. This mint–burn mechanism is the primary tool for maintaining the 1:1 peg between USDC and the dollar.

Price stability is enforced not by a formal peg in the central bank sense but by arbitrage and redemption. If USDC trades meaningfully below \(1\) U.S. dollar on exchanges, arbitrageurs can profit by buying USDC cheaply in secondary markets, redeeming it for full-value dollars from Circle, and pocketing the difference. Conversely, if USDC trades above \(1\) dollar, arbitrageurs can obtain new USDC from Circle at par, sell it on exchanges at a premium, and drive the price back down toward the peg. This dynamic depends critically on the credibility of Circle’s promise to redeem at par, the liquidity of secondary markets, and the efficiency of arbitrage across geographies and trading venues.

The reserve composition and transparency regime play a central role in buttressing this credibility. Circle emphasizes that USDC is backed 100% by highly liquid cash and cash-equivalent assets, mainly U.S. dollar deposits and short-dated U.S. Treasury securities held in a regulated government money market fund. The company publishes detailed reserve breakdowns and has structured the majority of the reserve within the Circle Reserve Fund (ticker: USDXX), an SEC-registered Rule 2a‑7 government money market fund managed by BlackRock, which can hold cash, short-term Treasuries, and overnight Treasury repurchase agreements. The remainder of the reserve is held as cash deposits at a small number of large, globally active banks with high capital and liquidity requirements. These design choices aim to ensure that USDC can meet redemption requests even under stress, while minimizing credit and liquidity risk relative to more complex or opaque portfolios.

Starknet adds shielded USDC balances and private transfers through STRK20, with Ready and XVerse integrations

Starknet says STRK20 now gives USDC on Starknet shielded balances, private transfers, and unshielding back into normal ERC-20 flow without creating a second token or changing the token contract. Private transfers hide asset type, amount, and wallets using ZK proofs, with fixed per-tx fees instead of percentage tolls. Ready and XVerse are the first integrations for confidential USDC swaps, while scoped viewing keys give regulators a legal audit path without exposing the whole pool.

Readers click USDC stories not to monitor its dollar peg, but to track whether it will remain the default DeFi settlement layer — yield-bearing rivals, chain-access restrictions, and institutional reserve moves all register as threats to that utility moat, not just product news.↗

Reserves, Transparency, and Risk Profile

The reserve structure behind USDC is a key differentiator among stablecoins and a central subject of regulatory and academic scrutiny. Unlike bank deposits, USDC balances are not insured by agencies like the FDIC or covered by deposit guarantee schemes; instead, user confidence rests on the segregation, quality, and transparency of reserve assets, as well as on Circle’s operational and legal practices. As USDC has scaled into a tens-of-billions-of-dollars instrument used across sectors, the composition of its backing and the robustness of its disclosure regime have become systemic considerations for parts of the crypto ecosystem.

USDC’s reserve strategy can be understood in three layers. The first is the asset layer, which defines what instruments are eligible as backing; the second is the structural layer, which determines how those assets are legally held, segregated, and custodied; and the third is the disclosure layer, which dictates how often and how granularly information about the reserve is published. Each of these layers influences the nature of risk USDC holders ultimately bear, ranging from credit and interest rate risk to liquidity, legal, and operational risk.

Reserve Composition and Custody

Circle discloses that the USDC reserve is composed entirely of U.S. dollar cash and short-dated U.S. government obligations or equivalent, with no exposure to commercial paper, corporate credit, or longer-duration securities. The largest portion of this reserve is invested in the Circle Reserve Fund, an SEC‑registered Rule 2a‑7 government money market fund, whose portfolio is restricted to cash, U.S. Treasuries, and overnight repurchase agreements backed by U.S. government collateral. Rule 2a‑7 imposes strict requirements on maturity, credit quality, diversification, and liquidity, implying that the fund holds very low-risk, highly liquid instruments suitable for daily redemptions. By embedding most of the USDC backing into this kind of fund, Circle aims to align USDC’s risk profile with that of high-quality money market shares rather than traditional bank deposits or unsecured corporate bonds.

The remainder of the reserve is held in cash deposits at a set of large, regulated banking partners that meet high capital and liquidity standards. These deposits are kept separate from Circle’s operational funds and are held for the benefit of USDC holders rather than as general corporate assets. According to Circle, USDC reserves are maintained in custody and management arrangements with leading U.S. financial institutions, including BlackRock as the investment manager of the Reserve Fund and BNY Mellon as a primary custodian. This design spreads reserve assets across both the banking system and the U.S. Treasury market, diversifying the sources of liquidity available to meet redemptions under various stress scenarios.

From a risk standpoint, this composition substantially reduces credit risk relative to stablecoins that invest reserves in commercial paper or other unsecured corporate obligations. However, it does not eliminate exposure to sovereign risk or interest rate risk, as the value of Treasury securities can move with yields, and U.S. government creditworthiness remains a nonzero risk factor, however remote. Moreover, cash deposits in commercial banks remain subject to bank failure and resolution risk, as highlighted by the collapse of Silicon Valley Bank in 2023, which temporarily impaired a portion of USDC’s reserves and triggered a depeg event. USDC’s reserve choices thus reflect a trade-off: a strong bias toward liquid, high-quality assets, but still within the envelope of conventional financial system vulnerabilities.

Transparency, Attestations, and Regulation

Transparency is central to Circle’s attempt to differentiate USDC from less-disclosed stablecoins and to satisfy regulatory expectations for payment instruments. Circle publishes regular reports on USDC reserves, including the total supply of tokens outstanding, the value and composition of backing assets, and the structure of the Circle Reserve Fund. These reports are based on attestations performed by independent accounting firms, which verify that the value of reserve assets at a given date meets or exceeds the value of USDC in circulation. While attestations are not the same as full financial audits, they provide periodic third-party confirmation that the reserve is appropriately sized and invested within disclosed parameters.

Circle also emphasizes its status as a regulated financial entity. The company notes that it is “one of the most widely regulated and licensed stablecoin issuers in the world,” operating under money transmission, e‑money, or equivalent licenses in multiple jurisdictions. Its issuance entities are subject to ongoing supervision by U.S. and international regulators, and its reserve fund is registered under the U.S. Investment Company Act with the Securities and Exchange Commission. These layers of oversight are meant to align USDC with emerging categories like “payment stablecoins,” which lawmakers increasingly view as akin to narrow banks or specialized payment institutions rather than unregulated investment schemes.

However, the regulatory regime for stablecoins remains in flux, particularly in the United States. Proposals such as the GENIUS Act (Guaranteed Electronic Notes for Instant Unified Stability) aim to create a comprehensive framework for payment stablecoin issuers, imposing requirements on reserve quality, redemption rights, governance, and supervisory arrangements. Brookings and other policy analysts have highlighted the need for such rules to mitigate run risk, protect consumers, and limit systemic contagion in the event of issuer distress or reserve asset shocks. As USDC scales, its alignment with these emerging standards—and the evolution of its regulatory treatment—will materially affect its risk profile and competitive positioning.

Stress Events: Silicon Valley Bank and Depeg Dynamics

The failure of Silicon Valley Bank (SVB) in March 2023 serves as a case study in how traditional banking stress can transmit into stablecoin markets. SVB entered resolution after experiencing over \(40\) billion dollars in withdrawal requests, and a portion of USDC’s cash reserves was held at the bank when it failed. When Circle disclosed that roughly \(3.3\) billion dollars of its then-reserve were temporarily stranded at SVB, markets reacted sharply, with USDC’s price on secondary venues falling significantly below \(\$1\) amid uncertainty over the recoverability of those funds. This episode effectively created a run on USDC, not because Circle had changed its redemption rules, but because participants doubted whether the backing remained fully intact.

Ultimately, U.S. authorities guaranteed all SVB deposits, including uninsured balances, and Circle confirmed that no USDC holders would suffer losses, enabling the token’s price to re-converge to the dollar peg. The speed of the recovery highlighted both the effectiveness of the underlying arbitrage mechanism once solvency was restored and the degree to which USDC’s stability depends on the broader regulatory and lender-of-last-resort framework backing the U.S. banking system. It also underscored the fact that even a fully reserved, highly transparent stablecoin can experience severe short-term deviations from its peg when confidence in the underlying reserves is shaken.

For regulators and market participants, the SVB event reinforced two key lessons. First, reserve concentration in a small number of banks can create vulnerabilities even when the overall reserve portfolio is conservative. Second, stablecoin users effectively bear credit and resolution risk of the banks and sovereigns holding their reserves, even if indirectly. Circle’s subsequent adjustments in bank partners and reserve allocation have sought to mitigate these risks, but the episode remains a seminal moment in USDC’s history and a template for assessing future stress scenarios involving banks, money market funds, or Treasury market disruptions.

Comparative Profile: USDC and Other Major Stablecoins

To situate USDC within the broader stablecoin market, it is useful to compare its design with other large tokens such as Tether (USDT) and DAI. While specific numbers fluctuate, data from aggregators like DeFiLlama and market trackers show that USDC ranks among the largest stablecoins by circulating supply, with a market capitalization around the mid‑\(70\) billion dollar range, similar in scale to USDT and exceeding most other alternatives. Yet the way each of these tokens achieves stability differs materially.

The following table summarizes key contrasts among three prominent stablecoins.

| Feature | USDC | USDT | DAI |

|---|---|---|---|

| Primary issuer / governor | Circle Internet Financial | Tether Limited | MakerDAO protocol (decentralized) |

| Backing model | Fiat-backed, cash and short-term U.S. Treasuries | Fiat-backed with mixed asset portfolio (fiat, bonds, others) | Overcollateralized crypto and tokenized real-world assets |

| Transparency | Regular reserve breakdowns and attestations | Periodic attestations, less granular disclosure | On-chain visibility into collateral positions |

| Regulatory posture | Payment stablecoin issuer under multiple licenses | Offshore issuer, varied oversight | DAO-governed protocol interacting with multiple regimes |

| Typical use | Payments, DeFi collateral, institutional settlement | Trading liquidity, offshore markets | DeFi-native collateral and savings |

The table highlights that USDC and USDT share a fiat-backed structure but diverge in transparency and regulatory positioning, with USDC emphasizing its alignment with regulated money markets and public reserve reporting. DAI, by contrast, is issued by a decentralized protocol, backed primarily by other crypto assets and some tokenized real-world collateral, and depends on overcollateralization and automatic liquidation mechanisms rather than redeemability at par from a centralized issuer. These differences mean that stablecoins are not interchangeable from a risk perspective, even if they all aim to track the same dollar benchmark.

For traders, protocols, and institutional users, the choice among these tokens often reflects trade-offs between regulatory comfort, decentralization, yield opportunities, and liquidity depth. USDC’s value proposition centers on its perceived regulatory credibility and integration into payment and financial infrastructure, while still maintaining the composability and interoperability of an on-chain asset. However, as later sections discuss, holding or using USDC still entails important risks, especially when it is deployed within DeFi protocols or wrapped through third-party bridges.

USDC in Crypto Markets and DeFi

As crypto markets have matured, USDC has evolved from a niche trading tool into a core settlement asset across centralized exchanges, decentralized finance platforms, and institutional trading desks. Its role is analogous to that of U.S. dollars in traditional financial markets: a base currency for quoting prices, a neutral collateral asset for leveraged positions, and a store of value for traders who wish to step out of volatility without fully exiting into the banking system. Because USDC lives on-chain and can be transferred 24/7, it also supports strategies and protocols that require real-time collateral movements, margining, and automated liquidity provisioning.

In DeFi, USDC has become one of the most widely used stablecoins for lending, liquidity pools, and yield strategies. Many protocols treat USDC as the default “risk-free” leg for yield-bearing vaults and as a primary collateral asset against which users can borrow volatile tokens. However, this ubiquity also means that stresses in USDC markets, or in the protocols where it is deployed, can propagate through the DeFi ecosystem, amplifying volatility or triggering liquidations when things go wrong.

Market Capitalization, Trading Pairs, and Liquidity

Market capitalization figures provide a first approximation of USDC’s footprint. Data from TradingView and DeFiLlama indicate that USDC’s circulating supply translates into a market cap around \$75 billion, making it one of the two largest dollar stablecoins by value alongside USDT. Stablecoins as a whole represent a substantial share of the crypto market’s aggregate capitalization, and USDC accounts for a significant fraction of that pool, especially on regulated and DeFi platforms. While these numbers fluctuate with issuance and redemptions, they underscore that decisions around USDC’s reserve management, regulatory status, or cross-chain deployments can affect liquidity conditions across multiple ecosystems.

On centralized exchanges (CEXs), USDC appears both as a quote currency and as a base asset for settlement. Major platforms like Coinbase, Kraken, and Binance list USDC trading pairs against bitcoin, ether, and numerous altcoins, enabling users to express price views or hedge positions while holding a synthetic dollar. Some exchanges have integrated USDC into advanced products: Coinbase, for example, allows U.S. traders on its advanced platform to hold USDC balances as dry powder for fractional stock and ETF trading, earning rewards on idle USDC through subscription services such as Coinbase One in some jurisdictions. Other venues use USDC as collateral for perpetual futures or as the settlement currency for margin products, marking P&L in USDC instead of in volatile crypto or fiat.

In decentralized exchanges (DEXs) and automated market makers, USDC is frequently one side of liquidity pools, paired against volatile tokens or other stablecoins. Using USDC in such pools allows LPs to earn trading fees while retaining one leg of their liquidity in a dollar-denominated asset, reducing directional exposure. Deep USDC liquidity pools also form the backbone of cross-asset routing on DEX aggregators, allowing traders to swap thousands of tokens indirectly via intermediate trades through USDC pairs. When centralized players like Kraken extend interfaces that tap into on-chain DEX liquidity, they often route user orders through USD and USDC rails, giving USDC an additional role as the bridge currency between CeFi and DeFi.

USDC on Centralized Platforms: Credit and Yield Products

Beyond spot trading, centralized platforms have built credit and yield products around USDC. Coinbase, for instance, offers the ability for certain customers to borrow USDC against crypto collateral like bitcoin or ether, with borrowing limits extending into the millions of dollars depending on collateralization levels. This effectively turns USDC into a synthetic dollar credit line for users who wish to access liquidity without selling their underlying assets, similar in spirit to securities-backed lending in traditional finance. Interest rates, margin requirements, and liquidation rules vary by platform, but the common thread is that USDC serves as the accessible, on-chain form of loan proceeds.

Some platforms also offer yield on USDC balances, sharing a portion of interest earned on underlying reserves or using user balances in low-risk lending or market-making strategies. Coinbase’s advanced trading offering, for example, has advertised that users can earn up to a few percentage points annually on USDC held in specific account types, subject to jurisdictional availability and program terms. While such yields are modest compared to speculative DeFi returns, they reflect a blurring of lines between traditional savings products and on-chain stablecoin holdings, with USDC acting as the underlying asset.

Rewards and incentives further cement USDC’s presence on CEXs. Trading competitions, loyalty programs, and promotional campaigns frequently denominate rewards in USDC, reinforcing its role as a neutral prize currency that winners can either hold, trade for other assets, or withdraw to external wallets. This has been evident in various exchange contests involving niche tokens where the prize pool is allocated in USDC rather than in the promoted asset, highlighting that even in speculative campaigns, the stablecoin plays the role of “hard” money that participants ultimately care about.

USDC in DeFi Lending, Yield, and Derivatives

In DeFi, USDC is deeply woven into lending markets, yield strategies, and derivatives protocols. Lending platforms typically allow users to deposit USDC to earn interest from borrowers who use the stablecoin as collateral or as loan currency, enabling both leveraged long and short positions on other assets. Because USDC is widely considered one of the more conservative stablecoin holdings, many protocols treat it as top-tier collateral, giving it favorable risk parameters such as higher borrowing limits and lower haircuts compared to more volatile or less transparent tokens.

Yield aggregation strategies frequently revolve around USDC as the base asset. Vaults built on top of lending protocols, automated market makers, and structured products direct USDC deposits into diversified or actively managed strategies, promising optimized yields while abstracting away the complexity of underlying protocols. In some cases, these strategies now incorporate confidential USDC positions, where technologies such as homomorphic encryption allow deposits and yield accruals to be encrypted even while the strategy operates on-chain. Recent launches of confidential USDC yield vaults on Ethereum, powered by collaborations between cryptography teams and DeFi protocols, aim to give institutions a way to earn on USDC without revealing position sizes or strategy allocations publicly.

Derivatives protocols also rely heavily on USDC. Perpetual futures exchanges, both centralized and on-chain, commonly margin and settle trades in USDC to minimize volatility in margin requirements and to make P&L accounting straightforward for users who think in dollar terms. Options protocols may use USDC as collateral for selling options or as the quote currency for option premiums, allowing sophisticated strategies around volatility and yield. Structured products like range-bound notes or principal-protected strategies are often built with USDC as the underlying funding asset, with returns paid in USDC upon maturity if certain conditions are met.

This deep integration, however, can magnify systemic risk. When leveraged positions are funded by USDC loans, sharp moves in underlying asset prices can trigger mass liquidations, forcing protocols to sell collateral rapidly and potentially stressing USDC liquidity pools. Overly aggressive assumptions about USDC’s “risk-free” nature can also lead to fragile constructions. A recent example in the broader DeFi landscape involved a separate stablecoin that lost over eighty percent of its value after its primary yield market, paired against USDC, reached full utilization amid liquidity fears. This episode illustrated how dependence on USDC liquidity and on-chain credit markets can create feedback loops that destabilize other tokens, even if USDC itself remains near its peg.

Case Studies: Whales, Exploits, and Confidential Positions

The ubiquity of USDC in DeFi is reflected not only in legitimate strategies but also in adversarial behavior. Protocol exploiters frequently convert stolen tokens into USDC soon after an attack, using deep liquidity pools to lock in the dollar value of their haul and reduce exposure to market moves while they attempt to launder or bridge funds. This pattern underscores both USDC’s efficiency as a store of value in crypto-native terms and the ongoing challenges in tracing and recovering funds once they have been transformed into liquid, widely accepted stablecoins.

Large individual traders—or “whales”—also rely heavily on USDC as a base asset for directional bets. It is not uncommon to see on-chain positions where tens of millions of USDC are deployed to purchase large blocks of tokens such as SOL, either through spot markets or through leveraged instruments. These trades use USDC as the funding currency, with the trader’s P&L effectively denominated in dollars even though the exposure is to volatile tokens. This dynamic reinforces USDC’s role as the de facto cash leg in on-chain speculation, analogous to institutional investors using dollars or Treasuries as the starting point for risk-taking in traditional markets.

At the same time, emerging privacy technologies are beginning to change how visible USDC positions are on-chain. Confidential USDC constructs—often denoted informally as cUSDC—allow institutions to maintain USDC-denominated exposure within encrypted smart contracts. Under such designs, the protocol can compute interest, liquidations, and strategy outcomes on ciphertexts, while external observers cannot see individual balances or flows. Collaborative initiatives between cryptography projects and DeFi protocols have recently launched the first such confidential USDC yield venues, offering a way for institutions to participate in DeFi while mitigating concerns about revealing trading strategies or balance sheet exposures. This trend suggests that USDC will increasingly exist across both transparent and privacy-preserving layers of the on-chain economy.

Circle and Nomura target $440B-a-day Japan FX market with USDC settlement by 2027

Circle and Nomura plan to launch USDC-based settlement and corporate payment rails in Japan as early as 2027, letting businesses swap yen into dollar stablecoins for cross-border payments and FX settlement. The target is Japan’s $440B-a-day foreign exchange market, where legacy bank transfers can still take two to three business days. Nomura handles client onboarding, compliance and bank integrations, while Circle gets a credible TradFi path into Japan after local rules cleared USDC for corporate use.

- 01yield-bearing USDC alternatives↗

Coinbase's 4% yield offer, Leshner's USTB, Ethena's BlackRock-backed USDtb, and USUAL all drew heavy clicks because readers see idle USDC as an opportunity cost problem actively being solved by competitors.

- 02USDC as DeFi liquidity anchor↗

Curve gauge votes for RLUSD/USDC, crvUSD PegKeeper additions, and Arbitrum Orbit gas-token support show readers tracking USDC's structural role as the settlement rail inside DeFi protocols.

- 03cross-chain access fragmentation↗

Binance dropping USDC TRC20 withdrawals and Wormhole enabling native multi-network stablecoin transfers signal that which chains USDC is natively available on is a live competitive battleground.

- 04institutional reserve management↗

Circle restarting Treasury purchases through its BlackRock-managed fund and Deutsche Bank conducting stablecoin swaps on UDPN drew clicks because readers see reserve composition as a systemic risk signal, not just a compliance footnote.

- 05CeFi collapse USDC redemptions↗

BlockFi creditor repayments via Coinbase and Hotbit's halt attracted readers watching whether USDC fulfills its promise as a stable exit asset when centralized platforms fail.

- 06retail onboarding via USDC promotions↗

Uniswap's Robinhood in-app integration with a $10 USDC incentive and the MetaMask Mastercard card reveal readers tracking USDC's role as the on-ramp token for new users entering DeFi.

USDC for Payments, Remittances, and Real-World Use

Although USDC emerged from trading and DeFi, its issuers and partners now emphasize its role in payments, cross-border transfers, and real-world commerce. Circle describes USDC as a “digital dollar” designed for rapid global payments and 24/7 financial markets, highlighting use cases ranging from business treasury management to remittances and humanitarian payouts. In practice, this means USDC is increasingly used not only inside the crypto ecosystem but also as a settlement medium between fintechs, merchants, creators, and end-users who may not think of themselves as “crypto traders” at all.

USDC’s potential advantages in this domain stem from its combination of dollar stability, near-instant settlement, and programmability. Transactions can be executed cross-border in minutes rather than days, often with lower fees than traditional correspondent banking arrangements, while smart contracts allow conditional or recurring payments to be automated. At the same time, integration with card networks, banking APIs, and consumer interfaces is needed to make USDC usable by non-technical users—a challenge that many fintechs and platforms are now actively addressing.

Global Access to Dollars and Humanitarian Uses

One of the most prominent narratives around USDC is its role in providing global access to dollars, particularly in regions with unstable local currencies or restrictive capital controls. Circle’s own reporting on the “state of the USDC economy” notes that a substantial portion of USDC usage today relates to accessing dollars, transacting in digital asset markets, and enabling payments and humanitarian aid. For individuals and businesses in emerging markets, holding USDC can be a way to gain synthetic exposure to the U.S. dollar using only a smartphone and an internet connection, bypassing local banking frictions.

This functionality has been leveraged by NGOs and humanitarian organizations in crisis zones. Stablecoins like USDC offer a way to distribute aid quickly, transparently, and with reduced leakage, converting into local currency only when needed. In some pilots, recipients have been able to receive USDC directly in wallets, then cash out through local exchanges or spend with merchants that accept crypto, reducing reliance on slow or corrupt intermediaries. While such programs face challenges around compliance, education, and fraud prevention, they illustrate how USDC’s design is compatible with mission-driven applications beyond trading.

BCRemit, a remittance-focused company, provides a concrete example of how USDC is used in cross-border payments infrastructure. The firm has integrated USDC into its backend to optimize remittance flows, using the stablecoin as a bridge asset to move value rapidly across borders before converting into local currencies on arrival. This approach allows BCRemit to benefit from 24/7 on-chain settlement, potentially lower liquidity costs, and improved transparency, while shielding end-users from the complexity of blockchain interactions. By keeping USDC largely behind the scenes, the company preserves a familiar user experience while tapping into the efficiency of digital dollars.

Merchant Payments, Digital Art, and Consumer Interfaces

On the merchant side, USDC is beginning to act as a settlement asset for online marketplaces, creators, and digital goods platforms. Some digital art and NFT marketplaces now allow artists to list works denominated in USDC while giving buyers the option to pay via debit or credit cards, Apple Pay, or Google Pay. Under the hood, the platform handles conversions and settlements so that creators receive USDC, while collectors can transact using traditional payment methods if they prefer. This hybrid approach makes it easier for non-crypto-native users to participate, while still anchoring the ecosystem in a stable, programmable digital currency.

Such integrations highlight USDC’s role as a bridge between card networks and on-chain assets. By pricing goods and services directly in USDC, platforms can standardize on a single unit of account across geographies, even if users pay in different fiat currencies. Payment processors can convert incoming card payments into USDC in real time, settle with merchants on-chain, and use smart contracts to automate royalties, revenue sharing, or escrow arrangements. For international marketplaces, this can reduce FX complexity and settlement delays compared to accepting many local currencies.

At the same time, card-based USDC products are subject to traditional financial system constraints and regulatory decisions. Some users have experienced disruptions when card programs tied to USDC changed issuers or adjusted their geographic coverage, leading to sudden cutoffs outside certain regions. These episodes underscore that while USDC itself is blockchain-native and globally transferable, consumer-facing access channels like cards and bank integrations remain bound by jurisdictional regulations, compliance requirements, and commercial arrangements.

Micropayments, AI Agents, and Machine-to-Machine Commerce

A growing frontier for USDC lies in micropayments and machine-to-machine transactions, particularly in the context of AI agents and content delivery. The economics of small online payments have historically been constrained by card fees and banking infrastructure, making pay-per-request or pay-per-API-call models difficult to sustain at scale. Public blockchains and stablecoins, by contrast, enable tiny, programmable transfers that can be settled globally with minimal overhead.

Circle has explicitly targeted this space through its developer platform, which supports “nanopayments” that allow USDC transfers as small as \(0.000001\) units for AI agents and new application experiences. Developers can use Circle’s APIs and smart contract tooling to create agents that hold USDC-funded wallets, discover services, and pay for access to APIs or computational resources on the fly. Circle’s Agent Stack demo, for example, shows how an AI agent can automatically create a USDC-funded wallet, locate services in a marketplace, and pay for API requests through a dedicated gateway, orchestrating complex workflows with real economic stakes. This model envisions a future where autonomous software interacts economically with other services using USDC as a native currency.

Similar ideas are being explored on layer‑1 networks focused on high throughput and low fees. On Solana, for instance, infrastructure has emerged that lets content publishers charge per-request fees for API calls or AI-generated content, receiving payments in USDC instead of relying on traditional advertising or subscriptions. Rather than blocking bot traffic, publishers can set granular prices and let automated clients pay in stablecoins, enabling new monetization models for AI-heavy workloads. In such designs, USDC’s stability and composability make it a natural settlement medium for microtransactions between machines and services, potentially unlocking revenue streams that were uneconomical with legacy payment rails.

Cards, Credit, and Yield: Consumer and Treasury Use

USDC also plays a role in consumer and corporate credit-like products. Platforms such as Coinbase allow users to borrow USDC against staked assets like ETH or SOL, providing liquidity without sacrificing staking rewards or triggering taxable disposals in certain jurisdictions. Borrowers can receive USDC directly into their wallets, use it for trading or spending, and repay loans according to platform-specific terms, with automated liquidation protecting lenders if collateral values fall too far. This arrangement mirrors margin and securities-backed credit in traditional finance but conducted entirely on-chain using USDC as the loan currency.

On the treasury side, businesses hold USDC as a dollar-denominated asset in their corporate wallets, sometimes earning yield either directly from Circle’s reserve structure or indirectly via third-party programs. Circle reports that many enterprises use USDC as part of their working capital stack, particularly those with large on-chain operations or frequent cross-border obligations. In some markets, fintech apps provide retail users with access to USDC-denominated savings, framing it as a way to access dollar stability and yield compared with local bank deposits. These models raise regulatory questions about securities law, deposit-taking, and consumer protection, which lawmakers are only beginning to address systematically.

At the same time, USDC has become a common reward currency for loyalty and engagement programs. Exchanges, NFT platforms, and DeFi projects offer USDC as a prize for trading competitions, educational campaigns, or community events, leveraging its neutrality and immediate liquidity. This stands in contrast to earlier phases of crypto, where rewards were often denominated in volatile native tokens whose value could quickly diverge from users’ expectations. By paying in USDC, platforms effectively treat stablecoins as the “cash” of the crypto world, even as they promote other tokens and ecosystems.

USDC Across Blockchains and Bridging

From a technical standpoint, one of USDC’s distinctive features is its multi-chain footprint. Rather than existing solely as an ERC‑20 token on Ethereum, USDC is natively issued on dozens of blockchains, with Circle noting support for 34 networks and counting. This broad deployment aims to put a canonical, fiat-backed stablecoin wherever developers and users are building, while minimizing fragmentation into unofficial or wrapped variants. A separate ecosystem of bridges, canonical transfer protocols, and interoperability layers has grown up around USDC to move it safely between chains.

However, the multi-chain reality also introduces complexity and risk. Different versions of “USDC” may exist on the same chain—some natively issued by Circle, others minted by third-party bridges that lock native USDC on a source chain and issue a wrapped representation on the destination. Users must distinguish between these assets, as only the native version is directly redeemable with Circle, while wrapped versions depend on the security and solvency of the bridge smart contracts and operators.

Native Multi-Chain USDC

Circle’s multi-chain USDC strategy involves deploying native USDC tokens on supported blockchains, each backed by the same central reserve. On EVM-compatible networks, USDC is typically implemented via a smart contract controlled by Circle or its designated administrative entities, enforcing mint and burn operations tied to off-chain deposits and redemptions. On non-EVM platforms, USDC is integrated using that chain’s native token standards, again under Circle’s issuance and redemption control. In each case, the total USD value of all native USDC tokens across chains is matched by the consolidated reserve held in cash and Treasuries.

Circle emphasizes that for 34 blockchain networks, USDC is natively supported, meaning that token holders can be confident they are dealing with an official, directly redeemable representation rather than a wrapped derivative. The company’s partnerships with large custodians and asset managers, such as BlackRock and BNY Mellon, underpin this multi-chain issuance by providing robust custody and investment management for the underlying assets supporting USDC on each network. Developers building on these chains can rely on a uniform set of semantics around transfers, approvals, and interactions, even as the underlying consensus mechanisms and virtual machines differ.

The proliferation of blockchains—over 160 tracked by developer platforms such as Alchemy—means that USDC does not exist on every network where users might want a stablecoin. Nonetheless, Circle’s strategy has been to prioritize chains with significant developer activity, DeFi ecosystems, or institutional interest, including major layer‑1s, Ethereum layer‑2s, and specialized ecosystems like Solana and Base. This has led to a patchwork landscape in which some chains enjoy native USDC liquidity, while others rely primarily on bridged or synthetic representations.

Bridged vs Native USDC and Canonical Transfers

Because USDC is native on multiple chains, moving it between them can be handled either by third-party bridges or by Circle’s own canonical mechanisms. Historically, many users used generic cross-chain bridges that locked USDC on one chain and minted wrapped “USDC” on another, creating assets whose redemption depends on the bridge rather than on Circle. These wrapped tokens often share the USDC ticker but are technically distinct, and they can trade at a discount if confidence in the bridge erodes or if liquidity is limited.

To address these challenges, Circle has developed canonical cross-chain transfer protocols that aim to treat USDC as a single multi-chain asset, burned on the source chain and minted on the destination while keeping total supply constant. Although the details vary by implementation, the core idea is to avoid the proliferation of unredeemable synthetic variants and to provide a more reliable way to move value across ecosystems. Recent integrations with networks such as Stellar illustrate how new chains are onboarded into this canonical transfer framework, with developers needing to understand address formats, forwarding contracts, and other specifics before moving USDC to or from those chains.

Despite these advances, third-party bridges remain deeply embedded in the DeFi landscape, and users often interact with wrapped USDC without realizing it. This can lead to surprises when bridges sunset support or restructure. For example, some projects have announced the end of bridging services across many networks, preserving the backing of their tokens but requiring users to perform on-chain recovery steps—such as burning tokens on a source chain and paying a flat USDC fee on a primary chain—to reclaim underlying assets. In these scenarios, USDC serves not only as a bridge asset but also as the fee currency for post-sunset asset recovery, highlighting its role as a neutral settlement medium even in wind-down processes.

Network-Specific Ecosystems: Ethereum, Solana, Base, and Beyond

USDC’s usage varies considerably across networks. On Ethereum mainnet, USDC is central to DeFi protocols, institutional settlement, and high-value transfers, benefiting from Ethereum’s security and composability at the cost of relatively high transaction fees. Many lending, derivatives, and structured product protocols on Ethereum treat USDC as a primary base asset, and institutional DeFi experiments often begin on Ethereum where infrastructure and tooling are mature.

On high-throughput chains like Solana, USDC is deeply integrated into DEXs, payments, and novel applications such as AI content monetization. Solana-based initiatives have demonstrated how publishers can charge per-request fees for API or AI interactions, collecting USDC as compensation without relying on traditional ad-based models. In parallel, centralized exchanges like Kraken have expanded their support for Solana-native DEX trading, enabling users to access on-chain tokens via their main exchange interface while settling in USD or USDC. This effectively connects retail and institutional users to Solana’s DeFi ecosystem through familiar fiat and stablecoin rails.

Layer‑2 networks and app chains, such as Base, also use USDC as core liquidity and incentive currency. Bridging solutions have brought assets like SOL and liquid-staked tokens such as jitoSOL onto these networks, where liquidity providers can receive USDC-denominated incentives across DEXs and yield platforms. These incentives reflect a trend: USDC functions as the default reward and subsidy token even for ecosystems where the core assets are not dollar-denominated, because it gives participants a predictable, stable payoff regardless of underlying token volatility.

Bridge Sunsets, Recovery Fees, and User Exposures

The complexity of the multi-chain environment has led some projects to rationalize or sunset support for certain networks. Restaking projects and synthetic asset platforms, for instance, have announced timelines for sunsetting their presence on long-tail chains, instructing users to bridge or burn tokens back to primary networks within specified windows. After such deadlines, they may require users to perform manual recovery procedures involving on-chain burns and the payment of flat USDC fees on a central chain to reclaim wrapped tokens or collateral. These fees are typically intended to cover operational costs and gas for consolidating positions and processing redemptions.

While such processes generally preserve the backing of tokens and are communicated in advance, they create a challenging user experience and highlight the importance of understanding which version of an asset one holds. For USDC itself, the key question is whether a token is native to the chain and redeemable with Circle, or whether it is a synthetic representation that carries additional bridge and protocol risk. The proliferation of wrapped assets, sunset announcements, and ad hoc recovery mechanisms underscores that “USDC on X chain” may not always mean the same thing, and that users must pay attention to contract addresses, issuer documentation, and protocol communications.

From a risk management perspective, these episodes show that multi-chain deployments can create operational risk and user confusion, even when the underlying stablecoin is well-backed and conservatively managed. They also illustrate USDC’s role as a kind of “meta-currency” within the crypto ecosystem: not only is it used for everyday transfers and DeFi strategies, but it also becomes the fee and settlement currency for resolving cross-chain migration and deprecation events.

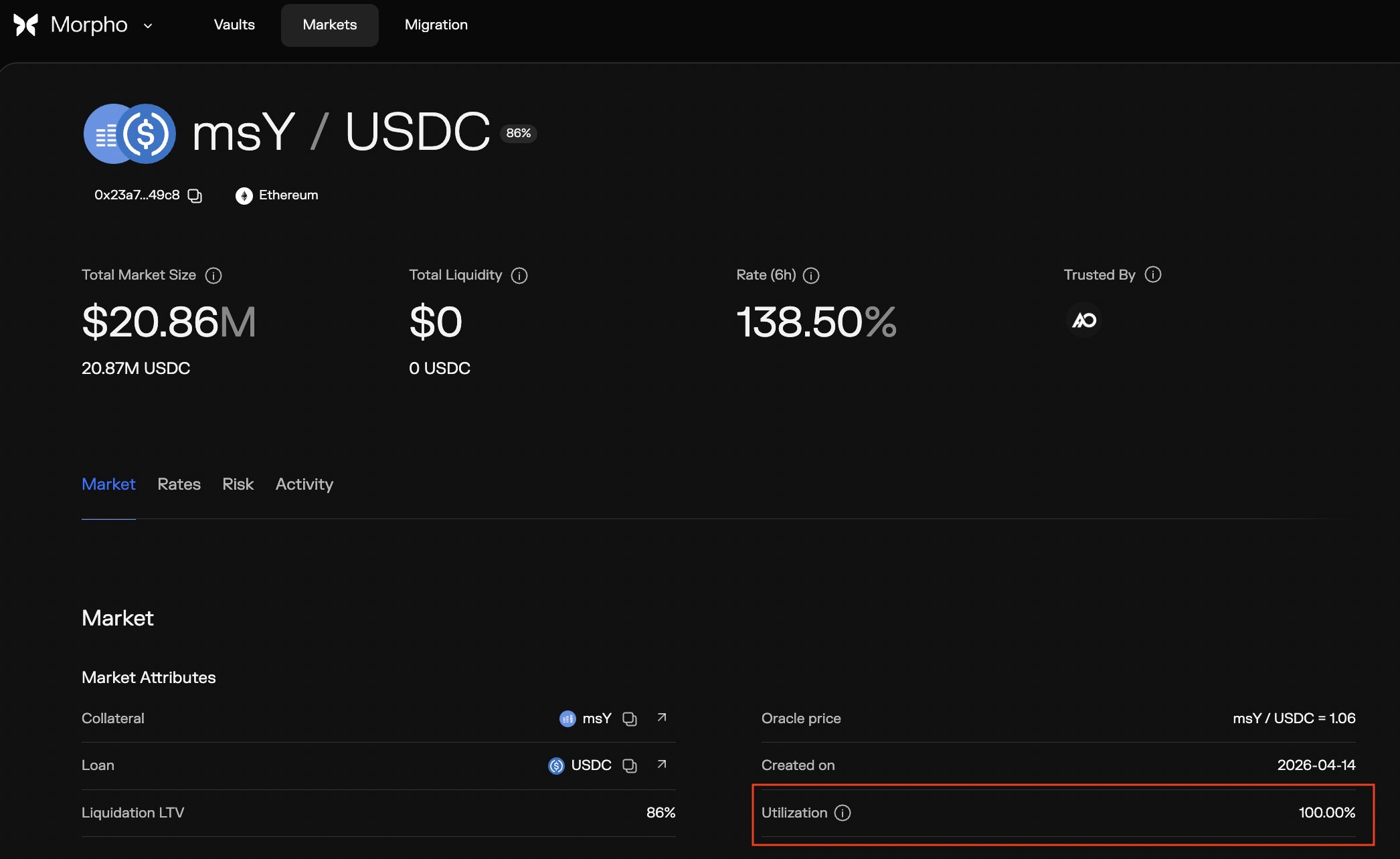

MainStreet-linked MSUSD plunges 85% as Morpho msY/USDC hits 100% utilization and $18M exposure

PeckShield says MainStreet-linked MSUSD fell as much as 85%, while Morpho’s msY/USDC market hit 100% utilization and AlphaUSDC Delta V2 has 30% exposure, roughly $18M, to the market. The sell-off followed Accountable ending its MainStreet verification agreement after saying the protocol failed its standards. MainStreet says assets remain fully backed, blames a third-party proof-of-reserves dashboard shutdown rather than insolvency, and says it has deployed over $8M USDC to support liquidity.

USDC launched by Centre Consortium (Circle + Coinbase)

SVB collapse triggers USDC depeg to ~$0.87

Centre Consortium dissolved; Circle assumes sole USDC governance

Circle Cross-Chain Transfer Protocol expands native USDC to additional networks

Coinbase announces 4% yield on USDC balances for retail customers

Total stablecoin supply exceeds $200 billion all-time high

Circle introduces Compliance Engine for programmable wallet regulatory tooling

Circle restarts US Treasury purchases in BlackRock-managed USDC reserve fund

Regulatory Landscape and Policy Debates

USDC sits at the center of ongoing debates about how to regulate stablecoins, how to prevent runs and systemic risk, and how to integrate private digital dollars into the broader monetary system. Policymakers see both promise and peril in tokens like USDC: they can make payments faster, cheaper, and more inclusive, but they can also amplify stress in traditional markets or circumvent capital controls and financial crime safeguards if poorly regulated. As a result, USDC’s regulatory posture is both a competitive advantage and a moving target.

In broad terms, regulators and researchers distinguish between “payment stablecoins” like USDC, which are used primarily for transactions and holdings as a cash substitute, and other tokens that behave more like investment products or unregulated money market funds. The policy question is whether these payment stablecoins should be treated as bank-like liabilities, e‑money, or a new category with bespoke rules. Circle has advocated for frameworks that recognize fully reserved stablecoins as a distinct class and has positioned USDC as compliant with emerging best practices around reserve quality, redemption rights, and transparency.

Policy Concerns: Runs, Contagion, and Monetary Sovereignty

Academic and policy analysis has highlighted several key risks associated with stablecoins. First, stablecoin holders can engage in rapid, digital runs if they lose confidence in an issuer’s backing, forcing fire sales of reserve assets and transmission of stress into underlying markets. Second, large-scale use of private stablecoins can affect monetary policy transmission and financial stability, especially if they become widely used in payments without clear supervisory oversight. Third, there are concerns about consumer protection, anti-money laundering, and sanctions compliance when stablecoins move across borders and into jurisdictions with weaker regulatory regimes.

The Federal Reserve’s post-mortem on the SVB failure noted that the bank run had spillover effects into the stablecoin sector, including the temporary depegging of USDC when a portion of its reserves was caught in SVB’s resolution process. This episode served as a concrete illustration of how traditional bank distress can interact with stablecoin markets, and vice versa, reinforcing regulators’ interest in comprehensive oversight of stablecoin issuers’ reserve management and bank exposures. It also underscored the possibility that large-scale redemptions of stablecoins could amplify shocks in the Treasury market if issuers had to liquidate holdings rapidly.

Monetary sovereignty is another concern. If private stablecoins like USDC become widely used for everyday payments in countries with weaker currencies, local central banks may lose control over domestic money supply and credit conditions. While this dollarization risk is not new—physical dollars and bank deposits already play that role—digital stablecoins could accelerate it by making dollar exposure more accessible via smartphones. Policymakers therefore debate whether to encourage regulated stablecoins as a complement to bank deposits and CBDCs, or to constrain their growth to preserve domestic monetary policy tools.

Circle’s Regulatory Posture and Licensing Regime

Circle has sought to position itself as a model issuer within the emerging stablecoin regulatory landscape. The company emphasizes that it is “one of the most widely regulated and licensed stablecoin issuers in the world,” operating under a patchwork of money transmission, e‑money, and payment institution licenses across multiple jurisdictions. These licenses typically impose requirements around capital, safeguarding of client funds, AML/KYC compliance, and supervisory reporting, aligning USDC issuance with standards applied to non-bank financial institutions.

In the United States and Europe, Circle works with regulators to ensure that its stablecoin issuance entities comply with applicable laws, such as money services business regulations and electronic money directives. Its collaboration with large, regulated financial institutions like BlackRock and BNY Mellon for reserve management and custody is part of an effort to embed USDC within existing regulatory frameworks rather than operating in parallel to them. Circle’s public disclosures and transparency reports are designed to anticipate regulatory demands for robust reserve segregation and high-quality assets.

Nonetheless, gaps and uncertainties remain. In many jurisdictions, stablecoin-specific legislation is still being drafted or debated, leaving issuers to interpret how existing categories apply in practice. Questions about how to treat interest on reserves, whether stablecoins should be allowed to pay yield directly, and what kind of capital or liquidity buffers issuers should hold are all under active discussion. As these rules crystallize, USDC may need to adjust its structure, reserve management, or distribution models to remain compliant while preserving its core value proposition.

The GENIUS Act and the Future of Payment Stablecoins

In the U.S., the proposed GENIUS Act represents one of the most detailed legislative efforts to create a dedicated regulatory framework for payment stablecoins. As analyzed by Brookings, the Act would establish licensing requirements for stablecoin issuers, mandate that reserves be held in cash and high-quality liquid assets, and enforce strict redemption rights at par value, among other provisions. It would also clarify the supervisory roles of federal and state regulators, set standards for risk management and corporate governance, and address cross-border and systemic risk concerns.

For USDC, such a framework could be both an opportunity and a constraint. On the one hand, Circle’s existing reserve composition—focused on cash and short-term U.S. Treasuries—and its practice of maintaining reserves separate from corporate funds align with the kind of backing model the GENIUS Act envisions. Its emphasis on monthly transparency reports and collaborations with regulated financial institutions would also fit well within a regime that prizes high-quality disclosure and oversight. If adopted, the Act could therefore formalize USDC’s status as a compliant payment stablecoin and provide regulatory clarity that encourages institutional adoption.

On the other hand, stricter rules might limit certain business models involving stablecoins, particularly those that rely heavily on rehypothecating reserves, offering high-yield products to retail users, or using riskier assets in reserve portfolios. USDC’s competition with other stablecoins might intensify if some issuers choose to operate outside the U.S. or under more lenient regimes, offering higher yields or more aggressive features at the cost of regulatory certainty. Circle’s strategic bet is that aligning with robust, risk-based regulation will be a competitive advantage as stablecoins become part of mainstream financial infrastructure rather than remaining purely crypto-native instruments.

Compliance, Freezing, and Privacy Debates

A defining feature of fiat-backed stablecoins like USDC is that their issuers can, in principle, freeze or blacklist addresses associated with illicit activity, complying with law enforcement requests or sanctions regimes. This capability is important for regulators concerned about money laundering and terrorist financing, but it also raises questions about censorship, privacy, and the degree to which stablecoins remain “neutral” across political and legal jurisdictions. For developers and users who value censorship resistance, such issuer controls are a double-edged sword.

USDC’s compliance capabilities mean that addresses can be restricted from moving tokens if they are associated with hacks, sanctions, or other flagged activities, and Circle has used these tools in response to specific incidents. From a risk standpoint, this protects the issuer from being used as a conduit for unlawful funds and can assist in recovering or containing stolen assets. From a user perspective, however, it means that USDC balances are not purely bearer instruments; they are subject to the legal environment and the issuer’s compliance obligations.

Privacy advocates point out that widespread use of centralized stablecoins creates detailed transaction histories that can be subpoenaed or analyzed, especially when combined with KYC data from centralized on- and off-ramps. The rise of confidential USDC constructs and privacy-preserving DeFi protocols reflects a desire to mitigate some of these concerns while retaining the benefits of a fiat-backed stablecoin. Regulators, in turn, are grappling with how to allow privacy-enhancing technologies without undermining AML/CFT frameworks—a delicate balance that will shape the trajectory of USDC and similar tokens in coming years.

Risks, Due Diligence, and User Considerations

Despite its conservative reserve structure and increasing regulatory alignment, USDC is not risk-free. Users, developers, and institutions need to understand the layers of risk they are assuming when they hold USDC directly, deploy it in DeFi protocols, or interact with wrapped versions on various chains. These risks span the issuer, the reserve assets, the banking and sovereign systems, the smart contracts and protocols where USDC is used, and the operational and user-experience layers that govern how people interact with the token.

In practice, the key questions are: What backs the USDC I hold? Who has control over the smart contracts and reserve assets? Through which intermediaries—bridges, protocols, platforms—does my exposure run? And what legal and regulatory protections, if any, apply in the jurisdictions where I operate? Addressing these questions requires a nuanced view of USDC not just as a monolithic token, but as an ecosystem of contracts, institutions, and interfaces.

Reserve and Issuer Risk

At the base layer, USDC holders take on issuer risk: the possibility that Circle or its issuance entities could become insolvent, mismanage reserves, or otherwise fail to honor redemption requests. While the reserve is designed to be fully matched and held in segregated accounts, it is not insured like bank deposits, and redemption rights are governed by legal agreements and applicable law rather than by a public guarantee. Users implicitly trust that Circle will manage reserves prudently, comply with regulatory requirements, and maintain robust operational controls.

Reserve risk also encompasses the quality and concentration of backing assets. Although USDC’s reserve is focused on cash and short-term U.S. government obligations, these assets are still subject to interest rate risk (for securities), operational risk at custodians, and, in extreme cases, sovereign risk. The SVB episode showed that concentration of deposits at specific banks can create localized vulnerabilities: even if the overall reserve is sound, temporary inaccessibility of a subset of assets can trigger market panic and depegging until resolution is achieved. Users must recognize that “fully backed” does not mean “riskless,” but rather that risk is shifted onto a portfolio of high-quality instruments and financial institutions.

From a due diligence perspective, institutions may want to review Circle’s transparency reports, attestations, and reserve fund disclosures regularly, assessing whether reserve allocation, custodial arrangements, and governance structures remain consistent with their risk tolerance. They should also consider legal questions such as whether USDC balances are treated as client assets in insolvency, how claims would be prioritized, and what jurisdictions govern contractual relationships. These factors can influence whether USDC is appropriate as a treasury asset, collateral, or transaction medium at institutional scale.

Market, Liquidity, and Peg Risk

Even when reserves are sound, USDC can experience short-term price deviations from its peg due to market dynamics, liquidity conditions, or information shocks. On exchanges with thin liquidity or during periods of extreme stress, USDC may trade at a discount or premium to \(\$1\), reflecting imbalances between buyers and sellers or delays in arbitrage flows. The SVB-driven depeg in 2023 is a prominent example of a discount driven by concerns about reserve impairments, but smaller deviations can occur for more mundane reasons, such as localized liquidity constraints or exchange outages.

In DeFi, liquidity risk can be amplified by protocol-specific factors. If a lending market becomes fully utilized—meaning all available USDC deposits have been borrowed—depositors may be unable to withdraw promptly, forcing them to accept discounted exits via secondary markets or liquidity tokens. A notable example involved a yield-bearing stablecoin whose main USDC-based lending market reached full utilization amid concerns about its backing, contributing to an 85% plunge in its price as confidence evaporated. While USDC itself remained broadly stable, its role as collateral and liquidity anchor in that market meant that USDC availability (or lack thereof) shaped the severity of the crisis.

For users, this implies that where and how they hold USDC matters as much as the token’s own peg. Holding USDC in a self-custodied wallet, in a reputable centralized exchange account, or inside a DeFi protocol with withdrawal queues and utilization dynamics are very different risk profiles. When USDC is locked in a protocol, its liquidity is contingent on that protocol’s rules and health, not just on Circle’s backing. Users should consider both primary-market redemption mechanisms and secondary-market liquidity when assessing peg risk and access to funds.

On-Chain, Protocol, and Smart Contract Risk

The moment USDC is deposited into a smart contract, additional layers of risk are introduced. Protocols can contain bugs, design flaws, or governance vulnerabilities that allow funds to be stolen, frozen, or misallocated. The DeFi ecosystem has seen numerous incidents where attackers exploited vulnerabilities such as reentrancy, integer overflows, or mis-specified token transfer logic to drain pools of USDC and other assets. In one recent case, a double-transfer bug in a token contract allowed an attacker to extract over a hundred thousand dollars’ worth of USDC from a liquidity pool on a prominent DEX, demonstrating how subtle coding errors can have outsized financial consequences.

Exploits often follow a predictable pattern: the attacker targets a vulnerable protocol, drains funds into a volatile asset, quickly swaps or routes the proceeds into USDC or another stablecoin to lock in value, and then attempts to launder or bridge out. Each step involves interacting with other protocols and liquidity pools, spreading risk and sometimes causing secondary losses if those pools are imbalanced or manipulated. Users whose USDC is locked in such protocols can suffer losses even if USDC itself remains fully backed and redeemable at the issuer level.

Governance and upgradeability add further complexity. Many DeFi protocols retain admin keys or multi-signature arrangements that can change parameters, pause operations, or upgrade contracts. While these controls can be used defensively in crisis, they also create centralized points of failure: a compromised key, a malicious governance vote, or a flawed upgrade can endanger user funds. When evaluating USDC-based opportunities in DeFi, users and institutions should assess not only smart contract audits but also governance structures, admin powers, and incident response plans.

Operational, Censorship, and User-Experience Risks

Finally, there are operational and user-experience risks that affect how safely people can use USDC day-to-day. On the operational side, issues can arise from bugs or outages in wallets, custodians, exchanges, or blockchain networks themselves, temporarily preventing transfers or causing user balances to display incorrectly. Multichain confusion—holding wrapped USDC under the same ticker as native USDC, sending USDC to incompatible chains or contract addresses, or mismanaging network fees—can lead to lost funds or complex recovery processes.

Censorship and blacklisting risks stem from USDC’s compliance capabilities. Addresses associated with hacks, sanctions, or other flagged activities can be frozen, making their USDC balance non-transferable. While this is generally viewed as a necessary compliance mechanism, edge cases can occur where legitimate users are swept up by mistaken or overbroad enforcement, resulting in temporary or prolonged loss of access. Users should be aware that USDC is not censorship-resistant in the way that some decentralized assets are; its use is subject to the legal obligations Circle must obey in the jurisdictions where it operates.

User-experience design can mitigate some of these risks but introduce others. For instance, consumer-facing apps that abstract away private keys can make USDC safer for non-technical users but at the cost of custodial risk and potential account freezes. Cards and bank integrations that connect USDC to everyday spending can broaden adoption but are bound by the regulatory and commercial decisions of issuers and partners, leading to unexpected service changes like card cutoffs in certain regions. As USDC becomes more embedded in mainstream finance, these operational and UX considerations will be as important as technical and reserve-related risks.

USDC itself carries no smart-contract risk, but it is the primary collateral in exploited protocols — Conic Finance, Penpie, and Radiant Capital hacks all drained USDC-paired pools, exposing holders to indirect loss.

Circle retains unilateral mint, burn, and address-freeze authority; its reserve fund is managed by BlackRock, concentrating systemic exposure in two regulated US entities whose decisions directly move USDC's backing.

The US GENIUS Act would impose reserve and audit requirements that Circle largely already meets, but passage uncertainty and potential non-US regulatory divergence could fragment USDC's global distribution network.

USDC maintains deep on-chain liquidity across major DEX pools and money markets, though Binance's removal of TRC20 support demonstrates that exchange-level decisions can abruptly shrink accessible liquidity on specific chains.

Yield-bearing stablecoins (USTB, USDtb, USDY, USDM) are systematically targeting the opportunity cost of holding zero-yield USDC, and USDT continues to lead in total supply, pressuring USDC's market share from both directions.

The March 2023 SVB collapse caused USDC to depeg briefly to ~$0.87 when $3.3B of reserves were trapped; Circle's subsequent shift to overnight repo and T-bills reduces but does not eliminate short-term bank-counterparty exposure.

Conclusion

USDC has emerged as a central piece of infrastructure in crypto markets and an increasingly important bridge between digital assets and traditional finance. Designed as a fully reserved, fiat-backed stablecoin, it offers dollar stability on public blockchains, supported by a reserve of cash and short-dated U.S. government obligations held in segregated accounts and managed under a regulated money market fund structure. Circle’s emphasis on transparency, regular reserve reporting, and regulatory alignment has positioned USDC as a leading example of the “payment stablecoin” model, even as the broader regulatory framework for such instruments continues to evolve.

In practice, USDC functions as a digital cash leg for trading, DeFi, and institutional settlement, with deep integration into centralized exchanges, lending markets, derivatives platforms, and yield strategies. Its stability and liquidity make it the preferred collateral asset and reward currency in many contexts, from leveraged trading and institutional borrowing to NFT marketplaces and on-chain rewards. At the same time, USDC is increasingly used behind the scenes in remittance corridors, merchant payments, and humanitarian efforts, providing global access to dollars and fast cross-border settlement without requiring end-users to navigate blockchain complexity.

The token’s multi-chain footprint and role in bridging add both power and complexity. Native USDC exists on dozens of blockchains, supported by canonical transfer protocols and a growing ecosystem of interoperability solutions. Yet users must navigate distinctions between native and wrapped USDC, understand bridge risks, and manage exposures during network sunsets or migration events. Even with a conservative reserve, USDC remains intertwined with traditional banking and sovereign risk, as the SVB-driven depeg demonstrated, and its deployment in DeFi introduces layers of smart contract, governance, and liquidity risk.

For regulators and policymakers, USDC is a test case for how private digital dollars can coexist with bank deposits, payment systems, and potential CBDCs. Proposals like the GENIUS Act seek to codify standards for payment stablecoins—standards that USDC largely anticipates through its current reserve structure and transparency regime but which could still reshape its operating environment. For users and institutions, the key is to treat USDC not as a riskless substitute for cash but as a layered instrument whose safety depends on issuer practices, reserve assets, regulatory frameworks, and the protocols and platforms through which it is used.

As the crypto and fintech landscape develops, USDC’s trajectory will illuminate broader trends in programmable money: the convergence of on-chain and off-chain finance, the rise of machine-to-machine economic activity, the tension between privacy and compliance, and the competition between private stablecoins and public digital currencies. Understanding USDC in detail—how it works, where it is used, and what risks it entails—provides a window into the future of digital dollars and their role in global markets.

Outlook

Looking ahead, USDC is likely to remain a cornerstone of crypto market infrastructure while expanding further into payments, remittances, and embedded finance. Continued growth of multi-chain ecosystems, L2s, and application-specific chains will deepen demand for a canonical, fiat-backed stablecoin, and Circle’s strategy of native issuance and canonical transfer protocols suggests USDC will continue to anchor liquidity in many of these environments. Institutional adoption of DeFi and tokenized assets will also reinforce USDC’s role as collateral and settlement currency, particularly as confidential USDC constructs and regulated yield venues mature.

Regulation will be the defining variable over the next cycle. If comprehensive stablecoin frameworks like the GENIUS Act or equivalent legislation in other jurisdictions are enacted, USDC could gain clearer legal status as a payment instrument, facilitating integration into banks, fintechs, and traditional payment systems. Conversely, overly restrictive or fragmented rules could drive some activity offshore or toward less transparent alternatives, challenging USDC’s positioning and market share. Circle’s ability to navigate this landscape while maintaining reserve integrity and operational resilience will be critical.

Finally, the evolution of AI, micropayments, and machine-to-machine commerce points toward new, less visible layers of USDC usage. As agents and services transact with each other in real time—paying for data, compute, and content—USDC’s role as a programmable, dollar-denominated medium of exchange may become increasingly important, even if end-users are only dimly aware of it. For a crypto news audience tracking the long arc of digital assets, USDC offers a lens on how stable, regulated tokens can move from trading tools to foundational components of the internet’s financial system.

Latest USDC news

Starknet adds shielded USDC balances and private transfers through STRK20, with Ready and XVerse integrationsCircle and Nomura target $440B-a-day Japan FX market with USDC settlement by 2027MainStreet-linked MSUSD plunges 85% as Morpho msY/USDC hits 100% utilization and $18M exposure Midas launches its tokenized private credit product mGLOBAL on Aave Horizon, letting investors borrow USDC against real-world assets while maintaining yield exposure

Midas launches its tokenized private credit product mGLOBAL on Aave Horizon, letting investors borrow USDC against real-world assets while maintaining yield exposureSources

- https://www.circle.com/usdc

- https://www.circle.com/transparency

- https://www.tradingview.com/symbols/USDC/

- https://www.circle.com/multi-chain-usdc