In-depth explainer on how crypto and stablecoins are reshaping payments, FX, and digital infrastructure across African markets, covering rails, regulation, use cases and the MENA–Asia trade corridors shaping the continent’s crypto future.

+20 sources across the wider coverage universe

Valr and Onafriq partner to enable mobile money funding for crypto accounts across 43 African markets.2026-04

Valr and Onafriq partner to enable mobile money funding for crypto accounts across 43 African markets.2026-04 Trident Digital Tech Holdings and Ripple Strategy Holding sign strategic cooperation agreement to co-build a stablecoin payment system for Africa market.2026-04

Trident Digital Tech Holdings and Ripple Strategy Holding sign strategic cooperation agreement to co-build a stablecoin payment system for Africa market.2026-04 Kredete partners with Visa to roll out stablecoin-linked card payments across Africa and the Gulf, enabling seamless USDC spending at 150M+ merchants globally2026-04

Kredete partners with Visa to roll out stablecoin-linked card payments across Africa and the Gulf, enabling seamless USDC spending at 150M+ merchants globally2026-04 Polygon expands DPTPay collaboration to push low-fee stablecoin payments across Africa2026-06

Polygon expands DPTPay collaboration to push low-fee stablecoin payments across Africa2026-06 Africa’s stablecoin market has moved beyond proving demand as regulators, banks and fintechs race to build the infrastructure needed for large-scale adoption2026-06

Africa’s stablecoin market has moved beyond proving demand as regulators, banks and fintechs race to build the infrastructure needed for large-scale adoption2026-06 Binance P2P suspension in Ethiopia exposes Africa’s deeper FX crisis as stablecoin markets become the real-time price discovery layer for USD liquidity2026-05

Binance P2P suspension in Ethiopia exposes Africa’s deeper FX crisis as stablecoin markets become the real-time price discovery layer for USD liquidity2026-05

Africa has emerged as one of the most dynamic, contested frontiers of the global crypto economy, with stablecoins, payments and digital infrastructure at the center of the story. This explainer maps how crypto is reshaping money, markets and rails across the continent—and what that means for builders, investors and policymakers.

Why Africa Matters in Crypto

Any serious discussion of the future of crypto payments has to grapple with Africa’s unique combination of demographics, financial exclusion, and mobile-first innovation. The continent is home to more than a billion people, a large youth population, and some of the world’s fastest-growing cities, but also some of the most fragmented and expensive financial systems. The result is a structural gap between how easily people can move data with a smartphone and how difficult it still is to move value across borders or even within national economies. Crypto—and particularly dollar-denominated stablecoins—has become a way to route around those frictions without waiting for legacy infrastructure to catch up.

On-chain data backs up the idea that Africa is not a marginal story but a structural one. Chainalysis estimates that Sub-Saharan Africa received more than 205 billion USD in on-chain value between July 2024 and June 2025, an increase of roughly 52% over the prior year. That scale is still smaller than in some larger economies, but the growth rate and usage patterns are striking, especially in light of macro headwinds and FX crises in several markets. In March 2025, the region saw an outlier spike in activity, with monthly on-chain volume reaching nearly 25 billion USD at a time when most other regions were slowing, underscoring how local dynamics rather than global hype cycles can drive African flows. At the same time, many countries across the region have faced rising inflation and heavy sovereign debt burdens, conditions that tend to push households and businesses toward alternative stores of value and channels for cross-border payments.

The structure of African crypto usage also looks different from that of wealthier markets. Chainalysis finds that more than 8% of all on-chain value transferred in Sub-Saharan Africa during that July 2024–June 2025 period involved transactions under 10,000 USD, compared with about 6% in the rest of the world. That higher share of smaller transfers is consistent with a region where ordinary users, SMEs, and freelancers—not just whales or institutions—use digital assets in their financial lives. It also mirrors the continent’s long history with mobile money and agent networks, where low-value transactions at high frequency can add up to systemically important flows. The line between “crypto user” and “everyday economic actor” is therefore thinner in Africa than in markets where crypto activity is still dominated by trading and speculation.

Underlying this growth is a long-standing mismatch between traditional financial rails and actual economic relationships. Many African economies are deeply connected to Europe, the Middle East and Asia via trade, remittances and services, yet their access to cross-border banking remains constrained by de-risking, correspondent banking retrenchment, and capital controls. Crypto payment networks and stablecoins have stepped into this gap, offering a way to move value that is more aligned with the speed and reach of digital commerce. Stablecoin transfers, in particular, now support sectors such as energy and merchant payments, functioning as a de facto settlement layer in places where domestic rails are slow or fragmented. For crypto builders and investors, that makes Africa less a “frontier bet” and more a proving ground for what a stablecoin-native financial system could look like.

Valr and Onafriq partner to enable mobile money funding for crypto accounts across 43 African markets.

Onafriq connecting ~1B mobile money wallets to stablecoin-settled crypto rails is quietly one of the largest fiat-to-stable on-ramps being built anywhere. Sub-Saharan mobile money contributed $190B to GDP in 2023 — route even a fraction of that through VALR's tokenized gold and private credit products, and you've got RWA distribution that makes Ethereum-native protocols look like pilot programs. Zero disclosure yet on which stablecoins clear settlement or what the FX spread looks like on KES/NGN conversion — that's where the cost actually lives for end users.

Readers clicking Africa crypto stories are not chasing gains — they are tracking dollar access: the dominant signal is that USD-pegged stablecoins are becoming the de facto FX safety valve in economies where local currency collapse and remittance costs make crypto a utility, not a speculation.↗

Use Cases: From Remittances to Merchant Payments

Cross-Border Payments and Remittances

The most intuitive use case for crypto in Africa remains cross-border payments. Remittances from diasporas in Europe, the Gulf and North America are life-and-death flows for many households, yet traditional channels can charge 5–10% in fees, take days to settle, and sometimes require recipients to travel long distances to cash out. Stablecoins offer a way to compress those costs and timelines while staying as close as possible to the US dollar that many families already target as their real unit of account. Instead of sending money through a chain of correspondent banks, a sender can acquire stablecoins on an exchange or through a fintech platform, transmit them in minutes, and have a local partner handle conversion into mobile money or bank deposits.

One of the most prominent examples of this bridge-building is the partnership between Crossmint and Paga Group. Paga is a major African payments company that processed over 11 billion USD in payments in 2025, operating extensive local fiat rails and agent networks across multiple countries. Crossmint, which provides multi-chain stablecoin and wallet infrastructure, is integrating Paga’s on- and off-ramps into its global payout network, creating a bidirectional bridge between African currencies and digital assets. This collaboration aims to support instant cross-border payments, programmable wallets, and stablecoin-powered merchant services for both consumers and enterprises, effectively treating stablecoins as payment infrastructure rather than a speculative asset.

At a more wholesale level, platforms like Juicyway illustrate how cross-border treasury operations are beginning to migrate to crypto-native rails. Juicyway, a cross-border payments platform that has processed more than 3 billion USD in transaction volume, has selected Aptos as its settlement layer for treasury and payments across Africa and other global markets. By using Aptos for stablecoin settlement, Juicyway can move capital across borders in seconds rather than days, at a fraction of the cost associated with legacy networks. Its customers gain access to stablecoin flows with predictable low fees and without having to interface directly with blockchain infrastructure, further blurring the line between “crypto” and “payments.”

The emergence of regulated corridors linking Africa with the Middle East and broader MENA region points to the next phase of this evolution. HashKey MENA, a Dubai-based virtual asset exchange licensed by the local regulator VARA, has launched a pilot B2B stablecoin payment corridor in partnership with the Aptos Foundation and Daya, a pan-African stablecoin payments platform. The initiative aims to enable corporates to fund local payments by on-ramping fiat in one jurisdiction and off-ramping in another, using stablecoins as the primary settlement asset across supported corridors. Daya provides virtual local-currency accounts, payroll and payment flows, and smart routing to maximize liquidity across African markets, while HashKey MENA offers compliant AED/USD and other fiat on- and off-ramps, creating a regulated cross-border channel that sits between purely crypto-native networks and traditional SWIFT rails.

These developments are taking place against a backdrop in which stablecoin-based FX has begun approaching “institutional-grade” parity with bank rails in some emerging markets. A recent report on stablecoin FX in Latin America and East Africa found that crypto-based FX markets are increasingly competitive in speed and pricing with traditional banking channels, albeit with different regulatory and counterparty risk profiles. In practice, that means African businesses and migrants can choose between conventional bank transfers and stablecoin corridors not merely on ideological grounds, but based on concrete trade-offs in cost, speed, and compliance.

Merchant Settlement and Everyday Spend

Beyond remittances and B2B flows, stablecoins are increasingly being used for merchant settlement and, in some cases, day-to-day spending. In markets where card penetration is low and local payment switches are fragmented, the ability to settle with merchants in a predictable digital dollar or euro can be a meaningful upgrade. Chainalysis observes regular multi-million-dollar stablecoin transfers in Sub-Saharan Africa that support sectors such as energy and merchant payments, highlighting how these instruments are already functioning as a settlement rail in the real economy. The underlying blockchain may be invisible to end users, but it is central to how value moves between buyers, sellers, and service providers.

Partnerships between blockchain networks and regional payment platforms are accelerating this shift. Polygon, for example, has expanded its collaboration with DPTPay, a payments provider, to power faster and more affordable stablecoin payments across Africa. The goal is to enable businesses to accept and settle payments in stablecoins with low fees and near-instant finality, opening the way for new models of cross-border commerce and local merchant services. By abstracting away the complexity of on-chain operations, such collaborations make it possible for SMBs and platforms to leverage stablecoin rails while remaining focused on their core businesses.

Card-linked stablecoin spending is also emerging as a bridge between crypto balances and everyday consumption. Kredete, a fintech offering a stablecoin-backed credit card, has expanded its product from 50 African countries into Gulf markets such as the UAE, Saudi Arabia, and Oman. The card allows users to tap stablecoin-backed credit for purchases at more than 150 million merchants globally via existing card networks, effectively turning USDC or similar assets into a funding source for conventional point-of-sale transactions. For African users, this can mean access to international online commerce and travel spending without the friction of foreign currency accounts, while for merchants the experience remains indistinguishable from any other card payment.

Major global networks are also adapting to this reality. Mastercard has deepened its partnership with Circle to enable settlement in USDC and EURC—the fully reserved stablecoins issued by Circle affiliates—for acquiring institutions in Eastern Europe, the Middle East and Africa. For the first time in this EEMEA region, acquirers can choose to receive settlement in stablecoins and then use those to settle with merchants, opening a path for stablecoin-denominated settlement to sit directly inside card network flows. Early partners such as Arab Financial Services and Eazy Financial Services illustrate how this model could serve both merchants and fintechs looking to operate across emerging market corridors where FX and cross-border settlement remain costly. For Africa in particular, the convergence of card rails and stablecoins suggests that “crypto payments” may soon feel much like any other digital payment, even as the underlying liquidity and FX management shift onto blockchains.

Mobile Money and Crypto On-Ramps

It is impossible to understand Africa’s crypto adoption without considering the role of mobile money and agent networks. For more than a decade, services like M-Pesa in Kenya and a host of regional competitors have provided basic digital wallets, cash-in/cash-out points, and domestic transfers for hundreds of millions of users. Crypto infrastructure in Africa increasingly plugs into these existing rails rather than trying to replace them outright. The synergy is straightforward: mobile money provides user familiarity, distribution, and regulatory cover; crypto provides cross-border reach, FX flexibility, and programmable settlement.

The partnership between South African exchange VALR and pan-African payments provider Onafriq is a case in point. The collaboration allows users across Africa to fund their VALR accounts via mobile money in local currencies, significantly lowering the barrier to acquiring digital assets. Instead of needing a bank account or card, users can convert local e-money balances into crypto and back again, widening participation beyond the already banked population. Because Onafriq operates across 43 African markets, this kind of integration also paves the way for mobile-to-mobile cross-border transfers mediated by stablecoins, even if end users remain mostly unaware of the blockchain component.

Meanwhile, platforms like Paga, already mentioned in the context of Crossmint, show how domestic payment processors can evolve into stablecoin gateways almost organically. Paga’s existing network of consumers, merchants, and agents becomes a ready-made off-ramp for multi-chain stablecoins once integrated with a global infrastructure provider. From the user’s perspective, funding a wallet or making a payment may feel almost identical to topping up mobile money, but under the hood value can be settling in USDC or other digital assets that offer more stable purchasing power and easier cross-border transfer. As more fintechs integrate stablecoins “under the hood,” the distinction between mobile money and crypto wallet may become largely semantic, governed more by licensing and compliance rules than by user experience.

Stablecoins as Financial Infrastructure

From “Crypto Product” to “Payments Rail”

One of the clearest shifts in the African crypto landscape is the repositioning of stablecoins from speculative trading instruments to core payments infrastructure. Industry dialogue captured by events like the Africa Fintech Summit reflects this change in mindset: a growing number of fintechs now describe stablecoins as payment infrastructure, not a “crypto product.” This may sound like semantics, but it signals a deeper realignment in how companies build, regulators supervise, and users interact with stablecoin-based systems. Rather than being marketed as an investment, stablecoins are increasingly embedded into wallets, cards, payroll platforms, and merchant tools as a means to an end: faster, cheaper, more predictable settlement.

This transition is visible in the breadth of use cases now live across the continent. Commentary from African ecosystem participants emphasizes that cross-border payments, remittances, treasury management, merchant settlement, and liquidity movement are no longer theoretical pilots but active, scaled uses of stablecoins. Stablecoins are used by SMEs importing goods, by freelancers serving international clients, by crypto exchanges managing internal treasury, and by infrastructure providers bridging FX gaps between corridors. In some markets, stablecoin trading pairs have become a de facto price discovery layer for scarce hard currency, particularly where official FX markets are heavily managed or under-supplied. In that sense, stablecoins function both as a payment rail and as a parallel financial market.

A key consequence of treating stablecoins as infrastructure is that the underlying blockchain becomes increasingly abstracted away. Many of the partnerships discussed—Crossmint/Paga, DPTPay/Polygon, Daya/Aptos, Anzens/Credit Bank—stress that users and many institutional partners do not need to understand, or even know, which network is settling their transactions. Instead, they interact with existing bank accounts, mobile wallets, or treasury dashboards, while smart contracts and stablecoin issuers handle the plumbing. This mirrors the evolution of the internet, where most users do not think about TCP/IP or DNS when they send an email or stream a video. For stablecoins to truly become part of Africa’s financial fabric, this kind of invisibility is not a bug but a feature.

USDC, EURC and Other Regulated Stablecoins

Within this emerging infrastructure stack, regulated fiat-backed stablecoins such as USDC, EURC and newer entrants like USDA play an outsized role. USDC, in particular, has positioned itself as a preferred asset for institutions and payment processors wary of opaque reserves or regulatory uncertainties. Mastercard’s expansion of its partnership with Circle to allow USDC and EURC settlement for acquirers in the EEMEA region reflects this institutional tilt. By enabling acquiring institutions to take settlement in stablecoins issued by regulated affiliates of Circle, Mastercard is effectively licensing stablecoins as a trusted settlement asset within its global network, including across African markets. This gives African fintechs and merchants a way to plug into a global dollar and euro liquidity pool without relying solely on local banks’ access to hard currency.

At the same time, region-specific stablecoins are emerging to address local regulatory and banking realities. Anzens, for instance, has launched USDA, a dollar-backed stablecoin designed explicitly for cross-border payments, and is working with Credit Bank PLC, a Kenyan commercial bank, to explore how USDA could be integrated into existing bank services. If regulators approve, USDA would become one of the first stablecoins in an emerging market to be minted, distributed and redeemed directly through a licensed commercial bank, fully embedded within existing banking relationships rather than sitting on the periphery. Crucially, Credit Bank would act as custodian of both Kenyan shillings and US dollars, while the underlying blockchain would remain invisible to end users, reinforcing the notion of stablecoins as back-end infrastructure.

Other global players are also eyeing Africa as a proving ground for regulated stablecoin frameworks. Ripple’s work with partners to introduce RLUSD, a proposed regulated stablecoin, into African payment flows (as described in recent market coverage) is one example of how competition over “which stablecoin becomes the default settlement asset” is playing out. These entrants face both traditional FX competitors—banks, money transfer operators, card networks—and native crypto options, including decentralized stablecoins and local custody providers. For African regulators, the policy question is not simply whether to “allow stablecoins” but how to structure oversight, reserve management, and interoperability in a way that supports innovation without undermining financial stability.

FX, Inflation and Dollar Access

Beneath the technical and institutional debates lies a more fundamental macroeconomic reality: in many African economies, stablecoins are attractive precisely because they provide synthetic access to dollars or euros in countries where foreign currency is scarce, tightly controlled, or rapidly depreciating. Chainalysis emphasizes that many Sub-Saharan African countries have struggled with rising inflation and debt, making cryptocurrencies—especially dollar-linked stablecoins—appealing as stores of value and mediums of exchange. For households, holding stablecoins can be a way to preserve purchasing power relative to a weakening local currency; for businesses, it can be a tool to manage FX risk on imports and exports or to pay overseas suppliers without waiting for bank approvals.

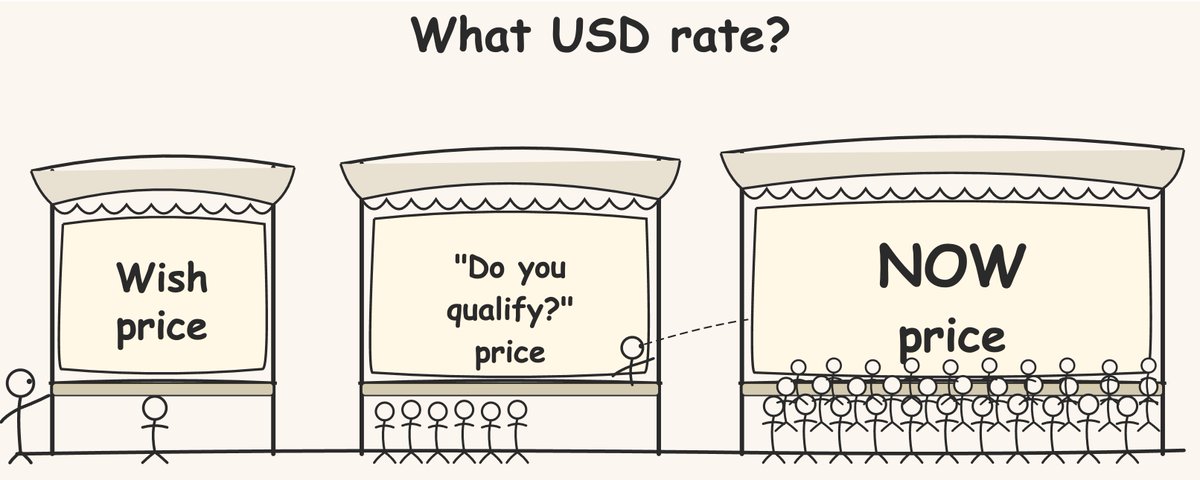

In some markets, stablecoin order books and P2P platforms have even become a quasi-official reference for real-time exchange rates. When Binance halted its naira and birr P2P services in Nigeria and Ethiopia amid regulatory pressures, local debates intensified around how crypto platforms had become a de facto FX price discovery layer for US dollars and other hard currencies. Similar dynamics can be seen in smaller marketplaces where USDT or USDC prices in local currency track black-market FX more closely than official rates. While these dynamics are partly captured in reports on how stablecoin FX is reaching parity with bank rails in pricing and execution quality in East Africa and Latin America, they also illustrate the political sensitivity of such markets.

The flip side is that heavy reliance on dollar stablecoins can accelerate de facto dollarization, potentially weakening central banks’ control over monetary conditions. If large segments of savings, trade invoicing, and even salaries migrate into dollar stablecoins, local authorities may find it harder to manage liquidity, implement capital controls, or maintain exchange rate regimes. This is not merely a hypothetical concern: in economies already battling high inflation and limited FX reserves, policymakers may view widespread stablecoin use as both a symptom and a driver of financial instability. The challenge will be to distinguish between use cases that genuinely improve efficiency—for example, lowering remittance costs—and those that primarily facilitate regulatory arbitrage or speculative dollar hoarding.

Trident Digital Tech Holdings and Ripple Strategy Holding sign strategic cooperation agreement to co-build a stablecoin payment system for Africa market.

TDTH stock dropped ~9% on this announcement, which tells you how the market reads a micro-cap proposing a $500M XRP treasury to fund African stablecoin ops. "Ripple Strategy Holding" is also conspicuously not Ripple Labs — the press release offers zero corporate registration details or formal relationship to Ripple, just vague "technology support" language. Seeding RLUSD/GHS liquidity pools with unnamed "partner banks" in Ghana by mid-2026 is ambitious given no regulatory approvals are in hand yet, and the 2.1M MSME target market is exactly the demographic that historically churns hardest on new fintech rails without heavy on-the-ground distribution.

- 01USD stablecoin escape valve↗

The $3B stablecoin boom headline and de-dollarization paradox drew the most clicks because readers recognized the irony: Africa's push away from dollar dependence is being answered by mass adoption of dollar-pegged crypto instruments.

- 02Regulatory obstacles vs. progressive laws↗

The tension between blanket Web3 restrictions across most of the continent and Kenya's widely praised comprehensive crypto law shows readers are tracking which jurisdictions will become the launchpad for the next wave.

- 03Remittance corridor infrastructure wars↗

Multiple high-click headlines around Ripple, Yellow Card, VALR, and Circle all converge on the same pain point — $200 transfers costing $100 in fees — making the race to own Africa's remittance rails a concrete, high-stakes story.

- 04Bitcoin adoption gap

The River data showing Africa at 1.6% BTC ownership versus 14% in the US reframed Africa's crypto story away from hype: readers engaged because the stat quantifies how far infrastructure must travel before Bitcoin is genuinely accessible.

- 05DeFi uncollateralized lending defaults

The Goldfinch story — institutional backers, promised 10% yields, and a claimed 70%-plus loss rate on Africa and Asia loans — landed because it exposed the gap between impact-DeFi marketing and the actual credit risk of frontier-market lending.

- 06Bank and fintech infrastructure buildout↗

Nedbank/Crypto.com, Circle/Sasai, VALR/Onafriq, and Kredete/Visa headlines clustered around one theme: legacy financial institutions are now racing to lay stablecoin rails rather than resist them.

Infrastructure: Rails, Nodes and Bridges

Layer-1 Settlement Networks

The settlement layer of Africa’s crypto economy is increasingly multi-chain and competitive. While Bitcoin and Ethereum remain foundational networks, newer layer-1s have positioned themselves explicitly as high-throughput, low-latency settlement fabrics for payments and stablecoin flows. Aptos is one of the most visible in the African context, thanks to its adoption by platforms like Juicyway and its role in HashKey MENA’s cross-border corridor. By offering fast finality and low transaction fees, Aptos allows intermediaries to batch and route stablecoin transfers across Africa, Latin America, Southeast Asia, and beyond in ways that would be prohibitively slow or costly on legacy rails.

HashKey MENA’s corridor pilot with Aptos and Daya showcases how a layer-1 can be embedded into a regulated cross-border framework rather than operating purely in the wild. On the African side, Daya provides local on- and off-ramps, virtual naira accounts, payroll and payment flows, and APIs, effectively acting as a fintech front-end for stablecoin transfers. On the Middle Eastern side, HashKey MENA uses its license and OTC infrastructure to provide compliant AED/USD and multi-currency ramps into and out of stablecoins. Aptos, meanwhile, serves as the neutral settlement layer on which tokens move and smart contracts execute, backed by ecosystem funding to subsidize more cost-efficient transfers. The goal is a two-phase rollout where initial flows lay the groundwork for a full-scale B2B trade settlement system with stablecoins as the primary settlement asset.

Other chains are pursuing similar roles. Polygon’s work with DPTPay to offer low-fee stablecoin payments across Africa demonstrates how EVM-compatible networks can piggyback on existing developer tooling and liquidity, making it easier for merchants and fintechs to integrate. Ripple’s technology stack, deployed through partnerships aimed at building stablecoin payment systems for African markets, leverages its history in cross-border banking integrations. Stellar and other networks not explicitly referenced in the cited sources have also cultivated remittance and aid-related corridors on the continent. From the perspective of African users and institutions, the particular chain matters less than its ability to provide reliability, low cost, and credible neutrality in an environment where local politics and global sanctions can shape access to traditional rails.

Banking and Card Integrations

While layer-1 networks provide the technical substrate, banks and card networks remain crucial gatekeepers for fiat connectivity and mainstream adoption. Anzens’ collaboration with Credit Bank in Kenya is a significant step in this direction because it locates the entire fiat–stablecoin–fiat cycle inside a licensed commercial bank. Under this model, Credit Bank’s customers would be able to convert Kenyan shillings to USDA and back again, initiate cross-border transactions from existing bank accounts, and have funds automatically converted into local currency at the destination, all with a flat 1.5% fee regardless of corridor. Credit Bank would hold the underlying fiat reserves in both local and US dollars, insulating users from direct exposure to external custodians or exchanges and giving regulators a single supervised entity to oversee.

Card networks are performing a similar bridging function at the consumer and merchant level. Mastercard’s integration of USDC and EURC for settlement in the EEMEA region effectively turns these stablecoins into back-end instruments for card acquirers in parts of Africa. Merchants and cardholders on the front end may continue to operate in local currencies, but somewhere in the settlement chain, value can be netted out in stablecoins rather than in traditional correspondent accounts. Kredete’s stablecoin-backed card, meanwhile, allows African and Gulf users to spend against stablecoin collateral at millions of merchants worldwide. Together, these models show how crypto balances can be monetized in traditional commerce with minimal friction, eroding the practical distinction between a “crypto wallet” and a “bank account with card access.”

As these integrations deepen, they also alter the risk and compliance landscape. Banks embedding stablecoins must manage reserve quality, counterparty risk with issuers, AML/CFT controls over on-chain flows, and cyber risk around wallet infrastructure. Card networks need to ensure that stablecoin settlement does not facilitate sanctioned transactions or create unhedged FX exposures. Yet the potential rewards are significant: for African banks struggling with low-fee competition from fintechs and mobile money operators, offering low-cost cross-border stablecoin settlement can be a way to regain relevance in the remittances and SME trade segments. For card networks seeking growth in emerging markets, stablecoin settlement offers a way to differentiate and to capture a greater share of cross-border expenditure.

Data Centers, Nodes and Sovereign Digital Infrastructure

Behind these visible products lies an often-overlooked layer of physical and digital infrastructure: data centers, node operators, and connectivity providers. Africa’s role in the global crypto economy is not limited to being a consumer of stablecoin-based services; it is increasingly a producer of computational resources and digital sovereignty. BitValue Capital’s 200 million USD Africa Growth Fund II, launched in partnership with decentralized AI platform FLock.io, aims to deploy what it calls “privacy-preserving AI node centers” and to transition the region from traditional raw-material extraction to high-value “digital power distillation.” While the initiative is framed primarily around AI, it speaks directly to the infrastructure demands of blockchain and crypto systems, which require reliable power, connectivity, and secure hardware for node operation and validation.

By investing in AI and blockchain-related node centers, funds like BitValue’s are effectively betting that Africa can become a hub for decentralized computing rather than merely an endpoint for consumer services. These facilities can support validator nodes, oracle services, storage networks, and AI inference engines, all of which can be integrated with crypto-based incentive structures and governance. The emphasis on privacy-preserving AI also aligns with emerging trends in zero-knowledge cryptography and confidential computing, where sensitive data can be processed without being fully exposed to operators. For African policymakers worried about data sovereignty and surveillance, the combination of local infrastructure and decentralized architectures offers a potential path away from dependence on foreign cloud providers.

Complementing these efforts are long-standing infrastructure players who operate the rails for moving both money and data. Some of these organizations, in partnership with groups like the World Economic Forum, have spent a decade building backbone connectivity and payment infrastructure for more than a billion people across the continent, relying on node operators such as Ankr to maintain 99.99% uptime and zero major incidents. Although such efforts are not always branded as “crypto,” they provide the resilient networking and compute layers on which stablecoin and DeFi services depend. Without reliable data centers, undersea cables, terrestrial fiber, and satellite links, Africa’s crypto economy would remain stuck in pilot mode, constrained by intermittency and local outages.

Wallets, APIs and Developer Platforms

At the top of the stack, wallets, APIs and developer platforms determine how easily African builders can create stablecoin-native products and how seamlessly users can access them. Crossmint’s infrastructure illustrates this: by offering multi-chain wallet and stablecoin primitives along with compliance tooling, it enables partners like Paga to integrate complex on-chain functionality without having to build everything in-house. Developers can focus on user experience and local regulatory nuances while relying on Crossmint to manage key custody, transaction routing and asset support. Paga, in turn, can leverage its existing user base and fiat rails to distribute stablecoin-enabled wallets at scale.

Daya offers a similar abstraction layer on the African side of the Aptos–HashKey MENA corridor. Through its full-stack API, Daya provides virtual accounts in local currencies, payroll and mass payout flows, fiat on- and off-ramps, and third-party payouts, all backed by a smart routing engine that optimizes liquidity and cost across different channels. For African fintechs and enterprises, integrating Daya’s API can mean instant access to cross-border stablecoin settlement without the overhead of building their own exchange, compliance and treasury operations. For global partners, it provides a single integration point into a heterogeneous set of African markets with varying regulations and payment habits.

Other players such as DPTPay, VALR, and regional neobanks are building their own API suites, enabling businesses to accept stablecoin payments, automate treasury operations, and embed crypto features into consumer apps. As more of these platforms emerge, interoperability and standards will become critical. The risk is that Africa’s crypto infrastructure replicates the fragmentation of its traditional payments landscape, with incompatible wallets and closed ecosystems. The opportunity is to use open standards, composable protocols, and cross-chain bridges to create a more unified and developer-friendly environment than exists in traditional finance.

Markets, Adoption and User Profiles

On-Chain Volumes and Retail Patterns

For market participants, understanding Africa’s crypto trajectory requires going beyond headline adoption numbers to examine user profiles and transaction patterns. Chainalysis data shows that Sub-Saharan Africa’s on-chain inflows reached roughly 205 billion USD in the twelve months ending June 2025, with a year-on-year growth rate of about 52%. This makes the region a relatively small portion of global on-chain activity, but one that is growing faster than many larger markets. More importantly, the composition of these flows is distinct: Africa has a higher proportion of smaller transactions under 10,000 USD compared with the global average. Such a pattern suggests extensive grassroots usage by individuals and small firms rather than concentration among a few large institutions.

The March 2025 spike in on-chain volume, reaching nearly 25 billion USD in a single month at a time when other regions were experiencing declines, highlights how African markets can decouple from global cycles. Drivers for such anomalies can include local political events, abrupt FX regime changes, regulatory shifts, or regional crises that prompt flight to stablecoins. For example, sudden depreciation episodes or changes in access to dollars at official rates can trigger a rush into on-chain dollar assets, just as capital controls can push more trade and remittance flows into crypto channels. Analysts and traders monitoring African markets increasingly pay attention to on-chain stablecoin flows, P2P trading volumes, and social chatter as leading indicators of stress in local FX and banking systems.

At the same time, Africa’s crypto adoption has proven remarkably resilient to global price cycles. Even during periods of depressed token prices and outflows from speculative DeFi protocols, stablecoin usage for real-economy use cases such as remittances and merchant settlement has continued to grow. This divergence between speculative and utilitarian demand means that African crypto markets may be less sensitive to global sentiment than those in advanced economies, making them an important diversifier for projects seeking more stable flow patterns. It also underscores the need for more granular metrics—such as the share of stablecoin volume tied to off-chain trade or payroll—to understand the real footprint of crypto in African economies.

North Africa and the MENA Bridge

North Africa occupies a particular position in this landscape, acting as both an African region and a natural bridge to the Middle East and Europe. Regulatory regimes in countries like Morocco, Egypt and Tunisia vary widely, but all share strong economic linkages with the Gulf and the EU. This makes the wider MENA region’s crypto infrastructure—licensed exchanges in Dubai and Bahrain, remittance corridors through Jordan and Lebanon, and growing stablecoin settlement networks—especially relevant. HashKey MENA’s Asia Connect network, now expanding into Africa through its Aptos-based corridor pilot with Daya, exemplifies how MENA-based players are integrating African routes into broader Asia–Middle East trade flows.

North African markets are also seeing increased institutional attention. BitGo MENA, for example, has expanded its regulated crypto offering in the region by launching electronic trading capabilities, complementing its custody, staking and OTC services. By providing institutional-grade trading infrastructure under local regulatory oversight, BitGo MENA lowers the barrier for regional banks, funds, and corporates to gain exposure to digital assets, including stablecoins used for cross-border settlement. For North African firms seeking to bridge into Sub-Saharan markets, combining such MENA infrastructure with African on- and off-ramps offers a path to integrated, multi-currency operations that would be difficult to replicate purely through domestic banking channels.

Card network initiatives like the Mastercard–Circle partnership also reinforce this North Africa–MENA nexus. By enabling acquirers in Eastern Europe, the Middle East and Africa to settle in USDC or EURC, Mastercard effectively creates a multi-regional stablecoin settlement fabric that can serve merchants and platforms operating across North Africa and beyond. As North African economies continue to deepen trade ties with both Europe and the Gulf, stablecoin rails spanning these regions are likely to become more important for everything from tourism receipts to oil payments and infrastructure contracts.

Regional Diversity: Nigeria, Kenya, South Africa and Beyond

Despite these cross-regional dynamics, Africa’s crypto landscape remains profoundly heterogeneous. Nigeria, Kenya and South Africa are often cited as leaders in adoption and innovation, but their regulatory and market structures differ markedly. Nigeria has seen extremely high grassroots adoption driven by naira volatility, FX shortages and a large, tech-savvy youth population, but also frequent regulatory swings between outright hostility and cautious engagement. Kenya combines an entrenched mobile money ecosystem with growing interest in regulated crypto banking experiments, such as the Anzens–Credit Bank USDA pilot overseen in dialogue with the Central Bank of Kenya and securities regulators. South Africa, with its more developed capital markets, has moved toward formal licensing for crypto service providers and tighter integration with traditional finance.

Pan-African players attempt to harmonize this patchwork through multi-country infrastructures. Onafriq’s mobile money network across 43 markets, now connected to VALR’s exchange services, enables cross-border flows that transcend national silos. Paga’s operations and partnerships cover multiple West and East African countries. Daya’s smart routing engine and virtual accounts similarly aim to smooth over differences among national payment systems. However, regulatory fragmentation remains a material constraint: licenses are still granted on a country-by-country basis, central banks maintain differing stances on stablecoins and crypto exchanges, and tax treatment of digital assets is inconsistent. For builders and investors, the opportunity lies in designing products that are modular enough to adapt to local rules while still benefiting from economies of scale across the continent.

Ethiopia illustrates both the promise and the tension. Binance’s decision to end birr P2P trading, followed by discussions between its Africa legal head and Ethiopia’s central bank, exposed deeper FX challenges facing the country and raised questions about how global exchanges should navigate markets where official rates diverge sharply from parallel markets. While Ethiopian authorities have made cautious moves toward digital modernization, they remain wary of uncontrolled capital outflows and dollarization pressures that might be exacerbated by stablecoin usage. Similar stories can be found across the continent, reinforcing the need for more coherent regional frameworks that can accommodate innovation without triggering regulatory whiplash.

DeFi, Credit and Real-World Assets

Africa’s crypto story is not limited to payments and stablecoins; it also includes experiments in decentralized credit and real-world asset (RWA) tokenization, some of which have produced hard lessons. DeFi credit protocols like Goldfinch sought to channel undercollateralized loans to businesses in Africa and Asia based on “social trust” and off-chain underwriting, promising double-digit yields to global investors. The subsequent wave of defaults, restructurings and write-downs—resulting in tens of millions of dollars in troubled loans and substantial realized losses—highlighted the difficulty of exporting DeFi-style risk assessment into opaque credit markets. For African borrowers, such protocols offered an alternative source of capital but also raised concerns about predatory terms and currency mismatch risk when loans were denominated in dollars.

Tokenization of infrastructure and commodities has followed a parallel arc. Projects like Solar DAO, which launched what it described as a digital autonomous closed-end fund to invest in utility-scale solar projects globally, raised capital via token sales and promised exposure to real-world solar assets. In Africa, similar concepts have been applied to solar home systems, mini-grids and other energy projects, as covered in reporting on the region’s “solar token trade.” While these initiatives can unlock new funding sources for underserved sectors, they also blur regulatory lines between securities, commodities and utility tokens, and can expose retail investors to complex project development and regulatory risks. The volatility of token prices can decouple dramatically from the underlying cash flows and asset performance, leaving investors vulnerable even if projects succeed on the ground.

Nevertheless, RWA tokenization and DeFi credit remain areas of intense experimentation in Africa because they speak directly to structural bottlenecks in trade finance, SME lending, and infrastructure funding. For protocols, the challenge is to move beyond yield marketing and incorporate robust, transparent risk models, local partnerships, and realistic return expectations. For regulators, the imperative is to develop frameworks that can distinguish between genuine innovation in capital formation and thinly disguised unregistered securities offerings.

Kredete partners with Visa to roll out stablecoin-linked card payments across Africa and the Gulf, enabling seamless USDC spending at 150M+ merchants globally

Stellar rails, not Ethereum — Circle's been running USDC-on-Stellar as its remittance primary since 2021, and Kredete's $9B annualized on 4.6M users validates the chain choice for payments over DeFi. Credit card, not debit, is the load-bearing detail: prefunded stablecoin debit exists everywhere (Gnosis Pay, Crypto.com), but underwriting a USDC-denominated revolving line across 50 markets with 15-30% local FX volatility is a different risk model. GCC leg is the harder lift given UAE's VARA-regulated AE Coin already sits first-class in the regional stack.

- 2021-01launch

Goldfinch launches uncollateralized DeFi loans to Africa and Asia

- 2023-06exploit

Goldfinch reports $53.8M troubled loans; real loss rate disputed above 70%

Chainalysis: Sub-Saharan Africa stablecoins surpass Bitcoin in on-chain volume

- 2025-08launch

Ripple distributes $700M RLUSD to Africa via Chipper Cash, VALR, Yellow Card

- 2025-09milestone

Altvest Capital becomes first African publicly listed company to hold BTC as treasury reserve

Bitvalue Capital launches $200M Africa Fund II for digital infrastructure

- 2026-04regulatory

Kenya enacts comprehensive crypto law; Yellow Card cites it as global benchmark

HashKey MENA, Aptos, and Daya pilot regulated B2B stablecoin corridor linking MENA and Africa

Regulation, Policy and Risk

Regulatory Patchwork and the AU Context

Regulation is perhaps the most decisive variable shaping Africa’s crypto trajectory, and it currently presents a patchwork rather than a unified landscape. A survey of legal and policy developments across the continent notes that the African Union has not yet issued a regional cryptocurrency regulation that could serve as a common baseline for member states. Instead, national authorities have pursued divergent approaches, ranging from outright bans or severe restrictions to proactive licensing regimes and sandbox programs. Motivations for regulation typically include anti-money laundering and counter-terrorist financing concerns, consumer protection, financial stability, and, increasingly, the desire to harness crypto to advance financial inclusion and digital economy goals.

This fragmentation has both costs and benefits. On one hand, it creates uncertainty for cross-border projects and discourages investment in pan-African infrastructures that might run afoul of inconsistent rules. On the other, it allows for regulatory experimentation and competition, with some countries positioning themselves as hubs for crypto businesses and others taking a more cautious stance. Over time, frameworks such as the African Continental Free Trade Area (AfCFTA) and AU-level bodies may seek to harmonize aspects of digital payments regulation, but crypto and stablecoin-specific rules remain largely national for now. For builders, this means that compliance strategy must be embedded at the design stage rather than treated as an afterthought.

Banking, FX Controls and Sandbox Experiments

Stablecoins and crypto payments intersect directly with sensitive policy domains such as FX management, capital controls, and banking supervision. Kenya’s approach to the USDA pilot provides a useful case study. The initiative between Anzens and Credit Bank is explicitly framed as exploratory and subject to ongoing engagement with the Central Bank of Kenya. Its stated aim is to assess how a regulated, dollar-backed stablecoin might complement existing cross-border payment systems within a licensed banking environment, rather than operate as an unregulated parallel system. By embedding issuance and redemption inside a commercial bank and keeping the blockchain layer invisible to end users, the model seeks to alleviate concerns about capital flight and illicit finance, while still delivering cost and speed benefits.

Regulatory sandboxes offer another avenue for controlled experimentation. In the Kenyan example, a firm called Yeshara has obtained sandbox approval from the Capital Markets Authority to enable USDA as a payment option for tokenized real estate and commodity assets, with Credit Bank serving as custodian. This creates a ring-fenced space where regulators can observe how tokenized RWAs and stablecoin payments interact with existing laws and market practices, and adapt their frameworks accordingly. Other African countries have launched similar sandboxes or innovation hubs, allowing fintechs to test crypto-linked products under close supervision.

However, sandbox-friendly rhetoric often coexists with strict enforcement against unlicensed exchanges or P2P platforms deemed to be facilitating unauthorized FX dealings. The Binance P2P suspensions in markets like Ethiopia illustrate how quickly authorities can move to constrain crypto flows perceived as undermining FX controls. Exchanges and OTC desks operating in Africa must therefore navigate a landscape where policy can shift rapidly and where activities tolerated in one jurisdiction may be criminalized in another. For users, this regulatory volatility adds another layer of risk on top of market and counterparty risk.

Consumer Risk, Scams and Volatility

For all its promise, Africa’s crypto boom has also exposed consumers to significant risks. DeFi credit failures such as those experienced by Goldfinch lenders, who saw substantial portions of their deposits impaired by defaults and restructurings, are one category of harm. In many African contexts, users attracted by advertised yields may lack the financial literacy or access to legal recourse needed to navigate these complex products. When stablecoins are involved, the perception of “dollar safety” can further obscure underlying credit or regulatory risks. Even regulated fiat-backed stablecoins carry exposure to issuer insolvency, regulatory seizures, or depegs in stressed markets.

Scams, Ponzi schemes and fraudulent investment schemes remain widespread, often leveraging the language of crypto and the aspiration for quick financial relief in environments of economic hardship. Rug pulls, fake mining operations, and impersonation of legitimate exchanges are common. While such phenomena are not unique to Africa, they can have outsized impact where formal consumer protection mechanisms are weak and where savings buffers are small. Regulators, civil society and industry groups have responded with a mix of public education campaigns, enforcement actions, and attempts to bring more activity into supervised channels, but the gap between innovation speed and regulatory capacity remains large.

Volatility is another persistent risk. While stablecoins can mitigate price swings for users, exposure to volatile crypto assets remains high in trading and speculative contexts. For businesses that hold stablecoins as working capital, sudden regulatory moves—such as banking partners shutting off access to cash-out channels—can create liquidity crises. For individuals, storing life savings in a centralized exchange or in a self-custodied wallet with inadequate security can result in loss through hacks, phishing, or lost keys. Balancing the empowerment provided by self-custody with the security and convenience of custodial services remains an open challenge, especially in regions with limited access to high-quality hardware and digital security education.

Macroeconomic and Sovereign Risk

Beyond individual and firm-level risks, policymakers must contend with macroeconomic and sovereign implications of widespread crypto adoption. Stablecoins that act as synthetic dollars can undermine local currency demand and complicate monetary policy, particularly in countries with shallow domestic capital markets. If a significant portion of domestic transactions and savings shift into stablecoins, central banks may find traditional tools—such as interest rate adjustments or reserve requirement changes—less effective. Moreover, stablecoin-based FX markets can erode the credibility of official exchange rates if they consistently quote a different price for the local currency.

On the other hand, ignoring or suppressing stablecoin usage carries its own dangers. It can push activity into unregulated offshore channels, reduce transparency, and forego opportunities to lower remittance costs or improve financial access. Some policymakers may see regulated stablecoin frameworks—where reserves are held domestically, issuers are licensed, and integration with tax and reporting systems is baked in—as a way to harness the benefits while containing the risks. Others may prefer to channel similar functionality into central bank digital currencies (CBDCs), though the trade-offs between CBDCs and open stablecoins in terms of innovation, privacy and interoperability are still being debated globally.

For African sovereigns, there is also a strategic dimension. Participation in setting global norms for stablecoin regulation, cross-border payment interoperability, and digital identity could influence the continent’s bargaining power in international finance. If Africa’s large and growing population becomes primarily a user base for foreign-issued stablecoins and foreign-operated L1s, with little local control over governance or fees, the long-term implications for digital sovereignty could be profound. Conversely, cultivating local or regional stablecoin issuers, validators, and infra providers—under robust oversight—could position African economies not just as consumers but as co-architects of the next generation of financial infrastructure.

Intersections with Asia and Global Markets

Trade Corridors Linking Africa, MENA and Asia

Africa’s crypto economy does not exist in isolation; it is deeply intertwined with developments in Asia and the wider Global South. Trade between Africa and Asia, particularly China, India and Southeast Asia, has grown rapidly over the past two decades, and remittance and investment flows have followed. Stablecoins and cross-border payment networks are beginning to serve these corridors directly. The Aptos ecosystem provides one concrete example, with integrations spanning Africa, Latin America and Southeast Asia via platforms like Juicyway, Yellow Card and others. By offering a single settlement layer for diverse corridors, Aptos is positioning itself as a backbone for south–south trade flows where traditional correspondent banking remains patchy.

HashKey’s Asia Connect network, launched from its base in East Asia and now extended into the Middle East and Africa via the Aptos–Daya corridor, embodies a similar ambition. In this model, Asian corporates can on-ramp local currency at one node, convert into stablecoins, route value to African counterparties, and off-ramp into local African currencies using Daya’s fintech infrastructure. The entire process is governed by a combination of local licenses, KYC/AML controls, and chain-level transparency, offering a hybrid between traditional trade finance and pure DeFi. For African exporters and importers dealing with Asian partners, these rails may offer more predictable settlement times and costs than letters of credit or open-account trade through smaller banks.

Other global players, including Ripple and major card networks, are similarly knitting together Asia–Africa routes through stablecoin-based products and partnerships. As more of these corridors come online, liquidity in key stablecoins—particularly USDC and regionally focused tokens like USDA and RLUSD—is likely to deepen, lowering spreads and making on-chain FX more competitive. This, in turn, will make it easier for African businesses and individuals to operate in a multi-currency world where dollars, euros, and regional units coexist on a spectrum from fiat accounts to programmable tokens.

Investment Flows and Venture Capital

Global capital is also flowing into Africa’s crypto and digital infrastructure space, often framed as part of a broader bet on “digital leapfrogging.” BitValue Capital’s 200 million USD Africa Growth Fund II is one example, dedicated to building “revolutionary digital infrastructure” through an “energy computing industry closed-loop model.” The fund’s strategy includes deploying privacy-preserving AI node centers and leveraging Africa’s energy resources for digital power distillation, with clear overlaps with blockchain validation and data center operations. By aligning incentives among energy producers, data center operators, AI platforms and blockchain ecosystems, such funds aim to extract more value from Africa’s position in global commodity and digital value chains.

Venture investment has also targeted payment and stablecoin-focused startups, including exchanges, on-ramp providers, and API platforms. Partnerships like Crossmint–Paga, DPTPay–Polygon, and Daya–Aptos–HashKey illustrate how VC-backed infrastructure is being localized for African contexts. For global funds, Africa offers a laboratory where real-world payment problems are acute and where incumbents may be less entrenched than in advanced economies. For local founders, access to capital and technical expertise can accelerate product development but also raises questions about control, data ownership, and alignment with local development priorities.

At the same time, the fallout from projects like Goldfinch underscores the need for more disciplined underwriting and realistic return expectations. When global capital chases double-digit yields in opaque credit markets under the banner of DeFi, the risk of mispricing and misaligned incentives is high. For Africa to benefit sustainably from crypto-related investment, a shift from “yield farming” mentalities to patient infrastructure and product investment will be necessary.

Most African jurisdictions lack clear crypto frameworks, creating operational uncertainty for fintechs; Kenya's 2025 law is the exception, not the rule across 54 nations.

Binance P2P suspension in Ethiopia and persistent FX shortages mean stablecoin markets have become the real-time price discovery layer for USD liquidity, exposing users to thin on-ramp/off-ramp depth.

- Smart-contract / CreditHigh

Goldfinch's uncollateralized lending model demonstrated that social-trust credit underwriting in frontier markets can produce loss rates that far exceed disclosed figures — $53.8M in troubled loans with claimed real losses above 70%.

Stablecoin infrastructure is consolidating around a small number of corridors — Yellow Card, VALR, Ripple/RLUSD, Circle/USDC — creating single-point-of-failure risk if any major operator loses a banking partner or license.

Dollar-pegged stablecoins hedge local currency collapse but concentrate users into USD exposure; de-dollarization policy pressure from governments creates a structural collision between user demand and state monetary goals.

Partnerships between crypto fintechs and traditional African banks (Nedbank, Credit Bank, Cassava) introduce counterparty risk on both sides — crypto volatility for banks, and charter/license revocation risk for fintechs.

How to Think About Africa as a Crypto Market

For crypto builders, investors and policymakers trying to make sense of Africa, a few analytical frames can be helpful. First, Africa is not a monolith; regulatory regimes, payment habits, and economic structures vary enormously between, say, Nigeria, Kenya, Egypt and Senegal. Any product or policy that treats the continent as a single market is likely to run into friction. Second, Africa’s crypto adoption is less about speculative trading and more about solving concrete payment and FX problems: remittances, merchant settlement, trade finance, and inflation hedging. Stablecoins dominate these use cases, making them a more important lens than native volatile tokens in many contexts.

Third, the most promising projects tend to integrate with existing rails—mobile money, banks, card networks—rather than attempting to bypass them entirely. Crossmint’s integration with Paga, Anzens’ work with Credit Bank, Mastercard’s USDC/EURC settlement, and VALR’s partnership with Onafriq all illustrate hybrid models where crypto provides new functionality while traditional institutions handle compliance and local distribution. Fourth, infrastructure matters: from L1 choice and node deployment to data center investment and developer tooling, the technical substrate of Africa’s crypto economy will shape which use cases can scale and how resilient they are to shocks.

Finally, risk management—regulatory, macroeconomic and consumer—is not a peripheral concern but central to the long-term viability of crypto in Africa. Projects that ignore FX controls or treat local laws as obstacles to be evaded risk provoking backlash that can set the sector back years. Conversely, well-designed pilots in sandboxes or supervised environments can build trust and pave the way for more permissive frameworks. The interplay between stablecoin adoption, dollarization, and monetary sovereignty will be one of the defining policy debates, with Africa’s experience offering lessons for other regions grappling with similar issues.

Outlook

Africa’s role in the global crypto economy is likely to expand as stablecoin rails mature, regulatory experiments proceed, and digital infrastructure investments bear fruit. In the near term, expect continued growth in cross-border stablecoin payments, deeper integration between crypto platforms and mobile money or banking systems, and more corridor pilots linking Africa with the Middle East and Asia. Institutional involvement—from card networks to licensed exchanges and banks—will grow, bringing stricter compliance but also greater resilience and access.

Over the medium term, key variables will include how African regulators choose to treat stablecoins and DeFi credit, whether regional bodies like the African Union move toward harmonized frameworks, and how central banks balance CBDC initiatives with private-sector stablecoin innovation. The trajectory of macroeconomic conditions—particularly inflation, FX availability, and debt sustainability—will also shape demand for crypto-based alternatives. If managed thoughtfully, Africa could become a leading example of how stablecoin-based infrastructure can support financial inclusion, trade and digital sovereignty. If mismanaged, the continent risks a patchwork of bans, capital flight, and consumer harm that could slow progress for years.

For crypto builders and investors, the message is clear: Africa is not a side market to be addressed opportunistically, but a central arena where the promises and pitfalls of a stablecoin-first financial system are being tested in real time. The projects that succeed will be those that treat local realities—regulatory, cultural, and economic—not as constraints to be evaded, but as design inputs for durable, inclusive infrastructure.

Latest Africa news

Valr and Onafriq partner to enable mobile money funding for crypto accounts across 43 African markets.Trident Digital Tech Holdings and Ripple Strategy Holding sign strategic cooperation agreement to co-build a stablecoin payment system for Africa market.Kredete partners with Visa to roll out stablecoin-linked card payments across Africa and the Gulf, enabling seamless USDC spending at 150M+ merchants globallyPolygon expands DPTPay collaboration to push low-fee stablecoin payments across AfricaAfrica’s stablecoin market has moved beyond proving demand as regulators, banks and fintechs race to build the infrastructure needed for large-scale adoptionBinance P2P suspension in Ethiopia exposes Africa’s deeper FX crisis as stablecoin markets become the real-time price discovery layer for USD liquiditySources

- https://www.chainalysis.com/blog/subsaharan-africa-crypto-adoption-2025/

- https://www.facebook.com/AfricaFintechSummit/posts/a-growing-number-of-fintechs-now-see-stablecoins-as-payment-infrastructure-not-a/1307465651558350/

- https://www.instagram.com/p/DYFNEGlnLc1/

- https://x.com/0xPolygon/status/2066531132024500514

- https://www.crossmint.com/announcement/paga-partnership-announcement

- https://techafricanews.com/2026/06/05/hashkey-mena-leads-aptos-powered-stablecoin-corridor-pilot-linking-middle-east-and-africa/

- https://thedigitalbanker.com/anzens-and-credit-bank-partner-to-explore-crypto-based-stablecoin-settlement-for-banking-in-east-africa/

- https://kredete.io/blog/visa-africa-gulf-expansion/

- https://www.chainalysis.com/blog/africa-cryptocurrency-adoption/

- https://solarmagazine.com/solar-dao-launches-first-digital-autonomous-closed-end-solar-investment-fund/

- https://markets.businessinsider.com/news/currencies/valr-and-onafriq-deliver-mobile-money-access-to-digital-assets-for-millions-across-africa-1036007133

- https://www.globenewswire.com/news-release/2026/04/06/3268610/0/en/bitvalue-capital-launches-200m-africa-fund-ii-to-build-revolutionary-digital-infrastructure-via-an-energy-computing-industry-closed-loop-model.html

- https://cryptonews.net/news/market/32682992/

- https://www.instagram.com/p/DZaVZ3ZDqQn/

- https://aptosnetwork.com/currents/juicyway-integrates-aptos

- https://group.hashkey.com/en/newsroom/hashkey-mena-partners-with-aptos-and-daya-to-build-regulated-stablecoin-payments-corridor-initiative

- https://www.bitgo.com/resources/blog/bitgo-mena-launches-electronic-trading/

- https://www.mastercard.com/news/eemea/en/newsroom/press-releases/en/2025-1/august/mastercard-expands-partnership-with-circle-to-transform-digital-settlement-for-merchants-and-acquirers-in-region

- https://papers.ssrn.com/sol3/Delivery.cfm/5103105.pdf?abstractid=5103105&mirid=1

Community notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…