Deep dive into USDH, the Hyperliquid-native stablecoin born from a high-stakes issuer war, its integration with HYPE and pmUSDH, the SPACEX-USDH oracle shock, and its eventual sunset as Hyperliquid pivots back to USDC.

+6 sources across the wider coverage universe

Coinbase acquires Hyperliquid's USDH deployer, Native Markets, to switch All USDH into USDC2026-05

Coinbase acquires Hyperliquid's USDH deployer, Native Markets, to switch All USDH into USDC2026-05 Hyperliquid introduces pmUSDH, a tokenized Portfolio Margin deposit that lets users earn yield while using USDH deposits as transferable DeFi collateral.2026-03

Hyperliquid introduces pmUSDH, a tokenized Portfolio Margin deposit that lets users earn yield while using USDH deposits as transferable DeFi collateral.2026-03 Check out this comprehensive report on the USDH proposal wars by Zach from Stablewatch. It's a full 24 page analysis covering all 6 proposals, the most indepth yet."2025-09

Check out this comprehensive report on the USDH proposal wars by Zach from Stablewatch. It's a full 24 page analysis covering all 6 proposals, the most indepth yet."2025-09 USDH goes live on Hyperliquid with more than $16.50M minted already on HyperEVM2025-09

USDH goes live on Hyperliquid with more than $16.50M minted already on HyperEVM2025-09 Track validator support and staking flows for the USDH ticker governance vote on Hyperliquid2025-09

Track validator support and staking flows for the USDH ticker governance vote on Hyperliquid2025-09 USDH bidding is peak crypto. Bunch of multi-billion dollar companies CEOs having to fight like rats for their lives getting proposals in, but having to speak in cat and role grind discord just to submit. Simply amazing to witness. !rank.2025-09

USDH bidding is peak crypto. Bunch of multi-billion dollar companies CEOs having to fight like rats for their lives getting proposals in, but having to speak in cat and role grind discord just to submit. Simply amazing to witness. !rank.2025-09

USDH: The Rise, Governance War, and Sunset of Hyperliquid’s Native Stablecoin

A dollar-pegged stablecoin originally launched as the “native” unit of account on the Hyperliquid blockchain, USDH was designed to be a fully backed, fiat-redeemable asset tightly integrated into Hyperliquid’s derivatives exchange, before a subsequent strategic pivot saw the ecosystem re-center around USDC and begin sunsetting USDH in favor of a Coinbase-driven stablecoin stack. At the same time, the USDH ticker has become contested across crypto, with different issuers – from regulated firms to illicit platforms – reusing the symbol, turning “USDH” into a case study in how stablecoin brands, governance, and economics intersect.

What is USDH?

At its core, USDH on Hyperliquid was conceived as a dollar-pegged stablecoin intended to trade at roughly one United States dollar per token and to be redeemable 1:1 against dollar-denominated reserves such as cash and short-duration U.S. Treasuries. The token was meant to serve as the primary quote currency and margin asset for Hyperliquid’s on-chain perpetual futures and spot markets, similar to how USDT or USDC function on centralized exchanges, but with economics and governance tuned specifically for the Hyperliquid ecosystem. Unlike algorithmic stablecoins such as the now-defunct UST, USDH was proposed and implemented as a fully collateralized, off-chain-reserve stablecoin, avoiding reflexive mint-and-burn mechanisms in favor of traditional issuance and redemption flows managed by a designated issuer.

However, the name “USDH” does not refer to a single, permanent asset across all of crypto. Even within the Hyperliquid story, the ticker is best understood as a kind of slot controlled by governance, rather than as a monolithic, immutable token design. Hyperliquid’s validators and HYPE token stakers ran a competitive bidding process to decide which firm would issue the chain’s official USDH; the winner, Native Markets, deployed one version of a fiat-backed stablecoin under that brand, but the governance framework left open the possibility of switching issuers or architectures over time. Outside Hyperliquid, entirely unrelated projects have launched their own USDH-branded stablecoins, including at least one associated with a major illicit marketplace, further increasing the risk of confusion for users who focus on ticker symbols rather than issuers, chains, and contracts.

For that reason, when this explainer refers to “USDH,” it primarily means the Hyperliquid-native USDH issued by Native Markets, unless explicitly stated otherwise. That version of USDH is notable both because it was the subject of an unusually public “stablecoin war” among large issuers and because it has already traversed a full lifecycle from proposal and launch to planned sunset as Hyperliquid re-aligns around USDC following a strategic partnership with Coinbase. Understanding USDH therefore requires understanding not only its technical and economic design, but also the governance, validator politics, and market events that defined its trajectory.

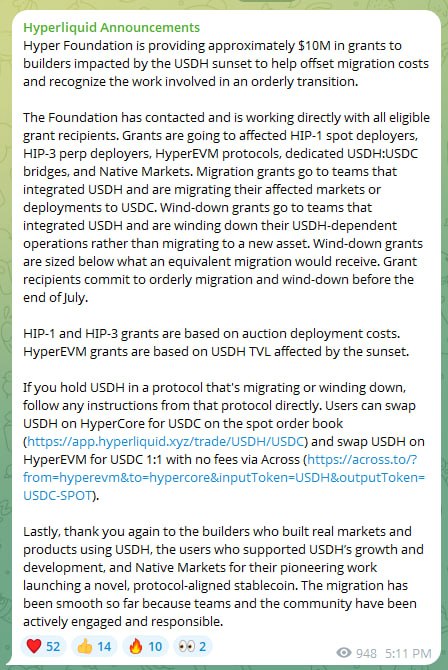

Hyper Foundation offers $10M in USDH sunset grants to HIP-1, HIP-3, and HyperEVM builders

Promoting from Tsunami auto-feed. Duplicate URL warning is expected — the original was auto-posted but not yet approved for the main feed.

Readers tracked the USDH saga not for stablecoin mechanics but for the political drama of who controls Hyperliquid's monetary layer — the top-clicked story being Coinbase's acquisition of the winner reveals that the entire proposal war ended with USDC dependency restored, the precise outcome the competition was designed to prevent.↗

Hyperliquid, HYPE and the Need for a Native Stablecoin

Hyperliquid as an On-Chain Derivatives Powerhouse

Hyperliquid is a layer-one blockchain specifically optimized for perpetual futures and spot trading of crypto assets, equities, commodities, foreign exchange, and synthetic markets, built around a high-performance on-chain order book. The chain’s native token, HYPE, plays the usual dual role seen in many modern L1s: it is used for staking and securing the network, and it aligns incentives among validators, traders, and governance participants who make decisions about protocol parameters and ecosystem partnerships. Beyond the flagship decentralized exchange often referred to as HyperCore, the ecosystem includes lending, real-world-asset integrations, and a fully featured EVM environment known as HyperEVM, allowing smart contract deployments interoperable with the exchange.

From its earliest growth phase, Hyperliquid relied heavily on USDC as the primary stablecoin for margin and settlement, mirroring the dominant role USDC and USDT play on centralized and DeFi venues alike. While this reliance delivered familiarity and deep liquidity, it also meant that critical monetary infrastructure on Hyperliquid depended on an external issuer’s business decisions, risk profile, and yield policies. Reserve yield on USDC’s underlying assets accrued to Circle and its partners, not to Hyperliquid validators or users, and the protocol had limited direct influence over how the stablecoin brand evolved. This dependency created both economic opportunity cost and governance risk for an exchange that aimed to be a full-stack on-chain trading platform rather than just a venue integrated into someone else’s stablecoin ecosystem.

Hyperliquid’s developers and community therefore began exploring the idea of a “native” stablecoin, one whose economics and governance would be expressly intertwined with the chain’s own tokenomics and validator set. In practice, this meant a stablecoin that would not just be widely used on Hyperliquid, but whose reserve yield, fee discounts, and ecosystem incentives could be routed back to HYPE stakers, validators, and users, strengthening the platform’s economic flywheel. The concept also aimed to create a more optimized trading experience: by denominating key spot pairs and some derivatives in a dedicated native stablecoin, Hyperliquid could offer lower fees and tighter integration with its portfolio-margin system, potentially differentiating itself from competitors.

Why a Native Stablecoin Mattered for HYPE and Validators

For HYPE holders and validators, a native stablecoin represented a chance to monetize the balance sheet that a successful trading platform effectively creates in the form of customer deposits and margin collateral. Reserve assets backing a fiat stablecoin are typically held in cash and short-dated treasuries that produce non-trivial interest income; the question is who captures that yield. By controlling the USDH brand and mandating that an issuer share a portion of reserve income or associated revenue with the protocol, Hyperliquid’s governance hoped to divert a stream of relatively low-risk, interest-based cash flow into the HYPE-centered economic system.

This dynamic set the stage for the USDH governance process: validators and HYPE stakers would effectively auction off the right to issue USDH to the highest bidder in terms of revenue share, growth incentives, and strategic value to the ecosystem. Revenue-sharing mechanisms included proposals to use reserve yield to buy and stake HYPE on behalf of token holders, or to direct a percentage of net revenues into ecosystem funds and validator rewards. By aligning a stablecoin issuer’s business model with HYPE’s success and validator security, the community aimed to transform what had been an external profit center (USDC reserves) into an endogenous driver of protocol value.

At the same time, Hyperliquid’s focus on institutional-grade derivatives, including pre-IPO products like SPACEX-USDH perpetuals, heightened the importance of having a reliable, liquid, and well-governed base stablecoin for margin and settlement. Institutions and sophisticated traders are sensitive to counterparty and stablecoin risk; a robust native stablecoin was seen as necessary infrastructure for scaling volumes and attracting more professional capital, especially if coupled with fiat on- and off-ramps controlled by reputable partners.

The USDH Governance War: Proposals, Validators, and Politics

The RFP and the “USDH War”

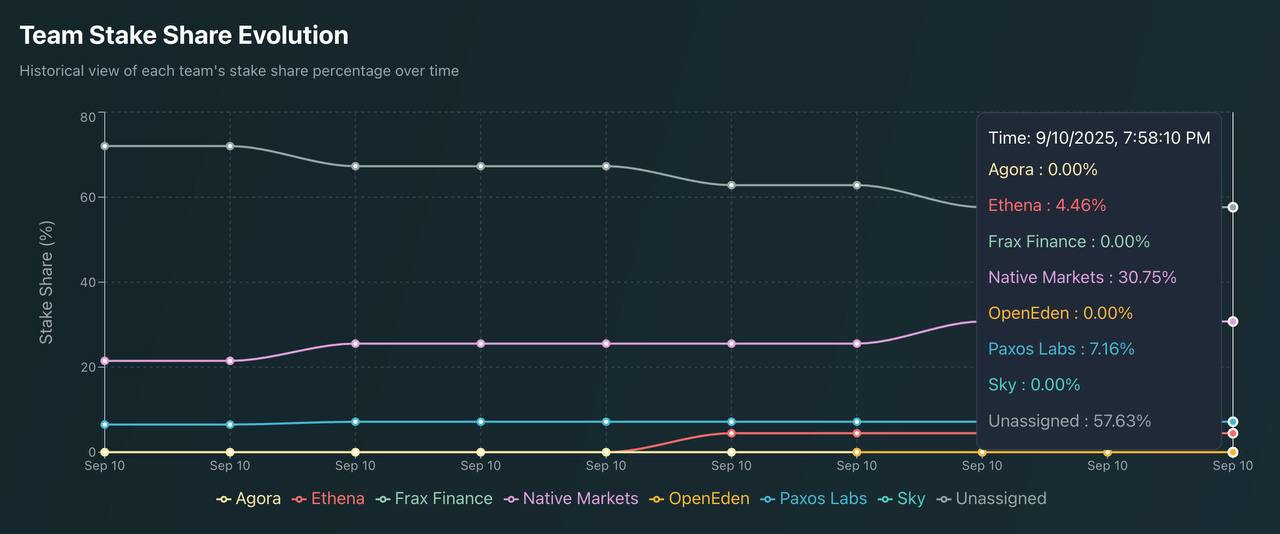

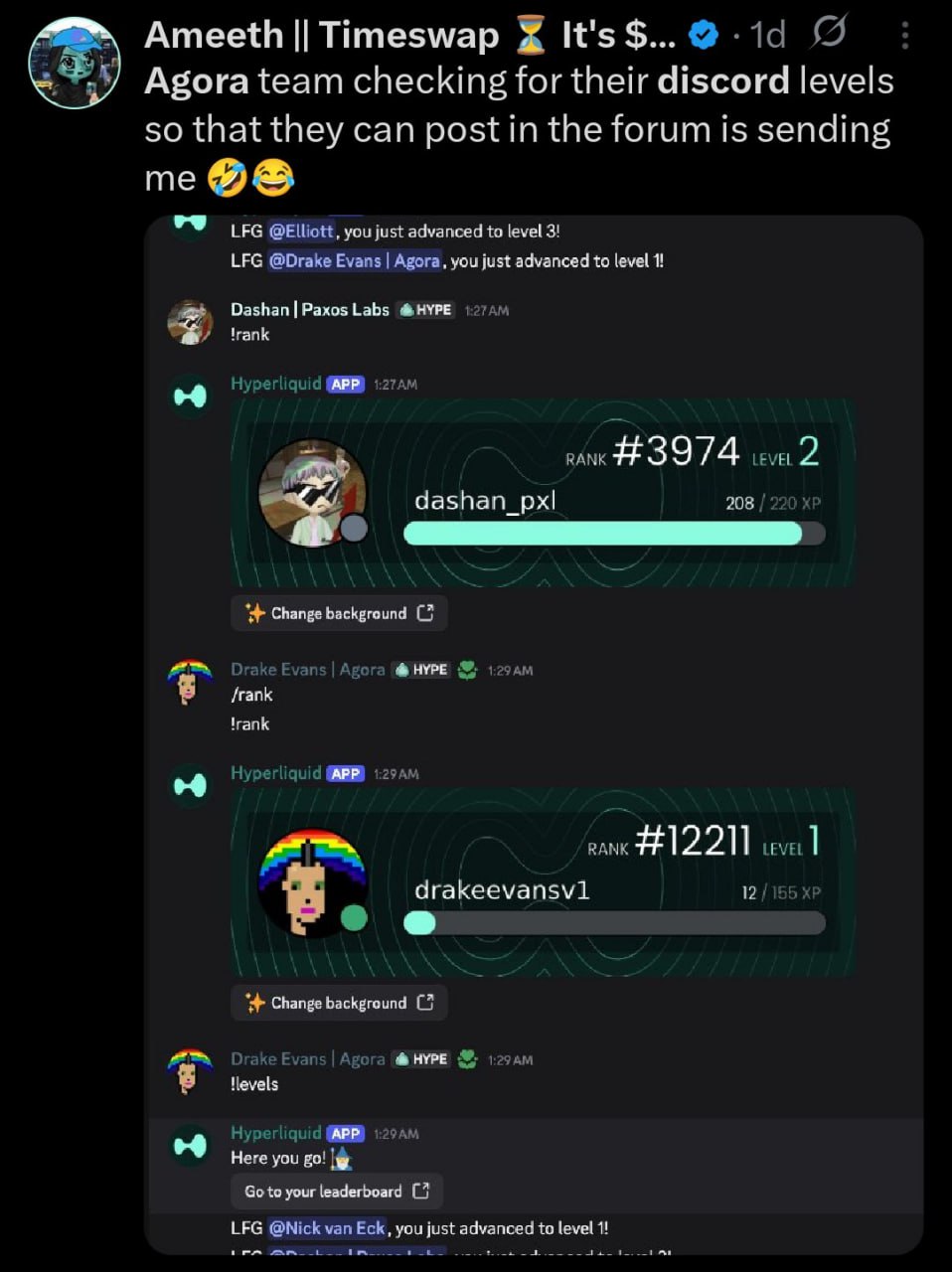

To choose an issuer for USDH, Hyperliquid’s foundation and core contributors published a request for proposals (RFP) inviting stablecoin providers to pitch the community on how they would design, issue, and steward the USDH asset. This process quickly turned into what onlookers dubbed the “USDH war” or “Hunger Games” for stablecoins, as multiple multi-billion-dollar companies and crypto-native teams competed intensely for the ticker. Coverage from analysts and newsletters emphasized how unusual it was to see executives from major stablecoin firms effectively campaigning in public Discord channels and governance forums, tailoring their proposals to anonymous validators and HYPE whales rather than traditional shareholders or boards.

Among the bidders were regulated stablecoin heavyweights like Paxos, teams associated with existing stablecoins such as Frax, and institutional custodians like BitGo, alongside a new entity formed specifically for the Hyperliquid opportunity called Native Markets. Each proposal offered different blends of regulatory posture, reserve management, on- and off-ramp integration, incentive budgets, and revenue-sharing formulas for HYPE stakers and the Hyperliquid treasury. Analysts at Galaxy and Oak Research produced detailed breakdowns comparing the proposals’ economics and risk trade-offs, underscoring how high the stakes were for both the chain and the issuers.

Competing Designs: Paxos, BitGo, Native Markets and Others

The Paxos camp emphasized its history as a New York-regulated trust company and its track record issuing stablecoins like USDP and PYUSD, arguing that a USDH backed by regulated custody and overseen by U.S. banking regulators would minimize compliance risk for Hyperliquid. In a revised “USDH v2” proposal, Paxos reportedly partnered with PayPal, offering tens of millions of dollars in incentives, potential listings of HYPE on PayPal and Venmo, and a revenue-sharing structure where a portion of reserve yield would be allocated to the protocol only after the stablecoin scaled beyond certain thresholds. The pitch aimed to trade somewhat lower early revenue share for the promise of mainstream distribution and institutional credibility.

BitGo’s proposal, by contrast, highlighted a model where each USDH token would be fully backed 1:1 by liquid U.S.-dollar-denominated assets such as cash and short-duration Treasuries, custodied in segregated accounts and audited regularly. BitGo proposed issuing USDH natively on Hyperliquid’s HyperEVM and making it interoperable with HyperCore, while enabling 24/7 minting and redemption across USDC, USDT, fiat via integrated banking rails, and other supported assets. A distinctive feature of the BitGo design was the use of reserve proceeds to buy back and stake HYPE, distributing rewards pro rata on-chain to the community, thereby tightly coupling USDH adoption to HYPE demand and staking yields.

Meanwhile, Native Markets emerged as a dark horse contender. Described in reporting as a new organization created specifically to compete for the right to issue USDH, Native Markets positioned itself as a Hyperliquid-first operator willing to deeply integrate with the chain’s infrastructure and governance. Its expanded proposal underscored that USDH would be native to Hyperliquid, issued on HyperEVM with seamless interoperability to HyperCore, and designed to maximize utility for traders through tight integration with portfolio margin and DeFi primitives on the chain. While Native Markets did not bring the same pre-existing regulatory brand recognition as Paxos or BitGo, its pitch leaned heavily on alignment with the Hyperliquid ecosystem and more aggressive sharing of upside with HYPE stakeholders.

Other bids and stakeholders added further complexity. Frax and other crypto-native projects reportedly floated hybrid models that blended overcollateralized crypto backing with fiat reserves, though these designs faced scrutiny from risk-averse validators wary of exposing a core settlement asset to crypto market volatility. A separate entity associated with a large Hyperliquid-aligned stablecoin known as USDT0 signaled that it would not submit its own USDH proposal but would continue supporting Hyperliquid regardless of the outcome, framing its role as a committed ecosystem partner rather than a direct competitor for the ticker. Across proposals, a central question was how much control and revenue the issuer would retain versus how much would be ceded to Hyperliquid’s governance and HYPE stakers.

Validator Power, Governance Drama and Allegations

Because the USDH issuer was to be chosen by validators and HYPE stakers, the RFP process thrust these on-chain stakeholders into a role more commonly associated with corporate boards or government regulators. Validators had to weigh not only headline incentive numbers and revenue share but also legal, operational, and reputational risks: a generous revenue split would be of little value if the issuer failed, faced enforcement action, or lost the peg during market stress. Research outlets like Oak Research framed the governance choice as a delicate balance between maximizing yield for HYPE holders and preserving the safety and neutrality of the core monetary layer.

Unsurprisingly, such high stakes fostered political controversy. Some commentators, including prominent venture investors, alleged that the competition might be “rigged” or influenced by behind-the-scenes deals, pointing to how quickly certain proposals appeared after the RFP and speculating that some teams had advance notice or privileged access. While concrete evidence of foul play was lacking, these accusations underscored the perception risk that arises when billion-dollar decisions depend on relatively opaque validator dynamics and social relationships. The very public nature of stablecoin issuers lobbying anonymous validators, sometimes in informal chat channels, was both celebrated as “peak crypto” and criticized as chaotic governance theater.

Ultimately, after rounds of community discussion and shifting validator alignments tracked publicly by analysts, Native Markets emerged as the winning bidder for the USDH ticker. This outcome surprised some observers who had expected a more established regulated firm like Paxos or BitGo to prevail, but it reflected the Hyperliquid community’s appetite for a highly aligned, chain-native partner willing to optimize specifically for Hyperliquid’s needs rather than treat USDH as another generic cross-chain product. With the vote decided, the spotlight shifted from governance to execution: how would Native Markets implement USDH in practice, and would it deliver on the promises of deep integration and attractive economics for HYPE stakeholders?

- 01multi-bidder proposal war spectacle↗

The sight of billion-dollar firms — Paxos, Frax, Agora, Native Markets, Sky — drafting competing proposals and lobbying validators in public Discord channels read as live reality television, driving sustained engagement across every stage of the contest.

- 02Coinbase acquisition ends USDC independence↗

The top-clicked headline revealed that Native Markets, the winning USDH deployer, was acquired by Coinbase and the stablecoin converted to USDC — an ironic reversal of Hyperliquid's stated goal of reducing USDC reliance.

- 03governance legitimacy and backroom deal accusations↗

Dragonfly's Haseeb Qureshi publicly claiming the contest was rigged and that Native Markets had advance notice of the RFP crystallised reader anxiety about whether validator votes on high-stakes economic decisions can be trusted.

- 04Stripe-Tempo sovereignty risk↗

Community warnings that a Stripe-linked proposal would hand Hyperliquid's monetary layer to a competitor building its own chain (Tempo) via Privy touched a live nerve about economic capture of a supposedly sovereign L1.

- 05HYPE tokenomics tied to stablecoin yield↗

Proposals routing reserve yield to HYPE buybacks — and the downstream VanEck ETF filing — framed the USDH winner selection as a direct lever on HYPE token value, pulling in stakers and speculators alike.

- 06pmUSDH and collateral composability

The launch of pmUSDH as a transferable, yield-bearing DeFi collateral token extended the USDH narrative beyond governance into concrete DeFi utility, attracting a separate reader segment focused on yield mechanics.

Native Markets’ USDH: Design, Integration and pmUSDH

Issuance Model, Backing and On/Off-Ramps

In line with the expectations set during the bidding process, the USDH implemented by Native Markets on Hyperliquid followed a fully collateralized, fiat-backed model, avoiding algorithmic stabilization mechanisms. USDH was issued natively on HyperEVM, the EVM-compatible environment of Hyperliquid, with seamless interoperability to HyperCore, the core exchange layer where perpetual and spot markets are hosted. This architecture allowed traders to use USDH as margin and settlement currency on HyperCore while interacting with DeFi protocols and other smart contracts on HyperEVM using the same asset, reducing fragmentation between trading and broader DeFi activity.

Although detailed reserve disclosure varied over time, Native Markets’ design drew heavily on the template used by other fiat-backed stablecoins, pledging to back each USDH 1:1 with USD-denominated liquid assets such as bank deposits and short-duration U.S. Treasuries. Users could mint USDH by depositing supported assets including USDC, USDT, and in some configurations even fiat currency via integrated banking rails, and could redeem USDH back into those assets at par, subject to standard compliance checks and potential fees. This multi-asset mint-and-redeem pathway was intended to give traders flexibility in onboarding capital into Hyperliquid while maintaining the dollar peg through arbitrage between on-chain and off-chain redemption channels.

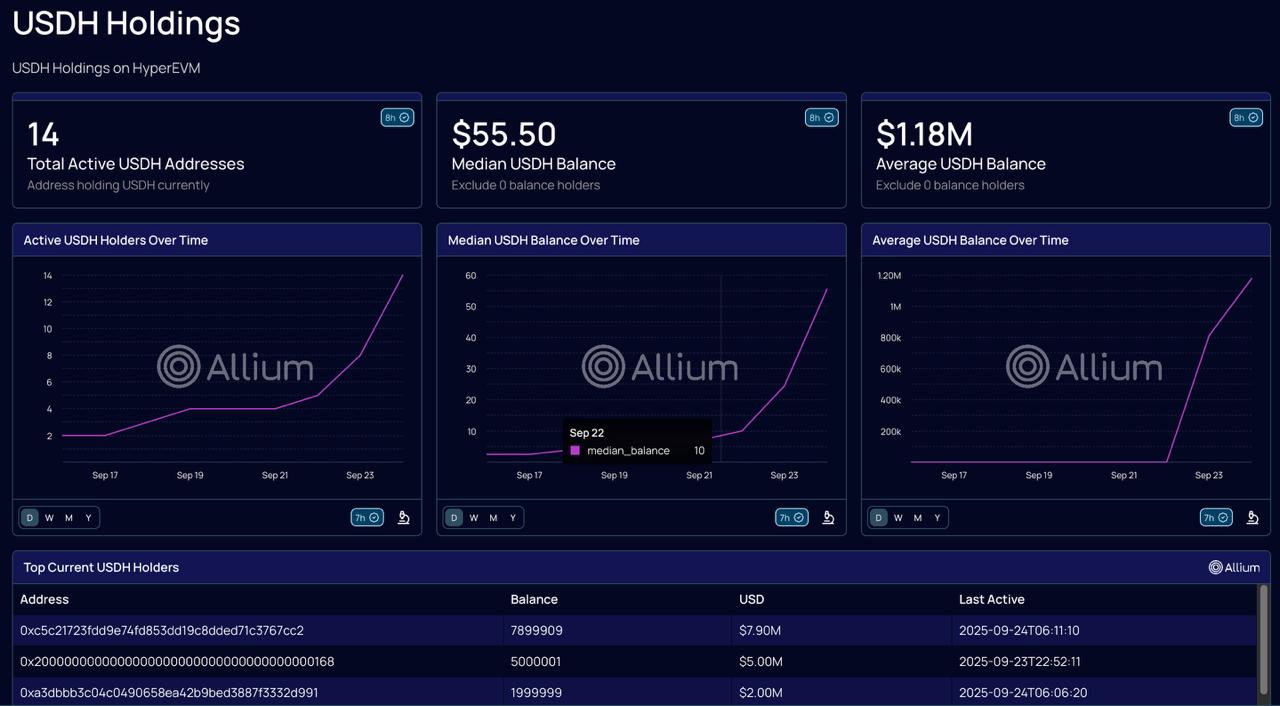

From the start, USDH’s design placed heavy emphasis on throughput and low friction for Hyperliquid users. Marketing materials and ecosystem commentary highlighted that USDH was meant to offer “the lowest fees and fastest free onramp” to Hyperliquid, positioning it as a superior gateway for active traders relative to routing capital through external stablecoins and bridges. The stablecoin went live with a non-trivial initial supply on HyperEVM—reports at the time cited more than roughly sixteen million dollars equivalent minted shortly after launch—signaling early uptake among users attracted by incentive programs, fee discounts, and Hyperliquid’s growing derivatives volumes.

USDH in Hyperliquid Markets and Fee Structures

One of the central promises of a native Hyperliquid stablecoin was that it would reshape market structure on the exchange. When Hyperliquid announced the USDH initiative, it signaled that selected spot pairs would be denominated in USDH and benefit from significantly lower trading fees—up to an 80% reduction relative to equivalent USDC-based pairs. This fee differential was intended both to reward users who migrated liquidity and trading activity into the USDH ecosystem and to bootstrap depth in USDH markets so that the stablecoin could credibly serve as the primary quote currency over time.

As USDH rolled out, it became a key unit of account for spot and perpetual markets on Hyperliquid, especially in portfolio-margin accounts where cross-collateralization allows traders to deploy USDH alongside other assets to support leveraged positions. The ability to deploy USDH as margin across a wide range of synthetic markets—from major cryptocurrencies to exotic pre-IPO products—added utility beyond simple value storage. For Hyperliquid’s architecture, a stablecoin tightly coupled to portfolio margin mechanics and fee incentives stood at the heart of how traders experienced the platform’s risk engine.

The economics extended beyond traders to HYPE holders and validators. Although Native Markets’ exact revenue-sharing formula differed from other bidders, the general structure involved allocating a portion of reserve yield and fee revenues related to USDH back to the Hyperliquid ecosystem, in some cases via mechanisms that accumulated and staked HYPE or contributed to an asset fund that indirectly supported the token. In this way, USDH adoption was meant to feed a virtuous cycle: more trading and margin in USDH would expand reserves and yield, which in turn would increase rewards for HYPE stakers and validators, reinforcing the security and attractiveness of Hyperliquid as a whole.

pmUSDH: Tokenizing Portfolio Margin Deposits

One of Native Markets’ more innovative contributions to the USDH ecosystem was pmUSDH, a tokenized form of portfolio-margin USDH deposits. In traditional exchange margin systems, funds posted as margin are effectively locked; while they may earn some yield or rebates, they cannot simultaneously be deployed in external DeFi protocols. Hyperliquid and Native Markets sought to break down this silo by allowing users to tokenize their USDH margin deposits, creating a liquid representation that could be used elsewhere without fully untying the margin backing their positions.

According to Native Markets and ecosystem announcements, USDH deposited into portfolio-margin accounts could be transformed on-chain into pmUSDH, which remained usable as margin while also existing as a transferable ERC-20-like token on HyperEVM. This design meant that pmUSDH could serve as collateral in DeFi protocols, be supplied to lending markets, or be bridged to other chains via infrastructure like Across Protocol, effectively enabling traders to earn yield on their margin and integrate Hyperliquid’s exchange balances with the broader on-chain economy.

The pmUSDH model showcased how closely intertwined USDH was with Hyperliquid’s broader DeFi ambitions. Rather than treating the exchange and the chain’s DeFi layer as separate silos, Native Markets and Hyperliquid treated margin deposits as composable building blocks. This approach appealed to sophisticated users comfortable with the added complexity and risk of rehypothecating margin, though it also raised questions about systemic risk if failures in DeFi protocols or bridges fed back into the stability of margin collateral and, by extension, the perceived safety of USDH deposits.

Market Risk, Oracles, and the SPACEX–USDH Perpetual Incident

The SPACEX–USDH Oracle Failure

The complexity of using USDH as margin and settlement currency across a wide range of synthetic markets came into sharp focus during a notable incident involving Hyperliquid’s SPACEX–USDH perpetual contract. In a widely discussed episode, the price of this pre-IPO perpetual pair plunged nearly forty-five percent in about thirty minutes, dropping from roughly 2,277 USDH to about 1,254 USDH before recovering toward 2,169 USDH. This dramatic intraday move triggered liquidations of approximately 405 users across nearly 1,400 positions, erasing about 1.51 million dollars in notional value for affected traders.

Subsequent investigation indicated that the root cause was not a failure of USDH itself but an oracle data error. The team behind the relevant pre-IPO markets, sometimes referred to as Ventuals, stated that incorrect data returned by an off-chain data provider used as part of the oracle mechanism caused both the oracle and the mark price for the SPACEX market to move sharply and incorrectly. As a result, the system treated a spurious price drop as real, mechanically liquidating positions as if traders had suffered massive mark-to-market losses. Ventuals indicated that it had taken immediate steps to prevent similar incidents across its pre-IPO markets and was evaluating how to compensate affected users, though the ultimate resolution would depend on governance and insurance mechanisms.

Implications for USDH as a Margin and Settlement Asset

Even though the SPACEX–USDH incident stemmed from an oracle failure rather than a de-pegging or collapse of USDH itself, it highlighted the indirect risks that stablecoin users face when their tokens serve as core infrastructure in leveraged derivatives systems. Traders whose positions were liquidated lost USDH or equivalent value, seeing their stablecoin balances reduced despite the absence of any macro instability in the dollar peg. The episode underscored that from a user’s perspective, holding USDH inside a portfolio-margin account on Hyperliquid is very different from passively holding USDH in a non-custodial wallet; the former is entangled with the behavior of the exchange’s risk engine, oracle providers, and governance decisions around compensation.

This risk interdependence has important implications for how one evaluates “stablecoin safety”. A fiat-backed stablecoin may preserve its peg and honor redemptions, yet users can still suffer large USD-denominated losses if the venues and protocols where the coin is used experience bugs, oracle errors, or governance failures. USDH’s deployment at the heart of Hyperliquid’s derivatives stack thus magnified both its utility and its risk exposure: it enabled a rich tapestry of leveraged strategies and pre-IPO speculation, but also tied the experiences of USDH holders to the reliability of complex infrastructure beyond the stablecoin issuer’s direct control.

For the Hyperliquid community, the SPACEX–USDH incident became a stress test of the social contract underpinning the ecosystem. Debates emerged about who should bear losses from oracle failures—individual traders, protocol insurance funds, the market-maker operators, or external data providers. The answers to these questions feed back into the perceived attractiveness of using USDH on Hyperliquid: if users believe the system will socialize losses from infrastructure failures, they may price that risk into their participation; if they believe they will be left to absorb such shocks alone, they may reduce exposure or demand higher returns elsewhere. In either case, the episode illustrated that stablecoin design cannot be fully separated from the risk architecture of the platforms where the stablecoin circulates.

Hyperliquid opens USDH stablecoin RFP to issuers

Six proposals submitted; community pushback over Stripe-linked bid

Validator on-chain vote scheduled for September 14; Native Markets wins

- 2025-10launch

USDH goes live on HyperEVM with $16.5M minted at launch

- 2025-11milestone

pmUSDH launched as transferable portfolio-margin DeFi collateral

Coinbase acquires Native Markets; USDH brand assets transferred, stablecoin converted to USDC

Hyperion DeFi announces USDH sunset and unwind of $29M HYPE deals

Pivot Back to USDC and the Sunset of Hyperliquid’s USDH

Coinbase, USDC, and a Strategic Realignment

While USDH launched amid great fanfare as Hyperliquid’s native stablecoin, the medium-term trajectory of the ecosystem took an unexpected turn when Coinbase and Hyperliquid announced a major partnership centered on USDC. Coinbase revealed that it would become the official treasury deployer of USDC on Hyperliquid, expanding support for on-chain markets on the chain and integrating its stablecoin operations more tightly with Hyperliquid’s exchange. Under this arrangement, Coinbase would manage USDC reserves and flows on Hyperliquid, effectively anchoring the ecosystem’s primary fiat stablecoin to a large, regulated U.S. public company.

At the same time, reports indicated that Coinbase and Hyperliquid reached an agreement under which most of the reserve yield from USDC held within the Hyperliquid ecosystem would be shared with the protocol, rather than accruing solely to the issuer. This shift directly addressed one of the original motivations for creating USDH: the desire for Hyperliquid and HYPE stakeholders to capture part of the yield generated by stablecoin reserves used on the platform. By negotiating a yield-sharing arrangement around USDC, Hyperliquid effectively reproduced much of the economic value proposition of a native stablecoin without bearing the operational and regulatory complexity of running its own branded fiat stablecoin through a less established issuer.

This realignment had immediate consequences for USDH’s strategic position. If USDC could now function as a de facto native stablecoin on Hyperliquid, complete with revenue sharing and official integration, the rationale for maintaining a separate USDH brand diminished. USDC already enjoyed broader adoption, deeper liquidity across chains, and a more widely understood risk profile. From an ecosystem perspective, consolidating around USDC while still capturing reserve yield could reduce complexity, avoid brand confusion, and mitigate regulatory uncertainty associated with newer issuers.

Coinbase’s Acquisition of Native Markets and USDH Brand Assets

The convergence between Hyperliquid and USDC went even further when Coinbase reportedly acquired Native Markets, the entity that had been serving as the USDH issuer on Hyperliquid. In tandem with this acquisition, Coinbase is said to have taken control of key USDH brand assets, including the deployer rights associated with USDH contracts on Hyperliquid. The strategic intent, as summarized in public commentary, was to convert all outstanding USDH into USDC and formally sunset USDH as a separate stablecoin line within the Hyperliquid ecosystem.

While full transaction details have not been publicly disclosed in all outlets, this move can be interpreted as a consolidation strategy. By absorbing Native Markets and its USDH infrastructure, Coinbase could both smooth the migration path for users—facilitating redemptions and conversions into USDC—and prevent fragmented or unauthorized use of the USDH brand on Hyperliquid post-sunset. For Hyperliquid’s governance, transferring the effective USDH slot to a USDC-centric model backed by Coinbase’s balance sheet and regulatory posture simplified the ecosystem’s stablecoin story: USDC would again sit at the center, but now with direct economic alignment via yield sharing and deep integration.

With the sunset plan in motion, USDH on Hyperliquid entered a winding-down phase. New minting would eventually be halted, while existing USDH holders would be encouraged or required to redeem their tokens for USDC at par through designated pathways. Collateral and margin systems that had previously treated USDH as a primary asset would be reconfigured to support USDC as the canonical stablecoin. Derivatives pairs and spot markets quoting in USDH would be migrated or retired in favor of USDC pairs, minimizing disruption while steering liquidity into the post-sunset architecture.

Hyperion DeFi, HYPE Flows and Second-Order Effects

The decision to sunset USDH also rippled into the broader Hyperliquid-aligned DeFi ecosystem, where various entities had structured deals and strategies around expectations of USDH’s long-term centrality. One particularly visible example was Hyperion DeFi, a firm that had previously committed substantial amounts of HYPE tokens to strategies involving USDH-related partners such as Native Markets and Felix Markets, a perpetuals venue whose markets were paired against USDH.

In public filings and announcements, Hyperion DeFi disclosed plans to unwind approximately twenty-nine million dollars’ worth of HYPE-related deals tied to Native Markets and Felix in light of the USDH sunset and Felix’s decision to close its perpetuals exchange. The company indicated that about 300,000 HYPE previously committed alongside Native Markets had become available for redeployment once that partnership ended on June 3, and that another roughly 500,000 HYPE associated with Felix would be freed as Felix wound down by late June, bringing the total expected return to the treasury to roughly 800,000 HYPE.

Importantly, Hyperion framed these developments not as a passive liquidation of positions but as the repatriation of capital for more profitable strategies in a changed environment. The firm emphasized that none of its other partnerships were materially impacted by the USDH sunset and that it planned to redeploy the returned HYPE into new opportunities rather than withdraw from the Hyperliquid ecosystem. Market commentators nevertheless scrutinized the potential impact of such sizable HYPE flows on token liquidity and price dynamics, particularly in conjunction with Ethereum market sentiment and broader DeFi risk-off periods.

From a systemic perspective, the Hyperion episode demonstrates how stablecoin governance decisions propagate through the broader DeFi stack. When a chain or major protocol pivots its chosen stablecoin, the impact is not limited to traders holding that asset; derivative venues, yield strategies, and tokenized exposure products built around that stablecoin may all need to be unwound or restructured. For HYPE and Hyperliquid, the USDH sunset thus served as a reminder that stablecoins are not just technical artifacts but also critical reference points for capital allocation, shaping where tokens, governance power, and risk ultimately reside.

Multiple USDHs: Brand Collisions, Illicit Use, and User Confusion

The USDH Ticker as a Contested Brand

As USDH’s story on Hyperliquid unfolded, the broader crypto ecosystem underscored a subtle but important reality: ticker symbols are not globally unique or legally protected identifiers. The ticker “USDH” has been used by more than one project over the years, including earlier stablecoins on other chains and new entrants unrelated to Hyperliquid. Some of these are benign or experimental DeFi projects; others are associated with riskier ventures and, in at least one reported case, with a large illicit marketplace.

This collision of brands matters because many users, especially those discovering assets via dashboards or price aggregators, tend to anchor on tickers rather than issuers or contract addresses. A trader who sees “USDH” on one chain may assume it is the same asset as “USDH” on another, overlooking differences in reserve backing, regulatory status, or governance. For more complex assets like USDH on Hyperliquid, where the token is deeply tied to a specific L1’s infrastructure and governance, this confusion can be particularly dangerous: taking assumptions about peg mechanisms or redemption rights from one USDH into another context may lead to mispriced risk.

The Hyperliquid case is especially instructive because the USDH ticker there was effectively governance-controlled, assigned through a validator vote to a specific issuer and then later re-aligned with USDC-centric infrastructure via the Native Markets acquisition. This shows that even within one chain, what “USDH” means can change over time as governance decisions reassign the brand to different implementations or phase it out entirely. Across chains and issuers, the situation is even more fragmented. Users must therefore recognize that a ticker is more like a nickname than a legal identity; the real questions are who issues the token, what backs it, and under which jurisdiction and governance regime it operates.

Illicit-Use USDH and Reputational Spillover

Reports of a USDH stablecoin launched by an illicit marketplace handling tens of billions of dollars in suspicious flows further complicate the brand’s reputation. While that USDH is unrelated to Hyperliquid’s Native Markets implementation or to Coinbase’s subsequent acquisition of USDH brand assets, the mere fact that the same ticker appears in connection with both regulated and illicit contexts risks reputational spillover. Observers unfamiliar with the distinctions may conflate the assets or assume a shared risk profile, especially when headlines shorten complex stories to ticker-level references.

This dynamic highlights a broader challenge in the stablecoin sector: name collisions and brand confusion are not just nuisances but can shape how regulators, institutional partners, and users perceive an asset. For Hyperliquid and its partners, aligning with USDC—a widely recognized and more carefully guarded brand—may partially reflect an awareness of these reputational dynamics. By relegating USDH to a sunset status on Hyperliquid and emphasizing USDC as the primary stablecoin, the ecosystem can more cleanly separate itself from any negative associations that other USDH-branded tokens may attract over time.

For users, the lesson is straightforward but often underappreciated: due diligence cannot stop at ticker symbols. Before holding, trading, or using any USDH, one must verify the chain, contract address, and issuer, and understand how that particular USDH is backed, governed, and regulated. The Hyperliquid USDH, while now in sunset, was a fiat-backed, exchange-integrated asset governed by HYPE validators and later subsumed into a Coinbase-driven USDC stack; an illicit-marketplace USDH is an entirely different instrument, with different issuers, controls, and legal exposure. Treating them as interchangeable would be a category error with potentially serious financial and legal implications.

The winning issuer, Native Markets, was acquired by Coinbase, consolidating USDH issuance under a single US-regulated custodian and reversing Hyperliquid's diversification rationale.

Public allegations of a pre-arranged outcome and validator vote concentrated among well-resourced bidders undermine the legitimacy of Hyperliquid's on-chain governance model for future high-stakes decisions.

Paxos and PayPal's compliance-first framing won validator favour, but Coinbase's acquisition now subjects USDH issuance to US regulatory constraints on a chain marketed as permissionless.

USDH launched with over $16.5M minted but ultimately sunset, with Hyperion DeFi unwinding $29M in HYPE deals tied to Native Markets, creating unwinding liquidity pressure across HyperEVM.

- Smart contract / protocolLow

No exploit of the USDH contract itself was reported; the primary risk realised was issuer-level (acquisition and sunset) rather than on-chain code failure.

USDH sunset announced June 2026 after Coinbase acquisition, leaving holders dependent on a migration path to USDC and exposing the fragility of a named-ticker stablecoin tied to a single corporate issuer.

USDH, USDC and Other Stablecoins on Hyperliquid: A Comparative View

Economic and Governance Trade-Offs

Hyperliquid’s journey from USDC reliance, to USDH experimentation, and back to a USDC-centric architecture with yield sharing provides a rich case study in stablecoin trade-offs. Initially, USDC on Hyperliquid functioned like any other cross-chain deployment: a highly liquid, widely trusted fiat-backed stablecoin issued by a regulated consortium, but with most reserve yield accruing to the issuer rather than the chain. USDH, issued by Native Markets, attempted to internalize that yield by tying reserve income and ecosystem incentives to HYPE and Hyperliquid’s governance, thereby making the chain’s “monetary base” more endogenous.

When Coinbase agreed to become the official USDC treasury deployer on Hyperliquid and to share most reserve yield revenue with the protocol, the economic gap narrowed dramatically. Hyperliquid could now enjoy a revenue stream similar in spirit to what USDH promised—participation in the interest earned on stablecoin reserves—without taking on the issuer risk and brand-building challenge of a new stablecoin. At the same time, USDC’s broader adoption across exchanges, DeFi protocols, and payment platforms made it a more convenient and familiar asset for users, especially institutional participants. In effect, Hyperliquid migrated from a world of “external but misaligned” USDC to “external but aligned” USDC, reducing the need for USDH as a separate brand.

Other stablecoins within the Hyperliquid orbit filled niche roles. USDT0, for example, was described by its operators as a Hyperliquid-aligned stablecoin and validator participant that would remain committed to the ecosystem regardless of the USDH vote, emphasizing a partner-first stance rather than a USDH-ticker-focused strategy. While USDT0 chose not to compete for the USDH slot, its ongoing support suggests that Hyperliquid benefits from pluralism in stablecoin options, even as governance chooses one primary unit of account and revenue-sharing stablecoin at the core.

A Simplified Comparison

The interplay between these assets on Hyperliquid can be summarized by considering their issuer, backing, governance alignment, and primary role within the ecosystem. The following table, while simplified, captures key contrasts between the main stablecoin configurations relevant to USDH’s evolution:

| Feature | USDH (Native Markets on Hyperliquid) | USDC on Hyperliquid (Coinbase deployer) | Other Hyperliquid-aligned stables (e.g., USDT0) |

|---|---|---|---|

| Primary issuer / operator | Native Markets, a Hyperliquid-focused entity | Circle/Center consortium, with Coinbase as on-chain deployer | Independent crypto-native teams aligned with Hyperliquid ethos |

| Backing model | Fiat-backed, 1:1 with USD cash and short-term Treasuries | Fiat-backed, 1:1 with USD cash and short-term Treasuries (USDC standard) | Typically fiat or crypto-backed; varies by stablecoin |

| Governance control of ticker | Hyperliquid validators assign USDH slot via vote | USDC ticker controlled externally; treasury deployment governed by partnership | Ticketers controlled by respective issuers and markets |

| Revenue / yield sharing | Reserve yield partially routed to HYPE / ecosystem | Majority of reserve yield on Hyperliquid shared with protocol | Case by case; not typically central to chain economics |

| Integration depth with exchange | Native to HyperEVM and HyperCore; tied to fee discounts | Deep, official integration as primary stablecoin after partnership | Used in specific venues and strategies, often secondary |

| Status in most recent architecture | Being sunset; USDH converted into USDC and phased out | Canonical stablecoin and unit of account after pivot | Ongoing but complementary, not central to governance decisions |

This comparison underscores that USDH’s main distinctives lay in its chain-native governance control and explicit integration with HYPE economics, not in backing or peg mechanisms, which were broadly similar to mainstream fiat-backed stablecoins. Once Hyperliquid succeeded in negotiating similar yield-sharing and integration features around USDC, the extra complexity of running a separate USDH brand became harder to justify.

Governance Lessons and Broader Stablecoin Takeaways

Validators as Monetary Policy Committees

One of the most intriguing aspects of the USDH saga is how clearly it shows L1 validators acting as de facto monetary policy committees. By voting on which issuer would control the USDH ticker, HYPE stakers and validators indirectly decided which balance sheet would underpin the chain’s primary stable unit, how reserve yield would be allocated, and what regulatory regime would govern a core piece of the ecosystem’s monetary infrastructure. This role goes far beyond choosing block parameters or approving minor protocol upgrades; it resembles the decisions of sovereign states choosing central bank partners or monetary anchors.

The process also surfaced the limits of on-chain governance. Validators had to synthesize complex information about legal regimes, custody arrangements, banking relationships, and compensation structures—topics often far removed from their technical expertise. While research outfits like Galaxy and Oak Research provided detailed analyses to aid decision-making, the final votes were still cast by token holders whose incentives and information varied widely. The allegations of favoritism or “backroom deals,” even if unproven, highlight the difficulty of ensuring that governance processes are perceived as legitimate and transparent when large economic stakes are involved.

The Power and Fragility of Economic Alignment

USDH’s creation and sunset also illustrate how economic alignment mechanisms can be powerful but fragile. The original motivation for USDH—capturing reserve yield and routing it to HYPE stakeholders—was compelling enough to justify a complex governance process and the launch of a new stablecoin. However, once Coinbase and Hyperliquid negotiated a comparable yield-sharing arrangement around USDC, the alignment that USDH created could be reimplemented via a different asset with stronger brand recognition and regulatory footing.

This dynamic suggests that alignment-based moats are only as strong as the alternatives available. If a chain depends on a third-party stablecoin without economic alignment, designing a native stablecoin like USDH can be a meaningful source of differentiation. But if the dominant external stablecoin is willing to share yield and integrate tightly, the added complexity of running a bespoke asset must be justified by additional benefits, such as greater sovereignty or regulatory flexibility. In Hyperliquid’s case, the calculus ultimately favored USDC once economic alignment was in place.

Stablecoin Brands in a Fragmented Regulatory Landscape

The USDH experience also speaks to the evolving nature of stablecoin brands in a fragmented regulatory environment. Firms like Paxos, BitGo, and Coinbase operate under different regulatory regimes and risk appetites; chains like Hyperliquid must decide which mix of regulatory exposure, censorship risk, and yield profile they are willing to embrace. The initial interest in Paxos and PayPal, with promises of integrating PayPal’s ecosystem and deploying large incentive budgets, shows the allure of marrying on-chain stablecoins with mainstream payment rails. At the same time, the final pivot toward USDC and Coinbase reflects the gravitational pull of incumbent brands that already enjoy broad regulatory and market acceptance.

Meanwhile, the emergence of illicit-use USDHs demonstrates that not all stablecoin issuers are playing by the same rules. This divergence raises the odds that regulators will treat stablecoins as a heterogeneous class, with stringent requirements for some and criminal scrutiny for others, further complicating life for chains that attach their monetary infrastructure to particular brands. For users and investors, this complexity reinforces the importance of understanding not just the on-chain mechanics of a stablecoin but also the off-chain legal and reputational context in which it operates.

Outlook

The story of USDH on Hyperliquid is already unusually complete for a relatively young DeFi asset: a governance-driven inception, a high-stakes competition among major issuers, a period as the chain’s native stablecoin integrated into portfolio margin and tokenized deposits, a market-stressing oracle incident, and finally a strategic sunset as the ecosystem re-centered around USDC and a Coinbase-led treasury model. For Hyperliquid, the episode delivered valuable experience in managing stablecoin governance, negotiating with large centralized issuers, and understanding how deeply a stablecoin’s design can affect HYPE economics, validator incentives, and downstream DeFi structures.

For the broader crypto industry, USDH stands as a case study in the political economy of stablecoins. It shows that the question of “which fiat-backed coin to use” is not merely technical; it touches on revenue distribution, regulatory risk, institutional partnerships, and the social legitimacy of governance processes. It also highlights the fluidity of stablecoin brands in an environment where tickers can migrate between issuers and chains, and where the same three or four letters can denote radically different instruments, from tightly regulated reserves to shadowy illicit-market tokens.

Looking ahead, the USDH brand may continue to surface in new contexts, but on Hyperliquid the center of gravity now lies with USDC, HYPE, and the validator-governed structures that mediate between them. Future experiments may yet revisit the idea of a deeply native stablecoin, perhaps under a different ticker or with novel collateral models, especially if regulatory or market shifts change the calculus around external issuers. Whatever form those experiments take, the lessons of USDH—about governance, alignment, risk, and brand ambiguity—will remain highly relevant for any protocol seeking to place a stablecoin at the heart of its economic system.

Latest USDH news

Sources

- https://usdh.com

- https://x.com/AcrossProtocol/status/2032943295463100705

- https://www.globenewswire.com/news-release/2026/06/08/3308030/0/en/hyperion-defi-reiterates-guidance-on-sunset-of-usdh-and-felix-markets.html

- https://tokenmetrics.com/hype/news/token-metrics-eth-bearish-hyperion-hype-deals/

- https://x.com/WuBlockchain/status/2060188182424256887

- https://www.coinbase.com/blog/coinbase-and-hyperliquid-aligning-markets-on-hyperliquid-to-usdc

- https://cryptorank.io/news/feed/ee028-paxos-paypal-partner-on-usdh-v2-proposal-with-20m-incentives-for-hyperliquid

- https://www.bitgo.com/resources/blog/usdh-proposal/

- https://bitcoinfoundation.org/news/defi/hyperliquid-stablecoin-shift-puts-usdc-back-again-at-the-center/

- https://stablecoindispatch.com/p/eurobanks-volume-8-03-10-25

- https://www.dlnews.com/articles/defi/paxos-frax-agora-and-native-markets-compete-to-build-usdh-stablecoin/

- https://www.techflowpost.com/en-US/newsletter/116785

- https://www.bankless.com/read/hyperliquids-usdh-bidding-war-2

- https://oakresearch.io/en/analyses/investigations/hyperliquid-usdh-war-detailed-analysis-opinion-proposals

- https://coinmarketcap.com/currencies/hyperliquid/

- https://x.com/zoomerfied/status/2054895066942931321

- https://seedalliance.org/wp-content/uploads/2017/04/2016_OSGC_Proceedings_FINAL_DIGITAL.pdf

- https://www.galaxy.com/insights/research/stablecoin-usdh-ticker-hyperliquid

- https://nativemarkets.substack.com/p/expanded-proposal-native-markets

- https://www.ainewscrypto.com/news/hyperion-defi-to-unwind-29m-hype-deals-with-felix-and-native-markets-as-usdh-sunsets

Community notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…