A decentralized, on-chain USD-pegged asset, fxUSD is the primary stablecoin of **f(x) Protocol**, minted against ETH and BTC collateral and tightly coupled to a novel leverage engine that splits yield and risk between stable holders and leveraged traders. By combining overcollateralized borrowing, protocol-native lever

fxUSD: A Decentralized Stablecoin at the Heart of f(x) Protocol

A decentralized, on-chain USD-pegged asset, fxUSD is the primary stablecoin of f(x) Protocol, minted against ETH and BTC collateral and tightly coupled to a novel leverage engine that splits yield and risk between stable holders and leveraged traders. By combining overcollateralized borrowing, protocol-native leverage, and yield from staked and lent collateral, fxUSD aims to offer a trustless alternative to centralized stablecoins such as USDC while addressing some of the structural flaws of traditional leverage products in DeFi.

Background: Stablecoins, Leverage, and the Push for “Trustless Dollars”

Stablecoins have become the unit of account and settlement layer for crypto markets, providing dollar-denominated liquidity in an ecosystem otherwise dominated by volatile assets like ETH and BTC. At a high level, today’s stablecoins fall into three broad categories: fiat-backed coins such as USDC that are redeemable against bank-held reserves; crypto-collateralized coins such as DAI that are overcollateralized by on-chain assets; and fully algorithmic designs that attempt to maintain a peg without explicit backing, a model that has largely fallen out of favor after high-profile failures. Each category makes different trade-offs between decentralization, capital efficiency, and stability, and the choice of stablecoin increasingly reflects a user’s appetite for custodial and regulatory risk versus smart contract and market risk.

Data aggregators such as DeFiLlama underscore how central stablecoins have become: their dashboards track aggregate stablecoin market cap, circulating supply, price stability, and flows across dozens of issuers, revealing that dollars on-chain now represent a substantial fraction of all value in DeFi. Within that landscape, fiat-backed coins still dominate both market capitalization and liquidity, thanks to their simple mental model and direct redeemability into bank money. Yet this dominance comes at the cost of heavy reliance on off-chain banking partners, blacklisting capabilities, and jurisdictional exposure, which has prompted parts of the Ethereum community to question whether such instruments are compatible with a credibly neutral, censorship-resistant base layer. Those concerns have intensified whenever reserve banks or issuers come under stress, reminding users that fiat-backed stablecoins live at the intersection of crypto and the regulated financial system.

In parallel, leverage has become ubiquitous in crypto markets, from centralized exchange margin to on-chain perpetual futures, options, and structured products. MetaMask’s own educational materials on leverage highlight how thin the margin for error can be: a 10x leveraged position typically has only around a 10% price cushion before liquidation, shrinking to roughly 5% at 20x and 2.5% at 40x, leaving traders highly exposed to routine volatility. In conventional leverage products, each account bears its own liquidation risk, meaning a sudden wick in price can wipe out individual traders even if the broader system stays solvent. Funding rates on perpetual futures further complicate the picture, as traders must pay ongoing fees to maintain directional exposure, turning long-term conviction trades into running cost centers.

This combination—centralized stablecoins as base money and fragile, funding-rate-driven leverage—has left DeFi with a paradox. On one hand, stablecoins and leverage enable sophisticated strategies and capital efficiency; on the other, they import off-chain risk and force traders into structures where funding costs and liquidation cascades can dominate investment outcomes. f(x) Protocol, and by extension fxUSD, emerged explicitly to address both sides of this problem by binding the stablecoin and leverage engines together in a single invariant-based system. Instead of treating stablecoins and leverage as separate products, f(x) ties them through a mathematical relationship that splits the risk and yield of underlying ETH and BTC between a stable tranche and a leveraged tranche.

The push toward what some researchers and builders now call “trustless stablecoins” sits squarely in this context. In a Leviathan News interview, a collective branding itself the Trustless Force argued that simply shifting around five percent of overall stablecoin holdings into fully on-chain, overcollateralized stablecoins—naming examples such as BOLD, fxUSD, and crvUSD—could meaningfully improve the resilience and decentralization of the stablecoin base layer. Their core criterion is that collateral should remain on-chain, transparently auditable, and free from reliance on banks or centralized issuers, even if that requires overcollateralization and complex on-chain risk management. Research outfits such as Pangea, which has analyzed designs like Curve’s crvUSD in detail, similarly frame these projects as attempts to build a more robust, monetary-policy-aware class of decentralized stablecoins.

Within this broader landscape, fxUSD positions itself as a composable building block that combines the familiar promise of a dollar peg with a distinctly DeFi-native architecture. It is designed not merely as a passive “tokenized dollar,” but as one leg of an engineered financial system whose other leg is a family of leveraged positions (xPOSITIONs) glued together through the f(x) invariant and supported by stability pools, reserve yield, and integration with external protocols. Understanding fxUSD therefore requires understanding not only how its peg works, but also how it shares risk and reward with traders seeking leveraged exposure to ETH and BTC.

f(x) Protocol aims to fix DeFi's stablecoin and leverage flaws by linking fxUSD, leveraged positions, staking yield, and liquidity into a single system managing $152M TVL and $56M supply

$56M fxUSD against ~$152M TVL is still a thin enough base that the stress variable is redemption depth when xPOSITION demand vanishes. f(x) makes leverage fees and wstETH/WBTC carry subsidize peg defense, cleaner than pure emissions, but it also couples stablecoin health to trader appetite. If ETH vol spikes while the fxUSD/USDC pool and Stability Pool stay bid with boring FXN incentives, the design earns credibility.

f(x) Protocol and the Origin of fxUSD

f(x) Protocol is a DeFi system incubated within the Aladdin DAO ecosystem that aims to create a less volatile, ETH-backed asset and complementary leveraged products by splitting the risk of underlying collateral through a custom invariant. A Dune Analytics description of the protocol summarizes the goal as providing a “less volatile, ETH-backed asset for users seeking lower risk and upside potential,” in contrast to purely fixed-value stablecoins or simple leveraged tokens. In its initial iterations, f(x) experimented with tranching ETH exposure into slices with different volatility profiles, effectively allowing users to choose where they sat on the risk spectrum while keeping collateral fully on-chain. This early work laid the conceptual foundation for fxUSD and the second-generation design of the protocol.

The central design idea is the f(x) invariant, a mathematical relationship that governs how changes in the price of underlying collateral are distributed between different tokenized claims. Instead of managing leverage via traditional debt and margin accounts, f(x) encodes leverage into the price behavior of distinct tokens that represent “stable” and “leveraged” claims on a shared collateral pool. When collateral prices move, the invariant dictates how value flows between these tranches, so that the stable side experiences minimal volatility while the leveraged side absorbs amplified gains and losses. In this architecture, the stablecoin is not simply backed by excess collateral in a vault; it is structurally intertwined with a complementary leveraged token, each being the other’s counterparty in a continuous, on-chain risk-sharing arrangement.

The launch of f(x) Protocol 2.0 marked a significant evolution of this design, introducing fxUSD as the flagship stablecoin and xPOSITION as a more generalized leveraged primitive. An in-depth technical review by MixBytes describes f(x) Protocol V2 as a stablecoin system whose stabilization mechanics involve dynamic rebalancing, redemptions, liquidations, specialized stability pools, and user positions arranged in a “concentrated-liquidity”-like structure. The review emphasizes that V2 not only refines peg management, including the introduction of price bands and more nuanced liquidation logic, but also integrates extensive interactions with external protocols such as Aave, Curve, and Morpho to source yield and liquidity. In parallel, an academic-style write-up on f(x) Protocol 2.0 highlights that xPOSITION introduces fixed-leverage trading with zero funding costs and no individual liquidation risk, positioning it as a novel DeFi primitive rather than a simple tweak to existing derivatives.

By design, fxUSD sits at the center of this architecture as the primary stable tranche backed by ETH and BTC collateral deposited into f(x)’s vaults. Users can mint fxUSD by depositing ETH or wrapped BTC through a mechanism called fxMINT, paying no ongoing interest and facing minimal liquidation risk, while retaining economic exposure to the underlying assets. On the other side of the invariant, traders can buy or mint xPOSITION tokens that deliver pre-defined leveraged exposure to the same collateral pool, with the f(x) invariant and stability mechanisms ensuring that the system as a whole remains solvent and that the fxUSD peg remains near one dollar. This co-design of stablecoin and leverage is what distinguishes fxUSD from more traditional crypto-collateralized stablecoins whose leverage ecosystem is largely external.

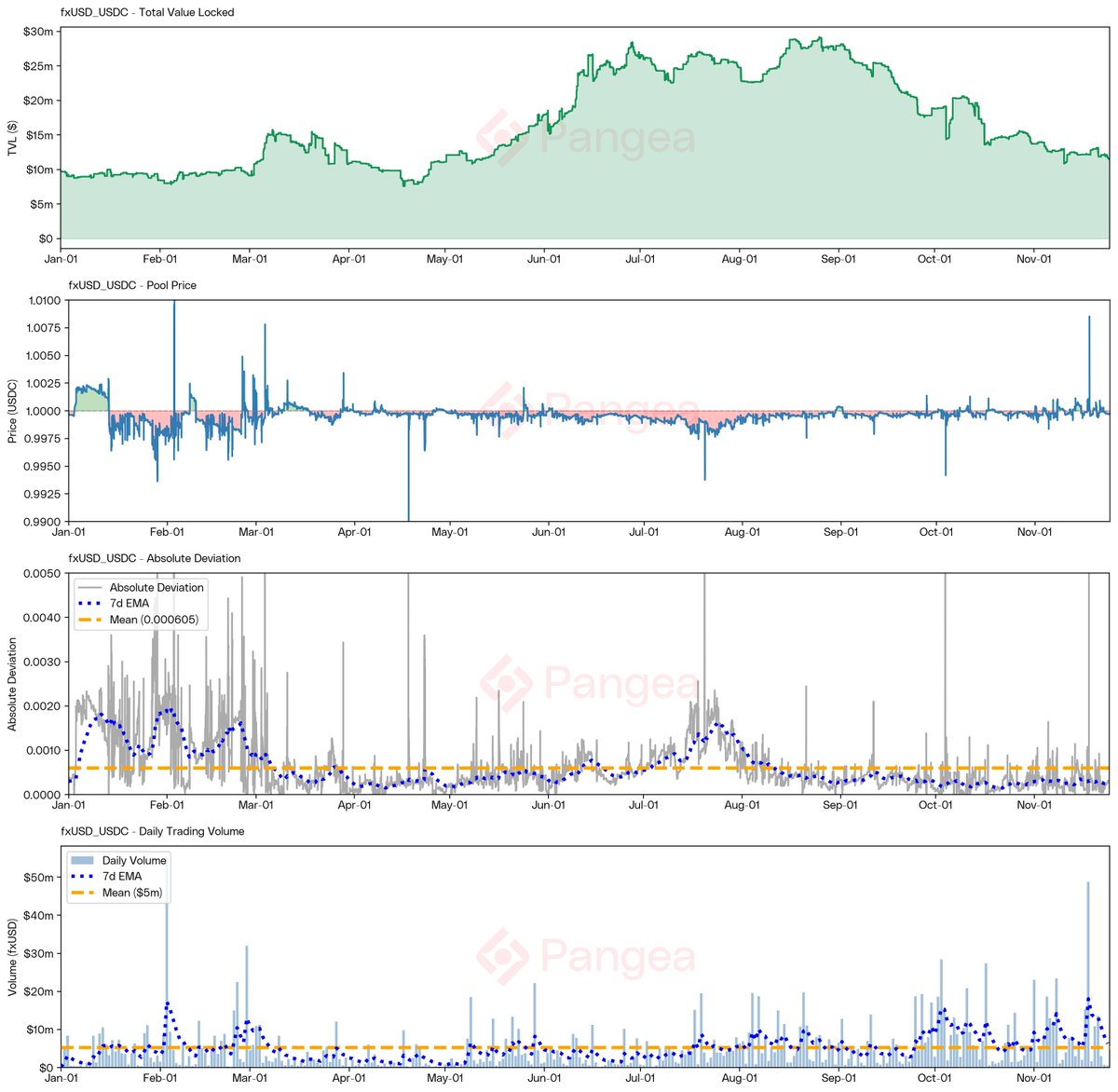

From a market perspective, fxUSD has transitioned from a niche experiment to a meaningful though still mid-sized player in the decentralized stablecoin space. Early coverage noted that shortly after launch, the protocol’s total value locked (TVL) was around the million-dollar mark, reflecting the cautious pace of initial adoption. Over time, integrations and product maturity led to compound growth. A later snapshot from Leviathan News highlighted that f(x) Protocol’s system was managing around $152 million in TVL with roughly $56 million fxUSD supply, reflecting both robust adoption of the stablecoin and the leveraged side of the system. More granular rankings show that fxUSD climbed into the top 30 stablecoins by market cap, with one update noting that it ranked #29 with over $39 million outstanding. DeFiLlama’s stablecoin dashboards and community Dune Analytics boards for f(x) offer users additional transparency into supply, peg behavior, and collateral composition over time.

Although numerical details such as TVL and market cap naturally fluctuate with prices and usage, the steady accumulation of liquidity across Curve, Convex, Morpho, and other integrations signals that fxUSD has moved beyond purely experimental status into what might be called the second tier of DeFi-native stablecoins. Crucially, this growth has occurred in parallel with increased emphasis on “trustless” design principles in the broader community, and fxUSD is frequently mentioned alongside peers like crvUSD and BOLD in discussions about how to reduce DeFi’s dependence on centralized stablecoins. With that backdrop, the mechanics of how fxUSD is minted, stabilized, and plugged into leverage become central to assessing both its potential and its risks.

How fxUSD Works: Collateral, Minting, and Stability Mechanics

At a high level, fxUSD is an overcollateralized, USD-pegged asset minted against ETH and BTC collateral deposited into f(x) Protocol vaults, with its stability maintained through a combination of overcollateralization, redemptions, liquidations, stability pools, price bands, and dynamic rebalancing. Unlike fiat-backed stablecoins that rely on an issuer’s off-chain reserves and redemption promises, fxUSD’s backing consists of on-chain assets such as ETH, wrapped BTC, and their staked or lent equivalents, often deployed into yield-generating strategies through protocols like Aave. The system’s distinctive feature is that the same collateral simultaneously supports fxUSD and a complementary set of leveraged positions, with a carefully designed invariant and stability framework ensuring that changes in collateral value are absorbed in a way that protects the peg. Users interact with this system primarily through three components: fxMINT for minting fxUSD against collateral, the f(x) invariant that splits risk between stable and leveraged tranches, and the Stability Pool that earns reserve yield and buffers liquidations.

Collateralization and fxMINT

The entry point for most fxUSD users is fxMINT, a minting module that allows users to borrow fxUSD directly against ETH and WBTC collateral while retaining exposure to the underlying crypto assets. According to f(x) Protocol’s documentation, fxMINT lets users deposit ETH or WBTC and mint fxUSD at a 0% annual interest rate, meaning there is no ongoing coupon or stability fee accruing on the borrowed amount. Instead of paying variable interest as in a traditional lending market, users pay a one-time open/close fee on the borrowed fxUSD, as emphasized in f(x) Protocol’s own social media communications, which state that “you pay only a one-time open/close fee on the borrowed fxUSD” while keeping your BTC/ETH exposure. This structure is designed to make long-term borrowing sustainable by avoiding the compounding burden of variable interest rates.

The absence of recurring interest is possible because the protocol captures yield from the underlying collateral—such as staking rewards on ETH or lending yield from Aave—and uses it to compensate stablecoin holders and liquidity providers rather than a centralized issuer. In effect, the foregone “interest income” that a bank or lending protocol might extract is instead recycled within the f(x) system, with fxUSD minters paying only upfront and exit fees while the ongoing yield on collateral accrues to the protocol’s internal accounting. From a user’s perspective, the ability to mint a stablecoin with no running interest charge and minimal liquidation risk is attractive for long-term holders of ETH and BTC who wish to unlock dollar liquidity without selling their assets.

The mention of “minimal liquidation risks” in the documentation is important. While fxMINT positions do face liquidation if collateral values fall far enough, the design of the f(x) invariant, price bands, and stability pool means that collateral buffers and system-level mechanisms absorb much of the volatility before individual positions are threatened. This contrasts with many CDP-style systems where each vault has a sharp liquidation threshold and relatively thin cushioning, so sudden price moves can quickly liquidate users even in non-catastrophic markets. By shifting part of the risk to leveraged counterparties and system-level stabilization, fxMINT aims to make borrowing fxUSD less fraught for long-term users, though it does not eliminate collateral risk altogether.

A further nuance is that the collateral deposited via fxMINT is not simply left idle; it is typically transformed into yield-bearing forms such as staked ETH (for example, wstETH) or supplied into lending protocols like Aave, with the resulting yield forming one leg of the system’s reward structure. The Stability Pool and reserve yield mechanisms, discussed below, are designed to channel this yield to users who help maintain the peg—such as stability providers—rather than to a central treasury. In combination, fxMINT’s 0% interest borrowing, the protocol’s use of yield-bearing collateral, and its invariant-based leverage design enable fxUSD to function not just as a passive stablecoin, but as the stable half of a yield-and-leverage sharing system.

The f(x) Invariant and Risk Tranching

At the heart of f(x) Protocol lies the f(x) invariant, an AMM-style mathematical relationship that governs how the value of collateral is split between the stablecoin (fxUSD) and leveraged positions (xPOSITIONs). While the precise formula is beyond the scope of this overview, the conceptual goal is clear: to create two or more tokenized claims on a shared collateral pool such that one claim (fxUSD) exhibits extremely low volatility around a target price of one dollar, while the other claim(s) exhibit amplified exposure to the underlying asset’s price movements. Community descriptions on Dune emphasize that the protocol aims to provide a “less volatile, ETH-backed asset for users seeking lower risk and upside potential,” implicitly contrasting it with the leveraged side of the system, which bears more risk in exchange for potential outsized returns.

In traditional collateralized lending systems, leverage is achieved by issuing debt (often denominated in a stablecoin) against collateral and allowing users to rehypothecate that debt into more collateral, creating recursive leverage. The risk is borne largely at the individual user level: fall below a loan-to-value threshold, and your position is liquidated. In f(x)’s invariant-based design, by contrast, leverage is encoded directly into the price behavior of xPOSITION tokens relative to the underlying collateral. When the price of ETH or BTC rises, xPOSITION tokens gain more than linearly, while fxUSD maintains its peg; when prices fall, xPOSITION tokens absorb more of the losses, cushioning fxUSD until extreme conditions. This is analogous to splitting a bond into senior and junior tranches, with the senior tranche (fxUSD) protected by the junior tranche (xPOSITION) that absorbs first losses in exchange for higher upside.

The invariant-based approach allows f(x) to offer fixed-leverage products—for example, xPOSITIONs that track 3x, 5x, or 7x exposure to ETH—without relying on ongoing funding rates or individualized margin calls. A write-up on f(x) Protocol 2.0 emphasizes that xPOSITION enables “fixed leverage trading with zero funding costs and no individual liquidation risk,” underscoring that the protocol’s mathematics, rather than periodic funding payments, maintain leverage and risk-sharing. From fxUSD’s perspective, this means that the stablecoin’s safety is underpinned by the existence of a leveraged counterparty whose returns are mathematically linked to the same collateral pool, rather than by external speculators in unrelated markets. The stability of fxUSD is therefore not purely a function of overcollateralization; it is a function of how effectively the invariant channels the consequences of price moves into leveraged positions and system reserves.

Compared with Maker-style CDPs or simple overcollateralized stablecoins, this structure is more explicitly tranching-based. In a Maker vault, for instance, the borrower both mints DAI and personally bears liquidation risk, while the system collects stability fees that can fund recapitalization in stress events. In f(x), the existence of xPOSITION as a junior tranche, together with yield from collateral and dedicated reserve pools, means that a larger share of market risk is absorbed before fxUSD holders are affected. This does not eliminate tail risk—extreme moves in ETH or BTC could threaten any crypto-backed stablecoin—but it does change the distribution of everyday volatility and the mechanics of how losses are socialized.

Price Bands, Redemptions, and Liquidations

Peg stability in fxUSD is maintained through a combination of price bands, redemptions, and liquidations, which together form a multi-layered stabilization scheme. The MixBytes analysis describes f(x) Protocol’s stabilization as being “based on price bands, liquidations, redemptions, reserve pools, and various additional stability measures,” highlighting that fxUSD does not rely on a single mechanism but rather on a toolkit of coordinated interventions. Price bands define a range around the one-dollar target within which the system tolerates minor deviations, reducing the need for continuous hard rebalancing and allowing natural market arbitrage to operate. Outside these bands, more forceful mechanisms such as redemptions and liquidations come into play to restore balance.

When fxUSD trades below its target price, arbitrage and protocol mechanisms are designed to create a profit opportunity for buying fxUSD and redeeming it for more than one dollar’s worth of collateral, or for adjusting positions so that demand for fxUSD increases. Because fxUSD is backed by a pool of ETH and BTC (and their yield-bearing variants), users who can redeem it for collateral at or near face value are incentivized to purchase it on the open market whenever the market price drifts significantly below one dollar. This redemption pressure removes discounted fxUSD from circulation and reduces system debt, while the injected demand supports the peg from below. In practice, redemptions also interact with the leveraged side of the system; when the stable side is redeemed, the effective leverage of remaining xPOSITIONs may increase, changing their risk profile and expected returns.

When fxUSD trades above its target price, the protocol encourages users to mint new fxUSD against collateral, sell it into the market, and thereby capture the premium. fxMINT makes this relatively straightforward: by depositing ETH or WBTC at 0% interest, users can mint fxUSD and immediately sell it if the price is materially above one dollar, pocketing the spread and helping to push the price back toward the peg. In this case, increased supply of fxUSD and the corresponding adjustments to the invariant and reserves ensure that the system remains overcollateralized while releasing additional stablecoins into circulation.

Liquidations come into play when collateral values fall to the point that certain positions become undercollateralized according to the protocol’s risk parameters. Rather than relying solely on external liquidators, f(x) uses specialized stability pools and reserve mechanisms to absorb such positions, selling collateral to stability providers at a discount and retiring corresponding fxUSD debt. This design aims to ensure that undercollateralized positions are resolved promptly and that the burden of absorbing losses is borne by actors who are both compensated via yield and explicitly opted into that role. Because the system also has access to external lending and liquidity via Aave and Curve, the liquidation engine can, in principle, tap into broader DeFi liquidity during stress events.

Price bands overlay these mechanisms as a kind of deadzone within which minor fluctuations are tolerated without heavy-handed intervention. By allowing fxUSD to oscillate within a narrow corridor around one dollar, the protocol reduces the need for constant redemptions and liquidations, minimizing unnecessary churn and transaction costs. This is conceptually similar to the way some algorithmic or hybrid stablecoins define soft bands around the peg, stepping in more aggressively only when deviations threaten to become persistent or systemic. In the case of fxUSD, however, the presence of overcollateralization, leveraged counterparty tranches, and reserve pools means that even outside the band, stabilization tools are backed by tangible on-chain assets rather than by purely reflexive monetary policy.

The Stability Pool and Reserve Yield

The Stability Pool is a central component in fxUSD’s design, serving both as a buffer for liquidations and as a conduit for distributing yield from the protocol’s collateral reserves. According to f(x) Protocol documentation, users can deposit fxUSD or USDC into the Stability Pool and, in return, earn yield sourced from the protocol’s wstETH and WBTC reserves as well as from Aave lending yields. In other words, the Stability Pool aggregates stablecoins that stand ready to absorb undercollateralized positions, and compensates depositors for this service by passing through the income generated by deploying collateral into staking and lending strategies. This arrangement allows fxUSD to offer organic yield on stable deposits that is directly linked to the performance of the underlying collateral, rather than relying solely on external token incentives.

From a risk perspective, Stability Pool depositors are effectively underwriting part of the system’s credit risk. When a position is liquidated, the pool may be used to cancel the debtor’s fxUSD and acquire their collateral at a discount, leaving depositors with exposure to the underlying assets rather than to fxUSD itself. If the liquidation system functions as intended and the discounts are correctly calibrated, depositors should, on average, profit from these events in addition to their share of staking and lending yield. However, they also bear the risk that in a severe market downturn, multiple liquidations and price slippage could erode returns or even lead to losses relative to simply holding stablecoins. The yield from wstETH, WBTC, and Aave is thus a risk premium paid to those who help backstop the system’s solvency and peg.

The MixBytes review highlights that f(x) Protocol V2 introduces a more sophisticated structure for such positions, describing user positions as being arranged in a “concentrated-liquidity”-like structure. In the context of fxUSD and its Stability Pool, this suggests that depositors may be able to choose how much price risk and liquidation exposure they are willing to bear, similar to how liquidity providers on Uniswap v3 can concentrate their liquidity in specific price ranges. A more granular design of this kind could, in principle, make the Stability Pool more capital-efficient by aligning risk preferences and expected yield more precisely, though it also increases complexity for users.

Community education around the Stability Pool, including detailed threads by contributors such as Cyrille, has emphasized that depositors can treat it as a delta-neutral strategy in which they hold stablecoins but earn yield derived from the leveraged counterparties and the protocol’s reserves. While such communications are promotional in tone, they reflect the underlying economic logic of the system: fxUSD holders willing to underwrite liquidations and peg stability are compensated by yield generated from ETH and BTC exposure that they themselves do not directly bear. This is a key part of fxUSD’s value proposition for yield-seeking DeFi users: it offers a way to earn return on stablecoins that is structurally tied to real collateral yields and trading flows, rather than to pure emissions.

In aggregate, the combination of fxMINT, the f(x) invariant, price bands, redemptions, liquidations, and the Stability Pool creates a layered stability mechanism for fxUSD. The invariant ensures that leveraged positions absorb much of the volatility; the Stability Pool and reserve yield compensate users who help absorb residual risk; and price bands and redemption logic align incentives for arbitrageurs and long-term participants to keep the price near one dollar. While the design is intricate and not trivial to explain to newcomers, it embodies a coherent attempt to engineer a decentralized stablecoin whose stability is grounded in on-chain collateral, explicit counterparties, and transparent incentive structures.

Leverage via xPOSITIONs and the Role of fxUSD

fxUSD’s design cannot be fully understood without examining xPOSITIONs, the leveraged tokens that share collateral and risk with the stablecoin. f(x) Protocol 2.0 explicitly frames xPOSITION as a novel DeFi primitive introducing fixed leverage trading with zero funding costs and no individual liquidation risk, thereby addressing some of the key pain points of perpetual futures and margin trading. In this architecture, each fxUSD in circulation is effectively balanced by a corresponding set of leveraged claims whose returns are governed by the f(x) invariant. fxUSD is thus not only a stablecoin, but also the “senior tranche” in a continuous on-chain risk-sharing arrangement between stable holders and leveraged traders.

xPOSITION: Fixed Leverage without Personal Liquidation

The key innovation of xPOSITION is its ability to deliver fixed leverage—for example, 3x, 5x, or even higher exposure to ETH—without requiring traders to manage margin, pay funding rates, or worry about the classic forced liquidation that characterizes margin accounts. In the language of the f(x) Protocol 2.0 write-up, xPOSITION allows users to engage in leveraged trading with “zero funding costs and no individual liquidation risk,” a striking departure from the standard perpetual futures model. Instead of constantly adjusting leverage via margin and mark-to-market PnL, xPOSITION tokens encode leverage into their price behavior, with the invariant ensuring that their returns track a multiple of underlying asset moves over a certain range.

By contrast, in traditional leverage systems such as those described in MetaMask’s primer on leverage, a 10x leveraged position affords a trader only around a 10% adverse price move before liquidation, with the buffer shrinking further at higher leverage levels. The trader must also pay or receive a funding rate, which compensates the side of the market that is net short or long in perpetual futures, making long-term directional positions costly if funding is persistently negative. These dynamics leave users vulnerable to sudden liquidations due to short-lived price spikes or wicks and can erode returns even when the broader thesis is correct. The combination of funding costs, margin calls, and liquidation cascades has been a recurring source of frustration in both centralized and on-chain derivatives markets.

In the f(x) model, xPOSITION holders are not subject to this kind of margin call. Instead, their leverage is encoded in the token’s payoff function relative to collateral, and they bear losses continuously as the price moves against them, rather than via discrete liquidation events. If ETH’s price declines significantly, the value of xPOSITION may fall much faster than spot ETH, but the holder is never forcibly closed out; their token simply becomes worth less in terms of both fxUSD and underlying collateral. Because there are no individual liquidations, there is also no need for individual liquidation penalties or auction processes on a per-account basis, which can simplify risk management and reduce forced selling pressure during volatile periods. The trade-off is that leveraged users must accept that the protocol will rebalance their exposure automatically as dictated by the invariant, and that in tail events, their tokens can lose a large share of value.

The elimination of funding costs is also significant. Because the stable side of the system (fxUSD and Stability Pool deposits) earns yield from underlying collateral and from the economic relationship with leveraged positions, the protocol does not need to charge ongoing funding fees to xPOSITION holders to remain solvent. Instead, the invariant and reserve design ensure that, over time, leveraged positions pay an implicit premium through their participation in a system where they absorb amplified volatility and share their upside and downside with stable holders. In this way, f(x) seeks to offer a more predictable and arguably more transparent form of leverage, though its complexity and risk-sharing model require careful explanation to end users.

Interaction between fxUSD and xPOSITION

The relationship between fxUSD and xPOSITION is that of two sides of the same balance sheet. When a user deposits ETH or WBTC into the protocol, they can, in principle, mint some amount of fxUSD and some amount of xPOSITION, subject to the invariant and collateralization constraints. The total economic claim on the collateral is split between these two classes of tokens: fxUSD aims to maintain a near-constant value in dollar terms, while xPOSITION fluctuates more than proportionally with the price of ETH or BTC. As price moves and users enter and exit positions, the invariant continuously recalibrates how much of the collateral’s value is notionally allocated to each side.

From a system-level perspective, fxUSD supply reflects demand for low-volatility, USD-denominated exposure to the collateral pool, while xPOSITION supply reflects demand for leveraged exposure. The f(x) invariant ensures that these demands are balanced such that the system remains solvent, and that there is always sufficient collateral backing the outstanding fxUSD, assuming parameters are set conservatively. When demand for leverage is strong, more xPOSITIONs are created, and the stable side may enjoy higher implicit premiums and yield; when demand for stable exposure is stronger, fxUSD may grow relative to leveraged supply, potentially reducing yields but increasing the robustness of the peg. In either case, fxUSD holders function as senior creditors whose position is protected by the junior leveraged tranche and by reserve pools.

Practically, this relationship is reflected in f(x) Protocol’s TVL composition. Coverage from Leviathan News has highlighted that at certain points, the system managed on the order of $152 million in total value locked, with approximately $56 million of that in fxUSD supply, implying a significant share of collateral was allocated to the stable side of the ledger. This aligns with the notion that, for the system to remain conservative, fxUSD should be overcollateralized and buffered by both leveraged claims and reserves. On-chain analytics, such as the Dune dashboards that track f(x) Protocol metrics, allow observers to monitor this balance in real time, including the relative size of stable and leveraged tranches.

For everyday users, the main practical implication is that holding fxUSD is not a claim on a centralized treasury but a claim on a dynamic system where leveraged counterparties and stability providers absorb much of the risk. In benign conditions, this enables fxUSD holders to benefit from collateral yield and robust peg behavior without dealing directly with leveraged products. In stressed conditions, the depth and resilience of the leveraged side and stability pools become critical: if xPOSITION holders and stability providers can absorb the shock, fxUSD remains stable; if not, the peg could be challenged. This interconnectedness is a defining feature of fxUSD and must be considered alongside its advertised benefits.

Flash Loans, External Protocols, and Capital Efficiency

A noteworthy aspect of f(x) Protocol’s architecture is its extensive use of flash loans and external DeFi primitives to improve capital efficiency and user experience. The MixBytes review notes that certain aspects of the system are “particularly innovative, including the use of flashloans to leverage positions,” underscoring that users can often enter and exit complex leveraged structures in a single transaction without manually managing intermediate steps. In practice, this may involve the protocol borrowing assets via a flash loan, depositing them as collateral, minting fxUSD and xPOSITION, and repaying the loan within the same block, leaving the user with their desired portfolio configuration. By automating these workflows, f(x) reduces friction for users who might otherwise be intimidated by the multi-step processes common in DeFi leverage strategies.

The protocol’s reliance on external yield sources and liquidity is equally central to fxUSD’s design. MixBytes highlights that f(x) “integrates extensively with external protocols such as Aave, Curve, and Morpho,” combining traditional lending primitives with staking and shares to construct its stability and yield mechanisms. For example, collateral deposited into f(x) may be further supplied to Aave to earn lending interest; in turn, the Stability Pool may route stablecoins into specific pools or strategies that complement the protocol’s risk management. Curve and Convex provide deep stablecoin liquidity, allowing fxUSD to trade against other stablecoins with low slippage, while also enabling the protocol and its users to earn additional rewards through liquidity mining and gauge incentives.

One recent development illustrating this composability is f(x) Protocol’s partnership with 9 Summits to launch an agentic fxUSD vault on Morpho, designed to bring leverage and liquidity to emerging AI-native assets. This vault uses Morpho’s optimized lending infrastructure and fxUSD’s trustless stablecoin properties to construct strategies where AI-related tokens can be financed and hedged more efficiently, reflecting how fxUSD is being used as a base currency for increasingly specialized DeFi applications. Similarly, the listing of fxUSD on Fluid extends its reach into additional lending markets, enabling users to borrow, lend, or collateralize fxUSD beyond the native f(x) front end.

The reliance on flash loans and third-party protocols does introduce additional smart contract and integration risk, which will be discussed later. However, it also underscores the DeFi-native nature of fxUSD: it is not a standalone product but a node in a web of composable contracts and protocols. By design, f(x) leverages the best available primitives—liquidity from Curve and Convex, lending markets from Aave and Morpho, and on-chain analytics from Dune and DefiLlama—to enhance the stability and utility of fxUSD. This approach positions fxUSD not merely as another stablecoin, but as an integral component of a full-stack leveraged yield system.

f(x) Protocol partners with 9 Summits to debut an agentic fxUSD vault on Morpho, bringing leverage and liquidity to emerging AI-native assets.

AGENTIC FXUSD VAULT ON MORPHO?? WITH LEVERAGE?? LFG WE'RE SO BACK 🚀🚀🚀 SER, THIS IS WHAT WE'VE BEEN WAITING FOR. AI AND DEFI COLLIDING. GONNA APE SO HARD INTO THIS. WEN AIRDROP FOR EARLY USERS? 👀👀 NEED TO FARM THOSE TOKENS. THIS IS IT FELLAS. WE'RE ALL GONNA MAKE IT. WAGMI. NFA.

Integrations and Liquidity: Where fxUSD Lives in DeFi

The utility and perceived safety of a stablecoin depend heavily on where and how it can be used. For fxUSD, liquidity and integrations have expanded steadily, reflecting both protocol-driven initiatives and external teams’ decisions to incorporate it into their products. Today, fxUSD circulates across Curve and Convex pools, is plugged into lending markets like Morpho and Fluid, appears in basket strategies such as Asymmetry’s “DeFi Stable Avengers LP,” and sits at the center of new vaults and agentic strategies aimed at AI-native assets. These integrations provide real-world venues where users can trade, farm, and borrow against fxUSD, reinforcing its peg and creating a feedback loop between adoption and stability.

Curve, Convex, Prisma, and Stable Pools

Curve Finance, the dominant stable swap AMM, has been a key venue for fxUSD liquidity. f(x) Protocol has seeded pools pairing fxUSD with other stablecoins, allowing traders to swap into and out of fxUSD with low slippage and enabling liquidity providers to earn trading fees and incentives. Over time, f(x) has worked with Convex Finance to secure Convex gauges for certain fxUSD pools, which allocate CVX-boosted CRV emissions to those pools and thus increase yields for LPs. Community updates have noted the addition of multiple new Convex gauges specifically targeting fxUSD liquidity, signaling both the protocol’s commitment to deepening its stablecoin pools and Convex’s willingness to recognize fxUSD within its gauge ecosystem.

A related integration pathway is Prisma Finance, a protocol focused on creating stablecoins backed by liquid staking tokens. A governance proposal titled FIP-028 in Prisma’s forum addressed adding Curve and Convex receivers for an fxUSD/ULTRA pool, enabling that pool to receive PRISMA rewards. The proposal exemplifies how cross-protocol governance decisions can shape the incentive landscape for fxUSD liquidity, as PRISMA emissions can attract LPs and sustain deeper liquidity in the fxUSD/ULTRA pair. For users, this means more robust markets where fxUSD trades closely around one dollar against other stablecoins and LSD-backed assets, supported by multiple layers of protocol incentives.

By embedding fxUSD into such flagship DeFi venues, f(x) Protocol effectively outsources part of its stability and adoption story to the broader ecosystem. Liquidity on Curve and Convex not only improves user experience for swaps, but also provides a price discovery venue that arbitrageurs can use alongside f(x)’s own peg mechanisms. If fxUSD deviates from its target on one venue, cross-market arbitrage can both restore the price and trigger internal protocol responses (such as redemptions or minting) that balance supply and demand. In this way, external liquidity venues become extensions of f(x)’s peg maintenance toolkit.

Lending Markets: Morpho, Fluid, and Others

Lending market integrations extend fxUSD’s utility beyond pure trading and yield farming. Morpho, an optimized lending protocol that builds on top of established pools, has incorporated fxUSD into its ecosystem, including through the aforementioned collaboration with 9 Summits on an agentic vault for AI-native assets. In such a vault, fxUSD can serve as both financing currency and risk-mitigating asset, allowing users to borrow against or earn yield on positions tied to new categories of tokens, such as those linked to AI projects. This sort of integration illustrates one of the promises of trustless stablecoins: they can function as neutral, programmable collateral for emerging niches without relying on bank rails or centralized issuers.

Similarly, the addition of fxUSD to Fluid reflects growing interest in including decentralized stablecoins in money markets. As a lending and borrowing venue, Fluid can host markets where fxUSD is supplied by lenders seeking yield and borrowed by users needing a stable medium of exchange or leverage. In these contexts, fxUSD competes head-to-head with USDC and other more established stablecoins, relying on its decentralization and yield-backed design to justify its inclusion. The interplay between its own Stability Pool and external lending markets also creates new strategy space, as users can rotate between protocol-native yields and lending rates depending on relative attractiveness and risk tolerance.

These lending integrations collectively move fxUSD beyond the confines of its home protocol. They allow users to treat fxUSD as a general-purpose stablecoin for collateral, debt, and liquidity provision, rather than as a specialized instrument usable only within f(x)’s own interfaces. At the same time, they introduce new dependencies: if a lending market suffers an incident, fxUSD holders and the protocol may be indirectly affected. The integration story is therefore intertwined with risk management, underscoring that broad composability comes with the need for robust monitoring and community governance.

Cross-Stablecoin Liquidity and Stablecoin Baskets

Beyond bilateral pairs, fxUSD has also found its way into multi-stablecoin baskets, which can diversify idiosyncratic risk. A notable example is Asymmetry’s upcoming DegenBoxAF “DeFi Stable Avengers LP”, a pool composed of USDaf, USDC, BOLD, and fxUSD with “efficient incentives” teased by the project’s communications. Such a basket groups fxUSD with both centralized (USDC) and decentralized (BOLD, USDaf) stablecoins, offering LPs exposure to a diversified set of peg mechanisms and collateral models. If one stablecoin in the basket experiences volatility or a depeg, the overall LP position may still remain relatively stable, reducing single-asset risk.

From fxUSD’s perspective, inclusion in these curated baskets is both a signal and a utility boost. It signals that other teams recognize fxUSD as part of the emerging family of “DeFi-native” or “trustless” stablecoins worthy of being paired with their own instruments. It also provides additional liquidity and arbitrage pathways, as traders can move between different baskets and pools to exploit pricing discrepancies. In combination with Curve and lending pools, these baskets help embed fxUSD in a web of cross-stablecoin relationships that can both stabilize and, in extreme cases, transmit shocks.

The Trustless Force interview on Leviathan News further contextualizes these efforts by arguing for a deliberate diversification of stablecoin TVL away from centralized coins toward fully on-chain designs like fxUSD, BOLD, and crvUSD. By promoting portfolios that blend multiple decentralized stablecoins, advocates hope to reduce systemic reliance on any single design or issuer, making DeFi more resilient to idiosyncratic failures. fxUSD’s presence in such multi-stablecoin constructs can therefore be seen as part of a broader ideological and practical shift toward building a more robust, decentralized base layer of “crypto dollars.”

User Experience, Wallets, and Tooling

While much of fxUSD’s design is technically intricate, user experience increasingly abstracts away these complexities. Standard Ethereum and EVM-compatible wallets support fxUSD like any other ERC-20 token, and front-end interfaces built by the f(x) team and community provide simplified flows for minting, swapping, and depositing into the Stability Pool or external integrations. Educational materials from f(x) Protocol, including the official documentation and social media threads, address common questions such as “Is fxUSD an algorithmic stablecoin?” and “Where does the yield come from?”, aiming to demystify the relationship between collateral, leverage, and staking/lending income.

External educational efforts have also played a role. Leviathan News, for example, hosted a long-form discussion titled “How fxUSD Scales to a Billion” with contributors kmets and Cryptovestor, exploring how the protocol might grow its stablecoin supply and integrations while maintaining its peg and risk management. Other venues, such as the “Stable School” series where Cyrille discussed f(x) Protocol, have contributed to community understanding of how fxUSD compares to other decentralized stablecoins like crvUSD or Liquity’s LUSD. Together with analytics platforms like Dune and DeFiLlama, which provide transparency into fxUSD’s supply, TVL, and peg behavior, these resources help sophisticated users and DAOs make informed decisions about integrating fxUSD into their own strategies.

As with all complex DeFi products, the onus remains on users to understand the underlying mechanics and risks. However, the combination of protocol-native UX improvements, external tooling, and independent analysis suggests that fxUSD is evolving from an expert-only instrument toward a more accessible yet still advanced stablecoin option. Where early users needed to piece together concepts like invariants, stability pools, and flash-loan-powered leverage, newer entrants can increasingly rely on curated vaults, one-click strategies, and familiar pool interfaces, even as the underlying system remains highly engineered.

Peg Performance, Market Standing, and Data

No matter how elegant its design, a stablecoin ultimately lives or dies by its peg and market acceptance. For fxUSD, the evidence to date points to a combination of steady growth into the mid-tier of DeFi stablecoins and robust peg behavior across a turbulent period for crypto markets. While its scale remains modest relative to giants like USDC or USDT, fxUSD’s ascent into the top 30 stablecoins by market cap, along with external analyses of its peg, provide empirical support for the protocol’s claims about stability and resilience.

Market Share and Growth Trajectory

DeFiLlama’s stablecoin dashboard shows a crowded landscape of stablecoins with varying designs and degrees of decentralization, tracking their collective market capitalization, supply, and peg stability. Against this backdrop, fxUSD has carved out a niche as a decentralized, crypto-backed stablecoin anchored in a sophisticated leverage and yield-sharing system. One snapshot reported by Leviathan News and echoed in community analytics noted that fxUSD had reached a position of #29 among stablecoins by market cap, with over $39 million in circulation at that time. While modest compared to the tens of billions held by major fiat-backed coins, this ranking places fxUSD ahead of many smaller experiments and underlines its emergence as a serious player in the decentralized stablecoin category.

From a TVL perspective, coverage has highlighted that f(x) Protocol’s overall system—encompassing both fxUSD and leveraged positions—was managing on the order of $152 million in total value locked, with fxUSD supply around $56 million at a certain point, underscoring substantial adoption of both sides of the invariant. These figures move well beyond the early days when the protocol’s TVL was measured in low single-digit millions shortly after launch. Community Dune dashboards dedicated to f(x) report metrics such as collateral composition, supply of stable and leveraged tokens, and pool utilization, offering granular visibility into how the system’s balance sheet evolves over time. Users and analysts can thus track not only absolute growth but also structural shifts, such as changes in the ratio of fxUSD to xPOSITION supply.

In market structure terms, fxUSD’s journey from launch to top-30 stablecoin reflects both deliberate integrations and a tailwind of growing interest in decentralized stablecoins. As trust in fully algorithmic designs waned after high-profile collapses, attention shifted toward overcollateralized, on-chain models that can demonstrate resilience via transparent on-chain data and independent analysis. fxUSD has benefited from this trend, especially as it has been grouped in narratives around “trustless stablecoins” and highlighted alongside peers like crvUSD and BOLD by advocates such as Trustless Force. However, its comparatively modest scale also means that liquidity and integration depth remain areas for continued development.

Peg Stability and Stress Events

Perhaps the most important empirical question for any stablecoin is how its price behaves during periods of market stress. In fxUSD’s case, external research and anecdotal evidence suggest that the peg has held up well through volatile conditions. A Leviathan News “Crypto Trading Signals” update, summarizing a report by Pangea, noted that a dedicated Pangea study found fxUSD’s peg held strong amidst a turbulent year, indicating that observed deviations from the one-dollar target remained limited even as broader crypto markets experienced sharp drawdowns and liquidity shocks. While the underlying Pangea report focuses in other work on crvUSD’s monetary policy, the mention of fxUSD in this context reflects that researchers are applying similar analytic lenses to multiple decentralized stablecoins.

Community communications have further highlighted specific stress episodes where fxUSD and its siblings performed well. In one notable period spanning three days, crypto markets saw over $282 million in ETH long positions liquidated across centralized and decentralized venues, yet internal data from f(x) Protocol reported zero liquidations on xETH and noted that both fxUSD and rUSD maintained their pegs throughout the turmoil. While such statements are necessarily self-reported, they align with the protocol’s design goals: by avoiding individual margin calls and relying on invariant-based rebalancing, the system aims to reduce the frequency of forced liquidations and spread volatility more smoothly between stable and leveraged tranches. For fxUSD holders, the key takeaway is that, at least in this episode, the stablecoin’s price did not exhibit significant dislocations despite extreme moves in its underlying collateral.

Of course, past performance does not guarantee future stability. Like any crypto-collateralized stablecoin, fxUSD remains exposed to extreme tail events in ETH and BTC markets, as well as to potential bugs or integration failures. Moreover, as the system scales, the absolute size of positions and the potential for feedback loops increase, making robust monitoring and parameter governance ever more important. Nonetheless, the combination of third-party analysis (such as Pangea’s work) and real-world stress episodes where the peg held provides meaningful evidence that fxUSD’s stability mechanisms are not purely theoretical.

Transparency and Monitoring

One advantage of fully on-chain stablecoins like fxUSD is the degree of transparency they offer to both users and external analysts. f(x) Protocol’s fx Docs explicitly address questions about how fxUSD maintains its stability, whether it should be considered “algorithmic,” and where the yield paid to stability providers and liquidity providers originates, emphasizing that backing comes from on-chain collateral and staking/lending income rather than from off-chain treasuries. MixBytes’ independent review of f(x) Protocol 2.0 provides another layer of scrutiny, dissecting the stabilization mechanisms—price bands, liquidations, redemptions, reserve pools—and describing the integration pathways with external protocols. Together, these documents give interested observers a basis for understanding and evaluating the system beyond marketing claims.

On the data side, Dune Analytics dashboards track key metrics for f(x) Protocol, including collateral composition, fxUSD supply, xPOSITION supply, and the health of stability pools. DeFiLlama’s stablecoin page, meanwhile, places fxUSD within the broader universe of stablecoins, showing its market capitalization, supply, and peg behavior alongside competitors. For more qualitative analysis, Pangea’s blog has become known for deep dives into stablecoin monetary policies, notably for Curve’s crvUSD, highlighting how design choices around soft pegs, interest rates, and liquidation mechanics feed into user experience and system stability. Although each stablecoin differs, this ecosystem of tools and research allows the community to monitor fxUSD in near real time and benchmark its behavior against peers.

This transparency does not eliminate risk, but it does make fxUSD’s risk profile legible in a way that many centralized stablecoins are not. Users can see the exact collateral backing, track the performance of stability pools, and observe how the protocol responds to volatility. Combined with public forums and governance processes, this visibility is a core part of fxUSD’s claim to being a “truly decentralized stablecoin,” as the project’s social media tagline emphasizes. Whether this transparency and design ultimately prove sufficient to withstand future crises remains an open question, but they provide a clear foundation on which that judgment can be made.

Governance, Decentralization, and the Trustless Stablecoin Narrative

Beyond mechanics and market data, fxUSD is part of a broader political and ideological debate about the future of money on Ethereum. Its design reflects a deliberate choice to prioritize on-chain collateral, transparent risk-sharing, and protocol-governed parameters over the simplicity and regulatory comfort of fiat-backed stablecoins. This places fxUSD squarely within the emerging movement for “trustless stablecoins,” which seeks to reduce reliance on centralized issuers and off-chain banking infrastructure even if it entails higher complexity and overcollateralization. Understanding this context is important for interpreting both advocacy around fxUSD and critical scrutiny of its design.

On-Chain Collateral and Non-Custodial Design

A defining feature of fxUSD is that its collateral—ETH, BTC via WBTC, and their staked or lent derivatives—remains on-chain in smart contracts rather than in bank accounts or money market funds. The fx Docs and f(x) Protocol’s messaging emphasize that fxUSD is a “truly decentralized stablecoin,” highlighting its non-custodial nature and the absence of centralized redemption controls. Unlike USDC, which can be frozen at the address level and depends on off-chain reserves held with banking partners, fxUSD’s backing is verifiable directly on Ethereum and its associated L2s, with no single custodian able to unilaterally seize or block user funds.

This on-chain collateral model aligns closely with the criteria articulated by the Trustless Force in their Leviathan News interview. They argued that for a stablecoin to be genuinely trustless, its collateral must remain fully on-chain and censorship-resistant, and its monetary policy must be governed by transparent code and open governance rather than by a centralized issuer. In their view, shifting even a small fraction of total stablecoin TVL into such designs—naming fxUSD, BOLD, and crvUSD as examples—would significantly improve systemic resilience by reducing exposure to the traditional banking system and regulator-imposed controls. fxUSD’s architecture, with its ETH/BTC collateral and invariant-based stabilization, fits squarely within this trustless stablecoin rubric.

That said, “trustless” does not mean riskless. fxUSD users trade off bank and regulatory risk for smart contract and market risk; they avoid exposure to a corporate issuer’s solvency and legal obligations but assume exposure to the security of f(x) Protocol’s code and its integrations with protocols like Aave, Curve, and Morpho. The choice between USDC and fxUSD is therefore not merely technical but ideological: do you prefer a dollar that relies on court-enforced contracts and bank reserves, or one that relies on math, game theory, and open-source code? For many in the Ethereum community, diversifying between these models—rather than betting exclusively on one—is a prudent approach.

Role of Aladdin DAO and Community Governance

f(x) Protocol’s roots in Aladdin DAO further situate fxUSD within a community-governed ecosystem rather than a corporate issuer model. Aladdin DAO emerged as a research-driven collective focused on curating DeFi yields and protocol designs, and f(x) can be seen as one of its more ambitious engineering efforts, turning the abstract idea of tranching ETH exposure into a full-fledged stablecoin and leverage system. Governance structures for f(x) encompass decisions about collateral types, risk parameters, integration whitelists, and incentive allocations, which are typically made through token-holder voting and community discussion, rather than by a centralized foundation alone.

Interactions with external governance processes illustrate this multi-DAO dynamic. The Prisma proposal to add fxUSD/ULTRA pool receivers for PRISMA rewards, for instance, required Prisma governance to recognize fxUSD as a valid and desirable asset within its incentive framework. Similarly, Convex gauges for fxUSD pools must be approved within Convex’s own governance process, reflecting a negotiation between different protocol communities about how to allocate scarce emission resources. In practice, this creates a network of overlapping governance decisions that collectively determine fxUSD’s liquidity, yield profile, and integration depth, making it a kind of “governance citizen” of the broader DeFi ecosystem rather than an isolated asset.

While decentralization through DAO governance aligns with the trustless ethos, it also introduces governance risk. Parameter choices around price bands, liquidation discounts, collateral whitelists, and incentive distributions can materially affect fxUSD’s risk-return profile. Poorly calibrated parameters could lead to undercollateralization, unstable pegs, or perverse incentives that stress the system in volatile markets. Governance capture by narrow interests is also a perennial concern in DAOs. For fxUSD, this means that decentralization must be paired with robust governance processes, including open discussion, expert input, and careful simulation and testing of proposed changes.

Trustless Force and the Diversification of Stablecoin TVL

The Trustless Force episode on Leviathan News crystallizes a growing narrative in the DeFi community: that stablecoin TVL is overconcentrated in centralized, fiat-backed designs and that this concentration represents a systemic vulnerability. In the interview, members of the Trustless Force urged the ecosystem to imagine a future where even 5% of stablecoin holdings shifted into “trustless stablecoins” like fxUSD, BOLD, and crvUSD, emphasizing that such coins keep their collateral entirely on-chain and avoid the single-point-of-failure risk of bank accounts. Their mission, as presented, is to evangelize and support decentralized stablecoin projects that align with this vision, using education, governance participation, and ecosystem-building efforts.

For fxUSD, inclusion in this trustless stablecoin cohort is both an endorsement and a challenge. It signals that key voices in the decentralization debate view fxUSD’s architecture as sufficiently robust and on-chain to qualify as a credible alternative to fiat-backed coins. At the same time, it places fxUSD under a sharper spotlight: if it is to function as part of the “trustless” base layer, its behavior during crises, its governance decisions, and its integration choices will be scrutinized as part of the ecosystem’s resilience strategy. Pangea’s deep-dive into crvUSD’s monetary policy, and their subsequent analysis of fxUSD’s peg behavior, exemplify the analytical attention such projects attract.

This narrative does not imply that fiat-backed stablecoins will disappear; they remain deeply embedded in exchanges, on-ramps, and institutional workflows. Instead, the argument is for diversification. By growing the share of on-chain, overcollateralized stablecoins like fxUSD, DeFi could, in theory, reduce its exposure to off-chain shocks and regulatory shifts while maintaining or even enhancing its ability to support complex financial activity. fxUSD’s trajectory—from launch to multi-protocol integrations and top-30 status—suggests it is one of the contenders for a meaningful role in such a diversified stablecoin portfolio.

If you still haven't watched this one, we definitely recommend you do so over the weekend. We were honored to be the outlet where the Trustless Force chose to have its first ever public appearance - to share the message of diversifying stablecoin TVL to actually decentralized stablecoins, like $BOLD, $fxUSD, $crvUSD and others. They are also our SQUID Pass holders for the week btw! Thank you for choosing Leviathan News, Trustless Force! Watch here:

@lampropeltis "The Trustless Force just launched and it's exactly what DeFi needed Initiated by @LiquityProtocol, @protocol_fx, and @CurveFinance , this isn't another alliance. It's a movement to bring Ethereum's core values back. Here's what matters 👇 🎯 The Mission: Shift 5% into Trustless Stables Right now, 99% of stablecoins are centralized. They have collateral in banks and rely on trust assumptions. The goal? Shift 5% of stablecoin holdings to trustless alternatives. Could move up to $15bn in demand for crypto collateral on-chain. You don't need to go all-in. Just shift 5% into trustless stables like BOLD, crvUSD, or fxUSD."

Use Cases and Strategies with fxUSD

Given its design and integrations, fxUSD supports a range of use cases that extend beyond simply holding a dollar-pegged token. Traders can use it as a base currency for leveraged bets via xPOSITIONs, yield seekers can deposit fxUSD or USDC into the Stability Pool or Curve/Convex pools, DAOs and treasuries can mint fxUSD against ETH to avoid selling into bear markets, and sophisticated users can weave fxUSD into multi-protocol strategies spanning Morpho, Fluid, and stablecoin baskets. Each use case reflects a different side of fxUSD’s risk-reward profile, from conservative to highly speculative.

Trading and Hedging

For active traders, fxUSD provides a stable base currency from which to deploy directional views on ETH and BTC via xPOSITIONs. Because xPOSITIONs offer fixed leverage without funding costs or individual liquidations, as described in f(x) Protocol’s 2.0 materials, traders can structure leveraged exposure with more predictable cost profiles than perpetual futures. Marketing from f(x) Protocol and its partners has emphasized that users can access up to 7x ETH exposure in certain guarded launches, with caps such as a $25 million fxUSD limit designed to constrain risk while the system proves itself. Subsequent messaging has referenced the possibility of up to 10x leverage on blue-chip crypto assets without personal liquidation risk or funding costs, highlighting the ambition of xPOSITION as a leverage engine.

In practice, a trader might choose to hold a portion of their portfolio in fxUSD to manage dollar-denominated risk while allocating another portion to xETH or other xPOSITIONs for leveraged exposure. The absence of funding rates means that carrying a long-term directional bet does not incur ongoing costs beyond the opportunity cost of capital, although the invariant will naturally scale down effective leverage if the underlying asset’s price falls significantly. Compared to centralized exchange margin, this structure can be more transparent and less prone to sudden, catastrophic liquidations, though it requires careful understanding of how the invariant shapes payoff profiles and of the underlying smart contract risk.

fxUSD can also serve as a hedging instrument for users with existing crypto exposure. For example, a user heavily long ETH may mint fxUSD against part of their holdings via fxMINT, locking in dollar liquidity while retaining upside on the remaining ETH. In combination with xPOSITIONs, they can construct tailored payoff structures—such as partially hedged or delta-neutral positions—without leaving the f(x) ecosystem. While such strategies are advanced and beyond the scope of casual users, they illustrate the composability that fxUSD and xPOSITIONs offer to sophisticated traders.

Yield, Delta-Neutral Strategies, and the Stability Pool

For yield-focused users, fxUSD’s main attraction lies in the Stability Pool and related yield-bearing integrations. By depositing fxUSD or USDC into the Stability Pool, users can earn yield sourced from wstETH and WBTC reserves and Aave lending yields, as explicitly noted in the protocol documentation. Unlike pure liquidity mining programs that rely primarily on token emissions, this yield is grounded in the actual performance of underlying ETH and BTC collateral, making it a more “organic” return stream. Additional protocol incentives or external rewards from Curve, Convex, or Prisma can further enhance returns, depending on the pool and governance decisions at any given time.

The Stability Pool offers what many describe as a delta-neutral opportunity: depositors hold their value primarily in stablecoins while earning yield that is economically linked to leveraged counterparties and collateral performance. They effectively sell volatility insurance to the system—standing ready to absorb undercollateralized positions in liquidations—in exchange for a premium composed of reserve yield and liquidation discounts. As long as the system remains well-collateralized and liquidations are orderly, this can produce attractive risk-adjusted returns compared to simply holding USDC or another stablecoin in a low-yield wallet. However, depositors must be comfortable with the possibility that extreme events or protocol bugs could impose losses, making due diligence essential.

Beyond the Stability Pool, fxUSD can be deployed into Curve and Convex pools for additional yield via trading fees and liquidity mining incentives. LPs pairing fxUSD with other stablecoins, such as USDC or ULTRA, may earn CRV, CVX, PRISMA, or protocol-native rewards, stacking multiple yield streams on top of the base stability provided by fxUSD’s peg. Advanced strategies might route fxUSD from fxMINT into Stability Pools, then into Curve/Convex pools or Morpho vaults, compounding returns at each step. As always in DeFi, such complexity magnifies not only potential reward but also integration and smart contract risk.

Treasury Management and Long-Term Holders

For DAOs, protocol treasuries, and long-term ETH holders, fxUSD offers a tool for unlocking liquidity without selling core assets. Instead of “dumping” ETH to raise dollars for operations or diversification, a treasury can deposit ETH into fxMINT, mint fxUSD at 0% interest, and use that fxUSD for expenses or further investments. Public commentary has even included a call for the Ethereum Foundation to consider minting fxUSD instead of selling ETH, illustrating how some advocates envision large institutions using decentralized stablecoins to manage treasury risk.

The appeal of such strategies lies in avoiding immediate sell pressure on ETH and retaining upside exposure while accessing dollar liquidity. If ETH appreciates over time, the effective collateralization of the fxUSD debt improves, and the treasury may eventually repay and close positions at a favorable ratio. Conversely, if ETH falls, the treasury must manage its loan-to-value ratio carefully to avoid system-level liquidations, even if individual liquidation risk is minimized by f(x)’s design. For treasuries wary of regulatory or censorship risk associated with USDC, fxUSD offers an alternative way to hold operational dollars backed entirely by on-chain assets.

However, this approach is not without trade-offs. Minting fxUSD against ETH introduces leverage on the treasury’s balance sheet; if ETH declines sharply, the real value of the treasury’s assets drops while its dollar-denominated liabilities (in fxUSD) remain constant. Overreliance on fxUSD or similar mechanisms could exacerbate losses in a prolonged bear market. Prudent treasury management would thus treat fxUSD as one tool among many, combining it with non-leveraged holdings of stablecoins, BTC, or real-world assets to balance risk.

Everyday Payments and Composability

While much of the conversation around fxUSD focuses on trading, leverage, and yield, it also functions as a general-purpose stablecoin that can be used for payments, remittances, and everyday DeFi interactions. As long as the peg holds and liquidity remains sufficient, merchants, DAOs, and individuals can accept fxUSD just as they might accept USDC or DAI, benefiting from its on-chain composability and censorship resistance. Any smart contract that supports ERC-20 tokens can be built to accept fxUSD, making it possible to integrate fxUSD into payroll systems, subscription services, or NFT marketplaces.

In practice, adoption in these everyday contexts depends on network effects and UX. Since USDC and USDT still dominate most on- and off-ramps, fxUSD is more likely to be used as an intermediate asset within DeFi strategies rather than as the primary unit of account for non-crypto-native users. However, as integrations expand to L2s and alternative EVM chains, and as more protocols support trustless stablecoins, the friction of using fxUSD for broader purposes should decline. For users and communities particularly concerned about censorship, an on-chain stablecoin like fxUSD can already serve as a politically attractive alternative, even if liquidity and tooling are not yet as ubiquitous as those of centralized competitors.

In sum, fxUSD functions simultaneously as a stable savings instrument, a leverage enabler, and a composable medium of exchange, with each role drawing on different aspects of its architecture and integration footprint. The diversity of use cases underscores both the promise and the complexity of the design: users can do more with fxUSD than with many other stablecoins, but they must also understand the system’s intertwined risks.

Risks, Limitations, and Open Questions

Despite promising design features and positive early data, fxUSD remains an experimental, crypto-collateralized stablecoin embedded in a complex web of smart contracts and protocols. Prospective users and integrators must weigh smart contract risk, market and liquidity risk, governance and oracle risk, and competitive dynamics when deciding whether and how to adopt fxUSD. Its trustless architecture mitigates some classes of risk—especially those linked to centralized custodians—but it introduces others that are unique to invariant-based leverage systems and heavily composable DeFi applications.

Smart Contract and Integration Risk

The most fundamental risk stems from the smart contracts that implement f(x) Protocol itself and its integrations with protocols like Aave, Curve, Morpho, Prisma, Convex, and Fluid. Any bug in the core f(x) contracts, in the logic of the f(x) invariant, or in the modules handling fxMINT, liquidations, and stability pools could lead to loss of funds or destabilization of the peg. Similarly, vulnerabilities in external protocols into which fxUSD or its collateral is deposited—such as Aave lending markets or Curve pools—can propagate into fxUSD’s backing and stability, even if f(x) itself is technically sound. The use of flash loans, while beneficial for capital efficiency, also exposes the system to potential flash-loan-driven exploits if invariants or oracle assumptions can be manipulated within a single transaction.

Mitigating these risks requires robust code audits, continuous monitoring, conservative parameter choices, and, where possible, caps on exposure to any single integration or pool. The fact that xPOSITIONs were initially launched in a guarded mode, with a cap such as $25 million fxUSD limiting the scale of new leveraged positions, reflects awareness of these risks and a desire to grow safely. Nevertheless, users must recognize that, unlike fiat-backed stablecoin issuers that can potentially tap into off-chain capital or legal recourse in the event of a failure, purely on-chain designs like fxUSD have limited options if a critical bug is exploited.

Market, Liquidity, and Peg Risk

fxUSD’s stability ultimately depends on the market value of its collateral (ETH, BTC), the depth of its liquidity across venues, and the effectiveness of its stabilization mechanisms under stress. A severe, rapid crash in ETH or BTC could test the limits of the f(x) invariant, the Stability Pool, and the willingness of xPOSITION holders and arbitrageurs to absorb volatility. While analyses such as the Pangea report summarized by Leviathan News have found that fxUSD’s peg held through a turbulent year, and anecdotal evidence indicates robust performance during episodes of massive ETH liquidations, future crises may be more severe or qualitatively different.

Liquidity is another crucial factor. Although fxUSD has secured listings and incentives on Curve, Convex, Morpho, Fluid, and basket strategies like DegenBoxAF, its total liquidity remains small compared to USDC and other major stablecoins. Thin liquidity can exacerbate price swings if large holders attempt to exit quickly, and can limit the ability of arbitrageurs to correct deviations from the one-dollar peg efficiently. Diversifying liquidity across venues and pairs mitigates this to some extent, but also requires careful monitoring to ensure that no single pool becomes a bottleneck or source of slippage.

Fat-tail risks are particularly salient for crypto-collateralized stablecoins. An extreme event affecting ETH or wstETH—for example, a critical bug in a staking protocol or a chain-level incident—could impair collateral across multiple protocols simultaneously, including f(x). In such scenarios, the fact that collateral is on-chain and transparently visible does not by itself guarantee solvency or peg maintenance, although it does enable rapid assessment and coordination. Users who treat fxUSD as equivalent in risk to fiat-backed stablecoins may be surprised by its behavior in such scenarios; understanding the underlying collateral risk is essential.

Governance, Oracle, and Policy Risk

The stability and safety of fxUSD also hinge on governance decisions and oracle integrity. As a protocol governed within the broader Aladdin DAO ecosystem and through its own processes, f(x) relies on token holders and contributors to set parameters such as collateralization ratios, price bands, liquidation penalties, and integration whitelists. Misjudged parameter changes—for instance, narrowing price bands too aggressively, or lowering collateralization thresholds to chase yield—could increase the likelihood of peg breaks or undercollateralization. Governance capture by a small group of stakeholders with short-term incentives could push the system toward riskier configurations.

Oracles present another subtle but critical risk vector. f(x) must rely on price feeds for ETH, BTC, and other collateral to determine when positions are undercollateralized and to execute redemptions and liquidations correctly. If these oracles are manipulated, delayed, or disrupted, the protocol could misprice collateral, triggering unnecessary liquidations, missing necessary ones, or miscalculating redemption values. While industry-standard oracle designs and multisource architectures can mitigate such risk, they cannot eliminate it entirely.

Regulatory policy adds a further layer of uncertainty. While fxUSD’s fully on-chain design may reduce direct regulatory leverage compared to fiat-backed stablecoins, evolving legal frameworks around stablecoins, DeFi, and on-chain leverage products could influence how exchanges, custodians, and institutional actors interact with fxUSD. For example, regulatory scrutiny of leveraged products might affect xPOSITION integration, while stablecoin rules could impact whether certain entities are allowed to hold or transact in fxUSD at scale. As with all DeFi protocols, fxUSD operates in a shifting legal landscape.

Competitive Landscape and User Understanding

fxUSD operates in a competitive environment that includes fiat-backed stablecoins (USDC, USDT), crypto-backed stablecoins (DAI, LUSD), and newer decentralized designs such as crvUSD and BOLD. Each competitor offers a different mix of liquidity, composability, risk, and decentralization. For some users and protocols, the convenience and regulatory clarity of USDC will continue to outweigh the benefits of a trustless design. For others, projects like crvUSD—with its own sophisticated monetary policy analyzed in depth by Pangea—and fxUSD represent the future of censorship-resistant dollars. Whether fxUSD can secure a durable niche depends not only on its technical merits but also on network effects, partnerships, and community momentum.