In crypto, leverage lets traders and DeFi users borrow against collateral to amplify exposure to assets like Bitcoin and USDC. This explainer unpacks margin, liquidation, DeFi loops, and regulation so readers can use leverage more safely.

+15 sources across the wider coverage universe

Lessons from 1890 Baring Crisis: Argentine Debt Bubble Triggers Transatlantic Contagion, Mirroring 2022 DeFi Cascade from Terra to FTX. Key Takeaways: Shun Unsustainable Yields and Hidden Leverage2026-03

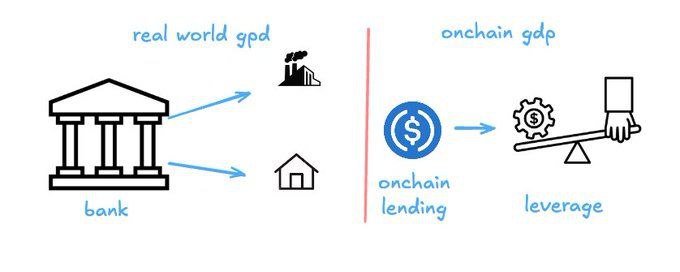

Lessons from 1890 Baring Crisis: Argentine Debt Bubble Triggers Transatlantic Contagion, Mirroring 2022 DeFi Cascade from Terra to FTX. Key Takeaways: Shun Unsustainable Yields and Hidden Leverage2026-03 Banks earn far higher margins than DeFi lenders like Aave because crypto lending is dominated by leverage and yield loops, not real-economy credit. As onchain lending expands into RWAs and structured credit, margins could rise beyond crypto cycles.2025-12

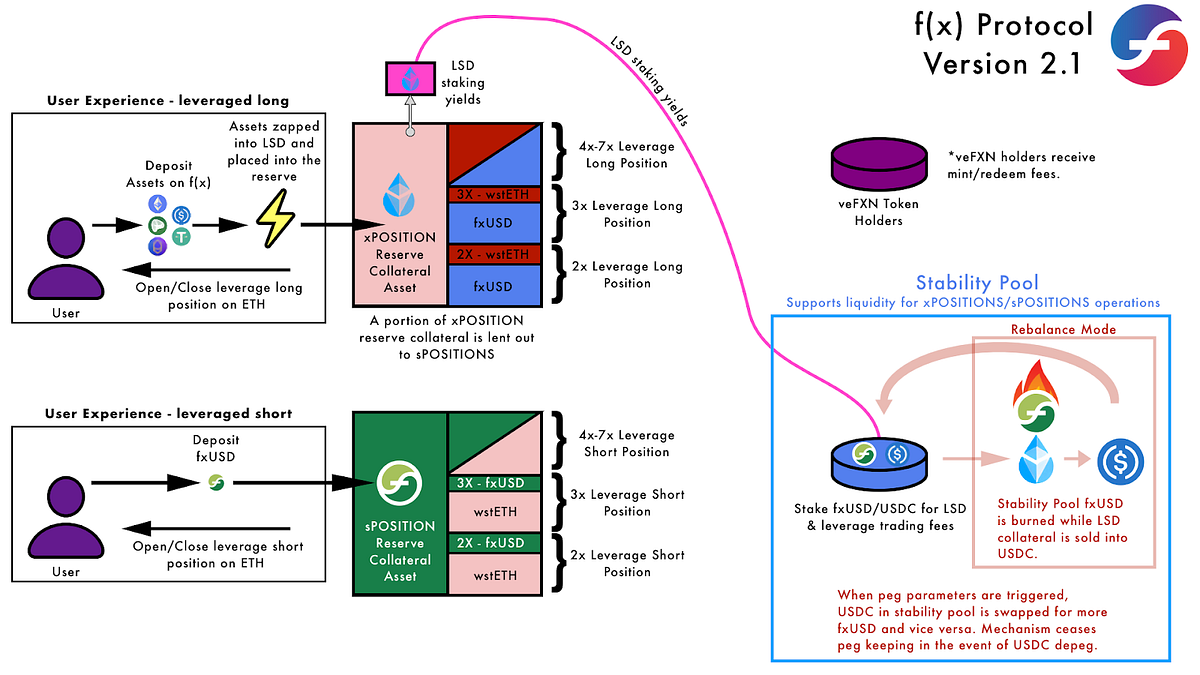

Banks earn far higher margins than DeFi lenders like Aave because crypto lending is dominated by leverage and yield loops, not real-economy credit. As onchain lending expands into RWAs and structured credit, margins could rise beyond crypto cycles.2025-12 f(x) Protocol introduces sPOSITIONs, a new way to short the market with fixed leverage, liquidation brake and zero funding costs2025-06

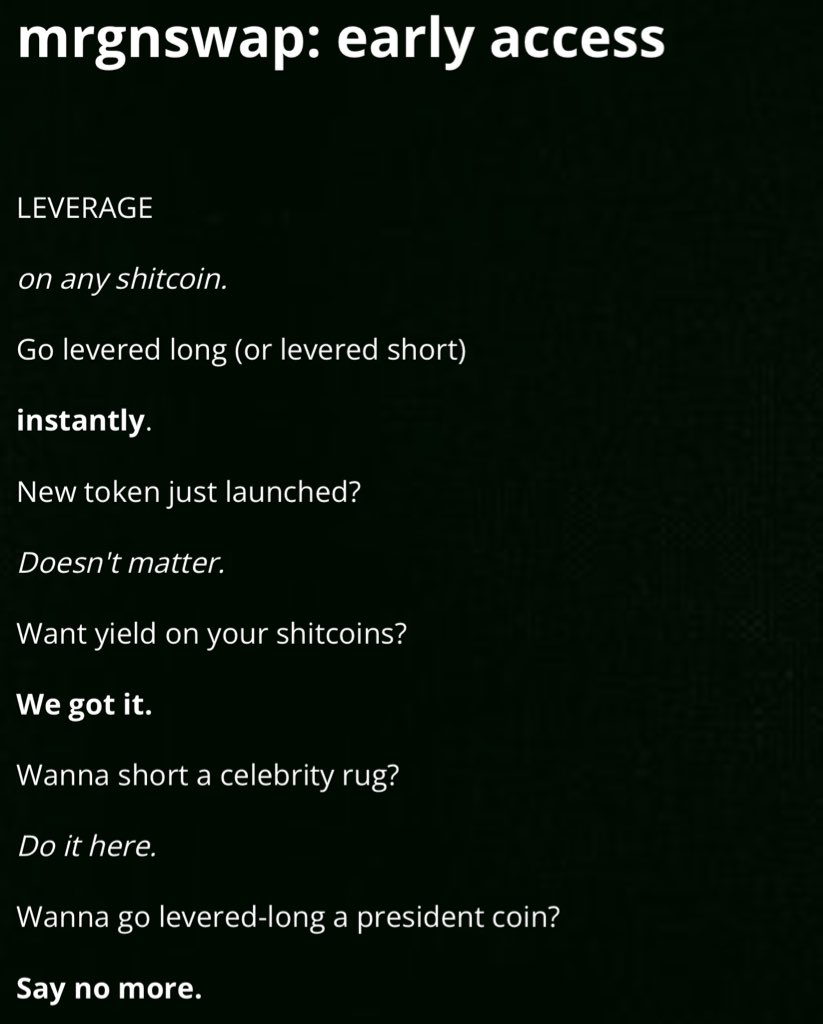

f(x) Protocol introduces sPOSITIONs, a new way to short the market with fixed leverage, liquidation brake and zero funding costs2025-06 Marginfi plans to launch “mrgnswap,” allowing traders to instantly long/short newly created meme coins with leverage.2024-07

Marginfi plans to launch “mrgnswap,” allowing traders to instantly long/short newly created meme coins with leverage.2024-07 Honestly - incredible to read these kinds of reviews about our sponsors - f(x) Protocol!

Wanna enjoy the benefits of leverage trading, without the personal liquidation risk? Prefer to just earn meaningful yield on your stablecoins instead?

f(x) Protocol is the dapp you should check out.

Use our ref code: LeviathanN2025-01

Honestly - incredible to read these kinds of reviews about our sponsors - f(x) Protocol!

Wanna enjoy the benefits of leverage trading, without the personal liquidation risk? Prefer to just earn meaningful yield on your stablecoins instead?

f(x) Protocol is the dapp you should check out.

Use our ref code: LeviathanN2025-01 Bitcoin's 10% Plunge: Was It Matrixport's Fault? Jim Cramer? Leverage? Conflicting reports suggest that Matrixport's announcement of potential spot BTC ETF rejections may have sparked the crash, but a K33 analyst argues that it was more likely driven by a leveraged market reaching its boiling point.2024-01

Bitcoin's 10% Plunge: Was It Matrixport's Fault? Jim Cramer? Leverage? Conflicting reports suggest that Matrixport's announcement of potential spot BTC ETF rejections may have sparked the crash, but a K33 analyst argues that it was more likely driven by a leveraged market reaching its boiling point.2024-01

Understanding Leverage in Crypto Markets

In crypto, leverage means using borrowed funds against posted collateral to control a position larger than your own capital, amplifying both profits and losses relative to your equity. Leverage underpins everything from Bitcoin perpetual futures on centralized exchanges to complex on-chain “leverage loops” in DeFi, and it is tightly linked to core concepts like margin, liquidation, and collateral quality.

Foundations: What Leverage Is and How It Works in Crypto

Leverage in financial markets is fundamentally a ratio between the size of your position and the amount of your own capital at risk, and in crypto this ratio can range from modest two-times exposure to triple‑digit figures on some derivatives venues. If you post \(1{,}000\) USDC as margin and open a \(10{,}000\) USDC notional Bitcoin futures position, your leverage ratio is \(10\times\), meaning a 1% move in the underlying asset produces a 10% change in your equity, ignoring fees and funding. In algebraic terms, total exposure is given by \( \text{Exposure} = \text{Margin} \times \text{Leverage} \), so raising leverage linearly scales the notional size of your trade. This simple formula hides a key asymmetry in outcomes: while your upside is multiplied, your downside is too, which is why even small price moves can push leveraged positions into distress much faster than spot holdings.

Mechanically, leverage in crypto is implemented by having a centralized exchange, broker, or DeFi protocol lend you additional buying power against the collateral you deposit, usually in the form of stablecoins like USDC, major assets such as BTC or ETH, or specialized collateral tokens. Your deposit serves as initial margin, the buffer that absorbs losses on the position; if the market moves against you, the unrealized loss is deducted from this margin in real time. When your remaining equity falls below a pre‑defined maintenance margin threshold, your position is forcibly closed or “liquidated” to ensure the platform can repay itself and avoid extending you unsecured credit. Because of these margin engines, most crypto derivatives platforms are structured so that you generally cannot lose more than the collateral you have posted, although certain contracts such as CFDs can expose traders to losses exceeding their initial deposit if markets gap violently. The presence or absence of recourse beyond your margin is therefore an important difference between products that all advertise “leverage.”

It is useful to distinguish between contract leverage and effective leverage when thinking about risk. Contract leverage is the number you choose when you open a trade, for example selecting \(5\times\) or \(20\times\) leverage on a Bitcoin perpetual futures order ticket. Effective leverage, by contrast, is dynamically defined as your current position size divided by your current account equity, and it evolves with price changes and with other positions in your portfolio. If a long Bitcoin position moves in your favor, your equity rises and your effective leverage falls, giving you more breathing room; if the price moves against you, your equity shrinks and effective leverage rises, making the position ever more sensitive to additional price moves. Risk‑conscious traders monitor effective leverage at the account level rather than focusing solely on the nominal leverage of a single position, because cascading liquidations often arise when multiple trades are all near their margin thresholds simultaneously.

Although the term “leverage” is sometimes used more loosely in technology and business discourse—for example, Aethir Mesh describes helping developers “leverage” top‑tier open‑source large language models through an API layer—the financial meaning in crypto trading is precise and directly tied to borrowing, collateral, and liquidation risk. In AI infrastructure, “leveraging” a model simply means harnessing an existing resource to amplify productivity, not taking on debt. The coexistence of these uses in the same industry underscores why crypto participants must pay close attention to context: when an exchange or protocol advertises higher leverage, it almost always refers to the ability to borrow more against your collateral, and thus to take on greater financial risk. Understanding this distinction is essential when evaluating new product launches, especially in an environment where both DeFi platforms and centralized venues market “capital efficiency” as a core selling point.

Lessons from 1890 Baring Crisis: Argentine Debt Bubble Triggers Transatlantic Contagion, Mirroring 2022 DeFi Cascade from Terra to FTX. Key Takeaways: Shun Unsustainable Yields and Hidden Leverage

1890 Baring Crisis: Argentine debt bubble bursts, triggers contagion to Brazil's Encilhamento; Barings rescued by BoE. Parallels 2022 DeFi: Terra collapse spreads to 3AC, FTX. Lessons: Avoid unsustainable yields, leverage; diversify truly.

Readers click leverage content not for generic risk education but for two opposing poles: innovations that promise leveraged upside without personal liquidation risk (f(x) Protocol dominated the top clicks), and spectacular real-money blow-ups that prove exactly why those innovations are being built.↗

Margin, Collateral, and Borrowed Funds

At the heart of leveraged crypto trading lies the margin account, a dedicated sub‑account where your collateral is held, your profits and losses are realized, and your borrowing capacity is calculated in real time. The funds you deposit into this margin account—whether they are USDC, BTC, ETH, or another approved asset—constitute your initial margin, the capital that backs your leveraged positions. When you open a trade, the platform computes how much initial margin is required using a formula such as \( \text{Initial Margin} = \frac{\text{Position Size} \times \text{Mark Price}}{\text{Leverage}} \), ensuring that higher leverage requires less capital per dollar of exposure but leaves a thinner buffer against adverse moves. In a practical example, MetaMask explains that with \(10\times\) leverage on \(1{,}000\) USDC of margin, you control a \(10{,}000\) USDC position, so a 1% move in the underlying translates to a \(100\) USDC gain or loss, which is 10% of your margin. This illustrates how shrinking the denominator—your margin—magnifies the impact of any given price change.

Alongside initial margin, platforms define a maintenance margin level, which is the minimum equity you must hold to keep your position open without triggering liquidation. On some derivatives exchanges, including DeFi protocols like Hyperliquid discussed by MetaMask, the maintenance margin for positions at maximum leverage can be roughly half the initial margin rate, meaning that once your equity has fallen by about half of the initial buffer, forced liquidation begins. In this framework, the liquidation price is the critical price level at which the mark‑to‑market loss on your position has eroded your equity down to the maintenance margin threshold, after which the platform will automatically reduce or close your position to prevent further losses. Crypto trading interfaces typically display this liquidation price upfront when you configure your trade, but the level can shift as you add or withdraw collateral or as funding payments adjust your equity over time. Because the liquidation price is determined by the interplay of leverage, collateral, and position direction, a deep understanding of margin mechanics is essential for any trader who uses leverage, even at moderate levels.

Collateral quality matters as much as quantity. Posting relatively stable collateral such as USDC or other dollar‑pegged tokens insulates your margin from the direct price swings of the underlying asset you are trading, while using volatile collateral like BTC to margin a BTC perp can create pro‑cyclical risk where both your collateral and your position move against you simultaneously. Many centralized exchanges implement collateral haircuts, effectively valuing volatile assets at a discount when computing your borrowing capacity, so that \(1{,}000\) USD worth of BTC might only count as \(800\) USD of margin, thereby lowering your maximum allowable leverage relative to posting USDC. Similar concepts appear in DeFi, where overcollateralized stablecoin systems and lending markets assign different collateral factors to assets, limiting how much you can borrow against each token to reflect its liquidity and volatility. Regular updates to these collateral ratios and margin tiers, often announced in response to market volatility or protocol incidents, are central tools for risk teams attempting to keep system‑wide leverage within tolerable bounds.

The borrowed side of the ledger is equally important. In centralized derivatives, the platform itself is usually your counterparty or intermediates between you and a liquidity provider, extending synthetic exposure rather than literally lending you coins; your “borrow” is implicit in the leveraged derivative contract. In DeFi lending protocols, by contrast, you directly borrow tokens from a global pool supplied by other users, who earn interest for providing liquidity. When you open a levered position by borrowing stablecoins like USDC against ETH, you owe those stablecoins back plus interest, regardless of how ETH performs; your leverage stems from selling borrowed USDC for more ETH and repeating the cycle. In both centralized and decentralized settings, the combination of collateral valuation, borrowing capacity, and margin thresholds determines how quickly stress in prices is transmitted into forced deleveraging through liquidations.

Profit and Loss Amplification

The critical feature of leverage is that it multiplies both profits and losses relative to your capital, a property that can be derived straightforwardly from the relationship between position size, price change, and equity. Suppose you hold \(1\) BTC on margin with \(10\times\) leverage and an initial notional exposure of \(30{,}000\) USD; your margin contribution is \(3{,}000\) USD and the remainder is effectively financed by the platform. If Bitcoin’s price rises by 10%, your position is now worth \(33{,}000\) USD, and your profit is \(3{,}000\) USD, which doubles your original margin, amounting to a 100% return on equity before fees and funding. Conversely, if Bitcoin’s price falls by 10%, your position declines to \(27{,}000\) USD, and you lose \(3{,}000\) USD, wiping out your entire initial margin and pushing you to or beyond your liquidation threshold. This symmetry means that at \(10\times\) leverage, a 10% adverse move can be enough to destroy your position, and at \(100\times\) leverage, even a 1% intraday price fluctuation can be fatal.

Educational materials often emphasize this amplification to highlight the risks of high‑leverage trading. In one illustrative example, a trader using \(5\times\) leverage on a \(1{,}000\) EUR deposit is effectively trading \(5{,}000\) EUR worth of Bitcoin; a 10% upward move in price generates a 500 EUR gain, corresponding to a 50% return on the original deposit, while a 10% downward move causes a 500 EUR loss, cutting the account in half. Pushing the leverage to extremes, a \(100\times\) leveraged position would double your money if the price rises by just 1%, but would wipe out your entire stake if the price falls by that same 1%, leaving no buffer for normal market noise. These simple arithmetic examples explain why many risk practitioners argue that there is a meaningful difference between modest leverage, such as \(2\times\) or \(3\times\) exposure used for hedging or capital efficiency, and very high leverage that transforms any trade into a binary bet on immediate price direction.

Leverage also affects the path dependency of returns. In a non‑levered spot position, a 10% loss followed by an 11.11% gain returns you approximately to breakeven; the impact of volatility on your portfolio is linear and relatively intuitive. In a leveraged position near its margin threshold, however, the same sequence might result in liquidation during the drawdown, preventing you from participating in the subsequent rebound. The Strive digital credit episode, where the STRC and SATA preferred‑like instruments fell sharply intraday before recovering as buyers stepped in, demonstrates how leveraged investors can be forced out at the lows by margin calls, even when asset prices later revert. This dynamic is intrinsic to the design of margin systems: they enforce discipline at the level of individual positions without regard to whether the price move is an overreaction that might reverse.

- 01Fixed leverage, no liquidation↗

f(x) Protocol's promise of leveraged exposure on blue-chip assets with no personal liquidation risk and zero funding costs drew the highest click volume, signaling readers want leverage upside without the existential downside.

- 02Extreme leveraged position spectacle↗

A 40x BTC short with a $85,300 liquidation price and the trader who forced Hyperliquid to revise risk parameters after a 50x ETH long both pulled strong clicks — real-money extremes make abstract leverage risk concrete.

- 03Leveraged meme coin access

Marginfi's mrgnswap for instant long/short on newly launched meme coins and Frax's BAMM fair-launch mechanic tapped the specific demand to apply leverage to the highest-volatility, shortest-lived assets.

- 04DeFi credit account protocols↗

Gearbox's credit accounts for Ethena yields (up to 90x on shards), Tren Finance's re-collateralization, and Curve's leveraged collateral integrations showed readers are tracking the infrastructure layer that makes leveraged loops composable.

- 05Leverage as macro crash trigger↗

The Bitcoin 10% plunge attributed to a leveraged market reaching a boiling point, elevated funding rates, and crypto debt hitting $53B all clicked because readers want to understand leverage as a systemic contagion mechanism, not just a personal trade tool.

- 06Yield loop leverage illusion

The xUSD/deUSD leverage illusion post and the BIS study on DeFi borrower behavior flagged that many 'yield' strategies are disguised leverage loops, and readers engaged with the unmasking of that hidden risk.

Why Traders Use Leverage

Despite its dangers, leverage remains central to crypto markets because it enables capital efficiency, hedging, and access to strategies that are difficult or impossible to implement using spot trading alone. For professional traders and institutions, one of the most compelling use cases is the ability to adjust net exposure without moving large amounts of capital on‑chain or through banking rails; for example, a fund might hold Bitcoin in cold storage while using regulated futures or perpetuals on a platform like Coinbase to hedge or fine‑tune their directional risk with up to \(10\times\) intraday leverage. Coinbase explicitly frames the introduction of CFTC‑regulated perpetual futures as a way for U.S. traders to “enhance capital efficiency and amplify their market positions” within a supervised environment, offering long‑dated contracts on Bitcoin and Ether that remain active for years rather than expiring every month. In such structures, leverage is a tool for optimizing portfolio logistics and basis trades rather than purely for speculative bets on short‑term price moves.

Leverage is also fundamental to hedging strategies used by miners, treasuries, and liquidity providers. A Bitcoin miner with significant expected output might short Bitcoin futures or perps with moderate leverage to lock in a floor price for their upcoming production; while the futures position may suffer mark‑to‑market losses if Bitcoin rallies, these losses are offset by higher realized prices for mined coins, stabilizing cash flows. Similarly, DeFi market makers often use leveraged derivatives to hedge the price risk of inventory held in automated market maker pools, aiming to isolate fee income while neutralizing directional exposure. In both cases, leverage allows the hedge to be sized appropriately without requiring the full notional value of the underlying asset to be held in the derivatives account, which would undermine capital efficiency. The downsides, however, are still present: poor margin management can lead to forced unwinds at the worst possible time, turning a hedged position into an unintended speculative loss.

Finally, for a subset of retail traders and some funds, leverage is explicitly a vehicle for speculation on volatility and directional moves, particularly in assets like Bitcoin that already exhibit high realized volatility. Swing‑trading strategies that seek to “profit from volatility” often rely on leveraged products to magnify the gains from correctly timing price swings, although the same amplification applies to timing mistakes. The introduction of leveraged futures and perpetuals on tokenized real‑world assets, such as stocks and ETFs, extends this speculative toolkit beyond native crypto, enabling traders to build cross‑asset macro positions that run 24/7. While these developments can deepen liquidity and make markets more complete, they also increase the scope for leverage‑driven contagion, where distress in one segment—whether Bitcoin, digital credit instruments like STRC and SATA, or a tokenized stock—spills over into others via forced deleveraging.

Banks earn far higher margins than DeFi lenders like Aave because crypto lending is dominated by leverage and yield loops, not real-economy credit. As onchain lending expands into RWAs and structured credit, margins could rise beyond crypto cycles.

Leveraged Instruments: From Futures to On‑Chain Loops

Leverage in crypto can be accessed through a variety of instruments, each with its own mechanics, risk profile, and regulatory treatment. The most prominent are centralized exchange futures and perpetual futures contracts, but DeFi has created its own ecosystems of lending‑based leverage, overcollateralized stablecoins, and on‑chain perpetuals.

Traditional futures contracts are standardized agreements to buy or sell an asset at a set price on a future date, and they have long been used in commodities and financial markets to hedge and speculate with leverage. Crypto exchanges extend this model to Bitcoin and other tokens, sometimes with monthly or quarterly expirations, requiring traders to roll their positions as contracts expire. Perpetual futures, or “perps,” modify this design by eliminating regular expirations and instead using a funding rate mechanism—a periodic payment between long and short positions—to keep the contract price anchored near the spot market. Coinbase’s U.S. platform offers a hybrid model: its “perpetual” futures on Bitcoin and Ether are long‑dated, with five‑year expirations, which allows traders to maintain exposure for extended periods without constant rollovers, while still granting up to \(10\times\) intraday leverage on crypto and even higher leverage on metals futures. These products bring one of the world’s most traded derivatives structures into a regulated crypto venue, extending the reach of leveraged trading for U.S. participants.

Other centralized platforms and derivatives venues provide leveraged exposure via CFDs (contracts for difference) and classic margin trading. In CFD models, as described by broker IG, traders can speculate on crypto price movements using leverage without owning the underlying coins; they post margin, gain full market exposure for a small deposit, and their profit or loss is the difference between entry and exit prices multiplied by the contract size. IG emphasizes that while this approach can magnify gains, it also increases risk, including the possibility that losses may exceed the initial deposit, particularly in fast markets or when stop‑loss orders are not used effectively. This stands in contrast to many crypto‑native derivatives exchanges, which employ auto‑liquidation algorithms to close positions before equity turns negative, although in extreme slippage scenarios or during outages, customers may still face deficits or socialized losses. The diversity of centralized leveraged products underscores the need for users to understand each platform’s specific margin policy and recourse rules before committing capital.

In DeFi, leverage often arises through lending‑borrowing platforms and overcollateralized stablecoin systems that allow “leverage loops.” Protocols such as f(x) Protocol are built around an overcollateralized stablecoin, fxUSD, which is backed solely by crypto collateral and designed to function both as a stable medium of exchange and as a component of a decentralized leverage trading system on Ethereum. Users deposit collateral (commonly liquid‑staking tokens or similar assets), mint fxUSD up to a certain collateralization ratio, and can then use that fxUSD to purchase more of the collateral or other leveraged exposures, effectively increasing their bet on the underlying asset. Venus Protocol extends this pattern with automated features such as “one‑click leverage boost,” which loops the process of supplying collateral, borrowing stablecoins, and buying more collateral into a single transaction, giving users a leveraged position without requiring manual repetition of each step. While these designs improve usability and capital efficiency, they also create highly levered structures where a downturn in collateral prices can rapidly cascade into liquidations across multiple protocols.

A particularly vivid example of on‑chain leverage concentration is the WLFI leverage loop on Dolomite, described by Chaos Labs and highlighted in community reporting. In that case, World Liberty Finance’s token WLFI serves as collateral backing a substantial amount of stablecoin debt—on the order of billions of tokens backing tens of millions of dollars worth of stablecoins, primarily USD1—through a looping structure that pushes the protocol close to its collateral cap. The mechanism involves borrowing a stablecoin like USD1 against WLFI, converting or pairing it with USDC, and re‑deploying the proceeds in ways that enable additional WLFI to be posted as collateral, thereby magnifying exposure to WLFI’s price. Such arrangements create tight coupling between the price of the collateral token, the stability of the borrowed stablecoin, and the solvency of the lending protocol; if WLFI’s price falls significantly, the protocol must liquidate WLFI to repay stablecoin lenders, which can push prices lower and potentially stress the stablecoin peg. This demonstrates how leverage in DeFi is not just an individual trader problem but an ecosystem‑level issue that can threaten the integrity of interconnected protocols.

- 2022-05exploit

Terra/LUNA collapse triggers DeFi leverage cascade to FTX

- 2024-01milestone

Bitcoin drops 10%; K33 analyst attributes crash to leveraged market overextension, not Matrixport ETF rejection alone

- 2024-04exploit

ezETH briefly depegs to 0.5 ETH; Gearbox users above 2x leverage liquidated

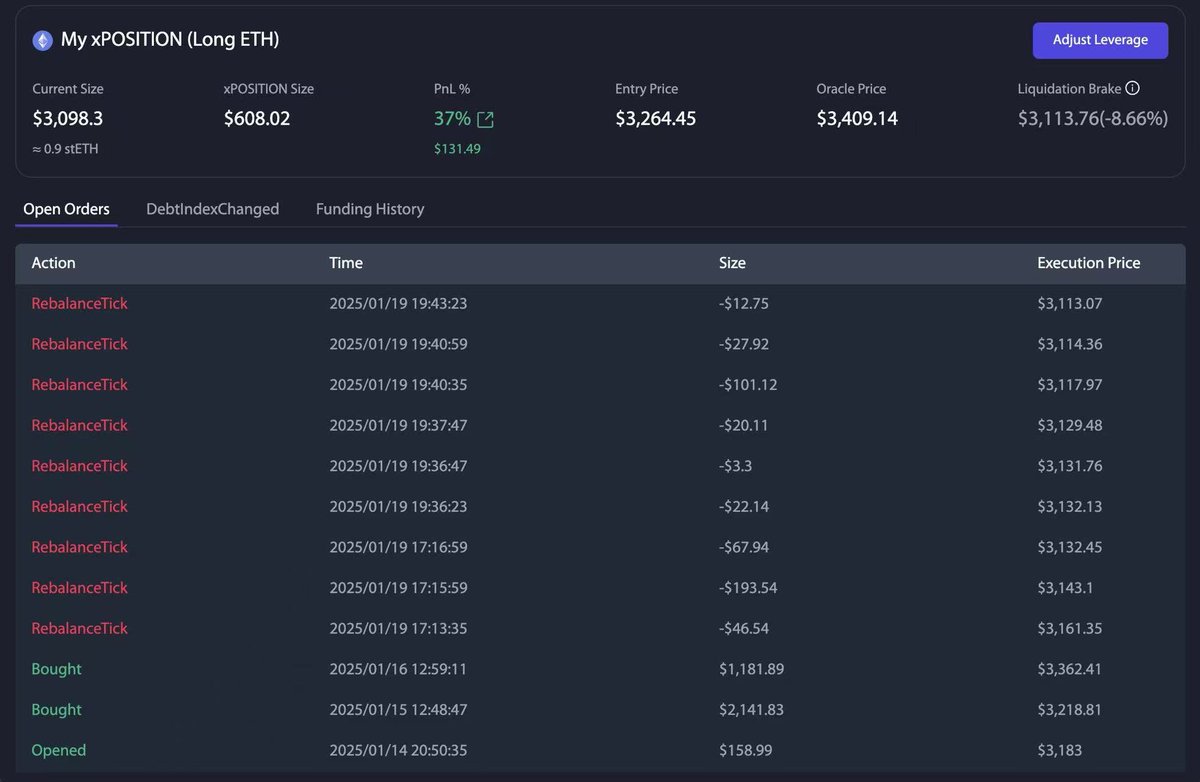

f(x) Protocol 2.0 launches xPositions and fxUSD dual-token model with fixed leverage and no personal liquidation risk

- 2024-11milestone

Bitcoin futures open interest hits $21B, highest since November 2021, amid leverage build-up warnings

f(x) Protocol introduces sPOSITIONs, adding fixed-leverage short capability with liquidation brake

- 2025-03milestone

Trader opens $332M BTC short at 40x leverage with $85,300 liquidation target, drawing wide market attention

- 2025-04governance

50x ETH long forces Hyperliquid to revise risk parameters for ETH and BTC after $4M profit trade

Liquidation Mechanics and Leverage Cycles

Given the ubiquity of leverage, understanding liquidation—the forced closure of a position when it no longer meets margin requirements—is crucial for any participant in leveraged crypto markets. Liquidation is triggered when the account equity, defined as margin plus unrealized profit and loss, falls below the required maintenance margin for a position. MetaMask explains that each leveraged perpetual futures position is governed by two margin thresholds: the initial margin needed to open the trade and the lower maintenance margin required to keep it open. On platforms such as Hyperliquid, the maintenance margin rate at maximum leverage can be set at roughly half the initial margin rate; for instance, at \(20\times\) maximum leverage, an initial margin rate of 5% corresponds to a maintenance margin rate of 2.5%. When the account’s equity falls below that 2.5% level, the liquidation engine steps in, typically selling part or all of the position into the market in order to restore margin compliance and protect the platform from counterparty risk.

Traders often encounter liquidation as a seemingly sudden event, but it is the predictable outcome of the margin arithmetic. When opening a leveraged position, exchanges display a liquidation price, which is the estimated price at which the combination of your leverage and collateral would cause equity to breach the maintenance threshold; however, this estimate assumes constant funding rates and no changes in collateral. Coinbase, in its guidance on avoiding liquidations in perpetual futures, emphasizes the need to monitor and adjust leverage over time, set stop‑loss orders that close positions before the liquidation price is reached, and maintain a liquidation buffer—additional funds above the maintenance margin that can absorb normal volatility. By keeping extra margin in the account, traders can withstand temporary drawdowns and price wicks that might otherwise trigger forced liquidations, especially in markets like Bitcoin where intraday swings of several percent are common. The fundamental principle is that liquidation should be treated as a failure of risk management, not as a routine exit strategy.

Liquidations can scale from individual events into market‑wide episodes when leverage is widespread and correlated across participants. The recent turmoil in digital credit products STRC and SATA, managed by Strive and Bitcoin‑focused Strategy, is a case in point. On a particularly volatile day, STRC, a high‑yield perpetual preferred stock designed to trade near a 100 USD par value, plunged to a record low in the low 80s before partially recovering, while its sibling SATA dropped from par into the low 90s and then rebounded later in the session. Strive’s CEO Matt Cole described the episode as “the most difficult day in the history of Digital Credit” and characterized the price action as a leverage liquidation event, not a deterioration in underlying credit quality. According to his account, investors seeking higher yields had borrowed against STRC and SATA positions; when prices began to fall, margin calls forced these leveraged holders to sell, pushing prices lower and triggering further liquidations in a self‑reinforcing spiral. Although both instruments later saw substantial buying interest off their intraday lows, the episode illustrated how leverage can transform ostensibly stable income products into highly volatile assets during stress.

In DeFi, liquidation waves are often tied to shifts in the on‑chain leverage ratio and exogenous shocks such as hacks or large market drawdowns. Binance Research has noted that a series of DeFi exploits drove around 13 billion USD in outflows from protocols over a single month, causing total value locked (TVL) to fall by 10.7% to roughly 82.7 billion USD. Because borrowing did not decline as quickly as deposits, the on‑chain leverage ratio—defined as total borrowing relative to TVL—rose to about 38%, a level last seen during the 2021 bull‑market cycle. This elevated leverage ratio indicated that deleveraging remained incomplete, leaving the system vulnerable to further shocks if collateral prices fell or if additional security incidents undermined confidence. In such conditions, even modest declines in asset prices can push large swaths of positions towards their liquidation thresholds, leading to automated selling of collateral, widening on‑chain slippage, and potentially destabilizing stablecoins and other assets tied into leverage loops.

Funding rates in perpetual futures add another dimension to these cycles by influencing the cost of leverage over time. Perpetual contracts generally include a periodic funding payment between longs and shorts, often every few hours, designed to keep the perp price aligned with spot markets. When the perp trades above spot, the funding rate tends to be positive, and long positions pay shorts; when it trades below spot, funding can be negative, rewarding longs at the expense of shorts. MetaMask’s analysis of funding frequency highlights that more frequent funding leads to more granular cost adjustments and can materially affect the profitability of strategies that rely on holding leveraged positions for extended periods. Some DeFi platforms position themselves explicitly as alternatives to funding‑bearing perps: Venus Protocol, for example, has contrasted its “Venus Trade” product with perpetual exchanges by emphasizing that there are no funding rates and that positions can earn net APY rather than incur continuous costs. Nonetheless, while removing funding charges can reduce the drag on long‑term leveraged positions, it does not eliminate liquidation risk, which remains governed by collateral values, borrow rates, and price volatility.

Risk Management: Using Leverage Without Blowing Up

Effective risk management is the key differentiator between using leverage as a professional tool and treating it as a form of gambling. One cornerstone concept is the idea of position sizing based on a predetermined maximum loss per trade, often expressed as a percentage of total account equity. IG suggests that traders consider what percentage of their account each leveraged position represents and recommends a rule of thumb that no more than roughly 2–5% of the account balance be put at risk on any single trade. This implies working backwards from an acceptable loss to determine both the position size and the leverage ratio: if a trader with a 10,000 USD account is willing to risk 300 USD on a Bitcoin trade and wants to place a stop‑loss 3% away from the entry price, the notional position should be sized so that a 3% price move corresponds to a 300 USD loss, regardless of how much leverage is employed. Thinking in this way forces a shift from focusing on “how big” a position can be to focusing on “how much can I comfortably lose” if the trade goes wrong.

Monitoring effective leverage across the portfolio is equally important, particularly in volatile markets like crypto where correlations can spike under stress. MetaMask emphasizes that effective leverage, defined as position size divided by account equity, changes in real time as positions move and as funding payments or realized PnL alter the equity base. A trader might open several moderate‑leverage trades on Bitcoin, Ether, and a DeFi index token, each individually within their risk limits, only to find that a correlated market move has pushed the account’s overall effective leverage to dangerous levels. Regularly calculating and tracking this metric, and adjusting positions accordingly, can help prevent situations where a sudden but plausible market drawdown threatens to liquidate multiple positions simultaneously. In practice, this may involve voluntarily reducing leverage or closing some positions during periods of heightened volatility, even if each individual trade still appears “safe” when evaluated in isolation.

Operational tools such as stop‑loss orders and liquidation buffers are practical mechanisms for enforcing discipline. Coinbase’s guidance on avoiding liquidations in perpetual futures stresses that setting stop‑loss orders at levels above the liquidation price allows traders to exit positions before their margin is exhausted, preserving capital for future opportunities. A stop‑loss that closes a position when it is down, for example, 30% on equity may be painful, but it is preferable to an automatic liquidation that not only realizes the loss but may also incur additional fees or slippage in a stressed order book. Coinbase also recommends maintaining a liquidation buffer by keeping extra funds in the account beyond the minimum maintenance margin, thus creating a cushion against short‑term volatility and market “wicks” that might temporarily push prices through key levels. Pro traders often treat this buffer as non‑negotiable capital dedicated to absorbing adverse moves, rather than as available margin for new trades, recognizing that the absence of such a buffer is what often turns normal volatility into catastrophic loss.

Diversification and analysis contribute to a holistic risk framework. Relying on a single, highly leveraged position concentrates risk and increases the likelihood of liquidation if the market moves against you, whereas spreading capital across different assets and contract types can mitigate idiosyncratic shocks. Coinbase notes that successful derivatives traders typically use both fundamental analysis, to assess the long‑term prospects and macro context of the underlying asset, and technical analysis, to identify price patterns, support and resistance levels, and potential entry and exit points. Coupling analysis with continuous monitoring of market conditions, news, and on‑chain data can help traders anticipate volatility events, such as protocol exploits or regulatory announcements, that might disproportionately impact leveraged positions. This multi‑layered approach to risk management does not guarantee success, but it shifts leverage from being a blunt instrument into a controlled variable within a broader trading plan.

Collateral selection is another lever for managing risk. Posting USDC or other high‑quality stablecoins as margin for Bitcoin or Ether perps can reduce the risk of collateral‑position correlation, where both the collateral and the underlying move adversely at the same time. However, stablecoins themselves carry risks, including de‑pegging and protocol‑specific vulnerabilities, especially when they are backed by leveraged DeFi positions or rehypothecated collateral, as in some overcollateralized stablecoin systems. Using volatile collateral such as WLFI, STRC, or smaller‑cap tokens to back leveraged positions may enable higher notional exposure but also exposes traders to the possibility of rapid collateral value erosion, as observed in episodes where such tokens experienced sharp sell‑offs tied to leverage unwinds. Balancing these considerations involves weighing the cost and availability of different collateral types against their volatility, liquidity, and systemic risk profile.

Europe is about to list 3x long and short Bitcoin and Ethereum ETFs, giving traders extreme leverage at a time when markets are already sliding. LeverageShares’ products hit the SIX Exchange next week, adding fuel to an already volatile environment.

wait x3 supposed to be extreme ?

Concentrated large leveraged positions (40x BTC short, 50x ETH long) can force protocol-level parameter changes and trigger chain liquidations that affect other users, as seen in the Hyperliquid and ezETH incidents.

Credit account architectures (Gearbox, Tren Finance) and novel invariant-based designs (f(x) fxUSD) introduce composable leverage that multiplies smart-contract attack surface across the protocols they integrate with.

- LiquidityHigh

ezETH's brief depeg to 0.5 ETH showed that leveraged positions on LRT collateral can force rapid unwinding when peg assumptions break, draining liquidity faster than liquidation mechanisms can absorb.

Elevated Bitcoin funding rates and $21B+ futures open interest signal crowded leveraged positioning; when the bet unwinds, price moves are amplified well beyond underlying news, as the Matrixport-linked January 2024 crash illustrated.

- RegulatoryMedium

Offshore perpetual futures offering up to 200x leverage (Ostium) and 50x on Binance face increasing scrutiny, with BIS researchers explicitly studying DeFi leverage as a financial-stability concern and calls for SEC/DOJ action surfacing in clicked headlines.

- Hidden / Systemic LeverageHigh

Crypto debt reached $53B in Q2 2024 with onchain loans up 42%, and BIS researchers noted DeFi leverage loops are under-documented; hidden leverage in yield strategies and RWA credit could propagate contagion analogous to the 2022 Terra-to-FTX cascade.

DeFi Design Choices: Stabilizing or Amplifying Leverage

DeFi protocols are not merely passive venues where leverage appears; they actively encode leverage dynamics through design choices around collateral factors, interest‑rate curves, liquidation penalties, and product architecture. Overcollateralized stablecoins such as fxUSD in the f(x) Protocol exemplify how seemingly conservative designs can still embody significant leverage. fxUSD is backed solely by crypto collateral deposited at a value greater than the stablecoin issued, with liquidation mechanisms that sell collateral if its value falls below a specified threshold relative to the outstanding fxUSD. Users who mint fxUSD and then use it to buy more of the same collateral asset, or to gain exposure through derivatives or liquidity positions, are effectively increasing their leverage, even though each individual transaction might appear “overcollateralized.” In aggregate, this creates an ecosystem where the stablecoin’s stability depends on the collateral’s market performance and where drawdowns can trigger waves of collateral auctions and liquidations.

Automation features such as Venus Protocol’s “one‑click leverage boost” further shape user behavior. By packaging the classic “looping” strategy—supplying collateral, borrowing stablecoins, buying more collateral, and re‑supplying—into a single user‑friendly interface, Venus lowers the technical barrier to entering leveraged positions while potentially increasing the typical leverage level that users choose. The protocol’s documentation explains that the boost function fully automates the looping process, enabling users to reach their target leverage ratio in one step, rather than performing multiple transactions manually. While this can be advantageous for sophisticated users who understand the risks and are comfortable managing them, it may also entice less experienced participants to take on complex, path‑dependent leverage exposures without fully grasping how quickly their positions can be liquidated if the collateral’s price falls. The tension between accessibility and complexity is a recurring theme in DeFi leverage design.

Some DeFi platforms consciously differentiate their offerings by emphasizing reduced risk dimensions relative to perpetual futures exchanges. Venus, for instance, contrasts its “Venus Trade” product with perps by highlighting that, on perp exchanges, funding rates continuously eat into positions, a single sharp move can cause 100% liquidation, and leverage can quickly work against traders, whereas on Venus Trade there are no funding rates and positions can earn net APY through lending yields. This framing underscores that Venus seeks to reorient leverage around interest‑bearing positions rather than around highly reflexive derivative contracts. However, even in such systems, the core mechanics of borrowing against collateral and facing liquidation if collateral value falls remain in place; the absence of a funding rate does not remove leverage risk but changes its cost structure and the way it accumulates over time. Evaluating claims of “safer” leverage therefore requires understanding which risk channels have been addressed and which remain intact.

Governance and protocol risk management play a critical role in mediating system‑wide leverage. Many lending and stablecoin protocols employ governance processes to adjust collateral factors, borrowing limits, and liquidation incentives in response to changing market conditions, often on the basis of analyses from risk firms and community researchers. When Binance Research notes that the on‑chain leverage ratio has risen back toward 2021 levels after a period of TVL contraction and exploits, it is effectively signaling that protocol‑level parameters may need to tighten to encourage deleveraging and reduce systemic fragility. Similarly, the WLFI leverage loop near Dolomite’s collateral cap demonstrates the need for dynamic caps and concentration limits that prevent any single asset or strategy from dominating a protocol’s risk profile. Regular updates to leverage and margin tiers, including those for USD‑margined perpetual contracts on centralized derivatives platforms, can be viewed as analogues of these on‑chain governance adjustments, reflecting a shared recognition that leverage levels must be actively managed rather than left to free‑market dynamics alone.

Regulation, Market Structure, and the Global Leverage Race

The evolution of leverage in crypto is closely intertwined with regulatory developments and the maturation of market structure. For many years, the highest leverage offerings—sometimes up to \(100\times\) or more—were concentrated on offshore exchanges with limited regulatory oversight, where retail traders could easily open accounts and access extreme margin. As regulators have taken a greater interest in crypto derivatives, there has been a shift toward bringing leveraged trading within supervised frameworks, particularly in major jurisdictions like the United States. Coinbase’s launch of CFTC‑regulated perpetual futures for U.S. customers, with up to \(10\times\) leverage on crypto and higher leverage on metals, is one manifestation of this shift. Barron’s has characterized the regulatory approval of such products as ushering in a “new era of high leverage crypto trading” for mainstream platforms like Coinbase and Robinhood, suggesting that leverage is moving from the periphery of speculative exchanges to the core of regulated financial services.

Regulated venues often adopt risk‑based margining practices informed by traditional finance. In the equities and options world, portfolio margin is a methodology that sets margin requirements based on the overall risk of a trader’s portfolio rather than on rigid percentage rules for each position. Charles Schwab explains that portfolio margin involves running stress tests on a portfolio across various scenarios of price and volatility changes—typically using at least a 15% price move up or down as the baseline for equities—and then setting the margin requirement equal to the largest theoretical loss observed under those scenarios. Eligibility criteria for portfolio margin are strict, requiring, for example, a minimum net liquidation value of 125,000 USD and advanced options trading approval, reflecting the higher complexity and potential risk of this margining approach. Crypto derivatives platforms that roll out “portfolio margin” features for professional users or cross‑asset margin across Bitcoin, altcoins, and tokenized instruments are implicitly adopting similar logic, even if their specific stress parameters differ due to the higher volatility of crypto assets.

At the same time, competitive pressures and marketing dynamics continue to push leverage offerings upward in some segments. MetaMask notes that while many decentralized platforms limit leverage to about \(10\times\) to \(25\times\) on major markets, some centralized exchanges list leverage up to \(125\times\) on certain pairs, particularly in Bitcoin and highly liquid altcoins. Retail‑oriented trading venues sometimes advertise increased leverage limits across crypto, commodities, equities, and index ETFs, promising traders the ability to “do more with less capital,” including high‑leverage trades on assets like gold and large‑cap technology stocks. Even meme‑coin ecosystems announce the introduction of leveraged trading as part of contests and marketing campaigns, framing higher leverage as a way to showcase conviction and compete on returns. These trends illustrate an ongoing global leverage race, where platforms balance regulatory constraints, risk management, and user demand for capital efficiency and speculative opportunity.

An additional layer of complexity arises from the tokenization of real‑world assets and the blending of crypto leverage with traditional asset classes. Perpetual futures on tokenized stocks or ETFs, operating on a 24/7 basis, enable traders to express views on conventional equities using crypto margin and often higher leverage than is available in traditional broker accounts. This convergence means that leverage‑driven disturbances in tokenized stock markets could spill over into crypto liquidity and vice versa, especially if collateral assets and stablecoins are shared across these markets. Episodes like the Strive digital credit sell‑off or the WLFI leverage loop remind observers that when structured products and novel instruments are interfaced with leverage, their behavior can deviate sharply from the expectations set by their nominal design—whether that design is “par‑linked” preferred shares or “stable” tokens. Regulators and risk managers must therefore adapt existing frameworks to address the question of how much leverage is appropriate when the underlying assets themselves are newly engineered.

Finally, the broader use of the term “leverage” in technology and governance discourse can obscure the risks of financial leverage if not clearly distinguished. Aethir Mesh’s description of helping developers “leverage” open‑source LLMs through a GPU‑powered API layer, for instance, revolves around enhancing computational and development efficiency rather than borrowing capital or taking on debt. While this metaphorical usage is widespread in tech and Web3, it can create ambiguity in product messaging when combined with explicit financial leverage offerings. For example, a protocol might claim to “leverage decentralized liquidity” while also offering highly leveraged trading; careful reading is required to understand which claims pertain to resource optimization and which refer to leveraged financial exposure. For a crypto news audience, clarifying this distinction is essential to accurate reporting and to helping users understand what kinds of risk they are truly assuming.

Conclusion

Leverage sits at the center of modern crypto markets, functioning simultaneously as a powerful tool for capital efficiency and hedging and as a source of fragility and sudden, often violent market dislocations. At the micro level, every leveraged trade is governed by the arithmetic of margin, collateral, and price volatility; concepts such as initial and maintenance margin, liquidation price, and effective leverage determine how quickly a position can transition from profit to forced closure. The amplification of returns that makes leverage attractive also means that seemingly small price moves or transient volatility spikes can wipe out positions, particularly when traders stretch to high nominal leverage ratios or fail to maintain adequate liquidation buffers. Case studies ranging from classic Bitcoin perps to digital credit instruments like STRC and SATA show that margin calls and leverage liquidations can overwhelm fundamentals in the short term, driving prices away from par or intrinsic value before opportunistic buyers step in.

At the system level, aggregate leverage metrics such as the on‑chain leverage ratio, open interest in futures, and concentrations of collateral and borrowing in DeFi protocols act as barometers of potential systemic stress. Binance Research’s observation that the on‑chain leverage ratio returned to around 38% as TVL contracted following DeFi exploits illustrates how markets can remain highly levered even after shocks, leaving them vulnerable to subsequent deleveraging waves. Structures like the WLFI leverage loop on Dolomite and overcollateralized stablecoin systems such as f(x) Protocol’s fxUSD demonstrate how interconnected leverage can tie the fortunes of multiple tokens and protocols together, where the failure or devaluation of one component can propagate swiftly through stablecoins, lending markets, and liquidity pools. Against this backdrop, both centralized exchanges and DeFi protocols rely on dynamic margin tiers, collateral ratios, and governance decisions to modulate leverage availability, aiming to mitigate—not eliminate—the risk of cascading liquidations.

Regulation and platform design increasingly shape how and where leverage is deployed. The emergence of CFTC‑regulated crypto perpetual futures in the U.S., as exemplified by Coinbase’s product suite, indicates that leverage is migrating into more supervised environments, bringing with it both the benefits of investor protections and the challenges of integrating high‑volatility assets into traditional risk frameworks. At the same time, competition among platforms for user capital continues to drive innovation in leverage offerings, from high‑multiple perps and cross‑asset portfolio margin to on‑chain leverage automation via one‑click “boost” features. For traders, investors, and protocol designers, the central task is to recognize leverage as neither inherently good nor bad but as a multiplier whose effects depend on how prudently it is used and how robustly it is managed at both the individual and system level.

Outlook

Looking ahead, leverage in crypto is likely to become more structurally embedded yet more carefully risk‑managed as markets mature. Regulated venues will probably expand their derivatives offerings on assets like Bitcoin and tokenized stocks while maintaining moderate leverage caps and sophisticated margining systems modeled on portfolio margin in traditional finance. In DeFi, protocols may continue to experiment with novel forms of leverage, including composable stablecoins, cross‑chain lending, and AI‑driven risk engines, even as risk managers and governance communities react to episodes like exploit‑driven deleveraging and concentrated leverage loops by tightening parameters and diversifying collateral bases. For market participants, the practical implication is that leverage will remain a defining feature of crypto, offering both opportunity and danger; those who invest in understanding its mechanics, costs, and systemic implications will be better positioned to navigate the cycles of exuberance and deleveraging that characterize this evolving market structure.

Latest Leverage news

Lessons from 1890 Baring Crisis: Argentine Debt Bubble Triggers Transatlantic Contagion, Mirroring 2022 DeFi Cascade from Terra to FTX. Key Takeaways: Shun Unsustainable Yields and Hidden LeverageBanks earn far higher margins than DeFi lenders like Aave because crypto lending is dominated by leverage and yield loops, not real-economy credit. As onchain lending expands into RWAs and structured credit, margins could rise beyond crypto cycles.Europe is about to list 3x long and short Bitcoin and Ethereum ETFs, giving traders extreme leverage at a time when markets are already sliding. LeverageShares’ products hit the SIX Exchange next week, adding fuel to an already volatile environment. Crypto-backed debt hit a new all-time high in Q3 2025, driven by onchain borrowing as lending apps now dominate 80% of the market—marking a far more disciplined environment than the 2021–22 leverage boom.

Crypto-backed debt hit a new all-time high in Q3 2025, driven by onchain borrowing as lending apps now dominate 80% of the market—marking a far more disciplined environment than the 2021–22 leverage boom. Former FTX US president Brett Harrison criticized crypto exchanges offering up to 1,000x leverage, calling it “irresponsible” and harmful to traders. His new platform, Architect, limits leverage to 25x on traditional assets.

Former FTX US president Brett Harrison criticized crypto exchanges offering up to 1,000x leverage, calling it “irresponsible” and harmful to traders. His new platform, Architect, limits leverage to 25x on traditional assets. Bitcoin and Ether treasury firms like Metaplanet, Lite Strategy, and ETHzilla are kicking off a $500M-plus buyback wave, signaling a shift toward corporate-style capital optimization as digital asset treasuries blend BTC leverage with traditional equity management.

Bitcoin and Ether treasury firms like Metaplanet, Lite Strategy, and ETHzilla are kicking off a $500M-plus buyback wave, signaling a shift toward corporate-style capital optimization as digital asset treasuries blend BTC leverage with traditional equity management.Sources

- https://www.youtube.com/watch?v=MYnkNaBMjlg&vl=en

- https://www.ig.com/au/crypto-need-to-knows/leverage-trading-crypto

- https://cryptonews.net/news/defi/33015271/

- https://www.coinbase.com/blog/perpetual-futures-have-arrived-in-the-us

- https://x.com/WuBlockchain/status/2067855554400370887

- https://metamask.io/news/perpetual-futures-funding-frequency-strategies

- https://financefeeds.com/strive-ceo-blames-strc-and-sata-sell-off-on-leverage-liquidation/

- https://cryptopotato.com/strive-ceo-sharp-strc-sata-drops-were-leverage-liquidations-not-credit-failures/

- https://x.com/DecryptMedia/status/2068016712843247735

- https://x.com/VenusProtocol/status/2054875298324222012

- https://docs-v4.venus.io/guides/leveraged-positions

- https://x.com/barronsonline/status/2060405260296839257

- https://veli.io/blog/how-to-profit-from-volatility-a-guide-to-crypto-swing-trading/

- https://x.com/WuBlockchain/status/2043513764897820782

- https://www.coingecko.com/en/coins/f-x-protocol

- https://www.coinbase.com/learn/perpetual-futures/key-strategies-to-avoid-liquidations-in-perpetual-futures

- https://metamask.io/news/leverage-margin-perpetual-futures-trading

- https://www.schwab.com/learn/story/understanding-portfolio-margin

- https://ecosystem.aethir.com/blog-posts/aethir-mesh-opens-the-llm-api-layer-to-everyone-leverage-top-tier-open-source-llms

Community notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…