Liquidation in crypto forcibly closes leveraged positions when collateral falls below required thresholds — a mechanism that can cascade across Bitcoin, Ethereum, and DeFi markets, erasing billions in minutes.

- x.com14

- coinglass.com11

- theblock.co9

- coindesk.com4

- leviathannews.substack.com3

- cryptonews.com2

- decrypt.co2

+10 sources across the wider coverage universe

InfiniFi makes case for duration-native RWA liquidator, arguing levered looping cannot scale without someone holding assets to maturity2026-03

InfiniFi makes case for duration-native RWA liquidator, arguing levered looping cannot scale without someone holding assets to maturity2026-03 Crypto liquidations hit $272M in 24 hours as stock market downturn impacts 81,838 traders, Coinglass data shows.2024-08

Crypto liquidations hit $272M in 24 hours as stock market downturn impacts 81,838 traders, Coinglass data shows.2024-08 BAMM is here, and it’s changing DeFi lending forever.

No price oracles. No sudden liquidations. Just pure on-chain borrowing inside an AMM. Frax just rewrote the lending playbook, and we broke it all down.

How BAMM works, the math behind oracle-free lending, and why this changes everything for LPs and borrowers.

Read the full deep dive now2025-02

BAMM is here, and it’s changing DeFi lending forever.

No price oracles. No sudden liquidations. Just pure on-chain borrowing inside an AMM. Frax just rewrote the lending playbook, and we broke it all down.

How BAMM works, the math behind oracle-free lending, and why this changes everything for LPs and borrowers.

Read the full deep dive now2025-02 Leviathan News Update on $SQUID Lending Market2025-06

Leviathan News Update on $SQUID Lending Market2025-06- Long positions suffer significant losses as market volatility triggers $138 million in liquidations on centralized exchanges within 24 hours, while short positions only contribute minor losses of around $18 million.2024-01

- Whitehats uncover exploitable vulnerability in Hyperliquid’s FRIEND-USD TVL-based oracle, sparking index changes and maintenance margin refunds for liquidations2023-08

When a leveraged position's collateral falls below the minimum required threshold, exchanges and protocols forcibly close it — a process called liquidation that can ripple across markets in seconds and erase billions in open interest.

What Liquidation Means in Crypto Markets

Liquidation is the mechanism that enforces solvency in leveraged trading and collateralized lending. It exists across two main contexts: centralized derivative exchanges (where traders use margin to open futures or perpetual contracts) and decentralized lending protocols (where borrowers lock up crypto assets to mint stablecoins or take out loans).

In both cases, the core logic is the same: a borrower or trader pledges collateral to control a position larger than their capital warrants. If the value of that collateral drops — or the value of the borrowed position rises against them — to a point where losses would exceed what the collateral can cover, the system intervenes. The position is closed, the collateral is seized (and usually sold), and the trader's equity goes to zero or near zero.

The mechanics differ slightly by venue. On centralized perpetual futures exchanges like Binance, OKX, or Bybit, the exchange's risk engine monitors a trader's maintenance margin ratio continuously. Once the ratio breaches a floor, an automated liquidation engine closes the position at market. On DeFi lending protocols like Aave or Kamino, a health factor (the ratio of collateral value to borrowed value, adjusted by risk parameters) governs the same process — when it drops below 1.0, third-party liquidators are incentivized to repay a portion of the debt and claim collateral at a discount.

InfiniFi makes case for duration-native RWA liquidator, arguing levered looping cannot scale without someone holding assets to maturity

122-day exit exposure on some RWA redemptions and DeFi is out here looping these things 3-4x like they're ETH. Gauntlet's levered RWA vaults auto-adjust leverage ratios, but that assumes a liquid counterparty can absorb the underlying when cascading liquidations hit — you can't atomically settle a private credit position the way you unwind an on-chain perp. InfiniFi's bet is that duration-matching at the liability layer (letting depositors self-select lock-up periods) creates the structural buyer that looping protocols assume exists but doesn't. DeFi is basically recreating the lender-of-last-resort problem from scratch, except this time the bank run happens in blocks, not days — and there's no Fed discount window to backstop the mismatch.

Readers click liquidation coverage for two opposite reasons at once: to benchmark cascade scale (exact dollar totals and trader counts validate their market read) and to discover protocols that make those cascades structurally avoidable — revealing an audience that is simultaneously leveraged risk-on and hunting for mechanisms that protect against itself.

How Margin and Leverage Set the Stage

The higher the leverage, the smaller the price move required to trigger liquidation. A trader using 10× leverage on a Bitcoin long position can be wiped out by a 10% adverse move before fees are even considered. At 50×, a 2% dip is enough.

Perpetual futures — the dominant derivative product in crypto — have no expiry date, which means positions can be held indefinitely as long as margin requirements are met. But they also accumulate funding rates (periodic payments between longs and shorts to keep the contract price anchored to spot), which slowly drain margin on the wrong side of a crowded trade. A position that survives volatile days can still be bled out over time by persistent negative funding.

As covered in recent market analysis, a single 1% price move on a highly leveraged perpetual can eliminate a position entirely. Strive Asset Management explicitly cited "leverage liquidations" as a proximate cause when holdings in SATA and Strategy's STRC fell sharply — illustrating that the damage from forced selling isn't limited to the trader being liquidated; it extends to any asset the affected entity holds or is associated with.

Cascading Liquidations: How a Dip Becomes a Crash

The most consequential aspect of liquidations is their self-reinforcing nature. When a large tranche of long positions is liquidated, the exchange's engine must sell the underlying asset to recover collateral. That selling pressure pushes the price lower. Lower prices breach the liquidation thresholds of the next tier of leveraged longs. Those get sold too. Prices fall further.

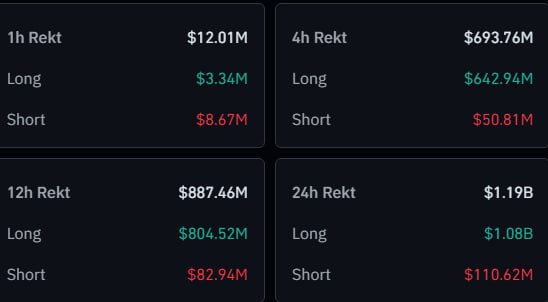

This cascade has played out repeatedly across Bitcoin and Ethereum markets. When Ethereum fell below $1,800 in mid-2025, it wasn't simply because of macro capital rotation — the decline was amplified by cascading liquidations that created forced selling precisely when buy-side liquidity was thinning. In one 24-hour window tracked by aggregators, 307,787 traders were liquidated for a combined $1.19 billion, with the single largest order — a $33.95 million BTC-USDT position on HTX — illustrating how concentrated leverage can concentrate the damage.

Key price levels function as liquidation clusters: a large number of positions are typically opened with stop-losses or liquidation prices around round numbers or prior highs/lows. Deribit's Chief Commercial Officer has pointed to $60,000 BTC as a historically significant level, with more than $1.2 billion in notional open interest tied to put options at that strike — meaning a break below it would not only trigger directional selling but could force delta-hedging flows from options dealers, amplifying the move.

- 01Cascade scale and trader counts

Headlines reporting precise totals ($520M, $677M, $1.35B) and exact trader counts (214,025 liquidated in 24 hours) drew the highest sustained engagement because readers use these figures to calibrate their own exposure against market-wide damage in real time.

- 02Soft liquidation vs hard liquidation

The stark contrast between Curve LLAMMA protecting only $4K in liquidations versus $436M wiped in raw on-chain markets during the same ETH crash gave readers a concrete performance comparison between protection architectures under live stress.

- 03Oracle-free AMM-native lending

BAMM's promise of liquidation-free borrowing inside an AMM attracted readers tracking whether oracle manipulation — the canonical liquidation attack vector — can be eliminated by design rather than patched.

- 04Macro triggers timing cascades

Trump tariff threats, the yen carry-trade unwind, and stock market selloffs appearing as direct 60-minute liquidation triggers gave readers a causal chain linking TradFi macro events to on-chain cascade timing they could trade around.

- 05CEX data opacity and undercounting

The framing that widely-cited $1B liquidation figures are systematic underestimates due to opaque exchange reporting resonated with readers skeptical of Binance and peers as authoritative data sources.

- 06Protocol-level liquidation system failures

Specific incidents — Hyperliquid's exploitable TVL-based oracle and f(x) Protocol's parallel RPC failure triggering rare liquidations — drew readers tracking which on-chain safety mechanisms break under real operational stress.

Short Liquidations: The Other Direction

Liquidations cut both ways. When prices rise sharply, short sellers face forced buybacks. These short squeezes can be as violent as long liquidations, because covering a short means buying the underlying asset, which lifts the price further and pressures more shorts into covering.

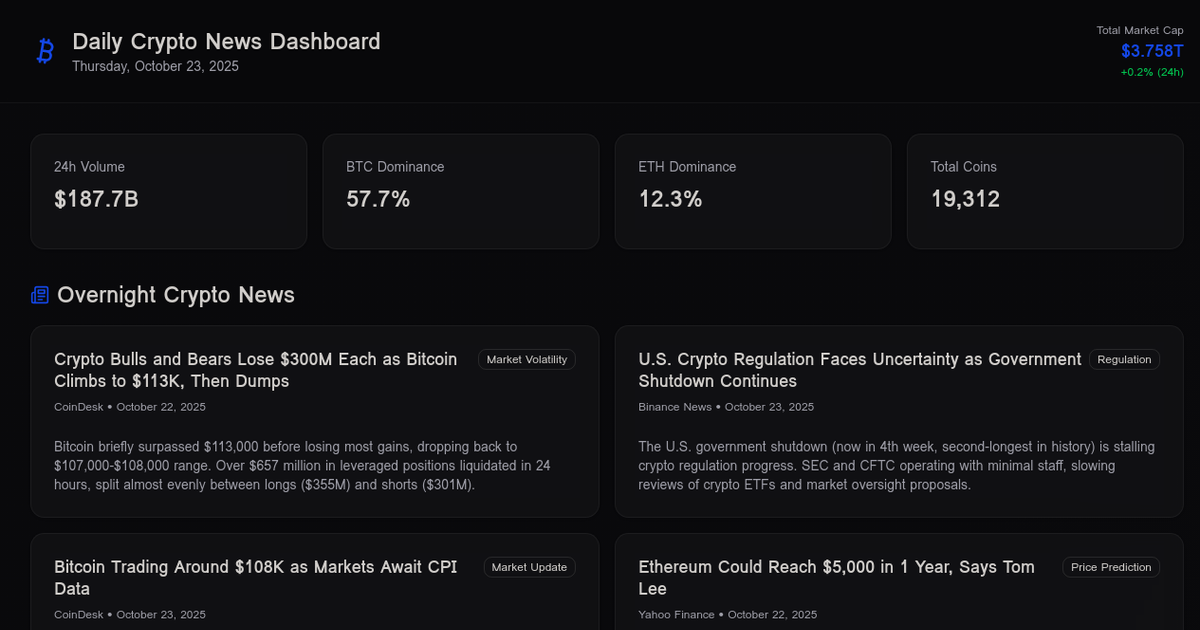

When Bitcoin and Ethereum jumped simultaneously in recent weeks, the result was a wave of mass short liquidations — traders who had bet on declining prices found their collateral evaporating. Data from the same 24-hour windows that record billion-dollar long wipeouts regularly show hundreds of millions in short liquidations during relief rallies. With Bitcoin swinging between $107,000 and $113,000 in a recent volatility episode, $657 million in total liquidations were recorded, with short and long positions taking losses in sequence as price whipsawed.

Crypto markets are increasingly bearish as Bitcoin sharply falls from recent all-time highs. Myriad predictors now assign higher odds to further declines, while hopes for a December Fed rate cut fade, adding macro uncertainty and fueling potential liquidations.

So the market is bound to crash the more. Not really a good time

DeFi Lending Liquidations

Decentralized lending introduces a different set of actors and risks. Protocols like Aave, Compound, Morpho, and Kamino allow users to deposit collateral and borrow against it. Rather than a centralized engine, these protocols rely on open liquidator bots — automated agents that monitor health factors and step in when a position becomes undercollateralized.

The incentive for liquidators is a discount: they repay a fraction of the borrower's debt and receive collateral worth more than what they paid. This creates a market for liquidation as a service — MEV (maximal extractable value) searchers compete to be first to trigger profitable liquidations, often within the same Ethereum block as a price oracle update.

This system works well under normal conditions but has failure modes. Aave suffered a significant incident when an oracle malfunction triggered $26 million in unfair wstETH liquidations — positions that should not have been undercollateralized were closed because the price feed temporarily reported incorrect values. Oracle manipulation is a recognized attack vector that can synthesize liquidation conditions that do not reflect real market prices.

Kamino's Q1 2026 growth report showed $2.93 billion in supply against $1.15 billion in borrows — a scale at which even moderate volatility can produce meaningful liquidation volumes, and where protocol design choices around liquidation thresholds and oracle selection carry systemic weight.

- 2023-05launch

Curve crvUSD with LLAMMA soft-liquidation mechanism launches on Ethereum mainnet

- 2024-08milestone

Yen carry-trade unwind and Jump Trading rumors trigger $840M crypto futures liquidation cascade

- 2024-08milestone

ETH price plunge generates $436M in on-chain lending liquidations, reported as second-largest ever

- 2024-10milestone

Bitcoin surges above $64K, short liquidations exceed $100M in 24 hours as bearish bets unwind

- 2025-02milestone

BTC drops below $89K on yen strength and stock risk aversion, triggering $1.35B in 24-hour liquidations

- 2025-02exploit

Hyperliquid FRIEND-USD TVL-based oracle vulnerability disclosed, forcing index restructuring and margin refunds

- 2025-04milestone

Trump China tariff threat triggers $459M in crypto liquidations within one hour as ETH and SOL fall 5%

- 2025-05launch

Frax launches BAMM, introducing oracle-free AMM-native lending designed to eliminate hard liquidation events

Hyperliquid and the Flash Crash Problem

Hyperliquid, the decentralized perpetuals exchange, has emerged as a case study in liquidation dynamics at the infrastructure level. Its total cumulative liquidations have surged to new highs as the platform's open interest has grown. In one episode, SpaceX-linked contracts on Hyperliquid plunged 45% in a flash crash, triggering a cascade of liquidations on a thinly traded market — highlighting how low-liquidity perpetuals can produce extreme moves disconnected from underlying asset fundamentals.

The platform's architecture — where liquidations are processed on-chain rather than by a centralized engine — means that large liquidation events are fully transparent and can be tracked by sophisticated traders who monitor on-chain liquidation logs and funding rate shifts as real-time signals. Some traders specifically target these liquidation clusters, positioning to absorb forced selling or ride the momentum it creates.

Protocol-Level Liquidation Protection

The industry has responded to liquidation risk with increasingly sophisticated protective mechanisms. Several DeFi protocols have experimented with soft liquidation models that partially reduce collateral risk rather than closing positions entirely, reducing the cliff-edge nature of traditional liquidation thresholds.

BOB's Bitcoin vault liquidation engine demonstrates another approach: atomic, partial, and open liquidations that support BTC-backed stablecoin lending while cutting settlement time from days to under an hour. Rather than holding the entire BTC position hostage to a single liquidation event, the system can adjust incrementally as prices move — a model sometimes called atomic liquidations.

f(x) Protocol pointed to 87 rebalance transactions leading to zero liquidations during a recent crash as evidence that algorithmic rebalancing can substitute for forced selling in some conditions. InfiniFi has argued that duration-native RWA liquidators — parties willing to hold assets to maturity rather than dump them immediately — are necessary for levered looping strategies to scale without amplifying volatility.

In the past 24 hours , 307,787 traders were liquidated , the total liquidations comes in at $1.19 billion. The largest single liquidation order happened on HTX - BTC-USDT value $33.95M

just use F(x)

- MarketHigh

Long positions consistently absorb the overwhelming majority of liquidation losses — one documented 24-hour window showed $153M in long liquidations versus $18M short — confirming that structural leveraged-long bias amplifies drawdown severity non-linearly.

- LiquidityHigh

Documented cascade events of $459M within a single hour on a tariff announcement and $1.35B in 24 hours on yen strength confirm that macro shocks compress liquidity faster than on-chain liquidation engines can clear, creating self-reinforcing price gaps.

- CentralizationHigh

CEX platforms — Binance holds the largest single liquidation orders in every major event — provide opaque aggregate data that systematically undercounts total market liquidations, concealing true systemic exposure from on-chain analysts.

- Smart-contractMedium

Soft-liquidation designs like LLAMMA and f(x) have demonstrated measurable protection under live crashes, but RPC endpoint failures and TVL-based oracle manipulation remain exploitable edge cases that have already produced unintended liquidations in production.

- OracleHigh

The Hyperliquid FRIEND-USD incident demonstrated that TVL-based oracle designs create liquidation attack surfaces exploitable by manipulating the index metric, forcing emergency index restructuring and maintenance margin refunds after the fact.

- RegulatoryLow

No regulatory events appeared in the clicked headline set; liquidation risk in this reader base is framed as mechanical and market-driven rather than enforcement-driven, suggesting regulatory exposure is not a primary concern for this audience.

Government and Institutional Liquidations

Not all liquidations stem from leverage. Governments that seize cryptocurrency in enforcement actions must eventually liquidate those holdings — and the scale can be market-moving. France's selection of tradias, Asset Reality, and Tangany for a multi-year framework for the sale of seized cryptocurrencies represents an attempt to manage this process professionally, with the first liquidations under the framework already completed.

The U.S. government has historically moved seized Bitcoin in ways that rattled markets; more structured frameworks aim to minimize price impact through over-the-counter sales rather than exchange dumps.

Reading Liquidation Data

Liquidation data is published in near-real-time by most major exchanges and aggregated by services like CoinGlass. Key metrics to understand:

- Total liquidations (24h): The dollar value of positions forcibly closed. Readings above $500 million in a single day typically indicate significant volatility.

- Long/short ratio: Whether longs or shorts are being liquidated more heavily signals directional pressure.

- Liquidation heatmaps: Price levels where large clusters of liquidations would be triggered if price moved there — often used by traders to identify likely support/resistance zones.

- Open interest (OI): The total value of outstanding derivative contracts. Rising OI combined with one-directional funding rates signals a crowded trade that is vulnerable to a squeeze.

- Funding rates: Persistent positive funding means longs are paying shorts, indicating a market leaning heavily bullish and therefore exposed to downside liquidation pressure.

S&P 500 credit analysts have noted in public commentary that Bitcoin-backed lending ABS structures face specific risks from liquidation cascades — where a sharp BTC price decline could trigger simultaneous margin calls across multiple lenders, producing coordinated forced selling that overshoots fundamental value.

Outlook

Liquidation dynamics are not going away — they are structurally embedded in how leveraged crypto markets function. As institutional participation grows through products like Bitcoin ETFs and BTC-backed lending, the pools of leveraged exposure will expand, and so will the potential scale of individual cascade events. Binance's $400 million "Together Initiative" — announced specifically to support traders affected by recent liquidations — reflects industry acknowledgment that liquidation risk is now a reputational and ecosystem-level issue, not just a problem for individual traders.

On the DeFi side, the push toward softer liquidation mechanisms, better oracle design, and atomic partial liquidations suggests that the next generation of lending protocols will treat liquidation as a failure mode to be minimized rather than a necessary feature to be accepted. Whether those designs hold under extreme market stress — the conditions that most test them — remains to be seen.

For traders, the enduring lesson is straightforward: in crypto's fragmented, 24/7 markets, leverage that looks manageable during calm periods can be lethal during volatility spikes that compress days of normal price movement into hours.

Latest Liquidations news

InfiniFi makes case for duration-native RWA liquidator, arguing levered looping cannot scale without someone holding assets to maturityCrypto markets are increasingly bearish as Bitcoin sharply falls from recent all-time highs. Myriad predictors now assign higher odds to further declines, while hopes for a December Fed rate cut fade, adding macro uncertainty and fueling potential liquidations.In the past 24 hours , 307,787 traders were liquidated , the total liquidations comes in at $1.19 billion.

The largest single liquidation order happened on HTX - BTC-USDT value $33.95M BOB unveils Bitcoin vault liquidation engine to power BTC-backed stablecoin lending. The new system enables bitcoin holders to borrow stablecoins against their native BTC as collateral, keeping assets secured on Bitcoin. The mechanism supports open, partial, and atomic liquidations, cutting settlement time from days to under an hour.

BOB unveils Bitcoin vault liquidation engine to power BTC-backed stablecoin lending. The new system enables bitcoin holders to borrow stablecoins against their native BTC as collateral, keeping assets secured on Bitcoin. The mechanism supports open, partial, and atomic liquidations, cutting settlement time from days to under an hour. Bitcoin Volatility Triggers $657M in Liquidations as BTC Swings Between $107K-$113K While U.S. Government Shutdown Stalls Crypto Regulation and Top Gainers River (+85%) and ChainOpera AI (+69%) Lead Market Rally

Bitcoin Volatility Triggers $657M in Liquidations as BTC Swings Between $107K-$113K While U.S. Government Shutdown Stalls Crypto Regulation and Top Gainers River (+85%) and ChainOpera AI (+69%) Lead Market Rally Binance announces $400 million “Together Initiative”, an industry recovery and confidence rebuilding plan to support crypto traders and institutional users affected by recent liquidations.

Binance announces $400 million “Together Initiative”, an industry recovery and confidence rebuilding plan to support crypto traders and institutional users affected by recent liquidations.Community notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…