In crypto, liquidation is the forced closure of leveraged or collateralized positions when margin or health factors fail. This explainer unpacks CeFi and DeFi mechanics, cascades, soft-liquidation designs, whale dramas, and risk tools shaping BTC, ETH and lending markets.

+11 sources across the wider coverage universe

Inspired by Curve's LLAMMA and f(x)'s Liquidation Brake, protocol architect outlines a fixed-rate lending model where collateral self-hedges before liquidation thresholds are breached2026-06

Inspired by Curve's LLAMMA and f(x)'s Liquidation Brake, protocol architect outlines a fixed-rate lending model where collateral self-hedges before liquidation thresholds are breached2026-06 Aave Chan Initiative Accuses Aave Labs of Diverting DAO Revenues and Privatizing Protocol Economics, Demands Clarity on CowSwap Integration, Vault Fees, Horizon Deals, and V4 Liquidation Engine Incentives.2025-12

Aave Chan Initiative Accuses Aave Labs of Diverting DAO Revenues and Privatizing Protocol Economics, Demands Clarity on CowSwap Integration, Vault Fees, Horizon Deals, and V4 Liquidation Engine Incentives.2025-12 The beautiful math behind Curve AMMs series part 3, this time diving into LLAMMA, Curve’s lending–liquidation AMM.2025-12

The beautiful math behind Curve AMMs series part 3, this time diving into LLAMMA, Curve’s lending–liquidation AMM.2025-12 Liquidation protection is pushing DeFi beyond cliff-edge liquidations, introducing automated slopes that adjust risk continuously onchain today.2026-02

Liquidation protection is pushing DeFi beyond cliff-edge liquidations, introducing automated slopes that adjust risk continuously onchain today.2026-02 A massive ETH position on Maker faces imminent liquidation risk—here’s how to track it and understand the process, courtesy of a former Maker employee.2025-03

A massive ETH position on Maker faces imminent liquidation risk—here’s how to track it and understand the process, courtesy of a former Maker employee.2025-03 FTX and FTX Digital Markets to merge assets and streamline customer claim handling, giving customers the option to seek repayment from either U.S. bankruptcy or Bahamian liquidation processes.2023-12

FTX and FTX Digital Markets to merge assets and streamline customer claim handling, giving customers the option to seek repayment from either U.S. bankruptcy or Bahamian liquidation processes.2023-12

Liquidation in Crypto: How Forced Position Closures Shape the Market

In crypto, liquidation is the forced closing of a leveraged or collateralized position when its value is no longer sufficient to meet margin or collateral requirements, typically resulting in automatic sale of assets to repay debt. Put simply, being liquidated means the exchange or protocol takes over your position and sells it to protect lenders and the platform from loss, often wiping out most or all of your margin or collateral.

Crypto liquidations sit at the intersection of leverage, volatility, and automated risk management, and they are one of the key mechanisms that keep both centralized exchanges and decentralized lending markets solvent. On derivatives platforms, liquidations are driven by margin ratios and leverage, while in DeFi lending they are triggered when a borrower’s health factor falls below a threshold as collateral prices fall. Recent cycles have shown how aggressive BTC and ETH leverage, whale-sized positions, and intricate liquidation engines can turn routine price swings into full-blown cascades, while new designs like Curve’s LLAMMA, f(x) Protocol’s “liquidation brake,” and options-based collateral aim to soften or even eliminate hard liquidations. Understanding how liquidation works—mechanically, economically, and behaviorally—has become essential for anyone trading crypto derivatives, borrowing against their assets, or trying to parse the flood of on‑chain alerts about whales “about to be liquidated.”

What Liquidation Means in Crypto Markets

In traditional finance, liquidation often refers to converting assets to cash, for example when an investment fund winds down or a company sells assets in bankruptcy. In crypto trading and DeFi, the term is narrower and more mechanical: liquidation is the forced closing of a position by an exchange or protocol because the account no longer meets the agreed margin or collateral conditions. On a centralized derivatives platform, this typically means the trader’s equity no longer covers the maintenance margin, so the exchange automatically closes the position to prevent the account from going deeply negative. In DeFi lending, liquidation occurs when the value of the collateral relative to outstanding debt falls below a protocol-specific threshold, at which point the protocol allows liquidators to repay debt and seize collateral at a discount.

It is crucial to distinguish between voluntary and involuntary liquidation. A trader can voluntarily close a long or short position at any time by submitting an order; that is not liquidation in the technical sense. Forced liquidations, by contrast, are triggered by risk-engine logic embedded in exchange code or smart contracts, often in response to sharp price moves and updated price oracles. In practice, many “liquidated” traders never press the sell button themselves; once their margin ratio or health factor crosses a line, the system sells for them, frequently at unfavorable prices during illiquid or highly volatile conditions.

Liquidations are tightly linked to leverage, which allows traders or borrowers to control more exposure than the capital they post upfront. In leveraged trading, an investor borrows funds to increase position size, amplifying both gains and losses. Borrowed funds in perpetual futures or margin trading come from the exchange or other users, while in DeFi lending they come from liquidity providers who deposit assets into lending pools. Liquidation is the safety valve that protects those lenders and the platform: when an account’s margin or health factor falls too low, the system cuts the position rather than allow lenders to eat the loss. That is why exchanges and protocols frame liquidation not as a punishment, but as a risk-control mechanism that allows high leverage and permissionless lending to exist at all.

The concept also extends beyond trading accounts into portfolio management and even regulation. When a prominent investor announces they have “liquidated” a large ETH stash to rotate into other coins and cash, as David Hoffman did in a widely discussed portfolio shift, the word refers to selling down a position voluntarily rather than margin failure. At the same time, policymakers have begun drawing boundaries around when custodians can forcibly liquidate dormant or inaccessible crypto, framing a legal distinction between contractual risk-engine liquidations and consumer-protection rules for account closures. Although these different uses share the same word, they operate under different incentives and legal frameworks, and only the first category is driven by automated margin logic.

Inspired by Curve's LLAMMA and f(x)'s Liquidation Brake, protocol architect outlines a fixed-rate lending model where collateral self-hedges before liquidation thresholds are breached

$10.2B of borrowed Aave debt still clears through cliff risk, while Pendle's $1.24B TVL shows DeFi users will buy fixed-maturity risk when the primitive is legible. A CPPI loan turns collateral management into an explicit short-vol spread: borrowers pay via whipsaw bleed and lower upside, lenders need that spread funding a gap-risk reserve, not just cleaner UX. Curve's 10/10 postmortem is the check on the design: LLAMMA saved about 22% of at-risk positions, but the CRV-long LlamaLend market still carried roughly $700k of bad debt at ~70% backing after the gap.

Readers click liquidation content in two distinct anxious modes — voyeuristically tracking specific named whale positions before they cascade, and urgently seeking protocol designs (LLAMMA, non-liquidatable leverage) that make personal liquidation structurally impossible, revealing that the real demand is risk avoidance intelligence, not mechanics education.↗

How Exchange Liquidations Work: Margin, Futures, and Perpetuals

Leverage, Margin, and Liquidation Price

On centralized exchanges and many perpetual DEXs, liquidation hinges on the relationship between account equity, borrowed funds, and the required maintenance margin. When a trader uses leverage—for example a 20x long on BTC or ETH—they post a fraction of the position value as initial margin and borrow the rest from the platform or other users. If the market moves in their favor, their margin is amplified into outsized profits; if it moves against them, losses eat into that same margin, bringing their equity closer to zero. Liquidation occurs when the remaining equity falls below the maintenance margin requirement, typically expressed as a margin ratio reaching 100 percent or an account value turning negative on a marked-to-market basis.

A practical way traders understand this is through the liquidation price, the approximate price at which their position will be forcibly closed if they do nothing. Educational resources from major exchanges show that this price depends on the leverage used, the entry price, the maintenance margin rate, and sometimes fees and funding. Very high leverage compresses the distance between entry and liquidation dramatically: a 50x or 100x position may be liquidated on a move of less than 2 percent against the trader, making it highly sensitive to short-term volatility and “wicks.” This is why on‑chain alert accounts commonly flag whales opening 20x or 50x BTC or ETH longs with liquidation prices only a few percentage points away; even a routine pullback can flatten such positions in minutes.

From a risk perspective, the leverage factor inversely shapes the tolerance for adverse price moves before liquidation. Simplified educational examples often explain that, roughly speaking, the higher the leverage, the smaller the permissible percentage drop before the position hits its liquidation trigger. For instance, at 10x leverage, a move of around 10 percent against the position may be enough to wipe the margin, while at 100x leverage a move of around 1 percent can do the same, ignoring fees and buffers. In reality, each exchange uses its own maintenance margin tiers and formulas, but the principle is the same: leverage magnifies both your upside and the speed with which liquidation can occur.

Liquidation Engines, Insurance Funds, and Auto‑Deleveraging

Behind the scenes, exchanges rely on liquidation engines that continuously monitor account equity and market prices. When an account’s margin ratio approaches the danger zone, the system can begin reducing position size or transferring it to an internal risk engine before it becomes unmanageable. If the market moves fast and liquidity is thin, the liquidation engine may struggle to exit at favorable prices; the resulting slippage can push realized losses beyond the trader’s posted margin, leaving a deficit. To absorb such deficits, exchanges maintain insurance funds, funded over time from trading fees, liquidation fees, or spreads between entry and exit prices of liquidated positions.

When even the insurance fund is not sufficient—typically during extreme volatility or large gap moves—some derivatives exchanges resort to auto‑deleveraging (ADL). ADL is an automated process that forcibly closes profitable positions held by other traders to offset the losses of liquidated accounts when the platform cannot fully absorb them, even after using insurance buffers. The mechanism ranks traders, usually by leverage and profitability, and then partially closes positions starting from those most highly leveraged and in the most profit, thereby reducing the exchange’s net exposure. While ADL protects the platform’s solvency, it is controversial because it imposes involuntary exits on traders who did nothing wrong, undermining trust if not clearly disclosed.

Perpetual DEXs have adopted similar patterns with on‑chain risk engines and insurance pools, though their implementation details differ. Protocols like Hyperliquid, for example, emphasize that their auto‑deleveraging and liquidation logic is designed to strictly ensure platform solvency, closing positions when account value becomes negative and using ranking systems to determine which opposing positions to offset first. The shared theme across CeFi and DeFi derivatives is that liquidation engines aim to keep the system whole, even at the cost of individual traders’ positions.

Liquidation Cascades and Market Volatility

Exchange liquidations do more than clean up individual accounts; they can reshape short‑term price action. Crypto markets are highly leveraged, and open interest in BTC and ETH perpetuals can build up at levels where a moderately large move triggers waves of forced selling or buying. When a price drop pushes many long positions below their maintenance margin, the liquidation engine begins closing those positions, selling into an already falling market and adding further downward pressure. That renewed pressure liquidates yet more longs whose liquidation prices were slightly lower, creating a feedback loop often described as a liquidation cascade.

Research and industry analyses highlight that large‑scale crypto liquidations are typically triggered by rapid price fluctuations combined with high leverage levels, especially when a significant share of open interest is on the same side of the market. Crypto liquidation dashboards from data providers like CoinMarketCap and CoinGlass show that in such episodes, billions of dollars in long or short positions can be liquidated across major exchanges within a single day or even a single hour. These liquidations do not merely reflect market moves; they become a key driver, transforming what might have been a manageable correction into an overshoot as forced orders slam into illiquid order books.

Liquidation cascades do not only happen on the downside. When the market squeezes higher against over‑leveraged short sellers, those shorts can be liquidated, forcing them to buy back the asset at increasingly higher prices, often fueling sharp short squeezes. Examples include whales heavily shorting synthetic exposure to equity indices or commodities, with liquidation prices well above the spot market; if prices spike unexpectedly, the covering and forced buybacks can create outsized moves that feed into futures and spot markets alike. In both directions, liquidations are not just outcomes but active participants in crypto price discovery.

DeFi Liquidations: Lending Protocols, Health Factors, and Liquidators

Overcollateralized Lending and Health Factors

In decentralized finance, liquidation is central to the design of overcollateralized lending protocols such as Aave, Compound, and newer systems like Curve’s crvUSD and LlamaLend. These protocols allow users to deposit BTC, ETH, or other assets as collateral and borrow stablecoins or other tokens against them, typically at a conservative loan‑to‑value (LTV) ratio. Because there is no credit scoring or KYC‑based assessment, risk management is handled entirely through collateralization: borrowers must always maintain collateral worth significantly more than their debt. When collateral prices fall, this overcollateralization ratio shrinks, and once it crosses a critical line, the protocol enables liquidation to protect depositors’ funds.

A key concept here is the health factor (HF), a risk metric that combines collateral value, liquidation thresholds, and debt into a single number indicating how close a position is to liquidation. In Aave v3, for example, the health factor is defined so that positions become eligible for liquidation when HF drops below 1; risk is tracked with per‑asset liquidation thresholds, and once the HF falls under that threshold, collateral can be partially liquidated. The HF is essentially the inverse of LTV adjusted for liquidation parameters, with values near 1 indicating proximity to liquidation and higher values indicating safer positions. Research formalizes this by treating HF as a ratio of collateral value to debt scaled by the liquidation threshold, and shows that a drop below a given threshold is the main trigger for liquidation events in DeFi lending protocols.

Different protocols choose different liquidation thresholds, collateral factors, and bonuses to balance borrower flexibility against protocol safety. Safer collateral such as staked ETH derivatives or highly liquid blue‑chip assets may be assigned higher borrowing power, while more volatile or thinly traded tokens are allowed lower LTVs to reduce the risk of bad debt. For instance, MixBytes’ analysis of Curve’s LlamaLend emphasizes how the protocol continuously swaps between collateral and debt assets to keep positions “healthy,” while designing liquidation bands that minimize protocol loss even under stress. Across designs, however, the fundamental trigger is the same: when the HF crosses a line, the system transitions from passive lending to active liquidation.

Liquidation Engines and Incentivized Liquidators

Because DeFi protocols are non‑custodial and permissionless, they cannot rely on a centralized risk desk to manage undercollateralized positions. Instead, they implement liquidation engines that combine on‑chain monitoring, oracle price feeds, defined risk parameters, and incentives for third‑party liquidators to step in and repair unhealthy positions. As FinanceFeeds explains, a DeFi liquidation engine consists of several interconnected systems that identify undercollateralized accounts based on health factor thresholds and then open those accounts to liquidation by external actors. Once the health factor drops below the minimum acceptable level, the protocol allows liquidators to repay part of the borrower’s debt in exchange for a portion of collateral plus an additional liquidation bonus.

In Aave’s design, for example, when a position’s health factor falls below 1, a liquidator can repay up to a certain percentage of the debt and receive collateral at a discount, known as the liquidation bonus. Compound v2 similarly defines a liquidation incentive, which is the extra collateral awarded to liquidators above the amount equivalent to the repaid debt, creating a profit opportunity that motivates liquidators to act quickly when positions go underwater. FinanceFeeds notes that these liquidators are often sophisticated bots operated by third parties, whose speed during volatile periods largely determines whether the protocol avoids accumulating bad debt. Because liquidation profits can be substantial when markets move fast, there is intense competition among bots, leading to gas fee bidding wars on chains like Ethereum and a significant interplay with MEV (maximal extractable value).

Academic work on DeFi liquidation dynamics underscores the role of transaction fees and network congestion in determining liquidation outcomes. When fees spike during periods of volatility, some would‑be profitable liquidations become unprofitable after accounting for gas, leading to delayed or partially executed liquidations and raising the risk of bad debt. This is particularly critical for volatile collateral such as ETH, where the value of collateral relative to debt can deteriorate rapidly between the time an HF drops below threshold and the time a transaction confirms. Protocol designers therefore must calibrate liquidation bonuses high enough to cover not only market risk but also the cost of gas and the uncertainty of transaction ordering.

Liquidation Cascades and Systemic Risk in DeFi

Liquidation in DeFi lending can also generate cascades, though the mechanism differs from exchange futures. Chainlink describes a liquidation cascade in crypto lending markets as a chain reaction of forced automated asset sell‑offs, triggered when falling asset prices push many borrower positions below liquidation thresholds. When many borrowers have used the same collateral asset, such as ETH, and prices drop sharply, liquidations force the sale of that collateral into spot markets, putting further downward pressure on the price. That further decline then pushes more positions below their thresholds, leading to additional liquidations and potentially amplifying the original move, particularly if liquidity is thin.

This kind of feedback loop is most dangerous when protocols share collateral types and when leverage is stacked across derivatives and lending. For example, a whale might borrow large amounts of stablecoins against ETH on one protocol and then use those stablecoins as margin for leveraged ETH futures elsewhere, creating multiple layers of liquidation risk anchored to the same underlying ETH price. When ETH falls, both the lending protocol and the futures exchange could attempt to liquidate simultaneously, concentrating sell pressure and increasing slippage. As Chainlink’s analysis emphasizes, high leverage, crowded collateral, and rigid liquidation thresholds can turn a single market shock into a systemic event across DeFi lending markets.

Protocol bugs and oracle failures add another layer of risk. While most lending platforms rely on robust price feeds and heavily audited code, incidents do occur in which a glitch in liquidation logic or a manipulated oracle briefly misprices collateral, triggering unintended liquidations. In such cases, communities often debate whether and how to compensate affected users, recognizing that the social legitimacy of automated liquidation depends on correct and predictable operation. These episodes highlight that, even in trust-minimized systems, liquidation is not purely mechanical but embedded in broader governance and risk‑sharing arrangements.

Aave Chan Initiative Accuses Aave Labs of Diverting DAO Revenues and Privatizing Protocol Economics, Demands Clarity on CowSwap Integration, Vault Fees, Horizon Deals, and V4 Liquidation Engine Incentives.

🍿

- 01LLAMMA soft liquidation adoption↗

Curve's gradual-rebalancing mechanism drew readers as both a protective innovation and a contested design that Aave was accused of appropriating for GHO v4, making it a proxy war over who owns the most consequential lending idea in DeFi.

- 02Whale position liquidation tracking↗

Readers engaged intensely with named, live at-risk positions — a Maker ETH whale, Michael Egorov's CRV debt, two whales holding 125k ETH — because specific threshold numbers ($1,805, $85,300) let them monitor a ticking clock in real time.

- 03Non-liquidatable leverage alternatives

Multiple high-click sponsored and editorial headlines for f(x) Protocol and yBOLD showed genuine reader demand for structural escape hatches from liquidation risk, not just hedging tactics.

- 04Protocol failure liquidations↗

Unexpected liquidations caused by governance parameter changes (ezETH/Pac Finance, zero warning LTV shift) and oracle malfunctions (Morpho/Pyth cbETH data) drew clicks because they reframed liquidation as an institutional failure, not a market outcome.

- 05CEX cascade liquidation scale↗

Headlines quantifying $500M–$19B single-day liquidation events — with Binance compensating users while DeFi ran uninterrupted — attracted readers comparing centralized and decentralized risk infrastructure under stress.

- 06FTX bankruptcy liquidation process

The FTX/FTX Digital Markets asset-merge headline pulled readers because it exposed how exchange insolvency liquidation differs structurally from DeFi collateral liquidation, with creditors choosing between two legal jurisdictions.

Innovations in Liquidation Design: Soft Liquidations, 0‑Liquidation Perps, and Options

Curve’s LLAMMA and Soft Liquidation

As DeFi has matured, designers have begun rethinking the binary nature of traditional liquidation, where a position instantly flips from “safe” to “liquidated” once a threshold is crossed. Curve’s stablecoin architecture, anchored by the LLAMMA (Lending‑Liquidating AMM Algorithm), is one of the most influential attempts to implement soft liquidation. LLAMMA is a specialized automated market maker that manages collateral (such as ETH) and crvUSD across a system of price “bands” or ticks, distributing a user’s collateral across multiple bands when a loan is opened. Instead of immediately closing a loan when the collateral price enters a liquidation range, LLAMMA gradually swaps collateral into crvUSD as the price falls and then back into collateral as it recovers.

Curve’s documentation explains that LLAMMA allows positions to be liquidated and de‑liquidated continuously within the liquidation range, without fully closing the loan. Only when the loan’s health metric falls below 0 percent does a hard liquidation occur, forcefully closing the loan at a specific price to cover shortfalls. The health function in Curve’s model incorporates discounted collateral inside the liquidation range and collateral above the bands, with a formula of the form \[ \text{health} = \frac{s \times (1 - \text{liqDiscount}) + p}{\text{debt}} - 1 \] where \(s\) represents collateral within liquidation bands and \(p\) represents collateral above the bands. By structuring collateral across bands and using this health function, LLAMMA reduces the cliff‑edge behavior of traditional liquidation engines.

Technical analyses of Curve’s stablecoin system highlight how LLAMMA can be viewed as a custom AMM designed to self‑rebalance collateral positions as prices move. Users specify the number of bands for their collateral, and the controller contract chooses a range that minimizes user risk while ensuring the protocol does not face bad debt under plausible price paths. As the price approaches the lower bands, more of the user’s collateral is converted to crvUSD, effectively hedging downside risk; as the price recovers, the AMM moves back into collateral. MixBytes’ overview of modern DeFi lending notes that in designs like LlamaLend, this continuous swapping of collateral to debt assets and back shifts positions towards healthier status in real time, reducing the need for sudden liquidations.

f(x) Protocol’s Liquidation Brake and Near‑0 Liquidation Perps

Another line of innovation appears in f(x) Protocol, which combines a CDP-like design with on‑chain perpetual exposure and a novel liquidation mechanism designed to protect users against hard liquidations. In a widely discussed presentation, the protocol’s architects describe a gradual liquidation mechanism that kicks in when the position’s LTV crosses a certain threshold, pushing it back to a safer level before it can reach a hard‑liquidation boundary. Specifically, for many positions, when LTV crosses roughly 88 percent, the protocol intervenes to move it back to that level, regardless of the absolute dollar size, so that the position never reaches around 95 percent LTV where a full hard liquidation would occur.

The protocol introduces a decentralized stablecoin, fxUSD, whose peg is helped by a stability pool called fxSAVE, which pools fxUSD and USDC and earns yield from underlying collateral, such as yield‑bearing staked ETH. The stability pool is used as the primary peg‑keeping mechanism, absorbing liquidations and earning fees from them, including almost 10 percent APY for liquidity providers in some periods, according to the project’s own description. If fxUSD trades below its peg, the protocol can introduce a temporary funding cost on leverage positions, effectively charging them a borrowing cost linked to USDC rates and directing that to the stability pool to attract more USDC and support the peg. If the peg stress intensifies, a second layer of higher funding can be applied, multiples of the base USDC borrowing cost, again paid by leverage users and used to bolster peg‑defense liquidity.

From a liquidation standpoint, this design creates a “liquidation brake”: instead of letting positions accelerate blindly toward hard liquidation as prices move, the system continuously trims leverage at pre‑set LTV thresholds. This approach shares conceptual DNA with LLAMMA’s soft liquidation but is implemented through stepwise adjustments of position leverage and dynamic funding rather than AMM‑based band mechanics. Both approaches attempt to reconcile the desire for high on‑chain leverage in assets like BTC and ETH with the user‑experience and systemic risk problems created by abrupt, all‑or‑nothing liquidations.

Vitalik’s Options‑Based DeFi and Self‑Hedging Collateral

A more radical direction for liquidation design has been articulated by Ethereum co‑founder Vitalik Buterin, who has proposed using options‑based structures to replace liquidation‑driven debt entirely in some DeFi applications. In a recent essay and subsequent coverage, Buterin suggested splitting 1 ETH into two paired option‑like assets that always sum back to 1 ETH, with one taking on leveraged upside exposure and the other absorbing downside. The key idea is that instead of a borrower posting ETH as collateral and taking on liquidation risk when ETH falls, the protocol would create synthetic claims whose payoff profiles ensure that overall exposure remains solvent without needing forced liquidation triggers.

Coverage of this proposal in DeFi media emphasizes that options‑based designs could allow users to obtain leverage or yield without the hard cliff of liquidation; positions would simply move along pre‑defined payoff curves. For instance, an options‑style product could replicate a 2x leveraged long ETH position but cap losses at a certain level, with counterparties or automated market makers taking the opposing risk. Because the exposure is embedded in the payoff structure and fully collateralized upfront, there would be no need to constantly monitor health factors or trigger liquidations when thresholds are breached. This concept aligns with broader experimentation in fixed‑rate lending, self‑hedging collateral, and interest‑rate derivatives that aim to route around the fragility of classic margin‑based liquidation.

Protocol architects have also proposed fixed‑rate lending models where collateral is automatically hedged as prices move, inspired by designs like Curve’s LLAMMA and f(x)’s liquidation brake. In these models, the system can slowly sell a portion of the collateral into hedging instruments or stable assets as the price falls, locking in value and maintaining solvency before traditional liquidation thresholds are breached. While many of these ideas remain theoretical or early in deployment, they reflect a growing consensus that crypto’s reliance on rigid liquidation triggers is both a strength and a vulnerability—and that a new generation of DeFi primitives will need more nuanced, stateful liquidation logic.

Human Stories Behind Liquidations: Whales, Degens, and Strategic Exits

Liquidation in crypto is not just a technical process; it is a narrative driver that shapes how market participants perceive risk, heroism, and folly. On‑chain analytics accounts and derivatives data dashboards have made the fortunes and misfortunes of whales and degen traders a kind of public theater, where every new 20x BTC short or 50x ETH long is accompanied by a prominently displayed liquidation price. When a whale takes out a $58 million 20x long on ETH with a liquidation price only a few hundred dollars below spot, observers immediately calculate how small a move is needed to wipe out the position and speculate whether a cascade might follow. Similar dynamics play out when large players short synthetic indices or commodities with extremely tight liquidation bands.

These stories often end in dramatic liquidations during volatile sessions, with traders losing millions in minutes as positions are force‑closed. Media coverage has highlighted cases where aggressive perps trading on platforms like Hyperliquid or Binance led to repeated large losses for certain addresses, including colorful figures whose accounts show a long history of being liquidated in meme coins or mid‑cap tokens. The spectacle of a “Fartcoin trader” losing millions as ADL mechanisms unwind leveraged bets, or a once‑dominant whale seeing their account fall from tens of millions to near zero after a series of liquidations, fuels a culture that both glamorizes and warns about the dangers of extreme leverage.

Not all high‑profile liquidations are involuntary. The phrase “strategic liquidation” has gained currency to describe deliberate portfolio de‑riskings, such as when Bankless co‑founder David Hoffman announced that he had completely liquidated his personal ETH holdings to rotate into a diversified mix of alternative cryptoassets, privacy coins, and stablecoin reserves. In that case, the liquidation was voluntary and pre‑planned, yet it still shook parts of the Ethereum community because of the symbolic weight of a prominent ETH advocate exiting his flagship position. The episode illustrates how the term “liquidation” bridges automated risk‑engine events and human decisions about repositioning or exiting markets.

Liquidation events have also become central to the reputations of certain traders and funds. A DeFi credit protocol or structured‑product issuer may frame its “most difficult day” around a particularly severe leverage liquidation event, in which cascading margin calls and forced sales temporarily stressed the system and tested its resilience. Similarly, well‑known traders and funds are tracked not only by their profits but by their largest liquidation losses, which can undermine investor confidence if they are perceived to have taken reckless leverage. In this sense, liquidation acts as a public scorecard for risk management: surviving brutal volatility without being liquidated becomes a badge of honor, while repeated liquidations signal structural problems in strategy design.

The beautiful math behind Curve AMMs series part 3, this time diving into LLAMMA, Curve’s lending–liquidation AMM.

TL;DR: Curve’s LLAMMA is a new AMM-based liquidation engine for crvUSD that replaces harsh, one-time liquidations with continuous soft liquidation. Collateral is split into price “bands,” and as the oracle price moves, LLAMMA automatically and gradually sells collateral when price drops and buys it back when it rises. It uses virtual balances (f, g) and a hyper-reactive price curve so the AMM price always moves faster than the oracle, creating arbitrage incentives that keep each loan safely rebalanced. The result: smoother liquidations, fewer liquidation cascades, and a mathematically driven lending system where collateral is constantly adjusted instead of wiped out all at once.

- 2022-11regulatory

FTX collapse triggers exchange liquidation proceedings across U.S. and Bahamas simultaneously

Curve launches crvUSD with LLAMMA soft-liquidation mechanism, replacing hard collateral seizure with continuous rebalancing bands

- 2023-06milestone

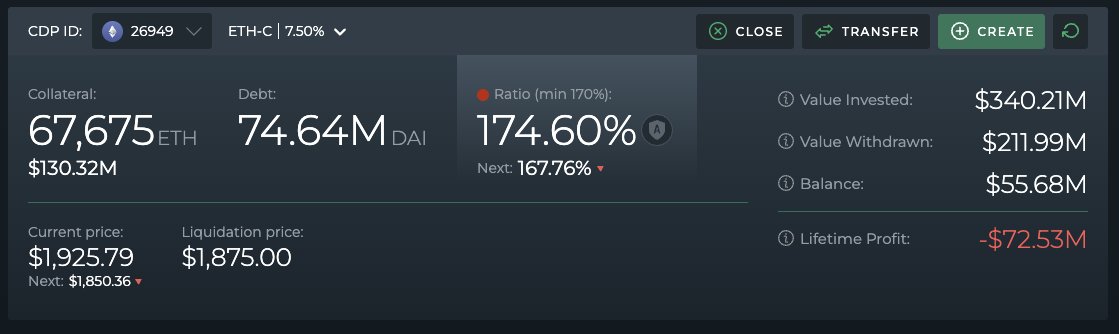

Michael Egorov's $168M CRV-collateralized borrow position faces systemic liquidation risk across multiple DeFi protocols

Pac Finance silently adjusts ezETH LTV, triggering $24M in immediate liquidations with no user warning

- 2024-04exploit

Morpho borrower suffers outsized liquidation loss after Pyth oracle delivers inaccurate cbETH price data

Curve warns Aave against incorporating LLAMMA-style soft liquidation into the GHO mechanism for Aave v4

Hyperliquid trader deliberately forces own JELLY position liquidation, offloading losses to the HLP community vault

Trump tariff announcement sparks estimated $19B single-day liquidation event; Binance compensates users for system failures while Aave and Uniswap operate without incident

Managing Liquidation Risk: Traders, Borrowers, and Protocols

How Traders Can Reduce Liquidation Risk

For individual traders using derivatives, the most effective way to reduce liquidation risk is to be conservative with leverage and proactive with risk controls. Exchange educational materials consistently emphasize that high leverage dramatically narrows the price band between entry and liquidation, making positions vulnerable to routine volatility and short‑term noise. Keeping leverage low—especially on volatile assets—or using cross‑margin only when supported by ample collateral can create a buffer that absorbs normal market swings without triggering forced closes. This is particularly important in assets like BTC and ETH, which can move several percent in minutes on macro news or large liquidations elsewhere.

Another central tool is the stop‑loss order, which allows traders to define an exit price before their margin runs out. Binance’s futures education, for example, describes stop‑losses as the “most obvious” way to avoid liquidation, since they can close the position at a predetermined loss level rather than waiting for the liquidation engine to kick in, which often happens at worse prices during panic moves. Using stop‑losses in combination with take‑profit orders lets traders bound their risk and avoid the psychological trap of hoping a losing position will bounce back. That said, in extremely fast markets stop‑losses can experience slippage, so traders still benefit from healthy margin buffers.

Monitoring margin ratios and adding collateral when necessary is another key practice. Exchanges typically display a margin ratio or liquidation threshold indicator, and once that hits 100 percent, the position becomes eligible for liquidation. By tracking this metric, traders can deposit more collateral or reduce position size before the trigger is reached, effectively extending the distance to liquidation. Binance notes that this strategy resembles “keeping a position alive when the trade is heading further in the wrong direction,” which can be dangerous if abused, but it remains a critical last‑resort tool for avoiding unwanted liquidations when a temporary drawdown is expected to mean‑revert.

Finally, traders should pay attention to aggregate leverage and open interest in the markets they trade. Analytics from services like CoinMarketCap and Bookmap point out that historically high open interest can indicate an over‑leveraged market where a relatively small price move may trigger mass liquidations. When funding rates are extreme and perpetuals are crowded on one side, any sudden reversal can cascade through leveraged accounts, closing positions not only on the losing side but also pulling in cross‑collateralized positions. Recognizing when markets are “primed” for liquidation events can help traders dial down leverage, hedge exposure, or sit out until conditions normalize.

How DeFi Users Can Manage Liquidation Risk

For DeFi borrowers, managing liquidation risk revolves around conservative collateralization, collateral selection, and monitoring health factors. Aave and similar protocols provide dashboards showing each user’s health factor, with values closer to 1 indicating higher liquidation risk. Borrowers who keep their HF comfortably above 1—say 1.5 or 2 or higher—are less likely to be liquidated on typical price swings, though extreme crashes can still wipe out even well‑buffered positions. The simplest way to reduce liquidation risk is therefore to borrow less against a given collateral base, accepting lower capital efficiency in exchange for greater safety.

Choosing less volatile collateral and avoiding highly correlated leverage also matters. Borrowing stablecoins against ETH, and then using those stablecoins to lever long more ETH, for example, stacks risk such that a single ETH drawdown can simultaneously push the lending position toward liquidation and erode the value of the newly purchased ETH. More resilient strategies might involve borrowing stables against relatively stable liquid staking tokens and deploying them into diversified yield strategies, while keeping health factors high and positions small relative to total portfolio value. Protocols like Curve’s crvUSD and LlamaLend attempt to assist users by distributing collateral across LLAMMA bands that minimize risk under typical price paths, but users still bear the responsibility of monitoring their health metrics.

Advanced users can also explore automation tools that help manage liquidation risk. On some platforms, bots or auxiliary contracts allow users to pre‑authorize deleveraging actions, such as selling a portion of collateral into debt repayment when HF falls below a certain threshold, similar to an automated stop‑loss for lending positions. Other tools send alerts when health factors approach danger levels or when oracle prices indicate that a liquidation band is near. However, these tools themselves are subject to smart‑contract risk and network congestion, so they complement rather than replace conservative borrowing practices.

From a protocol perspective, managing liquidation risk involves calibrating liquidation thresholds, bonuses, and oracle designs. Research shows that setting liquidation thresholds too tight may increase user‑facing liquidation events, while setting them too loose raises the risk of protocol‑level bad debt. Designers must also consider transaction fees and network latency: when gas spikes during volatile periods, liquidation margins must be wide enough and bonuses high enough to incentivize liquidators in all conditions. Innovations such as LLAMMA’s soft liquidation and f(x) Protocol’s gradual LTV resets illustrate how protocol‑level design can reduce the suddenness of liquidations, but they also introduce new parameters and failure modes that must be carefully stress‑tested.

Liquidation Data, Dashboards, and Market Microstructure

Liquidations have become highly visible in crypto, thanks to real‑time dashboards and analytics. CoinMarketCap’s Liquidations Dashboard, for instance, aggregates data on long and short liquidations over multiple time frames, showing how much notional value has been forcibly closed in the last 24 hours and which assets or exchanges are driving the totals. Similar services like CoinGlass provide live feeds of liquidation events across major futures platforms, including the size and direction of each liquidation, allowing observers to see in near real time when clusters of positions are being force‑closed. These tools help traders and analysts gauge whether a move is being amplified by liquidation flows and where pockets of residual leverage remain.

Understanding how liquidations interact with market microstructure is critical. When liquidation engines sell into thin order books, they can cause abrupt, spiky moves often called “liquidation wicks,” where price briefly overshoots before reverting once forced selling abates. These wicks can trigger additional stop‑losses and liquidations, creating short‑lived but violent swings. Conversely, when prices approach known liquidation clusters, opposing traders may attempt to “hunt” those levels, pushing price just far enough to trigger forced selling and then fading the move. This behavior contributes to the intuitive sense among many traders that markets “know where your liquidation is,” even though in reality it is simply a function of visible leverage and reflexive flows.

To conceptualize the differences between liquidation regimes across CeFi and DeFi, it can be helpful to summarize key features in a simple comparative table:

| Dimension | Exchange Margin/Futures Liquidation | DeFi Lending Liquidation |

|---|---|---|

| Trigger metric | Margin ratio, account equity vs maintenance margin | Health factor/LTV vs liquidation threshold |

| Executor | Exchange risk engine, internal liquidation bots | External liquidators incentivized by bonuses |

| Outcome | Position partially or fully closed; potential ADL of others | Portion of debt repaid, collateral seized at discount; loan may remain open |

| Main protection goal | Prevent negative equity and platform loss | Protect depositor funds and protocol solvency |

| Visibility to user | Liquidation price per position; margin ratio meter | Health factor and collateralization ratio dashboards |

Such distinctions matter because they shape how liquidation risk propagates through the broader crypto ecosystem. Exchange liquidations primarily affect derivatives markets but can spill into spot through arbitrage and hedging. DeFi liquidations directly affect on‑chain liquidity for collateral assets, especially when collateral is sold into AMMs or order books as part of liquidation auctions. In both domains, the rise of liquidations dashboards and on‑chain monitoring has turned these once opaque risk‑management processes into public signals that influence sentiment and positioning.

The Morpho/Pyth cbETH incident showed that a single inaccurate price feed can trigger wrongful liquidations on otherwise healthy positions, with no on-chain recourse for borrowers.

Pac Finance altered LTV thresholds without user notification, immediately liquidating $24M in ezETH — demonstrating that admin key holders can unilaterally move liquidation triggers on supposedly decentralized protocols.

Single-day liquidation events have exceeded $1B multiple times, with the April 2025 Trump tariff shock generating an estimated $19B event that broke Binance's matching engine, illustrating how concentrated leverage amplifies market dislocations into systemic cascades.

A single 40x leveraged $332M Bitcoin short with a published liquidation price at $85,300 creates an adversarial coordination target, where market participants can push price toward the threshold to collect liquidation fees.

Hyperliquid's JELLY incident — where a trader force-triggered their own liquidation to dump losses onto the HLP vault — exposed a structural flaw in perp DEX liquidation engines that assume liquidations are involuntary.

- Regulatory / legal riskMedium

The FTX dual-jurisdiction liquidation (U.S. Chapter 11 vs. Bahamian winding-up) showed that creditor recoveries can diverge significantly based on which legal liquidation process applies, a risk specific to offshore-domiciled CeFi entities.

Legal, Regulatory, and Ethical Dimensions of Liquidation

Liquidation also raises legal and ethical questions, especially as crypto intersects with consumer‑protection regulation and traditional financial law. In CeFi contexts, the right of an exchange to liquidate a user’s position is typically governed by the platform’s terms of service, which specify margin requirements, liquidation logic, and the possibility of ADL. Regulators increasingly expect exchanges to disclose these mechanisms in clear language, so that retail users understand that their BTC or ETH perps can be liquidated rapidly and that profitable positions can even be partially closed to absorb others’ losses when ADL is triggered. The fairness of ADL, in particular, is a contested ethical issue, because it forces risk‑sharing among traders who may not have consented to act as a backstop.

In DeFi, liquidation logic is encoded into smart contracts, and users interact with it through non‑custodial interfaces. From a legal perspective, this raises questions about liability when liquidation behaves unexpectedly, whether due to bugs, oracle failures, or extreme market conditions. Some argue that protocols should remain immutable and that users accept all risks by interacting with them, while others maintain that DAO governance has a responsibility to compensate users in cases where the protocol behaves contrary to its documented design. Debates around compensation after liquidation glitches or oracle exploits illustrate the tension between code‑is‑law and community‑is‑law approaches to DeFi governance.

Outside pure trading and lending, policymakers have begun to consider how forced liquidation should be treated in contexts such as dormant accounts, estate settlement, or bankruptcy. For instance, state‑level legislation in the United States has been introduced to protect dormant crypto from automatic forced liquidation by custodians, reflecting a desire to ensure that long‑term holders or heirs are not surprised by involuntary sales simply because an account was inactive. These initiatives draw a line between risk‑engine‑driven margin liquidation—which users explicitly opt into when trading—and custodial liquidation of assets held without leverage, where consumer‑protection norms are stronger.

Ethically, liquidation also forces conversations about financial literacy in crypto. Many retail users are attracted by stories of whales making millions in hours through leveraged BTC or ETH trades, but they may not fully grasp how liquidation risk scales with leverage or how sudden and irreversible liquidation events can be. Journalistic coverage that contextualizes these trades and highlights the losses as well as the wins can help counterbalance the glamorization of extreme leverage. Likewise, DeFi interfaces that prominently display health factors, liquidation prices, and risk warnings contribute to a more informed user base, reducing the odds that borrowers will accidentally drift into liquidation zones.

Outlook

Liquidation will remain one of the defining mechanisms of crypto markets for as long as leverage, volatility, and permissionless lending are central features of the ecosystem. On centralized exchanges, the growth of perpetuals and cross‑collateralized portfolios ensures that liquidation engines and ADL systems will continue to play a pivotal role in managing tail risk, even as regulators push for greater transparency and more conservative retail leverage limits. On‑chain, DeFi lending protocols will keep refining their health factors, liquidation thresholds, and liquidator incentives to balance capital efficiency with protocol safety, especially as new forms of collateral like liquid‑staking tokens and RWAs complicate risk models.

At the design frontier, soft‑liquidation AMMs like Curve’s LLAMMA, liquidation brakes like those in f(x) Protocol, and options‑based proposals from Vitalik Buterin and others point toward a future where liquidation is less binary and more continuous. As these designs mature, they may allow users to access BTC and ETH leverage with smoother risk profiles, fewer catastrophic liquidations, and more predictable outcomes under stress. Nevertheless, no design can eliminate the fundamental trade‑off between leverage and risk: the more exposure you assume relative to your capital, the closer you live to the edge where automation takes over and liquidates you to protect the system.

For a crypto news audience, liquidation will continue to provide both storylines and signals. Whale liquidations, lending‑protocol cascades, and liquidation glitches will remain headline events, while dashboards tracking aggregate liquidations and open interest will stay core tools for reading market structure. The challenge for builders, traders, and regulators alike is to harness the discipline that liquidation brings—keeping platforms solvent and curbing unpayable debts—without allowing its most violent manifestations to undermine trust or wipe out users who do not fully understand the stakes.

Latest Liquidation news

Inspired by Curve's LLAMMA and f(x)'s Liquidation Brake, protocol architect outlines a fixed-rate lending model where collateral self-hedges before liquidation thresholds are breachedAave Chan Initiative Accuses Aave Labs of Diverting DAO Revenues and Privatizing Protocol Economics, Demands Clarity on CowSwap Integration, Vault Fees, Horizon Deals, and V4 Liquidation Engine Incentives.The beautiful math behind Curve AMMs series part 3, this time diving into LLAMMA, Curve’s lending–liquidation AMM.Liquidation protection is pushing DeFi beyond cliff-edge liquidations, introducing automated slopes that adjust risk continuously onchain today. TermMax Alpha Live on BNB Chain!A liquidation-free module powered by TermMax Fixed Rate AMM engine, allows users, traders and market makers to bet and hedge on Binance Alpha Token and memecoins price fluctuations. https://x.com/TermMaxFi/status/1988607773626753162?s=20

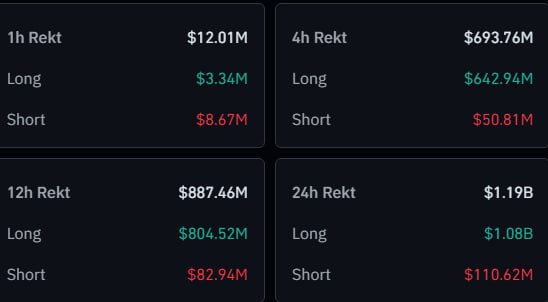

TermMax Alpha Live on BNB Chain!A liquidation-free module powered by TermMax Fixed Rate AMM engine, allows users, traders and market makers to bet and hedge on Binance Alpha Token and memecoins price fluctuations. https://x.com/TermMaxFi/status/1988607773626753162?s=20 In the past 24 hours , 307,787 traders were liquidated , the total liquidations comes in at $1.19 billion.

The largest single liquidation order happened on HTX - BTC-USDT value $33.95M

In the past 24 hours , 307,787 traders were liquidated , the total liquidations comes in at $1.19 billion.

The largest single liquidation order happened on HTX - BTC-USDT value $33.95MSources

- https://www.youtube.com/watch?v=619wKtFFh_g

- https://arxiv.org/html/2602.12104v1

- https://www.deribit.com

- https://coinmarketcap.com/charts/liquidations/

- https://chain.link/article/liquidation-cascade-crypto-lending

- https://mixbytes.io/blog/modern-defi-lending-protocols-how-its-made-curve-llamalend

- https://www.youtube.com/watch?v=3ObfS4ESdGI

- https://thedefiant.io/news/defi/vitalik-buterin-options-based-defi-replace-liquidation-driven-debt

- https://cleartoken.io/insight-hub/articles-papers/a-call-for-market-maturity/

- https://www.binance.com/el/blog/futures/421499824684902466

- https://financefeeds.com/how-liquidation-engines-work-in-defi-lending/

- https://financefeeds.com/the-strategic-liquidation-why-david-hoffmans-portfolio-shift-shook-the-crypto-community/

- https://resources.curve.finance/crvusd/loan-concepts/

- https://statemind.io/blog/curve-stablecoin-deep-dive

- https://hyperliquid.gitbook.io/hyperliquid-docs/trading/auto-deleveraging

- https://www.coinglass.com/liquidations

- https://aave.com/docs/aave-v3/overview

- https://docs.compound.finance/v2/comptroller/

- https://bookmap.com/blog/what-are-liqiuidations-in-crypto

Community notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…