f(x) Protocol splits liquid staking collateral into a trustless stablecoin (fxUSD) and leveraged positions, using a Liquidation Brake to prevent cascades — with $152M TVL and integrations across Morpho, Aladdin DAO, and Curve.

- x.com63

- youtube.com4

- medium.com3

- fx.aladdin.club2

- leviathannews.substack.com1

- github.com1

- convexfinance.medium.com1

+1 sources across the wider coverage universe

f(x) Protocol aims to fix DeFi's stablecoin and leverage flaws by linking fxUSD, leveraged positions, staking yield, and liquidity into a single system managing $152M TVL and $56M supply2026-05

f(x) Protocol aims to fix DeFi's stablecoin and leverage flaws by linking fxUSD, leveraged positions, staking yield, and liquidity into a single system managing $152M TVL and $56M supply2026-05 Inspired by Curve's LLAMMA and f(x)'s Liquidation Brake, protocol architect outlines a fixed-rate lending model where collateral self-hedges before liquidation thresholds are breached2026-06

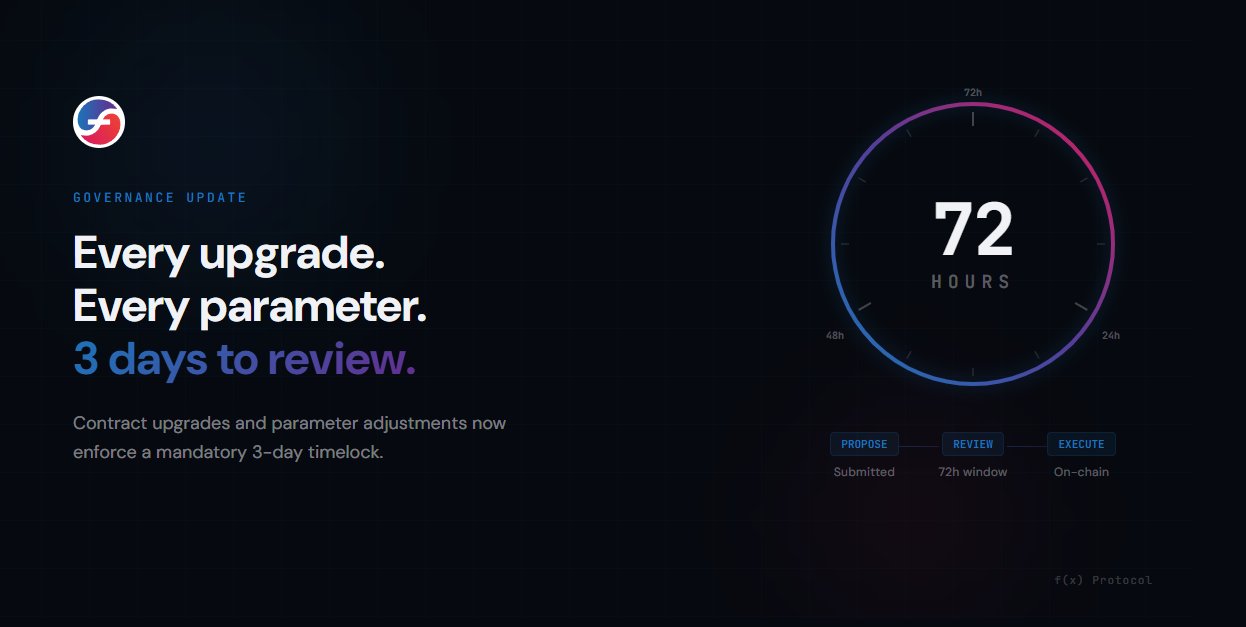

Inspired by Curve's LLAMMA and f(x)'s Liquidation Brake, protocol architect outlines a fixed-rate lending model where collateral self-hedges before liquidation thresholds are breached2026-06 f(x) Protocol introduces a 3‑day on‑chain timelock and 6‑of‑9 multisig approval for all contract upgrades and parameter changes, with only oracle updates and emergency pauses exempted to protect users.2026-04

f(x) Protocol introduces a 3‑day on‑chain timelock and 6‑of‑9 multisig approval for all contract upgrades and parameter changes, with only oracle updates and emergency pauses exempted to protect users.2026-04 f(x) Protocol partners with 9 Summits to debut an agentic fxUSD vault on Morpho, bringing leverage and liquidity to emerging AI-native assets.2026-02

f(x) Protocol partners with 9 Summits to debut an agentic fxUSD vault on Morpho, bringing leverage and liquidity to emerging AI-native assets.2026-02 Stand up for trustless solutions on Ethereum.

Be part of the Trustless Force.

Join Curve, f(x), Liquity and Leviathan this Wed. 3pm CET.2026-01

Stand up for trustless solutions on Ethereum.

Be part of the Trustless Force.

Join Curve, f(x), Liquity and Leviathan this Wed. 3pm CET.2026-01 Harbor, a friendly f(x) Protocol fork, has started their early liquidity seeding round.2025-12

Harbor, a friendly f(x) Protocol fork, has started their early liquidity seeding round.2025-12

A decentralized finance protocol built on Ethereum that splits collateral yield into a stable token and a leveraged position, f(x) Protocol attempts to resolve the long-standing tension between stablecoin stability, capital efficiency, and trustlessness.

What f(x) Protocol Is

Most stablecoin designs force a trade-off. Fiat-backed stablecoins like USDC are stable but centralized. Overcollateralized stablecoins like DAI sacrifice capital efficiency. Algorithmic designs have repeatedly collapsed under market stress. f(x) Protocol, developed under the Aladdin DAO umbrella, proposes a different architecture: instead of treating collateral as inert backing, it routes the yield and volatility of liquid staking tokens like wstETH into two distinct instruments — a low-volatility stablecoin (fxUSD) and a high-volatility leveraged position (xPOSITION) — letting each token serve users with opposite risk appetites from the same collateral pool.

The protocol launched its V2 in 2024 and has grown to approximately $152 million in total value locked with around $56 million in fxUSD supply, making it one of the more substantive experiments in what advocates call "trustless" stablecoins — those with no issuer capable of freezing balances or blacklisting addresses.

f(x) Protocol aims to fix DeFi's stablecoin and leverage flaws by linking fxUSD, leveraged positions, staking yield, and liquidity into a single system managing $152M TVL and $56M supply

$56M fxUSD against ~$152M TVL is still a thin enough base that the stress variable is redemption depth when xPOSITION demand vanishes. f(x) makes leverage fees and wstETH/WBTC carry subsidize peg defense, cleaner than pure emissions, but it also couples stablecoin health to trader appetite. If ETH vol spikes while the fxUSD/USDC pool and Stability Pool stay bid with boring FXN incentives, the design earns credibility.

Readers click f(x) Protocol stories most when they validate the core promise under real stress — the $300M ETH liquidation-survival story outperformed every product launch, revealing that the audience treats protocol resilience proofs as more valuable than feature announcements.

The Dual-Token Model

The core mechanic is straightforward in concept. A user deposits wstETH (Lido's wrapped, yield-bearing staked ETH) into f(x). The protocol splits the economics:

- fxUSD absorbs a small, dampened slice of ETH price movement, keeping it near a $1 peg. Holders receive predictable value without exposure to Ethereum's full volatility.

- xPOSITIONs absorb the remainder — including all the collateral's staking yield and the amplified price exposure the stablecoin holders gave up. xPOSITION holders are effectively leveraged long on ETH.

Because the total value in the system must always balance, fxUSD's stability is a mathematical consequence of xPOSITION holders absorbing volatility, not a promise backed by a reserve manager or algorithm. The staking yield generated by wstETH flows to xPOSITION holders, compensating them for the risk they bear — and crucially, no funding rate is charged, because yield from the collateral itself replaces it.

This structure is conceptually adjacent to what Curve Finance's LLAMMA mechanism does with debt rebalancing, and f(x)'s architects have publicly credited Curve's influence. The Trustless Force coalition — a loose alignment between f(x), Curve Finance, and Liquity — explicitly promotes this family of designs as an alternative to centralized stablecoin dominance.

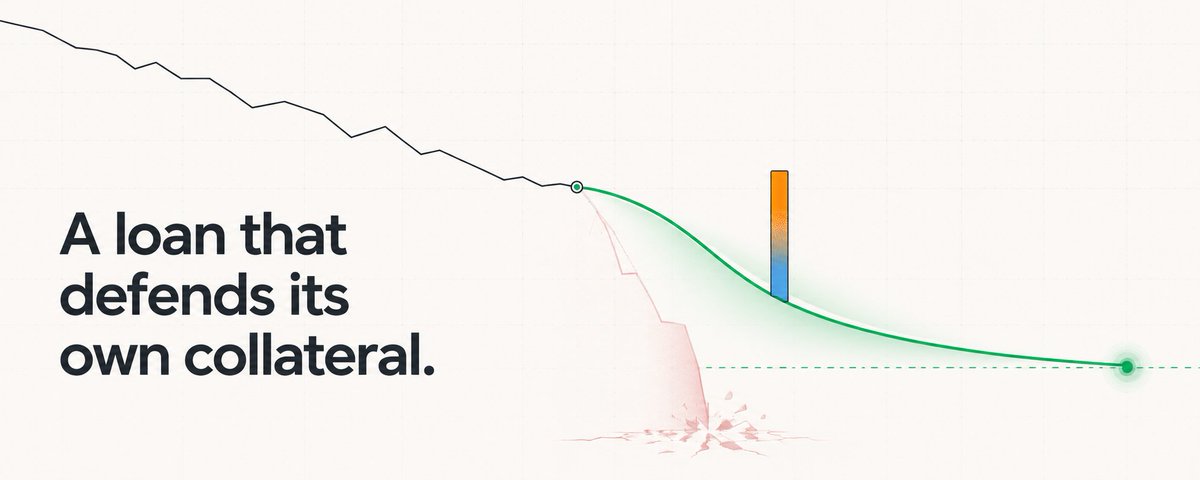

The Liquidation Brake

One of the protocol's most technically distinctive features is its Liquidation Brake, a rebalancing mechanism designed to prevent cascading liquidations during sharp market moves.

In conventional lending protocols, a price drop below a liquidation threshold triggers automatic collateral sales, which push prices lower, which trigger more liquidations — a well-documented death spiral. f(x)'s approach, inspired partly by Curve's LLAMMA model, attempts to self-hedge the collateral position before a hard liquidation threshold is reached. When the collateral ratio deteriorates, the protocol automatically rebalances between fxUSD and xPOSITION allocations, smoothing the system's exposure rather than forcing asset sales into a falling market.

During a significant market drawdown in 2025, the protocol recorded 87 rebalance transactions with zero liquidations — a result the team cited as validation of the design under real stress conditions.

A newer evolution of this thinking, outlined by a protocol architect in a piece on fixed-rate lending, extends the concept further: collateral could theoretically self-hedge so aggressively that fixed-rate borrowers never face a liquidation event at all, with the xPOSITION layer absorbing the residual risk dynamically.

- 01Liquidation-free leverage proof

The protocol's claim of non-liquidatable xPositions drew readers specifically when a live market stress event tested it — abstract promises became concrete validation.

- 02sPOSITIONs fixed-leverage shorts

A structured short product with no funding costs and a liquidation brake addresses a specific pain point traders know from perps, making it a sharp, differentiated pitch.

- 03Multi-asset stablecoin expansion

Each new collateral-backed stablecoin (fxUSD, arUSD via LRTs, btcUSD via WBTC) signals protocol breadth and unlocks new yield/leverage pairs readers want to track.

- 04Convex and ecosystem integrations

cvxFXN brought Convex's vote-locked flywheel into the picture, signaling maturity and aligning f(x) with an established DeFi power base readers already follow.

- 05RPC failure incident and keeper risk

The rare liquidations caused by parallel RPC endpoint failure revealed that keeper infrastructure — not the math — is the protocol's real operational vulnerability.

- 06TVL milestones and growth signals

Readers tracked the wstETH TVL climb (9,500 → 10,000+) as a proxy for conviction, treating milestone coverage as social proof rather than raw financial data.

fxUSD: The Stablecoin Layer

fxUSD is the protocol's primary stable output. Unlike USDC or USDT, it carries no issuer — no entity can freeze it or reverse a transaction. Unlike FRAX or earlier algorithmic designs, it does not rely on protocol-native token seigniorage that can evaporate in a bank run.

A report by Pangea covering 2024 found that fxUSD's peg held through a turbulent year for crypto markets, a period that saw multiple other stablecoin experiments fail or depeg. The stability is structurally enforced: if demand for fxUSD falls and the collateral ratio deteriorates, xPOSITION holders bear larger losses, incentivizing arbitrageurs and the rebalancer to restore equilibrium.

fxUSD has been integrated into broader DeFi infrastructure. It is accepted as collateral on Morpho, a modular lending protocol, and the yield-bearing variant fxSAVE — a savings vault that auto-compounds returns and claims gas-free — has also been listed there as collateral. This composability matters: a stablecoin that cannot be used in lending, liquidity provision, or structured products has limited utility regardless of its theoretical soundness.

Inspired by Curve's LLAMMA and f(x)'s Liquidation Brake, protocol architect outlines a fixed-rate lending model where collateral self-hedges before liquidation thresholds are breached

$10.2B of borrowed Aave debt still clears through cliff risk, while Pendle's $1.24B TVL shows DeFi users will buy fixed-maturity risk when the primitive is legible. A CPPI loan turns collateral management into an explicit short-vol spread: borrowers pay via whipsaw bleed and lower upside, lenders need that spread funding a gap-risk reserve, not just cleaner UX. Curve's 10/10 postmortem is the check on the design: LLAMMA saved about 22% of at-risk positions, but the CRV-long LlamaLend market still carried roughly $700k of bad debt at ~70% backing after the gap.

Leverage Without Funding Fees: xPOSITIONs and sPOSITIONs

The protocol's leverage products are structured around the same collateral pool that backs fxUSD.

xPOSITIONs offer leveraged long exposure to ETH (and now WBTC, following the launch of WBTC markets). Because leverage is derived from the structural split of collateral rather than from borrowed capital, there is no ongoing funding rate. xPOSITION holders receive staking yield from the underlying collateral, and they can set limit orders to automatically open or close positions at target prices — a feature added to reduce the need for active monitoring.

sPOSITIONs, introduced later, provide the short side: fixed leverage, no funding costs, and the same Liquidation Brake protection on the downside. Leverage is available up to 7x. For traders who find perpetual futures funding rates prohibitive — particularly in sustained bull markets where shorts pay heavily — the zero-funding structure is a meaningful structural difference.

Both products exist within a single system: the same collateral that backs fxUSD provides leverage for xPOSITION and sPOSITION traders, and the yield from that collateral compensates the leveraged side rather than going to a protocol treasury or being extracted as fees.

- 2023-08launch

Protocol v1 launches, ETH cap hits 1,000 ETH limit within days

- 2023-08milestone

Cap doubled to 2,000 ETH after reaching initial limit in five days

- 2023-10launch

FX token sale sells out for 300 ETH in under one minute

- 2024-03exploit

RPC endpoint failure causes rare liquidations; airdrop promised to affected users

- 2024-07governance

f(x) Protocol v2.0 whitepaper published

- 2024-09launch

f(x) Protocol v2 goes live on Ethereum mainnet

- 2024-11milestone

Convex adds cvxFXN, integrating f(x) into its vote-locking ecosystem

- 2025-04launch

fxSAVE savings vault and sPOSITIONs fixed-leverage shorts launch

fxMINT and Capital Efficiency

fxMINT, launched in early 2025, addresses a specific user need: borrowing stablecoins against ETH or BTC exposure without selling or giving up that exposure.

A user deposits BTC or ETH, mints fxUSD against it, and pays only a one-time fee on open and close — no ongoing interest rate, no funding cost. The borrowed fxUSD can be deployed elsewhere (into DeFi yields, for example) while the collateral continues to appreciate if markets move favorably. This is closer to a capital efficiency play than a stability product: users effectively monetize their holdings without triggering a taxable sale in jurisdictions where that matters, and without paying the continuous cost of a perpetual borrow position.

Governance and Security Architecture

f(x) Protocol operates under a governance model that has become more formalized as TVL has grown. All contract upgrades and parameter changes require a 3-day on-chain timelock combined with 6-of-9 multisig approval. The only exemptions are oracle price feed updates and emergency pause functionality — both require speed that a three-day delay would render useless.

This structure sits between pure immutability (which prevents upgrades but also bug fixes) and fully centralized admin keys (which allow fast iteration but introduce custodial risk). The timelock means that any malicious or mistaken upgrade is visible on-chain for three days before it takes effect, giving users time to exit.

The protocol is also a participant in the Open Gas Initiative, a coalition of DeFi protocols working to subsidize or redistribute gas costs for users — an acknowledgment that high Ethereum gas fees have historically been a barrier to participation in complex protocols like this one.

f(x) Protocol introduces a 3‑day on‑chain timelock and 6‑of‑9 multisig approval for all contract upgrades and parameter changes, with only oracle updates and emergency pauses exempted to protect users.

Oracle updates carved out of the timelock is exactly how Mango ($117M) and Inverse Finance ($15.6M) got drained — the "fast path" for price feeds becomes the fast path for attackers. 6-of-9 only means something if you know who the 9 are and whether any have ever voted against a proposal. Emergency pause is the other escape hatch governance attackers love — plenty of protocols have coincidentally paused right before an insider exit.

- Smart contractMedium

Trail of Bits completed a public security assessment, but the f(x) invariant math and dual-token model introduce novel complexity that standard audits may not fully stress-test.

- Keeper / infrastructure centralizationHigh

A confirmed incident where parallel RPC endpoint failures caused liquidations shows that off-chain keeper liveness is a hard dependency and a single point of failure under network stress.

- LiquidityMedium

arUSD is backed by liquid restaking tokens (LRTs) which themselves carry redemption queue risk; a coordinated LRT withdrawal crunch could stress arUSD's peg.

- Market / volatility absorptionHigh

xPosition holders absorb all price volatility for the paired stablecoin — in extreme downturns, xPosition NAV can approach zero before the system rebalances, concentrating tail-risk on leveraged side.

- Slashing / LSD penaltyLow

wstETH and LRT collateral introduce Ethereum validator slashing exposure, though diversified validator sets and insurance mechanisms keep this risk historically low.

- RegulatoryMedium

Offering structured leverage products and yield-bearing synthetic dollars without KYC on Ethereum mainnet places f(x) squarely in scope for evolving DeFi leverage and stablecoin regulations across major jurisdictions.

Ecosystem and Integrations

The protocol's connections extend in several directions:

Aladdin DAO is the governance layer that oversees f(x). A proposal on Aladdin DAO's forum sought approval for f(x) Protocol to license its codebase to Sigma, a project aiming to build a tiered fund protocol on BNB Chain based on f(x)'s design — a sign that the underlying architecture is being evaluated for cross-chain deployment.

Morpho is a key integration partner. Beyond fxUSD and fxSAVE collateral listings, f(x) partnered with 9 Summits to launch an agentic fxUSD vault on Morpho targeting AI-native assets — a niche but growing category as autonomous AI agents begin to hold and transact on-chain capital. The protocol has also published thinking on why AI agents might prefer trustless stablecoins over regulated fiat-backed equivalents, arguing that programmable, censorship-resistant money is structurally better suited to non-human counterparties.

Harbor, a protocol that describes itself as a friendly fork of f(x), began an early liquidity seeding round in 2025, suggesting that the architectural ideas are being refined and replicated by other teams.

Trustless Force is a public advocacy coalition involving f(x), Curve Finance, and Liquity. The three protocols have co-presented at events and published jointly under the banner of promoting decentralized stablecoin alternatives to USDC-style fiat backing. This is partly philosophical — all three teams argue that DeFi's long-term resilience depends on stablecoins that cannot be frozen by regulators or issuers — and partly commercial, as the coalition increases visibility for all three protocols.

Incentive Programs

f(x) has used airdrop campaigns to bootstrap adoption of its leverage products. A campaign distributed over $300,000 in xPOSITIONs to more than a thousand users, and a subsequent phase rewarded past xPOSITION holders with between $100 and $1,000 each for continued engagement. These programs are designed to generate real protocol usage rather than purely speculative farming — airdrop recipients received leveraged positions, not liquid tokens, meaning they had to engage with the product to realize value.

Risks and Limitations

No protocol design eliminates risk; it redistributes it. In f(x)'s case:

- xPOSITION holders bear concentrated risk. If ETH falls sharply and the xPOSITION layer is insufficiently capitalized, the Liquidation Brake may not fully prevent fxUSD depegging. The system requires sufficient demand for leverage to maintain a healthy collateral ratio.

- Smart contract risk remains. Despite the timelock and multisig governance, the protocol is complex — the rebalancer, the oracle system, and the leverage mechanics each introduce surface area for bugs.

- Liquidity risk. fxUSD's composability depends on sustained integrations. If Morpho or other venues de-list it, or if liquidity in exit pools dries up, holders may face slippage redeeming at par.

- Collateral concentration. The primary collateral is wstETH, meaning the protocol's stability is directly tied to Lido's continued operation and Ethereum's staking infrastructure.

Outlook

f(x) Protocol represents one of the more technically rigorous attempts to resolve the stablecoin trilemma without relying on centralized custodians or fragile algorithmic mechanisms. Its $152 million TVL and the zero-liquidation performance during market stress provide early validation, but the design has not yet been tested through a sustained, multi-month bear market with high redemption pressure.

The protocol's direction — fxMINT for capital-efficient borrowing, sPOSITIONs for two-directional trading, fxSAVE for yield aggregation, and Morpho integrations for composability — points toward a more complete financial stack rather than a single product. Whether that ambition can be sustained at scale, and whether the Trustless Force coalition can shift meaningful stablecoin volume away from USDC-backed designs, will define f(x)'s longer-term significance in DeFi.

Latest f(x) Protocol news

f(x) Protocol aims to fix DeFi's stablecoin and leverage flaws by linking fxUSD, leveraged positions, staking yield, and liquidity into a single system managing $152M TVL and $56M supplyInspired by Curve's LLAMMA and f(x)'s Liquidation Brake, protocol architect outlines a fixed-rate lending model where collateral self-hedges before liquidation thresholds are breachedf(x) Protocol introduces a 3‑day on‑chain timelock and 6‑of‑9 multisig approval for all contract upgrades and parameter changes, with only oracle updates and emergency pauses exempted to protect users.f(x) Protocol partners with 9 Summits to debut an agentic fxUSD vault on Morpho, bringing leverage and liquidity to emerging AI-native assets.Harbor, a friendly f(x) Protocol fork, has started their early liquidity seeding round. "The Great Decoupling: Why AI Agents Won’t Use "Human" Money" - a new article by f(x) Protocol

"The Great Decoupling: Why AI Agents Won’t Use "Human" Money" - a new article by f(x) ProtocolCommunity notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…