In-depth explainer on funding in crypto, covering venture raises, Ethereum dev financing, stablecoin yields, funding rates, onchain repo, quadratic funding, MEV, AI capital flows, and how these mechanisms shape risk, incentives, and market structure.

+26 sources across the wider coverage universe

Perplexity launches “Billion Dollar Build,” an 8-week competition challenging teams to create startups with $1B potential using its AI tools, offering up to $2M in funding and credits2026-04

Perplexity launches “Billion Dollar Build,” an 8-week competition challenging teams to create startups with $1B potential using its AI tools, offering up to $2M in funding and credits2026-04 Base unveils Batch 003 accelerator, selecting 12 teams from 1,100+ applicants to build DeFi, AI, and prediction market startups with funding support and Demo Day in SF2026-04

Base unveils Batch 003 accelerator, selecting 12 teams from 1,100+ applicants to build DeFi, AI, and prediction market startups with funding support and Demo Day in SF2026-04 Monad Foundation rolls out device subsidy program for teams with $2.5M+ TVL, funding dedicated signing laptops to boost multisig and treasury security across its ecosystem2026-04

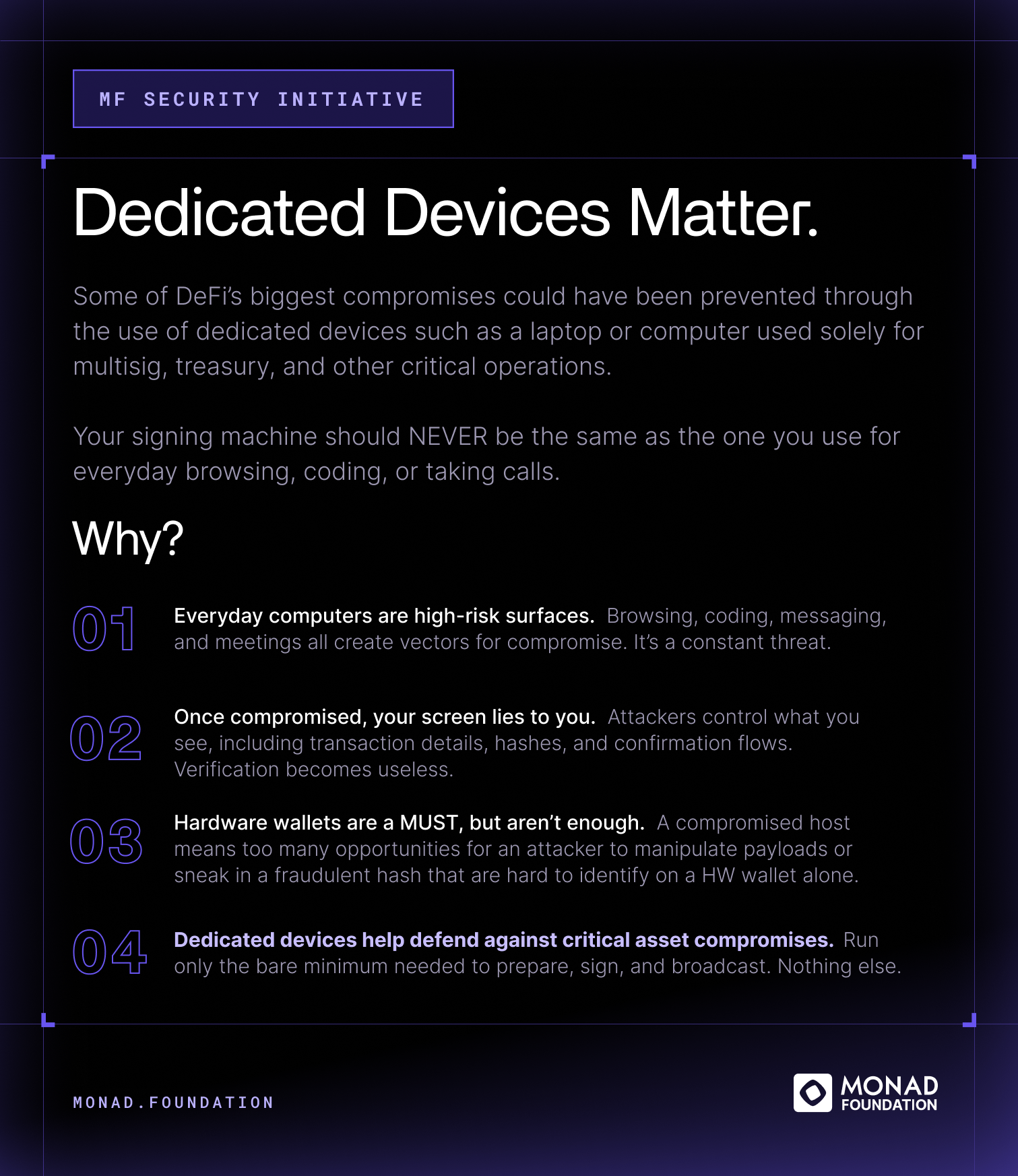

Monad Foundation rolls out device subsidy program for teams with $2.5M+ TVL, funding dedicated signing laptops to boost multisig and treasury security across its ecosystem2026-04 MoonPay partners with Moto Card to integrate virtual accounts via Iron, enabling instant fiat funding for crypto-backed Visa Infinite cards with BNPL perks and up to 5% cashback2026-04

MoonPay partners with Moto Card to integrate virtual accounts via Iron, enabling instant fiat funding for crypto-backed Visa Infinite cards with BNPL perks and up to 5% cashback2026-04 Pumpcade closes oversubscribed $5M funding round, sails ahead with instant-resolution prediction markets.2026-04

Pumpcade closes oversubscribed $5M funding round, sails ahead with instant-resolution prediction markets.2026-04 Propr unveils Hyperliquid trading platform, providing up to $100,000 funding to seize trading opportunities.2026-04

Propr unveils Hyperliquid trading platform, providing up to $100,000 funding to seize trading opportunities.2026-04

In crypto, “funding” describes how money and liquidity flow into, through, and out of digital asset ecosystems—from seed rounds and token launches to derivatives funding rates, stablecoin yields, and onchain repo that powers institutional markets. It is at once a corporate finance concept, a market-pricing mechanism, and a governance question about who pays for public goods like core protocol development.

1. What “Funding” Means In Crypto

In traditional finance, funding usually evokes images of banks raising wholesale capital, companies issuing bonds, or start-ups pitching venture capitalists. Crypto inherits all of these meanings and then adds several more. In digital asset markets, funding can refer to traders paying or receiving a periodic fee on perpetual futures contracts, exchanges paying yield to stablecoin holders, networks directing block rewards or MEV revenue to public goods, and protocols or founders raising capital through equity, tokens, or hybrids of the two. At the same time, the rapid rise of crypto-adjacent segments like AI and decentralized compute has created new funding bottlenecks and power concentrations, as seen in data showing that roughly 88% of AI-related startup funding has been going to U.S.-headquartered companies, with about 319 billion dollars of capital disproportionately flowing into just a handful of names. This convergence of crypto, AI, and markets means that “funding” is no longer only about balance sheets; it is about who controls digital infrastructure and who gets access to it.

A useful way to navigate this complexity is to distinguish between at least four overlapping layers of funding. The first is corporate or venture funding, where companies and protocols raise capital in pre-seed, seed, and later-stage rounds, sometimes complemented by token launches or revenue-sharing agreements. The second is protocol and public-goods funding, where communities must decide how to pay for ongoing maintenance, security, research, and ecosystem development, as illustrated by recent concern over a looming funding crunch for Ethereum core development as major client incentive programs expire and foundation spending slows. The third is market funding, where derivatives funding rates, basis trades, and repo transactions determine who effectively pays whom to hold risk over time. The fourth is user-facing yield and lending, where holders of stablecoins, bitcoin, or other cryptoassets either provide or receive funding to and from intermediaries, often without fully realizing they are participating in a large-scale wholesale funding system.

These layers are intertwined in practice. When a centralized exchange offers yield on stablecoins, for example, it is effectively paying customers to fund the exchange’s own market-making or lending activities, drawing on either safe reserve returns or more volatile trading income depending on its business model. When an institution runs an onchain repo trade—posting tokenized Treasuries as collateral to borrow tokenized dollars overnight—it is engaging in the same core funding activity as in traditional repo markets, but on a blockchain rail that operates outside legacy market hours. When a DeFi protocol uses quadratic funding to match small donations to ecosystem grants, it is designing a new funding process that mathematically privileges broad participation over deep pockets. Throughout this explainer, we will move between these layers to show how funding shapes crypto, AI, and broader digital markets.

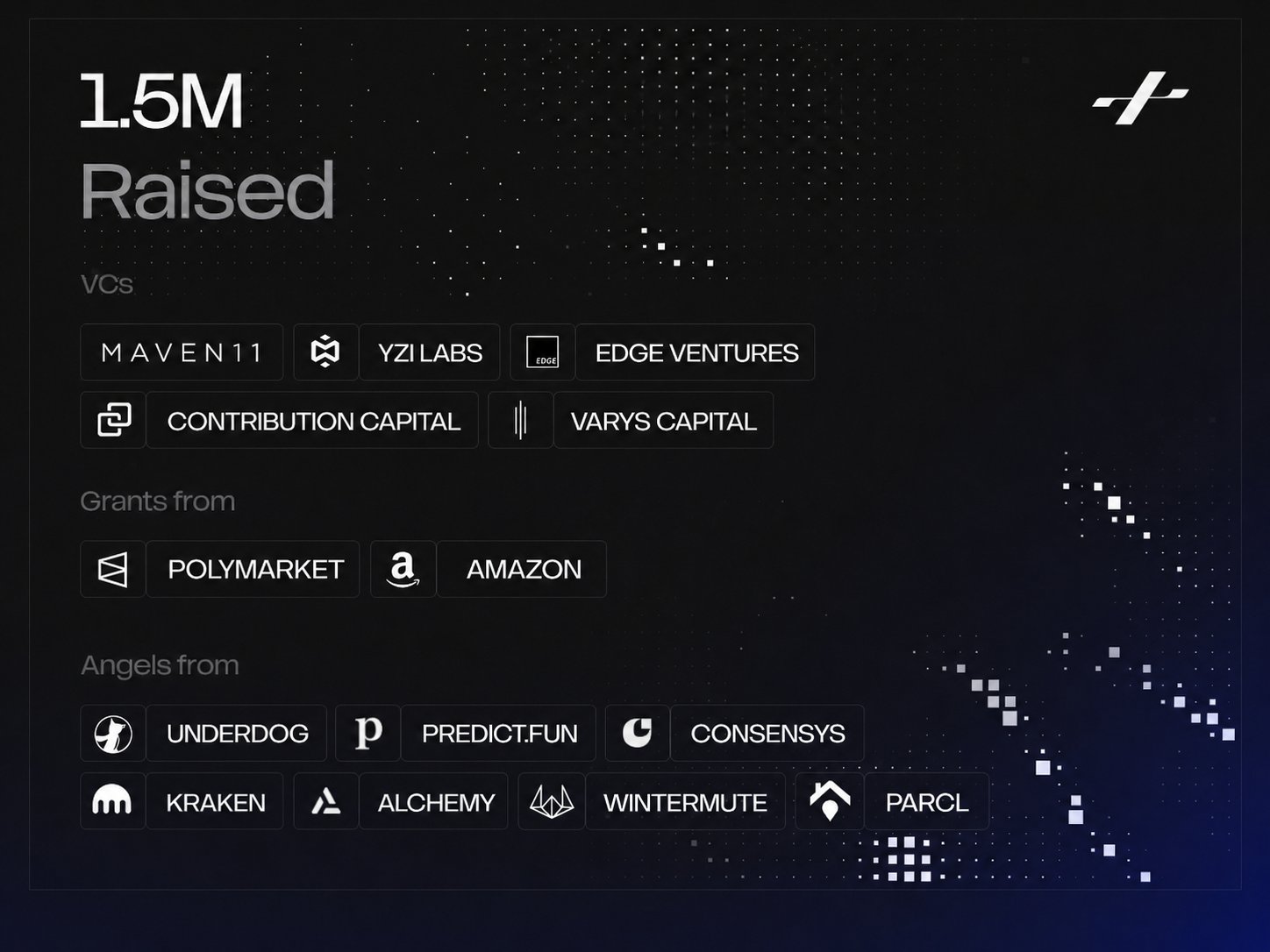

AI analytics platform Polysights raises $1.5M pre-seed funding to combat insider trading in prediction markets. The raise was backed by YZi Labs S3, Maven 11 Capital, and angels from Kraken and Consensys, plus grants from Polymarket and AWS.

13.36M Polymarket OrderFilled events still leave OrderPlaced and OrderCancelled off-chain, so surveillance has to infer intent from fills, wallet behavior, and public-event timing instead of reading a clean audit trail. Polysights sits in the compliance middleware lane prediction markets need if they want CFTC/Kalshi-level legitimacy without killing crypto-native liquidity; the hard part is separating sharp public-info traders from the 1,950-account “insider” heuristic bucket researchers are already arguing about.

Readers click 'funding' stories not for the dollar figures but to track a single macro bet: whether AI is permanently cannibalizing crypto VC allocation, making each major round either evidence of a surviving vertical or a data point in crypto capital's decline.↗

2. Funding Mechanics In Crypto Markets

2.1 Perpetual Futures And Funding Rates

Funding rates in perpetual futures markets illustrate how the word “funding” has taken on a very specific technical meaning in crypto trading. Perpetual futures are derivatives that, unlike traditional futures, do not expire; instead, they use a periodic funding payment between long and short positions to keep the contract price anchored to the underlying spot price. Because there is no fixed maturity date that naturally forces convergence, exchanges impose a funding rate mechanism where, typically every eight hours, traders on one side of the market pay those on the other side depending on whether the perp price is trading above or below spot. If the perpetual contract is rich to spot, longs usually pay shorts, and if it is cheap, shorts pay longs. This payment is the “funding rate.”

Most exchanges calculate their funding rates using a combination of an interest-rate term and a premium index, which measures the difference between the futures price and the spot price of the asset. The interest rate component is usually set by the exchange and remains relatively stable, while the premium index fluctuates with market conditions, becoming positive when the perp trades at a premium to spot and negative when it trades at a discount. A common simplified formulation is that the funding rate equals the premium index plus the interest rate term, though each venue may apply caps, floors, and smoothing rules to avoid extreme spikes. This mechanism creates a continuous incentive for traders to take positions that close the gap between perp and spot markets: when funding is very positive, it is attractive to be short perps and long spot; when funding is deeply negative, the opposite basis trade becomes appealing.

Over time, funding rates have become a widely watched sentiment indicator for assets like bitcoin and ether. In highly bullish phases, perpetual contracts tend to trade above spot as leveraged longs chase upside, causing funding rates to rise and effectively forcing those longs to subsidize short sellers to hold the other side. When fear dominates and traders rush to hedge, perps can flip to a discount, funding turns negative, and shorts end up paying longs to maintain exposure. Funding screens and averages across exchanges are now commonly used by analysts to assess whether leverage is stretched and whether there is room for a “short squeeze” or a “long flush,” and they often feature in commentary about whether a bitcoin bottom or top might be forming in the current cycle. These dynamics underline that funding rates are not just technical details; they are a pricing mechanism for leverage that directly affects who finances whom in the market.

2.2 Cross-Exchange Funding Arbitrage And Fixed Yield

The existence of divergent funding rates across exchanges and between derivatives and spot venues has given rise to a range of arbitrage and carry strategies. One prominent example is cross-exchange funding arbitrage, where traders take offsetting positions in perpetual futures across different platforms to capture a relatively predictable funding spread. If one exchange offers significantly higher positive funding on long positions than another, a trader might go long on the high-funding venue and short on the low-funding one, hedging out price risk while collecting the net positive funding payments. Some DeFi projects and prime brokers now market cross-exchange funding arbitrage as a “repeatable fixed-yield engine,” with claims of offering up to roughly thirty percent annualized returns in favorable conditions when combined with leverage and capital-efficient infrastructure.

Although these strategies can indeed transform noisy funding flows into something that resembles fixed income, they are not risk-free. Exchange credit risk, sudden changes in funding formulas, liquidity constraints, and basis risk between different instruments or collateral types can all erode returns or cause sudden losses. Nonetheless, the emergence of cross-exchange funding arbitrage illustrates how market “funding” in the derivatives sense can be turned into structured yield products and made accessible to a broader set of investors who may not trade perps directly. It also shows how crypto’s native funding mechanisms—like the perpetuals funding rate—and traditional concepts such as carry, duration, and credit interact in practice, blurring the lines between DeFi, centralized exchanges, and institutional prime brokerage.

3. Stablecoins, Yield, And Exchange Funding Models

3.1 Reserve-Based Versus Activity-Based Remuneration

Stablecoins now sit at the center of crypto’s funding ecosystem, functioning both as transactional media of exchange and as short-term funding instruments whose yields and risks depend heavily on how sponsors and intermediaries structure them. A recent Bulletin from the Bank for International Settlements (BIS) examined how centralized exchanges remunerate users who hold stablecoins on their platforms and emphasized that there are two broad models: reserve-based and activity-based remuneration. In the reserve-based model, exchanges pass through a portion of the interest income they earn on the safe reserve assets backing stablecoins, such as short-term government bills or bank deposits, to users in the form of relatively stable yields that tend to track policy interest rates. In the activity-based model, by contrast, exchanges pay users out of revenues generated by trading, lending, or other market activities involving those stablecoins, which can be more volatile and correlated with risk taking.

The BIS analysis highlights that these models have different risk and macro-financial implications. When remuneration is largely reserve-based, stablecoin yields effectively compete with money-market funds and bank deposits as a way for users to earn a policy-rate-linked return on cash-like assets. As central bank policy rates rise, the income available from holding stablecoins on compliant, well-managed platforms may become more attractive, potentially pulling funds out of traditional bank accounts into crypto venues. When remuneration is activity-based, however, high yields may signal that exchanges or counterparties are using stablecoin balances as funding for riskier activities such as leveraged trading, unsecured lending, or proprietary strategies, exposing users to opaque credit and liquidity risks. The collapse of several high-yield CeFi lenders in past cycles underscored how quickly activity-based funding structures can unravel when market conditions change.

From a user perspective, this means that a double-digit stablecoin yield should be understood as a funding cost someone else in the system is paying, not free money. If the yield is reserve-based, it is likely coming from a spread between what stablecoin issuers earn on safe assets and what they share with holders or intermediaries. If it is activity-based, it is likely coming from traders paying borrowing rates, funding rates, or spreads to take leveraged positions, or from the platform itself taking directional risk. The distinction is critical because it determines whether a stablecoin balance behaves more like a bank deposit with deposit insurance and regulatory oversight, or more like a short-term claim on a shadow bank or hedge fund that can impose losses or gates in stress.

3.2 Stablecoins As Bank Deposit Substitutes And Funding Sources

Central banks and regulators are increasingly focused on how the growth of stablecoins affects the traditional banking system’s funding structure. A note by economists at the Federal Reserve, for instance, examined how demand for stablecoins could alter bank deposits, credit supply, and financial intermediation. The impact depends heavily on which assets are redeemed to obtain stablecoins and where those funds ultimately reside. If households move money from bank deposits into stablecoins, but stablecoin issuers in turn invest their reserves in bank deposits or very short-term bank liabilities, then the banking system still indirectly retains much of that funding. If, however, reserves are mainly held in central bank liabilities or government securities, banks may lose a larger share of their cheap, sticky retail deposit base, potentially pushing them to rely more on wholesale funding or to shrink their balance sheets.

The same note stresses that stablecoins can also act as funding sources for exchanges and other intermediaries instead of, or in addition to, being simple pass-through instruments. When an exchange offers stablecoin yield sourced from activity-based revenues, it is effectively borrowing from users’ stablecoin balances and redeploying that capital into lending, market making, or other operations. In this sense, some crypto platforms resemble narrow banks or money-market funds, while others look more like lightly regulated broker-dealers or shadow banks. The line between funding the crypto ecosystem and subtly reconfiguring the broader financial system’s funding mix is therefore blurry. For investors and policymakers, the challenge is to ensure that funding flows into productive uses and that credit and liquidity risks are transparent, rather than allowing hidden maturity and liquidity mismatches to build.

These questions intersect directly with the growth of onchain finance and tokenized real-world assets. As more government securities, bank liabilities, and high-quality collateral instruments are tokenized, the set of options for how stablecoin reserves are managed will expand, potentially making reserve-based remuneration more flexible and competitive but also creating new channels for stress transmission between crypto and traditional funding markets. That evolution leads naturally to the topic of repo and secured funding on blockchains.

- 01Large crypto/fintech round announcements↗

Raises from Alpaca ($150M), KAST ($80M), ZODL ($25M), and MetaComp ($35M) signal which verticals still attract institutional conviction, giving readers a map of where serious capital is flowing.

- 02AI crowding out crypto VC↗

AI capturing 80% of global venture funding and Q1 2026 becoming the biggest AI funding quarter ever—while crypto VC dropped 75% in a single month—frames every crypto raise as a fight for a shrinking pool.

- 03Perpetual funding rates as exit signal↗

Sharpe AI's analysis linking 5+ days of negative funding rates to 15–25% price drops, Ethena's 15 loss scenarios, and Vitalik's proposal to eliminate funding-rate exposure gave readers an actionable risk-reading framework.

- 04On-chain and alternative funding models↗

BagsApp's on-chain founder raises, Propr's prop-trading capital deployment, and Base's accelerator cohort represent reader interest in whether crypto-native funding mechanisms can bypass traditional VC gatekeeping.

- 05Protocol shutdowns under funding pressure

20+ shutdowns in Q1 2026, Botanix's L2 collapse, and Hyli closing after raising $3.4M illustrated that runway, not technology, is the primary survival variable for early-stage protocols.

- 06Accelerator and grant-based funding

Monad's device subsidy, Base Batch 003, and Perplexity's Billion Dollar Build competition showed readers that non-dilutive and milestone-gated funding structures are proliferating as VC appetite softens.

4. Secured Funding, Repo, And Onchain Infrastructure

4.1 From Traditional Repo To Onchain Repo

Repurchase agreements, or repo, are a foundational funding tool for banks, broker-dealers, and asset managers. In a typical repo transaction, one party sells a security—often a government bond—to another party with an agreement to repurchase it at a slightly higher price at a later date, effectively borrowing cash against collateral for an overnight or term period. The aggregate volume of repo exposures is enormous; recent commentary associated with onchain repo initiatives has pointed to average daily outstanding exposures on the order of tens of trillions of dollars globally, underscoring how central repo is to modern market plumbing. In traditional settings, repo operates on legacy infrastructure and within market hours constrained by time zones and holidays, which can introduce settlement frictions and funding gaps when asset and cash legs are not perfectly synchronized.

Onchain repo aims to port this secured funding mechanism onto distributed ledger rails, allowing institutions to mobilize high-quality collateral like U.S. Treasuries and obtain dollar funding around the clock. In one example, HIFI, DRW, and Marex have piloted an onchain repo facility on the Canton Network, where they settle a tokenized dollar instrument (USDCx) against tokenized U.S. Treasuries and automatically reverse the transaction at maturity through smart contracts. This structure allows these actors to access dollar funding and mobilize Treasury collateral outside traditional U.S. market hours, potentially reducing the impact of settlement delays tied to holidays and time zones. By ensuring that both the cash and collateral legs of the repo operate on a shared, synchronized ledger, onchain repo can mitigate some settlement and funding exposures that arise when different jurisdictions’ calendars and closing times do not line up.

From a funding perspective, onchain repo has several implications. It can expand the set of counterparties who can transact secured funding directly with one another, particularly if regulatory frameworks evolve to recognize digital securities and tokenized cash as eligible instruments. It can also make intraday and overnight liquidity management more granular, since smart contracts can automate margin calls, substitutions, and rollovers. For institutions that already hold cryptoassets or tokenized Treasuries for other purposes, onchain repo offers a way to generate funding efficiency without constantly bridging between traditional custodians and blockchain venues. At the same time, it raises questions about how bankruptcy laws, collateral rehypothecation, and central bank backstops apply to tokenized collateral, which will be a key area of policy development as these markets grow.

4.2 Digital Bonds And Bank Funding On Blockchain

Beyond repo, established financial institutions are experimenting with using blockchains to issue funding instruments directly. South Korea’s KB Kookmin Bank, for example, has reported issuing the country’s first blockchain-powered dollar digital bond by a domestic lender, raising 100 million dollars in two-year funding. The bank described the instrument as the first case of a Korean bank applying blockchain technology to actual foreign currency funding, with the bond denominated in U.S. dollars and issued in Hong Kong. By using a blockchain rail, the bank can potentially streamline issuance, settlement, and reporting while reaching a global investor base more efficiently, though in practice the investor set for an inaugural deal may remain relatively conventional.

This type of digital bond fits into a broader trend of tokenizing traditional debt instruments and using distributed ledgers for wholesale funding and liquidity management. For banks, the appeal includes operational efficiency, programmability—such as embedding covenants or coupon features directly into smart contracts—and improved transparency of ownership and collateral chains. For crypto markets, each such issuance expands the universe of onchain high-quality collateral, which can be used in repo, derivatives margining, and structured products. Over time, if more banks and sovereign issuers adopt digital bonds, the boundary between “crypto funding” and “capital markets funding” may erode, with blockchains serving as a common settlement layer for both.

4.3 Bitcoin Miner Financing And Hashrate-Backed Funding

Funding is also a critical challenge for capital-intensive actors within the crypto ecosystem itself, such as bitcoin miners. Mining operations face substantial upfront costs for hardware, energy infrastructure, and maintenance, and historically have relied on a combination of equity, debt, and self-funding from mined coins. Newer approaches involve structuring investment products where hashrate—the computational power miners contribute to the Bitcoin network—is tokenized or otherwise used as the basis for financing. Platforms like STOKR have described supporting mining firms in designing offerings where investors obtain exposure to the future output or revenue stream of mining operations, sometimes using tokens that represent claims on hashrate or on a portion of mined bitcoin.

These arrangements effectively allow miners to monetize expected future production to obtain funding today, shifting some price and operational risk to investors who are willing to bear it in exchange for potential upside. They can be seen as a form of project finance tailored to Bitcoin’s unique economics. For the broader market, miner financing structures matter because they affect miners’ incentives to hold or sell coins, which in turn can influence supply dynamics, especially around halving events. They also illustrate how crypto-native business models push the frontier of what counts as collateral or securitizable cash flow, expanding the menu of funding instruments beyond traditional equity and debt.

Book of Eth defends Ethereum Foundation's five-year record, citing The Merge, Dencun, public goods funding and scaling upgrades amid growing criticism

$0.0015 median L2 fees by March 2026 is an insane scaling win, and also the source of the current ETH-holder anger: Dencun made Ethereum usable while compressing the burn that made the asset story easy. EF’s five-year record looks much better if the KPI is protocol durability and public-goods throughput; it looks messier if the KPI is value capture from Base, Arbitrum, OP and the rest of the rollup stack. The next credibility test is whether blob demand and sequencing economics route enough surplus back to ETH before users decide “Ethereum won” just means everyone else got cheaper blockspace.

5. Startup, Venture, And AI Funding In The Crypto Economy

5.1 From Pre-Seed To Growth: Evolving Venture Dynamics

The venture-funding landscape for crypto and crypto-adjacent projects has gone through several boom-and-bust cycles, and debates about whether pre-seed funding is “dead” reflect how the risk appetite of capital providers changes with macro conditions. Commentators within the ecosystem have argued that the raw timeline from having an idea to getting acquired is stretching, making it harder to justify extremely early bets and prompting some investors to skip pre-seed rounds in favor of later-stage opportunities with clearer product-market fit. At the same time, founders face higher expectations around security, compliance, and go-to-market execution, especially when they build at the intersection of crypto, AI, and regulated financial services.

Despite these headwinds, substantial funding continues to flow into infrastructure projects that promise to make crypto more palatable to institutional players. Morpho, a project focused on building a capital-efficient lending and borrowing layer that “dresses up” crypto for Wall Street, has raised about 175 million dollars in a round led by well-known firms such as a16z crypto, Paradigm, and Ribbit Capital. The fundraise has been described as “historic” in scale for a protocol arranging itself as a kind of technical intermediary or matching engine between DeFi and traditional finance, underscoring investor belief that better market plumbing and risk management will be rewarded. Deals like this indicate that while some speculative segments cool, there remains a robust appetite for platforms that sit at the core of future funding and credit markets.

Prediction market platform Kalshi offers another window into how crypto-adjacent firms scale funding over time. The platform has reportedly surpassed two billion dollars in annualized revenue and is now in informal talks with investment banks about a potential initial public offering after reaching a valuation of roughly 22 billion dollars in its latest funding round. According to reports, the company has tripled its revenue since November, driven by traders betting on a range of binary outcomes. While Kalshi operates under a regulated framework distinct from fully onchain decentralized markets, its trajectory shows how investor capital, regulatory engagement, and user demand can combine to transform niche trading venues into sizable financial institutions, reconfiguring how funding and risk are allocated in the process.

5.2 AI Funding Concentration And Decentralized Alternatives

The intersection of AI and crypto has become a particularly intense focus area for investors, but the distribution of AI funding is highly uneven. Data summarized by Crunchbase and cited in recent commentary shows that nearly 88% of AI-related startup funding—approximately 319 billion dollars—has gone to companies headquartered in the United States, and that a large fraction of that capital is concentrated in just two dominant firms. This leaves the remaining 12% of funding to be shared by the rest of the world’s AI ventures and by thousands of smaller teams, effectively creating an oligopolistic funding landscape where a tiny number of incumbents control most of the compute, data, and talent. For critics, this pattern undermines the idea of a competitive market and raises questions about innovation, diversity, and access.

Crypto proponents argue that decentralized compute networks, powered by token-based economic engines, can offer an alternative funding and resource-allocation model for AI. Under this vision, rather than relying solely on centralized hyperscalers and a handful of heavily funded labs, AI applications could tap into global networks of GPU providers, with tokens or stablecoins used to price and settle compute in a more open marketplace. Grants, quadratic funding, and protocol-level incentives could be used to support open-source AI agents, privacy-preserving infrastructure, and community-owned datasets. While these ideas remain early, they resonate with the broader critique that current AI funding flows are not a global phenomenon but a concentration of economic power that decentralized finance might help rebalance.

At the same time, AI-related hardware and infrastructure companies are raising large rounds to expand the plumbing that both centralized and decentralized AI systems will run on. Firms like AttoTude, for instance, have secured sizable Series C funding rounds—reportedly on the order of tens of millions of dollars—to advance interconnect technologies for hyperscale infrastructure, including ASIC over dielectric approaches designed to meet rising AI compute demand. These capital-intensive projects sit at the junction of semiconductors, networking, and data centers, and their funding conditions will shape the cost structure and geographic distribution of AI capabilities. Crypto networks that integrate with such hardware, for secure computation or agentic services, inhabit the same funding universe.

5.3 Grants, Ecosystem Funding, And Agentic Apps

Not all funding in the crypto and AI space is venture-style equity or token sales. Many ecosystems rely on grants programs to seed early applications and infrastructure, often with a focus on public goods that might not attract immediate commercial funding. Celo’s Prezenti grants program, for example, has launched multiple seasons in which builders can apply for funding pools totaling over fifty thousand dollars aimed at “anchor” apps that drive real transactions and volume, as well as “frontier” projects focused on agentic applications and infrastructure. In its second season, Celo’s program invited applicants to propose agentic apps and infra that deepen the ecosystem’s utility, with funds provided as non-dilutive support rather than as speculative investments.

Grants like these bridge the gap between pure volunteer-driven open-source work and fully commercial ventures, allowing teams to experiment, launch, and iterate without immediate pressure to generate revenue or tokens. In the context of AI, where agentic applications require careful alignment, safety, and integration with existing systems, such funding can be particularly impactful. It also interacts with more experimental funding models like quadratic funding, retroactive public goods funding, and MEV-based revenue-sharing, which we will explore in more detail below. Together, these mechanisms create an ecosystem in which seed capital, protocol incentives, and grants complement traditional venture raises, shaping which ideas get a chance to launch.

- 2026-02milestone

Global fintech funding surpasses $1B in 29 deals

Q1 2026 becomes largest AI funding quarter, surpassing all of 2025

- 2026-03milestone

20+ crypto protocols shut down amid funding pressure

- 2026-04milestone

Crypto VC monthly funding collapses 75% to $660M across 62 deals

- 2026-04milestone

Botanix Bitcoin L2 collapses as funding dries up

Morpho raises $175M from a16z, Paradigm, and Ribbit Capital

- 2026-06milestone

KAST raises $80M at $600M valuation for stablecoin payments

6. Protocol Funding, Public Goods, And Governance

6.1 Ethereum’s Looming Core Development Funding Crunch

One of the most pressing funding debates in crypto today concerns how major base-layer protocols finance their ongoing development and maintenance. Ethereum, which secures hundreds of billions of dollars in assets and hosts a large share of DeFi and NFT activity, has long relied on a mix of Ethereum Foundation resources, client incentives, and ecosystem contributions to support core developers. A former Ethereum Foundation contributor, Trent Van Epps, has warned that Ethereum’s core development ecosystem could face a “slow-burning funding crisis” within three to nine months, citing the expiration of the Client Incentive Program and cuts to foundation spending. Van Epps estimates that core protocol development requires on the order of thirty million dollars per year and suggests that new funding mechanisms may be needed to sustain that level of work.

The prospect of such a funding shortfall raises deep questions about who is responsible for the ongoing security and evolution of public blockchains. Unlike private companies, layer-1 networks often lack a centralized treasury with guaranteed revenues; instead, they depend on a patchwork of foundations, corporate contributors, and grants programs, many of which are funded by early token allocations or donations. As those early reserves are drawn down, the community must decide whether to introduce new revenue streams—such as protocol-level fees earmarked for development, staking commissions, or MEV redistribution—or to rely on voluntary contributions from large stakeholders who benefit from the network’s success. Each choice carries governance and political trade-offs, especially given the desire to keep base-layer protocols credibly neutral and resistant to capture.

The Ethereum case illustrates that even highly successful networks cannot take funding for granted. If core teams lack reliable compensation, they may leave for better-funded projects or for private companies, leading to a slow erosion of expertise and capacity that manifests only when bugs, security issues, or necessary upgrades pile up. Conversely, introducing aggressive funding mechanisms could be seen as taxation, prompting backlash from users or validators. For investors and users, keeping an eye on how protocol development is funded is essential to assessing long-term sustainability and security, much like one would examine R&D spending and maintenance budgets in traditional infrastructure sectors.

6.2 Quadratic Funding And Internet Freedom

Quadratic funding has emerged as one of the most interesting experiments in funding public goods in a way that mathematically values broad participation. Conceptually, quadratic funding extends ideas from quadratic voting to the domain of funding: it uses a matching pool provided by sponsors to disproportionately amplify small individual contributions, making it more impactful when many people each donate a little rather than when a single wealthy donor contributes a lot. The core formula allocates matching funds to projects in proportion to the square of the sum of the square roots of individual contributions, which means that the number of contributors matters more than the total amount contributed. Vitalik Buterin, Zoë Hitzig, and Glen Weyl have analyzed this mechanism in academic work and blogposts, arguing that under certain assumptions it is the mathematically optimal way to fund public goods in a democratic community.

In practice, quadratic funding relies on a matching pool supplied by “matching partners” such as companies, individuals, or protocols that wish to support a set of public-goods projects. Individual donors then contribute to specific projects, and the mechanism calculates how much each project should receive from the matching pool based on the diversity and size of its donor base, with diminishing marginal returns for larger contributions. This ensures that projects with broad grassroots support receive larger matches, while those backed mainly by a few big donors receive less relative amplification. The approach has already been used to distribute more than two million dollars to public goods via platforms like Gitcoin, demonstrating its practical viability.

Recent funding rounds for causes like Internet freedom illustrate how quadratic funding is applied in the wild. A funding round organized by the Tor Project and FundingCommons, for example, invited donors to support ten organizations working on privacy, anti-censorship, and secure journalism, with the final day of contributions highlighted by major ecosystem accounts to drive participation. Matching pools in such rounds often come from protocols or foundations that wish to support digital rights and open-source tooling, effectively leveraging their capital to crowd in small donations from thousands of individuals. Quadratic funding thus becomes not just a technical mechanism, but a political statement about who should have a say in allocating resources to critical but under-monetized infrastructure.

6.3 MEV For Public Goods And DeSci Funding

Miner/Maximal Extractable Value (MEV) has traditionally been seen as a source of rent extraction and inefficiency, but recent research and experiments explore whether portions of MEV can be redirected to fund public goods. Gitcoin has published a report examining proposals and protocols aimed at redirecting MEV from private extraction toward public goods funding, emphasizing that MEV is a powerful but underutilized revenue stream that, if harnessed transparently, could support open-source development, protocol maintenance, and ecosystem infrastructure. Ideas range from MEV auctions that route a share of proceeds to community treasuries, to onchain coordination schemes where validators voluntarily commit a fraction of their MEV gains to public goods. While implementation remains challenging, the research underscores that the very mechanisms that currently generate hidden costs for users could be repurposed as funding sources.

Beyond core protocol funding, the decentralized science (DeSci) movement is exploring how crypto-native funding tools can support research and biotech innovation. Events like DeSci Berlin have showcased projects working on drug development, peptide discovery, encrypted longevity data, and self-driving science, with sessions devoted to the legal and funding aspects of these new models. Grants, DAOs, and tokenized IP structures are being experimented with to fund early-stage scientific work that might be too speculative for traditional grants agencies or private venture. Here again, crypto mechanisms such as quadratic funding, retroactive rewards, and governance tokens intersect with real-world questions about who pays for long-term, high-risk research, and who owns the resulting knowledge.

Together, these experiments indicate that “funding” in crypto is not limited to profit-seeking ventures or trading strategies. It extends to the design of public institutions and digital commons that underpin privacy, free expression, scientific progress, and open infrastructure. The challenge is to ensure that these mechanisms are robust to manipulation, sybil attacks, and governance capture, and that they remain inclusive even as they interact with concentrated pools of capital.

7. Funding Rates, Options, And Alternative Stable Designs

7.1 Beyond Funding Rates: Option-Based Stablecoins

While perpetual-futures funding rates are now a staple of crypto derivatives markets, some designers are looking for ways to build leverage and stability mechanisms that do not rely on ongoing funding payments. Vitalik Buterin, for instance, has proposed option-based stablecoin designs that aim to create assets with relatively stable value without resorting to debt, liquidations, or funding rates, instead using options on volatile assets like ETH to absorb price shocks. In these designs, users who want upside exposure to ETH effectively pay a premium to support the stability of the stablecoin, which can then maintain collateralization without constant refinancing or liquidation cascades. Although still theoretical in many respects, such proposals highlight how funding-related frictions—like the need to pay or receive funding in perpetuity—can prompt exploration of alternative architectures.

Option-based designs also tie into a broader trend of integrating derivatives deeper into stable asset construction. Rather than relying solely on overcollateralized loans and funding costs, protocols can, in theory, use paths of option payoffs to manage risk and fundraising over time. For example, a protocol might sell covered calls on its treasury assets to generate funding, allocating that revenue to a stability reserve. Or it might offer users structured products that embed both yield and downside protection, implicitly transferring funding flows through option pricing rather than through visible funding rates. These approaches translate complex financial engineering into code and governance decisions, expanding the menu of funding options but also raising the bar for risk management.

7.2 Funding Rates As Building Blocks For Structured Products

At the same time, the existing funding-rate infrastructure is increasingly being packaged into structured products aimed at both retail and institutional investors. Cross-exchange funding arbitrage strategies discussed earlier are one example; they rely on the relatively predictable oscillations of funding rates to generate a carry-like yield. These strategies can be combined with prime brokerage services that provide leverage, margin netting, and custody, turning raw funding flows into more polished products advertised as “fixed yield engines.” In DeFi, similar strategies can be implemented algorithmically via smart contracts that automatically allocate capital to lending pools, perpetual DEXes, and basis trades depending on where funding spreads are most attractive.

These developments accentuate the need to think of funding rates as both a market indicator and a funding channel. When market conditions are frothy and funding is very positive, structured products that short perps and go long spot may appear to offer low-risk returns, but they implicitly depend on the continued willingness of leveraged longs to pay for funding. When sentiment shifts and funding compresses or flips negative, these products can underperform or even incur losses unless they dynamically adjust. For risk managers, understanding the sensitivity of portfolios to changes in funding regimes becomes as important as tracking traditional interest-rate or credit spread risk.

TX3 Futures rolls out capital funding platform after $35M in payouts, as futures traders face growing competition and platform risk.

$35M paid across 8,000 traders works out to roughly $4,375 per trader, so payout distribution matters more than the aggregate flex. The CFTC asking this week about 24/7 standard futures and energy perps pushes funded-trader shops toward crypto-exchange style risk: uptime, liquidation logic, and rule immutability start becoming solvency-adjacent. “No mid-eval rule changes” lands harder if traders can audit the rulebook history the way DeFi users audit contract diffs.

Perpetual futures funding rates can flip sharply negative during deleveraging events; Sharpe AI data correlates 5+ consecutive negative-rate days with 15–25% spot price drops, and Ethena's model carries direct exposure to sustained negative rates across its collateral.

Crypto VC funding fell 75% month-over-month to $660M in April 2026, compressing runway across the sector simultaneously and creating correlated shutdown risk for projects that raised in 2024–2025 bull conditions.

- Smart-contract / mechanism riskMedium

On-chain funding models (BagsApp share trading, Propr capital pools, IXS tokenized lending) introduce novel contract surfaces; a flaw in collateral logic or liquidation mechanics can wipe allocated capital with no recourse.

- RegulatoryMedium

Cross-border funding rounds involving Asian-regulated entities (MetaComp backed by Alibaba, IXS/Funding Societies in Southeast Asia) face multi-jurisdictional securities scrutiny as stablecoin payment rails become part of capital flows.

- LiquidityMedium

Prop-trading and accelerator funding structures (Propr's $100K USDC pools, Monad subsidies) tie liquidity to protocol TVL thresholds; a TVL drop can trigger automatic funding withdrawal, compressing the very activity needed to restore TVL.

AI companies absorbing the majority of global venture capital compresses crypto valuations at the margin; founders raising in this environment face down-round pressure and must compete against AI deal flow for the same LP dollars.

8. Illicit Funding, Compliance, And Risk

Funding flows in crypto are not always benign. Authorities in multiple jurisdictions have increasingly targeted the use of cryptocurrencies to fund illicit activities, including terrorism, sanctions evasion, and ransomware. Recent cases have seen courts convict individuals involved in using crypto networks to channel funds to extremist organizations, with investigations often revealing complex webs of addresses, mixers, and off-ramp entities. While the scale of such activities is small relative to both the broader crypto market and traditional illicit finance, their high-profile nature has prompted regulators to push for stricter controls on exchanges, stablecoin issuers, and other intermediaries.

From a funding perspective, the key issue is how to balance open access to permissionless infrastructure with robust controls on the fiat on- and off-ramps and on certain classes of stablecoins. Measures like the FATF Travel Rule, enhanced KYC/AML obligations, and sanctions lists create compliance obligations for centralized platforms where cryptocurrencies are converted into or out of traditional money. DeFi protocols, which often operate without identifiable operators, pose additional challenges, leading to experiments with onchain compliance filters, front-end geoblocking, and risk-scoring of wallet addresses. For legitimate actors, these developments underscore the importance of understanding not just how to obtain funding, but also how to demonstrate that funding sources and uses are compliant.

At the same time, overzealous enforcement or poorly designed regulations risk cutting off funding channels for civil society, privacy technology, and dissident movements that rely on crypto to bypass censorship and financial exclusion. This tension is vividly present in funding rounds for privacy-preserving tools like Tor, where donors may use cryptocurrencies to support anti-censorship infrastructure, and in debates over whether privacy-enhancing technologies should be treated as inherently suspicious. As crypto funding becomes more deeply intertwined with geopolitics and human rights, the question of whose funding is deemed legitimate and whose is not will remain contentious.

9. Funding Risk, Liquidity, And Market Cycles

Funding conditions in crypto are highly cyclical, mirroring broader macroeconomic trends yet often amplifying them. During bull markets, abundant venture capital, high token valuations, and expansive stablecoin yields create an environment in which both founders and traders can obtain funding cheaply. Perpetual futures funding rates tend to be positive and elevated, reflecting strong demand for leveraged long exposure that effectively subsidizes short sellers and basis traders. Stablecoin yields on both CeFi and DeFi platforms often spike as market-making, lending, and margin-trading activities expand, feeding a perception that high returns are normal and sustainable. In such phases, protocol treasuries grow, grants proliferate, and it becomes easier to finance ambitious long-shot projects in areas like DeSci or AI.

When the cycle turns, however, funding conditions tighten quickly. Token prices decline, venture investors retrench, and many high-yield lending platforms find themselves exposed to bad debt or liquidity mismatches, leading to defaults or restructurings. Perpetual funding rates compress or flip negative as traders hedge or short, and demand for leverage wanes. Stablecoin yields fall toward policy-rate levels or lower, exposing that much of the previous yield was tied to speculative activity rather than to sustainable spreads on safe assets. Protocols that had relied on ever-rising token valuations to fund development must re-evaluate their budgets, and discussions about sustainable funding mechanisms move to the forefront, as seen in Ethereum’s current debates about core development funding.

These cycles create both risks and opportunities. For conservative investors, understanding funding conditions can help avoid yield traps and mispriced risk—recognizing, for example, that a double-digit stablecoin yield during a risk-off period likely reflects concentrated credit exposure. For builders, cycles emphasize the importance of diversifying funding sources, including mixing equity, token allocations, revenue sharing, and grants, and of planning for multi-year runways that do not assume constant easy access to capital. For policymakers, the boom-and-bust pattern raises concerns about procyclicality in funding flows and about the potential for spillovers into traditional finance as stablecoins and tokenized assets become more integrated with bank funding markets.

10. How Builders And Users Should Think About Funding

For founders and protocol teams, funding decisions are strategic choices that shape governance, community alignment, and long-term resilience. Early in a project’s life, pre-seed and seed funding might come from angels, small funds, or grants programs, with equity or token warrants used to align incentives. As the project matures, larger rounds—Series A, B, or beyond—may bring in specialized crypto funds, strategic investors, or even traditional firms, as seen with Morpho’s institutional investor base. Token launches, whether through centralized exchanges, launchpads, or fair-launch mechanisms, can supplement or substitute venture funding, but they bring their own challenges around regulatory compliance and community expectations. The narrative that pre-seed funding is “dead” may be an overstatement, but it does reflect a shift toward more disciplined capital allocation and higher standards for investability.

For developers working on public goods and protocols, exploring alternative funding models such as quadratic funding, retroactive rewards, and MEV-based contributions can reduce dependence on a single foundation or benefactor. Participating in ecosystem grants, like those offered by Celo’s Prezenti program, can provide early runway while keeping control decentralized. At the same time, teams must be realistic about the limitations of such mechanisms and may need to combine them with more traditional revenue-generation strategies, such as fees, enterprise services, or partnerships, to achieve sustainability.

For users and investors, the central task is to understand what is being funded with their capital and on what terms. When depositing stablecoins on an exchange or DeFi protocol, they should ask whether yields are reserve-based or activity-based and what that implies about risk. When participating in cross-exchange funding arbitrage or structured products, they should recognize that the promised yield is another trader’s funding cost and that the spread can vanish if market conditions change. When supporting a quadratic funding round or public-goods grant, they should appreciate how their small contribution is amplified and how the matching pool is allocated. Across all these contexts, “funding” is not an abstract concept; it is the concrete mechanism through which capital, risk, and control are distributed in a system that aspires to be more open and programmable than its predecessors.

Outlook

Funding will remain the quiet power center of crypto, AI, and digital markets. As onchain repo, tokenized bonds, and stablecoin remuneration reshape wholesale and retail funding channels, and as public-goods mechanisms like quadratic funding and MEV redistribution mature, the question will be less whether capital is available and more whose values and incentives are embedded in its flow. For participants across the spectrum—from bitcoin miners and DeFi protocols to AI labs and privacy advocates—understanding funding structures is key to navigating both opportunity and risk in the next phase of the digital asset economy.

Latest Funding news

AI analytics platform Polysights raises $1.5M pre-seed funding to combat insider trading in prediction markets. The raise was backed by YZi Labs S3, Maven 11 Capital, and angels from Kraken and Consensys, plus grants from Polymarket and AWS.Book of Eth defends Ethereum Foundation's five-year record, citing The Merge, Dencun, public goods funding and scaling upgrades amid growing criticismTX3 Futures rolls out capital funding platform after $35M in payouts, as futures traders face growing competition and platform risk. Tokenized-equity perpetuals open rich new funding rate arbitrage lanes for savvy traders.

Tokenized-equity perpetuals open rich new funding rate arbitrage lanes for savvy traders.Sources

- https://www.coinbase.com/learn/perpetual-futures/understanding-funding-rates-in-perpetual-futures

- https://x.com/BSCNews/status/2067813370322129268

- https://x.com/pendle_fi/status/2068001118412779735

- https://www.bis.org/publ/bisbull125.pdf

- https://www.prnewswire.com/news-releases/hifi-drw-and-marex-advance-onchain-repo-on-the-canton-network-302802300.html

- https://x.com/ethereum/status/2067998361693696303

- https://x.com/DeSciBerlin/status/2067625061247279307

- https://x.com/solsticefi/status/2067535773830926820

- https://www.theinformation.com/articles/kalshi-passes-2-billion-annualized-revenue-early-ipo-talks

- https://www.upi.com/Top_News/World-News/2026/06/11/KB-Kookmin-Bank-blockhain-digital-bond/7561781100332/

- https://fortune.com/2026/06/09/morpho-fundraise-a16z-crypto-paradigm-ribbit-capital-175-million/

- https://www.fleetowner.com/resources/white-papers/whitepaper/55365505/guide-to-protecting-your-agency-with-unified-fleet-safety-data

- https://www.instagram.com/reel/C5vbpy5B4c_/?hl=en

- https://news.crunchbase.com/venture/us-ai-startup-funding-boom-data/

- https://x.com/Celo/status/2066620906898927846

- https://finematics.com/quadratic-funding-explained/

- https://gitcoin.co/research/mev-for-public-goods-funding

- https://stokr.io/stoke-post/bitcoin-miner-financing-part-2

- https://www.federalreserve.gov/econres/notes/feds-notes/banks-in-the-age-of-stablecoins-implications-for-deposits-credit-and-financial-intermediation-20251217.html

Community notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…