Deep explainer on Series A funding in crypto, unpacking structures, preferred stock, dilution, and recent stablecoin, payments, AI and UK deals to show how venture capital now backs Web3’s core financial infrastructure.

- x.com4

- theblock.co3

- businesswire.com1

- cointelegraph.com1

- mena.entrepreneur.com1

- 4pillars.io1

- blockworks.com1

+5 sources across the wider coverage universe

Pharos Network raises $44M Series A backed by Sumitomo, Chainlink, and Flow Traders to build financial-grade infrastructure bridging TradFi and DeFi globally2026-04

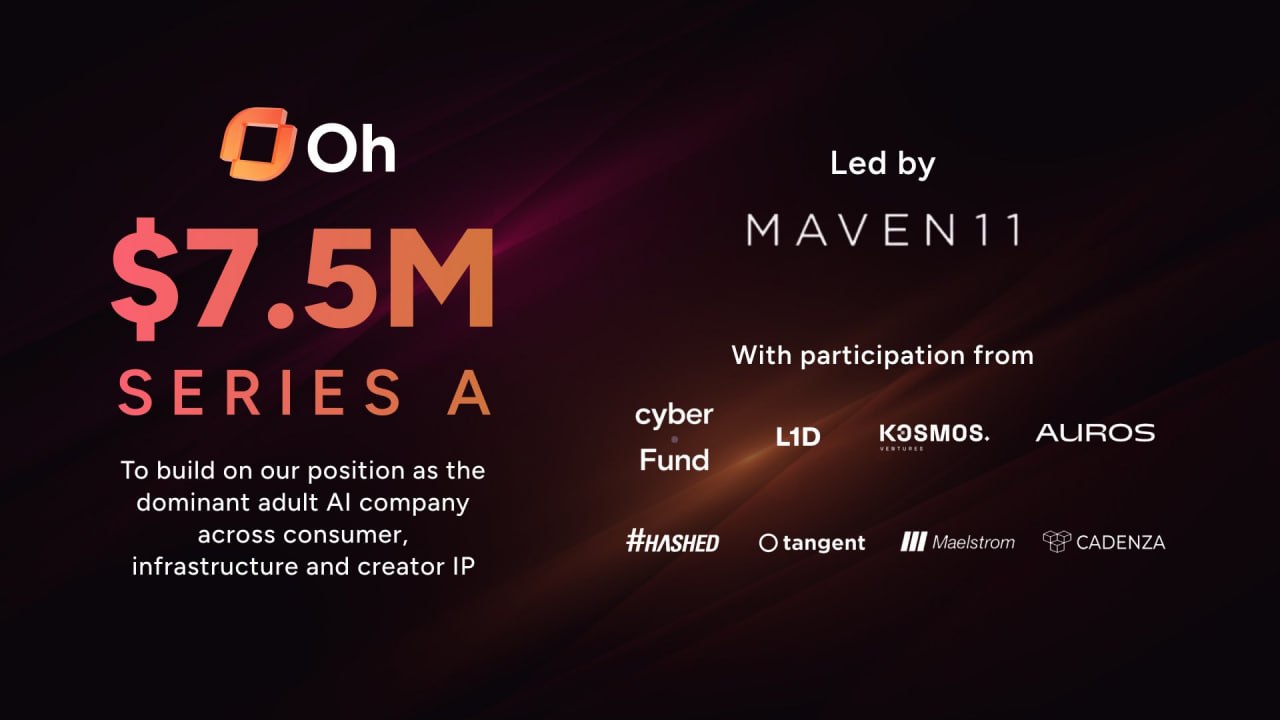

Pharos Network raises $44M Series A backed by Sumitomo, Chainlink, and Flow Traders to build financial-grade infrastructure bridging TradFi and DeFi globally2026-04 Oh hauls in $7.5m series A anchored by Maven 11, reaching $12m total with L1D, Auras, Hashed, Maelstrom, Cadenza and seed backers.2026-04

Oh hauls in $7.5m series A anchored by Maven 11, reaching $12m total with L1D, Auras, Hashed, Maelstrom, Cadenza and seed backers.2026-04 Paradigm leads El Dorado's $9M Series A as the LatAm payments app scales to 100K+ users, targeting a cross-border payments market estimated at up to $1T annually2026-06

Paradigm leads El Dorado's $9M Series A as the LatAm payments app scales to 100K+ users, targeting a cross-border payments market estimated at up to $1T annually2026-06 Trace Finance raises $32M Series A as stablecoin payments push takes valuation 10x above seed2026-06

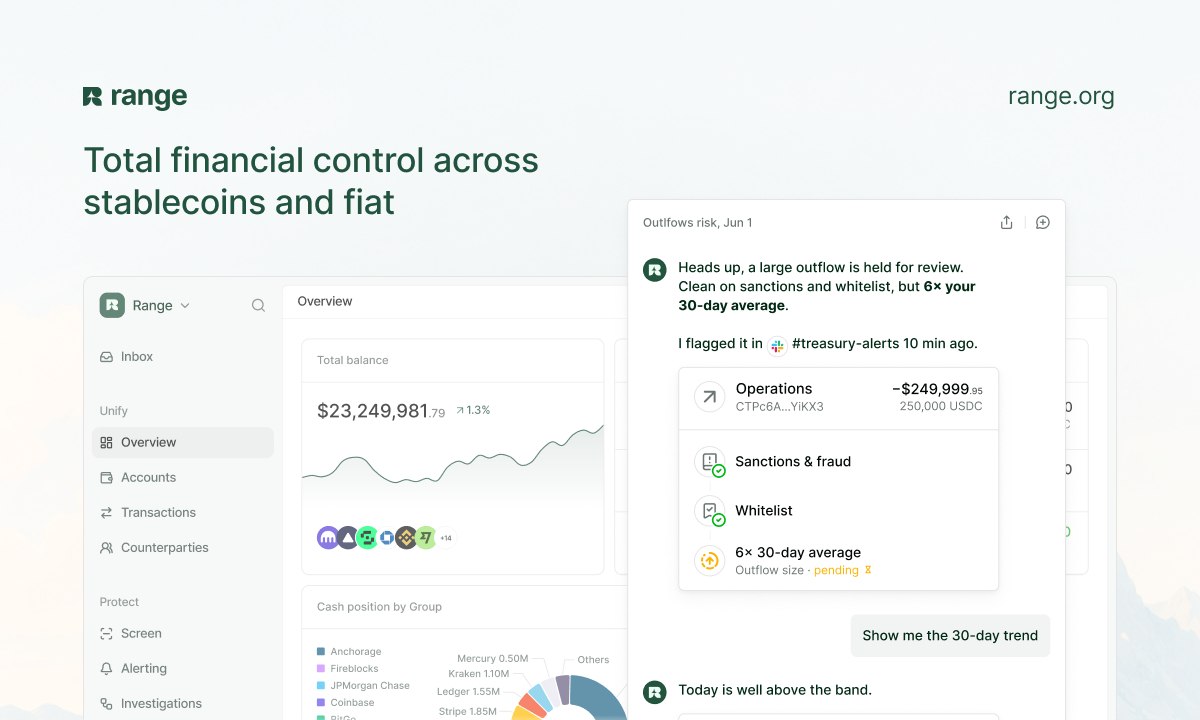

Trace Finance raises $32M Series A as stablecoin payments push takes valuation 10x above seed2026-06 Range raises $8.3m series A to chart unified treasury, risk and compliance across stablecoin and fiat waters2026-06

Range raises $8.3m series A to chart unified treasury, risk and compliance across stablecoin and fiat waters2026-06 Onramp raises Series A at $135M valuation led by Early Riders to expand financial platform built on multi-institution custody.2026-05

Onramp raises Series A at $135M valuation led by Early Riders to expand financial platform built on multi-institution custody.2026-05

Series A Funding in Crypto: An Evergreen Explainer

Series A is the first major institutional equity funding round for a startup after its seed stage, typically involving the sale of preferred shares to venture investors at a negotiated valuation. In crypto and Web3, Series A has become the moment when experimental ideas are expected to harden into regulated infrastructure, real revenue, and institutional‑grade products.

What “Series A” Actually Means

In traditional venture capital, the label “Series A” refers both to a financing milestone in a company’s life and to the class of shares issued in that round. Series A funding generally arrives once a startup has moved beyond a prototype or proof of concept and can demonstrate early product‑market fit, usage, and a path to scalable revenue. Unlike pre‑seed or seed rounds, which often rely on convertible instruments such as SAFEs or notes, Series A is usually a priced equity round in which investors buy a specific number of preferred shares at an agreed price, anchoring the company’s valuation.

The origin of the term is simple but important. When a company first sells preferred stock to outside investors in a priced round, that security is typically labeled “Series A Preferred.” If the company raises more institutional capital later, it issues new classes such as Series B or Series C preferred shares, each with its own set of rights and obligations. In practice, founders and investors use “Series A” as shorthand both for that first institutional round and for a general level of maturity: an organization that has outgrown the seed stage but is not yet at late‑stage growth.

In crypto and Web3, this conventional structure has mostly been imported wholesale from mainstream venture capital, but with important twists. Many crypto startups maintain dual capital structures, issuing equity to shareholders while also planning or maintaining a token that confers network access or governance rights. Series A equity rounds in crypto often occur alongside, or in anticipation of, token warrants, SAFTs, or other instruments that promise future token allocations. This duality makes understanding the equity side—what “Series A” means from a corporate and legal standpoint—especially important for teams, investors, and token holders.

The term “Series A” can also appear in public‑markets contexts that have nothing to do with early‑stage venture. Bitmine Immersion Technologies, a listed company that has become one of the largest holders of Ether, recently closed a 9.50% Series A Perpetual Preferred Stock offering on the NYSE, raising roughly 273.8 million dollars to expand its Ethereum treasury and fund its staking platform. That capital raise used the “Series A” label for a class of income‑bearing preferred shares rather than an early‑stage VC round, showing how the same nomenclature can describe very different transactions depending on context.

Understanding these nuances is essential for a crypto audience. In most news about Web3 startups, “Series A” still means the canonical first big venture equity round. Yet for token‑heavy or public companies, it may instead reference a particular preferred security in the capital stack. The rest of this explainer focuses on Series A in its traditional venture sense, with reference to how that structure interacts with crypto‑native business models, tokens, and the rapidly evolving stablecoin and digital‑asset ecosystem.

Upscale AI charts a $190M extension to its Series A, bringing total haul to half a billion

$500M into open-standard AI fabric is a bet that the rent in AI infra moves toward interconnects once GPU supply stops being the only choke point. Crypto has seen this movie with MEV, sequencers, and DA: the coordination layer starts as plumbing, then becomes the toll booth. If UALink, Ultra Ethernet, and ESUN make it into production clusters, neoclouds get a path out of single-vendor NVLink/InfiniBand gravity; if they stall, this becomes another expensive shovel vendor circling Nvidia’s stack.

Readers click Series A crypto deals primarily as a signal of which top-tier VC names (Paradigm, Pantera, Dragonfly, Sumitomo) are making directional bets on payments and infrastructure verticals — the investor roster, not the raise size, is the actual information being consumed.↗

From Seed to Series A: The Venture Capital Progression

The journey to a Series A round is best understood against the backdrop of the broader venture funding ladder. Early in a startup’s life, financing usually comes from founders’ savings, friends‑and‑family capital, and small angel or pre‑seed checks. These rounds often rely on simple, flexible instruments such as SAFEs or convertible notes, delaying a formal valuation until later. Seed rounds, which have grown larger in recent years, mark the point at which professional early‑stage investors typically get involved, funding the transition from an idea or prototype toward a product that real users can touch.

Series A is the point where the company’s story is expected to shift from possibility to proof. Venture literature describes Series A as the first institutional or “priced” round after the seed stage. By this time, startups are typically expected to have a functioning product, early traction metrics such as active users or revenue, and evidence that the underlying market is large enough to support a venture‑scale outcome. For crypto founders, this usually means more than on‑chain activity metrics; it increasingly involves revenue from real‑world clients, regulatory registrations or licenses, and enterprise‑grade reliability.

With each successive equity round—Series A, B, C, and beyond—the company issues new preferred stock classes, raising larger sums to fuel expansion, internationalization, and eventual exit via acquisition or public listing. In crypto markets, these later rounds often coincide with major protocol milestones, such as mainnet launches, token distributions, or expansion into new onchain verticals like stablecoins, derivatives, or tokenized real‑world assets. As the company matures, the legal, regulatory, and capital‑structure complexity also increases, making the initial Series A terms consequential far beyond the moment of fundraising.

Crypto has not been immune to macro cycles in venture activity. In Q4 2024, venture capitalists invested roughly 3.5 billion dollars into crypto and blockchain‑focused startups across 416 deals, representing a 46% quarter‑over‑quarter increase in capital even as the number of deals declined by 13%. This pattern—fewer deals, larger average round sizes—suggests that capital has concentrated in more mature, traction‑heavy companies, including those raising Series A rounds off a base of real usage and revenue. It contrasts sharply with the 2021 era, when pre‑product or token‑only projects sometimes raised large sums at high valuations purely on speculative narratives.

In the UK, a key jurisdiction for both fintech and digital assets, the broader venture landscape has remained relatively robust. UK startups raised approximately 17.2 billion dollars across 1,847 funding rounds in 2025, a roughly 12% increase over 2024, maintaining the country’s position as Europe’s largest venture market by attracting about 40% of all European startup funding. While this figure spans all sectors, not just crypto, it underscores the depth of capital available for UK‑based Web3 firms raising Series A rounds, including those building blockchain infrastructure, trading platforms, and tokenization tools.

For founders planning their fundraising journey, the key takeaway is that Series A sits at the intersection of proof and potential. To reach it, teams must move beyond speculative excitement and demonstrate that their technology can operate as part of real financial plumbing, whether in stablecoin settlement, cross‑border payments, institutional DeFi, or AI‑enabled operational intelligence. Once that threshold is crossed, however, Series A capital can be the catalyst that transforms a promising crypto idea into a durable piece of global financial infrastructure.

How a Series A Round Is Structured

The structural heart of a Series A round is the issuance of preferred stock to investors at a negotiated price per share, embedding explicit terms that allocate risk and reward between founders, employees, and capital providers. Unlike common stock, which is typically held by founders and employees, preferred stock carries special rights and protections designed to mitigate investor risk in high‑growth, high‑failure environments. In crypto startups, where regulatory outcomes and market cycles can be particularly volatile, these protections often play a decisive role in whether institutional capital is willing to engage.

Preferred stock granted in a Series A round usually sits above common stock in the liquidation stack, meaning that preferred holders are paid back before common shareholders if the company is sold or wound down. One of the central parameters is the liquidation preference, often expressed as a multiple of the original investment. A “1x non‑participating” preference lets investors choose either to get their money back or to convert their preferred shares into common and share pro‑rata in the exit proceeds, whichever yields more. By contrast, participating preferred allows investors to “double dip,” first recouping their initial investment and then also participating alongside common shareholders in the remaining proceeds, which can significantly reduce the upside left for founders and employees.

Series A rounds are typically the first point at which these terms are carefully negotiated, because earlier seed investments may rely on standardized documents that defer such details. Venture practitioners emphasize that each priced equity round—seed or Series A—creates new preferred shares and dilutes existing shareholders. This dilution is not inherently negative; it is the mechanism that brings in new capital and partners. But when stacked across multiple rounds with aggressive preferences or anti‑dilution clauses, it can erode common shareholders’ eventual stake in the outcome.

Another important structural dimension of Series A is governance. Investors in a lead position often secure one or more board seats, veto rights over major corporate actions, and information rights to oversee the company’s progress. In crypto startups deploying complex token or protocol roadmaps, governance provisions may intersect with decisions about token issuance, protocol upgrades, and revenue‑sharing arrangements. Although these protocol‑level decisions are often presented as decentralized or community‑driven, the underlying corporate entity that develops and markets the protocol remains subject to the board and shareholder agreements negotiated at Series A.

Against this backdrop, the example of Bitmine’s NYSE‑listed Series A Perpetual Preferred Stock helps clarify what Series A is—and is not—in different contexts. Bitmine’s offering involved a fixed‑dividend preferred security yielding 9.5%, raising approximately 273.8 million dollars to expand the company’s Ethereum holdings to about 5.62 million ETH and fund its MAVAN staking platform, with weekly preferred dividends promised to investors. While labeled “Series A,” this transaction is a capital markets financing for an established company, distinct from a venture Series A round that sets an early‑stage startup’s valuation and governance structure. For crypto readers, recognizing this distinction is crucial when parsing headlines: the same words can describe either a high‑yield income instrument or a classic VC milestone.

Crypto founders contemplating a Series A must therefore think in three layers. At the legal level, they are issuing preferred equity with specific rights that will govern their company for years. At the financial level, they are fixing a valuation and dilution percentage that determine how ownership is shared between founders, employees, and investors. At the strategic level, they are choosing partners who will shape the company’s token strategy, regulatory posture, and go‑to‑market choices, often in markets as sensitive as stablecoin payments, derivatives, or AI‑driven financial infrastructure.

- 01Payments infrastructure arms race↗

Multiple high-clicked rounds (Fun $72M, El Dorado $9M, Trace Finance $32M, Edge Markets $29.2M) all target cross-border stablecoin or fiat rails, signaling readers see payments as the defining battleground for this funding cycle.

- 02Marquee VC backing as directional signal↗

Paradigm on El Dorado, Pantera on Four Pillars, Dragonfly on Variational — readers clicked these specifically because the investor name telegraphs conviction about which subsector will win, not merely that a deal closed.

- 03Crypto data layer consolidation↗

Blockworks at $192M valuation explicitly betting on rolling up fragmented onchain data drew strong clicks as an infrastructure monopoly play, echoing the Messari acquisition story.

- 04TradFi-DeFi bridge infrastructure↗

Pharos Network's $44M round backed by Sumitomo and Chainlink positioning as 'financial-grade infrastructure' attracted clicks from readers tracking institutional entry points into DeFi.

- 05Geographic frontier expansion↗

El Dorado targeting a $1T LatAm cross-border market, Trace Finance scaling Brazil-U.S. rails, and Hata in Malaysia drew clicks as readers tracked where crypto payments adoption is actually happening outside Western markets.

- 06Choppy market fundraising conditions

Fun's headline explicitly naming 'storm clouds' over crypto payments resonated because it acknowledged the fundraising difficulty narrative rather than spinning the round as a triumph.

Preferred Stock, Dilution, and Investor Protections

To understand the stakes of a Series A negotiation, it is useful to look more closely at the mechanics of preferred stock and equity dilution. Preferred stock, as startup banking guides emphasize, is exactly what it sounds like: it gives its holders preferential treatment over common shareholders in specific situations, especially liquidity events and dividend payments. That preferential treatment is not monolithic; it is defined by detailed term sheets that can vary widely between deals and investors. However, certain patterns are common enough to be considered standard in venture‑backed Series A rounds.

Liquidation preferences sit at the center of these protections. A typical crypto infrastructure startup might raise a Series A with a 1x non‑participating preference, meaning investors are entitled to get back their invested capital before common shareholders receive anything if the company exits for a modest amount. For example, if a startup raises 20 million dollars at Series A and later sells for 25 million dollars, Series A investors would generally be entitled to their 20 million back first; the remaining 5 million would then be distributed to common shareholders unless investors choose to convert, in which case distribution would follow ownership percentages. Participating preferred stock strengthens this protection: investors receive their 20 million first and then participate pro‑rata in the remaining 5 million, effectively taking a larger share of the upside.

Anti‑dilution provisions are another critical term. These clauses adjust the conversion price of preferred shares if the company later issues new equity at a lower valuation, commonly known as a “down round.” While various formulas exist, from weighted average to full ratchet, their effect is to shield Series A investors from some of the economic impact of subsequent rounds that price the company below its Series A valuation. In crypto, where market cycles can be sharp and regulatory shocks can trigger sudden repricing, the probability of down rounds is not negligible, making anti‑dilution terms particularly salient.

Equity dilution itself is unavoidable in venture. As one venture firm’s founder guide notes, priced equity rounds—seed or Series A—are the most visible source of dilution, because the company creates new preferred shares and expands its overall share count. Founders who begin with 100% equity will own progressively less as each round adds new investors; employees, too, see their relative stake reduced as the option pool is sized and resized. The goal is not to avoid dilution altogether but to ensure that the growth in company value more than offsets the reduction in percentage ownership, leaving everyone better off in absolute terms.

To illustrate the dynamics, consider a simplified cap table before and after a Series A round. Suppose a crypto startup is initially owned 80% by founders and 20% by an employee pool. If it raises a Series A that sells 25% of the post‑money equity to new investors, the founders’ stake might fall to 60%, the employee pool to 15%, and the Series A investors would hold 25%. In return, the company receives the capital it needs to build out a stablecoin settlement network, institutional DeFi platform, or AI‑powered compliance engine. The trade‑off is clear: more capital and partners, less relative control and economic upside.

Series A terms also often include dividend provisions, though in high‑growth startups these are usually non‑cumulative and rarely paid in cash. Some preferred stock structures, especially in public‑market offerings like Bitmine’s, include cumulative dividends, requiring that unpaid dividends accumulate and be satisfied before any distributions to common shareholders. In early‑stage private crypto companies, cumulative dividends are less common, but their presence can further tilt the economic balance toward preferred holders. For founders, understanding each of these elements—preference, participation, anti‑dilution, dividends, and governance—is essential before signing a Series A term sheet.

Because of this complexity, practitioner advice consistently emphasizes that founders should not approach Series A negotiations alone. Bankers and lawyers urge founders to consult experienced advisors, understand liquidation scenarios, and model how their ownership and payout could evolve under different exit outcomes. In crypto, this modeling must also incorporate token economics, because investors may hold both equity and token rights. A structure that looks acceptable when reviewing only equity may look much less favorable when token allocations and vesting schedules are added to the picture.

Sports prediction app Onyx Odds raises $20M Series A at $220M valuation, with Kraken parent Payward leading the round and integrating crypto trading infrastructure

Onyx claiming nearly 1M users on less than $8M raised before this round makes the $220M tag less weird: Payward is buying a sports-native funnel into a CFTC-registered FCM/DCM plus Kraken crypto rails. Kalshi at $22B and Schwab/Cboe moving into binary options means distribution is about to compress margins; Onyx wins only if Payward's licensed stack lets it ship markets and spot/derivatives flows faster than state-by-state sportsbook incumbents can litigate. If sports outcomes become the top-of-funnel and crypto trading sits one tap away, Kraken gets a Robinhood-style growth loop without paying pure exchange CAC.

Series A in the Crypto, Stablecoin, and Payments Ecosystem

While the legal mechanics of Series A are largely sector‑agnostic, the types of companies raising Series A rounds in crypto reveal where capital believes the next generation of financial infrastructure is being built. Over the past few years, a clear concentration of Series A activity has emerged around stablecoin infrastructure, cross‑border payments, compliance tooling, trading and derivatives, and data and analytics.

Stablecoins have evolved from a niche DeFi primitive to a core piece of global financial plumbing. Between December 2018 and late 2025, total stablecoin supply climbed from roughly 3 billion dollars to about 265 billion, reflecting their rapid adoption as a medium for trading, remittances, and onchain settlement. Legal and advisory firms tracking digital assets argue that stablecoins increasingly function as the pipes of global finance, powering cross‑border payments, real‑time settlement, and T+0 clearing for businesses rather than just speculative trading. Industry analysts now project that stablecoin circulation could surpass 1 trillion dollars by 2026, driven largely by corporate treasury modernization and enterprise use cases rather than retail speculation.

This backdrop explains why a company like Trace Finance—a regulated infrastructure provider for cross‑border payments and stablecoin settlement across Brazil, the United States, and emerging markets—was able to raise a 32 million dollar Series A led by prominent crypto investors. Trace combines local payment rails, Brazil’s Pix system connectivity, banking infrastructure, and stablecoin‑enabled settlement to help enterprises and exchanges move money through complex markets at institutional scale, having already processed over 10 billion dollars in cross‑border volume. Its Series A capital is earmarked for scaling transaction capacity, expanding into new corridors, and deepening capabilities in foreign exchange, bank connectivity, compliance, and stablecoin settlement. This is exactly the kind of “financial plumbing” play that aligns with the stablecoin adoption narrative articulated by legal analysts.

Another example is Range, a platform that helps companies manage treasury, risk, and compliance across both stablecoins and traditional currencies. Range raised an 8.3 million dollar Series A in what its backers described as one of the toughest fundraising markets crypto has faced, bringing its total funding to 11 million dollars. The round attracted both traditional fintech funds and crypto‑native investors, underscoring how stablecoin‑related infrastructure now sits at the intersection of old and new finance. Range plans to use the capital to deepen its product, expand engineering and go‑to‑market teams, and extend coverage across more networks and integrations, essentially building the connective tissue that allows corporates and fintechs to operate seamlessly across fiat and stablecoin ecosystems.

Cross‑border consumer and B2B payments are another hotspot. El Dorado, a Latin American cross‑border payments app, secured a 9 million dollar Series A led by Paradigm, with participation from Coinbase Ventures and others, as it scales to hundreds of thousands of users and targets a regional remittances and payments market measured in the hundreds of billions of dollars annually. Although not all of this activity runs on crypto rails today, the strategic bet is that stablecoins and blockchain networks will increasingly underpin the settlement layer, especially in corridors plagued by high fees and slow correspondent banking. Series A capital in these companies is funding not just user growth but the connective infrastructure necessary to route value between traditional banking systems and stablecoin networks.

The following table illustrates, at a high level, how some recent Series A deals map onto key crypto and fintech verticals, based on public disclosures.

| Company | Round Size (USD) | Core Vertical | Geography |

|---|---|---|---|

| Trace Finance | 32M | Stablecoin settlement & cross‑border FX | Brazil / U.S. |

| Range | 8.3M | Treasury, risk & compliance (fiat/crypto) | Switzerland / global |

| El Dorado | 9M | Cross‑border payments app | Latin America |

| EDGE Markets | 29.2M | Payment rails for gaming & prediction | United States |

| Variational | 50M | Decentralized derivatives trading | UK / global |

| Pharos | 44M | Financial‑grade blockchain infrastructure | UK / global |

| Billables AI | 10.2M | AI‑driven operational intelligence | United States |

| Blockworks | n/a (extension) | Crypto data and analytics | United States |

Trace Finance’s and Range’s Series A rounds show how investors are backing the mid‑layer infrastructure that corporates, exchanges, and fintechs need to safely integrate stablecoins into their operations. El Dorado’s raise illustrates the consumer‑facing layer where user experience, regional regulatory compliance, and remittance economics intersect. EDGE Markets’ nearly 30 million dollar Series A, which supports payment rails in gaming, crypto, and prediction markets, highlights another edge of the same network: alternative markets that depend on fast, reliable, programmable payments infrastructure to function at scale.

Series A activity also extends into AI‑adjacent and operational intelligence plays that, while not purely crypto, are increasingly relevant to firms operating in digital‑asset markets. Billables AI, for instance, raised about 10.2 million dollars in a Series A to build an AI‑native operational intelligence platform for law firms. Its tools aim to optimize workflows, billing, and analytics in a highly regulated, document‑heavy domain—capabilities that overlap with the needs of crypto compliance, investigations, and institutional trading desks that must manage large volumes of legal and operational data. The convergence of AI and crypto is likely to deepen as regulators demand more robust surveillance and as onchain data becomes more complex.

Data and analytics themselves are another focus area. Blockworks, a New York‑based crypto data platform, closed a Series A extension at a 192 million dollar valuation, led by ParaFi and Reciprocal Ventures, with the goal of scaling its crypto data and analytics capabilities and building an onchain market‑data layer. In an ecosystem where real‑time, high‑quality data on tokens, protocols, and onchain activity is essential for both retail and institutional participants, Series A‑stage funding for data providers reflects a recognition that information is as critical an input as capital.

On the institutional trading side, Variational, a decentralized derivatives trading protocol, raised 50 million dollars in a Series A led by Dragonfly, with participation from Bain Capital Crypto, Coinbase Ventures, and others. The company is building onchain derivatives infrastructure that aims to serve both sophisticated traders and institutional liquidity providers, showing how Series A capital is being deployed to harden DeFi primitives into institutional‑grade platforms. Here, the focus is on risk management, latency, and composability rather than consumer UX, but the pattern is similar: Series A funding is underwriting the leap from early‑adopter experimentation to robust, scaled systems.

Taken together, these examples demonstrate that Series A in crypto has become less about speculative token bets and more about critical infrastructure: stablecoin rails, cross‑border payment networks, derivatives venues, data layers, AI‑enhanced tooling, and compliance platforms. Investors appear to be funding the building blocks of a future financial system in which digital assets and traditional finance converge.

Crypto VC deal count rebounds after 2023 trough

Crypto exits surge; Series A momentum builds industry-wide

Paradigm leads El Dorado $9M Series A for LatAm payments

Pharos Network closes $44M Series A with Sumitomo and Chainlink

Trace Finance raises $32M Series A led by CoinFund for stablecoin rails

Edge Markets raises $29.2M Series A for prediction and gaming payment rails

Blockworks extends Series A at $192M valuation, acquires Messari data assets

Jurisdictions, Regulation, and the UK as a Series A Hub

Jurisdictional dynamics play an increasingly important role in where and how crypto companies raise Series A rounds. The United Kingdom offers a good illustration, combining deep venture capital markets with a rapidly evolving digital‑assets regulatory framework. As noted earlier, UK startups collectively raised about 17.2 billion dollars across nearly 1,850 rounds in 2025, cementing the country’s role as Europe’s leading VC hub and attracting around 40% of all European startup funding. This pool of capital is highly relevant to crypto companies, especially those that fit within the UK’s strong fintech and capital‑markets heritage.

On the regulatory side, the UK has been methodically building a bespoke framework for digital assets. In April 2025, HM Treasury published a draft statutory instrument that would introduce new regulated activities for cryptoassets under the Financial Services and Markets Act, laying the groundwork for a more comprehensive regime. Legal analyses of this draft note that it seeks to bring a broad range of crypto activities—such as operating a trading venue, dealing in cryptoassets, and providing custody—within the perimeter of UK financial regulation, with the aim of aligning consumer protection and market integrity standards with those in traditional finance. For Series A‑stage crypto startups, this means that building from within the UK increasingly involves designing products, governance, and compliance processes that anticipate full regulatory oversight from day one.

This environment helps explain why companies like Pharos Network, a blockchain firm building financial‑grade infrastructure that bridges traditional finance and DeFi, have chosen to base themselves in the UK while raising substantial Series A rounds backed by both corporates and crypto‑native investors. Pharos raised 44 million dollars in Series A funding backed by Sumitomo Corporation’s corporate venture arm, Chainlink, and Flow Traders, positioning itself at the intersection of institutional capital markets and onchain finance. The company’s focus on building infrastructure that satisfies the requirements of banks, broker‑dealers, and asset managers aligns with the UK’s push to regulate crypto within its existing financial‑services architecture.

The UK is not alone. In Latin America, regulatory and market conditions are also shaping Series A trajectories. Brazil, for instance, has one of the world’s most sophisticated real‑time payments systems in Pix, alongside complex foreign‑exchange and compliance requirements. Trace Finance’s decision to build a regulated infrastructure stack that combines local Brazilian payment rails, FX, banking connectivity, compliance operations, and stablecoin settlement reflects a strategy tailored to that environment. Its 32 million dollar Series A round is both a bet on Brazil’s role as a financial hub for emerging markets and a response to increasing regulatory clarity around stablecoin and digital‑asset use in cross‑border flows.

In the Middle East and Asia, corporate and sovereign investors are also backing Series A‑stage blockchain infrastructure. Japanese conglomerate Sumitomo’s participation in Pharos’ 44 million dollar Series A underscores how corporate venture capital is increasingly active in Web3, often seeking strategic synergies rather than purely financial returns. This pattern is likely to intensify as more large financial institutions and corporates explore tokenization, onchain settlement, and programmable money.

These jurisdictional factors feed back into Series A structure and valuation. Startups that can credibly operate within clear regulatory frameworks, obtain licenses, and show that their products align with upcoming regimes—such as the UK’s cryptoasset rules under FSMA—may find it easier to raise larger, higher‑quality Series A rounds. Conversely, companies that rely on regulatory arbitrage or operate in gray zones may face higher costs of capital, more onerous investor protections, or difficulty attracting top‑tier institutional investors.

For founders, the implication is straightforward but demanding. Series A is no longer just a question of market traction and technology; it is also a referendum on jurisdictional and regulatory strategy. Choosing where to incorporate, where to seek licenses, and how to design governance so that it can evolve with regulation are all part of the Series A investment thesis, particularly in sectors like stablecoins, exchanges, and tokenized assets.

Market Cycles, Extensions, and the Evolution of Series A Terms

Series A rounds do not exist in isolation from broader crypto and macroeconomic cycles. The spike in venture capital deployment into crypto and blockchain in Q4 2024—3.5 billion dollars across 416 deals, up 46% in capital terms even as deal counts fell—occurred after a prolonged downturn following the 2021‑2022 boom and subsequent market stress events. This rebound suggests that investors have become more selective, concentrating capital in fewer, stronger projects that have weathered the bear market and built meaningful traction.

One visible adaptation to volatile conditions has been the proliferation of Series A extension rounds. Blockworks’ Series A extension, which valued the company at 192 million dollars, exemplifies this pattern: rather than leaping immediately to a Series B, the company chose to extend its Series A, adding capital while largely preserving its existing valuation structure. Extensions can provide breathing room in uncertain markets, allowing companies to hit new milestones before pricing a full up‑round. They can also soften the potential reputational and economic impact of down rounds, which trigger anti‑dilution protections and can erode employee morale.

Market conditions also influence the balance of power in Series A term negotiations. In frothy markets, founders may be able to insist on clean 1x non‑participating preferences, limited anti‑dilution, and founder‑friendly governance structures. In tougher environments—like the “hardest fundraising markets crypto has seen,” as described in coverage of Range’s oversubscribed 8.3 million dollar Series A—investors may be able to negotiate more protective terms or require stronger evidence of revenue and compliance readiness. The pendulum between founder‑friendly and investor‑friendly terms is not fixed; it swings with liquidity conditions, risk appetite, and regulatory uncertainty.

Stablecoins and interest‑rate regimes add another macro layer. As legal analysts point out, stablecoins are increasingly used by enterprises for cross‑border payments and real‑time settlement, and their overall circulation is projected to surpass 1 trillion dollars by 2026. At the same time, traditional yields on cash and short‑term instruments have remained elevated compared to the ultra‑low‑rate environment of the late 2010s. This combination has encouraged both corporates and crypto firms to treat stablecoins as part of active treasury management, seeking yield through onchain mechanisms or tokenized T‑bills, while also using them as operational settlement assets. Startups that can help institutional clients navigate this environment—by unifying treasury, risk, and compliance across fiat and stablecoins, as Range aims to do—are well positioned to justify substantial Series A valuations.

In parallel, Series A capital is also flowing into companies that help manage the risks of this new environment. AI‑powered platforms for legal and operational intelligence, such as Billables AI’s law‑firm‑focused tools, address the growing complexity of compliance, contract management, and workflow optimization in sectors that increasingly touch digital assets. Prediction‑market and gaming payments rails, like those built by EDGE Markets, respond to demand for specialized payment infrastructure capable of handling high‑frequency, programmable, and often cross‑jurisdictional flows. These businesses are not merely riding a speculative wave; they provide the scaffolding needed for digital‑asset markets to function safely and efficiently at scale.

For investors, the evolution of Series A deal terms and targets reflects a shift from narrative‑driven token bets to infrastructure‑centric equity bets. The focus has moved toward companies that can survive and grow across multiple crypto market cycles, generate sticky revenue from institutional clients, and operate within or alongside emerging regulatory frameworks. In this environment, Series A remains the pivotal point at which investors decide which projects graduate from experimentation to institutional relevance.

Multiple rounds in 2026 explicitly acknowledge 'choppy waters' and difficult conditions; down-rounds and extended timelines are live risks for companies that raised seed at peak valuations.

Stablecoin payments startups (Trace, Edge Markets, El Dorado) face rapidly shifting compliance requirements across jurisdictions — Brazil, U.S., and Malaysia each have distinct licensing regimes that could gate operations.

Instant-liquidity-layer products like Midas's $50M bet depend on sustained onchain volume and tokenized asset adoption that remains nascent; a demand shock could strand infrastructure built ahead of the curve.

Multi-institution custody (Onramp) and data-layer consolidation (Blockworks) create single points of failure and concentration risk that contradict decentralization principles core to DeFi's value proposition.

Financial-grade infrastructure projects (Pharos, Variational derivatives) introduce complex settlement logic bridging TradFi and DeFi; a single contract bug at this layer propagates across all integrated protocols.

Series A preferred stock terms (participation rights, liquidation preferences) are standard but compressible in down-round scenarios; startups like Trace Finance with 10x seed-to-A valuation jumps carry higher ratchet exposure.

Outlook

Looking ahead, Series A rounds in crypto and Web3 are likely to cluster even more tightly around three themes: regulated infrastructure, stablecoin and payments rails, and the intersection of AI, data, and onchain finance. As stablecoin circulation continues to rise and enterprises integrate digital assets into their treasury and operations, demand for platforms like Trace Finance and Range—those that unify bank connectivity, FX, compliance, and stablecoin settlement—is expected to grow, supporting larger and more competitive Series A rounds. Jurisdictions such as the UK, which are building comprehensive digital‑asset regulatory frameworks while hosting deep venture markets, will remain important hubs for Series A‑stage blockchain infrastructure companies like Pharos and Variational.

At the same time, founders should expect Series A expectations to remain high. Investors will look for evidence of real product‑market fit, regulatory and compliance readiness, durable business models, and the ability to navigate both token and equity capital structures responsibly. Preferred stock terms, liquidation preferences, and anti‑dilution protections will continue to matter, especially in a sector where market and regulatory shocks can test even well‑capitalized projects. The projects that successfully raise and deploy Series A capital over the coming cycles are likely to be those that treat crypto not as a speculative playground but as a set of tools for rebuilding financial and data infrastructure on a global scale.

Latest Series A news

Sources

- https://www.investopedia.com/articles/personal-finance/102015/series-b-c-funding-what-it-all-means-and-how-it-works.asp

- https://qubit.capital/blog/series-a-e-funding-rounds

- https://www.galaxy.com/insights/research/crypto-blockchain-venture-capital-q4-2024

- https://www.startupticker.ch/en/news/usd-8-3m-to-unify-treasury-risk-and-compliance-across-stablecoins-and-traditional-currencies

- https://www.businesswire.com/news/home/20260617597265/en/Trace-Finance-Raises-$32M-Series-A-Led-by-CoinFund-to-Scale-Regulated-Banking-and-Stablecoin-Infrastructure-Across-Brazil-U.S.-and-Emerging-Markets

- https://app.dealroom.co/news/note/paradigm-leads-9m-series-a-in-el-dorado

- https://billables.ai/blog/billables-ai-raises-10-million-series-a-to-accelerate-ai-powered-operational-intelligence-for-law-firms

- https://www.prnewswire.com/news-releases/edge-markets-raises-29-2-million-series-a-funding-round-302793671.html

- https://simplywall.st/stocks/us/software/nyse-bmnr/bitmine-immersion-technologies/news/bitmines-ethereum-treasury-expansion-and-high-yield-preferre

- https://x.com/WuBlockchain/status/2062307212576612516

- https://www.thesaasnews.com/news/blockworks-acquires-messari-to-build-onchain-market-data-layer-kucoin/

- https://x.com/pharos_network/status/2041850490078818490

- https://www.instagram.com/p/DYmh2Z-jx5J/?hl=en

- https://www.crv.com/content/equity-dilution

- https://www.winstontaylor.com/insights/uks-digital-assets-regulatory-framework-takes-shape

- https://www.foley.com/insights/publications/2026/01/crypto-exits-surge-in-2025-momentum-builds-for-an-even-bigger-2026/

- https://www.svb.com/startup-insights/startup-equity/startup-founders-should-know-preferred-stock/

- https://growthlist.co/uk-startups/

- https://www.bvp.com/atlas/stablecoins-from-defi-primitive-to-global-financial-infrastructure

Community notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…