Deep dive explainer on what equity is, how stock ownership and IPOs work, and how tokenization, onchain markets, and equity perps are reshaping access, rights, and risk at the intersection of crypto and traditional finance.

+22 sources across the wider coverage universe

OKX Ventures, HashKey take equity in VPBank's CAEX to compete for Vietnam's five-slot crypto pilot2026-04

OKX Ventures, HashKey take equity in VPBank's CAEX to compete for Vietnam's five-slot crypto pilot2026-04 Figure and Hastra expand DeFi credit with auto loans, bringing tokenized consumer lending beyond home equity and testing real-world yield markets onchain2026-04

Figure and Hastra expand DeFi credit with auto loans, bringing tokenized consumer lending beyond home equity and testing real-world yield markets onchain2026-04 SIX Group taps Chainlink DataLink to bring Swiss and Spanish equity data onchain2026-04

SIX Group taps Chainlink DataLink to bring Swiss and Spanish equity data onchain2026-04 TeraWulf stock drops ~6% after upsizing equity raise to $900M, pricing 47.4M shares at $19 to fund AI data center expansion2026-04

TeraWulf stock drops ~6% after upsizing equity raise to $900M, pricing 47.4M shares at $19 to fund AI data center expansion2026-04 Jane Street signs $6B CoreWeave AI cloud deal, takes $1B equity stake at $109 per share2026-04

Jane Street signs $6B CoreWeave AI cloud deal, takes $1B equity stake at $109 per share2026-04 Employers balk at adding crypto and private equity to 401(k)s over fiduciary lawsuit risk2026-04

Employers balk at adding crypto and private equity to 401(k)s over fiduciary lawsuit risk2026-04

Equity in a Crypto‑Native World: From Stocks to Tokenized Markets

Equity represents an ownership claim on the residual value of a business or asset, typically in the form of shares that entitle holders to economic upside and, in many cases, voting rights over key decisions. In the crypto era, that basic idea of ownership is being re‑implemented across blockchains, derivatives, and tokenization platforms, blurring the line between traditional stock markets and onchain markets while preserving the core concept of equity as shared risk and shared reward.

What “Equity” Means in Finance

In classical finance, equity is the portion of a company or asset owned by shareholders after all liabilities are accounted for, often summarized as the residual claim on assets once debts are paid. Common stock is the most familiar equity instrument: each share represents a proportional slice of ownership in a corporation, with potential claims on dividends, voting rights in governance, and participation in residual value if the company is liquidated. Preferred stock, partnership interests, and limited liability company units are alternative equity forms, but they share this same basic logic of residual ownership. Equity therefore sits at the opposite end of the capital structure from debt, which promises fixed repayments but no upside beyond contractual interest.

For public companies, equity is standardized into tradeable shares listed on stock exchanges, allowing investors to buy and sell ownership stakes continuously during market hours. Equity prices in these markets reflect expectations about future cash flows, growth prospects, and risk, all discounted into a present value. In practice, that valuation process is messy and driven by narratives as much as by models, but the foundational principle is that equity holders are effectively buying a share of the company’s future profits. These shares can be newly issued, raising fresh capital for the firm, or already outstanding and simply changing hands between investors.

The role of equity in corporate finance extends beyond simple ownership. Issuing new equity gives companies a way to fund expansion, acquisitions, or balance sheet restructuring without incurring fixed debt obligations, at the cost of diluting existing shareholders’ percentage stakes. Buybacks and dividends reverse that flow: by returning cash to shareholders or reducing the share count, firms adjust their capital structure and attempt to optimize the balance between growth investment and shareholder payout. Debates around whether specific equity issuance is “dilutive” therefore hinge on what the company does with the proceeds. For example, when a firm sells additional shares to purchase another asset—whether a rival business or Bitcoin for its treasury—supporters can argue that existing shareholders are trading a piece of their claim on cash for a piece of their claim on that new asset. Whether this is truly dilutive depends on whether the acquired asset is perceived as worth at least as much as the equity given up.

Equity also encodes control. Corporate voting rights allow shareholders, particularly large ones, to influence management, strategy, and capital allocation. That control dimension explains why equity has become central to debates about the ownership of emerging technologies like artificial intelligence. Proposals such as a sovereign wealth fund that would require leading AI labs to transfer significant portions of their equity to the state illustrate how ownership stakes are increasingly viewed not just as financial instruments, but as levers of political and social power. In this context, who holds equity in key platforms shapes how value, risk, and decision‑making authority are distributed across society.

In the crypto ecosystem, the term “equity” retains this classical meaning, but it also appears in analogical uses. Governance tokens can behave like equity in decentralized protocols, even when they are not legally classified as such, because they confer control rights and a claim on protocol cash flows. Tokenized equities are strictly legal equity interests wrapped into blockchain‑based representations. Synthetic equity exposures in perpetual futures or options emulate price behavior without conferring any ownership rights at all. Understanding equity in a crypto‑native world therefore starts with the traditional notion of ownership and then traces how different technologies recreate or abstract away pieces of that concept.

TradeXYZ's dominance in equity, commodity and index perps isn't an existential threat to Hyperliquid, it's a growth engine driving users, fees and HYPE buybacks

83 active xyz markets now carry about $2.85B OI and $2.6B in 24h notional on Hyperliquid API; SP500, SPCX, CL/BRENTOIL, GOLD and SILVER are already sitting in the top books. HIP-3 makes that accretive because deployers bond 500k HYPE and users pay 2x validator-perp fees while the protocol keeps the same fee take, but the stress point moves to oracle quality and slashing when SPCX/CBRS-style pre-IPO marks have no clean exchange close.

Readers are not clicking equity stories for tokenization-as-investment thesis — they click when equity becomes functional DeFi infrastructure: collateral inside a stablecoin reserve, an oracle feed powering a prediction market, or the underlying of a 20x leveraged perpetual, revealing demand for equity-as-primitive rather than equity-as-asset.↗

Traditional Equity Markets: IPOs, Indices, and Capital Formation

To understand what is changing, it is helpful to review how traditional equity markets function today. Public equity markets center on two phases: primary offerings, where companies sell newly created shares to raise capital, and secondary trading, where those shares subsequently exchange hands between investors. The archetypal primary event is the initial public offering, or IPO, where a private company lists shares on a stock exchange, often accompanied by a roadshow, book‑building process, and allocation to institutional and retail investors. The IPO price crystallizes years of private‑market valuations into a publicly tradeable reference point.

Recent mega‑listings illustrate both the scale and the constraints of traditional IPOs. When SpaceX priced roughly 555.6 million shares at about \(135\) dollars each, it implied around \(75\) billion dollars raised and catapulted the listing into the ranks of the largest IPOs in history, surpassing even Saudi Aramco’s 2019 deal in gross proceeds terms according to contemporary reporting. This transaction provided a textbook example of classic equity issuance: the company exchanged new ownership claims for capital, accessed a broad base of public investors through stock exchanges, and entered the world of index inclusion and benchmark tracking that shapes global portfolios.

Once listed, a company’s equity typically becomes part of broader market indices such as the S&P 500 or sector‑specific benchmarks. These indices underpin a vast ecosystem of mutual funds and exchange‑traded funds (ETFs), which pool capital from investors to buy diversified baskets of stocks. Investors thereby gain exposure to entire markets rather than single names. The behavior of these indices—driven by macroeconomic conditions, interest rates, earnings cycles, and sector rotations—anchors much of global asset allocation. It is this index‑centric structure that is now being mirrored onchain as developers tokenize broad market exposures and build perpetual index futures around them.

The rise of pre‑IPO valuation cycles in private markets has complicated this picture. Highly sought‑after companies can spend years as private “unicorns,” with limited access for ordinary investors. By the time such firms go public, much of the value appreciation may already have accrued to venture funds and early backers. This imbalance has fueled demand for mechanisms that allow earlier or more flexible access to equity exposure, whether through private market platforms, structured products, or, increasingly, tokenized and derivatives‑based structures on crypto exchanges. It is precisely this demand that products like pre‑IPO perpetual futures seek to address.

Traditional equity markets are also deeply intermediated. Brokers, clearinghouses, custodians, transfer agents, and market‑makers all play specialized roles in ensuring settlement finality, custody, and orderly price discovery. These intermediaries add resilience but also cost and latency. Trades generally settle on timescales of T+2 or faster, but still not instantaneously, leaving room for credit risk and operational failures. Access is constrained by geography, market hours, and regulatory barriers. This is the world that crypto‑native equity products are now intersecting: a complex, regulated, and globally important system that has historically been separate from onchain activity.

Tokenized Equities: Putting Stocks Onchain

Tokenized equities are digital tokens on a blockchain that represent shares of traditional assets such as individual stocks or ETFs. Each token corresponds to a claim on an underlying equity security held by a regulated custodian, typically at a one‑to‑one ratio. In practical terms, a tokenized share of a company like Apple is designed to track the same price as the underlying stock, while enabling 24/7 trading on crypto exchanges and DeFi platforms. Kraken, for example, defines tokenized equities as digital representations of traditional company shares recorded on a blockchain, backed one‑to‑one by actual equities held in custody by a regulated third party.

The tokenization process follows a series of steps. First, an issuer or platform selects the asset to be tokenized, whether it is a publicly traded stock, an ETF, or even shares in a private company. Next, blockchain‑based tokens are minted, each representing a specific quantity or fraction of the underlying equity. Smart contracts define the rights and rules associated with these tokens, including voting arrangements, dividend handling, transfer restrictions, and compliance logic. Know‑Your‑Customer (KYC) and Anti‑Money‑Laundering (AML) checks are typically embedded into onboarding processes to meet regulatory standards. Once issued, the tokens can trade on digital asset exchanges that support tokenized securities, providing secondary market liquidity and global accessibility.

Tokenized equities offer several functional advantages over traditional brokerage holdings. Because they live on blockchains, they can settle effectively instantly, rather than on a T+2 basis, reducing counterparty risk and freeing up capital. They can be traded outside of conventional market hours, allowing investors in different time zones or with different schedules to adjust their positions without waiting for stock exchanges to open. The tokens are divisible down to small fractions, enabling fractional ownership that lowers the minimum ticket size for participation in high‑priced stocks. Blockchain records also provide transparent, verifiable ownership histories and can automate actions like corporate event processing through smart contracts.

These features are not purely theoretical. A growing ecosystem of issuers and exchanges is already live. Ondo Finance’s Ondo Global Markets, for instance, has emerged as a leading tokenized stock and ETF platform, reaching more than \(1\) billion dollars in total value locked (TVL) by May 2026 and surpassing \(18\) billion dollars in cumulative trading volume within its first eight months. According to RWA.xyz data cited by Ondo, the platform holds over 70 percent market share among tokenized equity issuers. Ondo has also expanded to the Solana blockchain, offering access to over 200 tokenized U.S. stocks and ETFs, and becoming the largest real‑world asset issuer on Solana by asset count. This launch means Ondo represents around 65 percent of all tokenized real‑world assets live on Solana.

Competition is intensifying across chains and venues. Data from May 2026 suggests that Solana captured roughly 97 percent of tokenized equity spot trading volume, as venues such as Backpack, Ondo, xStocks, and PreStocks competed on holder rights, token structures, and regulatory posture. At the same time, Binance has moved to secure a strategic minority equity stake in Alpaca, a U.S. self‑clearing broker‑dealer whose API infrastructure reportedly custodies about 94 percent of tokenized U.S. stocks and ETFs. This makes Alpaca a central clearing highway connecting digital liquidity with Wall Street equities, and gives Binance access to payment‑for‑order‑flow revenues and securities lending profits tied to tokenized stock trading.

The overall tokenized equity market remains small relative to global equity capitalization but is expanding rapidly. Following the launch of tokenized access to the SpaceX IPO on Kraken, the combined market capitalization of tokenized equities was reported around 5.5 billion dollars, with much of that growth attributed to the SpaceX effect. Academic and institutional forecasts suggest significant room for further growth: Citigroup, for example, estimates that tokenized securities across asset classes could reach 4–5 trillion dollars by 2030, a projection frequently cited in the tokenization field. This number includes not only tokenized equities but also bonds, funds, and other real‑world assets, yet it illustrates the scale of the opportunity.

However, tokenized equities are not monolithic. Some products offer direct legal ownership of underlying shares with full voting and dividend rights, mediated through custodians and transfer agents. Others are economic synthetics that track stock prices without conferring any shareholder rights. The SpaceX IPO launch has highlighted this distinction vividly. Traditional equity acquisition through the IPO grants shareholders a slice of the company’s residual value and formal corporate rights, while blockchain‑based tokenized stock exposure can provide price tracking, fractional access, and 24/7 trading, but often without direct entry into the corporate cap table or access to shareholder votes. For investors, understanding whether a token represents true equity or merely price exposure is crucial.

Regulatory uncertainty further complicates the picture. In the United States, the Securities and Exchange Commission (SEC) has been working on an exemption framework that would allow crypto firms to trade tokenized assets linked to U.S. stocks under defined conditions. According to reporting, the SEC recently delayed its plan to provide broad exemptions, partly due to concerns about unauthorized equity tokens issued without issuer approval. Regulators are wary of structures that might infringe on existing securities laws or mislead investors about the rights they actually hold. This tension between innovation and investor protection is a recurring theme as tokenized equity markets mature.

On the infrastructure side, tokenization is also increasingly integrated into institutional‑grade platforms. Coinbase has positioned itself as a preferred tokenization infrastructure partner for projects like Centrifuge, spanning private credit, fixed income, and equity exposure moving onto Base, Coinbase’s Layer 2 network. Products like deSPXA on Morpho, which represents S&P 500 exposure that can be used as collateral in onchain lending markets, exemplify how tokenized equity indices are being woven into DeFi’s credit fabric. By allowing holders to borrow against their index positions, these systems transform passive equity exposure into active, composable collateral, enabling new leverage and hedging strategies onchain.

- 01tokenized equity infrastructure race↗

Solana capturing 97% of tokenized equity trading volume, Base adding S&P 500 exposure via Centrifuge, and Ondo's Solana deployment made readers track which chain wins the pipe-laying competition for real-world equity settlement.

- 02equity perps and onchain leverage↗

Ondo's 20x leveraged equity perps, Ostium's Nasdaq data integration, and the funding-rate arbitrage angle gave readers concrete products to evaluate — offshore leverage on stocks with no brokerage account required.

- 03pre-IPO and private equity access↗

OKX offering SpaceX and OpenAI perpetuals, Coinbase launching pre-IPO listings, and the $5.5B tokenized equity market milestone showed readers a genuine route into previously gated private-company exposure.

- 04equity as DeFi collateral

Ethena's USDe reserve overhaul adding equity basis trades alongside RWAs was the single highest-clicked story, signaling reader appetite for equity embedded inside stablecoin yield infrastructure rather than held as a standalone token.

- 05regulatory gatekeeping of retail access↗

The SEC's May 2026 delay on crypto stock rules, Securitize's SPAC hurdle, and employer 401k fiduciary liability fears clustered as a thread about which institutions get to block or unlock retail equity exposure.

- 06TradFi capital structure convergence↗

Jamie Dimon questioning the IPO drought, Franklin Templeton filing Bitcoin DRIP ETFs, and Strategy shifting from debt to equity financing read together as institutions quietly rewiring capital structure around crypto rails.

Equity Derivatives and Perpetuals in Crypto

Alongside fully backed tokenized equities, a parallel universe of synthetic equity exposure has grown on crypto venues through derivatives like perpetual futures, options, and structured products. Perpetual futures, or “perps,” are derivatives that track an underlying asset’s price without a fixed expiry date, relying on funding payments between longs and shorts to anchor the contract price around the spot market. In crypto, perps originally focused on Bitcoin and Ether, but they now extend to equities, indices, commodities, and even IPO‑linked exposures.

Centralized and decentralized exchanges are actively rolling out equity perps. Ondo Finance, building on its leadership in tokenized equities, is launching Ondo Perps, a platform that allows users outside the United States to trade leading U.S. stocks and indices with up to 20x leverage. These instruments are fully onchain, settling on Solana while drawing pricing from underlying U.S. equity markets and, in some cases, from the tokenized stock markets Ondo operates. On other chains, projects incubated by Aptos Labs are building equity perps and perpetual‑style equity indices with onchain order books and regulated real‑world asset issuance, showing how Layer 1 ecosystems are courting equity derivatives flows.

Crypto‑native derivatives venues like Hyperliquid offer a glimpse into the scale of demand. Hyperliquid recently hit 10 billion dollars in open interest, a milestone that coincided with growing activity in equity‑linked and commodity markets that trade 24/7 onchain. This suggests that a meaningful share of volume on such platforms now comes from products whose underlyings are traditionally off‑chain assets, including stocks and indices. For traders, the value proposition is straightforward: they can take leveraged positions on equity price movements, hedge existing exposures, or express macro views around economic events, without going through legacy brokers or being constrained by market hours.

Crypto exchanges are also building out comprehensive product suites that integrate spot crypto, tokenized equities, options, and perps under one roof. Coinbase, which began as a venue for buying Bitcoin, has announced a slate of new offerings including tokenized stocks, pre‑IPO perpetuals, equity options, crypto options, perpetual equity indices, and time‑based prediction markets. This lineup effectively turns a crypto exchange into a multi‑asset derivatives marketplace, where a user might simultaneously trade BTC options, equity index perps, and tokenized IPO exposures. Binance and other major exchanges are similarly expanding their non‑crypto perps menus, adding gold, silver, oil, and marquee equities such as NVDA, TSLA, GOOGL, and AMZN to their perpetual futures rosters, often in fully onchain implementations powered by partner chains like Aptos.

Pre‑IPO perpetuals exemplify how equity and crypto derivatives are converging. Coinbase’s launch of pre‑IPO perpetual futures starting with SpaceX allows users to trade a synthetic price for SpaceX equity before and around its public debut, based on expectations of IPO valuation and demand. Other exchanges, such as Bybit and Kraken, have provided tokenized subscription and spot trading for the SpaceX IPO, with Kraken explicitly offering tokenized access to the IPO for retail investors through tokenized shares that track SpaceX’s listing. These products blur the line between private and public market exposure and create a 24/7, global “grey market” in equity pricing that can front‑run or react to traditional IPO processes in real time.

There is growing evidence that such onchain equity markets may influence or anticipate traditional market behavior. Research from trading firms has suggested that stock perpetuals and tokenized indices can predict the next day’s cash equity open with high accuracy, effectively turning crypto exchanges into always‑on price discovery venues for mainstream equity markets. While specific predictive metrics vary by study, the underlying idea is that when traditional exchanges are closed, tokenized and derivative markets on crypto platforms continue to process information, causing their prices to move in response to news, macro shocks, or order flow. When stock exchanges reopen, their prices often converge toward the levels implied by overnight onchain trading.

This dynamic is reinforced as more investors use tokenized equity indices like deSPXA as collateral in lending protocols. If a market shock triggers liquidations in DeFi positions secured by equity tokens, it can force selling or hedging in the underlying markets or in related derivatives, adding new feedback loops between DeFi and TradFi. Similarly, the rapid growth of equity perps and non‑crypto perps on DeFi platforms suggests that onchain leverage is increasingly tied to movements in off‑chain asset classes. For risk managers and regulators, this raises questions about contagion and systemic risk: if a stress event occurs in either world, the other may feel the impact through these hybrid products.

The user experience of equity derivatives on crypto platforms diverges sharply from legacy markets. In traditional finance, access to equity options and futures often requires specific account approvals, margin arrangements, and knowledge of complex contract specifications. On crypto exchanges, by contrast, a retail user can open a perps trade on a tokenized index or single stock with a few clicks, using stablecoins as collateral and managing margin in real time. This ease of access is one reason why Binance’s U.S. equities product, which offers access to real U.S. stocks through a crypto exchange interface, reportedly averaged about 143 million dollars in daily trading volume during its first nine days, surpassing the tokenized equity spot market’s peak week according to CoinDesk Research data. For many users, particularly in emerging markets, the path into global equity exposure increasingly runs through crypto rails rather than traditional brokers.

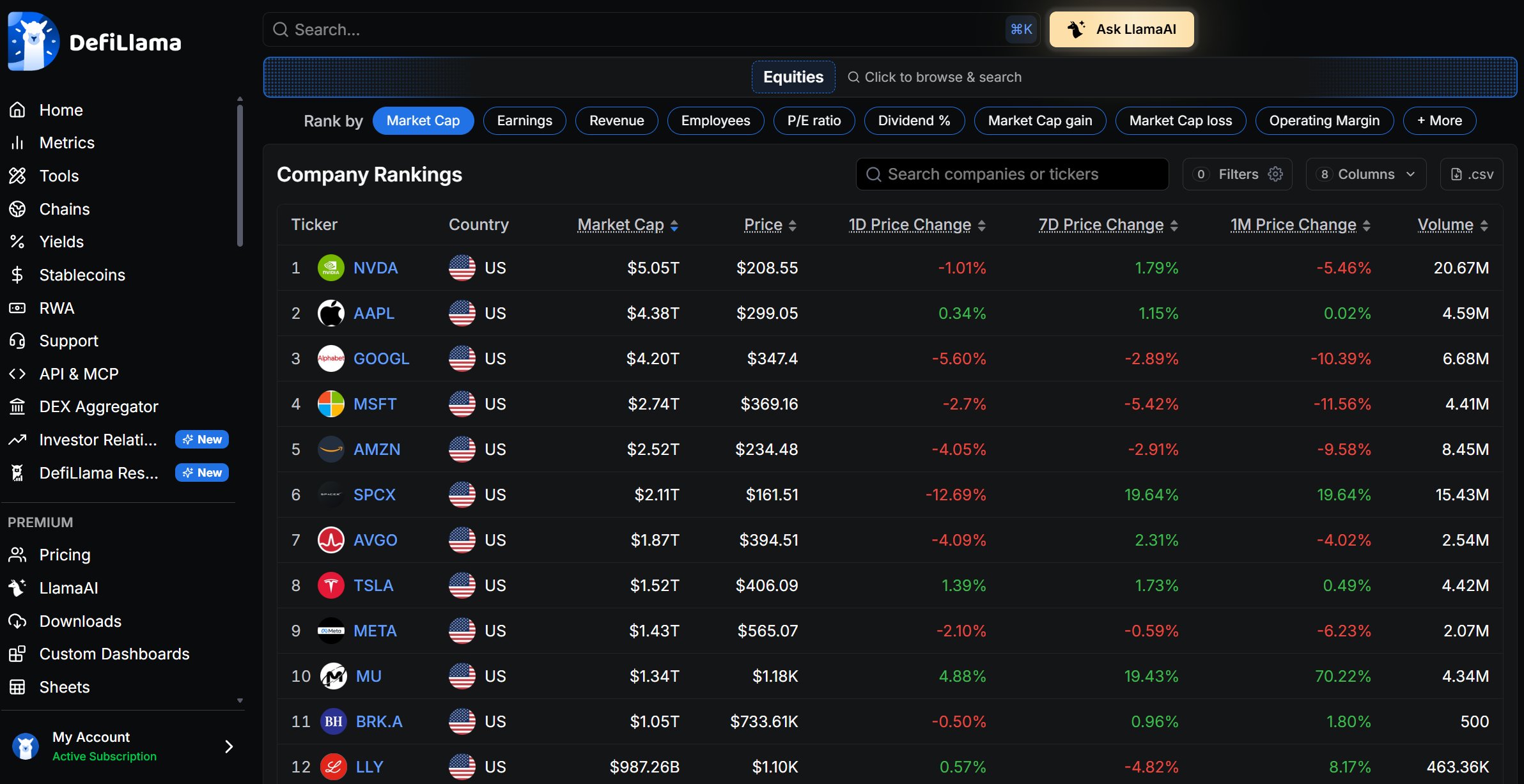

DefiLlama hoists new sails with 3,000+ TradFi equity tickers, opening vast nautical routes between stock markets and crypto

$1.59B of tokenized-equity market cap is still a rounding error, but clean stock financials inside DefiLlama gives DeFi traders the missing comp layer. Protocol fees and stock earnings on one screen turns AAVE vs JPM or HYPE vs HOOD into a one-click valuation fight instead of another FDV meme. With xStocks already showing the messy parts of SPV wrappers and off-hours price gaps, the data layer has to get good before the asset layer gets liquid.

Hybrid Products: Equities, Bitcoin, and New Capital Structures

As tokenized equities and equity derivatives grow, a new class of hybrid products that combine stocks with cryptocurrencies is emerging. Traditional asset managers are experimenting with ETFs that mix equity portfolios with Bitcoin exposure, using dividend flows and rebalancing rules to embed a small but persistent allocation to BTC within mainstream investment vehicles. Franklin Templeton’s recent filings with the U.S. SEC are a notable example. The firm has proposed two exchange‑traded funds—the Franklin U.S. Equity Bitcoin DRIP Index ETF and the Franklin U.S. Innovation Bitcoin DRIP Index ETF—that would launch with a 95 percent allocation to U.S. large‑cap equities and a 5 percent allocation to Bitcoin, with Bitcoin exposure capped at 20 percent.

These ETFs track indices where dividends generated by the underlying stock portfolios are automatically channeled into Bitcoin‑linked instruments rather than being paid out to investors or reinvested in equities. Eligible Bitcoin exposures include spot Bitcoin exchange‑traded products, futures contracts, options, and, in some cases, a wholly‑owned subsidiary in the Cayman Islands that can hold these positions. Under the index methodology, quarterly rebalancing trims Bitcoin allocations above 5 percent back to 4.5 percent, while a hard cap limits Bitcoin exposure to 20 percent between rebalancing dates. Analysts have described this structure as effectively creating an automatic, low‑maintenance 5 percent Bitcoin “feed” funded entirely by equity dividends.

From an equity perspective, such products reimagine dividends not as cash payouts, but as an internal source of capital for building a parallel balance sheet of Bitcoin holdings. They also highlight a broader trend: equity has become not only an asset class to be tokenized, but also the funding mechanism and reference base for crypto exposure. Companies have issued new equity to purchase Bitcoin for their treasuries, arguing that the resulting balance sheet transformation benefits shareholders by substituting cash or other assets with BTC. Debates between figures like Michael Saylor and Jack Mallers about whether this kind of issuance is dilutive boil down to how one values the Bitcoin acquired relative to the equity sold and to the original business’s cash‑generating ability.

Onchain, hybrid products manifest as structured vaults and strategies that combine tokenized stocks, crypto assets, and derivatives into a single position. A DeFi protocol might, for example, take in tokenized equity index tokens as collateral, borrow stablecoins against them, deploy those stablecoins into yield strategies, and hedge exposure with equity perps or options. Protocols like Morpho have begun to formalize this by allowing positions like deSPXA, representing S&P 500 exposure, to be pledged as collateral in lending markets, turning traditional equity exposure into a building block for onchain leverage and yield generation. Centrifuge and similar platforms tokenize real‑world credit and equity claims, route them into pools on chains like Base, and enable composability with other DeFi primitives, effectively wrapping complex capital structures into programmable tokens.

Centralized exchanges are also blurring the line between equity accounts and crypto wallets. MEXC’s “RealStocks” initiative, for instance, offers zero‑fee U.S. equity trading with pass‑through dividends while using a crypto‑exchange user interface, effectively merging a brokerage account into a crypto trading platform. Binance’s U.S. equities product follows a similar logic, offering access to thousands of U.S. stocks from a crypto exchange environment and capturing payment for order flow and securities lending revenue streams via its stake in Alpaca’s infrastructure. Binance Research has argued that crypto exchanges could bring trillions of dollars in incremental annual equity capital over the coming years by serving as gateways for crypto users—many in emerging markets—to global stock markets, illustrating the scale of this convergence.

In the policy realm, equity is increasingly intertwined with broader debates about technology and public interest. Proposals like Senator Bernie Sanders’s idea of an “American AI Sovereign Wealth Fund,” which would require leading AI companies such as OpenAI, Anthropic, and xAI to transfer half their equity to the U.S. government, frame equity not just as a financial claim but as a vehicle for socializing control and economic upside from transformative technologies. This mirrors earlier debates around nationalization, but with a new focus on intellectual property–rich tech platforms whose value is heavily tied to data and algorithms. For crypto markets, such ideas raise questions about how tokenized equity in AI companies might reflect or resist political attempts to reallocate ownership.

Capital formation itself is being reengineered. Structures like multi‑tiered equity financing designed to build Bitcoin reserves, or SPAC mergers involving tokenization platforms such as Securitize, point to a world where equity issuance, crypto asset acquisition, and exchange listings become part of an integrated strategy. A tokenization platform going public via a SPAC merger, for example, might simultaneously issue equity to fund further growth, deepen its role in tokenizing other companies’ equity, and list its own shares that could later be tokenized, creating a recursive loop between onchain and off‑chain equity markets. In that sense, equity is both the instrument being tokenized and the corporate funding tool that drives tokenization.

Cornell publishes institutional analysis as tokenized equity market gains momentum

SEC delays rulemaking for crypto-native versions of U.S. stocks

Franklin Templeton files two Bitcoin DRIP ETFs reinvesting equity dividends into BTC

Base integrates Centrifuge to offer 24/7 tokenized S&P 500 exposure onchain

Solana reaches 97% share of tokenized equity trading volume across all platforms

Ondo launches tokenized equity perpetuals with 20x leverage for non-U.S. traders

- 2026-06regulatory

Securitize clears SEC hurdle for SPAC merger with Cantor Equity Partners II, NYSE listing as SECZ imminent

Tokenized equity market surpasses $5.5B as SpaceX IPO access opens on Kraken and Bybit

Infrastructure and Market Plumbing: From Alpaca to Aptos

Underneath the visible layers of tokenized stocks and equity perps lies a complex infrastructure stack that connects crypto markets to traditional equity plumbing. Alpaca, a U.S. self‑clearing broker‑dealer and specialized API infrastructure provider, plays a pivotal role. According to filings cited in Binance’s updated securities trading terms, Alpaca currently commands around 94 percent market share in the custody of tokenized U.S. stocks and ETFs. By acquiring a strategic minority equity stake in Alpaca, Binance effectively embeds itself directly into this primary clearing highway between digital exchanges and Wall Street equities. The agreement entitles Binance to capture a significant portion of payment‑for‑order‑flow fees and residual net profits generated from lending user stock allocations to short‑sellers, after interest is passed through to account holders.

This arrangement illustrates how tokenized equity markets still depend on traditional brokerage and clearing infrastructure. Even when a user buys a tokenized share of a U.S. stock on a crypto exchange, the underlying share typically sits at a broker‑dealer like Alpaca. That broker must handle trade execution on U.S. exchanges, settlement with clearinghouses, custody, and, where applicable, corporate actions and dividend processing. The blockchain representation is an additional layer that maps onto this infrastructure, with smart contracts enforcing ownership records and exchange trading logic. In this sense, tokenization is less about replacing Wall Street plumbing and more about extending its reach into new user bases and platforms.

Onchain, order books and matching engines must be engineered to handle continuous equity trading with high performance and regulatory‑compliant data trails. Aptos Labs, for example, has emphasized its efforts to support onchain order books, real‑world assets issued by regulated institutions, and equity perps as part of a “full‑stack infrastructure” for future capital markets. Protocols incubated by Aptos Labs, such as DecibelTrade, showcase how fully onchain exchanges can list equity perps, commodity perps, and crypto derivatives together, with every order and fill recorded on a high‑throughput Layer 1. This design enables composability with other DeFi protocols but must also confront challenges around market data privacy, front‑running, and regulatory oversight.

Programmable privacy has emerged as a crucial focus here. As the Dusk Foundation notes, tokenized assets carry sensitive information, especially when they represent bonds, funds, equities, or other real‑world assets. A tokenized equity instrument is not just a balance moving between addresses; it may encode investor identity, eligibility restrictions, corporate action histories, and tax considerations. Before someone can buy, hold, or transfer such an asset, the system might need to verify their jurisdiction, accreditation status, or sanctions screening. Privacy‑preserving smart contract architectures, where certain data are revealed only to authorized parties or regulators while the broader network sees only necessary state changes, are therefore critical for scaling institutional adoption of onchain equities.

DeFi lending platforms and RWA protocols provide another foundational layer. Morpho’s integration of deSPXA, a token representing S&P 500 exposure, allows holders to borrow against their equity positions within onchain markets. This represents a shift from passive holding of tokenized equity to active use as collateral, making equities part of the balance sheet in DeFi protocols. Centrifuge, working with Coinbase as a preferred tokenization partner, similarly tokenizes pools of credit and other assets, including equity‑linked exposures, and routes them into lending markets on Base. These systems require robust price oracles, legal agreements, and risk management frameworks that tie tokenized claims to off‑chain enforcement in case of defaults or corporate events.

Centralized exchanges complement this by acting as gateways and liquidity hubs. Binance’s U.S. equities product and MEXC’s RealStocks platform give crypto users direct access to U.S. stocks with familiar interfaces, sometimes with zero trading fees and pass‑through dividends, while behind the scenes relying on broker‑dealers like Alpaca for execution and custody. Coinbase has begun to knit together tokenized stocks, pre‑IPO perps, stock options, crypto options, and prediction markets into a single app experience. In parallel, decentralized venues like Hyperliquid handle ever larger open interest figures and expand their offerings of equity‑linked markets. Together, these layers create a multi‑venue, 24/7 equity ecosystem where traditional exchanges are only one part of a broader network.

Regulation, Rights, and Risks

As equity migrates onto blockchains and into hybrid derivatives, legal and regulatory frameworks lag behind technological innovation. In most jurisdictions, equity is a heavily regulated asset class, with stringent rules around issuance, disclosure, insider trading, and investor protection. When equity is tokenized, those same rules generally still apply; the token is simply a different representation of a security interest. However, the cross‑border, pseudonymous, and composable nature of crypto markets introduces complexities that regulators are still grappling with.

The U.S. SEC’s recent decision to delay a plan that would have created broad exemptions for trading tokenized versions of U.S. stocks on crypto venues is a case in point. According to Bloomberg reporting, one of the SEC’s key concerns involves allowing the trading of third‑party equity tokens issued without authorization from the underlying companies or registered intermediaries. From the regulator’s perspective, permitting tokens that track U.S. stocks but are not backed by legally recognized share ownership could mislead investors and undermine existing safeguards. The delay underscores the tension between the desire to accommodate innovation and the need to ensure that securities laws remain effective when assets jump chains.

Investor rights are another crucial dimension. Traditional shareholders have well‑defined entitlements: they can vote on corporate matters, receive dividends, and pursue legal remedies if companies or intermediaries breach their obligations. Holders of tokenized equities need clarity on whether and how these rights translate. Some platforms guarantee full pass‑through of economic rights but not voting rights, or they may aggregate voting on behalf of token holders. Others explicitly offer only price exposure, structuring tokens as derivatives or contracts for difference rather than as true shares. The SpaceX IPO has spotlighted this contrast: while Kraken and Bybit’s tokenized IPO access products provide economic exposure to SpaceX’s listing, they are distinct from owning registered shares in the company’s cap table.

Privacy and compliance intersect with these rights questions. As Dusk and other privacy‑focused projects emphasize, tokenized equities carry sensitive information that cannot be fully public on a blockchain without compromising investor confidentiality. At the same time, regulators require visibility into beneficial ownership, transaction histories, and risk concentrations, particularly for large or systemically important issuers. Programmable privacy tools—such as zero‑knowledge proofs that allow compliance checks without revealing underlying personal data—are emerging as potential solutions, but their legal status and practical deployment remain early‑stage. Balancing transparency for market integrity with confidentiality for investors is an unresolved regulatory design challenge.

Systemic risk is another area of concern. As tokenized equities and equity perps integrate with DeFi, leverage can build up in opaque ways. A stress event in tokenized equity markets—perhaps triggered by an IPO disappointment, an earnings shock, or a regulatory crackdown—could cascade into DeFi lending platforms, force liquidations of collateral, and propagate back into traditional equity markets if underlying shares must be sold to honor redemptions or margin calls. Conversely, a crash in the traditional equity market could imperil DeFi positions linked to tokenized indices like deSPXA, causing liquidations that affect unrelated crypto markets. The 24/7 nature of onchain markets means these adjustments can occur outside of traditional market hours, adding another layer of complexity for risk managers.

Jurisdictional fragmentation further complicates matters. Crypto exchanges often serve users globally, but equity tokens may only be legally available in specific regions or to certain types of investors. Platforms respond by geofencing, KYC gating, or structuring products as synthetic derivatives rather than direct equity claims. Regulatory arbitrage can arise when some jurisdictions permit more permissive tokenization regimes than others, drawing issuers and liquidity to those venues. Over time, this may spur competitive pressures among regulators to craft frameworks that both protect investors and attract capital, much as has occurred with crypto spot and derivatives regulation.

Finally, there is a political economy of equity in emerging technologies that intersects with crypto. Proposals like national AI sovereign wealth funds, debates over whether Bitcoin‑funded equity issuance is responsible or speculative, and concerns about concentrated equity ownership in platforms that mediate online discourse all shape the narratives around equity. For crypto audiences, these debates are not abstract. They influence which companies come to public markets, how their shares can be tokenized or traded, and how regulators perceive the systemic importance of tokenized equity markets. As equity becomes more programmable and globally accessible through crypto rails, its governance and distribution become pressing policy issues rather than purely financial ones.

Tokenized-equity perpetuals open rich new funding rate arbitrage lanes for savvy traders.

10–17.5% full-capital excess on event-grade names is juicy only until the basis arb tourists arrive. Trade.xyz’s 0.5x funding multiplier, isolated single-name margin, and discovery-bounds design split the book cleanly: Binance/Kraken for carry, Hyperliquid for spread capture. The ugly part is weekend mechanics; if the hedge leg is an xStocks token and Sunday Asia spreads blow from ~1bp to 30bp, “delta-neutral” turns into an ops and liquidation-buffer problem.

The SEC delayed its crypto-native equity rulemaking in May 2026, leaving tokenized stock issuers operating without a clear legal framework and exposing holders to potential forced unwind or repatriation requirements.

Solana absorbing 97% of tokenized equity trading volume concentrates systemic risk on a single chain — one outage or targeted enforcement action could halt the entire nascent market simultaneously.

Ondo's 20x leveraged equity perpetuals and funding-rate arbitrage products amplify equity volatility inside crypto settlement rails with no circuit breakers equivalent to those on traditional exchanges.

Despite 24/7 trading claims, the $5.5B tokenized equity market remains a rounding error against underlying equity liquidity, creating de-peg and redemption-queue risk during stress periods.

- Smart ContractMedium

Tokenized equity protocols stack custody, oracle, and issuance layers on top of on-chain logic; a clean audit on one layer (as with Manifest Finance's Sherlock review) does not cover the full attack surface.

- Custodial / CounterpartyMedium

Tokenized equity holders carry legal exposure to the issuer's solvency and redemption mechanics rather than direct share ownership, a gap that 401k plan fiduciaries explicitly cited as a lawsuit liability in 2026.

Equity for Crypto Investors: How to Think About Exposure

For crypto‑native investors, equity now appears in multiple guises, each with distinct risk‑return profiles and legal implications. Traditional brokerage accounts remain the most straightforward way to hold equity, offering direct ownership rights, regulated protections, and integration with existing tax and reporting systems. However, for many users—especially in emerging markets with limited access to U.S. brokers—crypto exchanges and tokenization platforms have become the primary gateways to global equity exposure. Binance Research has noted that the vast majority of its stock trading users come from emerging markets, suggesting that crypto platforms are expanding the geographic and demographic reach of equity ownership.

Tokenized equities provide one avenue for integrating equity holdings into a crypto portfolio. A user might hold tokenized shares of a U.S. tech company alongside Bitcoin and stablecoins in the same wallet, move those tokens across chains, or deposit them into DeFi protocols that accept them as collateral. This composability enables strategies that are difficult or impossible in traditional brokers, such as using a tokenized S&P 500 index as collateral for borrowing stablecoins, then swapping into Ether or governance tokens while hedging with equity perps. However, these efficiencies come with new risks, including smart contract vulnerabilities, oracle failures, and counterparty risk at the custodial and brokerage layers underpinning the tokenization.

Synthetic equity exposures via perps and options offer a different trade‑off. They typically provide no voting or dividend rights, but they are highly capital efficient for traders seeking short‑term directional bets or hedges. A trader can go long or short an equity perp with leverage, post USDC or another crypto asset as collateral, and close or adjust the position at any time. This suits active strategies and allows for complex cross‑asset trades, such as going long a basket of AI‑related equities while shorting a correlated crypto index, or vice versa. It also enables pre‑IPO and after‑hours speculation that traditional brokers may not offer. Yet the leverage involved magnifies losses as well as gains, and the legal classification of some synthetic products remains unsettled in major jurisdictions.

Hybrid products, such as the Franklin Templeton Bitcoin DRIP ETFs, may appeal to investors who want a simple, regulated wrapper that blends equity and Bitcoin exposure. For crypto users accustomed to self‑custody and DeFi composability, these ETFs may feel limiting, but they offer familiar brokerage integration and institutional oversight. For equity‑first investors curious about Bitcoin, the automatic dividend reinvestment into BTC might provide a psychologically comfortable way to build exposure over time without actively trading crypto markets. Understanding the fee structures, tracking behavior, and tax treatment of such products is essential, as is recognizing that they still sit primarily within the traditional financial system.

At the portfolio level, equity exposure can diversify crypto holdings and vice versa. Bitcoin and major equities are increasingly correlated during macro risk‑off events but can diverge in other regimes, providing hedging opportunities. Tokenized equity indices allow crypto portfolios to embed broad market beta without leaving onchain ecosystems, while equity perps enable fine‑tuned macro views. However, as the two systems become more intertwined, shocks in one market may increasingly propagate to the other, reducing diversification benefits. Portfolio construction in this hybrid world requires awareness of cross‑market linkages, leverage channels, and liquidity conditions across both centralized and decentralized venues.

Finally, crypto‑native investors must navigate evolving regulations and platform risks. Not all tokenized equities are created equal; some represent fully compliant, custodian‑backed claims with robust legal documentation, while others are purely synthetic price feeds. Some exchanges hold underlying shares directly, others rely on partners like Alpaca, and still others may simply mirror prices without any underlying ownership. Platform solvency, legal jurisdiction, and governance practices all matter. As more users enter equity markets via crypto channels, education about these distinctions becomes critical to avoiding misunderstandings about what is actually owned and what rights are attached.

Conclusion

Equity, in its traditional sense as an ownership stake in productive assets, remains one of the foundational building blocks of modern finance. The crypto revolution has not replaced this concept but rather extended and reconfigured it, creating new ways to represent, trade, and leverage equity exposure. Tokenized equities bring shares and indices onto blockchains, enabling fractional, 24/7, globally accessible trading, and embedding these instruments into DeFi’s composable architecture. Synthetic equity derivatives on crypto exchanges turn tokenized or off‑chain reference prices into perpetual futures and options, allowing continuous, leveraged speculation and hedging that increasingly influences traditional markets.

The growth of infrastructure players like Alpaca, the expansion of tokenization platforms such as Ondo and Centrifuge, and the integration of equity perps and indices on chains like Solana and Aptos underscore how deeply equity is now tied into onchain market plumbing. At the same time, traditional asset managers are launching hybrid vehicles like Franklin Templeton’s Bitcoin DRIP ETFs, embedding Bitcoin exposure into equity portfolios and reimagining dividends as funding flows into crypto assets. Centralized exchanges like Coinbase and Binance, as well as decentralization‑focused venues like Hyperliquid, are evolving into cross‑asset hubs where users can trade crypto, tokenized stocks, commodities, and equity derivatives within a single interface.

Regulation and policy remain works in progress. The SEC’s caution around tokenized stock exemptions, concerns about unauthorized equity tokens, and the need for programmable privacy for tokenized RWAs highlight the unresolved legal and compliance challenges. At the same time, political debates over AI ownership, Bitcoin‑funded equity issuance, and national sovereign wealth claims on tech platforms show that equity is increasingly seen as a locus of power as much as of financial return. For crypto audiences, these developments mean that participating in tokenized and derivative equity markets is not just a matter of chasing yields, but also of understanding how ownership, control, and risk are being redefined across intertwined financial systems.

Looking forward, equity’s role in crypto is likely to deepen. Tokenized indices as collateral in DeFi, real‑world asset pools on chains like Base, onchain order books listing equity perps, and global exchange products offering zero‑fee access to U.S. equities all point toward a future in which the distinction between “crypto markets” and “equity markets” becomes more porous. The task for builders, regulators, and investors alike is to harness the efficiencies and inclusivity of this convergence while preserving the rights, protections, and stability that have evolved around equity over decades.

Outlook

Over the next decade, equity is poised to become a truly multi‑venue, 24/7 asset class spanning regulated exchanges, tokenization platforms, and fully onchain derivatives markets. Citigroup’s projection of trillions of dollars in tokenized securities by 2030 suggests that onchain representations of stocks, funds, and indices could move from niche to mainstream, with platforms like Ondo Global Markets and infrastructure providers like Alpaca and Coinbase’s Base network at the center of this shift. As Solana and other high‑throughput chains capture the bulk of tokenized equity trading volume, and as exchanges roll out richer suites of equity perps, pre‑IPO products, and hybrid crypto‑equity ETFs, the boundaries between “Wall Street” and “onchain” will continue to blur.

For a crypto news audience, the key is to treat equity not as an alien relic of traditional finance, but as a core concept being reimplemented and extended in a programmable, global context. Tokenized stocks, equity indices as collateral, perpetuals that front‑run IPO pricing, and ETFs that drip dividends into Bitcoin are all variations on the same theme: how to allocate, trade, and govern ownership in an economy increasingly mediated by both blockchains and artificial intelligence. The winners in this evolving landscape are likely to be those who can integrate deep understanding of equity’s legal, economic, and political foundations with technical mastery of onchain infrastructure and a clear view of regulatory trajectories.

Latest Equity news

TradeXYZ's dominance in equity, commodity and index perps isn't an existential threat to Hyperliquid, it's a growth engine driving users, fees and HYPE buybacksDefiLlama hoists new sails with 3,000+ TradFi equity tickers, opening vast nautical routes between stock markets and cryptoTokenized-equity perpetuals open rich new funding rate arbitrage lanes for savvy traders. Syndio acquires Embrace.ai to strengthen its pay equity platform with AI expertise

Syndio acquires Embrace.ai to strengthen its pay equity platform with AI expertiseSources

- https://business.cornell.edu/article/2026/02/tokenized-equities/

- https://bitcoinmagazine.com/news/franklin-templeton-files-two-etfs-bitcoin

- https://x.com/leviathan_news/status/2067833723115171892/photo/1

- https://www.coinbase.com/blog/pre-ipos-are-launching-on-coinbase-starting-with-spacex

- https://cryptofuturesplatform.com

- https://www.tradingview.com/news/cointelegraph:fe0fa059e094b:0-hyperliquid-s-10b-open-interest-coincides-with-growth-in-equity-linked-markets-talos/

- https://x.com/coinbase/status/2067977606880759898

- https://x.com/WuBlockchain/status/2066474455707140193

- https://www.crowdfundinsider.com/2026/06/285340-spacex-ipo-launch-highlights-fundamental-contrast-between-blockchain-based-tokenized-stocks-exposure-and-traditional-equity-acquisition/

- https://www.thestreet.com/crypto/innovation/ondo-is-bringing-leveraged-stock-trading-on-chain

- https://www.instagram.com/p/DZfK8CtH6tc/

- https://financefeeds.com/binance-secures-high-stakes-equity-slice-of-alpaca-to-corner-tokenized-equity-pipelines/

- https://x.com/DuskFoundation/status/2064605972560220395

- https://www.instagram.com/p/DZf7aKMirGE/

- https://www.bloomberg.com/news/articles/2026-05-22/sec-delays-plan-allowing-for-crypto-versions-of-us-stocks

- https://www.kraken.com/learn/tokenized-equities

- https://solana.com/news/ondo-global-markets-tokenized-stocks-etfs-solana

- https://morpho.org/stories/centrifuge/

- https://x.com/AptosLabs/status/2064905474483642411

Community notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…