Bitcoin is a decentralized digital asset capped at 21 million coins, now held by ETFs, corporations like Strategy, and sovereign states — navigating record ETF outflows, rising on-chain activity, and growing institutional infrastructure in 2026.

+62 sources across the wider coverage universe

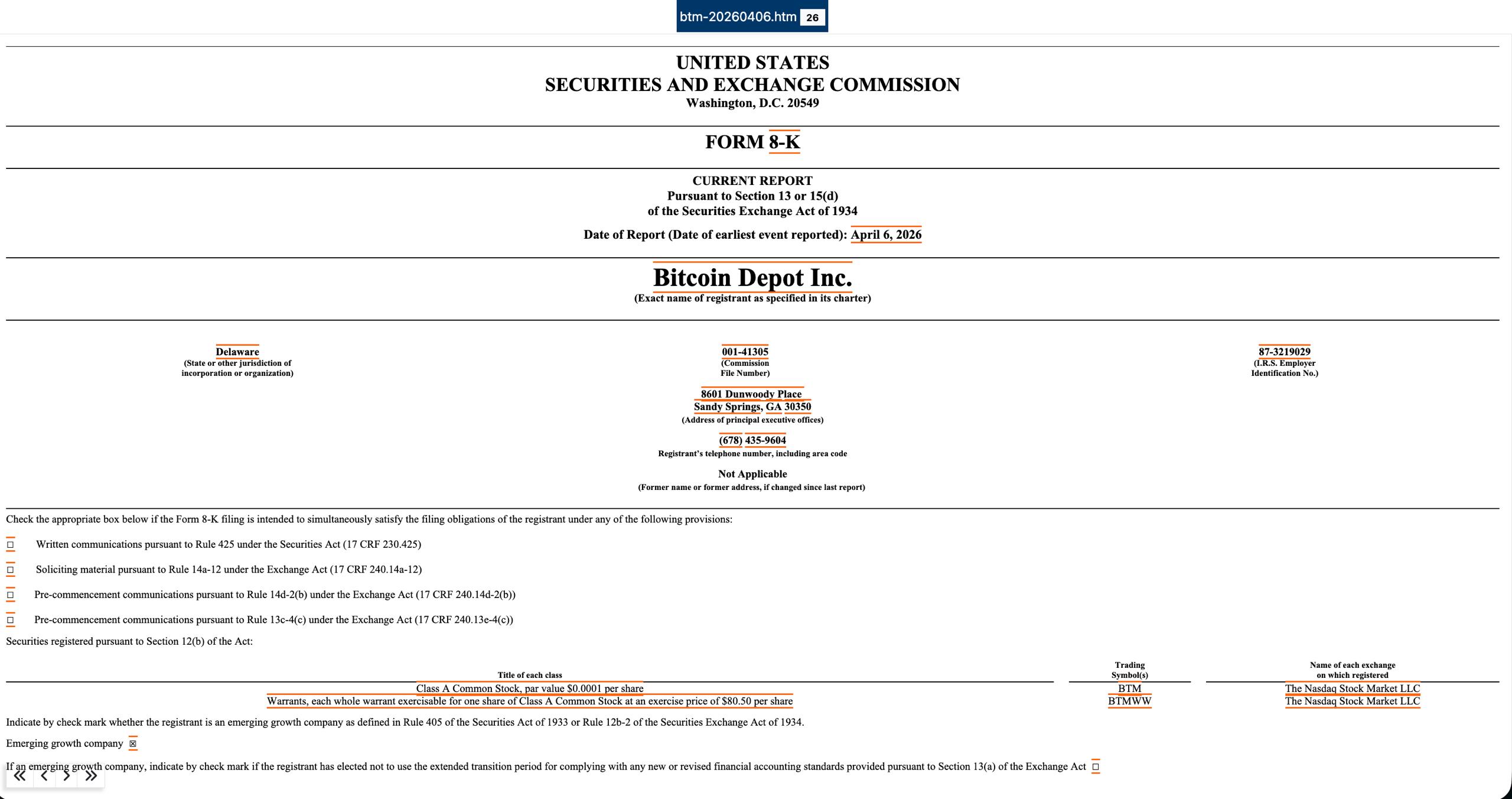

Bitcoin Depot discloses $3.6M BTC theft from corporate wallets in SEC filing, two weeks after breach2026-04

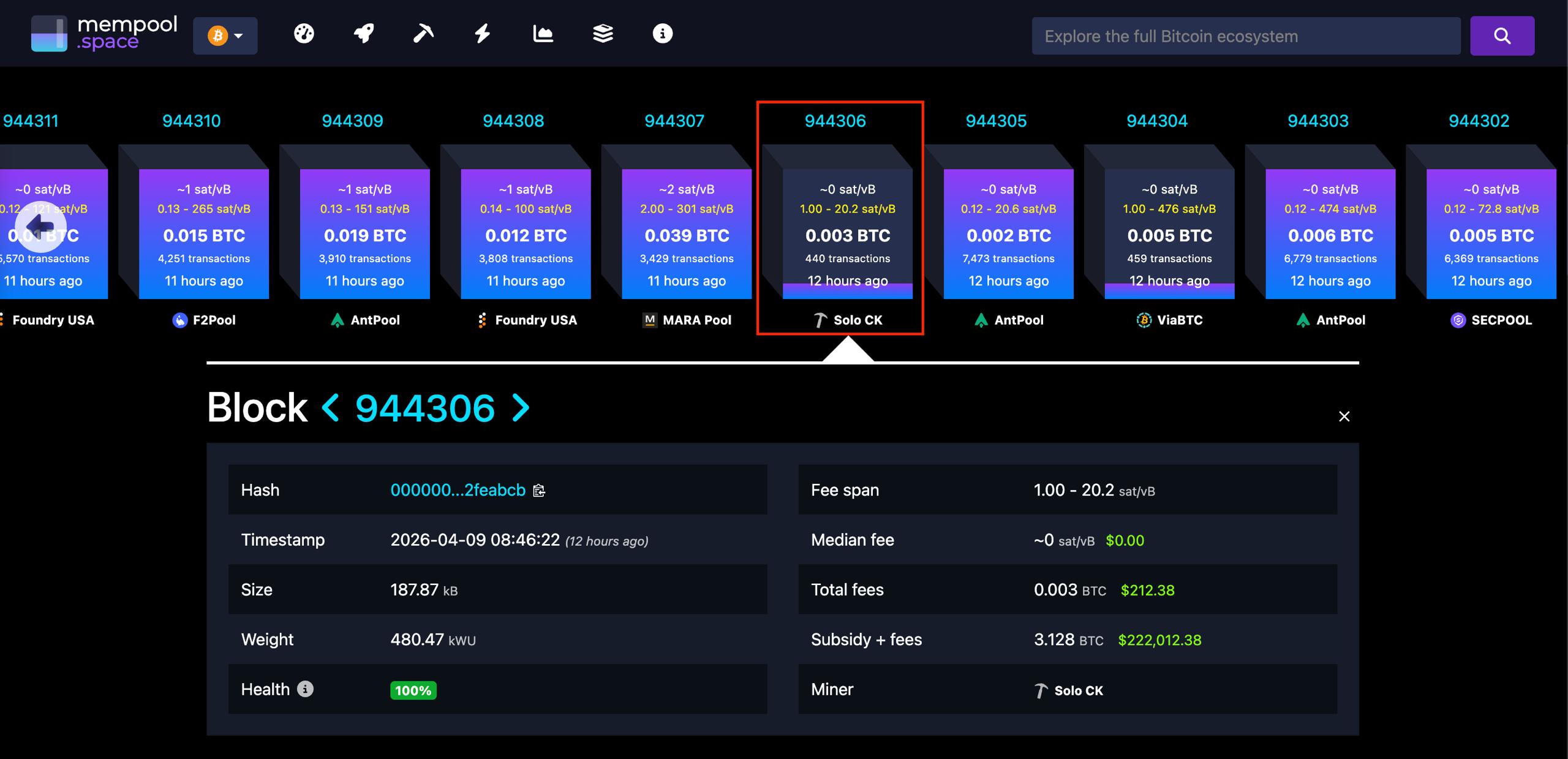

Bitcoin Depot discloses $3.6M BTC theft from corporate wallets in SEC filing, two weeks after breach2026-04 Solo miner with 70 TH/s defies 300-year odds to claim $222K Bitcoin block reward on CKPool2026-04

Solo miner with 70 TH/s defies 300-year odds to claim $222K Bitcoin block reward on CKPool2026-04 Suspected Thorchain exploit drains $7.4M+ across Bitcoin, Ethereum, BSC, and Base2026-05

Suspected Thorchain exploit drains $7.4M+ across Bitcoin, Ethereum, BSC, and Base2026-05 IMF calls Tether's Bitcoin reserves a vulnerability, warns stablecoins susceptible to runs2026-04

IMF calls Tether's Bitcoin reserves a vulnerability, warns stablecoins susceptible to runs2026-04 Exodus Pay brings Visa and Apple Pay spending to self-custodial Bitcoin wallets, rolls out in five states2026-04

Exodus Pay brings Visa and Apple Pay spending to self-custodial Bitcoin wallets, rolls out in five states2026-04 Bitcoin taps $73K as March CPI beats expectations at 3.3%, April rate cut odds still at zero2026-04

Bitcoin taps $73K as March CPI beats expectations at 3.3%, April rate cut odds still at zero2026-04

The world's first and largest cryptocurrency by market capitalization, Bitcoin (BTC) is a decentralized digital asset operating on a peer-to-peer network without a central issuing authority, governed instead by open-source software and a fixed monetary policy enforced in code.

What Bitcoin Is and How It Works

Introduced in a 2008 whitepaper by the pseudonymous Satoshi Nakamoto and launched in January 2009, Bitcoin solved a problem that had stumped digital-currency researchers for decades: how to prevent the same unit of value from being spent twice without a trusted central intermediary. The solution was the blockchain — a public, append-only ledger maintained by a distributed network of computers (nodes) that continuously verify and record transactions in cryptographically linked blocks.

Transactions are confirmed through a process called proof-of-work mining, in which specialized computers (ASICs) compete to solve a computationally difficult puzzle. The winner adds the next block and collects a block subsidy of newly issued BTC plus transaction fees. As of the April 2024 halving — the fourth in Bitcoin's history — that subsidy stands at 3.125 BTC per block, producing roughly 450 new bitcoins per day. The next halving is expected around 2028, when the reward drops again to approximately 1.5625 BTC.

The network's total supply is capped at 21 million coins, a rule baked into the protocol. As of June 2026, more than 20 million BTC have been mined — over 95% of the eventual total. The 20 millionth coin was issued in March 2026. The final fraction of a bitcoin is not projected to be mined until approximately 2140, as block rewards geometrically diminish.

Michael Saylor signals another bitcoin buy as Strategy sits about $13 billion underwater

$335.5M of ATM issuance for $34.9M of BTC is a very different machine than the old infinite-buy meme. The marginal buyer is now underwriting STRC at distressed yields, a $1.4B USD reserve, and common dilution before they get exposure to the 847,363 BTC stack. BTC still gets a Saylor bid, but it now comes wrapped in credit-market fragility, and that reflexivity cuts both ways when MSTR trades like a funding vehicle instead of spot beta.

Readers click Bitcoin stories not for price speculation but for the collision between its store-of-value identity and its new role as DeFi collateral and yield substrate — the same institutional adoption pulling Bitcoin into ETFs and sovereign reserves is simultaneously pulling it into governance failures, impermanent loss, and liquidation cascades it was never designed to absorb.

The Supply Scarcity Argument

Bitcoin's hard cap is its most-cited economic property. Proponents compare it to gold: a commodity whose scarcity confers long-term store-of-value properties. Unlike gold, however, Bitcoin's supply schedule is mathematically precise and cannot be altered by any government, central bank, or company.

This framing has attracted prominent believers. Ricardo Salinas Pliego, the Mexican billionaire and founder of Grupo Salinas, has publicly stated his accumulation strategy is straightforward: "As soon as I get my hands on some fiat, I turn it into Bitcoin." He has urged holders to treat BTC the way most people treat a home — buy it, hold it, and stop checking the price. The risks of such a concentrated personal bet are real: a single holder converting large fiat positions rapidly can amplify short-term volatility, and Salinas himself has been flagged by analysts for the concentration risk his buying represents.

Michael Saylor's firm Strategy (formerly MicroStrategy) has pursued the thesis at a corporate scale. As of late April 2026, Strategy held approximately 818,334 BTC, acquired at a blended average near $75,537 per coin for a total outlay of roughly $61.8 billion — making it the single largest publicly known corporate holder of Bitcoin. Saylor has said Strategy has never sold a coin from its treasury, though in mid-2026 the firm sold a small tranche for the first time. The company's preferred stock vehicle STRC has experienced significant price turbulence, with analysts at Strive attributing sharp drawdowns to embedded leverage in Strategy's capital structure rather than any change in Bitcoin's fundamentals.

Network Activity vs. Price: A Divergence to Watch

One of the more counterintuitive signals entering mid-2026 is the decoupling between price and on-chain activity. With BTC trading near $64,000 — roughly 40–50% below its prior all-time high — metrics tracked by blockchain analytics firm CryptoQuant show network activity approaching record highs, driven largely by a surge in microtransactions. Daily transaction counts are climbing even as large-wallet movement stalls, suggesting a broadening of the user base even during a price correction. Historically, rising on-chain activity during price weakness has preceded accumulation phases rather than further sell-offs — though past patterns are not guarantees.

Tether and Ledn plan XAUT-backed loans, turning $23B gold reserve into bitcoin-style collateral

Tether and Ledn are adding XAUT to Ledn’s platform, with gold-backed loans expected later this year alongside BTC and stablecoin rails. XAUT is backed by roughly $23B of physical bullion, with each token representing one troy ounce stored in Swiss vaults. The real move is Tether turning its gold stack into usable collateral, letting holders borrow against tokenized bullion without selling it.

- 01Bitcoin ETF institutional race

Readers tracked the SEC approval timeline, BlackRock and Fidelity's record-breaking launch, and the concentration risk of BlackRock accumulating nearly 4% of all supply — a single narrative arc from anticipation to systemic concern.

- 02Bitcoin DeFi yield integrations

The emergence of LRT vaults, tokenized-BTC lending, and impermanent-loss solutions for wrapped Bitcoin signaled that BTC holders are being pulled into DeFi risk profiles they did not historically sign up for.

- 03Sovereign and corporate accumulation

From MicroStrategy to nine governments to Trump and Senator Lummis pitching a strategic reserve, readers engaged heavily with Bitcoin as a geopolitical and balance-sheet asset rather than a retail trade.

- 04Bitcoin collateral governance failures

USDD removing 12,000 BTC from collateral without DAO approval crystallized reader anxiety about opaque governance in protocols that use Bitcoin as backing.

- 05Market crash and liquidation cascades

The $50K dip wiping $600M in leveraged positions and stalling carry-trade arbitrage drew readers who wanted to understand the structural fragility beneath Bitcoin's rally.

- 06Bitcoin custody and security threats

Deepfake Bitcoin scam proliferation and the Bitcoin Fog mixing service conviction revealed a security threat landscape that is simultaneously technical, social-engineering-based, and regulatory.

Bitcoin ETFs: Institutional Bridge or Exit Ramp?

The January 2024 approval of U.S. spot Bitcoin ETFs by the SEC marked a structural shift in how institutional capital accesses BTC. Products from BlackRock (IBIT), Fidelity (FBTC), and others quickly attracted tens of billions in assets. BlackRock's IBIT alone held approximately $67 billion in assets under management by early May 2026, making it one of the fastest-growing ETFs in history by that metric.

The flow picture has grown more complicated since. Total spot Bitcoin ETF assets, which peaked above $100 billion, fell to roughly $94 billion by early June 2026, following a 30-day period that saw a record $6.35 billion in net outflows — the largest such stretch since the products launched. Weekly outflows subsequently slowed sharply, dropping from $1.72 billion to $226 million over a single week, suggesting the exit wave may have been concentrated rather than structural.

Wall Street firms continue to build out the ETF infrastructure around Bitcoin. Franklin Templeton filed in mid-2026 for ETFs that automatically convert stock dividends into BTC exposure, a product aimed at equity investors seeking passive Bitcoin accumulation. Morgan Stanley disclosed it was quietly doubling its BTC position amid the selloff. Analysts who projected ETF AUM could reach $180–220 billion by year-end 2026 point to expanding distribution — Bank of America, Wells Fargo, and others are opening Bitcoin ETF access to retail clients.

The tension between those projections and current outflow data reflects a broader debate: whether the ETF wrapper has attracted long-term holders or traders who move in and out of BTC the same way they trade leveraged equity products.

Bitcoin's Expanding Use Cases

Payments. Despite persistent criticism that Bitcoin is "too slow" for everyday commerce, development continues. GoMining's launch of the GoBTC Pay SDK and API in 2026 targets point-of-sale integration for merchants wanting to accept BTC. The Lightning Network, a second-layer protocol enabling near-instant, low-fee BTC payments, continues to expand in merchant adoption across Latin America and parts of sub-Saharan Africa.

Bitcoin-native yield. Traditionally, holding BTC generated no income. Layer-2 protocols built on Bitcoin — most notably Stacks — have introduced self-custodial stacking mechanisms that let BTC holders participate in Proof-of-Transfer consensus to earn yield without relinquishing control of their keys. Stacks reported a strong Q3 trajectory in 2026, and the launch of institutional staking partnerships (such as with UTXOmgmt) signals growing demand for BTC yield products that avoid wrapping BTC on Ethereum or other chains.

Lending and collateral. New research published in 2026 highlights a persistent "collateral gap" in Bitcoin lending: institutional lenders are still reluctant to accept BTC as collateral at the same terms available for traditional assets, citing volatility and custody complexity. As those friction points diminish — partly driven by improved prime brokerage services at firms like Coinbase — BTC-backed lending is expected to grow, giving long-term holders liquidity without requiring them to sell.

Strategy's enterprise mNAV falls below 1 for the first time, signaling investors now value the firm's capital structure below the Bitcoin held on its balance sheet

$1.2B of annual preferred dividends against roughly $1.4B of cash is the reflexivity problem Saylor tried to securitize away. STRC trading about 25% below par turns every future raise into a cost-of-capital test, because plugging the reserve with common stock dilutes the exact premium the machine depends on. Metaplanet and Nakamoto already below 1x enterprise mNAV puts the BTC treasury trade in a harsher regime: buy-and-hold is easy, funding the hold without a premium bid is the part markets are repricing.

- 2023-07governance

Celsius approved to liquidate altcoins for BTC and ETH

- 2024-01regulatory

SEC approves spot Bitcoin ETFs; BlackRock and Fidelity launch to record inflows

- 2024-03regulatory

Roman Sterlingov convicted for operating Bitcoin Fog darknet mixing service

- 2024-03milestone

Bitcoin rallies above $60K on post-ETF institutional demand; US spot ETFs record $263M single-day inflows

- 2024-08milestone

Bitcoin drops below $50K; market crashes 17%, liquidating $600M in leveraged positions

- 2024-09launch

Fractal Bitcoin scaling solution goes live on mainnet backed by Unisat

- 2024-10milestone

BlackRock Bitcoin ETF surpasses MicroStrategy, holding nearly 4% of total supply

- 2025-01regulatory

Trump and Senator Lummis publicly pitch US strategic Bitcoin reserve to reduce national debt

Bitcoin vs. Ethereum and the Broader Crypto Ecosystem

Bitcoin and Ethereum are routinely compared but serve meaningfully different purposes. Ethereum is a programmable smart-contract platform; Bitcoin's scripting language is intentionally limited, prioritizing security and simplicity over flexibility. Critics argue this makes Bitcoin inflexible; supporters argue it makes Bitcoin a more credible monetary asset precisely because the rules cannot easily be changed.

The two assets have diverged in institutional narrative. Bitcoin is increasingly discussed in macro terms — as "digital gold," a hedge against currency debasement, or a reserve asset. Ethereum competes more directly with fintech infrastructure and Web3 application platforms. Both trade with high correlation during risk-off events but diverge significantly in periods of sector-specific momentum.

Geopolitical Currents

Bitcoin's censorship resistance has made it a politically sensitive asset. Iran has been cited in multiple reports as using Bitcoin mining to circumvent oil export sanctions — converting stranded energy into a liquid, internationally transferable asset. The U.S. Treasury has sanctioned specific Bitcoin addresses linked to Iranian entities, but the pseudonymous nature of the network makes comprehensive enforcement difficult.

More broadly, sovereign interest in Bitcoin has risen. El Salvador adopted BTC as legal tender in 2021 and has continued accumulating; other smaller economies have debated similar moves. The U.S. itself has seen legislative proposals for a "strategic Bitcoin reserve," though no formal policy has been enacted as of mid-2026.

- RegulatoryHigh

Spot ETF approvals resolved US uncertainty but Singapore's MAS blocked Bitcoin ETFs, and ongoing SEC posture toward crypto infrastructure keeps regulatory risk elevated globally.

- CentralizationHigh

BlackRock's ETF accumulating nearly 4% of total Bitcoin supply concentrates custodial and market-influence risk in a single traditional-finance entity.

- Market / LiquidityHigh

A single 17% market correction wiped $600M in leveraged positions and invalidated carry-trade strategies, demonstrating that Bitcoin's liquidity profile remains fragile under institutional leverage.

- GovernanceMedium

USDD's unilateral removal of 12,000 BTC from collateral without DAO approval shows that protocols using Bitcoin as reserve collateral carry governance opacity risk independent of Bitcoin's own design.

- Smart-contractMedium

Tokenized and restaked Bitcoin in LRT vaults and DeFi lending protocols introduces smart-contract failure modes to an asset historically prized for its off-chain simplicity.

- Custody / SecurityMedium

AI-generated deepfake scams and the prosecution of large-scale Bitcoin mixing operations illustrate a maturing but persistent threat surface against both retail and institutional holders.

Risks and Criticisms

Volatility. Bitcoin remains highly volatile relative to traditional asset classes. A single $13 billion options expiry in June 2026 was sufficient to generate significant uncertainty across the market. Traders were pricing put options targeting $52,000, suggesting meaningful bearish conviction even among sophisticated market participants.

Leverage and contagion. Strategy's $60+ billion concentrated bet has introduced a new systemic variable: if BTC prices fall sharply, margin calls on Strategy's debt instruments could force liquidations that amplify the decline. Saylor has publicly reflected on a near-miss during the 2022 debt crisis, when falling BTC prices stressed the company's balance sheet without triggering formal default. The STRC preferred stock turbulence in 2026 has revived that concern.

Regulatory uncertainty. Regulatory frameworks for Bitcoin vary widely by jurisdiction. The U.S. has clarified that spot BTC ETFs are permissible, and the CFTC has long treated BTC futures as a commodity derivative. Full legislative clarity — particularly around staking, lending, and mining — remains incomplete.

Environmental impact. Proof-of-work mining consumes significant electricity. The network's hashrate hit new all-time highs in early 2026, surpassing 800 exahashes per second, which corresponds to substantial energy demand. The mix of renewable energy used by miners varies considerably by region and is a persistent point of contention in ESG-focused investment contexts.

Outlook

Bitcoin enters the second half of 2026 in a structurally interesting position: on-chain activity is rising, institutional infrastructure (ETFs, lending, custody) continues to mature, and corporate accumulation at scale has become normalized. At the same time, the asset remains nearly 50% below its prior peak, ETF outflows have been the largest on record, and leverage embedded in the largest corporate holder introduces a contagion variable the market has not fully stress-tested.

The comparison that keeps circulating — Bitcoin as a smartphone-era paradigm shift, with early adopters accumulating before mainstream understanding arrives — captures the bull case. The bear case is simpler: at current network valuations, the asset still prices in an enormous amount of future adoption that has not yet materialized as sustained transaction volume or broad use as a medium of exchange. How quickly that gap closes, or whether it closes at all, is the central question Bitcoin faces heading into its next halving cycle.

Latest Bitcoin news

Michael Saylor signals another bitcoin buy as Strategy sits about $13 billion underwaterTether and Ledn plan XAUT-backed loans, turning $23B gold reserve into bitcoin-style collateralStrategy's enterprise mNAV falls below 1 for the first time, signaling investors now value the firm's capital structure below the Bitcoin held on its balance sheet Investors turn to Strategy's June 30 STRC ex-dividend date as markets await the preferred stock's monthly dividend rate reset amid heightened Bitcoin volatility

Investors turn to Strategy's June 30 STRC ex-dividend date as markets await the preferred stock's monthly dividend rate reset amid heightened Bitcoin volatility Public firms now hold over 1M BTC as Strategy, Tesla, Block and Metaplanet embrace Bitcoin treasury strategies to hedge inflation and attract investors

Public firms now hold over 1M BTC as Strategy, Tesla, Block and Metaplanet embrace Bitcoin treasury strategies to hedge inflation and attract investors Standard Chartered sees Aave outperforming Bitcoin and Ethereum through 2030, citing V4 upgrades, GHO growth, token buybacks and a 37x expansion in DeFi assets

Standard Chartered sees Aave outperforming Bitcoin and Ethereum through 2030, citing V4 upgrades, GHO growth, token buybacks and a 37x expansion in DeFi assetsCommunity notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…