In-depth explainer on Strategy, the Bitcoin-focused public company behind MSTR and STRC. Covers its Bitcoin treasury model, funding flywheel, STRC depeg, market impact, investor exposures and evolving risks in Bitcoin-linked yield products.

+37 sources across the wider coverage universe

Public firms now hold over 1M BTC as Strategy, Tesla, Block and Metaplanet embrace Bitcoin treasury strategies to hedge inflation and attract investors2026-06

Public firms now hold over 1M BTC as Strategy, Tesla, Block and Metaplanet embrace Bitcoin treasury strategies to hedge inflation and attract investors2026-06 European BTC treasury firms forge own playbook as capital market and regulatory gaps block Strategy model2026-04

European BTC treasury firms forge own playbook as capital market and regulatory gaps block Strategy model2026-04 TD Cowen trims Strategy to $350, initiates buy on four Bitcoin treasury firms with $140K BTC thesis2026-04

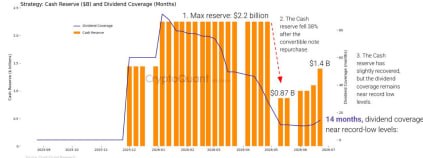

TD Cowen trims Strategy to $350, initiates buy on four Bitcoin treasury firms with $140K BTC thesis2026-04 The math is becoming harder to ignore: Strategy's annual dividend obligations have climbed to $1.2 billion, cash reserves have fallen 38% in 2026, and dividend coverage has dropped from more than seven years to only 14 months. Rebuilding liquidity may soon take precedence over additional Bitcoin purchases.2026-06

The math is becoming harder to ignore: Strategy's annual dividend obligations have climbed to $1.2 billion, cash reserves have fallen 38% in 2026, and dividend coverage has dropped from more than seven years to only 14 months. Rebuilding liquidity may soon take precedence over additional Bitcoin purchases.2026-06 Grayscale warns Bitcoin may struggle to find a sustainable bottom after Strategy's BTC sale since 2022, arguing new buyers must replace the firm's historically dominant demand2026-06

Grayscale warns Bitcoin may struggle to find a sustainable bottom after Strategy's BTC sale since 2022, arguing new buyers must replace the firm's historically dominant demand2026-06 Strive shares surged after unveiling a “daily dividend” strategy for SATA preferred stock while becoming debt-free and expanding Bitcoin holdings past 15,000 BTC2026-05

Strive shares surged after unveiling a “daily dividend” strategy for SATA preferred stock while becoming debt-free and expanding Bitcoin holdings past 15,000 BTC2026-05

Strategy: Inside Bitcoin’s Most Aggressive Corporate Treasury Bet

Strategy is a publicly traded U.S. company that has transformed itself from an enterprise software vendor into the largest corporate holder of Bitcoin, using equity and complex preferred stock structures to accumulate and hold BTC as its primary treasury reserve asset. In doing so, it has become a de facto leveraged proxy for Bitcoin in traditional equity markets, and a central player in the evolving market for Bitcoin-linked yield products such as its STRC perpetual preferred shares.

What Is Strategy?

Strategy, formerly known as MicroStrategy, began life as a business intelligence and enterprise analytics company but has since become best known as a Bitcoin-focused holding company with a still-operating software business in the background. The firm is listed on Nasdaq under the ticker MSTR and is frequently described in market coverage as a “Bitcoin giant” or “Bitcoin titan,” reflecting the fact that its market value and trading activity are now dominated by its Bitcoin strategy rather than its legacy software revenues. This dual identity is part of what makes Strategy unique: it remains an operating company with real products and customers, yet its equity has come to trade primarily as a high-beta instrument linked to Bitcoin’s price cycles.

At the core of Strategy’s evolution is a simple thesis articulated repeatedly by its founder and executive chairman, Michael Saylor: Bitcoin is a superior long-term store of value compared with cash or traditional fixed-income instruments, especially in a world of monetary expansion and low real yields. Instead of holding excess cash in dollars or short-term bonds, the company has chosen to accumulate Bitcoin on its balance sheet and to treat BTC as its primary treasury reserve asset. This move effectively transformed the corporate treasury function into an active macro bet: rather than minimizing volatility and preserving nominal capital, Strategy is intentionally concentrating its financial resources in what it views as a scarce digital asset with outsized upside over long horizons.

Bitcoin, in turn, is a decentralized digital asset governed by a fixed issuance schedule, with a maximum supply of \(21\,\text{million}\) coins enforced by the network’s consensus rules. It trades globally, 24/7, and has historically exhibited extreme volatility, with drawdowns of 50% or more occurring multiple times across market cycles. That volatility is central to Strategy’s story: it provides the potential for large mark-to-market gains when the company times issuance and accumulation well, but it also exposes the firm to substantial balance-sheet stress during bear markets, as seen both in the 2022 downturn and the more recent price slide from late-2025 highs.

Analysts and the company itself increasingly describe Strategy as a prototype “Digital Asset Treasury” or DAT, a corporation whose primary economic function is to hold digital assets—principally Bitcoin—and whose equity price is engineered to mirror and amplify Bitcoin’s moves. As Strategy’s CEO has put it, when Bitcoin rises, the firm’s digital asset treasury plan drives “outsized gains” in its common stock, and when Bitcoin falls, the shares tend to decline more sharply than the underlying asset. This engineered correlation is not accidental; rather, it is the product of a deliberate capital structure and funding model, including the use of perpetual preferred stock and at-the-market equity issuance to accumulate ever more BTC over time.

The scale of Strategy’s Bitcoin holdings underscores its centrality to the Bitcoin ecosystem. In early 2026, the company disclosed that its digital assets consisted of approximately 713,502 bitcoins, acquired at an aggregate cost of about \$54.26 billion and carrying a market value of roughly \$59.75 billion at a Bitcoin price of \$83,740. That implied an average purchase price of around \$76,052 per BTC, meaning that even modest fluctuations around those levels can swing the firm’s balance sheet between large unrealized gains and sizable paper losses. Subsequent purchases—such as discrete buys of hundreds or tens of thousands of coins—have pushed this total higher, but the underlying pattern remains constant: Strategy’s corporate identity is now inseparable from its role as a large, highly visible Bitcoin holder.

Michael Saylor signals another bitcoin buy as Strategy sits about $13 billion underwater

$335.5M of ATM issuance for $34.9M of BTC is a very different machine than the old infinite-buy meme. The marginal buyer is now underwriting STRC at distressed yields, a $1.4B USD reserve, and common dilution before they get exposure to the 847,363 BTC stack. BTC still gets a Saylor bid, but it now comes wrapped in credit-market fragility, and that reflexivity cuts both ways when MSTR trades like a funding vehicle instead of spot beta.

Readers click Strategy coverage not for Bitcoin bull thesis but for stress-testing the flywheel: whether leveraged accumulation funded by dilutive preferred stock can survive cheaper ETF wrappers and a BTC price drawdown simultaneously.↗

From Software Firm to Bitcoin Treasury Giant

Strategy’s transformation did not happen overnight. For decades, the company operated as MicroStrategy, selling business intelligence and analytics tools to enterprise customers around the world. Its revenues and valuation were tied to the growth of data warehousing, reporting, and corporate decision-support software, placing it firmly within the traditional technology sector rather than the cryptocurrency domain. This legacy business still exists and generates cash flow, but its strategic importance is now primarily as a funding source and credibility anchor for the much larger Bitcoin bet that sits on top of it. The journey from conventional software vendor to Bitcoin treasury giant illustrates how a strong-willed leadership team, access to capital markets, and a high-conviction macro thesis can reshape a public company’s identity.

The formal pivot to Bitcoin began when the company’s management decided that holding large dollar cash balances exposed shareholders to inflation risk and currency debasement, a concern amplified by expansive monetary policy and fiscal stimulus in the early 2020s. Instead of returning capital via buybacks or routing it into traditional low-yielding securities, Strategy started to purchase Bitcoin directly for its balance sheet and to characterize these purchases as a core component of long-term corporate strategy rather than a side bet or opportunistic investment. This move attracted widespread attention, both from Bitcoin advocates who hailed the company as a pioneer and from skeptics who viewed the decision as an aggressive form of speculative leverage packaged inside a public company wrapper.

As Bitcoin’s price climbed through successive bull markets, Strategy’s book gains on its BTC holdings grew rapidly, creating a feedback loop between the company’s equity valuation and its perceived success as a Bitcoin accumulator. The more Bitcoin it held, the more closely its stock traded in line with BTC, and the more it could raise in new equity or debt to purchase additional coins. The underlying software business, once the main driver of valuation, became a relatively small piece of the overall enterprise value, though it remained operationally important as a source of steady revenue and as a justification for Strategy’s continued listing as an operating company rather than an externally managed fund or trust.

Scaling the Bitcoin Balance Sheet

The magnitude of Strategy’s Bitcoin accumulation is best appreciated through its reported figures and capital-raising history. In its fourth-quarter 2025 financial results, the company disclosed that it had raised \$25.3 billion of capital during 2025 alone to advance its Bitcoin treasury strategy, making it the largest equity issuer among U.S. public companies that year. That capital took the form of common stock offerings, including at-the-market issuance programs, as well as various forms of debt and, increasingly, perpetual preferred securities such as STRC. The proceeds were primarily used to acquire additional BTC, reinforcing the company’s stated objective of expanding its Bitcoin holdings over time.

By early 2026, Strategy reported that it held approximately 713,502 bitcoins, acquired for \$54.26 billion, resulting in an average cost basis around \$76,052 per coin and a then-current market value near \$59.75 billion at a spot price of \$83,740. These figures illustrate the firm’s tolerance for volatility: even at a moment when Bitcoin traded comfortably above the company’s average purchase price, the notional swings in value associated with double-digit percentage price moves could translate into multi-billion-dollar changes in reported assets. The company supplements these large strategic acquisitions with more tactically timed purchases during market dips, such as the May 18 purchase of 24,869 BTC as the Bitcoin price slid toward \$76,000.

Strategy’s pattern of buying into weakness is not always perfectly timed. In one widely discussed episode, the company purchased 855 bitcoins for about \$75.3 million at an average price of \$87,974 per coin, funded entirely through the sale of common stock. Shortly thereafter, Bitcoin fell below \$75,000 and later dropped to around \$72,000, briefly pushing Strategy’s treasury close to \$1 billion in unrealized losses on that tranche of purchases. These episodes highlight the inherent difficulty of timing acquisitions in a volatile market and underscore the point that Strategy’s approach is less about short-term trading accuracy than about long-term accumulation, even at the cost of large interim drawdowns.

Crisis in 2022 and Post-Crisis Expansion

The inherent risk of Strategy’s approach became starkly apparent during the 2022 Bitcoin downturn, when the BTC price fell below \$16,000 and market participants questioned the sustainability of the company’s leveraged exposure. At the nadir of that drawdown, Strategy’s debt exceeded the combined value of its Bitcoin holdings and cash reserves, raising legitimate concerns about its solvency and the possibility of forced liquidations. For a period, the company served as a live test of whether a heavily indebted corporate Bitcoin holder could survive a deep and prolonged bear market without triggering systemic selling pressure.

Michael Saylor has since framed this period as a near-death experience that ultimately validated the company’s resilience. He has stated that after the 2022 downturn, Strategy raised more than \$60 billion of additional capital and deployed those funds into further Bitcoin acquisitions, turning a position where debt surpassed asset value into one where its Bitcoin and U.S. dollar reserves exceed debt by roughly \$48 billion. This narrative emphasizes the company’s ability to access capital markets even in challenging conditions and to lean into weakness by expanding its BTC holdings when sentiment is depressed. It also underscores the extent to which Strategy’s fate depends on continued investor willingness to finance its strategy.

The period following the 2022 crisis saw Strategy refine its funding model in response to the lessons learned. Reliance on traditional debt, particularly secured loans backed by Bitcoin, was seen as dangerous because falling BTC prices could trigger margin calls and forced sales at precisely the worst times. Instead, the company shifted more heavily toward equity-like instruments—common stock and perpetual preferreds—that do not carry the same kind of hard collateralized triggers but do expose existing shareholders to dilution and dividend obligations. This evolution set the stage for the design and introduction of STRC, the variable-rate perpetual preferred stock that would become both a key pillar of Strategy’s Bitcoin flywheel and, more recently, a visible point of fragility.

The Bitcoin Flywheel: Funding Model and Treasury Mechanics

The concept of a “Bitcoin flywheel” has become shorthand for describing Strategy’s self-reinforcing cycle of Bitcoin accumulation, equity market performance, and capital raising. In its simplest form, the flywheel operates as follows. Rising Bitcoin prices increase the market value of Strategy’s existing BTC holdings, which in turn boosts investor enthusiasm for the company’s stock and preferred shares. As the equity and preferred securities trade at higher valuations, the company can issue new shares at relatively attractive prices, raising capital that is then used to purchase even more Bitcoin. The new BTC adds to the balance sheet, further increasing the company’s sensitivity to Bitcoin’s price and reinforcing the perception of Strategy as a leveraged Bitcoin vehicle.

This mechanism works powerfully in both directions. When Bitcoin enters a sustained downtrend, Strategy’s equity tends to fall even more sharply, as investors reprice both the company’s existing BTC holdings and its ability to raise fresh capital to expand those holdings. A decline in the market price of its preferred shares, particularly STRC, can effectively shut down a key channel for funding new Bitcoin purchases, because issuing preferreds significantly below their par value or intended trading range becomes economically unattractive. In such environments, Strategy faces a more constrained set of options: rely on common equity issuance at depressed prices, tap cash reserves, seek alternative financing, or—if conditions worsen—consider selling some Bitcoin to meet obligations.

Capital-Raising Channels and Balance-Sheet Design

Strategy’s recent capital structure has three main legs: common equity, perpetual preferred equity, and, to a lesser extent than in the past, debt. On the equity side, the company has relied heavily on at-the-market (ATM) offerings, which allow it to issue small quantities of stock into the open market over time, rather than in a single large block. This approach lets Strategy opportunistically raise capital when trading volumes and demand for its shares are strong, particularly during periods when Bitcoin’s price is rising and MSTR trades at a premium to the value of the underlying BTC holdings. These equity raises are inherently dilutive, but the dilution can be more than offset by the incremental Bitcoin acquired if BTC appreciates over time.

Debt has historically played a role, notably via convertible notes that allowed Strategy to borrow at relatively low interest rates while giving investors the option to convert into equity if the stock appreciated. However, the 2022 downturn revealed the risks of relying too heavily on leverage backed by volatile collateral, especially when market conditions tighten and risk premiums rise. In a higher-rate environment, fresh debt financing becomes more expensive, and the risk of entering into unfavorable covenants or collateral arrangements increases. Consequently, Strategy has emphasized perpetual preferred equity, particularly STRC, as a more flexible tool that combines the characteristics of fixed-income securities with the equity-like nature of perpetual capital.

The company’s own disclosures highlight the extent of its capital-raising activity. In 2025, Strategy reported raising \$25.3 billion of capital specifically to advance its Bitcoin treasury strategy, a figure that underscores both the aggressiveness and the scale of the flywheel. Saylor has also noted that the firm raised more than \$60 billion in additional capital after the 2022 downturn, a period during which it significantly expanded its BTC stack. These numbers illustrate how Strategy’s Bitcoin strategy is as much about engineering and maintaining access to capital markets as it is about selecting an asset to hold; without fresh capital, the flywheel slows, and the company’s ability to accumulate additional Bitcoin diminishes.

Equity as Leveraged Bitcoin Exposure

From an investor’s perspective, Strategy’s common stock functions as a leveraged Bitcoin exposure, with an embedded operating business attached. Market performance bears this out. Coverage has noted episodes where Strategy’s shares sank more than 20% over a five-day stretch as Bitcoin itself dropped to around \$72,000, highlighting the “tight correlation” between MSTR and the underlying digital asset. On a single trading day, the stock has been observed falling about 9% while Bitcoin slid toward multi-week lows, reinforcing the view that MSTR acts as a high-beta proxy for BTC in traditional equity markets.

This leverage arises from several sources. First, Strategy’s balance sheet holds a large quantity of Bitcoin relative to its equity capital, so price movements in BTC translate into substantial changes in net asset value per share. Second, because the company has used debt and preferred equity to finance a portion of its holdings, movements in Bitcoin’s price affect not only the value of assets but also the level of coverage over fixed obligations, which can prompt outsized reactions in equity valuations. Third, the market often prices in expectations about future capital raises: when sentiment is strong, investors may assume that the company will be able to issue additional equity at high prices and buy more Bitcoin, effectively bootstrapping its way into even higher exposure.

This reflexivity has made Strategy’s stock a favorite among some Bitcoin bulls who want more than one-to-one exposure to BTC but also attracts criticism from those who see it as an unnecessarily complex and risky way to express a Bitcoin view. For traders, MSTR offers deep liquidity and the ability to gain Bitcoin-linked exposure within traditional brokerage accounts, without dealing with wallets or custodians. For fundamental investors, however, the stock embeds several layers of risk that are absent in direct Bitcoin ownership: corporate governance, capital allocation decisions, regulatory risk, and the sustainability of the company’s funding model. Understanding these layers is crucial, particularly when the company introduces innovative but complex instruments like STRC into the capital stack.

Preferred Equity as Funding Stabilizer

The introduction of STRC, a variable-rate perpetual preferred stock with a target trading price of \$100 per share, was designed to add a relatively stable funding leg to Strategy’s flywheel. Unlike common equity, which is inherently volatile and fully exposed to upside and downside in the business, preferred stock typically offers a fixed or variable dividend and sits higher in the capital structure, providing a more bond-like profile for investors seeking income. STRC was engineered to pay dividends at a rate that could be adjusted to keep the security trading close to its par value, effectively creating a Bitcoin-linked yield product that, in theory, would offer Bitcoin believers income “without the volatility” of MSTR’s common stock.

Michael Saylor has said that STRC’s design emerged from an unusual process: he claims to have used artificial intelligence to scan U.S. securities markets and identify a structure that had never been attempted but was legally feasible. According to his account, the AI spent about ten minutes analyzing existing instruments and concluded that no one had ever created a variable-rate perpetual preferred tied to a Bitcoin treasury, yet nothing in the regulations prevented it. This anecdote underscores both the novelty of STRC and the experimental nature of Strategy’s financing approach. It also hints at the potential risks: unprecedented structures lack historical performance data, and investors must rely on theoretical models and issuer assurances rather than long track records.

In practice, STRC’s role in the flywheel is straightforward. When the security trades near or above its target \$100 par value, Strategy can issue new STRC shares via an at-the-market program, raising capital that is then used to buy more Bitcoin. Because STRC sits above common equity in the capital structure and carries dividend obligations, it offers a way to raise relatively patient capital from income-focused investors while leaving the common stock to absorb most of the volatility. However, this mechanism depends critically on STRC maintaining its intended trading range. When the preferred falls significantly below par, issuing more of it becomes less attractive and potentially destabilizing, weakening one of the key funding levers in Strategy’s accumulation strategy.

Strategy's enterprise mNAV falls below 1 for the first time, signaling investors now value the firm's capital structure below the Bitcoin held on its balance sheet

$1.2B of annual preferred dividends against roughly $1.4B of cash is the reflexivity problem Saylor tried to securitize away. STRC trading about 25% below par turns every future raise into a cost-of-capital test, because plugging the reserve with common stock dilutes the exact premium the machine depends on. Metaplanet and Nakamoto already below 1x enterprise mNAV puts the BTC treasury trade in a harsher regime: buy-and-hold is easy, funding the hold without a premium bid is the part markets are repricing.

- 01Saylor accumulation flywheel sustainability↗

Headlines asking 'is more buying coming?' and tracking each purchase signal readers are monitoring whether the self-reinforcing BTC-buy loop can keep running as ETF competition and preferred-stock costs mount.

- 02Preferred stock dilution mechanics↗

STRK and STRC issuance drew readers because they introduced a new shareholder-harm vector — selling yield-bearing equity to fund BTC buys — that most retail holders hadn't modeled.

- 03BlackRock ETF displacing MSTR↗

The ETF accumulating 4% of all bitcoin faster than MicroStrategy reframes MSTR's 'BTC proxy' premium as unnecessary cost rather than unique access.

- 04DeFi clones of Saylor model

ETH Strategy and similar permissionless protocols attracted clicks as readers assessed whether replicating the corporate treasury playbook on-chain creates leverage risk without equity guardrails.

- 05Geopolitical stablecoin rivalry

ECB warnings about dollar-backed crypto threatening Eurozone banks framed the U.S. stablecoin strategy as a geopolitical weapon, elevating the stakes beyond corporate treasury.

- 06Corporate treasury Bitcoin adoption pressure↗

Activist calls for Big Tech to copy MicroStrategy and El Salvador reversing mandatory BTC acceptance show readers tracking the real-world limits of the 'Bitcoin standard' corporate playbook.

STRC Preferred Stock: Design, Depeg and Systemic Risks

STRC occupies a unique niche at the intersection of corporate finance, Bitcoin exposure, and yield-seeking investor demand. It is structured as a perpetual, variable-rate preferred stock with a par value of \$100 and a dividend policy designed to keep the market price near that par. Unlike traditional preferred shares that offer a fixed coupon, STRC’s dividend can adjust based on prevailing market conditions and the company’s objectives, allowing Strategy to fine-tune the yield in response to investor appetite and Bitcoin’s volatility. In theory, this flexibility enables the firm to offer an income product that remains relatively stable in price while deriving its economic backing from an underlying Bitcoin treasury.

The target audience for STRC consists of investors who share Strategy’s bullish long-term view on Bitcoin but are uncomfortable with the day-to-day price swings associated with owning BTC directly or holding MSTR common stock. By purchasing STRC, these investors receive regular cash dividends funded by the company’s operations and capital-raising activity, with the security’s price intended to hover around \$100 through yield adjustments. Saylor has positioned this as a way for “Bitcoin believers” to gain exposure to the asset’s long-term monetization without suffering full mark-to-market volatility, though real-world trading has demonstrated that the preferred is far from risk-free.

Peg Mechanics and Income Promises

The “peg” of STRC to \$100 is not a hard peg in the sense of a guaranteed redemption value at par; rather, it is a soft target maintained through a combination of dividend policy and market expectations. If STRC trades above \$100, the yield implied by its dividend becomes relatively less attractive, which should, in theory, reduce demand and encourage issuance until the price drifts back toward par. Conversely, if the price falls below \$100, the yield rises, potentially attracting buyers who view the income as attractive relative to the risk and thereby pushing the price back up. Strategy can also adjust the dividend rate, within certain constraints, to entice buyers or moderate demand, using payout frequency and level as tools to influence trading behavior.

In practice, Strategy has experimented with these levers. Initially, STRC paid dividends monthly, but the company later shifted to twice-monthly payments in an effort to reduce post-dividend price drops and smooth the trading pattern. The logic was that more frequent, smaller payouts might lessen the tendency for the stock to fall immediately after going ex-dividend, thereby supporting a more stable price around par. Meanwhile, competitor products such as Strive Asset Management’s SATA opted for even more frequent payments, moving to daily dividend distributions while offering a headline yield around 13%, a move widely interpreted as an attempt to outcompete STRC on perceived income attractiveness.

Despite these engineering efforts, the peg mechanism has limitations. It assumes that investors will respond to incremental changes in yield in a predictable way and that there will be sufficient demand for Bitcoin-linked income products at yields achievable within Strategy’s economic constraints. During periods of market stress, however, the risk premium demanded by investors may rise sharply, particularly if they perceive heightened credit or structural risk in the issuer. In such conditions, even substantial increases in the dividend rate may be insufficient to keep the preferred’s price near par, leading to sustained deviations—“depegs”—that reveal deeper concerns about the underlying funding model and risk-sharing arrangement.

Depeg Episodes and Market Reaction

Recent trading in STRC has illustrated how quickly the peg can break under adverse conditions. In one documented episode, STRC fell below \$83, roughly 17% under its intended \$100 par value and its lowest level since debuting in July 2025. At another point, the security briefly touched lows around \$82.70 before recovering slightly to close near \$88.80, with the decline coinciding with a broader slide in Bitcoin’s price and negative interest-rate news that weighed on risk assets. Other coverage has noted STRC trading near \$85 after briefly hitting \$84.88, a drop of about 15% from par, as Bitcoin extended a broader market decline. These sustained discounts to target levels constitute a meaningful depeg, not just a transient fluctuation.

The timeline around these depegs underscores the interplay between Bitcoin’s price, competitive pressures, and Strategy’s own corporate actions. According to one reconstruction, Bitcoin had already fallen significantly from its October record of about \$126,000, and STRC was only managing to hold \$100 in the run-up to its ex-dividend date, not consistently throughout the month. As Bitcoin continued to drop, sliding toward \$78,000 and below, investor worries about Strategy’s balance sheet and the sustainability of its dividend commitments intensified. At the same time, Strive’s SATA was offering a higher yield around 13% and had just shifted to daily dividend payments, increasing competitive pressure precisely as Strategy sought shareholder approval to adjust STRC’s payout frequency from monthly to semi-monthly.

External commentators have interpreted the STRC plunge as a sign that a crucial leg of Strategy’s financing mechanism is under strain. One analysis argued that the drop in the preferred shares had “effectively shut down” a key funding channel, since issuing more STRC at such a deep discount would be unattractive for both the company and investors. Another described the fall in STRC as evidence of fragility in Strategy’s capital structure, noting that when the preferred trades well below par, the firm must rely more heavily on common equity issuance, cash reserves, or alternative financing, all of which may be less efficient or more dilutive. Crypto-market coverage has further suggested that these concerns about Strategy’s funding model have contributed to broader volatility in Bitcoin and crypto markets, as traders price in the possibility of reduced corporate demand or even forced sales.

Competitive Landscape: SATA, BITA and Other Yield Products

STRC does not exist in a vacuum. It is part of a broader ecosystem of Bitcoin-linked yield instruments designed to appeal to investors who want some exposure to BTC but prefer a steady income stream and familiar wrappers such as preferred stock or ETFs. Strive Asset Management’s SATA is one such competitor—another preferred stock tied to a Bitcoin-related strategy that has moved to daily dividend payments and advertises a yield around 13%. Like STRC, SATA has experienced trading below its intended par value, suggesting that the pressures affecting Bitcoin-linked preferred equity are not unique to Strategy but reflect structural sensitivity to underlying crypto volatility and broader risk sentiment.

Another notable competitor in this space is BlackRock’s iShares Bitcoin Premium Income ETF (BITA), a fund that seeks to track the performance of Bitcoin while generating additional income through an actively managed options strategy. According to BlackRock, BITA invests in Bitcoin and then sells options—typically covered calls—against its holdings, using the option premiums to pay out regular distributions to shareholders. This approach places BITA in the broader category of “options income ETFs,” which are actively managed funds that invest in a portfolio of assets and systematically sell options to generate premiums, with the primary goal of delivering recurring income in a simple, tradable ETF structure. Commentary has framed BITA as “competing with Strategy,” with reported target yields in the 15–25% range, positioning it as an alternative for investors seeking Bitcoin-linked income without the idiosyncratic corporate risk associated with a single issuer.

The emergence of SATA, BITA, and similar products reveals a meaningful demand segment within the crypto-investing public: those who want Bitcoin exposure but are dissatisfied with the asset’s lack of native yield compared to staking-based systems like Ethereum. Saylor himself has argued that Bitcoin does not need Ethereum-style yield and that its “yield” is effectively embedded in long-term price appreciation, yet the existence of STRC indicates that Strategy also recognizes the commercial appeal of yield-bearing Bitcoin proxies. At the same time, Adam Back and other long-time Bitcoiners emphasize more conservative strategies such as dollar-cost averaging—investing equal amounts at regular intervals regardless of price—as a way to manage volatility without resorting to leverage or complex yield structures. The tension between these philosophies is central to the debate over Bitcoin-linked income products.

Complexity, Disclosure and Regulatory Questions

The novelty and complexity of STRC raise important questions about disclosure, suitability, and regulatory oversight. By Saylor’s own account, the structure is unprecedented—an AI-driven search of prior securities apparently found no historical analogs—so investors lack a long data set to evaluate how such an instrument behaves across full market cycles. The security blends elements of preferred equity, variable-rate income, and exposure to a volatile underlying asset, all within the context of a corporate issuer whose fortunes are deeply tied to Bitcoin. For sophisticated institutional investors, these nuances may be manageable, but for retail buyers attracted by headlines about high yields and Bitcoin-backed dividends, the risk of misunderstanding is significant.

Criticism from within the Bitcoin policy community has focused on the way STRC is marketed and explained to the public. Some advocates and commentators have described aspects of the promotional messaging as misleading or “dishonest,” particularly when it implies that STRC offers Bitcoin-like upside with reduced volatility and minimal additional risk. While such characterizations are contested, they underscore the degree of skepticism that exists even among Bitcoin supporters toward complex financial engineering layered on top of BTC. Unlike a simple spot Bitcoin ETF, which directly tracks the underlying asset’s price, STRC exposes investors to issuer-specific risks including dividend coverage, capital-raising capacity, and governance decisions about when and whether to sell BTC to meet obligations.

Regulators have not, as of this writing, taken public enforcement action specifically targeting STRC-like instruments, but the broader environment for high-yield, complex products remains under scrutiny. The combination of novel structure, retail marketing, and embedded exposure to volatile crypto assets makes STRC a likely candidate for close attention, especially if losses mount or if a major dislocation forces Strategy to restructure its obligations. For crypto-market observers, therefore, STRC is not just another preferred stock; it is a live experiment in how far Bitcoin-linked financial innovation can stretch within the existing securities framework before encountering legal, reputational, or systemic constraints.

Strategy’s Role in Bitcoin and Crypto Markets

Because of its scale and visibility, Strategy has become a market-moving participant in Bitcoin and, by extension, in the broader crypto ecosystem. With more than 700,000 bitcoins on its balance sheet at various times, the company is one of the largest single corporate holders of BTC, rivaling or exceeding many exchange-traded products and surpassing most hedge funds and institutional allocators. Each time Strategy announces a new acquisition—whether a large lump-sum purchase of tens of thousands of coins or a smaller tactical buy—market participants scrutinize the timing, size, and funding source for clues about corporate demand and the health of the firm’s capital-raising machinery.

The company’s buying and selling activity can influence Bitcoin’s price both directly and indirectly. Directly, large acquisitions create immediate buy-side pressure in the spot market, especially if executed over a short window or via block trades that tighten available liquidity. Indirectly, Strategy’s announcements shape sentiment: when the firm buys aggressively into price weakness, bulls often interpret this as a sign of long-term confidence and a potential floor, while any indication of selling can trigger fears of broader deleveraging. Standard Chartered and other macro analysts have begun treating Strategy’s moves as one among several signals when assessing potential Bitcoin bottoms, noting that episodes of sharp corporate-related selling or funding stress can coincide with capitulation phases.

Sentiment, Narratives and Bitcoin Maximalism

Michael Saylor has emerged as one of Bitcoin’s most prominent corporate evangelists, repeatedly articulating a maximalist view that regards BTC as superior to all other monetary and investment assets over multi-decade horizons. His framing of Bitcoin as “digital energy” or “digital property” and his public explanations of Strategy’s treasury policy have influenced not only his own shareholders but also other high-net-worth individuals and corporate decision-makers. Saylor’s story of having led Strategy through the 2022 crisis—when debt briefly exceeded the combined value of Bitcoin and cash reserves—only to emerge with massively larger holdings and a reported \$48 billion cushion of BTC and USD over debt, reinforces a narrative of resilience that appeals to committed Bitcoin believers.

This narrative resonates with other billionaire Bitcoin advocates, such as Ricardo Salinas, who has explained his personal accumulation strategy in similarly uncompromising terms. Salinas has said that his approach is straightforward: as soon as he gets his hands on fiat currency, he converts it into Bitcoin, advising ordinary investors to treat BTC like a long-term asset and to avoid obsessing over daily price movements. He has even suggested that, for many people, converting home equity into Bitcoin may be a rational strategy if they share his conviction about BTC’s long-term trajectory. While such views are controversial and not universally accepted even within the Bitcoin community, they illustrate the high-conviction mindset that also underpins Strategy’s corporate behavior.

The tension between simple, long-horizon strategies like dollar-cost averaging into Bitcoin and more complex, leveraged approaches like Strategy’s flywheel is increasingly visible in community debates. Adam Back, a long-time Bitcoin developer and CEO of Blockstream, has emphasized that dollar-cost averaging is a conservative approach well-suited to volatile assets such as BTC, particularly given the dangers of leverage. His comments that some recent Bitcoin selling might have been driven by liquidations rather than fundamental shifts in long-term investor behavior underscore the risk of overinterpreting short-term price moves as changes in structural demand. Against this backdrop, Strategy’s aggressive financial engineering can be seen either as a sophisticated extension of the HODL ethos or as a departure from it, depending on one’s tolerance for complexity and systemic risk.

Leverage, Liquidations and Feedback Loops

Strategy’s capital structure is embedded in a broader landscape of leveraged Bitcoin exposure, from futures and options to crypto derivatives on exchanges and structured products held by institutions. When Bitcoin’s price falls sharply, this ecosystem is prone to cascades of forced selling as leveraged positions hit margin calls, collateral values drop, and liquidity dries up. Strive, the manager behind SATA, has directly blamed leverage liquidations for plunges in both its own preferred stock and Strategy’s STRC, suggesting that investor panic and forced deleveraging across crypto markets contributed to the drawdown rather than fundamental credit deterioration alone.

Adam Back has made similar observations about Bitcoin price dynamics, noting that temporary episodes of selling pressure can stem from liquidations linked to leveraged traders or specific structured products, even when broader stock indexes remain stable. In such episodes, large Bitcoin holders like Strategy can find themselves caught in a feedback loop: falling BTC prices hurt their balance sheets and funding capacity, which in turn raises market concerns about potential sales or funding shortfalls, further pressuring Bitcoin as traders front-run possible corporate moves. This dynamic was visible when coverage highlighted worries about “Strategy selling” as a factor in Bitcoin’s slide to new short-term lows, even when the company had not publicly announced any large disposals.

The interaction between Strategy’s preferred stock and Bitcoin markets adds another layer to this feedback loop. When STRC trades far below par, undermining its usefulness as a funding tool, investors may fear that the company will eventually need to tap other sources of liquidity, including selling some BTC, to meet dividend and operating obligations. Strategy itself has acknowledged in disclosures that in stress scenarios, depletion of reserves could necessitate Bitcoin sales to meet obligations, highlighting the interconnected nature of its balance sheet. The mere possibility of such sales can become self-fulfilling if markets front-run them, emphasizing the importance of confidence and expectations in maintaining the flywheel.

Interactions with ETFs and Institutional Flows

Strategy is no longer the only way for mainstream investors to gain exposure to Bitcoin through traditional financial infrastructure. The launch and expansion of spot Bitcoin ETFs, as well as specialized products like BlackRock’s BITA, provide alternative channels that may compete for capital with MSTR and STRC. Spot ETFs hold Bitcoin directly and issue shares that track the asset’s price, offering a simpler and more transparent structure than a corporate vehicle whose value is mediated through operating businesses, leverage, and complex preferred equity. Options income ETFs like BITA go a step further by overlaying a covered-call strategy on top of Bitcoin holdings, generating option premium that can be distributed as yield.

According to BlackRock, BITA is designed to track Bitcoin’s performance while generating “premium income” through an actively managed options program, situating it within a broader class of options-income ETFs that aim to deliver regular distributions from option-selling strategies. Commentary has suggested that BITA may target yields in the 15–25% range and is framed, at least in part, as a competitor to Strategy’s yield-oriented products, particularly for investors who prefer an ETF wrapper to corporate preferred stock. The success of such ETFs could impact Strategy in two ways: by providing a benchmark for what constitutes an attractive Bitcoin-linked yield and by drawing away incremental capital that might otherwise have flowed into MSTR or STRC.

Institutional allocators, meanwhile, may view Strategy’s instruments and Bitcoin ETFs as complementary rather than directly competing. A multi-asset portfolio might hold a mix of spot Bitcoin, ETFs like BITA, and corporate exposures like MSTR to express different risk-return preferences and liquidity needs. However, in periods of stress or when Bitcoin is out of favor relative to other themes—such as the current Wall Street emphasis on AI and data center financing—capital can rotate away from Bitcoin-linked vehicles in general. Saylor himself has noted that markets appear to be in an “AI summer,” with Wall Street promoting AI financing deals that temporarily siphon capital from Bitcoin, but he has argued that capital could flow back into BTC by year-end as relative valuations and themes shift.

Macro Influences: Interest Rates and Thematic Rotations

Strategy’s trajectory cannot be understood in isolation from broader macroeconomic conditions. Rising interest rates increase the opportunity cost of holding non-yielding assets like Bitcoin and raise the hurdle rate for leveraged strategies that depend on cheap capital. Coverage has linked Bitcoin’s slide back toward the \$60,000 level not only to concerns about Strategy’s unraveling funding model but also to apprehensions about further interest-rate increases that suppress appetite for riskier investments. When risk-free yields on government bonds are more attractive, some investors may be less willing to fund highly levered, volatile propositions like Strategy’s Bitcoin flywheel, putting pressure on both BTC and Strategy’s securities.

Thematic rotations also matter. In phases when AI, green energy, or other sectors capture market imagination, capital may flow into those sectors at the expense of Bitcoin and related vehicles. Saylor’s commentary about an ongoing “AI summer” reflects this reality, as capital allocators prioritize data center financing and AI infrastructure deals over additional Bitcoin allocations. Yet thematic cycles are not static; they ebb and flow as valuations shift and narratives evolve. For Strategy, the key question is whether its funding model can survive prolonged periods of relative neglect or risk aversion, and whether it can capitalize on renewed Bitcoin enthusiasm when the pendulum swings back.

Investors turn to Strategy's June 30 STRC ex-dividend date as markets await the preferred stock's monthly dividend rate reset amid heightened Bitcoin volatility

$73 STRC against $100 par puts the pref at a ~15% effective yield, junk-credit math wrapped around a BTC treasury trade. If Strategy keeps ratcheting the coupon while MSTR sits near $85 and BTC chops around $58k-$60k, the flywheel shifts from BTC-per-share accretion to cash-reserve defense. $0.48 is dust; the market will care more about whether new paper still clears without recursive dilution or another BTC sale to protect the pref stack.

MicroStrategy makes first Bitcoin treasury purchase

BTC falls below $16K; MicroStrategy margin crisis scrutinized

BlackRock iShares Bitcoin ETF launches, begins rapid BTC accumulation

- 2024-10milestone

Bernstein initiates MSTR coverage at outperform, $2,890 target citing $1M BTC in 10 years

Strategy reports Q4 2025 results; BTC holdings reach 244,800 BTC at $9.45B

Strategy introduces STRK preferred stock, triggering shareholder dilution debate

Bloomberg reports STRC depeg and Strategy funding flywheel under stress as BTC slides toward $60K

Investment Exposure: Evaluating Strategy-Linked Instruments

For crypto-market participants, Strategy represents not only a corporate case study but also a set of investable instruments that provide different forms of Bitcoin exposure. The two primary securities are MSTR common stock, which offers leveraged directional exposure to Bitcoin plus an embedded operating business, and STRC preferred stock, which offers income-oriented exposure tied to Strategy’s Bitcoin treasury and capital-raising capacity. Investors may also consider competing products such as Strive’s SATA preferred and BlackRock’s BITA ETF, each with its own risk profile and structural features. Understanding how these instruments differ from holding Bitcoin directly or through spot ETFs is essential for informed allocation.

MSTR Stock for Directional Bitcoin Exposure

MSTR functions as a high-beta Bitcoin proxy with an added layer of company-specific risk. Empirically, the stock’s price often moves in greater percentage terms than Bitcoin itself, both upwards and downwards, reflecting the leverage embedded in Strategy’s balance sheet and the market’s expectations about future capital raises. In one recent episode, Strategy’s shares plunged more than 20% over five days as Bitcoin crashed to around \$72,000, illustrating how equity investors may react more violently than Bitcoin holders during drawdowns. On that same day, the stock fell roughly 9% intraday, underscoring its sensitivity and making clear that MSTR is not a low-volatility alternative to BTC but rather a more extreme version of it.

Investors considering MSTR must evaluate not just their view on Bitcoin but also their confidence in Strategy’s management, governance, and capital allocation decisions. The company’s ability to issue shares at favorable prices, avoid destructive dilution, and manage dividend and interest obligations is crucial to the long-term equity story. While Saylor’s track record in steering the firm through the 2022 crisis and aggressively expanding the balance sheet since then inspires confidence among many Bitcoin bulls, skeptics point out that success so far has been heavily reliant on buoyant capital markets and supportive macro conditions. A prolonged Bitcoin bear market combined with tighter credit conditions could stress-test the model more severely than past episodes.

From a portfolio-construction standpoint, MSTR may appeal to traders and investors who want amplified exposure to Bitcoin within traditional brokerage accounts, perhaps in jurisdictions or account types where direct Bitcoin custody is inconvenient or constrained. It can also serve as a tactical instrument for expressing views on Bitcoin’s short- to medium-term direction, given its high liquidity and responsiveness. However, for long-term allocators seeking pure Bitcoin exposure, the additional idiosyncratic risks inherent in MSTR—including corporate governance, regulatory scrutiny, and the possibility of strategic missteps—mean that the stock cannot be treated as a simple substitute for holding BTC itself.

STRC and Preferreds for Income-Oriented Investors

STRC was designed as an income-oriented instrument for investors who share Strategy’s bullishness on Bitcoin but prefer a more bond-like security that pays regular dividends. As a perpetual, variable-rate preferred stock, STRC sits above common equity in the capital structure and carries defined dividend obligations, giving holders contractual claims that common shareholders lack. The intended trade-off is clear: investors accept a capped upside relative to MSTR in exchange for steadier income and, in theory, a more stable trading price around the \$100 par level. In practice, however, the recent depegs have demonstrated that STRC’s price can be quite volatile under stress, especially when market doubts about Strategy’s funding model and balance-sheet resilience intensify.

An additional complexity is that STRC’s dividends are ultimately funded by the same underlying economics that drive Strategy’s common stock: Bitcoin price appreciation, operating cash flows, and continued access to capital markets. When Bitcoin trades below the company’s average purchase price—around \$76,056 per BTC at one point—Strategy’s holdings may show sizable unrealized losses, as was the case when BTC traded near \$67,422, generating approximate paper losses of \$6.1 billion. In such environments, the coverage ratio of preferred dividends becomes a topic of investor scrutiny, and the security’s yield may need to rise to compensate for these perceived risks, putting downward pressure on the price.

Income-focused investors comparing STRC to alternatives like SATA and BITA must weigh the trade-offs between issuer-specific and structural risks. SATA, as another Bitcoin-linked preferred stock, shares many of STRC’s characteristics, including sensitivity to Bitcoin volatility and reliance on a specific issuer’s capital-raising and treasury management approach. BITA, by contrast, is an ETF that uses covered-call options to generate income on top of Bitcoin holdings, exposing investors to option-premium risk and capped upside but avoiding direct exposure to a single corporate balance sheet. For some, the ETF’s diversified structure and regulatory framework may be more appealing; for others, the explicit corporate backing and narrative around Strategy may hold greater attraction.

Comparing Strategy Instruments to Direct BTC and ETFs

A useful way to visualize the differences among these exposure options is to compare their key structural features and risk factors side by side. The following table provides a simplified snapshot of how direct Bitcoin holdings, spot ETFs, MSTR common stock, STRC preferred stock, and BITA-style options income ETFs differ along several dimensions.

| Instrument | Structure | Underlying Exposure | Income Source | Key Risks |

|---|---|---|---|---|

| Direct BTC | On-chain asset or custodial claim | 1:1 Bitcoin price | None (unless lending) | Price volatility; custody and security; regulatory treatment |

| Spot BTC ETF | Fund holding Bitcoin | 1:1 Bitcoin price (minus fees) | None (aside from potential lending) | Price volatility; fund fees; ETF-specific risks |

| MSTR stock | Operating company equity | Bitcoin plus software business | None (no regular dividend) | High volatility; leverage; dilution; corporate governance |

| STRC preferred | Perpetual variable-rate preferred stock | Strategy’s Bitcoin treasury and operations | Cash dividends set by issuer policy | Price and credit risk; depeg risk; issuer-specific funding model |

| BITA-style ETF | Bitcoin ETF with covered-call strategy | Bitcoin plus options overlay | Option premiums distributed as income | Capped upside; option-pricing risk; path dependence |

This table is necessarily simplified, but it underscores that Strategy-linked instruments are not interchangeable with direct Bitcoin or spot ETFs. MSTR and STRC introduce layers of corporate and structural risk that do not exist when holding BTC outright, while BITA-like funds introduce derivatives-related complexity. For some investors, these additional risks are acceptable or even desirable, given the potential for enhanced income or leveraged upside; for others, they may be unnecessary complications that detract from the core investment thesis.

Behavioural and Portfolio-Construction Considerations

Beyond structural differences, behavioural factors play a significant role in determining which exposure path is appropriate for a given investor. Direct Bitcoin ownership requires comfort with private-key management, exchange risk, and the psychological challenge of enduring large drawdowns with no offsetting income stream. Strategy’s instruments, by contrast, allow investors to access Bitcoin-linked exposure through familiar brokerage accounts and receive regular statements, dividends, and corporate disclosures, which may feel more manageable to those used to traditional securities. However, this familiarity can be deceptive if it leads investors to underestimate the volatility and complexity embedded in MSTR, STRC, or similar instruments.

For long-term allocators aligned with the maximalist view articulated by Saylor and Salinas, simple strategies like dollar-cost averaging into Bitcoin for 5–10 years may be more consistent with their goals than attempting to optimize yield through complex structures. The temptation to chase high headline yields, whether in STRC, SATA, or options income ETFs, must be weighed against the risk that such yields come hand-in-hand with hidden forms of leverage, path dependence, or issuer-specific credit exposure. As Adam Back has noted, leverage is particularly dangerous in volatile assets, and many investors underestimate the long-run benefits of patience and simplicity.

Ultimately, whether and how to use Strategy-linked instruments is a question of risk tolerance, time horizon, and understanding. For those who grasp the mechanics of the Bitcoin flywheel, are comfortable with corporate risk, and desire either leveraged upside (via MSTR) or income (via STRC), Strategy can be an intriguing but speculative part of a broader crypto portfolio. For those seeking straightforward exposure to Bitcoin’s long-term monetary thesis, direct BTC ownership or spot ETFs may suffice. In all cases, the key is to recognize that Strategy is not “just Bitcoin in equity form” but a distinct, complex financial entity whose fortunes are intertwined with—but not identical to—the underlying asset.

Risk Factors and Criticisms

Strategy’s prominence and innovation have naturally attracted scrutiny and criticism, both from traditional financial analysts and from within the Bitcoin community itself. The very features that make the company a compelling case study—the aggressive use of leverage, the experimental capital structure, the dependence on capital markets, and the marketing of novel yield products—also represent key risk factors. These risks manifest at multiple levels: balance-sheet solvency, shareholder dilution, market contagion, and reputational or regulatory pushback.

Leverage, Solvency and Path Dependence

The 2022 crisis made clear that Strategy’s survival is intimately linked to Bitcoin’s price path. At Bitcoin’s lows near \$16,000, the company’s debt exceeded the combined value of its BTC holdings and cash, raising questions about potential insolvency and forced liquidation. While Strategy ultimately navigated this period by raising over \$60 billion in additional capital and expanding its Bitcoin position, the episode highlighted the path dependence of its strategy: success depends not just on where Bitcoin ends up in 10 or 20 years, but also on the sequence of prices in between and the company’s ability to finance itself through downturns.

Leverage amplifies this path dependence. When Bitcoin prices rise, leverage magnifies gains, allowing the company to report substantial improvements in net asset value and to raise new capital on favorable terms. When prices fall, the same leverage magnifies losses and compresses the cushion protecting creditors and preferred shareholders, potentially triggering changes in market sentiment or covenant breaches. The fact that Strategy now reports its Bitcoin and USD reserves as exceeding its debt by tens of billions does not eliminate this risk; a sufficiently deep and prolonged downturn could reverse that coverage again, particularly if access to new capital is constrained.

Funding-Model Fragility and Dilution Risk

The fragility of Strategy’s funding model has become more apparent as STRC has traded persistently below par. When the preferred stock trades near \$100, the company can issue additional shares via its at-the-market program, raising capital to buy more Bitcoin and continuing to spin the flywheel. However, when STRC trades around \$85 or lower, as it has during recent depegs, issuing new preferred equity becomes less attractive and potentially more expensive, especially if investors demand even higher yields to compensate for perceived risk. Under such conditions, Strategy may need to lean more heavily on common equity issuance, which can be significantly more dilutive when MSTR trades at depressed prices.

Bloomberg analysis has framed the plunge in Strategy’s preferred securities as having “effectively shut down” a key leg of its financing mechanism, underscoring how reliant the company has become on this particular instrument. Additional commentary has linked Bitcoin’s slide back toward the \$60,000 level to concerns about the unraveling of Strategy’s funding model, suggesting that equity and preferred investors are reassessing the sustainability of the flywheel in a higher-rate environment with less risk appetite. If the company is unable to restore confidence in STRC’s stability or to find alternative, non-dilutive funding sources, it may be forced to slow its Bitcoin accumulation or even consider asset sales to meet obligations, both of which would mark a significant shift from its prior posture.

Moral Hazard and Narrative Risk in Yield Marketing

Strategy’s promotion of STRC as a pathway for “Bitcoin believers without the volatility” has raised concerns about moral hazard and narrative risk. While the preferred stock is designed to offer a more stable experience than the common equity, its recent price behavior demonstrates that it can still experience double-digit percentage drawdowns and sustained deviations from par. Critics argue that emphasizing the Bitcoin connection and the stability of the par target without equally emphasizing the potential for depegs and issuer-specific risks may leave some investors with an incomplete understanding of what they are buying.

Within the Bitcoin ecosystem, there is a broader wariness of yield promises, shaped by the collapse of prior “crypto yield” platforms such as centralized lenders and DeFi protocols that offered high returns only to fail during stress events. While STRC is structurally different—it is a regulated security issued by a public company rather than an offshore lending scheme—the psychological appeal of high, seemingly reliable yields backed by Bitcoin is similar. If STRC were to experience deeper losses or require restructuring, the reputational fallout could extend beyond Strategy to Bitcoin itself, reinforcing narratives that BTC is primarily a vehicle for speculative, yield-chasing schemes rather than a straightforward hard-money asset.

Systemic and Contagion Considerations

Because Strategy is such a large holder of Bitcoin, its balance-sheet decisions carry systemic implications for the BTC market. Analysts have expressed concern that, in extreme stress scenarios, the firm might be forced to liquidate a portion of its Bitcoin to meet obligations, particularly if reserves are depleted and access to capital markets dries up. Strategy itself has acknowledged that if reserves were heavily drawn down, it might need to sell Bitcoin to meet obligations, highlighting the interconnectedness between its treasury, funding commitments, and the broader crypto market. Such a sale could trigger further price declines, potentially leading to additional liquidations and a downward spiral reminiscent of previous crypto credit crises.

Even short of forced selling, perception alone can trigger contagion. News stories that tie Bitcoin’s price drops to concerns about Strategy’s funding model—such as headlines about Bitcoin sliding as Strategy’s stock sinks or about the unraveling of its preferred stock mechanism—can influence market psychology and short-term flows. Traders may preemptively sell BTC or Strategy-linked securities in anticipation of potential corporate moves, amplifying volatility. In this sense, Strategy has become a systemic node in Bitcoin’s market structure, not because it controls the protocol or the mining ecosystem, but because its capital decisions have become focal points for investor attention and positioning.

Philosophical Debates Within the Bitcoin Community

Finally, Strategy’s approach raises philosophical questions about Bitcoin’s role and the appropriate level of financial engineering around it. Saylor has insisted that Bitcoin does not need Ethereum-style yield mechanisms and that its primary value proposition lies in its scarcity and long-term appreciation potential. Yet STRC and similar instruments effectively create synthetic yield streams backed by Bitcoin holdings, blurring the line between pure HODLing and yield-chasing behavior. This tension is not lost on critics, who argue that building complex, leveraged yield products on top of Bitcoin risks repeating mistakes from prior crypto cycles, even if the wrappers are more traditional.

In contrast, voices like Adam Back and Ricardo Salinas emphasize simplicity, advocating strategies such as dollar-cost averaging and long-term holding while warning against leverage and overcomplication. For these proponents, Bitcoin’s strength lies in the robustness of its base-layer rules—ultimately decided in the market by users, miners, and developers—rather than in elaborate financial constructs layered on top. Strategy sits between these poles, embodying both Bitcoin maximalism and Wall Street-style structuring. How the community and regulators ultimately judge this synthesis will depend not just on philosophical arguments, but on how the experiment plays out in practice over multiple cycles.

Strategy's equity premium collapses rapidly in BTC drawdowns; Bloomberg reported the stock and NAV premium failed to recover near all-time highs even as BTC rebounded toward $72K.

STRC preferred stock depegged when Bitcoin weakened, exposing the circular dependency between BTC price, equity issuance appetite, and the ability to fund further purchases.

A single executive controls both the accumulation thesis and public narrative; Saylor's personal statements on Bitcoin community factions and deepfake responses show strategy risk concentrated in one person.

- Regulatory / TaxMedium

Strategy lobbied against unrealized-gains tax treatment on BTC holdings, revealing that existing accounting rules could generate multi-billion-dollar tax bills without a cash event.

Serial issuance of convertible notes and preferred shares (STRK, STRC) structurally subordinates common equity; redemption of $1.05B in 2027 convertible notes signaled debt consolidation pressure.

- Contagion / Copycat riskMedium

DeFi-native replicas of the Saylor model remove equity guardrails entirely; on-chain leverage loops amplify BTC price volatility into protocol liquidation cascades with no board-level circuit breaker.

Outlook

Strategy has carved out a singular position at the junction of corporate finance and Bitcoin, turning its balance sheet into a live experiment in what a publicly traded “Bitcoin standard” can look like over time. Its success thus far rests on a combination of high-conviction leadership, an aggressive capital-raising engine, and periods of strong Bitcoin performance that have supported both asset values and investor enthusiasm. At the same time, the recent stress in its STRC preferred stock and the associated concerns about its funding model highlight the fragility inherent in relying on complex, market-dependent mechanisms to sustain an ever-expanding Bitcoin treasury.

Looking ahead, much depends on the interplay between Bitcoin’s price trajectory, global interest-rate dynamics, and the evolution of alternative Bitcoin investment vehicles. A renewed bull market in BTC, especially if accompanied by easing financial conditions, could reignite Strategy’s flywheel, allowing the company to repair STRC’s peg, raise fresh capital, and continue expanding its holdings. Conversely, a prolonged period of subdued or declining Bitcoin prices, combined with persistent high rates and competing themes such as AI infrastructure, could further strain its funding channels and force more conservative behavior, including slower accumulation or selective asset sales.

For the broader crypto market, Strategy will remain an important barometer and actor, but not the only one. Spot ETFs, options income funds like BITA, and other corporate or institutional allocators are diversifying the sources of Bitcoin demand and the forms of tradable exposure available to investors. In this more complex ecosystem, Strategy’s importance lies as much in the lessons it offers—about leverage, innovation, and risk management—as in the specific quantity of BTC it holds. Whether the company ultimately stands as a triumphant example of corporate Bitcoin maximalism or a cautionary tale about the limits of financial engineering on top of volatile assets will be determined not by any single crisis or rally, but by the cumulative outcome of many market cycles.

Latest Strategy news

Michael Saylor signals another bitcoin buy as Strategy sits about $13 billion underwaterStrategy's enterprise mNAV falls below 1 for the first time, signaling investors now value the firm's capital structure below the Bitcoin held on its balance sheetInvestors turn to Strategy's June 30 STRC ex-dividend date as markets await the preferred stock's monthly dividend rate reset amid heightened Bitcoin volatilityPublic firms now hold over 1M BTC as Strategy, Tesla, Block and Metaplanet embrace Bitcoin treasury strategies to hedge inflation and attract investorsThe math is becoming harder to ignore: Strategy's annual dividend obligations have climbed to $1.2 billion, cash reserves have fallen 38% in 2026, and dividend coverage has dropped from more than seven years to only 14 months. Rebuilding liquidity may soon take precedence over additional Bitcoin purchases. Grant Cardone says Cardone Capital will keep buying Bitcoin with rental cash flows, positioning its $200M BTC strategy as an alternative to Strategy's debt-funded playbook

Grant Cardone says Cardone Capital will keep buying Bitcoin with rental cash flows, positioning its $200M BTC strategy as an alternative to Strategy's debt-funded playbookSources

- https://www.strategy.com/purchases

- https://cryptonews.net/news/bitcoin/33038448/

- https://www.strategy.com/press/strategy-announces-fourth-quarter-2025-financial-results_02-05-2026

- https://news.bitcoin.com/michael-saylor-reflects-on-strategys-bitcoin-crisis-after-btc-fell-below-16k/

- https://bitcoinmagazine.com/markets/mstr-shares-sink-as-bitcoin-hits-72000

- https://x.com/CoinDesk/status/2067670392911667278

- https://beincrypto.com/strategy-preferred-stock-mstr-stock-impact/

- https://www.youtube.com/watch?v=qpkvpSp-wBY

- https://www.bloomberg.com/news/articles/2026-06-18/bitcoin-btc-slides-toward-60-000-as-saylor-s-strategy-funding-model-unravels

- https://www.bloomberg.com/news/newsletters/2026-06-18/michael-saylor-s-bitcoin-flywheel-has-a-preferred-stock-problem

- https://www.youtube.com/watch?v=5gMMbAl_z6U

- https://x.com/DecryptMedia/status/2068016712843247735

- https://www.blackrock.com/us/individual/products/350678/ishares-bitcoin-premium-income-etf

- https://www.fidelity.com/learning-center/trading-investing/crypto/dollar-cost-averaging

- https://www.schwab.com/learn/story/investors-guide-to-options-income-etfs

- https://www.crowdfundinsider.com/2026/06/286778-bitcoin-and-crypto-markets-face-significant-challenges-amid-strategys-preferred-stock-strc-turmoil/

- https://alpha-maven.com/industry/hedge-fund/news/directory?page=24

- https://www.youtube.com/watch?v=SabmUOudR6M

- https://www.kucoin.com/news/flash/michael-saylor-claims-strc-was-designed-using-ai-product-depegged-recently

- https://www.unlock-bc.com/en/strategys-strc-preferred-stock-falls-as-bitcoin-weakens

Community notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…