In-depth explainer on Metaplanet, Japan’s Bitcoin-first public company. Covers its BTC treasury strategy, zero-coupon bonds, Siiibo acquisition, venture and asset arms, accounting risks, and how it’s reshaping Bitcoin finance in Japan.

+7 sources across the wider coverage universe

Public firms now hold over 1M BTC as Strategy, Tesla, Block and Metaplanet embrace Bitcoin treasury strategies to hedge inflation and attract investors2026-06

Public firms now hold over 1M BTC as Strategy, Tesla, Block and Metaplanet embrace Bitcoin treasury strategies to hedge inflation and attract investors2026-06 Metaplanet raises $50M via zero-interest bonds to double down on Bitcoin accumulation, reinforcing corporate treasury shift toward BTC reserves2026-04

Metaplanet raises $50M via zero-interest bonds to double down on Bitcoin accumulation, reinforcing corporate treasury shift toward BTC reserves2026-04 Metaplanet set to acquire licensed securities firm Siiibo for $13M to build bitcoin-linked yield products under Metaplanet Securities brand2026-06

Metaplanet set to acquire licensed securities firm Siiibo for $13M to build bitcoin-linked yield products under Metaplanet Securities brand2026-06 Metaplanet boosts Bitcoin stash to 40,177 BTC after latest purchase, ranking third among public firms despite declining BTC yield performance this quarter2026-04

Metaplanet boosts Bitcoin stash to 40,177 BTC after latest purchase, ranking third among public firms despite declining BTC yield performance this quarter2026-04 Metaplanet announces launch of 2 new subsidiaries, Metaplanet Ventures and Metaplanet Asset Management, bets on Japanese stablecoin JPYC.2026-03

Metaplanet announces launch of 2 new subsidiaries, Metaplanet Ventures and Metaplanet Asset Management, bets on Japanese stablecoin JPYC.2026-03 Metaplanet purchases additional 150 BTC ($12.6M), increasing total holdings to 3,350 BTC after appointing Eric Trump as strategic advisor.2025-03

Metaplanet purchases additional 150 BTC ($12.6M), increasing total holdings to 3,350 BTC after appointing Eric Trump as strategic advisor.2025-03

Metaplanet: Japan’s Bitcoin-First Public Company Explained

Metaplanet is a Tokyo-listed investment company that has reoriented its entire corporate strategy around accumulating Bitcoin (BTC) and building a Bitcoin-centric financial platform, making it one of the largest public Bitcoin treasuries in the world and a bellwether for institutional BTC adoption in Japan. In little more than a few years, the firm has evolved from a traditional hospitality business into a highly financialized, Bitcoin-focused vehicle that uses bonds, equity, and structured products to expand its BTC reserves and distribute Bitcoin-linked yield products to investors.

What Is Metaplanet?

Metaplanet Inc. is a publicly traded Japanese company listed on the Tokyo Stock Exchange under ticker 3350 and on U.S. OTC markets under the symbol MTPLF, positioning itself explicitly as a Bitcoin treasury company rather than a conventional operating firm. The company is widely described in crypto circles as “Asia’s MicroStrategy,” a reference to the U.S. software firm that similarly transformed itself into a leveraged corporate vehicle for holding large quantities of Bitcoin on its balance sheet. Metaplanet’s core thesis is that BTC will outperform fiat currencies over the long term, especially the Japanese yen, and that a publicly traded vehicle holding and structuring Bitcoin exposure can unlock value for both domestic and international investors seeking regulated BTC exposure in equity form.

Metaplanet’s Bitcoin holdings have grown from fewer than 2,000 BTC at the start of 2025 to tens of thousands of coins, backed by an increasingly complex capital structure that includes zero-coupon bonds, private placements, warrants, and Bitcoin-backed credit facilities. Company disclosures and independent trackers indicate that the firm now holds over 40,000 BTC, placing it among the very largest public corporate Bitcoin treasuries globally and firmly establishing it as Japan’s most aggressive corporate buyer of BTC. Alongside the accumulation strategy, Metaplanet is building a broader financial ecosystem around Bitcoin, including the planned acquisition of a licensed securities firm, the launch of venture and asset management subsidiaries, and early investments in Japan’s first licensed yen stablecoin issuer.

Public firms now hold over 1M BTC as Strategy, Tesla, Block and Metaplanet embrace Bitcoin treasury strategies to hedge inflation and attract investors

Strategy's own June 22 filing put the USD reserve at $1.4B, and that's the part treasury-copycats should care about: once BTC is wrapped in ATMs, perpetual prefs and mNAV math, the bid depends on capital markets staying open. ETFs can bleed and just redeem; levered treasurycos have dividends, spreads and dilution thresholds, so a BTC drawdown can turn them from mechanical buyers into balance-sheet managers. Metaplanet chasing BTC-per-share yield is fun while equity trades rich, but if the premium disappears the scarce asset isn't the constraint anymore, the cost of fiat capital is.

Readers click Metaplanet not as a passive Bitcoin story but as an active financial engineering case study — each purchase headline doubles as a signal that Japanese zero-interest debt markets and dilutive warrant structures can be weaponized for BTC accumulation at a speed that outpaces even MicroStrategy.↗

From Hotel Operator to Bitcoin-First Investment Firm

Metaplanet did not begin life as a crypto-native company. It originally operated in the hospitality sector and later repositioned itself as an investment firm before fully embracing a Bitcoin-first strategy. This path mirrors a broader theme in the corporate Bitcoin narrative: legacy businesses with modest or declining core operations increasingly view BTC as a way to repurpose their corporate shells, balance sheets, and listings into high-beta vehicles on the Bitcoin price. In Metaplanet’s case, the pivot is especially notable given Japan’s traditionally conservative financial culture and the country’s relatively strict regulatory framework for crypto-assets.

According to educational materials and company communications, Metaplanet’s management concluded that their previous business model offered limited scalability compared with the asymmetric upside they perceived in long-term Bitcoin exposure. The firm repositioned itself explicitly as a Bitcoin treasury company, effectively stating that its primary “product” would be exposure to Bitcoin, financed through capital markets and structured under Japanese corporate and securities law. This involved not only buying BTC for the balance sheet but also reshaping the corporate strategy, investor messaging, and operating roadmap around Bitcoin-centric initiatives, including BTC-linked financial products and infrastructure investments.

The strategic pivot was also influenced by Japan’s macroeconomic backdrop, characterized by decades of low interest rates, deflationary pressures, and periodic episodes of yen weakness against the U.S. dollar. For a management team convinced that Bitcoin represents a superior long-term store of value compared with fiat currencies, particularly the yen, committing the balance sheet to BTC and tapping cheap or zero-interest capital became a coherent—if high-risk—thesis. Rather than simply holding BTC as a small treasury allocation, Metaplanet opted for a more radical approach: maximize Bitcoin exposure, engineer low-cost funding, and then build financial infrastructure and products around that core position.

The company’s transformation was gradual but accelerated sharply from 2024 onward, as Metaplanet began announcing increasingly large BTC purchases, ambitious accumulation targets, and an ecosystem strategy that extended well beyond passive holding. By the time the firm was widely being labeled “Asia’s MicroStrategy,” the pivot was effectively complete: Metaplanet’s identity, investor base, and business roadmap were all centered on Bitcoin, turning the company into a live experiment in how far a publicly traded Japanese issuer can push a BTC-first corporate strategy.

Inside Metaplanet’s Bitcoin Treasury Strategy

Accumulating BTC at Scale

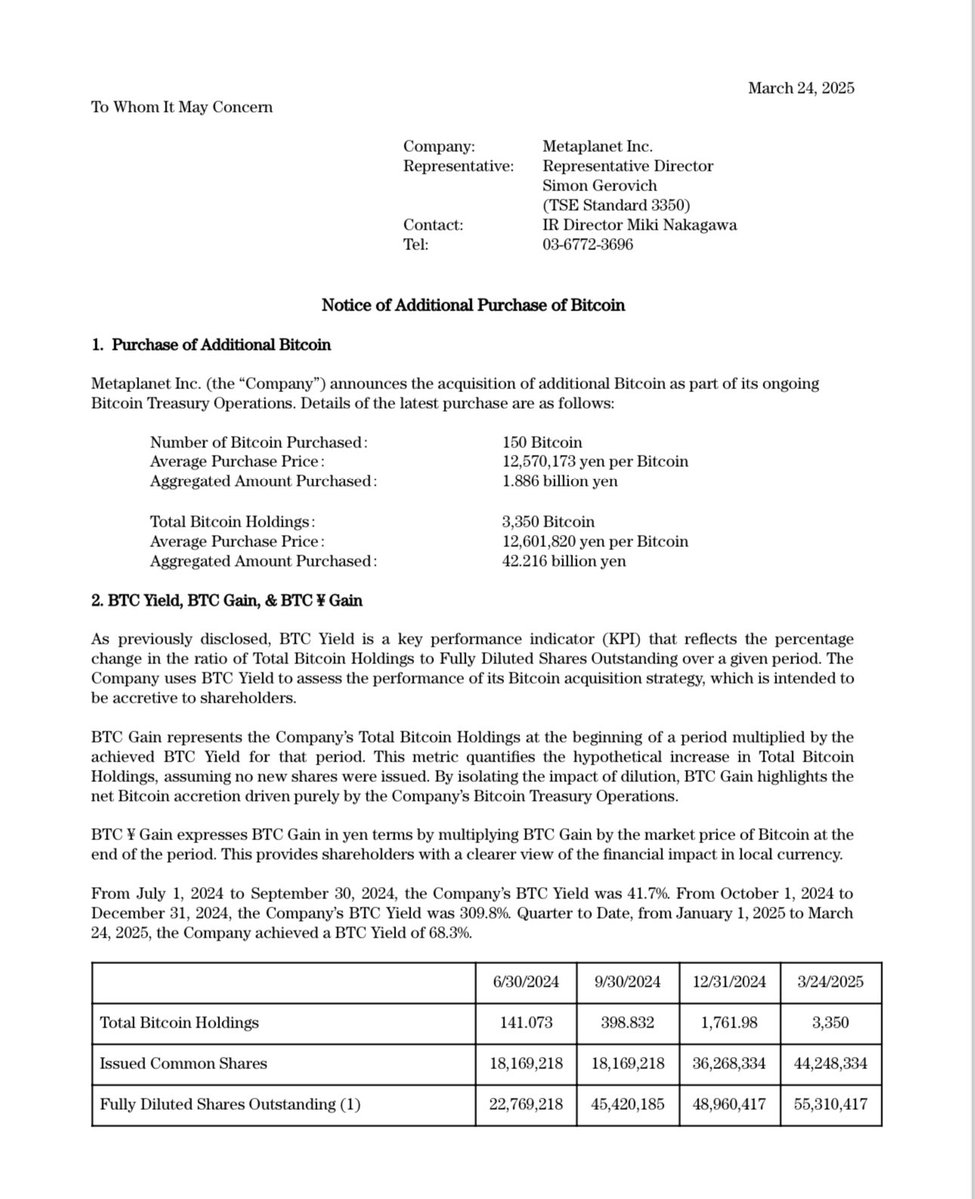

At the heart of Metaplanet’s strategy is a simple quantitative ambition: acquire as much Bitcoin as possible and keep it on the balance sheet as a strategic reserve. Early educational coverage described the company’s initial goal of reaching 10,000 BTC, which it reportedly hit by mid-2025 after a series of purchases, including a large 1,112 BTC acquisition in June of that year. At that stage, Metaplanet’s BTC holdings were already sufficient to propel it into the upper tier of public corporates holding Bitcoin, surpassing some well-known crypto firms in raw BTC terms.

The accumulation pace did not stop there. Company disclosures and news reports indicate that Metaplanet’s holdings grew from fewer than 2,000 BTC at the start of 2025 to around 35,102 BTC within roughly a year, a more than tenfold increase driven by a mix of bond issuance, equity financing, and retained capital. As of subsequent updates, the firm’s stash expanded further to about 40,177 BTC, helped by continued purchases financed through zero-coupon bond offerings and other capital-raising efforts. This rapid scaling has placed Metaplanet third among public companies in terms of Bitcoin held, according to both company statements and independent treasury trackers.

The firm has also set extremely ambitious forward-looking targets. Management has articulated a goal of holding 100,000 BTC by the end of 2026 and 210,000 BTC by the end of 2027, which would equate to roughly 1% of Bitcoin’s maximum possible supply if achieved. These targets are not merely symbolic; they define the firm’s funding needs, acquisition tempo, and risk profile. To move from tens of thousands of BTC to over 200,000 coins in such a short window, Metaplanet must continuously access significant capital, navigate market cycles, and manage the operational and regulatory complexities of such a large BTC position.

The strategic logic is straightforward but aggressive: if Bitcoin appreciates significantly over time, a large, low-cost BTC position can generate outsized equity returns for shareholders, especially when backed by fixed-cost or zero-interest liabilities. However, this approach also exposes the firm to substantial downside risk in the event of deep or prolonged drawdowns in BTC’s price. The more BTC Metaplanet acquires relative to its operating earnings and conventional assets, the more its equity value, solvency metrics, and refinancing prospects become tethered to Bitcoin’s volatility.

To clarify the scale and trajectory of Metaplanet’s treasury program, it is useful to summarize key milestones in approximate form:

| Stage / Event | Approx. BTC Held | Key Details |

|---|---|---|

| Early 2025 (pre-acceleration) | < 2,000 BTC | Initial Bitcoin allocation before the full treasury strategy ramp-up |

| June 2025 milestone | 10,000+ BTC | First major target reached after large purchases including 1,112 BTC |

| Around early–mid 2026 (pre-bond and placement) | 35,102 BTC | Significant growth via bonds, credit lines, and retained capital |

| After 20th zero-coupon bond issuance (April 2026) | 40,177 BTC | Third-largest public corporate BTC treasury, according to reports |

| Long-term public target (end of 2026 / 2027) | 100k–210k BTC | Stated ambition to reach 100,000 BTC by 2026 and 210,000 BTC by 2027 |

While exact holdings fluctuate with new purchases and possible collateral arrangements, the trajectory is clear: Metaplanet is moving from being a mid-sized corporate holder to a potential megascale Bitcoin treasury, contingent on its ability to execute its funding plan and manage the underlying risks.

Funding the BTC War Chest: Bonds, Equity and Credit

To finance its accumulation, Metaplanet has relied heavily on innovative and sometimes unconventional capital markets tools, with a strong emphasis on zero-interest bonds and equity-linked structures designed to minimize cash interest expense while maximizing balance sheet exposure to BTC.

One cornerstone of this approach is a recurring program of zero-coupon, or zero-interest, bonds subscribed largely by EVO FUND, a Cayman Islands-based vehicle affiliated with Evolution Financial Group. In April 2026, Metaplanet issued its 20th series of such bonds, raising approximately 8 billion Japanese yen, or around 50 million U.S. dollars, with the proceeds earmarked entirely for Bitcoin purchases. These unsecured notes carry a 0% coupon and mature in April 2027, redeeming at par, which means Metaplanet repays exactly what it borrowed without incurring periodic interest costs over the life of the debt.

This structure offers clear benefits for a Bitcoin-maximalist treasury strategy. By borrowing at a zero nominal interest rate, Metaplanet can convert the full proceeds into BTC exposure; any appreciation in Bitcoin’s price accrues to the company’s balance sheet rather than being siphoned off as interest payments. EVO FUND’s role as a repeat anchor for these issuances also gives Metaplanet a relatively predictable pipeline of debt financing, at least as long as market confidence and regulatory conditions remain supportive. Of course, the principal still needs to be repaid or refinanced at maturity, which means that Metaplanet is effectively betting that either Bitcoin appreciates sufficiently or capital markets remain open for rollovers or equity conversions.

Alongside bond issuance, Metaplanet has tapped equity markets through sizeable private placements. In one notable transaction, the company raised approximately 255 million dollars from global institutional investors by issuing new shares at 380 yen per share, a small premium to the market price at the time. The financing package included fixed-strike warrants exercisable at 410 yen per share, about a 10% premium to the placement price, which could generate an additional 276 million dollars in proceeds if fully exercised before their March 2028 expiration. Taken together, the placement and attached warrants provide up to roughly 531 million dollars of potential capital, much of which is earmarked for Bitcoin purchases over a multi-year period.

Company disclosures indicate that about 56.9 billion yen, or around 357 million dollars, from this broader financing plan is allocated for buying additional Bitcoin between April 2026 and March 2028. A further 21.1 billion yen is slated for repaying borrowings under existing credit facilities, while roughly 6.3 billion yen will support Metaplanet’s Bitcoin income-generation business, including margin collateral for options underwriting and other BTC-linked structures. This breakdown underscores that Metaplanet’s capital structure is not solely about buying and holding BTC; it also reflects a move into more complex, yield-oriented strategies built on top of its core treasury position.

In addition, Metaplanet has arranged Bitcoin-backed credit facilities that can be drawn upon for acquisitions and working capital. When announcing its deal to acquire Siiibo Securities, the company noted that it could use cash on hand, borrowings, and optional BTC-backed credit lines with an aggregate capacity of up to 500 million dollars to fund the transaction if needed. This blending of unsecured zero-coupon bonds, equity placements with warrants, and secured credit lines illustrates a highly financialized approach to treasury management, where the balance sheet is actively engineered to maximize Bitcoin exposure while seeking to maintain flexibility and regulatory compliance.

Options, Yield and the Move Beyond “Buy and Hold”

Metaplanet’s treasury strategy increasingly extends beyond simple spot BTC purchases. Company statements and independent analysis indicate that the firm has explored options strategies, including selling options and other derivatives, to generate yield or acquire Bitcoin at favorable prices while collecting premiums. Such activities are consistent with broader trends in crypto markets, where institutional players use covered calls, cash-secured puts, and structured products to enhance returns or manage risk on underlying BTC positions.

In its financing disclosures, Metaplanet explicitly referenced the use of part of its newly raised capital to support its “bitcoin income generation business,” including margin collateral for options underwriting. This suggests an emerging business line where the firm not only holds Bitcoin but also uses that BTC as the underlying asset for yield strategies, possibly in both over-the-counter and exchange-traded derivatives markets. While these activities can boost revenue and help offset some of the carrying costs of the treasury, they also introduce additional layers of market, liquidity, and counterparty risk, particularly in stressed conditions.

Analysis of Metaplanet’s strategy by external commentators has framed this as a delicate balancing act. On one hand, using BTC reserves to underwrite options can make the treasury more productive, generating income in sideways or moderately volatile markets. On the other hand, misjudging volatility, liquidity, or hedging can exacerbate losses in sharp market moves, especially given the size and leverage of the underlying BTC position. As the company’s Bitcoin stash has grown, so too has the scale at which any such strategies might operate, magnifying both the potential benefits and the risks.

For investors and observers, this evolution means that Metaplanet should increasingly be viewed not just as a passive “Bitcoin vault,” but as an active balance-sheet trader and structurer in BTC-linked markets. That positioning may help explain some of the firm’s moves to acquire a securities license, launch asset management operations, and build infrastructure around Bitcoin capital markets, all of which can create internal platforms for deploying and monetizing its BTC treasury.

Accounting, JGAAP and Mark-to-Market Volatility

A critical, often misunderstood aspect of Metaplanet’s public financials is how Japanese accounting standards treat Bitcoin holdings. Under Japanese GAAP (JGAAP), guidance such as Practical Advisory Report No. 38 requires that crypto-assets with an active market be valued at market price at the end of each reporting period, with unrealized gains or losses flowing through the income statement. This contrasts with some other jurisdictions where certain corporate BTC holdings can sometimes be treated as indefinite-lived intangibles, with asymmetric recognition of impairments versus gains.

For Metaplanet, JGAAP’s mark-to-market treatment means that its reported net income is highly sensitive to quarter-end Bitcoin prices, even if the company has not sold any BTC. When BTC trades lower at the balance sheet date than at the previous reporting point, the firm must recognize non-cash valuation losses; when BTC trades higher, it can recognize valuation gains. As a result, fairly modest changes in Bitcoin’s price can translate into large swings in reported profits or losses, particularly when the company holds tens of thousands of coins.

This dynamic was on full display in the company’s Q1 2026 results. Metaplanet reported a net loss of about 725 million dollars for the quarter, primarily due to non-cash markdowns on its sizeable Bitcoin holdings, even as underlying operational metrics showed growth. In an earlier period, the firm also disclosed a net loss of around 114.5 million yen that was again tied mainly to BTC valuation adjustments rather than deteriorating operating performance. These episodes underline that headline profit and loss figures can be a poor proxy for underlying health in a company where the balance sheet is dominated by a volatile financial asset marked to market.

From a crypto-treasury perspective, the accounting treatment has two major implications. First, investors must disentangle operational results, such as revenue from services or financial products, from non-cash gains or losses driven solely by quarter-end Bitcoin prices. Second, management’s ability to communicate its long-term strategy becomes more challenging when reported earnings can swing dramatically due to short-term BTC moves, even if the firm remains solvent, liquid, and committed to holding its Bitcoin.

Japanese legal and accounting specialists have highlighted that any future changes in domestic or international guidance on crypto-asset valuation, hedging treatment, or capital adequacy rules could materially impact how companies like Metaplanet structure and report their Bitcoin treasuries. Regulatory or standard-setting bodies could, for instance, tighten risk-weighting requirements, adjust disclosure expectations, or refine how derivatives and structured products tied to crypto-assets are treated on corporate balance sheets. For Metaplanet, which has built its identity around a massive BTC position within this existing framework, such changes represent a non-trivial regulatory risk.

- 01BTC accumulation pace and milestones↗

Readers tracked every incremental purchase — from 2,031 to 40,177 BTC — treating each headline as a live scoreboard for the most aggressive corporate Bitcoin accumulation in Asia.

- 02Zero-interest bond and warrant financing↗

Multiple headlines about ¥2B zero-coupon bonds and the ¥116B warrant raise revealed that Metaplanet's edge is exploiting Japan's cheap debt environment, not equity returns — a structurally novel angle readers found non-obvious.

- 03Eric Trump strategic advisor appointment

The highest-clicked headline linked the advisor appointment directly to a fresh 150 BTC purchase, signaling that political brand associations now move corporate BTC treasury news.

- 04Institutional Bitcoin supply concentration↗

Headlines framing Strategy and Metaplanet together as controlling 12.3% of total BTC supply pulled readers who see corporate treasury hoarding as a macro Bitcoin liquidity risk.

- 05Japan regulatory scrutiny of crypto treasuries

The Japan Exchange Group (JPX) headline about stricter rules for listed crypto-holding firms introduced a regulatory ceiling risk that readers recognized as unique to Metaplanet's listed-company structure.

- 06Expansion beyond pure BTC holding↗

Announcements of Metaplanet Ventures, Metaplanet Asset Management, JPYC stablecoin bets, and the Siiibo Securities acquisition signaled a pivot from single-asset treasury to financial conglomerate, attracting readers watching diversification risk.

Building a Bitcoin-Centric Financial Platform in Japan

Metaplanet’s ambitions extend beyond being a large Bitcoin holder. The company has articulated a broader vision of becoming a Bitcoin-centric financial platform in Japan and a bridge between Asian and Western capital markets for BTC-focused credit and investment products. To pursue this, Metaplanet is expanding both horizontally—through acquisitions like Siiibo Securities—and vertically, through the launch of new subsidiaries and targeted investments in Bitcoin-related infrastructure.

Project Nova and the Siiibo Securities Acquisition

A central pillar of this expansion is the planned acquisition of Siiibo Securities, a Japanese online securities firm, for approximately 2.1 billion yen, or about 13 million dollars. Metaplanet announced that it would acquire 100% of Siiibo, which operates a digital platform for private placement corporate bonds, historically a segment dominated by institutional investors and high-net-worth individuals. The deal, expected to close in mid-2026, marks the first major transaction under Metaplanet’s “Project Nova,” its medium- to long-term strategy to build a Bitcoin-centric financial platform in Japan.

Crucially, Siiibo holds a Type I Financial Instruments Business Operator registration, the license required under Japanese law to structure and distribute a wide range of securities products, including to retail investors. Metaplanet itself did not previously possess such a license, meaning that without an acquisition it would have been limited in its ability to originate and sell Bitcoin-linked financial products directly to the public. By acquiring Siiibo and rebranding it as Metaplanet Securities Inc., the company gains both the regulatory passport and an existing distribution platform with an established customer base.

Metaplanet has outlined several synergies it expects from this deal. It plans to distribute Siiibo’s existing corporate bond products to Metaplanet’s own shareholder base, which is reported to be roughly a quarter of a million investors. It also intends to develop new BTC-linked financial products—such as bonds tied to Bitcoin’s price or yield-enhancing BTC structures—to be offered through Siiibo’s platform. Joint underwriting of bond and digital securities issuances is envisioned in partnership with Metaplanet Ventures, particularly for startups in the cryptocurrency and decentralized finance space, and the company has flagged a pilot program for security tokens and other digitized instruments as part of the roadmap.

In strategic terms, the Siiibo acquisition gives Metaplanet something it previously lacked: a regulated infrastructure through which it can package its Bitcoin expertise and treasury into investment products for a broader investor base, including Japanese retail savers. It also positions the firm to experiment with BTC-linked bonds and structured products that might appeal to investors seeking fiat-denominated cash flows with Bitcoin exposure layered on top. For a company aiming to be more than a passive BTC holder, this move is central to turning its treasury and know-how into a revenue-generating financial services business.

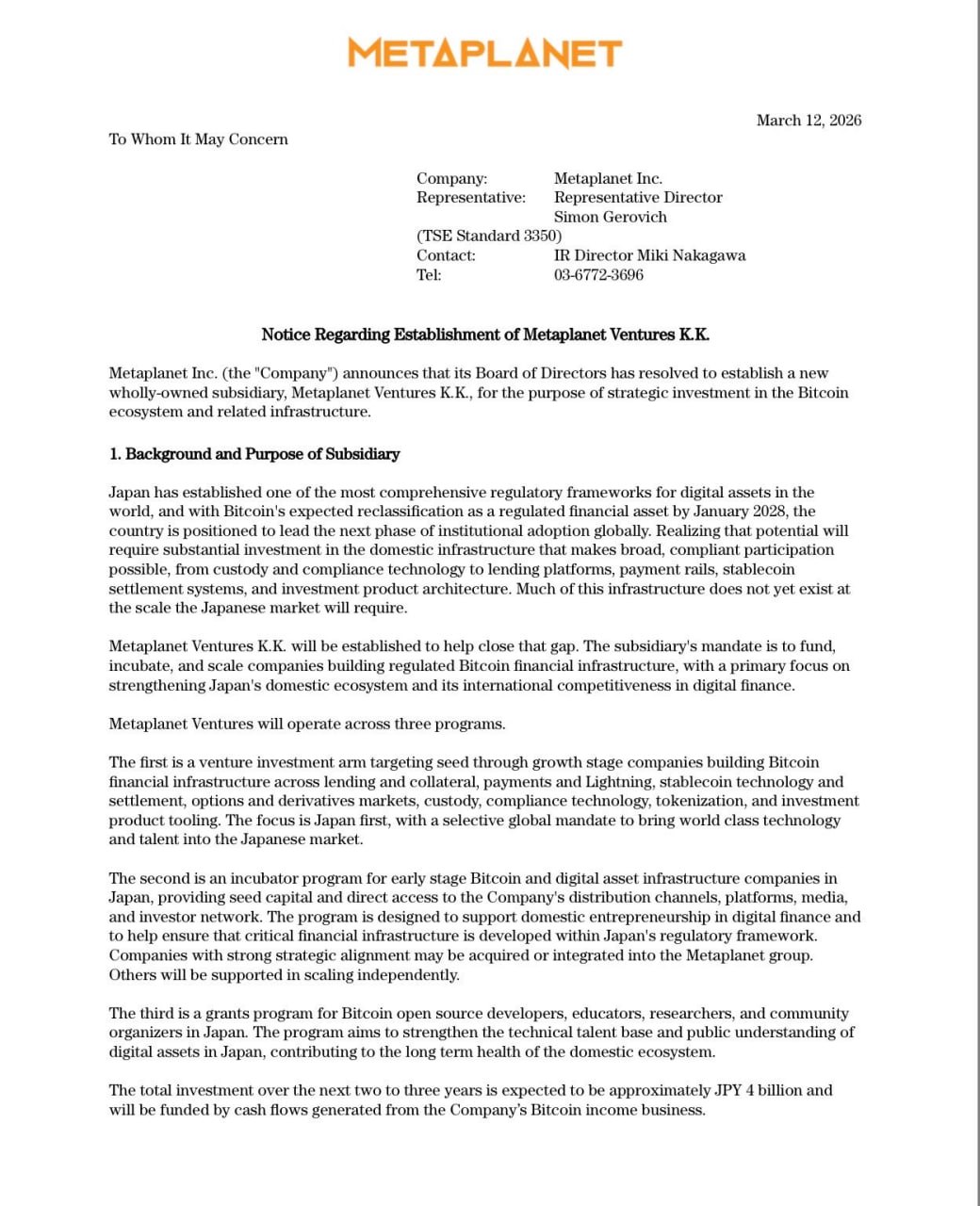

Metaplanet Ventures: Seeding Japan’s Bitcoin Infrastructure

Complementing its securities ambitions, Metaplanet is launching a venture capital arm, Metaplanet Ventures, designed to invest in the broader ecosystem of companies building financial infrastructure for Bitcoin in Japan. The board has approved a commitment of roughly 4 billion yen, or about 25 million dollars, to be deployed over several years into startups focused on areas such as lending, payments, custody, derivatives, stablecoins, and compliance tools. This initiative signals that Metaplanet sees value not only in holding BTC itself but also in owning stakes in the companies that will enable wider Bitcoin adoption and integration into Japan’s financial system.

Metaplanet Ventures plans to operate across three primary channels: traditional venture investments in early- and growth-stage startups, an incubator program for founders building Bitcoin-related infrastructure, and a grants initiative aimed at open-source developers, researchers, and educators working in the BTC ecosystem. Such a multi-pronged approach reflects an understanding that Bitcoin’s success as an asset class and monetary network depends not just on price appreciation but on a robust surrounding infrastructure of wallets, exchanges, custodians, compliance systems, and on-chain or second-layer applications.

The venture arm’s first announced investment underscores this strategy. Metaplanet has committed up to 400 million yen, around 2.5 million dollars, to JPYC Inc., a Japanese firm that issues JPYC, a yen-denominated stablecoin designed to maintain a 1:1 peg with the Japanese yen via reserves held in bank deposits and other assets. JPYC is described as Japan’s first licensed yen stablecoin issuer, making it a key player in any attempt to integrate digital yen instruments with Bitcoin-focused services and products. By backing JPYC, Metaplanet is positioning itself at the intersection of Bitcoin, stablecoins, and Japanese regulatory innovation.

From a strategic standpoint, investing in JPYC gives Metaplanet exposure to a core piece of digital payment infrastructure that can complement Bitcoin-based offerings. Yen stablecoins can facilitate on- and off-ramps between traditional bank accounts and crypto platforms, enable programmable payments, and support the settlement of BTC-linked securities and derivatives. For Metaplanet, whose platform ambitions rest on being able to connect Bitcoin and traditional finance in a compliant way, having a stake in a licensed stablecoin issuer is both a hedge and a potential growth driver.

Metaplanet Asset Management: Bridging Asian and Western BTC Capital Markets

Beyond Japan, Metaplanet is also laying the groundwork for a cross-border Bitcoin capital markets business. The company is establishing Metaplanet Asset Management as a Miami-based subsidiary focused on digital credit and Bitcoin-linked investment strategies. According to company statements, this unit will function as a platform for asset management and advisory services tied to Bitcoin, offering a range of products spanning BTC yield instruments, fixed-income structures, and actively managed strategies that cover equity, credit, commodities, and volatility.

The stated goal is to bridge Asian and Western capital markets by structuring regulated Bitcoin-related investment products that can appeal to institutional investors on both sides of the Pacific. By basing the asset management arm in Miami, a growing hub for digital asset finance, Metaplanet aims to tap into U.S. capital markets, regulatory frameworks, and investor networks while leveraging its Japanese corporate identity and BTC treasury as differentiating assets.

This strategic move reflects a recognition that Bitcoin capital markets are increasingly global and fragmented, with different jurisdictions offering varying levels of regulatory clarity, investor demand, and product innovation. By positioning itself as a cross-border specialist, Metaplanet seeks to monetize its treasury and structuring capabilities via management fees, advisory mandates, and proprietary strategies, rather than relying solely on the mark-to-market appreciation of its BTC holdings. If successful, this could diversify the company’s revenue base and reduce its reliance on dilutive equity issuance or debt to fund further Bitcoin accumulation.

Taken together, the Siiibo acquisition, the launch of Metaplanet Ventures and Metaplanet Asset Management, and the strategic investment in JPYC illustrate an integrated blueprint: hold a large Bitcoin reserve, build the infrastructure and regulatory licenses to create BTC-linked products, invest in the ecosystem that enables Bitcoin’s financialization, and connect domestic and international capital to that platform. This is a more complex and ambitious vision than simply being a corporate BTC “hodler,” and it carries correspondingly higher execution risk.

Financial Results, Stock Volatility and Investor Reactions

Metaplanet’s aggressive Bitcoin strategy has had dramatic effects on its financial statements and share price, drawing both enthusiastic support and serious concern from different segments of the market. For crypto-focused investors, the stock offers leveraged exposure to BTC with the added upside of a growing financial services ecosystem. For skeptics, it looks like a highly concentrated macro bet wrapped in a thin operating company, with significant dilution and downside risk if Bitcoin underperforms.

Q1 Losses and the Mechanics Behind Them

As noted earlier, Metaplanet’s reported earnings are heavily influenced by JGAAP’s mark-to-market treatment of Bitcoin. This has resulted in large swings in net income tied primarily to movements in BTC’s price rather than to changes in the firm’s operating performance. The most striking example to date came in the first quarter of 2026, when Metaplanet reported a net loss of approximately 725 million dollars. According to reports, this loss was driven largely by non-cash valuation adjustments on its Bitcoin holdings, which had declined in price relative to prior reporting dates during the period.

The magnitude of this loss attracted headlines, especially amid broader market scrutiny of highly leveraged Bitcoin treasuries. However, closer analysis indicates that the company’s operational metrics—such as revenue from its investment and financing activities—were improving, and that the loss reflected transient market prices rather than realized BTC disposals. In an earlier reporting period, the company similarly posted a net loss of about 114.5 million yen despite “strong operational growth,” again due mainly to Bitcoin revaluation losses under JGAAP. The recurring pattern is that Metaplanet’s P&L substantially oscillates with Bitcoin’s quarter-end price.

For a traditional equity analyst, this makes Metaplanet’s financials challenging to interpret using standard valuation multiples like earnings per share or simple P/E ratios. One must separate the non-cash, volatile BTC mark-to-market component from the more stable, underlying business performance, including any fees from financial products, trading revenues, and income from BTC yield strategies. In effect, part of the company’s income statement behaves like a large trading book in a highly volatile asset, which can swamp signals from its nascent operating segments.

This dynamic is not unique to Metaplanet; other Bitcoin-heavy corporates face analogous issues under their respective accounting regimes. However, because Metaplanet is both relatively smaller in terms of non-BTC operations and more aggressive in its targeted BTC accumulation, the impact on reported earnings is particularly pronounced. The Q1 2026 loss illustrates how quickly net income can plunge when Bitcoin corrects, even if the firm remains liquid and continues to believe in BTC’s long-term trajectory.

Share Price, Leverage and Dilution Risk

Metaplanet’s share price has mirrored the high beta nature of its strategy. In earlier stages of its pivot, the stock delivered extraordinary gains: one educational profile noted that as of mid-2025, the company’s shares had risen over 1,900% on a one-year basis, with more than 400% gains year-to-date and nearly 200% growth over a single month. These returns reflected both speculative enthusiasm for a “Japanese MicroStrategy” and the mechanical effect of Bitcoin’s appreciation on a relatively illiquid equity with a growing BTC position.

However, as the company has ramped up its capital-raising program, investors have also had to confront dilution risk. The 255 million dollar private placement of new shares at 380 yen per share, along with associated warrants exercisable at 410 yen, increases the potential share count significantly if all securities are taken up. The issuance of additional “MS Warrants” authorized by the board further expands this potential overhang, even though the resulting capital would be used partly to buy more Bitcoin and partly to support the company’s BTC income-generation business.

For existing shareholders, the key question is whether the per-share value of the firm’s Bitcoin holdings and operating business can outpace the dilutive effect of new equity and the risk of future capital raises. If Bitcoin appreciates strongly and Metaplanet effectively deploys new capital into BTC at favorable prices, dilution may be offset or even more than compensated by the resulting increase in net asset value per share. If BTC stagnates or falls, or if the company must raise additional funds under stress to service or refinance its obligations, existing shareholders may be left with a shrinking claim on a volatile asset base.

The behavior of sophisticated investors provides some insight into how market participants are weighing these trade-offs. Nakamoto, a digital asset investment firm, disclosed that it had sold around 20 million dollars’ worth of Bitcoin and exited a significant portion of its Metaplanet equity position at a loss in the first quarter. Nakamoto had reportedly acquired eight million Metaplanet shares at 3.75 dollars per share but later recorded an unrealized loss of approximately 9.29 million dollars on the position, with the carrying value falling to about 20.7 million dollars. The decision to exit suggests that at least some large investors are cautious about the risk-reward profile at current valuation and leverage levels, even if they remain bullish on Bitcoin itself.

From a balance sheet perspective, Metaplanet’s use of zero-coupon bonds mitigates immediate cash interest expense but does not eliminate leverage risk. The principal on these bonds must still be repaid or refinanced at maturity, and the company’s ability to do so on favorable terms depends heavily on Bitcoin’s price, access to capital markets, and the success of its operating businesses. In a scenario of severe or prolonged BTC weakness, the combination of mark-to-market losses, potential margin requirements on derivatives, and looming bond maturities could significantly strain the company’s finances, particularly if equity markets are less receptive to further placements.

Metaplanet Stock Versus Direct BTC Exposure

For a crypto-savvy audience, a natural question is whether owning Metaplanet shares is a sensible alternative or complement to holding Bitcoin directly. The answer depends on risk tolerance, investment horizon, and views on the company’s ability to execute its broader platform strategy.

Compared with holding BTC outright, owning Metaplanet equity provides a form of leveraged exposure to Bitcoin, because the firm typically finances a portion of its BTC purchases with debt and new equity. When Bitcoin’s price rises, the equity value can increase disproportionately if the spread between BTC appreciation and funding costs accrues to shareholders. The company’s ambitions to build profitable businesses around securities, asset management, and venture investments also offer potential additional sources of return beyond simple price appreciation of its Bitcoin holdings.

On the other hand, Metaplanet equity exposes investors to risks that do not exist when holding BTC directly. These include corporate governance risk, regulatory risk at the issuer level, dilution from future share issuances, refinancing risk on bonds and credit facilities, and execution risk in building new operating businesses. The stock can also underperform Bitcoin in scenarios where BTC appreciates but the company’s capital structure or operating results fail to translate that into per-share value, as suggested by large investors exiting at a loss despite a generally bullish long-term BTC thesis.

For these reasons, Metaplanet may function best as a specialized instrument for investors who are comfortable with both Bitcoin volatility and corporate leverage, and who believe that management can successfully extend the business into securities, asset management, and venture capital in ways that enhance the value of the underlying BTC treasury. It is arguably less suitable as a conservative proxy for Bitcoin exposure, especially for investors who prioritize capital preservation or prefer the simplicity and transparency of spot BTC holdings or regulated exchange-traded products.

Red Planet Japan rebrands to Metaplanet, pivots to Bitcoin treasury strategy

Holdings reach 2,031 BTC; becomes Asia's second-largest corporate BTC holder

First ¥2B zero-interest bond issuance to fund BTC purchases

- 2025-03governance

Eric Trump appointed strategic advisor; holdings at 3,350 BTC

¥116B raised via 21M zero-strike warrants — Asia's largest equity BTC raise

10,000 BTC milestone reached, surpassing Coinbase corporate holdings

- 2025-10milestone

EVO Fund exercises 540K Series-20 warrants, delivering $515M; 30K BTC 2025 and 100K BTC 2026 targets announced

Holdings reach 40,177 BTC; $50M zero-interest bond raise; third-largest public BTC holder globally

Strategic Significance for Japan and Global Bitcoin Treasuries

Metaplanet’s strategy carries implications that extend beyond its own balance sheet. It is a test case for how far a Japanese listed company can go in constructing a Bitcoin-centric corporate identity, and it contributes to emerging global patterns in how corporates hold and deploy BTC.

“Asia’s MicroStrategy”? Similarities and Differences

The widespread description of Metaplanet as “Asia’s MicroStrategy” reflects genuine parallels between the two companies. Both began as firms in traditional industries—software in MicroStrategy’s case, hospitality and then investment in Metaplanet’s—and pivoted to a strategy centered on acquiring large Bitcoin positions financed by debt and equity issuance. Both communicate a long-term conviction that Bitcoin will outperform fiat and other assets, and both aim to deliver leveraged BTC exposure to shareholders through a publicly traded corporate structure rather than a regulated fund or trust.

However, there are important differences. MicroStrategy operates under U.S. GAAP, whereas Metaplanet must comply with JGAAP, which imposes a different set of valuation and disclosure practices for crypto-assets, leading to distinct reporting dynamics and regulatory oversight. The Japanese regulatory environment for retail crypto exposure, securities licensing, and stablecoins also differs from that of the United States, influencing Metaplanet’s decision to acquire a licensed securities firm and invest in a regulated yen stablecoin issuer. Moreover, Metaplanet’s explicit strategy of building a full-stack financial platform—including securities distribution, asset management, and venture investments—marks a broader institutional ambition than MicroStrategy’s relatively narrower focus on its software business plus BTC treasury.

These distinctions mean that while the “Asia’s MicroStrategy” label is helpful shorthand, it can obscure the fact that Metaplanet is experimenting with a somewhat different model: not just a corporate balance sheet levered to Bitcoin, but a regional Bitcoin financial hub rooted in Japan’s regulatory framework and connected to global capital markets. Success or failure in this endeavor will provide important signals to other corporates considering similar pivots, especially in jurisdictions with stringent securities and crypto regulation.

Japan’s Evolving Stance on Bitcoin Treasuries

Japan has long been a key jurisdiction in the history of cryptocurrency, from early exchange booms to high-profile hacks and subsequent regulatory tightening. Today, the country maintains one of the more structured regulatory regimes for crypto-assets, with clear licensing requirements for exchanges and custodians, and explicit accounting guidance for corporate holdings of crypto-assets under JGAAP. This framework provides both opportunities and constraints for companies like Metaplanet.

On the opportunity side, clear rules around licensing and asset classification allow Metaplanet to design its strategy with a reasonably well-defined regulatory perimeter. Its acquisition of Siiibo to secure a Type I Financial Instruments Business license is a direct response to Japan’s requirement that securities distributors be licensed, enabling the company to legally structure and sell Bitcoin-linked financial products to retail investors. Its investment in JPYC, a licensed issuer of a yen-pegged stablecoin, aligns with regulators’ push to bring stablecoins under clear legal categories rather than allowing them to operate in grey zones.

On the constraint side, JGAAP’s mark-to-market requirement for crypto-assets can make large Bitcoin treasuries look more volatile and risky on paper than they might under alternative accounting frameworks, potentially affecting investor sentiment, credit ratings, and access to more conservative pools of capital. Additionally, Japanese regulators could at any time adjust their stance on Bitcoin-related securities, derivatives, and bank exposures in ways that would affect Metaplanet’s ability to scale BTC-linked products or use Bitcoin as collateral for large credit lines. As Metaplanet grows more systemically visible within Japan’s financial system, regulatory scrutiny is likely to intensify rather than diminish.

Legal and policy analysts have noted that if Metaplanet’s strategy proves successful—both financially and in terms of compliance—other Japanese corporates may feel more comfortable exploring measured Bitcoin treasury allocations within the existing JGAAP and licensing rules. Conversely, if the strategy backfires spectacularly, resulting in large losses or liquidity stress, it could prompt more restrictive attitudes among regulators, auditors, and boards of directors toward aggressive crypto-asset positions on corporate balance sheets.

A New Archetype in Global Bitcoin Treasury Rankings

By amassing over 40,000 BTC and targeting up to 210,000 coins, Metaplanet has catapulted itself into the top tier of global corporate Bitcoin holders. According to Bitcoin treasury trackers and company disclosures, this scale currently places the firm as the third-largest public corporate BTC holder, behind only a small number of major players. This ranking elevates Metaplanet from a regional curiosity to a globally relevant entity in discussions about Bitcoin supply dynamics and institutional adoption.

The company’s stated target of 210,000 BTC by the end of 2027, equivalent to roughly 1% of Bitcoin’s theoretical maximum total supply, has symbolic as well as practical implications. If Metaplanet were to achieve this target, it would join a very small group of entities—such as large long-term holders and certain funds—with direct control over 1% or more of the BTC supply, underscoring how corporate balance sheets can concentrate digital assets in ways analogous to large shareholders of traditional commodities or equities.

In the broader landscape of Bitcoin treasuries, Metaplanet’s approach illustrates a particular archetype: the mid-sized or smaller operating company that transforms itself into a Bitcoin-first vehicle, uses financial engineering to build a large BTC position, and then attempts to monetize that position via adjacent financial services. This differs both from large-cap tech firms that might hold modest BTC allocations as part of diversified balance sheets, and from pure-play crypto-native entities whose core operations revolve around mining or exchanges rather than treasury management.

For the Bitcoin ecosystem, Metaplanet’s rise underscores that the “corporate adoption” theme now includes not only household-name multinationals but also nimble public companies willing to experiment aggressively with capital structure, regulatory arbitrage, and BTC-centered business models. How markets reward or punish such strategies will shape the next wave of corporate decisions about whether and how to integrate Bitcoin into their treasuries and product offerings.

What Metaplanet Means for Bitcoin, Corporates and Crypto Markets

Metaplanet’s trajectory offers several lessons and implications for different stakeholders in the crypto and traditional finance ecosystems.

For Bitcoin itself, the company is a significant source of incremental demand and a potential contributor to supply concentration. Each major bond issuance or equity raise earmarked for BTC purchases represents an additional buy-side impulse, often executed in a relatively compressed timeframe. As long as Metaplanet continues to accumulate, this adds to the broader corporate and institutional demand profile for Bitcoin, alongside ETFs, miners, long-term holders, and other treasuries. If the company eventually stabilizes or reduces its holdings—whether voluntarily or under stress—that could also impact supply-demand dynamics at the margin.

For corporates considering Bitcoin treasuries, Metaplanet demonstrates both the possibilities and perils of an aggressive approach. On the positive side, the company has shown that it is possible, within Japan’s regulatory and accounting framework, to build a large BTC position, access capital markets repeatedly to finance that position, and use a combination of securities licenses, asset management operations, and venture capital to construct an ecosystem business around Bitcoin. On the negative side, Metaplanet’s large reported losses during BTC drawdowns, share price volatility, and dilution concerns highlight how quickly market sentiment can turn, especially when operating income is small relative to balance sheet exposure.

For investors, Metaplanet serves as a reminder that not all Bitcoin proxies are created equal. The risk-return profile of a leveraged BTC treasury company differs markedly from that of Bitcoin itself, regulated ETFs, or diversified crypto firms. Assessing such companies requires a holistic view that encompasses capital structure, accounting treatment, regulatory risks, management quality, and the credibility of any adjacent business lines in securities, asset management, or venture capital. The presence of prominent investors exiting positions at a loss, even while the company continues to accumulate BTC, underscores that enthusiasm for Bitcoin does not automatically translate into confidence in every corporate vehicle that holds it.

For regulators and policymakers, Metaplanet is a live case study in how existing frameworks handle large corporate exposures to crypto-assets. JGAAP’s mark-to-market rules, Type I securities licensing, and stablecoin regulation are being tested in real time by the company’s actions, providing feedback on whether current standards adequately capture the risks and opportunities associated with Bitcoin-heavy balance sheets and BTC-linked products. The outcome of this experiment will likely influence future guidance not just in Japan, but in other jurisdictions watching how such strategies play out in practice.

In the crypto markets more broadly, Metaplanet’s use of zero-coupon bonds, private placements with warrants, and Bitcoin-backed credit lines contributes to the ongoing financialization of BTC. The company is actively turning Bitcoin from a passive asset into collateral and underlying for yield products, bonds, and structured instruments distributed to both domestic and international investors. If Metaplanet’s platform ambitions succeed, it could become a meaningful node in Bitcoin’s emerging fixed income and credit markets, alongside miners, exchanges, funds, and banks experimenting with BTC-backed loans and securities.

- RegulatoryHigh

Japan Exchange Group is actively considering stricter listing rules for firms with large crypto treasuries, and Metaplanet's publicly listed structure makes it uniquely exposed to domestic rule changes that could constrain further BTC purchases or force disclosures.

With 40,177 BTC on its balance sheet and an average cost basis around ¥15.53M per BTC, a sustained Bitcoin price decline directly impairs the company's net asset value and its ability to service or roll zero-interest bond obligations.

Metaplanet has authorized up to 555 million new shares alongside multi-billion-yen warrant programs; aggressive share issuance to fund BTC purchases continuously dilutes existing shareholders, and mNAV decline triggered a $500M buyback to defend the premium.

Zero-interest bonds carry no coupon cost but do carry principal repayment obligations at maturity; if BTC prices fall sharply near maturity dates, Metaplanet would face refinancing pressure without the ability to liquidate BTC at favorable prices.

- Centralization / CounterpartyMedium

A single institutional counterparty, EVO Fund, exercised 540,000 Series-20 warrants delivering $515M — heavy dependence on one structured-finance relationship concentrates rollover and dilution risk.

Simultaneous launches of Metaplanet Ventures, Metaplanet Asset Management, a JPYC stablecoin position, and a Siiibo Securities acquisition introduce operational complexity that could divert management focus from the core BTC treasury mandate.

Outlook

Metaplanet sits at a crossroads of opportunity and risk. On the opportunity side, the company has already secured a place among the largest corporate Bitcoin treasuries, gained access to substantial low- or zero-cost funding, and sketched out a multi-pronged plan to turn its BTC holdings into the backbone of a broader financial platform spanning securities, asset management, and venture capital. Its pending acquisition of Siiibo Securities, the launch of Metaplanet Ventures and Metaplanet Asset Management, and its investment in JPYC position it to offer Bitcoin-linked bonds, yield products, and digital asset strategies to both Japanese and international investors in a regulated format.

On the risk side, the firm’s fate is increasingly interwoven with Bitcoin’s price trajectory, Japanese and global crypto regulation, and its own capacity to execute complex financial and operational initiatives. A sharp or prolonged downturn in BTC could simultaneously depress the value of its treasury, generate large accounting losses under JGAAP, strain its ability to refinance zero-coupon bonds, and test investor appetite for further equity or warrant exercises. Even in benign markets, missteps in integrating Siiibo, building profitable asset management products, or selecting venture investments could tarnish the value proposition of Metaplanet as more than a simple BTC holding vehicle.

For a crypto news audience, Metaplanet is likely to remain a closely watched bellwether of corporate Bitcoin experimentation, particularly in Asia. Key signposts to monitor include the pace and pricing of future BTC acquisitions, progress toward the 100,000 and 210,000 BTC targets, the integration and product pipeline of Metaplanet Securities, the growth of its asset management platform, and regulatory developments affecting Bitcoin treasuries and BTC-linked securities in Japan. The company’s ongoing story will help answer a broader question facing the Bitcoin era: can a publicly listed firm sustainably build a large, leveraged BTC treasury and an ecosystem of financial services around it, or does such ambition inevitably collide with the realities of volatility, regulation, and capital markets discipline?

Latest Metaplanet news

Sources

- https://bitcointreasuries.net/public-companies/metaplanet

- https://learn.bybit.com/en/bitcoin/what-is-metaplanet

- https://bitcoinfoundation.org/news/crypto-companies-news/metaplanet-q1-losses/

- https://x.com/coin_post/article/2065368169053818975

- https://news.bitcoin.com/metaplanet-raises-50m-via-zero-interest-bonds-to-expand-its-40177-btc-treasury/

- https://www.tradingview.com/news/cointelegraph:505adf164094b:0-metaplanet-raises-255m-and-adds-warrant-structure-for-bitcoin-buys/

- https://bitcoinmagazine.com/news/metaplanet-expands-bitcoin-strategy

- https://www.mexc.com/news/995813

- https://x.com/BitcoinNewsCom/status/2054654769424171308

- https://www.kavout.com/market-lens/is-metaplanet-s-bitcoin-treasury-strategy-a-genius-move-or-a-risky-gamble

- https://bitcoinmagazine.com/news/metaplanet-acquires-siiibo-securities

- https://www.facebook.com/CoinMarketCap/posts/latest-metaplanet-has-raised-50-million-through-zero-coupon-bonds-to-buy-more-bi/1380633514094038/

- https://www.altcoinbuzz.io/cryptocurrency-news/metaplanet-plans-bitcoin-fueled-digital-bank-acquisition/

- https://www.tradingview.com/news/cointelegraph:580d11827094b:0-metaplanet-raises-50m-in-zero-interest-bonds-to-buy-more-bitcoin/

- https://x.com/gerovich/status/2031894444216304020

- https://bitcoinmagazine.com/news/metaplanet-raises-255-million

- https://www.instagram.com/p/DV8yR8nDbrq/

- https://innovationlaw.jp/en/tag/bitcoin-treasury/

Community notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…