Comprehensive explainer on BTC covering Bitcoin’s design, 21M cap, network activity, ETFs, DeFi integrations, security risks, and its role alongside ETH, USDT, and traditional markets, written for long-term crypto investors.

+28 sources across the wider coverage universe

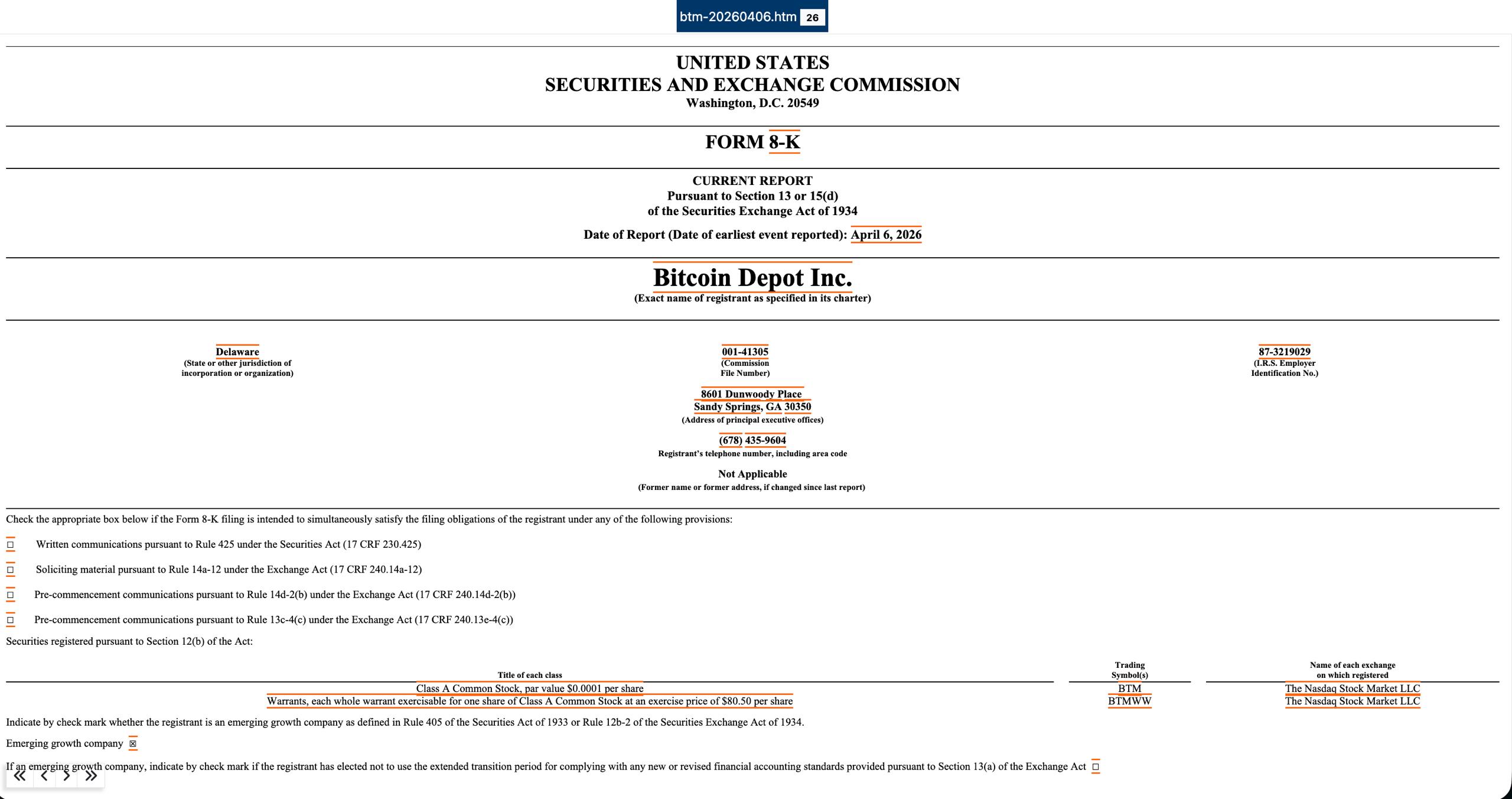

Bitcoin Depot discloses $3.6M BTC theft from corporate wallets in SEC filing, two weeks after breach2026-04

Bitcoin Depot discloses $3.6M BTC theft from corporate wallets in SEC filing, two weeks after breach2026-04 IXS selects BitGo to secure Bitcoin collateral for institutional yield products, enabling BTC-backed liquidity and RWA exposure through regulated, bankruptcy-remote infrastructure2026-04

IXS selects BitGo to secure Bitcoin collateral for institutional yield products, enabling BTC-backed liquidity and RWA exposure through regulated, bankruptcy-remote infrastructure2026-04 Public firms now hold over 1M BTC as Strategy, Tesla, Block and Metaplanet embrace Bitcoin treasury strategies to hedge inflation and attract investors2026-06

Public firms now hold over 1M BTC as Strategy, Tesla, Block and Metaplanet embrace Bitcoin treasury strategies to hedge inflation and attract investors2026-06 European BTC treasury firms forge own playbook as capital market and regulatory gaps block Strategy model2026-04

European BTC treasury firms forge own playbook as capital market and regulatory gaps block Strategy model2026-04 Charles Schwab launches direct BTC/ETH trading via new Schwab Crypto arm to rival Robinhood at 0.75% fee.2026-04

Charles Schwab launches direct BTC/ETH trading via new Schwab Crypto arm to rival Robinhood at 0.75% fee.2026-04 Zonda admits 4,500 BTC locked in inaccessible wallet as Polish prosecutors launch probe2026-04

Zonda admits 4,500 BTC locked in inaccessible wallet as Polish prosecutors launch probe2026-04

BTC (Bitcoin) – An Evergreen Explainer for Crypto Investors

Bitcoin’s native asset, BTC, is a digitally native, bearer-style token secured by the Bitcoin blockchain, designed to provide a scarce, censorship-resistant store of value and peer-to-peer payment asset with a hard cap of \(21\,000\,000\) coins. In practice, BTC now functions both as the monetary backbone of the Bitcoin network and as a globally traded macro asset with deep spot, derivatives, and ETF markets across the broader crypto and traditional financial system.

What BTC Actually Is

At its core, BTC is the unit of account of the Bitcoin network, a decentralized payment system launched in 2009 by the pseudonymous creator Satoshi Nakamoto. BTC is not a company share, bond, or claim on cash flows; it is a native digital commodity that exists purely as entries in a distributed ledger maintained by thousands of nodes worldwide. Holders control BTC through private keys, which authorize transfers on-chain, and every transaction is recorded in the public Bitcoin blockchain, allowing independent verification of all balances and movements. This design, combining scarce digital issuance with permissionless transfer, is what underpins Bitcoin’s appeal as a form of “internet-native” money.

From a market perspective, BTC has grown into the largest crypto asset by market capitalization, with highly liquid spot markets on major exchanges and billions of dollars in daily trading volume. BTC trades against fiat currencies such as the U.S. dollar, the euro, and the Korean won, as well as against stablecoins like USDT and other crypto assets, and it serves as a base asset in both centralized and decentralized trading venues. Exchanges such as Coinbase and Binance list dozens or hundreds of assets against BTC trading pairs, while leading Asian platforms like Upbit maintain BTC and USDT markets side by side for new listings, underscoring BTC’s role as a reference asset within the broader ecosystem.

Philosophically and legally, BTC is often treated as a digital commodity rather than a traditional security, aligning it more with gold or oil than with equities, though it exhibits far higher volatility than most commodities. Grayscale and other institutional managers explicitly use this framework, arguing that BTC’s valuation is primarily driven by supply–demand dynamics and macro expectations rather than cash flows or governance rights in an issuer. This commodity framing has shaped regulatory approaches in jurisdictions like the United States and informed how investors blend BTC with other risk assets such as equities, ETH, and stablecoins in portfolio construction.

Public firms now hold over 1M BTC as Strategy, Tesla, Block and Metaplanet embrace Bitcoin treasury strategies to hedge inflation and attract investors

Strategy's own June 22 filing put the USD reserve at $1.4B, and that's the part treasury-copycats should care about: once BTC is wrapped in ATMs, perpetual prefs and mNAV math, the bid depends on capital markets staying open. ETFs can bleed and just redeem; levered treasurycos have dividends, spreads and dilution thresholds, so a BTC drawdown can turn them from mechanical buyers into balance-sheet managers. Metaplanet chasing BTC-per-share yield is fun while equity trades rich, but if the premium disappears the scarce asset isn't the constraint anymore, the cost of fiat capital is.

BTC readers click hardest not on price moves but on trust-in-intermediaries failures — unauthorized collateral removal, custodians misrepresenting BTC backing, government asset seizures, and exchange hacks reveal a persistent anxiety that Bitcoin's trustless promise collapses the moment a human institution touches it.

How the Bitcoin Network Works

Blockchain, Proof of Work, and Consensus

The Bitcoin network is maintained by a decentralized set of nodes that validate transactions and enforce the protocol’s rules. Nodes receive transactions broadcast by users, verify that the signatures are valid and that the inputs have not already been spent, and relay them to peers. These transactions are grouped into blocks by miners, specialized participants who expend computational energy to solve cryptographic puzzles in a process known as proof of work. The first miner to find a valid block hash earns the right to append the block to the chain and collect the block reward plus transaction fees.

This proof-of-work mechanism provides security by making it economically and technically difficult for an attacker to reorganize the chain or double-spend coins. To alter confirmed history, an adversary would need to control a majority of the network’s hash rate and continuously outmine honest participants—a costly and visible endeavor. Over time, as more blocks are added on top of a transaction, the cost of reversing it becomes prohibitive, giving Bitcoin its settlement assurances that many compare to high-value financial systems.

Consensus in Bitcoin is not enforced by any central authority but emerges from the collective behavior of nodes enforcing the same software-defined rules. If a miner produces a block that violates rules—for example, by exceeding the block size limit or minting more BTC than allowed—honest nodes reject it, meaning the miner’s effort is wasted. This alignment of incentives among miners, nodes, and users underpins Bitcoin’s resilience and has allowed the protocol’s core monetary rules, like the \(21\,000\,000\) BTC cap, to remain unchanged for more than a decade.

Issuance, Halvings, and the 21 Million Cap

BTC’s issuance schedule is codified in the protocol via a predictable, declining block subsidy. New BTC enter circulation as part of the block reward, which started at 50 BTC per block and halves approximately every four years (210,000 blocks). This schedule means the flow of new supply falls over time, approaching zero asymptotically. The total number of BTC that can ever exist is capped at \(21\,000\,000\), a hard limit enforced by every full node.

According to widely accepted projections, the last fraction of BTC will be mined sometime around the year 2140, after which no new coins will be created. At that point, miners will earn revenue solely from transaction fees, rather than from newly minted BTC, a transition many analysts already see underway as block subsidies decline. The expectation that issuance will permanently stop reinforces Bitcoin’s scarcity narrative, which is often likened to “digital gold” and invoked to explain investor demand during periods of monetary expansion or concern about fiat debasement.

This halving-driven scarcity has historically coincided with pronounced boom-and-bust cycles in BTC’s price as each reduction in new supply interacts with shifting demand. However, the protocol itself remains agnostic to price; it simply enforces the issuance curve and leaves markets to discover BTC’s value. As more BTC is mined and the remaining unissued supply dwindles, the focus of monetization increasingly shifts from inflationary rewards to fee-based compensation for securing the network, a dynamic with important implications for long-term miner economics and transaction costs.

Fees, Microtransactions, and Network Activity

In addition to block subsidies, miners earn transaction fees paid by users who want their transactions included in blocks. Each block has limited space, so when demand for block space rises, users bid higher fees to prioritize their transactions. Over time, this fee market has become more complex, reflecting not only basic transfers but also emerging use cases such as inscriptions, ordinals, and other forms of on-chain data embedding.

Recent analytics from CryptoQuant show that Bitcoin’s network activity has been increasing even during periods of price weakness, driven in part by near-record counts of microtransactions. CryptoQuant’s Activity Index has broken above its longer-term trend for the first time since mid-2024, indicating that underlying usage is rising despite BTC trading well below prior peak prices. Independent coverage echoes this pattern, noting that Bitcoin network activity has surged on the back of small-value transfers and more frequent on-chain interactions, even as market sentiment remains cautious.

This divergence between on-chain activity and price illustrates one of Bitcoin’s structural features: the protocol continues to process transactions regardless of market cycles, and new applications can drive demand for block space even in bear phases. Microtransactions may reflect retail adoption, experimental protocols built on Bitcoin, or automated flows linked to sidechains and layer-2s. For investors, rising network usage during price drawdowns can be interpreted as a sign that utility and experimentation are progressing beneath the surface of market volatility, though it does not guarantee future price appreciation.

BTC as a Market Asset

Price History, Volatility, and Cyclical Drawdowns

BTC’s market history is characterized by dramatic cycles of appreciation and retracement. After early years of thinly traded markets, Bitcoin matured into a globally recognized asset with deep liquidity and a market capitalization measured in the hundreds of billions of dollars. Current spot data show BTC trading in the mid–\(\$60,000\) range with tens of billions in daily volume, though this level is still well below its all-time high, leaving BTC roughly 50% off peak valuations.

From a traditional market standpoint, recent price action has put Bitcoin into what many would term a cyclical bear phase, with some analysts noting that BTC has traded more than 20% below its peak and erased hundreds of billions of dollars in notional market value. Commentary from research desks highlights that BTC is on track for multiple consecutive negative quarters, with an 8% decline in the second quarter and the longest losing streak since the 2022 downturn, when it fell for four straight quarters. This context underscores that while BTC has delivered extraordinary long-term returns for early adopters, it remains prone to severe drawdowns and extended consolidation periods.

These cycles have become increasingly intertwined with broader macro and equity markets. In one recent episode, capital rotation into the artificial intelligence sector and high-growth tech names coincided with a slump in BTC, raising the odds of a break below the psychologically important \(\$60,000\) level according to some market strategists. At the same time, analysts at Cabot Wealth observed signs that Bitcoin may be decoupling from stocks in periods of U.S. dollar weakness, suggesting that correlations are regime-dependent rather than fixed. For investors, this means BTC can behave alternately like a high-beta tech proxy, a macro hedge, or an idiosyncratic asset, depending on the prevailing narrative and positioning.

The scale of Bitcoin relative to traditional assets also remains modest. Private market valuations such as SpaceX’s, reportedly surging to around \$2.5 trillion, now approach or exceed twice the entire BTC market value, a reminder that even at current levels Bitcoin is far from dominating global capital markets. This relativity cuts both ways: BTC is large enough to attract institutional attention and support ETF markets, yet still small enough that shifts in marginal demand, regulatory stance, or macro conditions can dramatically move price.

Spot Markets, Derivatives, and ETFs

BTC’s market structure spans spot exchanges, derivatives platforms, and regulated investment products. On the spot side, BTC is listed on virtually every major centralized exchange, trading against fiat currencies and stablecoins such as USDT. Regional exchanges like Upbit in South Korea list new altcoins simultaneously in BTC and USDT markets, reinforcing BTC’s role as a base pair alongside dollar-pegged instruments. The coexistence of BTC and USDT quote markets allows traders to express relative views on Bitcoin versus stable dollar exposure while rotating into smaller tokens.

Derivatives markets add another layer of complexity and liquidity. Bitcoin futures and perpetual swaps (perps) enable leveraged long and short positions, while options markets allow more nuanced expressions of directional and volatility views. Recent data point to sizeable options interest: on June 19, for instance, about 31,000 BTC options with a notional value of approximately \(\$1.92\) billion expired, with a put–call ratio of 0.78 and a “max pain” level near \(\$65,000\). By comparison, ETH options expiring the same day totaled roughly 138,000 contracts with a put–call ratio close to 1.03 and a max pain level around \(\$1,725\), but a smaller notional size of roughly \(\$230\) million. These figures underscore BTC’s dominance in the crypto options space and the degree to which derivatives flows can influence spot market behavior around key expiry dates.

Perhaps the most significant structural shift in recent years has been the rise of Bitcoin ETFs and similar exchange-traded products. Aggregators now track a growing roster of spot and futures-based Bitcoin ETFs around the world, publishing metrics on inflows, outflows, assets under management (AUM), and net asset value (NAV) for investors. These vehicles allow institutions and retail investors who cannot or do not wish to self-custody BTC to gain exposure through traditional brokerage accounts. The advent of U.S. spot Bitcoin ETFs, in particular, has been widely credited with broadening BTC ownership, even as flows ebb and flow with macro conditions.

Innovation continues within this ETF segment. Asset manager Franklin Templeton, for example, has filed for two Bitcoin DRIP (Dividend Reinvestment Plan) ETFs designed to reinvest stock dividends into BTC. The proposed products would start with a 95/5 split between U.S. equities and Bitcoin, capping BTC exposure at 20% while automatically channeling equity dividends into periodic BTC purchases. This structure effectively blends traditional equity exposure with systematic Bitcoin accumulation, framing BTC as a strategic satellite allocation within diversified portfolios rather than an all-or-nothing bet. Such designs illustrate how Bitcoin is being integrated into legacy financial products in ways that try to balance volatility with familiar income streams.

On-Chain Flows: Miners, Governments, and Large Holders

Beyond exchange order books, on-chain flows reflect the behavior of miners, governments, and large private holders. Miner economics are particularly important because miners both secure the network and represent a persistent source of potential sell pressure as they liquidate BTC to cover operating costs. Their holdings and flows can influence market structure, especially during periods of stress or after halvings.

Governments have also emerged as notable BTC holders, sometimes as a result of strategic accumulation and sometimes via asset seizures or state-backed mining programs. A striking example is Bhutan, whose government-linked wallets appear to have gradually sold around 10,451 BTC since June 2025, realizing roughly \(\$979\) million in value. Recent on-chain analysis suggests that about 533.2 BTC, worth around \(\$34.5\) million at the time of transfer, was sent to Binance, indicating continued offloading of their holdings. Such large-scale sales can create episodic supply overhangs but also illustrate that sovereign actors now meaningfully participate in Bitcoin markets.

Large mining pools and industry insiders likewise shape perceptions. Addresses linked to F2Pool co-founder Wang Chun, one of China’s most prominent Bitcoin miners, have reportedly been accumulating both ETH and wrapped BTC (WBTC), withdrawing thousands of ETH and over 120 WBTC from exchanges in recent transactions. This behavior highlights the increasingly multi-asset strategies of sophisticated players, who may hold BTC as a core position while simultaneously allocating to ETH and tokenized representations of BTC for use in DeFi. At the same time, corporate treasuries and listed firms that previously accumulated BTC have begun experimenting with dynamic allocation policies; for instance, Strategy’s decision to sell a portion of its BTC reserves to fund shareholder dividends has prompted debate about whether such sales signal weakening conviction or simply portfolio rebalancing.

Exchange reserves and transparency efforts offer another perspective on flows. Binance, for example, publishes recurring Proof of Reserves reports, with its 43rd report, based on a June 1 snapshot, indicating that user BTC holdings rose 4.26% from May to approximately 630,000 BTC, an increase of 25,838 BTC in a single month. User ETH balances also increased over the same period, though to a lesser extent. While Proof of Reserves does not fully eliminate counterparty risk or prove solvency, it provides a window into aggregate BTC accumulation on centralized platforms and demonstrates growing expectations that large exchanges offer verifiable accounting of customer assets.

Hashi adds Cumberland, Fluid, and SwissBorg before July global testnet to unlock over $1T in dormant BTC

Sui says Cumberland, Fluid, and SwissBorg have joined Hashi, its native Bitcoin finance primitive, weeks before a July global testnet. The bet is to turn over $1T of idle BTC into verifiable collateral without moving Bitcoin off its native chain: Sui smart contracts handle the programmatic rights, while the partner stack covers custody, liquidity, lending, oracles, insurance, and audits. It is an institutional BTCfi push, but still testnet-first; the real signal comes when liquidity and borrowers show up on mainnet.

- 01custodial and collateral fraud

The top two governance stories — USDD removing BTC collateral without DAO approval and Coinbase offering loans 'not backed by real BTC' — together drew over 1,000 clicks, showing readers track whether BTC held by third parties is real and accounted for.

- 02government BTC seizure and sale

US government moving $1.92B in BTC and Germany selling confiscated holdings attracted sustained attention because sovereign actors liquidating large tranches directly threaten price support and raise questions about state confiscation risk.

- 03leveraged liquidation cascades↗

The 17% crash wiping $600M in positions and the DeepSeek-triggered futures basis flip both show readers watch BTC as a leverage amplifier — the mechanism by which a macro catalyst becomes a crypto catastrophe.

- 04institutional legitimacy gatekeeping↗

Goldman Sachs hedging, Bill Miller affirming, and Vitalik attacking Saylor's bank-custody proposal formed a cluster of establishment-versus-crypto debate that readers treated as a proxy vote on whether BTC had 'arrived.'

- 05Bitcoin DeFi yield capture↗

Zest's BTC lending raise, Babylon's staking model, and the DLC.Link comparison attracted readers because they represent a novel risk frontier — putting BTC to work on-chain without wrapping it on Ethereum.

- 06exchange and wallet security failures

The DMM Bitcoin hack (4,502 BTC), the 139-BTC wallet theft generating an 84-BTC fee, and the investment-fraud stabbing incident collectively confirm that readers treat custody incidents as BTC's most concrete near-term threat.

Use Cases: From Digital Gold to Everyday Payments

Store of Value and “Digital Gold”

Many investors approach BTC primarily as a store of value, often likening it to digital gold. The rationale rests on several pillars: a fixed supply cap of \(21\,000\,000\) coins, a predictable issuance schedule with halvings, global accessibility, and resistance to censorship or seizure compared with some traditional assets. In theory, as more people come to view BTC as a desirable long-term savings vehicle, its price should reflect increasing demand for a finite set of coins.

However, BTC’s role as a store of value must be weighed against its high volatility and the reality of multi-year drawdowns. Long-term frameworks have emerged to help investors navigate these cycles. One widely cited metric is Bitcoin’s 200-week moving average (200W MA), which smooths out short-term price noise to highlight long-term trends. Dashboards such as Bitbo’s 200W MA chart allow market participants to compare spot price against this long-term average and identify periods when BTC trades significantly below its historical trend. Research shared in the market community suggests that historically, buying BTC when it dipped below the 200W MA has delivered strong median returns over one- and two-year horizons, though these patterns are backward-looking and do not guarantee future results.

Despite the caveats, this kind of long-horizon analysis reflects a broader shift in how BTC is perceived. Rather than treating Bitcoin purely as a speculative “trade,” many allocators frame it as a volatile but potentially rewarding component of a diversified portfolio, one that may benefit from disciplined, multi-year holding strategies. In this context, BTC competes not only with other crypto assets like ETH but also with gold, equities, and even real estate as a vehicle for preserving and growing purchasing power over time.

Medium of Exchange, Microtransactions, and Merchant Payments

Bitcoin’s original white paper framed it as a peer-to-peer electronic cash system, emphasizing its role in payments. While high on-chain fees and scaling limitations have constrained BTC’s use for everyday microtransactions at times, recent developments show renewed momentum around payment-focused infrastructure.

On-chain, analytics indicate a spike in small-value transactions, pushing Bitcoin’s microtransaction counts close to record levels and driving CryptoQuant’s Activity Index above its long-term trend. Coverage notes that this surge in network activity has occurred despite relatively weak price performance, suggesting that transactional usage is not solely a byproduct of speculative bubbles. These microtransactions may reflect retail transfers, experimental protocols, or activity on sidechains and payment channels that settle back to Bitcoin.

Off-chain, payment processors and infrastructure providers are working to reduce friction for merchants. GoMining, for instance, has introduced the GoBTC Pay Gen1 SDK and API, which enables merchants to accept instant, non-custodial Bitcoin payments for goods and services. The system is designed around BTC, aiming to provide an alternative to traditional processors such as Square by giving businesses more direct control over settlement and custody. By abstracting away technical complexity through developer tools and APIs, such initiatives seek to make Bitcoin usable for everyday commerce while preserving the security benefits of non-custodial architectures.

Wallet providers are also improving user experience. Some multi-chain wallets now support trading tokenized securities on networks like BSC and ETH, while offering enhanced tools for liquidity management and more granular Bitcoin fee controls, such as standard, fast, and instant fee tiers. These features are particularly relevant in volatile fee environments, allowing users to tailor their BTC transactions to their urgency and cost sensitivity. Together, these developments suggest that Bitcoin’s payments narrative is evolving in tandem with its store-of-value role, with infrastructure increasingly designed to handle both.

Yield, DeFi, and Bitcoin “Staking”

Unlike proof-of-stake networks, Bitcoin’s base layer does not natively support staking yields for BTC holders. Nevertheless, a range of off-chain and layer-2 solutions have emerged to offer BTC-denominated returns, blurring the lines between traditional yield products and crypto-native finance.

One prominent example is Stacks, a Bitcoin-linked smart contract layer that uses a consensus mechanism called Proof of Transfer (PoX). In the Stacks design, miners commit real BTC every roughly ten minutes to compete for STX block rewards, and that BTC is distributed to STX holders who participate in a process often called “Stacking.” Bitcoin holders can lock BTC under their own keys alongside STX to form a protocol bond and earn BTC-denominated yield, with payouts arriving roughly every Bitcoin week. According to Stacks’ documentation, the protocol has distributed over 4,200 BTC to participants since January 2021, and target annualized yields are around 3%, though realized returns vary with miner behavior and bonding dynamics.

This model is notable because it allows BTC holders to earn BTC yield without relinquishing custody of their coins to centralized platforms, at least in the idealized case. However, it introduces new layers of protocol risk, smart contract risk, and asset-price correlation risk through the STX component. Beyond Stacks, wrapped versions of BTC such as WBTC on Ethereum are widely used as collateral in DeFi protocols, enabling lending, borrowing, and liquidity provision. The aforementioned accumulation of WBTC by addresses linked to F2Pool’s co-founder illustrates how sophisticated actors integrate tokenized BTC into multi-chain strategies alongside ETH and other assets.

Centralized platforms have also promoted BTC yield products, offering interest-bearing accounts or structured notes. Past failures of some CeFi lenders and exchanges underscore the counterparty and rehypothecation risks associated with such offerings. For investors, the key distinction is between protocol-level yield mechanisms that are transparently enforceable on-chain and off-chain promises that rely on the solvency and risk management of intermediaries. Regardless of mechanism, any yield above the risk-free rate implies exposure to additional risk factors that must be carefully evaluated.

BTC as Collateral and Base Asset in Crypto Markets

BTC functions as a foundational asset in crypto market infrastructure. Many centralized exchanges allow users to post BTC as collateral for trading derivatives, margin products, and other instruments. Because BTC is highly liquid and widely accepted, it serves as a convenient and efficient form of collateral within the crypto-native financial system. Liquidations and margin calls are often denominated in BTC, which can amplify selling pressure when markets move sharply.

BTC is also deeply embedded as a base trading pair. On exchanges like Upbit, new tokens are often listed against both BTC and USDT, allowing traders to express relative value views between these assets and the broader altcoin universe. USDT, as a dollar-pegged stablecoin, provides a proxy for cash, while BTC functions as a crypto-native benchmark asset. The prevalence of BTC pairs reinforces its role as a unit of account within the ecosystem, even as stablecoins increasingly serve as the transactional medium in many DeFi protocols.

In decentralized finance, tokenized BTC such as WBTC, tBTC, or BTCB on chains like Ethereum and BSC is used extensively as collateral for lending, yield farming, and derivatives. This cross-chain usage expands BTC’s utility but also introduces bridge and smart contract risks. The interplay between base-layer BTC holdings and tokenized representations in DeFi portfolios underscores how Bitcoin now operates simultaneously as a settlement asset, a macro investment, and a programmable building block in multi-chain financial systems.

Infrastructure, Security, and Governance

Nodes, Mining, and Long-Term Security

Bitcoin’s security model rests on a combination of economic incentives and decentralized enforcement of rules by nodes. Full nodes verify every block and transaction, ensuring that the ledger remains consistent with consensus rules, while miners provide the computational work that makes rewriting history prohibitively expensive. This architecture is robust precisely because it minimizes trust in any single entity: users can run their own nodes, inspect the supply, and validate that the protocol’s monetary policy is being followed.

As block subsidies decline with each halving, the long-term question is whether transaction fees alone will provide sufficient incentive for miners to continue securing the network. Over time, BTC’s value must be high enough—and demand for block space must be strong enough—that fee revenue justifies miners’ capital and energy expenditures. The recent surge in microtransactions, inscriptions, and other on-chain activity suggests that there are plausible sources of fee demand beyond simple value transfer, but it remains an open research and policy question how this will evolve as issuance approaches zero.

Governance in Bitcoin is informal and emergent. Changes to the protocol typically require broad social consensus among developers, miners, businesses, and users, with controversial proposals often leading to extended debate. The lack of a central governance body makes rapid upgrades more difficult but also reduces the risk of unilateral rule changes, particularly around core parameters like the supply cap. This conservative ethos has reinforced Bitcoin’s identity as a stable monetary base layer, even as more experimental features are pushed to second-layer protocols and sidechains.

Security Risks, Social Engineering, and On-Chain Forensics

While the Bitcoin protocol itself has proven remarkably resilient, risks arise at the edges where human behavior and off-chain systems intersect. The most common threats to BTC holders are not protocol exploits but operational mistakes, counterparty failures, phishing attacks, and social engineering scams. Because BTC transactions are irreversible and pseudonymous, once funds are sent to a scammer’s address, victims rarely recover them without law enforcement or exchange intervention.

Recent investigations by on-chain sleuths highlight the sophistication and human toll of such schemes. On-chain investigator zachxbt, for example, traced approximately \$475,000 in frozen BTC back to a cluster of social engineering scams that appeared to target elderly Americans, after a suspected money mule reached out for help recovering funds. In a related case, he linked around 5.73 BTC frozen at the exchange Changelly to a broader scam network believed to have stolen over \$1 million, illustrating how scammers chain transactions across services to obscure provenance before funds are intercepted. These episodes demonstrate both the transparency and the limitations of Bitcoin’s public ledger: on-chain data can reveal the movement of funds and help cluster addresses, but legal and jurisdictional barriers often constrain remediation.

Such cases underline the importance of security hygiene for BTC users. Best practices include safeguarding seed phrases and private keys, using hardware wallets or other secure signing devices, verifying recipient addresses out of band, and treating unsolicited communications—especially those promising recovery of lost funds or insider opportunities—with extreme skepticism. Institutional investors add layers like multi-signature schemes, segregation of duties, and periodic audits. The rise of social engineering, particularly against vulnerable populations, suggests that education and robust consumer protections will be increasingly important as Bitcoin adoption widens.

Custody, Exchanges, and Proof of Reserves

For many participants, the biggest practical decision is whether to self-custody BTC or rely on custodial services such as exchanges, brokers, and institutional custodians. Self-custody offers maximum control and reduces counterparty risk but requires operational discipline and technical competence. Custodial solutions streamline user experience and facilitate integration with regulated products like ETFs and tax reporting, but concentrate risk in centralized entities.

In response to past exchange failures and regulatory scrutiny, some large platforms have adopted Proof of Reserves frameworks. Binance’s recurring PoR reports are illustrative: the exchange publishes Merkle-tree-based attestations that its on-chain BTC and ETH holdings at least match user balances, with its June 1 snapshot showing user BTC holdings at roughly 630,000 BTC, up 4.26% from the prior month. These disclosures help users monitor aggregate holdings and provide auditors with tools to verify reserve sufficiency, though critics note that PoR cannot, by itself, prove the absence of off-balance-sheet liabilities or rehypothecation.

For ETF and ETP investors, custody is handled by institutional custodians who must meet regulatory standards for capital adequacy, insurance, and operational security. This setup abstracts away key management but introduces a layer of trust in custodial practices and legal frameworks. Across all segments, the trend is toward more transparency, better risk management, and clearer delineation of responsibilities among exchanges, custodians, and users, as the ecosystem responds to both market failures and evolving regulatory expectations.

Grant Cardone says Cardone Capital will keep buying Bitcoin with rental cash flows, positioning its $200M BTC strategy as an alternative to Strategy's debt-funded playbook

22%-32% projected returns on a BTC/rent-roll hybrid only work if NOI keeps compounding while BTC volatility is doing the discounting for you. The cleaner part versus MSTR is less mNAV reflexivity; the ugly part is that a property downturn can hit rent collections, cap rates, and the DCA bid at the exact moment BTC is cheapest.

- 2023-07regulatory

Celsius court approves altcoin-to-BTC conversion

US SEC approves spot Bitcoin ETFs

- 2024-05exploit

DMM Bitcoin hacked — 4,502 BTC ($305M) stolen

- 2024-07governance

German government sells confiscated BTC tranche on Kraken and Coinbase

BTC crosses $100,000 for the first time

- 2025-01milestone

DeepSeek AI rout drops BTC 6%, flips CME futures basis negative

- 2025-01regulatory

Czech Republic BTC capital-gains exemption takes effect for 3-year holders

Near-record Bitcoin micro-transaction counts drive network activity surge

BTC in Relation to ETH, Stablecoins, and the Wider Crypto Ecosystem

BTC vs. ETH: Digital Commodity and Programmable Asset

BTC and ETH occupy distinct but overlapping roles in the crypto landscape. BTC, with its conservative monetary policy and limited scripting language, is widely seen as a digital commodity optimized for security and predictability. ETH, by contrast, powers a general-purpose smart contract platform capable of hosting decentralized applications, stablecoins, and complex financial protocols. This functional difference contributes to distinct valuation frameworks: BTC is often analyzed like a non-yielding macro asset whose value derives from scarcity and adoption, while ETH is increasingly framed as a productive asset whose value may be tied to transaction fees, staking yields, and application growth.

Institutional commentary, such as Grayscale’s conceptual “spectrum” of digital assets, explicitly separates BTC from tokens like HYPE, which are more directly tied to project revenues or tokenomics resembling equity. In this view, BTC sits at the commodity end of the spectrum, whereas many other tokens straddle the line between utility and quasi-equity. That distinction matters for regulation, tax treatment, and portfolio construction, even if price correlations between BTC and ETH remain elevated at times.

Nevertheless, the behavior of large market participants suggests that BTC and ETH are often treated as complementary exposures. On-chain data linking F2Pool co-founder Wang Chun to addresses accumulating both ETH and wrapped BTC indicates that major miners and whales may view ETH and tokenized BTC as part of a holistic multi-chain strategy, rather than as mutually exclusive bets. Wrapped BTC on Ethereum allows BTC holders to access DeFi yields and services, while ETH exposure reflects confidence in smart contract infrastructure and application growth. This coexistence highlights that, in practice, BTC’s dominance as a store of value does not preclude investors from simultaneously allocating to Ethereum’s programmable ecosystem.

Stablecoins, USDT Pairs, and BTC’s Role in Liquidity

Stablecoins such as USDT, USDC, and others have become integral to crypto trading by offering a dollar-pegged asset that can move natively on-chain. USDT in particular serves as the quote currency for many BTC trading pairs on centralized exchanges, giving traders a liquid way to move between Bitcoin exposure and synthetic cash without touching the banking system. BTC/USDT markets often command some of the highest volumes in crypto, reflecting this central role in liquidity formation.

The prominence of stablecoins does not diminish BTC’s importance; instead, it reframes BTC as one leg of a triangle that also includes stablecoins and other crypto assets. Exchanges like Upbit listing new tokens in both BTC and USDT markets exemplify this structure, with BTC representing a benchmark crypto asset and USDT standing in for fiat. DeFi protocols extend this pattern: pools pairing BTC with stablecoins, or tokenized BTC with ETH and other assets, form the backbone of many on-chain liquidity systems.

The growth of tokenized real-world assets, such as securities offered on BSC and ETH and traded through certain wallet extensions, further embeds BTC in a multi-asset ecosystem. Investors can hold BTC alongside tokenized equities, bonds, and commodities, shifting exposure fluidly across chains and products. In this environment, BTC’s role is as much about being a neutral, highly liquid collateral and benchmark asset as it is about being a day-to-day medium of exchange in its own right.

Cross-Asset Narratives and Capital Rotation

BTC no longer trades in isolation; its price is influenced by flows into and out of other risk assets, from U.S. tech stocks to alternative cryptocurrencies. Periods of intense enthusiasm for AI and space technology, exemplified by surging valuations in companies like SpaceX, can draw capital away from Bitcoin as investors chase perceived higher-growth opportunities. This type of capital rotation has been cited as a factor in BTC’s recent slumps, with some analysts warning of increased odds of a drop below key price levels such as \(\$60,000\) as flows redirect.

Within crypto, rotations occur between BTC, ETH, stablecoins, and altcoins. When sentiment turns risk-off, traders often move from smaller tokens into BTC and USDT, seeking relative safety. Conversely, when speculative appetite returns, capital can rotate from BTC into higher-beta altcoins. On-chain and exchange data showing increased BTC holdings on platforms like Binance, alongside rising ETH positions, suggest that users may be rebalancing between these core assets in response to changing narratives and relative value perceptions.

Government and corporate actions add another layer. Bhutan’s progressive sale of thousands of BTC, Strategy’s treasury rebalancing decisions, and accumulation patterns among miners and whales all contribute to supply–demand dynamics at the margin. Together, these cross-asset flows underscore that BTC’s price is not solely a function of its internal fundamentals; it is deeply entwined with global risk sentiment, technological themes, and regulatory developments across multiple asset classes.

Trading BTC: Strategies, Metrics, and Market Microstructure

Time Horizons, Valuation Frameworks, and the Long View

Investors approach BTC through diverse time horizons and frameworks. Some view it as a short-term trading instrument, exploiting volatility within days or weeks. Others adopt a long-term “digital gold” thesis, accumulating BTC over years based on conviction in its scarcity and network effects. Between these poles lie systematic strategies that rely on on-chain metrics, technical indicators, or macro signals.

One influential long-term tool is the 200-week moving average discussed earlier. Historically, BTC has only briefly traded below this average during severe bear markets, and such episodes have often preceded substantial recovery over subsequent years. Combined with halving cycles and on-chain measures of realized price, dormant supply, and address growth, the 200W MA forms part of a broader analytic toolkit for assessing when BTC is “cheap” or “expensive” relative to its own history. Market commentary citing median one- and two-year returns from purchasing below the 200W MA highlights the appeal of this approach, even as practitioners acknowledge that structural changes—such as ETF adoption or regulatory shifts—could alter future dynamics.

Valuation frameworks for BTC differ markedly from those for traditional securities. There are no cash flows to discount, no dividends, and no management teams. Instead, analysts focus on metrics such as market capitalization, realized capitalization, stock-to-flow ratios, and adoption proxies like wallet counts and transaction volumes. Grayscale’s “digital commodity” framing suggests that BTC’s value is best understood through the lens of supply–demand imbalances, network security, and its perceived role in portfolios, rather than through earnings-based models used for equities.

Leverage, Derivatives, and Liquidation Risk

Leverage is a powerful but dangerous feature of BTC markets. Many centralized and decentralized platforms offer margin and perpetual futures with high leverage multiples, allowing traders to amplify both gains and losses. Liquidation engines automatically close positions when margin falls below maintenance thresholds, creating feedback loops during sharp price moves.

Recent episodes underscore how quickly leverage can unwind. High-profile traders like Andrew Tate have reportedly been liquidated multiple times over short periods while flipping between leveraged BTC long and short positions, resulting in rapid depletion of account balances. While such anecdotes are specific, they are emblematic of a broader pattern: aggressive use of leverage in a volatile asset can lead to repeated forced exits and capital loss, even for experienced market participants.

Options markets add another dimension to leverage and risk management. The June 19 expiry of roughly \(1.92\) billion dollars’ worth of BTC options, with a put–call ratio of 0.78 and a max pain level at \(\$65,000\), illustrates the magnitude of capital deployed in structured BTC bets. Traders use calls and puts both to hedge spot holdings and to speculate on large moves, and clusters of open interest around key strikes can influence spot price behavior as expiration approaches. By analyzing put–call ratios, max pain levels, and open interest distributions, market participants attempt to anticipate potential “magnet” zones or volatility spikes around expiry dates, though such forecasts are far from precise.

On-Chain Indicators, Exchange Data, and Network Activity

Beyond price and derivatives, BTC traders increasingly look to on-chain data for signals. Metrics such as transaction counts, active addresses, UTXO age distributions, and realized profits and losses help gauge whether long-term holders are accumulating or distributing, whether new entrants are flooding in, and whether network usage is rising or falling.

CryptoQuant’s recent observations of near-record Bitcoin microtransaction counts and a rising Activity Index, especially during periods of price weakness, have been interpreted as signs that underlying network usage remains robust or is even accelerating. Crowdfundinsider’s coverage of surging microtransactions despite price declines reinforces this interpretation, suggesting that users may be leveraging Bitcoin for smaller transfers and novel on-chain applications. For some traders, this divergence between on-chain activity and price raises the possibility of eventual mean reversion in price; for others, it simply reflects decoupling between usage metrics and speculative demand.

Exchange data complement on-chain metrics. Proof of Reserves reports from platforms like Binance, showing rising user BTC and ETH balances, offer insight into aggregate accumulation on centralized venues. Government-linked transfers, such as Bhutan’s multi-year sale of more than 10,000 BTC and recent transfers to Binance, similarly inform assessments of large-scale supply overhangs and their potential impact on market structure. On-chain forensics used in scam investigations, while primarily focused on compliance and victim restitution, also demonstrate the transparency of BTC flows and the growing role of analytics in shaping market narratives.

- Custodial / CounterpartyHigh

Repeated incidents — DMM exchange hack, Coinbase misrepresenting BTC loan collateral, USDD removing BTC reserves without DAO vote — show that off-chain BTC custody remains a systemic vulnerability regardless of on-chain security.

- Governance / TransparencyHigh

Protocols and companies routinely move or encumber BTC holdings without on-chain consent, as the USDD collateral removal and the Celsius-Tether lawsuit both illustrate; BTC's governance-minimalist design leaves no native remedy.

A single 17% drawdown liquidated $600M in levered positions, and CME futures basis turned negative during the DeepSeek rout, confirming that derivatives overlays regularly amplify BTC volatility beyond spot fundamentals.

SEC ETF delays and government BTC liquidations signal ongoing policy uncertainty, but the eventual approval of US spot ETFs and Czech Republic's three-year capital-gains exemption indicate the regulatory trend is gradually accommodative.

Native Bitcoin DeFi protocols (Babylon pooled staking, Zest lending, DLC.Link) introduce smart-contract exposure to an asset whose base layer has none; the security trade-offs between models remain unresolved and under-audited.

BTC's 6% drop alongside Nasdaq during the DeepSeek AI shock and its inverse move ahead of the Trump inauguration suggest decoupling from equities is episodic rather than structural, undermining the pure store-of-value thesis.

Outlook

BTC has evolved from an experimental peer-to-peer cash system into a multi-faceted macro asset that anchors the broader crypto ecosystem while gradually integrating with traditional finance. Its protocol-level fundamentals—fixed supply, predictable issuance, and robust proof-of-work security—remain intact and widely understood, even as questions about long-term miner incentives and fee dynamics continue to invite debate. Network activity data, including rising microtransaction counts and a surging Activity Index, point to expanding on-chain usage that is not strictly tied to bull markets, suggesting a base layer of utility that persists through cycles.

On the market side, BTC’s maturation is evident in the depth of its spot and derivatives markets, the proliferation of ETFs and ETPs, and its adoption as collateral and base asset across exchanges and DeFi protocols. Innovations like Franklin Templeton’s proposed DRIP ETFs, Stacks’ self-custodial BTC yield model, and merchant-focused payment solutions such as GoBTC Pay illustrate how Bitcoin is being woven into diversified portfolios, yield strategies, and real-world commerce. At the same time, episodes of leveraged liquidations, government sales, and capital rotation into AI and tech equities underscore that BTC remains a high-volatility asset whose price is sensitive to broader risk sentiment and macro narratives.

Security and governance will continue to be central to Bitcoin’s long-term trajectory. The protocol’s conservative design and decentralized governance have so far preserved its monetary properties, but human-layer vulnerabilities—from social engineering scams targeting vulnerable populations to custodial failures—pose ongoing challenges that require education, regulation, and technological safeguards. As adoption widens, the interplay between self-custody, institutional custody, and regulatory frameworks will shape how different classes of investors access BTC and how systemic risks are managed.

Relative to other crypto assets, BTC’s role as a digital commodity and base layer appears secure, even as ETH and other networks compete for mindshare in programmable finance and application platforms. The coexistence of BTC with stablecoins, tokenized assets, and multi-chain DeFi suggests that Bitcoin will likely remain a foundational element of the crypto landscape rather than an isolated system. Whether BTC ultimately fulfills its loftiest ambitions—as a neutral, global reserve asset—will depend on factors ranging from regulatory acceptance and macroeconomic trends to continued innovation in scaling, custody, and integration with real-world financial infrastructure.

For now, BTC sits at the intersection of technology, economics, and geopolitics: a scarce digital asset with a transparent monetary policy, deeply integrated into both crypto-native and traditional markets, yet still subject to the sentiments, behaviors, and decisions of a rapidly evolving global investor base.

Latest BTC news

Public firms now hold over 1M BTC as Strategy, Tesla, Block and Metaplanet embrace Bitcoin treasury strategies to hedge inflation and attract investorsHashi adds Cumberland, Fluid, and SwissBorg before July global testnet to unlock over $1T in dormant BTCGrant Cardone says Cardone Capital will keep buying Bitcoin with rental cash flows, positioning its $200M BTC strategy as an alternative to Strategy's debt-funded playbookSources

- https://coinmarketcap.com/currencies/bitcoin/

- https://www.investopedia.com/tech/what-happens-bitcoin-after-21-million-mined/

- https://coinmarketcap.com/etf/bitcoin/

- https://www.benzinga.com/etfs/new-etfs/26/06/60002555/franklin-templeton-files-bitcoin-drip-etfs-that-reinvest-stock-dividends-into-crypto

- https://cryptoquant.com/insights/research/6a340f769139404af2b01f8f-18-June-2026-The-Surge-Near-Record-Bitcoin-Micro-Transaction-Counts-Drive-Networ

- https://www.stacks.co/bitcoin-staking

- https://www.cabotwealth.com/daily/tech-stocks/is-bitcoin-decoupling-from-stocks

- https://charts.bitbo.io/ma-200w/

- https://cryptorank.io/news/feed/2922b-bitcoin-options-1-9b-expiry-june-19

- https://gomining.com/blog/gobtcpay

- https://www.crowdfundinsider.com/2026/06/286518-bitcoin-btc-network-activity-surges-due-to-uptick-in-micro-transactions-despite-price-weakness/

- https://www.youtube.com/watch?v=yoJu-N0f8gk

- https://cryptoquant.com/insights/research/6a340f769139404af2b01f8f-18-June-2026-The-Surge-Near-Record-Bitcoin-Micro-Transaction-Counts-Drive-Network

- https://x.com/CoinDesk/status/2067990599127482762

- https://x.com/WuBlockchain/status/2068001885324493217

- https://www.facebook.com/vantagemarkets.glb/posts/bitcoin-is-on-track-to-close-three-consecutive-weeks-in-the-red-since-the-start-/992895763641669/

- https://www.advfn.com/stock-market/COIN/BTCUSD/crypto-news/98774939/bitcoin-decouples-from-tech-stocks-is-60k-btc-s

- https://x.com/WuBlockchain/status/2067598519670641109

- https://x.com/WuBlockchain/status/2067519630810522035

Community notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…