In‑depth explainer on crypto bear markets, covering definitions, cycles, on‑chain indicators, sector impacts on BTC, ETH, USDC and Coinbase, and how investors can navigate crypto winter and spot signs a downturn may be nearing its end.

+9 sources across the wider coverage universe

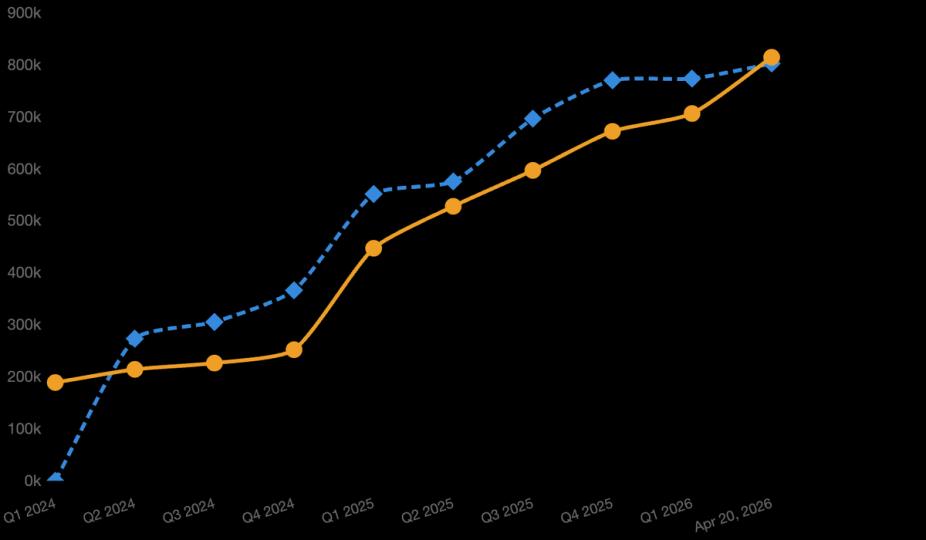

Strategy overtakes BlackRock's IBIT with 815,061 BTC after $2.54B bear market buy, biggest weekly add since November 20242026-04

Strategy overtakes BlackRock's IBIT with 815,061 BTC after $2.54B bear market buy, biggest weekly add since November 20242026-04 Eli Ben-Sasson reflects on bear market from stormy seas, calls TradFi's grip a crushing bear hug2026-03

Eli Ben-Sasson reflects on bear market from stormy seas, calls TradFi's grip a crushing bear hug2026-03 Bitcoin is stuck in a slow bear market as ETF demand stays negative, drawdowns age, and no macro catalyst signals reversal.2026-02

Bitcoin is stuck in a slow bear market as ETF demand stays negative, drawdowns age, and no macro catalyst signals reversal.2026-02 ConfluxCapital trading bots gain traction as investors seek stable returns amid volatility, using automated long/short strategies to profit in both bull and bear markets2026-04

ConfluxCapital trading bots gain traction as investors seek stable returns amid volatility, using automated long/short strategies to profit in both bull and bear markets2026-04 Pantera Capital says 2025 was a macro-driven year with extreme dispersion, where Bitcoin held up while most altcoins stayed in a prolonged bear market. Looking into 2026, Pantera sees improving setups driven by institutional adoption, clearer product-market fit, and supportive liquidity conditions.2026-01

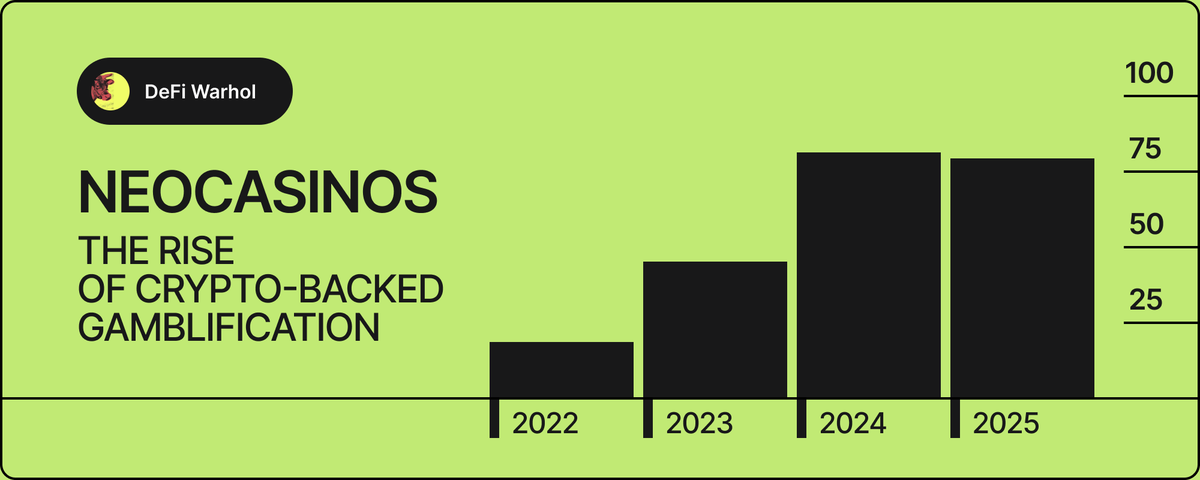

Pantera Capital says 2025 was a macro-driven year with extreme dispersion, where Bitcoin held up while most altcoins stayed in a prolonged bear market. Looking into 2026, Pantera sees improving setups driven by institutional adoption, clearer product-market fit, and supportive liquidity conditions.2026-01 Analyst breaks down the rise of neocasinos—crypto-backed casinos, prediction markets, and high-leverage trading platforms—showing how provably fair tech, stablecoin rails, and regulatory arbitrage drove GambleFi to $80B+ revenue and strong bear-market resilience.2026-02

Analyst breaks down the rise of neocasinos—crypto-backed casinos, prediction markets, and high-leverage trading platforms—showing how provably fair tech, stablecoin rails, and regulatory arbitrage drove GambleFi to $80B+ revenue and strong bear-market resilience.2026-02

A bear market in crypto is a prolonged period in which asset prices trend downward, liquidity thins out, and sentiment is dominated by caution or outright pessimism, often following a sharp drawdown from prior highs. While painful, these phases are also when market structure resets, unsustainable projects are flushed out, and longer‑term opportunities quietly emerge for disciplined participants.

Bear Markets in Crypto: An Evergreen Guide

Understanding bear markets is essential for anyone serious about digital assets, whether you are trading Bitcoin futures on a daily basis or dollar‑cost averaging into ETH and USDC in a long‑term portfolio. Traditional finance generally defines a bear market as a fall of at least 20% in a broad market index over a period of roughly two months or more. Crypto inherits that framework, but because Bitcoin (BTC), Ethereum (ETH), and other tokens are more volatile than equities, their drawdowns frequently exceed 50–80%, and the associated “crypto winter” conditions can last many months. Recent cycles have illustrated how bear markets ripple through every layer of the ecosystem, from Bitcoin miners capitulating at or below their production cost, to centralized exchanges like Coinbase facing weaker spot volumes, to DeFi protocols such as Satori Finance shutting down in the face of declining trading activity and liquidity. At the same time, on‑chain analytics, halving‑driven cycle models, and metrics like MVRV Z‑Score have given investors a richer toolkit for identifying where they are in the cycle and for distinguishing between temporary corrections and deep structural bear phases. This explainer walks through what a bear market is, how it unfolds in crypto, which indicators matter, how different sectors are affected, and how sophisticated investors think about risk, opportunity, and timing in these periods.

Defining a Bear Market: From TradFi to Crypto

A natural starting point is to understand how bear markets are defined in traditional markets, because much of crypto’s vocabulary and market lore is inherited from equities and macro investing. In conventional finance, regulators and educators often describe a bear market as a time when stock prices are declining and sentiment is pessimistic, usually measured as a decline of 20% or more in a major index such as the S&P 500, sustained for at least two months. This threshold is somewhat arbitrary, but it provides a convenient line between ordinary volatility and a more serious, cyclical downturn. Bull markets, by contrast, refer to extended periods of rising prices and broadly favorable economic conditions. For decades, this bull–bear distinction has framed how investors talk about cycles, risk tolerance, and asset allocation across equities, bonds, and commodities.

Crypto markets imported the same language almost immediately, but the numbers behind it had to be reinterpreted. In a technology‑driven asset class where 10–20% intraday swings are not uncommon, a 20% drawdown from a local peak may say little about the underlying regime. Because of this heightened volatility, practitioners often treat drawdowns greater than 50% from all‑time highs in BTC or ETH, combined with sustained pessimism and lower volumes, as a more realistic threshold for a full‑blown crypto bear market. That is why periods like 2018 or 2022–2023 are remembered as bear markets, even though they included powerful rallies: the dominant trend was downward, and repeated relief rebounds ultimately rolled over into lower lows. The term “crypto winter,” which emphasizes both the depth and the duration of the downturn, has become shorthand for these more extreme phases.

It is useful as well to distinguish between structural bear markets and shorter‑lived corrections. Markets that are experiencing sustained and substantial declines, accompanied by deteriorating sentiment and macro headwinds, are typically categorized as bear markets. A correction, by contrast, might involve a 10–30% pullback in BTC or ETH within a larger bull phase, often driven by profit‑taking or temporary risk aversion rather than a fundamental deterioration of liquidity and credit conditions. The line between the two can only be drawn decisively in hindsight, but practitioners rely on a combination of price, volume, macro data, and on‑chain behavior to infer whether a correction is evolving into a deeper bear phase.

Finally, in crypto the bear/bull distinction is not only about direction but also about the underlying market microstructure. A bull market in Bitcoin, Ethereum, or altcoins tends to be characterized by rising prices, expanding volumes, tight spreads, aggressive venture fundraising, and a proliferation of new tokens and protocols, many of which are speculative. A bear market reverses most of these conditions: volumes contract, spreads widen, leverage is reduced, under‑collateralized lenders face stress, and the market selectively rewards projects with genuine product‑market fit while punishing those reliant on reflexive token incentives. The same words—bull and bear—thus describe not just price trends but the entire environment in which crypto participants operate.

Robinhood's layoffs reflect a late-stage crypto bear market, but Altcoin Pro analysts argue the industry's restructuring is a reset rather than a reason to panic

Robinhood cut ~290 roles while June ADV in equities, options, and prediction markets was hitting records, so the stress sits in crypto mix compression rather than platform survival. Crypto revenue fell 47% YoY to $134M in Q1; if that stays soft, HOOD will keep pushing prediction markets, tokenized equities, and other low-touch rails while treating spot crypto as a customer-acquisition funnel. For alts, the pain is less dramatic but nasty: thinner retail flow at the app layer means wider CEX spreads and more speculative beta moving back to perps, points farms, and on-chain leverage.

Leviathan readers treat bear markets as a shopping aisle, not a warning sign — the highest-clicked angles are specific yield products, builder playbooks, and infrastructure pivots *within* the drawdown, revealing an audience that is hunting alpha through the pain rather than fleeing it.↗

The Anatomy of a Crypto Bear Market

A crypto bear market typically unfolds in recognizable phases, even though each cycle has its own catalysts and nuances. The first phase is usually a topping process, in which BTC, ETH, and high‑beta altcoins stop making new highs despite still‑strong sentiment and inflows. During this stage, market indicators such as the MVRV Z‑Score or long‑term moving averages may show that Bitcoin is becoming historically overvalued relative to its realized or “fair” value. In some cycles, such as those centered around Bitcoin halving events, price peaks have aligned with specific on‑chain and technical signals, including crossovers of key moving averages like the 111‑day and doubled 350‑day simple moving averages. This topping phase can produce a series of failed breakouts and growing divergences between price and on‑chain activity as large holders quietly reduce exposure into strength.

The second phase is often the initial liquidation cascade, where leveraged longs are forced to unwind, creating a rapid and sometimes violent down‑move. In 2022, for example, the failure of large projects and crypto lenders amplified the downside, leading to steep price falls across the sector and seeding the conditions for what many described as a crypto winter. This kind of deleveraging is not unique to crypto; equities and commodities experience similar dynamics when margin calls and risk limits force asset sales. However, because crypto’s leverage is distributed across centralized exchanges, offshore derivatives platforms, and on‑chain money markets, the contagion path can be complex and hard to map in real time. When confidence falters, the interplay of forced liquidations, stablecoin redemptions, and cross‑asset collateral sales can drive price action well beyond what traditional valuation models would suggest.

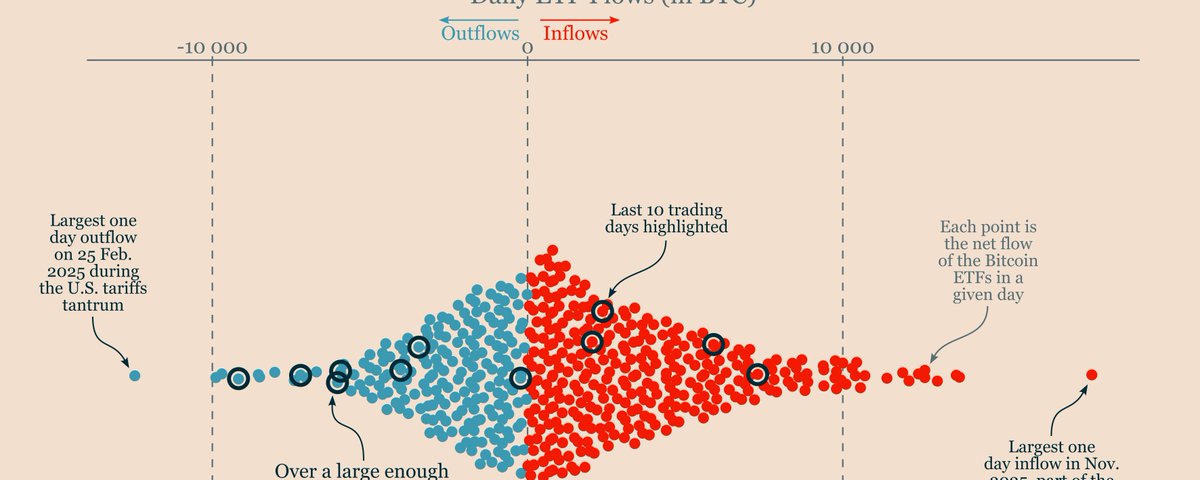

After the initial cascade, bear markets often enter a grinding phase characterized by lower highs, lower lows, and extended periods of sideways price action. In this environment, rallies become opportunities for trapped holders to exit at improved prices, reinforcing a ceiling on recovery attempts. CoinGecko’s analysis of early‑2026 conditions, for instance, describes how Bitcoin’s 22% quarterly drop, combined with a 20.4% contraction in total crypto market capitalization and a nearly 40% decline in spot exchange volumes, marked a decisive shift from correction to fully‑fledged crypto winter. During such phases, the narrative tends to shift from euphoric adoption stories to sober discussions of regulation, macro risk, and the sustainability of token‑based business models. Retail participation fades, institutional flows become more selective, and projects with weak balance sheets or unclear value propositions begin to falter.

The final phase of a bear market is often referred to as capitulation and subsequent accumulation. Capitulation is the point at which even committed holders begin to sell into weakness, driven by a mix of exhaustion, loss aversion, and the belief that “this time is different” in a structurally negative way. On‑chain data has documented this pattern in multiple assets. XRP, for example, has recently exhibited a realized profit‑to‑loss ratio where on‑chain sellers are realizing approximately $2.63 in losses for every dollar of profit, a dynamic analysts interpret as a textbook capitulation event that historically signals a bear market may be nearing exhaustion. Similarly, Bitcoin miner metrics show periods where miners operate on razor‑thin margins, or even at a loss, and some capitulate by selling reserves when BTC trades near or below estimated production and electrical costs. These conditions can coincide with powerful narrative pessimism, yet they have historically been associated with attractive long‑term entry points for patient investors.

Bear Markets and the “Crypto Winter” Concept

The phrase “crypto winter” has become closely associated with the most severe bear markets in digital assets, particularly those following the 2017 and 2021 bull cycles. The term evokes not only price declines but a persistent chill in sentiment, funding, and activity across the ecosystem. The World Economic Forum has described crypto winter as a period during which cryptocurrency prices have dropped a long way and then stayed low for weeks or months, often following a combination of macro headwinds and industry‑specific shocks. In 2022, for example, the collapse of the TerraUSD stablecoin project and the subsequent troubles of lenders such as Celsius Network triggered sharp sell‑offs, driving Bitcoin to multi‑year lows and eroding confidence in crypto’s internal credit system. As deleveraging spread, venture investment slowed, hiring freezes and layoffs became more common, and many retail investors exited the market.

More recently, CoinGecko’s quarterly analysis for the first quarter of 2026 uses similar language to characterize the environment. Their report highlights a 20.4% contraction in total crypto market capitalization, equivalent to roughly $622 billion, leaving the asset class about 45% below its October 2025 all‑time high. Bitcoin’s 22% drop during the quarter underperformed major equity indices, including the Nasdaq and S&P 500, indicating that digital assets bore the brunt of risk‑off sentiment as geopolitical tensions and a more hawkish Federal Reserve weighed on global markets. Spot trading volumes on the top ten centralized exchanges fell by nearly 40%, underscoring how both directional interest and short‑term trading activity can evaporate as bear conditions set in. Together, these data points illustrate how the crypto winter concept captures both market performance and a broader cooling in ecosystem momentum.

Crypto winter has important behavioral implications. For builders and long‑term investors, winter can be a season for consolidation, product refinement, and accumulation at lower prices. For more marginal projects, it is a survival test that often ends in shutdowns or forced mergers. In this environment, stories such as Satori Finance announcing it will shut down due to challenging market conditions, or certain Bitcoin layer‑2 projects facing reality checks on adoption and economics, become emblematic of how bear markets separate durable protocols from speculative experiments. Yet at the same time, one sees examples of contrarian accumulation, such as Nasdaq‑listed Bit Digital purchasing around $20 million in ETH for its corporate treasury at an average cost in the low $2,300s, bringing its holdings to over 158,000 ETH despite the Ethereum bear market backdrop. These contrasting behaviors are a hallmark of late‑stage bear markets, where pessimism and strategic positioning coexist.

Tools and Indicators for Identifying Bear Markets in Crypto

Because crypto trades around the clock and has no underlying cash flows in the way that stocks do, market participants rely on a mixture of price‑based, technical, and on‑chain indicators to diagnose bear markets and assess where they are in the cycle. At the simplest level, investors look at drawdowns from all‑time highs: when BTC or ETH has fallen by more than 50% and remains suppressed for months, the case for a bear market is straightforward. Bitcoin’s 2022 episode, where it lost almost 65% of its market value before eventually recovering and rising more than 500% from the low, is an example of this dynamic. However, price alone can be misleading, since bear markets often include sharp rallies that retrace a significant portion of prior losses before rolling over, sometimes luring in new participants who mistake the move for the start of a fresh bull run.

Technical indicators based on moving averages and trend signals add nuance. One widely cited family of signals focuses on the relationship between shorter‑ and longer‑term moving averages of BTC’s price. For example, CoinMarketCap highlights an indicator using the 111‑day simple moving average and the 350‑day simple moving average multiplied by two, noting that crossings of the 111‑day moving average above the doubled 350‑day average have coincided with prior Bitcoin bull market peaks. Conversely, when spot prices fall below long‑term moving averages such as the 200‑week moving average, analysts often interpret this as evidence of deep bear conditions and potential value zones. Market strategists have pointed out that Bitcoin testing levels near its 200‑week moving average, which in some analyses also aligns with the estimated production cost for efficient miners, has historically corresponded with major bear market lows or accumulation ranges. These relationships are not deterministic, but they provide historical context for current price action.

On‑chain metrics bring a different lens by looking at blockchain‑level data rather than only exchange‑traded prices. The MVRV Z‑Score, for instance, compares Bitcoin’s market capitalization to its realized capitalization (a proxy for the aggregate cost basis of coins) and standardizes the result to highlight periods when BTC appears extremely over‑ or undervalued relative to previous cycles. In past bear markets, MVRV Z‑Score readings near zero or negative have coincided with major cyclical bottoms, as in 2014, 2018, and 2022, because they indicate that the market price is close to or below the average on‑chain acquisition price of coins. Current analysis often focuses not only on the aggregate MVRV but also on separate readings for long‑term and short‑term holders, with convergence between these cohorts interpreted as a sign that the market has largely digested prior gains and losses and is closer to resetting. When MVRV approaches zero but long‑term and short‑term metrics have not yet fully converged, some analysts argue that the bottoming process may still have more time to run.

Realized losses and profit‑taking patterns provide another window into bear markets. Data showing that Bitcoin’s realized losses remain significantly below those seen at the depths of the 2022 bear market suggests that the current downturn may not yet have fully exhausted holders’ willingness to sell below cost, raising the possibility of further downside or at least continued choppy conditions. Similarly, CryptoQuant research has examined the share of unspent transaction outputs (UTXOs) held for six months or longer and observed that in prior bear markets, this long‑term holder share collapsed sharply as large‑scale distribution took place. The absence of such a collapse in a given drawdown has led some analysts to argue that, structurally, the market may not yet be in a classic bear market phase, or that long‑term holders are behaving differently in the current cycle. These debates highlight that no single metric can define a bear market; instead, investors triangulate using multiple indicators and historical analogies.

Mining‑related metrics are particularly important for Bitcoin. Because miners incur real‑world costs in electricity and hardware, their breakeven levels create economically meaningful reference points for market valuation. Recent analysis from quantitative managers such as Capriole Investments suggests that Bitcoin’s spot price has at times traded near its estimated production cost, with miners’ profit margins shrinking to under 5%, levels near prior cycle lows. Mining “capitulation” indicators, which track the relationship between price, network difficulty, and miner behavior, have historically turned deeply negative near bear market bottoms, signaling that weaker miners are exiting and selling reserves while stronger operators survive and consolidate. Traders sometimes view miner capitulation as a powerful contrarian buy signal, arguing that there has been “no clearer sign” to add BTC exposure than when miners finally give up after months of pressure. Nonetheless, these signals are probabilistic rather than guaranteed; cycle timing and macro conditions can alter their reliability.

The table below summarizes several commonly discussed bear market indicators in crypto and what they typically signal.

| Indicator | What it measures | Bear‑market interpretation |

|---|---|---|

| Drawdown from ATH | Percent decline from all‑time high | Sustained drops >50% in BTC/ETH often associated with bear markets |

| 200‑week moving average | Long‑term trend and support | Price below or near this level historically marks deep value zones |

| MVRV Z‑Score | Market cap relative to realized cap | Values near or below zero align with prior bear market lows |

| Realized losses | Aggregate realized loss on‑chain | Peaks in realized losses often occur near capitulation bottoms |

| Miner profit margins/capitulation | Mining profitability and forced selling | Thin margins and miner exits coincide with late‑stage bear markets |

| Spot/trading volumes | Market activity on exchanges | Significant volume declines reinforce bear‑market conditions |

Each of these tools should be used in context rather than isolation. For example, a low MVRV Z‑Score is more meaningful when accompanied by signs of miner stress, subdued trading volumes, and a macro backdrop of risk aversion, all of which together make it more plausible that a bear market is maturing or approaching its end. Similarly, a sharp drop below the 200‑week moving average may be a better signal when it follows months of distribution and leverage unwinding rather than occurring suddenly amid an idiosyncratic shock. For investors in Bitcoin, Ethereum, or diversified crypto portfolios, the art lies in synthesizing these quantitative signals with qualitative assessments of technology, regulation, and macro trends.

- 01Bear market yield hunting↗

The top headline — Gearbox's 60%+ APY Curve V2 pools framed explicitly against the bear market's day count — pulled nearly 400 clicks, with YieldNest TVL growth adding confirmation that readers want specific, named products generating outsized returns in down conditions.

- 02Builder and developer playbook↗

Coinbase CEO's 10 developer ideas and Seed Club's incubator-in-the-bear framing both performed strongly, showing readers seek structured guidance on where to direct attention when speculation dries up.

- 03Market neutral survival strategies↗

The 'market neutral trenches' headline drew 175 clicks on pure tactical framing, indicating readers are actively looking for delta-neutral or hedged approaches rather than directional bets.

- 04RWA-to-DeFi-native capital rotation↗

The Ethena Labs founder's quote — that RWA demand is a bear market phenomenon, with capital rotating back to DeFi-native risk as sentiment shifts — crystallised a regime-change thesis readers found immediately useful.

- 05Bitcoin macro bottom signals↗

Three separate bear-bottom-timing headlines (ETF demand staying negative, Stage 5 capitulation thesis, and the Black Monday global cascade) clustered around 58–81 clicks each, reflecting sustained demand for macro reversal cues.

- 06Corporate treasury leverage danger↗

Bit Digital CEO's warning that secured debt could wipe out Ethereum treasury firms attracted 94 clicks, surfacing reader anxiety about the new wave of companies levering up on digital assets during a down cycle.

How Bear Markets Affect Different Parts of the Crypto Ecosystem

Bear markets do not impact all crypto sectors equally. Bitcoin, as the largest and most liquid asset, often sets the tone for the broader market. When BTC enters a bear phase, correlations across digital assets tend to rise, and portfolios dominated by altcoins can suffer even larger percentage drawdowns as liquidity concentrates in perceived “safer” majors. Empirical research on the Covid‑19 bear market illustrates that Bitcoin itself can move in lockstep with equities during crises, undermining the notion that it is a reliable safe haven and highlighting its substantial downside risk when combined with traditional risk assets. During that period, portfolios mixing the S&P 500 with even modest allocations to Bitcoin experienced greater downside risk than the S&P alone, with measures such as Value‑at‑Risk and Conditional Value‑at‑Risk increasing meaningfully as BTC weightings rose. These findings suggest that in bear markets, Bitcoin behaves more like a high‑beta component of the risk asset complex than a hedge.

Ethereum and other smart‑contract platforms face their own set of challenges and opportunities in bear markets. On the negative side, reduced speculative activity in sectors like NFTs, DeFi, and gaming translates into lower on‑chain transaction volumes and fee revenues, which can dampen the economic value of base‑layer tokens like ETH and SOL. On the positive side, bear markets often accelerate the shift from speculative use cases toward more durable adoption themes, such as real‑world assets (RWAs), institutional DeFi, and blockchain infrastructure that solves concrete business problems. Even in the face of a challenging market backdrop, Ethereum has continued to deepen its role in RWA tokenization and institutional pilots, while some builders and analysts argue that ETH and competing platforms like Solana may be poised for gains once the crypto bear market ends and capital rotates back into growth narratives. These dynamics emphasize that bear markets are periods of re‑pricing and re‑prioritization, not simply uniform decline.

Altcoins and layer‑2 ecosystems experience particularly acute stress during prolonged bears. Tokens with weaker fundamentals, unclear governance, or reflexive tokenomics often suffer 80–95% drawdowns from their highs, and some never reclaim prior levels even in subsequent bull cycles. This process of creative destruction can be brutal for holders but also serves as a selection mechanism, rewarding architectures and communities that can continue shipping and maintaining user engagement despite lower token prices. Reports of Bitcoin layer‑2 projects facing bear‑market reality checks, where assumptions about user growth, fee revenue, or security models are tested against actual usage, illustrate how downturns expose weaknesses that were masked by rising prices and abundant liquidity. At the same time, protocols that endure through these conditions often emerge with stronger market share, improved capital efficiency, and more sustainable incentives.

Stablecoins such as USDC play a distinctive role in bear markets as both a refuge and a vector of contagion. When risk appetite collapses, many traders and investors rotate from volatile assets into dollar‑pegged stablecoins, either to preserve capital or to keep “dry powder” on‑chain for future deployment. This can support demand for high‑quality, transparently backed stablecoins, while under‑collateralized or poorly managed ones come under scrutiny. The failure of algorithmic stablecoins, most notably TerraUSD, during prior downturns underscored the importance of robust collateral frameworks and risk management. For market participants using USDC on Ethereum, Solana, or other chains, bear markets are often a time when stablecoin balances increase relative to risky token holdings, and yield opportunities—such as lending USDC into money markets—are reassessed in light of counterparty risk and protocol security.

Centralized exchanges and brokers, including major venues like Coinbase, are highly sensitive to bear‑market conditions because their revenues are often tied to trading volumes and asset prices. CoinGecko’s observation that spot volume on the top ten centralized exchanges dropped nearly 40% in a single quarter during early 2026 gives a sense of how quickly business conditions can deteriorate when market activity dries up. Lower volumes mean lower fee revenues, while reduced retail interest can also limit the growth of ancillary services such as staking, derivatives, or subscription products. At the same time, bear markets increase regulatory scrutiny and operational challenges, as risk management, compliance, and custody standards come under the microscope. For listed companies such as Coinbase, this combination of cyclical and structural pressures often translates into share price volatility and shifting investor narratives between “survivor with leverage to the next bull cycle” and “exposed to prolonged crypto winter.”

Crypto‑native lenders, market‑makers, and DeFi protocols are also deeply affected. When prices fall and volatility spikes, margin calls, liquidations, and collateral shortfalls can propagate through interconnected balance sheets. The events of 2022 demonstrated how quickly stresses at one lender or hedge fund can spread through the system, as rehypothecated collateral, unsecured lending, and opaque risk transfers created a web of exposures that only became visible after defaults. In the current cycle, some decentralized protocols and trading platforms have been forced to shut down or pivot as volumes and liquidity waned, with Satori Finance’s decision to close operations standing out as a recent example of how bear markets claim casualties among innovative but vulnerable projects. By contrast, better‑capitalized market‑makers and DeFi blue chips might use the period to consolidate market share, refine risk engines, and prepare for future growth.

Finally, the culture and public perception of crypto shift markedly in bear markets. Whereas bull markets are associated with high‑profile sponsorships, lavish conferences, and mainstream media attention, bear phases often reveal a more introspective and sometimes contradictory industry psyche. For instance, reports of the crypto industry hosting extravagant events, including lap‑dance parties, in the midst of a bear market have sparked criticism that parts of the ecosystem remain distracted by excess even as investors nurse large losses. Such episodes can influence regulators’ and the public’s views of the sector, potentially shaping policy debates and institutional willingness to engage with Bitcoin, Ethereum, and other digital assets. Understanding these social and reputational dimensions is part of understanding bear markets as more than just price charts.

Trading, Investing, and Risk Management in a Bear Market

For investors and traders engaging with BTC, ETH, and the wider crypto market, bear markets pose a different set of challenges and opportunities than bull markets. In a rising market, simply being long a diversified basket of assets can deliver strong returns, and the main risk is failing to participate enough. In a bear market, by contrast, the primary risk is capital destruction, and even previously “safe” strategies—such as yield‑farming stablecoins or providing liquidity to blue‑chip pools—can carry underappreciated tail risks. The Covid‑19 crisis highlighted that adding Bitcoin to a traditional equity portfolio can increase downside risk during systemic stress, rather than providing a hedge. That finding should encourage investors to think carefully about position sizing, diversification, and correlations when structuring portfolios for bear‑market resilience.

Long‑term investors who treat Bitcoin or Ethereum as strategic allocations often adopt dollar‑cost averaging (DCA) approaches in bear markets, allocating a fixed amount of capital at regular intervals regardless of price. This method reduces the risk of attempting to “catch the bottom” and ensures participation in any eventual recovery, though it also demands strong conviction and patience. Historical data showing that Bitcoin has risen multiple‑fold from prior bear market lows—for example, climbing more than 500% from its 2022 bottom—can strengthen that conviction, but the past does not guarantee future performance. Moreover, long‑term investors must be psychologically prepared for prolonged underwater periods and significant volatility even after the cycle turns, as early bull phases can include large pullbacks that test resolve.

Active traders, on the other hand, often see bear markets as an arena for short‑selling, volatility trading, and relative‑value strategies. Declining prices and increased two‑sided order flow can create opportunities for those who can accurately anticipate trend continuations, mean‑reversion, or liquidation cascades. However, leveraged short positions carry their own risks, particularly during bear‑market rallies that can produce sharp, sudden squeezes. Trading on futures platforms or using options requires careful margin and risk management, attention to funding rates, and awareness of counterparty risk. Derivatives volumes can sometimes remain robust even as spot volumes decline, but liquidity conditions can deteriorate during extreme moves, leading to slippage and execution challenges.

Stablecoins and cash‑equivalents play an important strategic role in bear markets for both investors and traders. Holding USDC on‑chain or fiat in brokerage accounts offers optionality to deploy capital when risk‑reward improves, while also reducing exposure to drawdowns in BTC, ETH, and altcoins. Some participants seek yield by lending stablecoins or providing liquidity to low‑risk pools, but bear‑market episodes such as the Celsius and TerraUSD failures illustrate that even ostensibly conservative yield‑seeking strategies can entail counterparty and protocol risk when market conditions deteriorate. A prudent approach often involves prioritizing safety and liquidity over marginal yield, especially if the primary objective is to preserve capital and maintain flexibility.

Risk management in bear markets extends beyond asset selection and leverage to encompass operational and behavioral considerations. Operationally, participants need to evaluate exchange risk, custody arrangements, and smart‑contract exposures, recognizing that system stress can reveal previously unseen vulnerabilities. Behaviorally, emotions such as fear, regret, and impatience can drive sub‑optimal decisions, from panic‑selling at lows to revenge‑trading after losses. Setting clear time horizons, position size limits, and maximum drawdown thresholds before entering trades or investments can help counteract these tendencies. For institutions managing digital asset treasuries, a well‑defined governance framework, including investment policies and risk committees, can be the difference between opportunistic accumulation and uncontrolled exposure. The decision by firms like Bit Digital to continue accumulating ETH despite the bear environment reflects one side of this strategic calculus.

Terra/LUNA collapse wipes $40B+, accelerates bear onset

FTX collapse deepens crypto winter, contagion spreads to lenders

Curve Finance reentrancy exploit (~$70M) strikes at bear market nadir

US Bitcoin spot ETFs approved, opening institutional on-ramp

Bitcoin fourth halving reduces block reward to 3.125 BTC

Global 'Black Monday': BOJ rate hike triggers Nikkei -15%, BTC -15%, $900M liquidated

Pantera Capital notes macro-driven dispersion: BTC resilient, most altcoins in prolonged bear

Strategy acquires 815,061 BTC after $2.54B bear market buy, surpassing BlackRock IBIT

Macro, Correlation, and the Safe‑Haven Debate

One of the defining features of recent crypto bear markets has been their interaction with macroeconomic cycles and traditional risk assets. In theory, Bitcoin was often marketed as “digital gold,” a hedge against inflation, monetary debasement, or financial repression. In practice, empirical evidence from episodes like the Covid‑19 bear market indicates that Bitcoin has behaved more like a high‑beta risk asset, moving largely in tandem with equities and amplifying downside risk rather than providing a safe haven. During the 2019–2020 period studied by researchers, even modest allocations of Bitcoin to an S&P 500 portfolio increased measures of downside risk, and at no tested allocation weight did BTC reliably act as a shelter during stress. This challenges narratives that treat Bitcoin as a straightforward hedge and underscores the importance of scenario analysis across different macro regimes.

The macro backdrop can also shape the depth and duration of crypto bear markets. For example, CoinGecko’s Q1 2026 analysis ties the shift from sharp correction to full‑blown crypto winter to a combination of ongoing bearish momentum, geopolitical tensions, and a hawkish turn in US monetary policy after the nomination of Kevin Warsh as Federal Reserve Chair, which raised expectations of tighter financial conditions. Higher interest rates generally increase the opportunity cost of holding non‑yielding or speculative assets, while also tightening liquidity across global markets. This macro tightening can push risk‑sensitive assets like BTC, ETH, and growth stocks into deeper drawdowns, even if their underlying technologies continue to develop.

Correlation patterns during bear markets further complicate portfolio construction. When cross‑asset correlations rise, diversification benefits diminish, and portfolios that combine Bitcoin, Ethereum, tech stocks, and other growth exposures may suffer simultaneous drawdowns. Stablecoins like USDC provide some relief by offering dollar exposure on‑chain, but they introduce their own risks related to issuer creditworthiness, regulatory treatment, and collateral management. As a result, sophisticated allocators increasingly consider crypto exposure as part of an integrated risk budget covering all risk assets, rather than as an isolated “alternative” bucket presumed to behave differently under stress.

Regulation and policy responses to crypto also tend to accelerate during bear markets, when policymakers feel less pressure from highly visible price appreciation and more urgency to address perceived risks. Failures of major platforms or systemic events in DeFi can lead to calls for stricter oversight of exchanges, stablecoin issuers, and custodians, while securities regulators may scrutinize token issuances and marketing practices more aggressively. For firms like Coinbase, this often means navigating both cyclical revenue pressures due to lower trading volumes and structural shifts in the regulatory environment, including licensing, capital requirements, and disclosure standards. For investors, understanding how regulatory trajectories differ across jurisdictions becomes part of assessing medium‑term bear‑market risks and long‑term adoption prospects.

Signals That a Bear Market May Be Ending

Investors are naturally interested in identifying when a bear market is nearing its end, even though no indicator can provide certainty. Historically, crypto bear markets have often ended with a cluster of signals suggesting capitulation, valuation reset, and structural healing. Capitulation, as noted earlier, shows up both in price and in on‑chain realized loss data. When indicators suggest that market participants are realizing large aggregate losses—such as Bitcoin’s realized losses approaching or surpassing prior cycle peaks, or XRP holders realizing multiple dollars of loss for every dollar of profit—analysts infer that weaker hands are being washed out and that selling pressure may be close to exhaustion. This process is emotionally and financially painful, but it helps reset the supply–demand balance.

On‑chain valuation metrics provide complementary perspectives. MVRV Z‑Score readings near zero or negative have historically coincided with periods when Bitcoin was trading close to or below its aggregate cost basis, a condition associated with long‑term value zones rather than late‑cycle euphoria. When such readings are combined with signals of miner capitulation and historically low miner profit margins, as well as subdued spot trading volumes and neutral or negative funding rates, the argument strengthens that the market is in a late bear or early accumulation phase. Nonetheless, analysts also watch for convergence between long‑term and short‑term holder MVRV metrics, as persistent divergence can suggest that the distribution process is incomplete and that further volatility is possible even after initial value signals flash.

Price action around key technical and economic levels is another piece of the puzzle. The 200‑week moving average has repeatedly acted as a long‑term support region for Bitcoin during past major bear markets, and some strategists view spot prices near this level as opportunities to build or add to positions, while recognizing that intraday or intraweek deviations can occur. Simultaneously, estimates of miners’ production and electrical costs provide a fundamental floor of sorts: when BTC trades at or below these breakeven levels, weaker miners are squeezed, but stronger ones may choose to hold or even accumulate coins rather than sell into depressed markets. The interaction between these cost‑based supports, long‑term moving averages, and on‑chain valuation metrics offers a triangulated view of where the market stands.

Sentiment and narrative also evolve as bear markets mature. Early in a downturn, newsflow often centers on failures, regulatory threats, and reports of structural weakness, such as warnings that Bitcoin’s bear market shows signs of fragility or that an additional “purge” is possible because realized losses remain below prior cycle peaks. Later, coverage begins to highlight mixed signals: some analysts caution that a rally may be a “trapdoor” into a deeper bear stage, with potential final bottoms in specific price zones, even as others point to improving indicators such as MVRV Z‑Score approaching zero or institutional buyers quietly accumulating. Simultaneously, stories emerge of corporate treasuries or asset managers using the downturn to build positions, like the strategy that accumulated large BTC holdings through sizeable bear‑market purchases, or Bit Digital’s ETH acquisition. The coexistence of pessimism and strategic optimism is characteristic of turning points, though not every such configuration leads immediately to a sustained bull market.

It is important to recognize that bear‑market endings are processes rather than moments. Recovery often involves a sequence of higher lows and higher highs in BTC and ETH, compressing volatility, improving breadth across altcoins, and gradually rising volumes. Macro conditions may shift toward a more supportive stance, whether through stabilization of interest rates, easing of geopolitical tensions, or increased institutional adoption of blockchain infrastructure. Yet setbacks and sharp pullbacks remain common, and narratives about “new bull markets” can prove premature. Investors should treat bottom‑calling with caution and instead focus on whether their frameworks for valuation, risk, and time horizon remain valid as the data evolves.

RWA demand fell 37% as DeFi-native risk appetite returned, showing capital rotation can drain liquidity from yield-bearing instruments rapidly when sentiment flips.

Secured debt taken against digital asset treasuries risks forced liquidation in a prolonged drawdown; the Bit Digital CEO warning specifically flagged Ethereum treasury firms as most exposed.

Negative ETF demand, aging drawdowns, and the August 2024 Black Monday cascade — where BTC fell 15% and $900M was liquidated in 24 hours — illustrate how macro shocks amplify crypto-specific selling.

Curve's 2023 reentrancy exploit hit during the bear market nadir when liquidity was already thin, demonstrating that protocol-level risk is not lower in bear conditions and recovery can take the full cycle.

Miners pivoting 70%+ revenue to AI and firms like Strategy accumulating 815,061 BTC concentrate economic weight in a handful of corporate actors whose distress could cascade across markets.

The Digital Euro's privacy and bear-market headwinds, combined with Eli Ben-Sasson's characterisation of TradFi's grip as a 'crushing bear hug', reflect ongoing friction between crypto infrastructure and regulatory incumbents.

Lessons from Past Bear Markets

Looking back at prior crypto bear markets provides context for interpreting current conditions, even though no cycle is identical. The 2014–2015 bear market, following Bitcoin’s early speculative surge and the Mt. Gox collapse, saw BTC prices fall more than 80% from the peak, with extended periods of sideways trading and limited mainstream attention. This episode illustrated that technology and development can continue during market winters, as core protocol upgrades and early experiments in colored coins and tokenization happened largely out of the spotlight. It also underscored how concentrated infrastructure risk—such as reliance on a single dominant exchange—can amplify the impact of failures on both prices and sentiment.

The 2018 bear market, following the 2017 ICO boom, offered a different pattern. Massive issuance of ERC‑20 tokens on Ethereum, many tied to speculative funding promises, fueled a euphoric bull market that eventually reversed as regulatory scrutiny increased and project fundamentals failed to match valuations. When the cycle turned, Bitcoin and Ethereum experienced deep drawdowns, but ICO tokens suffered even worse, with many losing the majority of their value and some effectively going to zero. On‑chain indicators such as MVRV Z‑Score and long‑term holder distribution were instrumental in documenting the unwind. This period demonstrated how excess leverage and speculative funding can concentrate in particular sectors—in this case, ICOs—and how bear markets reprice not just assets but entire narratives about what blockchain innovation should prioritize.

The Covid‑19 bear market in early 2020 introduced a new set of lessons about crypto’s interaction with global macro shocks. As the pandemic triggered a rapid sell‑off in equities, bonds, and commodities, Bitcoin’s price declined in tandem with the S&P 500, rather than providing a hedge. Empirical studies showed that holding BTC alongside the S&P 500 increased portfolio downside risk, with measures such as Value‑at‑Risk rising as Bitcoin allocation weights grew. This challenged the thesis of Bitcoin as a straightforward safe haven and suggested that its role in portfolios may resemble that of a macro‑sensitive, high‑beta asset more than that of digital gold, at least under certain conditions. Yet the post‑crash recovery and subsequent bull market also demonstrated that severe drawdowns can precede periods of extraordinary growth, reinforcing the idea that bear markets sow the seeds of future cycles.

The 2022–2023 bear market and subsequent recovery into 2024 and beyond combined elements of all these prior episodes. Structural excesses in DeFi, centralized lending, and algorithmic stablecoins contributed to a dramatic unwinding of leverage, with high‑profile failures eroding trust and liquidity. At the same time, regulatory scrutiny increased, and macro headwinds from inflation and rising interest rates pressured all risk assets. Bitcoin’s decline of roughly 65% from its high, followed by a more than 500% rally from the eventual bottom, illustrated the magnitude of cycle swings and the potential rewards for those who survived the downturn. Throughout this period, tools such as MVRV Z‑Score, miner capitulation metrics, and cycle‑based models informed analysis of where the market stood relative to historical bear patterns. For Ethereum, the transition to proof‑of‑stake and growth in new sectors like RWAs and institutional DeFi showed how fundamental innovation can proceed even amid harsh price environments.

One recurring theme across all these bear markets is the importance of distinguishing between signal and noise. For every rigorous analysis of on‑chain data or macro conditions, there are episodes of speculative exuberance or despair, including instances of the industry celebrating excess even as prices fall, such as the much‑discussed lap‑dance party held during a bear market period. Investors and builders who succeeded over multiple cycles tended to focus less on short‑term narratives and more on core questions: whether Bitcoin’s security and adoption continue to strengthen; whether Ethereum and other platforms are solving real problems; whether stablecoin and DeFi architectures are robust; and how regulation and macro trends are shaping the environment for long‑term growth. Bear markets, by compressing valuations and exposing weaknesses, often make it easier to see which answers are credible.

Outlook

Bear markets in crypto are both a recurring feature of the asset class and a crucial mechanism through which excesses are purged, capital is reallocated, and new leadership emerges. For Bitcoin and Ethereum, each completed bear cycle has, so far, been followed by new all‑time highs and broader adoption, although the path between those points has been highly volatile and uncertain. For altcoins and experimental protocols, the outcomes have been more varied, with many projects failing to recover while a subset solidifies its position and captures greater mindshare. What is common across cycles is that the line between survivorship and obsolescence is often drawn during bear markets rather than bull phases.

Looking ahead, investors should expect that future crypto bear markets will continue to be influenced by macroeconomic conditions, regulatory developments, and technological evolution. On‑chain analytics, such as MVRV Z‑Score and realized loss metrics, are likely to remain central to how the community gauges cycle positioning, while mining data, ETF flows, and corporate treasury activity will shape narratives around institutional adoption and structural demand. Stablecoins like USDC, centralized platforms such as Coinbase, and major smart‑contract networks including Ethereum will all face tests of resilience whenever liquidity tightens and sentiment sours. At the same time, new sectors—whether RWAs, modular blockchain infrastructure, or Bitcoin layer‑2 solutions—will be evaluated not just on their token prices but on their traction and robustness under bear‑market conditions.

For participants today, the most constructive approach is to treat bear markets neither as existential threats nor as guaranteed buying opportunities, but as complex phases that demand careful analysis, disciplined risk management, and humility. Understanding the anatomy of bear markets, the indicators that characterize them, and the ways they reshape the crypto landscape can help investors, builders, and policymakers navigate these periods more effectively. Whether one is holding BTC and ETH for the long term, trading altcoin volatility, or managing a corporate treasury that includes stablecoins and digital assets, integrating bear‑market thinking into strategy is essential. Cycles will continue, but the outcomes for each participant will depend on how well they prepare for winter, endure it, and position themselves for the eventual thaw.

Latest Bear Market news

Sources

- https://www.investor.gov/introduction-investing/investing-basics/glossary/bear-market

- https://www.coinbase.com/learn/crypto-basics/what-is-a-bull-or-bear-market

- https://www.fidelity.com/learning-center/trading-investing/four-year-bitcoin-and-crypto-cycles

- https://www.weforum.org/stories/2022/06/cryptocurrency-crash-crypto-winter/

- https://coinmarketcap.com/charts/crypto-market-cycle-indicators/

- https://www.bitcoinmagazinepro.com/charts/mvrv-zscore/

- https://www.tradingview.com/news/cointelegraph:a55d3cb28094b:0-bitcoin-miner-capitulation-comes-as-trader-sees-later-2026-bear-market-bottom/

- https://www.binance.com/en/square/post/332587758435185

- https://www.facebook.com/BitcoinMagazine/posts/just-in-bitcoin-is-up-over-574-since-the-2022-bear-market-low-this-is-just-the-b/1277481253784286/

- https://www.instagram.com/p/DZwsR8fjsDi/

- https://blockchair.com/news/bitcoin-risks-new-purge-with-bear-market-losses-still-35b-below-2022-total--718dbb7563b2abee

- https://www.youtube.com/watch?v=b-kQkhXchFU

- https://cryptoquant.com/insights/quicktake/69c21dfb5b3e5f5175a7cc33-We-Are-Not-in-a-Bear-Market

- https://www.bloomberg.com/news/articles/2026-05-09/crypto-industry-throws-lap-dance-party-in-middle-of-bear-market

- https://www.investopedia.com/insights/digging-deeper-bull-and-bear-markets/

- https://www.crowdfundinsider.com/2026/04/273910-bitcoin-bear-market-and-crypto-winter-indicate-sharp-shift-in-investor-sentiment-analysis/

- https://pmc.ncbi.nlm.nih.gov/articles/PMC7246008/

- https://x.com/WuBlockchain/status/2059996499686334867

Community notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…