In-depth explainer on crypto market structure, from classical theory to DeFi and derivatives, and how U.S. bills like the CLARITY Act, stablecoin rules and tokenization pilots are reshaping trading, banking links and regulation.

+11 sources across the wider coverage universe

NYDIG says the Senate’s crypto market structure bill may not pass until August, warning the legislation could stall entirely if it misses the pre-midterm window2026-05

NYDIG says the Senate’s crypto market structure bill may not pass until August, warning the legislation could stall entirely if it misses the pre-midterm window2026-05 Over 100 crypto firms push U.S. Senate to advance market structure bill, demanding clear SEC-CFTC roles and protections for non-custodial developers2026-04

Over 100 crypto firms push U.S. Senate to advance market structure bill, demanding clear SEC-CFTC roles and protections for non-custodial developers2026-04 Galaxy Digital says seven Senate Democrats could decide the fate of the CLARITY Act, a key crypto market structure bill facing markup this Thursday2026-05

Galaxy Digital says seven Senate Democrats could decide the fate of the CLARITY Act, a key crypto market structure bill facing markup this Thursday2026-05 BREAKING: Banks and crypto firms have privately agreed on a deal for the Bitcoin market structure bill. An announcement is expected this week.2026-04

BREAKING: Banks and crypto firms have privately agreed on a deal for the Bitcoin market structure bill. An announcement is expected this week.2026-04 Trump pledges future-proof crypto market structure as CLARITY Act faces 60-vote Senate math2026-05

Trump pledges future-proof crypto market structure as CLARITY Act faces 60-vote Senate math2026-05 SEC Says Most Crypto Assets Aren’t Securities, Clarifying That Protocol Mining, Staking and Airdrops Do Not Create Securities and Paving the Way for Clearer U.S. Crypto Market Structure Rules [2026-03

SEC Says Most Crypto Assets Aren’t Securities, Clarifying That Protocol Mining, Staking and Airdrops Do Not Create Securities and Paving the Way for Clearer U.S. Crypto Market Structure Rules [2026-03

Market Structure in Crypto: How Trading, Rules and Technology Fit Together

How buyers and sellers meet, trade and set prices is what economists call market structure—and in digital assets, that structure is being redesigned in real time. Understanding it is increasingly essential for anyone trading crypto, building protocols, or following the U.S. debate over the CLARITY Act and broader “crypto market structure” legislation now moving through the Senate.

What Do We Mean by “Market Structure”?

In classical economics, market structure describes how an industry is organized: how many buyers and sellers there are, how much power each has, how differentiated the products are, and how easy it is for new competitors to enter or exit. These characteristics shape pricing power, profit margins and the overall efficiency of an industry, from commodities to consumer goods. For example, a market with many small firms selling identical products and no barriers to entry approximates perfect competition, while a market dominated by a single firm is a monopoly. Between these extremes lie oligopolies, where a handful of large firms control most of the volume, and monopolistic competition, where many firms offer similar but differentiated products.

In finance, the term is used more narrowly to describe the architecture of trading itself. It encompasses where orders are posted and matched, who can see what information when, how trades are cleared and settled, and which intermediaries sit in the middle of each step. A stock may trade on exchanges, dark pools and over‑the‑counter desks; each of these venues has its own rules, fee structures and incentives, and together they define the equity market’s structure. Crypto markets follow the same basic logic but layer in new variables, from automated market makers (AMMs) and perpetual futures to on‑chain settlement and composable DeFi protocols.

This is why “crypto market structure” has become a term of art in Washington as well as on trading desks. In Congress and at agencies like the Securities and Exchange Commission (SEC) and Commodity Futures Trading Commission (CFTC), the phrase now refers to the entire regulatory and institutional design of how digital assets are issued, traded, custodied and supervised. The CLARITY Act and parallel Senate bills are, at their core, attempts to hard‑code a durable market structure for crypto into U.S. law—defining what counts as a security or commodity, which regulator oversees which activity, and where traditional banking rules intersect with stablecoins and DeFi.

For traders and builders, market structure is not an abstract policy idea. It determines who can access which venues, what kinds of strategies are viable, how easily capital can move between CeFi and DeFi, and what protections exist when things go wrong. It also shapes competitive dynamics: whether liquidity concentrates on a few centralized exchanges, fragments across many on‑chain pools, or migrates to jurisdictions with more permissive rules. As the White House’s crypto adviser has warned, countries that lag in building coherent market structure frameworks risk “falling behind in the digital assets race.”

Crypto enters its “Graham era” as looming U.S. market structure laws could unlock value-accruing tokens, shifting investors from memecoin speculation toward fundamentals

15-9 out of Senate Banking is the kind of catalyst desks can underwrite: if fee switches, burns, or distributions stop being an SEC roulette table, UNI, AAVE, and MKR/SKY get priced against fee durability instead of vibes. Uniswap’s fee-switch fight already showed why this matters: the market wants return of capital, but governance has to prove it can route cash flow without insider capture or LP revolt. Memecoins keep their casino bid, but the opportunity cost changes once capital can buy provable on-chain P/E with legal-ish value return.

Readers are tracking the CLARITY Act as a political prediction market, clicking hardest on swing-vote counts, odds cuts, and backroom deal rumors — not on the policy substance — revealing that the audience treats U.S. crypto market structure legislation as a binary risk event rather than a regulatory process.↗

Market Structure in Traditional Economics and Finance

To understand crypto’s trajectory, it helps to start with how economists and financial regulators think about market structure in established markets. Classical industrial organization focuses on three main dimensions: the number and size distribution of firms, the characteristics of the products they sell, and the conditions of market entry and exit. In perfectly competitive markets, many small firms offer a homogeneous good, each is a price taker, and new firms can enter freely. No single firm can move prices, and long‑run profits tend toward zero. In monopolies, a lone firm controls supply, faces the market demand curve directly, and can set prices well above marginal cost; barriers to entry, such as patents or regulatory franchises, prevent rivals from emerging.

Between those poles, oligopolies and monopolistic competition offer mixed features. In an oligopoly, a small number of large firms—think major airlines or big oil companies—dominate supply and often respond strategically to each other’s price and output choices. In monopolistic competition, many firms sell differentiated versions of similar products, such as branded consumer goods, soft drinks, or restaurants in a city. Firms possess some pricing power because of brand loyalty or differentiation, but entry is still relatively easy, limiting long‑run abnormal profits. These classical categories matter in crypto because they help frame debates over whether, for instance, a handful of centralized exchanges constitute an oligopoly, or whether a dominant stablecoin issuer has quasi‑monopolistic power over dollar liquidity on‑chain.

In financial markets, regulators and market participants focus on market microstructure, which studies the mechanisms and rules through which securities are traded and prices are formed. Order‑driven exchanges match buyers and sellers through centralized limit order books; dealer markets rely on market makers quoting bid and ask prices and standing ready to trade. Key design choices include transparency (who sees which orders), priority rules (price‑time priority versus pro‑rata), and tick sizes. These microscopic details influence spreads, volatility, and the incentives of high‑frequency traders. Because financial markets are networks of venues and intermediaries, “market structure” also encompasses how exchanges, brokers, custodians, clearing houses and settlement systems connect.

Regulators like the SEC and CFTC supervise traditional market structure through detailed rulebooks and enforcement programs. The SEC, which oversees securities markets, has published dedicated resources on crypto, including a “Crypto Task Force” that seeks to clarify how federal securities laws apply to digital assets. The CFTC, which regulates futures and certain spot commodity markets, has likewise outlined its role in overseeing virtual currency derivatives and processes like self‑certification by exchanges listing new products. In traditional finance, equities market structure reforms such as Regulation NMS in the United States have reshaped how orders are routed between exchanges and dark pools, how quotes are consolidated, and how competition between venues is managed.

Market structure in traditional finance is therefore the product of both private innovation and public rulemaking. Innovations such as electronic communication networks, high‑frequency trading and dark pools all began as market structure experiments; regulators then adjusted rules to address perceived abuses or inefficiencies. Crypto is going through a similar cycle, but at a higher speed and with more fundamental questions still unresolved about asset classification, jurisdiction and the boundaries between banking and capital markets.

Crypto Market Structure: Core Building Blocks

Digital asset markets add several new layers to the basic idea of market structure. At the highest level, crypto market structure involves three interlocking domains: centralized finance (CeFi), decentralized finance (DeFi), and the interface between crypto and traditional banking. Each domain has its own venues, intermediaries and rules, and the balance between them is still evolving.

On the centralized side, most retail and institutional trading still happens on centralized exchanges that operate order books much like traditional stock exchanges. These platforms aggregate spot trading, leveraged margin products, and in some jurisdictions derivatives such as perpetual swaps and futures. They also often act as custodians for user funds, integrating wallet infrastructure, fiat on‑ramps, and staking or lending products on a single platform. Because they are often global and lightly regulated compared to national securities exchanges, their internal market structure—fee tiers, maker‑taker rebates, margin rules, risk management—has emerged largely through competition rather than prescriptive regulation. This concentration of functions in a few large exchanges raises familiar concerns from traditional finance about conflicts of interest and too‑big‑to‑fail institutions, which are now appearing in legislative debates.

On the decentralized side, DeFi protocols implement trading and lending functions entirely via smart contracts. Automated market makers such as constant‑product pools allow users to swap tokens against liquidity provided by other users, with prices adjusting algorithmically based on pool balances rather than a centralized order book. Lending protocols operate as pooled balance sheets, where users supply collateral and borrow against it at floating rates set by supply and demand. These systems mimic many functions of banks and broker‑dealers—maturity transformation, leverage, liquidity provision—but do so without insured deposits, capital requirements, or lender‑of‑last‑resort support. As a result, legislators and regulators are now considering how DeFi fits into existing market structure frameworks and where new rules are needed.

Stablecoins occupy a central role in crypto market structure by serving as the primary settlement and collateral asset for much of the ecosystem. Dollar‑pegged tokens backed by reserves in bank accounts have become the de facto base currency on many exchanges and in DeFi pools. This gives their issuers and the banks that hold their reserves significant influence over liquidity conditions on‑chain and on centralized platforms. The growth of stablecoins has also raised concerns from banking groups that they could displace traditional deposits and reduce the availability of bank credit, particularly if stablecoin holders can earn interest or yield that competes with bank savings accounts. These concerns directly inform the stablecoin provisions in current U.S. market structure bills.

The third pillar is the interface between crypto and the banking system. Fiat on‑ and off‑ramps, custodial partnerships, and bank‑issued tokenization platforms all live here. Recent U.S. legislative drafts explicitly contemplate allowing banks and credit unions to use distributed ledger systems and digital assets in otherwise authorized activities, including tokenization of securities and other financial instruments. In parallel, experiments such as on‑chain repo transactions executed on permissioned networks show how traditional institutions are testing blockchain rails for familiar market structure workflows, including competitive price discovery via existing RFQ platforms and atomic settlement within regulated frameworks. Together, these developments underline that crypto market structure is converging with, rather than replacing, much of the existing financial stack.

- 01CLARITY Act Senate vote math↗

Readers fixated on the precise head-count — seven swing Democrats, 60-vote threshold, and TD Cowen's probability cut — treating passage odds like a tradeable asset.

- 02SEC vs CFTC jurisdiction lines↗

The SEC's declaration that most crypto assets are not securities, and that mining, staking, and airdrops don't create securities, directly sets the boundary between the two regulators that the CLARITY Act formalizes.

- 03Derivatives volume dominance↗

The structural shift of crypto exchange competition toward derivatives — now dominating spot trading volume — signals a maturation that makes exchange-level market structure rules more urgent.

- 04Industry lobbying pressure↗

A coalition of 100+ firms including Coinbase, Ripple, and a16z demanding clear SEC-CFTC role splits showed readers that industry had moved from commentary to coordinated political action.

- 05Stablecoin-market structure linkage↗

The Circle and Coinbase rally tied to lawmakers redefining stablecoin yield incentives revealed that stablecoin policy and market structure bills were being negotiated as a package, not independently.

- 06AI-driven VC model disruption

Falling build costs from AI collapsing the value of capital-for-product VC deals shifted reader attention to how project financing and token distribution economics will change under new market structure rules.

Microstructure in Crypto: Liquidity, Derivatives and Basis Trades

Under the hood, crypto markets have distinctive microstructural features that shape how prices are formed and how risk is transferred. One of the most important is the heavy use of perpetual futures and other derivatives. On many global exchanges, not subject to U.S. restrictions, perpetual swaps referencing bitcoin and major altcoins account for a large share of trading volume. These products roll indefinitely and use funding rates to keep futures prices anchored to spot. The prevalence of derivatives means that a significant fraction of crypto price action is driven by leveraged traders, market makers and arbitrageurs rather than simple spot buying and selling.

A classic example is the bitcoin basis trade, where an investor goes long spot bitcoin and short bitcoin futures to capture the difference between the futures price and the spot price. When the basis is positive and wide, this trade can generate attractive low‑risk yields, drawing in institutional capital and hedging activity. Recently, analysts have noted that the unwind of basis trades has been reflected in shifting futures market structures, with the gap between futures and spot narrowing as leveraged longs and carry traders reduce positions. Such shifts in the term structure of futures prices can signal changes in market sentiment, funding conditions, and the composition of participants, and thus are themselves part of the evolving market structure narrative.

On the DeFi side, AMM designs influence slippage, capital efficiency and the distribution of returns between traders and liquidity providers. Concentrated liquidity models, stable‑swap curves and hybrid order‑book/AMM systems are all experiments in market microstructure. They determine how quickly prices adjust to large trades, how sensitive pools are to impermanent loss, and how easily sophisticated participants can arbitrage price discrepancies across venues. These factors feed back into where liquidity chooses to reside; professional market makers may favor centralized exchanges with deep order books, while long‑tail tokens may rely on AMMs where listing is permissionless.

Liquidity fragmentation is another defining feature of crypto market structure. Because tokens can trade on dozens of centralized exchanges and across multiple chains and DeFi protocols, no single venue has a complete view of the market. This fragmentation makes price discovery more complex and creates opportunities for cross‑venue arbitrage, but it can also increase volatility and reduce transparency. Aggregators and smart routers have emerged to stitch together liquidity across DEXs and chains, much as smart order routers do across stock exchanges and dark pools in traditional finance. From a regulatory perspective, one of the challenges the CLARITY Act and related bills confront is how to apply concepts like national best bid and offer, consolidated audit trails, and best execution duties in such a fragmented, global environment.

In CeFi, the vertical integration of trading, custody, lending and staking on single platforms introduces market structure questions that have direct policy implications. When an exchange also runs a proprietary trading desk or lends out customer assets, conflicts of interest arise reminiscent of pre‑unbundling eras in traditional markets. Some of the collapse narratives in past crypto crises involved opaque rehypothecation and maturity mismatches that would likely have been constrained or prohibited under traditional market structure rules. These episodes have strengthened the hand of policymakers arguing that crypto firms performing exchange, broker‑dealer and custody functions should be subject to comparable safeguards, including segregation of customer assets and robust bankruptcy protections.

The U.S. “Crypto Market Structure Bill” Debate

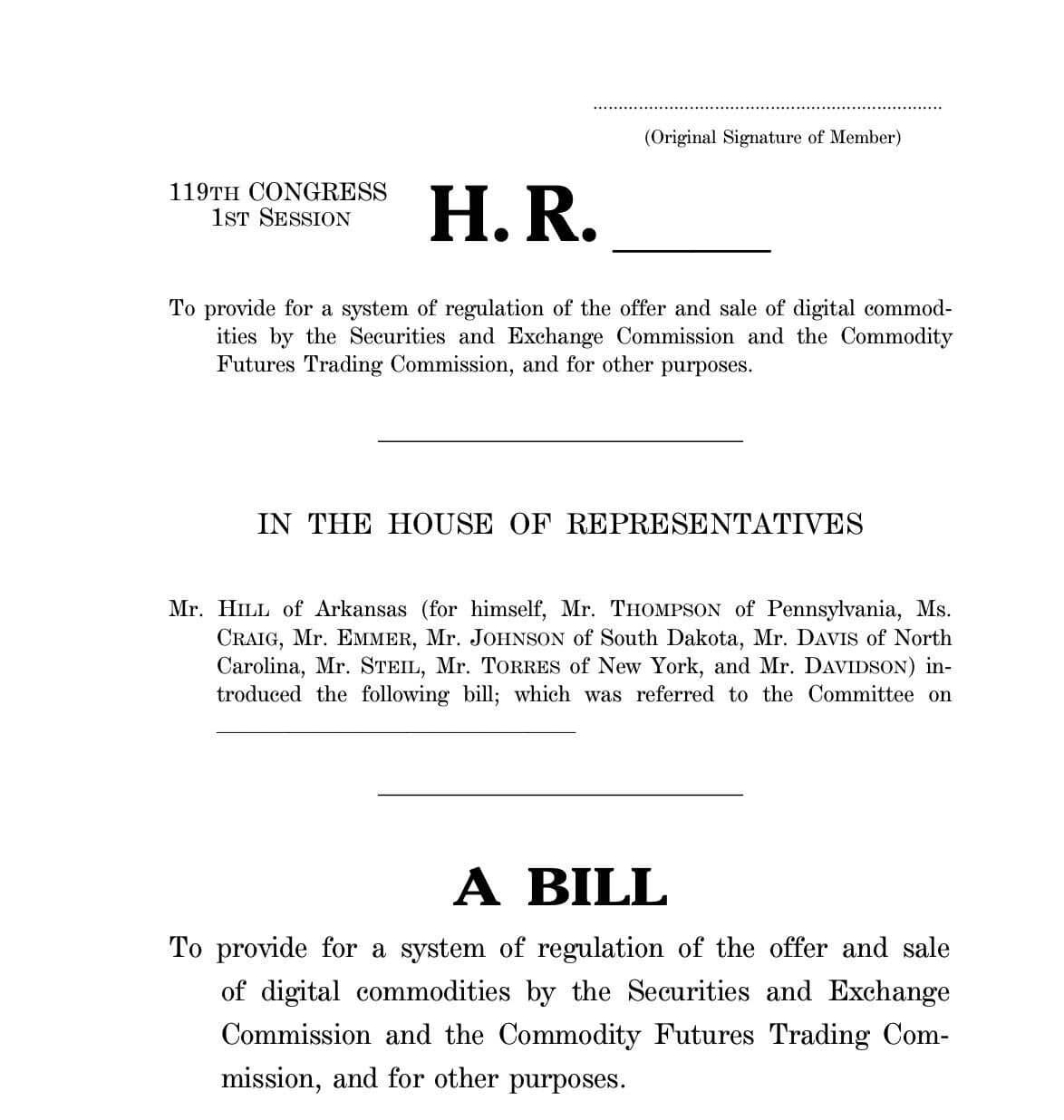

In the United States, “market structure” is no longer just a technical term used by quants and policy analysts. It is the label attached to the most ambitious legislative effort to define the legal architecture of the digital asset industry. The centerpiece is the Digital Asset Market Clarity Act—often shortened to the CLARITY Act—which aims to establish clearer rules for classifying crypto assets, overseeing exchanges, and dividing jurisdiction between the SEC and CFTC. Proponents describe it as one of the most significant attempts to build a formal market structure framework for crypto in U.S. law, arguing that without such a roadmap the country risks ceding leadership to jurisdictions that already offer comprehensive digital asset regimes, such as the European Union or certain Asian financial centers.

The Senate Banking Committee has been at the center of this effort, advancing a version of market structure legislation styled as the Digital Asset Market Clarity Act and debating extensive substitute text that touches on illicit finance, DeFi, stablecoin yield, tokenization standards, developer protections, and customer property in bankruptcy. According to reporting and committee disclosures, members have submitted over 100 amendments ahead of key markup votes, reflecting intense negotiation over issues ranging from ethics rules for officials to the treatment of decentralized protocols. This amendment flood underscores how many aspects of crypto’s market structure remain contentious, including which activities should be permissible for banks and how far regulators should go in policing non‑custodial software developers.

One of the thorniest issues involves stablecoin yield. Banking industry groups and some lawmakers worry that if regulated payment stablecoins are allowed to pay interest or yield simply for being held, they could become functional substitutes for bank deposits, drawing funds out of the traditional banking system and weakening banks’ capacity to lend. Analysis from industry‑adjacent think tanks and banking trade associations warns that large‑scale migration of deposits into interest‑bearing stablecoins could exacerbate deposit flight risk in times of stress and undermine financial stability. In response, the Senate Banking substitute bill incorporates compromise language that prohibits the payment of interest or yield “solely for holding payment stablecoins” while leaving room for activity‑based rewards or incentives tied to actual usage, such as transactions or platform participation.

This compromise is mirrored in market commentary noting that revised legislative drafts limit passive stablecoin interest but still allow rewards tied to real transactions and platform activity, with regulators given a window to develop detailed rules on stablecoin rewards and yield structures. Exchanges and issuers that previously marketed yield on stablecoin balances may need to redesign their products to comply with these constraints, shifting from deposit‑like offerings to rewards tied to spending, payments, or participation in defined programs. The distinction between “interest” and “rewards” is not merely semantic; it reflects deeper questions about whether stablecoins should be treated as narrow payments instruments or as competitors to deposit accounts.

Another focal point is the treatment of DeFi. Drafts of the Senate legislation direct the SEC and Treasury to develop specific rules clarifying how individuals or groups that control a DeFi trading protocol can comply with obligations such as disclosure, recordkeeping and securities laws. Treasury is also tasked with defining how DeFi platforms meet anti‑money‑laundering and Bank Secrecy Act requirements, recognizing that unhosted wallets and decentralized applications can otherwise be used by criminals and sanctions evaders to access the U.S. financial system. These provisions seek to close what critics view as “crypto pathways” for illicit finance while avoiding sweeping liabilities for developers of non‑custodial software.

Jurisdictional clarity between the SEC and CFTC is another central goal. The SEC’s Crypto Task Force has stressed the importance of applying federal securities laws to digital asset offerings that meet the criteria for investment contracts, while the CFTC has highlighted its role in overseeing derivatives and certain spot commodity markets. The CLARITY Act aims to codify which crypto assets fall under securities versus commodities regulation and how exchanges and intermediaries should register, a division that has so far been hammered out largely through enforcement actions and guidance rather than statute. Industry groups and companies like Coinbase have publicly urged lawmakers to provide clear SEC‑CFTC roles and protections for non‑custodial developers, warning that regulatory uncertainty is pushing jobs and capital offshore.

The politics of the bill are complex. Analysis from Galaxy Digital has identified a small group of Democratic senators as pivotal swing votes whose support could determine whether the CLARITY Act garners the 60 votes needed to overcome a filibuster. At the same time, some prominent Democrats, including Senator Elizabeth Warren and others, are seen as likely opponents, citing concerns about investor protections and systemic risk. Labor unions have also weighed in, calling on senators to reject the market structure bill out of concern that it could expose millions of workers to new risks or weaken regulatory safeguards if digital asset markets are overly liberalized. In contrast, more than 100 crypto firms, including major exchanges and venture firms, have publicly urged the Senate Banking Committee to advance the CLARITY Act, emphasizing that the absence of a U.S. framework is driving business to more welcoming jurisdictions.

Ethics provisions have emerged as another stumbling block. Earlier drafts of Senate market structure text reportedly contained language barring senior government officials, including the president, from owning or promoting digital asset businesses while in office, but this language was removed from the substitute bill to secure bipartisan support in committee. Some lawmakers have insisted that ethics safeguards are essential to maintain public trust and avoid conflicts of interest, while others argue that such provisions fall outside the Banking Committee’s jurisdiction and could trigger a presidential veto if seen as targeting specific individuals. This deadlock has led some observers to describe the current legislative moment as “now or never,” with the risk that if market structure bills do not pass before a political window closes, they could stall for an extended period.

CCMR publishes U.S. digital asset regulatory framework blueprint

SEC crypto task force issues guidance: most tokens not securities; mining, staking, airdrops excluded

Senate Banking Committee targets April markup for crypto market structure bill

Senate Banking Committee holds CLARITY Act markup hearing

100+ crypto firms including Coinbase, Ripple, a16z send joint Senate letter demanding CLARITY Act passage

TD Cowen cuts CLARITY Act passage odds to one-in-three as Democratic swing votes waver

Banks and crypto firms reach private deal on Bitcoin market structure bill; announcement imminent

Banks, Coinbase and the Battle Over Stablecoin‑Era Market Structure

The tug‑of‑war over stablecoin yield illustrates a broader contest between traditional banks and crypto‑native firms over who will occupy key positions in the future market structure. Banking groups fear that if non‑bank stablecoin issuers can offer deposit‑like products with higher yields, they will siphon off cheap funding that banks rely on to make loans to households and businesses. These concerns are amplified by the possibility that stablecoin issuers could engage in de facto maturity transformation, investing reserves in longer‑dated assets while promising immediate liquidity to token holders, without being subject to bank‑style capital and liquidity requirements. For regulators charged with safeguarding financial stability, such a scenario raises echoes of shadow banking runs.

Crypto firms, by contrast, argue that customers should be free to choose between bank accounts and digital dollar tokens and that stablecoins can coexist with, rather than replace, bank deposits if appropriately regulated. They point to benefits such as 24/7 settlement, programmable payments, and cross‑border efficiency. Some exchanges and issuers have been willing to accept constraints on explicit “interest” in exchange for preserving the ability to offer rewards tied to usage, such as cashback‑style incentives for spending or staking‑adjacent programs tied to protocol participation, provided these are clearly defined in statute. Coinbase and others have characterized current Senate texts as “generally a very good piece of legislation” that nevertheless contains problematic issues they hope to address through ongoing engagement with lawmakers.

The emerging compromise on stablecoin rewards—banning passive interest for simply holding a payment stablecoin while allowing activity‑based incentives—reflects this balancing act. It echoes earlier efforts such as the GENIUS Act, which sought to prohibit stablecoins from paying interest or yield, and attempts to close loopholes through which issuers might indirectly pay interest via affiliates or revenue‑sharing agreements. Banking advocates warn that allowing such indirect arrangements would undermine the intent of the prohibition and heighten deposit flight risk, especially in periods of financial stress when higher‑yielding stablecoin products might appear safer or more liquid than bank deposits.

Beyond stablecoins, the bills also address whether and how banks can engage with tokenization and digital asset custody. Senate drafts contemplate giving banks and credit unions explicit permission to use distributed ledger systems in authorized activities, including the tokenization of securities and other real‑world assets. This dovetails with broader policy research arguing that the regulatory framework should permit combined services for traditional financial assets, digital asset commodities, and digital asset securities, enabling integrated platforms that handle both tokenized and non‑tokenized instruments under consistent rules. Such an approach would bring aspects of crypto market structure inside the perimeter of bank regulation while also exposing banks to new forms of technological and operational risk.

Institutional Experiments: Tokenization, On‑Chain Repo and RFQ Markets

While legislation inches forward, institutional market structure experiments are already underway. One notable example is the use of permissioned blockchain networks to execute repurchase agreements, or repo, between large financial institutions. In a recent on‑chain repo transaction on the Canton Network, firms including Hifi, DRW and Marex completed a collateralized financing trade using tokenized instruments, with competitive price discovery occurring through a familiar RFQ platform, Tradeweb, and settlement taking place atomically on‑chain. Confidential payment flows and regulatory‑grade controls were maintained within the same market structure institutions already use, showing that tokenization can modernize plumbing without discarding trusted workflows.

This type of experiment demonstrates how blockchain‑based settlement can be plugged into existing market structure rather than attempting to replace it wholesale. Traders interact with RFQ and execution venues they already know; the main difference is that the lifecycle of the trade—confirmation, collateral movement, and settlement—is compressed and automated through smart contracts. For regulators, this raises questions about whether tokenized versions of traditional securities should be regulated exactly like their underlying instruments, as some policy proposals suggest, or whether additional rules are needed to address unique operational and cyber risks in distributed ledger environments.

At the same time, regulators are exploring whether tokenized stocks or other securities could eventually trade on DeFi platforms under strict conditions. Proposals floated at the SEC and in policy circles contemplate allowing regulated broker‑dealers or alternative trading systems to operate on‑chain venues where tokenized equities or funds trade within a framework that preserves investor protections and surveillance. This would represent a significant shift in market structure, blurring the line between traditional securities markets and crypto protocols and raising fresh questions about how to handle issues such as front‑running, best execution and market manipulation in automated environments.

These institutional pilots sit alongside ecosystem‑driven initiatives on public chains. Efforts to cultivate “frontier traders” on networks like Solana, for example, combine incentives, dedicated infrastructure and governance participation to shape the emerging market structure of high‑performance DeFi venues. By assembling communities of sophisticated firms and individuals who actively trade and provide liquidity, such programs seek to deepen order books, stress‑test new instruments, and give key participants a voice in designing protocol rules, fee schedules and risk controls. In effect, they are market structure laboratories operating in the open, with token economics and governance mechanisms as core design tools.

Without enacted legislation, the SEC and CFTC operate under overlapping and sometimes contradictory authority over digital assets, creating enforcement uncertainty for every exchange, protocol, and token issuer.

NYDIG warned the CLARITY Act could stall entirely if it misses the pre-midterm window, and TD Cowen placed passage odds at one-in-three, making the bill's fate a near-term binary risk for the entire industry.

Derivatives now dominate crypto trading volume, concentrating systemic risk in leveraged venues that existing spot-focused market structure frameworks were not designed to govern.

Bitcoin basis-trade unwinds in derivatives markets have cascaded into spot price dislocations, exposing fragility in the connection between futures and underlying asset liquidity.

- CentralizationMedium

The VC model shift toward backing founders and distribution channels rather than products concentrates early-stage crypto capital in fewer hands and fewer networks, increasing systemic correlation.

- Smart contractLow

For market structure specifically, smart contract risk is secondary; the dominant risk is regulatory ambiguity that delays institutional adoption rather than on-chain protocol failure.

AI, Real‑World Finance and the Next Market Structure Layer

Crypto market structure does not exist in isolation from broader shifts in finance and technology. Industry observers increasingly point to three interlinked forces reshaping the “financial stack”: market structure reform, digital asset regulation, and AI‑driven capital allocation. As governments and regulators refine rules for digital assets, and as institutions integrate blockchain‑based settlement and tokenization, artificial intelligence is simultaneously changing how capital is allocated, how liquidity is provided, and how risk is managed across both traditional and crypto markets. These dynamics intersect in areas such as algorithmic market‑making, where AI‑enhanced models optimize quoting strategies across centralized and decentralized venues, or portfolio construction tools that allocate between tokenized and non‑tokenized assets.

The RealFi narrative—tying real‑world assets and cash flows to on‑chain representations—adds another dimension. As tokenized treasuries, credit exposures, and structured products proliferate, the market structure question becomes not just where and how these instruments trade, but how they connect to existing regulatory frameworks and systemic risk monitoring. If large proportions of short‑term funding markets migrate to tokenized repos or on‑chain money market funds, central banks and supervisors will need visibility into these flows comparable to what they have in current wholesale funding markets. Frameworks such as those outlined in digital asset regulatory proposals emphasize preserving the role of existing prudential regulators while enabling innovation in combined digital and traditional platforms.

In this landscape, the CLARITY Act and related bills can be seen as one layer in a broader market structure transformation, rather than a standalone crypto project. They aim to set baseline rules for what counts as a digital asset security versus a commodity, who supervises exchanges and intermediaries, and how consumer protections and anti‑money‑laundering obligations apply in both CeFi and DeFi. On top of this legal infrastructure, technology choices—permissioned versus public chains, AMMs versus order books, centralized versus distributed custody—will determine where liquidity concentrates. Finally, AI and advanced analytics will influence how efficiently market participants can navigate this structure, arbitrage inefficiencies, and allocate capital.

Why Market Structure Matters for Traders, Builders and Policymakers

For active traders, market structure shapes everything from slippage and fees to the viability of complex strategies. Understanding where liquidity resides—on a handful of centralized exchanges, a web of DeFi pools, or institutional RFQ venues—is crucial when sizing positions or running basis trades and arbitrage. Regulatory changes can directly alter these conditions; restrictions on stablecoin yield might reduce leverage in certain carry trades, while clearer SEC‑CFTC boundaries could make it easier for U.S. institutions to access regulated derivatives markets. Shifts in futures market structures, such as those associated with the unwind of bitcoin basis trades, can signal changing regime dynamics that sophisticated traders must incorporate into their risk management.

For protocol builders and crypto entrepreneurs, market structure is both a design space and a constraint. Decisions about whether to use AMMs, order books or hybrid models; how to structure fees and incentives; and whether to rely on permissionless or permissioned access all influence who can participate and how resilient the protocol will be in stress scenarios. At the same time, legislative and regulatory frameworks define what is legally permissible. Proposals to hold non‑controlling software developers harmless from certain forms of liability, for example, are welcomed by open‑source communities, while rules assigning compliance obligations to “controlling persons” of DeFi protocols could shape governance structures and upgrade mechanisms.

Policymakers, for their part, use market structure as a tool to balance competing objectives: investor protection, financial stability, innovation, and international competitiveness. The White House’s crypto advisers have stressed the need for a coherent market structure framework to avoid falling behind global competitors, while some lawmakers and unions emphasize the risks of moving too fast or creating loopholes that benefit large crypto firms at the expense of consumers and workers. Legislators like Representative Tom Emmer have framed the CLARITY Act as the product of multiple iterations of work in the House, underscoring that market structure debates have been brewing for years rather than emerging overnight. Political figures such as Donald Trump have pledged to codify “future‑proof” digital asset market structures, signaling that crypto market design is now part of broader electoral narratives.

The interplay between these constituencies—banks, crypto firms, labor groups, regulators, and politicians—will determine how the next generation of financial plumbing is built. If bills like the CLARITY Act successfully reconcile concerns about stablecoin yield, DeFi compliance, and ethics provisions, they could offer the industry a long‑awaited roadmap and unlock greater institutional participation. If they stall, U.S. crypto market structure will continue to be shaped piecemeal by enforcement, agency guidance and offshore innovation, increasing fragmentation and legal uncertainty.

Outlook

The evolution of crypto market structure is entering a critical phase, with legislative “now or never” moments in Washington intersecting with rapid experimentation in tokenization, DeFi design and AI‑driven trading. In the near term, the fate of U.S. market structure bills such as the CLARITY Act and the Senate’s Digital Asset Market Clarity Act will hinge on political compromises over stablecoin yield, DeFi obligations and ethics safeguards, as well as on whether a small group of swing senators can be persuaded that the benefits of clarity outweigh the risks of codifying crypto too quickly. Even if timelines slip, as some analysts caution they may, the direction of travel is clear: regulators and lawmakers are moving from conceptual debates to concrete drafting choices that will matter operationally for exchanges, issuers and service providers.

Over a longer horizon, the boundary between “crypto” and “traditional” market structure is likely to blur. As tokenization of securities, on‑chain repo, and regulated DeFi platforms mature, the underlying question shifts from whether to use blockchain rails to how to ensure that those rails support fair, transparent and resilient markets. Jurisdictions that manage to align robust market structure rules with technological openness will be well‑positioned to attract talent, capital and innovation, while those that rely solely on enforcement or cling to outdated frameworks risk seeing liquidity migrate elsewhere. For traders, builders and policymakers alike, staying fluent in the evolving language of market structure is therefore no longer optional; it is central to understanding how digital assets will integrate into, and reshape, the global financial system.

Latest Market Structure news

Sources

- https://bpi.com/4-things-to-know-about-crypto-market-structure-legislation/

- https://corporatefinanceinstitute.com/resources/economics/market-structure/

- https://www.dwt.com/blogs/financial-services-law-advisor/2026/05/senate-banking-crypto-market-structure-bill

- https://www.youtube.com/watch?v=WBUKHSP3TNs

- https://www.youtube.com/watch?v=XbqhCO7qbu4

- https://www.sec.gov/securities-topics/crypto-task-force

- https://www.cftc.gov/LearnandProtect/digitalassets/index.htm

- https://capmktsreg.org/wp-content/uploads/2025/05/CCMR-Designing-a-U.S.-Digital-Asset-Regulatory-Framework-05.14.25-Final.pdf

- https://coinbureau.com/education/what-are-crypto-market-structures

- https://blockchair.com/pl/news/clarity-act-banking-groups-continue-stablecoin-yield-push-as-senate-focus-shifts-to-ethics-defi--24cfe6630210cd8c

- https://x.com/pharos_network/status/2064170915047563668

- https://x.com/SolanaFndn/status/2065154420791496728

- https://cryptoslate.substack.com/p/bitcoin-basis-trade-unwind-reflected

- https://financefeeds.com/7-democrats-could-decide-fate-of-us-crypto-market/

- https://www.binance.com/en/square/post/05-12-2026-us-labor-unions-warn-against-crypto-market-structure-bill-322332413692082

- https://www.facebook.com/CoinMarketCap/posts/latest-over-100-crypto-firms-including-coinbase-ripple-and-a16z-are-urging-the-s/1379963440827712/

- https://x.com/TheBlockCo/status/2059820404374405182

- https://x.com/CantonNetwork/status/2067256702169502161

- https://www.mexc.com/news/1071701

- https://x.com/CoinDesk/status/2044493088119296268

Community notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…