In-depth explainer on how crypto legislation is reshaping digital assets, covering GENIUS and CLARITY Acts, strategic Bitcoin reserve bills, mining policy, SEC–CFTC roles, DeFi rules, and global trends for traders, builders, and policymakers.

+16 sources across the wider coverage universe

Cassidy and Lummis drop Mined in America Act to wean U.S. miners off Chinese hardware and cement Trump's strategic Bitcoin reserve2026-03

Cassidy and Lummis drop Mined in America Act to wean U.S. miners off Chinese hardware and cement Trump's strategic Bitcoin reserve2026-03 Lummis touts bipartisan CLARITY Act revisions as strongest-ever legal shield for DeFi developers2026-03

Lummis touts bipartisan CLARITY Act revisions as strongest-ever legal shield for DeFi developers2026-03 Indiana State Rep. Kyle Pierce introduced a broad crypto bill arguing U.S. legislation shouldn’t favor Bitcoin alone, aiming to support the wider digital asset market, protect miners, and expand crypto exposure in public retirement programs.2025-12

Indiana State Rep. Kyle Pierce introduced a broad crypto bill arguing U.S. legislation shouldn’t favor Bitcoin alone, aiming to support the wider digital asset market, protect miners, and expand crypto exposure in public retirement programs.2025-12 The Bank of Russia proposed a new crypto framework expanding retail and professional investor access under tiered limits, while keeping crypto barred from domestic payments and routed through licensed intermediaries, with full legislation targeted for 2026.2025-12

The Bank of Russia proposed a new crypto framework expanding retail and professional investor access under tiered limits, while keeping crypto barred from domestic payments and routed through licensed intermediaries, with full legislation targeted for 2026.2025-12 Australian regulators, led by ASIC, are preparing legislation that will require cryptocurrency exchanges to obtain financial services licenses, expanding beyond current digital currency regulations, as ASIC Commissioner Alan Kirkland emphasized at the AFR Crypto and Digital Assets summit.2024-09

Australian regulators, led by ASIC, are preparing legislation that will require cryptocurrency exchanges to obtain financial services licenses, expanding beyond current digital currency regulations, as ASIC Commissioner Alan Kirkland emphasized at the AFR Crypto and Digital Assets summit.2024-09 US lawmakers propose legislation to outlaw SEC's controversial rule crippling the viability of crypto custody businesses.2023-10

US lawmakers propose legislation to outlaw SEC's controversial rule crippling the viability of crypto custody businesses.2023-10

Legislation in Crypto: How Lawmakers Are Writing the Rules of Digital Assets

Legislation in crypto refers to formal laws passed by elected bodies like Congress or national parliaments that define how digital assets such as Bitcoin, stablecoins, and decentralized finance (DeFi) are treated in areas ranging from market structure and custody to taxation and national security. Unlike agency guidance or court rulings, these laws can reshape the entire regulatory landscape at once, which is why the current wave of U.S. bills—from the stablecoin‑focused GENIUS Act to the market‑structure‑oriented CLARITY Act and strategic Bitcoin reserve proposals—is widely seen as a once‑in‑a‑decade inflection point for the industry.

What Crypto Legislation Is And Why It Matters

At its core, legislation is the process by which democratically elected bodies convert political priorities into binding rules, typically in the form of statutes that sit above agency regulations and enforcement actions. In crypto, this distinction matters because the industry’s first decade was governed mainly through existing securities, commodities, and banking laws interpreted case‑by‑case by regulators and courts, rather than through laws written specifically with digital assets in mind. That approach led to years of uncertainty over whether a given token was a security, a commodity, or something else entirely, and over which agency—the Securities and Exchange Commission (SEC) or the Commodity Futures Trading Commission (CFTC)—had authority. Statutory crypto legislation aims to replace that patchwork with purpose‑built frameworks that define asset taxonomies, assign responsibilities to agencies, and create tailored rules for exchanges, stablecoin issuers, DeFi developers, and custodians.

The stakes are unusually high because these laws do not just clarify compliance obligations; they influence where developers build, how banks and crypto platforms compete, and how quickly institutional capital enters the space. When JPMorgan analysts note that approval of sweeping U.S. crypto market‑structure legislation could materially lift markets in the second half of the year, they are pointing to the way legal clarity affects risk premia, capital allocation, and product development across the financial system. For retail users, legislation can determine whether they can legally hold a dollar‑backed stablecoin with explicit federal protections, whether their crypto exchange assets are segregated in bankruptcy, and whether they retain the right to self‑custody or face a central bank digital currency (CBDC) they fear could be used for surveillance. Put simply, legislation is where abstract debates about “crypto regulation” are translated into concrete rights and obligations for every actor in the ecosystem.

Crypto legislation also sits at the intersection of technology, politics, and geopolitics. The Trump administration’s stated ambition to make the United States the “crypto capital of the world,” combined with its push for a Strategic Bitcoin Reserve and a federal digital asset stockpile, has turned Bitcoin and related infrastructure into objects of U.S. industrial and national security policy, not merely financial regulation. At the same time, central banks and finance ministries worldwide—ranging from Hong Kong and Canada on stablecoins to Brazil’s central bank on broader crypto asset classification—have begun crafting their own statutory frameworks, creating a competitive landscape for regulatory regimes. For a crypto‑savvy audience, understanding legislation therefore means understanding not only the legal text but the political coalitions, economic interests, and international dynamics that drive it.

Cassidy and Lummis drop Mined in America Act to wean U.S. miners off Chinese hardware and cement Trump's strategic Bitcoin reserve

Bitmain already controls ~82% of ASIC production and announced a US assembly line for 2026 — tariff pressure is doing the heavy lifting here before this bill even hits committee. The gap nobody's addressing: "domestic manufacturing" of mining hardware still routes through TSMC for chip fab, so you can assemble Antminers in Texas all day but the silicon bottleneck sits in Hsinchu, not Shenzhen. 37% of global hashrate running on hardware designed by three Chinese companies is a strange foundation for a "strategic reserve" — voluntary certification with no phase-out timeline is a press release, not a supply chain strategy.

Readers bypass the abstract 'regulatory clarity' framing and click hardest on legislation that settles permission-to-exist for specific business models — exchange licenses, custody viability, stablecoin issuers — revealing they are tracking which firms survive the regulatory cut, not the philosophy behind the rules.↗

How Crypto Laws Are Made In Washington

In the United States, most major crypto laws start in Congress, where members of the House of Representatives and Senate introduce bills that are then referred to relevant committees such as House Financial Services, House Agriculture, Senate Banking, and Senate Agriculture. These committees hold hearings to gather testimony from industry leaders, academics, regulators, and affected stakeholders, and they often commission drafts that reflect months of negotiation among staff, lobbyists, and the executive branch. For digital assets, the committee structure is particularly important because jurisdiction is split: securities issues fall to financial services and banking committees, while commodities and derivatives, including aspects of crypto spot markets, are shared with agriculture committees that traditionally oversee futures markets.

Once a bill is introduced, the committee may hold a markup session where members debate, amend, and ultimately vote on whether to advance the legislation to the full chamber. The Digital Asset Market Clarity Act—commonly called the CLARITY Act—offers a concrete example: after passing the House with strong bipartisan support in July 2025, it moved to the Senate Banking Committee, which scheduled a markup to discuss and amend the bill before sending it to the Senate floor. Over time, the Senate Banking Committee developed its own substitute text, incorporating elements from prior amendments and related bills like the Senate Agriculture Committee’s Digital Commodity Intermediaries Act, to create a comprehensive market‑structure framework addressing illicit finance, DeFi, tokenization, stablecoin yield, customer property protections, and more. That substitute then moved toward reconciliation—first between Senate committees, and ultimately between the Senate and House versions—before any final vote in both chambers.

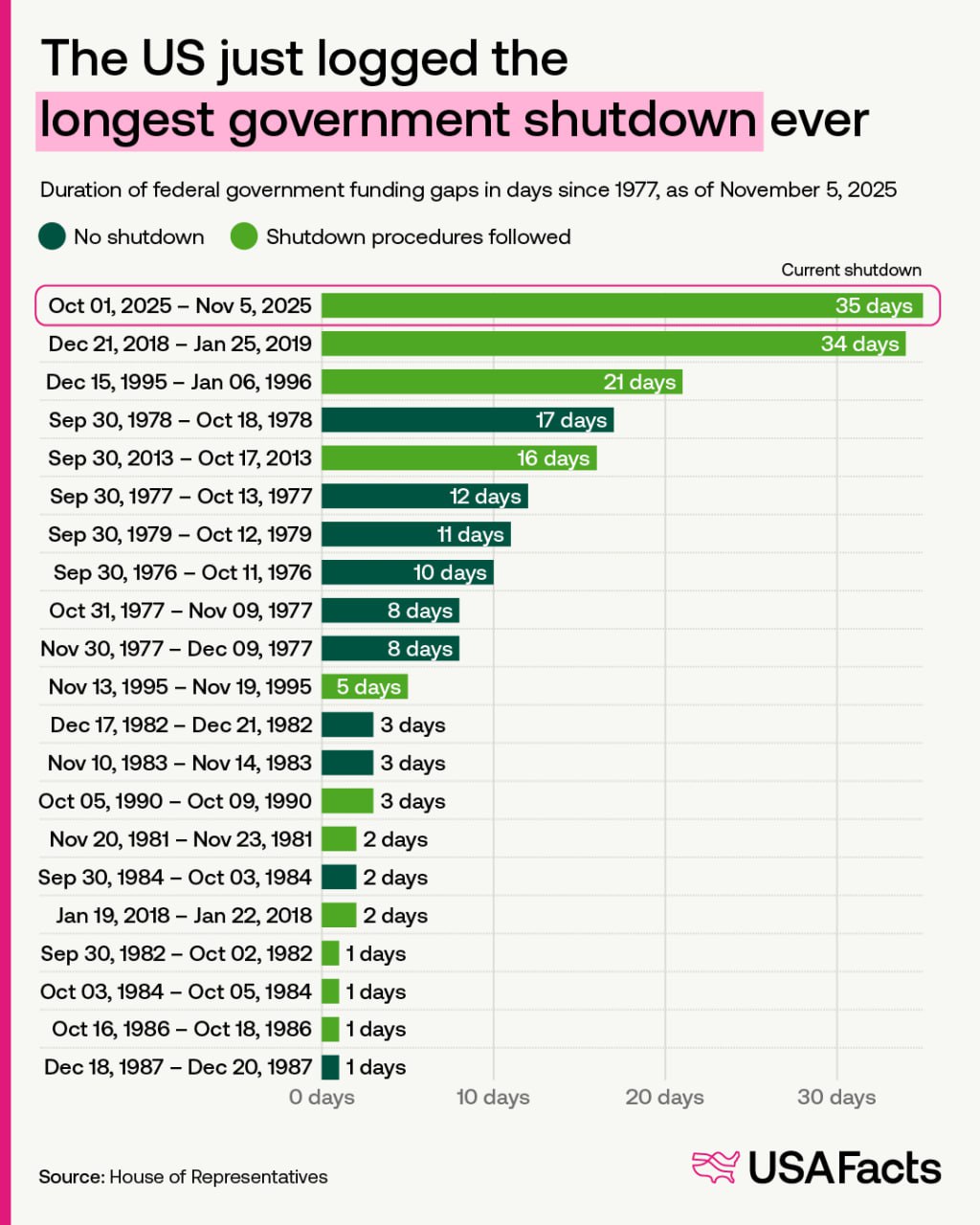

Political timing and the broader state of Congress shape this process in ways that are not obvious from the text of bills alone. Government shutdowns, midterm elections, and leadership fights can freeze committee calendars and delay even widely supported legislation, as seen when a record‑length shutdown raised concerns that it could derail crypto market‑structure bills despite strong momentum in prior months. Representative Bryan Steil, for example, has argued in interviews that despite shutdown‑related disruptions, there remained a realistic opportunity to get key clarity legislation “across the line” by the end of the year, reflecting the tension between political gridlock and bipartisan interest in resolving digital asset uncertainty. At the same time, Senator Cynthia Lummis has warned that if this Congress fails to pass comprehensive digital asset legislation, the next significant window for action may not open until around 2030, underscoring how election cycles and shifting congressional priorities can stretch out policy uncertainty for years.

The executive branch plays a parallel, sometimes complementary role. Presidents can signal priorities through executive orders, such as the Trump administration’s order establishing a Strategic Bitcoin Reserve and a U.S. Digital Asset Stockpile, but enduring frameworks typically require Congress to codify these initiatives in law. Agencies like the Treasury Department, Federal Reserve, SEC, CFTC, and banking regulators then implement statutes through rulemaking, guidance, and enforcement, filling in technical details and ensuring day‑to‑day compliance. For example, after Congress passed the GENIUS Act, the Treasury launched an advance notice of proposed rulemaking to gather input on how to operationalize its stablecoin mandates, illustrating how legislation sets broad parameters while agencies translate those mandates into granular requirements for issuers and intermediaries. Understanding crypto legislation in the U.S. therefore requires tracking both the visible theater of congressional votes and the quieter but equally critical work of regulatory implementation.

- 01Stablecoin bill showdown↗

The GENIUS Act vs. STABLE Act rivalry forced readers to pick sides on whether stablecoin legislation would fuel mainstream adoption or entrench incumbents, with real money and DeFi survival in the balance.

- 02State Bitcoin reserve race↗

Thirty-plus states introducing reserve bills — with Minnesota naming BTC outright and Alabama writing criteria only Bitcoin fits — signaled a decentralized legislative push that felt like a real political movement, not a lobby wish list.

- 03Exchange and custody licensing↗

ASIC's licensing push and the congressional bid to kill the SEC's crypto custody rule directly threatened whether existing businesses could legally operate, making these the highest-stakes stories for practitioners.

- 04DeFi developer legal shield↗

The CLARITY Act's promise to give DeFi builders an explicit legal safe harbor attracted readers tracking whether developers could build without retroactive liability exposure.

- 05Political gatekeeping dynamics↗

The Democratic walkout, Sherrod Brown's Senate loss, and partisan stalemates showed readers that crypto legislation lives or dies on individual political actors, not just policy merit.

- 06International regulatory divergence↗

MiCA rollouts, Sweden's civil-asset-forfeiture expansion, and Russia's tiered framework illustrated that global crypto rules are fracturing by jurisdiction, creating compliance arbitrage readers needed to understand.

The Major U.S. Crypto Bills On The Table

Stablecoins and the GENIUS Act

The Guiding and Establishing National Innovation for U.S. Stablecoins Act, known as the GENIUS Act, is the United States’ first comprehensive federal framework for payment stablecoins and has become a cornerstone of global stablecoin policy debates. Signed into law by President Donald Trump, it creates a federal regulatory system for stablecoin issuers, requiring that payment stablecoins be backed 100 percent by high‑quality reserves such as U.S. dollars or short‑term Treasury securities, with monthly public disclosures of reserve composition. Those requirements are designed to address the core risks exposed by earlier stablecoin collapses and de‑peggings: opaque reserves, run‑like redemption dynamics, and contagion into broader markets. They also ensure that stablecoins more closely resemble narrow banks or money‑market‑like instruments, rather than fractional‑reserve deposit substitutes, which has implications for competition with traditional banks and money market funds.

The GENIUS Act also integrates stablecoins into the federal supervisory perimeter. It sets up licensing and oversight mechanisms that allow qualified issuers to operate under clear federal standards, potentially with pathways for banks and non‑banks alike, rather than leaving stablecoins to a patchwork of state money transmitter laws. This statutory clarity allows the Treasury and other agencies to design detailed rules on issues like reserve custody, redemption rights, risk management, and disclosure formats, which they began pursuing via the ANPRM process following the Act’s passage. By mandating transparency and strong reserves, the law is intended to build trust in dollar‑denominated stablecoins as reliable payment instruments and to foster innovation in programmable money, cross‑border payments, and tokenized financial products within a regulated environment.

Politically, the GENIUS Act reflects the Trump administration’s broader digital asset strategy. The White House has framed the law as part of a plan to “make America the crypto capital of the world,” positioning U.S.‑regulated stablecoins as pillars of dollar strength in a digitizing financial system. The Act sits alongside the administration’s creation of a Strategic Bitcoin Reserve and Digital Asset Stockpile, which aim to consolidate federal digital asset holdings under Treasury and establish a strategic foothold in crypto markets. These moves have drawn both support and criticism: supporters argue they enhance financial innovation and national security, while skeptics worry about implicit backstops for private stablecoin issuers and the potential for regulatory arbitrage with the banking system. Nonetheless, GENIUS has become a reference point internationally, with jurisdictions like Canada designing draft stablecoin laws that mirror its 1:1 reserve backing and qualified custody requirements, and with Hong Kong developing its own statutory stablecoin regime.

Market Structure and the Digital Asset Market Clarity Act

The Digital Asset Market Clarity Act—often called the CLARITY Act—is widely regarded as the most consequential piece of crypto market‑structure legislation Congress has seriously considered. Its central objective is to end the long‑running turf battle between the SEC and CFTC by creating a taxonomy that splits digital assets into clear buckets, with digital commodities (such as tokens on sufficiently decentralized networks) falling under the CFTC and digital asset securities remaining under the SEC. The bill codifies criteria for when a token can transition from being treated as a security—typically in its early, fund‑raising phase—to being treated as a commodity once the network is sufficiently decentralized, often described as a “mature blockchain” test. Proposed thresholds include measures of decentralization, such as limits on any single entity’s control of token supply and open access to network functionality, providing long‑sought clarity for projects like Solana, XRP, or Cardano that have faced prolonged regulatory overhangs.

In market‑structure terms, the CLARITY Act seeks to define registration, disclosure, and operational expectations for exchanges, brokers, custodians, and other intermediaries dealing in digital assets. It includes safe harbors and legal shields for DeFi developers and validators, aiming to protect those who build and maintain decentralized protocols from being treated as traditional financial intermediaries so long as they do not exercise centralized control over user funds or order flow. The bill also contains anti‑CBDC provisions that restrict the Federal Reserve from issuing a retail central bank digital currency directly to individuals, reflecting civil‑liberties concerns about financial surveillance and government access to transaction‑level data.

After passing the House in July 2025, the CLARITY Act moved to the Senate, where its fate hinges on reconciliation with the Senate Banking Committee’s own Digital Asset Market Clarity Act text and with the Senate Agriculture Committee’s digital commodity intermediaries bill. In May 2026, the Senate Banking Committee advanced a substitute version of the Digital Asset Market Clarity Act, incorporating a broad framework that touches on illicit finance, DeFi regulation, limitations on stablecoin yield, tokenization standards, developer protections, and customer‑property rules in bankruptcy. That markup was historic: it marked the first time the Senate Banking Committee advanced a major crypto market‑structure bill out of committee, in a bipartisan vote that many analysts interpreted as a turning point in the legislative process. Yet key differences remain between the House and Senate versions, particularly regarding DeFi treatment, stablecoin yield, taxonomy details, and the inclusion of ethics provisions for policymakers, which must be resolved before a unified bill can reach the President’s desk.

Strategic Bitcoin Reserve and Mining‑Focused Bills

One of the more distinctive strands of recent crypto legislation is the move to treat Bitcoin and certain digital assets as strategic reserves, analogous to gold or petroleum stockpiles, and to shape mining infrastructure through statute. In March 2025, President Trump signed an executive order establishing a Strategic Bitcoin Reserve and a U.S. Digital Asset Stockpile, signaling that the federal government saw value in holding Bitcoin and other digital assets directly. Building on that groundwork, Representative Nick Begich introduced the American Reserve Modernization Act of 2026 (ARMA), a bipartisan bill to establish a secure Strategic Bitcoin Reserve within the Treasury and a separate Digital Asset Stockpile for non‑Bitcoin digital assets held by the federal government.

ARMA would consolidate custody and management of digital assets held across federal agencies under Treasury, with robust transparency measures including quarterly public “proof of reserve” reports, independent third‑party audits, and congressional oversight. The bill requires that Bitcoin in the Strategic Reserve be held for at least twenty years, underscoring its strategic rather than speculative character, and it directs a study of budget‑neutral acquisition strategies to expand the reserve without raising taxes or increasing the national debt. Importantly, ARMA also affirms that the federal government may not impair individuals’ lawful right to own, transfer, or self‑custody digital assets, thereby codifying a protection for digital property rights that aligns with broader industry advocacy around self‑custody.

In parallel, Senators Bill Cassidy and Cynthia Lummis introduced the Mined in America Act, which seeks to bolster domestic digital asset mining and codify the Strategic Bitcoin Reserve within Treasury. The bill would create a voluntary “Mined in America” certification program for mining facilities and pools, phase out the use of hardware linked to foreign adversaries, and integrate certified projects into existing federal energy and rural development programs rather than creating new spending authorities. It also directs standards bodies like the National Institute of Standards and Technology to support secure, energy‑efficient U.S. manufacturing of mining hardware, explicitly tying crypto mining to industrial policy and supply‑chain security. Together, ARMA and the Mined in America Act reflect a legislative vision in which Bitcoin is both a strategic asset and an industrial sector, aligned with the Trump administration’s pledge to cement U.S. leadership in digital assets.

Anti‑CBDC Legislation

A distinct track of crypto‑related legislation focuses less on enabling private digital assets and more on constraining public digital money in the form of a retail CBDC. The Anti‑CBDC Surveillance State Act, which House leaders scheduled alongside the CLARITY and GENIUS Acts during a high‑profile “Crypto Week” in Washington, aims to block the issuance of a retail CBDC by the Federal Reserve. Supporters argue that a direct‑to‑consumer CBDC could give the federal government unprecedented visibility into individual transactions and even the ability to program or restrict spending, posing risks to privacy, financial freedom, and the traditional banking system. Critics counter that carefully designed CBDCs could improve payment efficiency and financial inclusion, though such arguments currently have less legislative traction in the U.S. compared with Europe or China.

The CLARITY Act amplifies this anti‑CBDC stance through provisions that prevent the Fed from offering a digital dollar directly to individuals, steering innovation toward private stablecoins regulated under frameworks like the GENIUS Act. That statutory alignment between market‑structure and stablecoin legislation reflects a broader ideological coalition that favors privately issued, dollar‑backed tokens over public digital money, as long as those tokens operate under strict reserve and disclosure requirements. The debate is not purely technical: it is also a proxy for disagreements about the role of the state in digital finance, the balance between surveillance and anonymity, and the future of commercial banking in a tokenized economy. For crypto users, these anti‑CBDC laws are seen by many as a critical defense of the right to transact outside direct central bank control, even as skeptics warn that they could limit policy options for future crises.

Comparative Snapshot of Key U.S. Crypto Bills

To situate the main U.S. crypto legislative efforts, it is useful to juxtapose their core focus, status, and defining features in a simplified overview.

| Bill / Act | Primary Focus | Status (mid‑2026) | Defining Features |

|---|---|---|---|

| GENIUS Act | Payment stablecoins | Enacted; implementation under Treasury rulemaking | 100% liquid reserves, monthly disclosures, federal stablecoin regime |

| Digital Asset Market Clarity Act | Market structure, asset taxonomy | Passed House; Senate Banking advanced substitute | SEC–CFTC split, “mature blockchain” test, DeFi safe harbors, anti‑CBDC elements |

| American Reserve Modernization Act | Strategic Bitcoin Reserve, custody | Introduced; in House Financial Services Committee | Strategic Bitcoin Reserve, Digital Asset Stockpile, self‑custody rights |

| Mined in America Act | Mining, infrastructure, strategic BTC | Introduced in Senate | “Mined in America” certification, hardware de‑risking, codifies BTC reserve |

| Anti‑CBDC Surveillance State Act | Restricting a retail CBDC | Advanced in House; bundled in “Crypto Week” agenda | Prohibits Fed retail CBDC, reinforces private‑token model |

This table compresses a complex legislative landscape, but it highlights how U.S. crypto laws increasingly intersect: stablecoin rules, market structure, strategic reserves, mining policy, and CBDC constraints are all being debated as parts of a coherent, if contested, national digital asset strategy.

Lummis touts bipartisan CLARITY Act revisions as strongest-ever legal shield for DeFi developers

Section 604 carves out non-custodial devs from BSA/KYC obligations, but Storm's conviction already proved prosecutors will stretch "control" to cover governance multisigs and admin keys — the exact ambiguity Chervinsky flagged as non-negotiable. Until the April markup defines a bright-line custody test, every protocol running upgradeable proxies or timelocked admin functions sits one aggressive SDNY filing away from Tornado Cash treatment. Lummis-Wyden bipartisanship gives this real legs, but the stablecoin yield debate is eating all the oxygen while the definitional question that actually matters to builders stays unresolved in draft language nobody's seen yet.

- 2024-11regulatory

Sherrod Brown unseated; key Senate crypto blocker removed

- 2024-11regulatory

Sweden crypto civil-asset confiscation law takes effect

Trump executive order establishes U.S. strategic Bitcoin reserve

GENIUS Act signed into law by President Trump

Stand With Crypto launches 2026 midterm candidate vetting program

Senate banking committee circulates crypto market structure bill draft

Core Policy Themes Running Through Crypto Legislation

Who Regulates What: SEC, CFTC, And The “Mature Blockchain” Test

One of the foundational questions in crypto legislation is jurisdictional: which agency regulates what, and under what criteria. For years, the SEC asserted expansive authority over many tokens by treating them as investment contracts under the Howey test, while the CFTC claimed jurisdiction over Bitcoin, Ether, and certain other assets as commodities, particularly in the derivatives markets. This overlapping and sometimes conflicting oversight led to uncertainty for issuers, exchanges, and DeFi projects, many of which faced enforcement actions without clear ex ante rules. The CLARITY Act attempts to resolve this by explicitly dividing responsibility between the SEC and CFTC, while codifying a process by which digital assets can transition from securities to commodities as networks decentralize.

Under the CLARITY framework, assets that function like traditional securities—such as tokenized equity in a start‑up or tokens sold primarily as speculative investment contracts with managerial efforts driving returns—would remain under SEC jurisdiction, with associated registration and disclosure obligations. By contrast, tokens on sufficiently decentralized networks, where no single entity controls the supply or core functionality and where tokens are primarily used for consumption or network access rather than investment, would be classified as digital commodities under the CFTC. The bill’s “mature blockchain” test operationalizes this shift, relying on criteria such as the dispersion of token ownership, the absence of unilateral upgrade authority, and open‑access usage to determine when an asset is no longer a security.

The Senate Banking Committee’s substitute bill builds on this taxonomy, reflecting negotiated compromises among lawmakers concerned with both innovation and investor protection. It incorporates digital asset definitions, SEC and CFTC roles, and a framework for intermediaries that is broadly consistent with the House’s CLARITY approach, while adding detailed provisions on DeFi, tokenization, and stablecoin yield. In doing so, it aims to give market participants the predictability they have long requested: projects can design token economics with a clearer view of their eventual regulatory classification, exchanges and custodians can structure listings and risk controls accordingly, and courts can apply statutory standards rather than stretching legacy laws to fit novel technologies.

Stablecoin Yield, Payments, And Bank Competition

Another recurring theme across crypto legislation is the treatment of stablecoins, not just as instruments requiring safe reserves, but as potential competitors to bank deposits and traditional payment rails. The GENIUS Act addresses the safety and transparency of payment stablecoins by mandating full reserve backing and frequent disclosure, but it largely leaves questions of yield and interest to subsequent rulemaking and related bills. The Senate Banking Committee’s Digital Asset Market Clarity substitute takes a more explicit stance: it prohibits the payment of interest or yield “solely for holding payment stablecoins,” while leaving room for certain activity‑based rewards or incentives.

The logic behind this prohibition is to prevent stablecoins from functioning as unregulated high‑yield savings vehicles that siphon deposits away from banks without comparable prudential oversight or backstops. Banking groups have expressed concerns that interest‑bearing stablecoins could erode their funding base, undercutting the traditional model whereby insured deposits support lending and other credit intermediation. Crypto advocates counter that well‑regulated stablecoins can coexist with banks, enhancing payment efficiency and financial inclusion, and that activity‑based rewards—such as cashback on transactions or loyalty programs—offer a workable compromise between innovation and financial stability.

This battle over yield encapsulates a broader rivalry between banks and crypto platforms. Bloomberg has described how the advancement of landmark crypto legislation marks a shift from arguing whether crypto belongs in regulated finance at all, to fighting over the terms on which it competes with banks for deposits, payments, and customer relationships. JPMorgan analysts note that if market‑structure legislation passes, the competitive dynamic will sharpen as well‑regulated exchanges and stablecoin issuers vie with banks to serve both retail and institutional clients, potentially lifting the crypto market but also intensifying regulatory scrutiny. In this light, the GENIUS Act’s strict reserve and transparency requirements, combined with the Senate bill’s yield limitations, can be seen both as enablers of stablecoin legitimacy and as guardrails designed to preserve the core role of the banking system.

DeFi, Tokenization, And Developer Protections

DeFi poses a conceptual challenge for legislation because it blurs traditional boundaries between issuers, intermediaries, and users. Protocols operating via smart contracts may resemble exchanges, lending desks, or derivatives platforms, yet they often lack a central operator, complicating the application of existing laws built around identifiable entities. The CLARITY Act addresses this by providing safe harbors and legal shields for DeFi developers and validators, especially where they do not retain control over user funds or exercise ongoing discretionary power over protocol operations. These protections aim to ensure that writing open‑source code or running a validating node does not, by itself, trigger the full weight of securities or commodities regulation.

The Senate Banking Committee’s substitute bill complements this approach by directing the SEC and Treasury to develop specific rules on how persons or groups that control DeFi trading protocols must comply with disclosure, recordkeeping, and securities requirements. It also instructs Treasury to define how DeFi platforms conform to the Bank Secrecy Act and anti‑money‑laundering rules, a significant step toward integrating decentralized protocols into the existing financial crime framework. Coinbase’s analysis of the draft legislation highlights that, while the bill creates pathways for compliance, it also imposes obligations on those who retain control over DeFi systems, reinforcing a distinction between truly decentralized protocols and those that are decentralized in name only.

Beyond DeFi, both the Senate substitute and broader policy discussions emphasize tokenization—using blockchain infrastructure to represent securities, funds, bonds, and other real‑world assets (RWAs). Industry and policy reports anticipated that 2025 and 2026 would bring clearer tokenization frameworks, including wholesale market pilots and more explicit custody and segregation rules for tokenized instruments, and the Senate bill’s focus on tokenization standards reflects that trajectory. By defining how tokenized assets fit within securities and commodities law, and by establishing customer property protections in insolvency, legislators aim to unlock institutional adoption of tokenized RWAs while avoiding the ambiguity that has hindered past experiments.

Consumer Protection, Illicit Finance, And Bankruptcy

Consumer and systemic risk considerations run through almost every crypto bill. Lawmakers remain concerned about fraud, hacks, market manipulation, and the potential use of crypto for money laundering or sanctions evasion, especially in the wake of high‑profile exchange collapses and enforcement actions. The Senate Banking substitute addresses illicit finance by including provisions that expand compliance expectations for platforms that list or facilitate trading in digital assets, while directing Treasury to integrate DeFi into the Bank Secrecy Act framework. This aligns with the broader policy trend away from “regulation by prosecution,” which the Department of Justice has been encouraged to de‑emphasize in favor of clearer rules, and toward a system in which obligations are spelled out in statute and rulemaking rather than inferred from enforcement.

Another key focus is the treatment of customer assets in insolvency. The Senate substitute bill includes customer‑property protections in bankruptcy and an insolvency safe harbor aimed at ensuring that customer digital assets remain segregated and retrievable even if an exchange or custodian fails. This responds directly to the confusion seen in prior failures, where customers discovered that their assets might be treated as general unsecured claims rather than property held in trust. By clarifying that customer digital assets are not part of an intermediary’s estate, and by prescribing how they should be segregated and accounted for, legislators seek to rebuild trust in centralized platforms without stifling innovation.

Taxation is another area where legislation intersects with consumer protection and market integrity. While major tax reform bills for digital assets have not yet advanced as far as GENIUS or CLARITY, the Senate Finance Committee has scheduled hearings on digital asset taxation, indicating a desire to clarify issues such as cost basis reporting, wash sales, staking rewards, and cross‑border transactions. These hearings are meant to reduce uncertainty that can trap retail users in unexpected tax liabilities or create arbitrage opportunities for sophisticated actors. Combined with consumer‑oriented provisions in market‑structure bills, such as disclosure requirements for token issuers and limits on insider and related‑party sales, the emerging legislative framework seeks to balance innovation with robust safeguards against abuse.

The U.S., EU, Australia, and Russia are each building incompatible licensing and compliance regimes simultaneously, creating cross-border legal exposure for any operator serving multiple markets.

Until the U.S. crypto market structure bill is enacted, the boundary between securities and commodities remains contested, leaving exchanges and token issuers unable to reliably classify their products.

Competing GENIUS Act and STABLE Act proposals contain conflicting reserve, interest-bearing, and foreign-issuer rules that could segment or shrink stablecoin liquidity depending on which version passes.

Without the Blockchain Regulatory Certainty Act or CLARITY Act protections formally enacted, non-custodial developers remain potentially liable as unlicensed intermediaries under existing broker and money-transmission rules.

State-level Bitcoin reserve legislation concentrates public-fund Bitcoin holdings under government custody, introducing single-point political and custodial risk at the state treasury level.

Government shutdowns, partisan walkouts, and election-cycle turnover have repeatedly deferred crypto market structure legislation, and the 2026 midterm cycle adds further uncertainty to any bill's passage window.

Politics, Lobbying, And Power Struggles

Trump And The Push To Make America The “Crypto Capital”

The Trump administration has made digital assets an explicit part of its economic and geopolitical agenda, promising to make the United States the “crypto capital of the world.” The White House’s crypto policy page emphasizes strengthening American leadership in digital financial technology and encourages federal agencies to operationalize this vision, including through implementation of the GENIUS Act and support for broader market‑structure reforms. Executive actions like the creation of a Strategic Bitcoin Reserve and a U.S. Digital Asset Stockpile further signal a willingness to treat Bitcoin and other digital assets as strategic resources, not merely speculative instruments.

Patrick Witt, a senior White House adviser on digital assets, has described the GENIUS Act as one of the administration’s major achievements, arguing that it “crystallized” the regulatory environment for payment stablecoins. He has also highlighted the Senate Banking Committee’s advancement of its Digital Asset Market Clarity text as historic—the first time the Senate has moved a significant crypto bill out of committee—and underscored the administration’s support for giving the CFTC spot authority over digital commodities markets. At the same time, the White House has backed efforts to codify the Strategic Bitcoin Reserve and pursue crypto tax legislation, though Witt acknowledges that not all of these bills may pass in the current Congress.

President Trump has not hesitated to publicly pressure opponents of his crypto agenda, including large banks. In social media posts and public remarks, he has accused banking interests of holding up landmark crypto legislation and urged them to stop undermining the legislative push around bills like the CLARITY Act and GENIUS Act. This rhetoric reflects a broader political framing in which crypto is cast as both a tool of financial innovation and a challenge to entrenched financial institutions, with the administration positioning itself as an ally of crypto users, miners, and entrepreneurs against what it portrays as risk‑averse incumbents. Whether or not one accepts that framing, it has contributed to a sharpening of partisan and industry lines around key bills, even as significant bipartisan support remains for aspects such as stablecoin regulation and digital asset taxation.

Banks, Labor, And Other Skeptics

Opposition to parts of the crypto legislative agenda comes from multiple directions. Banking trade groups have lobbied aggressively against elements of market‑structure bills that they believe could erode their competitive position, especially provisions that enable stablecoin issuers and exchanges to compete for deposits, payment flows, and customer relationships. Bloomberg reporting notes that the Senate Banking Committee advanced its crypto market‑structure bill despite a late push from banking interests, marking a significant defeat for those groups in the early phase of the legislative fight. However, banks are likely to continue advocating for strict stablecoin yield limits, stringent prudential requirements for non‑bank issuers, and careful oversight of tokenized deposits and other bank‑like crypto products.

Labor unions and consumer advocates have also expressed concerns. They worry that poorly designed legislation could weaken worker protections, enable speculative excesses that ultimately harm pension funds and retail investors, or entrench new forms of financial concentration. Politico has reported on efforts by crypto CEOs to salvage landmark digital asset bills amid Senate gridlock, suggesting that some opposition stems from skepticism about the industry’s promises and its track record on issues like fraud and volatility. While unions and consumer groups are not necessarily aligned with banks—they often support stricter oversight of finance more generally—their warnings can complicate efforts to brand crypto legislation as unambiguously pro‑innovation and pro‑consumer.

Skepticism also extends to certain strategic initiatives, such as the Strategic Bitcoin Reserve. Critics question whether government ownership of Bitcoin might distort markets or expose taxpayers to asset‑price risk, particularly if acquisition strategies rely on purchases rather than solely on seized or forfeited assets. Others argue that codifying a long‑term hold requirement for Bitcoin reserves could limit fiscal flexibility or send confusing signals about the government’s role in digital asset markets. These debates underscore that crypto legislation is not only about regulating private actors; it also involves decisions about how deeply the state itself should engage with digital assets.

Industry Advocacy: Coinbase, Stand With Crypto, And Grassroots Pressure

The crypto industry has invested heavily in lobbying and grassroots mobilization to shape legislation. Major firms like Coinbase have become central participants in policy debates, providing detailed feedback on market‑structure bills and publicly analyzing their implications for exchanges, stablecoin issuers, and DeFi projects. In commentary on the Senate Banking Committee’s draft, Coinbase representatives have highlighted provisions that prohibit stablecoin rewards for mere holding while allowing transaction‑based incentives, as well as sweeping coverage of DeFi protocols and tokenized stocks. They have emphasized the need for clear pathways to compliance that recognize the unique characteristics of on‑chain activity rather than forcing it into legacy molds.

Coinbase has also helped organize broader advocacy through initiatives like Stand With Crypto, which has launched a 2026 midterm program, a voter hub, and candidate vetting efforts focused on digital asset policies. The organization’s polling suggests that crypto owners could form a significant swing voting bloc, especially in closely contested districts, giving pro‑crypto legislators an incentive to champion bills like CLARITY and GENIUS. Advocacy campaigns encourage retail users to contact their representatives, with messages that frame the right to own, transfer, and self‑custody crypto as a core civil liberty and warn that failure to pass comprehensive legislation will drive innovation overseas.

These campaigns operate alongside more traditional lobbying by industry associations, venture capital firms, and individual crypto companies. Politico’s reporting on crypto CEOs racing to rescue a landmark Senate bill amid gridlock illustrates how industry leaders can converge to press for last‑minute amendments or votes when legislative windows open. At the same time, advocacy does not always produce immediate results: David Sacks’s departure from a White House crypto advisory role, while key legislation remains unresolved, underscores how personnel changes and political realignments can disrupt even well‑organized policy efforts. Nonetheless, the sustained presence of industry voices at the negotiating table—confirmed by comments from Coinbase’s litigation head that “no one’s left the table” despite setbacks—indicates that crypto is now a permanent fixture in Washington’s legislative landscape rather than a passing fad.

Global Signaling: How Other Countries Shape The Debate

U.S. crypto legislation does not exist in a vacuum. Lawmakers are acutely aware that other jurisdictions are racing to establish their own frameworks, influencing where capital, talent, and infrastructure migrate. Fireblocks’ analysis of digital asset policy trends in 2025 and 2026 highlights, for example, Hong Kong’s comprehensive stablecoin bill, which passed in May and took effect in August, and Canada’s draft stablecoin law that mirrors the GENIUS Act’s structure by requiring 1:1 reserve backing and qualified custody. Brazil’s central bank has introduced a regulatory framework that classifies certain crypto transactions as foreign‑exchange operations, further integrating digital assets into mainstream financial regulation.

These developments inform U.S. debates in two ways. First, they offer reference models: policymakers can observe how foreign regimes handle issues like stablecoin licensing, tokenization of securities, and crypto taxation, then borrow successful elements or avoid observed pitfalls. Second, they raise competitive concerns: if the U.S. fails to act, or if its rules are perceived as overly restrictive or unpredictable, developers and token issuers may prefer jurisdictions like Hong Kong, Singapore, or the European Union, where legal frameworks such as MiCA are already in place or advancing rapidly. Senator Lummis’s warning that the current Congress may be the last realistic window for major U.S. crypto legislation before 2030 echoes these fears, suggesting that delay could yield a persistent disadvantage in capturing the next wave of digital financial innovation.

Even countries with more cautious stances, such as Russia, are experimenting with frameworks that expand controlled access to crypto for retail and professional investors while prohibiting domestic payments in crypto and routing transactions through licensed intermediaries. Those approaches illustrate a global trend toward tiered, risk‑based access that many policymakers see as balancing innovation with control. U.S. lawmakers thus find themselves calibrating legislation not only against domestic political constraints but also against a moving global benchmark for digital asset regulation.

Indiana State Rep. Kyle Pierce introduced a broad crypto bill arguing U.S. legislation shouldn’t favor Bitcoin alone, aiming to support the wider digital asset market, protect miners, and expand crypto exposure in public retirement programs.

Reading And Using Crypto Legislation As A Market Participant

For Traders And Investors

For traders and long‑term investors, crypto legislation is not just background noise; it is a central driver of market structure, liquidity, and risk pricing. Analysts at major banks like JPMorgan have explicitly tied the outlook for crypto markets in the second half of the year to the prospects for U.S. market‑structure legislation, arguing that passage of sweeping bills like the Digital Asset Market Clarity Act could reduce regulatory uncertainty and attract institutional capital. When House or Senate committees advance key bills, markets often react, as seen when the CLARITY Act passed the House and when the Senate Banking Committee approved its substitute text in a bipartisan vote, leading commentators to suggest that the odds of final passage had risen significantly.

In practical terms, investors should pay close attention to how legislation defines asset taxonomies, exchange registration requirements, custody rules, and stablecoin treatment. For example, if Bitcoin and Ether continue to enjoy relatively clear commodity status, they may face less direct impact from the CLARITY Act beyond indirect benefits from overall market growth and institutional adoption. By contrast, altcoins whose status has been contested by the SEC could see substantial re‑rating if a mature blockchain test allows them to transition into the commodity bucket, freeing exchanges and institutional investors to treat them more like established assets. Stablecoin frameworks like GENIUS influence which tokens are considered safe for use as collateral or settlement assets, potentially shifting liquidity toward those with explicit federal backing and away from unregulated or under‑collateralized alternatives.

Investors should also consider the timing of legislative events relative to macroeconomic conditions and market cycles. Past experience suggests that significant gains may come not from the passage of a law itself, but from the subsequent wave of product launches, ETF approvals, custody offerings, and institutional flows that clearer rules make possible. Conversely, failure to pass key bills, or the introduction of unexpectedly restrictive amendments, could dampen risk appetite and push activity offshore. As Senator Lummis and others have cautioned, a missed legislative window could leave U.S. markets operating under ambiguous rules for years, with courts and regulators filling the gap in ways that may be less favorable to innovation.

For Builders And Developers

For builders, legislation is both a risk and an opportunity. On the risk side, poorly designed laws could impose burdens that are ill‑suited to open‑source software projects, push DeFi developers into unworkable compliance models, or restrict access to core infrastructure. On the opportunity side, clear safe harbors and taxonomies can allow developers to design protocols with confidence that, if they meet specified decentralization criteria, they will not be treated as unregistered securities issuers or unlicensed intermediaries. The CLARITY Act’s protections for DeFi developers and validators, combined with its mature blockchain test, are particularly relevant: they suggest that truly decentralized protocols, where control is widely distributed and no single team retains privileged power, can be afforded legal treatment distinct from centralized platforms.

The Senate Banking substitute’s directives to the SEC and Treasury to craft DeFi‑specific rules create another planning horizon for builders. Developers need to assume that if they retain upgrade authority, operate front‑ends, or otherwise control user interactions, they may be treated as responsible persons for purposes of disclosure, recordkeeping, and AML compliance. Designing governance structures, access controls, and operational roles with these obligations in mind can help position projects to comply with forthcoming rules rather than retrofitting after enforcement actions occur. Tokenization of RWAs introduces further complexities, but also new markets: projects that can meet securities‑law requirements while offering the efficiency of on‑chain settlement may find fertile ground once legislation clarifies custody and segregation rules for tokenized instruments.

Builders should also track how legislation handles self‑custody, open‑source development, and developer liability. Provisions in ARMA that affirm individuals’ rights to own, transfer, and self‑custody digital assets, along with CLARITY’s safe harbors, help protect the foundational ethos of permissionless innovation. At the same time, DeFi‑related AML expectations will push projects to think more seriously about how to balance decentralization with necessary compliance, especially where centralized interfaces or governance processes remain. In this environment, engaging early with policymakers, participating in consultations, and aligning protocol design with evolving statutory frameworks can become as important as technical excellence.

For Miners And Infrastructure Providers

Miners and other infrastructure providers face a distinct set of legislative considerations. The Mined in America Act exemplifies how lawmakers increasingly view mining as both an economic and national security issue, not just an energy or environmental one. By creating a voluntary certification program, incentivizing a shift away from hardware linked to foreign adversaries, and integrating mining into existing federal energy and rural development programs, the bill signals that compliant, domestically anchored mining is a favored policy outcome. Miners who align with these standards could gain reputational and, potentially, financial advantages, such as easier access to public funding channels or preferential treatment in certain procurement or energy programs.

At the same time, miners must anticipate how broader legislation—such as the CLARITY Act and ARMA—will affect their operating environment. The codification of a Strategic Bitcoin Reserve, for instance, could create new demand sources or liquidity patterns in the Bitcoin market, though ARMA’s requirement that reserve holdings be maintained for at least twenty years emphasizes stability over trading. Energy policy debates, including discussions of nuclear power and renewable integration that have been championed in other Senate hearings, may intersect with mining incentives, especially if legislators see mining as a flexible load that can support grid resilience. Global trends, including countries that seek to concentrate mining domestically or to restrict it due to energy concerns, further influence where miners choose to locate and how they invest in hardware.

Infrastructure providers beyond mining—such as custodians, node operators, and data centers—also need to watch customer‑property rules, cybersecurity standards, and licensing frameworks embedded in market‑structure bills. Robust customer‑asset protections in bankruptcy, for example, can become a competitive differentiator for custodians that invest in segregation and transparent auditing, particularly as institutional investors demand bank‑grade safeguards. As with other sectors, legislative engagement is not optional: infrastructure providers that ignore policymaking risk being defined by it, while those that participate constructively can help shape rules that recognize the technical realities of distributed systems.

Outlook

Crypto legislation has moved from the periphery of policy to center stage, with the United States now possessing an enacted stablecoin law in the GENIUS Act, advanced market‑structure bills in the form of the House and Senate versions of the CLARITY Act, and active proposals for a Strategic Bitcoin Reserve, mining incentives, and anti‑CBDC safeguards. The Trump administration’s explicit embrace of digital assets, combined with bipartisan recognition that the status quo of regulation by enforcement is unsustainable, has created real momentum, as reflected in the Senate Banking Committee’s historic advancement of its crypto bill and in the White House’s calls to operationalize a national digital asset strategy. Yet obstacles remain: banking and labor interests continue to push back, gridlock and shutdowns can still derail timelines, and senators like Cynthia Lummis warn that the current Congress may be the last realistic window for comprehensive action before 2030.

For crypto users, builders, miners, and investors, the path forward will likely be incremental rather than explosive. Stablecoin regulation is already reshaping issuance and reserve practices, while market‑structure rules will gradually clarify which tokens can be listed where, under what disclosure regimes, and with what customer protections. Global developments in jurisdictions like Hong Kong, Canada, and Brazil will continue to influence U.S. debates, as policymakers seek to balance competitiveness with safety. Regardless of the exact sequencing, one trend is clear: digital assets are no longer operating in a legal vacuum. Instead, they are being woven, statute by statute, into the fabric of financial law, industrial policy, and national strategy—a process that will define the contours of the crypto ecosystem for the next decade and beyond.

Latest Legislation news

Cassidy and Lummis drop Mined in America Act to wean U.S. miners off Chinese hardware and cement Trump's strategic Bitcoin reserveLummis touts bipartisan CLARITY Act revisions as strongest-ever legal shield for DeFi developersIndiana State Rep. Kyle Pierce introduced a broad crypto bill arguing U.S. legislation shouldn’t favor Bitcoin alone, aiming to support the wider digital asset market, protect miners, and expand crypto exposure in public retirement programs.The Bank of Russia proposed a new crypto framework expanding retail and professional investor access under tiered limits, while keeping crypto barred from domestic payments and routed through licensed intermediaries, with full legislation targeted for 2026. Stand With Crypto is gearing up for 2026 by vetting candidates on digital asset policies, signaling another major push to shape U.S. crypto legislation. With Congress shifting, pro-crypto voices aim to influence the next wave of policymakers.

Stand With Crypto is gearing up for 2026 by vetting candidates on digital asset policies, signaling another major push to shape U.S. crypto legislation. With Congress shifting, pro-crypto voices aim to influence the next wave of policymakers. U.S. Government shutdown stretches to record 36 days, continues risk of derailing crypto bill. Market structure legislation could still see movement this year, but likely won't become law before 2026.

U.S. Government shutdown stretches to record 36 days, continues risk of derailing crypto bill. Market structure legislation could still see movement this year, but likely won't become law before 2026.Sources

- https://www.globalgovernmentfinance.com/crypto-week-usa-clarity-genius-anti-cbdc-acts/

- https://www.dwt.com/blogs/financial-services-law-advisor/2026/05/senate-banking-crypto-market-structure-bill

- https://www.whitehouse.gov/fact-sheets/2025/07/fact-sheet-president-donald-j-trump-signs-genius-act-into-law/

- http://begich.house.gov/media/press-releases/congressman-nick-begich-leads-legislation-establish-strategic-bitcoin-reserve

- https://x.com/WuBlockchain/status/2060579493262377182

- https://www.whitehouse.gov/crypto/

- https://www.bloomberg.com/news/articles/2026-05-15/crypto-s-win-on-landmark-legislation-reshapes-rivalry-with-banks

- https://www.youtube.com/watch?v=XbqhCO7qbu4

- https://www.cassidy.senate.gov/newsroom/press-releases/cassidy-lummis-introduce-bill-to-boost-u-s-digital-asset-mining-back-president-trumps-strategic-bitcoin-reserve/

- https://www.bloomberg.com/news/articles/2026-02-26/jpmorgan-sees-crypto-boost-if-market-structure-bill-passes

- https://www.youtube.com/watch?v=Ix3_wsQw5Jc

- https://www.politico.com/news/2025/10/23/crypto-ceos-senate-digital-assets-bill-00619335

- https://www.youtube.com/watch?v=3pFltnh0AJ0

- https://www.youtube.com/watch?v=LInLy7pxTi8

- https://www.avemarialaw.edu/clarity-act/

- https://www.fireblocks.com/blog/policy-changes-2025-outlook-2026

- https://www.politico.com/live-updates/2026/03/03/congress/trump-crypto-bill-fight-00810684

- https://www.disruptionbanking.com/2026/03/26/stand-with-crypto-launches-2026-midterm-program-with-new-voter-hub-first-endorsements/

- https://blockchair.com/de/news/u-s-government-shutdown-stretches-to-record-36-days-continues-risk-of-derailing-crypto-bill--bd8f66b7c0a94039

Community notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…