Comprehensive explainer on Bitcoin reserves, covering national strategic BTC reserves, state and corporate treasuries, exchange and DeFi reserve models, legal and governance challenges, and how growing BTC reserves could reshape crypto markets.

+11 sources across the wider coverage universe

El Salvador's Strategic Bitcoin Reserve surpasses 7,600 BTC, now valued at $506M2026-03

El Salvador's Strategic Bitcoin Reserve surpasses 7,600 BTC, now valued at $506M2026-03 Florida lawmakers renew push to launch State Bitcoin Reserve. On Tuesday, Florida lawmakers introduced another bill for the creation of a strategic Bitcoin reserve, less than a year after two attempts were shelved.2026-01

Florida lawmakers renew push to launch State Bitcoin Reserve. On Tuesday, Florida lawmakers introduced another bill for the creation of a strategic Bitcoin reserve, less than a year after two attempts were shelved.2026-01 Bitcoin soars past $106k as Trump hints at US Bitcoin strategic reserve, fueling bullish sentiment and market optimism.2024-12

Bitcoin soars past $106k as Trump hints at US Bitcoin strategic reserve, fueling bullish sentiment and market optimism.2024-12 In his CNBC interview, SkyBridge Capital's Anthony Scaramucci calls Bitcoin “a crucial long-term strategic asset” and advocates for a U.S. strategic Bitcoin reserve.2025-03

In his CNBC interview, SkyBridge Capital's Anthony Scaramucci calls Bitcoin “a crucial long-term strategic asset” and advocates for a U.S. strategic Bitcoin reserve.2025-03 Donald Trump hasn’t even taken office yet, but reports suggest the President-elect is preparing sweeping crypto-friendly executive orders for day one. Among them: reversing restrictive accounting policies, tackling de-banking, and potentially designating Bitcoin as a national reserve asset. Could this be the “orange candle” moment the market has been waiting for?

Meanwhile, Ethena takes a major step forward by integrating into Spark’s Liquidity Layer, unlocking direct access to up to $1.1 billion in holdings and driving higher yields for DeFi users. Bubblemaps launched $BMT to incentivize community-driven blockchain investigations, and Derive unveiled its $DRV token with staking rewards and governance features, kicking off a new era for on-chain derivatives trading.

Check out today’s newsletter for the full story and deeper insights into these developments.2025-01

Donald Trump hasn’t even taken office yet, but reports suggest the President-elect is preparing sweeping crypto-friendly executive orders for day one. Among them: reversing restrictive accounting policies, tackling de-banking, and potentially designating Bitcoin as a national reserve asset. Could this be the “orange candle” moment the market has been waiting for?

Meanwhile, Ethena takes a major step forward by integrating into Spark’s Liquidity Layer, unlocking direct access to up to $1.1 billion in holdings and driving higher yields for DeFi users. Bubblemaps launched $BMT to incentivize community-driven blockchain investigations, and Derive unveiled its $DRV token with staking rewards and governance features, kicking off a new era for on-chain derivatives trading.

Check out today’s newsletter for the full story and deeper insights into these developments.2025-01 President Trump establishes U.S. Strategic Bitcoin Reserve using forfeited assets, causing Bitcoin to drop $5,000 after the announcement; Crypto Czar David Sacks emphasizes no taxpayer funds will be involved.2025-03

President Trump establishes U.S. Strategic Bitcoin Reserve using forfeited assets, causing Bitcoin to drop $5,000 after the announcement; Crypto Czar David Sacks emphasizes no taxpayer funds will be involved.2025-03

Bitcoin Reserves: How BTC Became A Strategic Asset For States, Corporates, And DeFi

In its simplest sense, a Bitcoin reserve is a pool of BTC set aside for long‑term, strategic purposes rather than short‑term trading, whether that reserve sits on a sovereign balance sheet, a corporate treasury, or inside a DeFi protocol. As governments from El Salvador to the United States explore “Strategic Bitcoin Reserves,” and institutions build dedicated Bitcoin treasuries, the idea that BTC can function as a reserve asset—alongside gold, foreign currency, or cash—has moved from fringe talking point to an active policy and market design question.

What Is A Bitcoin Reserve?

The term Bitcoin reserve does not have a single legal definition, but in practice it describes Bitcoin that is deliberately held back from day‑to‑day spending or trading and earmarked for stability, resilience, or strategic optionality. For a government, that can mean BTC accumulated through purchases or seizures that is locked away for decades and only tapped during financial crises or for major national projects. For a corporation, it can refer to Bitcoin on the balance sheet as part of a treasury strategy, intended to preserve value over the long term rather than fund near‑term operating expenses. For exchanges and custodians, a Bitcoin reserve encompasses the coins they hold to meet client withdrawal obligations, often subject to proof‑of‑reserves attestations. In DeFi, reserves underpin tokenized Bitcoin instruments and are increasingly verified onchain.

The key idea is intentionality: BTC is held not merely as another volatile tradeable asset, but as a reserve that supports other obligations, signals credibility, or hedges against macroeconomic risks. That framing borrows directly from the way states and banks talk about gold and foreign exchange reserves and reflects Bitcoin’s evolving narrative as “digital gold” and potential collateral of last resort. As a result, the mechanics of Bitcoin reserves—how they are acquired, secured, accounted for, and disclosed—are no longer only a technical or ideological issue. They are now matters of public policy, corporate governance, and market infrastructure design, with concrete legislative proposals and regulatory frameworks emerging across multiple jurisdictions.

El Salvador's Strategic Bitcoin Reserve surpasses 7,600 BTC, now valued at $506M

Bukele took a $1.4B IMF loan that explicitly required scaling back government Bitcoin involvement — then kept the 1 BTC/day DCA running, literally buying BTC the day after the IMF reiterated its restrictions in March 2025. With accumulation running since Sept 2021 through multiple bear market lows, their average cost basis is likely sub-$45K, putting the treasury up 40%+ on a position partially funded by fiat debt at concessional IMF rates. Sovereign carry trade: borrow cheap dollars, stack sats, let the spread compound — and no other nation-state has the political runway to copy it.

Readers click Bitcoin Reserve stories in strict order of political commitment — federal executive action dwarfs state bills, which dwarf foreign precedents — revealing they are not tracking a crypto trend but a specific question: will sovereign governments actually put BTC on their balance sheets, or will the signal evaporate before legislation crystallizes?↗

Why Bitcoin Is Being Treated As A Reserve Asset

To understand why Bitcoin reserves are now on legislative calendars and corporate board agendas, it helps to revisit what makes an asset suitable for reserve status. Traditional reserve assets such as gold and high‑quality sovereign bonds are valued for liquidity, global acceptance, predictable issuance or scarcity, and insulation from domestic political risk. Bitcoin’s advocates argue that BTC satisfies several of these properties in digital form: its supply is capped at 21 million coins by protocol, issuance follows a known halving schedule, and it trades in deep global markets that operate essentially continuously.

From a macro perspective, Bitcoin’s growing market capitalization and liquidity have made it more plausible to hold in size without immediately moving the market, especially when accumulation is phased in over time. At the same time, persistent concerns about inflation, fiscal deficits, and the long‑term purchasing power of fiat currencies have led some policymakers and treasurers to look for assets that are neither liabilities of another state nor dependent on any single central bank. The idea of Bitcoin as non‑sovereign collateral fits neatly into that search for diversification, even if Bitcoin’s volatility and regulatory uncertainty remain major obstacles to treating it like traditional reserves.

The convergence of crypto‑native and traditional financial market structures has also played a role. Regulated futures, options, and structured products referenced to BTC now allow large holders to hedge price risk more effectively, which is an important ingredient in any reserve management program. The Commodity Futures Trading Commission’s approval of KalshiEX’s BTCPERP contract, a perpetual futures referencing the spot price of Bitcoin, is one example of how U.S. regulators are starting to accommodate hedging tools around BTC in a more explicit way. By recognizing such derivatives under the Commodity Exchange Act and requiring that the contract comply with core principles for designated contract markets, the CFTC is laying groundwork for a more sophisticated reserve management toolkit.

Finally, Bitcoin’s political symbolism has shifted. Where a decade ago holding BTC was often framed as anarchic or anti‑system, proposals for Bitcoin reserves now feature in mainstream parliamentary debates in France, national legislation in the United States, and hearings before Senate committees. That does not mean consensus exists—many central bankers and finance ministries remain deeply skeptical—but the agenda has undeniably moved from the margins into formal institutions.

Sovereign And National Strategic Bitcoin Reserves

The United States: From Executive Order To Legislation

In the United States, the concept of a Strategic Bitcoin Reserve moved from advocacy circles into federal policy via a presidential executive order signed on March 6, 2025. The order directed the Secretary of the Treasury to establish an office to administer custodial accounts collectively known as the “Strategic Bitcoin Reserve,” capitalized with all Bitcoin held by the Department of the Treasury that had been finally forfeited in criminal or civil asset forfeiture cases or collected as civil money penalties, provided those funds were not needed for statutory purposes. Agencies across the federal government were instructed to review their authority to transfer any such “Government BTC” into the Reserve and report back within 30 days, kicking off a process to centralize scattered BTC holdings under Treasury’s control.

A notable feature of this executive design is the no‑sale rule: Government BTC deposited into the Strategic Bitcoin Reserve “shall not be sold” and must instead be maintained as reserve assets of the United States used to meet governmental objectives in accordance with applicable law. In parallel, the order called for the creation of a United States Digital Asset Stockpile, a separate set of secure accounts for other government‑held digital assets, again with agencies required to provide a full accounting of holdings and the custodial arrangements in place. This approach effectively treats forfeited or otherwise acquired BTC as a long‑term sovereign reserve, rather than a pool of assets to be liquidated for dollars, and it signals an intention to manage Bitcoin within a distinct reserve policy framework.

Because an executive order can be modified or revoked by future administrations, legislators moved to create a statutory framework around the concept. In May 2026, Representative Nick Begich introduced the American Reserve Modernization Act of 2026 (ARMA), a bipartisan bill that would establish a secure Strategic Bitcoin Reserve within the Treasury, alongside a separate Digital Asset Stockpile for non‑Bitcoin digital assets held by federal agencies. The legislation would consolidate custody and management of these digital assets under Treasury to ensure consistent oversight and transparent stewardship of taxpayer‑owned assets acquired through forfeitures, penalties, and other legal proceedings. ARMA explicitly frames this as an effort to modernize how the United States handles digital reserve assets, positioning the country as a leader in responsible digital asset custody.

ARMA goes beyond mere consolidation by embedding transparency and time‑horizon constraints. It requires all federal agencies to provide a full accounting of digital assets they hold or control, mandates quarterly public “proof‑of‑reserve” reports, and calls for independent third‑party audits, subject to congressional oversight. To reinforce the strategic nature of the Bitcoin Reserve, the bill requires BTC held there to be maintained for at least 20 years, effectively locking it in as a generational asset unless extraordinary circumstances justify change. The bill also affirms that the federal government cannot impair the lawful right of individuals to own, transfer, or self‑custody digital assets, linking sovereign reserve management to broader digital property rights.

In parallel, lawmakers have pushed for complementary legislation focused on regulatory clarity and feasibility studies. Scott Bessent told the Senate Finance Committee that the administration’s CLARITY Act should pass in the near term and that the Strategic Bitcoin Reserve is progressing at a measured pace, underscoring the administration’s view that reserves must be anchored in a coherent legal framework for digital assets more broadly. Separately, members of Congress are backing bills that would require the Treasury to study within a fixed period the feasibility, custody, cybersecurity, and legal authority for a Strategic Bitcoin Reserve. While those study mandates do not themselves create reserves, they could set federal standards for Bitcoin custody and accounting that shape practices across both public and private sectors.

The White House has also signaled that further guidance is imminent. Patrick Witt, executive director of the President’s Council of Advisors for Digital Assets, has said that a formal update on the Strategic Bitcoin Reserve is close, citing a “breakthrough” on the legal basis, custody arrangements, and interagency reporting framework. That comment suggests ongoing negotiation across departments and agencies about how Bitcoin reserves should fit alongside existing federal financial controls, security protocols, and reporting obligations. Meanwhile, one Senate proposal dubbed the “Mined in America Act,” introduced by Senators Bill Cassidy and Cynthia Lummis, aims to both establish a voluntary crypto mining certification program and codify the Strategic Bitcoin Reserve into statute, explicitly tying reserve policy to domestic Bitcoin mining and energy use. In short, the U.S. debate has moved from “should we hold Bitcoin?” to the more granular question of how to structure, secure, and oversee a sovereign BTC reserve.

State‑Level Bitcoin Reserves: Texas, North Carolina, Florida And Beyond

While federal policymakers debate national strategy, several U.S. states are exploring their own versions of Bitcoin reserves, often motivated by local economic development goals and a desire to hedge state balance sheets. Texas in particular has positioned itself as an early mover. In 2026, acting Texas Comptroller Kelly Hancock announced the formation of the Texas Strategic Bitcoin Reserve Advisory Committee, a five‑member body created under Senate Bill 21 and made up of Hancock and experts in investments and digital assets. The committee is tasked with advising on administration and management of the state’s reserve, including how to value digital assets, manage risk, and develop policies around custody of virtual currency. The Comptroller’s office simultaneously issued a request for proposals seeking a qualified firm to provide custody and liquidity services for the reserve, with responsibilities that include securely acquiring, holding, managing, and reporting on the state’s Bitcoin and other cryptocurrency holdings. The selected provider must deliver institutional‑grade security and key management, support legislative reporting, and build a public website to transparently display reserve holdings and educational materials.

North Carolina has gone a step further by drafting detailed statutory language for a state Bitcoin reserve. Senate Bill 327, the North Carolina Bitcoin Reserve and Investment Act, authorizes the State Treasurer to allocate up to \(10\%\) of public funds into Bitcoin as part of the state’s long‑term financial strategy, with any BTC acquired to be placed into a dedicated Bitcoin Reserve. The bill allows the Treasurer to pursue Bitcoin‑backed investment strategies, such as lending and other regulated yield‑generating activities, but requires that the reserve be managed as a strategic asset subject to stringent safeguards. Among those safeguards are requirements that Bitcoin be held in cold storage wallets with multi‑signature authentication to prevent unauthorized access, that a dedicated department within the Treasurer’s office have custody over the reserve to maintain direct state control, that a Bitcoin Economic Advisory Board of industry experts provide ongoing guidance, and that monthly audits verify the reserve’s status, balance, security, and performance. The bill also mandates state‑backed insurance policies to protect the reserve against cyber threats and economic downturns, and it instructs the Treasurer to explore Bitcoin mining operations as a way to increase holdings at minimal cost.

Crucially, North Carolina’s proposal sharply limits when the Bitcoin Reserve can be used. The reserve is to be held as a long‑term asset, with liquidation permissible only under specified conditions: responding to a severe financial crisis when other reserves are insufficient, pursuing a state‑approved investment strategy to enhance the reserve’s value, financing critical infrastructure and development projects approved by the legislature, or funding Bitcoin‑related research and business incentives to foster economic growth. Even then, liquidation of reserve BTC requires approval by at least two‑thirds of members present and voting in both legislative chambers, and the reserve can also be used to back bonds as an alternative financing mechanism. The bill explicitly requires compliance with all federal and state laws on cryptocurrency holdings and taxation and directs the state to advocate for Bitcoin‑friendly regulations at the federal level to protect its reserves. In effect, North Carolina’s act sketches a full governance, security, and policy architecture for state‑level Bitcoin reserves.

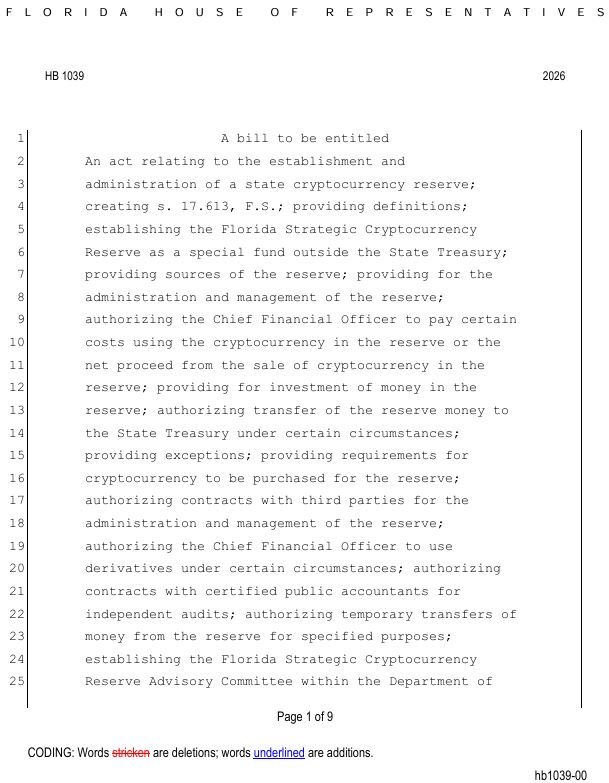

Florida’s efforts reveal that such initiatives can also stall. The Florida Strategic Cryptocurrency Reserve Act (CS/SB 1038) would have authorized the state’s Chief Financial Officer to create and manage a Strategic Cryptocurrency Reserve and established an advisory committee for that purpose, but the bill died in committee in March 2026. The proposal envisioned allowing the CFO to use specific funds to cover the cost of administering the reserve and to purchase cryptocurrency under defined conditions. Although that attempt failed, Florida lawmakers have since renewed their push with fresh legislation, illustrating that political interest in state‑level Bitcoin reserves can persist even after initial setbacks.

Smaller jurisdictions and municipalities are also testing the waters. Local advocates in places such as Vancouver have pushed for municipal Bitcoin reserves to diversify city treasuries, only to encounter bureaucratic and legal roadblocks that highlight how ill‑fitting many existing public finance rules are for crypto assets. Taken together, U.S. state‑level experiments show a spectrum of approaches, from Texas’s advisory‑committee‑plus‑custody‑RFP model to North Carolina’s highly prescriptive reserve statute, each grappling with the same core issues of security, transparency, and political control.

International Experiments: El Salvador, France, Philippines, Switzerland

Outside the United States, the most visible example of a national Bitcoin reserve remains El Salvador. While the country’s controversial move to adopt Bitcoin as legal tender attracted global headlines, less attention has gone to the mechanics of its strategic holdings. Public disclosures indicate that El Salvador’s Strategic Bitcoin Reserve surpassed 7,600 BTC, with reported holdings of 7,605.37 BTC worth roughly \( \$512 \) million at the time of the announcement. The government has portrayed this reserve as a long‑term asset, not a short‑term speculative bet, and recent moves to redistribute coins from a single large address into multiple new, unused addresses reflect a gradual shift toward best practices in operational security and preparation for potential threats such as advances in quantum computing. That kind of address management—moving from concentrated to more distributed custody—mirrors patterns seen in sophisticated institutional Bitcoin operations.

France offers a different model, one that is still aspirational but unusually comprehensive in scope. A pro‑crypto bill introduced by the center‑right Union of the Right and Centre (UDR) party and led by lawmaker Éric Ciotti proposes a national Bitcoin Strategic Reserve that would aim to acquire up to \(2\%\) of Bitcoin’s total supply, or around 420,000 BTC, over seven to eight years. The legislation would create a dedicated Public Administrative Establishment to manage the reserve, mirroring institutions that currently handle France’s gold and foreign currency reserves. Funding would come from multiple channels: public Bitcoin mining operations powered by surplus nuclear and hydroelectric energy, adapted taxation to encourage domestic mining, retention of some crypto assets seized in legal proceedings, and the allocation of roughly a quarter of funds collected through popular savings vehicles such as the Livret A and LDDS to daily Bitcoin purchases. The proposal estimates that this could translate into about 15 million euros per day in BTC buying, or around 55,000 BTC annually, subject to market conditions.

Beyond reserves, the French bill embraces euro‑denominated stablecoins for everyday payments, proposing tax and social contribution exemptions for small transactions under €200 and allowing certain taxes to be paid in stablecoins. It explicitly opposes a centralized European Central Bank digital euro on privacy grounds and suggests adjustments to electricity taxation and tariffs to support data centers and mining operations. The bill would encourage institutional adoption of Bitcoin and other crypto assets via exchange‑traded notes and calls for revisions to European prudential rules that currently impose high risk weights, limiting the use of crypto as collateral for loans. However, its political prospects are uncertain: the UDR holds just 16 of 577 seats in the National Assembly, making passage unlikely without substantial cross‑party support. Regardless of its fate, the proposal illuminates how a national Bitcoin reserve can be embedded within a broader industrial and financial policy agenda.

In the Philippines, Representative Migz Villafuerte has taken a more focused approach with House Bill 421, which would create a Philippine Strategic Bitcoin Reserve by directing the central bank (Bangko Sentral ng Pilipinas) to purchase 2,000 BTC annually for five years, totaling 10,000 BTC. The bill envisions these holdings being maintained for 20 years as part of a long‑term national strategy, mirroring the multi‑decade horizon in several U.S. and European proposals. By setting a fixed annual purchase schedule and a long lock‑up period, the Philippine initiative seeks to dollar‑cost‑average into Bitcoin over time while insulating the reserve from short‑term political pressures to sell during crises or rallies.

Not all national experiments have succeeded. In Switzerland, a grassroots campaign known as the Bitcoin Initiative sought to amend the constitution to require the Swiss National Bank to hold Bitcoin alongside its gold and foreign currency reserves. Under Swiss rules, campaigners had 18 months to collect 100,000 valid signatures to trigger a referendum, but as the deadline approached they had gathered only around half that number. Organizers announced that the effort would end early, effectively shelving the idea of a legally mandated Bitcoin allocation on the SNB’s balance sheet for now. The Swiss experience demonstrates that while Bitcoin reserve proposals can attract media attention, translating them into binding law—especially in direct‑democracy systems with stringent procedural thresholds—remains challenging.

What Makes A Reserve “Strategic”?

Across these examples, the modifier “strategic” is more than rhetorical. Strategic Bitcoin reserves tend to share three traits: long time horizons, constrained usage, and signaling value. Long time horizons are evident in the 20‑year minimum holding periods proposed in ARMA and the Philippine bill, as well as in El Salvador’s and France’s emphasis on multi‑year accumulation and retention strategies. Constrained usage shows up in rules that limit when reserves can be tapped—North Carolina’s requirement of a supermajority legislative vote and clearly defined emergency or investment conditions, ARMA’s implicit framing of the reserve as generational, and executive orders that forbid routine liquidation. These constraints are meant both to protect the reserve from opportunistic short‑term politics and to enhance its credibility as a backstop.

The signaling function operates on several fronts. Internationally, holding Bitcoin reserves can signal technological openness and financial innovation, particularly for smaller economies hoping to attract crypto investment and tourism. Domestically, it can signal a commitment to preserving purchasing power outside the traditional fiat system, which may resonate with certain voter blocs. Within markets, a government or large institution that commits to long‑term BTC holdings may influence perceptions of Bitcoin’s durability and safe‑haven status, especially if reserves are large relative to circulating supply. That signaling cuts both ways: critics argue that making Bitcoin a strategic asset could expose public finances to extreme volatility, while supporters contend that early movers will benefit disproportionately if BTC matures into a widely accepted reserve asset.

Importantly, calling a Bitcoin reserve “strategic” does not automatically resolve practical questions around risk management, hedging, and integration with existing reserve frameworks. Instead, it highlights the need to treat Bitcoin not as a speculative side bet, but as a component of formal reserve policy that must coexist with bonds, cash, and gold under coherent guidelines. Much of the emerging legislation—whether in Washington, Austin, Raleigh, Paris, or Manila—can be read as an attempt to write those guidelines down in advance.

Florida lawmakers renew push to launch State Bitcoin Reserve. On Tuesday, Florida lawmakers introduced another bill for the creation of a strategic Bitcoin reserve, less than a year after two attempts were shelved.

Let them keep trying harder 💪🏾

- 01Trump federal reserve action↗

The highest-clicked headlines all pivot on whether Trump would convert campaign rhetoric into a signed executive order, making each new signal a potential 'orange candle' moment for price.

- 02State legislation wave↗

Readers tracked a rolling count of states introducing reserve bills — Alabama, Minnesota, Texas, Arizona, Illinois, Florida, Pennsylvania — treating each new state entry as confirmation of a bottom-up political inevitability.

- 03Congressional codification risk↗

Even after Trump's EO, readers clicked on whether Congress would lock in the reserve permanently, with Lummis publicly doubting sufficient backing and Donalds moving to codify the order.

- 04Custodial proof-of-reserve risk↗

The cbBTC headline — warning of no audits, freeze capability, and seizure risk — tapped reader anxiety that 'Bitcoin reserves' held through custodians replicate the central bank model Bitcoin was designed to escape.

- 05Sovereign and corporate reserve precedents↗

Bhutan's 40%-of-GDP BTC position, El Salvador's 7,600 BTC, and Strategy's €620M preferred-stock raise gave readers concrete proof-of-concept data points for the reserve thesis before the US moved.

- 06International policy divergence↗

The UK's flat rejection, France's pro-crypto bill proposing a national reserve, Brazil's ambitions, and Switzerland's failed signature campaign showed readers the US move was contested globally, not inevitable.

Corporate And Institutional Bitcoin Reserves

Bitcoin As A Treasury Asset

Long before states talked about Strategic Bitcoin Reserves, corporate treasurers and public‑company CEOs were experimenting with using Bitcoin as a balance‑sheet asset. The logic is straightforward: if management believes Bitcoin will outperform cash and sovereign bonds over a multi‑year horizon, allocating part of treasury reserves to BTC might enhance shareholder value, especially in an environment of low real yields and persistent inflation concerns. At the same time, Bitcoin’s volatility, accounting treatment, and regulatory ambiguity make such strategies controversial. Under prevailing accounting standards in many jurisdictions, BTC is treated as an indefinite‑lived intangible asset, with unrealized losses recognized in earnings while unrealized gains often are not, creating asymmetric reporting outcomes that can discourage adoption.

Nevertheless, some companies have doubled down. A notable recent example is Strategy, the firm led by prominent Bitcoin advocate Michael Saylor, which raised €620 million in an upsized offering of 10% Series A Perpetual Stream Preferred Stock (ticker STRE) to fund further Bitcoin purchases and business expansion. The offering reflects a pattern in which certain companies effectively operate as leveraged Bitcoin holding vehicles, raising capital through debt or hybrid instruments and deploying proceeds into BTC. Such strategies amplify exposure to Bitcoin’s upside but also magnify downside risk and can create complex interactions between capital structure, market sentiment, and BTC price cycles.

Beyond headline names, Bitcoin is increasingly held in more prosaic corporate contexts. Some firms treat limited BTC positions as innovation pilots, learning tools, or marketing signals rather than core treasury reserves. Others, particularly in crypto‑adjacent industries, see Bitcoin holdings as a way to align with their customer base and brand identity. The distinction between operational holdings (for example, BTC used to facilitate payments or settlement) and reserve holdings (BTC kept for balance‑sheet strength and strategic optionality) is not always clear, but it matters for risk management and disclosure. As with sovereign reserves, the key questions are time horizon, governance, and alignment with broader financial policy.

Specialized Bitcoin Treasury Firms

A newer development is the emergence of dedicated Bitcoin treasury specialists—public companies whose primary business is to hold and manage BTC on behalf of themselves and, indirectly, their investors. France‑based Capital B offers one illustration. The firm, listed on a French exchange, recently raised €15.2 million through a targeted private placement, issuing around 23 million new shares bundled with subscription warrants priced at €0.66 per unit, a modest premium to recent trading levels. Institutional investors including Adam Back, creator of the Hashcash proof‑of‑work concept foundational to Bitcoin, and asset manager TOBAM participated in the raise. Capital B has said that it plans to deploy most of the roughly €14.4 million in net proceeds toward acquiring additional Bitcoin, potentially adding up to 182 BTC and lifting total holdings toward 3,125 BTC.

This kind of firm effectively converts equity capital into a leveraged Bitcoin reserve that public markets can access via shares, similar in spirit to a closed‑end fund or a corporate ETF. Investors who buy the stock gain exposure to Bitcoin’s upside and downside, filtered through corporate governance, capital structure, and operational decisions. For companies like Capital B, the challenge is to manage Bitcoin reserves with institutional‑grade security and risk control while maintaining enough transparency and liquidity to satisfy regulators and shareholders. Their existence underscores a broader trend: reserve management around Bitcoin is no longer confined to central banks and individual holders; it is becoming a specialized institutional domain with its own intermediaries.

Traditional companies in other sectors are also building sizable BTC reserves. A large ready‑made meal conglomerate, for instance, has publicly targeted a 10,000 BTC crypto reserve—roughly \( \$1 \) billion at certain price levels—and continues to add to its holdings via periodic purchases. This pattern of gradual accumulation, often described as “stacking sats” at corporate scale, borrows tactics from retail dollar‑cost‑averaging but applies them to treasury operations. Over time, as more such companies emerge, the line between “corporate Bitcoin reserve” and “Bitcoin ETF” could blur, especially if firms derive a significant share of their market value from BTC holdings rather than from operating businesses.

Institutional Products, Derivatives, And Hedging

Institutional adoption of Bitcoin reserves also depends on the availability of robust hedging tools. While spot BTC exposure can be acquired on exchanges, managing downside risk and duration typically entails futures and options. The CFTC’s decision to approve KalshiEX’s BTCPERP contract, a perpetual futures referencing the spot price of Bitcoin, is noteworthy because it represents a U.S. regulator explicitly green‑lighting a product that behaves much like perpetual swaps on offshore crypto exchanges but within a regulated futures framework. Kalshi submitted the contract under Commission Regulation 40.3, and after review the CFTC concluded that BTCPERP complies with the Commodity Exchange Act and all applicable regulations, including core principles for designated contract markets. The approval order requires Kalshi to list and maintain BTCPERP in full compliance as rules evolve, signaling that regulators are prepared to incorporate crypto‑linked derivatives into existing oversight structures rather than create entirely new regimes.

At the same time, major venues such as CME have rolled out more flexible Bitcoin futures trading hours that approximate 24/7 availability, helping better align traditional derivatives markets with the around‑the‑clock nature of spot crypto trading. This evolution gives treasury desks holding Bitcoin reserves more tools to manage risk, including the ability to hedge weekend gaps and respond quickly to macro news. As reserve‑focused legislation matures, public and private BTC holders may find themselves relying heavily on these derivatives to smooth volatility without violating long‑term holding commitments.

Prediction markets provide a different kind of signal. Platforms like Polymarket host contracts on whether the United States will formally establish or expand a Strategic Bitcoin Reserve by specific dates, with market odds reflecting the aggregated beliefs of traders about legislative and executive trajectories. While such markets are thin and speculative, they highlight how the existence—and perceived likelihood—of sovereign Bitcoin reserves has itself become a tradable narrative. For policymakers, this kind of “market‑implied probability” can be a double‑edged sword: it can serve as feedback on policy credibility but also risk being misinterpreted as consensus.

How Corporate And Sovereign Reserves Interact

Corporate and sovereign Bitcoin reserves do not exist in isolation. Large‑scale government buying or non‑selling commitments can influence market liquidity and price dynamics, which in turn affect corporate treasuries. Conversely, widespread corporate accumulation can normalize Bitcoin as a reserve asset and provide political cover for sovereign adoption, especially if corporate adopters are major employers or national champions. This feedback loop is another reason why clear standards for custody, disclosure, and risk management matter: failures in one domain can undermine trust in the other.

Exchange, Custodial, And DeFi Bitcoin Reserves

Exchange Reserves And Proof‑Of‑Reserves

For centralized exchanges and custodial platforms, “Bitcoin reserves” primarily refer to the BTC held on behalf of customers to meet withdrawal obligations. Historically, opacity around these reserves has contributed to catastrophic failures when platforms engaged in fractional practices or misused client assets. In response, a growing number of exchanges have adopted proof‑of‑reserves mechanisms, where they publish cryptographic or audited attestations showing that onchain balances match or exceed customer liabilities. While methodologies differ, the goal is to provide users and regulators with assurance that the platform is solvent in BTC terms.

The legislative push for sovereign Bitcoin reserves has heightened expectations around transparency in the private sector as well. ARMA’s requirement that federal digital asset reserves publish quarterly proof‑of‑reserve reports and undergo independent audits mirrors standards now expected of leading exchanges. Texas’s requirement that its reserve custodian build a public website to display holdings and provide educational materials similarly echoes exchange dashboards that show live wallet balances and security practices. As more public entities normalize proof‑of‑reserves, pressure is likely to grow on custodians and exchanges to converge on best practices, combining cryptographic verification with conventional financial audits.

Kraken’s Bitcoin Vault And Yield‑Bearing Reserves

One way exchanges are re‑framing Bitcoin holdings as reserves is by offering yield‑bearing products that position long‑term BTC as a kind of savings account. Kraken’s Bitcoin Vault, for example, is a product within its Kraken Earn suite that allows customers to allocate Bitcoin from their exchange balance into a separate vault and earn BTC‑denominated rewards without selling the underlying asset. Marketing materials describe yields of up to around 1.83%–2.5% annual percentage yield (APY), although the rate is variable and depends on underlying market conditions. The basic flow is that users deposit BTC from their Kraken balance, the funds are allocated onchain to Bitcoin lending markets where borrowers pay for liquidity, and rewards accrue automatically, paid in BTC. Users can withdraw back to their main balance at any time, subject to network conditions.

Under the hood, the Vault routes customer assets through DeFi infrastructure built by a third‑party provider, Veda, with strategy design and risk oversight handled by Sentora. Kraken itself does not control these external protocols, and the company explicitly warns users of technological, market, and operational risks, including the potential loss of some or all assets. Bitcoin Vault is offered by Payward Wallet, LLC, classified as an unregulated product, and is unavailable in certain jurisdictions such as the United Kingdom, the United Arab Emirates, and Australia. From a reserve‑management perspective, this kind of product turns idle customer BTC into an interest‑bearing reserve that supports lending and liquidity in broader crypto markets while promising users incremental BTC yield on top of price exposure.

For individual holders, Bitcoin Vault‑type products make it easier to build personal BTC reserves that feel more like savings accounts than speculative positions. However, they also introduce additional layers of risk and counterparty dependence. The distinction between self‑custodied reserves—BTC held in personal cold wallets with no yield—and platform‑based reserves—BTC parked in yield products or on exchanges—has profound implications for security and sovereignty. As sovereign and corporate actors adopt multi‑signature cold storage and insurance for their reserves, retail holders face similar trade‑offs between convenience and control.

Tokenized And Cross‑Chain Bitcoin Reserves In DeFi

Decentralized finance adds another twist: Bitcoin reserves can be tokenized and deployed across chains. One challenge in Bitcoin DeFi is enabling BTC to move into other ecosystems for yield and composability without fragmenting liquidity into multiple wrapped representations or introducing unmanageable trust assumptions. The Lombard project’s LBTC token, powered by RedStone oracles, is an example of how onchain reserve verification is being used to address this. Lombard’s goal is to create a cross‑chain form of Bitcoin that can be used in DeFi while maintaining a single pool of underlying BTC reserves, avoiding the proliferation of loosely collateralized wrapped tokens.

RedStone provides real‑time data feeds that bring information about the state of Lombard’s Bitcoin reserves onchain, allowing smart contracts to verify that the BTC backing LBTC is present, sufficient, and not double‑used. This approach aims to combine the advantages of centralized custody—such as robust security and regulatory compliance—with decentralized transparency, as anyone can monitor reserve ratios and flows via onchain data. For DeFi protocols integrating LBTC or similar tokens, the ability to rely on up‑to‑date reserve proofs is critical for risk management, especially when reserves underpin lending, leverage, or stablecoin systems. As with sovereign and exchange reserves, the technical and governance design of DeFi Bitcoin reserves will heavily influence trust and adoption.

Reserve Transparency And Onchain Proofs

Reserve transparency sits at the intersection of regulation, market discipline, and cryptography. Public entities such as the U.S. Treasury, under ARMA, would be required to publish periodic proof‑of‑reserve disclosures, likely combining traditional financial audits with data about onchain holdings. State‑level initiatives like Texas’s mandate for a public website displaying reserve holdings and North Carolina’s monthly audit requirements similarly emphasize regular reporting. In the DeFi world, projects like Lombard push transparency even further by making reserve proofs machine‑readable and integrated into protocol logic.

A key question for the coming years is whether onchain proof systems—using Merkle trees, zero‑knowledge proofs, and oracle‑fed data—can be standardized and recognized by regulators as acceptable evidence of solvency and reserve adequacy. If so, we could see a convergence where both centralized institutions and decentralized protocols use shared technical standards for Bitcoin reserve verification. Conversely, if regulators insist on conventional audits to the exclusion of cryptographic methods, some of the advantages of Bitcoin’s transparency may be underutilized. The direction chosen will influence how credible Bitcoin reserves are perceived by markets and the public.

Michael Saylor’s Strategy raises €620M in an upsized 10% Stream Preferred Stock offering to fund Bitcoin purchases and expansion, highlighting continued institutional confidence in BTC as a reserve asset.

At what percentage ownership does Michael Saylor become bad for BTC...at what point does Tom Lee become bad for ETH?

- 2024-07regulatory

Senator Lummis introduces BITCOIN Act to create US strategic reserve

- 2024-11milestone

Bitcoin surpasses $106k as Trump hints at national strategic reserve post-election

- 2025-01regulatory

Trump crypto executive orders issued on day one, including Bitcoin reserve designation

Trump signs EO formally establishing US Strategic Bitcoin Reserve from forfeited assets

- 2025-06milestone

30+ states have introduced Bitcoin reserve legislation

Florida Bitcoin reserve bills HB 487 and SB 550 indefinitely postponed and withdrawn

Texas Governor signs SB 21 into law; acting Comptroller names Strategic Bitcoin Reserve advisory committee

Treasury Secretary Bessent pushes Senate to pass Clarity Act; reserve described as advancing at 'deliberate speed'

Legal, Technical, And Governance Challenges

Custody, Security, And Quantum Risk

No discussion of Bitcoin reserves is complete without addressing custody. Sovereign and institutional holders routinely manage tens of billions of dollars in gold and foreign currency reserves with elaborate physical and procedural controls. Translating those disciplines into the digital realm means grappling with private key management, hardware security modules, multi‑signature schemes, geographic distribution, and incident response. North Carolina’s Bitcoin Reserve and Investment Act codifies some of these best practices by requiring that state BTC be held in cold storage wallets with multi‑signature authentication, explicitly to prevent unauthorized access. It also mandates state‑backed insurance against cyber incidents and economic downturns, acknowledging both technical and market risks.

Texas’s search for a custodian for its Strategic Bitcoin Reserve underscores similar concerns. The request for proposals calls for a firm capable of delivering institutional‑grade digital asset security, key management, and operational controls, along with robust reporting and support for legislative oversight. This effectively imports the trust standards of traditional asset custody into the Bitcoin context. For large public reserves, third‑party custodians may be attractive due to specialized expertise and scale, but they also introduce new dependencies and jurisdictional considerations.

Emerging threats such as quantum computing add another layer of complexity. While practical quantum attacks on Bitcoin’s cryptographic primitives remain speculative, prudent reserve managers cannot ignore the risk altogether. Actions like El Salvador’s shift from storing substantial BTC in a single address to distributing holdings across multiple new, unused addresses can be seen as incremental steps toward more robust security postures, reducing single‑point‑of‑failure exposure and preparing for more advanced key schemes in the future. Sovereign and institutional holders may eventually adopt post‑quantum signature schemes or key‑rotation rituals as standards evolve, but those transitions will have to be carefully managed to avoid operational disruptions and onchain confusion.

Who Controls The Keys? Governance And Democratic Oversight

Beyond technical security lies the question of governance: who decides when reserves are tapped, rebalanced, or re‑secured? For sovereign reserves, this is a constitutional and democratic issue. Trump’s executive order assigns custody of the Strategic Bitcoin Reserve to the Treasury Department and prohibits selling deposited BTC absent further legal authority. ARMA would cement that arrangement, giving Treasury centralized control while subjecting it to congressional oversight, periodic audits, and public reporting. State‑level acts, such as North Carolina’s, maintain reserve custody within the Treasurer’s office but add an external Bitcoin Economic Advisory Board to guide policy. Texas’s advisory committee, which includes experts from investment and digital asset sectors, plays a similar role, advising the Comptroller on reserve management.

The composition and mandate of such advisory bodies matter. They must balance technical competence with public accountability, ensuring that decisions about multi‑billion‑dollar reserves are informed by deep Bitcoin and cybersecurity expertise but remain aligned with democratic priorities. One risk is that highly specialized, relatively opaque bodies could become de facto decision‑makers without sufficient scrutiny. Another is politicization, where reserve decisions are driven by short‑term electoral considerations rather than long‑term strategy. Supermajority requirements for liquidation, as in North Carolina’s two‑thirds legislative approval threshold, are one way to guard against impulsive decisions. However, they also reduce flexibility, potentially hampering crisis response.

Internationally, governance structures vary. France’s proposed Public Administrative Establishment would sit somewhere between a central bank department and a sovereign wealth fund, with its own legal personality and governance rules. The Philippine reserve proposal hinges on the central bank, a technocratic institution, executing a fixed purchase schedule and custody strategy. Switzerland’s failed initiative would have placed Bitcoin reserve management directly under the Swiss National Bank’s mandate, subject to its existing governance structures and independence. These variations underscore that there is no single “right” model; instead, Bitcoin reserve governance must be tailored to each jurisdiction’s constitutional and institutional context.

Legal Authority, Accounting, And Regulation

Legal authority is another foundational question. In the U.S., Trump’s executive order relies on powers granted to the presidency and existing asset forfeiture statutes, but it operates in a landscape where the precise regulatory status of Bitcoin—commodity, security, or something else—has been contested. ARMA and the CLARITY Act are attempts to bring coherence by explicitly designating roles and clarifying regulatory boundaries for digital assets, including Bitcoin. Similarly, bills that instruct the Treasury to study the feasibility and legal basis for a Strategic Bitcoin Reserve reflect awareness that any durable reserve framework must withstand judicial scrutiny and align with pre‑existing financial controls.

Accounting rules add a more subtle constraint. For sovereigns, how Bitcoin reserves are booked—whether as foreign exchange, non‑monetary financial assets, or something else—affects reported fiscal positions and may interact with debt and deficit limits. Private‑sector accounting standards like GAAP and IFRS currently treat Bitcoin as an intangible asset, which can lead to earnings volatility and impairment charges that many CFOs find unappealing. Some advocacy groups and firms have lobbied for fair‑value treatment that would allow Bitcoin’s market price to be reflected more symmetrically on balance sheets. Until such changes occur, however, accounting frictions will likely slow the growth of corporate Bitcoin reserves relative to what pure economic analysis might predict.

Regulatory treatment also influences how reserves can be used. If Bitcoin is classified strictly as a commodity or property, using it as collateral for loans or as backing for bonds may require bespoke legal arrangements. France’s proposed revisions to European prudential rules, aimed at lowering risk weights on certain crypto‑assets to facilitate their use as collateral for “Lombard” loans, exemplify an effort to integrate Bitcoin into the existing collateral ecosystem. In the U.S., agencies like the CFTC and SEC, as well as banking regulators, will play pivotal roles in determining whether and how banks can hold Bitcoin reserves directly or via products such as ETFs and ETNs.

Geopolitics, Energy, And Mining

Bitcoin reserve policy is increasingly intertwined with energy and industrial policy. France’s bill explicitly envisions funding its Bitcoin reserve through public mining operations powered by surplus nuclear and hydroelectric energy, with adapted taxation for miners to encourage domestic participation. North Carolina’s act instructs the Treasurer to explore Bitcoin mining as a way to grow the state’s holdings at minimal cost, potentially leveraging local energy resources and infrastructure. In the U.S. Senate, the “Mined in America Act” would establish a voluntary certification program for crypto mining and codify Trump’s Strategic Bitcoin Reserve, linking reserve status to domestically produced BTC and suggesting a preference for “clean” or geopolitically aligned hashpower.

Texas, already a major North American Bitcoin mining hub thanks to its large energy sector and relatively friendly regulatory environment, illustrates how state‑level reserve policy can dovetail with mining. A Texas Strategic Bitcoin Reserve could, in principle, purchase BTC directly from in‑state miners, providing a local buyer of last resort and anchoring the region’s mining industry. Critics, however, worry that tying reserves to mining may entangle digital asset policy with contentious debates over energy consumption, climate change, and grid stability.

Geopolitically, the prospect of countries amassing sizable Bitcoin reserves raises questions about contagion and competition. In a scenario where multiple states view Bitcoin as a hedge against sanctions or currency debasement, reserve accumulation might accelerate during periods of geopolitical tension, potentially tightening BTC’s free float and amplifying price swings. Conversely, coordinated international norms—similar to those governing gold and FX reserves—could emerge, emphasizing transparency and restraint. For now, the landscape remains fragmented, with a few early adopters experimenting while most major economies watch from the sidelines.

Comparing Bitcoin Reserve Models

To synthesize the diverse approaches discussed so far, it is useful to compare the main types of Bitcoin reserves across several dimensions.

| Reserve Type | Typical Owner | Primary Objective | Time Horizon | Main BTC Sources | Transparency Tools |

|---|---|---|---|---|---|

| National strategic reserve | Sovereign (Treasury, central bank) | Financial sovereignty, crisis backstop, signaling | Multi‑decade (e.g., 20+ years) | Forfeitures, purchases, mining, seized assets, savings | Public reports, audits, potential onchain proofs |

| State/local reserve | State governments, municipalities | Diversification, economic development, mining link | Long‑term (decades) | Budget allocations, mining, investment returns | Legislative reports, advisory committees, public dashboards |

| Corporate treasury reserve | Public/private companies | Hedge, diversification, marketing, speculation | Multi‑year, revisited periodically | Capital raises, retained earnings, operational surplus | Financial statements, investor disclosures |

| Exchange/custodial reserve | Centralized platforms | Meet withdrawals, support yield products | Varies; often short‑ to medium‑term | Customer deposits, proprietary holdings | Proof‑of‑reserves attestations, audits |

| DeFi tokenized reserve | Protocols (DAOs, foundations) | Collateral backing, cross‑chain liquidity | Protocol‑dependent | Custodial BTC, user deposits, liquidity providers | Onchain oracles, real‑time reserve proofs |

This table is necessarily simplified, but it highlights an important point: “Bitcoin reserve” is a family of practices, not a single institution. The same underlying asset—BTC—can serve very different roles depending on who holds it, under what rules, and for what purpose. That diversity is both a strength, in terms of experimentation, and a risk, in terms of potential confusion or misaligned incentives.

Trump's EO established the reserve via executive action using only forfeited assets, but it lacks Congressional codification; Lummis cited insufficient Senate backing and the order remains reversible by a future administration.

Wrapped and custodied BTC products used as reserve proxies (e.g. cbBTC) carry unilateral freeze risk, no proof-of-reserve audits, and are vulnerable to government subpoenas — concentrating trust in a single custodian.

Bitcoin dropped roughly $5,000 immediately after Trump's actual EO signing because the reserve was funded only from forfeited assets rather than new purchases, demonstrating that execution details matter more than headline announcements.

Only approximately 86,000 BTC (43% of US government holdings) is classified as forfeited and available for a reserve; the remaining 112,000 BTC is ring-fenced for Bitfinex restitution and unavailable.

State reserve bills vary widely in asset scope and investment caps, and several have already been withdrawn (Florida HB 487 / SB 550), signaling that state-level momentum is uneven and reversible.

For sovereign reserves holding native BTC the smart-contract risk is minimal; risk is material only for tokenized or wrapped reserve vehicles, where on-chain proof-of-reserve integrations (e.g. Chainlink PoR for dlcBTC) partially mitigate but do not eliminate custodial failure modes.

How Bitcoin Reserves Could Reshape The Crypto Market

As Bitcoin reserves grow across these domains, they are likely to influence both the crypto ecosystem and the broader financial system. One obvious effect is on supply dynamics. If sovereigns, states, corporations, and DeFi protocols all commit to long‑term holdings, the effective free float of BTC available for trading diminishes. In a market with fixed maximum supply, increased strategic hoarding can contribute to tighter liquidity and potentially higher price sensitivity to new information. However, this effect can be mitigated if some reserve holders actively lend BTC into the market or use derivatives to synthetically adjust exposure without selling.

Another impact lies in market infrastructure. The emergence of regulated instruments like Kalshi’s BTCPERP futures, combined with institutional custody solutions and proof‑of‑reserve standards, is moving Bitcoin closer to the toolkit used for traditional reserve assets. As more entities treat BTC as a component of reserve or collateral portfolios, demand may grow for standardized settlement conventions, collateral haircuts, and risk models that integrate Bitcoin’s unique characteristics. Initiatives like VanEck’s U.S. Strategic Bitcoin Reserve vs. Debt calculator, which allows users to explore hypothetical scenarios for how a national Bitcoin reserve might affect the U.S. debt profile, show that traditional asset managers are already thinking about Bitcoin in macro‑fiscal terms.

On the DeFi side, robust, transparently managed Bitcoin reserves underpinning tokenized BTC could catalyze a new wave of Bitcoin‑collateralized lending, derivatives, and stablecoins. Projects like Lombard, powered by RedStone’s real‑time reserve proofs, illustrate how cross‑chain Bitcoin reserves can be made auditable and composable, lowering risk for protocols that depend on BTC collateral. If onchain Bitcoin reserves become widely trusted, they could help bridge the gap between “Bitcoin land” and “DeFi land,” allowing BTC to play a larger role in decentralized credit and liquidity markets.

For retail and smaller institutions, the normalization of Bitcoin reserves at higher levels of the system may reinforce the view of BTC as a long‑term savings asset rather than just a speculative instrument. Products like Kraken’s Bitcoin Vault, which package yield‑bearing strategies in an accessible interface, blur the line between personal savings accounts and institutional‑grade reserve management. At the same time, these products re‑emphasize the perennial crypto trade‑off between convenience and self‑sovereignty. As states and institutions adopt multi‑signature cold storage, air‑gapped hardware, and insurance, some individual users may feel pressure to opt back into custodial solutions that appear more “professional,” even if that means surrendering direct control of keys.

Finally, the political symbolism of Bitcoin reserves will likely continue to evolve. In some contexts, establishing a strategic Bitcoin reserve is framed as a declaration of monetary independence and alignment with crypto innovation. In others, it is criticized as speculation with public money. Prediction markets, media narratives, and electoral politics will shape how voters interpret these moves, and the performance of early adopters like El Salvador will be closely watched. If Bitcoin reserves weather volatility and prove accretive to fiscal stability, copycat policies may proliferate. If they contribute to fiscal stress or political scandal, they may serve as cautionary tales.

Outlook

Bitcoin reserves have moved from obscure thought experiments to concrete policy proposals, appropriation bills, and market products. National governments are testing Strategic Bitcoin Reserves that lock in BTC for decades; U.S. states are drafting detailed governance and custody frameworks; corporations are raising capital explicitly to expand their Bitcoin treasuries; exchanges and DeFi protocols are engineering new ways to put BTC reserves to work while proving their solvency in real time. Alongside this innovation has come a parallel wave of regulation, legislative oversight, and technical standard‑setting.

For now, Bitcoin remains a small share of global reserves compared with gold or major currencies. But the institutional scaffolding being built around BTC—executive orders, statutes, advisory committees, proof‑of‑reserves standards, cross‑chain oracles—suggests that reserve use cases will only grow more sophisticated. Whether Bitcoin ultimately becomes a mainstream reserve asset or remains a niche hedge will depend on factors far beyond crypto itself, including macroeconomic conditions, technological developments such as quantum computing, regulatory choices, and political will. What is clear is that “Bitcoin reserve” is no longer a fringe slogan; it is an emerging framework through which states, firms, and protocols are rethinking what it means to hold value for the long term.

Latest Bitcoin Reserve news

El Salvador's Strategic Bitcoin Reserve surpasses 7,600 BTC, now valued at $506MFlorida lawmakers renew push to launch State Bitcoin Reserve. On Tuesday, Florida lawmakers introduced another bill for the creation of a strategic Bitcoin reserve, less than a year after two attempts were shelved.Michael Saylor’s Strategy raises €620M in an upsized 10% Stream Preferred Stock offering to fund Bitcoin purchases and expansion, highlighting continued institutional confidence in BTC as a reserve asset. France’s First Comprehensive Pro-Crypto Bill Proposes Bitcoin Reserve, Stablecoin Payments, and Mining Incentives

France’s First Comprehensive Pro-Crypto Bill Proposes Bitcoin Reserve, Stablecoin Payments, and Mining Incentives US lawmakers are pushing a bill that would require the Treasury to study a Strategic Bitcoin Reserve, covering feasibility, custody, cybersecurity, and legal authority within 90 days. If passed, it could set federal standards for Bitcoin custody and accounting, shaping benchmarks for the wider industry.

US lawmakers are pushing a bill that would require the Treasury to study a Strategic Bitcoin Reserve, covering feasibility, custody, cybersecurity, and legal authority within 90 days. If passed, it could set federal standards for Bitcoin custody and accounting, shaping benchmarks for the wider industry. In the face of a potential quantum attack, El Salvador moves funds from a single Bitcoin address into multiple new, unused addresses as part of a strategic initiative to enhance the security and long-term custody of the National Strategic Bitcoin Reserve. This action aligns with best practices in Bitcoin management and prepares for potential developments in quantum computing

In the face of a potential quantum attack, El Salvador moves funds from a single Bitcoin address into multiple new, unused addresses as part of a strategic initiative to enhance the security and long-term custody of the National Strategic Bitcoin Reserve. This action aligns with best practices in Bitcoin management and prepares for potential developments in quantum computingSources

- https://www.whitehouse.gov/presidential-actions/2025/03/establishment-of-the-strategic-bitcoin-reserve-and-united-states-digital-asset-stockpile/

- http://begich.house.gov/media/press-releases/congressman-nick-begich-leads-legislation-establish-strategic-bitcoin-reserve

- https://x.com/CoinDesk/status/2038570144465662316

- https://comptroller.texas.gov/about/media-center/news/20260528-acting-texas-comptroller-kelly-hancock-names-strategic-bitcoin-reserve-advisory-committee-members-1778774749224

- https://www.ncleg.gov/BillLookup/2025/S327

- https://www.flsenate.gov/Session/Bill/2026/1038

- https://cryptopotato.com/swiss-bitcoin-reserve-dream-collapses-after-signature-campaign-falls-short-report/

- https://bitcoinmagazine.com/news/france-proposes-national-bitcoin-reserve

- https://unchainedcrypto.com/bessent-pushes-senate-to-pass-clarity-act-this-summer-as-strategic-bitcoin-reserve-advances-at-deliberate-speed/

- https://x.com/WuBlockchain/status/2056972808597782717

- https://www.kraken.com/bitcoin-vault

- https://blog.redstone.finance/2026/03/23/redstone-powers-lombard-to-bring-real-time-bitcoin-reserve-verification-onchain/

- https://www.cftc.gov/PressRoom/PressReleases/9240-26

- https://x.com/BitcoinNewsCom/status/1958868757067227189

- https://www.crowdfundinsider.com/2026/05/278571-france-based-digital-assets-treasury-firm-capital-b-strengthens-bitcoin-reserve-with-institutional-backing/

- https://www.kucoin.com/news/flash/strategy-raises-620m-in-stream-preferred-stock-offering

- https://lrs.sog.unc.edu/billsum/s-327-2025-2026

- https://www.vaneck.com/us/en/us-bitcoin-strategic-reserve-calculator/

- https://bitcoinmagazine.com/news/kraken-launches-bitcoin-vault-yield

Community notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…