Digital asset treasury companies hold BTC or ETH as primary balance-sheet assets, raising capital via ATMs, convertibles, and preferreds to accumulate crypto. This explainer covers how they work, key risks, and what the sector's maturation means for CFOs and investors.

+4 sources across the wider coverage universe

Crypto treasury firms pivot to dilutive preferreds and PIPEs as falling prices choke off easy ATM raises2026-05

Crypto treasury firms pivot to dilutive preferreds and PIPEs as falling prices choke off easy ATM raises2026-05 Boyaa Interactive, Asia's third-largest corporate BTC holder, proposes $70M crypto treasury mandate earmarked mainly for Bitcoin2026-04

Boyaa Interactive, Asia's third-largest corporate BTC holder, proposes $70M crypto treasury mandate earmarked mainly for Bitcoin2026-04 Sono Group abandons core solar business for crypto treasury gamble2026-03

Sono Group abandons core solar business for crypto treasury gamble2026-03 Treasure Global launches ethereum-based digital asset treasury with BitGo as licensed custody provider.2026-05

Treasure Global launches ethereum-based digital asset treasury with BitGo as licensed custody provider.2026-05 MSCI will not exclude digital asset treasury companies from indexes2026-01

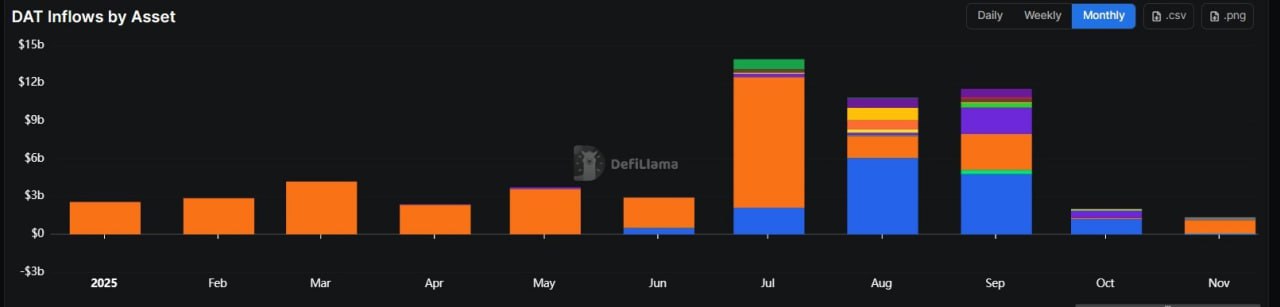

MSCI will not exclude digital asset treasury companies from indexes2026-01 Digital asset treasury inflows plunged to $1.32B in November the weakest month of 2025 as the corporate treasury boom cools, with Bitcoin firms driving $1.06B of the total while Ether treasuries slipped into $37M of outflows despite continued BitMine accumulation2025-12

Digital asset treasury inflows plunged to $1.32B in November the weakest month of 2025 as the corporate treasury boom cools, with Bitcoin firms driving $1.06B of the total while Ether treasuries slipped into $37M of outflows despite continued BitMine accumulation2025-12

A corporate entity that holds cryptocurrency—most commonly Bitcoin or Ethereum—as a primary or significant balance-sheet asset, rather than as a speculative side position, is known as a digital asset treasury (DAT) company.

What Makes a Company a Digital Asset Treasury

The defining characteristic is intentionality. A conventional public company might accumulate some Bitcoin as a hedge against dollar inflation; a digital asset treasury company structures its entire financial identity around that accumulation. The treasury asset is not incidental—it is the product.

The model was popularized at scale by Strategy (formerly MicroStrategy), which began purchasing Bitcoin in August 2020 and by mid-2026 held well over 500,000 BTC on its balance sheet. Strategy's approach established the template: raise capital through equity offerings (at-the-market, or ATM, programs), convertible notes, and preferred shares, then deploy proceeds into Bitcoin continuously. The goal is to increase "BTC per share" over time, giving equity holders indirect, leveraged exposure to Bitcoin's price appreciation without the operational complexity of running a crypto exchange or mining operation.

This structure has since been replicated across dozens of companies. Some are purpose-built shells launched specifically to hold crypto. Others are operating businesses—a rideshare platform here, a gaming company there—that have pivoted their corporate identity around a digital asset mandate.

Crypto treasury firms pivot to dilutive preferreds and PIPEs as falling prices choke off easy ATM raises

With stock prices no longer comfortably above mNAV, crypto treasury firms are turning to riskier capital structures — PIPEs, convertibles, perpetual preferreds — to keep buying coins. Strategy alone issued $7B in preferreds last year (a third of all Wall Street preferred raises), while Metaplanet recently pulled in $255M via warrant-tied share placements with mNAV exercise clauses. The problem: PIPE-backed names like Nakamoto and Strive are already trading below their issuance prices with mNAV under 1.0, and CryptoQuant warns of potential 50% downside as the entire accretive-issuance playbook breaks down.

Readers' clicks reveal they are treating Digital Asset Treasury Companies not as an investment opportunity but as a systemic risk story — the dominant pull is regulatory capture and structural fragility (debt structure, equity premiums, bear market survivability), not upside from crypto accumulation.

The Capital-Raising Machine

The mechanics matter because they expose the model's core tension. DAT companies depend on a virtuous cycle: rising asset prices inflate net asset value (NAV), which supports premium equity valuations, which enables dilutive capital raises at prices above NAV, which fund further purchases, which theoretically support prices further.

ATM programs are the workhorse of this cycle. A company registers millions of shares with the SEC and sells them continuously into the market at prevailing prices, funneling proceeds directly into crypto buys. When Bitcoin or Ethereum prices are rising and investor appetite is high, ATMs are extraordinarily efficient—low cost, no roadshow, continuous.

When prices fall, the cycle reverses. Equity premiums to NAV compress or invert, ATM raises become dilutive at unfavorable prices, and companies must turn to more expensive instruments. Recent coverage shows DAT firms pivoting to dilutive preferred shares and private investments in public equity (PIPEs) as falling crypto prices choke off easy ATM access. Preferred shares carry fixed dividends or coupon obligations, layering fixed-income pressure onto what is already a volatile asset base. This is where leverage risk accumulates quietly.

Analysts at Keyrock have identified roughly a $5.6 billion gap in idle corporate crypto treasury capital—assets sitting undeployed in custody without generating yield—which they flag as a structural inefficiency that also creates latent debt-service risk if borrowed capital funded the initial purchases.

Bitcoin vs. Ethereum: Two Accumulation Tracks

Bitcoin has dominated the DAT landscape since Strategy set the precedent, but Ethereum-focused treasuries have emerged as a distinct category.

Bitcoin track: Strategy remains the largest corporate BTC holder globally. Asia has its own emerging cohort: Boyaa Interactive, the Hong Kong-listed gaming firm, has proposed a $70 million crypto treasury mandate earmarked primarily for Bitcoin, positioning itself as Asia's third-largest corporate BTC holder. South Korean firms have also entered the space, though BitMax's public denial of BTC sales amid financial pressure illustrates the volatility of that commitment.

Ethereum track: BitMine has become the most prominent Ethereum-focused DAT company, continuing to accumulate ETH even during bear-market conditions, most recently with a $41 million purchase that deepened its ETH holdings. Consensys CEO Joseph Lubin has publicly backed ETH treasury firms, calling digital asset treasuries a "profound innovation" driving long-term capital formation for the Ethereum ecosystem. Treasure Global launched an Ethereum-based digital asset treasury with BitGo as licensed custody provider, signaling that institutional-grade infrastructure is now available for ETH as well as BTC.

The choice between Bitcoin and Ethereum reflects distinct investment theses. Bitcoin treasuries emphasize store-of-value and scarcity; the asset has no cash flows, and the thesis is purely monetary. Ethereum treasuries carry an additional productive-asset argument—ETH can be staked to generate yield, and the network's usage dynamics create a deflationary supply mechanism via EIP-1559 fee burning. That said, Ethereum's price has historically been more volatile than Bitcoin relative to drawdown depth, and its regulatory classification remains contested in some jurisdictions.

Boyaa Interactive, Asia's third-largest corporate BTC holder, proposes $70M crypto treasury mandate earmarked mainly for Bitcoin

Hong Kong's Boyaa Interactive — the Web3-pivoting gaming firm — filed with HKEX on March 22 seeking shareholder approval for a 12-month mandate to spend up to $70M on crypto, with the filing specifying new capital will be mainly Bitcoin. The company already holds 4,092 BTC (Asia's third-largest corporate stack) plus 302 ETH and 7M USDT, and spent roughly $80.5M on Bitcoin between August and November 2025 — which triggered HK listing rules that require shareholder approval for the bundled purchases as a major transaction. Trades will route through licensed HK venues HashKey and OSL; the formal circular is due by April 24.

- 01Regulatory crackdown on DATCOs

The single highest-clicked headline by a wide margin was US Treasury proposed reporting regulations, and follow-on clicks on Hong Kong SFC blocking firms and Japan exchange scrutiny show readers are tracking the tightening legal perimeter around this model globally.

- 02Bear market debt structure risk

Readers engaged strongly with warnings that secured debt could zero out ETH treasury firms and that equity premiums underpinning $100B+ in holdings could collapse, signaling anxiety about leverage mechanics rather than enthusiasm for the model.

- 03Corporate pivot desperation plays

Headlines about a solar company abandoning its core business, a design firm raising $1.65B for Solana, and a real estate firm buying LINK pulled consistent clicks — readers are drawn to the spectacle of non-crypto companies betting their identity on token treasuries.

- 04DATCO market cap collapse

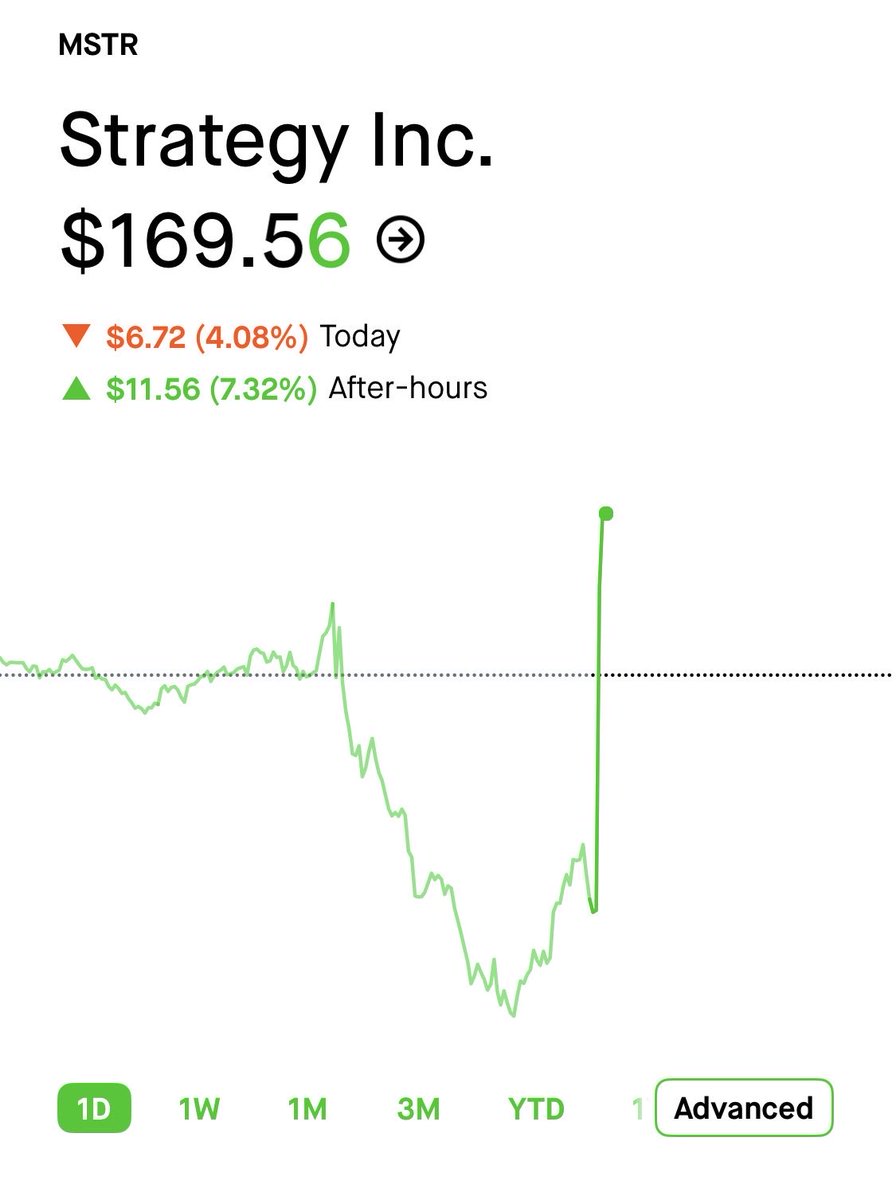

The crash from $176B to $99B combined market cap and the slide in Bitcoin treasury stocks captured readers tracking whether the MicroStrategy playbook is breaking down under selling pressure.

- 05Evolution beyond passive holding

Multiple clicked pieces examined whether DATCOs must evolve into cash-flow-generating operators or staking-native businesses to survive, with SOL Strategies' Berkshire Hathaway framing resonating as a rebuttal to the pure accumulation model.

- 06Political and celebrity-backed treasuries

Trump Jr.'s Thumzup holdings and share acquisition drew repeated reader attention, tying DATCO speculation to the broader narrative of political figures monetizing crypto treasury structures.

Who Is Launching These Vehicles

The DAT space in 2025–2026 has attracted a wide range of entrants, which itself is a signal worth examining carefully.

Purpose-built treasury companies: A16z led a $300 million funding round into a digital asset treasury focused operation, signaling that top-tier venture capital sees the model as durable enough to back at scale.

Legacy operating companies pivoting: Sono Group, a solar vehicle startup, abandoned its core business to pursue a crypto treasury strategy—an extreme example of the "pivot to treasury" trend that analysts and CFOs are increasingly scrutinizing. Ryde, a Southeast Asian ridesharing platform, has made Bitcoin and Ethereum moves that reframe its corporate identity. These pivots raise governance questions: are boards making strategic decisions or chasing narrative momentum?

SPACs and shell vehicles: Yorkville Acquisition Corp., trading as $MCGA, filed a confidential Form S-4 with the SEC to complete a business combination that would establish a digital asset treasury company focused on Cronos (CRO), with Trump Media Group CRO Strategy as the resulting entity. The appointment of Steve Gutterman as CEO and Sim Salzman as CFO ahead of an anticipated Q1 close reflects the formalization of the DAT structure even for non-BTC/ETH assets.

Enterprise finance entrants: Ripple has added crypto treasury tools specifically for enterprise finance teams, and Sygnum launched a service targeting unmanaged corporate crypto treasury assets—a segment the firm estimates at $100 billion. This infrastructure layer is a meaningful signal: institutional-grade custody, reporting, and yield tools are now available at scale, lowering the operational barrier for CFOs considering a crypto treasury mandate.

How Index Inclusion and Analyst Coverage Are Changing the Market

MSCI's decision not to exclude digital asset treasury companies from its indexes was a pivotal moment for the asset class. Index inclusion means passive fund flows—trillions of dollars managed against MSCI benchmarks—now have structural exposure to DAT equities. This normalizes the model for institutional investors who cannot or will not make active crypto bets but whose mandates no longer filter out companies with large on-balance-sheet BTC or ETH.

Equity research coverage has followed. TD Cowen named four crypto treasury stocks as buy opportunities, a signal that sell-side analysts are developing valuation frameworks for these vehicles. The standard approach is to assess the premium or discount to NAV (the market cap divided by the crypto holdings at current prices), then layer in the quality of management's capital-raising track record, the cost of debt or preferred obligations, and the pace of BTC/ETH accumulation per diluted share.

For CFOs, the considerations are more operational. Events like the April 16 gathering organized by Investments (covering "Top Digital Asset Treasury Considerations for CFOs") reflect demand for practical guidance on custody arrangements, accounting treatment under FASB's updated fair-value rules for crypto assets, tax implications of holding versus staking, and the governance disclosures required of public companies.

Sono Group abandons core solar business for crypto treasury gamble

Go where the light shine 😅

- 2023-10regulatory

US Treasury / IRS propose digital asset transaction reporting regulations

- 2023-11regulatory

IRS extends public comment deadline to November 13, 2023

- 2025-11milestone

DATCO treasury inflows hit 2025 low of $1.32B; Ether treasuries post $37M net outflows

- 2025-12regulatory

MSCI confirms it will not exclude digital asset treasury companies from indexes

- 2026-03milestone

Combined DATCO market cap crashes from $176B to $99B amid BTC, ETH, SOL selloff

- 2026-04regulatory

Hong Kong SFC blocks five companies from adopting digital asset treasury models

- 2026-05launch

Forward Industries raises $1.65B to launch Solana treasury; shares surge 128% pre-market

- 2026-06regulatory

Japan Exchange Group begins review of stricter listing rules for crypto-treasury public firms

The Risks That Practitioners Are Naming

Competent DAT coverage cannot ignore the structural risks that have become visible as the sector matures.

Leverage and credit risk: Digital credit—structured debt instruments used to fund crypto purchases—can mask dangerous leverage risks when the denominator (crypto price) falls faster than the numerator (asset value) can recover. Companies that issued convertible notes or preferred shares at high prices must service those obligations regardless of where BTC or ETH trades.

Dilution dynamics: The ATM model works in rising markets. In flat or declining markets, repeated equity issuance to fund purchases that don't appreciate transfers value from long-term shareholders to new buyers. The pivot to preferreds and PIPEs signals that some companies have exhausted their ATM runway at acceptable prices.

Operational legitimacy questions: The "move fast and break things" ethos that is acceptable for software UI is genuinely dangerous for corporate treasury management. Poor controls around custody, key management, counterparty selection, or hedging can result in irreversible losses. The Crypto Treasury Strategy firm that "dropped anchor" and halted its asset oversight function mid-operation illustrates what governance failure looks like in practice.

Concentration and correlation: DAT companies are not diversified. Their equity is effectively a leveraged call option on a single (or a few) crypto assets. In a broad market downturn, they will be more correlated with crypto than with the S&P 500, which makes them poor diversifiers and high-beta hedges.

Inflow slowdown: Digital asset treasury inflows slumped to $1.32 billion in November 2025, the weakest month of that year. Bitcoin firms drove $1.06 billion of that total, while Ether treasuries slipped into $37 million of outflows. The corporate treasury boom is cooling from its 2024 peak, and analysts at several firms are predicting consolidation among DAT companies in 2026 as the weaker vehicles face capital pressure.

What "Actively Value-Creating" Looks Like in Practice

Critics of the pure holding model argue that passive token accumulation is not, on its own, a sustainable business. The more sophisticated argument—increasingly made by operators in the space—is that DAT companies must evolve from holding shells into entities that actively compound their crypto assets.

In practice this means: staking ETH for protocol-level yield, participating in governance, deploying treasury assets into DeFi yield strategies with appropriate risk controls, using crypto collateral to access credit efficiently, and potentially acquiring operational businesses that generate crypto cash flows. The fix-it-men analogy—companies that identify undervalued crypto assets, improve their operational context, and compound returns—represents the maturation thesis for the sector.

This evolution requires custody infrastructure (BitGo, Sygnum, and others are building for this), legal clarity on staking income treatment, and management teams with both capital markets experience and on-chain operational competency. Few existing DAT companies have all three.

- RegulatoryHigh

US Treasury proposed mandatory transaction reporting, Hong Kong SFC has already blocked five DATCO applicants citing inflated valuations, and Japan's exchange regulator is drafting stricter listing rules for crypto-holding public companies.

- Market / Equity PremiumHigh

Galaxy Digital warned that the entire $100B+ DATCO sector is structurally dependent on ever-rising equity premiums over net asset value; a sustained crypto drawdown could compress premiums to zero, destroying the capital-raise flywheel.

- Leverage / Debt StructureHigh

Secured debt against volatile crypto collateral was identified as an existential threat in a bear market, with industry participants explicitly urging a shift to unsecured instruments to reduce forced-liquidation risk.

- LiquidityMedium

As ATM equity raises dried up under falling token prices, DATCO firms pivoted to dilutive preferred shares and PIPE deals — more expensive, less flexible capital that signals deteriorating market access rather than balance sheet strength.

- Index Inclusion / Institutional AccessMedium

S&P 500 rejected Strategy (formerly MicroStrategy) despite index eligibility, and JPMorgan flagged that other index providers may follow, constraining passive capital inflows that have been a key demand driver for DATCO equities.

- Business Model ViabilityMedium

Analysts drawing dotcom-era parallels warned that most DATCOs lack cash-flow generation and will fail in a downturn, while the firms that survive will need to operate as active asset managers rather than passive token warehouses.

Outlook

The digital asset treasury sector is moving through an early consolidation phase. The easiest capital—ATM programs at NAV premiums in rising markets—is less available than it was in 2024. Companies that built durable capital structures with low-cost debt, genuine operational differentiation, and management teams capable of active asset management are likely to emerge as the durable players. Those that launched as narrative vehicles with thin capitalization and no plan beyond price appreciation will face difficult choices as bear-market pressures mount.

Institutional infrastructure—index inclusion, analyst coverage, regulated custody, enterprise treasury tooling—is now sufficiently mature that the question is no longer whether large organizations can hold digital assets. It is whether specific DAT equity structures offer superior risk-adjusted exposure compared with holding the underlying asset directly. That is a live question with no settled answer, and it will define the sector's trajectory through the remainder of the decade.

Latest Digital Asset Treasury news

Crypto treasury firms pivot to dilutive preferreds and PIPEs as falling prices choke off easy ATM raisesBoyaa Interactive, Asia's third-largest corporate BTC holder, proposes $70M crypto treasury mandate earmarked mainly for BitcoinSono Group abandons core solar business for crypto treasury gambleTreasure Global launches ethereum-based digital asset treasury with BitGo as licensed custody provider.MSCI will not exclude digital asset treasury companies from indexesDigital asset treasury inflows plunged to $1.32B in November the weakest month of 2025 as the corporate treasury boom cools, with Bitcoin firms driving $1.06B of the total while Ether treasuries slipped into $37M of outflows despite continued BitMine accumulationCommunity notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…