Michael Saylor is Strategy's executive chairman and architect of its $60B Bitcoin treasury model — a capital-markets flywheel involving equity, preferred stock, and convertible debt that has made the firm crypto's most debated public company.

+16 sources across the wider coverage universe

Strategy is repurchasing $1.5B in 0% convertible notes as Michael Saylor’s bitcoin treasury giant moves to reduce debt and gradually shift toward equity financing2026-05

Strategy is repurchasing $1.5B in 0% convertible notes as Michael Saylor’s bitcoin treasury giant moves to reduce debt and gradually shift toward equity financing2026-05 Strategy faces criticism after Arca labels Saylor's AI-driven explanation for bitcoin's decline as 'nonsense,' pointing instead to the firm's reported 32 BTC sale as a key catalyst2026-06

Strategy faces criticism after Arca labels Saylor's AI-driven explanation for bitcoin's decline as 'nonsense,' pointing instead to the firm's reported 32 BTC sale as a key catalyst2026-06 Strategy halts weekly Bitcoin buys as Michael Saylor signals pause ahead of Q1 earnings, with Wall Street forecasting deeper losses tied to mark-to-market BTC accounting2026-05

Strategy halts weekly Bitcoin buys as Michael Saylor signals pause ahead of Q1 earnings, with Wall Street forecasting deeper losses tied to mark-to-market BTC accounting2026-05 Saylor teases Strategy BTC buy while 80% retail STRC holders face June 8 dividend vote2026-05

Saylor teases Strategy BTC buy while 80% retail STRC holders face June 8 dividend vote2026-05 Saylor says Strategy may sell BTC from its $65B stack to prove Bitcoin remains a usable asset2026-05

Saylor says Strategy may sell BTC from its $65B stack to prove Bitcoin remains a usable asset2026-05 Saylor signals more Bitcoin buying as Strategy's 761K BTC stack sits 10% underwater2026-03

Saylor signals more Bitcoin buying as Strategy's 761K BTC stack sits 10% underwater2026-03

I have enough from the provided coverage and my training knowledge to write the article without additional web research.

Michael Saylor is the executive chairman and co-founder of Strategy (formerly MicroStrategy), the Nasdaq-listed business-intelligence firm that became the world's largest corporate holder of Bitcoin and the central figure in institutional BTC treasury adoption.

Who Is Michael Saylor?

Born in 1965 and educated at MIT, Saylor founded MicroStrategy in 1989 and built it into a data analytics company. For two decades the firm operated in relative obscurity. That changed in August 2020, when Saylor announced that MicroStrategy had converted its entire $250 million cash reserve into Bitcoin, calling the dollar "a melting ice cube." The move was unprecedented for a public company and made Saylor the most recognizable corporate evangelist for Bitcoin globally.

In 2022 MicroStrategy rebranded its operating identity around its Bitcoin holdings; by 2024 the holding company was formally renamed Strategy, signaling that Bitcoin accumulation—not business intelligence—was now the primary corporate mission.

Michael Saylor signals another bitcoin buy as Strategy sits about $13 billion underwater

$335.5M of ATM issuance for $34.9M of BTC is a very different machine than the old infinite-buy meme. The marginal buyer is now underwriting STRC at distressed yields, a $1.4B USD reserve, and common dilution before they get exposure to the 847,363 BTC stack. BTC still gets a Saylor bid, but it now comes wrapped in credit-market fragility, and that reflexivity cuts both ways when MSTR trades like a funding vehicle instead of spot beta.

Readers click Saylor content as a real-time buy-signal feed — 'is he buying next?' consistently outperforms policy analysis or price predictions — revealing that the market has fully internalized him as a leading indicator, not merely a commentator.

The Bitcoin Treasury Playbook

Strategy's accumulation model is built around a capital markets loop that Saylor calls the "Bitcoin flywheel." The mechanics are straightforward in outline, if aggressive in execution:

1. Raise capital via equity offerings (at-the-market, or ATM), convertible notes, and preferred stock. 2. Deploy proceeds into Bitcoin purchases, increasing BTC-per-share. 3. Use rising MSTR stock price (which trades at a premium to underlying BTC net asset value) to raise further capital on favorable terms. 4. Repeat, growing both the Bitcoin stack and the narrative of a self-reinforcing "digital capital" machine.

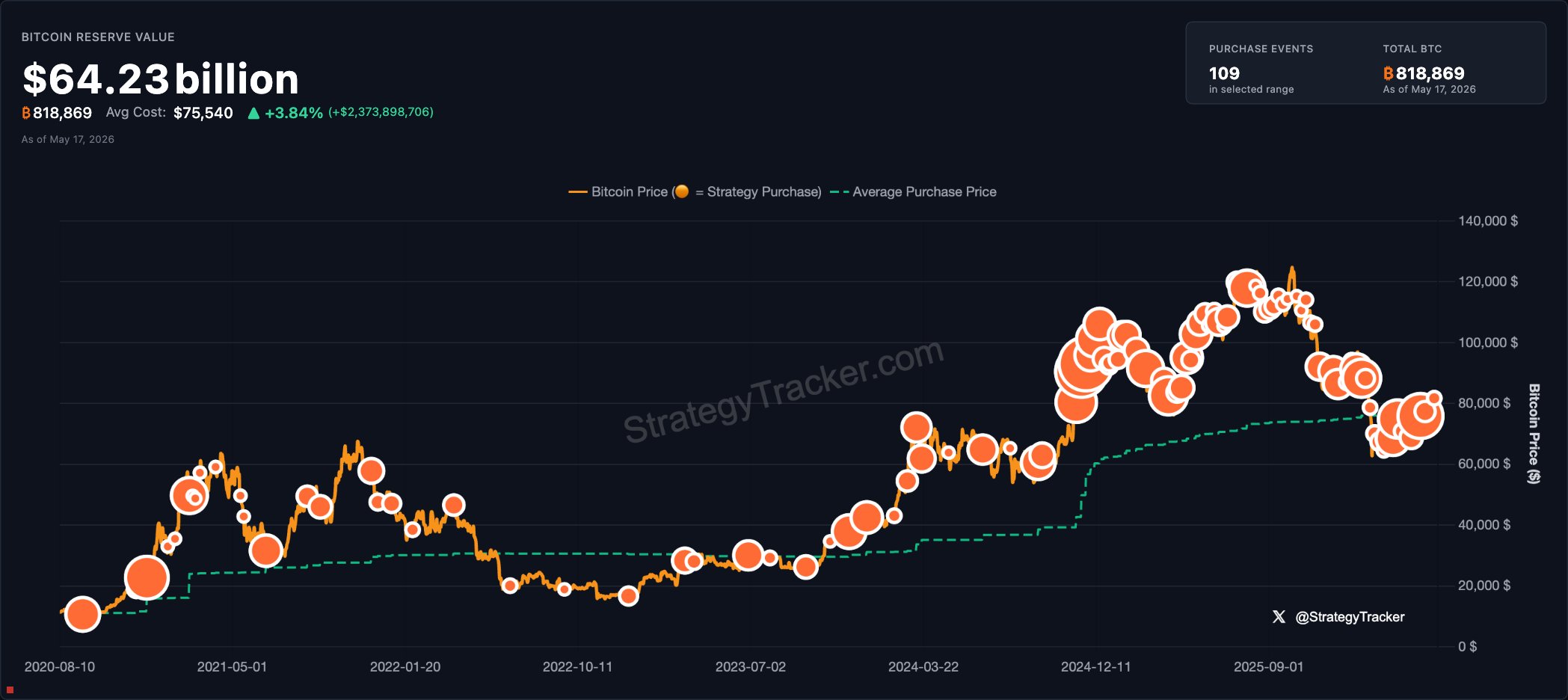

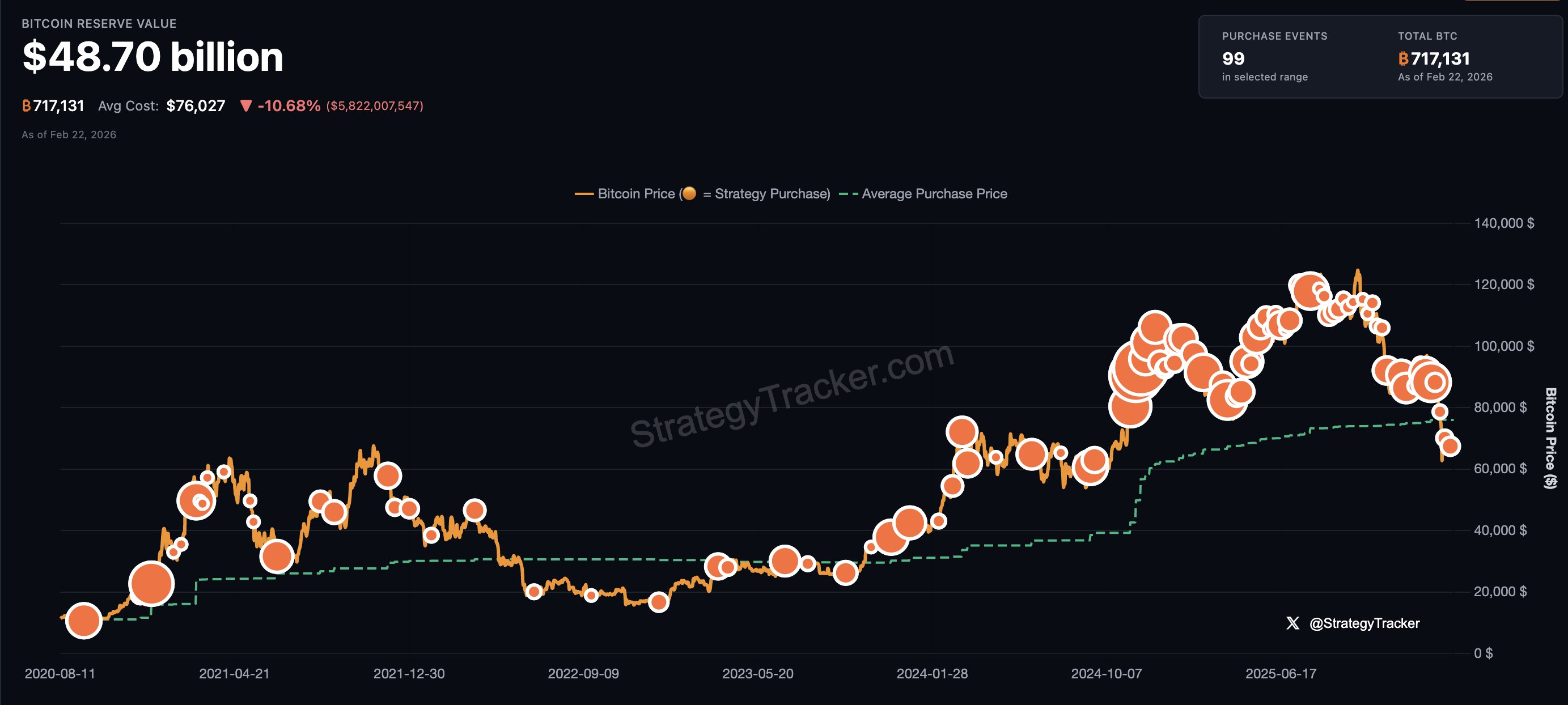

As of mid-2026, Strategy holds approximately 846,842 BTC—roughly 4% of Bitcoin's total capped supply of 21 million coins—accumulated at an aggregate cost of around $60 billion. The sheer scale makes Strategy's balance sheet more correlated to Bitcoin price than to any operating business metric.

Saylor frames this accumulation through a proprietary metric he calls CEBE BPS (Cumulative Earnings Before Earnings, per share), which he argues is a more conservative risk-adjusted measure for Bitcoin treasury firms than traditional leverage ratios. Critics note that standard metrics—debt-to-equity, interest coverage—tell a less flattering story, particularly during prolonged Bitcoin bear markets.

The 2022 Near-Miss and Its Lessons

The model's structural risk came into sharp focus during the 2022 crypto bear market. When Bitcoin fell to approximately $16,000, Strategy was carrying billions in convertible debt and faced collateral calls on a secured loan backed partly by its Bitcoin holdings. Saylor later acknowledged the episode publicly, describing the experience as a wake-up call about the dangers of leverage concentrated in a single volatile asset.

The firm survived—partly because Bitcoin recovered before forced liquidation became unavoidable, and partly because it had retained enough unencumbered BTC to absorb margin requirements. The episode hardened Saylor's conviction rather than moderating it: he has since argued that the 2022 crisis demonstrated Bitcoin's resilience relative to traditional financial assets. Whether that reasoning satisfies credit analysts is a separate question; the underlying leverage structure has grown substantially since.

- 01Next purchase timing signals

Readers treat Saylor's public hints and cryptic posts as actionable market intelligence, making every 'signal' headline a trigger for speculation about BTC price movement.

- 02Leverage model systemic risk

Multiple high-click headlines probe whether the preferred-stock/debt flywheel survives a downturn, framing Strategy as a single point of failure for corporate BTC exposure.

- 03Institutional Bitcoin evangelism

His pitches to Microsoft's board and the Bitcoin Policy Institute position him as the primary ambassador converting legacy capital markets, drawing readers who track corporate adoption.

- 04Community conflict and orthodoxy battles

Attacks on Bitcoin anarchists and dismissal of self-custody drew clicks because they expose a philosophical split between Saylor's institutionalist vision and cypherpunk foundations.

- 05Deepfake and AI scam proliferation

The highest-clicked headline shows readers are alarmed that Saylor's brand is the most-impersonated surface for AI-generated Bitcoin fraud, making him an involuntary scam vector.

- 06DeFi clones of the Strategy model

Protocols reimagining the MSTR treasury playbook onchain for ETH attracted readers curious whether the leverage-to-hold model can be permissionlessly replicated outside equities.

STRC and the Preferred Stock Controversy

Strategy's capital-raising toolkit expanded in 2026 with the launch of STRC, a perpetual preferred stock designed to pay a fixed dividend and offer investors a "safer" entry into the Strategy ecosystem compared to volatile MSTR common equity. Saylor disclosed that he used AI tools to help design the instrument—a detail that drew both curiosity and criticism.

The market's verdict has been cool. STRC, intended to trade near its $100 par value, was changing hands at roughly $87 as of mid-2026, approximately 13% below par. The discount signals that yield-seeking investors are pricing in meaningful risk: either that dividends could be strained by a sustained BTC decline, or that the preferred structure ranks too low in the capital stack to offer the safety its design implies.

Bitcoin Policy UK's CEO publicly called Saylor's promotion of STRC "dishonest," arguing that retail investors may not fully appreciate the instrument's subordination to senior creditors. The criticism reflects a broader concern: as Strategy layers ever more complex capital structures atop a single-asset Bitcoin position, the distance between headline yield and actual risk-adjusted return grows harder to communicate accurately.

Saylor vs. Ethereum: A Deliberate Positioning

Saylor has been a consistent and increasingly pointed critic of Ethereum and its yield model. At Bitcoin Corporate Day in June 2026, he argued that investors have "lost confidence in Ethereum," pointing to Bitcoin's rising market dominance—which, excluding stablecoins, he said had climbed from roughly 41% in 2021 to significantly higher by mid-2026.

His argument against Ethereum-style yield deserves examination on its own terms, separate from obvious competitive incentives. Saylor's case is that Bitcoin's lack of native yield is a feature rather than a bug: yield in proof-of-stake systems introduces inflation, counterparty risk, and regulatory uncertainty. Bitcoin's scarcity, he argues, derives precisely from its refusal to dilute holders through issuance.

Critics counter that this framing conveniently sidesteps the fact that Strategy itself dilutes common shareholders aggressively through ATM offerings to fund additional BTC purchases. Jack Mallers and Saylor debated this directly, with Saylor arguing that issuing equity to buy Bitcoin is non-dilutive because shareholders receive tangible assets in return. Mallers challenged whether the premium at which MSTR trades to NAV makes the math work the way Saylor describes. The debate remains live.

- 2020-08milestone

MicroStrategy makes first corporate Bitcoin purchase

- 2024-11milestone

Saylor presents Bitcoin treasury case to Microsoft board

- 2025-02milestone

MicroStrategy rebrands to Strategy, signals BTC-first identity

- 2025-04governance

Vitalik publicly criticizes Saylor's bank-custody advocacy

- 2025-07milestone

Strategy launches largest single-day BTC haul since July 2025 program

- 2026-01milestone

Strategy initiates quantum-security program for Bitcoin holdings

- 2026-03regulatory

Treasury signals easing of CAMT unrealized-gains rule affecting Strategy

- 2026-06milestone

Strategy raises €620M via upsized preferred stock to fund further BTC purchases

The AI Summer Narrative and Capital Competition

In June 2026, Saylor offered a new macro frame for Bitcoin's short-term price pressure: what he called an "AI summer." Speaking with commentator Natalie Brunell, he argued that Wall Street is currently prioritizing AI data center financing—citing roughly $400 billion in pending capital raises by OpenAI, Google, SpaceX, and similar firms—over Bitcoin allocation. In his framing, this is a temporary diversion of institutional capital, not a structural shift.

The explanation drew skepticism. Investment firm Arca called it "nonsense," noting that Strategy's own brief sale of 32 BTC—its first BTC sale since 2022—was a more plausible contributor to short-term market sentiment than macroeconomic capital flows. The back-and-forth illustrates a recurring dynamic: Saylor commands enough market attention that his public statements themselves move prices, but that influence cuts both ways when the narrative appears self-serving.

Strategy moved quickly to reassert its buying posture, purchasing 1,550 BTC for approximately $101 million shortly after the sale, followed by another 1,587 BTC for $100 million, bringing total holdings above 846,000 BTC. The oscillation—sell, signal, buy—drew renewed scrutiny of whether such moves are operationally driven or strategically timed communications.

How the Market Prices Strategy

MSTR's persistent premium to its Bitcoin NAV is both the enabler and the achilles heel of the flywheel. When MSTR trades at 1.5–2× NAV, new equity issuances are accretive: each dollar raised buys more Bitcoin per share than the dilution cost. When the premium compresses—as it has during risk-off periods—the flywheel slows, and the cost of carry on outstanding debt becomes comparatively more painful.

This dynamic has prompted debate about whether MSTR is a leveraged Bitcoin ETF (with management fees embedded in the premium), a financial innovation, or a structure that transfers risk asymmetrically onto retail shareholders and preferred stock holders while Saylor and institutional insiders retain the upside. The honest answer is that it contains elements of all three, and the relative weight depends on where Bitcoin's price is when you check.

- Market / ReflexivityHigh

Strategy's model requires perpetual BTC appreciation to service dilutive preferred-stock issuance; a sustained drawdown compresses mNAV and cuts off the capital raise flywheel entirely.

- Liquidity / Capital StructureHigh

Stacked preferred-share tranches (including STRC and €620M offerings) create layered redemption claims ahead of common equity; in a stress scenario, BTC liquidation pressure could be forced and disorderly.

- RegulatoryMedium

The Biden-era CAMT unrealized-gains tax briefly threatened billions in phantom tax liability on BTC holdings, demonstrating that accounting-rule changes remain a live legislative risk for corporate treasury strategies.

- CentralizationMedium

Strategy's position as the world's largest single corporate BTC holder means its forced selling or insolvency would constitute a structurally significant supply shock, concentrating systemic risk in one balance sheet.

- Reputational / Scam SurfaceMedium

Saylor's public profile is the most-cloned identity for AI deepfake Bitcoin doubling scams, with his team manually removing ~80 videos per day, creating ongoing brand-damage and retail-investor harm independent of Strategy's fundamentals.

- Governance / Custody PhilosophyLow

Saylor's endorsement of big-bank BTC custody and dismissal of self-custody drew direct criticism from Vitalik Buterin as regulatory capture, creating a soft governance risk around whose values guide institutional BTC adoption norms.

Regulatory and Ethical Scrutiny

Saylor's dual roles—as Strategy's executive chairman and as arguably Bitcoin's most prominent evangelist—create tensions that regulators and commentators have begun to examine more carefully. His promotion of STRC to retail investors, his public Bitcoin price commentary, and his position as the operator of the world's largest corporate BTC hoard mean that his statements have material market consequences.

The Bitcoin Policy UK criticism of STRC promotion as "dishonest" reflects a concern that Saylor's public persona as a Bitcoin educator and his commercial interest in selling Strategy financial products to retail investors have become difficult to disentangle. This is not a resolved question; it is an active area of reputational and potentially regulatory attention.

Outlook

Strategy's trajectory depends heavily on three variables: Bitcoin's price, the cost of capital in broader markets, and the durability of MSTR's premium to NAV. Saylor has indicated that capital could flow back into Bitcoin toward year-end 2026 as the AI infrastructure financing cycle matures, and he has signaled continued accumulation appetite.

The preferred stock overhang—STRC trading below par, dividends as a cash obligation, and an increasingly layered capital structure—introduces a complexity that the simple "buy Bitcoin forever" narrative does not fully address. As Strategy grows from a software company into something closer to a leveraged Bitcoin closed-end fund with multiple share classes, the risks and rewards become correspondingly harder to describe in a single sentence. That complexity, more than any single trade, is the story to watch.

Latest Saylor news

Community notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…