Deep explainer on Nasdaq’s structure, tech bias, and evolving role in crypto—from bitcoin ETFs and crypto‑linked equities to tokenized collateral, RWAs, and DeFi perps tied to QQQ—framed for digital asset investors and traders.

+27 sources across the wider coverage universe

Nakamoto proposes reverse stock split to stave off Nasdaq delisting after 99% share price plunge2026-04

Nakamoto proposes reverse stock split to stave off Nasdaq delisting after 99% share price plunge2026-04 European asset manager CoinShares begins U.S. push after Nasdaq listing, managing $6B+ AUM and aiming to compete with Wall Street giants in crypto ETF market2026-04

European asset manager CoinShares begins U.S. push after Nasdaq listing, managing $6B+ AUM and aiming to compete with Wall Street giants in crypto ETF market2026-04 Evernorth adds OpenAI Foundation CFO to board ahead of Nasdaq listing, strengthening XRP treasury play with AI and institutional finance expertise2026-05

Evernorth adds OpenAI Foundation CFO to board ahead of Nasdaq listing, strengthening XRP treasury play with AI and institutional finance expertise2026-05 Safello lists staked TAO ETP on Nasdaq Stockholm with ~18% annual yield, first for Nordic investors2026-03

Safello lists staked TAO ETP on Nasdaq Stockholm with ~18% annual yield, first for Nordic investors2026-03 Nasdaq and Talos partner to unlock $35B in trapped institutional collateral via tokenization2026-03

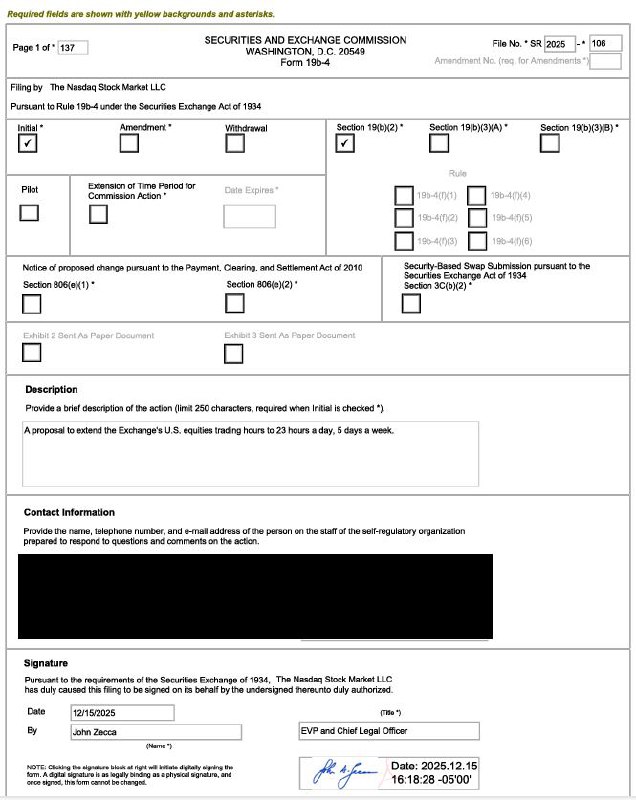

Nasdaq and Talos partner to unlock $35B in trapped institutional collateral via tokenization2026-03 Nasdaq, home of Coinbase, Strategy stocks, seeks 23-hour trading amid investor demand. Crypto's 24/7 trading has influenced investor expectations, with Nasdaq acknowledging that many of its clients are already active overnight.2025-12

Nasdaq, home of Coinbase, Strategy stocks, seeks 23-hour trading amid investor demand. Crypto's 24/7 trading has influenced investor expectations, with Nasdaq acknowledging that many of its clients are already active overnight.2025-12

Nasdaq and Crypto: How a Tech Exchange Became a Gateway to Digital Assets

A fully electronic U.S. stock exchange, the Nasdaq Stock Market is the world’s second‑largest equity marketplace by listed market capitalization and the primary home for many of the world’s leading technology companies. For crypto investors, it has become the key public‑market venue where digital asset exposure, bitcoin ETFs, tokenization initiatives, and crypto‑adjacent companies intersect with traditional finance.

Origins and Role of Nasdaq in Global Markets

From dealer screens to a fully electronic marketplace

The Nasdaq Stock Market began life in 1971 as the National Association of Securities Dealers Automated Quotations, an electronic quotation system designed to bring transparency and automation to what had been a fragmented over‑the‑counter dealer market. Unlike the New York Stock Exchange’s historic floor‑based open‑outcry model, Nasdaq was conceived from the outset as a screen‑based network, with dealers posting firm two‑sided quotes and competing for order flow through terminals rather than shouting across a trading pit. That design choice established the exchange as a pioneer of electronic trading and set the template for the limit‑order books and matching engines that now dominate equity and derivatives venues globally. Over the following decades, regulatory reforms and technology upgrades gradually transformed Nasdaq from a quote display system into a fully fledged national securities exchange under U.S. law, with its own listing standards, surveillance framework, and order‑matching infrastructure.

Today, Nasdaq is recognized as the first fully electronic stock market and remains one of the most active trading venues in the United States by volume. It is operated by Nasdaq, Inc., a for‑profit public company that also owns a range of market technology, data, and index businesses, many of which are increasingly entangled with digital asset markets. The exchange is based in Manhattan’s financial district, but its data centers and matching engines are distributed across several U.S. locations to provide redundancy and low‑latency connectivity for a global trading community. From a crypto investor’s perspective, this history matters because the same engineering culture that built Nasdaq’s electronic order books now underpins its push into digital asset market infrastructure, tokenized collateral, and surveillance technology for crypto venues.

A tech‑heavy exchange with global reach

Nasdaq has long been synonymous with growth‑oriented, innovation‑driven companies, especially from the technology, biotechnology, and communications sectors. Major global firms across software, semiconductors, internet services, and consumer technology historically chose Nasdaq as their primary listing venue, reinforcing its reputation as the “tech exchange” and shaping the factor exposures embedded in its flagship indexes like the Nasdaq‑100. This tech bias has important implications for crypto markets because bitcoin and other digital assets often trade as high‑beta expressions of the same risk‑on macro themes that drive large‑cap technology stocks.

Despite its U.S. base, Nasdaq has always sought international listings, becoming a key venue for foreign issuers seeking access to U.S. capital. The exchange lists companies from dozens of jurisdictions, with China and Israel standing out as two of the largest sources of foreign‑domiciled issuers. For crypto investors, that global footprint means that many of the firms building trading infrastructure, mining operations, or blockchain‑based platforms worldwide—whether in Asia, Europe, or the Middle East—may eventually seek a Nasdaq listing to tap U.S. liquidity and investor demand. The recent decision by European digital asset manager CoinShares to list in the United States under the ticker CSHR illustrates how non‑U.S. crypto firms view Nasdaq as the natural venue for scaling their access to American institutions and retail investors.

Why crypto investors care about Nasdaq

For a crypto‑focused audience, Nasdaq matters on three overlapping levels: as a barometer of global risk sentiment, as the main public market gateway for crypto‑related companies and bitcoin ETFs, and as an increasingly active player in tokenization and digital asset infrastructure. First, because of its concentration in technology, communications, and consumer growth stocks, the Nasdaq complex (especially the Nasdaq‑100 index) has become one of the cleanest representations of “risk‑on” appetite in global markets. Bitcoin’s returns have shown a persistently high positive correlation with the Nasdaq‑100 in recent years, meaning that major moves in tech equities often coincide with similar directional moves in BTC and other digital assets.

Second, a growing share of crypto exposure reachable through regulated brokers now comes in the form of Nasdaq‑listed instruments: equities in firms like Coinbase, MicroStrategy, or crypto‑mining companies; spot bitcoin exchange‑traded funds such as iShares’ IBIT; and increasingly, structured products and options written on those securities. For investors who cannot hold tokens directly—whether due to mandate restrictions, custodial constraints, or regulatory limits—these Nasdaq vehicles have become crucial on‑ramps into digital assets. Third, Nasdaq is actively positioning itself within the broader digital asset ecosystem, from tokenized collateral partnerships to surveillance tools for crypto markets, suggesting that the boundary between on‑chain and listed markets will continue to blur.

Nakamoto proposes reverse stock split to stave off Nasdaq delisting after 99% share price plunge

Bailey doubled the outstanding share count in February acquiring his own companies at fire-sale prices, and now asks those same diluted shareholders to approve a reverse split while keeping 10 billion authorized shares on the books. That authorized share ceiling post-consolidation leaves room to issue ~14x the post-split float — so anyone voting yes on May 8 is basically handing him a blank check for future dilution. Meanwhile they already liquidated 284 BTC in March just to keep lights on, which kind of kills the "treasury company" thesis when you're a forced seller at the worst time. Chanos had it right with "Theater of the Absurd."

Readers are tracking NASDAQ as a two-way legitimacy bridge: crypto companies racing to list there for institutional credibility while NASDAQ itself adopts crypto-native attributes — 24/7 trading hours, tokenized settlement, and ETF rule rewrites — revealing that the influence now runs in both directions.↗

Market Structure: How Trading on Nasdaq Actually Works

Order books, dealers, and screen‑based trading

Nasdaq operates as an electronic limit‑order market in which participants submit buy and sell orders that are matched according to price‑time priority within centralized order books for each listed security. In contrast to a specialist model, Nasdaq supports multiple competing market makers who are obligated to provide continuous two‑sided quotes in many securities and who help stabilize liquidity during volatile conditions. The U.S. Securities and Exchange Commission’s Form 1 description of Nasdaq emphasizes that it is a “screen‑based market, operating in an efficient, highly competitive electronic trading environment,” highlighting the role of technology and competition rather than physical floor intermediaries. Orders from brokers, proprietary traders, and institutional investors flow into Nasdaq’s matching engines through low‑latency connections, where they interact with resting liquidity from both passive and algorithmic participants.

From a crypto trader’s standpoint, this structure will feel conceptually familiar. Central limit‑order books (CLOBs) are standard on centralized crypto exchanges and increasingly common in DeFi protocols that support order‑book style trading. The difference lies in the regulatory regime, data symbology, and participant base: Nasdaq operates under the U.S. national market system, integrates with consolidated market data feeds, and connects to a network of broker‑dealers that must comply with SEC and FINRA rules. Nonetheless, the microstructural dynamics—such as order‑book depth, spread behavior, and the impact of large market orders—are closely analogous to those observed on major crypto venues, making cross‑market execution strategies more portable than many newcomers assume.

Trading sessions and the clash with 24/7 crypto markets

While crypto markets trade around the clock, Nasdaq maintains defined trading sessions, with a normal continuous session from 9:30 a.m. to 4:00 p.m. Eastern Time. The exchange also supports extended‑hours sessions, with pre‑market trading from 4:00 a.m. to 9:30 a.m. and after‑hours trading from 4:00 p.m. to 8:00 p.m., during which liquidity is thinner and spreads wider than in the main session. These windows broadly match those cited by market education sources, which describe U.S. equity pre‑market trading between 4:00–9:30 a.m. ET and after‑hours trading between 4:00–8:00 p.m. ET. For crypto investors, the existence of these defined windows is crucial because many key bitcoin proxies—spot ETFs, crypto‑related equities, and Nasdaq‑based structured products—can only be traded during these periods, even while BTC and ETH trade nonstop.

The mismatch in trading hours creates familiar phenomena such as “weekend gaps,” where material news affecting digital assets breaks while U.S. equities are closed, causing sharp repricing at the next Nasdaq open. Crypto derivatives traders often attempt to anticipate these gaps by monitoring flows in perpetual futures on major centralized exchanges, which remain open when U.S. equities are shut. Conversely, pre‑market and after‑hours moves in bitcoin proxies on Nasdaq can foreshadow spot and derivatives action during overlapping time zones, especially when large institutions are rebalancing exposure using ETFs and equities rather than spot tokens.

IPOs, price discovery, and mega listings

Bringing a company to market on Nasdaq involves a multi‑step initial public offering (IPO) or direct listing process, during which underwriters work with the issuer to set an offering range, allocate shares, and orchestrate initial price discovery through a specialized opening auction. Nasdaq’s IPO listings page highlights how the exchange serves as the venue for both domestic and foreign companies across sectors, and provides investors with offering prices and subsequent performance data. Before a new listing begins trading, Nasdaq uses tools such as the Net Order Imbalance Indicator (NOII) to show the aggregated buy and sell interest at different price levels, helping underwriters and market participants gauge where supply and demand will intersect when the stock first crosses.

The recent listing of Space Exploration Technologies Corp. (SpaceX) under the ticker SPCX offers a vivid example of Nasdaq’s capacity to handle extraordinary scale. According to Nasdaq’s own coverage, the SpaceX debut raised approximately 85.7 billion U.S. dollars, setting a record for capital raised in a single public offering and placing the company’s opening market capitalization at about 2.1 trillion dollars. The stock opened at 150 dollars per share on an initial cross of roughly 58 million shares, with the exchange’s infrastructure processing unprecedented share volume without operational disruption. The transaction also leveraged a coordinated dual‑listing architecture, tapping both Nasdaq’s primary U.S. venue and Nasdaq Texas, underscoring the exchange group’s multi‑location design for resiliency and throughput. For crypto market participants accustomed to network congestion during peak NFT mints or token launches, this kind of scalable, fault‑tolerant market infrastructure is an instructive benchmark for what institutional‑grade on‑chain trading may one day resemble.

Listing standards, reverse splits, and delisting risk

Nasdaq’s value to investors depends heavily on its listing standards, which specify minimum thresholds for share price, market capitalization, shareholder equity, and ongoing disclosure. Companies that fall below these thresholds—most commonly by trading under 1 U.S. dollar per share for an extended period—risk receiving deficiency notices and ultimately being delisted from the exchange. One common tactic for restoring compliance is a reverse stock split, in which a company consolidates outstanding shares into a smaller number of higher‑priced shares without changing its overall market capitalization. The SEC has documented Nasdaq’s efforts to keep its rules aligned with federal requirements governing such corporate actions.

In a 2024 rule filing, Nasdaq proposed extending the deadline by which companies must notify the exchange of an upcoming reverse stock split from “5 business days” to “10 calendar days” before the market‑effective date. The change was designed to ensure that notice given under Nasdaq’s listing rules would also satisfy SEC Rule 10b‑17, which governs timeliness of public disclosure for distributions and other stock events. A separate business press example illustrates why these mechanics matter: a company named Nakamoto, whose share price had suffered a roughly 99% decline, announced a 1‑for‑40 reverse split, combining every 40 shares of common stock into one in an effort to regain compliance and avoid Nasdaq delisting. In practice, the reverse split raised Nakamoto’s per‑share price but did not by itself improve the company’s fundamentals, mirroring how token redenominations in crypto can change unit prices without altering underlying value.

For digital asset investors, these episodes offer a reminder that listed crypto‑adjacent equities combine both crypto‑specific risk and the familiar hazards of small‑cap equity markets, including dilutive financings, governance disputes, and compliance challenges. They also highlight why Nasdaq periodically files further rule changes with the SEC—often designated by serial numbers such as SR‑NASDAQ‑2026‑044, ‑048, ‑049, or ‑056—to refine its treatment of mergers, corporate actions, and market structure in response to evolving deal activity and technology. Although each filing is narrowly technical, together they shape the environment within which many crypto‑linked companies raise capital and maintain their listings.

The Nasdaq‑100, Invesco QQQ, and Tech Risk

Key Nasdaq benchmarks and their construction

Beyond the exchange itself, Nasdaq’s influence is deeply felt through its equity indexes, which serve as benchmarks for trillions of dollars in passive funds, derivatives, and structured products. The most widely referenced include the Nasdaq Composite, which covers nearly all Nasdaq‑listed common stocks, and the Nasdaq‑100 Index (ticker NDX), which tracks 100 of the largest non‑financial domestic and international companies listed on the exchange. The methodology document for the Nasdaq‑100 specifies that constituents are selected based on market capitalization, subject to eligibility screens, and weighted through a modified capitalization approach that caps extreme concentrations to maintain diversification. Rebalances are conducted periodically, with securities added or removed according to criteria laid out in the index rules.

This index family is critical for crypto markets because it defines the target universe for many exchange‑traded funds and derivatives that crypto traders use as macro hedges or correlation trades. When traders speak of “Nasdaq performance,” they often mean the Nasdaq‑100 rather than the broader composite, since the former is more tech‑heavy and more relevant to risk sentiment in growth assets. The sectoral tilt of the Nasdaq‑100 toward software, semiconductors, and consumer internet firms amplifies its sensitivity to interest rates, inflation expectations, and innovation cycles—macro variables that also drive risk appetites in digital assets.

Invesco QQQ: ETF wrapper for the Nasdaq‑100

The Invesco QQQ Trust (commonly referred to by its ticker, QQQ) is the flagship exchange‑traded fund tracking the Nasdaq‑100 Index. Invesco describes QQQ as a passively managed product that seeks to replicate the performance of the Nasdaq‑100, thereby offering exposure to many industry‑leading companies in a single investable instrument. Because it trades intraday on exchanges, QQQ combines the diversification benefits of an index with the flexibility of a stock, allowing investors to implement tactical views on technology and growth with relative ease. Its deep liquidity and tight spreads have made it one of the most actively traded ETFs in the world, frequently used as a proxy for U.S. tech risk both by retail traders and institutional asset managers.

For crypto investors, QQQ plays several distinct roles. First, it provides a convenient benchmark for gauging how “risk‑on” or “risk‑off” the broader tech equity complex is at any given time, information that often maps onto short‑term moves in bitcoin and other major tokens. Second, because QQQ underlies a large ecosystem of options and futures, its implied volatility surface can serve as a reference point for understanding how traditional markets price macro uncertainty relative to crypto options. Third, QQQ has increasingly become the underlying for real‑world asset (RWA) products and synthetic perps in DeFi: our newsroom has covered how Orderly Network, for example, launched a permissionless perpetual market tracking the Nasdaq‑100 via $QQQ, allowing any DEX built on its infrastructure to offer QQQ‑linked trading by tapping shared liquidity and oracles. This illustrates how a traditional ETF can become a building block both in regulated portfolios and in on‑chain derivatives.

Bitcoin–Nasdaq‑100 correlations and diversification

One of the most closely watched statistics in crypto macro is the correlation between bitcoin returns and those of the Nasdaq‑100. Nasdaq’s own options education content, highlighted by ETF Trends, noted that over a significant period the correlation between bitcoin and the Nasdaq‑100 (NDX) had reached approximately 0.805, which is quite high by cross‑asset standards. In other words, bitcoin has often behaved like a high‑beta version of a tech equity index, moving in the same direction but with larger amplitude. This empirical reality complicates the narrative of bitcoin as a pure “digital gold” safe haven, at least over short‑ to medium‑term horizons when macro risk dominates.

Academic research provides additional nuance. A study published in Physica A examined bitcoin relative to high‑performance technology stocks, finding that while bitcoin and tech equities share certain characteristics, bitcoin displayed distinct diversification properties vis‑à‑vis global stock markets. The authors reported that in U.S. markets bitcoin often acted as a hedge during bullish conditions, whereas its relationship with European and Asian markets was more mixed. In some cases, particularly when priced in Korean won, bitcoin exhibited safe‑haven‑like behavior during bearish episodes in Asian equities, though the evidence was not uniformly strong across all specifications. For a crypto portfolio manager, the key takeaway is that correlations are regime‑dependent: in tranquil or inflation‑focused regimes, bitcoin may trade like levered tech; in localized crises or currency‑specific stress, its behavior can diverge.

Comparing core Nasdaq exposures

To orient where Nasdaq fits within a crypto‑adjacent portfolio, it is useful to contrast the exchange, its index, and the QQQ ETF in structured form.

| Instrument / Entity | Type | Underlying Universe | Primary Use Case |

|---|---|---|---|

| Nasdaq Stock Market | Stock exchange | Listed equities and ETFs across sectors | Trading venue and price discovery |

| Nasdaq‑100 (NDX) | Equity index | 100 largest non‑financial Nasdaq‑listed companies | Benchmark for tech‑heavy large caps |

| Invesco QQQ | Exchange‑traded fund | Physical portfolio replicating Nasdaq‑100 index | Tradable wrapper for NDX exposure |

This framing helps clarify that when crypto traders discuss “Nasdaq correlation,” they are usually referring not to the exchange as an institution, but to indexes such as the Nasdaq‑100 and investable vehicles like QQQ that capture the performance of large‑cap growth equities.

European asset manager CoinShares begins U.S. push after Nasdaq listing, managing $6B+ AUM and aiming to compete with Wall Street giants in crypto ETF market

$6B AUM and 34% European market share, then they pull their XRP, SOL, and LTC spot ETF filings right before listing — that's Mognetti publicly conceding the single-asset fee war to BlackRock and Fidelity before it even starts. Pivoting to thematic baskets and active crypto equity strategies is the higher-margin play, but it's the same bet Grayscale is making post-GBTC conversion, and those flows haven't exactly been kind. US distribution is a completely different game from European ETP dominance — a $1.2B SPAC war chest alone won't close that gap.

- 01Crypto ETF rule filings↗

Readers closely tracked every SEC/NASDAQ filing for spot Bitcoin and Ethereum ETFs and novel digital asset listing rules, treating each amendment as a signal of regulatory trajectory.

- 02Bitcoin treasury Nasdaq listings↗

A wave of small-cap NASDAQ companies pivoting to Bitcoin treasury strategies — Strategy, Fold, Semler Scientific, ProCap — gave readers a leveraged-proxy bet on BTC within a regulated equity wrapper.

- 03Macro contagion and BTC correlation↗

The DeepSeek AI rout and tariff-driven Black Monday events showed readers that NASDAQ futures moves now function as leading indicators for crypto drawdowns, reinforcing BTC's risk-on classification.

- 0424/7 trading hours push↗

NASDAQ's proposal for near-round-the-clock trading was read as crypto culture bleeding into traditional markets, with readers recognizing their own 24/7 behavior as the forcing function.

- 05Tokenized securities and onchain NASDAQ↗

The Ondo Finance–SEC clash over NASDAQ's tokenized securities plan, and the Talos collateral tokenization deal, showed readers that the fight to bring NASDAQ-grade instruments onchain is now a live regulatory and commercial battle.

- 06Crypto-native companies IPOing on NASDAQ↗

Listings by Galaxy Digital, CoinShares, Gemini (planned), and American Bitcoin signaled that NASDAQ IPO is now the canonical legitimacy event for maturing crypto businesses.

Nasdaq as a Public Market for Crypto Exposure

Crypto‑related operating companies

Even before regulators approved spot bitcoin ETFs, public equities functioned as the primary channel through which mainstream investors gained crypto exposure via regulated accounts. Several of the most prominent crypto‑related companies are listed on Nasdaq, including centralized exchanges, software firms with large bitcoin treasuries, and miners whose revenues are tied to block rewards and transaction fees. A social‑media post from Business Insider’s finance feed, for instance, highlighted how shares of Coinbase, MicroStrategy, and Marathon Digital were all viewed as “crypto‑related” plays, with their stocks rallying alongside bitcoin as investors responded to bullish BTC price action. Each of these companies provides a different economic linkage: Coinbase as a fee‑driven exchange and custody provider, MicroStrategy as a leveraged bitcoin treasury vehicle, and Marathon as an infrastructure operator dependent on mining economics.

The performance of such equities often exhibits even higher beta to bitcoin than BTC itself, particularly in bull markets when speculative enthusiasm and risk premia compress. However, they also introduce idiosyncratic corporate risks—governance decisions, regulatory enforcement actions, and capital‑structure dynamics—that pure token exposure does not entail. For crypto investors building a multi‑asset portfolio, it is therefore crucial to distinguish between directional BTC exposure via derivatives or spot, and equity exposures whose returns blend crypto price risk with company‑specific operational and regulatory outcomes. Nasdaq’s listing and disclosure standards, enforced through periodic reporting and corporate governance requirements, provide some protection to shareholders, but they do not eliminate the volatility inherent in early‑stage or highly levered crypto‑adjacent businesses.

Digital asset managers and ETF issuers on Nasdaq

The listing of CoinShares on Nasdaq in the United States underscores how digital asset managers are using the exchange to broaden their investor base. According to the company’s press release, CoinShares—described as Europe’s largest asset manager specializing in digital assets with over 6 billion U.S. dollars in assets under management—began trading on the Nasdaq Stock Market under the ticker CSHR on 1 April 2026. The firm characterized itself as a leading global asset manager focused on digital assets, and indicated that its U.S. listing marked a significant step in competing with Wall Street incumbents in the burgeoning crypto ETF market. Coverage from ETF‑focused outlets similarly framed the debut as a SPAC‑structured merger valued around 1.2 billion dollars, positioning CoinShares as a material player in the U.S. crypto ETP landscape.

This development aligns with the broader trend of asset‑management firms seeking exchanges like Nasdaq as platforms from which to launch, list, and scale crypto‑linked products, from physically backed bitcoin ETPs to actively managed multi‑asset crypto funds. Our newsroom has reported on other Nasdaq‑listed entities moving in similar directions, such as Datavault AI (ticker DVLT) preparing to list a portfolio of meme coins and RWA tokens on a centralized crypto exchange, underscoring how traditional public companies are integrating token portfolios into their business strategies. For crypto investors, this means that the line between “crypto asset” and “listed equity” is increasingly blurred, with balance sheets and income statements reflecting direct token holdings, staking yields, and DeFi strategies.

Bitcoin spot ETFs and the rise of IBIT options

Perhaps the most transformative development for bitcoin’s integration into traditional markets has been the approval and launch of U.S. spot bitcoin ETFs, several of which list on Nasdaq. Among these, the iShares Bitcoin Trust ETF (IBIT) has rapidly grown into the world’s largest and most liquid bitcoin ETF, with Nasdaq highlighting assets under management exceeding 22 billion U.S. dollars. In 2026, the U.S. Securities and Exchange Commission approved Nasdaq’s rule filing to list options on IBIT, marking the first‑ever regulatory approval for options on a spot bitcoin ETF. Nasdaq described this as a first‑of‑its‑kind milestone that expands the toolkit available to institutional and sophisticated investors seeking to hedge or leverage their bitcoin exposure through regulated derivatives.

The significance of IBIT options is hard to overstate for a crypto‑savvy audience. Prior to their introduction, traders looking to construct options strategies on bitcoin were largely confined to offshore crypto‑derivatives venues or CME‑listed futures options, each with its own frictions and constraints. By enabling listed options directly on a spot bitcoin ETF, Nasdaq and the SEC have effectively imported a familiar equity‑options market structure into the bitcoin realm, complete with standardized contracts, margin rules, and U.S. investor protections. This development also deepens the interplay between Nasdaq’s tech‑heavy risk factors and bitcoin’s own volatility, as cross‑asset vol‑arbitrage strategies now have more instruments through which to express relative value views between IBIT, QQQ, and Nasdaq‑100 derivatives.

Corporate treasuries and on‑exchange crypto bets

Another way crypto exposure creeps into Nasdaq is through corporate treasury strategies and balance‑sheet allocations. Our newsroom has covered, for example, Forward Industries (ticker FWDI), described as a Solana‑focused treasury company backed by a large private investment in public equity (PIPE) consortium and holding several million SOL tokens on its balance sheet. Similarly, Eightco (ticker ORBS) has reported significant holdings of Worldcoin (WLD) and ether (ETH), while firms like Beeline Holdings (BLNE) have integrated blockchain technology into their core businesses, such as mortgage platforms. These cases echo the earlier example set by MicroStrategy, but extend it into other layer‑1 ecosystems and token categories.

For equity investors, such treasury strategies create a hybrid exposure that blends the operating performance of the underlying business with the mark‑to‑market swings of the token holdings. From a risk‑management perspective, Nasdaq’s disclosure framework requires these companies to detail their crypto positions and valuation methodologies in financial filings, giving investors some visibility into the extent of their digital asset leverage. However, the volatility of these holdings can still dominate valuation in stressed markets, leading to scenarios where a nominally “traditional” Nasdaq equity trades primarily as a proxy for a specific token ecosystem, whether bitcoin, Solana, or XRP. This dynamic complicates factor analysis and portfolio construction for asset managers who may inadvertently accumulate concentrated crypto exposure via baskets of tech and fintech equities.

Tokenized Collateral, RWAs, and Nasdaq’s Digital Market Strategy

The Nasdaq–Talos tokenized collateral initiative

Beyond listings and ETFs, Nasdaq is directly engaging with digital assets at the infrastructure layer. In March 2026, Nasdaq and Talos announced a partnership to connect Talos’s institutional digital asset trading platform with Nasdaq’s Calypso and Trade Surveillance systems, with the goal of creating an integrated solution for managing tokenized collateral across mainstream and digital asset markets. The joint announcement emphasized that the collaboration would enable institutions to move, monitor, and optimize tokenized forms of collateral—such as tokenized fiat, treasuries, or other digital securities—within the same risk and surveillance frameworks that govern traditional collateral management.

This initiative exemplifies the “RWA” narrative from the vantage point of a major exchange group. Rather than issuing tokens itself, Nasdaq is effectively standardizing the plumbing through which tokenized assets can be recognized as collateral within existing capital markets workflows, from margining and repo to derivatives clearing. The partnership’s integration with Nasdaq’s Trade Surveillance platform underscores an important theme: that for large institutions to accept tokenized assets at scale, they must be able to monitor them for market abuse, counterparty risk, and operational anomalies with a level of sophistication comparable to that used for equities and futures. In our newsroom’s framing, this collaboration aims to unlock tens of billions of dollars in “trapped” institutional collateral—assets that are encumbered or under‑utilized because they cannot yet flow seamlessly between traditional and digital venues.

RWAs and synthetic Nasdaq exposure in DeFi

At the same time that Nasdaq is moving into tokenized collateral from above, DeFi protocols are reaching up toward Nasdaq from below by creating synthetic exposures to Nasdaq‑linked instruments on‑chain. Orderly Network’s launch of a permissionless perpetual futures market tracking QQQ is one example: any decentralized exchange built on Orderly can now list and route orders to a perpetual swap that mirrors the performance of the Nasdaq‑100 via QQQ pricing, settled in crypto collateral. In parallel, other DeFi projects and on‑chain derivatives platforms have introduced synthetic stocks and indexes, allowing users to trade virtual representations of Nasdaq‑listed names like NVDA, GOOGL, or META on automated market makers or order‑book DEXs, sometimes marketed through campaigns such as “Trade Nasdaq stocks on‑chain with leverage.”

These synthetic RWAs typically rely on oracles to feed off‑chain prices into smart contracts, combined with overcollateralized positions in stablecoins or other crypto assets to back the notional exposure. While they do not confer the legal rights associated with actual share ownership—such as dividends or voting—they provide economic exposure to price movements, making them attractive to traders constrained from accessing offshore brokers or U.S. exchanges directly. The emergence of permissionless Nasdaq‑linked perps on protocols like Orderly or Hyperliquid, which has rolled out strategies tied to Nasdaq options, underscores the growing two‑way flow of ideas: traditional exchanges are tokenizing collateral and data, while DeFi is re‑creating traditional exposures atop crypto rails.

Synthetic dollars, public companies, and on‑chain yield

Another frontier at the intersection of Nasdaq and crypto involves synthetic dollar assets backed in part by offerings from Nasdaq‑listed entities. Our newsroom has highlighted the eSui Dollar (suiUSDe), a synthetic dollar for the Sui network issued in collaboration with Ethena and Sui Group Holdings, the latter of which carries a Nasdaq listing under ticker SUIG. While the specifics of suiUSDe’s design evolve, the basic pattern is increasingly common: a publicly listed entity provides governance, branding, or off‑chain infrastructure for a synthetic stable asset, while on‑chain protocols manage collateral, pegs, and yield strategies. This approach blends the credibility and regulatory oversight of a Nasdaq listing with the composability and transparency of DeFi.

For investors, such hybrids raise questions about how to price risk across the corporate and protocol layers. Holders of SUIG equity are exposed to the economics of the synthetic dollar program—potentially including fees, seigniorage, or liability for peg maintenance—while holders of suiUSDe are exposed to smart‑contract risk and collateral risk within Sui DeFi. Because the public company trades on Nasdaq, its disclosures and governance decisions become part of the information set that DeFi participants may need to monitor. This feedback loop, in which equity‑market events can impact on‑chain assets and vice versa, foreshadows a world in which the boundaries between corporate finance and protocol design are increasingly porous.

Institutional infrastructure: validators, multi‑sigs, and governance

Institutional actors tied to Nasdaq are also working on the raw infrastructure of blockchains themselves. The Jito Foundation’s partnership with a Nasdaq‑listed company focused on Solana infrastructure—reported in our newsroom under the ticker HSDT—highlights how public‑market firms are co‑operating with crypto foundations to operate validators and low‑latency backbone networks across Asia‑Pacific hubs like Hong Kong, Singapore, Japan, and South Korea. By committing to run validator nodes and backbone connections, such firms effectively turn block‑production and staking into part of their business model, potentially with their equity offering investors indirect exposure to staking yields and validator economics.

Similarly, features such as multi‑sig key governance for custodial arrangements, discussed in coverage of Antalpha (ticker ANTA), show how institutions are formalizing crypto‑native risk controls in ways that resonate with traditional corporate governance and audit expectations. When an exchange like Nasdaq becomes a venue where such governance‑heavy crypto infrastructure players list, the result is a more legible and regulated interface between on‑chain protocols and capital markets. For crypto‑native users, this may eventually mean that some of the infrastructure they rely on daily—validators, bridges, or custody platforms—is ultimately governed by boards, shareholder votes, and SEC‑filed proxy statements, even while the associated tokens and smart contracts remain permissionless.

Evernorth adds OpenAI Foundation CFO to board ahead of Nasdaq listing, strengthening XRP treasury play with AI and institutional finance expertise

"XRP showing interesting technicals here. Currently testing the $0.55 support level that's held since May - daily RSI at 42 suggests neither overbought nor oversold. Volume profile shows accumulation between $0.52-$0.58. Break above $0.60 with volume could target $0.68 resistance, but watch the 200DMA at $0.57 acting as dynamic resistance. Bear case: loss of $0.52 opens door to $0.48 support. This news could provide fundamental catalyst if it brings fresh institutional interest." (280 chars)

Spot Bitcoin ETF options begin trading on NASDAQ (IBIT)

MicroStrategy added to NASDAQ 100 index

DeepSeek AI shock — BTC -6%, NASDAQ futures -2.6%

CoinShares begins trading on NASDAQ after U.S. push

- 2025-04milestone

Black Monday: NASDAQ futures -6%, BTC -15%, $900M liquidated

NASDAQ and Talos partner on $35B tokenized collateral network

- 2025-06launch

Galaxy Digital begins trading on NASDAQ under ticker GLXY

NASDAQ files proposal for 23-hour near-continuous trading

Regulation, Surveillance, and the SEC–Nasdaq Relationship

Nasdaq as a national securities exchange

Under U.S. law, Nasdaq operates as a registered national securities exchange subject to oversight by the Securities and Exchange Commission. The SEC’s Form 1 for Nasdaq describes in detail the exchange’s electronic trading environment, governance, and regulatory obligations. As a self‑regulatory organization (SRO), Nasdaq bears frontline responsibility for enforcing its own listing standards, monitoring trading for market abuse, and cooperating with the SEC and FINRA on cross‑market surveillance. This dual identity—as both a for‑profit business and a quasi‑regulatory entity—gives Nasdaq considerable influence over how listed companies structure their governance and disclosures, and how member firms conduct trading.

For crypto audiences used to exchanges that are purely commercial enterprises with limited regulatory obligations, Nasdaq’s SRO status is a salient difference. It means that when a crypto‑related company lists on Nasdaq, its management not only answers to shareholders and securities regulators, but also to exchange staff tasked with enforcing rules on corporate actions, timely disclosures, and fair‑practice standards. This layered oversight is reflected in the procedural rigor around events like reverse splits, mergers, and symbol changes, where companies must coordinate with Nasdaq and provide advance notice according to specific rule‑book timelines.

Rule filings and market evolution

Nasdaq’s rulebook is not static; it evolves through a formal process of rule filings with the SEC, often designated with identifiers such as SR‑NASDAQ‑2024‑068 or SR‑NASDAQ‑2026‑044. In the 2024 filing associated with number 2024‑068, Nasdaq proposed modifications to its listing standards related to notification and disclosure of reverse stock splits, including the shift from “5 business days” to “10 calendar days” for advance notice to the exchange. The filing emphasized the need to align Nasdaq’s timing requirements with SEC Rule 10b‑17, and clarified that the rule change would not alter the separate obligation to make public disclosure at least two business days before the market‑effective date. The SEC’s approval of the proposal and its effective date of January 30, 2025, illustrate how exchange and regulator coordinate on detailed aspects of market operations.

Subsequent filings in 2026, referenced in our newsroom coverage under identifiers such as SR‑NASDAQ‑2026‑044, ‑048, ‑049, and ‑056, reflect similar fine‑tuning in response to shifting market conditions, including heightened M&A activity and the introduction of new products like bitcoin ETF options. Each filing tends to address specific clauses—such as how to handle disclosures around complex corporate restructurings or how to integrate new order types—yet collectively they form the evolving scaffolding that allows Nasdaq to host both blue‑chip tech giants and volatile crypto‑adjacent small caps on the same venue. For crypto investors, this underscores that the exchange’s microstructure and compliance environment are subject to incremental change, not unlike the way DeFi protocols implement governance upgrades via on‑chain votes.

Market surveillance across TradFi and crypto

One of Nasdaq’s most exportable capabilities is its market‑surveillance technology. The exchange group operates sophisticated systems that monitor trading across its venues for patterns indicative of insider trading, spoofing, layering, and other forms of market manipulation. These surveillance tools are not limited to equities; Nasdaq licenses its technology to exchanges and regulators worldwide, positioning itself as a global vendor of capital‑markets infrastructure. The partnership with Talos explicitly calls for integrating Nasdaq’s Trade Surveillance platform with Talos’s digital asset workflows, suggesting that similar pattern‑recognition and alerting techniques will be applied to spot and derivatives trading in bitcoin and other tokens.

For crypto markets plagued by concerns over wash trading, pump‑and‑dump schemes, and thinly regulated offshore venues, the application of Nasdaq‑grade surveillance tools is a double‑edged development. On the one hand, it offers a path toward greater market integrity and institutional comfort, potentially unlocking more capital from risk‑averse allocators who demand strong compliance controls. On the other hand, bringing digital asset trading under the ambit of systems designed for securities markets may accelerate regulatory convergence, pushing more activity into venues where KYC, transaction monitoring, and suspicious‑activity reporting are the norm. For DeFi protocols seeking to interoperate with such systems—whether through tokenized collateral, on‑chain KYC, or oracle connections—the emerging challenge is how to maintain sufficient decentralization while satisfying the risk controls of Nasdaq’s institutional customer base.

Lessons for crypto from Nasdaq’s rulebook

The contrast between Nasdaq’s deeply codified rulebook and the often ad hoc governance of crypto projects offers several lessons. First, disclosure discipline matters: Nasdaq’s listing standards and SEC reporting requirements force companies to document their risk factors, conflicts of interest, and related‑party transactions in ways that token projects often lack. For example, a Nasdaq‑listed company that holds significant amounts of a native token or stablecoin typically must detail its valuation methods, custody arrangements, and concentration risks in filings, whereas many DAOs provide only cursory dashboards. Second, procedural clarity around corporate actions—reverse splits, spinoffs, recapitalizations—reduces uncertainty for investors and facilitates orderly trading, even when the underlying economics are unfavorable, as in the Nakamoto reverse split case.

For crypto teams considering tokenized equity, on‑chain governance, or hybrid structures that involve public listings, studying Nasdaq’s rule framework can help anticipate how regulators and institutional investors will scrutinize their choices. The rise of companies preparing for Nasdaq listings while maintaining significant crypto treasuries—such as Evernorth, which reportedly strengthened its board with an OpenAI Foundation CFO to bolster its XRP‑centric treasury strategy ahead of a planned listing—illustrates how traditional corporate governance and crypto balance‑sheet management are converging. The more that tokens, validators, and synthetic dollars intersect with public‑company obligations, the more relevant the Nasdaq rulebook becomes to protocol designers and DAO delegates.

Using Nasdaq in Crypto Trading and Portfolio Strategy

Nasdaq as a macro risk barometer

In practical terms, many crypto traders treat the Nasdaq‑100 and QQQ as real‑time gauges of global risk appetite. During U.S. trading hours, intraday swings in QQQ often coincide with moves in bitcoin and ether, reflecting high cross‑asset correlations documented in both practitioner commentary and academic work. When interest‑rate expectations shift—due to macroeconomic data, central‑bank speeches, or geopolitical events—the transmission mechanism frequently runs through technology equities first, with Nasdaq‑100 futures reacting, followed by risk re‑pricing in crypto as traders update their expectations of liquidity conditions and growth prospects.

The empirically observed correlation of around 0.8 between bitcoin and the Nasdaq‑100 does not mean that BTC is simply “another tech stock,” but it does imply that ignoring equity markets when trading crypto is unwise. For macro‑oriented crypto funds, daily routines often begin with monitoring pre‑market QQQ futures, cross‑asset vol surfaces, and key single‑stock names within the Nasdaq‑100 that may drive index‑level moves. Thematic developments—such as surges in AI‑related chipmakers or software firms—can spill over into AI‑linked crypto tokens, while drawdowns in unprofitable growth names can presage de‑risking in speculative DeFi projects. In this sense, Nasdaq functions as both a thermometer and an amplifier of the risk conditions that shape digital asset flows.

Trading around the open, close, and gaps

Because Nasdaq trades only during specific windows, crypto traders seeking to arbitrage or hedge cross‑market exposures must pay close attention to the opening and closing auctions, as well as to pre‑market and after‑hours liquidity. The main session open at 9:30 a.m. ET often serves as a focal point for price discovery in bitcoin proxies like IBIT, Coinbase, and crypto miners, particularly after weekends or holidays when significant news has accumulated. Gaps between Friday’s Nasdaq close and Monday’s open are notoriously common when bitcoin has moved sharply over the weekend, forcing ETF and equity prices to catch up in a single jump. Conversely, after‑hours earnings reports from Nasdaq‑listed crypto firms or macro‑sensitive tech giants can move QQQ and relevant single names, with traders then projecting the impact onto overnight crypto markets.

The existence of extended‑hours sessions from 4:00 a.m. to 9:30 a.m. and 4:00 p.m. to 8:00 p.m. ET softens some of these discontinuities, but liquidity during these windows remains thinner than during the main session. For sophisticated market participants, this creates opportunities and risks. One can, for example, use after‑hours trading in QQQ or IBIT to hedge or express views on bitcoin price moves that occur while U.S. cash equities are closed, but doing so involves wider spreads and higher impact. Conversely, crypto derivatives traders might anticipate how order books will reset at the Nasdaq open and position accordingly, expecting that dislocations between spot bitcoin and Nasdaq‑traded proxies will compress once both markets are fully liquid.

Equity, ETF, and on‑chain exposures: a practical comparison

For portfolio construction, it is useful to distinguish among the main vehicles through which an investor can access bitcoin‑related or Nasdaq‑related risk. Conceptually, one can think about exposure along two dimensions: what underlying risk is being targeted (bitcoin vs tech equities vs a mixture), and where it is being expressed (on‑chain vs on a regulated exchange). The table below sketches a simplified comparison.

| Vehicle | Venue / Wrapper | Primary Underlying Risk | Key Use Cases |

|---|---|---|---|

| Spot BTC | On‑chain / CEX | Bitcoin price | Pure BTC exposure, DeFi collateral |

| IBIT spot BTC ETF | Nasdaq ETF | Bitcoin price via custodial trust | Regulated BTC exposure for brokerage accounts |

| Coinbase equity (e.g.) | Nasdaq common stock | Exchange fees, crypto volumes, regulation | Levered, operationalized crypto exposure |

| QQQ ETF | Nasdaq ETF | Nasdaq‑100 tech and growth equities | Tech beta, macro risk barometer |

| QQQ perpetual on DeFi | On‑chain derivatives | Synthetic Nasdaq‑100 via oracles | Permissionless tech exposure, cross‑margining |

In practice, many investors combine several of these, using spot BTC or perpetuals for core crypto exposure, IBIT for compliance‑friendly holdings in brokerage accounts, QQQ for broader tech risk, and on‑chain perps to integrate everything into a margin‑efficient DeFi strategy. Understanding how Nasdaq underpins the ETF and equity components of this stack is essential for managing liquidity, basis risk, and regulatory constraints.

Treasuries, RWAs, and corporate crypto bets in portfolios

As more Nasdaq‑listed companies adopt crypto‑heavy treasury strategies or build tokenization businesses, equity portfolios naturally accumulate RWA‑style crypto exposure. For instance, a diversified small‑cap tech basket might include firms like Forward Industries (Solana treasury), Datavault AI (meme‑coin and RWA token portfolios), or Beeline Holdings (blockchain‑based mortgages), each introducing their own blend of on‑chain and off‑chain risks. Similarly, our newsroom has covered how companies preparing for Nasdaq listings—such as Evernorth, which reportedly seeks to position itself as an XRP‑treasury‑heavy fintech—are explicitly pitching their token strategies as part of their equity investment case.

For digital asset allocators, this raises strategic questions. Should crypto exposure be concentrated in tokens and derivatives, or is there value in owning the listed entities building infrastructure and products around those tokens? Nasdaq’s role as the primary listing venue for many such firms means it will remain central to this debate. Over time, we may see more sophisticated multi‑asset products—both on Nasdaq and in DeFi—that blend token and equity exposures, using Nasdaq‑listed instruments as building blocks for structured crypto‑equity hybrid portfolios.

NASDAQ ETF rule filings and SEC review of tokenized securities proposals create binary approval risk; a single adverse ruling can reprice entire crypto-equity categories overnight.

Empirical events — DeepSeek rout, Black Monday tariff panic — confirm BTC now moves in tight lockstep with NASDAQ futures, eliminating its diversification value in risk-off episodes.

NASDAQ acting as gatekeeper for crypto ETF listings and settlement indexes concentrates access and pricing power for digital assets in a single incumbent exchange operator.

The $35B institutional collateral tokenization pilot with Talos is promising but unproven at scale; mismatches between onchain settlement finality and NASDAQ's T+1 cycle could create intraday gaps.

- Smart-contractLow

NASDAQ's own infrastructure is off-chain; smart-contract risk is inherited only indirectly through DeFi products (e.g., Ostium's 200x onchain NASDAQ futures) that reference NASDAQ prices via oracles.

NASDAQ's proposed 23-hour trading window introduces overnight liquidity thinness and new arbitrage windows against 24/7 crypto markets, raising flash-crash and manipulation surface area.

Outlook

Looking ahead, the relationship between Nasdaq and crypto is likely to deepen along three dimensions: product innovation, infrastructure convergence, and corporate strategy. On the product front, the approval of options on the IBIT spot bitcoin ETF is unlikely to be the last word. As trading volumes and regulatory comfort grow, one can reasonably expect more complex derivatives—such as spread options between QQQ and bitcoin ETFs, or structured notes linked to baskets of crypto‑related equities and tokens—to find homes on or around Nasdaq’s ecosystem. Each new product will further entangle bitcoin’s volatility surface with that of tech equities, reinforcing the need for cross‑asset risk management among both traditional and digital‑native firms.

On the infrastructure side, collaborations like the Nasdaq–Talos tokenized collateral project point toward a future in which institutional capital can flow more fluidly between traditional and digital venues, with tokenized treasuries, stablecoins, and perhaps even tokenized equities recognized as eligible collateral across trading, lending, and clearing systems. As DeFi protocols continue to list synthetic Nasdaq exposures—whether QQQ perps on Orderly or Nasdaq options overlays on platforms like Hyperliquid—the technical and conceptual distance between a Nasdaq order book and an on‑chain AMM will shrink. This convergence will not erase regulatory differences, but it will make it increasingly natural for traders to think of “Nasdaq risk” and “on‑chain risk” as components of a single, integrated portfolio.

Corporate strategy is the third axis on which the Nasdaq–crypto relationship will evolve. The steady drumbeat of crypto‑linked firms listing or preparing to list on Nasdaq—from CoinShares and Solana‑treasury companies to AI‑crypto crossovers—suggests that public‑equity markets will remain a primary route for scaling digital asset businesses. At the same time, the presence of synthetic dollars, validator infrastructure, and multi‑sig governance in the business models of Nasdaq‑affiliated entities indicates that the core mechanics of blockchains are becoming part of public‑company operations, not just experimental side projects. For crypto investors, this means that monitoring Nasdaq filings, earnings calls, and rule changes will be as integral to understanding the digital asset landscape as following protocol governance forums or on‑chain analytics dashboards.

Conclusion

The Nasdaq Stock Market began as a bold experiment in electronic trading and has grown into a central pillar of the modern financial system, particularly for technology and growth‑oriented companies. For the crypto ecosystem, Nasdaq now serves as the primary bridge into traditional capital markets, hosting listings for exchanges, miners, digital asset managers, and firms with substantial token treasuries, while also providing the platform for bitcoin spot ETFs and, increasingly, listed derivatives on those products. Its tech‑heavy benchmarks, notably the Nasdaq‑100 and the QQQ ETF, have become key reference points for macro risk sentiment, with bitcoin often moving in close step with these indexes in risk‑on and risk‑off regimes.

At the same time, Nasdaq is actively shaping the next phase of digital asset integration through initiatives in tokenized collateral, market surveillance, and cross‑venue infrastructure, as exemplified by its partnership with Talos. Rule filings with the SEC and refinements to listing standards—ranging from reverse split notifications to corporate‑action procedures—demonstrate an ongoing effort to adapt the exchange’s governance framework to a world in which crypto‑adjacent companies and products are part of the mainstream. DeFi protocols and on‑chain derivatives platforms, for their part, are mirroring Nasdaq exposures through synthetic RWAs and QQQ perps, creating a feedback loop in which price discovery and risk management span both centralized and decentralized venues.

For crypto investors, the practical implication is clear: understanding Nasdaq—its structure, indexes, products, and regulatory environment—is no longer optional. Whether one trades spot BTC, perps, RWAs, or tokenized treasuries, a growing share of digital asset price dynamics, funding flows, and institutional behavior is mediated through instruments and entities listed on or linked to Nasdaq. As product innovation, infrastructure convergence, and corporate strategy continue to intertwine the two domains, those who grasp the nuances of both Nasdaq and on‑chain markets will be best positioned to navigate the evolving frontier between traditional and digital finance.

Latest NASDAQ news

Nakamoto proposes reverse stock split to stave off Nasdaq delisting after 99% share price plungeEuropean asset manager CoinShares begins U.S. push after Nasdaq listing, managing $6B+ AUM and aiming to compete with Wall Street giants in crypto ETF marketEvernorth adds OpenAI Foundation CFO to board ahead of Nasdaq listing, strengthening XRP treasury play with AI and institutional finance expertiseSafello lists staked TAO ETP on Nasdaq Stockholm with ~18% annual yield, first for Nordic investorsNasdaq and Talos partner to unlock $35B in trapped institutional collateral via tokenizationNasdaq, home of Coinbase, Strategy stocks, seeks 23-hour trading amid investor demand. Crypto's 24/7 trading has influenced investor expectations, with Nasdaq acknowledging that many of its clients are already active overnight.Sources

- https://www.nasdaq.com

- https://en.wikipedia.org/wiki/Nasdaq

- https://www.nasdaq.com/topic/market-infrastructure

- https://www.nasdaq.com/articles/tech-tuesday-sec-approves-first-kind-options-spot-bitcoin-etf-nasdaq-ibit

- https://investor.coinshares.com/pressreleases/coinshares-begins-trading-on-the-nasdaq-stock-market

- https://www.talos.com/insights/nasdaq-and-talos-partner-to-advance-tokenized-collateral-management-across-mainstream-and-digital-asset-markets

- https://www.sec.gov/pdf/nasd1/systems.pdf

- https://www.invesco.com/qqq-etf/en/home.html

- https://www.facebook.com/BusinessInsider.Finance/posts/shares-of-crypto-related-coinbase-microstrategy-and-marathon-digital-look-set-to/6272038339527093/

- https://indexes.nasdaq.com/docs/Methodology_NDX.pdf

- https://www.etftrends.com/etf-education-content-hub/understanding-bitcoin-nasdaq-100-correlations/

- https://www.sec.gov/files/rules/sro/nasdaq/2024/34-101693.pdf

- https://www.thestreet.com/crypto/markets/battered-stock-attempts-reverse-split-to-avoid-nasdaq-delisting

- https://www.etftrends.com/coinshares-content-hub/crypto-etf-issuer-coinshares-debuts-nasdaq-spac-merger/

- https://www.sciencedirect.com/science/article/abs/pii/S0378437121004349

- https://www.investopedia.com/ask/answers/06/preaftermarket.asp

- https://www.nasdaq.com/market-activity/ipos

- https://www.nasdaq.com/newsroom/spacex-makes-history-raising-85-billion-through-nasdaq-listing

- https://forwardindustries.com

Community notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…