A crypto-focused explainer on financial indexes: how they're built, the major benchmarks (CME/Nasdaq, Cboe Bitcoin ETF, Fear & Greed), and how futures, ETFs, and DeFi products use them as settlement references.

+20 sources across the wider coverage universe

Coinbase and MarketVector launch volatility-weighted Bitcoin-gold index, backtested at 31% CAGR since 20162026-04

Coinbase and MarketVector launch volatility-weighted Bitcoin-gold index, backtested at 31% CAGR since 20162026-04 Paystack’s new AI agent Index handles Nigerian payments but raises fresh questions on trust, UX and regulatory risk2026-06

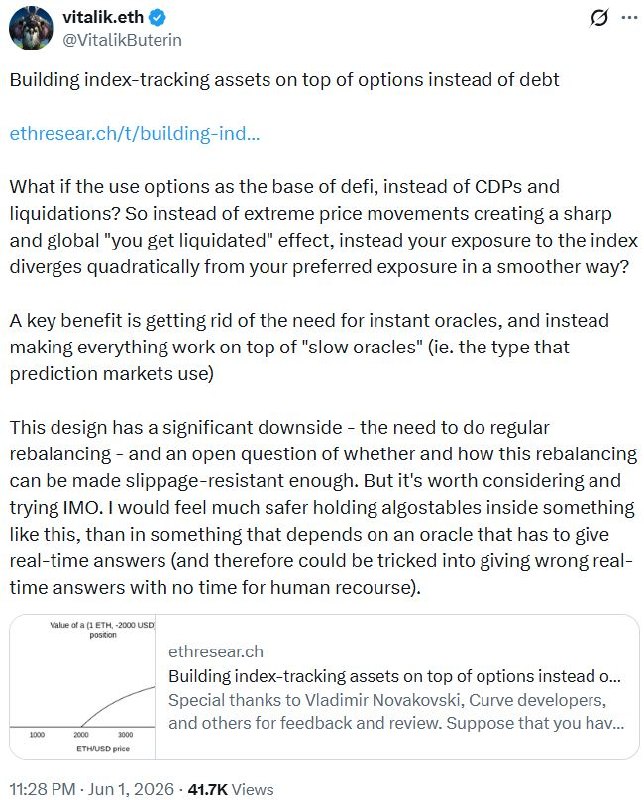

Paystack’s new AI agent Index handles Nigerian payments but raises fresh questions on trust, UX and regulatory risk2026-06 Vitalik Buterin proposes options-based DeFi without debt or liquidations. Users deposit 1 ETH to mint P and N tokens, redeemable for the full ETH at maturity based on a slow oracle's index check.2026-06

Vitalik Buterin proposes options-based DeFi without debt or liquidations. Users deposit 1 ETH to mint P and N tokens, redeemable for the full ETH at maturity based on a slow oracle's index check.2026-06 Index Ventures leads Fomo's $75M Series B as crypto trading app hits $550M valuation2026-06

Index Ventures leads Fomo's $75M Series B as crypto trading app hits $550M valuation2026-06 Jane Street’s $1B trading-strategy lawsuit backfires, triggering multi-continent probes into alleged index manipulation, ETF abuses, and insider crypto trades that freeze over $500M in assets2026-03

Jane Street’s $1B trading-strategy lawsuit backfires, triggering multi-continent probes into alleged index manipulation, ETF abuses, and insider crypto trades that freeze over $500M in assets2026-03 CME targets June 8 for its first market-cap weighted Nasdaq CME crypto index futures across seven assets2026-05

CME targets June 8 for its first market-cap weighted Nasdaq CME crypto index futures across seven assets2026-05

A financial index is a standardized benchmark that tracks the aggregate performance of a defined basket of assets — giving investors, traders, and analysts a single number to represent market conditions across an otherwise unwieldy universe of individual securities or tokens.

Market participants have used indexes as navigation tools since Charles Dow calculated the first industrial average by hand in 1896. Crypto adopted the concept early, and in 2026 the infrastructure around digital-asset indexes has grown sophisticated enough that regulated futures, options, and ETFs all hang off benchmark prices that didn't exist a decade ago. Understanding how indexes are constructed, maintained, and traded is now a prerequisite for anyone operating across both traditional and decentralized markets.

What an Index Actually Measures

An index is not an asset you can hold directly. It is a price, calculated by a methodology and published by an index provider, that represents the collective value of its constituent components. Three design choices determine almost everything about how an index behaves:

Weighting scheme. Market-capitalization weighting — the dominant method in equities and crypto — gives larger assets more influence. The S&P 500 weights stocks by float-adjusted market cap; the Nasdaq CME Crypto Index, launched by CME Group in mid-2026, tracks the top eight cryptocurrencies by market cap, meaning Bitcoin and Ethereum together account for the bulk of index movement. Equal-weight and liquidity-weight alternatives exist and behave differently during large-cap rallies.

Constituent selection. A rules-based methodology screens candidates by size, liquidity, trading venue, and sometimes sector. The Russell Microcap Index, for instance, uses size and liquidity gates — which is why the decentralized-AI firm TAO Synergies' inclusion in that index in 2026 was treated as a signal of emerging legitimacy for Web3-adjacent public companies. Similar momentum drove Sharplink's Russell inclusion after pivoting to an Ethereum treasury strategy.

Rebalancing cadence. Most equity indexes rebalance quarterly or annually. Crypto indexes often rebalance monthly because token market caps can shift dramatically in weeks.

TradeXYZ's dominance in equity, commodity and index perps isn't an existential threat to Hyperliquid, it's a growth engine driving users, fees and HYPE buybacks

83 active xyz markets now carry about $2.85B OI and $2.6B in 24h notional on Hyperliquid API; SP500, SPCX, CL/BRENTOIL, GOLD and SILVER are already sitting in the top books. HIP-3 makes that accretive because deployers bond 500k HYPE and users pay 2x validator-perp fees while the protocol keeps the same fee take, but the stress point moves to oracle quality and slashing when SPCX/CBRS-style pre-IPO marks have no clean exchange close.

Readers click 'Index' stories not for passive investing logic but for the collision points — when a TVL-based oracle becomes an exploit vector, when an altcoin season index signals macro regime shifts, or when Wall Street licenses the S&P 500 to a DeFi perp exchange — revealing that crypto index interest is driven by institutional boundary-crossing and systemic fragility, not benchmark construction.

The Major Index Families in Crypto

Broad-Market Benchmarks

The Nasdaq CME Crypto Settlement Price Index is currently the most institutionally significant broad crypto benchmark. CME Group and Nasdaq jointly developed it to underpin new cash-settled futures covering Bitcoin, Ether, Solana, XRP, Chainlink, Cardano, and others in the top eight by market cap. Cash settlement means no physical coin delivery; the contract simply pays the difference between entry price and the index value at expiration. This structure is important for regulated venues that cannot hold spot crypto.

The CF Benchmarks family (used in Cboe's Bitcoin ETF index options, ticker CBTX, and its mini variant MBTX) serves a similar anchoring role for single-asset Bitcoin products. Cboe filed rule changes with the SEC in 2026 to amend transaction fees on those contracts — routine maintenance that nonetheless illustrates how quickly a new asset class can accumulate regulatory paperwork.

Volatility Indexes

Borrowing directly from equity markets' VIX, crypto has its own implied-volatility benchmarks. The Bitcoin Volmex Implied Volatility Index (BVIV) tracks the 30-day implied volatility priced into Bitcoin options. In mid-June 2026 BVIV fell to 36.11, a nine-month low, signaling that options markets expected relatively calm near-term price action — a notable contrast to the sentiment picture elsewhere (see below). Low implied volatility typically makes option buying cheaper and option selling less rewarding.

Sentiment Indexes

The Alternative.me Fear & Greed Index compresses social media volume, volatility, market momentum, surveys, and dominance readings into a single 0–100 score. On June 19, 2026, it registered 14 — firmly in "Extreme Fear" territory — a reading consistent with Binance Research's concurrent observation that capital appeared to be rotating out of crypto and into U.S. equities, as evidenced by elevated Cboe Dispersion Index readings in traditional markets. Sentiment indexes are not predictive on their own, but they quantify crowd psychology in a format that systematic traders can act on.

Indexes as the Foundation for Tradeable Products

The practical importance of indexes is that they enable derivative products — futures, options, and ETFs — that give investors exposure to a benchmark without requiring them to build and rebalance the underlying basket themselves.

ETFs

A spot or synthetic ETF that tracks an index must hold (or synthetically replicate) its constituents and report daily how closely it follows the benchmark — the "tracking error." The NYSE Arca fast-tracked a rule change in 2026 to allow new trading structures around the United States Copper Index Fund, illustrating how quickly exchange operators can adapt their rulebooks when index products gain traction. In crypto, spot Bitcoin ETFs approved by the SEC in early 2024 now have their own index-options layer stacked on top: the Nasdaq PHLX received conditional SEC approval to list cash-settled Bitcoin index options under the ticker QBTC, pending CFTC sign-off.

Futures

Futures on indexes lock in a price for delivery at a future date. CME's new Nasdaq CME Crypto Index Futures give institutional traders regulated access to broad crypto market exposure — the same category of product that introduced equity-index futures to Wall Street in 1982. For crypto, regulated futures matter because they are accessible to pension funds, endowments, and other fiduciaries who face restrictions on spot crypto holdings.

Options on Index Moves

A newer layer sits between pure derivatives and prediction markets: event-based options that pay out based on whether an index finishes above or below a specific level at a specific time. Charles Schwab announced plans in 2026 to offer customers the ability to bet on S&P 500 index moves in this format, entering a space where Coinbase and Robinhood were already expanding. These products blur the line between financial derivatives and prediction markets, but they are anchored to an index price — the benchmark provides the settlement reference.

Perpetual Futures on Index ETFs

Decentralized-finance platforms have taken this further. DecibelTrade (built on Aptos, incubated by Aptos Labs) launched perpetual futures on SPY, QQQ, and EWY — the U.S. and Korean index ETFs — offering 24/7 onchain exposure to instruments that traditional exchanges close on weekends. Tria similarly raised leverage limits across crypto, commodities, equities, and index ETFs simultaneously, treating them as a single unified risk surface. Coinbase also increased price precision for its INDEX-USD spot pair, refining the market microstructure around index-related tokens.

Settlement for crypto perpetual futures — including the now-suspended Coinbase TON-PERP — is typically calculated as the average index price over a 60-minute window before expiration, a design that makes it harder for any single trade to manipulate the settlement print.

Paystack’s new AI agent Index handles Nigerian payments but raises fresh questions on trust, UX and regulatory risk

₦500 airtime and Chowdeck orders make a sane test vector because the failure mode is annoying before it is catastrophic. Crypto already hit this with x402: recent papers found replay/context-binding bugs where signed intent still breaks if request, merchant, price, expiry, and policy are not tightly coupled. Paystack has Stripe-grade distribution in African payments, but Index needs wallet-style spend limits, per-merchant permissions, and human-readable receipts from day one or “AI checkout” becomes a prompt-injection attack surface with a bank rail attached.

- 01Spot crypto index ETF race

The multi-year SEC filing saga around Bitwise's 10-asset crypto index ETF drew repeated clicks as readers tracked regulatory milestones with real capital implications for altcoin baskets.

- 02TVL-oracle exploit vectors

Whitehats exposing a vulnerability in Hyperliquid's FRIEND-USD TVL-based oracle showed readers that index construction methodology itself can become an attack surface.

- 03Sentiment index as macro signal

Fear & Greed and Altcoin Season Index headlines drew clicks because readers use these numbers as regime-change indicators, not just sentiment gauges.

- 04TradFi licensing crypto perps

S&P Dow Jones licensing the S&P 500 to Hyperliquid for 24/7 perpetual futures crystallized the tokenization-of-traditional-assets thesis in one concrete deal.

- 05Memecoin and niche index products

VanEck's MEMECOIN index and Aevo's Friend.tech market-cap perp showed readers that index infrastructure now wraps even the most speculative crypto sub-categories.

- 06Cross-market index contagion

The Black Monday global equity and crypto selloff, with Japan's Nikkei crashing 15% alongside BTC dropping 15%, illustrated how crypto indexes now move in lockstep with traditional market stress events.

How Index Composition Affects Real Markets

When a stock or token is added to a major index, passive funds that track it must buy the new constituent. This "index inclusion effect" can produce meaningful price movement before the official rebalancing date as arbitrageurs front-run the anticipated buying. BitMine's inclusion signal following the Russell Index update was cited by analyst Tom Lee as a liquidity catalyst precisely because of this mechanical demand.

Conversely, removal from an index triggers forced selling by index-tracking funds. The effect is more pronounced in less-liquid markets, which is one reason crypto index rebalancings are watched closely by active traders.

DeFi's Take on Indexing

Decentralized index protocols let anyone hold a basket of tokens without trusting a centralized custodian. Products like those in AWE's Polyvaults lineup (which expanded throughout May 2026) represent on-chain index funds: smart contracts hold the underlying tokens, mint shares, and handle rebalancing automatically via rules baked into the code.

Vitalik Buterin's 2026 proposal for options-based DeFi — where users deposit ETH to mint paired P and N tokens redeemable at maturity based on a slow oracle's index check — points toward a future where index-like payoff structures exist natively on-chain, without the debt and liquidation risk that plagues most current DeFi lending. The "slow oracle" design is specifically intended to prevent the price manipulation that can distort settlement on faster-moving benchmarks.

Index Ventures leads Fomo's $75M Series B as crypto trading app hits $550M valuation

Fomo raised a $75 million Series B led by Index Ventures at a $550 million valuation, with Union Square Ventures and angels including Mark Pincus, Humam Sakhnini, and Kevin Hartz also in the round. The dYdX-alumni team is building a non-custodial, global trading app that abstracts cross-chain onboarding, lists perps, and says it is adding roughly 3,500 users per day with 17 employees. The bet is that social trading UX becomes a Robinhood-style wedge for stocks, derivatives, and other assets as they move onchain.

- 2024-01regulatory

Bitwise 10 Crypto Index ETF SEC filing submitted

- 2024-08milestone

Black Monday: Nikkei -15%, BTC -15%, $900M crypto liquidated

- 2024-09launch

Aevo launches Friend.tech market-cap index perpetual

- 2024-11launch

VanEck MarketVector launches $MEMECOIN index

- 2024-12regulatory

SEC delays Bitwise 10 Crypto Index ETF decision

- 2025-01exploit

Hyperliquid FRIEND-USD oracle vulnerability disclosed; index changes and margin refunds issued

- 2025-03milestone

S&P Dow Jones licenses S&P 500 to Hyperliquid for 24/7 perp futures

- 2025-04launch

Franklin Templeton launches $EZPZ BTC/ETH weighted index ETF

Regulatory Landscape

Every index-based product that touches U.S. markets eventually runs into the SEC and, for futures, the CFTC. The regulatory picture in 2026 is one of cautious expansion:

- The SEC approved spot Bitcoin ETFs in early 2024 and has since allowed index options on top of those ETFs (QBTC pending CFTC).

- Cboe has filed multiple rule changes to adjust fees and expand access for its Bitcoin ETF index options (CBTX/MBTX), each of which requires a comment period before going effective.

- CME's launch of Nasdaq-branded crypto index futures went through CFTC oversight as a designated contract market.

- NYSE Arca's fast-tracked rule change for the Copper Index Fund shows how exchanges can use "immediate effectiveness" procedures for certain rule changes that don't require full notice-and-comment.

The pattern is incremental: each new product type requires its own regulatory clearance, but the precedents accumulate, making the next product slightly easier to approve.

Reading Index Data Practically

A few common mistakes when interpreting index readings:

Confusing level with return. An index at 5,000 tells you nothing without knowing where it started. Always compare returns over a defined period, not absolute levels.

Ignoring methodology changes. Index providers occasionally change constituent criteria or weighting rules. A crypto index that was cap-weighted in 2023 may use liquidity-adjusted weights in 2026 — the name stays the same but the thing being tracked is different.

Treating sentiment indexes as signals. The Fear & Greed Index at 14 describes current market psychology; it does not predict the next move. Markets have rallied sharply from similar readings and fallen further.

Conflating index price with ETF price. ETFs trade at market-determined prices that can deviate from net asset value (NAV). Arbitrage mechanisms keep them close, but the gap is not always zero, especially in illiquid hours.

- Smart-contract / OracleHigh

Hyperliquid's TVL-based oracle for FRIEND-USD was exploitable by whitehats, requiring index changes and maintenance margin refunds — proof that novel index construction inputs inherit smart-contract attack surface.

- RegulatoryHigh

The SEC's repeated delays on Bitwise's 10 Crypto Index ETF and concurrent approval of narrower index benchmarks signal an inconsistent, asset-by-asset gating approach that leaves multi-asset index products in prolonged limbo.

- Market / LiquidityHigh

The Altcoin Season Index dropping to 27 alongside a Black Monday event with $900M in crypto liquidations demonstrates that index-based products face sharp liquidity withdrawal during correlated global risk-off episodes.

- CentralizationMedium

Index construction authority — whether MarketVector for MEMECOIN, CF Benchmarks for Mag7+Crypto, or Kaiko for tokenized iBoxx — is concentrated in a small number of third-party calculation agents whose methodology changes can reprice leveraged positions instantly.

- Market manipulationMedium

Jane Street's $1B lawsuit triggered multi-continent probes into alleged index manipulation and ETF abuses, freezing over $500M in assets and exposing how traditional market-making practices can distort crypto-adjacent index products.

- Composability / SystemicMedium

Onchain index funds (Yearn yETH, AAVE V3 at $10B TVL, Vitalik's options-based DeFi) layer index logic on top of DeFi primitives, meaning an index rebalance or oracle update can cascade through lending and liquidity pools simultaneously.

Outlook

Index infrastructure in crypto is maturing rapidly. The CME/Nasdaq benchmark, Cboe's options suite, and the SEC's incremental approvals collectively indicate that regulated index products will continue expanding — with more assets, smaller lot sizes, and tighter bid-ask spreads as liquidity deepens. On-chain, DeFi index protocols are adding institutional-grade safety features (slow oracles, non-liquidating structures) that could eventually make decentralized index exposure credible for larger allocators. The gap between traditional market indexes and crypto-native benchmarks is narrowing from both directions. Sentiment readings in mid-2026 suggest capital is rotating toward equities, but historical patterns show that index flows reverse: passive crypto exposure, once infrastructure is in place, tends to grow steadily regardless of the short-term sentiment cycle.

Latest Index news

TradeXYZ's dominance in equity, commodity and index perps isn't an existential threat to Hyperliquid, it's a growth engine driving users, fees and HYPE buybacksPaystack’s new AI agent Index handles Nigerian payments but raises fresh questions on trust, UX and regulatory riskIndex Ventures leads Fomo's $75M Series B as crypto trading app hits $550M valuationCommunity notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…