Deep explainer on what “liquidated” means in crypto, covering margin and DeFi mechanics, BTC/ETH futures, liquidation cascades, Coinglass data, Hyperliquid, and practical ways traders can manage risk and avoid forced closures.

+5 sources across the wider coverage universe

Despite $300 million worth of ETH being liquidated in the last 24 hours, f(x) protocol prevented any losses through flawless rebalances, extra keepers, and fully functional RPCs. Leviathan is sponsored by the f(x) Protocol.2025-02

Despite $300 million worth of ETH being liquidated in the last 24 hours, f(x) protocol prevented any losses through flawless rebalances, extra keepers, and fully functional RPCs. Leviathan is sponsored by the f(x) Protocol.2025-02 Synthetix founder donates funds to ex-treasurer who was liquidated after weekend market plunge.2024-08

Synthetix founder donates funds to ex-treasurer who was liquidated after weekend market plunge.2024-08 Another $1 Billion in Crypto liquidated in 24 Hours amid ongoing market turbulence according to Coinglas2025-02

Another $1 Billion in Crypto liquidated in 24 Hours amid ongoing market turbulence according to Coinglas2025-02 In the last 24h over 1.07b where liquidated on hyperliquid.2024-12

In the last 24h over 1.07b where liquidated on hyperliquid.2024-12 Over 313,000 traders were liquidated in the last 24 hours, totaling $850M; 93.4% in longs, with the largest being a $98.46M BTC position on HTX.2025-01

Over 313,000 traders were liquidated in the last 24 hours, totaling $850M; 93.4% in longs, with the largest being a $98.46M BTC position on HTX.2025-01 Bitcoin options traders anticipate imminent breakout above $74K to new ATHs. BTC "ready to squeeze higher" with some $1.5 billion worth of shorts concentrated around the $72,000 that can be liquidated.2024-06

Bitcoin options traders anticipate imminent breakout above $74K to new ATHs. BTC "ready to squeeze higher" with some $1.5 billion worth of shorts concentrated around the $72,000 that can be liquidated.2024-06

Liquidated: How Forced Selling Shapes Crypto Trading, From Bitcoin to DeFi

In crypto, being liquidated means your position or collateral is forcibly sold—usually by an exchange or smart contract—because the value of your account has fallen below the minimum margin or collateral required to keep the trade or loan open. Unlike a voluntary exit or a stop‑loss order you place yourself, liquidation is an automated risk‑management process designed to ensure lenders, venues, and counterparties are repaid, even if you lose some or all of your collateral in the process.

Why “Liquidated” Headlines Dominate Crypto Markets

Every major market cycle in crypto leaves behind a trail of liquidation stories. In bull phases, short sellers in BTC and ETH are wiped out in short squeezes as prices rip higher; in sharp drawdowns, over‑levered long traders watch positions vanish in minutes as cascading liquidations accelerate the sell‑off. Aggregators like Coinglass regularly show hundreds of thousands of traders liquidated in a single day, with notional losses running into the hundreds of millions or even billions of dollars during periods of extreme volatility. These metrics capture only formal derivative liquidations, not the quieter voluntary selling by spot holders or risk‑off portfolio managers, which means the true impact of “forced selling” can be even larger than the headline numbers suggest.

In newsroom coverage, phrases like “$1 billion liquidated in 24 hours,” “Bitcoin longs wiped out,” or “Hyperliquid whale blown up” have become shorthand for episodes when leverage and volatility collide. Such headlines often accompany inflection points: a rapid BTC drop below a psychological level, an ETH rally that catches heavily shorted traders offside, or the blow‑up of a prominent whale on platforms like Hyperliquid or GMX. The repeated appearance of those stories underscores a structural reality of crypto markets: high leverage, thin liquidity at the tails, and 24/7 trading combine to make liquidation risk a central part of how price moves are formed and amplified.

Understanding what it means to be liquidated therefore matters far beyond individual traders. Liquidation mechanics help determine whether a sell‑off stops as a local shakeout or snowballs into a full‑scale cascade, and they influence how protocols are designed, how exchanges manage risk, and how data platforms such as Coinglass visualize systemic stress. For a crypto‑news audience tracking BTC, ETH, and the broader markets, unpacking the term “liquidated” is a gateway to understanding the plumbing behind many of the most dramatic price moves.

Black Friday 🔥 sale in the crypto market BTC below $82K, ETH 2700, SOL $127 Over $1 Billion liquidated in last 4hrs

Still expecting further decline especially SOL to $100 range

Readers click liquidation stories not for the mechanics but for the accountability gap: who designed the system that failed, who bore the loss, and whether anyone stepped up — the f(x) resilience story and the Synthetix founder's personal donation to a liquidated treasurer both outperformed raw billion-dollar wipeout headlines, revealing that protocol behavior and human responsibility outrank scale.↗

What Liquidation Means in Crypto

At its core, liquidation in crypto is about converting assets—usually leveraged positions or pledged collateral—into cash or stablecoins to cover losses or repay borrowed funds when the market moves against you. In derivative markets, this typically involves a futures or margin position being closed by the venue when the trader no longer meets margin requirements; the platform sells the position into the market to recover funds and protect its books. In lending markets such as Aave, liquidation refers to a liquidator repaying part of a borrower’s debt when their collateral has fallen too much in value, seizing some of that collateral at a discount in the process. Both mechanisms share the same underlying goal: making sure that loans are over‑collateralized and that the system, not just the individual, stays solvent.

A key distinction often glossed over in headlines is the difference between voluntary and forced liquidation. Voluntary liquidation occurs when a trader or investor chooses to close a position—selling BTC for stablecoins after a gain, reducing an ETH futures position ahead of a macro event, or unwinding collateral to exit a DeFi loan. Forced liquidation, by contrast, takes place when control is taken out of the user’s hands: the exchange’s risk engine or the DeFi protocol’s smart contract closes the position automatically once risk metrics breach preset thresholds. Most of the time, when you see reports of “$1 billion liquidated,” the focus is on forced liquidations in leveraged products, not discretionary portfolio management decisions.

It is also important to separate liquidation from related but distinct concepts such as margin calls and stop‑loss orders. Traditional finance often gives traders a margin call before liquidating them, allowing them time to deposit additional collateral or close positions manually; in fast‑moving crypto markets, margin calls can be effectively instantaneous, with liquidation carried out automatically when maintenance requirements are breached. Stop‑loss orders, by comparison, are placed by traders to exit positions at predefined price levels; these can trigger well before any liquidation threshold is reached, and in prudent risk management they are meant to prevent liquidation rather than replace it. Understanding where liquidation sits relative to these mechanisms helps explain why it is so often associated with severe adverse outcomes for traders.

Margin, Leverage, and Collateral

Liquidation risk is inseparable from the use of leverage, which allows traders to control a larger position than the capital they put up themselves. When you open a leveraged BTC or ETH position on a derivatives exchange, you deposit margin—your collateral—and borrow additional funds from the platform to scale the trade. Leverage is simply the ratio between the total notional value of the position and your own capital: a 10x leveraged position on 1 BTC notionally worth \(P\) dollars means you are contributing roughly \(P/10\) in margin and borrowing the rest. Leverage magnifies both gains and losses, and because your downside is limited to your margin while the borrowed funds must be repaid, the platform tightly monitors your equity to ensure it always covers liabilities.

Exchanges and protocols define two critical margin levels. Initial margin is the amount required to open a position, reflecting the maximum leverage permitted for that asset and product. Maintenance margin is the minimum equity that must be preserved to keep the position open; if account equity falls below this threshold due to adverse price moves, the liquidation process is triggered. For example, Hyperliquid defines maintenance margin as a fraction of the initial margin at maximum leverage, with the maintenance requirement ranging from about \(1.25\%\) of position size for assets with 40x maximum leverage to around \(16.7\%\) for assets capped at 3x leverage. This scaling reflects the intuitive idea that more volatile or riskier assets should support less leverage and demand higher maintenance buffers.

In practice, these margin relations tie directly into the liquidation price of a position. When you open a leveraged BTC long, the exchange calculates the price at which your equity will equal the maintenance margin; that is the point at which the system will start closing your position to protect lenders and the platform. The higher your leverage, the smaller the price move needed for losses to consume your margin, and thus the closer your liquidation price sits to your entry. Conversely, adding more collateral or using lower leverage pushes the liquidation price further away, giving you more room to withstand volatility in Bitcoin, Ether, and other assets.

Liquidation Price and Account Equity

Although every venue implements its own formulas, the basic logic is the same: liquidation begins once your account equity falls below the required maintenance margin. Equity is generally defined as your collateral plus any unrealized profit and loss; for Binance Futures, liquidation is triggered when the collateral available for a position—initial margin plus realized and unrealized PnL—drops below the maintenance margin requirement. Hyperliquid’s documentation gives an explicit expression for the liquidation price as a function of current price, side, margin available, and position size, illustrating how margin buffers and position direction interact. In simplified terms, for a long position, the liquidation price will be below the current price and move closer as leverage increases, while for a short position it will sit above current price and similarly tighten with more leverage.

The price reference used for liquidation is also crucial. Most derivatives platforms use a mark price or fair price, not the latest traded price, to determine margin and liquidation events. This mark price is often derived from a basket of spot exchange prices or an index, sometimes smoothed to avoid temporary wicks, and the goal is to reduce the risk of manipulative trades triggering liquidations. Binance, for example, explicitly states that liquidation occurs when the mark price, not the last executed price, hits the liquidation level. This design choice matters because in thin markets a single trade can print far away from the true fair value, and without mark pricing that wick could force unnecessary or even abusive liquidations on BTC or ETH futures books.

Once the mark price crosses the liquidation threshold, the position transitions from trader control to the platform’s liquidation engine. On venues like Deribit, this means the system begins to close positions incrementally, reducing the maintenance margin requirement until it falls below the remaining account equity. During this period the trader often cannot place new orders, including closing the position manually, because the risk engine has priority and must ensure losses are contained. If the position can be closed within available liquidity and fees, any leftover collateral remains in the account; if not, the account can go bankrupt, at which point insurance funds or auto‑deleveraging mechanisms may be used to socialize residual losses.

How Centralized Exchanges Liquidate Positions

On centralized derivatives exchanges, liquidation is deeply embedded in platform‑wide risk management. The core idea is that the exchange acts as a central counterparty: it matches longs and shorts but cannot allow large deficits to accumulate, because a failure to pay out winners damages trust in the venue itself. To prevent this, exchanges run sophisticated risk engines that continuously recalculate margin requirements and equity for every open position, often across multiple assets and contracts. When conditions breach pre‑defined thresholds, the engine steps in automatically, prioritizing system solvency over individual positions.

Binance Futures provides a representative example of this process. It defines a clear condition for liquidation: when the collateral allocated to a futures position, including initial margin and realized and unrealized PnL, becomes smaller than the maintenance margin requirement, the position is subject to forced closure. Liquidation is initiated when the mark price reaches the position’s liquidation price, and the system first attempts to reduce the trader’s margin deficit without wiping out the entire position. This is done by placing a large “Immediate or Cancel” (IOCO) order into the market, aiming to offload as much of the position as necessary to restore sufficient margin while minimizing disruption. If the resulting collateral and remaining maintenance margin are again in balance, liquidation stops; if not, further steps may be taken, potentially leading to full closure or transfer to an auto‑deleverage queue.

Deribit takes a similar but incrementally focused approach. Its documentation describes liquidation as beginning when maintenance margin requirements exceed the trader’s margin balance, at which point the liquidation engine takes full control of the account. The engine then gradually reduces positions in order to bring the maintenance margin requirement back below account equity, during which time the trader cannot intervene. Any remaining funds or positions after the process ends return to the user, but the path can be painful, as the engine may need to execute trades into unfavorable order books, resulting in worse prices than a proactive exit would have achieved. To cover cases where an account becomes bankrupt—meaning its equity is insufficient even after complete liquidation—Deribit uses an insurance fund, financed in part by liquidation fees, to absorb deficits before resorting to broader socialization of losses.

Partial vs Total Liquidations

Not every liquidation ends in a total wipeout. Many exchanges and protocols now implement partial liquidations, where only a portion of a position is closed to restore margin safety, rather than selling the entire position at once. This approach aims to reduce systemic shock: liquidating a huge BTC or ETH position in full at once can move the market, worsening slippage for the liquidated trader and potentially triggering further liquidations across the venue. By executing smaller tranches and testing whether the margin deficit can be resolved, partial liquidation mechanisms can stabilize both individual accounts and broader order books.

Nevertheless, in highly stressed conditions, partial liquidation may not be enough. If markets are moving rapidly, or if liquidity in the order book is thin, attempts to gradually offload positions can themselves push prices further against the liquidated side. In such scenarios, what starts as a partial reduction can quickly escalate into a full liquidation, especially when price moves outpace the risk engine’s ability to rebalance. Crypto’s 24/7 nature compounds this problem, as there are no closing auctions or circuit breakers in most derivative venues to pause trading and allow order books to reset. The upshot is that while partial liquidations reduce the probability of total annihilation in normal conditions, they offer no guarantee against complete wipedowns during extreme BTC or ETH moves.

Risk Engines, Insurance Funds, and Auto‑Deleveraging

To manage these risks system‑wide, centralized exchanges pair liquidation mechanisms with insurance funds and auto‑deleveraging (ADL) frameworks. Insurance funds accumulate over time from liquidation fees and other charges, creating a buffer that can absorb losses when accounts go bankrupt after liquidation. If an exchange can close a losing position only at prices that leave the account with negative equity, the shortfall is covered by the insurance fund instead of being imposed on profitable counterparties. This structure preserves market confidence, as traders know that their winning BTC or ETH positions will be fully honored even when others are blown out.

Auto‑deleveraging is a last‑resort mechanism used when neither liquidation nor the insurance fund can fully resolve a shortfall. In ADL, profitable positions on the opposite side of the market are reduced in a prioritized manner to absorb losses from bankrupt accounts. While this sounds draconian, it is rare in major markets and typically activated only during extreme volatility or low liquidity events, such as sharp BTC crashes or sudden exchange‑specific disruptions. The risk that one’s profitable position could be involuntarily reduced is one reason why traders pay attention not just to their own liquidation levels but also to platform‑wide risk metrics and insurance fund sizes, especially on smaller venues.

- 01Protocol behavior under pressure↗

The f(x) vs. Pac Finance contrast — one protocol flawlessly rebalanced through $300M in ETH liquidations while the other silently adjusted LTV parameters with zero user warning — drew readers into a direct comparison of protocol design philosophy and operator accountability.

- 02Founder and whale positions liquidated↗

Named individuals losing massive positions (Curve's Egorov on Llama Lend, James Wynn's $99.3M BTC on Hyperliquid, GMX whale $13M) turned abstract market events into personal narratives readers could follow and judge.

- 03Community response to liquidated peers

The Synthetix founder personally donating funds to an ex-treasurer wiped out by the weekend plunge surfaced a rare moment of DeFi social accountability, making it the second-highest clicked headline in the set.

- 04Short squeeze cascade triggers↗

Headlines about billions in short positions wiped in hours after a Trump Truth Social post or BTC rally above $71K revealed how concentrated short bets become liquidation fuel, drawing readers who track market structure for trading signals.

- 05Aggregate scale: daily Coinglass totals↗

Recurring '$X billion liquidated in 24 hours' Coinglass reports drove consistent moderate engagement, functioning as a daily volatility barometer readers check reflexively during turbulent market periods.

- 06Platform-specific liquidation risk↗

Hyperliquid appearing multiple times — $1.07B in 24h, James Wynn's named position — elevated it from a venue to a character, with readers tracking whether a perp DEX handles extreme stress differently than centralized venues.

DeFi Liquidations: Aave and On‑Chain Lending

Liquidation in decentralized finance (DeFi) is conceptually similar to centralized platforms but implemented through transparent smart contracts and externally triggered networks of liquidators. In lending protocols like Aave, users deposit assets as collateral and borrow other assets against that collateral, with the system ensuring that every loan remains over‑collateralized. The key risk metric here is the health factor, which captures the relationship between the value of the user’s collateral and the value of their debt, adjusted by asset‑specific risk parameters. Aave defines the health factor as \( \text{HF} = \frac{\text{Total Collateral Value} \times \text{Weighted Average Liquidation Threshold}}{\text{Total Borrow Value}} \), with values above 1 indicating a safe position and values below 1 indicating an at‑risk or liquidatable position.

Each collateral asset on Aave is assigned a liquidation threshold, reflecting how much can be safely borrowed against it. More volatile or less liquid assets typically receive lower thresholds, meaning users can borrow only a smaller percentage of their collateral’s value before risking liquidation. The health factor evolves in real time as market prices change, debt accrues interest, and users modify their positions, and if it falls below 1, the protocol marks the position as eligible for liquidation. Users can restore safety by repaying some of their debt or adding more collateral, both of which raise the health factor. This dynamic is analogous to adding margin on a futures platform to push the liquidation price further away, but it is computed on‑chain and is fully transparent to anyone monitoring the protocol.

Once a position becomes liquidatable, Aave allows permissionless liquidations: any network participant can repay part or all of the borrower’s debt and seize a proportional amount of their collateral, plus a liquidation bonus. The protocol defines how much debt can be liquidated depending on the health factor and the size of the position. When the health factor is above 0.95 and both the collateral and debt are at least \(2{,}000\) USD in value, up to 50% of the total debt can be liquidated; when the health factor is 0.95 or below, or when either side is smaller than \(2{,}000\) USD, up to 100% of the debt is eligible for liquidation. There are also dust rules to prevent tiny residual positions: partial liquidations must leave at least \(1{,}000\) USD of both collateral and debt in place, otherwise the position must be fully cleared. These rules shape the incentives for liquidators and determine how aggressively troubled positions are unwound.

Oracle Risk and Liquidation Cascades in DeFi

Because DeFi protocols rely on on‑chain oracles for pricing, oracle risk is central to liquidation behavior. Lending protocols typically pull asset prices from oracle networks such as Chainlink, which aggregate data from multiple exchanges and feed it on‑chain. If oracle updates lag during violent market moves, or if oracle sources are manipulated, collateral can be mispriced, leading either to delayed liquidations that put the protocol at risk or to premature liquidations that harm users unnecessarily. Protocol documentation and risk analyses often emphasize the importance of robust oracle design and monitoring, and guidance around evaluating DeFi venues recommends examining oracle documentation and liquidation parameters before depositing significant capital.

DeFi can also experience liquidation cascades, particularly when many users have deposited the same volatile collateral and borrowed against it in correlated ways. Chainlink’s analysis of liquidation cascades in crypto lending describes how declining asset prices can trigger waves of automated collateral sell‑offs, pushing prices further down and forcing more liquidations in a feedback loop. When collateral prices drop rapidly, leveraged lending positions across a protocol can simultaneously cross their liquidation thresholds, leading liquidators to sell large amounts of the same assets into already falling markets. This dynamic mirrors cascading liquidations in centralized futures markets but is executed programmatically on‑chain, which means it can be tracked in real time yet is difficult to stop once underway.

Risk frameworks for DeFi lending now explicitly treat liquidation parameters as a core dimension of protocol design. Analysts look at liquidation thresholds, penalties, oracle configurations, and governance processes to assess how a protocol is likely to behave during stress. Some newer architectures experiment with isolated lending markets or modular vaults, aiming to contain collateral risk and prevent cross‑asset contagion when a liquidation cascade hits a particular collateral type. For users, the takeaway is that being liquidated in DeFi is not just a function of individual leverage but also of protocol design and oracle reliability.

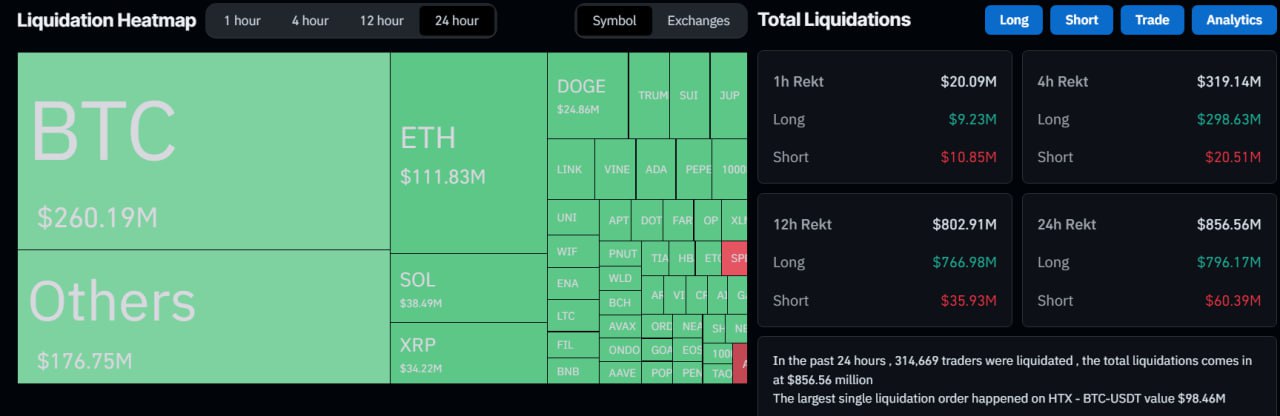

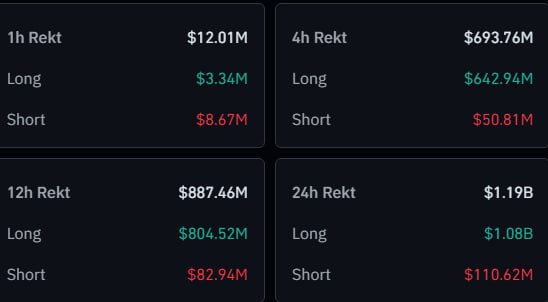

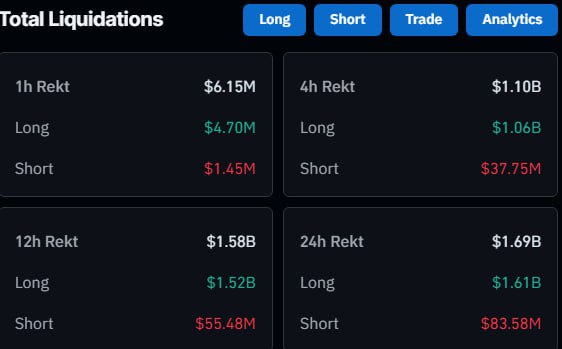

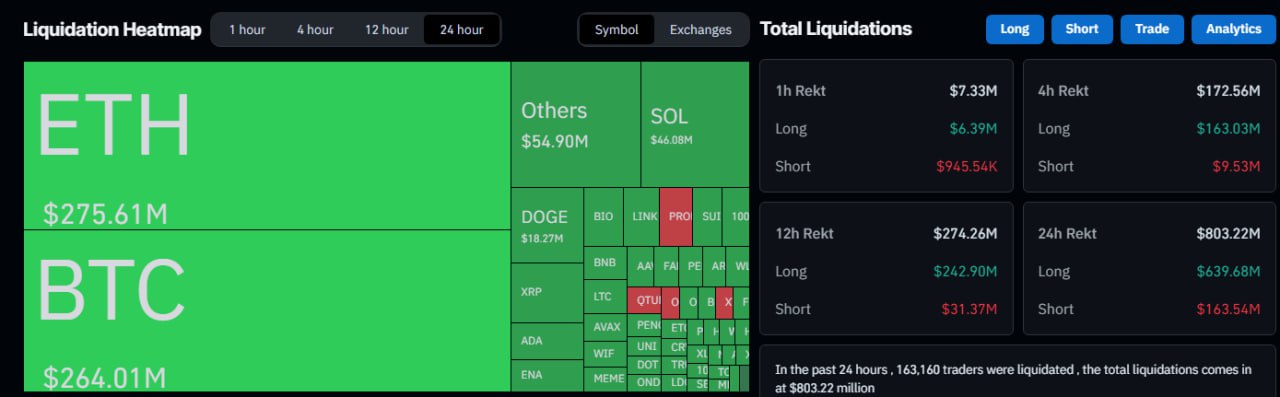

In the past 24 hours , 307,787 traders were liquidated , the total liquidations comes in at $1.19 billion. The largest single liquidation order happened on HTX - BTC-USDT value $33.95M

just use F(x)

Perpetual Futures, Hyperliquid, and On‑Chain Derivatives

Beyond spot margin and DeFi lending, liquidation plays a defining role in perpetual futures markets, where traders can hold long or short exposure indefinitely without expiry. Perpetual contracts, widely used for BTC, ETH, and other large‑cap assets, use funding payments rather than expiry settlements to keep futures prices anchored around the spot market. Because they allow high leverage and attract both speculative traders and hedging institutions, perpetuals are frequent sites of large liquidation events that show up in Coinglass dashboards and news coverage.

Platforms like Hyperliquid illustrate how liquidation mechanics are adapted for advanced derivatives venues. Hyperliquid defines a liquidation event as occurring when a trader’s positions move against them to the point where account equity falls below maintenance margin, much like on centralized exchanges. Its documentation explains that maintenance margin is set as a fraction of initial margin at maximum leverage, varying by asset between roughly \(1.25\%\) and \(16.7\%\) of position size. Hyperliquid also publishes an explicit formula for liquidation price as a function of current price, margin available, position size, and side, making it transparent how different inputs shift the level at which forced closure occurs. This level of detail helps sophisticated traders model their risk precisely and understand how adding or removing collateral affects their liquidation distance on BTC or ETH perpetuals.

Metamask’s educational materials on perpetual futures further highlight that with the flexibility of indefinite duration comes heightened liquidation risk. Since there is no natural expiry at which positions are settled, perpetuals rely entirely on margin maintenance and collateral monitoring to prevent losses from exceeding deposited capital. In practice, this means that volatility events—whether triggered by macro news, crypto‑native developments, or exchange‑specific issues—can rapidly translate into mass liquidations, especially when leverage is crowded in the same direction. This dynamic has been evident in many episodes of Bitcoin and Ether history, where funding ratios and open interest build up before a sudden move triggers a rush of liquidations that amplify the initial price swing.

When these liquidation events involve high‑profile traders or unusually large positions, they often become news stories in their own right. Reports of whales being liquidated on Hyperliquid or GMX, or of large oil‑linked or altcoin short positions being blown out as prices spike, illustrate how liquidation can serve as a narrative focal point for broader discussions about positioning, crowding, and market structure. These stories do not just signal individual misfortune; they reveal where leverage was concentrated and how the unwinding of those positions might affect subsequent BTC and ETH price action.

Ethereum lending liquidations spike to cycle high

Curve founder Egorov's CRV positions partially liquidated across multiple DeFi protocols after Curve exploit pressures CRV price

ezETH depegs to 0.5 ETH; Pac Finance liquidates $24M with zero user warning after silent LTV adjustment

Black Monday: Japan Nikkei crashes 15%, BTC falls 15%, $900M liquidated in crypto in 24 hours

Trump Truth Social crypto reserve post triggers $500M in short liquidations within hours

April Ethereum lending liquidations hit highest monthly volume since June 2022

James Wynn's $99.3M BTC position liquidated on Hyperliquid, becoming one of the largest single named-trader wipeouts on a perp DEX

Cascading Liquidations, Short Squeezes, and Market Structure

The term cascading liquidations describes episodes where a chain reaction of forced liquidations produces outsized and often sudden price moves. As Coinmetro explains, this phenomenon is especially common in markets with high leverage, such as crypto derivatives, where a wave of liquidations triggered by an initial price drop can push prices further down, forcing more positions to liquidate in a domino effect. Chainlink’s analysis similarly focuses on liquidation cascades in lending, where declining collateral values cause widespread liquidations that depress prices further, compounding the cycle. In both cases, forced selling begets more forced selling, and the resulting spiral can turn an ordinary correction into a dramatic flush.

On the bearish side, cascading liquidations often manifest as long squeezes, in which long traders are liquidated en masse as prices fall. Data from dashboards like CoinMarketCap’s liquidation tracker and Coinglass frequently show periods where hundreds of millions or billions of dollars in BTC and ETH longs are liquidated within hours during sharp downturns. The mechanism is straightforward: as prices decline, leveraged longs on futures and margin platforms see their equity erode until it breaches maintenance levels; exchanges then close those positions by selling into the market, adding further downward pressure. If many traders entered positions with similar liquidation levels—often clustered around popular support zones or psychological round numbers—the resulting forced selling can be highly concentrated, producing dramatic wicks or steep intraday declines.

The mirror image is a short squeeze, where aggressive upside moves trigger forced liquidation of short positions. In this case, exchanges buy back BTC or ETH futures to close liquidated shorts, adding upward pressure that accelerates the rally. Short squeezes can be especially violent when sentiment has turned broadly bearish and many traders are leaning short with high leverage; a positive catalyst or simply an absence of further bad news can spark a rally that forces shorts to cover, driving prices higher in a feedback loop. Real‑time liquidation data often show large volumes of short liquidations during these episodes, and Coinglass and similar platforms highlight whether liquidations are skewed toward longs or shorts in a given 24‑hour window.

Using Coinglass and Liquidation Dashboards

Aggregators like Coinglass, CoinGlass’s specialized heatmaps, and CoinMarketCap’s liquidation pages have become standard tools for monitoring these dynamics. These platforms pull derivatives data from multiple exchanges and display metrics such as total long and short liquidations over various time frames, the largest individual liquidation orders, and the distribution of liquidations across assets. They also offer historical views, allowing analysts to correlate liquidation spikes with major BTC and ETH price moves and to identify recurring patterns in how different exchanges respond to volatility.

CoinGlass in particular provides a liquidation heatmap for instruments like Binance’s ETH/USDT futures, showing estimated price ranges where large liquidation events may occur based on current open interest and margin profiles. This visualization helps traders anticipate potential trigger zones where a move into a specific price band could set off substantial forced selling or buying. Combined with order‑book data, these tools allow market participants to gauge whether an impending breakdown might be fueled by liquidation flows or whether a rally has enough short positioning behind it to catalyze a squeeze.

CoinMarketCap’s liquidation dashboard similarly emphasizes that large‑scale liquidations exert significant short‑term pressure on asset prices by creating forced selling in the market. It reiterates that liquidations occur when leveraged positions are forcibly closed after margin balances fall below maintenance thresholds and underscores that rapid price swings combined with high leverage levels are the usual triggers for such events. For a news audience tracking market structure, these data points provide quantitative context for headlines about “$500 million in shorts wiped out” or “over $1 billion liquidated in 24 hours,” linking anecdotal stories to systematic measures of leverage and risk.

Risk Management: How Not To Get Liquidated

While liquidation is an essential risk‑management tool for exchanges and protocols, for individual traders it is usually an outcome to avoid. Educational materials from venues and wallets consistently stress that prudent leverage, robust position sizing, and proactive risk controls are key to staying out of the liquidation engine’s crosshairs. Arkham’s guidance on crypto liquidation, for example, notes that using lower leverage, employing stop‑loss orders, sizing positions appropriately relative to account equity, and actively controlling margin are all effective ways to reduce liquidation risk. These principles apply across BTC, ETH, and altcoins, even though volatility regimes and liquidity conditions differ across assets.

One of the most fundamental tools is the stop‑loss order, which, unlike liquidation, is placed by the trader and triggers at a chosen price level. A stop‑loss is essentially an automated voluntary exit: you instruct the exchange to close your position if the market moves a specified amount against you, crystallizing a defined loss but staying well clear of liquidation. Educational videos and articles emphasize that stop‑loss orders should ideally sit comfortably above or below liquidation prices, providing a buffer zone in which you can exit before your equity is consumed. By contrast, relying on liquidation as a de facto stop‑loss is generally considered poor risk management, since liquidation fees, slippage, and loss of control over execution can make the outcome significantly worse than a planned exit.

Position sizing and leverage choice are the next line of defense. Traders can reduce liquidation risk simply by using lower leverage, which widens the gap between entry and liquidation prices and allows more room for normal volatility. In a 5x leveraged BTC futures trade, for example, a 20% adverse move might be required to trigger liquidation, whereas at 20x leverage, only a 5% move could be enough, especially after fees. Keeping notional exposure modest relative to account equity also reduces the risk that a single position’s liquidation will significantly impair overall capital. Educational resources repeatedly emphasize that emotional discipline—resisting the temptation to max out leverage in search of quick gains—is critical, as is reviewing liquidation levels before entering trades to ensure they are at distances that make sense given the asset’s volatility profile.

Margin management matters not only in isolated positions but also in cross‑margin setups, where collateral is shared across multiple positions. While cross‑margin can help prevent isolated positions from being liquidated due to temporary drawdowns, it also means that a liquidation event in one heavily leveraged trade can threaten the rest of the portfolio. Traders using cross‑margin on BTC and ETH perps therefore need to monitor total portfolio risk, not just individual position metrics, and may choose to ring‑fence certain trades in isolated margin mode to contain potential damage. Exchanges’ margin documentation and risk dashboards help users understand these trade‑offs and visualize how different positions interact under stress.

DeFi Risk Controls: Managing Health Factor and Protocol Risk

In DeFi lending, avoiding liquidation centers on managing the health factor and understanding protocol‑specific parameters. Aave stresses that maintaining a health factor well above 1 is crucial to prevent liquidation, recommending that borrowers regularly monitor this metric, especially when holding volatile collateral. If the health factor trends toward 1 due to market moves or accumulating interest, users can either supply more collateral or repay part of their borrow to increase the ratio and move away from the liquidation threshold. This process is similar to topping up margin on a futures platform but is initiated by the user’s on‑chain transactions rather than by an off‑chain risk engine.

More broadly, risk frameworks advise evaluating a protocol’s liquidation rules, oracle design, and governance before depositing significant funds. Guides to DeFi lending suggest reviewing audits, reading oracle documentation, and checking liquidation parameters as part of basic due diligence. This is because differences in liquidation penalties, asset thresholds, and update frequencies can significantly affect the likelihood and severity of liquidation under stress. A protocol with aggressively low liquidation thresholds on volatile collateral, for instance, may see large numbers of users liquidated during a moderate downturn, whereas a more conservative design with higher buffers may weather the same move with fewer forced sales. For borrowers, choosing where to open a position is as important as managing its size after the fact.

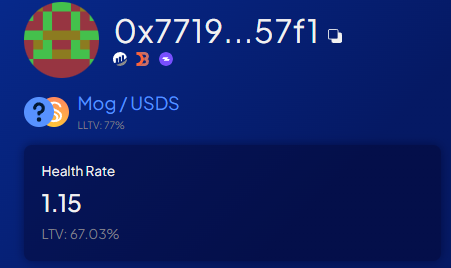

👀 Is the $MOG team is a bit over levered 2% of the supply ready to be liquidated below $0.6 (per 1M MOG)The $MOG team appears overleveraged, with 2% of the token supply—valued at 1M MOG—set to be liquidated if the price falls below $0.60, raising concerns of potential sell pressure.

Another Egorov situation? Or is actually the MOG protocol wallet or treasury or something?

Pac Finance's unannounced LTV adjustment that liquidated $24M in ezETH demonstrates that admin-controlled risk parameters can wipe users with no on-chain warning; the risk is not confined to bugs but extends to privileged parameter changes.

Single-day liquidation events routinely exceed $1B across perp and lending markets, and cascading forced sells — where liquidations push prices lower, triggering further liquidations — can compress weeks of losses into 15 minutes, as seen with the $1.4B BTC wipeout.

Correlated macro shocks such as the August 2024 Black Monday session drove BTC down 15% and eliminated $900M in crypto positions within 24 hours, demonstrating that liquidation cascades are not DeFi-isolated events but can be triggered by global equity sell-offs.

Protocols with admin keys capable of adjusting collateral ratios, liquidation thresholds, or oracle sources mid-session expose users to governance-by-surprise; decentralized alternatives require on-chain votes but introduce slower response to genuine risk.

Centralized exchange liquidation engines (Binance seeing an $8.21M single BTCUSDT liquidation, HTX handling a $98.46M BTC position) operate with proprietary mark-price mechanisms that can diverge from spot, forcing liquidations before on-chain prices would trigger them.

LRT depegs such as ezETH briefly trading at 0.5 ETH can cascade into immediate liquidations for any protocol using real-time spot prices as collateral value, even when the depeg is temporary and the underlying asset is not impaired.

Psychological and Structural Drivers of Liquidations

Beyond mechanics and data, liquidation is deeply intertwined with trader psychology and market narratives. Crypto’s culture of high risk‑taking, amplified by social media and the allure of outsized gains in BTC, ETH, and meme tokens, encourages many traders to push leverage to levels that would be uncommon in traditional markets. This often leads to crowded positioning, where large numbers of traders enter similar leveraged trades with stops and liquidation levels clustered in narrow price bands. When those bands are breached, news stories of “Black Friday‑style” selloffs with billions liquidated in hours reflect the human tendency to over‑extend in good times and to unwind abruptly when conditions turn.

High‑profile liquidations—whether of well‑known pseudonymous whales, funds, or teams holding significant token supplies—also play a symbolic role in market cycles. Reports of individual traders being liquidated for tens of millions of dollars on Hyperliquid or other venues turn abstract risk into relatable narratives, offering cautionary tales about over‑leveraging and poor risk management. In some cases, news that a heavily watched whale has finally been liquidated is interpreted as a cathartic event, marking the capitulation phase of a downtrend or the exhaustion of aggressive short sellers in an uptrend. These interpretations are not always accurate, but they shape sentiment and influence how traders position themselves after large liquidation events.

On the structural side, protocol and venue designers wrestle with trade‑offs between efficiency, capital utilization, and liquidation risk. Higher maximum leverage and lower collateral thresholds attract more trading volume and borrowing demand but increase the system’s vulnerability to liquidation cascades. Conversely, more conservative settings can reduce systemic risk but may push traders to seek higher leverage elsewhere, potentially fragmenting liquidity. Newer protocols explore mechanisms to reduce the pain of liquidation, such as incremental or “soft” liquidations, dynamic risk parameter adjustments, and backstop liquidity providers designed to absorb stressed collateral without severe slippage. While these innovations may mitigate some of the worst outcomes, the underlying tension between leverage and liquidation is unlikely to disappear.

Conclusion

To be “liquidated” in crypto is to lose control of your position or collateral, as exchanges or smart contracts enforce the rules that keep leveraged markets functioning. Whether in BTC and ETH futures on centralized exchanges, in perpetual contracts on venues like Hyperliquid, or in collateralized borrowing on protocols such as Aave, liquidation exists to ensure that loans are repaid and that counterparties receive what they are owed. The cost of this protection is borne by traders and borrowers whose positions move too far against them, often resulting in the loss of most or all of their margin or collateral, plus additional fees and slippage.

From a market‑wide perspective, liquidations play an outsized role in shaping short‑term price action. Cascade events, where waves of forced selling or buying feed on themselves, can turn routine volatility into dramatic moves, driving headline statistics like “$1 billion liquidated in 24 hours” that capture the attention of traders and the public alike. Tools like Coinglass and CoinMarketCap’s liquidation dashboards have made these dynamics more visible, allowing observers to quantify the scale and direction of liquidation flows and to connect them to price behavior in BTC, ETH, and other major assets. Meanwhile, DeFi’s on‑chain transparency exposes liquidation processes at the protocol level, making it possible to watch in real time as health factors deteriorate and liquidators step in.

For individual market participants, the lesson is clear: liquidation is not an inevitable cost of trading but a risk outcome that can be managed, mitigated, and often prevented. Thoughtful leverage choices, disciplined position sizing, proactive use of stop‑loss orders, and careful monitoring of margin and health factors are essential tools for avoiding the worst‑case scenario. At the same time, understanding how liquidation works at the system level—how risk engines, oracles, and insurance funds operate—helps traders interpret news about mass liquidations and assess whether such events signal deeper structural problems or are simply acute episodes in the ongoing interplay between leverage and volatility.

Outlook

Looking ahead, liquidation will remain a central feature of crypto markets for as long as leverage, margin, and collateralized lending exist. Exchanges are likely to continue refining their risk engines, experimenting with more nuanced partial liquidation schemes, dynamic margin requirements, and expanded insurance funds to reduce the frequency and severity of cascading events. In DeFi, protocol designers will keep iterating on collateral frameworks, oracle integrations, and market architectures—such as isolated lending markets and modular vaults—to limit contagion when liquidation waves hit specific assets.

For BTC, ETH, and other major cryptocurrencies, the interplay between leverage and liquidation will continue to produce the kind of volatile episodes that dominate news cycles and drive short‑term sentiment. However, as data tools like Coinglass, CoinMarketCap’s liquidation dashboards, and venue‑specific heatmaps become more sophisticated and more widely understood, market participants may grow better at anticipating where liquidation clusters lie and at positioning themselves accordingly. Over time, this greater transparency and improved risk literacy could make liquidation events more orderly and less catastrophic at the individual level, even if the structural tension between leverage and forced selling remains an enduring feature of the crypto landscape.

Latest Liquidated news

Black Friday 🔥 sale in the crypto market BTC below $82K, ETH 2700, SOL $127 Over $1 Billion liquidated in last 4hrsIn the past 24 hours , 307,787 traders were liquidated , the total liquidations comes in at $1.19 billion.

The largest single liquidation order happened on HTX - BTC-USDT value $33.95M 👀 Is the $MOG team is a bit over levered 2% of the supply ready to be liquidated below $0.6 (per 1M MOG)The $MOG team appears overleveraged, with 2% of the token supply—valued at 1M MOG—set to be liquidated if the price falls below $0.60, raising concerns of potential sell pressure. 📉 In the past 24 hours, 397,028 traders have been liquidated, with total losses reaching $1.7 Billion, according to Coinglass.com

📉 In the past 24 hours, 397,028 traders have been liquidated, with total losses reaching $1.7 Billion, according to Coinglass.com In the past day, 163,209 traders were liquidated, totaling $803.38m, according to Coinglass. The largest single wipeout was a $12.49m BTC-USDT swap on OKX.

In the past day, 163,209 traders were liquidated, totaling $803.38m, according to Coinglass. The largest single wipeout was a $12.49m BTC-USDT swap on OKX. Ether slid 5% to $4,588 after hitting a record $4,954 over the weekend, erasing gains from Powell’s rate-cut hint. Bitcoin dipped 1% to $111,502. Over $420M in long crypto positions were liquidated in 24 hrs, per CoinGlass.

Ether slid 5% to $4,588 after hitting a record $4,954 over the weekend, erasing gains from Powell’s rate-cut hint. Bitcoin dipped 1% to $111,502. Over $420M in long crypto positions were liquidated in 24 hrs, per CoinGlass.Sources

- https://www.youtube.com/watch?v=rzhpCtz931E

- https://support.coindcx.com/articles/futures-trading/what-is-liquidation/6381b999e36cb741dd8e67d2

- https://faq.pluang.com/s/article/Understanding-Liquidation-in-perpetual-trading

- https://archlending.com/blog/crypto-margin-call/

- https://chain.link/article/liquidation-cascade-crypto-lending

- https://www.coinglass.com/liquidations

- https://hyperliquid.gitbook.io/hyperliquid-docs/trading/liquidations

- https://eco.com/support/en/articles/14800882-best-defi-lending-protocols-2026-tvl-rates-risk

- https://www.coinmetro.com/glossary/cascading-liquidations

- https://coinmarketcap.com/charts/liquidations/

- https://aave.com/help/borrowing/liquidations

- https://www.youtube.com/watch?v=Q3Wpn2bEwXM

- https://metamask.io/news/perpetual-futures-liquidation-mechanics

- https://www.coinglass.com/pro/futures/LiquidationHeatMap?coin=ETH

- https://info.arkm.com/research/crypto-liquidation-meaning-futures-perpetuals-guide-avoid

- https://www.coinglass.com

- https://www.cube.exchange/what-is/liquidation

- https://www.ledger.com/academy/glossary/liquidation

- https://www.binance.com/en/support/faq/detail/360033525271

- https://insights.deribit.com/education/liquidation/

Community notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…