Deep dive explainer on seed rounds in crypto and Web3: how they work, how they differ from pre-seed and Series A, key deal structures, strategic investors, risks, and AI-driven case studies shaping the next funding cycle.

+5 sources across the wider coverage universe

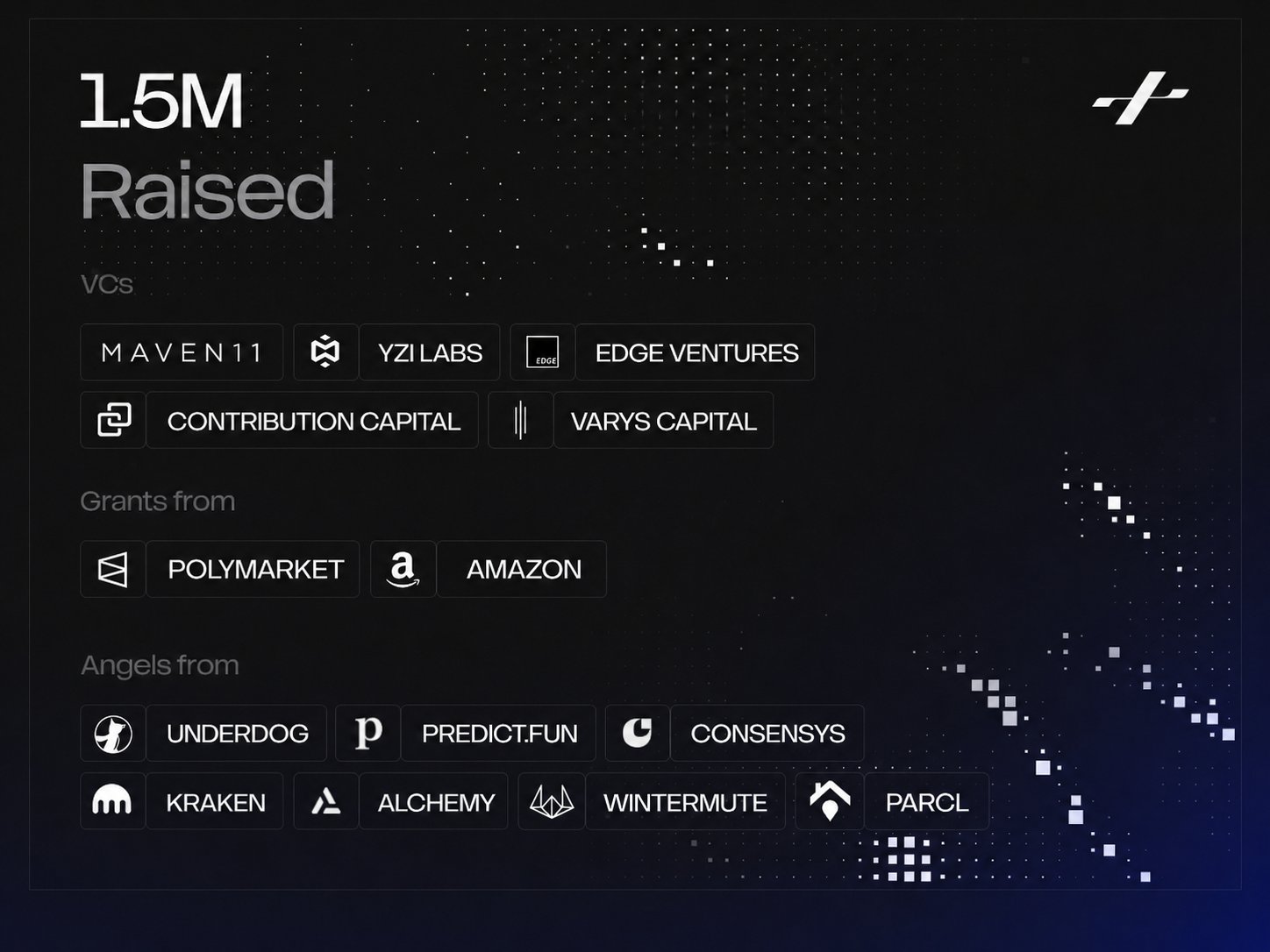

AI analytics platform Polysights raises $1.5M pre-seed funding to combat insider trading in prediction markets. The raise was backed by YZi Labs S3, Maven 11 Capital, and angels from Kraken and Consensys, plus grants from Polymarket and AWS.2026-06

AI analytics platform Polysights raises $1.5M pre-seed funding to combat insider trading in prediction markets. The raise was backed by YZi Labs S3, Maven 11 Capital, and angels from Kraken and Consensys, plus grants from Polymarket and AWS.2026-06 Mirendil raises $200m seed round led by a16z to build AI that automates AI engineering work2026-06

Mirendil raises $200m seed round led by a16z to build AI that automates AI engineering work2026-06 a16z leads Ornn's $33M seed round to build financial markets for AI compute, introducing GPU price indices, futures, and capital products for data center investors2026-06

a16z leads Ornn's $33M seed round to build financial markets for AI compute, introducing GPU price indices, futures, and capital products for data center investors2026-06 Mirage raises seed funding from Seed Club Ventures and Kyber Knight, launches closed alpha for private stablecoin transfers.2026-04

Mirage raises seed funding from Seed Club Ventures and Kyber Knight, launches closed alpha for private stablecoin transfers.2026-04 Tether and Gnosis lead $4.4M Sorted Wallet seed round as 10MB app targets feature phones2026-05

Tether and Gnosis lead $4.4M Sorted Wallet seed round as 10MB app targets feature phones2026-05 Uniblock raises $5.2M to unify blockchain infrastructure after its oversubscribed seed round brought the total capital raised to $7.5M.2026-04

Uniblock raises $5.2M to unify blockchain infrastructure after its oversubscribed seed round brought the total capital raised to $7.5M.2026-04

Seed Rounds in Crypto and Web3: An Evergreen Explainer

A seed round is the first significant external funding that a startup raises once it has moved beyond the idea or hobby phase, providing capital to build a product, validate market demand, and assemble a core team before pursuing larger Series A and later rounds. In crypto and Web3, seed rounds often blend traditional venture capital structures with token-based incentives, strategic ecosystem support, and on-chain community signals, making them a distinctive and sometimes confusing stage in the funding journey.

What Is a Seed Round?

Seed funding sits at the transition point between a founder’s bootstrapped efforts and the more structured, metrics-driven world of institutional venture capital. At this stage, a startup usually has a clear thesis, an early product or prototype, and at least a partial team, but it is still searching for repeatable product–market fit and durable business or protocol economics. The seed round provides enough capital to test whether the idea can become a real company or sustainable protocol: to hire engineers, run experiments with users, navigate early legal and regulatory work, and prepare for the expectations of a Series A. In crypto, seed rounds serve the additional function of funding token design, security audits, and initial liquidity bootstrapping, which adds complexity but also opens new paths to align founders, investors, and communities.

Position in the startup funding lifecycle

In the canonical venture lifecycle, a startup typically moves from pre-seed or angel capital to seed, then to Series A, B, C, and beyond as it proves progressively more mature milestones. Pre-seed capital is often used to validate a concept, assemble an initial founding team, and produce a prototype, and it is frequently provided by angels, friends and family, small pre-seed funds, or accelerators rather than large institutional firms. Seed funding follows once the team has clarified its thesis and begun to demonstrate some early user or market traction, but before the business has enough predictable revenue or growth metrics to justify a Series A at institutional scale. Later, Series A capital tends to focus on scaling a product that has found some product–market fit, financing go-to-market functions, and beginning to build a more formal company structure around operations, compliance, and governance.

This evolution is visible in aggregate data. Outlier Ventures, which tracks fundraising in Web3, reported that in 2024 the average pre-seed Web3 round was about 2.5 million dollars, the median seed round about 5.6 million dollars, and the median Series A about 17.6 million dollars, illustrating how capital intensity grows as companies move through the lifecycle. Those figures also suggest that in crypto and Web3, seed rounds have grown to a size that would once have been considered closer to a small Series A, reflecting both the rising costs of technical development and the ambition of projects that must ship production-grade protocols early to attract users and liquidity. Yet compared with large growth rounds, where late-stage firms can raise hundreds of millions of dollars at multi-billion-dollar valuations—as seen in AI and robotics companies such as Standard Bots, which raised 200 million dollars in a Series C round at a one billion dollar valuation—seed capital remains fundamentally about exploration and validation rather than scale.

Typical size, investors, and objectives

The precise size of a seed round varies widely by sector, geography, and market cycle, but some broad patterns are visible across technology and especially within crypto. In more traditional software, seed rounds often range from the high six figures to a few million dollars, though competitive markets and hot themes can push those numbers higher. Within Web3, seed rounds skew larger on average, reflecting the dual need to build both product and token infrastructure; Outlier Ventures’ 2024 review placed the median seed round at 5.6 million dollars, more than double the typical pre-seed size of 2.5 million dollars. AI-related startups have also pushed up valuations and sometimes round sizes, with Carta reporting that in 2024 seed-stage AI startups commanded median pre-money valuations of 17.9 million dollars, roughly 42 percent higher than non‑AI peers. Even when a project is crypto-native, if it sits at the junction of AI and finance—such as quantitative AI trading or AI-driven prediction markets—these valuation dynamics tend to spill over.

Seed investors typically include specialized seed funds, multi-stage venture capital firms willing to back companies early, strategic corporate venture arms, ecosystem funds, and occasionally well-resourced angels or founders. In crypto, there is an additional category of ecosystem and protocol-aligned investors, such as exchange ventures arms, stablecoin issuers, or layer‑1 protocol foundations that invest at seed stage to bootstrap activity in their ecosystems. Coinbase Ventures, for example, participates in early-stage crypto rounds like the seed financing for Tenor Labs, an on-chain fixed-rate lending protocol, as part of a broader strategy to support projects that could deepen the Coinbase ecosystem or expand crypto’s use cases. Similarly, Solana Ventures operates as the strategic investment arm for the Solana ecosystem, focusing on early-stage projects in DeFi, NFTs, Web3 gaming, and blockchain infrastructure, often at pre-seed and seed stages.

The objectives of a seed round can be summarized as transforming a promising hypothesis into a validated business or protocol with enough traction to justify a Series A. This usually involves building a robust minimum viable product, signing early customers or community members, demonstrating some positive user behavior, and clarifying the project’s tokenomics and governance model if it is crypto-native. In crypto, a seed round might also fund smart contract audits, the design of token incentive programs, regulatory analysis, and partnerships to ensure liquidity and distribution at launch. These objectives frame the expectations that investors and founders should bring to a seed round: it is neither a casual check nor a guaranteed bridge to later financing, but a focused opportunity to prove that the idea works in the real world.

To ground this in current practice, consider a few illustrative examples across AI, finance, and Web3. Aether AI, for instance, recently raised 20 million dollars in seed funding to build what it calls “causal world models,” AI systems designed to reason about cause-and-effect relationships rather than merely extrapolating from correlations. That comparatively large seed round reflects both the capital intensity of deep research in AI and investor belief that causal reasoning will be critical for robotics and physical-world applications. At the other end of the spectrum, Ralo, an AI-driven mortgage brokerage, raised 2.9 million dollars in a seed round to expand its AI mortgage broker services, targeting operational efficiency and faster loan closings rather than purely foundational AI research. In crypto-native domains, Fortune Protocol secured a seed round to expand AI-powered prediction markets on BNB Chain, combining Web3 infrastructure with AI tooling that aims to support more efficient market forecasting. And Kulipa, a Paris-based infrastructure startup, raised 6.2 million dollars in seed funding to build stablecoin-native card issuing infrastructure enabling fintechs and wallets to launch white-label payment cards without handling the operational burden themselves. Each of these deals sits at seed stage, but the capital needs and risk profiles differ significantly, which is why clear definitions and expectations around seed rounds are so important.

AI analytics platform Polysights raises $1.5M pre-seed funding to combat insider trading in prediction markets. The raise was backed by YZi Labs S3, Maven 11 Capital, and angels from Kraken and Consensys, plus grants from Polymarket and AWS.

13.36M Polymarket OrderFilled events still leave OrderPlaced and OrderCancelled off-chain, so surveillance has to infer intent from fills, wallet behavior, and public-event timing instead of reading a clean audit trail. Polysights sits in the compliance middleware lane prediction markets need if they want CFTC/Kalshi-level legitimacy without killing crypto-native liquidity; the hard part is separating sharp public-info traders from the 1,950-account “insider” heuristic bucket researchers are already arguing about.

Readers don't click seed rounds for the capital amount — they click for the backer list: when BlackRock, Vitalik, a16z, Franklin Templeton, or Paradigm appears, clicks spike regardless of whether the raise is $1M or $25M, revealing that crypto seed announcements function as VC credentialing signals and conviction proxies, not capital-formation news.↗

Seed Rounds in Crypto and Web3

Although seed rounds in crypto share many features with early-stage financing in other technology sectors, several structural differences make them unique. Crypto projects often ship products that are simultaneously software, economic systems, and governance experiments, all of which must work reasonably well from the outset to attract users and capital. Protocols and decentralized applications can be globally accessible from day one, meaning that even seed-stage projects may need to contend with cross-border regulatory questions and security standards that traditional startups might postpone until later stages. Finally, the presence of tokens introduces new ways to finance, incentivize, and govern projects, but also adds complexity around investor protections, community ownership, and long-term alignment.

How tokens change seed-stage economics

Tokens fundamentally reshape what “ownership” means at seed stage. In a traditional seed round, investors receive equity, often in the form of preferred shares or convertible securities that will convert into equity at a future priced round. In crypto, investors typically seek exposure not only to the equity of the development entity but also to the future tokens of the protocol or platform, which may carry governance rights, fee claims, or other utility. This dual structure is often implemented via combinations such as a SAFE (Simple Agreement for Future Equity) for the corporate entity and a token warrant that entitles investors to a share of the protocol’s tokens once they launch. As Hashed’s analysis of SAFE plus token warrant structures notes, the equity component is usually linked to a future “priced round” in which the company issues preferred stock at a negotiated valuation, while the token warrant is anchored to the project’s eventual token generation event or to valuations implied by that priced equity round.

The presence of tokens has at least three important implications for seed-round economics. First, it allows early participants—including founders, investors, and in some models the community—to hold liquid or semi-liquid assets that may appreciate in value well before the company achieves a traditional exit via M&A or IPO. Second, it complicates dilution and ownership calculations: cap tables must now account for both equity and token allocations, often under different vesting schedules, and founders must ensure that future community and ecosystem incentives are preserved despite potentially large allocations to seed investors. Third, tokens alter the timing and nature of investor returns, since investors may start to realize value via token unlocks months or years before any equity liquidity event, which may influence their behavior around secondary markets and governance proposals.

At the same time, crypto projects increasingly face regulatory scrutiny over whether their tokens may be treated as securities, especially if they are distributed to investors via private agreements that resemble traditional securities offerings. This has led many teams to adopt more conservative structures, such as delaying token launches, creating non-transferable “points” systems during beta phases, or emphasizing clearly functional utility tokens over speculative assets. Even when token warrants are used, their terms often include long vesting and lockup periods designed to align investors with the protocol’s long-term health rather than short-term price spikes. In this environment, seed-round structuring must balance the advantages of token-based incentives with careful legal design.

On-chain traction and community as seed-stage signals

Another distinctive feature of seed rounds in Web3 is the importance of on-chain traction and community engagement as investable signals. Traditional early-stage investors often evaluate startups on qualitative factors such as the founding team’s experience, the clarity of the problem being solved, and initial customer feedback, supplemented by nascent quantitative metrics like early revenue or usage. In crypto, these factors remain important, but investors can also examine on-chain data such as transaction counts, protocol revenues, liquidity metrics, governance participation, and wallet distribution to assess whether a protocol is gaining real adoption.

For example, institutional-grade infrastructure projects like AlphaNet, which raised a 10 million dollar seed round to build a quantitative AI trading platform targeting institutional investors, may be evaluated not just on their team and roadmap but also on the robustness of their trading algorithms, the volume and quality of on-chain strategies they can execute, and the depth of their integration with exchanges and DeFi protocols. Similarly, AI-powered prediction market platforms such as Fortune Protocol must convince investors that they can attract sufficient liquidity and participation on chains like BNB, which is partly observable via on-chain order books, volumes, and the performance of AI-powered tools in helping users make informed bets. More consumer-facing infrastructure like Kulipa’s stablecoin card issuing platform is evaluated on relationships with fintechs and wallets, the resilience of its payments infrastructure, and its ability to safely bridge stablecoin balances into existing card networks.

Community engagement also plays an outsized role in crypto seed rounds, especially for consumer-facing apps, gaming projects, or memecoins. A Vegas-themed memecoin raising funding to expand licensed IP, original content, and esports-style tournaments is not just selling a product; it is selling a cultural and community narrative that must be credible and resilient beyond the initial hype cycle. The same is true for gaming or creator platforms that combine AI, blockchain, and user-generated content: investors at seed stage must assess whether these communities are organic and sustainable rather than purely driven by speculative token activity. Because many crypto projects distribute tokens to users through airdrops, liquidity mining, or contribution programs, the community’s composition and motivations can materially influence long-term outcomes.

This emphasis on on-chain and community data means that even very early projects may benefit from launching minimal but functional versions of their products and experimenting in public, rather than staying in stealth until a Series A. It also makes due diligence more transparent: sophisticated investors can parse blockchain explorers and analytics tools to derive their own view of traction, rather than relying solely on internally reported metrics. For founders, this is both an opportunity and a challenge; it rewards genuine use but makes it harder to gloss over weak engagement.

Ecosystem funds and strategic capital

Because Web3 is composed of interoperable protocols and platforms, many projects choose to raise seed capital from ecosystem funds that can provide strategic advantages beyond money. Solana Ventures, for instance, was created to accelerate the growth of the Solana blockchain and adjacent ecosystems, providing capital and strategic support to early-stage crypto projects in areas such as DeFi, NFTs, gaming, and core infrastructure. By backing pre-seed and seed rounds, Solana Ventures helps ensure a pipeline of applications that drive network usage, which in turn can increase the value of the underlying token and ecosystem. Projects backed by such funds often receive technical support, co-marketing assistance, and introductions across the ecosystem, which can be as valuable as the capital itself.

Exchange-linked funds like Coinbase Ventures operate under a similar logic, though with a broader, multi-chain scope. Coinbase Ventures invests in projects that could expand crypto use cases or integrate with Coinbase’s products, such as Tenor Labs, which raised 2.5 million dollars in seed funding to build an on-chain fixed-rate lending protocol. Having a major exchange’s venture arm as a seed investor can enhance a project’s credibility, ease future listing conversations, and open doors to institutional users, though it rarely guarantees any specific commercial relationship. Stablecoin issuers and protocol treasuries sometimes play analogous roles: Tether and Gnosis, for example, co-led a 4.4 million dollar seed round for a lightweight mobile-friendly wallet focused on feature phones, signaling their interest in expanding the practical use of stablecoins and Ethereum in emerging markets, while Tether also participated in infrastructure deals like Kulipa’s seed round aimed at bringing stablecoins into the card network rails.

These strategic investors are joined by multi-stage crypto-native funds like Paradigm, which describes itself as a frontier technology investment firm active in crypto, AI, robotics, and other emerging areas from the earliest stages. Paradigm has participated in seed rounds for projects ranging from gaming platforms to complex DeFi protocols, often bringing both technical depth and policy expertise. Market-making firms such as DWF Labs also increasingly act as seed investors; DWF describes its model as spanning the lifecycle from pre-seed and seed investing to providing liquidity as traction builds and ultimately market making, blurring the lines between pure venture capital and trading firms. This multifaceted approach can help seed-stage projects bootstrap liquidity and price discovery once they launch tokens, but it also introduces new dynamics around incentives and governance that both founders and communities must understand.

From Pre-Seed to Series A: Mapping the Journey

Understanding seed rounds requires situating them relative to adjacent stages, especially pre-seed and Series A. In theory, the funding ladder is clean: founders progress from idea to pre-seed, then seed, then Series A as they achieve increasingly demanding milestones. In practice, especially in crypto, the boundaries blur. Market cycles, thematic manias such as AI, and the rapid pace of token-based exits can compress timelines or reorder stages entirely. Some projects skip pre-seed, bootstrapping their way directly into a substantive seed round, while others raise multiple seed-like rounds at different valuations before calling one of them a Series A. This fluidity has led some observers to ask whether pre-seed as a distinct category is “dead” or simply evolving.

Pre-seed versus seed in Web3

Pre-seed is often the least formalized stage, but it plays an important role, particularly in capital-intensive sectors or for first-time founders. HubSpot describes pre-seed funding as the earliest round, used to test the viability of an idea and build a prototype, typically raised from founders’ personal networks, angel investors, or early-stage funds. At this point, there may be little or no revenue, and the product might be an early beta or even just a well-articulated concept. Seed funding, by contrast, usually arrives when there is at least some product development and early customer or user feedback, and when the team wants to accelerate toward measurable traction. CRV’s analysis of seed versus Series A highlights that by the time founders raise a seed round, investors expect some proof points such as early user growth, pilot customers, or evidence of technical feasibility, even if the business model is still evolving.

In Web3, this distinction is complicated by the fact that projects can quickly deploy smart contracts and experiment with on-chain products, even with small teams. A Hyperliquid-based proprietary trading platform like Hypernova, which raised a few million dollars in pre-seed funding to build an on-chain prop trading experience, might already be running early testnets or closed beta tournaments, blurring the line between pre-seed and seed. Likewise, infrastructure projects such as SizeProp, which raised a pre-seed round to build infrastructure for crypto prop trading, are investing in heavy technical development that might in another era have required seed-level capital. The Outlier Ventures data showing pre-seed round sizes already averaging 2.5 million dollars in Web3 underscores how capital-intensive even the earliest stages have become.

Despite this, the conceptual difference remains useful. Pre-seed is about answering whether the idea and team are compelling enough to justify significant investment. Seed is about showing that the idea works in practice and deserves to be scaled. Founders who frame their fundraising narrative around these distinctions—especially in an environment where some investors worry that pre-seed labels are being stretched—can better align expectations with backers.

Seed versus Series A in a shifting market

If pre-seed answers “should this exist?” and seed answers “does this work in the wild?”, Series A aims to answer “can this scale into a durable business or protocol?” CRV emphasizes that Series A investors generally seek evidence of product–market fit, including user retention, revenue growth, or other meaningful metrics, and expect companies to have a clearer go-to-market strategy and organizational structure. At Series A, round sizes and valuations jump again; Outlier Ventures’ 2024 data for Web3 projects shows median Series A round sizes of 17.6 million dollars, compared with 5.6 million at seed, underscoring that Series A is intended to fuel scaling rather than initial discovery.

In crypto, this progression can be disrupted by rapid token launches and liquidity events. A protocol that successfully launches a token shortly after or even during its seed phase might see its fully diluted valuation soar into the billions, at least on paper, based on secondary market trading. This can make it harder to price an equity-based Series A and may encourage founders to raise larger seed rounds upfront to avoid a near-term dilutive equity round. On the other hand, some projects delay token generation events and pursue a more traditional Series A, particularly if they are building complex infrastructure or must navigate regulatory uncertainty before launching a token. Infrastructure startups like Kulipa or AI-driven trading platforms like AlphaNet clearly require substantial build-out and institutional partnerships before they can fully realize their business models, making Series A capital important even in a tokenized world.

Meanwhile, in adjacent sectors like AI robotics, later-stage rounds can reach impressive magnitudes, as shown by Standard Bots’ 200 million dollar Series C at a one billion dollar valuation. This raises questions about how seed-stage valuations anticipate or extrapolate such outcomes. Carta’s analysis that AI seed valuations are already 42 percent higher than non‑AI peers suggests that investors are pricing in significant future upside, which could either be justified by transformative businesses or lead to painful corrections if growth stalls. Crypto founders and investors must navigate similar dynamics, particularly in hot verticals such as AI–crypto convergence, where expectations can outpace fundamentals.

Debates about the “death” of pre-seed

The blurring of stage boundaries has led some commentators to question whether pre-seed, as a coherent category, is “dead.” A widely circulated discussion on social media framed the problem as a “broken” timeline, in which the period from having an idea to being acquired has compressed so dramatically—especially in software and crypto—that the classic ladder of pre-seed, seed, Series A, and beyond no longer reflects reality. From this perspective, founders either bootstrap long enough to attract a sizable seed from multi-stage funds, or they skip directly into larger rounds backed by strategic capital, leaving little room for small, standalone pre-seed checks. In crypto, the ability to generate early liquidity via tokens or to raise community funding from users can further compress the timeline.

Yet pre-seed clearly persists in practice, particularly for founders outside established networks or for projects with unconventional theses. Deals like Hypernova’s pre-seed round for an on-chain proprietary trading platform, or SizeProp’s pre-seed to build infrastructure for crypto prop trading, show that there is demand for capital dedicated to the riskiest and most experimental ideas. Hackathons and accelerators, such as the Colosseum hackathon offering pre-seed funding boosts for AI agent projects, also function as quasi pre-seed platforms, giving teams small amounts of capital and validation to pursue their ideas more seriously. The real shift may not be the death of pre-seed, but rather its absorption into a wider variety of mechanisms—angel syndicates, DAO grants, hackathon prizes, and ecosystem funds—that collectively perform pre-seed’s function without always carrying the label.

For founders, the takeaway is that labels matter less than clarity about stage, goals, and expectations. Whether a round is called “pre-seed” or “seed,” what matters is aligning the amount of capital with the milestones to be achieved and ensuring that the investor base is appropriate for the level of risk and support required. For investors, being explicit about the stage and risk profile of their commitments can avoid misaligned expectations down the line.

Mirendil raises $200m seed round led by a16z to build AI that automates AI engineering work

$1B valuation for a 20-person team says the scarce asset is not codegen UX, it's access to people and GPUs that can close the AI R&D loop. Nvidia joining the round matters because an agent that “controls its own GPUs” turns infra allocation into part of the product. For Akash, Render, io.net, and other decentralized compute plays, the comp is uncomfortable: buyers may want managed research loops with evals and scheduling baked in, not just cheaper FLOPs.

- 01TradFi institutions entering seed stage↗

BlackRock's ETF seed filing, Standard Chartered/SBI's $100M multi-stage commitment, Franklin Templeton leading Cap's round, and Ondo seeding the State Street/Galaxy tokenized fund collectively signaled that legacy finance had moved from observation to early-stage DeFi ownership — a threshold readers treated as a structural legitimacy signal.

- 02DeFi celebrities as angel investors

Vitalik joining Nocturne's $6M seed alongside VCs, and Lido's Shapovalov, Yearn's Banteng, and Gearbox's ivangbi co-investing in Hedgehog Protocol, drew readers who track where DeFi's inner circle deploys personal capital as a conviction signal about emerging primitives.

- 03Yield-bearing stablecoin infra raises↗

A cluster of seed rounds — Mountain Protocol, Reflect, Agora Dollar backed by Dragonfly, and Cap led by Franklin Templeton — revealed an intensifying race to own the yield-bearing stablecoin infrastructure layer, which readers followed as a competitive bracket.

- 04Top-tier VC lead as conviction proxy↗

Shadow's Paradigm-led $9M round, Miden's a16z-led $25M round, Catena Labs' a16z-led $18M round, and Reflect's a16z CSX backing showed readers using the lead investor's identity — not the capital — as a signal of technical credibility at the seed stage.

- 05Prediction market rival funding↗

A former Polymarket executive raising $15M from Coinbase Ventures and USV for The Clearing Company, alongside Limitless Exchange's $10M seed from 1confirmation and Coinbase Ventures, revealed reader appetite for tracking competitive pressure building against a dominant incumbent.

- 06Bitcoin L2 and high-TPS chain seed rounds

Corn's Bitcoin-as-gas-token L2 ($6.7M from Polychain, Binance Labs, and Framework Ventures) and MegaETH's $20M seed targeting 100,000 TPS attracted readers tracking infrastructure bets on the next performance tier beyond existing L2s.

Deal Mechanics and Legal Instruments

Beneath the surface of every seed round lies a dense thicket of legal instruments and deal mechanics. In traditional venture capital, the main options are priced equity rounds and convertible securities like SAFEs and convertible notes. Crypto adds additional layers in the form of token warrants, SAFT-style agreements, and on-chain vesting and governance arrangements. Understanding these mechanisms is essential for both founders and investors, as they determine how ownership, control, and economic upside are allocated over time.

Priced equity rounds and valuation

A priced equity round, sometimes called a preferred stock financing or priced round, is one in which investors buy a specific number of shares at a negotiated price per share, implying a particular pre-money and post-money valuation for the company. In such a round, the company issues preferred stock—rather than common stock—often with rights such as liquidation preferences, anti-dilution protection, and sometimes board seats. Carta notes that the defining feature of a priced round is precisely this per-share price, which allows stock to be sold as a set number of shares rather than as a vague promise of future equity. Priced rounds also commonly act as “qualified financing” events that trigger the conversion of prior SAFEs and convertible notes into equity, crystallizing the cap table at that moment.

At seed stage, founders and investors must negotiate a valuation that balances the company’s early promise with its high risk. Too low a valuation can lead to excessive dilution for founders, making it harder to stay motivated and to allocate equity to future team members. Too high a valuation can create pressure for the company to grow into its price quickly, setting up difficult negotiations for later rounds if traction lags. In AI and Web3, where hype cycles can push valuations upward, this balance becomes particularly delicate. Outlier Ventures’ data indicating median Web3 seed round sizes of 5.6 million dollars and Carta’s finding that AI seed valuations average around 17.9 million dollars offer some benchmarks, but individual deals often deviate based on team pedigree, market opportunity, and competitive dynamics.

In crypto, many early companies still use priced rounds, especially if they are building infrastructure, B2B platforms, or compliance-heavy products that resemble traditional startups. For example, infrastructure providers like Kulipa, offering stablecoin-native card issuing services for fintechs and wallets, raised a 6.2 million dollar seed round structured as conventional venture funding, because its business involves complex integrations with existing financial rails and card networks rather than issuing a speculative token. AI-driven trading platforms like AlphaNet, which raised 10 million dollars at seed, similarly adopt institutional-grade structures to attract investors accustomed to traditional financial products. For these companies, priced rounds provide clarity, align with investor expectations, and can co-exist with later token-related structures if the company eventually launches a protocol token.

SAFEs, SAFTs, and token warrants

While priced rounds are straightforward, they can be time-consuming and expensive to negotiate and close, which is why many early-stage startups use simpler instruments like SAFEs (Simple Agreements for Future Equity) or convertible notes. A SAFE entitles the investor to future equity in the company, typically upon a subsequent priced round, at a discount or subject to a valuation cap, without currently issuing shares or setting a per-share price. Convertible notes operate similarly but are structured as debt that converts into equity under specified conditions. These instruments allow seed-stage companies to raise capital more quickly, deferring valuation decisions until more information is available at a later financing.

In crypto, these instruments are often paired with token-related agreements. Hashed’s analysis of the SAFE plus token warrant “meta” describes a common structure in which an investor signs a SAFE for equity and simultaneously receives a warrant giving the right to purchase or receive tokens at a future date, often when the project conducts its first “priced” equity round or launches its token. The equity SAFE is tied to the company’s future valuation in its first priced round—whether that is called a pre-Series A, Series A, or even a down round compared with the SAFE’s valuation cap—while the token warrant is typically anchored to a specific share of the token supply or a valuation cap applied to the fully diluted token valuation. When a qualifying equity round occurs, the SAFE converts into preferred stock, and the token warrant’s terms become clearer as the token’s economic model solidifies.

Other structures sometimes used in crypto include SAFTs (Simple Agreements for Future Tokens), which entitle investors to receive tokens in the future once a network is live, often with vesting and transfer restrictions. These are more controversial in regulatory terms, and their use has evolved in response to enforcement actions and legal guidance in various jurisdictions. Regardless of the specific instrument, the key issues for both founders and investors are similar: how much of the eventual token supply is being committed at seed stage, what vesting and lockup periods will apply, and how the economics of tokens and equity interrelate over time. Poorly designed token warrant terms can over-allocate scarce token supply to early investors, leaving insufficient room for community incentives, ecosystem grants, and later rounds.

Token allocations, vesting, and lockups

Token allocations at seed stage must be considered not only in terms of investor economics but also governance, community perception, and long-term protocol sustainability. Many crypto projects design token distributions with a mix of allocations for founders and early team, investors, treasury and ecosystem funds, and community distribution mechanisms such as airdrops or liquidity mining. Seed investors typically receive a portion of tokens that vest over time, sometimes with a cliff period, and may be subject to post-vesting lockups intended to reduce immediate sell pressure after token launch. The aim is to align investors with the project’s multi-year trajectory rather than short-term price moves.

For example, when ecosystem or strategic investors such as Tether and Gnosis back early-stage projects like wallets or infrastructure providers, their economic interest is often tied to broader ecosystem growth rather than solely to a quick profit. However, communities can be sensitive to the perception that seed investors hold too much of the token supply, especially if unlock schedules cluster in ways that risk large selling events. Protocols that rely on on-chain governance may also need to ensure that token governance is not dominated by a handful of early investors, which can undermine decentralization and potentially create regulatory issues.

Vesting schedules for team and investors thus become more than just financial tools; they are governance instruments. Projects like Fortune Protocol or AlphaNet, which blend complex AI-driven services with financial exposure, must consider how token governance can be designed to give users meaningful voice while preserving the ability to iterate quickly and comply with evolving regulations. Meanwhile, dev fund restructurings—where a protocol’s development fund is reallocated or its governance mechanisms altered—have raised concerns in some communities that protections for long-term development and decentralization are being eroded in favor of near-term incentives for insiders. These tensions often trace back to decisions made at seed stage about who holds what and under which conditions.

Strategic Seed Investors and Their Roles

Seed rounds in crypto rarely involve purely financial capital. Because Web3 projects depend on network effects, liquidity, and composability, the identity and capabilities of seed investors can be as important as the size of their checks. Different classes of investors—venture funds, ecosystem and corporate funds, market makers, and community-driven capital—play distinct roles in nurturing early-stage projects and shaping their trajectories.

Venture funds and multi-stage firms

Traditional and crypto-native venture capital funds remain central actors in seed rounds. Multi-stage firms such as Paradigm explicitly market their willingness to invest from the “earliest stages” through to later growth rounds, reflecting a strategy of building deep relationships with founders and compounding their knowledge across a portfolio of related technologies. In crypto, this often means providing not only capital but also technical expertise, policy and regulatory guidance, and help designing tokenomics and governance. Paradigm, for example, has invested at seed in projects that span DeFi, gaming, and infrastructure, leveraging its network to support integrations and liquidity bootstrapping when those projects later launch tokens.

Generalist venture funds also participate in crypto seed rounds, especially where projects intersect with broader trends like AI, fintech, or robotics. Aether AI’s 20 million dollar seed round to develop causal world models attracted investors who see the future of AI reasoning as integral to robotics and physical-world systems, even if the project is not strictly a crypto protocol. Similarly, Ralo’s 2.9 million dollar seed round for an AI-native mortgage broker appealed to backers interested in the application of AI to financial services. As AI increasingly intersects with crypto—for example, in platforms like AlphaNet, which combine quantitative AI trading with on-chain infrastructure—multi-stage investors can bring cross-domain expertise on how AI models, data infrastructure, and blockchain systems interlock.

Exchange, stablecoin, and protocol ecosystem investors

Exchange venture arms, stablecoin issuers, and protocol foundations or ecosystem funds play a particularly strategic role at seed stage in crypto. Coinbase Ventures, for example, invests in projects that can deepen or expand the Coinbase ecosystem, such as on-chain lending protocols or infrastructure that may integrate with Coinbase’s custody, trading, or developer tools. By backing seed-stage projects like Tenor Labs’ fixed-rate lending protocol, Coinbase Ventures helps foster new primitives that, if successful, can eventually appear on Coinbase’s platform or attract usage that benefits Coinbase’s core business.

Stablecoin issuers and protocol treasuries have similar incentives. Tether’s participation in seed rounds for infrastructure providers like Kulipa, which specializes in stablecoin-native card issuing, helps extend the adoption of stablecoins into everyday payments contexts. Gnosis’s involvement in seed funding for lightweight wallets targeting low-resource devices aligns with its interest in broadening access to Ethereum-based tools. Protocol ecosystem funds like Solana Ventures go a step further by focusing on projects that build directly on their chain, offering strategic advantages such as expedited technical support, access to grants, and co-marketing campaigns that can accelerate user acquisition. These investors often take a longer view, focusing on how seed-stage projects will contribute to network health and usage over time.

Y Combinator’s move to unlock instant USDC seed funding on Solana illustrates how traditional accelerators are also experimenting with crypto rails to deliver capital faster and more globally. By distributing seed investments in USDC over the Solana network, YC can enable founders worldwide to access funds quickly, avoid some of the friction of traditional banking, and interact natively with Web3 financial primitives. This convergence of legacy venture programs with on-chain infrastructure may reshape what seed funding looks like for global startups.

Market makers and liquidity-focused backers

Market-making firms such as DWF Labs represent a newer category of seed-stage investor that is particularly prominent in crypto. DWF’s VP of Ecosystems, Alessia Baumgar, has described the firm’s model as spanning multiple stages: acting as an investor at pre-seed and seed, providing liquidity as traction builds, and eventually serving as a market maker in token and secondary markets. This integrated approach can help seed-stage projects plan not only for build-out but also for liquidity and market depth once their token launches, which is critical for user confidence and price discovery. Having a committed market maker early can reduce slippage, enable more robust trading, and signal to other investors that the project is serious about managing its token’s market microstructure.

However, multi-role investors also raise potential conflicts of interest. A firm that is both a seed investor and a market maker might have incentives that differ from those of long-term token holders, especially around short-term price movements or listing strategies. Communities and founders therefore need to carefully structure agreements and governance mechanisms to ensure that liquidity providers are aligned with sustainable growth rather than opportunistic trading. The same logic applies to other liquidity-focused backers, including proprietary trading firms and derivatives platforms that invest seed capital in protocols they intend to trade on. Transparency around roles and expectations is crucial.

a16z leads Ornn's $33M seed round to build financial markets for AI compute, introducing GPU price indices, futures, and capital products for data center investors

CoreWeave already proved GPUs can be collateral when it raised $2.3B against H100s in 2023; Ornn is trying to make that underwriting repeatable instead of bespoke. If OCPI and token-cost indices get liquid enough for forwards, Akash/Render-style DePIN compute stops being just spot capacity plus emissions and starts looking like hashprice markets for AI: hedgeable revenue, explicit depreciation, and a cleaner way to finance racks without pretending every GPU is perpetual scarce collateral.

- 2023-02milestone

Lens Protocol raises $15M seed from 30+ VCs, angels, and DAOs

- 2023-09launch

Mountain Protocol closes $4M seed round for yield-bearing stablecoin

- 2024-01regulatory

BlackRock Bitcoin spot ETF approved; SEC filing discloses $100K seed from statutory underwriter

- 2024-06milestone

Standard Chartered unit SBI Holdings commits $100M to crypto startups across seed through Series C

- 2025-03launch

Miden raises $25M seed led by a16z Crypto, Hack VC, and 1kx

- 2025-11launch

Catena Labs closes $18M seed led by a16z to build AI-native bank on crypto rails

Seed Rounds Across Segments: Case Studies and Patterns

Seed rounds are not monolithic; they look very different in an AI research lab, a DeFi protocol, a trading infrastructure startup, or a consumer-facing wallet or game. Examining patterns across segments can clarify how seed funding functions in practice and how AI, crypto, and traditional finance are converging.

AI and crypto/finance convergence

One of the most striking trends of the current cycle is the overlap between AI and financial technology, including crypto. Aether AI’s 20 million dollar seed round to build causal world models exemplifies the deep-tech end of this spectrum. The company, founded by a UC San Diego researcher, is developing AI systems designed to understand causal relationships in physical environments, targeting robotics and physical AI systems where machines must reason about the effects of their actions rather than merely predict outcomes from historical data. Such foundational research demands substantial seed capital to fund a large research team, computational infrastructure, and early partnerships, even before monetization is fully defined.

By contrast, Ralo’s 2.9 million dollar seed round reflects an applied AI approach focused on a specific vertical: mortgage brokerage. Ralo claims its AI-native platform can reduce mortgage rates by an average of 0.6 percentage points and cut closing times from industry norms down to 15–17 days, using AI to optimize lender matching, underwriting, and workflow automation. This is a much more targeted thesis, with a clearer near-term commercial model, which justifies a smaller seed round. Both examples illustrate how seed capital is underwriting experiments at different depths of the AI stack.

In crypto and finance, AI is increasingly used to drive trading, risk management, and prediction markets. AlphaNet, which raised a 10 million dollar seed round led by Joffre Capital, is building an institutional-grade quantitative AI trading platform that aims to bridge traditional quantitative strategies with digital asset markets. The company’s seed funding is earmarked for building infrastructure that can ingest vast datasets, deploy AI models, and interface with exchanges and on-chain venues in an institutional-compliant manner. Fortune Protocol’s seed round, focused on AI-powered prediction markets on BNB Chain, similarly blends AI and Web3 by using machine learning to help users make better-informed bets and to structure markets more efficiently. These projects underscore how seed rounds are financing the intersection of AI reasoning, algorithmic trading, and on-chain markets.

DeFi, trading, and on-chain markets

DeFi and trading infrastructure remain core domains for crypto seed activity. Seed capital here is often used to fund smart contract development, audits, liquidity incentives, and partnerships with other protocols and exchanges. Coinbase Ventures’ backing of Tenor Labs’ 2.5 million dollar seed round for an on-chain fixed-rate lending protocol is an example of a seed-stage project tackling a fundamental financial primitive: the ability to borrow or lend at predictable interest rates. Fixed-rate lending requires careful design of interest rate markets, collateral systems, and risk management, all of which must be encoded in smart contracts that can withstand adversarial environments. Seed funding allows the team to experiment with interest rate models, build front-ends, and attract early liquidity providers.

On-chain proprietary trading platforms like Hypernova, built on derivatives-focused venues such as Hyperliquid, also raise pre-seed and seed rounds to build novel trading experiences, including esports-style live trading competitions. These projects must design both the trading infrastructure and the game mechanics that keep users engaged, a dual challenge that fits well with seed-stage risk capital. SizeProp’s pre-seed financing to build infrastructure for crypto prop trading similarly illustrates how early-stage money backs the building blocks of complex trading ecosystems.

Prediction markets like those pursued by Fortune Protocol add another dimension by allowing users to trade on event outcomes, blending elements of derivatives, information markets, and sometimes regulatory scrutiny. Seed funding here supports both the technical foundation and the careful navigation of regulatory frameworks that may treat some prediction markets as off-limits if they resemble unregulated gambling or financial instruments. AI-driven features, such as prediction assistance and risk scoring, complicate and enrich the product but also increase the technical demands on the team.

Infrastructure, wallets, and consumer applications

Infrastructure and consumer applications form the other major clusters of crypto seed activity. Kulipa’s 6.2 million dollar seed round for stablecoin-native card issuing infrastructure highlights how critical middle-layer services are to crypto’s mainstream adoption. By enabling fintechs and wallets to launch white-label payment cards that directly draw on stablecoin balances, without those fintechs needing to manage card operations internally, Kulipa is bridging stablecoin rails with traditional payment networks. Seed funding is used to build APIs, secure partnerships with card issuers and processors, and ensure compliance with payment regulations across jurisdictions.

Wallets and access tools are another fertile area. A lightweight wallet targeting feature phones, backed in a seed round co-led by Tether and Gnosis, aims to minimize app size (on the order of 10MB) while still supporting secure custody and transaction capabilities on low-resource devices. The goal is to make crypto accessible in environments where smartphones and high-speed data are not ubiquitous, a mission aligned with stablecoin issuers’ interest in expanding global usage. Mirage, which raised seed funding and launched a closed alpha for private stablecoin transfers, represents a more experimental infrastructure play: its privacy-preserving technology for stablecoin transfers promises greater confidentiality but also raises questions about regulatory acceptance and technical robustness. Some investors and commentators have expressed concern that unproven privacy tech at seed stage could expose users and backers to outsized risk if not carefully vetted.

Consumer-facing applications range from gaming and creator platforms to memecoins and social experiences. PixieChess, which raised a 5.2 million dollar seed round led by Paradigm, illustrates how gaming projects combine on-chain assets with traditional game loops; its thesis revolves around vibecoded, composable game creation in an AI and blockchain-infused environment. Another example is Uniblock, which raised 5.2 million dollars in seed funding (part of a total 7.5 million dollars raised) to unify blockchain infrastructure and simplify developers’ interactions with multiple chains. Consumer-focused memecoins, such as the Vegas memecoin raising capital to expand licensed IP, original content, and esports-style tournaments, take a more culturally driven approach, but they still use seed funding to hire teams, secure licensing deals, and build community infrastructure.

Together, these cases show that seed rounds support a wide spectrum of risk and ambition, from deep infrastructure to playful consumer apps. The common thread is that at seed stage, none of these projects are proven; investors are betting on vision, team, and early signs of traction, knowing that many will never reach a Series A or large token market.

Valuations, Risks, and Governance Implications

Seed rounds crystallize not just capital structures but power dynamics, valuation expectations, and governance trajectories. Founders and investors must grapple with how much ownership to trade for early capital, how high to set valuations in the face of uncertain markets, and how to embed safeguards for communities and long-term protocol health.

The valuation ladder from seed to growth

Valuations at seed stage are as much art as science, especially in volatile sectors like crypto and AI. Aggregate data provides a rough ladder: Outlier Ventures’ 2024 report suggests median Web3 pre-seed, seed, and Series A round sizes of 2.5 million, 5.6 million, and 17.6 million dollars respectively, implying a rough scaling of capital as projects mature. Carta’s data that AI seed valuations average 17.9 million dollars pre-money, 42 percent higher than non-AI startups, underscores that thematic enthusiasm can lift valuations even when fundamental metrics are sparse. Late-stage rounds like Standard Bots’ 200 million dollar Series C at a one billion dollar valuation demonstrate how companies that do succeed in scaling can command very large valuations.

In crypto, token markets can both inform and distort valuation ladders. A protocol that launches a token shortly after seed might achieve a fully diluted valuation in the billions based on speculative trading, even if its actual revenue or user numbers remain modest. This creates a disconnect between private and public valuations and can complicate subsequent equity or token rounds. Conversely, protocols that delay token launches and stick to equity rounds might appear under-valued relative to heavily traded peers, even if their fundamentals are stronger. The fundraising cycles of companies like Circle—with a reported multi-billion dollar valuation for its Arc Blockchain initiative—and prediction markets like Kalshi, which reportedly reached a 22 billion dollar valuation after a large raise, have sparked debate about whether such valuations are sustainable and what they imply for earlier-stage pricing.

These dynamics feed back into seed negotiations. If founders and investors expect that a successful project could quickly achieve a nine- or ten-figure token valuation, they may push for higher seed valuations. While this can be rational in some cases, it also increases the risk of “overpriced seed” rounds where the company has little room to grow into its valuation before hitting a wall at Series A or experiencing a down round. Seed investors must therefore balance optimism about technology and markets with sober assessments of execution risk and the likelihood of future capital availability.

Dilution, cap tables, and community ownership

Every seed round reshapes the cap table: the distribution of ownership among founders, team, investors, and, in crypto, the community via tokens. Excessive dilution at seed can demotivate founders and limit the equity pool available for future hires, especially if the company needs several more rounds of financing. Conversely, under-diluting at an inflated valuation can create unrealistic expectations and make it harder to attract strong lead investors at Series A who may balk at re-pricing the company downward.

In crypto, these cap table decisions intersect with token allocations. A project might allocate, for example, a certain percentage of tokens to the team and investors, another portion to a community or ecosystem fund, and the rest to future incentives or treasury. If seed investors receive both equity and a significant share of tokens, their total economic stake may be very large, potentially overshadowing that of the community. This can backfire when the token launches and users perceive the distribution as unfair, leading to backlash or apathy. Dev fund restructurings, in which previously community-oriented pools of tokens are reallocated or governance constraints loosened, have also raised alarms that long-term development commitments can be quietly altered after the fact.

For founders, thoughtful design of both equity and token ownership at seed is crucial. It is often better to accept slightly more dilution in equity in exchange for preserving more flexible token allocations for community and ecosystem development. Investors who truly believe in decentralization and long-term network growth may be willing to compromise on token share in favor of more sustainable models. Transparent communication about vesting, lockups, and governance rights at seed stage can build trust with future users, which is essential for protocols that rely on community participation.

Regulatory and technological risk at seed stage

Seed rounds in crypto face higher layers of regulatory and technological risk compared with many other sectors. On the regulatory side, the classification of tokens, the legality of certain market structures (such as prediction markets or high-leverage derivatives), and evolving rules around KYC/AML and data privacy all affect the viability of seed-stage projects. For example, projects like Fortune Protocol, operating AI-powered prediction markets on BNB Chain, must navigate whether their markets could be interpreted as unregulated gambling or financial instruments in certain jurisdictions. Privacy-focused stablecoin transfer platforms like Mirage risk running afoul of financial surveillance and anti-money-laundering regulations if their tools are perceived as enabling illicit activity, and they must also prove their cryptography and implementation are robust to avoid catastrophic exploits.

Technologically, seed projects often push the limits of what is possible, especially in AI–crypto fusion domains. Aether AI’s causal world models must prove that their fundamental scientific approach yields practical advantages in robotics and physical AI before they can justify the very large seed investment. AlphaNet’s AI trading systems must perform reliably in both traditional and crypto markets, facing adversarial conditions, market regime changes, and the complexity of integrating with multiple exchanges and on-chain venues. Infrastructure like Kulipa must ensure transactional security and resilience while interfacing with both blockchain and card network systems, where failures can have immediate financial consequences.

These risks underscore the importance of rigorous due diligence at seed stage, both by investors and by founders evaluating potential backers’ sophistication and support capabilities. For investors, it is not enough to be excited about a theme; they must understand the technical and regulatory contours of the specific project. For founders, choosing investors who bring relevant domain expertise and who are willing to support the project through inevitable regulatory and technical challenges can be more important than securing the highest possible valuation.

- Smart-contract / TechnicalHigh

Seed-stage code is pre-audit and often pre-mainnet; the gap between whitepaper and production-grade security is where the majority of capital losses originate in early-stage crypto projects.

SAFE-plus-token-warrant structures widely used in crypto seed rounds remain under active SEC scrutiny over whether the token warrant leg constitutes an unregistered securities offering.

Seed allocations typically carry 12–24 month lockups with a one-year cliff, leaving investors unable to exit during adverse market conditions that may materialize well before unlock.

Early-stage cap tables concentrate token supply among a small founding team and a handful of VCs, creating governance capture risk and predictable price-impact events at TGE unlock.

Web3 fundraising data shows that the majority of seed-stage projects either fail to reach TGE or launch into unfavorable market conditions that erase seed-price returns; vintage year dominates individual project quality as a predictor of outcome.

Practical Guidance for Founders and Investors

Given the complexity of seed rounds in crypto, both founders and investors benefit from a disciplined approach to structuring, storytelling, and decision-making. While each situation is unique, some recurring patterns can serve as guideposts.

Designing a credible seed story and structure

For founders, the first task is to articulate a clear seed-stage narrative. Investors at this stage know that financial projections are speculative, but they expect clarity on the problem being solved, why it matters, why now, and why this team is uniquely suited to tackle it. In crypto, this narrative should also explain why blockchain is necessary or beneficial, how tokens (if any) fit into the model, and how the project plans to navigate regulatory and security challenges. Projects like Fortune Protocol that blend AI and prediction markets must articulate not only how AI improves user outcomes but also why a decentralized, on-chain setup is superior to a centralized platform. Infrastructure startups like Kulipa must show how their product unlocks new capabilities—such as stablecoin-native cards for fintechs—that cannot be easily replicated without blockchain.

Choosing the right financing structure is equally important. Founders should consider whether a priced equity round, SAFE with token warrant, or other instrument best aligns with their stage and needs. If the company is pre-revenue but has strong technical talent and early traction, a SAFE with a reasonable valuation cap and clear token warrant terms may allow them to avoid premature pricing while still attracting quality investors. If the project is further along, with clear revenue or user growth and a defined token plan, a priced round can provide clarity and trigger conversion of earlier instruments. In all cases, founders should model how different structures impact dilution, token allocations, and runway.

Running a raise in crypto: networks, platforms, and community

Seed rounds in crypto are as much about relationships and networks as about term sheets. Founders often leverage accelerator programs, hackathons, and ecosystem grants to gain initial visibility and credibility. Events like the Colosseum hackathon, which offers pre-seed funding to AI agent projects, or ecosystem-specific accelerators on chains like Solana and Ethereum, can be effective on-ramps to a later seed round, especially when combined with mentorship and technical support. Y Combinator’s use of USDC on Solana to deliver seed funding demonstrates how even mainstream accelerators are embedding crypto rails into their workflows, which can also serve as a signaling device for investors that a project is serious and globally minded.

Founders should also think beyond traditional VC when raising seed capital. Exchange venture arms, protocol treasuries, and stablecoin issuers may provide strategic seed funding aligned with ecosystem goals, as seen with Coinbase Ventures backing DeFi lending projects or Tether and Gnosis supporting wallets and infrastructure that deepen stablecoin and Ethereum usage. However, these strategic investors often have specific expectations around integration, go-to-market strategies, or network choice, which founders must be comfortable with. Community funding, whether through small token sales, NFT drops, or DAO-managed grants, can complement VC capital but also adds governance and communication responsibilities.

Equally crucial is transparent communication with prospective investors and, where appropriate, the community. Seed investors will want to understand how future funding, token launches, and potential exits might play out. They will also want comfort that the project takes security, compliance, and risk management seriously. For community-facing projects, founders must explain early on how seed investors fit into the token and governance landscape, to avoid perceptions of unfair insider advantage later. Open-source development, public roadmaps, and clear token documentation can all help.

Evaluating a seed deal as an investor

For investors, evaluating seed deals in crypto requires a blend of traditional venture assessment skills and domain-specific knowledge. The usual questions—about team quality, market size, competitive differentiation, and execution risk—remain central. But investors must also consider token design, regulatory exposure, and on-chain evidence of traction.

In AI–crypto convergence projects like AlphaNet or Fortune Protocol, investors should assess the robustness of AI models, the defensibility of data pipelines, and the quality of the team’s quantitative and engineering talent. For DeFi protocols, security practices, audit plans, and mechanisms for handling incidents are critical. Infrastructure plays like Kulipa require due diligence on banking relationships, card issuer partnerships, and compliance frameworks. Wallets and consumer apps like lightweight feature-phone wallets or Mirage’s private stablecoin transfers must be evaluated not only for UX but also for their ability to operate within regulatory bounds and to secure users’ funds.

Investors should also scrutinize deal structures. SAFE plus token warrant deals need careful reading to understand the share of tokens allocated to investors, vesting schedules, and rights in governance. Valuation caps on SAFEs must be benchmarked not just against peers but against realistic expectations of progress before the next financing event. Priced equity rounds should be reviewed for standard protective provisions, board composition, and any unusual clauses that might disadvantage either party later.

Finally, investors should evaluate alignment with other backers. Strategic investors like Coinbase Ventures, Solana Ventures, Tether, or Gnosis can be powerful allies but may also shape the project’s direction. Market-making investors like DWF Labs bring liquidity but may have different time horizons. Understanding how these pieces fit together—and how they affect governance and exit paths—is essential before committing capital.

Outlook

Seed rounds will remain the crucible where the next generation of crypto, AI, and financial infrastructure is forged. Despite debates about the “death” of pre-seed or the sustainability of late-stage valuations, the fundamental role of seed capital—to underwrite experimentation at the frontier of technology and markets—has not changed. What is changing is the toolkit: on-chain data, programmable tokens, instant stablecoin payouts, and globally distributed accelerators are reshaping how founders raise and how investors deploy at this stage.

For crypto specifically, the interplay between AI and Web3, the rise of ecosystem and corporate strategic capital, and the gradual mainstreaming of on-chain infrastructure suggest that seed rounds will become even more structurally diverse. Some will look like traditional priced equity financings; others will be hybrid equity-token deals anchored to future network launches; still others will be partially community-funded or DAO-governed. Founders and investors who understand the mechanics, risks, and strategic possibilities of seed rounds in this environment will be better positioned to build enduring protocols and companies rather than short-lived speculative flashes.

Latest Seed Round news

AI analytics platform Polysights raises $1.5M pre-seed funding to combat insider trading in prediction markets. The raise was backed by YZi Labs S3, Maven 11 Capital, and angels from Kraken and Consensys, plus grants from Polymarket and AWS.Mirendil raises $200m seed round led by a16z to build AI that automates AI engineering worka16z leads Ornn's $33M seed round to build financial markets for AI compute, introducing GPU price indices, futures, and capital products for data center investors Sazabi's $8M seed round and beta launch mark a major leap toward autonomous self-healing software

Sazabi's $8M seed round and beta launch mark a major leap toward autonomous self-healing softwareSources

- https://www.investopedia.com/articles/personal-finance/102015/series-b-c-funding-what-it-all-means-and-how-it-works.asp

- https://www.crv.com/content/seed-funding-vs-series-a

- https://outlierventures.io/article/2024-in-review-fundraising-in-web3/

- https://www.hubspot.com/startups/fundraising/preseed-vs-seed-funding

- https://carta.com/learn/startups/fundraising/priced-rounds/

- https://hashedem.substack.com/p/safe-token-warrant-meta

- https://carta.com/data/ai-fundraising-trends-2024/

- https://www.paradigm.xyz

- https://www.coinbase.com/ventures/news

- https://startupintros.com/orgs/solana-ventures

- https://theaiinsider.tech/2026/06/19/aether-ai-raises-20m-in-seed-round-funding-to-build-causal-world-models/

- https://www.housingwire.com/articles/ralo-ai-mortgage-broker-seed/

- https://x.com/solsticefi/status/2067535773830926820

- https://x.com/DWFLabs/status/2067415756183413070

- https://www.prnewswire.com/news-releases/standard-bots-raises-200-million-series-c-at-1-billion-valuation-to-scale-american-made-ai-native-industrial-robots-302795268.html

- https://defi-planet.com/2026/05/fortune-protocol-secures-seed-funding-to-expand-ai-powered-crypto-prediction-markets/

- https://x.com/join_ef/status/2044812956936909257

- https://www.finextra.com/newsarticle/47529/kulipa-raises-62m-for-stablecoin-native-card-issuing-infrastructure-platform

- https://chainwire.org/2026/04/15/quantitative-ai-trading-platform-alphanet-raises-10m-seed-round-led-by-joffre-capital/

- https://www.instagram.com/p/DYazulpmZe2/

Community notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…