In-depth explainer on Kalshi, the CFTC-regulated prediction market and crypto perps venue, covering its products, regulation, legal battles, integrations, and relevance for crypto traders and DeFi prediction platforms.

+34 sources across the wider coverage universe

DOJ and CFTC move to block Arizona’s prosecution of Kalshi, arguing its sports and election event contracts qualify as regulated financial swaps under federal law2026-04

DOJ and CFTC move to block Arizona’s prosecution of Kalshi, arguing its sports and election event contracts qualify as regulated financial swaps under federal law2026-04 Fox News to integrate sponsored prediction market odds from Kalshi2026-04

Fox News to integrate sponsored prediction market odds from Kalshi2026-04 Kalshi to launch parent portal and AI checks to stop underage users exploiting ID loopholes on prediction markets2026-04

Kalshi to launch parent portal and AI checks to stop underage users exploiting ID loopholes on prediction markets2026-04 Crypto.com enters prediction markets via High Roller partnership, targeting $1T opportunity and challenging platforms like Kalshi and Polymarket with US-based event contracts2026-04

Crypto.com enters prediction markets via High Roller partnership, targeting $1T opportunity and challenging platforms like Kalshi and Polymarket with US-based event contracts2026-04 Polymarket, Kalshi, and Hyperliquid face bipartisan House scrutiny as CFTC signals incoming prediction market rules2026-04

Polymarket, Kalshi, and Hyperliquid face bipartisan House scrutiny as CFTC signals incoming prediction market rules2026-04 Meta reportedly builds points-based Arena prediction market app to rival Polymarket and Kalshi2026-06

Meta reportedly builds points-based Arena prediction market app to rival Polymarket and Kalshi2026-06

Kalshi: A Regulated Prediction Market Bridging Crypto, Derivatives, and Real-World Events

Kalshi is a federally regulated prediction market and derivatives exchange that lets traders buy and sell event-linked contracts on everything from macro data and elections to crypto prices and sports, operating as a designated contract market (DCM) overseen by the US Commodity Futures Trading Commission (CFTC). Built to look and feel like a modern trading venue rather than a gambling site, it now dominates US event-contract volume and is rapidly expanding into perpetual futures tied initially to crypto assets, while drawing growing attention from regulators, institutional partners, and competitors across both TradFi and crypto.

Origins and Regulatory Status of Kalshi

Kalshi was founded to answer a question that had long hovered at the edge of both derivatives and crypto circles: could prediction markets be recognized not as gray-area betting platforms, but as regulated financial exchanges built around event-based risk? The company pursued the most conservative possible route, applying to the CFTC for designation as a contract market, the same status enjoyed by major futures venues such as CME Group. In 2020, the CFTC granted KalshiEX LLC an order of designation as a DCM, formally bringing event contracts into the scope of US derivatives regulation when listed on its platform. This designation placed Kalshi under core principles for exchanges, including requirements around fair access, market surveillance, and protection against manipulation, and distinguished it sharply from offshore or purely crypto-native prediction protocols that operate outside US federal oversight.

From the outset, Kalshi emphasized that it was an exchange, not a sportsbook, and that its products were engineered as financial instruments for hedging and speculation rather than entertainment wagers. The firm’s marketing and user interface nevertheless resembled modern retail brokerage apps, making it intuitive for individual traders to express views on yes/no outcomes, but the legal infrastructure behind the scenes followed futures-market norms: participants faced KYC checks, trading rules, position limits, and surveillance akin to what they would encounter at any other CFTC-regulated marketplace. This combination of consumer-facing simplicity and institutional-grade regulation quickly attracted attention from both retail users and established market participants.

Over its first several years, Kalshi expanded its menu of event contracts across macroeconomic releases, policy decisions, politics, and financial markets, effectively creating a standardized way to trade “Will X happen by Y date?” as a dollar-denominated derivative. By mid-2020s reporting, it had grown into the dominant US venue for event contracts, with one industry summary attributing to Kalshi more than 90% of domestic activity in this segment. This scale coincided with a broader resurgence of interest in prediction markets across crypto and TradFi, as decentralized venues like Polymarket grew their global user bases and traditional brokerages and exchanges began experimenting with all-or-nothing options that closely resemble event contracts.

The company’s maturation into a significant revenue-generating business further reinforced its status as a core institutional player rather than a niche crypto side-bet. By 2026, reporting from The Information indicated that Kalshi had surpassed $2 billion in annualized revenue, roughly tripling its run rate from only months earlier as trading volumes intensified across its markets. That same coverage reported that Kalshi had closed a Series F round at around a $22 billion valuation and entered informal talks with investment banks about a potential IPO, though any listing was framed as a late-2020s prospect rather than an imminent event. In a sector where many prediction platforms have remained small, lightly regulated, or experimental, Kalshi’s regulatory status and revenue scale marked a break from the past.

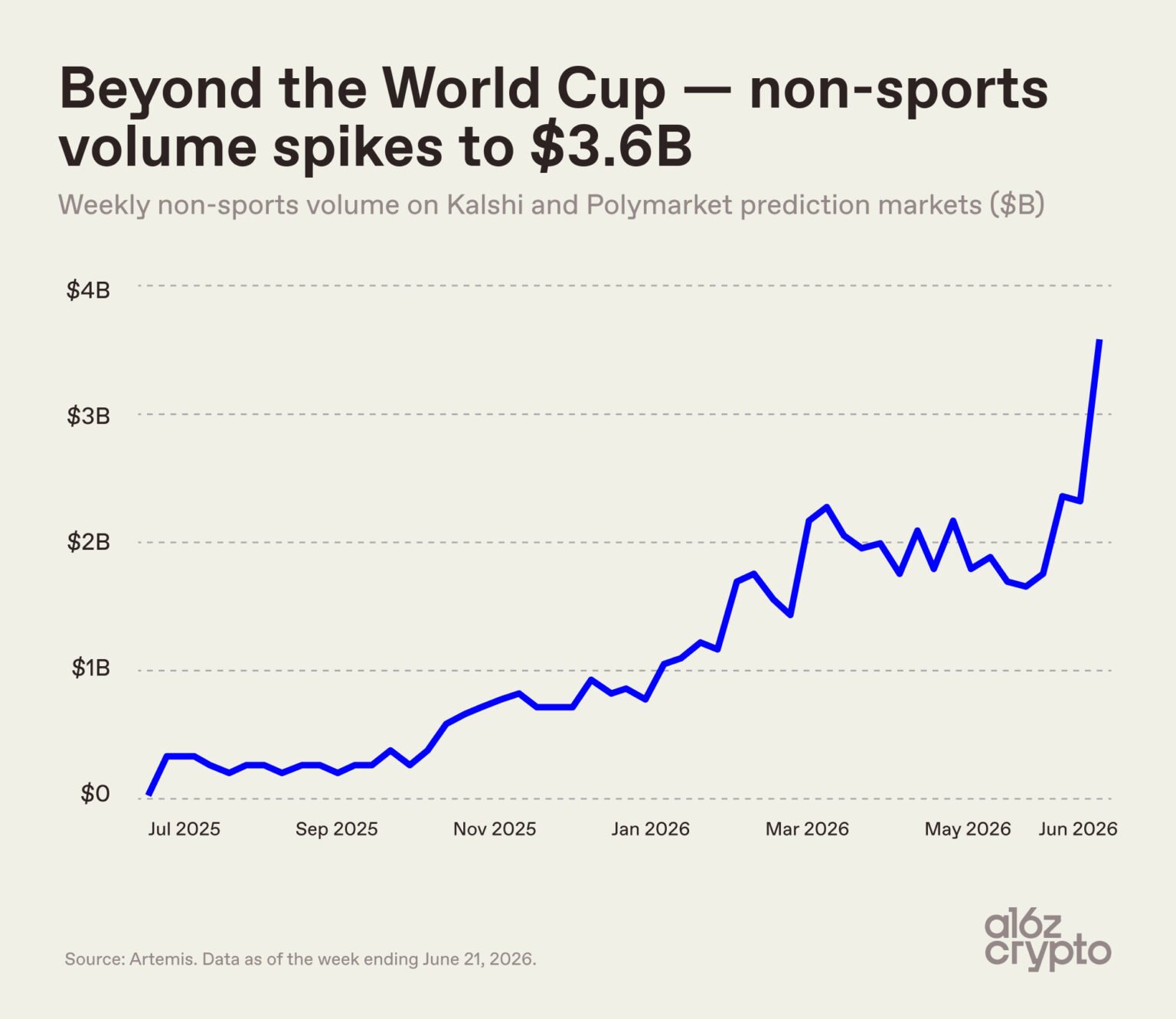

Kalshi and Polymarket non-sports volume hits $3.6B in a week, up 18x since July

a16z crypto says Kalshi and Polymarket cleared $3.6B of non-sports prediction-market volume last week across politics, economics, geopolitics, and current events. That category was around $200M per week in July 2025, so the move is roughly 18x in under a year. World Cup markets may be sucking oxygen, but the sharper signal is that non-sports prediction markets are turning into the real growth engine.

Readers click Kalshi not for trading mechanics but for the jurisdictional war it embodies: federal regulators say prediction markets are swaps, 20+ states say they are unlicensed gambling, and whoever wins that fight determines whether a regulated, Wall Street-backed forecasting layer can exist in America.↗

How Kalshi’s Prediction Markets Work

Understanding Kalshi begins with understanding event contracts. At their core, event contracts are binary derivatives that pay a fixed amount, typically \(1\) US dollar, if a defined future event occurs, and \(0\) if it does not. On Kalshi, each contract is tied to a precisely specified outcome—such as whether the Federal Reserve will hike rates at a particular meeting, whether a certain inflation print will fall within a range, or whether Bitcoin will be above a threshold at a given timestamp. Traders can buy or sell these contracts at prices between \(0.01\) and \(0.99\) dollars, with the price representing the market’s implied probability of the event occurring, abstracting away from fees and risk preferences.

If a trader buys a contract at \(0.40\), for example, they are effectively betting that the event has more than a 40% chance of occurring: if the event happens, they receive \(1\), realizing a profit of \(0.60\); if it does not, they lose the \(0.40\) they paid. If instead a trader sells the contract at \(0.60\), they profit if the event does not occur and the contract expires at \(0\), while they lose \(0.40\) per contract if it does occur. Because the payoff is fixed and the price is bounded, event contracts have a clearly defined maximum gain and loss, giving them a profile akin to very short-term, binary options rather than open-ended futures.

Kalshi’s markets cover a wide range of themes. Macroeconomic markets allow users to trade on outcomes such as CPI prints, nonfarm payrolls, interest-rate decisions, or GDP figures, which are directly relevant to both TradFi and crypto risk managers. Political markets capture electoral outcomes and legislative milestones, while financial markets include event contracts on indices or asset levels at specific times, such as whether the S&P 500 or Bitcoin crosses a threshold over an hourly window. In each case, the contract specs define the reference data source, observation window, and resolution criteria, which are crucial for minimizing ambiguity and disputes.

From a market-microstructure standpoint, Kalshi operates an order book where limit orders and market orders meet, similar to a traditional exchange. Market participants can provide liquidity by posting bids and offers at various prices, and as trading flows in, the evolving price reflects a consensus estimate of the event’s likelihood. Because the contracts are standardized and fully collateralized, settlement is straightforward: after the event is resolved based on predefined rules and reference sources, the exchange credits winning positions with \(1\) per contract and debits losing positions accordingly. Margin requirements ensure that traders have sufficient funds to cover potential losses, aligning with CFTC core principles and reducing counterparty risk.

For crypto-focused traders, Kalshi’s model is conceptually familiar from on-chain prediction markets and DeFi platforms. Protocols like Polymarket similarly allow users to buy and sell outcome tokens representing “Yes” or “No” on a given event, with prices conveying an implied probability and liquidity provided through automated market makers or order books. The difference is primarily in jurisdiction and infrastructure: whereas Polymarket operates on public blockchains and has faced CFTC enforcement actions resulting in US restrictions, Kalshi is a centralized, KYC-based platform operating as a regulated exchange under federal law. For many US-based market participants, this makes Kalshi a legally safer avenue to express event-driven views than offshore or purely DeFi alternatives.

Kalshi’s positioning as a venue for both speculation and hedging is central to its narrative. Firms exposed to specific risks—such as a startup whose revenue is highly sensitive to Fed rate decisions, or a crypto business whose income is tied to Bitcoin’s price—can use event contracts to manage that risk more precisely than with broad futures or options, by targeting the exact contingency that matters to them. At the same time, individual traders can use the markets as a way to monetize information and opinions about politics, macro, or crypto, turning qualitative forecasts into tradable positions. The result is a marketplace where information, incentives, and regulation intersect.

Kalshi’s Expansion into Perpetual Futures

While event contracts defined Kalshi’s early identity, the company has increasingly moved into territory that looks more familiar to crypto derivatives traders: perpetual futures. In 2026, Kalshi launched a suite of never-expiring futures contracts tied to crypto assets, quickly generating significant volume and sparking a broader debate about the overlap between prediction markets, traditional derivatives, and the fast-growing perpetual swap markets in crypto.

Perpetual futures, often called “perps” in crypto, are derivatives with no fixed expiry date. Instead of settling on a preset date like a conventional futures contract, perps remain open indefinitely, with a funding mechanism used to keep the contract’s price anchored to a reference index. If the perp trades above the reference price, long positions pay a periodic funding fee to short positions; if it trades below, shorts pay longs. This design, popularized by crypto exchanges, allows traders to hold directional exposure indefinitely without rolling over futures contracts, making it one of the dominant instruments in crypto derivatives markets.

Kalshi’s crypto perpetuals follow this general pattern but incorporate institutional benchmarks for pricing and settlement. The exchange uses indices from CF Benchmarks, a regulated benchmark provider that aggregates data from multiple regulated exchanges to produce robust, manipulation-resistant reference prices. For Bitcoin, Kalshi relies on the Bitcoin Real-Time Index (BRTI), which updates every second and is already widely used in institutional contexts. By tying its perps to these benchmarks, Kalshi aligns its products with broader efforts to professionalize and standardize crypto pricing.

At launch, Kalshi’s perpetual futures lineup focused on a set of major crypto assets, with contracts structured around standard sizes such as 1 or 10 units of the underlying. Early reporting indicated that the exchange listed eleven perpetual contracts exclusively tied to crypto tokens, with more than $5.5 billion in trading volume recorded during the first two weeks after launch. This rapid uptake underscored the appetite among both existing Kalshi users and crypto-native traders for products that combined the flexibility of perps with the regulatory framework of a US DCM.

The new products also drew the attention of data and infrastructure providers. Crypto analytics firm The Block, for instance, announced that it had begun tracking Kalshi’s perpetual swaps on its dashboards, positioning itself as the first crypto data provider to monitor these instruments in real time. This integration signaled that Kalshi’s perps were not merely an add-on but had become a relevant part of the broader crypto derivatives landscape, warranting coverage alongside on-exchange and on-chain perpetual markets.

From a strategic perspective, Kalshi’s leadership has articulated plans to extend perpetual futures beyond digital assets, leveraging the same funding and index-based design for other asset classes. This could eventually include perps tied to equity indices, commodities, or macro variables, blurring the line between traditional futures exchanges and prediction markets. In doing so, Kalshi is positioning itself as a venue where traders can access a spectrum of instruments—from discrete event contracts to continuous directional perps—under one regulatory umbrella.

However, this expansion has not been frictionless. The introduction of perpetual futures on Kalshi and on other platforms such as Coinbase prompted CME Group to sue the CFTC, challenging the regulator’s decision to allow these types of contracts to be offered outside the traditional futures complex. The lawsuit reflects competitive tensions in US derivatives markets and raises questions about how innovative instruments—especially those that originate in crypto—will be partitioned between incumbent exchanges and newer, more specialized venues. For crypto traders, the outcome of this dispute may shape where and how regulated perps can be traded in the US in the years ahead.

- 01CFTC vs state jurisdiction clash↗

The core tension — a federal court blessing election contracts while states issue restraining orders and sue for illegal gambling — created a live legal cliffhanger readers followed across multiple headlines.

- 02Election market accuracy vs gambling label

Readers engaged with whether money-backed crowd forecasts outperform Wall Street economists, because the answer justifies or condemns the entire product category.

- 03Institutional and 401k adoption↗

Headlines about ARK Invest hedging, Galaxy Digital liquidity, and Robinhood pushing event contracts into retirement accounts signaled Kalshi crossing from niche to mainstream finance.

- 04Arbitrage mechanics between platforms

The specific 12–20% monthly return figure in a cross-platform arbitrage explainer attracted readers seeking actionable edge rather than narrative.

- 05State-level crackdowns and cease orders↗

Each new state action — Nevada freeze, Tennessee cease order, Washington lawsuit as the 20th state — read as an escalating countdown that kept readers checking back.

- 06Volume rivalry with Polymarket↗

Concrete volume numbers ($2.74B Kalshi vs $1.44B Polymarket in September) gave readers a scoreboard to track which regulated or crypto-native model was winning.

Ecosystem, Integrations, and Institutional Adoption

Kalshi’s trajectory has increasingly been defined not just by its own platform, but by its integrations with a wider ecosystem of brokers, fintechs, and trading technology providers. These partnerships are crucial for bringing prediction markets and event-linked derivatives into the workflows of both retail and professional traders who might not otherwise seek out a standalone venue.

Retail-focused brokerages have been among the first movers. Webull, a popular trading app, now offers users the ability to trade hourly predictions on S&P 500, Nasdaq, Bitcoin, and Ethereum movements, as well as Federal Reserve events, through a product powered by Kalshi. Webull emphasizes that Kalshi is the first CFTC-regulated exchange to offer prediction markets, framing the integration as a way to give users access to “unique” instruments for managing intraday market risk. In practice, this means that Webull customers can take event-driven positions—such as whether Bitcoin will be above or below a certain price at a specific hour—without leaving their existing brokerage interface, while the underlying contracts are executed on Kalshi’s exchange.

Robinhood, another major retail brokerage, has similarly introduced prediction markets that let users trade views on real-world events ranging from sports to politics to economics. While Robinhood’s public materials do not always foreground Kalshi by name, public statements from regulators have described Robinhood as an affiliate or partner in Kalshi-linked prediction offerings, particularly in the context of state-level scrutiny over sports-related event contracts. For users, the result is similar: prediction markets appear alongside stocks, options, and crypto trading, making event contracts part of a broader order-entry experience rather than a separate silo.

Beyond retail brokerage channels, Kalshi is also integrating into professional trading infrastructure. Trading Technologies (TT), a long-standing provider of futures and derivatives trading software, announced that it would support trade execution on Kalshi, enabling its institutional clients to access US-regulated prediction markets through the TT platform. According to the announcement, trading connectivity to Kalshi is expected to go live with the full suite of execution and algorithmic tools TT provides, positioning Kalshi as the first of several regulated prediction markets that TT plans to support. This integration is notable because TT caters to professional traders, prop shops, and institutions that are already active in futures and options, potentially bringing event contracts and Kalshi perps into quantitatively driven, cross-asset strategies.

Data and analytics providers are also building around Kalshi’s markets, particularly its perpetual futures. As noted earlier, The Block’s decision to track Kalshi’s perps reflects a broader recognition that these products carry sufficient liquidity and relevance to warrant inclusion in crypto market dashboards. For market participants who rely on such data aggregators to monitor liquidity and price dynamics across venues, this kind of coverage lowers the barrier to incorporating Kalshi into their analytic and trading frameworks.

At the same time, Kalshi has pursued capital markets milestones that signal its institutional ambitions. As previously noted, the company has reportedly reached more than $2 billion in annualized revenue and raised a substantial Series F round, valuing it at around $22 billion. These developments underpin reports that Kalshi is in early-stage talks with investment banks about a possible IPO in the late 2020s, though no firm timeline has been set and any listing would depend on market conditions, regulatory clarity, and continued growth. For institutional investors watching the intersection of TradFi and crypto, Kalshi’s potential path to the public markets could offer a direct equity exposure to the growth of regulated prediction markets and crypto-linked perps.

Kalshi’s ecosystem positioning is also shaped by its role in a competitive field that now includes both crypto-native platforms and major incumbents. Coinbase has partnered with Kalshi on certain offerings, including sports-related prediction products that became the subject of state-level enforcement actions. Meanwhile, Charles Schwab, in collaboration with Cboe Global Markets, has announced plans to launch “all-or-nothing” options tied to the S&P 500, a product that effectively moves Schwab into the prediction market arena alongside Coinbase, Robinhood, Polymarket, and Kalshi. These yes/no S&P contracts resemble event contracts in payoff structure and may compete for the same user demand to express binary views on market outcomes, highlighting how prediction-like instruments are being adopted by some of the largest names in brokerage and exchange infrastructure.

The result is a complex and increasingly interlinked ecosystem. Kalshi serves as the CFTC-regulated core for event contracts and perps; retail brokerages plug into it to offer prediction products within familiar interfaces; professional trading systems integrate it into multi-exchange workflows; and data providers surface its markets alongside other crypto derivatives. This structure mirrors, in some ways, the role of centralized exchanges in the broader crypto landscape, where liquidity pools align around a few core venues that then power a range of front ends and analytics tools.

DraftKings launches proprietary prediction markets exchange DKeX as annualized consumer volume tops $3.4B, intensifying competition with Polymarket and Kalshi

$11.3B annualized trading volume off one DraftKings Predictions week puts sportsbook UX directly against Kalshi’s CFTC wrapper and Polymarket’s crypto-native CLOB. Sportsbooks already know how to acquire and retain retail at scale; crypto’s edge is composable settlement and open books, and that pitch gets shakier when Polymarket research is finding 1.95M reverted match-order txs and $1.78B at risk from off-chain match/on-chain settle gaps. If DKeX owns the fiat funnel while Kalshi owns regulatory precedent, Polymarket has to prove liquidity quality beats on-chain branding.

Legal and Regulatory Controversies

Despite its status as a CFTC-regulated exchange, Kalshi has become a focal point in ongoing legal and policy battles over the boundary between financial derivatives and gambling, particularly around sports-related and crypto-linked contracts. These disputes involve not only federal regulators but also state attorneys general, consumer protection bodies, and incumbent exchanges.

A key flashpoint has been whether certain event contracts—especially those tied to the outcomes of sports contests—should be treated as legitimate derivatives for hedging and risk management, or as entertainment wagers subject to state gambling laws rather than federal commodities regulation. A coalition of 41 state attorneys general, for example, submitted a formal comment to the CFTC arguing that sports-related event contracts are essentially entertainment gambling and therefore fall outside the CFTC’s jurisdiction. The attorneys general urged the federal regulator to reaffirm that authority over such contracts belongs to the states, warning that allowing them to proliferate as futures-like products could undermine state gambling frameworks and consumer protections.

State-level enforcement actions have followed. In Kentucky, Attorney General Russell Coleman filed lawsuits against Kalshi, Polymarket, and other platforms, alleging that they were operating unlicensed and illegal sports betting and gambling services in violation of the state’s laws. The complaint against Kalshi and its affiliates, including Coinbase, asserts that the companies allow users to place wagers on game winners, point spreads, and player statistics without obtaining a Kentucky gaming license or complying with state regulations. According to the lawsuit, Coinbase partners with Kalshi to offer sports-related markets on its platform, sharing in the fees generated by each bet, and thus participates in unlicensed sports gambling.

The Kentucky lawsuits also argue that Kalshi, Polymarket, and associated entities such as Robinhood and Webull provide inadequate resources for users to identify or seek help for problem gambling, failing to meet the consumer-protection requirements mandated under Kentucky law. In response to concerns like these, Kentucky enacted the Wagering Consumer Protection Act, which prohibits licensed sports wagering operations from contracting with Kalshi or Polymarket once it takes effect, effectively seeking to wall off state-sanctioned betting from federally regulated or offshore prediction markets. This legislative move illustrates how states are using both litigation and statutory tools to assert control over sports-related prediction products, even when those products are traded on a federally regulated exchange.

Kalshi has also drawn attention from consumer protection and advertising watchdogs. The Better Business Bureau’s National Advertising Division referred Kalshi to regulators after the company declined to participate in an inquiry into its influencer marketing disclosures. The inquiry reportedly focused on whether Kalshi adequately disclosed material connections with influencers promoting the platform, and the referral signals that regulators may scrutinize not only the legality of specific products but also how prediction markets are advertised to retail users. In a sector where retail speculation can easily cross into gambling-like behavior, such marketing scrutiny is likely to intensify.

At the federal level, Kalshi’s evolving product set has raised questions within the derivatives community itself. CME Group’s lawsuit against the CFTC, challenging the agency’s approval of Kalshi’s and Coinbase’s perpetual futures offerings, reflects concerns that new, crypto-inspired instruments are encroaching on the domain of traditional futures exchanges. From CME’s perspective, allowing perps with certain structures outside the established futures complex may create regulatory inconsistencies or competitive imbalances. From the perspective of crypto firms and prediction markets, the lawsuit underscores the difficulty of fitting novel derivatives into an older regulatory framework while still permitting innovation.

For Kalshi, navigating these parallel fronts—state-level gambling law challenges, federal jurisdiction debates, advertising scrutiny, and competition-driven lawsuits—is now a central strategic risk. The company’s core defense rests on its status as a CFTC-designated contract market with rules and surveillance systems designed to treat event contracts and perps as financial instruments rather than wagers. Yet as the Kentucky cases show, federal compliance is not always a shield against state enforcement, especially where sports and retail users are involved. The ultimate resolution of these disputes will have significant implications not only for Kalshi, but for the broader trajectory of prediction markets and crypto-linked derivatives in the US.

CFTC formally blocks Kalshi election contracts

- 2024-09regulatory

DC Circuit rules CFTC exceeded authority; election markets go live

Kalshi hits $2.74B monthly volume, surpassing Polymarket

- 2025-01regulatory

Tennessee orders Kalshi to cease sports contracts by Jan 31, refund deposits

- 2025-06regulatory

Nevada court issues 14-day restraining order over unlicensed gambling claim

Robinhood launches NFL/NCAA prediction markets via Kalshi partnership

Washington sues Kalshi, becomes 20th state to challenge prediction markets

Kalshi launches perpetual futures with $5.5B debut volume; IPO talks reported

Market Integrity, Surveillance, and Insider Trading

A critical part of Kalshi’s pitch to regulators and institutional partners is that it can run prediction markets with robust safeguards against manipulation, insider trading, and fraud. This challenge is more complex for event contracts than for traditional equities or futures, because the underlying “asset” is a discrete event whose outcome may be influenced by non-public information or by the actions of specific individuals or organizations.

Kalshi’s rulebook explicitly prohibits insider trading in event markets. The company defines insider trading as trading on material non-public information relating to an event contract, including by individuals who have access to such information before it becomes public, employees or affiliates of agencies that serve as sources for contract data, and decision-makers or those with direct or indirect influence over the outcome of the underlying event. For example, a staffer at a government agency who knows a macroeconomic release before it is published, or a corporate insider who can influence a key decision that is the subject of a market, would be barred from trading on that information. These definitions echo traditional securities and derivatives law but applied to the specific context of event contracts.

Beyond insider trading, Kalshi’s rules prohibit any fraudulent, abusive, manipulative, or deceptive trading practices. Traders are barred from making material misstatements or omissions in connection with their trading activity, or engaging in any practice that operates as a fraud or deceit upon other participants. These provisions are designed to address concerns that prediction markets could be used to launder money, manipulate public perception, or coordinate misinformation campaigns around sensitive events such as elections, economic data releases, or major crypto protocol upgrades.

To enforce these rules, Kalshi has invested in market surveillance infrastructure and partnerships. The company has announced that it is working with external software providers to enhance its surveillance capabilities, with the goal of detecting suspicious trading patterns, coordinated manipulation, or insider activity across its markets. This collaboration has been framed as part of Kalshi’s broader response to increased scrutiny from both US state regulators and the CFTC, which have signaled that they expect prediction markets to uphold high standards of market integrity given the potential sensitivity of the events being traded. By adopting surveillance tools similar to those used on established futures and equities exchanges, Kalshi positions itself as a credible, institutionally aligned venue rather than an experimental or lightly monitored platform.

Kalshi’s internal policies have also evolved in response to specific concerns. Industry reporting and regulatory commentary have highlighted worries about “fraud rings” and coordinated schemes to exploit prediction markets, particularly in areas where small groups might have outsized influence over outcomes. In response, Kalshi has introduced additional safeguards, including requiring traders to disclose their employers when trading in certain high-risk markets. The goal is to identify and flag situations where a trader’s professional role could give them access to material non-public information or control over an event’s outcome, enabling more targeted monitoring and enforcement.

According to company statements and third-party reporting, Kalshi has referred multiple suspected cases of insider trading or rule violations to regulators, indicating an active enforcement stance rather than a passive posture. This pattern aligns with its attempt to reassure regulators that a robust compliance culture can coexist with the speculative, sometimes politically sensitive nature of prediction markets. For crypto users accustomed to largely anonymous, permissionless trading on DeFi platforms, these measures may feel restrictive, but they also represent the cost of operating within the US regulatory perimeter.

The focus on integrity extends to the perpetual futures side as well. While perps are not event contracts in the strict binary sense, they are tied to indices and reference prices that can be vulnerable to manipulation, particularly in thin or fragmented markets. By relying on CF Benchmarks indices, which aggregate data from multiple regulated exchanges and are subject to benchmark regulation, Kalshi aims to reduce the risk that a single venue’s anomalies or wash trading could distort the settlement price of its perps. Combined with surveillance and position limits, this approach seeks to make Kalshi’s crypto perps more resilient and transparent than many offshore alternatives, at the cost of requiring KYC and tighter oversight.

Comparing Kalshi, Polymarket, and Crypto-Native Prediction Platforms

For a crypto news audience, the natural question is how Kalshi compares with decentralized or offshore prediction markets like Polymarket, as well as with emerging TradFi-style products such as Schwab and Cboe’s all-or-nothing options. The answer hinges on regulatory posture, user experience, product design, and risk profile.

Polymarket runs on public blockchains and allows users to trade outcome tokens tied to real-world events, often using stablecoins and interacting through non-custodial wallets. Its markets have covered a wide range of topics, from political elections to crypto protocol milestones and macroeconomic data, and it has become a widely cited source of crowd-implied probabilities in media and analysis. However, Polymarket has also faced CFTC enforcement actions for offering event contracts to US persons without registering as a designated contract market or swap execution facility, leading to fines and restrictions on its US-facing activities. While it continues to operate globally, Polymarket’s regulatory status is fundamentally different from Kalshi’s.

By contrast, Kalshi was built from the ground up as a direct-access, federally regulated exchange under US commodities law. US traders must complete KYC, and the platform is subject to ongoing CFTC oversight, including rulebook approvals, market surveillance requirements, and reporting obligations. This structure provides legal clarity and greater protections for US-based users and institutional partners but reduces anonymity and permissionless access. It also constrains the types of markets Kalshi can list, especially when state regulators or the CFTC determine that certain events—such as some sports-related outcomes—should not be treated as bona fide hedging instruments.

Meanwhile, new entrants from traditional finance, like Schwab and Cboe’s planned yes/no S&P 500 options, sit somewhere in between. The all-or-nothing options are essentially binary options tied to index levels, offering a payoff structure similar to event contracts but embedded within a conventional options framework. Schwab’s move into this space places it alongside Coinbase, Robinhood, Polymarket, and Kalshi in what is increasingly seen as a “prediction markets” sector, even though each player’s legal and technical architecture differs. For users, the distinctions may matter less than the basic functionality: the ability to express a binary view—“will the S&P close above X?”—through a simple, leveraged payoff.

The table below summarizes some of the key contrasts relevant to a crypto-focused audience:

| Feature | Kalshi | Polymarket | Offshore Crypto Perps Venue (Generic) |

|---|---|---|---|

| Regulatory Status | CFTC-designated contract market (US) with event contracts and perps regulated as derivatives. | Has faced CFTC enforcement; operates globally but with US restrictions; not a registered US exchange. | Typically unregulated or lightly regulated offshore; varies by jurisdiction. |

| Access and KYC | Full KYC/AML; US residents allowed subject to rules. | Wallet-based, on-chain; often geofences US users after enforcement. | Often allows pseudonymous accounts with minimal KYC. |

| Settlement Infrastructure | Centralized exchange infrastructure; fiat and stablecoin rails; uses institutional benchmarks for perps. | Smart contracts on public blockchains; uses on-chain oracles. | Centralized order book; may use internal indices with varying transparency. |

| Product Scope | Event contracts across macro, politics, markets, sports (subject to legal limits), plus crypto perps. | Event markets across many topics, including politics and crypto; no regulated perps. | Mainly perpetual swaps and futures on crypto; limited event markets. |

| Target Users | US retail, sophisticated traders, and institutions via integrations (Webull, Robinhood, TT). | Global crypto users comfortable with DeFi; often non-US after geofencing. | Global speculative traders; high leverage focus. |

For crypto traders deciding where to allocate capital or derive signals, these distinctions are significant. Kalshi offers the comfort of US regulation and integration with mainstream brokers, but requires identity verification and operates within a narrower regulatory perimeter. Polymarket and on-chain platforms offer openness and global access, but with higher legal and regulatory risk for US participants, and sometimes less formalized governance around insider trading or market manipulation. Offshore perps venues offer deep liquidity and high leverage but come with their own counterparty and jurisdictional risks.

Importantly, these platforms are not mutually exclusive. Kalshi’s markets can be used as inputs into DeFi protocols or quantitative strategies, either through manual integration or via data providers that aggregate odds and prices from multiple sources. Conversely, on-chain prediction prices may inform how traders position on Kalshi or hedging strategies around event-driven perps. Over time, the information layer—where probabilities from different sources are synthesized—may become as important as any single venue.

Meta reportedly builds points-based Arena prediction market app to rival Polymarket and Kalshi

Meta is reportedly building a standalone app called Arena after Zuckerberg tasked a small internal team with cloning the prediction-market behavior driving Polymarket and Kalshi. The first version would use points instead of real-money wagering, but Meta has not ruled out monetized participation later and reportedly views the product as a top priority. The irony is obvious: after Forecast died in 2022, Meta is circling back just as prediction markets move from crypto niche to mainstream attention.

At least 20 U.S. states have filed suits or cease orders treating Kalshi's event contracts as unlicensed gambling, creating jurisdictional conflict with its CFTC-regulated federal status.

Kalshi opened 200 insider-trading investigations after the CFTC publicly vowed prosecution, indicating the information-edge problem in political markets is structural, not anecdotal.

- Liquidity / retail-vs-algorithmMedium

A small cohort of algorithmic traders captures most profits while retail participants consistently lose, making the platform's liquidity depth dependent on continued institutional participation.

- CentralizationMedium

Paradigm — Kalshi's largest backer — simultaneously built its own prediction-market trading terminal while holding a board seat, creating a conflict of interest at the governance level.

Kalshi operates as a CFTC-designated contract market with centralized custody; it announced blockchain expansion but the core settlement layer is not a decentralized smart-contract system.

An ad-watchdog referral for refusing to cooperate with an influencer-advertising inquiry adds a compliance surface risk that is minor relative to the regulatory litigation load.

Use Cases for Crypto Traders and Investors

For a crypto-oriented audience, Kalshi’s relevance is not limited to its crypto perpetual futures. The platform’s broader menu of event contracts offers several ways for traders, investors, and builders in the digital asset space to manage risk, express views, and gather information.

One straightforward use case is hedging event-specific risk that is not easily covered by conventional derivatives. Crypto companies, funds, or DAO treasuries often have significant exposure to macro and regulatory events that are only indirectly correlated with BTC or ETH prices. Federal Reserve policy decisions, US inflation data, or major legislative votes can dramatically impact crypto markets, yet hedging these events purely through crypto futures or options is imprecise. Kalshi’s contracts on Fed meetings, CPI ranges, or other macro data releases offer a way to isolate and hedge those binary or discrete outcomes directly. A crypto fund worried about a surprise rate hike, for example, could buy event contracts that pay out if the Fed raises rates, partially offsetting anticipated losses in risky assets.

Another use case is speculating on crypto-specific milestones and price levels using a different payoff profile than standard perps or options. Kalshi’s hourly markets on Bitcoin and Ethereum levels, offered through integrations like Webull, allow traders to bet on short-term price direction with fully bounded downside and upside, rather than the variable PnL of leveraged perps. For some users, this can be a more intuitive way to express short-term conviction, particularly when combined with macro or policy markets that shape crypto’s near-term trajectory.

Kalshi’s crypto perps themselves present a distinct proposition for traders who value regulatory clarity and benchmark quality. Because these perps are tied to CF Benchmarks indices and operate on a CFTC-regulated exchange, they may appeal to institutions that are restricted from trading on offshore venues but want continuous directional exposure to BTC, ETH, and other tokens. In theory, such institutions could use Kalshi’s perps as part of basis trades, hedging, or structured products that require a regulated foundation. For sophisticated individual traders, the appeal lies in combining perps and event contracts in one environment, enabling complex strategies such as hedging a long Bitcoin perp with a short event contract on a negative regulatory ruling, or vice versa.

Information extraction is a third major use case. Prediction markets tend to produce probability estimates that are forward-looking and continuously updated, often incorporating dispersed information faster than traditional polling or analyst reports. Crypto treasuries, DeFi protocols, and on-chain governance participants can use Kalshi’s markets as an input into their decision-making—monitoring odds on macro events, elections, or regulatory developments that could influence protocol revenues, user growth, or legal risks. For example, a DAO contemplating expansion into the US might pay attention to Kalshi markets on key regulatory milestones or elections relevant to crypto policy, using those signals to time or calibrate their initiatives.

Finally, Kalshi and similar platforms can serve as a bridge between TradFi and crypto participants. Traders who are comfortable with options, futures, and perps in traditional markets may find Kalshi’s event contracts a natural extension, with a payoff structure that maps cleanly onto their existing playbooks. Conversely, crypto-native traders versed in DeFi perps and on-chain prediction markets may see Kalshi as a regulated complement, offering overlapping exposures in a compliant venue. Over time, this bidirectional flow of users and strategies may be one of the most important ways prediction markets deepen the connection between digital assets and mainstream finance.

Conclusion

Kalshi occupies a distinctive and increasingly influential position at the intersection of prediction markets, crypto derivatives, and regulated US financial infrastructure. As a CFTC-designated contract market, it has transformed event contracts from a legal gray area into a formally recognized class of derivatives when traded on its exchange, while simultaneously expanding into perpetual futures that borrow heavily from crypto market design. In doing so, it has built a platform where traders can express binary views on macro, politics, markets, and sports, and where crypto traders can access both event contracts and regulated perps tied to institutional benchmarks.

The company’s growth—measured in revenue, volume, and market share—underscores the demand for such instruments. Reporting that Kalshi has surpassed $2 billion in annualized revenue, commands over 90% of US event contract activity, and is exploring IPO possibilities demonstrates that prediction markets can be more than niche curiosities or DeFi experiments; they can be substantial businesses at the heart of a new asset class. Partnerships with Webull, Robinhood, Coinbase, Trading Technologies, and data providers like The Block further integrate Kalshi into both retail and institutional trading ecosystems.

At the same time, Kalshi’s trajectory highlights the unresolved regulatory tensions surrounding prediction markets and crypto-linked derivatives. State attorneys general and gambling regulators argue that sports-related event contracts are entertainment betting that should fall squarely under state jurisdiction, leading to lawsuits and new legislation aimed at constraining platforms like Kalshi and Polymarket. CME Group’s lawsuit against the CFTC over the approval of perpetual futures offered by Kalshi and Coinbase reflects a different, industry-driven confrontation over how new derivatives should be governed and who gets to list them. These conflicts underscore that the legal status of prediction markets is still evolving, even when platforms operate under federal oversight.

Facing these pressures, Kalshi has invested heavily in market integrity, surveillance, and compliance. Its rulebook’s explicit insider trading prohibitions, efforts to enhance surveillance through software partnerships, and policy changes such as employer disclosure in high-risk markets signal a willingness to meet regulators at least halfway in erecting safeguards around sensitive event trading. For crypto users accustomed to permissionless, pseudonymous markets, these measures may feel constraining, but they also differentiate Kalshi from both offshore prediction sites and lightly regulated venues, positioning it as a potential long-term bridge between crypto-native innovation and traditional regulatory expectations.

For the crypto ecosystem as a whole, Kalshi represents both an opportunity and a test case. It shows one path by which crypto-inspired products—such as perps and event markets—can be brought into the US regulatory perimeter, integrated with mainstream brokers, and scaled into multi-billion-dollar businesses. It also illuminates the trade-offs involved: between openness and compliance, between global access and jurisdictional constraints, and between rapid experimentation and the slower pace of rulemaking and legal adjudication. How Kalshi navigates its next phase—expanding beyond crypto perps, managing legal challenges, deepening institutional ties, and potentially going public—will help shape the future of prediction markets and their place in both crypto and TradFi.

Outlook

Looking ahead, Kalshi sits at a crossroads that is highly relevant to crypto traders, builders, and investors. On one side is the continued expansion of its product suite, particularly in perpetual futures and potentially in new asset classes beyond digital tokens. If Kalshi successfully extends perps into equities, rates, or commodities while maintaining CFTC approval, it could emerge as a hybrid exchange that blurs traditional category boundaries, making event contracts and perps interchangeable tools in cross-asset strategies. For crypto users, this would mean a single, regulated venue where macro, political, and crypto exposures can be traded in a unified framework.

On another side is the regulatory and legal landscape, which remains fluid and contentious. The outcome of state-level lawsuits like those in Kentucky, the AG coalition’s pressure on the CFTC over sports-related contracts, and CME’s litigation over perps will determine how much room Kalshi and similar platforms have to innovate. A favorable resolution could create a more defined, albeit narrower, perimeter within which prediction markets can flourish as hedging and speculative tools. An adverse one could force retrenchment in certain areas, especially sports, and push some activity back to offshore or on-chain platforms.

For crypto-native prediction markets and derivatives venues, Kalshi’s evolution will serve as a reference point. If a regulated exchange can sustain robust liquidity in event contracts and crypto perps while satisfying US regulators, it will strengthen arguments that more crypto infrastructures should move into the regulatory light. Conversely, if regulatory frictions constrain Kalshi’s growth or limit its product scope too sharply, some market participants may continue to prefer DeFi platforms and offshore exchanges, accepting higher legal and counterparty risks in exchange for flexibility and global reach.

In the near to medium term, the most likely scenario is coexistence. Kalshi will continue to grow as a regulated hub for US-facing event contracts and crypto perps, integrated into major brokerages and trading systems, while on-chain and offshore platforms capture more permissionless, global flows. For a crypto news audience, monitoring Kalshi’s markets—both as trading venues and as indicators of crowd expectations—will remain a valuable lens on the intersection of macro, regulation, and digital assets. As prediction markets mature from curiosities into core financial infrastructure, Kalshi’s trajectory will be one of the key stories to watch.

Latest Kalshi news

Kalshi and Polymarket non-sports volume hits $3.6B in a week, up 18x since JulyDraftKings launches proprietary prediction markets exchange DKeX as annualized consumer volume tops $3.4B, intensifying competition with Polymarket and KalshiMeta reportedly builds points-based Arena prediction market app to rival Polymarket and Kalshi TurboFlow raises $6M seed led by Pantera Capital to build the "Kalshi of APAC," targeting Asia's underserved prediction markets sector with localized onchain trading products

TurboFlow raises $6M seed led by Pantera Capital to build the "Kalshi of APAC," targeting Asia's underserved prediction markets sector with localized onchain trading productsSources

- https://kalshi.com

- https://www.cftc.gov/PressRoom/PressReleases/8302-20

- https://www.bloomberg.com/news/articles/2026-06-16/kalshi-aims-to-expand-perpetual-futures-after-5-5-billion-debut

- https://www.theinformation.com/articles/kalshi-passes-2-billion-annualized-revenue-early-ipo-talks

- https://www.facebook.com/CoinMarketCap/posts/latest-charles-schwab-is-working-with-cboe-global-markets-to-roll-out-all-or-not/1430143249143064/

- https://bitcoinfoundation.org/news/prediction-markets/kentucky-sues-kalshi-polymarket-over-sports-betting/

- https://x.com/ReutersLegal/status/2067730351510733116

- https://kalshi.com/market-integrity/insider-trading

- https://tradingtechnologies.com/news-releases/trading-technologies-to-enter-prediction-markets-with-support-for-trade-execution-on-kalshi/

- https://www.law360.com/articles/2487023/ad-watchdog-refers-kalshi-for-refusing-influencer-ad-inquiry

- https://kentucky.gov/Pages/Activity-stream.aspx?n=AttorneyGeneral&prId=1944

- https://help.kalshi.com/en/articles/15357566-what-perpetuals-are-available-on-kalshi

- https://www.webull.com/trading-investing/prediction-markets

- https://www.si.com/prediction-markets/reviews/kalshi-vs-polymarket

- https://cryptorank.io/news/feed/28add-prediction-market-kalshi-eyes-ipo

- https://robinhood.com/us/en/prediction-markets/

- https://x.com/TheBlockCo/status/2067639484254945547/photo/1

- https://www.tradingview.com/news/cointelegraph:36af98ac1094b:0-kalshi-adds-software-partner-as-it-looks-to-boost-prediction-market-surveillance/

- https://www.youtube.com/watch?v=S2g0TwfecJE

- https://oag.maryland.gov/News/Pages/Attorney-General-Brown-Urges-CFTC-to-Recognize-State-Authority-Over-Sports-Related-Prediction-Markets--.aspx

Community notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…