In‑depth explainer on how gambling, prediction markets, and crypto intersect, covering Polymarket, Kalshi, Robinhood, UK regulation, global crackdowns, AML risks, and the blurring line between trading and betting.

+15 sources across the wider coverage universe

Hyperfinancialisation: On the rise and ouroboric nature of gambling and financialisation. This piece was written as an accompaniment to long degeneracy.2025-12

Hyperfinancialisation: On the rise and ouroboric nature of gambling and financialisation. This piece was written as an accompaniment to long degeneracy.2025-12 A UK man has been sentenced to 33 months after embezzling $650K from his employer and converting it into crypto for gambling. Experts warn that crypto-related white-collar crime is rising, but blockchain transparency can aid detection.2025-12

A UK man has been sentenced to 33 months after embezzling $650K from his employer and converting it into crypto for gambling. Experts warn that crypto-related white-collar crime is rising, but blockchain transparency can aid detection.2025-12 Connecticut regulators issued stop-orders to Kalshi, Robinhood, and Crypto com for allegedly running unlicensed online gambling disguised as prediction markets. Officials say the platforms pose consumer risks and must halt services immediately.2025-12

Connecticut regulators issued stop-orders to Kalshi, Robinhood, and Crypto com for allegedly running unlicensed online gambling disguised as prediction markets. Officials say the platforms pose consumer risks and must halt services immediately.2025-12 Robinhood CEO slams UK’s 'Backwards' crypto stance, comparing It to regulated gambling.2024-11

Robinhood CEO slams UK’s 'Backwards' crypto stance, comparing It to regulated gambling.2024-11 Massachusetts investigates Robinhood for linking March Madness Prediction Market to brokerage accounts, citing youth gambling concerns.2025-03

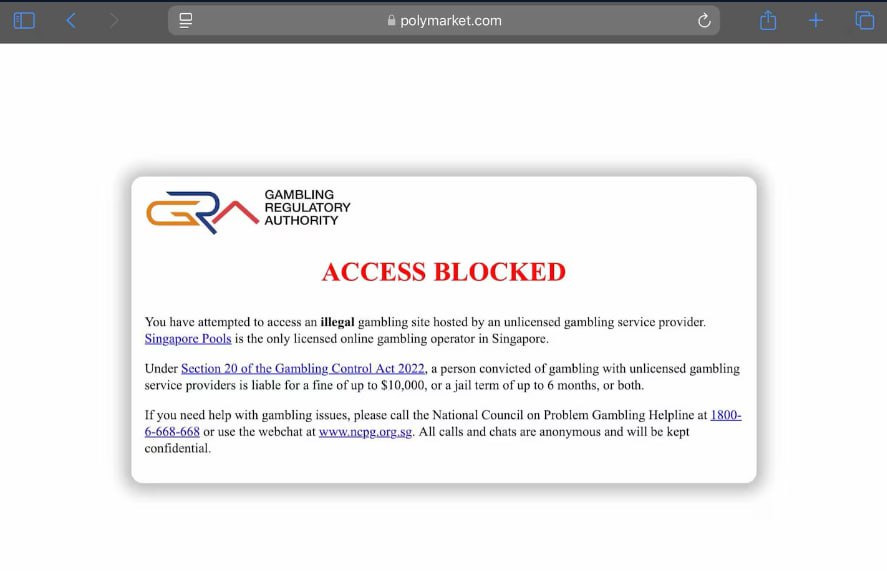

Massachusetts investigates Robinhood for linking March Madness Prediction Market to brokerage accounts, citing youth gambling concerns.2025-03 Singapore declares Polymarket illegal gambling, blocks access amid global crackdown.2025-01

Singapore declares Polymarket illegal gambling, blocks access amid global crackdown.2025-01

Gambling, Prediction Markets, and Crypto: An Evergreen Explainer

Gambling is the staking of something of value on an uncertain outcome in the hope of gain, with full awareness that loss is possible or even likely. As crypto, prediction markets, and hyper‑financialised trading platforms proliferate, this simple idea now reaches far beyond casinos and sportsbooks into exchanges, decentralized apps, and brokerage apps that look increasingly like gambling venues with an order book attached.

What Is Gambling? Core Concepts and Definitions

Gambling has a long and cross‑cultural history, but most modern legal systems converge on a relatively precise definition. Encyclopaedia Britannica describes it as the betting or staking of something of value on the outcome of a game, contest, or other uncertain event, undertaken with consciousness of risk and the hope of gain. This captures three essential elements: there must be consideration (something of value put at risk), an uncertain event outside the bettor’s full control, and a prize or payout that depends on that event. The structure applies equally to a roulette spin, a sports bet, a lottery ticket, or a crypto‑denominated wager on an on‑chain casino. It is this formal structure, rather than the specific technology used, that drives how regulators classify activity as gambling rather than investment or entertainment.

From a legal and economic perspective, gambling is distinguished less by the asset being staked and more by the nature of the risk being taken. Where the expected return is negative on average, and participants are primarily paying for excitement or entertainment rather than long‑term financial gain, policymakers are more likely to treat the activity as gambling and to apply consumer‑protection and harm‑reduction frameworks. At the same time, the boundary between gambling and financial speculation is porous. Even Britannica acknowledges that stock markets can be described as a form of gambling in a broad sense, albeit one in which knowledge and skill can matter significantly more than in games driven almost entirely by chance. This conceptual ambiguity lies at the heart of current disputes over crypto‑based prediction markets, meme‑coin trading, and leveraged derivatives platforms that feel to many users like digital casinos with tickers attached.

In economic theory, gamblers and traders face similar mathematical structures. Both confront uncertain future states of the world and decide how much of their wealth to expose to outcomes with known or estimated probabilities. The concept of expected value, variance, and risk preference applies equally well to a sportsbook parlay and to a leveraged Bitcoin long. Yet law and social norms treat these practices very differently. Financial speculation is often viewed as productive or at least tolerable when it supports capital formation or risk transfer, while gambling is frequently framed as a vice to be constrained, taxed, or channeled into regulated environments. The crypto ecosystem, with its blend of high‑beta assets, 24/7 markets, and gamified interfaces, forces stakeholders to continually renegotiate where that line should be drawn.

Legal and Economic Definitions

Legal definitions of gambling tend to focus on formal elements rather than specific technologies or asset classes. Many US state statutes, for example, define unlawful wagering as staking something of value on a “contingent future event” not under the bettor’s control, a formulation that has recently been applied to everything from sports betting markets to federally regulated event‑contract exchanges. Arizona’s criminal case against Kalshi, a registered derivatives exchange, explicitly alleges that its contracts are wagers on “contingent future events,” in direct conflict with Kalshi’s position that these are financial derivatives governed by federal commodities law rather than bets covered by state gambling prohibitions. Different jurisdictions vary in how they carve out exceptions for insurance, hedging, or regulated futures, but the core concepts are surprisingly consistent.

Economists, by contrast, typically care less about doctrinal lines and more about payoff structures. In a pure gambling game, the house edge ensures that the expected value of each wager is negative for the player and positive for the operator after accounting for all odds and pay tables. In financial markets, there is no formal house edge; trading is closer to a zero‑sum game before fees, although the issuance of productive assets and long‑term economic growth can produce positive‑sum outcomes when capital is allocated well. That said, the line is increasingly blurry. High‑fee retail trading environments, ultra‑leveraged perpetual futures, and opaque prediction markets can generate effective house edges that leave retail participants in a structurally losing position. This convergence is closely tied to what researchers at the Levy Institute and elsewhere describe as financialization: a process in which financial markets, institutions, and elites gain outsized influence over economic policy, corporate behavior, and everyday life, often with distributional and stability costs.

The digital asset sector is one of the starkest embodiments of this trend. Crypto exchanges, on‑chain derivatives, and prediction markets effectively financialize everything from meme culture to elections and geopolitics. Polymarket, for example, allows traders to buy and sell binary “Yes” and “No” shares on topics ranging from sports and entertainment to public policy and tax law. A market on whether a cap on gambling loss deductions will be repealed before a specified date translates a subtle tax detail into a coin‑flippable instrument whose price reflects crowd‑sourced probabilities. Whether these contracts are treated as gambling, derivatives, or some hybrid category is not merely a semantic issue: it determines which agencies regulate them, what consumer protections apply, and where platforms are allowed to operate.

Games of Chance, Skill, and Mixed Forms

The classic triptych of gambling divides activities into games primarily of chance, primarily of skill, and mixed games where both matter. Pure games of chance, like roulette or lotteries, have outcomes determined almost entirely by randomization devices; skill cannot change the underlying probabilities, only the choice of whether and how much to bet. Skill‑dominant games, like chess or competitive esports, may involve wagering but are not themselves structurally random, which is why many jurisdictions regulate fantasy sports or poker differently from roulette or slot machines. Mixed games occupy a wide spectrum between these poles, with sports betting, poker, and many financial trading strategies falling into this category.

Crypto‑aligned gambling products increasingly sit at the intersection of these categories. On‑chain casinos often replicate pure games of chance, using verifiable randomness functions instead of physical dice, while sports‑or event‑related prediction markets invite participants to apply skill, information, and analysis to price contracts efficiently. However, even where skill can in principle improve outcomes, the distribution of information and capacity is highly unequal. Retail bettors on a Polymarket election market, a Robinhood March Madness pool, or a complex options trade may be competing against far better‑resourced institutions and insiders. Regulators worry that the veneer of skill or “investing” can make inherently risky, negative‑sum activities more socially acceptable, masking their gambling‑like nature and encouraging over‑participation, especially among younger or more vulnerable users.

The presence of skill does not, on its own, resolve the classification question. Connecticut regulators, for example, explicitly rejected the idea that event contracts on platforms like Kalshi or Robinhood’s prediction hub constitute investments, stressing instead that they are wagers regardless of how they are marketed. The Romanian gambling regulator has taken a similar stance toward Polymarket, describing its markets as “counter bets” between users that qualify as gambling despite their use of blockchain technology and advanced trading mechanics. These positions underline a core theme of the current regulatory moment: in the eyes of many authorities, it is the functional structure of risk and reward, not the sophistication of the interface or the presence of order books and order types, that determines whether activity is gambling.

Gambling, Speculation, and Investing

The distinction between gambling, speculative trading, and long‑term investing matters because it shapes not only regulation but also social attitudes and individual behavior. Traditional investing is framed around allocating capital to productive enterprises, with returns tied to underlying business performance over long horizons. Speculation and active trading lean more heavily on short‑term price movements and attempts to anticipate or exploit volatility. Gambling, in everyday language, often implies taking high risks with poor odds, typically for entertainment, thrill, or desperation rather than rational portfolio construction. In practice, these categories overlap: a meme‑coin trader on a high‑leverage derivatives exchange may believe they are investing, while regulators and mental‑health professionals might see their activity as indistinguishable from casino gambling.

Crypto’s round‑the‑clock markets, low entry barriers, and social media amplification intensify this convergence. As scholars of financialization have argued, when financial logics permeate daily life, activities that were once clearly separate from markets become sites of speculative calculation. The rise of prediction platforms where users bet on everything from presidential elections to central‑bank decisions is one manifestation of this phenomenon. So is the use of Robinhood‑style apps to trade fractional options or meme stocks in ways that resemble sports betting more closely than they resemble traditional portfolio management. Marketed as democratization and empowerment, these tools also make it easier for retail users to overtrade, over‑leverage, and underestimate risk—a pattern that regulators increasingly interpret as a public‑health and consumer‑protection concern rather than simply a matter of caveat emptor.

Hyperfinancialisation: On the rise and ouroboric nature of gambling and financialisation. This piece was written as an accompaniment to long degeneracy.

"In a hyperfinancialised economy, financial activities like speculative trading overshadow productive services which contribute more widely to society, while household wealth and inequality become increasingly tied to asset prices. to put it simply, wealth is no longer directly correlated to hard work and is disconnected from the means of production. this leads to more capital being channeled into speculative activities"

Readers are not clicking on crypto gambling as a vice story — they are clicking on the jurisdictional legitimacy war over whether prediction markets are financial instruments or illegal gambling, with Robinhood as the central defendant across multiple regulators simultaneously.↗

From Casinos to Blockchains: The Digital Evolution of Gambling

The move from physical gambling venues to online platforms reshaped the industry long before crypto arrived. Internet sportsbooks and casinos allowed users to bet from home, expanded the range of markets, and made micro‑wagering possible on previously unthinkable scales. What crypto adds is a set of payment rails and infrastructure that bypass traditional financial intermediaries, reduce friction in cross‑border transactions, and enable non‑custodial or semi‑custodial wagering systems. These traits are valued by operators and users alike, particularly in jurisdictions where gambling is tightly constrained, but they also heighten regulatory and enforcement challenges.

Online Gambling, Mobile Apps, and “Fintech‑ified” Betting

Online sportsbooks and casinos pioneered many of the digital design patterns now widely used in crypto: live dashboards, rapid-fire bet slips, in‑play micro‑markets, and retention mechanics tied to bonuses and VIP tiers. As smartphones became ubiquitous, gambling shifted further toward mobile environments, blending into the same devices and notification streams that users associate with social media and messaging. The experiential gap between placing a sports parlay and buying a speculative altcoin narrowed as both became tappable, gamified interactions executed in seconds.

Fintech platforms have increasingly imported gambling‑adjacent mechanics into trading and investing apps. Robinhood’s commission‑free model and confetti‑like interface features were widely criticized for encouraging excessive trading, with critics framing the app as “a casino on your phone” even before it began experimenting with prediction markets. Massachusetts regulators have opened investigations into Robinhood’s introduction of a prediction‑markets hub, especially its linking of March Madness wagers to brokerage accounts, citing concerns about youth exposure and the blurring of investing with gambling. Connecticut’s consumer‑protection authorities have gone further, ordering Robinhood, Kalshi, and Crypto.com to halt what they describe as unlicensed online sports gambling disguised as event contracts. These moves illustrate a broader trend: regulators increasingly scrutinize not only what people can bet on but also how those bets are framed, marketed, and integrated into other financial products.

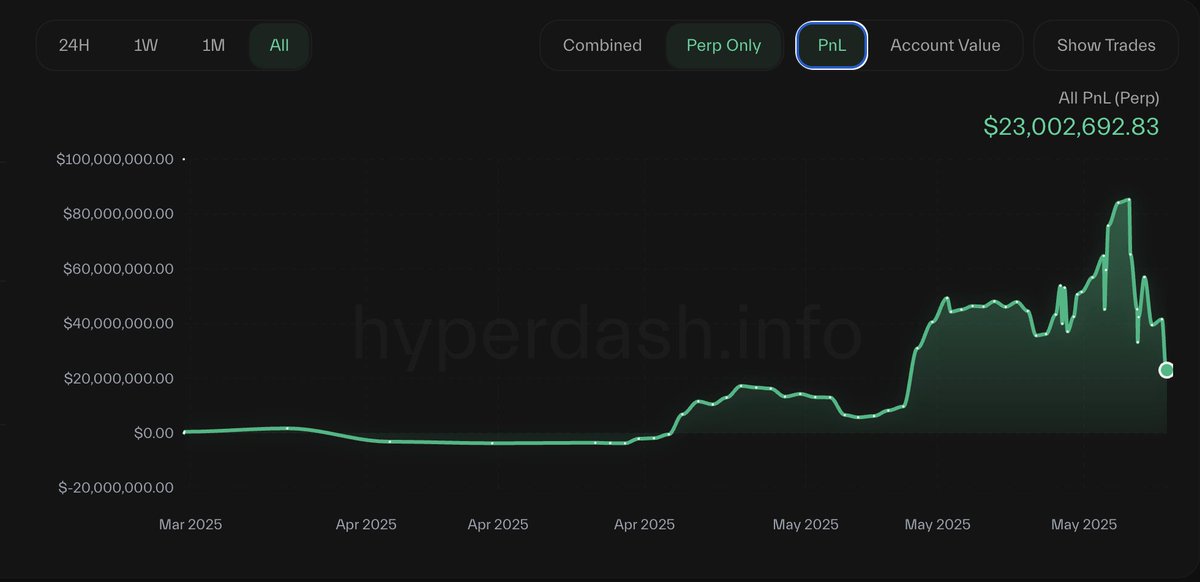

Social media has amplified these dynamics. Influencers streaming their trading, betting, or prediction‑market activity transform personal risk‑taking into entertainment content, normalizing high‑stakes behavior and potentially incentivizing copycat conduct among followers. In crypto specifically, displays of extreme leverage and massive unrealized profits or losses are common, with public liquidation levels and profit‑and‑loss screenshots serving as a form of performative bravado. When a trader publicly “longs near the top” with hundreds of millions of dollars in notional exposure and then endures multi‑million‑dollar drawdowns, the spectacle reinforces the idea of markets as arenas for gambling‑like heroics rather than spaces for measured risk management. For platforms whose business models depend on volume and churn, there is a commercial incentive to cultivate this culture, which brings them into conflict with regulators concerned about consumer protection.

Crypto Casinos and On‑Chain Betting

Crypto casinos and betting platforms leverage digital assets as both stake and payout, often with minimal onboarding friction and few formal identification checks. Academic and policy analyses note that users and operators increasingly employ cryptocurrencies and virtual private networks to circumvent national gambling regulations and access offshore online casinos. Crypto deposits can be near‑instant, borderless, and less constrained by chargeback rules or bank‑level transaction monitoring, making them attractive to operators who wish to avoid conventional payment rails. For some users, the combination of pseudonymous wallets, VPN‑obscured IP addresses, and non‑custodial platforms creates a perception of untraceability, though blockchain analytics and cross‑border cooperation are steadily eroding that assumption.

Regulators view these developments with growing alarm. The British Gambling Commission, for example, has classified cryptoassets as a high‑risk payment method in its assessments of money‑laundering and terrorist‑financing risks in the gambling sector. Its analyses emphasize that crypto can facilitate rapid cross‑border flows, makes beneficial ownership harder to determine, and can be combined with privacy‑enhancing technologies that complicate transaction tracing. Platforms that accept crypto without robust know‑your‑customer (KYC), anti‑money‑laundering (AML), and responsible‑gambling frameworks may thus become focal points for both criminal activity and consumer harm. Similarly, Romania’s gambling regulator criticized Polymarket not only for operating without a license but also for lacking fiscal reporting, player‑protection mechanisms, and AML procedures, despite substantial betting volumes tied to politically sensitive events such as national elections.

Celebrity endorsements and entertainment tie‑ins further complicate the picture. The betting brand 1win, for instance, has promoted a VIP ecosystem tied to high‑profile figures, including rapper Tyga, as it seeks to blend crypto, entertainment, and high‑tier gambling experiences. While such partnerships can boost brand visibility, they also risk normalizing high‑intensity gambling among fanbases that may skew young or financially inexperienced. Combined with crypto payment rails and aggressive VIP perks, including loss rebates and higher betting limits, this marketing strategy raises familiar questions about exploitation, informed consent, and the balance of responsibility between operators and individuals. The convergence of influencer culture, crypto wealth narratives, and gambling products is a frontier area where regulators are only beginning to formulate coherent responses.

Crypto, White‑Collar Crime, and Gambling Losses

The same attributes that make crypto useful for global, round‑the‑clock gambling also attract individuals seeking to misuse other people’s money. A case from the United Kingdom illustrates the risk starkly: a 39‑year‑old man from North Yorkshire embezzled more than £500,000 from his employer over several years, converted the funds into cryptocurrency, and used them for online gambling. He falsified financial records to disguise the thefts, and when unusual transactions were flagged, he falsely claimed they came from the sale of a personal business. Ultimately, the combination of internal investigation and blockchain‑based tracing by law‑enforcement’s economic crime unit led to his conviction and a prison sentence, with investigators specifically highlighting how crypto transactions formed part of the evidentiary trail.

Incidents like this underscore a dual reality. On the one hand, crypto‑denominated gambling can facilitate the rapid dissipation of misappropriated funds across borders and platforms, complicating recovery for victims. On the other hand, blockchain’s inherent transparency allows specialized analytics firms and law‑enforcement units to reconstruct transaction flows in ways that are impossible with cash and more laborious with traditional banking data. National gambling regulators and financial‑crime agencies increasingly cooperate with such firms, as reflected in annual crypto‑crime reports that track flows to and from high‑risk gambling venues and darknet markets. Although these reports are not themselves legal instruments, they shape regulatory priorities and enforcement strategies.

Tax treatment adds another layer of complexity. In many jurisdictions, gambling winnings are taxed differently from capital gains, and losses may be deductible only in limited fashion or not at all. This has become a live political issue in contexts where prediction markets and financialized wagering blur categories. On Polymarket, for instance, traders can bet on whether the cap on gambling loss deductions enacted in a hypothetical future tax bill will be repealed by a particular date. Market prices in such contracts express the crowd’s evolving assessment of legislative probabilities, but they also serve as a meta‑commentary on how policymakers and taxpayers perceive gambling relative to other forms of risk‑taking. If gambling losses are treated less favorably than investment losses for tax purposes, yet the underlying behaviors look increasingly similar, pressure builds for coherent definitions and consistent treatment across domains.

- 01Robinhood as gambling flashpoint↗

Three separate high-click stories cast Robinhood's CEO and platform as the face of prediction-market gambling, drawing readers tracking whether a regulated broker can operate what states call an unlicensed gambling operation.

- 02Polymarket global ban cascade↗

Singapore, France, Romania, Indonesia, Argentina, Spain, and South Korea each moved against Polymarket, giving readers a running map of which jurisdictions treat event markets as illegal gambling.

- 03US state enforcement against prediction markets↗

Connecticut, Massachusetts, and Arizona each took independent enforcement action against platforms like Kalshi and Robinhood, signalling that federal inaction has pushed the gambling-vs-finance classification fight to the state level.

- 04Crypto gambling crime and harm↗

Bitrace's crime report and the UK embezzlement sentence together showed readers that crypto's pseudonymity enables gambling-driven white-collar crime while blockchain forensics simultaneously aids prosecution.

- 05Hyperfinancialisation and degeneracy culture↗

The long-form essay and the $800M liquidation story attracted readers drawn to the meta-narrative that crypto trading and gambling have converged into a single social phenomenon with real psychological and financial casualties.

- 06Rollbit and on-chain casino narrative

The Rollbit thread highlighted how blockchain-native casinos turned gambling into a tokenised growth narrative, blurring the line between protocol investment and house-edge speculation.

Prediction Markets: Information Tools or Gambling Platforms?

Prediction markets have been a theoretical fascination for economists and technologists for decades. They promise to aggregate dispersed information about future events by allowing participants to bet on outcomes, with prices serving as real‑time probability estimates. Crypto has provided a fertile environment for implementing these ideas at scale, but it has also thrust prediction markets into the crosshairs of gambling regulators. Platforms like Polymarket and Kalshi sit at the center of an intense debate: are they innovative financial and informational infrastructures, or simply sophisticated gambling operations by another name?

How Prediction Markets Work

A typical prediction market allows users to buy and sell contracts whose payoff depends on whether a specific event occurs. These contracts are often binary: a “Yes” share pays 1 unit of currency if the event happens, and 0 if it does not, while a “No” share pays the opposite. The current market price of a “Yes” share between 0 and 1 can be interpreted as the crowd‑implied probability of the event, assuming rational traders and sufficient liquidity. If “Yes” trades at 0.11 units, the market is effectively signaling an 11 percent chance that the outcome will occur, with arbitrage opportunities for anyone who believes the real probability is substantially higher or lower.

Polymarket, an American crypto‑based prediction platform, exemplifies this model. It enables users to place bets on a wide range of future events using stablecoins and other digital assets, with markets covering sports, politics, economics, and even highly specific policy questions. In the market titled “Cap on gambling loss deductions repealed before 2027?”, traders buy “Yes” or “No” shares depending on their expectations about future tax legislation. If “Yes” is priced at 11 cents, the platform’s interface clearly explains that this corresponds to an 11 percent crowd‑sourced probability, and that a successful bet would yield 1 dollar per share at resolution. This combination of simplicity and flexible topic coverage has attracted significant trading volume and media attention.

Proponents argue that such markets produce valuable information. Academic studies have shown that, under certain conditions, prediction markets can outperform polls and expert forecasts in predicting election outcomes and other measurable events, because they incentivize participants to put money behind their beliefs and to incorporate new information quickly. In crypto contexts, prediction markets are also used as hedging tools and as on‑chain oracles, feeding resolved outcomes into smart contracts that depend on real‑world events. Nonetheless, from the standpoint of gambling law, the central fact remains: participants are staking something of value on contingent future events in the hope of profit, a structure that fits squarely within many statutory definitions of wagering.

Major Platforms: Polymarket, Kalshi, Robinhood, and Others

Polymarket’s trajectory illustrates both the appeal and the legal risks of crypto‑based prediction markets. The platform has grown into a major venue, with Romania’s National Gambling Office noting that total trading volume exceeded $600 million, including more than $16 million wagered on the Bucharest mayoral election alone. Its growth, however, has triggered pushback across multiple jurisdictions. In 2022, the US Commodity Futures Trading Commission fined Polymarket for offering off‑exchange binary options without proper registration, forcing it to restrict access for US users. More recently, Argentina ordered a nationwide block on the platform, arguing that it was operating without required approvals and thus constituted illegal gambling. Romanian authorities blacklisted Polymarket as an unlicensed gambling operator and instructed internet service providers to restrict access, emphasizing that the use of blockchain is irrelevant to the legal classification.

Other countries in Asia and Europe have taken similar steps. Indonesian authorities have blocked access to Polymarket as part of a broader crackdown on online gambling, noting that its betting and speculation activities violate local law. They acted shortly after markets on the platform attracted attention for allowing bets on when President Prabowo Subianto would leave office, raising concerns about political stability and public order alongside gambling law compliance. In South Korea, police have launched an investigation into local users of Polymarket over alleged illegal gambling, clarifying that the probe currently targets individuals rather than the platform itself. This user‑focused approach signals a willingness to pursue domestic bettors who circumvent national restrictions via VPNs or other means, even when platforms are headquartered abroad.

Kalshi occupies a different but related niche. It is a US‑based, CFTC‑regulated designated contract market (DCM) authorized under the Commodity Exchange Act (CEA) to list “event contracts,” which are essentially standardized prediction‑market instruments treated as derivatives. As a DCM, Kalshi can self‑certify that its contracts comply with CEA and CFTC regulations, and in some cases has successfully argued that federal commodities law preempts certain state restrictions on event‑based trading. In Nevada and New Jersey, federal courts have found that the CEA preempted state gaming regulations under the Supremacy Clause of the US Constitution, allowing Kalshi to offer certain sports‑related event contracts. However, this federal imprimatur has not shielded Kalshi from all local challenges. Connecticut’s consumer protection department has ordered it to cease offering unlicensed online sports wagering to residents, asserting that its event contracts violate state law and policy. Arizona’s attorney general has filed 20 misdemeanor criminal counts against Kalshi, alleging that the platform operates an illegal gambling business under state law despite its federal registration.

Robinhood represents yet another variation on the theme: a mainstream brokerage that has begun integrating prediction‑market functionality into an already gamified trading environment. Massachusetts’ top securities regulator has opened an investigation into Robinhood’s decision to introduce a prediction‑markets hub, focusing particularly on how it linked March Madness betting opportunities to existing brokerage accounts. Connecticut’s cease‑and‑desist orders against Robinhood similarly emphasize that only licensed entities may offer sports wagering, that Robinhood lacks such a license in the state, and that its event contracts are deceptive insofar as they are marketed as investments rather than wagers. Together, these cases suggest that regulators are increasingly unwilling to accept semantic distinctions between “event contracts,” “prediction markets,” and “sports bets,” especially when the same platforms also facilitate options trading and other high‑risk financial activity for largely overlapping user bases.

Legal Classification: Derivatives Exchange or Gambling Operator?

The central legal question for prediction markets is whether their contracts should be treated as derivatives subject to financial regulation, wagers subject to gambling regulation, or some hybrid of the two. The answer varies by jurisdiction and sometimes by contract type. Under US federal law, the CEA and CFTC treat many binary event contracts as derivatives, particularly when they relate to economic indicators, financial variables, or hedging needs. This framework underpins Kalshi’s DCM registration and its argument that its contracts are federally regulated products, not subject to state gaming prohibitions. However, the CFTC has also shown a willingness to classify unregistered prediction‑market platforms as illegal off‑exchange binary options venues, as in its enforcement action against Polymarket. The agency thus occupies an ambivalent position, both legitimizing some forms of event‑contract trading and sanctioning others.

State gambling regulators often take a more categorical approach. Arizona’s criminal case against Kalshi is grounded in a statutory definition of wagering that encompasses bets on “any contingent future event,” without carving out a clear exception for federally supervised derivatives. Connecticut’s orders against Kalshi and Robinhood similarly insist that event contracts offering payouts based on sports or entertainment outcomes are sports wagers, and therefore illegal without a state gambling license. In Europe and Latin America, regulators appear even less inclined to treat prediction markets as financial exchanges. Romania’s gambling office has explicitly rejected the idea that Polymarket’s operations are financial in nature, calling them “counter bets” and stressing that both crypto and fiat wagers require gambling licenses. Argentina and Spain have blocked Polymarket and Kalshi on the basis that they are unlicensed gambling platforms, not commodity exchanges.

These divergent classifications create significant uncertainty for operators and users alike. Platforms that obtain federal or national financial licenses may still face criminal or administrative exposure at the state or provincial level, while users who believe they are engaging in lawful derivatives trading may be treated as gamblers in the eyes of their local laws. This fragmentation is particularly challenging for crypto‑based platforms that can be accessed globally and do not easily segregate users by jurisdiction. It also raises deeper policy questions. If prediction markets do, in fact, generate valuable information and enable useful hedging, should they be nurtured within financial regulation, perhaps with tailored rules for retail access? Or should they be restricted and taxed like gambling, given the potential for addiction, insider exploitation, and negative‑sum outcomes for unsophisticated participants? At present, most regulators are erring on the side of the latter, especially where consumer protection and political sensitivity intersect.

A UK man has been sentenced to 33 months after embezzling $650K from his employer and converting it into crypto for gambling. Experts warn that crypto-related white-collar crime is rising, but blockchain transparency can aid detection.

France blocks Polymarket following national gambling authority investigation

Romania blacklists Polymarket over $16M in unlicensed Romanian election betting

Singapore declares Polymarket illegal gambling and blocks access

Connecticut orders Kalshi, Robinhood, and Crypto.com to cease unlicensed gambling operations

Massachusetts opens investigation into Robinhood's March Madness prediction market

Arizona files first criminal charges against a prediction market operator (Kalshi)

South Korean police open first illegal gambling probe targeting Polymarket users

Regulation, Crypto, and the Global Crackdown on Unlicensed Gambling

Gambling has long been subject to intense regulation because of its social and economic externalities. Crypto and prediction markets have not changed that reality; if anything, they have sharpened it by making high‑intensity wagering more accessible and less geographically constrained. Across multiple continents, regulators are recalibrating their regimes to address crypto‑denominated bets, cross‑border platforms, and the convergence of trading and gambling on global apps.

Traditional Gambling Regulation and Its Extension to Crypto

Conventional gambling regulation rests on several pillars: licensing of operators, geographic restrictions, age limits and identity verification, technical standards for fairness and integrity, AML and counter‑terrorist‑financing controls, and mechanisms for responsible gambling and player protection. These pillars are reflected in the language used by regulators confronted with crypto platforms. Connecticut’s Department of Consumer Protection, for example, emphasizes that only licensed entities may offer sports wagering in the state, that unlicensed platforms like Kalshi, Robinhood, and Crypto.com violate local law, and that their users lack the protections afforded to patrons of regulated operators. The agency notes that these platforms are not subject to state technical standards, do not have integrity controls to prevent insider betting or market manipulation, and may not pay out winnings as advertised because their house rules are unreviewed by regulators.

Romania’s National Gambling Office voices similar concerns in its decision to blacklist Polymarket. It criticizes the platform for failing to implement fiscal reporting, player‑protection mechanisms, and AML procedures, and it highlights elevated activity during local elections, where large volumes of bets raised worries about both political influence and consumer exploitation. Argentina frames its nationwide block on Polymarket in terms of operating without proper approval, underscoring that any platform taking bets from residents must obtain a local license and comply with domestic gambling law. Spain has gone further by blocking both Polymarket and Kalshi over unlicensed gambling concerns and signaling that companies continuing to operate without licenses after a specified date will face fines. These actions demonstrate that, from the perspective of many regulators, crypto‑based prediction markets and casinos are simply new forms of the same underlying activity and must submit to familiar licensing and compliance frameworks.

Age restrictions and marketing constraints are another flashpoint. Connecticut’s orders stress that licensed platforms must restrict participation to individuals over 21 for sports wagering and must not target college campuses or individuals on voluntary self‑exclusion lists. Regulators accuse unlicensed prediction‑market platforms of advertising to these prohibited groups, thereby exacerbating the risks of gambling harm. Massachusetts’ investigation into Robinhood’s prediction markets reflects analogous concerns that brokerage accounts, which are widely used by young adults for investing, are being leveraged to cross‑sell gambling‑like products without adequate safeguards. As social media platforms such as X update their policies to ban or restrict paid partnerships related to gambling and crypto promotions, the marketing environment around these products is likely to evolve, though enforcement of platform policies remains uneven.

Crypto as Payment Method: The UK’s Emerging Approach

The United Kingdom offers an instructive case study in how a major gambling market is grappling with crypto. The UK Gambling Commission (UKGC) has identified cryptoassets as a high‑risk payment method in its money‑laundering and terrorist‑financing risk assessments for licensed gambling operators. The Commission notes that the pseudonymous nature of many crypto transactions, the use of unregulated exchanges or mixers, and the potential for cross‑border obfuscation all raise red flags relative to traditional payment systems. As a result, operators that accept crypto must implement enhanced due‑diligence and transaction‑monitoring procedures, or else risk regulatory sanctions.

At the same time, UK authorities recognize that a significant share of bettors want to use cryptocurrencies, and that forcing all crypto wagering into unlicensed offshore venues may increase harm rather than reduce it. Recent reports indicate that the UKGC is exploring ways to allow punters to pay with crypto within the country’s regulated gambling system, as part of a broader digital‑asset regulatory framework being finalized by the Financial Conduct Authority (FCA). Under this approach, licensed operators could accept crypto deposits and withdrawals under strict conditions, integrating on‑ramp and off‑ramp controls, robust KYC, and transaction screening. The aim is to keep bettors on licensed sites rather than driving them to offshore platforms that offer no domestic recourse if funds are lost or stolen.

This strategy reflects a pragmatic calculus. Outright prohibition of crypto in gambling is increasingly difficult to enforce given the proliferation of DeFi protocols, decentralized exchanges, and peer‑to‑peer wallets. By allowing crypto payments within a tightly supervised framework, regulators hope to capture data, mitigate AML risks, and preserve some degree of consumer protection. However, even under a permissive crypto‑payments regime, the UKGC is unlikely to relax its scrutiny of novel gambling products that blur into financial speculation. Prediction markets on political events, for example, remain heavily constrained or banned in many European jurisdictions because of concerns about election integrity and public confidence, and there is no indication that crypto‑denomination alone will change that stance.

AML, Terrorist Financing, and Tax Concerns

Anti‑money‑laundering and counter‑terrorist‑financing frameworks apply with particular force to gambling because cash‑intensive, high‑transaction‑volume environments are attractive to criminals seeking to move or launder funds. Crypto can both exacerbate and mitigate these risks. On the one hand, its rapid, borderless nature facilitates the movement of large sums across platforms and jurisdictions without the friction of bank wires. Offshore crypto casinos and prediction markets that operate without KYC controls or transaction reporting can serve as hubs for layering and integration in money‑laundering schemes. The British Gambling Commission’s designation of cryptoassets as high‑risk payment instruments reflects precisely this concern. On the other hand, blockchain’s transparency allows regulators and analytics providers to trace flows in ways that are impossible with cash and harder with certain traditional instruments, as illustrated by the UK embezzlement case where police reconstructed the suspect’s crypto gambling activity to secure a conviction.

Tax authorities have their own reasons to scrutinize crypto‑enabled gambling. Gains on crypto bets may or may not be treated the same as gains on investments, depending on local law. Some jurisdictions tax gambling winnings only above certain thresholds, while others treat them as ordinary income or capital gains. Loss deductions are typically more constrained for gambling than for investing, which is one reason why the design of gambling‑loss caps and their interaction with prediction markets has become a topic of speculation in both policy and markets. Platforms that do not provide adequate reporting or documentation compound the problem, leaving users to navigate complex tax obligations on their own and exposing them to enforcement risk if they under‑report or misclassify gambling‑related income.

Crypto‑specific AML regulations are tightening in parallel. Travel‑rule obligations for virtual asset service providers, enhanced due diligence for high‑risk customers, and requirements to monitor for gambling‑related patterns in transaction flows are becoming more common. Gambling operators that accept crypto must therefore build or procure sophisticated compliance capabilities, including blockchain analytics and transaction monitoring. Those that do not, whether out of negligence or design, are likely to face heightened enforcement, as regulators seek to prevent gambling venues from becoming de facto money‑laundering infrastructures.

At least eight jurisdictions have classified crypto prediction markets as unlicensed gambling and issued bans or criminal charges within a 12-month window, with no harmonised international standard in sight.

- Market / ManipulationHigh

Public mega-positions create social pressure that distorts rational risk management, as demonstrated by the trader who held an $800M leveraged long to a $4M loss under crowd scrutiny.

Regulatory blocks can instantly strand user funds or freeze withdrawal access, as seen when multiple countries simultaneously cut off Polymarket users with no notice period.

Platforms like Polymarket and Kalshi present single legal targets that regulators can block at the domain or payment-rail level despite underlying smart-contract decentralisation.

- Smart-contractMedium

On-chain gambling protocols inherit standard DeFi exploit risk, but the more immediate threat is oracle manipulation of event outcomes rather than fund-drain vulnerabilities.

The UK Gambling Commission flagged crypto's pseudonymity as an emerging AML risk, and Bitrace's 2025 crime report documented rising crypto-denominated gambling fraud volumes globally.

Financialization, “Gamblification,” and the Crypto Zeitgeist

Beyond the mechanics of regulation and platform design lies a broader socio‑economic phenomenon: the progressive financialization and “gamblification” of everyday life. Crypto sits at the epicenter of this process, with effects that extend well beyond formal gambling sectors.

Stock Markets as Gambling and the Rise of Hyperfinancialisation

The idea that stock markets resemble gambling is not new. Britannica itself notes that in a broad sense, stock markets may be considered a form of gambling, although skill and information can play a considerable role in shaping outcomes. Margin trading, shorting, and complex derivatives all introduce leverage and optionality that magnify both gains and losses, often in ways that are poorly understood by retail participants. When trading costs fall to near zero, as on many digital platforms, and when app interfaces are designed to emphasize excitement and immediacy, the behavioral dynamics begin to resemble those of casinos more than those of traditional investment houses.

Researchers at the Levy Economics Institute describe financialization as a process in which financial markets, institutions, and elites gain increasing influence over economic policy and outcomes, often with negative consequences for inequality and stability. In this environment, more aspects of life become mediated by markets, and more individuals feel compelled to engage in speculative activity just to maintain their standard of living. Crypto adds another layer by creating new, highly volatile asset classes and trading venues that operate 24/7 with global reach. The result is a form of hyperfinancialisation in which memes, politics, cultural events, and even regulatory decisions become tradable, often via instruments that are functionally indistinguishable from bets.

Prediction markets are perhaps the purest example of this trend. When individuals can bet on elections, policy changes, central‑bank interest‑rate decisions, or celebrity behavior, they are effectively invited to treat civic and cultural phenomena as gambling opportunities. Polymarket’s markets on local elections in Romania, which attracted millions in trading volume, exemplify how quickly such instruments can turn public affairs into speculative playgrounds. Robinhood’s integration of March Madness prediction markets into brokerage accounts illustrates how sporting events are folded into financialized interfaces that already host options trading and crypto speculation. These developments raise questions about the long‑term social effects of turning more and more aspects of life into venues for wagering.

Behavioral Finance, Addiction, and Loss‑Chasing

From a behavioral‑finance perspective, gambling and speculative trading tap many of the same psychological vulnerabilities. Variable‑ratio reward schedules, near‑miss effects, and social reinforcement all contribute to compulsive behavior. Crypto and online gambling amplify these tendencies by providing immediate feedback, constant price updates, and global communities celebrating outsized wins. Loss‑chasing—the tendency to increase bet size after losses in an attempt to break even—is a particularly harmful pattern that can rapidly escalate financial and emotional damage.

The UK embezzlement case involving crypto gambling underscores how addiction can drive individuals to extreme lengths, including criminal acts, to sustain their betting behavior. VIP programs and loss‑rebate schemes, such as those marketed by some crypto‑aligned gambling platforms, can exacerbate these tendencies by cushioning short‑term losses while encouraging continued play at higher stakes. Celebrity endorsements lend social legitimacy to such programs, potentially obscuring their risks for fans who may not fully grasp the mathematics of house edges and long‑term expected losses.

Regulators’ concerns about youth exposure and vulnerable populations reflect these dynamics. Connecticut’s complaints about prediction‑market platforms advertising on college campuses and to individuals on self‑exclusion lists highlight how easily digital marketing can circumvent traditional safeguards. Massachusetts’ focus on Robinhood’s prediction‑markets hub similarly hinges on fears that younger adults, already heavily engaged with app‑based trading, will extend their risk‑taking into more overtly gambling‑like products without adequate understanding or restraint. As social media platforms recalibrate their policies on paid crypto and gambling partnerships, and as public discourse around “degen culture” and hyper‑speculation evolves, industry participants will need to consider not only legal compliance but also ethical questions about how much risk and gamification is appropriate to embed in widely accessible consumer products.

Connecticut regulators issued stop-orders to Kalshi, Robinhood, and Crypto com for allegedly running unlicensed online gambling disguised as prediction markets. Officials say the platforms pose consumer risks and must halt services immediately.

"Under the cease-and-desist orders, Kalshi, Robinhood and Crypto.com must immediately stop advertising, offering, promoting or otherwise making sports event contracts or any other unlicensed online gambling products to Connecticut residents. They must also allow residents to withdraw any funds currently held on their platforms. Failure to comply could trigger civil penalties under the Connecticut Unfair Trade Practices Act and potential criminal action for breaches of the state’s gaming statutes. For now, the state reminded residents that only three operators are authorised to take sports bets, namely DraftKings through Foxwoods, FanDuel through Mohegan Sun and Fanatics through the Connecticut Lottery, with a minimum age of 21 for sports wagering and 18 for fantasy contests."

Practical Considerations for Crypto Users

For readers immersed in the crypto ecosystem, the convergence of gambling, prediction markets, and trading is not an abstract issue but a daily reality. Navigating it responsibly requires attention to legal, financial, and ethical dimensions that are often glossed over in promotional materials and social‑media discourse.

Legal Exposure and Jurisdictional Risk

One of the most important considerations is that legality is intensely jurisdiction‑specific. A platform may be fully compliant in one country and yet considered illegal gambling in another. Polymarket users in South Korea, for example, now face a police investigation into alleged illegal gambling, even though the platform itself is not the direct target of the probe. Authorities have indicated that they requested the investigation at the national level, underlining that domestic users who access offshore prediction markets via VPNs or other workarounds may still be held accountable under local law. Similarly, residents of Romania, Argentina, Spain, and Indonesia may find that their access to Polymarket or similar platforms is blocked at the ISP level and that any attempt to circumvent these blocks could be interpreted as participation in unlawful gambling activity.

In the United States, the picture is complicated by the interplay between federal and state law. A CFTC‑registered platform like Kalshi may be authorized to list certain event contracts under the CEA, yet still face state‑level enforcement for alleged violations of gambling statutes, as the Arizona criminal case illustrates. Connecticut’s cease‑and‑desist orders against Kalshi, Robinhood, and Crypto.com emphasize that “a prediction market wager is not an investment” and that offering such wagers without a gambling license violates state law, regardless of how they are labeled. Users who assume that federal financial regulation automatically insulates them from state gambling laws risk unpleasant surprises.

Prudent participants therefore need to understand not only the terms of service of the platforms they use but also the regulatory environment of their own jurisdictions. That may involve consulting legal counsel, following local regulatory announcements, and recognizing that accessing restricted services via VPNs or other methods can carry real legal risk. It also means appreciating that regulatory attitudes are in flux, especially around prediction markets and crypto payments, so practices that seem tolerated today may become enforcement priorities tomorrow.

Platform Risk, Custody, and Counterparty Exposure

Even when legal issues are set aside, platform risk is a central concern. Unlicensed gambling and prediction‑market platforms often operate outside established consumer‑protection frameworks. Connecticut regulators warn that such platforms are not required to adhere to technical standards designed to protect users’ financial and personal data, nor to maintain integrity controls that prevent insider wagering or market manipulation. House rules for bet settlement may be opaque, unreviewed, and subject to change, leaving users with little recourse if a platform voids markets, delays payouts, or interprets ambiguous outcomes in self‑serving ways. Romania’s critique of Polymarket similarly stresses the absence of player‑protection mechanisms and fiscal reporting, elements that are standard in regulated gambling environments.

Crypto introduces additional layers of risk related to custody and smart contracts. Some on‑chain gambling and prediction platforms are non‑custodial, meaning users retain control of their funds until settlement; others require deposits into platform‑controlled wallets that could be vulnerable to hacks, mismanagement, or seizure. Smart‑contract bugs, oracle failures, and governance disputes can all disrupt market resolution. While these technological risks differ from those in traditional online casinos, they serve the same function from the user’s perspective: they increase the probability that wagers will not be honored as expected. Users should therefore evaluate platforms not only on their offerings and odds but also on their security track record, code transparency, and contingency policies for disputed outcomes.

Responsible Gambling and Self‑Care in a Crypto Context

Finally, there is the question of personal risk management and responsible participation. The line between high‑risk trading and gambling is often blurred in crypto, but the underlying principles of self‑care remain similar. Setting clear limits on the proportion of one’s net worth exposed to speculative bets, distinguishing between funds earmarked for entertainment and those needed for essential expenses, and avoiding the temptation to “chase losses” are basic but critical practices. So is recognizing early signs of compulsive behavior, such as preoccupation with betting, lying about losses, or using gambling to escape stress or other problems.

Many regulated gambling operators offer tools for self‑exclusion, deposit limits, and cooling‑off periods. Some crypto platforms are beginning to experiment with analogous mechanisms, though the decentralized nature of many services makes enforcement challenging. In jurisdictions such as Connecticut, regulators have criticized unlicensed platforms for marketing to individuals on voluntary self‑exclusion lists, underscoring the importance of robust identity and cross‑platform coordination in any effective harm‑reduction strategy. For users in regions without such infrastructure, or on platforms that do not participate in it, self‑regulation becomes even more important.

Community norms also matter. When social media and crypto communities celebrate only the spectacular wins and meme‑ify the devastating losses, they can foster an environment where taking extreme, poorly understood risks is valorized rather than questioned. Counter‑narratives that emphasize long‑term financial health, transparency about losses, and critical engagement with platform incentives are essential to balance the discourse. For media outlets and educators addressing a crypto‑savvy audience, the challenge is to provide nuanced coverage that neither demonizes all speculative activity nor ignores the very real risks and harms associated with gambling‑like practices.

Outlook

The entanglement of gambling, prediction markets, and crypto is likely to deepen rather than recede. On one trajectory, regulated environments will adapt by integrating crypto payments, as the UK Gambling Commission is exploring, and by developing tailored frameworks for event‑contract markets that recognize their informational value while constraining their potential for harm. On another trajectory, unlicensed offshore platforms will continue to innovate at the edge of the law, leveraging decentralization and jurisdictional arbitrage to offer products that blur the boundaries between trading and gambling even further. Regulatory responses—from South Korea’s focus on individual Polymarket users to Arizona’s criminal charges against Kalshi—suggest that authorities are prepared to pursue both platforms and participants when they perceive consumer risk or threats to public order.

For the crypto ecosystem, the key question is whether it will lean into the image of a global casino or evolve toward a more balanced model in which speculative tools are embedded within robust safeguards and clear legal frameworks. The concept of financialization reminds us that markets are not neutral; they reshape social relations and priorities. As more aspects of life become tradable—from elections and policies to meme narratives and personal reputations—the need for thoughtful governance, transparent rules, and responsible participation becomes more pressing. For a crypto news audience, understanding gambling in all its dimensions—legal, economic, behavioral, and technological—is essential to navigating this landscape with eyes wide open.

Latest Gambling news

Hyperfinancialisation: On the rise and ouroboric nature of gambling and financialisation. This piece was written as an accompaniment to long degeneracy.A UK man has been sentenced to 33 months after embezzling $650K from his employer and converting it into crypto for gambling. Experts warn that crypto-related white-collar crime is rising, but blockchain transparency can aid detection.Connecticut regulators issued stop-orders to Kalshi, Robinhood, and Crypto com for allegedly running unlicensed online gambling disguised as prediction markets. Officials say the platforms pose consumer risks and must halt services immediately. Risky retail trading is roaring back—and Robinhood CEO Vlad Tenev has become the movement’s cult hero as the app fuels a surge in options, crypto, and prediction-market gambling.

Risky retail trading is roaring back—and Robinhood CEO Vlad Tenev has become the movement’s cult hero as the app fuels a surge in options, crypto, and prediction-market gambling. Romania’s gambling regulator has blacklisted Polymarket, calling it unlicensed “counterparty betting” rather than event trading. The move follows massive betting volumes on Romanian elections surpassing $16 million.

Romania’s gambling regulator has blacklisted Polymarket, calling it unlicensed “counterparty betting” rather than event trading. The move follows massive betting volumes on Romanian elections surpassing $16 million. Longed $800M near the top, now down $4M with liquidation at $107K—a harsh lesson in the dangers of public big bets, where pressure from thousands watching can shake even the calmest traders.

Longed $800M near the top, now down $4M with liquidation at $107K—a harsh lesson in the dangers of public big bets, where pressure from thousands watching can shake even the calmest traders.Sources

- https://www.britannica.com/topic/gambling

- https://ecollections.law.fiu.edu/cgi/viewcontent.cgi?article=1703&context=lawreview

- https://en.wikipedia.org/wiki/Polymarket

- https://www.stinson.com/newsroom-publications-sportsbooks-or-commodity-exchanges-the-rising-legal-tensions-between-sports-betting-and-prediction-markets

- https://polymarket.com/event/cap-on-gambling-loss-deductions-repealed-before-2027

- https://www.gamblingcommission.gov.uk/licensees-and-businesses/guide/page/emerging-money-laundering-and-terrorist-financing-risks-from-april-2025

- https://www.youtube.com/watch?v=Nz4ZfJX1W2s

- https://www.levyinstitute.org/pubs/wp_525.pdf

- https://x.com/WuBlockchain/status/2058905371033350648

- https://www.facebook.com/groups/newsposter/posts/1730106235007226/

- https://es.tradingview.com/news/coinpedia:5d2b049d6094b:0-argentina-orders-nationwide-block-on-polymarket-over-gambling-concerns/

- https://forklog.com/en/romanian-regulator-blacklists-polymarket/

- https://www.bloomberg.com/news/articles/2026-06-05/korean-police-launch-gambling-probe-targeting-polymarket-users

- https://www.morganlewis.com/pubs/2026/03/arizona-files-first-criminal-charges-against-a-prediction-market

- https://portal.ct.gov/dcp/news-releases-from-the-department-of-consumer-protection/2025-news-releases/connecticut-consumer-protection-orders-cease-and-desist-conducting-unlicensed-online-gambling

- https://www.gpwa.org/forum/massachusetts-investigates-robinhood-over-prediction-markets-betting-269825.html

- https://x.com/CryptosR_Us/status/2029436499570151425

- https://x.com/CoinDesk/status/2027407179326599422

- https://www.binance.com/en/square/post/12-02-2025-uk-man-sentenced-for-embezzling-funds-to-fuel-crypto-gambling-33177717023345

- https://next.io/news/b2b-news/tyga-enters-1win-vip-program-as-platform-blends-crypto-and-entertainment/

Community notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…