Explores how “COIN” spans native cryptocurrencies, Coinbase stock, Binance COIN‑M futures, institutional deposit tokens, national projects, stablecoins, memecoins and tokenized equities, and explains how to interpret and manage risk across these overlapping meanings.

+70 sources across the wider coverage universe

Trump family disclosure reveals Q1 Coinbase, MARA, and Strategy buys led by up to $250K COIN purchase2026-05

Trump family disclosure reveals Q1 Coinbase, MARA, and Strategy buys led by up to $250K COIN purchase2026-05 UAE’s largest fuel retailer ADNOC Distribution will accept stablecoin in 980 stations in three countries. The company has partnered with Al Maryah Community Bank to enable AE Coin payments via the AEC Wallet at fuel pumps, convenience stores, and car washes. AE Coin, the UAE's first stablecoin licensed by the Central Bank, is backed 1:1 with dirhams.2025-12

UAE’s largest fuel retailer ADNOC Distribution will accept stablecoin in 980 stations in three countries. The company has partnered with Al Maryah Community Bank to enable AE Coin payments via the AEC Wallet at fuel pumps, convenience stores, and car washes. AE Coin, the UAE's first stablecoin licensed by the Central Bank, is backed 1:1 with dirhams.2025-12 A LOOK INTO COINBASE:

Coinbase’s “brand refresh” is really a pivot into an everything exchange—AI agents, stocks, perps, prediction markets, regulated token sales, B2B stablecoins, SocialFi, and curated DeFi—all on crypto rails. Bull case: this makes Coinbase a global financial utility, pulls TradFi liquidity onchain, scales revenue, and accelerates mass adoption. Bear case: it dilutes altcoins, centralizes power, invites heavy regulation, and could kill degen culture as capital rotates from speculative tokens into real, cash-flow assets.2025-12

A LOOK INTO COINBASE:

Coinbase’s “brand refresh” is really a pivot into an everything exchange—AI agents, stocks, perps, prediction markets, regulated token sales, B2B stablecoins, SocialFi, and curated DeFi—all on crypto rails. Bull case: this makes Coinbase a global financial utility, pulls TradFi liquidity onchain, scales revenue, and accelerates mass adoption. Bear case: it dilutes altcoins, centralizes power, invites heavy regulation, and could kill degen culture as capital rotates from speculative tokens into real, cash-flow assets.2025-12 Trump Billionaires Club, a licensed mobile game launching this year, will reward players with $1M in TRUMP meme coin as they compete in a billionaire-themed board-game system on Solana.2025-12

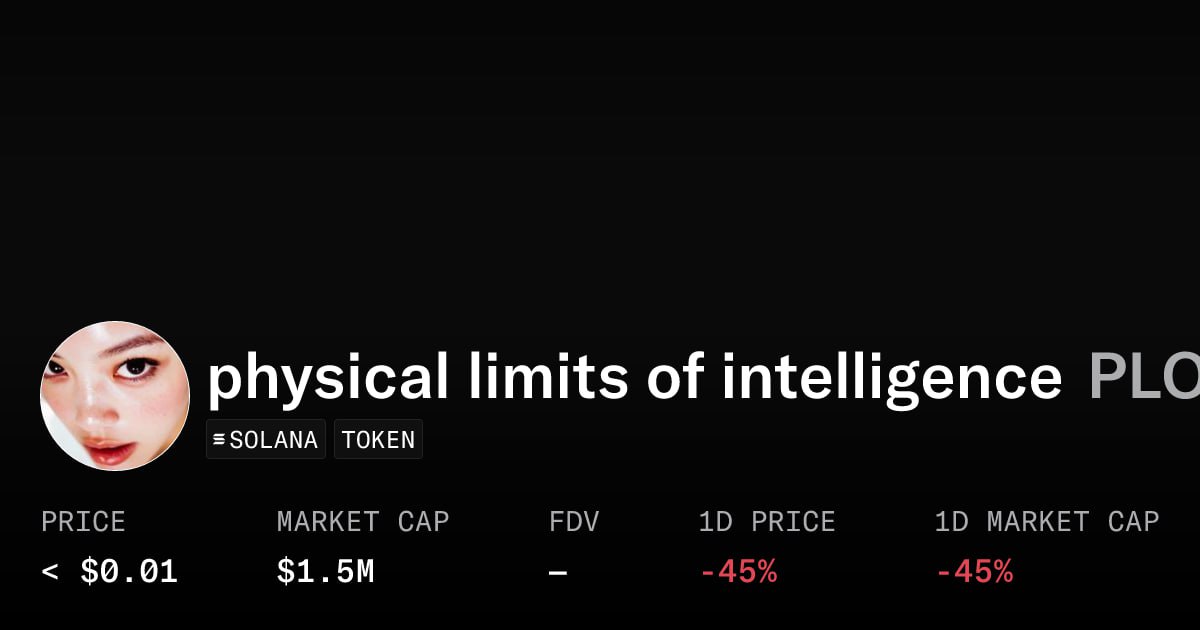

Trump Billionaires Club, a licensed mobile game launching this year, will reward players with $1M in TRUMP meme coin as they compete in a billionaire-themed board-game system on Solana.2025-12 After faking death, Zerebro founder Jeffy Yu unveils AI-penned manifesto and new Solana coin. The manifesto, which did not mention a token, argues for a future in which AI and humans will converge biologically, chemically, and surgically in a new form of humanity. Physical Limits of Intelligence (PLOI) quickly surged to a $5.4 million market cap before retracing to a recent $1.1 million market cap. The top trader, known as PainCrypt0, realized profits of over $26,800 from a $2,634 investment, according to DEX Screener.2025-12

After faking death, Zerebro founder Jeffy Yu unveils AI-penned manifesto and new Solana coin. The manifesto, which did not mention a token, argues for a future in which AI and humans will converge biologically, chemically, and surgically in a new form of humanity. Physical Limits of Intelligence (PLOI) quickly surged to a $5.4 million market cap before retracing to a recent $1.1 million market cap. The top trader, known as PainCrypt0, realized profits of over $26,800 from a $2,634 investment, according to DEX Screener.2025-12 Binance co-CEO Yi He’s WeChat account hacked to push meme coin MUBARA (Mubarakah). The attackers profited by selling the memecoin after creating artificial demand through the false endorsement. CZ wrote on X to warn users to ignore the messages and stay safu.2025-12

Binance co-CEO Yi He’s WeChat account hacked to push meme coin MUBARA (Mubarakah). The attackers profited by selling the memecoin after creating artificial demand through the false endorsement. CZ wrote on X to warn users to ignore the messages and stay safu.2025-12

In crypto, the word “coin” has grown into a loaded term that can describe everything from a blockchain’s native asset to a listed stock ticker, a futures category on Binance, a government-backed stablecoin, or a viral Solana memecoin. Understanding which “COIN” you are actually dealing with is now a core skill for anyone navigating modern crypto markets.

What “COIN” Means In Today’s Crypto Landscape

For a long time, “coin” had a fairly narrow meaning in crypto: it referred to a native digital currency that lives on its own blockchain and acts primarily as money. Bitcoin on the Bitcoin network and ether on Ethereum are canonical examples of this original definition. A coin in this sense is usually the base unit of value in its ecosystem, used to pay transaction fees, reward validators or miners, and function as a medium of exchange and store of value. Over time, that clean definition has collided with marketing, regulation, and financial engineering, leading to a much messier reality in which “COIN” appears in ticker symbols, derivatives products, and branded corporate and national projects.

When traders today see “COIN,” it might refer to a layer‑1 asset like BTC, a meme coin launched last night on Solana, a tokenized share of Coinbase stock, or a “COIN‑M” futures contract on Binance that is margined and settled in the underlying cryptocurrency instead of dollars. It might describe a bank-issued deposit token like JPM Coin, designed for institutional settlements on public networks. It can even refer to a central bank–licensed stablecoin like AE Coin in the UAE, or to a questionable national project such as Sango Coin or Central African Republic Meme (CAR), which watchdogs have flagged for governance and money‑laundering risks. Against that backdrop, headlines about “COIN listings,” “COIN futures,” or “COIN pumps” can be deeply ambiguous.

For a crypto‑savvy readership, the challenge is not just vocabulary but risk assessment. Each use of “COIN” carries different legal status, counterparty risk, liquidity profile, and correlation to crypto beta. Coinbase’s COIN stock trades in traditional equity markets and is increasingly wrapped into tokenized products and on‑chain collateral frameworks, whereas Solana meme coins are often unregistered, highly speculative instruments that move on social sentiment and influencer behavior. Tokenized COIN equities can trade side by side with BTC, SOL, and BONK or TRUMP memecoins on 24/7 venues, but they are not the same thing economically or legally. This explainer unpacks the major meanings of “COIN” in circulation today, connects them to recent developments from Binance, Coinbase, institutional issuers, and meme culture, and offers a framework for interpreting what “COIN” really signals in any given context.

Trump family disclosure reveals Q1 Coinbase, MARA, and Strategy buys led by up to $250K COIN purchase

Trump's latest 278-T filing shows combined holdings for Donald Trump, Melania Trump, and dependent children bought Coinbase, MARA, and Strategy shares during Q1, including nine Coinbase-related purchases. The biggest COIN buy was valued at $100,001-$250,000; Strategy saw eight buy/sell entries and MARA had two purchases under $50,000. Crypto equities were only a small slice of 2,000-plus disclosed buys, but the optics are obvious while Trump's administration is pushing friendly digital asset policy.

Readers click 'COIN' stories not for price discovery but for exposure — the dominant pull is watching insiders, politicians, and scammers exploit the meme coin format to extract money from retail while investigators, advocacy groups, and short-sellers race to assign blame.

Coins Versus Tokens: The Technical Foundation

Any serious discussion of “COIN” must start with the technical distinction between a coin and a token. In most contemporary crypto literature, a coin is defined as a digital asset that operates on its own native blockchain, serving as the primary unit of value and medium of exchange in that network. Bitcoin, for instance, exists on the Bitcoin blockchain and is created via mining, a process where network participants validate transactions and add them to the ledger in exchange for new BTC. The coin not only represents value; it also anchors network security and incentive design, because miners or validators are remunerated in that same native asset.

Tokens, by contrast, typically do not have their own blockchain. Instead, they are issued on top of an existing chain like Ethereum, Solana, or Base, using standardized smart contract templates. These tokens may represent utility access, governance rights, claims on external assets, or simple speculative memecoins, but they rely on the infrastructure and security model of their host chain. Stablecoins like USDC on Ethereum or a game token on Solana are illustrative: they are crypto assets, but not coins in the strict sense of being native base‑layer currencies. As one mainstream overview puts it, coins are “central to their own systems,” while tokens “function off the back of a blockchain.”

The terminology is somewhat muddied by history and practice. In a broad technical sense, any digital asset secured by cryptography could be called a “token.” Many early users referred to all cryptocurrencies as “tokens,” and some communities still do so informally. Over time, however, industry usage has converged on calling base‑layer currencies like BTC and ETH “coins,” while reserving “token” for assets issued on those chains, such as ERC‑20 tokens on Ethereum. Crypto.com’s own glossary reflects this nuance when it notes that all coins are a type of token, but not all tokens are coins. For traders, the operational takeaway is that “coin” usually hints at a native asset with protocol‑level significance, whereas “token” suggests something built on top.

This distinction matters practically because coins and tokens tend to have different security, governance, and regulatory profiles. Coins like BTC and ETH are often positioned as commodities or foreign currency analogues, with partially clarified regulatory treatment in some jurisdictions. Tokens, especially those that convey rights to revenues or external assets, more frequently trigger securities analysis. The recent wave of real‑world asset tokens and tokenized equities, including shares of Coinbase’s COIN stock on platforms like Kraken’s xStocks, falls squarely in this token category. That means a headline about a “COIN token” may be describing something quite different from a base‑layer coin such as BTC or SOL.

Edge cases blur the neat categories further. Ethereum’s native asset is universally called a coin, yet most DeFi assets on Ethereum are tokens. JPM Coin is issued on Base, an Ethereum layer‑2 network, and functions more like a tokenized bank deposit than a free‑floating cryptocurrency, yet the bank brands it a “coin.” Similarly, AE Coin is described as a stablecoin but runs within a bank wallet framework and is explicitly backed one‑to‑one by fiat dirham reserves. These examples underscore that “coin” has become as much a marketing and UX term as a purely technical one.

Coins as native value layers

When industry veterans talk about “coins,” they usually mean the native value layers of public blockchains. A native coin fulfills three intertwined roles: it serves as a medium of exchange within the network, a store of value for users and investors, and a mechanism for securing and operating the protocol. On Bitcoin, BTC is required to pay transaction fees and rewards the miners who expend energy to append new blocks to the chain. On Ethereum, ETH is required to pay gas for executing smart contracts and compensates validators who stake capital and run nodes. This link between the coin and the protocol’s consensus mechanism makes the coin foundational to the network’s economic design.

Because of this centrality, native coins tend to anchor entire ecosystems of tokens and applications. Bitcoin’s BTC has become a macro asset in its own right, with futures, options, and exchange‑traded products built around it. Ethereum’s ETH plays a similar role for DeFi, NFTs, and layer‑2 networks. Market structure often reflects this hierarchy: BTC and ETH dominate spot and derivatives volume, while tokens built on those platforms are typically quoted against them or against stablecoins. When Binance or another exchange lists “COIN‑M BTC Quarterly 1225” futures, the “COIN‑M” category is highlighting that the contract is margined and settled in the underlying coin, such as BTC itself, rather than in a dollar‑pegged asset.

Native coins also anchor community identity and memes. Whole cultures have grown up around BTC and ETH, shaping narratives about digital gold, ultrasound money, or world computer economics. These memes, in turn, influence capital flows, governance outcomes, and the perceived legitimacy of both coins and the broader crypto space. In that sense, the original meaning of “coin” as a base‑layer asset continues to matter deeply, even as the term is repurposed in a widening array of contexts.

Tokens as application and abstraction layers

Tokens leverage these native value layers to represent more granular or specialized forms of value. Technically, a token is an entry in a smart contract ledger, not in the base blockchain itself, although the base chain secures that contract. Developers can rapidly launch new tokens to represent governance rights in a DAO, claim on off‑chain collateral, liquidity provider positions, or purely speculative memes. Solana’s ecosystem, for instance, has seen an explosion of memecoins and game tokens that are easy to launch and trade via bots and mobile wallets, as illustrated by instructional videos on “how to trade Solana meme coins using BONK bot.”

Tokens inherit the base chain’s security guarantees, but their economics, governance, and legal status depend entirely on their specific contracts and issuers. Many memecoins have anonymous teams, no formal disclosures, and extremely concentrated ownership, making them more akin to lottery tickets than to native coins with robust decentralized communities. Others, such as regulated stablecoins or tokenized equities, operate under explicit legal frameworks. Kraken’s xStocks, for example, allows 24/5 trading of tokenized shares of US stocks and ETFs, where each token represents exposure to an underlying regulated security like AAPL or potentially COIN. Although these trade on crypto rails, they remain tied to traditional market structures and regulations.

Understanding this layered architecture helps clarify one source of confusion: a user might see “COIN” in a DeFi interface and be looking at a tokenized representation of an underlying COIN stock or COIN‑M futures PnL, not at a native coin at all. For risk management and tax purposes, the distinction can be decisive.

COIN On Wall Street: Coinbase Stock And Tokenized Equities

The ticker “COIN” has a specific and increasingly prominent meaning in traditional finance: it is the stock symbol for Coinbase Global, Inc., the largest US‑listed crypto exchange operator. As of a recent snapshot, Coinbase shares traded around the low hundreds of dollars with a multi‑tens of billions market capitalization and a high earnings multiple, reflecting both growth expectations and cyclicality with crypto markets. Market commentators routinely describe COIN as a leveraged bet on the crypto sector, with the stock’s performance closely tied to Bitcoin’s price cycles and overall trading volumes across digital assets.

Coinbase has explicitly leaned into its bridging role between crypto and traditional markets. In corporate communications it has pitched itself as an “everything exchange,” aiming to host not only spot crypto and derivatives but also tokenized equities, prediction markets, B2B stablecoins, and curated DeFi access—all running on crypto rails. The strategic vision is that COIN, as a stock, becomes a gateway to a broader financial stack where tokenized assets, stablecoins, and AI‑driven agents transact seamlessly. The bullish narrative sees Coinbase evolving into a global financial utility and liquidity hub, while the more skeptical view warns about centralization, regulatory drag, and potential crowding out of smaller altcoin projects.

One important development for crypto‑native traders has been the emergence of tokenized representations of COIN stock itself. Platforms such as Kraken’s xStocks allow users to trade tokenized shares of top US stocks and ETFs, including large‑cap tech names, 24 hours a day on weekdays. While specific inclusion of COIN varies by platform and time, the broader trend is clear: equity tickers are being wrapped into on‑chain tokens that can serve as collateral, be fractionally owned, and trade alongside BTC, ETH, and other crypto assets. In parallel, perpetual futures and options on COIN are accessible on both traditional derivatives venues and, increasingly, on crypto‑native derivatives DEXs that integrate tokenized equities and RWAs into unified collateral pools.

This blending leads to headlines about “COIN listings” in crypto that can refer either to Coinbase’s own tokenized equity going live on a DeFi platform, or to new coins being listed by Coinbase the company. It also creates interesting feedback loops: COIN’s stock price can be influenced by Bitcoin’s volatility and volumes, which are in turn affected by Coinbase’s product roadmap and regulatory posture. In extreme cases, COIN may trade as a high‑beta proxy for BTC itself, leading some traders to arbitrage or hedge between BTC derivatives and COIN equity or its tokenized mirrors.

Tokenization adds yet another layer. When tokenized COIN equities are used as collateral on DeFi platforms or centralized venues offering cross‑margin, their price dynamics directly feed into leverage and liquidation cascades. Kraken’s xStocks, for example, emphasizes that tokenized stocks can be traded around the clock on weekdays, extending access beyond traditional market hours. As other platforms integrate COIN and peer stocks into perpetual lending, borrowing, and derivatives protocols, the line between “crypto coin” and “stock of a crypto company” will blur further in practice, even as their legal identities remain distinct.

For investors, the key is to distinguish clearly between COIN as an equity security subject to corporate fundamentals, COIN‑denominated or COIN‑linked tokens in DeFi, and base‑layer coins like BTC or ETH whose economics are governed by protocol rules rather than corporate earnings. That distinction becomes even more consequential as tokenized COIN shares are routed into on‑chain treasuries, structured products, and yield strategies that sit side by side with native coins and speculative memecoins.

COIN as collateral and RWA building block

One emerging use case is the deployment of COIN stock, or its tokenized equivalents, as collateral in crypto‑native credit and derivatives systems. As real‑world asset tokens mature, platforms are beginning to accept tokenized stocks and ETFs alongside stablecoins and blue‑chip crypto as lending collateral. Kraken’s xStocks explicitly frames tokenized shares as accessible around the clock, which makes them appealing in leverage strategies that require responsive collateral management. In parallel, other ecosystems have highlighted new listings of tokenized RWAs, including COIN, on orderbook‑based DEXs that offer perpetual futures, high leverage, and the option for third parties to launch new markets with no code.

From a risk perspective, treating COIN as collateral is very different from using BTC or ETH. COIN embeds exposure to corporate governance, regulatory enforcement, and operational risk at Coinbase, in addition to sector‑wide crypto cycles. It can also be subject to trading halts or delistings in its primary market, which can create stress for on‑chain instruments that expect continuous price discovery. Those frictions will shape how deeply COIN integrates into DeFi and structured products over time.

- 01Meme coin fraud scale

42,000 victims and $32M lost in a single scam that defeated top rug-pull detectors made readers confront how industrialized meme coin fraud has become.

- 02Political insider coin exploitation

Trump, MELANIA, and LIBRA coins — all with revealed insider teams, fee extraction, and access-selling — turned abstract 'crypto risk' into a concrete political scandal readers couldn't ignore.

- 03ZachXBT on-chain investigations

Readers followed his Bybit hack laundering trace and GCRClassic hack because he converts opaque blockchain data into named culprits and mapped fund flows.

- 04$COIN stock as crypto bellwether↗

Coinbase crossing $300 and ARK's $17.8M buy-in gave TradFi-watching readers a single ticker to measure the entire industry's recovery.

- 05JPM Coin institutional legitimacy↗

A $1B-per-day settlement rail and a euro-denominated corporate product from JPMorgan signaled to readers that bank-grade blockchain is operational, not theoretical.

- 06Coin Center vs. surveillance state

Coin Center's refusal to answer Warren and a fellow's DOJ lawsuit framed crypto advocacy as a genuine constitutional fight, not just lobbying, drawing clicks from readers invested in the policy outcome.

COIN In Derivatives Markets: COIN‑M Futures And Margining

A second major context in which “COIN” appears is derivatives trading, particularly on Binance and similar centralized exchanges. Here “COIN‑M” does not refer to a specific cryptocurrency, but to a class of futures contracts that are margined and settled in the underlying coin rather than in USD or a stablecoin. On Binance Futures, for example, traders can access both USDⓈ‑M contracts, which use stablecoins like USDT as collateral and settlement currency, and COIN‑M contracts, which use assets such as BTC, ETH, BNB, XRP, or SOL for margin and settlement.

Binance regularly lists and expires quarterly COIN‑M delivery contracts with specific maturity dates, such as “Quarterly 1225,” corresponding to a December 25 settlement. When an older quarterly series like “0626” expires and settles, Binance will often list a new corresponding COIN‑M and USDⓈ‑M “1225” series a few hours later, ensuring continuity of tradable maturities. At the same time, the exchange periodically delists underperforming or illiquid COIN‑M perpetual contracts, such as those tied to particular altcoins, as part of risk management and product lifecycle management. Official announcements specify the exact contracts, timelines, and fee schedules associated with these listings and delistings.

In practice, COIN‑M futures appeal to traders who want to increase or hedge their exposure to a specific cryptocurrency while holding their collateral in that same asset. For example, a BTC‑denominated fund may prefer to post BTC as margin for COIN‑M BTC contracts, aligning its liabilities and assets and allowing it to earn funding fees or directional PnL directly in BTC rather than in USDT. This approach can be attractive in bullish markets where the underlying coin is appreciating, because gains compound in the asset traders ultimately want to accumulate. It also introduces unique risk: if the coin’s price falls sharply, the value of both collateral and position PnL declines in tandem, increasing liquidation risk.

Binance’s differentiation between USDⓈ‑M and COIN‑M has become standard language in derivatives circles. Institutional clients, market‑makers, and sophisticated retail traders need to understand that “COIN‑M” in a headline likely signals a futures category, not a specific coin project. When news reports mention “COIN‑M listings” or “COIN‑M delistings,” they are generally referring to changes in the menu of coin‑margined linear and delivery futures on major exchanges, which can impact liquidity and basis trade opportunities across the ecosystem.

How COIN‑M contracts interact with spot and options

The presence of COIN‑M contracts affects market structure beyond derivatives. Because they settle in the underlying asset, they create natural demand for that coin at expiry, particularly for quarterly delivery contracts. This can influence funding rates, basis spreads, and spot liquidity around settlement windows. Arbitrageurs monitor the relative pricing between COIN‑M, USDⓈ‑M, and spot markets, seeking to capture risk‑free or low‑risk returns by going long in one venue and short in another.

Moreover, COIN‑M futures often coexist with options markets on the same underlying. For BTC and ETH, for instance, traders may use COIN‑M futures to hedge or replicate exposure to options positions, fine‑tuning delta and gamma exposure while keeping their collateral in the underlying coin. The interplay between coin‑margined futures, stablecoin‑margined futures, and options contributes to the overall efficiency—or instability—of perpetual futures rates, implied volatility, and cross‑exchange spreads.

The language around “COIN” in this context can be especially confusing when combined with branded coins and equities. A trader might, on the same dashboard, see COIN‑M BTC contracts, tokenized COIN equities, and Solana meme coins, all displayed with slightly different tickers and collateral rules. Understanding that “COIN‑M” here is a category label for margining, not a specific asset, is essential for avoiding mis‑allocation and leverage mistakes.

UAE’s largest fuel retailer ADNOC Distribution will accept stablecoin in 980 stations in three countries. The company has partnered with Al Maryah Community Bank to enable AE Coin payments via the AEC Wallet at fuel pumps, convenience stores, and car washes. AE Coin, the UAE's first stablecoin licensed by the Central Bank, is backed 1:1 with dirhams.

Wow, this is beautiful 😍

Branded And Institutional “Coins”: From JPM Coin To AE Coin And Sango Coin

A third strand in the modern “COIN” story involves branded coins issued by banks, fintechs, governments, and corporate ecosystems that want to harness blockchain infrastructure without embracing the volatility and open governance of public cryptocurrencies. These projects often use “coin” in their name for familiarity and branding, even when the underlying design is closer to a tokenized bank deposit or e‑money instrument than to a permissionless coin like BTC.

JPM Coin is a leading example. It is described as a deposit token issued by J.P. Morgan on Base, an Ethereum layer‑2 network operated by Coinbase, and designed for institutional use cases such as cross‑border payments, intraday liquidity management, on‑chain collateral posting, and programmable payment execution. Unlike BTC or ETH, JPM Coin is fully backed by US dollar deposits at the bank and is available only to approved institutional clients, not retail users. The bank emphasizes that JPM Coin enables “programmable, bank‑backed digital money” that settles 24/7 on public blockchains while remaining within a regulated banking perimeter. Technically, this makes it a tokenized liability of J.P. Morgan rather than a native coin of a new public blockchain.

A similar pattern appears in the UAE with AE Coin, described as a dirham‑denominated stablecoin supported by Al Maryah Community Bank. AE Coin is marketed as the region’s first AED stablecoin licensed by the Central Bank, fully backed one‑to‑one by dirham reserves. Through the AEC wallet, users can buy, hold, transfer, receive, and sell AE Coin at “internet speed,” and a major fuel retailer, ADNOC Distribution, has announced it will accept AE Coin payments at hundreds of fuel stations, convenience stores, and car washes across multiple countries. Here, the “coin” terminology masks the fact that this is effectively a regulated stablecoin integrating with existing retail payment rails.

On the more speculative end are national and quasi‑national coins like Sango Coin in the Central African Republic. Launched in 2022, Sango Coin was marketed as a transformative project that would open access to land, natural resources, and citizenship through tokenization, inviting foreign investment into the country’s economy. However, a detailed report by the Global Initiative against Transnational Organized Crime concluded that Sango Coin and related projects in the Central African Republic’s crypto push are plagued by opacity, poor design, and a high risk of enabling money laundering and foreign exploitation. The report highlights the lack of transparency about who controls the project, how funds are managed, and what real‑world rights token holders actually receive, painting a picture very different from the glossy launch marketing.

Meanwhile, the same jurisdiction has spawned a more overtly speculative “Central African Republic Meme” coin, whose CAR token trades on crypto markets as a meme asset distinct from Sango Coin. CAR Meme’s price data shows low unit prices and modest trading volumes, underscoring that “coin” in its name functions mainly as a meme wrapper to attract speculative interest. These overlapping projects in a single country illustrate how “coin” can be stretched from quasi‑sovereign branding to pure meme speculation, with very different risk and governance profiles.

Deposit tokens, stablecoins, and the path to on‑chain banking

The example of JPM Coin highlights a broader trend toward deposit tokens and bank‑issued coins. J.P. Morgan describes JPM Coin as a deposit token that represents claims on customer deposits and can be used to move money, post collateral, and settle transactions on public blockchains in a programmable manner. This is distinct from traditional stablecoins issued by non‑bank entities, which may rely on varying mixes of cash, treasuries, and other reserves. Deposit tokens like JPM Coin are designed to sit squarely within banking regulation, offering on‑chain functionality while preserving the familiar legal structure of bank deposits.

In this context, “coin” serves primarily as a user‑friendly label. From a technical and legal standpoint, JPM Coin is a permissioned token on a public L2, controlled by the issuing bank, with strict onboarding and usage controls. Yet by framing it as a coin, J.P. Morgan can align it conceptually with other digital monies and emphasize speed, programmability, and composability with DeFi‑style infrastructure on Base. Similar dynamics play out with AE Coin, which relies on bank licensing and centralized reserves but markets itself as a next‑generation coin for payments and wallets.

For crypto participants, the key question is how far these branded coins will integrate with open DeFi and whether they will compete or coexist with more decentralized stablecoins and base‑layer coins. JPM Coin’s deployment on Base suggests a deliberate move toward bridging institutional finance with public chains, while still controlling counterparties and use cases. That could create a two‑tier ecosystem where regulated coins like JPM Coin and AE Coin circulate alongside permissionless coins and tokens, with varying degrees of interoperability.

BONK airdrop to Solana community

Coinbase Q2 2024 earnings NFT minted on-chain

- 2025-01launch

TRUMP meme coin launch, surges to $75

- 2025-01launch

MELANIA coin launch; Hayden Davis admits shared team with LIBRA

- 2025-02exploit

Bybit hack; ZachXBT traces laundering through 920 meme-coin addresses

LIBRA / CAR meme coin scandals prompt Bermuda to announce national coin

$COIN stock crosses $300 for first time in years

ARK Invest acquires $17.8M in COIN and $11.2M in HOOD during market sell-off

Memecoins, Game Coins, And Creator Coins

No discussion of “COIN” in crypto would be complete without addressing memecoins and the broader culture of speculative “coins” launched for entertainment, viral marketing, or pure financial play. In this domain, “coin” often refers to tokens issued on existing chains like Solana, Ethereum, or BNB Chain, rather than to native coins in the strict sense. The terminology persists because it resonates culturally: people “ape into coins,” “launch coins,” and “hold bags” of coins, regardless of the underlying technical classification.

Solana has become a prominent venue for memecoin launches, supported by user‑friendly wallets like Phantom and trading bots such as BONK BOT or Trojan, which streamline buying and selling meme tokens directly from chat interfaces. Educational content shows users how to export private keys from bots, import them into Phantom, fund them with SOL from centralized exchanges like Binance or OKX, and then use bot interfaces to buy and sell newly launched Solana meme coins with varying allocations of SOL. This workflow illustrates how easy it has become for retail participants to rotate into fresh meme “coins” within minutes of launch, using mobile‑friendly tooling.

Regulated products are beginning to touch this space as well. Bitcoin Capital, for example, has launched an exchange‑traded product (ETP) that holds the Solana meme coin BONK and trades on the SIX Swiss Exchange, Switzerland’s third‑largest stock exchange. This Bonk ETP allows investors to gain exposure to BONK through a traditional brokerage account, transforming a high‑volatility Solana meme asset into a regulated, exchange‑listed instrument. It is a striking instance of how a memecoin can be wrapped into institutional infrastructure without losing its identity as a “coin” in popular discourse.

Game and social coins add another layer. The Trump Billionaires Club, a licensed mobile game themed around billionaire lifestyles, is launching with a play‑to‑earn model powered by a TRUMP meme coin, offering a rewards pool of one million dollars’ worth of TRUMP coin to players. The game runs on Solana and positions TRUMP coin as both an in‑game currency and an externally tradable meme asset. Creator coins, social tokens, and fan coins operate similarly, with individuals or communities issuing their own branded “coins” to represent membership, influence, or speculative expectation of future relevance.

This proliferation has created fertile ground for abuse and manipulation. Binance recently suspended an employee after an internal investigation found that they had secretly assisted in launching a BNB Chain meme coin and then used an official Binance Futures X account to promote it immediately after launch, driving its market cap briefly to around six million dollars before an internal audit and whistleblower program exposed the misconduct. In a separate incident, Binance co‑CEO Yi He’s WeChat account was hacked to promote a memecoin called MUBARA, with attackers profiting by dumping the token after creating artificial demand via false endorsements. These episodes show how the language and culture of “coins” can be weaponized, especially when users conflate official communications with personal endorsements.

Speculation, narratives, and AI‑driven launches

The memecoin phenomenon is increasingly interwoven with AI narratives and meta‑commentary about crypto culture itself. One recent Solana coin launch involved the founder of Zerebro, Jeffy Yu, who had previously faked his death and then resurfaced with an AI‑generated manifesto about the convergence of humans and AI into a new form of intelligence. Although the manifesto did not mention a token, a new Solana coin called Physical Limits of Intelligence (PLOI) quickly launched and surged to a multi‑million‑dollar market cap before retracing.[User newsroom text] Top traders realized substantial profits from early entries, underscoring how swiftly narratives—especially those blending AI, transhumanism, and crypto mythology—can be packaged into new “coins” on high‑throughput chains like Solana.

In such cases, “coin” is almost entirely a narrative device. There is rarely a mature product, cash flow, or governance structure underpinning the token’s valuation; instead, the “coin” represents a temporary crystallization of social attention, fear of missing out, and the possibility of life‑changing upside. From an evergreen perspective, this segment of the “coin” universe will likely persist as long as human psychology and digital platforms make speculative coordination easy. For professionals and regulators, the challenge is to recognize the memetic dynamics without confusing them with the more structural uses of “coin” in banking, derivatives, or governance.

How Traders Encounter “COIN” Across CeFi And DeFi

In day‑to‑day practice, a crypto trader or investor will encounter “COIN” in multiple guises across centralized exchanges, DeFi protocols, wallets, and news feeds. On a platform like Binance, “COIN” appears in menus for COIN‑M futures, indicating coin‑margined contracts on assets such as BTC, ETH, BNB, XRP, and SOL, coexisting with USDⓈ‑M futures that are margined in stablecoins. Portfolio margin programs may treat balances in COIN‑M and USDⓈ‑M wallets as components of a unified risk engine, blending collateral contributions from various coins and tokens. For a user, toggling between these categories without fully understanding the margin rules can lead to accidental leverage or unexpected liquidation cascades.

On Coinbase itself, users may see COIN used in market commentary as shorthand for the company’s stock, especially when analyzing correlations between Coinbase revenues and crypto asset prices. As Coinbase expands into tokenized stocks, prediction markets, and regulated token sales, some of those instruments may, in turn, reference COIN equity or COIN‑linked indices, creating layered instruments that blur the boundary between crypto coin exposure and equity exposure. In multi‑asset interfaces, BTC, ETH, SOL, BONK, TRUMP, AE Coin, and tokenized COIN shares might appear in a single portfolio view, each labeled as a “coin” or “asset” from a UX perspective.

DeFi and DEX environments add still more complexity. Aggregators and order‑book DEXs increasingly list tokenized RWAs such as shares of COIN, alongside perps on BTC, ETH, and altcoins, and a rotating cast of meme tokens. Some allow users to launch their own perpetual DEX with no code, using ready‑made integrations with on‑chain order books, risk engines, and oracles, so that a “COIN” market might refer either to COIN equity perps, COIN‑M BTC perps, or entirely new tokens whose ticker happens to be COIN. This can lead to misunderstandings when traders assume that any ticker containing “COIN” has some privileged link to Coinbase, Bitcoin, or institutional finance, when in fact it may simply be a random meme ticker.

On the infrastructure side, wallets and custody solutions often do not enforce a clear distinction between coins and tokens, presenting them all in a single “coins” list. Mobile wallets like Phantom, MetaMask, or CEX‑issued wallets may show native chains, ERC‑20 tokens, stablecoins, and memecoins under the same visual category, further diluting the technical meaning of “coin.” Educational content sometimes explains that coins are native and tokens are built on top, but the user interfaces rarely require users to internalize this structure beyond selecting the correct network before sending funds.

Institutional users confront different but related challenges. A treasury team evaluating JPM Coin, AE Coin, and USDC will see multiple “coins” with distinct legal statuses, counterparty risks, and on‑chain behaviors. A hedge fund might use COIN‑M BTC futures for directional bets, while also trading tokenized COIN equities in a DeFi lending market and speculating in Solana memecoins for asymmetric upside. For risk committees, having a common taxonomy that distinguishes base‑layer coins, bank‑issued coins, tokenized equities, and memecoins is crucial to avoid category errors.

UX confusion and ticker collisions

One persistent practical issue is ticker collision. The same three or four letter ticker may be used by unrelated projects across chains and venues. “COIN” itself is the ticker for Coinbase stock on NASDAQ, but could also be chosen by a new ERC‑20 project, a Solana meme coin, or a BNB Chain token. While reputable exchanges vet tickers to avoid obvious conflicts, decentralized exchanges and unpermissioned networks do not. This means that traders must rely on contract addresses, issuing platforms, and metadata rather than tickers alone to correctly identify assets.

News coverage can unintentionally exacerbate confusion by using shorthand. Headlines that speak of “COIN rallying” or “COIN delistings” may be referring to Coinbase stock, to coin‑margined derivatives, or to a specific token. Specialist outlets increasingly specify context—for example, “Binance Futures will delist multiple USDⓈ‑M and COIN‑M perpetual contracts” or “tokenized stocks set sail with COIN among supported tickers”—but readers still need to parse the underlying meaning. For more casual participants, the safest approach is to assume ambiguity and verify which “COIN” is in play before acting.

A LOOK INTO COINBASE: Coinbase’s “brand refresh” is really a pivot into an everything exchange—AI agents, stocks, perps, prediction markets, regulated token sales, B2B stablecoins, SocialFi, and curated DeFi—all on crypto rails. Bull case: this makes Coinbase a global financial utility, pulls TradFi liquidity onchain, scales revenue, and accelerates mass adoption. Bear case: it dilutes altcoins, centralizes power, invites heavy regulation, and could kill degen culture as capital rotates from speculative tokens into real, cash-flow assets.

- Fraud / Rug PullHigh

Meme coin launches by political insiders and anonymous teams have repeatedly extracted tens of millions from retail buyers, with even purpose-built detection tools failing to flag novel schemes.

- Regulatory / LegalHigh

Coin Center's standoff with Senator Warren, an active DOJ prosecution of a crypto developer, and calls to impeach a sitting president over a meme coin all signal an adversarial U.S. regulatory environment.

TRUMP coin surged to $75 at launch then faced immediate insider-selling pressure; BONK rose 200% in two weeks — meme-coin-driven price swings contaminate broader market sentiment.

- CentralizationHigh

MELANIA and LIBRA sharing the same undisclosed founding team illustrates how nominally independent coin launches are routinely controlled by a single coordinated insider group.

JPM Coin processing $1B daily in cross-border settlements is real traction, but it is a permissioned, bank-controlled network — not public blockchain exposure.

- On-Chain LaunderingMedium

ZachXBT's mapping of 920 connected addresses laundering Bybit hack proceeds through meme-coin swaps into SOL demonstrates that illiquid meme coins are now a preferred laundering hop.

Risks, Regulation, And Due Diligence Around “Coins”

Because “coin” encompasses such a wide variety of instruments, from native cryptocurrencies to bank liabilities and meme tokens, risk profiles differ dramatically. Native coins like BTC and ETH are subject to protocol risk, market volatility, and macro factors, but they lack centralized issuers and have transparent supply and consensus rules. Bank‑issued coins like JPM Coin or AE Coin depend on the solvency and regulatory regime of their issuers, and may offer legal claims that resemble deposits or e‑money, but they also introduce counterparty and jurisdictional risk. Tokenized equities like COIN stock are governed by securities law and corporate disclosures, yet when wrapped as on‑chain tokens they also inherit smart contract and exchange risk.

National “coins” such as Sango Coin highlight governance and corruption risks. The GI‑TOC report on the Central African Republic’s crypto experiments argues that such projects can be co‑opted by political and criminal elites, providing new channels for money laundering, opaque asset sales, and foreign exploitation under the guise of innovation. In Sango Coin’s case, the promised link between tokens and access to land and resources appears poorly defined, raising concerns about both investor protection and local sovereignty. The simultaneous presence of a CAR meme coin further muddies the waters, suggesting that speculative appetite can be harnessed without delivering credible development outcomes.

Memecoins and game coins introduce their own vectors of harm. The Binance employee who secretly launched a memecoin and then promoted it via an official Binance Futures X account leveraged institutional trust to drive speculative demand, before internal controls intervened. Hacks of high‑profile accounts, such as the compromise of Binance co‑CEO Yi He’s WeChat account to promote the MUBARA memecoin, show how social engineering can combine with “coin” hype to victimize users.[User newsroom text] The relative ease of spinning up a new token on Solana or BNB Chain means that such schemes can proliferate rapidly, outpacing formal enforcement.

From a regulatory standpoint, authorities are increasingly scrutinizing how different categories of “coins” fit into existing frameworks. Stablecoins like AE Coin fall under central bank supervision in the UAE, while deposit tokens like JPM Coin are treated as bank liabilities subject to prudential rules. Native coins face varied treatment as commodities, payment instruments, or unregulated assets depending on jurisdiction. Tokenized COIN equities and other RWAs are clearly securities in their underlying form, but the on‑chain wrappers may raise new questions about jurisdiction, investor rights, and disclosure obligations when traded on global DeFi platforms.

Practical due diligence for any “coin”

Given this landscape, a robust due diligence framework is essential whenever a trader or institution engages with a new “coin.” The first question is what the coin actually represents. If it is a native blockchain asset, one can examine the underlying protocol, consensus mechanism, supply schedule, and track record. If it is a token, the smart contract address, issuing entity, and linkage to off‑chain assets or rights become critical. For branded coins like JPM Coin or AE Coin, understanding the legal agreements and regulatory approvals is paramount. For tokenized equities such as COIN on platforms like Kraken xStocks, investors must assess both the underlying stock and the tokenization provider’s custody and redemption arrangements.

A second question is who controls issuance and governance. Permissionless coins with broad communities differ fundamentally from centrally controlled coins whose parameters can be changed by a single entity. Sango Coin’s opacity around governance and ownership is one red flag identified by investigators. Memecoins with anonymous teams and heavy insider allocations merit particular caution; the Binance internal case shows how insiders can abuse privileged information and branding to launch and pump such coins, even in ostensibly regulated environments.

A third dimension is market structure and liquidity. COIN‑M futures on BTC or ETH enjoy deep liquidity and sophisticated market‑maker participation, whereas obscure meme coins may have only a single thin liquidity pool on a DEX. Tokenized COIN equities may trade actively during US market hours and thinly overnight, depending on the design of the tokenization vehicle. Liquidity conditions directly influence slippage, execution risk, and the feasibility of exiting positions during stress.

Risk management also entails understanding settlement and redemption. For deposit tokens like JPM Coin, redeemability into fiat deposits is a key promise. For AE Coin, the claim of one‑to‑one backing by dirham reserves under central bank supervision underpins its use in payments. For memecoins and many game coins, there is no such redemption promise; the only exit path is selling the token on a secondary market.

Conclusion

The term “COIN” has evolved from a relatively precise label for a blockchain’s native currency into a sprawling signifier that spans native cryptocurrencies, meme tokens, bank deposit instruments, national experiments, tokenized equities, and derivatives categories. Coins in the original sense, such as BTC and ETH, remain the economic bedrock of public blockchains, anchoring security and serving as base money within their ecosystems. At the same time, institutional actors like J.P. Morgan and Al Maryah Community Bank have appropriated “coin” to brand regulated deposit tokens and stablecoins, while governments like the Central African Republic have launched “coins” with contested governance and development credentials.

In parallel, the rise of tokenized RWAs and equities has brought COIN, the ticker for Coinbase stock, into the on‑chain world, where it can trade and be used as collateral on crypto venues alongside native coins and memecoins. Derivatives markets have layered on additional meanings with COIN‑M futures, which refer to coin‑margined contracts rather than specific assets. Memecoins, game coins, and creator coins have further blurred boundaries, turning “coin” into shorthand for any speculative digital asset, regardless of its technical or legal characteristics.

For a crypto news audience, the central message is that context is everything. A headline about COIN can be describing institutional on‑chain banking, a national development gamble, a Solana meme pump, or the equity performance of a listed exchange. Understanding the underlying reference—native coin, token, stock, futures category, or branded instrument—is a prerequisite for sound analysis and risk management. As tokenization accelerates and TradFi and DeFi converge, the semantic overload around “COIN” will likely intensify, making disciplined taxonomy and due diligence even more important.

Outlook

Looking forward, the word “coin” is unlikely to regain a single, clean meaning. Instead, it will continue to function as a versatile, sometimes misleading, label for digital value objects across a spectrum from fully permissionless to tightly regulated. Native coins like BTC will remain central to crypto’s macro narrative and market cycles, with price projections and halving‑driven cycles shaping the fortunes of exchanges like Coinbase and the broader COIN ecosystem. Institutional coins such as JPM Coin and AE Coin are likely to proliferate as banks and corporates seek on‑chain settlement efficiencies while staying within regulatory guardrails, embedding “coins” deeply into enterprise finance.

On the speculative frontier, memecoins and game coins will keep exploiting the cultural power of “coin” to attract attention and liquidity, with Solana and similar high‑throughput chains providing fertile ground for rapid launches. Regulatory and enforcement actions, such as internal crackdowns at major exchanges and scrutiny of national crypto projects, will shape the boundaries of acceptable behavior but are unlikely to eliminate the appetite for new “coins.” Tokenized COIN equities and other RWAs will tie the fate of crypto infrastructure companies even more closely to on‑chain markets, blurring distinctions between equity and coin exposure.

In that environment, sophisticated market participants will treat “COIN” as a starting point, not an endpoint. The real work lies in drilling down into what any given coin actually is: its legal nature, governance, collateral, redemption, and role in the broader market structure. As the lexicon stretches, the ability to decode “COIN” precisely may become one of the most valuable skills in crypto.

Latest COIN news

Trump family disclosure reveals Q1 Coinbase, MARA, and Strategy buys led by up to $250K COIN purchaseUAE’s largest fuel retailer ADNOC Distribution will accept stablecoin in 980 stations in three countries. The company has partnered with Al Maryah Community Bank to enable AE Coin payments via the AEC Wallet at fuel pumps, convenience stores, and car washes. AE Coin, the UAE's first stablecoin licensed by the Central Bank, is backed 1:1 with dirhams.A LOOK INTO COINBASE:

Coinbase’s “brand refresh” is really a pivot into an everything exchange—AI agents, stocks, perps, prediction markets, regulated token sales, B2B stablecoins, SocialFi, and curated DeFi—all on crypto rails. Bull case: this makes Coinbase a global financial utility, pulls TradFi liquidity onchain, scales revenue, and accelerates mass adoption. Bear case: it dilutes altcoins, centralizes power, invites heavy regulation, and could kill degen culture as capital rotates from speculative tokens into real, cash-flow assets.Trump Billionaires Club, a licensed mobile game launching this year, will reward players with $1M in TRUMP meme coin as they compete in a billionaire-themed board-game system on Solana.After faking death, Zerebro founder Jeffy Yu unveils AI-penned manifesto and new Solana coin. The manifesto, which did not mention a token, argues for a future in which AI and humans will converge biologically, chemically, and surgically in a new form of humanity. Physical Limits of Intelligence (PLOI) quickly surged to a $5.4 million market cap before retracing to a recent $1.1 million market cap. The top trader, known as PainCrypt0, realized profits of over $26,800 from a $2,634 investment, according to DEX Screener.Binance co-CEO Yi He’s WeChat account hacked to push meme coin MUBARA (Mubarakah). The attackers profited by selling the memecoin after creating artificial demand through the false endorsement. CZ wrote on X to warn users to ignore the messages and stay safu.Sources

- https://crypto.com/en/glossary/coin

- https://cryptoforinnovation.org/how-do-coins-and-tokens-shape-the-crypto-ecosystem/

- https://www.binance.com/en/blog/futures/421499824684903739

- https://www.binance.com/en/fee/deliveryFee

- https://robinhood.com/us/en/stocks/COIN/

- https://www.jpmorgan.com/kinexys/jpm-coin

- https://www.mbank.ae/aec-wallet/

- https://globalinitiative.net/analysis/behind-the-blockchain-cryptocurrency-and-criminal-capture-in-the-central-african-republic/

- https://coinmarketcap.com/currencies/central-african-republic-meme/

- https://www.youtube.com/watch?v=FUXFVlRKobg

- https://n26.com/en-eu/blog/what-is-token

- https://www.binance.com/en/support/announcement/detail/81092181ec124efea616f591cf335c05

- https://www.binance.com/en/futures/home

- https://www.kraken.com/xstocks

- https://www.coinbase.com/blog/system-update-the-future-of-finance-is-on-coinbase

- https://www.binance.com/en/price-prediction/bitcoin

- https://cex.io/trump-mobile-game-reward

- https://www.dlnews.com/articles/people-culture/binance-suspends-employee-who-used-official-x-account-to-pump-token/

- https://www.bitcoincapital.com/products/bonk

Community notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…