In‑depth explainer on 21Shares, the crypto ETP issuer behind ARK’s Bitcoin ETF, Polkadot, Hyperliquid and Canton products, detailing its structures, staking and yield strategies, regulatory posture and impact on institutional crypto adoption.

+10 sources across the wider coverage universe

21Shares Advances Hyperliquid Spot ETF with THYP Ticker, Targets Nasdaq2026-04

21Shares Advances Hyperliquid Spot ETF with THYP Ticker, Targets Nasdaq2026-04 21Shares co-founder Ophelia Snyder warns tokenization enthusiasm is outpacing Wall Street readiness, citing unprepared financial infrastructure for institutional adoption2026-06

21Shares co-founder Ophelia Snyder warns tokenization enthusiasm is outpacing Wall Street readiness, citing unprepared financial infrastructure for institutional adoption2026-06 21Shares lists Strategy Yield STRC ETN on London Stock Exchange, offering UK investors first exchange-traded access to Strategy’s perpetual preferred stock2026-05

21Shares lists Strategy Yield STRC ETN on London Stock Exchange, offering UK investors first exchange-traded access to Strategy’s perpetual preferred stock2026-05 HYPE jumps 23% as Bitwise, 21Shares ETFs and Coinbase USDC deal feed Hyperliquid bid2026-05

HYPE jumps 23% as Bitwise, 21Shares ETFs and Coinbase USDC deal feed Hyperliquid bid2026-05 Tesseract taps IPOR Fusion for institutional vault infrastructure, onboarding 21Shares as pilot partner to deploy compliant onchain yield strategies with segregated client vaults2026-04

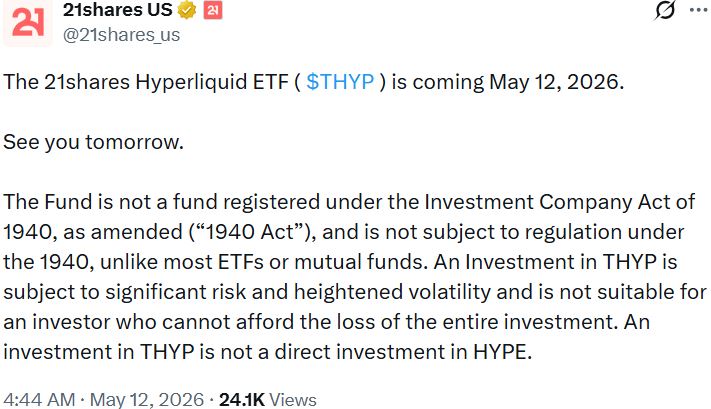

Tesseract taps IPOR Fusion for institutional vault infrastructure, onboarding 21Shares as pilot partner to deploy compliant onchain yield strategies with segregated client vaults2026-04 21Shares announces launch of Hyperliquid ETF (THYP). The ETF is not registered under the Investment Company Act of 1940 and carries significant risk and volatility.2026-05

21Shares announces launch of Hyperliquid ETF (THYP). The ETF is not registered under the Investment Company Act of 1940 and carries significant risk and volatility.2026-05

21Shares: Crypto Exchange‑Traded Products for a Regulated World

A specialist issuer of crypto exchange‑traded products, 21Shares builds ETFs, ETPs and ETNs that wrap digital assets like Bitcoin, Polkadot, Solana and Hyperliquid’s HYPE token into familiar securities accessible via traditional brokerage and bank accounts. By combining physically backed holdings, staking strategies and yield‑linked instruments, the firm has become a central player in the evolving market for regulated crypto exposure across Europe, the United States and the United Kingdom.

Background and Position in the Crypto ETP Ecosystem

The story of 21Shares is tightly intertwined with the institutionalization of crypto investing through exchange‑traded products. According to the company’s own disclosures, it listed what it describes as the world’s first physically backed crypto ETP in 2018, at a time when most traditional asset managers still regarded digital assets as a niche or speculative sideline. That early move into regulated, exchange‑listed vehicles set the template for a product suite that would grow to include single‑asset trackers, multi‑asset baskets, staking‑enabled products and yield‑linked ETNs. The firm’s stated mission is to make cryptocurrency more accessible and to bridge the gap between traditional finance and decentralized finance, positioning itself not as a trading venue but as a manufacturer of wrappers that fit seamlessly into existing brokerage and custody workflows. Over time, this specialization has allowed 21Shares to claim one of the largest line‑ups of crypto ETPs globally, with listings across multiple major European and U.S. exchanges.

A distinctive feature of 21Shares’ trajectory is the way it has moved from European exchanges into the U.S. ETF market and back out again into new geographies and asset classes. Its early European presence, including listings on platforms such as SIX, Xetra, Euronext and others, established operational credibility around custody, market‑making and regulatory engagement for crypto‑backed notes and certificates. That experience laid the groundwork for later forays into the U.S. ETF ecosystem, where it partnered with ARK Invest on the ARK 21Shares Bitcoin ETF (ARKB) and, more recently, began launching single‑asset ETFs tied to blockchain networks like Polkadot, Hyperliquid and Canton. The overall strategy is not simply to track flagship assets like Bitcoin but to systematically add support for what the firm views as "next‑generation" infrastructure chains, staking protocols and yield strategies. As a result, 21Shares has increasingly become a bellwether for the kinds of crypto assets that regulators and mainstream markets are willing to accept inside regulated wrappers.

Corporate structure and strategic partnerships have amplified that role. 21Shares is now a subsidiary of FalconX, described as one of the world’s largest digital asset prime brokers, which provides institutional trading, lending and market access services. While 21Shares emphasizes that it operates independently from FalconX, it also acknowledges that it leverages FalconX’s resources and reach to accelerate product development and distribution. This combination of a specialized ETP issuer with a large prime brokerage parent is unusual in the ETF industry and reinforces the firm’s ability to navigate both the on‑chain world of liquidity venues and the off‑chain world of regulated securities exchanges. At the same time, it introduces potential questions around related‑party transactions and conflicts of interest that investors must weigh, even as the firm highlights operational separation and institutional‑grade risk controls.

The ARK 21Shares partnership has been particularly important in legitimizing crypto ETFs in the eyes of mainstream investors and regulators. ARK Invest, known for its high‑conviction thematic equity strategies, joined forces with 21Shares to launch ARKB, a spot Bitcoin ETF that seeks to track the CME CF Bitcoin Reference Rate – New York Variant, adjusted for the trust’s expenses and liabilities. By tying the fund’s performance directly to a widely used institutional Bitcoin benchmark, the partners aimed to make the product function as a transparent proxy for spot Bitcoin exposure, while leaving the operational work of custody, creations and redemptions to specialized service providers. Regulatory filings show that the Cboe BZX Exchange later submitted a rule change to amend the ARK 21Shares Bitcoin ETF, which the U.S. Securities and Exchange Commission allowed to become effective immediately, illustrating how the structure of crypto ETFs continues to evolve even after launch. Together, ARK’s brand and 21Shares’ crypto ETP experience effectively turned ARKB into a flagship example of how spot digital asset exposure can be packaged within the ETF rulebook.

It is also significant that 21Shares has not limited itself to Bitcoin and Ethereum but has made altcoins a central part of its product roadmap. In Europe, the firm has long offered single‑asset ETPs on networks such as Solana, while more recent products in the United States target assets like Polkadot (DOT), Hyperliquid’s HYPE token and Canton Coin (CC). Internal and external commentary alike frame these offerings as milestones in the expansion of the crypto ETF universe beyond Bitcoin, with the firm often among the first to bring new layer‑1 chains or DeFi‑adjacent tokens into an exchange‑traded format. This focus has made 21Shares central to debates about which tokens are sufficiently decentralized, liquid and institutionally relevant to justify ETF status, and it has forced regulators to grapple with the specific risks associated with each underlying blockchain.

A final contextual point is the broader macro‑market and regulatory environment in which 21Shares operates. The firm’s monthly flows report for crypto ETPs and ETFs, for example, documents fluctuations in European crypto ETP assets under management, noting a 5.5% decline in overall AUM to 13.6 billion dollars during one observed December period, even as new spot altcoin ETFs like an XRP product from 21Shares and a Solana ETF from Invesco/Galaxy came to market. That juxtaposition—falling aggregate AUM alongside a proliferation of new products—captures the cyclical and competitive nature of the space. It suggests that issuers like 21Shares must navigate not just regulatory uncertainty and technological risk but also investor sentiment swings, liquidity pressures and competition from peers in both spot and derivatives‑based offerings. Within this context, the company’s strategy of diversifying across regions, asset types and wrapper structures can be seen as an attempt to create resilience in a volatile sector.

21Shares co-founder Ophelia Snyder warns tokenization enthusiasm is outpacing Wall Street readiness, citing unprepared financial infrastructure for institutional adoption

$15.1B in tokenized Treasuries is already onchain, but the top products still behave like permissioned receipts: BUIDL, USDY, BENJI and OUSG depend on whitelists, fund-admin NAVs and issuer-controlled transfers. The nasty edge case is a weekend collateral move or redemption where the token leg clears instantly and the cash, compliance, margin and recordkeeping legs wait for TradFi ops. Until broker-dealers and custodians can net that whole stack 24/7, DeFi gets composable wrappers while Wall Street keeps the kill switch.

Readers click 21Shares stories not for ETF mechanics but for the tension between regulatory capitulation (staking stripped from ETH filing) and aggressive product expansion into assets with indefensible fundamentals — signaling anxiety about whether the ETF wrapper is laundering speculative risk into institutional legitimacy.↗

Product Structures: ETFs, ETPs, ETNs and Staking

Understanding 21Shares requires some clarity on the alphabet soup of wrappers it uses: ETFs, ETPs, ETNs and staking‑enabled notes. An exchange‑traded fund, or ETF, is typically a regulated vehicle under the U.S. Investment Company Act of 1940 or analogous regimes, with strict rules on diversification, leverage and governance and with shares that trade on exchanges and can be created or redeemed via authorized participants. An exchange‑traded product (ETP) is a broader term that can encompass ETFs as well as collateralized notes and certificates that seek to track an underlying asset or index but may not fall under the '40 Act mutual fund framework, particularly in Europe. An exchange‑traded note (ETN), like those issued by 21Shares in some jurisdictions, is an unsecured debt security of the issuer that promises to deliver the performance of a reference asset or strategy, subject to the issuer’s credit risk. 21Shares uses all of these structures, tailoring each to the regulatory environment and investor demand in a given market.

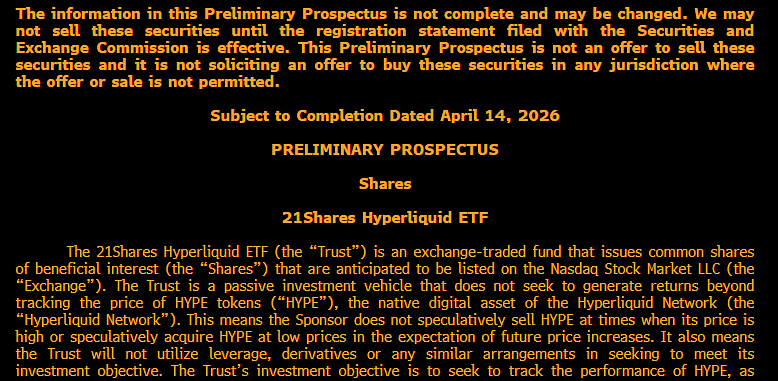

The distinction between '40‑Act and non‑'40‑Act products is especially important for U.S. investors. The 21Shares Hyperliquid ETF (THYP), for example, is explicitly described as not being registered under the Investment Company Act of 1940 and, therefore, as not subject to the same regulations and protections as '40‑Act registered ETFs and mutual funds. The firm states that THYP is an exchange‑traded product that maintains exposure to spot HYPE, the native token of the Hyperliquid blockchain, and emphasizes that the ETF is subject to significant risk and heightened volatility and may not be suitable for investors who cannot afford to lose their entire investment. By contrast, the 21Shares Canton Network ETF (TCAN) is structured as a '40‑Act fund with a "holding period design" and seeks results that correspond before fees and expenses to the price performance of Canton Coin (CC), investing at least 80% of its net assets in CC and related instruments under normal circumstances. The divergence in regulatory regimes between THYP and TCAN shows that 21Shares is willing to operate across both sides of the '40‑Act boundary depending on the nature of the underlying asset and the legal path available.

Physical backing is another central design choice. Products like the 21Shares Polkadot ETF (TDOT) and the Solana Staking ETP (ASOL) are described as "physically backed," meaning that they hold the underlying token—DOT or SOL—directly as their primary asset, rather than using futures contracts or synthetic swaps. For TDOT, 21Shares explains that the fund is intended to provide investors with exposure to the performance of Polkadot by holding DOT as its primary asset, while stressing that an investment in the fund is not a direct investment in DOT and that investors will forgo certain rights associated with holding the token directly. Similarly, ASOL tracks SOL’s performance while capturing staking yields, and it is fully backed by SOL held in cold storage by an institutional‑grade custodian, which the firm argues offers greater protection than many retail custody options. These design features underscore how the firm attempts to replicate as closely as possible the economic exposure of holding a coin, while also inserting an intermediary layer that changes the investor’s legal and operational position.

Perhaps the most distinctive innovation in 21Shares’ toolkit is the integration of staking within exchange‑traded products. The Hyperliquid ETF documentation states that the trust may stake a portion of its HYPE holdings to support the operations of the Hyperliquid blockchain and potentially earn rewards, provided the sponsor believes this can be done without undue legal or regulatory risk. The net staking rewards rate, which reflects the estimated annualized return on staked assets after the deduction of applicable fees and expenses, is disclosed but explicitly framed as not reflective of the fund’s overall performance and subject to change based on network conditions and the proportion of assets deployed. In the case of ASOL, the product is designed to track SOL’s price while capturing staking yields that are reinvested back into the ETP, which may enhance long‑term performance relative to a non‑staking spot tracker but also introduces additional staking‑specific risks. These hybrid structures position 21Shares at the intersection of ETF engineering and protocol economics, raising questions about how on‑chain validator risk, slashing penalties or governance changes might feed through to exchange‑traded investors.

To understand how these products function in practice, it is helpful to look at the mechanics described in regulatory filings such as the S‑1 registration statement for THYP. According to that document, the 21Shares Hyperliquid ETF is a passive investment vehicle that does not seek to generate returns beyond tracking the price of HYPE as measured by a specified pricing benchmark, nor does it engage in speculative trading, leverage or derivatives. The trust issues common shares of beneficial interest that are expected to trade on an exchange and values its shares daily based on HYPE prices reported by the pricing benchmark. Creations and redemptions occur in baskets of shares, with authorized participants transferring HYPE into or out of the trust in exchange for blocks of shares that reflect the quantity of HYPE per share, net of accrued fees and expenses. Aside from these primary‑market transactions and extraordinary circumstances, the trust does not intend to buy or sell HYPE, instead simply holding the token and adjusting share supply as needed to meet investor demand. This architecture mirrors that of commodity‑backed ETFs and demonstrates how 21Shares adapts a familiar mechanism to crypto assets.

The diversity of wrappers can be illustrated by comparing several flagship products side by side. Drawing on issuer disclosures and exchange listings, one can summarize some of the key characteristics of selected 21Shares products as follows:

| Product | Wrapper Type | Ticker | Underlying Asset | Exchange | Fee (Mgmt) | Notable Feature |

|---|---|---|---|---|---|---|

| ARK 21Shares Bitcoin ETF | ETF (U.S., spot BTC) | ARKB | Bitcoin (CME CF BRRNY benchmark) | Cboe BZX | Varies by prospectus | Joint venture with ARK; spot BTC exposure |

| 21Shares Polkadot ETF | Digital Asset ETF (non‑'40 Act) | TDOT | DOT (Polkadot) | Nasdaq | 0.30% | First U.S. spot Polkadot ETF; physically backed |

| 21Shares Hyperliquid ETF | Digital Asset ETF (non‑'40 Act) | THYP | HYPE (Hyperliquid) | Nasdaq | 0.30% (waived 2025‑26) | Spot HYPE exposure plus potential staking rewards; high‑risk disclaimer |

| 21Shares Canton Network ETF | Digital Asset ETF ('40‑Act) | TCAN | Canton Coin (CC) | Nasdaq | 0.50% (waived 2025‑26) | Tracks CC; 80%+ in CC and related instruments |

| Solana Staking ETP | ETP | ASOL | SOL (Solana) | European exchanges | Varies | 100% physically backed; staking yields reinvested |

| Strategy Yield ETN | ETN | STRC | Stretch preferred stock (Strategy Inc.) | LSE and others | 0.00% | High‑yield, equity‑linked note referencing Bitcoin‑backed corporate treasury |

This table highlights that 21Shares operates across a spectrum of regulatory classifications and underlying exposures. Some products, like ARKB and TCAN, sit firmly within the ETF paradigm, while others, such as THYP and TDOT, are digital asset ETFs not registered under the '40 Act and therefore subject to different oversight. Still others, including ASOL and STRC, rely on European ETP and ETN structures that reflect distinct legal traditions and investor protections. For market participants, correctly interpreting the wrapper is as important as understanding the underlying token, because it determines the nature of credit risk, governance, disclosure and the degree to which securities laws apply.

Core and Altcoin Exposure: Bitcoin, Polkadot, Canton and Solana

The cornerstone of 21Shares’ product set remains Bitcoin, and the ARK 21Shares Bitcoin ETF (ARKB) is the most visible expression of that focus in the U.S. market. The fund’s objective is to track the performance of Bitcoin as measured by the CME CF Bitcoin Reference Rate – New York Variant (BRRNY), providing investors with a regulated vehicle whose performance should approximate spot Bitcoin minus expenses. By anchoring the ETF to a regulated, institutionally recognized benchmark, 21Shares and ARK aim to reassure investors and regulators that price discovery is based on transparent and robust underlying markets rather than idiosyncratic exchange prints. Regulatory filings further show that the Cboe BZX Exchange, which lists ARKB, sought and obtained immediate SEC effectiveness for a rule change to amend the ETF, a sign that both the issuer and the listing venue continue to optimize fund operations as the spot Bitcoin ETF ecosystem matures. In practice, ARKB has become part of the broader competitive landscape of U.S. spot Bitcoin ETFs, where flows, fees and liquidity conditions are watched closely by both crypto natives and traditional allocators.

Beyond Bitcoin, Polkadot is a key test case for whether altcoins can achieve ETF scale. 21Shares advanced its Polkadot strategy by filing an updated S‑1 registration statement for a spot Polkadot ETF with the SEC in early March 2025, following an initial application in January. Commentary around that filing emphasized that the firm appeared to be actively engaging with the regulator and potentially incorporating feedback to strengthen its case, underscoring how altcoin ETF approvals remain more iterative and contested than Bitcoin’s. Those efforts eventually culminated in the launch of the 21Shares Polkadot ETF (TDOT), which offers regulated exposure to DOT through a physically backed fund listed on Nasdaq. According to issuer and secondary reports, TDOT charges a 0.30% management fee and was seeded with roughly 11 million dollars in initial assets, with 21Shares holding DOT as the fund’s primary asset. As with its other physically backed products, the firm notes that TDOT provides economic exposure to DOT but does not confer the same on‑chain governance or staking rights as direct token ownership.

The Canton Network ETF (TCAN) illustrates 21Shares’ push into blockchain infrastructure explicitly designed for institutional finance. The firm describes Canton as a network that connects institutional finance with decentralized infrastructure through privacy‑preserving interoperability and tokenized asset settlement, framing it as a kind of connective tissue between traditional, permissioned systems and public‑chain technologies. The 21Shares Canton Network ETF seeks investment results that correspond, before fees and expenses, to the price performance of Canton Coin (CC), the network’s native token. Under normal circumstances, the fund invests at least 80% of its net assets, plus any borrowing for investment purposes, in CC and instruments that provide exposure to or returns consistent with CC’s price. The product is structured as a '40‑Act digital asset ETF, and as of mid‑June 2026 it reported approximately 7.05 million dollars in assets under management, a net asset value per share of around 27.13 dollars and about 260,000 shares outstanding. Notably, 21Shares has marketed TCAN as offering a liquid way to integrate exposure to Canton into portfolios while it simultaneously participates directly in the network as an active validator and Global Synchronizer participant, according to recent coverage, thereby intertwining its role as issuer with on‑chain infrastructure stewardship.

Solana provides another lens into 21Shares’ approach to altcoin exposure, particularly around staking. The 21Shares Solana Staking ETP (ASOL) is described as 100% physically backed by SOL held in cold storage by an institutional‑grade custodian. The ETP aims to track Solana’s performance while capturing staking yields, which are reinvested into the product for what the issuer characterizes as enhanced performance. By delegating the staking process to professional managers and integrating it within a regulated, exchange‑traded wrapper, ASOL allows investors to benefit from Solana’s network yields without directly locking assets in their own wallets or managing validator relationships. This design is particularly relevant because Solana is marketed as one of the most active blockchain networks for applications such as gaming, finance and identity protection, and staking is a core component of its security and reward model. The ETP, therefore, acts as a bridge between Solana’s on‑chain activity and off‑chain portfolios, but it also concentrates staking power in institutional hands, raising broader governance questions.

Altcoin expansion extends beyond these marquee names. The firm’s December flows report mentions the launch of a new XRP ETF by 21Shares and a Solana ETF by Invesco/Galaxy, suggesting that competition in the altcoin ETF space is intensifying as multiple issuers race to secure early mover advantage in each asset. That same report notes that European crypto ETP AUM declined during the period, demonstrating that product launches do not guarantee net inflows and that issuers must contend with macro sentiment and asset price cycles. Meanwhile, recent coverage has highlighted that 21Shares has also pursued ETFs tracking other tokens such as Injective (INJ), with filings from both 21Shares and other issuers awaiting SEC decisions, further illustrating the fragmentation and experimentation within the altcoin ETF segment. In aggregate, these moves position 21Shares as a leading advocate for bringing a broad menu of layer‑1 and DeFi‑adjacent tokens into regulated wrapper form, even as regulators, investors and market structure experts debate the prudence of doing so.

- 01Spot altcoin ETF filing race↗

VanEck co-filings and Cboe 19b-4 submissions for Solana drove the highest click volume, revealing readers tracking which assets win the next regulatory approval cycle after Bitcoin and Ethereum.

- 02Staking removal under SEC pressure↗

ARK 21Shares stripping staking from its Ethereum ETF application crystallized the regulatory cost of accessing institutional capital — readers wanted to understand what product integrity was being sacrificed.

- 03Meme and low-fundamentals coin ETFs↗

Dogecoin S-1 filings and the CRO ETF launch with a reported 1,873 price-to-sales ratio provoked clicks driven by disbelief and concern that credibility of the ETF vehicle is being stretched.

- 04FalconX acquisition and consolidation

The news that a prime broker is acquiring 21Shares while eyeing an IPO signaled structural consolidation in crypto ETF infrastructure, pulling in readers tracking who controls the custody and capital rails.

- 05Emerging L1 and DeFi-native ETFs↗

Hyperliquid (THYP), Polkadot (TDOT), SUI, and Sei filings showed 21Shares racing to wrap every new Layer-1 narrative — readers clicked to assess whether these products had genuine demand or were filing-as-marketing.

- 06Institutional onchain yield structuring↗

The Tesseract and IPOR Fusion vault partnership positioned 21Shares inside compliant onchain yield infrastructure, attracting readers tracking how TradFi-grade compliance is being ported to DeFi primitives.

Hyperliquid and the THYP ETF: 24/7 Markets in an ETF Wrapper

Hyperliquid has emerged as one of the most striking examples of 21Shares’ willingness to package novel crypto ecosystems into ETF form. The Hyperliquid blockchain is described as its own network on which the HYPE token functions as the native digital asset, and the broader Hyperliquid platform has been portrayed as a decentralized exchange that allows users to trade not only cryptocurrencies but also commodities like oil, silver and gold around the clock. HYPE is the token that underpins this system, and it has experienced periods of sharp price appreciation, such as a 23% jump over a single day that pushed it toward 47 dollars, driven in part by growing demand linked to ETF flows and a treasury management deal involving Coinbase and USDC according to recent coverage. Importantly, Hyperliquid is not directly available to U.S. users, meaning that for many American investors, exposure via ETFs tied to HYPE represents the primary avenue to participate economically in the network’s growth without interacting with the protocol itself.

The 21Shares Hyperliquid ETF (THYP) is designed to track the performance of HYPE by holding the token directly and valuing the fund based on a specified pricing benchmark, namely the FTSE Hyperliquid Index. The product page describes THYP as a digital asset ETF that maintains exposure to spot HYPE and is primarily listed on Nasdaq, with Anchorage Digital Bank and BitGo Bank & Trust serving as custodians. As of mid‑June 2026, THYP reported approximately 83.8 million dollars in assets under management, about 2 million shares outstanding and a net asset value per share of roughly 41.92 dollars, with daily trading volume on the order of 197,000 units. The management fee is stated at 0.30%, although the sponsor has committed to waiving this entire fee between October 9, 2025 and October 8, 2026, meaning that investors will effectively pay zero sponsor fee during that period, notwithstanding other costs such as brokerage commissions. The fund’s structure and disclosures emphasize that an investment in THYP is not the same as directly owning HYPE, that the ETF carries significant risk and volatility and that investors could lose their entire investment.

Regulatory documentation reinforces these themes. The S‑1 registration statement for the 21Shares Hyperliquid ETF describes the trust as a passive vehicle that will not use leverage, derivatives or speculative trading strategies but will instead hold HYPE and adjust share supply via creations and redemptions. It explains that when authorized participants wish to create new shares, they will deliver HYPE to the trust in exchange for baskets of shares, while redemptions will involve the trust delivering HYPE back to those participants in exchange for shares being retired. The number of HYPE tokens per share reflects the trust’s holdings net of accrued but unpaid sponsor fees and extraordinary expenses, ensuring that the fund’s per‑share value tracks net HYPE exposure. Aside from these primary‑market transactions and potential staking activities, the trust does not intend to enter into active trading of HYPE. This structure aligns THYP with commodities‑style ETFs and avoids the complexity of derivatives‑based replication, but it also ties the fund’s fate directly to the operational and regulatory status of the Hyperliquid network.

From a market‑demand perspective, 21Shares executives have framed THYP’s early performance as evidence of appetite for 24/7 trading exposure through regulated wrappers. In an interview with CoinDesk’s "Public Keys," the firm’s global head of research, Eli Ndinga, noted that the Hyperliquid ETF recorded more than 5 million dollars in inflows within days of launch and generated roughly 8 million dollars in trading volume on a single day, underscoring brisk initial interest. Ndinga pointed out that 21Shares had previously launched a Hyperliquid product in Europe and considered bringing the strategy to U.S. investors a priority, suggesting that cross‑regional experiences inform its product roadmap. He also highlighted that Hyperliquid allows traders to access crypto, oil, silver and gold markets on a 24/7 basis and cited trading activity during geopolitical tensions involving Iran, when investors turned to the platform after traditional markets had closed. According to Ndinga, this illustrates broader demand for always‑on financial infrastructure that traditional exchanges cannot currently match, and he argued that ETFs like THYP allow conventional portfolios to tap into that demand indirectly.

The interplay between THYP flows and HYPE’s spot price appears to be significant. Reporting has indicated that HYPE’s 23% rally to near 47 dollars came amid heightened attention from multiple ETF products, including offerings from 21Shares and Bitwise, as well as a deal in which Coinbase played a role as a treasury deployer or USDC partner on Hyperliquid. Separate coverage described how the 21Shares Hyperliquid ETF posted its "best day" of inflows at around 5 million dollars as Coinbase became a treasury deployer, reinforcing the impression that strategic partnerships and corporate treasury decisions can have immediate impact on ETF demand. These dynamics resemble those observed in earlier cycles when institutional allocation announcements to Bitcoin or Ethereum appeared to catalyze price moves, but they take place in a context where the underlying protocol is more experimental and, by the issuer’s own admission, subject to substantial regulatory uncertainty. For investors, the linkage between on‑chain developments, corporate partnerships and ETF flows requires careful monitoring, because it can magnify both upside and downside volatility.

A further layer of complexity arises from the availability of leveraged Hyperliquid exposure within the 21Shares product suite. The firm offers a 2x Long HYPE ETF (TXXH) that provides leveraged daily exposure to HYPE’s price, alongside similar 2x products tied to Dogecoin (TXXD) and Sui (TXXS). The website explicitly characterizes leveraged crypto ETFs as instruments built for short‑term traders that offer boosted exposure to the daily performance of a single cryptocurrency, implicitly warning that they are unsuitable as long‑term core holdings due to the effects of compounding and volatility drag. In the context of HYPE, this means that traders can not only access spot‑like exposure through THYP but also pursue amplified directional bets via TXXH, multiplying both potential gains and losses over short horizons. For the broader Hyperliquid ecosystem, the existence of these products can increase price sensitivity to short‑term sentiment and news, as leveraged flows chase intraday trends, potentially adding reflexivity to a market already influenced by protocol‑level and regulatory headlines.

From a regulatory and compliance standpoint, Hyperliquid is particularly delicate because the protocol itself restricts access in certain jurisdictions, including the United States, to comply with local laws and sanctions requirements. Ndinga acknowledged in his CoinDesk interview that Hyperliquid is not directly available to U.S. users and that this reality both constrains and motivates the ETF strategy, since 21Shares can offer economic exposure to HYPE without facilitating direct use of the platform. At the same time, he identified regulatory uncertainty as one of the biggest risks for Hyperliquid and, by extension, THYP, noting that changes in the legal treatment of decentralized derivatives platforms or the classification of specific tokens could materially affect the investment thesis. The product page reinforces these concerns by repeating that THYP is not suitable for investors who cannot afford to lose their entire investment and by underlining that it is not a '40‑Act fund and thus lacks certain investor protections associated with traditional ETFs. For regulators, THYP is a test of how far they are willing to permit ETF wrappers to reach into experimental DeFi infrastructure, and for investors, it is a reminder that not all crypto‑linked ETFs are created equal in terms of risk profile.

Yield, Staking and Onchain Strategies

Yield has become another defining theme in 21Shares’ product architecture, manifesting through staking‑enabled funds, yield‑linked ETNs and partnerships aimed at institutional DeFi strategies. The Solana Staking ETP (ASOL) is perhaps the clearest example of how staking can be integrated into a physically backed ETP to alter its return profile. ASOL is advertised as tracking SOL’s performance while simultaneously capturing staking yields, which are reinvested into the product for incremental performance over a pure price tracker. The ETP is 100% physically backed by SOL held in cold storage by an institutional‑grade custodian, a configuration meant to reassure investors that both the base asset and the staking operations are handled with robust security practices. The messaging emphasizes that investors can gain access to staking yields without directly locking their assets on‑chain, delegating node selection, performance management and slashing risk to professional managers operating within a regulated framework. In effect, ASOL turns an otherwise operationally intensive strategy—running or delegating to validators—into a simple ticker that can be bought or sold alongside equities and bonds.

Staking also features in the design of the Hyperliquid ETF (THYP), albeit with different emphasis. The trust’s documentation states that it may participate in staking a portion of its HYPE holdings to support the operations of the Hyperliquid blockchain and, in return, generate additional rewards for the fund. These rewards, after deduction of staking fees and expenses, contribute to a disclosed net staking rewards rate, but this metric is explicitly flagged as separate from the fund’s overall performance and as subject to change based on network conditions and the proportion of assets deployed. The sponsor retains discretion over whether and how much to stake, conditioned on its assessment of legal and regulatory risks, which may include concerns over whether staking could alter the regulatory characterization of the token or the fund. In interviews, 21Shares has emphasized that it prefers to rely on third‑party staking providers rather than in‑house infrastructure, arguing that this improves transparency and reduces potential conflicts of interest. That choice reflects a broader trend in institutional staking toward specialization and segregation of duties between asset owners, validators and service providers.

The Strategy Yield ETN (STRC) illustrates a different approach to yield that is not directly tied to staking but rather to corporate finance and bitcoin‑centric treasury management. Issued as an exchange‑traded note, STRC provides exposure to "Stretch," a variable rate series A perpetual preferred stock issued by Strategy Inc., which is described as a software company and the world’s largest corporate holder of Bitcoin. The underlying preferred stock is structured to trade close to its 100‑dollar par value, with a distribution rate reviewed monthly to maintain price stability and aligned with market conditions, and it currently offers an 11.50% yield with monthly cash payments that are tax‑deferred according to 21Shares’ marketing. The ETN charges a 0.00% annual fee, meaning that investors’ return is primarily driven by the underlying distribution and any changes in the preferred stock’s price rather than an additional management layer. The note has been listed on the London Stock Exchange and, according to 21Shares, across venues such as Xetra, Euronext Paris, Euronext Amsterdam and SIX, further extending the firm’s footprint in yield‑oriented products.

The listing of STRC also demonstrates how 21Shares is broadening its remit beyond pure token exposure into equity‑linked strategies that nevertheless retain a crypto‑centric logic. The underlying issuer, Strategy Inc., maintains both Bitcoin and U.S. dollar reserves, with distribution coverage of more than 50 years, and its reserve policy is explicitly Bitcoin‑centric, meaning that the preferred stock’s risk‑return profile is tightly bound to Bitcoin’s long‑term performance. In this configuration, STRC provides investors with a high‑income stream linked indirectly to Bitcoin’s role on a corporate balance sheet rather than directly to spot BTC, offering a different way to express a bullish view on Bitcoin’s integration into corporate treasury management. At the same time, as an ETN, STRC exposes holders to the credit risk of the issuer and to the structural complexities of perpetual preferred stock, including sensitivities to interest rates and corporate governance decisions. Recent coverage, including commentary around a high‑risk STRC yield ETP listing on Euronext Amsterdam, has noted that such products may be particularly volatile and that investors should treat double‑digit yields with caution.

Beyond listed products, 21Shares is also engaging with DeFi yield generation in more experimental forms. A partnership announced by Tesseract, a crypto‑focused institution, highlights that Tesseract selected IPOR Fusion for institutional vault infrastructure, with vaults designed to tap into DeFi lending markets such as Aave, Morpho, SparkLend and Euler. As part of this initiative, 21Shares was onboarded as a pilot partner to deploy compliant on‑chain yield strategies with segregated client vaults, suggesting that the ETP issuer is exploring ways to integrate DeFi yield generation into institutional frameworks that could eventually underpin future exchange‑traded products or separate mandates. The use of Fusion’s "Fuse" integrations and segregated vaults is presented as a way to meet institutional requirements for risk management, transparency and regulatory compliance while accessing on‑chain liquidity and returns. Although no specific ETF or ETP has yet been publicly tied directly to this infrastructure, the collaboration points toward a future in which 21Shares might package DeFi lending or interest‑rate strategies inside exchange‑traded wrappers subject to ongoing oversight.

Against this backdrop of yield innovation, 21Shares’ research arm has also been vocal about the risks associated with new token issuance and speculative market structures. At the EthCC conference, 21Shares researcher Darius Moukhtarzade reportedly observed that token issuance failure rates had reached record levels, attributing the core issue to a combination of low circulating supply and high fully diluted valuations (FDV). He argued that such conditions create "FDV icebergs" and "low‑circulating‑supply storms," where a small fraction of tokens trade at inflated prices relative to the eventual supply, setting up investors for significant dilution and price pressure as vesting schedules unlock. This analysis reinforces the message that not all yield or token opportunities are created equal and that even within a regulated ETP framework, due diligence on underlying tokenomics remains crucial. For an issuer like 21Shares, which must decide which assets to wrap into ETPs or ETFs, such research likely informs internal asset selection and risk scoring processes, affecting what does or does not make it into a product lineup.

ARK 21Shares removes staking from Ethereum ETF application

VanEck and 21Shares file 19b-4s for spot Solana ETF

21Shares files S-1 for Dogecoin ETF with Nasdaq

21Shares launches Polkadot ETF (TDOT) on Nasdaq — first US spot DOT ETF

Cboe files amendment for ARK 21Shares Bitcoin ETF (SR-CboeBZX-2026-020)

21Shares lists Strategy Yield STRC ETN on London Stock Exchange

Tesseract taps IPOR Fusion for institutional onchain vaults with 21Shares as pilot

- 2026-06governance

FalconX announces acquisition of 21Shares amid crypto ETF deal surge

Regulation, Risk Management and SEC Engagement

Regulation is arguably the single most important external force shaping what 21Shares can and cannot offer, particularly in the United States. The distinction between '40‑Act and non‑'40‑Act structures underpins much of the firm’s U.S. product design. TCAN, as noted, is structured as a '40‑Act fund with a holding period design and an 80% asset test in Canton Coin and related instruments, which brings it under the familiar governance, reporting and diversification rules of U.S. mutual funds and traditional ETFs. By contrast, THYP and TDOT are explicitly stated to not be registered under the Investment Company Act of 1940, placing them in a category of exchange‑traded products that rely on alternative regulatory pathways and are not subject to the same protections and oversight as conventional ETFs. These differences can influence everything from how the funds handle leverage and securities lending to the nature of board oversight and the resolution of potential conflicts of interest.

SEC filings for specific products demonstrate how 21Shares navigates these constraints. The ARK 21Shares Bitcoin ETF, for example, operates within the framework established for spot Bitcoin ETFs, which were approved after a long period of regulatory hesitancy. Its registration statement explains how the fund tracks the CME CF BRRNY index, handles custody and manages creation and redemption processes, all subject to the SEC’s conditions for preventing market manipulation and ensuring fair disclosure. The Cboe BZX Exchange’s notice of filing and immediate effectiveness of a proposed rule change to amend ARKB underscores that even after approval, crypto ETFs remain subject to ongoing regulatory adjustments, which can include changes to listing rules, redemption mechanisms or fee structures. Similarly, 21Shares’ updated S‑1 filings for the Polkadot ETF in March 2025 and later for the Hyperliquid ETF illustrate a pattern of iterative engagement with the SEC, where the issuer refines prospectus language and structural features to address evolving regulatory feedback before launch. This back‑and‑forth underscores how crypto ETF approvals are not one‑off events but continuous processes.

Risk disclosures embedded in product materials reflect regulators’ and issuers’ shared concern about investor protection. THYP’s product page is explicit in stating that the ETF is subject to significant risk and heightened volatility and that it is not suitable for investors who cannot afford to lose their entire investment. It also emphasizes that an investment in the ETF is not a direct investment in Hyperliquid and that the assets are not protected by the same regulatory safeguards that apply to '40‑Act funds. TDOT’s launch announcement similarly notes that the fund is not registered under the '40 Act and therefore is not subject to that regime’s protections, even as it is physically backed by DOT and listed on Nasdaq. These warnings are particularly salient in the context of altcoins and newer networks, where smart contract vulnerabilities, governance attacks, regulatory classifications and liquidity shocks can have outsized impact on token prices and thus on ETF net asset values.

Jurisdictional access restrictions add another layer of complexity. Hyperliquid, for instance, is not accessible to U.S. users directly, as the platform imposes geofencing and other restrictions to align with local laws and sanctions regimes. ETF investors, therefore, may gain price exposure to HYPE through THYP without being able to use the underlying protocol for trading or liquidity provision, creating a disconnect between economic exposure and functional utility. In parallel, of course, U.S. regulators are still grappling with how to categorize and oversee decentralized exchanges and perpetuals platforms more broadly, and any shift in their stance could affect not only Hyperliquid’s operations but also the perceived legitimacy of ETFs tied to its token. Similar jurisdictional issues arise in Europe and the U.K., where different regulators have imposed varying restrictions on retail access to crypto derivatives and leveraged ETPs, leading issuers like 21Shares to tailor their offerings and disclosures accordingly.

Despite these challenges, regulatory progress has been notable in some areas. Spot Bitcoin ETFs such as ARKB have opened the door to institutional capital that prefers regulated securities over direct token holdings, and recent coverage has highlighted that major European banks have significantly increased their crypto ETF holdings, including positions in ARK 21Shares’ Bitcoin ETF. That trend underscores the role of issuers like 21Shares in creating entry points compliant with banks’ and asset managers’ internal risk and compliance frameworks. Similarly, the SEC’s willingness to consider altcoin ETFs like TDOT and prospective Injective ETFs from 21Shares and other issuers suggests that, while more cautious than with Bitcoin, regulators are at least engaging with the idea of broadening the crypto ETF universe, subject to asset‑specific risk assessments and legal classifications.

Market Impact and Institutional Adoption

The availability of 21Shares products has tangible implications for crypto market structure and institutional adoption. The firm’s monthly flows report for European crypto ETPs shows that assets under management and net flows can swing meaningfully from month to month, with declines in overall AUM sometimes coinciding with the launch of new products, such as an XRP ETF from 21Shares or a Solana ETF from competing issuers. This pattern suggests that new wrappers do not automatically expand the investor base; rather, they compete for capital within a finite risk budget allocated to digital assets. At the same time, the very existence of ETPs on a growing range of tokens can deepen secondary market liquidity by drawing in market makers, authorized participants and arbitrageurs who link ETF prices to underlying spot and derivatives markets. For altcoins like DOT, SOL, HYPE or CC, inclusion in a regulated ETP lineup can serve as a signal of perceived legitimacy and operational robustness, potentially influencing which networks institutional investors consider.

Institutional demand is increasingly visible. Recent coverage from crypto news outlets has noted that large banks and asset managers in Europe have been increasing their holdings of crypto ETFs, including both Bitcoin‑focused funds like ARK 21Shares’ ARKB and diversified or altcoin products. In one notable case, a major Italian bank reportedly more than doubled its crypto ETF holdings in a single quarter, adding exposure to XRP and Ethereum alongside increased positions in BlackRock’s IBIT and the ARK 21Shares Bitcoin ETF. This kind of activity indicates that regulated exchange‑traded products are becoming the preferred channel for institutional balance sheet and portfolio exposure to digital assets, particularly for entities constrained by custody, compliance or mandate limitations that make direct token ownership impractical. For 21Shares, this institutional shift validates its strategy of building a broad, exchange‑listed product shelf.

The launch of the first U.S. ETF offering direct exposure to Canton Coin (TCAN) further illustrates how 21Shares products can catalyze institutional engagement with newer blockchain infrastructures. By framing the Canton Network as a system that connects institutional finance with decentralized infrastructures through privacy‑preserving interoperability and tokenized asset settlement, the firm and its partners are effectively inviting banks, asset managers and infrastructure providers to experiment with permissioned‑style chains via a familiar ETF format. The fact that 21Shares also participates as a validator and Global Synchronizer participant, according to coverage, means that it is not merely a passive observer but an active stakeholder in the network’s evolution. This dual role raises questions about how ETF providers might influence network governance and how on‑chain roles might feedback into ETF marketing and positioning.

Another dimension of market impact arises from price discovery and volatility transmission between ETFs and underlying tokens. HYPE’s 23% rally amid ETF launches and Coinbase treasury involvement is a case in point. When a new ETF like THYP attracts substantial inflows, authorized participants must acquire the underlying token to create new shares, thereby importing ETF demand into the spot market. Conversely, sustained outflows or discount widening can pressure underlying token prices if redemptions lead to net selling. For Bitcoin, with deep and liquid spot and derivatives markets, ETF flows are one factor among many, but for smaller tokens like HYPE or CC, ETF‑driven demand may represent a much larger share of overall volume, amplifying the impact of marginal flows. This feedback loop means that, in practice, 21Shares’ decisions about which tokens to list and how to structure products can shape liquidity, volatility and even governance dynamics in the underlying networks.

Yield products and staking ETPs add further complexity to this picture. When an ETP like ASOL accumulates large amounts of SOL for staking, it contributes to the network’s overall stake distribution and can influence validator economics and security assumptions. Concentration of stake in the hands of a few large custodians and ETP sponsors may raise decentralization concerns, even as it improves the consistency and professionalism of validator operations. Similarly, a yield ETN like STRC, tied to a corporate issuer with substantial Bitcoin holdings, can indirectly influence perceptions of Bitcoin’s role in corporate treasuries, especially if distributions remain stable through volatile market conditions. These interactions blur the boundary between primary crypto markets and the traditional capital markets where ETFs and ETNs trade, creating a multi‑layered ecosystem in which shocks in one domain can propagate to the other.

SEC scrutiny forced removal of staking yield from the Ethereum ETF product, and multiple altcoin S-1 filings (Dogecoin, Sei, Injective) remain pending with no approval certainty; any rule change on what constitutes a security directly cuts product viability.

- Token quality / selection riskHigh

The CRO ETF launched on an asset with a reported price-to-sales ratio of 1,873 and only $2.05M in annual blockchain fees, illustrating that 21Shares' product selection prioritizes novelty and partner relationships over fundamental valuation discipline.

The ARK Invest partnership concentrates distribution through a single major brand, and the pending FalconX acquisition would consolidate custody and prime brokerage under one counterparty, reducing structural independence.

Several underlying assets (Polkadot, Sei, Hyperliquid) carry thin secondary market liquidity; in a risk-off environment, ETF redemption pressure could force large-lot sells into illiquid spot markets, widening spreads materially.

The Tesseract institutional vault infrastructure using IPOR Fusion introduces smart-contract execution risk for segregated onchain yield strategies; any protocol exploit or oracle failure could affect compliant client vaults.

ARKB (ARK 21Shares Bitcoin ETF) has demonstrated meaningful inflow capacity — recording $64M in a single day — suggesting the flagship product has durable demand even as altcoin products remain marginal by AUM.

Using 21Shares Products: Investor Profiles and Considerations

For investors and traders, 21Shares’ lineup offers several distinct use cases, each with its own risk considerations. Long‑term allocators seeking core exposure to Bitcoin may gravitate toward the ARK 21Shares Bitcoin ETF (ARKB), which provides spot‑like exposure through a regulated ETF structure that is relatively well understood by institutional risk committees and regulators. Such investors may view ARKB as a portfolio building block analogous to gold ETFs, suitable for strategic allocations within a broader asset‑allocation framework, subject to volatility and macro‑driven drawdowns. Others may use products like TDOT or TCAN to express more targeted views on specific blockchain ecosystems, such as Polkadot’s multi‑chain architecture or Canton’s institutional‑grade settlement infrastructure, while relying on 21Shares to handle custody, tax reporting and operational nuances. In all cases, investors must appreciate that these funds are proxies: they track token prices or token‑linked assets but do not grant the full suite of on‑chain rights or governance capabilities associated with direct token ownership.

More tactical investors may use Hyperliquid‑related products to seek high beta to market narratives around 24/7 trading and DeFi‑native derivatives. THYP offers unlevered, spot‑like exposure to HYPE with potential incremental return from staking rewards, while TXXH provides 2x leveraged daily exposure for short‑term trading strategies. Traders might deploy TXXH to express views around specific catalysts, such as protocol upgrades, major listings, treasury announcements or macro events that could drive volume to Hyperliquid’s platform. However, the issuer itself cautions that leveraged ETFs are built for short‑term traders and that compounding effects over multiple days can lead to returns that diverge markedly from 2x the cumulative change in the underlying asset. For this reason, such products are generally unsuitable for buy‑and‑hold investors and require careful monitoring and risk controls, including attention to gaps between ETF trading hours and the 24/7 trading of underlying tokens.

Yield‑seeking investors occupy yet another niche. Those attracted to staking yields might consider ASOL, accepting Solana’s network risk and volatility in exchange for reinvested staking rewards that could, over time, enhance total returns relative to spot SOL. Others may prefer STRC’s corporate‑credit‑style yield, which offers an 11.50% variable rate linked to Strategy Inc.’s Bitcoin‑backed balance sheet, with distributions paid monthly in cash and structured to maintain a trading price near par. For income‑focused portfolios, STRC’s ETN format may be more familiar than direct DeFi lending or staking, but it comes with its own complexities, including issuer credit risk and the unique features of perpetual preferred stock. In all these cases, yield should be evaluated in the context of risk, recognizing that double‑digit yields typically imply exposure to significant market, credit, duration or protocol risk factors.

Operational considerations also play an important role in determining whether 21Shares’ products are suitable for a given investor. One of the firm’s core value propositions is that its ETPs and ETFs can be bought and sold through existing bank or brokerage accounts, eliminating the need for investors to manage private keys, on‑chain transactions or direct interactions with crypto exchanges. Custody is handled by specialized providers such as Anchorage Digital Bank and BitGo Bank & Trust for U.S. products, while European ETPs rely on institutional‑grade cold storage solutions. This can significantly reduce operational risk for institutions with limited digital asset infrastructure, but it also introduces reliance on a small set of custodians and intermediaries. Moreover, tax treatment, reporting and regulatory capital treatment of crypto ETPs can vary by jurisdiction, requiring careful coordination with legal and tax advisors.

Finally, there is the question of how 21Shares’ own risk research and market views should inform investor decisions. The firm’s warnings about token issuance failure rates and FDV‑driven distortions, as articulated by researcher Darius Moukhtarzade, suggest a cautious stance toward tokens with low circulating supply and inflated fully diluted valuations. Investors might reasonably expect that such analysis feeds into the firm’s internal screening and asset selection for new products, potentially skewing the product lineup toward assets that demonstrate more robust fundamentals or market depth. Nonetheless, the presence of high‑risk products like THYP, TXXH or STRC in the lineup indicates that 21Shares is willing to cater to risk‑tolerant segments of the market, provided that disclosures are clear and regulatory requirements are met. For users of these products, aligning position size and time horizon with their risk appetite and understanding of the underlying tokenomics is essential.

Outlook

Looking ahead, 21Shares appears poised to remain a central actor in the evolution of crypto exchange‑traded products. Its willingness to push into new territory—whether by launching the first U.S. spot Polkadot ETF, debuting a Hyperliquid ETF with staking features, or bringing Canton Coin into a '40‑Act ETF—suggests that it will continue to test the boundaries of what regulators and investors are willing to accept in ETF form. Competition from other issuers, including Bitwise and Grayscale in the Hyperliquid space and various players in the altcoin ETF race, means that differentiation will increasingly depend on the quality of product structuring, staking implementation, fee policy and research‑driven asset selection. At the same time, partnerships like the one with IPOR Fusion and Tesseract point toward a future where on‑chain yield strategies and DeFi primitives could be packaged into institutional‑grade vaults and, ultimately, exchange‑traded products, raising fresh questions about how securities law and DeFi regulation intersect.

For the broader market, the continued expansion of 21Shares’ product shelf reinforces the trend toward treating digital assets as an investable asset class accessible through conventional brokerage channels. As more banks, asset managers and corporate treasuries allocate to crypto via ETFs, ETPs and ETNs, feedback loops between on‑chain liquidity, off‑chain derivatives and regulated securities markets are likely to intensify. This could improve price discovery and deepen liquidity but also amplify contagion pathways between crypto and traditional markets, particularly in stress scenarios. In this environment, the choices that issuers like 21Shares make—about which networks to support, how to manage staking, how to handle governance and how to communicate risk—will have consequences that extend beyond individual funds to the broader architecture of crypto finance. For investors and observers alike, tracking these developments will be essential to understanding how the next phase of crypto’s integration into global capital markets unfolds.

Latest 21Shares news

Sources

- https://www.21shares.com/en-us

- https://cdn.21shares.com/uploads/current-documents/monthly-flows/21shares_MonthlyFlowsReport_Dec25.pdf

- https://www.ark-funds.com/funds/arkb

- https://www.federalregister.gov/documents/2026/04/02/2026-06353/self-regulatory-organizations-cboe-bzx-exchange-inc-notice-of-filing-and-immediate-effectiveness-of

- https://www.21shares.com/en-us/products-us/thyp

- https://www.sec.gov/Archives/edgar/data/2090011/000121390025103237/ea0262697-s1_21shares.htm

- https://www.globenewswire.com/news-release/2026/03/06/3251056/0/en/21shares-launches-polkadot-etf-tdot-in-the-united-states.html

- https://www.21shares.com/en-us/products-us/tcan

- https://x.com/21shares/status/2051986460815786122

- https://www.21shares.com/en-uk/product/asol

- https://www.moomoo.com/news/post/70257683/21shares-says-hyperliquid-etf-demand-shows-appetite-for-24-7

- https://www.tradingview.com/news/cointelegraph:28836aefd094b:0-why-is-hyperliquid-s-hype-token-price-up-23-in-one-day/

- https://x.com/TheBlockCo/status/2055276193759244458

- https://bitdigest.substack.com/p/wednesday-may-13-2026

- https://www.youtube.com/watch?v=rZd8p4LxNk0

- https://www.mexc.com/news/868991

- https://x.com/DecryptMedia/status/2052460025293963677

- https://www.globenewswire.com/news-release/2026/05/06/3288532/0/en/21shares-launches-strategy-yield-etn-strc-on-the-london-stock-exchange-strengthening-uk-presence.html

- https://x.com/ipor_io/article/2038960123066892489

- https://www.wublockchain.xyz/news/news-18554

Community notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…