Deep explainer on how crypto ETFs work, covering bitcoin and Ethereum spot and futures funds, creation/redemption, flows, risks, income and active strategies like BITA and T. Rowe’s crypto ETF, and how tokenization and onchain finance mirror the $20T ETF boom.

+39 sources across the wider coverage universe

Morgan Stanley debuts spot Bitcoin ETF at 0.14% fee, undercutting BlackRock and Fidelity2026-04

Morgan Stanley debuts spot Bitcoin ETF at 0.14% fee, undercutting BlackRock and Fidelity2026-04 Avalanche gains Wall Street access as Bitwise Asset Management lists AVAX ETF on NYSE, unlocking institutional exposure and staking yields2026-04

Avalanche gains Wall Street access as Bitwise Asset Management lists AVAX ETF on NYSE, unlocking institutional exposure and staking yields2026-04 21Shares Advances Hyperliquid Spot ETF with THYP Ticker, Targets Nasdaq2026-04

21Shares Advances Hyperliquid Spot ETF with THYP Ticker, Targets Nasdaq2026-04 Goldman Sachs files with the SEC for new managed fund, Goldman Sachs Bitcoin Premium Income ETF.2026-04

Goldman Sachs files with the SEC for new managed fund, Goldman Sachs Bitcoin Premium Income ETF.2026-04 NYSE welcomes Morgan Stanley Investment Management to launch $MSBT, the first spot Bitcoin ETF from a major U.S. bank, marking a milestone in institutional crypto adoption2026-04

NYSE welcomes Morgan Stanley Investment Management to launch $MSBT, the first spot Bitcoin ETF from a major U.S. bank, marking a milestone in institutional crypto adoption2026-04 Injective becomes first altcoin with CFTC-regulated futures on Bitnomial, starting ETF approval clock2026-04

Injective becomes first altcoin with CFTC-regulated futures on Bitnomial, starting ETF approval clock2026-04

Exchange-Traded Funds (ETFs) in Crypto: Structure, Mechanics, and Market Impact

An exchange-traded fund (ETF) is an investment vehicle that pools assets and issues shares that trade on stock exchanges throughout the day, giving investors diversified or targeted exposure via a familiar brokerage wrapper. In crypto, ETFs have rapidly become a central bridge between traditional capital markets and digital assets, reshaping how institutions and retail investors access bitcoin, Ethereum, and other tokens.

ETFs sit at the intersection of fund management, market microstructure, and regulation, which makes them uniquely important for understanding how crypto is becoming “financialized” and integrated into mainstream portfolios. The core ETF design—open-ended shares that can be created and redeemed by large dealers to keep prices tethered to underlying assets—has been adapted for everything from stock indexes to physical gold, and now to spot and futures-based crypto products. Bitcoin futures ETFs first introduced regulated, exchange-traded exposure to bitcoin derivatives in the United States, while the approval of spot bitcoin exchange-traded products (ETPs) and, later, Ethereum ETPs marked a watershed for direct crypto exposure in brokerage accounts. Flagship spot products such as BlackRock’s iShares Bitcoin Trust (IBIT) and the converted Grayscale Bitcoin Trust pulled tens of billions of dollars of assets into listed vehicles, even as flows have swung between heavy inflows and sizable outflows as market sentiment shifts. A second wave of innovation is now layering options overlays, active management, and multi-asset strategies on top of these core exposures, typified by income-focused covered-call products such as BlackRock’s iShares Bitcoin Premium Income ETF (BITA) and the T. Rowe Price Active Crypto ETF approved for listing on NYSE Arca. At the same time, critics warn that packaging bitcoin “into an ETF” risks undermining its ethos of self-custody and decentralization, while large ETF sponsors and custodians come to control a growing share of the asset’s float. Against this backdrop, the ETF template is also informing onchain finance: tokenization efforts are explicitly modeled on the ETF industry’s rise, with issuers like Ondo Finance hiring veteran ETF executives to build fully tokenized portfolio products that blur the line between traditional ETFs and decentralized finance. Understanding what an ETF is, how it works, and how crypto ETFs are regulated and traded has therefore become essential for anyone following digital asset markets.

What Is an ETF? Core Concepts and Crypto Adaptation

Exchange-traded funds were originally designed as open-ended pooled vehicles that track an index or strategy while trading on exchanges like a stock. At their core, ETFs hold a basket of assets—such as stocks in an index, bonds in a sector, or physical commodities—and issue shares that represent proportional claims on that basket. These shares can be bought and sold throughout the trading day in the secondary market, with prices that fluctuate in response to supply and demand but remain anchored to the fund’s net asset value (NAV) through a creation and redemption mechanism handled by authorized participants. In the United States, ETFs are generally regulated by the Securities and Exchange Commission (SEC) as investment companies under the Investment Company Act of 1940, although commodity- and currency-based products are often structured under different rules as exchange-traded products (ETPs) or trust shares.

In crypto, regulators and issuers have adopted this basic structure but with important legal and operational twists. Bitcoin futures ETFs, for example, are structured as funds that gain exposure by investing in standardized bitcoin futures contracts listed on CFTC-regulated exchanges, rather than holding bitcoin directly. These products are still overseen by the SEC at the fund and share level, but their primary underlying contracts fall under the jurisdiction of the Commodity Futures Trading Commission (CFTC), which regulates bitcoin futures trading on venues such as the Chicago Mercantile Exchange. Spot bitcoin products, by contrast, are typically organized as commodity-based trust shares that hold actual bitcoin in custody for the benefit of shareholders, and are listed pursuant to exchange rules governing commodity-based ETPs rather than as traditional 1940 Act mutual fund ETFs. Ethereum and other crypto-based ETPs have followed similar templates, with the SEC approving listings under commodity-based trust share rules while layering on asset-specific conditions such as prohibitions on staking.

The ETF label is therefore somewhat elastic in crypto discourse. Market participants and media often refer to any listed, exchange-traded vehicle that tracks a crypto asset as an “ETF,” even when the legal structure is a grantor trust or commodity pool rather than a 1940 Act fund. This is partly because, from an end-investor’s perspective, these vehicles behave like ETFs: they trade intraday on stock exchanges, can be held in brokerage and retirement accounts, and provide economic exposure to the underlying asset without requiring direct custody or onchain interaction. However, the nuances of their structure—whether they hold futures or spot, whether they are taxed as partnerships or trusts, and whether they can engage in activities like staking—have material implications for performance, risk, and regulatory treatment. As crypto markets mature, distinguishing between “ETF-like” wrappers and their exact legal form has become increasingly important for both compliance and portfolio construction.

ETF Structure in Traditional Markets

In traditional finance, an ETF is typically organized as an open-ended investment company or unit investment trust that is sponsored by an asset manager, holds a portfolio of assets, and issues shares that represent fractional ownership interests. The fund’s objective is usually to track the performance of a specified index or benchmark, such as the S&P 500, a sector index, or a rules-based strategy. To maintain alignment between the ETF’s market price and the value of the underlying portfolio, the fund relies on a group of large institutional trading firms known as authorized participants (APs). These APs have the right, but not the obligation, to create new ETF shares by delivering a “creation basket” of underlying securities (or cash) to the fund, or to redeem shares by delivering ETF shares back to the fund in exchange for the underlying holdings.

This creation and redemption process takes place in the primary market and is distinct from the secondary-market trading that most investors experience when they buy or sell ETF shares on exchanges. When the ETF’s share price drifts above its NAV, APs can buy the underlying securities in the open market, deliver them to the ETF sponsor in exchange for new shares, and then sell those shares on the exchange at the higher market price, pocketing the difference. Conversely, if the ETF trades below NAV, APs can buy ETF shares in the secondary market, redeem them with the sponsor for the underlying securities, and sell those securities, again capturing arbitrage profits. These arbitrage activities are opaque to most investors but are crucial for keeping ETF prices closely aligned with the value of their holdings and for ensuring that funds can expand or contract in line with demand.

The SEC oversees ETFs both at the fund level and through regulation of the exchanges on which they trade. ETFs are required to provide detailed disclosure of their holdings, strategy, fees, and risks, and must comply with rules governing diversification, leverage, and fair treatment of shareholders. In return, they benefit from a framework that permits intraday trading, in-kind creations and redemptions that can be tax-efficient for certain portfolios, and the ability to deliver index exposure at relatively low cost. Over the past three decades, this structure has fueled explosive growth, turning ETFs into a multi-trillion-dollar industry and the primary vehicle through which many investors access equities, bonds, and commodities.

ETF, ETP, Trust, and Commodity Pool: Why Labels Matter for Crypto

While “ETF” has become shorthand for any index-like exchange-traded vehicle, the legal structures used in crypto exposure products differ in important ways. Bitcoin futures ETFs registered under the Securities Act issue shares in investment companies that hold futures contracts via a wholly owned subsidiary, which is itself organized as a commodity pool. The CFTC oversees the trading of the underlying futures on regulated exchanges and the operation of the commodity pool, while the SEC regulates the ETF and its shares as securities. These funds must comply with both sets of rules, including position limits and margin requirements in the futures market, and investment company regulations in the securities market.

Spot bitcoin products approved in the United States are not 1940 Act funds. Instead, exchanges have listed them as commodity-based trust or grantor trust shares under exchange-specific rules like NYSE Arca Rule 8.201-E, which governs commodity-based ETPs. The SEC’s approval orders and accompanying statements emphasize that these products are fundamentally different from traditional ETFs, even though they trade similarly on exchanges and are marketed to many of the same investors. They are structured as trusts that hold bitcoin, with each share representing a fractional undivided interest in the underlying bitcoin held in custody on behalf of shareholders, and with sponsor fees paid from the trust’s assets. Because they are not investment companies, they do not fall under the Investment Company Act’s protections and restrictions, but they are still subject to disclosure, listing standard, and anti-fraud provisions of the federal securities laws.

Ethereum and other crypto-based ETPs have followed a similar pattern. When the SEC approved the listing and trading of eight Ethereum ETPs—including products from Grayscale, Bitwise, iShares, VanEck, ARK 21Shares, Invesco Galaxy, Fidelity, and Franklin—it did so under commodity-based trust share rules. The approval orders explicitly prohibited these ETPs from staking ETH, reflecting the SEC’s view that staking might raise additional regulatory questions and investor-protection issues that were not addressed in the initial rule filings. At the same time, exchanges like NYSE Arca have pursued rule changes to treat certain active crypto ETPs—such as the T. Rowe Price Active Crypto ETF—as “generic” commodity-based trust shares, signaling that digital asset ETPs are beginning to be integrated into standardized listing frameworks rather than treated as novel, non-generic products.

For crypto investors and observers, this alphabet soup of structures—ETF, ETP, trust, commodity pool—can be confusing, but it is central to understanding both regulatory risk and product behavior. Futures-based ETFs may suffer from roll costs and tracking error relative to spot prices, while spot ETPs face custody, security, and premium/discount dynamics tied to trust structures. Income-oriented products like BITA add another layer by organizing as partnerships for tax purposes, which can change how gains, losses, and distributions are reported to investors. In practice, all of these vehicles are often labeled “ETFs” in conversation because the end-user experience centers on exchange-traded shares that provide economic exposure to crypto. The underlying structure nonetheless matters for performance, tax treatment, and the legal protections that apply.

Crypto critic Nouriel Roubini backs Atlas's USAFi token, bringing Nasdaq-listed ETF collateral onchain in Q3 2026

Nouriel Roubini, one of crypto's loudest skeptics, co-authored Atlas's USAFi whitepaper and is backing a Q3 2026 launch under Dubai VARA. USAFi is pitched as a permissionless ERC-20 backed by the SEC-registered, Nasdaq-listed Atlas America Fund ETF, with reserve assets at Bank of New York and exposure across Treasuries, gold, commodities, defense, cyber, and AI-linked equities. Securitize says it will provide the tokenization stack, putting Roubini inside the RWA boom he can square with his old critique: unbacked tokens bad, real collateral onchain acceptable.

Readers click ETF coverage not for mechanics but for market-power scorecards: who is accumulating how much BTC, who is winning the regulatory race, and whether TradFi giants like BlackRock are quietly cornering the asset — approval itself was almost secondary to the dominance story that followed.↗

Creation, Redemption, and ETF Price Alignment

The creation and redemption mechanism is the engine that keeps ETF share prices closely linked to the value of their underlying holdings. Understanding this engine is essential for evaluating ETF liquidity, tracking error, and the potential impact of large flows on the underlying crypto markets.

Primary vs Secondary Markets in ETFs

When investors think about trading ETFs, they generally think of buying and selling shares on an exchange, just as they would a stock. This activity takes place in the secondary market, where buyers and sellers transact with each other at market-determined prices, and where market makers post bid and ask quotes to facilitate liquidity. The volume that appears on an exchange’s tape reflects this secondary-market activity and is often used as a proxy for an ETF’s liquidity. However, ETF liquidity is also fundamentally supported by the primary market, where authorized participants transact directly with the fund.

In the primary market, APs can assemble or disassemble large blocks of ETF shares—often 25,000 or 50,000 shares at a time—known as creation units. To create new shares, an AP delivers the specified creation basket of securities or other assets (or sometimes cash) to the ETF sponsor, which in turn issues a creation unit of ETF shares that the AP can sell in the secondary market. To redeem shares, the AP delivers a creation unit of ETF shares to the sponsor and receives the underlying basket or cash in exchange. This primary-market process does not involve retail investors directly; rather, it is a wholesale mechanism that allows the ETF share supply to expand or contract in response to demand.

The interplay between primary and secondary markets becomes particularly important in periods of heavy trading or volatile markets. When trading volume in the secondary market increases significantly and pushes ETF prices away from NAV, APs can step in through the primary market to create or redeem shares, thereby arbitraging away price discrepancies. If more investors want to buy the ETF than sell it, pushing the price above NAV, APs create new shares and sell them, increasing supply until the price re-converges toward NAV. If selling pressure pushes the ETF price below NAV, APs buy shares in the secondary market, redeem them for the more valuable underlying assets, and reduce the supply of ETF shares until the discount narrows. This dynamic, combined with competition among multiple APs and market makers, is what allows ETFs to trade very close to their NAV in ordinary conditions.

How Creation and Redemption Work in Practice

In traditional equity or bond ETFs, the creation basket typically mirrors the composition of the ETF’s underlying index, with some flexibility for substitutions or sampling. APs obtain the underlying securities, deliver them to the fund’s custodian, and receive ETF shares in-kind, rather than transacting purely in cash. This in-kind mechanism can be tax-efficient because it allows the fund to purge appreciated positions by delivering them out in redemptions, potentially minimizing the realization of capital gains within the fund. It also reduces trading costs inside the ETF itself, since APs handle much of the necessary buying and selling of underlying securities.

For commodity and crypto ETPs, the mechanics can vary. Some physically backed commodity ETFs take in-kind deliveries of the underlying commodity (such as gold bars), while others operate on a cash basis and rely on the sponsor or a designated agent to source or unwind the underlying exposure. In the case of bitcoin futures ETFs, creations and redemptions typically occur in cash: APs deliver cash to the fund in exchange for shares, and the fund’s commodity pool subsidiary uses that cash to enter into bitcoin futures positions on a CFTC-regulated exchange. The fund then manages its futures positions, rolling expiring contracts into new ones and adjusting exposure in line with creations, redemptions, and market movements. Because futures prices can differ from spot prices and because rolling contracts can incur costs or benefits depending on the shape of the futures curve, these funds may diverge from the performance of spot bitcoin over time.

Spot bitcoin ETPs such as IBIT and the converted Grayscale Bitcoin Trust are structured to hold bitcoin directly in custody accounts. Creations and redemptions can be done in-kind, with APs delivering bitcoin to the trust and receiving shares, or can involve cash that the sponsor uses to buy or sell bitcoin through authorized counterparties. The precise mechanics depend on the product’s design, its authorized participant agreements, and the capabilities of its custodians and trading partners. Operationally, this process must reconcile the 24/7 nature of the bitcoin market with the limited operating hours of traditional securities markets and custodians. When large inflows or outflows occur, the fund or its agents must source or sell significant amounts of bitcoin without unduly impacting prices or exposing the fund to counterparty risk.

These creation and redemption flows are a key channel through which ETF demand can influence spot crypto markets. Heavy net creations in a spot bitcoin ETP imply net purchases of bitcoin by the trust, which must be acquired on the underlying spot exchanges or OTC venues, potentially supporting prices. Heavy net redemptions imply net sales of bitcoin, which can pressure spot markets if not carefully managed. Similarly, in bitcoin futures ETFs, net creations and redemptions translate into net long or short open interest in futures, which can affect funding spreads and basis relative to spot. Market makers and arbitrageurs monitor these flows closely, as do crypto-native firms like Wintermute that track ETF, stablecoin, and other digital asset transfer (DAT) flows as signals of market risk appetite.

Creation/Redemption in Crypto ETFs: Specific Challenges and Adaptations

Adapting the ETF mechanism to crypto assets poses several distinctive challenges. First, the underlying markets for assets like bitcoin and ether trade continuously, across a fragmented set of exchanges and OTC desks with varying degrees of regulation and surveillance. ETF sponsors and APs must choose which venues to use for price discovery and execution, while exchanges and regulators scrutinize whether these venues are sufficiently resistant to fraud and manipulation to support a listed product. This was a central issue in the SEC’s years-long reluctance to approve spot bitcoin ETPs, with the Commission ultimately being persuaded in part by proposals that relied on regulated spot markets and surveillance-sharing agreements with large exchanges.

Second, custody of crypto assets requires secure key management, insurance frameworks, and robust operational controls to mitigate hacking and loss risks. Spot crypto ETPs typically rely on specialized custodians—sometimes affiliates of large financial institutions—to hold bitcoin or ether in segregated accounts on behalf of the trust. The integrity of these custodians is critical: any compromise could endanger the trust’s assets and thereby ETF shareholders. Futures-based ETFs avoid direct custody of bitcoin but must manage margin collateral and counterparty risk on futures exchanges, as well as the complexities of rolling contracts and maintaining target exposure.

Third, the creation and redemption process must mesh with both onchain settlement and the conventional T+2 settlement cycle in securities markets. In-kind creations involving bitcoin require APs to deliver bitcoin to a designated wallet, which can raise issues of transaction fees, confirmation times, and the timing of trades relative to the close of the ETF’s trading session. Some sponsors opt for cash creations to simplify operations, at the cost of potentially higher trading and slippage costs borne by the fund. Meanwhile, APs and market makers must manage intraday inventory, hedging their exposures in both the ETF and the underlying crypto markets, sometimes using futures, options, or perpetual swaps to bridge gaps.

Despite these complexities, the ETF mechanism has proven adaptable to crypto. The strong growth of spot bitcoin ETPs after approval, followed by alternating periods of net inflows and net outflows, demonstrates that APs and sponsors can process large primary-market flows without persistent dislocations between ETF prices and underlying spot markets. However, episodes of stress—such as rapid price declines, liquidity squeezes on underlying exchanges, or regulatory shocks—remain important test cases for how robust these structures truly are in crypto.

Types of Crypto ETFs and ETPs

Crypto exposure in ETF-like wrappers now spans a spectrum of structures and strategies, from futures-based funds to physically backed spot ETPs, options-enhanced income products, and actively managed multi-asset portfolios. Each type entails distinct risks, costs, and use cases.

Bitcoin Futures ETFs

Bitcoin futures ETFs were the first widely accessible, regulated vehicles for obtaining bitcoin-linked exposure via mainstream brokerages in the United States. These funds invest primarily in standardized cash-settled bitcoin futures contracts traded on CFTC-regulated exchanges, such as the CME, rather than directly holding bitcoin. The ETFs are registered with the SEC as investment companies, but they gain their exposure through a subsidiary—often organized in a jurisdiction like the Cayman Islands—that operates as a commodity pool trading bitcoin futures. This subsidiary structure reflects the fact that direct investment in commodity futures is generally outside the scope of the Investment Company Act’s permitted activities, requiring a separate vehicle regulated under commodity-pool rules.

Bitcoin futures ETFs aim to track the performance of spot bitcoin, but several factors can cause returns to diverge. First, because the funds hold futures contracts that expire and must be rolled into new contracts, they are exposed to the term structure of the futures market. When the futures curve is in contango—meaning longer-dated contracts trade at higher prices than near-dated ones—rolling can impose a negative “roll yield” that drags on returns relative to spot. In backwardation, roll yield can be positive, boosting returns. Second, the funds must maintain margin collateral and may hold cash or short-term fixed income instruments for this purpose, which can influence performance. Third, management fees and operating expenses reduce net returns. The CFTC emphasizes that because of these factors, the risks and returns of a bitcoin futures ETF will differ from those of buying bitcoin on the spot market or trading futures directly, and that futures-based ETFs may never fully replicate spot performance.

Despite these limitations, futures ETFs offered an important initial compromise between investor demand and regulatory caution. Futures trade on regulated exchanges with robust surveillance, clearing, and margin systems, and are subject to CFTC oversight of market integrity and position limits. For the SEC, this made it easier to assess the risk of manipulation relative to fragmented spot markets. For investors and advisors constrained to holding SEC-registered securities in traditional accounts, futures ETFs provided a way to participate in bitcoin’s price movements without setting up specialized crypto custody. Over time, however, as spot market surveillance improved and legal challenges mounted, the limitations of futures-based exposure became more apparent and pressure increased to approve spot bitcoin products.

Spot Bitcoin ETFs and ETPs

The approval of spot bitcoin ETPs in the United States marked a turning point in crypto’s integration into mainstream capital markets. In a statement accompanying the Commission’s decision to approve the listing and trading of multiple spot bitcoin ETP shares, SEC Chair Gary Gensler noted that the Commission was approving these products under the rules for commodity-based trust shares, while reiterating that bitcoin itself remains a highly speculative, volatile asset and that the approval did not constitute an endorsement of bitcoin. The approvals were conditioned on exchange rule changes that, among other things, relied on surveillance-sharing agreements with large, regulated bitcoin trading venues to mitigate concerns about fraud and manipulation in the underlying spot market.

Spot bitcoin ETPs such as BlackRock’s iShares Bitcoin Trust (often traded under ticker IBIT) and the converted Grayscale Bitcoin Trust hold bitcoin directly in custody accounts, with each share representing a claim on a specific amount of bitcoin held in the trust. BlackRock describes IBIT as offering exposure to bitcoin through an exchange-traded product, simplifying the operational and custody complexities of holding bitcoin directly. When Grayscale converted its long-standing closed-end trust into a spot ETF-like product, it eliminated a persistent discount to net asset value that had plagued GBTC, enabling more efficient arbitrage and aligning the share price more closely with the underlying bitcoin holdings.

Flows into and out of these spot products have been substantial and volatile. In the months following their launch, spot bitcoin ETPs attracted tens of billions of dollars of inflows, contributing to upward pressure on bitcoin’s price and signaling strong demand from asset managers, advisors, and institutional allocators seeking regulated exposure. Subsequently, data showed significant periods of net outflows, including a week in which spot bitcoin ETFs recorded approximately 1.72 billion dollars in net withdrawals, the second-largest weekly outflow since their inception. That week was led by a roughly 1.34 billion dollar outflow from BlackRock’s IBIT, underscoring that even flagship products can see sizable redemptions when sentiment turns. Other reporting has noted days when bitcoin ETFs bled cash even as ETFs linked to other crypto assets attracted inflows, highlighting that “crypto ETF flows” are not monolithic but differ by asset and strategy.

Flows have important feedback effects. Heavy inflows require trusts to purchase large quantities of bitcoin, potentially adding to buy pressure in spot markets, while heavy redemptions can contribute to selling pressure as trusts unwind holdings or reduce hedges. Market makers and crypto-native trading firms watch these flows closely. For example, Wintermute, a major crypto market maker and OTC desk, has warned that even after rebounds in bitcoin’s price from the low 60,000s, ETF, stablecoin, and other digital asset transfer flows have sometimes shown no clear reversal, suggesting that structural bottoms may not yet be confirmed and that bitcoin could still fall into the 50,000 dollar range. Such commentary reflects the increasingly tight linkage between ETF flows and broader market structure.

Ethereum and Other Crypto Asset ETFs

Bitcoin has been the flagship for crypto ETPs, but it is not the only asset migrating into ETF-like wrappers. Following the success and controversy around spot bitcoin approvals, the SEC in May 2024 approved the listing and trading of eight Ethereum ETPs on SEC-regulated exchanges, including products from Grayscale, Bitwise, iShares, VanEck, ARK 21Shares, Invesco Galaxy, Fidelity, and Franklin. The Commission approved these applications under the rules for commodity-based trust shares, echoing the framework used for spot bitcoin products, but did so largely on its own initiative rather than in response to a court remand, suggesting a deliberate policy shift. Importantly, the approvals came with specific conditions, including a prohibition on staking ETH via the ETFs, which prevents these products from participating directly in Ethereum’s proof-of-stake validation rewards.

The prohibition on staking has several implications. It means that ETF investors forego staking yield that onchain ETH holders can earn, which may affect the relative attractiveness of holding ETH via an ETF versus directly in a self-custodied wallet or through a staking service. It also shields ETF sponsors and custodians from the regulatory and operational complexity of running validators or engaging staking providers. From a securities-law standpoint, the SEC may view staking as potentially implicating different issues than passive asset holding, which the Commission has signaled it was not prepared to address within the initial ETF approvals. The net result is that Ethereum ETFs offer price exposure but not native yield, reinforcing the broader pattern in which ETFs provide a subset of an asset’s onchain functionality in exchange for regulatory comfort and operational ease.

Beyond bitcoin and Ethereum, ETF-like products and proposals are emerging for other large-cap crypto assets and for thematic baskets. In some jurisdictions, ETPs referencing assets such as XRP and Solana have launched, and reporting indicates that XRP and Solana ETF holders have shown resilience even during periods when bitcoin and ether ETFs experienced net outflows or price volatility. This suggests that investor bases can differ significantly across asset-specific ETPs, with some segments perhaps more long-term oriented or less sensitive to short-term macro shifts. At the same time, issuers such as VanEck have pitched their proposed ETFs on the basis of underlying network fundamentals, including protocol revenues and user metrics, arguing that such data support the investability of assets like BNB. Although regulatory approval for many non-bitcoin, non-ether spot products remains uncertain in the United States, the direction of travel is toward a broader menu of exchange-traded crypto exposures.

Income and Options-Based Crypto ETFs: The BITA Example

A second wave of crypto ETF innovation builds on core spot exposure by layering options strategies and income distribution policies. BlackRock’s iShares Bitcoin Premium Income ETF (BITA) is a prominent example of this trend. BITA is designed to give income-seeking and risk-conscious investors a way into bitcoin through a covered call options strategy built on top of IBIT, the world’s largest spot bitcoin ETP. The fund gains bitcoin exposure through a combination of direct spot bitcoin holdings and shares of IBIT, then systematically writes call options on a portion of its IBIT holdings to generate option premium, which is distributed to investors, targeting a relatively high yield.

According to product disclosures and analysis, BITA writes call options on approximately 25 to 35 percent of its portfolio’s IBIT shares, with the strategy implemented in a laddered fashion across weekly option expiries. Practically, this translates into writing call options on about 7.5 percent of its bitcoin exposure each week, creating a rolling 30 percent overwrite. The options are typically out-of-the-money, allowing BITA to retain some upside participation while sacrificing a portion of potential gains beyond the strike price in exchange for premium income. Because call options sold by BITA are written on IBIT shares rather than directly on bitcoin itself, the strategy intertwines the spot bitcoin ETP market with the listed options market, deepening the financialization of bitcoin exposure.

Structurally, BITA is organized as a partnership rather than as a traditional 1940 Act ETF, meaning that investors receive a Schedule K-1 for tax reporting instead of a Form 1099. BlackRock has argued that this design allows spot bitcoin gains inside the fund to compound in a tax-deferred manner until investors sell their shares, while options gains may receive favorable blended capital gains treatment under U.S. tax rules governing Section 1256 contracts. In addition, capital losses can potentially be passed through to offset other investment gains, and the structure aims to avoid mandatory year-end capital gains distributions common in some funds. For investors, these features may be attractive, but they also introduce complexity in tax reporting and underscore that not all “crypto ETFs” are alike in their legal and tax characteristics.

The emergence of products like BITA exemplifies how Wall Street is “productizing” crypto, transforming bitcoin from a simple buy-and-hold speculative asset into a component within a broader menu of yield-bearing and volatility-harvesting strategies. For institutions that cannot or will not hold bitcoin directly, such products provide a packaged way to earn income from bitcoin’s volatility while limiting directional exposure. For crypto purists, however, these developments raise questions about whether the asset is becoming just another source of structured-product yield, divorced from its original ethos and technical properties.

Active and Multi-Asset Crypto ETFs: T. Rowe Price and Beyond

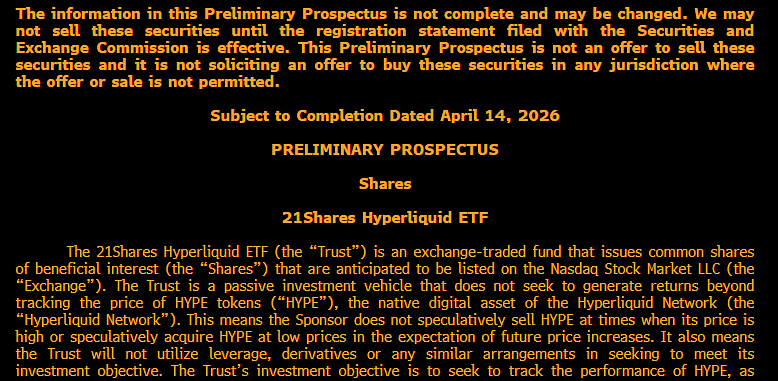

Alongside passive and options-based products, active crypto ETFs are emerging as asset managers seek to apply discretionary or systematic strategies within listed vehicles. A notable example is the T. Rowe Price Active Crypto ETF, for which NYSE Arca initially proposed a rule change to list and trade under its non-generic commodity-based trust share rules. Subsequent regulatory developments culminated in an order granting approval for NYSE Arca’s proposed rule change, as modified by amendments, to list and trade shares of the T. Rowe Price Active Crypto ETF under NYSE Arca Rule 8.201-E (Generic) Commodity-Based Trust Shares. This evolution from non-generic to generic treatment signifies that regulators and exchanges are beginning to view certain crypto-based ETPs as sufficiently standardized and well-understood to fit within existing commodity-based listing frameworks.

As an active product, the T. Rowe Price ETF is designed to adjust its portfolio in response to market conditions and the manager’s views, rather than simply tracking a static index of crypto assets. While specific strategies may include tactical allocations across large-cap tokens, stablecoins, or cash equivalents, or the use of derivatives to manage risk, the key point is that active management introduces a layer of discretionary decision-making on top of underlying crypto exposures. This raises new questions for investors about manager skill, benchmark selection, and fees, while also giving traditional asset managers a way to bring their brand and research capabilities into the crypto ETF space.

Active and multi-asset crypto ETFs also intersect with broader trends in tokenization and onchain portfolio management. Ondo Finance, for instance, has explicitly framed its tokenization efforts as mirroring the roughly 20 trillion dollar ETF boom, arguing that blockchain-based tokens can play a role similar to ETFs in packaging and distributing exposure, but with the added benefits of 24/7 trading and composability with decentralized finance protocols. To advance this vision, Ondo hired a former Invesco ETF executive to lead its onchain portfolio products, signaling a convergence between traditional ETF expertise and onchain strategy design. Over time, one can imagine active crypto ETFs that exist both as listed securities and as tokenized representations onchain, or that use onchain data and AI-driven signals to adjust exposure, blurring the boundary between ETFs and decentralized autonomous funds.

- 01BlackRock accumulation dominance↗

Headlines showing BlackRock IBIT eclipsing MicroStrategy and approaching 4% of all BTC supply framed the ETF story as a TradFi power grab, triggering outsized reader engagement around who actually controls the asset now.

- 02SEC approval timing drama↗

The drawn-out will-they/won't-they regulatory saga — fake approval announcements, analyst disagreements, comment periods, and last-minute delays — kept readers checking back for each new development.

- 03ETH ETF second wave race↗

After Bitcoin ETFs launched, readers tracked the Ethereum ETF approval process as a sequel race, with ARK filings, VanEck timing signals, and the SEC's surprise approval generating repeated high-click moments.

- 04Whale vs ETF investor divergence

Bloomberg analyst data showing whales bought dips while ETF investors sat out revealed that the two cohorts behave as distinct market actors, surfacing a structural insight readers found genuinely novel.

- 05TradFi institutional entanglement

Storylines like Vanguard hiring the BlackRock ETF architect, DRW's $200M ETF holdings, and banking coalitions lobbying the SEC signaled that crypto ETFs had become a TradFi turf battle, not just a crypto milestone.

- 06Basis trade collapse and outflows↗

Hedge funds unwinding the market-neutral Bitcoin basis trade and triggering billions in ETF outflows showed readers that ETF products had introduced new, non-obvious contagion vectors into crypto price structure.

Regulation and Market Infrastructure for Crypto ETFs

The regulatory and infrastructural backbone of crypto ETFs spans securities law, commodities regulation, exchange listing standards, custody frameworks, and derivatives markets. Understanding these layers helps explain why different types of crypto ETFs exist, why some activities (like staking) are prohibited, and how market access is expanding through ETF-linked derivatives.

SEC, CFTC, and Jurisdictional Lines

In the United States, ETFs and ETPs are primarily overseen by the SEC, which regulates both the funds themselves as securities issuers and the exchanges on which their shares trade. For funds holding securities such as stocks or bonds, the SEC’s Investment Company Act framework applies, imposing restrictions on leverage, diversification, and affiliated transactions, among other things. However, many commodity-based and currency-based exchange-traded products, including spot bitcoin and Ethereum ETPs, are structured as commodity-based trust shares or grantor trusts, which fall outside the 1940 Act but still require Securities Act registration of shares and adherence to exchange listing standards.

For products that invest in commodity derivatives such as bitcoin futures, the regulatory picture is more complex. Bitcoin futures contracts are regulated by the CFTC and must trade on CFTC-regulated designated contract markets. A bitcoin futures ETF typically gains exposure by having an investment company organize a subsidiary that acts as a commodity pool, which in turn trades bitcoin futures contracts in an effort to mimic the spot price of bitcoin. The CFTC oversees the futures market and the commodity pool’s activities, including risk management and adherence to position limits, while the SEC oversees the ETF and its shares as securities. This dual jurisdiction requires coordination and has influenced the design and risk disclosures of such products. The CFTC has underscored that “regulated” does not mean “risk-free,” noting that the risks and returns of a bitcoin futures ETF will differ from buying bitcoin on spot or trading futures directly, and urging investors to understand roll premiums, management fees, and other costs before investing.

The SEC’s statement on the approval of spot bitcoin ETPs further clarifies its stance. Chair Gensler emphasized that the Commission was acting in light of specific court decisions and the development of surveillance-sharing agreements, and that the approvals were limited to bitcoin, which he characterized as a non-security commodity, and not to other crypto assets that may be offered and sold as securities. He also reiterated that the Commission “does not endorse” bitcoin, that investors should remain cautious about its volatility and the potential for loss, and that the approval did not signal a general softening on enforcement against unlawful crypto securities offerings. For Ethereum ETPs, the Commission’s approval under commodity-based trust share rules, coupled with the prohibition on staking, suggests a cautious, asset-by-asset approach to extending ETF-like treatment.

Exchange Rule Changes and ETF Listings

Before a crypto ETF or ETP can trade on a U.S. exchange, the exchange must have appropriate listing standards in place and, in many cases, must file a proposed rule change with the SEC under Section 19(b) of the Securities Exchange Act. For novel products such as the first spot bitcoin ETPs or active crypto ETFs, exchanges like NYSE Arca and Cboe Global Markets have filed detailed rule change proposals describing the product’s structure, underlying index or asset, surveillance mechanisms, and how the listing would be consistent with investor protection and fair and orderly markets. The SEC then reviews these filings, sometimes requesting amendments or delaying decisions, before either approving, disapproving, or allowing the rule to become effective by operation of law.

The case of the T. Rowe Price Active Crypto ETF illustrates this process. NYSE Arca initially filed a proposed rule change to list and trade shares of the fund under its non-generic commodity-based trust share rules, which are used for products that do not meet standardized criteria and thus require case-by-case evaluation. After public comment, amendments, and further analysis, the SEC ultimately issued an order granting approval of a proposed rule change, as modified by Amendment No. 2, to list and trade shares of the T. Rowe Price Active Crypto ETF under NYSE Arca Rule 8.201-E (Generic) Commodity-Based Trust Shares. This meant that the fund would be listed under generic listing standards designed for commodity-based trusts that meet specified criteria, reflecting the Commission’s view that such products can be handled within a broader framework rather than treated as bespoke experiments.

Similarly, the SEC’s approvals for Ethereum ETPs involved rule filings by exchanges specifying how the ETH-based products would meet listing criteria and how surveillance arrangements would mitigate concerns about manipulation. Exchanges must also file and update rules regarding transaction fees and other terms for ETF-linked derivatives. For example, Cboe Exchange, Inc. filed a proposed rule change with immediate effectiveness to amend standard transaction fees for its Cboe Bitcoin U.S. ETF Index options (CBTX) and Cboe Mini Bitcoin U.S. ETF Index options (MBTX), reflecting the need to calibrate fee structures as trading in these options grows. Collectively, these processes demonstrate that crypto ETFs and their derivatives are deeply integrated into the same rule-based ecosystem that governs traditional ETFs and exchange-traded derivatives.

ETF Derivatives: Options and Index Products

The growth of crypto ETFs has been accompanied by the proliferation of ETF-linked derivatives, particularly options. Options on individual bitcoin ETFs and on indexes referencing bitcoin ETF prices allow traders and hedgers to express views on volatility, manage downside risk, or implement income strategies like covered calls. Cboe’s Cboe Bitcoin U.S. ETF Index options (CBTX) and Mini Bitcoin U.S. ETF Index options (MBTX), for example, are based on an index designed to reflect the price return performance of spot bitcoin as represented through U.S.-listed bitcoin ETFs. By basing the index on ETF prices rather than directly on spot or futures, Cboe creates a derivative product that fits naturally within the existing securities options ecosystem and can be traded alongside equity and ETF options.

Cboe has periodically adjusted standard transaction fees for CBTX and MBTX options via rule filings, signaling that these products are gaining traction and require thoughtful fee design to balance market-maker incentives, customer costs, and exchange economics. The existence of such options also complements income products like BITA, which themselves rely on selling call options on bitcoin ETFs to generate yield. In a sense, BITA internalizes an options-writing strategy that some investors might otherwise implement directly using ETF options, packaging it into a single share that includes both the underlying exposure and the overlay.

The availability of ETF-linked derivatives also deepens the interaction between crypto markets and macro hedging strategies. Institutional investors can use options on bitcoin ETFs or on indices like CBTX to hedge portfolios that include bitcoin ETPs, to express convex views on crypto risk within a broader multi-asset framework, or to trade relative value between spot, futures, and ETF prices. This layering of derivatives on top of ETF structures contributes to the “financialization” of bitcoin and other crypto assets, as their price dynamics become intertwined with volatility targeting, correlation trading, and risk-parity strategies in traditional capital markets.

Custody, Surveillance, and Market Integrity

Custody and market surveillance are at the heart of regulatory assessments of crypto ETFs. For spot ETPs, custodians must safeguard private keys, manage cold and hot storage arrangements, maintain robust cybersecurity practices, and implement internal controls to prevent unauthorized movements of assets. Sponsors such as BlackRock emphasize that their bitcoin ETPs simplify operational and custody complexities for investors by handling these tasks on their behalf. Nonetheless, investors ultimately bear the risk that a custodian failure, hack, or other operational mishap could impair the trust’s holdings.

From the SEC’s perspective, the suitability of the underlying markets for supporting an ETF hinges on whether they are sufficiently resistant to fraud and manipulation, and whether there are surveillance-sharing agreements that facilitate cross-market monitoring. In its statement on spot bitcoin ETP approvals, the Commission underscored the importance of agreements between listing exchanges and large, regulated bitcoin trading venues, which enable the sharing of order and trade data for surveillance purposes. The SEC argued that such arrangements, combined with the presence of regulated futures markets and other factors, helped satisfy the statutory requirement that exchange rules be designed to prevent fraudulent and manipulative acts and practices. Similar considerations informed the approval of Ethereum ETPs, although the Commission imposed additional conditions such as no staking.

At the same time, crypto-native voices have raised concerns about the implications of concentrating large amounts of bitcoin and potentially other tokens in custodial ETP structures. Executives from hardware wallet companies like Trezor have argued that “putting bitcoin in an ETF” is a poor outcome for the asset’s original vision, as it encourages investors to hold synthetic claims on bitcoin rather than the asset itself and potentially centralizes control over large pools of coins in a small number of custodians. These critics worry that such concentration could make bitcoin more vulnerable to political pressure, censorship, or rehypothecation, and could dull users’ appreciation for the self-sovereign properties of holding private keys. Regulators, for their part, focus on the need for robust oversight of those custodians to protect investors, even if doing so runs counter to some of crypto’s decentralization ethos.

ETF Flows, Market Impact, and Investor Behavior

The rise of crypto ETFs has introduced a new set of data streams and behavioral patterns into digital asset markets. Net flows into and out of ETFs, secondary-market trading volumes, and ETF-linked derivatives activity all interact with spot, futures, and onchain markets in ways that can amplify or dampen price moves.

Net Inflows, Outflows, and Price Dynamics in Bitcoin

One of the most closely watched metrics in the era of crypto ETFs is net flow: the dollar value of creations minus redemptions over a given period. During periods of enthusiasm, spot bitcoin ETPs have recorded strong net inflows, with some analysts linking these inflows to significant price appreciation as trusts buy substantial amounts of bitcoin to back new shares. Conversely, when sentiment turns or macro conditions deteriorate, outflows can be sharp. In early June 2024, for example, spot bitcoin ETFs in the United States recorded approximately 1.72 billion dollars in net outflows over a single week, marking their fourth consecutive week in negative territory and their second-largest weekly outflow since launch. BlackRock’s IBIT was the largest contributor, with an estimated 1.34 billion dollars of net redemptions that week.

Subsequent reporting indicated that outflows, while continuing, sometimes slowed markedly, illustrating how ETF flows can swing in magnitude rather than move monotonically. Data from mid-June showed that crypto ETF outflows remained under pressure, with bitcoin and ether funds losing roughly 249 million dollars in a single day amid broader market volatility. However, flows into certain thematic or alternative-asset ETFs were not uniformly negative, with some products tied to crypto sectors or non-bitcoin assets experiencing inflows even as flagship bitcoin funds bled cash. In some weeks, analysts noted that net outflows from bitcoin ETFs dropped sharply from prior peaks, signaling that selling pressure may have exhausted itself in the short term, even if a clear reversal to sustained net inflows had not yet materialized.

These flow dynamics feed back into price and volatility. When spot ETPs are in net creation mode, trusts must buy bitcoin in the market, adding to demand and potentially lifting prices if supply is inelastic. In net redemption mode, trusts either sell bitcoin or reduce hedges, contributing to supply. Market structure firms such as Wintermute watch ETF, stablecoin, and other digital asset transfer flows as key indicators of risk appetite, arguing that a sustained reversal in these metrics is often needed to confirm a durable market bottom. When ETF outflows persist alongside tepid stablecoin inflows, it may signal that both institutional and retail capital remain cautious, even if prices have bounced from local lows.

Segmenting Investors: Institutions vs Retail, Speculators vs Allocators

ETF wrappers attract a variety of investor types, from retail traders using brokerage apps to large institutions and registered investment advisors (RIAs) allocating client portfolios. The profile of buyers and sellers can differ significantly across crypto ETFs, influencing how sensitive each product is to short-term price moves or macro news. Spot bitcoin ETPs like IBIT and the converted GBTC have seen participation from pension funds, endowments, and other long-horizon allocators, as well as tactical macro funds and retail traders seeking directional exposure. Futures-based ETFs may attract more trading-oriented investors comfortable with derivatives-linked risk and tracking differences.

Income-focused products such as BITA are explicitly marketed to income-seeking and risk-conscious investors who want bitcoin exposure but also wish to generate regular cash flow and reduce upside volatility. By selling covered calls on IBIT shares, BITA effectively caps some upside participation in exchange for monthly distributions funded by option premiums, which may appeal to investors with a low-conviction or range-bound view on bitcoin. At the same time, the partnership structure and Schedule K-1 reporting may make these products more suitable for taxable accounts of sophisticated investors rather than small retail holders.

Investor behavior also differs across asset types. XRP and Solana ETF holders have been described as showing resilience, with some reports noting that these investors held through periods of heightened volatility and regulatory noise, and that ETFs tied to these assets saw net inflows even as bitcoin ETPs suffered net outflows. This may reflect different narratives and use cases: some investors may view altcoin ETFs as high-beta plays or as specific bets on ecosystem growth, while viewing bitcoin ETFs as macro hedges or digital gold proxies. The presence of whales and large institutional holders in XRP-related instruments, as indicated by “record whale volumes” around certain price levels, further suggests that the investor base in these markets is heterogeneous and may respond differently to ETF developments than bitcoin’s base.

Performance, Tracking, and Roll Costs

Assessing crypto ETF performance requires attention to tracking difference, fees, and structural factors such as roll yield. For bitcoin futures ETFs, tracking differences relative to spot can be pronounced over time because the funds must roll expiring futures into new contracts, and because the futures curve may be persistently in contango or backwardation. In contango, rolling from cheaper near-term contracts into more expensive later-dated ones imposes a drag; in backwardation, the opposite can enhance returns. Moreover, management fees and operating expenses subtract from gross performance. The CFTC highlights these issues in its educational materials, emphasizing that bitcoin futures ETFs will not track spot prices perfectly and may underperform or overperform depending on market conditions, costs, and portfolio management choices.

Spot bitcoin ETPs eliminate futures-based roll risk but still exhibit tracking differences relative to spot bitcoin. These differences arise from sponsor fees—typically charged as a percentage of assets and paid by periodically selling small amounts of bitcoin—as well as from operational friction, such as spreads on underlying trades and any cash held temporarily. For converted products like GBTC, the shift from closed-end fund structure to ETF-like structure reduced chronic premiums or discounts to NAV, improving tracking, but did not eliminate all sources of deviation. Intra-day premiums and discounts can still arise during volatile markets when creation and redemption lags, or when APs are reluctant to arbitrage aggressively because of execution risk.

Options and income products overlay additional complexities. BITA’s covered call strategy means that its returns will lag a pure spot bitcoin ETF in strongly trending bull markets, because sold calls will be exercised or bought back at losses when prices rally sharply beyond strike levels. In range-bound or modestly trending markets, however, the option premiums received can materially boost total returns and reduce volatility. Evaluating such products requires understanding not just their fee levels and asset allocation, but also their option-writing rules, strike selection, and risk management.

ETFs Beyond Bitcoin: XRP, Solana, and Thematic Baskets

While the U.S. regulatory framework has focused first on bitcoin and then on Ethereum, other jurisdictions have moved ahead with ETF-like products tied to a wider array of tokens. In these markets, ETFs or ETPs referencing XRP, Solana, and other assets have attracted flows that sometimes diverge from those of bitcoin. Reports have highlighted that XRP and Solana ETF holders have maintained strong positions even when broader crypto ETF flows were under pressure, suggesting that these investors may be expressing specific theses about network adoption, protocol revenues, or regulatory outcomes. This is consistent with the idea that altcoin ETF investors may be more thesis-driven and less focused on bitcoin’s macro hedge narrative.

Thematic crypto ETFs also play a role, grouping multiple assets around a concept such as “Web3,” “DeFi,” or “metaverse.” These baskets can dilute single-asset risk but may also entangle investors in complex correlations and idiosyncratic regulatory issues. For example, a DeFi ETF might hold tokens from protocols that face varying degrees of regulatory scrutiny, governance risk, and smart contract risk. While such products promise diversification, they also demand careful due diligence on index construction and rebalancing rules. As more single-asset and basket products seek approvals—sometimes supported by issuer presentations highlighting metrics like protocol revenues and user counts—the ETF landscape is likely to fragment into a richer array of choices that require more nuanced analysis than simply “bitcoin versus everything else.”

Ark Invest scoops up $32.5M in SpaceX shares as the stock tumbles 16%, making the aerospace giant one of the firm's top ETF holdings weeks after its Nasdaq debut

A $2T issuer selling IG notes weeks after an $85B IPO while sitting on $100.8B cash is capital-structure engineering, not a liquidity crisis. ARK averaging down through daily-transparent ETFs turns SPCX into a reflexive wrapper trade: inflows let Cathie buy the drawdown, outflows make the same position a sell-pressure source. Crypto already saw this movie with GBTC/ETHE; when the wrapper owns the narrative, flows can matter more than fundamentals for a while.

SEC approves first U.S. spot Bitcoin ETFs

BlackRock IBIT and 10 competing spot BTC ETFs begin trading

Grayscale GBTC converts from closed-end trust to spot ETF

SEC unexpectedly approves spot Ethereum ETF S-1 filings

Spot Ethereum ETFs begin U.S. trading; BlackRock ETHA launches

BlackRock ETHA surpasses $1B net inflows, first ETH ETF to do so

NYSE Arca files to list options on Bitcoin ETFs and GBTC

SEC grants approval for additional crypto ETF rule change via NYSE Arca

Strategic Uses and Trade‑Offs of Crypto ETFs

Crypto ETFs are more than just access vehicles; they can be used strategically for portfolio construction, risk management, and income generation. At the same time, they involve trade-offs relative to direct onchain holdings.

Why Use an ETF Instead of Holding Coins?

For many investors, the primary appeal of crypto ETFs is operational simplicity and integration with existing financial infrastructure. Holding bitcoin or ether directly requires managing wallets, private keys, security practices, and sometimes interactions with exchanges that may be unfamiliar or inaccessible to institutions. By contrast, an ETF allows investors to buy and sell shares through existing brokerage accounts, with positions visible alongside stocks and bonds, and with tax reporting handled via familiar forms. Sponsors such as BlackRock explicitly tout that their bitcoin products “simplify the operational and custody complexities of holding bitcoin directly,” pointing to professional custody, insurance arrangements, and institutional-grade risk management as selling points.

ETFs also fit naturally into portfolio allocation frameworks used by advisors and institutions. A wealth manager can allocate, for instance, 2 percent of a client’s portfolio to a spot bitcoin ETP as part of an alternative or inflation-hedge sleeve, implement rebalancing rules, and report performance within compliance systems designed for registered securities. For some institutional investors, mandates or internal policies prohibit direct holdings of crypto assets but permit holdings of SEC-registered securities such as ETFs. In such cases, ETFs are the only practical path to crypto exposure.

The trade-offs are significant, however. ETF investors typically cannot access an asset’s onchain utility: they cannot send or receive bitcoin, participate in DeFi, stake tokens, or directly vote in onchain governance using ETF shares. Ethereum ETPs cannot engage in staking under current SEC-imposed conditions, meaning investors forego staking rewards. Bitcoin held in a trust cannot be used in Lightning channels or other second-layer protocols. Additionally, ETF investors bear management fees and, in some cases, more complex tax treatment, as with partnership-structured products like BITA.

Critics argue that ETFification of bitcoin undermines its core ethos of self-custody and censorship resistance. A Trezor executive, for example, has been quoted as saying that “putting bitcoin in an ETF” is the worst outcome for the asset, contending that it turns bitcoin into a paper asset controlled by large financial institutions and dampens users’ appreciation for the importance of holding private keys. From this perspective, ETFs may be useful for price exposure but are at odds with the cultural and political motives that drew many early adopters to bitcoin.

Yield, Options, and Structured Strategies

As the crypto ETF space matures, more complex strategies are being packaged into ETF wrappers. Income-focused products like BITA use covered call strategies to convert bitcoin volatility into cash distributions, targeting yields that can be attractive to income-hungry investors. By writing call options on IBIT shares, BITA “sells” some of bitcoin’s upside to option buyers in exchange for upfront premium, which it then distributes monthly. The fund’s systematic approach—writing options on a set fraction of its exposure each week—aims to provide a predictable income stream while maintaining partial upside participation.

Beyond covered calls, there is scope for ETFs that implement put-writing strategies, volatility targeting, or more exotic options overlays on crypto assets or ETFs. These strategies could appeal to investors with specific risk-return preferences, such as those seeking downside protection or those willing to take on tail risk in exchange for higher income. The existence of ETF-linked options, such as CBTX and MBTX on Cboe, provides the building blocks for such strategies. Funds can write or buy options directly, or investors can implement their own overlays by trading ETF options in their accounts.

Structured strategies introduce additional layers of complexity and risk. Performance becomes sensitive not only to the price path of the underlying crypto asset but also to volatility, skew, and option market liquidity. Moreover, options strategies can magnify the impact of sharp market moves, as funds must manage delta hedging, potential assignment, and liquidity needs during stress. For crypto ETFs that already sit at the crossroad of volatile underlying assets and traditional market infrastructure, adding structured overlays increases both the opportunity set and the need for sophisticated risk management.

Active Management, Tokenization, and the Next Wave

Active crypto ETFs like the T. Rowe Price Active Crypto ETF represent another frontier, bringing discretionary or systematic trading strategies into listed vehicles. Such funds can adjust exposure across assets, rotate between cash and crypto, and potentially use derivatives to manage risk or express tactical views. For investors, active ETFs offer the prospect of outperformance relative to passive benchmarks and the comfort of delegating decision-making to a recognized asset manager. For regulators, they raise questions about suitability, disclosure of investment processes, and alignment with investor expectations.

In parallel, tokenization initiatives are explicitly taking cues from the ETF industry. Ondo Finance’s leadership has argued that tokenization mirrors the 20 trillion dollar ETF boom, as blockchain-based tokens can similarly package traditional assets and strategies into portable, tradable units. By hiring a former Invesco ETF executive to lead onchain portfolio products, Ondo is attempting to translate the know-how of building, distributing, and managing ETFs into the realm of fully tokenized investment strategies. These strategies could, in principle, be represented both as tokens on a blockchain and as ETF shares on a traditional exchange, or they could exist solely onchain but adopt ETF-like liquidity, transparency, and indexation principles.

Some observers suggest that perpetual futures, already widely used in crypto-native markets, could become “crypto’s next ETF moment” by providing simple, standardized access to leveraged or hedged exposure through centralized and decentralized exchanges. The interplay between perps, centralized futures, and ETF-linked derivatives further blurs the line between onchain and offchain exposure. Over time, investors may be able to choose between holding a tokenized representation of an ETF onchain, holding ETF shares in a brokerage account, or gaining economically similar exposure through perps and other derivatives, with arbitrage linking these markets.

Interplay with Derivatives and Perpetuals

Crypto is unusual in that sophisticated derivatives—perpetual swaps, options, leveraged tokens—emerged at scale before regulated ETFs. Now that ETFs exist, the interplay between these products and existing derivatives is shaping market structure. A trader might, for example, buy a spot bitcoin ETF in a brokerage account, hedge directional risk by shorting bitcoin perps on a crypto exchange, and sell call options on ETF-linked indices like CBTX to generate income. Institutional desks might use futures-based ETFs to manage exposure when direct access to spot or perps is constrained by compliance considerations, while crypto-native funds might arbitrage price differences between ETF shares, spot coins, and perps.

The growth of ETF-linked options and index products adds another layer. Options on indices like CBTX that reference spot bitcoin ETF performance allow investors to trade volatility around the ETF ecosystem itself, potentially leading to feedback loops where ETF flows influence options markets, which in turn influence hedging flows in spot and futures markets. This complex web underscores the degree to which bitcoin and other crypto assets are being woven into the broader tapestry of global derivatives and risk management.

Risks, Critiques, and Systemic Considerations

Crypto ETFs bring with them many of the risks associated with both crypto assets and traditional financial products, as well as new risks arising from their interaction.

Market, Liquidity, and Tracking Risks

The most obvious risk for investors in crypto ETFs is market risk: bitcoin, Ethereum, and other underlying assets are highly volatile, and ETF share prices will reflect that volatility. The SEC and CFTC repeatedly stress that investors in bitcoin-related ETFs must be prepared for significant price swings and the possibility of losing their entire investment, even when investing in regulated products. ETF wrappers do not eliminate underlying asset risk; they simply provide a different access channel.

Liquidity risk arises both at the ETF level and in the underlying markets. While many crypto ETFs trade with tight spreads and deep order books during normal conditions, liquidity can thin out during sharp sell-offs, leading to wider bid-ask spreads, larger premiums or discounts to NAV, and potentially higher trading costs. In extreme cases, creation and redemption may be temporarily constrained if APs are unwilling to transact due to uncertainty or operational bottlenecks. Underlying spot or futures markets may also experience reduced liquidity, exchange outages, or sudden spikes in transaction fees, complicating the ability of ETF sponsors to adjust holdings.

Tracking risk, as discussed earlier, is another concern. For futures-based ETFs, tracking can diverge significantly from spot due to roll costs, margin requirements, and cash management. For spot ETPs, tracking errors may stem from fees, trading frictions, and the mechanics of primary-market flows. Investors who expect a one-to-one correspondence between ETF returns and spot asset returns may be surprised by these deviations, particularly over longer horizons.

Structural and Regulatory Risks

Crypto ETFs also face structural risks tied to their design and legal status. Custodial risk is paramount for spot ETPs: the safety of the underlying bitcoin or ether depends on the custodians’ security practices and governance. A high-profile custody failure could have systemic implications, undermining confidence in ETF structures and potentially triggering regulatory backlash. Futures-based ETFs face counterparty and clearinghouse risks, albeit within highly regulated environments designed to mitigate such risks.

Regulatory risk is pervasive. The SEC’s evolving views on which crypto assets are securities, how staking should be treated, and what constitutes sufficient market surveillance create uncertainty for the expansion of crypto ETFs beyond bitcoin and Ethereum. Even for existing products, regulatory changes—such as new disclosure requirements, leverage limits, or restrictions on certain activities—could alter economics or limit growth. For Ethereum ETPs, the prohibition on staking reflects a cautious approach that could shift as the Commission’s views on staking evolve, but for now it deprives investors of native yield. Any reclassification of major assets or major enforcement action affecting key exchanges or custodians could reverberate through ETF structures.

There is also the risk that regulators outside the United States take divergent approaches, creating regulatory arbitrage or fragmented markets. For example, some non-U.S. ETPs engage in staking or hold a broader array of tokens, potentially offering features that U.S. ETFs cannot, but also exposing investors to different regulatory regimes and risks. Global investors must navigate these differences when allocating across jurisdictions.

Systemic Concentration and the Financialization of Bitcoin

As bitcoin ETFs and ETPs accumulate assets, a growing portion of the circulating bitcoin supply is effectively held in custodial structures controlled by large asset managers and custodians. This concentration raises questions about governance, systemic risk, and the nature of bitcoin’s decentralization. If a handful of institutions hold or control the voting rights (where applicable) or operational decisions over a large share of ETF-held bitcoin, then those institutions become potential chokepoints, even if the underlying protocol remains decentralized.

Critics argue that this concentration is antithetical to bitcoin’s original design as peer-to-peer electronic cash and self-sovereign money. A Trezor executive, for instance, has warned that treating bitcoin as just another ETF-able asset undermines the incentive for individuals to learn self-custody and exposes the ecosystem to the same kinds of systemic risks and political pressures that afflict traditional finance. The proliferation of income products like BITA, which turn bitcoin into a yield-generating instrument via options overlays, further integrates bitcoin into the logic of portfolio income strategies, potentially weakening its distinct identity as “hard money” held outside the financial system.

Regulators, for their part, focus on investor protection and systemic stability within the financial system’s boundaries. The SEC’s spot bitcoin ETP approvals emphasize that the Commission does not endorse bitcoin but is responding to legal developments and investor demand by bringing existing crypto exposure out of the shadows of unregulated markets into the purview of regulated exchanges and disclosures. From this vantage point, ETFs are a way to mitigate some harms associated with offshore or unregulated trading venues. The tension between this regulatory logic and crypto’s ideological aspirations is unlikely to disappear.

Data, Transparency, and Surveillance

One underappreciated aspect of ETF adoption in crypto is the increase in data transparency. ETF holdings, flows, and, in some cases, detailed baskets are published regularly by sponsors and exchanges. Market data providers track creations and redemptions, bid-ask spreads, and trading volumes, enabling analysts to infer institutional positioning and sentiment. Some onchain analytics platforms now monitor wallets associated with major ETFs and custodians, integrating data about ETF holdings into broader dashboards. As noted in recent coverage, for example, BITA’s holdings have been tracked on platforms like Arkham, allowing market participants to observe changes in real time as the fund writes options and adjusts exposure.

At the same time, regulators and law enforcement gain additional windows into crypto markets through ETF-related reporting and surveillance. Surveillance-sharing agreements between exchanges listing crypto ETPs and large spot or futures trading venues allow the sharing of data on suspicious trading patterns, wash trading, or potential manipulation. This increased transparency can enhance market integrity but also raises privacy and sovereignty concerns for those who view bitcoin as a tool for financial autonomy. Market makers like Wintermute, meanwhile, treat ETF and stablecoin flows as important signals for market-making and risk decisions, showing how transparency can feed back into market dynamics.

The SEC has repeatedly delayed, rejected, and conditioned crypto ETF approvals, and enforcement posture can shift with each administration, leaving product issuers in perpetual legal uncertainty.

BlackRock's IBIT alone accumulated nearly 4% of the entire Bitcoin supply, concentrating custodial and voting influence in a single TradFi entity with no on-chain accountability.

Spot Bitcoin ETFs recorded a $1.72 billion weekly outflow — their second-largest since launch — demonstrating that institutional redemptions can amplify crypto price dislocations rather than dampen them.

ETF inflow and outflow cycles have introduced a new basis-trade dynamic where hedge funds arbitrage spot ETF premiums; when those trades unwind simultaneously they drive correlated sell pressure across BTC.

- Counterparty / CustodyMedium

Most U.S. spot Bitcoin ETFs custody assets through Coinbase, creating a single point of operational failure; a Coinbase outage or regulatory action would simultaneously affect the majority of ETF product AUM.

Spot BTC and ETH ETFs hold actual native assets via regulated custodians rather than on-chain contracts, so smart-contract exploit risk is structurally absent from the core product — though futures-based and index ETFs carry basis and tracking risk.

ETFs, Tokenization, and the Future of Onchain Finance

Crypto ETFs are not only endpoints of financialization but also reference points for new onchain structures that seek to replicate or surpass the ETF model.

Lessons from the ETF Boom

The ETF industry’s growth from niche innovation to multi-trillion-dollar juggernaut offers a roadmap for tokenization. ETFs succeeded because they combined low-cost index exposure, tax efficiency, intraday liquidity, and transparency into a single, standardized wrapper. They allowed investors to access broad or targeted exposures without buying individual securities or dealing with complex fund subscription processes. As a result, ETFs became the default way for many investors to implement asset allocation decisions, displacing mutual funds in key segments and reshaping capital markets.

Executives at tokenization-focused firms like Ondo Finance explicitly draw parallels between this history and their vision for onchain asset packaging. In an interview, an Ondo executive argued that tokenization mirrors the roughly 20 trillion dollar ETF boom, as blockchain and AI converge to enable efficient creation and management of tokenized portfolios. Just as ETFs unlocked scale for index investing, tokenized funds aim to unlock scale for onchain representations of treasuries, credit, and multi-asset portfolios. AI tools can help design, manage, and personalize these portfolios, while smart contracts handle bookkeeping and enforcement.

From this perspective, crypto ETFs in traditional markets are both competitors and complements to tokenized funds. They compete for assets and investor attention, but they also normalize the idea of accessing crypto exposures through diversified, rule-based vehicles rather than direct trading. In the long run, some ETF strategies may themselves migrate onchain, with tokenized shares backed by onchain or offchain assets, blurring distinctions.

Tokenized ETFs and Onchain Wrappers

One potential future path involves tokenized representations of ETF shares, where an entity holds ETF shares in custody and issues tokens on a blockchain that represent fractional claims on those shares. These tokens could then trade on decentralized exchanges, be used as collateral in DeFi protocols, or be integrated into onchain structured products, extending the reach of ETF strategies into the crypto-native realm. Conversely, tokenized funds might seek listings as ETFs or ETPs on traditional exchanges, effectively reversing the direction of migration: starting onchain and then entering securities markets.