In‑depth explainer on rug pulls in crypto and DeFi, covering definitions, mechanics, major case studies, detection tools, legal responses, and practical steps investors can take to avoid scams while still participating in Web3.

+3 sources across the wider coverage universe

Authorities freeze $41M in crypto tied to $150M BG Wealth Sharing Ponzi, as Binance, Tether, and OKX help track and halt laundering linked to alleged rug pull2026-05

Authorities freeze $41M in crypto tied to $150M BG Wealth Sharing Ponzi, as Binance, Tether, and OKX help track and halt laundering linked to alleged rug pull2026-05 South Korea indicts CATFI crew in first DEX rug pull arrest case after $260K profit, $600K losses2026-05

South Korea indicts CATFI crew in first DEX rug pull arrest case after $260K profit, $600K losses2026-05 White House blasts Coinbase’s last‑minute exit from Trump’s CLARITY Act talks as a “rug pull” on both the administration and the wider crypto industry, after the exchange abruptly withdrew support over DeFi, tokenized‑equity, privacy and stablecoin‑yield provisions that also forced a Senate Banking markup delay.2026-01

White House blasts Coinbase’s last‑minute exit from Trump’s CLARITY Act talks as a “rug pull” on both the administration and the wider crypto industry, after the exchange abruptly withdrew support over DeFi, tokenized‑equity, privacy and stablecoin‑yield provisions that also forced a Senate Banking markup delay.2026-01 Meme Coin scam dupes over 42,000 victims, accumulating $32 Million in fraud. Experts baffled as even top "rug pull detectors" were fooled by this unprecedented method.2024-01

Meme Coin scam dupes over 42,000 victims, accumulating $32 Million in fraud. Experts baffled as even top "rug pull detectors" were fooled by this unprecedented method.2024-01- BaseBros Fi, a DeFi protocol on the Base blockchain, vanishes after orchestrating a rug pull through an unaudited contract, stealing users' funds.2024-09

- Arkham customers rally behind crypto bounty initiative to expose culprits behind FTX, Wintermute hacks and meme-coin rug pull2023-07

Rug Pulls in Crypto: How They Work, Why They Keep Happening, and What You Can Do

A rug pull is a crypto exit scam in which the people controlling a project suddenly withdraw liquidity or misappropriate funds, abandoning tokens or NFTs and leaving investors with assets that are nearly worthless. In DeFi and Web3 more broadly, the term has also become shorthand for any abrupt, bad‑faith reversal of commitments, from meme coin collapses to political deals, because it captures the feeling that the metaphorical rug has been yanked out from under participants.

Rug pulls sit at the intersection of code, culture, and regulation in the digital asset ecosystem. On one level, they are enabled by the same permissionless infrastructure that powers decentralized finance: anyone can deploy a token, spin up a liquidity pool, and solicit capital from strangers around the world without passing a listing committee or brokerage due‑diligence check. On another level, they are social phenomena driven by memes, celebrity endorsements, and the fear of missing out on the next ten‑thousand‑percent pump, which create the perfect conditions for fraudsters to pose as visionary founders or insider “alphas.” As enforcement actions in the United States, South Korea, and Europe begin to catch up with these schemes, on‑chain sleuths, auditors, and machine‑learning researchers are racing to spot patterns of fraud earlier and build defenses directly into wallets and DeFi protocols. This explainer unpacks what a rug pull is, how it differs from other crypto scams, the mechanics behind some of the highest‑profile cases, and how both individual users and institutions can better protect themselves without abandoning DeFi’s core promise.

Defining Rug Pulls in Crypto and Beyond

Narrow definition: the classic DeFi rug

In its narrow, technical sense in crypto markets, a rug pull describes a scenario where developers or insiders behind a token or protocol abruptly withdraw liquidity or otherwise extract value, causing the price of associated assets to collapse while they keep the proceeds. On decentralized exchanges, this often means the team adds an initial pool of liquidity for a new token paired with a reputable asset like ETH or USDC, markets the token aggressively to attract buyers, then removes most or all of that liquidity once the pool becomes large, leaving traders with tokens they can no longer meaningfully sell. Other classic variants include protocols where insiders drain smart contracts of deposited funds, or token contracts that allow the creator to mint an arbitrary number of new tokens at will, diluting existing holders and offloading the surplus onto the market. In each case, the common pattern is that the people who marketed and controlled the project secretly retained unilateral control over the critical levers of value and used that control to exit at the expense of their community.

Blockchain security firms, exchanges, and analytics providers broadly converge on this definition. CoinMarketCap, for example, describes a rug pull as a “malicious maneuver in the cryptocurrency industry where crypto developers abandon a project and run away with investors’ funds.” Solana‑focused wallet Solflare similarly defines it as a scheme where the people behind a token or project “suddenly drain the liquidity (usually from decentralized exchanges) or disappear with investors’ funds — leaving holders with worthless tokens.” CertiK, a major smart contract auditor, emphasizes the element of intent, calling rug pulls an attack pattern where a malicious team lures users through hype and marketing, then drains a project once enough capital has been attracted. That focus on intent matters, because it distinguishes a rug pull from failed experiments or market crashes where teams may be incompetent or unlucky but not necessarily fraudulent.

Academic work on DeFi fraud has adopted similar language while attempting to formalize how these schemes unfold. The RPHunter framework, for instance, defines rug pulls as “a pernicious form of scam prevalent within the DeFi ecosystem” in which scammers launch seemingly promising tokens, attract capital, and then withdraw funds and abandon the project, leaving investors with worthless assets. In their model, rug pulls are distinguished from external hacks or exploits by the fact that the perpetrators are typically the token issuers themselves or those with privileged control over smart contracts. This distinction becomes important both for legal classification and for designing detection systems.

Broader usage: from Libra to legislation

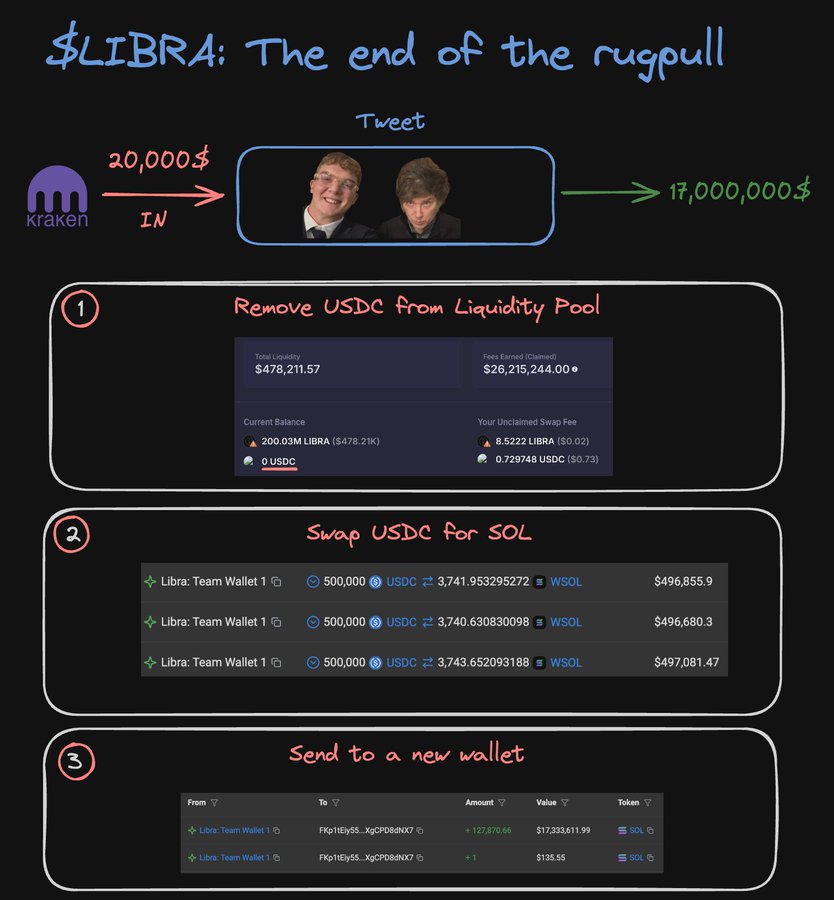

Outside that narrow technical scope, “rug pull” has become a cultural shorthand for any abrupt, perceived betrayal in crypto and even in mainstream politics. When Argentina’s President Javier Milei amplified the $LIBRA meme coin online, its price soared before collapsing amid allegations that insiders had orchestrated a massive exit at the top, leading commentators and some investors to describe the episode as a rug pull on both the market and the president’s followers. According to post‑mortems, the token’s market value spiked after Milei’s promotion and then experienced a severe price drop, with estimates of up to hundreds of millions of dollars in value wiped out, fueling accusations that early holders or promoters had engineered a coordinated dump. In such cases, not every participant may be legally culpable, but the community uses the rug‑pull label to signal that the core dynamic felt like a bait‑and‑switch.

The metaphor has also migrated into regulatory and political discourse. Reporting on U.S. policy debates described tensions around the proposed CLARITY Act, a legislative package meant to address DeFi, tokenized equities, privacy tools, and stablecoin yields. When Coinbase, the company behind the COIN ticker on Nasdaq, abruptly withdrew support for the bill after extensive negotiations, sources close to the White House were described as viewing the move as a “rug pull” on both the administration and the wider crypto industry because it undermined months of bipartisan process. Here, of course, no one drained a liquidity pool or ran off with tokens. But the language persisted because the pattern—apparent commitment followed by abrupt withdrawal, leaving others exposed—mirrored what traders experience when a token team disappears.

This broadening of the term’s meaning has both advantages and drawbacks. On the one hand, it highlights that rug pulls are not just technical exploits but a form of broken trust that resonates well beyond crypto charts. On the other hand, it can blur analytic clarity. If everything from a collapsed meme coin to a failed bill is branded a rug pull, it becomes harder to distinguish between criminal fraud, reckless behavior, and ordinary political negotiation. For investors and policymakers, keeping both the narrow and broad senses in mind is essential.

Taxonomy: hard vs soft, DeFi vs NFTs

Within the crypto‑native context, practitioners increasingly distinguish between different subtypes of rug pull. CertiK popularizes a binary between hard and soft rug pulls. A hard rug pull is the stereotypical, noisy exit: the team or a privileged wallet drains liquidity or contract funds in a single, observable on‑chain transaction or short series of transactions, after which the token’s price collapses and the project’s social channels often go dark. Because of their abruptness, hard rugs tend to trigger immediate community outrage and post‑mortems by on‑chain analysts.

Soft rug pulls, by contrast, are quieter and more ambiguous. In a soft rug, founders might gradually dump their holdings into upward price momentum, fail to deliver on promised features, or slowly siphon treasury funds into affiliated entities, while continuing to communicate with the community just enough to keep hope alive. From the outside, it can be difficult to distinguish a soft rug from a project that is simply poorly managed or hit by adverse market conditions. That ambiguity can shield perpetrators from legal consequences and complicate coverage by news outlets that try to avoid libel while still warning readers.

Another critical dimension of the taxonomy is asset type. Early rug pulls clustered around ERC‑20‑style tokens and DeFi liquidity pools, but the pattern quickly migrated to non‑fungible tokens (NFTs). In the Frosties case, two young founders allegedly sold about 8,888 cartoon ice cream NFTs, raised roughly 1.1 million dollars, then shut down the project’s websites and social channels and transferred funds to personal wallets, prompting the FBI’s first NFT rug pull bust. Similarly, in the Evolved Apes case, U.S. prosecutors charged three U.K. nationals with wire fraud and money laundering based on allegations that they promised a fighting game tied to their NFT collection, raised funds, then abandoned the project and laundered proceeds through multiple crypto transactions. These NFT rug pulls demonstrate that the underlying scam pattern is portable across different token standards.

Finally, rug pulls can be categorized by the infrastructure layer they target. Some occur on decentralized exchanges (DEXs) like Uniswap or Solana‑based platforms, where anyone can list a token without permission. Others are tied to centralized platforms or CeFi‑like schemes that resemble traditional Ponzi operations but use crypto rails for deposits, as in the BG Wealth Sharing case where the FBI seized the website and warned participants they were unlikely to recover funds. Still others blur the line between protocol and investment product, such as “eco‑friendly” blockchains or staking platforms that market hardware or carbon credits alongside tokens, as Rowan Energy did before its supply manipulation and hidden mint function were exposed. For users, appreciating this diversity is crucial, because protections that work in one category do not always translate cleanly to another.

Authorities freeze $41M in crypto tied to $150M BG Wealth Sharing Ponzi, as Binance, Tether, and OKX help track and halt laundering linked to alleged rug pull

Readers click rug pulls not for the mechanics but for the power map — every top headline names a recognizable actor (a president, a celebrity, a VC firm) with insider access who faced little immediate consequence, revealing that identity and immunity of the rugging party drives engagement far more than the size of the theft.↗

How Rug Pulls Actually Work

The lifecycle of a DeFi rug pull

While every rug pull is unique in its branding and narrative, many follow a recognizable lifecycle that can be broken into several phases. The RPHunter study formalizes this into a sequence beginning with tactic injection, followed by token launch, market building, and finally liquidity extraction. In the tactic injection phase, scammers embed fraud‑enabling logic or structures into the token contract or protocol architecture. That might mean coding in a mint function that allows them to create additional tokens later, setting privileged roles that can change fees or trading parameters, or designing liquidity pool rights so that they alone control its removal. Because these features can be obfuscated within complex smart contracts, many retail traders never realize the latent risks.

The token launch phase is where the public story begins. Scammers deploy the token, often pairing it with a reputable asset like ETH, SOL, or USDC in a liquidity pool on a DEX, and begin marketing it as a novel DeFi opportunity or meme coin with explosive upside. They may cultivate narratives about community ownership, green energy, or alignment with popular political or cultural figures, sometimes even seeding rumors that a celebrity or influencer is secretly involved. To boost credibility, they may point to superficial audits, paid promotional articles, or fake partnerships, while the actual smart contract code either remains unaudited or is too complex for casual review.

Once the token is live, the focus shifts to market building. This is the period when memes, aggressive social media campaigns, and coordinated “shilling” on platforms like X and Telegram are used to attract liquidity and secondary buyers. Insiders might engage in wash trading to create the appearance of organic volume, use bots to inflate follower counts, or orchestrate circular trading across multiple wallets to disguise how much of the supply they actually control. In the CATFI case on Solana, for example, prosecutors allege that the team behind the meme coin created the token on Pump.Fun, listed it on a DEX, then used circular trading, fake online personas, and misleading announcements to pump its price roughly 1,001‑fold within 26 hours. Thousands of investors bought in, believing they were riding a viral meme, while the issuing side retained effective control of the token’s float.

The final phase is liquidity extraction: the actual rug pull. Once enough capital has accumulated and insiders judge that additional upside is limited compared to the risk of waiting, they exploit their privileged position to drain value. On a DEX, this might mean removing the bulk of liquidity from the pool, swapping tokens for a blue‑chip asset, and sending proceeds to fresh wallets that then route funds through privacy tools like Tornado Cash. In the CATFI case, South Korean prosecutors allege that after the pump, the group pulled liquidity, causing steep losses for 256 investors who were left holding tokens that had lost nearly all value, while the organizers pocketed around 400 million won—roughly 260,000 dollars—in illegal profits. In other schemes, such as some staking or yield optimization protocols, insiders may trigger a function in an unaudited contract that transfers user deposits to a wallet they control, as seen in the BaseBros Fi incident on the Base blockchain, where an unaudited vault contract allegedly contained a backdoor allowing the team to withdraw funds from strategy contracts. Once the rug is pulled, project websites and social channels often vanish, and support disappears.

Technical mechanics: liquidity pools, hooks, and backdoors

At the heart of many DeFi rug pulls are liquidity pools, the automated market‑making structures that allow tokens to be traded without centralized order books. When a new token is launched, its creators typically deposit a certain amount of that token plus a more established asset into a pool; the ratio between the two sets the initial price. As traders buy the new token, the pool’s composition shifts, and the price moves according to a bonding curve. The critical detail is that whoever controls the pool’s liquidity provider (LP) tokens can withdraw the underlying assets. In a legitimate project, a substantial portion of LP tokens may be burned or locked in a time‑locked contract to reassure investors that liquidity cannot be arbitrarily removed. In a rug pull, LP tokens remain under the team’s sole control, allowing them to remove most of the pool at once.

Innovations at the DEX layer can unintentionally expand the attack surface. Uniswap v4, for example, introduced “hooks”—custom smart contracts that can plug into the lifecycle of a pool and modify its behavior. One such hook, dubbed Clanker, has been used to permissionlessly initialize hundreds of thousands of pools, with Uniswap citing over 517,000 pools created by the Clanker hook as evidence that on‑chain rails enable broad experimentation. While the hook itself is not necessarily malicious, the ease with which pools can be deployed at scale by third‑party contracts has raised concerns among security researchers that scammers could spin up many near‑identical pools, use one for a rug pull, then abandon it and move on, complicating reputation‑based filters. The very composability that makes DeFi vibrant also gives fraudsters more levers.

Smart contract backdoors can take several forms beyond simple liquidity withdrawal. One pattern involves upgradable proxy contracts. Instead of deploying a fixed logic contract, developers deploy a proxy that can be pointed to a new implementation at any time, often controlled by a single admin key or a small multisig. While upgradability can be useful for patching bugs or adding features, it also means that developers can swap in malicious logic after an initial audit or during a quiet period, enabling hidden fees, balance freezes, or direct drains. Another pattern is the hidden mint: a function that allows trusted addresses to mint new tokens beyond the advertised maximum supply. Rowan Energy’s so‑called eco‑friendly blockchain allegedly claimed a supply of 545 million tokens while secretly holding 945 million and retaining a mint function that enabled the creation of hundreds of millions of “ghost” tokens. Over time, that surplus allowed insiders to dump into markets that believed supply was capped, undermining the price and turning what looked like a green revolution into what Rekt News dubbed an “eco‑friendly rug pull.”

BaseBros Fi illustrates the backdoor pattern in a DeFi yield context. The project marketed itself as a yield optimization protocol on Coinbase’s Base network, attracting deposits into strategy contracts that were supposed to farm yields across the ecosystem. According to blockchain security firm Chain Audits, while some of BaseBros’ contracts had been audited, the crucial vault contract that held user funds was unaudited and unverified and contained a backdoor that allowed the owners to withdraw deposited funds. When the alleged rug occurred, BaseBros’ website and social media channels disappeared, and about 130,000 dollars in crypto was siphoned off and laundered through Tornado Cash, leaving users scrambling and illustrating how even partially audited projects can hide critical risks in unsupervised components.

ZKasino, a crypto betting platform, presents yet another variation. Users bridged ETH into the platform with the expectation they could later withdraw equivalent value, only to find withdrawals halted and official communication channels restricted, prompting widespread allegations of a 30‑million‑dollar rug pull. Dutch police later arrested a 21‑year‑old suspected of orchestrating the scheme, and on‑chain sleuths noted that a wallet tied to ZKasino reportedly placed a highly leveraged ETH trade that was liquidated, suggesting reckless speculation with user funds. ZKasino’s subsequent attempt to introduce a complex “two‑step bridge back process” for partial refunds only underscored how platform‑level rug pulls can blend elements of mismanagement, misrepresentation, and outright fraud.

Meme coins, celebrity hype, and social engineering

If DeFi provides the infrastructure for rug pulls, meme culture supplies much of their fuel. Meme coins, by definition, rely less on fundamentals than on narratives, in‑jokes, and viral moments, which creates fertile ground for scammers to spin up tokens that appear culturally relevant and temporarily irresistible. During periods of meme coin mania, scammers can exploit this dynamic to execute more sophisticated scams that deceive tens of thousands of victims. One widely cited episode involved a meme coin scheme that reportedly duped over 42,000 victims and accumulated around 32 million dollars in fraud, with even top “rug pull detector” tools initially failing to flag the project because its on‑chain patterns differed from past scams. That incident highlighted how novel combinations of tokenomics, social tactics, and transaction patterns can outpace automated defenses.

Political associations magnify the effect. The $LIBRA episode tied to Argentina’s President Milei is a case in point. After the president promoted a token bearing the Libra name on social media, its price spiked dramatically, only to crash amid allegations that insiders had positioned themselves to sell into the pump, wiping out latecomers. Reports described the crash as a rug pull that generated hundreds of millions in paper losses, though the precise distribution of gains and losses remains contested. Regardless of the legal outcome, the perception that a meme coin linked to a head of state could be weaponized for such a rapid transfer of wealth shook confidence and underscored how memes, politics, and speculation can fuse into a potent but dangerous mix.

The CATFI case in South Korea adds another dimension: the use of fake influencer personas to create the illusion of independent endorsement. Prosecutors allege that the main suspect, identified only by the surname Park, operated under the persona “Eth Father,” posing as an unrelated third‑party influencer while in fact controlling CATFI’s social media accounts and promotion. By recommending CATFI as if he were a neutral observer, managing its online presence, inflating follower counts, and posting false positive announcements, Park allegedly manufactured organic‑seeming hype that masked the team’s central role. When the rug pull occurred and CATFI’s price collapsed after its 1,001‑fold surge, many investors had believed they were following a trusted meme account rather than buying directly into a founder‑controlled scheme.

Celebrity rumors and insider culture also play a role. Even when stars like Cristiano Ronaldo or Kanye West are not directly involved, the mere suggestion that a token is associated with a famous figure can bring in speculative flows. Reports of a CR7‑branded meme coin or a $YZY token allegedly linked to Kanye have drawn attention not only for their rapid pumps but also for evidence of insider wallets sniping early allocations and extracting seven‑figure profits within hours, leaving the public to absorb subsequent dumps. While these specific cases fall outside the documented sources here, they fit a pattern established by Libra and CATFI: meme‑driven coins leveraging celebrity or cultural capital are particularly vulnerable to rug‑pull dynamics because they short‑circuit normal due diligence processes. Traders focus on memes instead of mechanics.

NFTs, gaming, and the metaverse

Rug pulls in the NFT space underscore that the scam is not limited to fungible token trading. In the Frosties case, two twenty‑something U.S. residents allegedly launched an NFT collection of cartoon ice cream characters, promising holders community benefits, giveaways, and a metaverse game. After selling out and collecting roughly 1.1 million dollars in ETH, they allegedly abandoned the project, shut down the Discord and website, and transferred funds to wallets they controlled, prompting federal prosecutors to charge them with conspiracy to commit wire fraud and money laundering. Notably, the defendants were reportedly already planning a follow‑up NFT project, “Embers,” which investigators interpreted as a sign that they viewed rug pulls as a replicable business model rather than a one‑off exploit.

The Evolved Apes case extends this logic into a cross‑border setting. According to the U.S. Department of Justice, three U.K. nationals marketed the Evolved Apes NFT collection with promises of a fighting game and long‑term development, then misappropriated funds instead of delivering. Prosecutors characterize the scheme as a classic rug pull: developers advertised a digital project, collected funds, then abandoned it while keeping the money, laundering the misappropriated funds through multiple crypto transactions to obscure their origin. The charges—conspiracy to commit wire fraud and conspiracy to commit money laundering, each carrying a theoretical maximum of 20 years in prison—illustrate how authorities are increasingly willing to treat NFT rug pulls as serious financial crimes.

These NFT scams demonstrate that the “rug” in rug pull need not be a liquidity pool. In an NFT context, the rug can be the promised roadmap, game, or utility that gives the tokens value. When that roadmap is abruptly abandoned by insiders who have already cashed out, the effect on holders is analogous to a DeFi rug: they are left standing on empty ground where value once seemed to be growing. The fact that NFTs often attract different demographics—including artists, gamers, and sports fans—means rug pulls in this segment can also damage crypto’s reputation beyond the pure trading community.

Rug Pulls versus Other Crypto Scams

Pump‑and‑dump schemes and Ponzi structures

Rug pulls often get conflated with pump‑and‑dump schemes, but the mechanics and emphasis differ. Sumsub, a compliance and risk firm, helpfully contrasts the two: in simple terms, a pump‑and‑dump uses hype to get you to buy at the wrong time, whereas a rug pull exploits investor trust by attracting funds to a project that insiders later abandon or drain. In a classic pump‑and‑dump, operators accumulate a position in an existing asset, then artificially pump its price through misleading statements, coordinated buys, or manipulative trading before dumping their holdings on unsuspecting buyers, often without any privileged control over the asset’s underlying infrastructure. The scam lies in market manipulation and deceptive promotion, not necessarily in owning the contract or platform.

By contrast, a rug pull depends on control. Insiders control the token supply, the liquidity pool, the smart contract, or the platform account that holds user deposits, and they use that control to extract value directly. Many meme coin rug pulls, such as CATFI and other DEX‑listed tokens launched via platforms like Pump.Fun, blend pump‑and‑dump dynamics with rug mechanics: insiders both promote the coin to pump its price and retain privileged access that allows them to pull liquidity or mint tokens. But recognizing the distinct control element helps analysts distinguish between manipulative but technically external trading and scams that are built into a project’s architecture.

Ponzi and pyramid schemes add another layer. BG Wealth Sharing, for example, functioned more like a Ponzi than a pure DeFi rug. Participants were promised outsized returns and revenue sharing, likely funded by the deposits of newer investors rather than genuine profits. When U.S. authorities seized the website, victims reported being told they had to pay a 12 percent “tax” to withdraw their money, a classic hallmark of recovery‑room fraud, where scammers demand additional payments from victims under the pretense of unlocking funds. A commentator in a YouTube explainer warned that those funds were effectively gone, urging victims not to send more money and to report the scheme only through official government channels rather than dubious “lawyers” advertising on social media. While some observers loosely called BG Wealth a rug pull because the operators disappeared with the money, structurally it is closer to a Ponzi with an exit scam component.

Understanding these differences matters for legal classification and regulatory responses. Pump‑and‑dump schemes raise questions about market manipulation and disclosure obligations. Ponzi structures implicate securities and banking laws. Rug pulls, especially those involving hidden contract functions or misrepresented supply caps, squarely raise issues of fraud and misappropriation by insiders who had privileged control over investor funds or token infrastructure. That said, in the eyes of many retail participants, the precise legal category matters less than the outcome: their crypto is gone, and someone they trusted appears to have engineered its disappearance.

Hard versus soft rugs and the grey zone of failure

The hard‑versus‑soft rug distinction is particularly useful when distinguishing fraud from failure. In a hard rug, as CertiK notes, the team executes an obvious, usually on‑chain, maneuver that drains funds or permanently cripples the token’s value, often accompanied by a rapid shutdown of communication channels. The BaseBros Fi vault drain and subsequent disappearance of its website and social accounts fits this pattern: a single unaudited contract backdoor was used to siphon off deposits, after which the project effectively vanished. Many meme coin rugs, where liquidity is pulled from a DEX pool in a single transaction once volume peaks, are similarly hard rugs.

Soft rugs, however, unfold more gradually and can be harder to classify. A team might repeatedly delay promised features, spend treasury funds on lavish marketing or personal expenses, or sell their own large token allocations into every price rally while publicly insisting they are “long‑term.” Over time, the project’s token price may grind down, liquidity may thin, and the community may shrink, but there is no single transaction that clearly marks a rug pull. Critics may call it a soft rug; defenders may say it was simply a failed startup in a volatile industry. Rowan Energy’s slow‑burn supply manipulation, conducted over years under the guise of a green‑crypto revolution, sits somewhere between these categories. The existence of a hidden mint function and undisclosed extra tokens suggests clear intent to deceive, but the fraud played out over an extended period rather than in a single exit transaction.

The grey zone becomes even murkier with venture capital and institutional actors. In some cases, funds that receive large allocations of a project’s token as early investors sell aggressively as soon as lockups expire, causing sharp price drops that feel like rug pulls to retail holders who bought near the top. The Nima Capital episode, in which a venture fund allegedly shut down its website and dumped nine million SNY tokens, sparked accusations of a “VC rug pull” even though the actions might technically have complied with existing agreements. Without evidence of misrepresentation or breach of contract, such exits may be more ethically dubious than legally fraudulent. Yet to the broader crypto public, they blur into the same pattern: insiders exit first, outsiders eat the losses.

Hacks, exploits, and “inside jobs”

Another important distinction is between rug pulls and external hacks. When a DeFi protocol loses funds due to a smart contract vulnerability exploited by an outside attacker, the event is often called a “hack” rather than a rug pull. However, in practice, the line can be blurry. In the case of Hypervault Finance, a yield platform that lost around 3.6 million dollars in an abnormal withdrawal, the project’s website and socials disappeared shortly after, leading many to suspect an inside job rather than a purely external exploit. While the available sources here focus more on analogous cases like BaseBros and ZKasino, the pattern of simultaneous fund loss and team disappearance is commonly interpreted as a rug pull even when the initial explanation is “we were hacked.”

This ambiguity creates challenges for forensics and coverage. In a genuine external exploit, the team may have been negligent in security but did not intentionally steal funds; in an inside job, insiders may stage the exploit themselves to create plausible deniability. RPHunter’s focus on combining code‑level features and transaction behavior reflects an attempt to algorithmically distinguish between these possibilities by analyzing whether fraud‑enabling features were embedded from the outset and how funds moved post‑incident. Nonetheless, for users assessing risk, it is prudent to treat any protocol with opaque governance, unaudited contracts, or weak operational security as a candidate for both hacks and rugs, since the end result—loss of funds—can be similar.

- 01Celebrity and political insider exits↗

LIBRA/Milei and CR7 headlines dominated because readers were drawn to the outrage of politically-connected insiders profiting while retail was wiped out — a named, powerful face attached to the theft.

- 02Detection tools beaten at scale

The 42,000-victim meme coin story spiked because even purpose-built rug-pull detectors failed, exposing a systemic gap in the infrastructure retail investors rely on for protection.

- 03Accountability hunts and legal firsts↗

The Arkham bounty, Evolved Apes DOJ charges, and South Korea's first DEX arrest all drew readers hungry for evidence that perpetrators can actually be identified, caught, and punished.

- 04VC and institutional fund dumps

Nima Capital dumping 9M SNY tokens and Hypervault's vanishing act showed readers that rug pulls are not confined to anonymous retail devs — credentialed, VC-backed actors exit the same way.

- 05Long-con legitimacy disguise↗

Rowan Energy's five-year green crypto fraud, using hidden mint functions beneath a carbon-neutral narrative, showed readers how thoroughly a rug can masquerade as a credible ESG project for years.

- 06DeFi protocol disappearances↗

BaseBros Fi and ZKasino illustrated the classic unaudited-contract exit playbook: protocol launches, attracts meaningful TVL, then team and funds vanish simultaneously.

The Scale and Impact of Rug Pulls

Data, detection, and the growth of the problem

While precise numbers vary, there is broad consensus that rug pulls account for a significant share of crypto‑related fraud losses. Chainalysis has estimated that as much as 280 million dollars was stolen from investors in rug pulls in 2021 alone, a figure cited in coverage of the Frosties NFT case as context for why U.S. law enforcement began prioritizing such scams. Statista’s compilation of the largest confirmed rug pulls by estimated value shows individual incidents in the tens of millions of dollars, with most major cases outside of extraordinary outliers clustering in the 22 to 58 million dollar range, underscoring that even “small” rug pulls can wipe out substantial capital. Those figures likely understate the total, as many smaller or cross‑chain schemes go unreported.

Academic and industry research provides additional granularity. The RPHunter study applied a hybrid code‑and‑transaction analysis model to detect rug pulls, first establishing declarative rules and performing flow analysis to extract code risk information, then constructing a semantic risk code graph. Simultaneously, the authors modeled token transaction activities as a token flow behavior graph, capturing patterns indicative of market manipulation and insider dominance. Using graph neural networks to extract features from both graphs and fusing them via an attention mechanism, RPHunter achieved high detection performance and, when applied to Ethereum mainnet data, identified 4,801 rug pull tokens with a precision of about 91 percent. Those numbers suggest that rug pulls are not confined to a handful of headline cases but represent a broad, structural pattern in the DeFi token universe.

A complementary study published in 2025 focused specifically on detecting rug pulls among tokens listed on decentralized exchanges during the rise of meme coins. Analyzing a dataset of 7,633 tokens created between November 2023 and February 2024, the authors considered 31 features spanning liquidity, holder distribution, price dynamics, and developer behavior. They concluded that machine‑learning models could flag likely rug pulls with meaningful accuracy before the actual exit occurred, particularly by focusing on suspiciously concentrated ownership and abnormal liquidity patterns. However, they also cautioned that attackers adapt, sometimes intentionally mimicking the profiles of legitimate tokens to evade detection.

The Instagram‑documented case where scammers orchestrated a meme coin fraud affecting over 42,000 victims and netting about 32 million dollars illustrates this arms race. According to the post, even some of the better known rug‑pull detector tools failed to catch the scheme in time, suggesting that attackers exploited blind spots in existing models or combined features in novel ways. As detection improves, attackers can fine‑tune their code and transaction behaviors to sit just inside whatever thresholds models deem “normal,” underscoring that automated defenses must be complemented by human judgment and better structural incentives.

Economic, reputational, and regulatory fallout

Beyond direct financial losses, rug pulls impose a broader set of costs on the crypto and DeFi ecosystem. Economically, they can trigger cascading liquidations and loss of confidence that extends beyond the immediate project. When a prominent green‑energy blockchain like Rowan Energy is revealed to have secretly maintained a hidden mint function and hundreds of millions of undisclosed tokens, for example, it not only impoverishes its own investors but also sours public sentiment on other “eco‑friendly” crypto initiatives and undermines trust in on‑chain carbon credit schemes. Similarly, when a meme coin tied to a political figure like Milei implodes amid rug‑pull allegations, it can deepen skepticism among policymakers and regulators who already view crypto as a venue for speculative excess and fraud.

Reputationally, repeated high‑profile rug pulls reinforce a narrative that the space is rigged in favor of insiders. This perception is amplified when respected voices in the industry lament a culture where, in their words, there is “literally no fear of repercussions anymore,” pointing to insider teams that openly boast about sniping pre‑launch allocations and rugging tokens like $YZY while treating it as a game. Even when that rhetoric is hyperbolic, the pattern of meme coin after meme coin launching, pumping, and rugging within hours or days creates a sense that the crypto casino primarily exists for insiders to extract value from retail rather than for building sustainable DeFi infrastructure.

The regulatory implications are already visible. In South Korea, rug pulls had traditionally been pursued in the context of centralized exchanges or influencer pump schemes. The CATFI case, which prosecutors describe as the country’s first criminal case targeting a DEX rug pull, marks a shift. Under the recently enacted Virtual Asset User Protection Act, the Seoul Southern District Prosecutors’ Office arrested and indicted multiple individuals linked to CATFI, accusing them of market manipulation, “the use of fraudulent means, plans, or techniques,” and false statements about material facts in connection with digital asset trading. Investigators relied heavily on on‑chain analysis to trace wallet addresses, as well as social media evidence linking the “Eth Father” persona to the main suspect Park and his associates. The case signals that regulators are increasingly comfortable treating DEX‑based rug pulls as prosecutable crimes rather than as regrettable but ungovernable outcomes of decentralized markets.

At the same time, rug pulls contribute to broader shifts in investor behavior. Reporting from South Korea, for example, noted that South Korean investors pulled more than 41 billion dollars’ worth of value out of virtual assets over roughly a year, a decline influenced by Bitcoin price slumps but also by growing concern over fraud and scams in local and global crypto markets. When retail participants repeatedly experience rugs or see friends lose savings in meme coin collapses, they may shift capital back into traditional equities or regulated products, slowing the organic growth of DeFi and Web3 adoption. Rebuilding trust becomes both an ethical imperative and a business necessity for the industry.

Human costs and cross‑border obstacles

The most immediate impact of a rug pull is on the individuals who lose money. For many victims, especially those drawn in by memes, celebrity rumors, or community pressure, the losses are not just numbers on a screen but life savings, tuition funds, or emergency reserves. Psychological research on financial fraud suggests that victims often experience a mix of shame, anger, and withdrawal from social networks, which can exacerbate mental health challenges. In the BG Wealth case, for example, victims were being told that if they just paid a 12 percent “tax,” they could withdraw their funds, a tactic that preys on desperation and denial. A YouTube commentator who had warned clients about the scheme emphasized that the money was gone and that victims should not pay additional fees to purported “lawyers” or recovery services advertising on Facebook, as those often constitute secondary scams targeting the same emotionally vulnerable population.

Cross‑border enforcement adds another layer of difficulty. As Solflare notes in its educational materials, even when rug pulls are traced on‑chain, catching the perpetrators is rare, particularly if they operate across multiple jurisdictions and use privacy tools or mixers. Coordinating investigations among agencies in different countries can be slow, and legal frameworks for digital asset fraud may be incomplete or inconsistent. This is one reason why Solflare advises that, in most cases, there is no practical path to recourse for small investors harmed by rug pulls, and that once a rug has occurred, funds are usually gone for good. High‑profile prosecutions like Frosties, Evolved Apes, CATFI, and ZKasino demonstrate that law enforcement can succeed when there are clear suspects, significant sums, and political will. But they remain the exception rather than the rule.

This enforcement gap fuels a cynical but rational calculus among would‑be scammers: the potential upside of a successful rug pull may outweigh the perceived risk of getting caught. That calculus is reinforced when insiders brag online about sniping and rugging tokens and face no immediate consequences. Over time, such impunity can corrode norms even among otherwise legitimate builders, pushing the boundary of acceptable behavior toward more aggressive tokenomics and looser commitments. Restoring a culture where rug pulls are seen as both morally unacceptable and legally risky is therefore essential for the long‑term health of crypto markets.

South Korea indicts CATFI crew in first DEX rug pull arrest case after $260K profit, $600K losses

South Korea’s Seoul Southern District Prosecutors indicted two alleged CATFI market manipulators in custody, one without detention, and two accused of helping the ringleader flee, making it the country’s first DEX rug pull arrest case. Prosecutors say the group launched the Solana meme coin on pump.fun in early 2025, used fake SNS promotion and wallet-splitting to hide control, then dumped after CATFI ran 1001x in 26 hours. Around 6,000 people bought in, 256 investors lost KRW 900 million, and the crew allegedly turned KRW 10 million in seed capital into KRW 400 million in criminal profit.

Case Studies: Memes, “Green” Energy, and Betting Platforms

Meme coin rugs: CATFI and LIBRA

The CATFI meme coin rug pull in South Korea offers a textbook example of how memes and DEX infrastructure can be weaponized. According to prosecutors, the group behind CATFI created the token on Pump.Fun, a Solana‑based launchpad that allows users to generate and list tokens with minimal friction. They then listed it on a decentralized exchange, used the “Eth Father” persona and other tactics to promote it aggressively, and engaged in circular trading across multiple wallets to obscure the fact that the issuing side effectively controlled the token. Within about 26 hours of issuance, CATFI’s price had risen approximately 1,001‑fold, attracting around 6,000 investors eager to ride the meme. After insiders pulled liquidity, 256 investors were left with combined losses of roughly 900 million won—about 586,000 dollars—while the organizers allegedly pocketed roughly 400 million won, or around 260,000 dollars, in criminal proceeds. The case’s significance lies not just in the numbers but in the fact that it is the first DEX rug pull to be prosecuted under South Korea’s virtual asset law, setting a precedent for future enforcement.

LIBRA illustrates the political meme variant. When a meme coin stylized as $LIBRA surged following social media promotion by President Milei, traders speculated that his backing signaled tacit approval or insider knowledge, leading to a frenetic rally. Shortly thereafter, the coin’s price crashed, with reports suggesting that early holders had dumped into the mania, resulting in allegations of a rug pull estimated at up to 251 million dollars in value destroyed. Investigations by exchanges and on‑chain analysts pointed to premeditated positioning by insiders who may have exploited the president’s tweet as a liquidity event, while some in meme coin circles reportedly treated the impending rug as an “open secret.” Such dynamics blur the line between organic political enthusiasm, cynical memetic speculation, and outright fraud.

In both cases, the projects weaponized memes—the cat imagery and influencer culture in CATFI, the libertarian symbolism of Libra and Milei’s brand in LIBRA—to short‑circuit rational evaluation. The tokens were not pitched as carefully designed DeFi primitives but as cultural tokens whose value derived from belonging to a movement or being early to a viral joke. That framing makes it harder for traditional risk frameworks to apply, because investors may be willing to overlook red flags in the name of fun or ideological alignment. Yet as the aftermath shows, the economic consequences are very real.

Protocol‑level rugs: BaseBros Fi, Kannagi Finance, ZKasino

Beyond pure meme coins, several DeFi protocols have suffered rug pulls or rug‑like exits that exploit trust in more complex ways. BaseBros Fi promised yield optimization strategies on the Base blockchain, likely marketing itself as an infrastructure‑style DeFi product rather than a speculative meme. The discovery that its unaudited vault contract contained a backdoor enabling the team to withdraw user funds, and the subsequent draining of about 130,000 dollars and disappearance of its online presence, revealed a classic rug built into the protocol’s architecture. For users who believed they were depositing into a sophisticated but legitimate yield aggregator, the revelation that the core contract was unaudited and unverified underscored how a DeFi veneer can mask basic custodial risk.

Kannagi Finance, a smaller protocol whose rug pull wiped out nearly a million dollars in total value locked, provides another cautionary tale from the yield farming world. Although detailed sources are not included here, reporting from the period noted that Kannagi’s TVL collapsed from roughly 2.13 million to almost zero in a short period, consistent with a liquidity or contract drain executed by insiders. These cases show that even modestly sized protocols can attract enough capital to make a rug profitable, especially if they target niche chains or ecosystems where users feel a false sense of security due to smaller community size.

ZKasino differs in that it straddles the line between DeFi and platform‑based betting. Users bridged ETH into ZKasino with the expectation of receiving chips or tokens they could later redeem, effectively trusting the platform with their funds. When withdrawals were halted, the official Telegram was banned, and approximately 10,500 ETH—valued at around 30 to 33 million dollars—became stuck, many in the community labeled it a rug pull. Dutch authorities eventually arrested a 21‑year‑old named Ildar Ilham in connection with the case, and on‑chain analysis suggested that ZKasino‑linked wallets had engaged in risky leveraged trading that may have contributed to losses. In response to the backlash, ZKasino announced a convoluted “two‑step bridge back process” for users to withdraw a portion of their share, but confidence in the platform had already been shattered. For many observers, the incident demonstrated how rug pulls can occur even in contexts that look more like centralized online gambling than pure DeFi.

“Green” revolutions and long‑con rugs: Rowan Energy

Rowan Energy’s saga highlights that not all rug pulls are fast or overt. Marketed as a clean‑energy blockchain focused on carbon‑neutral mining and environmental impact, Rowan courted investors with the promise of aligning profits with planetary good. The project claimed a total token supply of around 545 million, with narratives about scarcity and fair distribution. Investigations by Rekt News and on‑chain analysts, however, uncovered that the true supply was closer to 945 million and that the contract contained a mint function enabling insiders to create an additional 400 million “ghost” tokens that were not publicly disclosed. Over five years, this discrepancy allowed founder David Duckworth and associates to allegedly run a sustained fraud, using the hidden supply to dump tokens into the market while gaslighting critics and leaning on green branding to deflect scrutiny.

Unlike a sudden DEX liquidity rug, Rowan’s fraud operated as a slow siphon. Investors were not wiped out in a single transaction; instead, their holdings were gradually diluted and devalued as insider‑minted tokens hit the market. This pattern resembles a soft rug pull on a multi‑year timescale and underscores how traditional equity‑style fraud—misrepresenting supply and control—can be implemented via smart contracts. The fact that the project’s narrative centered on environmental responsibility likely made some investors less inclined to scrutinize tokenomics carefully, illustrating how virtue signaling can be weaponized in crypto just as in traditional finance.

CeFi‑like Ponzi rugs: BG Wealth Sharing

BG Wealth Sharing sits somewhat outside the pure DeFi rubric but is instructive as a CeFi‑style rug pull. Participants reported being drawn into a wealth‑sharing or revenue‑sharing platform that promised attractive returns and may have used multi‑level marketing tactics to encourage recruitment. As long as new money flowed in, some early participants were able to withdraw funds, reinforcing the perception that the scheme was legitimate. When U.S. authorities moved in, seized the website, and posted an FBI warning, victims found themselves locked out of accounts that still showed paper balances. Many were then told by promoters or affiliated parties that they needed to pay a 12 percent “tax” or fee to access their funds, a claim that a financial educator in a YouTube video debunked as impossible and a red flag for further fraud.

The commentator stressed that in such cases, funds are typically gone and that victims should not send additional money to anyone claiming they can recover it, including purported lawyers advertising on social media or in unofficial groups. Instead, they should report the fraud through official government websites and accept that recovery is unlikely. BG Wealth’s collapse shares with DeFi rug pulls the core pattern of insiders disappearing with funds and leaving misleading interfaces that suggest balances still exist. But its reliance on off‑chain promises and custodial control aligns it more with traditional Ponzi schemes than with smart contract exploitation. For the broader crypto narrative, however, the distinction is academic: the public sees yet another crypto‑branded platform where the rug was pulled.

Evolved Apes NFT rug pull — developer 'Evil Ape' vanishes with ~$2.7M in mint proceeds

ZKasino halts all withdrawals, trapping ~10,500 ETH from users

US DOJ charges three UK nationals over Evolved Apes NFT scam — first major NFT rug pull federal prosecution

$LIBRA meme coin rug — Milei-promoted token collapses, destroying ~$100M in hours

South Korea indicts CATFI crew — first criminal prosecution for a DEX-based rug pull

Rowan Energy five-year green crypto fraud exposed — hidden mint functions and fake supply caps drained investors under ESG branding

Detection and Prevention: Tools, Red Flags, and On‑Chain Analytics

Common red flags and basic due diligence

Despite the diversity of rug pull designs, several red flags recur often enough that they form the backbone of basic due diligence. Both Solflare and CertiK emphasize that anonymous or pseudonymous teams, while not inherently malicious, raise the bar for trust because they can more easily disappear without consequences. When combined with a lack of verifiable LinkedIn profiles, GitHub activity, or public interviews, anonymity should prompt extra caution. Another red flag is the absence of clear, detailed project documentation. If a token’s website and whitepaper consist mainly of memes, slogans about “going to the moon,” and vague promises of viral growth, with no concrete roadmap, token utility, or governance model, it is more likely to be a pump vehicle than a serious DeFi protocol.

Liquidity characteristics are especially important. Solflare recommends checking whether a token’s liquidity is locked using blockchain explorers and tools such as Solscan, DexTools, or Birdeye. If all or most liquidity is controlled by a single wallet linked to the deployer and not locked in a time‑locked contract, the team can, in principle, pull the plug at any time. Holder distribution is another key factor: if one wallet, or a small cluster of wallets, holds a majority of the token supply, that concentration gives insiders disproportionate power to affect price, dump into rallies, or control governance. Extremely high promised yields or zero‑fee structures that seem too good to be true also warrant skepticism, as they often rely on unsustainable token emissions or hidden fees.

Social proof can be misleading. Solflare warns against relying solely on follower counts or Telegram member numbers, which can be faked or purchased. Prospective users should probe engagement quality by reading replies on X, asking questions in Discord or Telegram, and observing how moderators handle criticism. Is the conversation focused on building features and managing risk, or is it dominated by price talk and aggressive shilling? Projects that immediately ban skeptics or respond to substantive questions with memes may be signaling that they are not prepared for serious scrutiny.

Smart contract review and ownership structures

Even without being a developer, users can perform basic smart contract checks that materially reduce rug pull risk. Solflare suggests using explorers like Solscan or Etherscan to look up a token contract and examine fields such as total supply, mintability, and ownership. If the total supply is not fixed or the contract clearly contains mint functions that can be called by the owner or privileged addresses, there is a risk of hidden dilution. If the contract is marked as a proxy or upgradable, users should check whether the upgrade authority has been renounced or transferred to a robust multisig; if a single externally owned account retains upgrade control, the developer can, at least in principle, change core logic after deployment, potentially introducing malicious features.

Ownership of the contract itself is another vector. Contracts where the owner has been renounced or transferred to a well‑structured multisig that requires multiple independent signers to approve changes are generally safer than those where a single key controls everything. For liquidity pools, users should verify whether LP tokens are locked or burned. If they remain in a deployer‑linked wallet, the risk of a liquidity rug is high. Many projects now advertise liquidity locks as a badge of credibility, but users should confirm these claims on‑chain rather than taking marketing at face value.

Rowan Energy’s hidden mint function and undisclosed supply show what can happen when such checks are not performed or are obfuscated. By claiming a 545‑million token supply while secretly holding 945 million and retaining mint capabilities, the project exploited information asymmetry between insiders and the market. BaseBros’ unaudited vault contract similarly underscores the importance of verifying not just the main token contract but also any ancillary contracts that hold user funds. A single unaudited component with withdrawal privileges can enable a rug even if other parts of the system look clean.

On‑chain analytics and machine‑learning approaches

Beyond manual checks, a growing ecosystem of on‑chain analytics tools and research projects aims to automate rug pull detection. RPHunter’s approach of constructing a semantic risk code graph and a token flow behavior graph reflects a recognition that both code features and transaction patterns matter. Code features capture static risk factors such as mint functions, ownership structures, and transfer restrictions, while transaction patterns capture dynamic behaviors like sudden concentration of tokens in a small number of wallets, abnormal liquidity additions and removals, and wash‑trading loops. Graph neural networks are well suited to this task because they can model relationships between addresses and contracts in a flexible way, learning latent representations that encode subtle risk signals.

The ScienceDirect study focusing on DEX‑listed meme tokens adds another dimension by highlighting the predictive power of features like initial liquidity size, the speed and pattern of liquidity changes, the distribution of token holdings among early addresses, and price volatility in the first days of trading. Models trained on historical rug pulls can flag new tokens whose early behavior closely matches past scams, allowing exchanges, wallets, or even retail users to avoid them before the rug is pulled. Some projects have begun integrating such models into wallet interfaces, displaying risk scores or warnings when users attempt to interact with high‑risk contracts.

However, the 42,000‑victim meme coin scam that fooled even top “rug pull detectors” serves as a cautionary example. Attackers can study public detection criteria and intentionally design projects that stay just within “normal” bounds on each individual metric while still exploiting unsuspecting users via novel combinations of tactics. They might distribute token holdings more broadly at first, lock a portion of liquidity, or time dumps carefully to avoid triggering threshold‑based alerts. As a result, while machine‑learning and on‑chain analytics are powerful tools, they are not panaceas. They must be continuously updated, and users should treat them as advisory rather than definitive.

The role of centralized actors and law enforcement

Centralized entities—exchanges, stablecoin issuers, and custodial platforms—play a complex role in the rug pull ecosystem. On the one hand, permissionless DEXs like Uniswap or Solana‑based platforms enable anyone to list tokens without centralized vetting, which is both a feature and a bug. On the other hand, centralized exchanges (CEXs) can choose which assets to list, perform due diligence, and respond to suspicious activity. In the BG Wealth case, for instance, authorities worked with major exchanges and stablecoin issuers such as Binance, Tether, and OKX to freeze around 41 million dollars in crypto linked to a broader 150‑million‑dollar Ponzi and alleged rug pull, highlighting how centralized chokepoints can be leveraged to disrupt laundering. Similarly, in some rug pull cases, Tether has frozen USDT held in addresses linked to scams, and exchanges have blacklisted or flagged wallets associated with known frauds.

Law enforcement agencies are also improving their capacity to handle crypto‑specific fraud. The Frosties and Evolved Apes prosecutions by the U.S. Department of Justice show a willingness to apply traditional wire fraud and money laundering statutes to NFT rug pulls. In Frosties, investigators used on‑chain tracing and exchange records to link pseudonymous wallets to real‑world identities and to demonstrate the flow of misappropriated funds. The Evolved Apes indictment similarly describes how defendants laundered funds through multiple crypto transactions, which prosecutors interpret as evidence of intent to conceal. In South Korea, the CATFI case under the Virtual Asset User Protection Act illustrates how specialized virtual asset crime units can use on‑chain analysis and social media evidence in tandem to build cases against DEX‑based rug pullers.

At the same time, as Solflare emphasizes, cross‑border enforcement remains limited, and small victims rarely see restitution. For every high‑profile bust, there are dozens of rug pulls where perpetrators remain unidentified or reside in jurisdictions with weak enforcement capacity. This reality reinforces the importance of prevention and self‑protection. It also raises questions about how far centralized actors should go in curating or censoring access to high‑risk DeFi products. The Coinbase‑White House CLARITY Act dispute reflects these tensions in a different arena: regulators seek clearer rules for DeFi, tokenized equities, and yield products, while industry players worry about stifling innovation or exposing themselves to unpredictable political dynamics. When policy negotiations themselves are described as rug pulls, it underscores how fraught the path forward is.

Wallet‑level protections and transaction awareness

One promising frontier for mitigation is at the wallet layer. Solflare and other modern wallets have begun offering transaction simulation features that show users, before they sign, what a proposed transaction will actually do on‑chain. For example, if a decentralized app attempts to set an unlimited spending approval on a token or to transfer assets to an unfamiliar contract, the wallet can display this clearly, allowing users to abort if something looks off. Some wallets also integrate contract verification checks, warning users when they are interacting with unverified or unaudited contracts or with addresses flagged by security firms as high risk.

Solflare’s educational materials emphasize that many users are not rugged because they chose a bad token but because they approved a bad contract, granting it permission to move tokens or NFTs from their wallet. Understanding what one is signing, double‑checking token names and contract addresses, and avoiding connecting wallets to unknown websites are therefore practical steps that can dramatically reduce exposure to rug pulls and related scams. Wallets that prioritize such safeguards—by defaulting to least‑privilege approvals, surfacing risk information, and making revoking approvals easy—can help shift the ecosystem away from a caveat emptor model toward a more balanced one where responsibility is shared between users and infrastructure providers.

Legal and Ethical Dimensions

When does a rug pull become a prosecutable crime?

Legally, not every failed or abandoned crypto project is a rug pull, and not every rug pull is prosecuted as such. The key elements that typically transform a rug pull from a moral wrong into a prosecutable crime are misrepresentation, intent, and misappropriation. In the Evolved Apes case, U.S. prosecutors allege that the defendants knowingly misrepresented their plans to build a game and long‑term ecosystem, induced buyers to purchase NFTs based on those false promises, then diverted funds for personal use and laundered them. Those facts fit neatly within traditional wire fraud and money laundering statutes, even though the assets involved are NFTs rather than fiat currency.

Similarly, the Frosties case charges the founders with conspiracy to commit wire fraud and money laundering, emphasizing their alleged pattern of promising benefits and then suddenly abandoning the project and transferring proceeds to personal wallets. In both instances, the Department of Justice treats the rug pull not as a novel crypto‑specific offense but as a variant of established fraud crimes executed through digital assets. That approach has the advantage of relying on well‑developed case law while signaling that crypto’s perceived anonymity will not shield perpetrators.

In South Korea’s CATFI case, the legal theory centers on market manipulation and the use of fraudulent means under the Virtual Asset User Protection Act. Prosecutors argue that the group’s use of false statements, circular trading to conceal issuer control, and fake influencer personas constituted a deliberate plan to deceive investors in connection with digital asset trading. The fact that CATFI was listed on a DEX rather than a regulated exchange did not exempt it from scrutiny; instead, the case demonstrates that, at least in some jurisdictions, DEX‑based schemes are now squarely within the scope of financial crime enforcement.

By contrast, many soft rugs and ethically dubious exits fall into legal grey areas. A team that simply overpromises, fails to deliver, and gradually sells its token allocation into a falling market may be guilty of poor judgment or negligence, but unless there is clear evidence of intentional deception or misappropriation of designated funds, prosecutors may decline to bring charges. Similarly, venture funds that aggressively dump tokens after lockups expire may contribute to sharp price declines but generally operate within contractual rights. For regulators and courts, drawing lines in this space requires careful analysis of disclosures, governance structures, and the intent inferred from communication and on‑chain behavior.

Pseudonymity, jurisdiction, and the culture of impunity

Crypto’s culture of pseudonymity complicates enforcement. Many projects are launched by developers using only handles, with no public linkage to legal identities. While pseudonymity can protect privacy and encourage experimentation, it also lowers the perceived cost of bad behavior. Attackers can rug one project, disappear, and resurface under a new alias. As Solflare notes, even when rug pulls are tracked on‑chain, catching the people behind them is rare when they operate across multiple jurisdictions and use privacy tools to obscure flows. That reality contributes to what some industry observers describe as a culture of impunity, where insiders boast on Instagram or X about sniping pre‑launch allocations and rugging tokens, confident that no one will connect the dots.

Jurisdictional fragmentation exacerbates this. While U.S. and South Korean authorities have demonstrated a willingness to pursue certain rug pulls, not all countries have clear legal frameworks for digital asset fraud. Cooperation between agencies can be slow, and extradition may be politically sensitive. Attackers can exploit these gaps by routing funds through exchanges in lenient jurisdictions, using mixers or privacy chains, and cashing out via OTC desks. RPHunter’s identification of thousands of rug pull tokens on Ethereum underscores that the problem is systemic, not limited to a handful of unlucky cases. Without credible deterrence, the cost‑benefit calculation for potential scammers remains skewed.

From an ethical standpoint, the normalization of rug pulls and insider games corrodes crypto’s original ethos of fairness, transparency, and permissionless innovation. When high‑profile builders or venture capitalists are seen as tolerating or even participating in borderline rug behavior, it sends a signal to the broader ecosystem that exploitation is acceptable as long as it is technically legal or cleverly disguised. Reversing this trend requires not just enforcement but also cultural leadership: prominent figures must unequivocally condemn rug pulls, refuse to back serial offenders, and build systems that make it harder to profit from fraud.

The rhetorical “rug pull” and public perception

The use of “rug pull” as a metaphor in political and regulatory debates shapes public perception in subtle ways. When the White House reportedly characterized Coinbase’s withdrawal from CLARITY Act negotiations as a rug pull on the administration and the wider crypto industry, it framed the company’s strategic decision as a betrayal rather than a policy disagreement. For some, that language resonates: after months of engagement, a sudden change of heart can feel like the rug being pulled. For others, applying a term associated with investor fraud to legislative bargaining risks trivializing the harm suffered by actual rug pull victims.

Similarly, when commentators describe policy shifts, exchange delistings, or protocol parameter changes as rug pulls, they risk conflating structurally different phenomena. A change in staking rewards or a governance decision to reallocate treasury funds may be controversial but, if executed through transparent processes and in line with disclosed rules, is not a rug pull in the fraud sense. Overuse of the term can also reinforce the narrative that crypto is inherently scam‑ridden, making it harder for legitimate builders and advocates to argue for nuanced regulation.

For news organizations and analysts, precision in language matters. Reserving “rug pull” for cases where insiders exercise undisclosed control to extract value at others’ expense helps maintain its analytic sharpness. At the same time, recognizing the term’s cultural evolution can aid in understanding how communities experience sudden shifts—as betrayals rather than simply adverse events—even when no crime occurred.

White House blasts Coinbase’s last‑minute exit from Trump’s CLARITY Act talks as a “rug pull” on both the administration and the wider crypto industry, after the exchange abruptly withdrew support over DeFi, tokenized‑equity, privacy and stablecoin‑yield provisions that also forced a Senate Banking markup delay.

Let the drama begin

Hidden mint functions, unaudited withdrawal logic, and owner-privileged liquidity removal are the technical levers behind hard rugs — BaseBros Fi used an unaudited contract and Rowan Energy embedded a hidden mint to drain investors over five years.

Single-operator or insider-wallet control over liquidity pools enables instant exits; LIBRA and $YZY both showed insider wallets sniping at launch and draining pools within hours of token creation.

Thin or non-locked liquidity pools can be fully drained in a single transaction with no recourse; ZKasino trapped approximately 10,500 ETH and Hypervault lost $3.6M before users could withdraw.

Meme coin launch windows compress fraud timelines to minutes — the CR7 token generated a $143M rug in 15 minutes and LIBRA destroyed roughly $100M in under 24 hours.

Enforcement is accelerating with cross-border cooperation — the DOJ charged three UK nationals over Evolved Apes and South Korea secured its first DEX rug pull prosecution via the CATFI case — but asset recovery after bridging and Tornado Cash laundering remains rare.

How to Protect Yourself Without Quitting DeFi

Practical due diligence for everyday users

Complete safety is impossible in any financial market, and DeFi’s permissionless nature ensures that risk will always exist. However, individual users can materially reduce their exposure to rug pulls through disciplined habits. The mantra “Do Your Own Research” (DYOR) remains valid, but it must go beyond reading a few bullish tweets. At a minimum, prospective investors should investigate who is behind a project, what track record they have, and whether their identities are verifiable. Pseudonymous teams are not automatically suspect—some of the most respected DeFi protocols were launched by pseudonymous founders—but anonymity should prompt deeper scrutiny of code, audits, and governance.

Reading project documentation with a skeptical eye is essential. Does the whitepaper explain how value will accrue to the token, or does it rely on vague promises of viral growth? Are there clear plans for revenue, sustainability, and risk management, or just aggressive emissions schedules and talk of “number go up”? Understanding tokenomics—supply caps, vesting schedules, allocation to founders and investors, and mechanisms for liquidity—helps identify situations where insiders hold disproportionate power.

On the technical side, even non‑developers can learn to check fundamental contract data using explorers. Looking up a token on Solscan or Etherscan and examining the top holders can quickly reveal whether one wallet owns 70 percent of the supply, a glaring red flag. Checking whether liquidity is locked, and for how long, provides additional context: a token whose entire liquidity can be withdrawn by a single wallet tomorrow is inherently riskier than one with multi‑year locks. Combining these checks with social observations—how the team responds to criticism, whether they provide meaningful updates, whether independent auditors or researchers have reviewed the code—creates a more holistic risk picture.

Risk management, position sizing, and FOMO control

Even with careful due diligence, some rug pulls will slip through. That reality makes risk management and position sizing critical. Treating speculative meme coins or unaudited DeFi protocols as lottery tickets rather than core portfolio holdings can prevent life‑altering losses. Allocating only a small portion of one’s capital to high‑risk plays, and resisting the urge to “ape in” large sums based on FOMO, is a pragmatic response to an environment where rugs are a known hazard.

Psychologically, this means learning to recognize FOMO triggers. Huge APY promises, viral memes, celebrity rumors, and screenshots of overnight millionaires are classic bait. Legitimate projects can grow quickly, but they rarely rely solely on hype; their teams typically engage with security researchers, publish code, and show progress over time. A healthy skepticism toward “once in a lifetime” opportunities helps counter the cognitive biases that scammers exploit.

Diversification across protocols, chains, and asset types can also mitigate the impact of any single rug pull. While diversification is not a shield against systemic risks, it reduces the likelihood that a single failure will wipe out most of one’s holdings. At the same time, over‑diversification into dozens of obscure tokens can create a different problem: difficulty tracking risks. Striking a balance—holding a manageable number of positions that one can monitor—is often more effective.

Community defense, bounty programs, and the limits of detectors

Communities can play a powerful role in identifying and deterring rug pulls. On‑chain sleuths who share analyses on platforms like X and Discord have exposed many scams before or shortly after they executed, sometimes convincing exchanges to freeze funds or block suspicious tokens. Bounty programs, such as initiatives where analytics platforms or firms offer rewards for information leading to the unmasking of rug pull perpetrators, harness crowdsourced intelligence. Arkham’s bounty efforts to expose culprits behind major hacks and meme coin rug pulls, for instance, reflect this model of decentralized investigative incentives.

At the same time, the 32‑million‑dollar meme coin scam where even top rug pull detectors were fooled serves as a reminder that tools and crowds alike can be outpaced. As detection models become more sophisticated, attackers study them and design around their criteria. Some projects may even attempt to game reputation systems by securing superficial endorsements from influencers or low‑quality audits to appear legitimate. Community defense is most effective when it combines technical analysis, open debate, and a willingness to update views as new evidence emerges.

Users should also be cautious about relying on any single detector or “safe list.” A token labeled “safe” today could deploy new contracts or governance changes tomorrow that alter its risk profile. Conversely, a token flagged as high risk might be an experimental but honest project. Treating risk scores as inputs into a broader decision process, not as absolute truths, is a more resilient approach.

What to do if you suspect or experience a rug pull

If you suspect a rug pull is in progress—perhaps because liquidity has suddenly dropped, a project’s website has gone offline, or funds have been drained from a contract—the first step is to stop interacting with the affected contracts and revoke any outstanding approvals. Tools exist on most major chains to revoke token allowances, which can prevent further unauthorized spending by malicious contracts. While revoking approvals will not recover lost funds, it can limit additional damage.

Reporting the incident to relevant platforms and authorities is also important. Exchanges may be able to freeze funds if stolen assets are deposited there, as seen in cases where centralized actors collaborated with law enforcement to halt laundering of scam proceeds. Wallet providers and security firms can update blacklists or warning systems to alert other users. Government agencies, such as the FBI in the U.S. or specialized virtual asset crime units in other jurisdictions, may collect reports to identify patterns across multiple cases.