Comprehensive explainer on memecoins: what they are, how they launch and trade (esp. on Solana and Pump.fun), celebrity and political tokens like TRUMP, legal risks, market structure, and how these volatile assets fit alongside Bitcoin, ETH and stablecoins.

+3 sources across the wider coverage universe

MEXC names ex-Bitget exec Vugar Usi CEO to add compliance without losing its memecoin listing edge2026-04

MEXC names ex-Bitget exec Vugar Usi CEO to add compliance without losing its memecoin listing edge2026-04 Predict.fun Adds Memecoin Prediction Markets for Fees, Listings and Market Cap Using Onchain Data2026-04

Predict.fun Adds Memecoin Prediction Markets for Fees, Listings and Market Cap Using Onchain Data2026-04 Trump memecoin conference drops minimum holding from $55K to $8,460, now counts merch sales as $TRUMP slides 80%2026-04

Trump memecoin conference drops minimum holding from $55K to $8,460, now counts merch sales as $TRUMP slides 80%2026-04 Crypto critic alleges Trump family turned post‑2024 “pro‑crypto” agenda into a self‑enriching empire of memecoins, USD1 stablecoin, and pay‑to‑play regulation that looted crypto’s future2026-03

Crypto critic alleges Trump family turned post‑2024 “pro‑crypto” agenda into a self‑enriching empire of memecoins, USD1 stablecoin, and pay‑to‑play regulation that looted crypto’s future2026-03 Pumpfun and Solana Face $5.5B RICO Lawsuit Alleging Coordinated Memecoin Scheme That Wiped Out Retail Investors2025-12

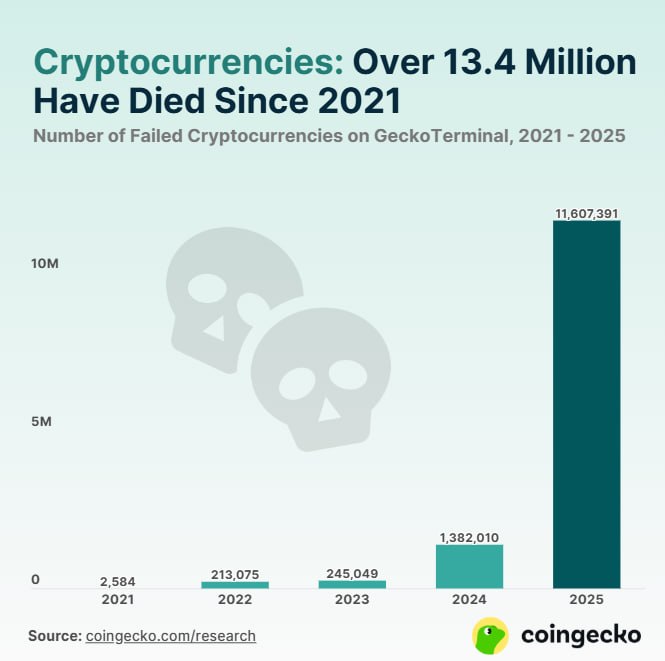

Pumpfun and Solana Face $5.5B RICO Lawsuit Alleging Coordinated Memecoin Scheme That Wiped Out Retail Investors2025-12 Over half of all cryptocurrencies launched since mid‑2021 have already died, with more than 13.4 million tokens—86% of them in 2025 alone—ceasing to trade after an explosive memecoin boom and a brutal late‑2025 washout.2026-01

Over half of all cryptocurrencies launched since mid‑2021 have already died, with more than 13.4 million tokens—86% of them in 2025 alone—ceasing to trade after an explosive memecoin boom and a brutal late‑2025 washout.2026-01

Memecoins: An Evergreen Guide To Crypto’s Most Controversial Assets

Memecoins are cryptocurrencies whose primary value proposition is cultural rather than technological: they are tokens built around internet jokes, viral images, or personalities, and traded largely on attention, narrative, and speculation rather than cash flows or clear utility. In every crypto cycle they re-emerge as both a barometer of risk appetite and a flashpoint for debates about regulation, ethics, and whether crypto is building a new financial system or just a global on-chain casino.

What Are Memecoins?

At the most basic level, a memecoin is any crypto asset whose core “fundamental” is a meme. Instead of promising to power a smart contract platform, collateralize a lending protocol, or maintain a peg like a stablecoin, a memecoin usually exists mainly because people find an idea funny, resonant, or socially meaningful enough to buy and hold the token. The meme might be an image of a Shiba Inu, a political figure, a celebrity, or a piece of internet lore, but the price still trades on the same market dynamics as any other token: supply, demand, liquidity, and expectations about future buyers. In this sense memecoins are less a specific technical category and more a cultural and market phenomenon that can emerge on any programmable blockchain.

The appeal of memecoins lies in their combination of extreme volatility and shared narrative. Traders can move from zero to seven-figure market caps in hours if a meme goes viral, but just as quickly collapse back to near zero when the narrative moves on or large holders sell. For many participants this is closer to entertainment or gambling than to long-term investment, yet the same speculative flows can generate real on-chain fees, liquidity, and activity that sometimes rival or exceed “serious” DeFi usage on a chain. In practice, memecoins and blue-chip assets like Bitcoin and Ether tend to coexist rather than compete, with memecoins acting as high-beta side-bets on overall crypto sentiment.

From an infrastructure perspective, memecoins are simply fungible tokens—ERC‑20 on Ethereum, SPL tokens on Solana, or analogous standards on other networks—created and traded through smart contracts. The contracts themselves are typically straightforward: a fixed supply or inflation schedule, basic transfer logic, and often no governance or protocol revenue hooks at all. On Solana, platforms like Pump.fun even abstract contract creation away entirely, allowing users to launch new tokens through a front-end interface that automatically wires up a bonding curve and liquidity pool. This low technical barrier explains why thousands of memecoins can be created in a single week during peak mania.

Crucially, the memecoin label says almost nothing about whether a token is legally compliant, fairly launched, or free from insider advantage. Some memecoins begin as community jokes with no pre-mine, no team allocation, and fully on-chain liquidity from day one; others are heavily pre-allocated to insiders who then market to retail buyers; still others are outright scams designed to “rugpull” investors by draining liquidity and disappearing. This wide spectrum is why regulators, courts, and lawmakers increasingly treat memecoins not as a harmless sideshow but as a test case for how securities law, consumer protection, and ethics rules should apply in crypto markets.

Crypto enters its “Graham era” as looming U.S. market structure laws could unlock value-accruing tokens, shifting investors from memecoin speculation toward fundamentals

15-9 out of Senate Banking is the kind of catalyst desks can underwrite: if fee switches, burns, or distributions stop being an SEC roulette table, UNI, AAVE, and MKR/SKY get priced against fee durability instead of vibes. Uniswap’s fee-switch fight already showed why this matters: the market wants return of capital, but governance has to prove it can route cash flow without insider capture or LP revolt. Memecoins keep their casino bid, but the opportunity cost changes once capital can buy provable on-chain P/E with legal-ish value return.

Readers click memecoins not to speculate but to watch powerful people expose themselves — the highest-performing headlines all orbit a single question: who extracted value from whom, and was the stated valuation real?↗

Origins And Evolution Of Memecoins

The memecoin story begins well before Solana and Pump.fun: it is rooted in Dogecoin, launched in 2013 as a fork of Litecoin branded with the then-popular Doge meme. Dogecoin’s creators never claimed it would replace traditional money or power a new internet; it was explicitly a joke about the proliferation of altcoins, yet it nonetheless developed a community that used DOGE for tipping, sponsorships, and experiments in collective action. In hindsight Dogecoin established the template: a culturally recognizable symbol, a relatively simple technical design, and an open-ended invitation for the internet to imbue the token with meaning far beyond its codebase.

During the 2020–2021 bull cycle, that template metastasized. Shiba Inu (SHIB), branded as a “Dogecoin killer,” rode a wave of speculative enthusiasm and social media virality to become one of the largest tokens by market capitalization, cementing the idea that meme-based assets could capture enormous paper wealth in a short time. Other dog-themed tokens and viral references followed, turning memecoins from a single oddity into a recognizable sector. By 2025, memecoins like DOGE and SHIB were established enough that newer entrants such as Dogwifhat (WIF), Pepe (PEPE), and Bonk (BONK) were routinely described as part of an ongoing memecoin tradition rather than isolated anomalies.

What changed over time was less the basic concept and more the speed and scale of memecoin lifecycles. On earlier chains, higher transaction costs and slower block times limited the volume of micro-cap experimentation. With the rise of high-throughput, low-fee networks—particularly Solana—traders could spin up and trade new tokens at a pace that made Dogecoin’s early days look quaint. Tools like Pump.fun, which abstracted away contract deployment and initial liquidity, pushed this evolution one step further by making the memecoin launch process accessible even to users with no coding knowledge. Memecoins thus moved from being rare curiosities to an always-on conveyor belt of new narratives.

The expansion of memecoins also spilled into Bitcoin’s ecosystem through the advent of Ordinals and BRC‑20-style fungible tokens. Platforms such as Ord.io grew up to help users browse and trade these inscriptions, some of which functioned effectively as memecoins on Bitcoin’s base layer. Ord.io’s announcement that it would shut down after three years of operation due to running out of money highlighted that even as memecoin volumes rise, the supporting infrastructure can be fragile, and business models built purely on speculative trading activity may not be sustainable in every market environment. This dynamic—booms in new token formats followed by consolidation and attrition—is a recurring pattern in the broader memecoin story.

By 2025–2026, memecoins had diversified not just across chains but also across themes. In addition to dog coins and pure internet jokes, markets saw political tokens, celebrity-branded tokens, regionally focused memes, and community-driven experiments tied to identity or cause-based fundraising. WIF, PEPE, and BONK continued to trade as some of the most popular tokens of their kind, while new Solana memecoins attracted fresh capital that some commentators argued might be “more than just a flash-in-the-pan moment” for the chain. At the same time, regulators and critics increasingly questioned whether these assets were simply rebranded penny stocks with worse disclosures and faster feedback loops.

How Memecoins Launch And Trade

Understanding memecoins requires understanding their launch mechanics, because those mechanics often determine who profits, who bears risk, and how the narrative evolves. On chains like Ethereum, traditional memecoin launches typically involve a developer deploying an ERC‑20 contract, minting a fixed supply of tokens, and then seeding a liquidity pool on a decentralized exchange like Uniswap. The developer might retain a portion of the supply, send some to early backers, and leave the rest for public trading. Centralized exchanges may later list the token if liquidity and demand are sufficiently strong. While these steps are technically straightforward, the exact allocation choices—pre-mines, team wallets, “burns”—can create substantial asymmetries between insiders and retail traders.

Solana’s Pump.fun platform reimagined this flow by putting launch and early trading behind a simple interface and an automated bonding curve. On Pump.fun, users can create a new Solana memecoin without writing code, and the token is immediately tradable via a bonding curve contract that sells tokens to buyers at increasing prices as more liquidity flows in. The idea is that if demand is strong enough to push the token to a predefined threshold—often framed in terms of market cap or liquidity—the token “graduates” off the bonding curve into a conventional liquidity pool on a platform like Raydium, where it trades like any other SPL token. This graduation mechanism turns the launch phase into a kind of on-chain audition: only tokens that attract sufficient early interest escape the curated Pump.fun environment.

For a period in late 2025 and early 2026, Pump.fun’s model was extraordinarily successful. Data reported by The Block and summarized by Cointelegraph indicate that Pump.fun accounted for more than one-third of Solana’s total revenue in the first quarter of 2026, pulling in around 124.7 million dollars and becoming the network’s single largest revenue generator. That concentration underscores how deeply memecoin activity had become intertwined with Solana’s economic profile: a substantial share of validator and fee revenue was effectively downstream of speculative trading on a single memecoin launchpad.

Yet the same data also show how quickly market conditions can change. Over the subsequent three months, Pump.fun’s “graduation rate”—the percentage of tokens that reached the threshold to leave the bonding curve—fell about 80% to just 0.26%, while the platform’s average daily revenue dropped to around 800,000 dollars. This collapse suggests that fewer memecoin launches were able to sustain community interest long enough to reach scale, and that speculative capital may have rotated elsewhere or become more selective. In other words, memecoin launch platforms are themselves subject to boom-and-bust cycles as traders adapt to changing narratives, saturation, and regulatory scrutiny.

Beyond simple launch mechanics, memecoin trading has been shaped by the rise of bots, sniping tools, and arbitrage systems. On fast chains like Solana, automated programs can detect new token deployments and buy within seconds of liquidity being added, aiming to front-run human traders. While some view this as a natural extension of market-making, others argue it entrenches unfair advantages and turns memecoin launch events into “bot casinos” where retail users are systematically disadvantaged. Pump.fun’s controlled bonding curves partially mitigate this by standardizing the early pricing path, but even there, sophisticated traders can attempt to optimize entry and exit points around presumed graduation thresholds.

New product experiments continue to blur the line between trading and spectacle. Pump.fun’s “GO” bounty platform, launched as an adjacent product, allowed users to post tasks—anything from creating content to performing stunts—and pay bounties for completion. One widely discussed episode involved a user offering roughly 2,000 dollars for someone to tattoo a memecoin ticker on their forehead; due to a typo in the bounty text, the participant permanently tattooed “$Boutywork” rather than the intended ticker, turning both the typo and the stunt into an instant meta-meme across Crypto Twitter. The incident highlighted both the performative extremes to which some participants will go for memecoin clout and the ethical questions such platforms raise about incentives and exploitation.

As memecoins mature, many move beyond on-chain pools on decentralized exchanges to listings on centralized exchanges, which can dramatically increase liquidity and visibility. Dogwifhat, for example, has been listed on leading Korean exchange Upbit’s fiat and crypto markets according to recent coverage, signaling that certain memecoins can cross into quasi-mainstream markets when trading volumes and community engagement reach sufficient scale. At that stage, traders may also gain access to derivatives such as perpetual futures and margin trading, further amplifying both upside and downside. However, these centralized listings typically come later in the lifecycle and only for a small subset of memecoins; most tokens never escape the long tail of illiquid on-chain markets where slippage and manipulation risks are high.

From the perspective of market structure, memecoins now exist along a continuum of sophistication. At one end are ephemeral tokens that live and die entirely within a launchpad or DEX with no external recognition; at the other are large-cap memes with deep order books, derivatives markets, and institutional liquidity providers. Across this spectrum, market cap figures can be misleading because fully diluted valuations often assume that all tokens will eventually circulate, even when most supply is locked in team wallets or treasury addresses. Traders who focus only on headline market cap without examining float, liquidity, and concentration risk may badly misjudge the real depth of the market they are entering.

- 01Political memecoin valuation distortion↗

The $75B vs. $13B float-adjusted TRUMP coin discrepancy made FDV manipulation legible to general readers, turning a token launch into a story about financial deception at the highest level of power.

- 02Solana as memecoin infrastructure↗

Solana's DEX volume record and subsequent chain-wide outflows from memecoin decline showed readers that an entire L1's market narrative was being dictated by meme trading cycles.

- 03Celebrity and political launch accountability↗

A rapid succession of high-profile launches — Trump, Melania, Enron, McAfee's widow, Luigi — framed memecoins as a repeating celebrity exit-liquidity mechanism, making 'who profits at whose expense' the structural pull.

- 04Pump.fun platform dominance and failure↗

Pump.fun's capture of a third of Solana's Q1 revenue, combined with reports of tokens failing even to launch, made it the industrial infrastructure story beneath the individual coin noise.

- 05AI memecoin sector as narrative anchor↗

AI-themed memecoins crossing $10B gave the otherwise chaotic space a defensible thesis that readers could engage without dismissing the entire category.

- 06Influencer pump-and-dump exposure

ZachXBT naming Ansem and $500M in 2024 rug-pull losses reframed memecoins as a structured extraction machine with identifiable perpetrators, not random speculation.

The Solana Era, Pump.fun, And The On-Chain Casino

In public debate, Solana is often cast as a chain torn between two identities: a high-speed, low-cost platform enabling serious applications like stablecoin payments and institutional flows, and a hyperactive venue for memecoin speculation. Both realities can be true at once. On one hand, reports highlight that Solana is increasingly being used for real-world payment rails, including corporate stablecoin salary payouts and large financial institutions moving significant volumes through its ecosystem. On the other hand, on-chain data show that a sizable portion of its fee revenue and user activity has at times been driven by memecoin launches and trading, with Pump.fun at the center of the storm.

The economics are stark. When a single memecoin launchpad accounts for more than a third of a major layer‑1 network’s revenue over a quarter, as Pump.fun reportedly did on Solana in early 2026, the chain’s validators and stakeholders are partially dependent on continued memecoin mania to sustain fee levels. This is not unique to Solana; Ethereum experienced similar dynamics during the DeFi summer and NFT booms, when specific sectors dominated gas consumption. But in Solana’s case, the branding fight has been especially acute because critics have used the memecoin frenzy to paint the network as a venue for pure gambling rather than “serious” finance, even as traditional firms and infrastructure providers build on it.

Memecoins can also exert cultural gravitational pull. Tokens like BONK and WIF became informal mascots for the Solana ecosystem, with community members using them to express loyalty, fund marketing efforts, or reward participation in projects. This has both benefits and risks. On the positive side, successful memecoins can attract new users, generate marketing buzz, and bootstrap liquidity for decentralized exchanges and wallets. On the negative side, they can create the impression that the chain’s primary value proposition is speculation rather than robust, mission-critical applications. This is why initiatives like the “State of Solana” reports and coverage emphasizing institutional and stablecoin use cases have explicitly framed themselves as counterweights to the memecoin narrative.

The volatility of Solana’s memecoin markets is illustrated by episodes like the RKC token saga. Tied loosely in public perception to Roaring Kitty, the trader associated with the original GameStop short squeeze, the Solana-based RKC memecoin surged to an 11 million dollar market cap following viral posts on X (formerly Twitter) that suggested some level of endorsement. When those posts were deleted and the token’s developer reportedly sold roughly 611,000 dollars’ worth of RKC, the coin crashed by about 67%, wiping out much of the paper gains for late-arriving holders. For critics, this was yet another example of memecoin markets being driven by transient social media signals and insider liquidity events rather than underlying value.

Regulators and law enforcement are increasingly treating memecoin-related misconduct as a priority. In South Korea, for instance, authorities arrested suspects behind the Solana-based CatFi memecoin in what was reported as the country’s first rugpull case prosecuted under its new digital asset law. The case involved allegations that the developers had lured investors with promises and then drained funds, causing substantial losses. By framing the prosecution explicitly as a “rugpull” under a new legal regime, regulators signaled that memecoin scams would not be dismissed as mere internet shenanigans but treated as serious financial crimes.

Episodes on other chains reinforce the same message. Two Americans were reportedly arrested after a memecoin-related stunt involving Japan’s beloved internet monkey mascot caused public alarm, illustrating that offline consequences can arise when memecoin promotion crosses into physical spaces and local cultural sensitivities. While details vary, the underlying dynamic is similar: memecoins blur lines between online fandoms, speculative markets, and real-world behavior, often faster than legal and ethical norms can keep up.

At the ecosystem level, the rise and partial retracement of memecoin activity on Solana offers a case study in how quickly on-chain “casinos” can both enrich and strain a network. Periods of intense memecoin trading drive fees, transaction volumes, and new user sign-ups; they can also clog blockspace, increase latency, and crowd out less speculative uses. As Pump.fun’s graduation rate and revenues fell sharply over a three-month span, daily fee income on Solana dropped as well, highlighting the fragility of revenue bases that depend on speculative cycles. For chain stakeholders, the challenge is to harness the onboarding benefits of memecoins without letting them define the network’s long-term identity or economic stability.

Celebrities, Politics, And Legal Risk

Where there is attention, celebrities and politicians rarely lag far behind, and memecoins have become a natural vehicle for both to monetize their brands and test new forms of digital fandom. The legal system is now grappling with how to treat these projects, with recent cases providing early precedent while leaving many questions open.

The Caitlyn Jenner memecoin, JENNER, is a prominent example. Investors filed a class-action lawsuit alleging that the token was an unregistered security and that its promotion had violated securities laws. In May 2025, United States District Judge Stanley Blumenfeld dismissed the suit for failure to state a claim, and after the plaintiffs filed an amended complaint, he again threw the case out, finding that they had not adequately pleaded that JENNER was a security under established tests. Reports emphasized that the judge concluded the memecoin did not meet the criteria of an “investment contract” and therefore fell outside the securities regime, at least on the facts presented, while also noting jurisdictional deficiencies. Although the ruling is narrow and jurisdiction-specific, it has been interpreted in crypto circles as a modest win for celebrity tokens, suggesting that not every celeb-branded memecoin automatically counts as a regulated security.

If JENNER offered a partial win for promoters, the MOTHER memecoin associated with rapper Iggy Azalea has been a cautionary tale. A class-action suit in the United States accuses Azalea of misleading investors about the token’s real-world utility and future prospects, alleging that promotional materials and social media posts overstated what the project would deliver. The token reportedly fell about 99.5% from its peak price, causing heavy losses for late buyers. Whatever the eventual outcome, the case illustrates that even if a memecoin is not a security in a narrow legal sense, aggressive marketing claims can trigger liability under consumer protection, fraud, or disclosure laws if they are found to be deceptive or materially misleading.

Political memecoins add another layer of complexity because they intersect not just with securities regulation but also with campaign finance and ethics rules. Donald Trump has been linked to multiple crypto initiatives, including an “official” TRUMP memecoin and the World Liberty Financial protocol, a DeFi project founded in 2024 by members of the Trump family and several partners. Coverage has noted that Trump’s TRUMP memecoin has experienced sharp drawdowns—extending its slide even as he hosted exclusive gatherings for top token holders, including closed-door investor galas where participation thresholds were set in dollar terms of TRUMP holdings. Subsequent events, such as conferences lowering minimum holding requirements from roughly 55,000 dollars to under 10,000 dollars and counting merch sales toward participation, have raised questions about whether political access is being effectively priced through a speculative token.

These concerns have reached the legislative arena. Senator Kirsten Gillibrand, a key figure in ongoing efforts to pass comprehensive U.S. crypto market structure legislation, has publicly warned that there will be “no deal” on a sweeping bill without an ethics provision that addresses potential conflicts of interest arising from politicians’ ties to crypto ventures, including memecoins and DeFi protocols like World Liberty Financial. By tying ethics language directly to the fate of broader crypto legislation, Gillibrand’s stance underscores that high-level political involvement in memecoins is not just a curiosity; it has the potential to reshape how the entire sector is regulated and perceived.

Outside the United States, legal responses to memecoins increasingly focus on their use in fraud and market manipulation. The CatFi case in South Korea, cited earlier, marks the first rugpull prosecution under the country’s new digital asset law, signaling a willingness to treat memecoin developers as responsible actors subject to criminal penalties when they deceive investors. This is likely a harbinger of more coordinated global enforcement, particularly in jurisdictions where retail investors have suffered large losses from token schemes marketed via social media and celebrity endorsements.

Even those critical of memecoin speculation acknowledge that not all high-profile figures in crypto behave the same way. Ethereum co-founder Vitalik Buterin, for instance, has repeatedly used his personal wealth to fund philanthropic causes, including a donation of 64 ETH to the Animal Welfare Fund that he disclosed publicly while encouraging others to support non-human animals. While not explicitly framed as an anti-memecoin statement, gestures like these contribute to a broader contrast between building and giving versus promoting short-lived speculative tokens. They also influence community norms about what it means to be a responsible public figure in crypto, even as memecoins continue to offer tempting routes to quick attention and capital.

For participants, the key takeaway is that celebrity and political memecoins sit at the intersection of several overlapping legal regimes: securities law, consumer protection, anti-fraud statutes, campaign finance rules, and ethics codes. A token might avoid classification as a security yet still be subject to enforcement if marketing crosses certain lines. Conversely, a politically linked token might raise ethics concerns even if its launch mechanics are technically compliant. In such a fluid environment, relying solely on a promoter’s fame or perceived political power as a proxy for safety is a recipe for disappointment.

Pump.fun offers up to $5M annual compensation for a chief legal officer as the Solana memecoin giant navigates lawsuits, global regulation, and mounting compliance demands

$1M-$5M for legal only pencils if the job is venue survival, not product counsel. U.S. securities claims, the UK/FCA geoblock, MiCA, and now GO-style bounty escrow all collapse into one question: is Pump.fun a neutral token factory or an issuer/distributor with duties? Research on Q4 2024 had Pump.fun at up to 71.1% of Solana token mints and 40-67.4% of DEX transactions while under 2% graduated off the bonding curve; add KYC, age gates, promo review, or issuer-style disclosures and the Solana memecoin flywheel gets a lot less permissionless.

- 2024-12launch

Luigi token surges to $77M market cap following UnitedHealth CEO shooting

$TRUMP official memecoin launches three days before presidential inauguration, rises 10,000%

- 2025-01launch

Melania Trump launches $MELANIA on Solana; authenticity immediately disputed

AI-themed memecoins collectively exceed $10B market cap per CoinGecko

PumpSwap DEX surpasses $10B in cumulative volume within 10 days of launch

Caitlyn Jenner memecoin lawsuit dismissed; judge rules token not a security

Sen. Gillibrand blocks crypto bill progress without Trump memecoin ethics provision

Market Structure, Derivatives, And Prediction Markets

Memecoins do not exist in isolation; they are embedded in a broader crypto market structure that includes spot trading, derivatives, and increasingly sophisticated tools for betting on future outcomes. In each layer, memecoins play a distinctive role as high-volatility instruments that both reflect and amplify broader sentiment.

In spot markets, memecoins typically function as the highest-beta segment of the crypto risk curve. When Bitcoin and Ether are rallying, capital often rotates into major memecoins as traders seek higher percentage gains; when the majors retrace, memecoins can suffer outsized drawdowns as liquidity evaporates and risk appetite collapses. This pattern echoes a recurring observation in crypto cycles: before the proliferation of thousands of altcoins, many portfolios boiled down to a small set of categories—Bitcoin, Ether, a memecoin, an exchange token, and a “crypto dollar” or stablecoin—and despite the growth in token count, those core categories still explain much of market behavior today. In that simplified picture, the memecoin occupies the role of pure risk sentiment, similar to how small-cap growth stocks function in traditional equity portfolios.

Derivatives extend these dynamics. On centralized exchanges, large memecoins often have perpetual futures contracts that allow traders to go long or short with leverage, intensifying volatility and creating complex feedback loops between spot and derivatives pricing. On the decentralized side, platforms like MYX Finance are specifically targeting memecoin traders with permissionless perpetual markets. Promotional materials and social media posts from MYX highlight the ability to get exposure to memecoins via MYX V2 perpetuals in roughly twenty seconds, framing the product as a way for those who “missed” opportunities like a SpaceX-related token allocation to cope with anxiety by aping into memecoins via leverage. While such messaging resonates with a certain trading demographic, it also underscores how memecoins have become vehicles for outsized, emotionally driven bets.

Prediction markets add yet another layer of structure, turning meta-speculation about memecoins themselves into tradable instruments. Platforms like Predict.fun describe prediction markets as venues where users buy and sell contracts whose value depends on whether a specified future event occurs, with prices often reflecting the probability of that outcome. Because participants have financial incentives to be accurate, these markets can aggregate dispersed information into real-time odds about political events, sports outcomes, or—increasingly—crypto metrics. Recent coverage has highlighted prediction markets for memecoin-related questions, such as whether a token will reach a certain market cap, be listed on a major exchange, or maintain a given fee level over a period. By tying contracts to observable on-chain data, these platforms aim to create transparent betting markets around memecoin trajectories.

The regulatory status of prediction markets remains complex, but conceptually they differ from memecoins in that each contract explicitly references a clearly defined outcome rather than an open-ended narrative. Still, as memecoin prediction markets grow, the line between trading a meme token and trading on expectations about that token’s popularity can blur. For example, a trader might buy a memecoin, then buy prediction market contracts that pay out if the token reaches a certain listing milestone, effectively constructing a levered bet on its social adoption. The existence of such instruments can also feed back into the narrative, as market-based probabilities become part of the community discourse.

While memecoins capture the headlines, a quieter revolution has been unfolding around stablecoins, whose primary function is to maintain a peg to a reference asset like the U.S. dollar and serve as reliable payment instruments. The GENIUS Act passed in the United States in 2025, for instance, defined certain stablecoins issued by permitted entities as payment instruments rather than securities or commodities, giving them a clearer regulatory home and paving the way for more mainstream financial integration. Analysts have argued that 2026 could be the year stablecoins truly go mainstream, with banks and corporates using them for payroll, settlement, and cross-border flows, even as public attention remains fixated on memecoin pump-and-dump cycles. This contrast is important: while memecoins exemplify crypto’s speculative frontier, stablecoins exemplify its emerging role in everyday finance.

To frame these relationships, it can be useful to compare memecoins with other major crypto asset types:

| Asset type | Primary purpose | Typical volatility | Cash flow / revenue link | Regulatory clarity (US / major markets) |

|---|---|---|---|---|

| Bitcoin | Store of value, digital commodity | High but declining over time | None intrinsic; some protocols build on top | Increasingly treated as commodity-like but still evolving |

| Ether | Smart contract gas, staking asset | High | Tied to network fees and staking rewards | Partial clarity; debates over security vs commodity continue |

| Memecoin | Cultural expression, speculation | Extremely high; frequent 50–90% swings | Generally none; some add dubious “utility” later | Highly uncertain; fact-specific, with cases like JENNER showing nuance |

| Exchange token | Fee discounts, governance, ecosystem incentives | High but more anchored | Sometimes linked to exchange revenues or buybacks | Under scrutiny; some treated as securities in enforcement actions |

| Stablecoin | Payments, settlement, on/off-ramp bridge to fiat | Low if peg holds | None directly; issuer profits from reserves | Increasing clarity for permitted issuers under laws like the GENIUS Act |

This comparison highlights why memecoins are both alluring and problematic. They offer enormous upside potential in short windows but lack both cash-flow support and regulatory clarity. Stablecoins, by contrast, may never 100× in price but are steadily gaining legal and institutional acceptance. For traders and policymakers alike, memecoins and stablecoins represent opposite ends of the crypto spectrum: one dominated by narrative volatility, the other by regulatory integration.

Memecoins Versus “Serious” Crypto: Value, Use Cases, And Critiques

A recurring question in every crypto cycle is whether memecoins are an embarrassment or a feature—whether they dilute crypto’s credibility or represent an authentic expression of internet-native culture and risk-taking. The reality is more nuanced: memecoins can be simultaneously parasitic, symbiotic, and experimental in ways that challenge simple moral judgments.

From a critical perspective, the case against memecoins is straightforward. Most projects launch with no clear roadmap, no revenue model, and no plan to return value to holders beyond the hope that someone else will buy at a higher price later. Many are thinly veiled pump-and-dump schemes where insiders hold large pre-allocations, use viral marketing or celebrity endorsements to attract retail buyers, and then dump their tokens into the resulting liquidity. The average life expectancy of a small memecoin is short; most will never be listed on major exchanges or accumulate meaningful liquidity, and a significant portion will trend toward zero over time. Episodes like the RKC crash following social media deletions and developer sales reinforce the perception that memecoin markets are dominated by asymmetric information and insider moves.

Additionally, memecoins can impose negative externalities on their host chains. During peak mania, they can congest networks, drive transaction fees higher, and crowd out bandwidth that might otherwise be used for DeFi, gaming, or real-world asset applications. This has been a concern on chains like Solana, where memecoin activity via Pump.fun and similar platforms at times dominated blockspace and fee revenue. For developers building more infrastructure-like products, the sense that their chain is viewed primarily as a speculative casino can complicate enterprise partnerships and institutional adoption, even if the underlying technology is robust.

Yet the case for memecoins is not entirely frivolous. At a minimum, they serve as a pure expression of market discovery around cultural value. If a particular joke, symbol, or identity cluster is powerful enough to coordinate capital flows and sustained community engagement, that says something about what people care about in the digital age. Projects like the Vegas memecoin, which reportedly raised funding to expand licensed IP, original content, and esports-style tournaments for its community, hint at how memecoin-originated communities can evolve into broader entertainment ecosystems rather than remaining static tokens. Similarly, the emergence of interest in LGBT- or queer-themed memecoins reflects a desire by some groups to see their identities and values reflected in the symbols they trade and rally around, even if the economic structures remain risky.

In some cases, memecoins act as proto-social tokens, where holding the token is a form of membership in a club with its own rituals, language, and sometimes offline events. Trump’s exclusive galas for top TRUMP holders, where token holdings or merch purchases effectively gate access to in-person experiences, are an example of this logic applied to politics. Other projects host esports tournaments, conferences, or meetups funded by token treasuries. The boundaries between speculation, fandom, and patronage blur: buying a memecoin might be partly an investment, partly a social signal, and partly a ticket to participate in a specific subculture.

Critics would argue that similar community experiences could be built with more sustainable tokenomics or even without tokens at all, and in many cases they are right. But memecoins have one advantage that is difficult to replicate: they offer instant, liquid, and globally accessible exposure to a shared narrative. Someone in Seoul, Lagos, and São Paulo can all buy into the same meme in seconds, with transparent on-chain records and the ability to exit at any time, for better or worse. That liquidity—even if thin—encourages participation in ways that non-tradable community badges or memberships might not.

The regulatory and ethical challenge is to allow for this kind of cultural experimentation without letting predatory behavior go unchecked. Cases like the CatFi rugpull prosecution in South Korea, the MOTHER lawsuit, and Senator Gillibrand’s push for ethics provisions tied to political memecoins all suggest that authorities are moving toward a world where memecoins are neither banned outright nor left entirely in a legal gray zone. Instead, they are likely to be subject to stricter rules around marketing, disclosures, conflicts of interest, and perhaps even suitability criteria for certain kinds of investors.

For individual traders and communities, the practical implication is clear: treat memecoins as high-risk, entertainment-first assets. That means position sizing appropriately, avoiding leverage unless fully prepared for total loss, and recognizing that most memecoin narratives will fade long before the broader crypto market does. It also means adopting a skeptical mindset toward promises of “utility” bolted onto existing memecoins after the fact, especially when those promises involve complex revenue-sharing, staking, or real-world business tie-ins with little track record. In a domain where the consensus expectation is chaos, prudence is not cynicism; it is survival strategy.

Finally, memecoins must be understood in relation to the quieter, more structural changes happening elsewhere in crypto—particularly around stablecoins, institutional adoption, and regulatory frameworks. As stablecoins gain legal recognition as payment instruments under laws like the GENIUS Act and banks explore issuing or integrating them into existing systems, crypto is slowly embedding itself into the plumbing of global finance. At the same time, memecoins remind the world that crypto’s roots are in open, permissionless, sometimes anarchic experimentation. The tension between these two visions—crypto as systemic infrastructure and crypto as chaotic playground—is unlikely to disappear. Memecoins are where that tension is most visible.

FDV vs. float distortions on political launches like $TRUMP routinely overstate market caps by 5x or more, with no mandatory disclosure or correction mechanism.

U.S. senators explicitly tied memecoin ethics provisions to the passage of broader crypto legislation, making political memecoins a direct chokepoint for the entire industry's regulatory path.

Solana recorded $39M in net outflows driven directly by declining memecoin trading volume, demonstrating how rapidly chain-level liquidity collapses when the meme cycle reverses.

Five-minute issuance via Pump.fun, Vyper/boa, and tweet-to-launch tools eliminates technical barriers to both creation and rug pulls, contributing to over $500M in reported 2024 losses.

Pump.fun accounted for over one-third of Solana's Q1 revenue, concentrating memecoin issuance within a single gatekeeper whose policy decisions cascade across the ecosystem.

Class-action suits against Iggy Azalea and a dismissed case against Caitlyn Jenner reflect an unsettled legal standard for celebrity token promotion that leaves promoters and buyers in regulatory limbo.

Conclusion

Memecoins occupy a paradoxical place in the crypto landscape. They are at once the most derided and the most magnetic assets, drawing in newcomers with the promise of life-changing gains while exasperating builders who see them as distractions from deeper innovation. Historically, from Dogecoin through SHIB and into the Solana era of WIF, PEPE, BONK, and countless short-lived experiments, memecoins have functioned as highly volatile instruments that track not fundamentals but the ebb and flow of collective attention. Their trajectories illustrate how culture, narrative, and market structure interact on-chain: a viral meme can become a billion-dollar market cap in days, yet that same market cap can evaporate just as quickly when the joke gets old or insiders sell.

Platforms like Pump.fun have industrialized the memecoin launch process, lowering technical barriers and turning early-stage liquidity into algorithmic bonding curves that feed back into network revenues. For networks like Solana, this has created periods where memecoin activity drives a substantial share of fees and economic activity, raising both upside and systemic risk. Regulatory systems are responding in kind, with cases like CatFi’s rugpull prosecution and the JENNER and MOTHER lawsuits beginning to sketch the legal boundaries for what memecoin promoters can and cannot do. Political entanglements, including Trump-linked tokens and Senator Gillibrand’s insistence on ethics provisions tied to such relationships, further demonstrate that memecoins are no longer a sideshow but a factor in mainstream policy debates.

For investors, the lesson is not to ignore memecoins—they are too central to crypto market cycles for that—but to contextualize them. Memecoins are best understood as speculative cultural derivatives: expressions of collective mood that can yield outsized gains for a few, losses for many, and valuable information about what narratives are resonating at a given moment. In contrast, assets like Bitcoin, Ether, and regulated stablecoins represent longer-term bets on monetary systems, computation, and payment infrastructure. Both sides are part of the same story, but they play very different roles, and confusing one for the other can be costly.

Ultimately, the health of the crypto ecosystem will not be judged by whether memecoins disappear—they will not—but by whether the industry can channel the energy they represent into more durable forms of innovation and value creation. That means building better consumer protections, clearer regulatory frameworks, and more honest communication around risk, even as the next viral meme token inevitably launches and captures the spotlight.

Outlook

Looking ahead, memecoins are likely to remain a permanent, if cyclical, fixture of crypto markets. Each major bull run will probably anoint one or two flagship memecoins as symbols of the era, while thousands of others fade into obscurity or outright scams. Chains with low fees and fast finality, such as Solana, will continue to be fertile ground for this activity, and platforms like Pump.fun—or their successors—will iterate on launch mechanisms, fees, and social features. At the same time, increasing regulatory scrutiny, from rugpull prosecutions to ethics provisions tied to political memecoins, will constrain some of the more egregious behavior and possibly drive activity toward jurisdictions and platforms that balance innovation with investor protection.

For serious builders and long-term investors, the challenge will be to harness the onboarding and engagement benefits of memecoins without letting speculative manias define the narrative of what crypto can be. As stablecoins and institutional use cases quietly integrate crypto into mainstream finance under clearer legal frameworks, memecoins will likely continue to serve as both a release valve for speculative excess and a laboratory for new forms of community-building. Navigating the next cycle will require recognizing memecoins for what they are: powerful cultural instruments and risky financial products, demanding both respect for their influence and caution toward their claims.

Latest Memecoins news

Crypto enters its “Graham era” as looming U.S. market structure laws could unlock value-accruing tokens, shifting investors from memecoin speculation toward fundamentalsPump.fun offers up to $5M annual compensation for a chief legal officer as the Solana memecoin giant navigates lawsuits, global regulation, and mounting compliance demandsSources

- https://www.cfx.co.id/en/news/popular-memecoin-2025

- https://id.tradingview.com/news/cointelegraph:22f3cd122094b:0-pump-fun-accounts-for-over-one-third-of-solana-s-q1-revenue-despite-memecoin-slowdown/

- https://x.com/WuBlockchain/status/2066989377797206343

- https://id.tradingview.com/news/cointelegraph:0b8b5ea52094b:0-trump-s-official-memecoin-extends-slide-as-he-hosts-exclusive-investor-gala/

- https://www.securitiesdocket.com/2026/05/07/sen-gillibrand-no-crypto-bill-without-ethics-provision-amid-president-trumps-ties-through-memecoins-world-liberty-the-block/

- https://id.tradingview.com/news/cointelegraph:dc29c43d9094b:0-caitlyn-jenner-escapes-memecoin-lawsuit-as-judge-says-token-not-a-security/

- https://id.tradingview.com/news/cointelegraph:39269b11a094b:0-iggy-azalea-faces-class-lawsuit-over-mother-memecoin/

- https://x.com/cryptounfolded/status/2059560046254604567

- https://id.tradingview.com/symbols/MYXUSDT/markets/

- https://www.solflare.com/ecosystem/pump-fun-where-memes-meet-markets-on-solana/

- https://www.instagram.com/p/DZTGu8wEwQD/

- https://x.com/VitalikButerin/status/2054105653988270113

- https://bitcoinfoundation.org/news/altcoins/top-sol-tokens-dominating-the-market-solana-memecoins-pumping-again/

- https://cryptorank.io/news/feed/e2fe0-ordinals-browser-ord-io-shutdown-june-1

- https://www.fintechweekly.com/magazine/articles/stablecoins-mainstream-payments-genius-act-2026

- https://predict.fun/learn/what-is-prediction-market

- https://en.wikipedia.org/wiki/World_Liberty_Financial

- https://www.ccn.com/education/crypto/roaring-kitty-linked-memecoin-crashes-67-viral-x-post/

- https://x.com/MYX_Finance/highlights

Community notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…