In-depth explainer on Polymarket, the USDC-based crypto prediction market: how its yes/no event contracts work, where it fits alongside Kalshi and Schwab’s binary options, and why regulators from the CFTC to Kentucky are circling the fast-growing sector.

+64 sources across the wider coverage universe

White House warns staff against Iran war bets after Polymarket traders net $600K on ceasefire timing2026-04

White House warns staff against Iran war bets after Polymarket traders net $600K on ceasefire timing2026-04 Astaria announces launch of 100x leveraged trading on Polymarket, introducing high-risk prediction market exposure with waitlist now open ahead of official rollout2026-04

Astaria announces launch of 100x leveraged trading on Polymarket, introducing high-risk prediction market exposure with waitlist now open ahead of official rollout2026-04 Polymarket paid creators to stage $900K in fake winning bets on cloned sites, courting American users it's banned from serving2026-06

Polymarket paid creators to stage $900K in fake winning bets on cloned sites, courting American users it's banned from serving2026-06 Polymarket launches $5M bug bounty on Cantina, exposing full-stack prediction market infra including smart contracts, oracles, and web app to security researchers2026-04

Polymarket launches $5M bug bounty on Cantina, exposing full-stack prediction market infra including smart contracts, oracles, and web app to security researchers2026-04 CFTC Chair Michael Selig says prediction markets like Polymarket outperform polls and help fight fake news, urging US rules to support innovation and keep jobs onshore2026-04

CFTC Chair Michael Selig says prediction markets like Polymarket outperform polls and help fight fake news, urging US rules to support innovation and keep jobs onshore2026-04 Crypto.com enters prediction markets via High Roller partnership, targeting $1T opportunity and challenging platforms like Kalshi and Polymarket with US-based event contracts2026-04

Crypto.com enters prediction markets via High Roller partnership, targeting $1T opportunity and challenging platforms like Kalshi and Polymarket with US-based event contracts2026-04

Polymarket: Crypto-Native Prediction Markets Explained

Polymarket is a crypto-based prediction platform where users trade on the outcomes of real-world events using yes/no contracts priced in stablecoins, effectively turning questions about politics, sports, economics, and geopolitics into markets that resemble event-based binary options. Operating at the intersection of decentralized finance and regulated derivatives, Polymarket has grown into what it markets as the world’s largest prediction market, drawing attention not only from traders and crypto users but also from regulators, traditional brokerages, and policymakers worldwide.

What Is Polymarket?

At its core, Polymarket is an exchange-like platform where people buy and sell shares in the outcome of future events, with each share settling to a fixed payoff—typically one US dollar—if the specified outcome occurs, and zero otherwise. The price of each share fluctuates between 0 and 1 USDC, which traders interpret as an implied probability that the event will occur, making the platform a live, market-driven forecast of everything from election results to sports scores and diplomatic breakthroughs. From the perspective of US derivatives law, the Commodity Futures Trading Commission (CFTC) has described these instruments as “event-based binary options contracts,” a classification that carries important regulatory implications for how and where they may legally be offered. According to the CFTC, Polymarket has been operating such event markets since at least June 2020, during which time it grew into a prominent venue for off-exchange binary options trading before coming under federal scrutiny.

Unlike traditional sportsbooks or centralized bookmakers, Polymarket does not set odds directly but instead provides an order book where users trade with one another, with prices emerging from the balance of supply and demand. If a “Yes” share trades at 0.64 USDC, that implies an approximate 64% market-implied probability that the event will resolve in favor of the “Yes” outcome, assuming no arbitrage and efficient pricing. Since each contract ultimately pays either 1 or 0 USDC at settlement, traders can use Polymarket both to express views and to hedge specific risks, such as geopolitical conflict, macroeconomic releases, or election outcomes. This market-based probability mechanism has made prediction markets an object of interest for economists and social scientists, who see them as tools for aggregating dispersed information in a transparent and quantitative form.

Polymarket positions itself explicitly as a crypto-native platform, relying on stablecoins and public blockchains rather than bank transfers or traditional brokerage accounts. Most trading on the global product takes place using USDC on the Polygon network, which offers low transaction fees and fast confirmation times, making it suitable for relatively small, frequent trades that are common in prediction markets. The platform has also developed a separate US-facing business, sometimes referenced in litigation and filings as “Polymarket’s US division,” which reflects the need to tailor offerings to the fragmented and evolving regulatory landscape in the United States. This dual character—as both a decentralized, global protocol and a company dealing with US regulators—shapes many of the debates around Polymarket’s future.

Polymarket paid creators to stage $900K in fake winning bets on cloned sites, courting American users it's banned from serving

70% of the 1,100 WSJ-reviewed clips being shot on dummy Polymarket UIs lands on the same weak spot as the recent Ghost Fills paper: most of the trust surface sits off-chain, from creator funnels to CLOB matching, while Polygon only sees whatever survives to settlement. If regulators are already looking at 1.95M reverted match-order txs and $1.49M in extractable profit, staged wins aimed at U.S. users turn “transparent markets” into a much harder sell. Kalshi and the CFTC side can now frame this as consumer protection instead of anti-crypto panic.

Readers click Polymarket coverage not for gambling mechanics but for what the odds reveal that official sources hide — insider war-strike positioning, Biden's exit before the announcement, and ETF approval windows — treating it as a shadow intelligence feed rather than a betting product.↗

Prediction Markets 101: Context And Theory

To understand Polymarket, it is helpful to first situate it within the broader history and theory of prediction markets. A prediction market is an exchange where individuals trade contracts whose payoff depends on the outcome of a future event, such as whether a candidate wins an election or whether a particular economic indicator exceeds a threshold by a certain date. The simplest and most common format is the binary option, which pays a fixed amount if the event occurs and zero otherwise, allowing prices to be interpreted directly as probabilities under standard no-arbitrage assumptions. For example, if a contract on “Candidate A wins the election” trades at 0.70, that suggests traders collectively assign about a 70% chance to that outcome, given the information and risk preferences embedded in the order book.

Economists have long argued that prediction markets can function as efficient aggregators of dispersed information, because participants with private insights or strong views have direct financial incentives to trade until prices reflect their information. This idea has been tested both in public markets, such as election prediction exchanges, and in private corporate settings, where companies like Google have run internal markets to forecast product launches, sales milestones, and other key performance indicators. At Google, an internal prediction platform called Prophit was studied over its first two and a half years, and research by Cowgill and coauthors found that the market’s forecasts displayed high calibration—meaning events forecast with 70% probability occurred about 70% of the time—while also improving as participants gained experience. Those findings support the notion that even relatively small, self-selected communities can generate probabilistic forecasts comparable to or better than conventional polling or expert opinion.

At the same time, prediction markets straddle conceptual and legal boundaries between “information markets” and gambling. From a mathematical perspective, trading a binary option on an election or sports match looks very similar to placing a bet with a bookmaker, in that both involve staking capital on uncertain outcomes with payoff odds determined by perceived probabilities. Yet the academic literature has emphasized their value in revealing collective beliefs, enabling corporate planning, and even guiding public policy, which has led some advocates to argue that prediction markets should be legally distinguished from gambling and instead treated as a form of regulated derivatives or research infrastructure. Regulators, however, have been cautious, particularly when markets touch politically sensitive topics such as elections, terrorism, or public health, or when retail users can potentially sustain large losses without robust consumer protections. Polymarket sits squarely in this contested space, showcasing both the informational potential of prediction markets and the regulatory risks they pose.

The Polymarket Platform: Design, Mechanics, And Fees

Trading Structure And Market Design

Polymarket’s trading mechanics are built around simple yes/no event contracts, each linked to a clearly specified question and resolution criteria. A typical market might ask whether a peace deal between two countries will be signed by a certain date, whether a specific stock will reach a target valuation, or whether a team will win a tournament, with the market description outlining precisely what counts as a “Yes” outcome. Traders can buy “Yes” or “No” shares, each representing a claim on 1 USDC if that outcome occurs and 0 if it does not, and can freely trade in and out of positions before resolution, capturing profits from changing probabilities. Because contracts are fully collateralized using stablecoins, settlement is straightforward: once the market resolves, winning shares are redeemable for their full face value, while losing shares expire worthless.

Under the hood, Polymarket runs an order book where users can post limit orders to buy or sell shares at specific prices, or execute immediate trades at the best available prices, mirroring the structure of a traditional exchange. This design allows for tighter spreads and deeper liquidity in popular markets, while still supporting niche questions with smaller but active order books, such as highly specific geopolitical or cultural events. Markets operate continuously, with prices adjusting in real time to incorporate new information, news events, and trading flows, making Polymarket a continuous barometer of crowd sentiment across a wide range of topics. For many traders, the appeal lies not only in potential profits but also in the ability to see and act on collective beliefs before they show up in more traditional indicators like polls or analyst forecasts.

Although Polymarket is often associated with decentralized finance, the user experience is closer to a hybrid model that combines on-chain settlement with a relatively streamlined web or app interface. Users can connect via wallet integrations such as MetaMask, which offers direct in-app access to Polymarket’s global prediction markets for users outside the United States, or they can access the platform through partner sites that integrate its markets, illustrating how Polymarket functions both as a front-end exchange and as back-end infrastructure for other applications. This composability is a hallmark of crypto-native systems, enabling prediction markets to be embedded in wallets, gaming platforms, and community portals while still settling trades on a shared, transparent ledger.

USDC, Polygon, And On-Chain Settlement

One of the defining design choices of Polymarket is its reliance on the USDC stablecoin and the Polygon network for most trading activity. USDC is a dollar-pegged stablecoin, so denominating contracts in USDC minimizes the exchange-rate risk that would otherwise arise if contracts were settled in more volatile cryptocurrencies like ETH or MATIC. Polygon, a layer-2 scaling solution for Ethereum, offers lower gas fees and faster confirmation times than the Ethereum mainnet, making it practical for users to place frequent, relatively small trades without incurring prohibitive transaction costs. According to Polymarket’s own fee documentation, deposits and withdrawals in USDC on Polygon are not subject to platform fees, and gas costs on that network are typically negligible compared to layer-1 Ethereum.

Polymarket only allows trading using USDC, which simplifies accounting and reduces the cognitive load for users, who can think directly in dollar terms when evaluating potential returns and risks. Funding an account with USDC via Polygon incurs minimal network costs and no additional platform fee, whereas funding via other coins or networks may involve gas fees and third-party charges from providers like Coinbase or MoonPay, depending on the route chosen. Withdrawals are also executed in USDC, allowing users to hold their winnings in a relatively stable asset or transfer them to other platforms and wallets without immediately facing market volatility. This focus on stablecoins aligns with a broader trend in decentralized finance, where stable denominations are preferred for derivative-like products that depend on probabilistic payoffs rather than speculative appreciation.

Although Polymarket’s settlement infrastructure is crypto-native, many users access it through interfaces that abstract away some of the complexities of on-chain interaction. MetaMask, for example, offers a dedicated prediction markets experience where users can fund a predictions account with any EVM-compatible token or trade directly using top tokens from their wallet, before routing the underlying settlement through Polymarket’s contracts. Similarly, BC.GAME, an online gaming and casino platform, has integrated Polymarket as the backend for its new Prediction Center, allowing BC.GAME users to access sports, crypto, and real-world event markets powered by Polymarket’s liquidity and pricing without needing to interact directly with smart contracts. These integrations underscore how USDC and Polygon-based settlement can be embedded in a variety of front-end experiences, extending Polymarket’s reach beyond its own website.

Fees, Maker Incentives, And Market Categories

Polymarket’s fee structure is designed to strike a balance between competitive costs for active traders and incentives for liquidity provision across many markets. According to its published fee schedule, Polymarket charges very small trading fees, and only on certain categories of markets, while leaving others—most notably geopolitical and world-event markets—free of explicit trading fees. The platform describes itself as a crypto-based prediction market that uses USDC for trades, and emphasizes that deposits and withdrawals via USDC on Polygon incur no additional platform fees, meaning users can enter and exit the ecosystem without facing direct charges from Polymarket itself.

Within the trading environment, Polymarket distinguishes between “makers,” who add liquidity by posting limit orders, and “takers,” who consume liquidity by executing trades against existing orders, and it applies fees only to takers. The taker fee is expressed as a percentage of the price of the contract share multiplied by the number of shares traded, with different categories of markets subject to different maximum rates. Published figures indicate that taker fees can range up to 1.8% of the contract price at mid-range probabilities, with the highest fees applying to event contracts priced around 0.50 USDC, corresponding to a 50% implied chance of occurrence. By contrast, contracts priced at 0.25 and 0.75 USDC have lower effective fees, and makers who place limit orders do not pay trading fees at all but may instead receive rebates through Polymarket’s liquidity incentives program.

The fee documentation points to a variety of market categories that are currently charged fees and qualify for maker rebates, including crypto, sports, finance, politics, economics, culture, weather, tech, mentions, and other or general markets. Geopolitical and world event contracts, however, are explicitly exempt from trading fees on the platform, reflecting both their popularity and perhaps a strategic decision to promote trading in markets that showcase Polymarket’s informational value. All trading fees collected are used to reward traders who provide liquidity and help keep pricing competitive and balanced across the platform, effectively recycling fees into maker rewards to sustain active markets in both popular and niche topics. This fee-and-rebate structure aligns with broader exchange industry practices, where maker-taker models are used to incentivize order book depth and tighter spreads.

Market Resolution, Disputes, And The Role Of Oracles

Because Polymarket’s contracts are tied to real-world events, market resolution is a central and sometimes contentious aspect of the platform’s operation. According to Polymarket’s help documentation, resolving a market begins with a “proposal” in which an outcome is suggested along with supporting evidence, and the proposer must post a bond in USDC.e that will be forfeited if the proposal is ultimately deemed incorrect. This bond serves both as a spam deterrent and as a way to align the proposer’s incentives with accurate, good-faith interpretation of the market’s resolution criteria. If no one disputes the proposed outcome within a defined window, the market resolves to that outcome, and winning shares pay out accordingly; if a dispute is raised, additional rounds may follow, potentially escalating to a final resolution by designated arbitrators or oracles depending on the platform’s governance procedures.

The resolution process is meant to ensure that markets settle in a way that is consistent with their pre-defined rules and with verifiable public information, but high-stakes or ambiguous events can generate significant controversy. A prominent example is the U.S.–Iran permanent peace deal market, which asked whether Iran and the United States would agree to a permanent peace deal by a specified date, with resolution depending on whether certain diplomatic developments met that standard. As reports emerged of a potential deal to end hostilities and ease tensions, equities and bond markets reacted positively, while Polymarket traders engaged in intense debate over whether the reported arrangements satisfied the “permanent peace deal” conditions spelled out in the market. At one point, the market had attracted more than $120 million in trading volume and eventually rose above $345 million in cumulative trading, making it one of Polymarket’s largest and most contentious markets.

When Polymarket’s operators or community members proposed a resolution for the Iran peace market, some traders disputed the determination, arguing that the specific diplomatic steps taken did not meet the precise wording of the question, prompting the market to enter a formal dispute process. This episode illustrates both the power and the fragility of event-based markets: they can quickly become focal points for public discussion and financial hedging around major geopolitical developments, but they also depend heavily on careful market design and unambiguous resolution criteria to avoid perceived unfairness. Users who do not read the fine print or misunderstand how resolution will be determined may find that seemingly obvious outcomes do not translate into expected payouts, as highlighted by cases in which traders have seen large apparent gains evaporate when markets resolve contrary to their expectations. For Polymarket, maintaining confidence in the resolution process—through transparent rules, dispute mechanisms, and credible oracles—is critical to the platform’s long-term viability.

Access, KYC, And Geographic Restrictions

Access to Polymarket is shaped by a patchwork of regulatory requirements, platform policies, and third-party risk controls. Historically, one of the attractions of on-chain prediction markets was the ability for anyone with a compatible wallet to participate pseudonymously, but this model has come under increasing pressure as regulators and service providers seek to curb fraud, money laundering, and unlicensed gambling. MetaMask’s promotional materials emphasize that it offers in-app mobile access to Polymarket’s global prediction markets outside of the United States, with no know-your-customer (KYC) checks required, allowing users to fund prediction accounts with various EVM-compatible tokens. However, more recent reporting indicates that Polymarket has tightened its own rules by introducing mandatory KYC for active traders and warning that the use of VPNs or other methods to obscure jurisdiction can lead to account suspension.

According to coverage by the Bitcoin Foundation, Polymarket has implemented mandatory KYC for active users and has blocked its platform in 35 countries, reflecting both regulatory constraints and internal risk management decisions. The same report notes that traders who attempt to access the platform via VPNs may face account restrictions or suspension, as Polymarket seeks to ensure that it can enforce jurisdictional compliance and prevent abuse. These measures align with broader industry trends, where even ostensibly decentralized platforms are under pressure from regulators, payment providers, and banking partners to adopt more conventional compliance practices, including identity verification and monitoring of suspicious activity. For users, this means that participation in prediction markets increasingly requires not only a wallet and stablecoins, but also a willingness to undergo KYC and abide by country-specific restrictions.

In some jurisdictions, interaction with Polymarket can trigger additional consequences beyond the platform itself. A Japanese crypto exchange, Bitbank, has warned its users that on-chain activity linked to Polymarket and similar prediction markets could lead to account suspension, framing such activity as potentially incompatible with its own compliance obligations. In effect, Bitbank is signaling that users who send funds to or receive funds from Polymarket-related addresses may be seen as engaging in unlicensed gambling or high-risk activity, even if Polymarket itself is not directly regulated in Japan. These kinds of warnings illustrate how prediction market participation can be constrained not only by the platforms and regulators directly involved, but also by intermediaries like exchanges and wallet providers that impose their own risk appetites and policy interpretations.

- 01token launch airdrop farming↗

Speculation about a POLY airdrop drove readers to farm positions early, making the launch itself a tradeable meta-event before any token existed.

- 02election market dominance

Polymarket's presidential betting volumes approaching $1B made it a credibility test for whether prediction markets could outforecast pollsters, pulling in readers who wanted a real-time signal on the race.

- 03regulatory crackdown pressure↗

The CFTC, FBI raid on the CEO, Singapore ban, and Senate push to outlaw election betting layered into a sustained existential threat narrative that kept readers returning across many news cycles.

- 04oracle dispute manipulation↗

UMA's role as the resolution layer — susceptible to whale manipulation and at odds with media consensus on events like the Zelenskyy suit market — revealed a structural vulnerability readers found more alarming than any smart-contract risk.

- 05insider trading war markets↗

Freshly funded wallets netting $1M on Iran airstrikes and the White House warning staff off ceasefire bets made geopolitical markets a proxy for detecting state-level information advantages.

- 06AI and oracle integrations

Partnerships with Perplexity, EigenLayer, and Pyth positioned Polymarket as infrastructure rather than a standalone app, attracting readers tracking the composability stack being built around prediction data.

Use Cases And Notable Polymarket Markets

Geopolitics And The U.S.–Iran Peace Deal

One of the most high-profile examples of a Polymarket market intersecting with real-world policy debates is the U.S.–Iran permanent peace deal contract. The market’s core question is whether Iran and the United States will agree to a permanent peace deal by a specified date, with resolution depending on the existence of a clearly defined, verifiable agreement. At various points, particularly during periods of diplomatic negotiation, this market attracted enormous trading interest, with cumulative volume exceeding $120 million and later reaching more than $345 million as traders and observers sought to price the chances of a durable diplomatic breakthrough. For traditional financial markets, news of a possible reduction in tensions between the two countries has moved equities and bond prices, while on Polymarket the same developments are distilled into an explicit, quantitative probability reflected in the price of the “Yes” and “No” contracts.

The Iran peace market also illustrates how contingent and contested real-world definitions can be when translated into binary financial contracts. The phrase “permanent peace deal” is politically and legally loaded, and determining whether a specific set of agreements or de-escalation measures qualify as such can require interpretive judgments that go beyond simple factual verification. When reports emerged of a proposed deal that would reduce hostilities, traders debated whether the arrangement met the market’s resolution criteria, with some arguing that the deal fell short of a formal, permanent peace treaty, while others believed it satisfied the market’s wording. As Polymarket’s resolution and dispute system was invoked, the market became a case study in the importance of precise question design and clearly stated resolution sources, both to minimize ambiguity and to set expectations for how borderline cases will be handled.

For policymakers and observers, the Iran peace market underscores both the promise and the potential pitfalls of using prediction markets to inform public discourse. On one hand, it provided a continuous, crowd-sourced probability estimate of an event that is otherwise difficult to quantify, potentially offering insights that complement diplomatic analysis and expert commentary. On the other hand, the market’s large size and high visibility meant that any perceived mis-resolution or unfairness could damage trust not only in Polymarket but in prediction markets more generally, especially if substantial sums were at stake. As prediction markets move into more sensitive geopolitical territory, their operators must grapple with these reputational and ethical stakes, ensuring that the mechanics of market design, resolution, and dispute handling are robust enough to support the weight of real-world consequences.

Sports, World Cup Shocks, And Million-Dollar Swings

Sports have been a natural fit for prediction markets, and Polymarket has hosted an array of markets on major tournaments, league outcomes, and individual match results. During international football competitions, for example, Polymarket’s volumes have surged as traders speculate on match winners, group standings, and tournament champions, turning each game into a series of tradable probabilities that update in real time. Upsets and surprise results can produce dramatic swings in market prices and trader fortunes, as expectations built into the odds are abruptly revised in light of on-field events. In at least one widely reported case, a shock draw between the Republic of the Congo and Portugal in a major tournament resulted in a Polymarket bettor winning $1 million, illustrating how large, concentrated positions on perceived long shots can pay off when improbable outcomes occur.

Such episodes highlight both the excitement and the risk inherent in event-based trading. For traders who are skilled at identifying mispriced odds or who have access to superior information, Polymarket offers opportunities to profit from contrarian views, much as traditional sportsbooks do. However, the same dynamics mean that users who overestimate the certainty of favorites or fail to diversify their positions can incur large losses when upsets occur, particularly if they treat probabilities as certainties rather than as risk-weighted expectations. The visibility of seven-figure wins and losses in sports markets can also have ambiguous effects on user behavior, potentially normalizing high-stakes trading and encouraging risk-taking in pursuit of similar windfalls, a phenomenon that concerns regulators and consumer protection advocates.

From a market design standpoint, sports markets tend to be relatively straightforward to resolve, since outcomes are clear, time-bounded, and well documented, which reduces the scope for disputes. This simplicity may explain why regulators like the Kentucky Attorney General have focused on sports-related markets when framing Polymarket and Kalshi as illegal sportsbooks, arguing that allowing users to place wagers on game winners, point spreads, and player statistics without a state gaming license amounts to unlicensed sports betting. For Polymarket, the challenge is that the same sports markets that drive engagement and volume are often the ones most likely to trigger gambling-related regulatory scrutiny, forcing the platform to navigate a delicate balance between user demand and legal risk.

Crypto, Tech, Finance, And Market Sentiment

Beyond politics and sports, Polymarket hosts numerous markets tied to crypto assets, technology companies, macroeconomic indicators, and other financial variables. According to its fee and category documentation, Polymarket charges taker fees—and offers maker rebates—in categories such as crypto, finance, tech, and economy, reflecting active trading in questions related to asset prices, monetary policy decisions, and corporate valuations. Markets might ask whether a particular token will exceed a specified market cap by a certain date, whether a central bank will cut interest rates at its next meeting, or whether a high-profile company will achieve a given valuation threshold, turning macro and micro financial questions into binary contracts that mirror the style of prediction markets. In this sense, Polymarket overlaps conceptually with more traditional derivatives markets, albeit often on nonstandard or more speculative underlyings.

These markets function both as speculative vehicles and as indicators of sentiment within specific communities. For example, markets on whether a major crypto project will launch a token by a certain date can provide a crowd-sourced view of developer timelines and community expectations, while markets on tech company valuations or IPO outcomes can reveal investor beliefs about future growth and regulatory risk. In some cases, market-implied probabilities may even feed back into decision-making by the actors involved, as project teams and corporate managers observe how the crowd interprets their plans, although empirical evidence on such feedback loops remains limited. By offering a common interface for trading on crypto, tech, and traditional finance topics, Polymarket positions itself at the boundary between decentralized finance and conventional financial forecasting.

Culture, Weather, And Miscellaneous Events

Polymarket’s catalogs also include markets on cultural events, weather phenomena, and idiosyncratic “mentions” or general-interest questions, as reflected in the fee schedule’s enumeration of categories such as culture, weather, mentions, and other/general. These markets can range from questions about whether a particular film will win an award to whether a notable public figure will make a specific announcement by a given date, as well as meteorological events like temperature thresholds or storm impacts in particular locations. While such markets may attract smaller volumes than major political or sports markets, they serve to broaden the platform’s appeal and illustrate the flexibility of the prediction market format, which can be applied to almost any verifiable yes/no question.

For researchers and observers, these diverse markets offer a window into public interest and attention, as the topics that gather significant liquidity often reflect broader trends in media coverage and social conversation. At the same time, the inclusion of offbeat or whimsical markets underscores that Polymarket is not purely a tool for sober forecasting, but also a venue for entertainment and expressive trading, where users can stake small amounts on events they find intriguing or amusing. This blend of serious and playful markets complicates the task of regulators who seek to classify prediction platforms as either information tools or gambling venues, since in practice they are often both at once.

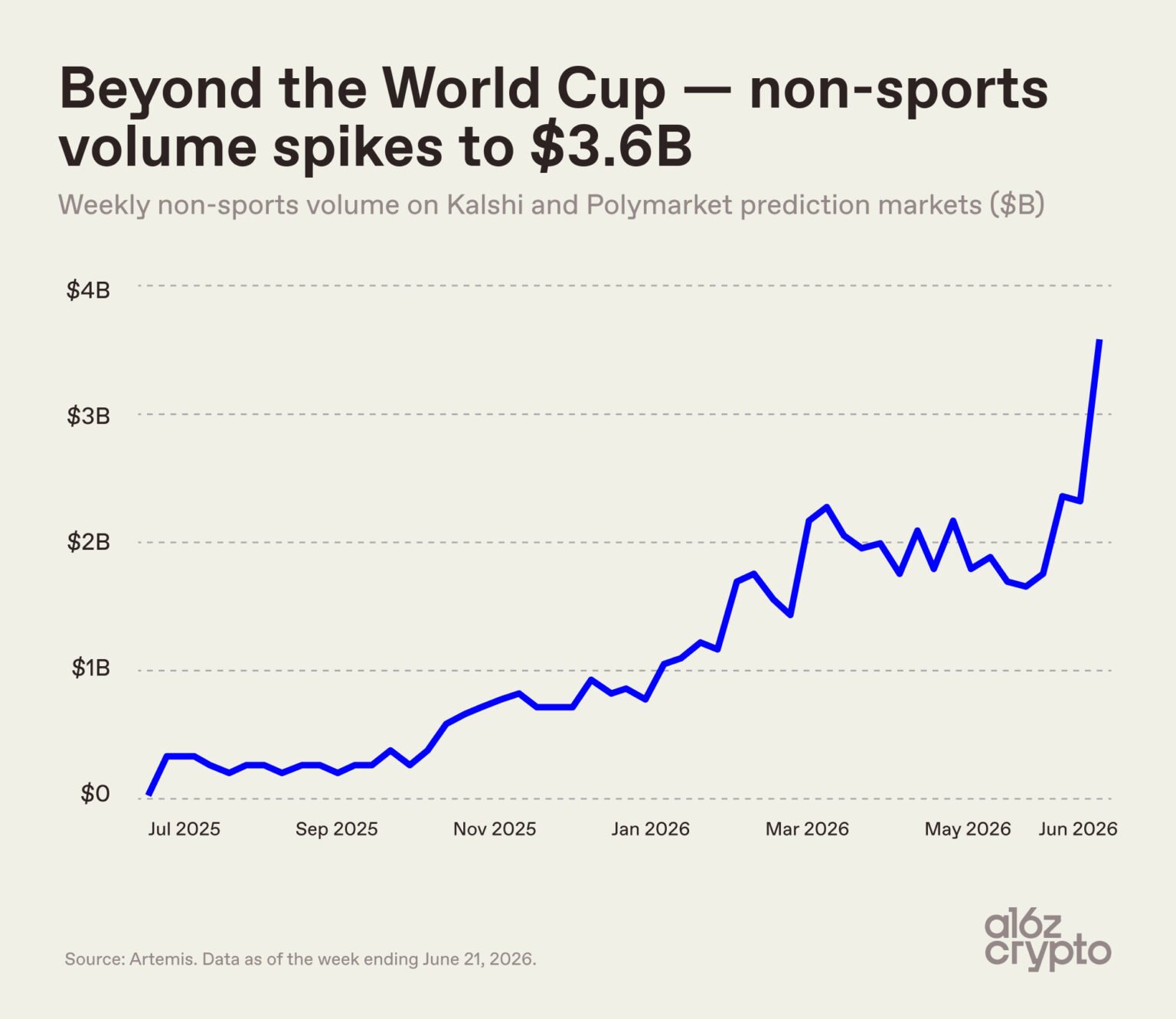

Kalshi and Polymarket non-sports volume hits $3.6B in a week, up 18x since July

a16z crypto says Kalshi and Polymarket cleared $3.6B of non-sports prediction-market volume last week across politics, economics, geopolitics, and current events. That category was around $200M per week in July 2025, so the move is roughly 18x in under a year. World Cup markets may be sucking oxygen, but the sharper signal is that non-sports prediction markets are turning into the real growth engine.

Regulation, Enforcement, And Legal Uncertainty

CFTC Enforcement And The 2022 Settlement

Polymarket’s rapid growth has unfolded under increasing regulatory scrutiny, particularly from the U.S. Commodity Futures Trading Commission. In early 2022, the CFTC announced an order filing and settling charges against Blockratize, Inc., doing business as Polymarket, for offering off-exchange event-based binary options contracts without registration as a designated contract market (DCM) or swap execution facility (SEF). The order found that, beginning in approximately June 2020, Polymarket had been operating an illegal unregistered or non-designated facility for event-based binary options online trading contracts, referred to as “event markets,” in violation of the Commodity Exchange Act and applicable CFTC regulations. As part of the settlement, Polymarket was required to pay a $1.4 million civil monetary penalty and to wind down any markets on Polymarket.com that did not comply with the CEA and CFTC rules, while ceasing and desisting from further violations.

The CFTC’s actions underscored that event-based contracts, including those on elections, economic indicators, and other real-world outcomes, can fall within the definition of swaps or options subject to federal derivatives regulation. By offering such contracts to U.S. users without operating as a registered exchange or facility, Polymarket ran afoul of the CEA’s core requirements that trading in such instruments occur on regulated venues with appropriate oversight. The enforcement order did not attempt to shut down Polymarket entirely, but it did force the platform to restructure its operations, limiting U.S. access and ensuring that certain types of markets—particularly those involving sensitive topics—were no longer available to U.S. residents. In practice, this contributed to the emergence of a more clearly delineated “Polymarket US division,” which is separately referenced in subsequent litigation and regulatory disputes.

For the broader prediction markets ecosystem, the Polymarket settlement signaled that federal regulators are prepared to treat many event-based trading products as derivatives rather than mere entertainment, bringing them squarely within the jurisdiction of agencies like the CFTC. This stance complicates efforts to operate global, retail-facing prediction platforms from within the United States, and has led some projects either to geofence U.S. users or to pursue more laborious paths toward CFTC-regulated status, as in the case of Kalshi’s efforts to operate a federally designated event contracts exchange. It also raises difficult questions about how to draw lines between permissible informational markets and impermissible gambling or unlicensed derivatives, particularly in areas where U.S. law is unsettled.

State-Level Enforcement: Kentucky And Michigan

If federal regulators have primarily framed prediction markets as derivatives issues, some U.S. states have approached them through the lens of gambling and consumer protection. In June 2026, Kentucky Attorney General Russell Coleman announced three lawsuits against prediction market platforms Kalshi and Polymarket, along with a sweepstakes gambling platform and a cryptocurrency platform, accusing each of operating unlicensed and illegal sports betting and gambling services within the state. The lawsuits allege that Kalshi and Polymarket allow users to place wagers on game winners, point spreads, and player statistics, thereby functioning as sportsbooks that bypass the consumer protections and tax requirements mandated under Kentucky’s gambling laws. According to the complaints, these companies are doing business without Kentucky gaming licenses or compliance with state regulations, and their affiliated entities—including Coinbase, Robinhood, and Webull—allegedly offer users few or no resources to identify or seek help for gambling problems.

The Kentucky suits invoke multiple legal theories, including violations of the state’s Consumer Protection law, the Loss Recovery Act, and other gambling statutes, reflecting a broad-based attempt to categorize prediction markets as illegal gambling rather than as regulated derivatives platforms. The Attorney General’s public statements have been particularly pointed, describing Kalshi and Polymarket as “illegal sportsbooks” and arguing that multi-billion-dollar corporations and their legal entities “don’t pass the sniff test” when they claim not to be engaged in unlicensed betting. At the same time, Kentucky’s recently enacted Wagering Consumer Protection Act restricts sports wagering operating licenses to the state’s horse racing associations and explicitly prohibits licensed sports wagering operations from contracting with Kalshi or Polymarket, further entrenching a regulatory framework that favors incumbent operators.

Polymarket has also faced challenges at the state level in Michigan, where its U.S. division sought temporary protection against regulatory actions by state authorities. According to reporting from Bloomberg Law, Polymarket’s U.S. division failed to persuade a federal judge to reverse course and grant temporary relief, meaning Michigan regulators retained authority to pursue enforcement actions against the company. While details of the underlying state claims are less public than in Kentucky, the denial of an initial shield illustrates the vulnerability of prediction markets to state-level enforcement, even where operators attempt to structure their offerings in ways they believe are compliant with federal law. For platforms like Polymarket, this state-federal tension adds another layer of complexity to jurisdictional risk, particularly given the diversity of gambling and derivatives laws across U.S. states.

Taxation And The Kentucky Excise Tax Dispute

Beyond licensing and gambling classifications, Kentucky has also become a focal point in debates over taxation of prediction markets. In April 2026, the Kentucky General Assembly enacted what has been described as the nation’s first state-specific excise tax on prediction markets, imposing a 14.25% levy on prediction market operators’ transaction fees. Shortly thereafter, a coalition that includes Kalshi, Crypto.com, and Polymarket filed a lawsuit challenging the tax, arguing that it is discriminatory, unconstitutional, and preempted by federal law. The coalition, operating under the name Coalition for Fair Markets, contends that the new tax is significantly higher than the 9.75% tax imposed on wagers at horse tracks, favoring Kentucky’s incumbent gambling industry over newer prediction platforms.

The lawsuit further argues that no state currently levies a state-specific excise tax on derivatives transactions that take place on federally designated exchanges, and that Kentucky’s tax therefore represents an unprecedented and targeted burden on prediction markets. Kalshi, which operates as a CFTC-regulated event contracts exchange, has stated that taxing federally regulated markets in this manner would push users toward illegal platforms with no oversight or protections, undermining the policy goal of steering activity into transparent and supervised environments. From Polymarket’s perspective, the tax is problematic both as a direct financial burden on its transaction fees and as a signal that states may seek to treat prediction markets as a special category subject to higher tax rates than traditional gambling or derivatives.

Kentucky Attorney General Coleman has vowed to defend the excise tax and the state’s broader regulatory stance, framing the dispute in gambling terms and emphasizing the state’s right to regulate and tax betting within its borders. This clash illustrates how prediction markets now sit at the intersection of tax policy, gambling regulation, and derivatives law, with states exploring novel ways to both capture revenue from and constrain the growth of these platforms. For Polymarket and its peers, the Kentucky tax fight is both a practical issue and a symbolic one, as its outcome may influence how other states approach prediction markets in the future.

International Compliance, Exchange Risk, And Access

Outside the United States, Polymarket faces a patchwork of implicit and explicit regulatory constraints that shape both user behavior and platform strategy. As noted earlier, the platform has introduced mandatory KYC for active traders and has blocked access from 35 countries, reflecting an effort to navigate differing legal regimes and risk levels across jurisdictions. However, even where Polymarket itself remains accessible, local financial institutions and crypto exchanges may impose their own restrictions on users who interact with prediction markets. The Japanese exchange Bitbank, for example, has warned that on-chain activity linked to Polymarket and similar platforms may result in account suspension for its users, indicating that such activity is viewed as noncompliant or excessively risky under its policies.

Bitbank’s warnings highlight a broader phenomenon in which exchanges and financial intermediaries treat prediction market participation as a compliance risk, perhaps due to concerns about unlicensed gambling, money laundering, or regulatory scrutiny. For individual traders, this creates a layer of indirect regulation, where even if Polymarket is technically accessible from their country, they must consider the risk that their local exchange will cut off service if it detects transfers to or from prediction market smart contracts. In some cases, this may have a chilling effect on participation, particularly among risk-averse users or those who rely heavily on specific centralized exchanges for fiat on-ramps and off-ramps.

Polymarket’s global presence is also mediated by wallet providers and front-end integrators, such as MetaMask and BC.GAME, which must evaluate their own regulatory obligations when deciding whether to offer access to prediction markets. MetaMask’s decision to promote Polymarket access outside the United States signals a view that such markets can be accommodated within its risk framework for non-U.S. users, but that calculus may change as regulators in more jurisdictions issue guidance or enforcement actions. As a result, Polymarket’s international footprint remains dynamic, shaped by evolving laws, enforcement priorities, and risk management decisions across a distributed network of platforms and intermediaries.

Prediction Markets Versus Regulated Derivatives: Schwab, Cboe, And Kalshi

A key aspect of Polymarket’s legal and competitive landscape is the convergence between prediction markets and regulated derivative products offered by traditional financial institutions. Charles Schwab, one of the largest U.S. brokerages, is collaborating with Cboe Global Markets to introduce yes-or-no options tied to the performance of the S&P 500 index, a product structure that closely resembles prediction markets in its binary payoff and probability-like pricing. According to reporting based on sources familiar with the plan, these S&P 500 yes/no options would allow Schwab clients to take positions on whether the index reaches certain levels, effectively joining the cohort of platforms—including Coinbase, Robinhood, Polymarket, and Kalshi—that are building or offering products in a fast-growing sector centered on binary event trading.

Kalshi, meanwhile, has pursued a more explicitly regulatory path by operating as a U.S.-based, CFTC-regulated venue for event contracts, emphasizing its status as an American company regulated at home. In the Kentucky excise tax litigation, Kalshi has argued that state-specific taxes on derivatives transactions conducted on federally designated exchanges are discriminatory and preempted by federal law, seeking to insulate its markets from such state-level burdens. This posture stands in contrast to Polymarket’s more crypto-native origins and its earlier CFTC settlement, highlighting divergent strategies for operating prediction-like markets in the U.S. regulatory environment.

The emergence of Schwab- and Cboe-branded yes/no options further blurs the line between prediction markets and mainstream derivatives, suggesting that the core economic function of event-based trading is increasingly recognized and integrated into traditional finance. For regulators, this convergence raises questions about consistency: if binary, event-based contracts offered by regulated exchanges and brokerages are permissible and subject to standard derivatives oversight, under what conditions should on-chain platforms like Polymarket be treated similarly, and when should they instead be classified as gambling or unregistered derivatives venues? The answers will shape not only Polymarket’s future but also the broader integration of prediction markets into global financial infrastructure.

To summarize the different positions in the ecosystem, the following illustrative table contrasts Polymarket, Kalshi, and Schwab/Cboe’s S&P 500 yes/no options across a few dimensions, based on publicly available information:

| Platform | Core Product Type | Regulatory Posture / Venue Type | Funding / Settlement | Typical Users / Access Context |

|---|---|---|---|---|

| Polymarket | On-chain event-based binary options on diverse real-world outcomes (politics, sports, geopolitics, crypto, etc.) | Settled CFTC charges for unregistered off-exchange event markets; operates global on-chain platform with U.S. division navigating state and federal constraints | Primarily USDC on Polygon; crypto-native settlement with wallet integration | Global crypto users via wallets and partner platforms; access restricted in some countries; KYC for active traders |

| Kalshi | Event contracts on economic and other measurable events, positioned as regulated derivatives | Operates as a U.S.-regulated exchange for event contracts; emphasizes federal oversight in challenging state excise taxes | Fiat on-ramps and regulated account structure; conventional brokerage-like interface | U.S. users seeking regulated event-contract exposure with KYC and compliance requirements |

| Schwab / Cboe S&P 500 yes/no options | Yes-or-no options tied to S&P 500 index performance, similar in structure to prediction markets | Offered through major regulated brokerage and options exchange; integrated into existing derivatives framework | Traditional brokerage accounts and margin systems, settled in fiat-linked instruments | Mainstream retail and institutional brokerage clients using Schwab and Cboe platforms |

This comparison underscores that Polymarket operates in a markedly different institutional and regulatory context than its more traditional counterparts, even as the underlying economic logic of binary, event-based trading is increasingly shared across platforms.

CFTC consent order — $1.4M fine for offering illegal binary options

- 2024-05milestone

$45M raise from Founders Fund, Vitalik Buterin, and others

- 2024-07milestone

Bettors staked $80M on Biden exit — correctly called his withdrawal hours early

- 2024-10regulatory

US election betting volume approaches $1B; Senate pushes CFTC to ban it

- 2024-11regulatory

FBI raids CEO Shayne Coplan's home, seizes phone and electronics

- 2025-03regulatory

DOJ closes Polymarket investigation, signaling regulatory thaw

POLY token and airdrop confirmed alongside $2B ICE investment

Iran peace deal market hits $345M; White House warns staff against trading it

Risk, Fairness, And Market Integrity

Resolution Risks, Fine Print, And User Expectations

One of the most significant sources of risk for Polymarket users is not price volatility per se, but the possibility that a market will resolve in a way that diverges from their expectations, due either to ambiguous wording or to a misreading of the fine print. As seen in the Iran peace deal market, even highly engaged traders can disagree about whether real-world developments satisfy a contract’s resolution criteria, leading to disputes and contentious resolutions. In some cases, users who thought they had constructed near risk-free arbitrage trades based on their interpretation of market rules have discovered, upon resolution, that their assumptions did not align with the platform’s or the oracle’s interpretation, causing their positions to lose value unexpectedly. Media coverage has highlighted instances where a student or retail trader turned a relatively small stake into a large paper profit on Polymarket, only to see the position go to zero when the market resolved differently than they expected, illustrating both the potential for dramatic gains and the importance of understanding resolution mechanics.

Polymarket’s structured resolution and dispute process—requiring outcome proposals backed by USDC.e bonds and subject to challenge—aims to ensure that markets settle on a defensible interpretation of their criteria. However, the presence of a dispute process does not eliminate the possibility of controversy; rather, it provides a channel for contestation that may or may not satisfy all participants. For users, the key protection is careful reading and understanding of each market’s description, rules, and designated resolution sources, including any specified news outlets or data providers that will be used to verify outcomes. From a consumer protection perspective, these complexities may be difficult for casual users to fully grasp, reinforcing arguments by some regulators that prediction markets can expose retail traders to non-obvious risks that go beyond normal financial volatility.

Fraud, Identity Theft, And KYC

Another category of risk for Polymarket and its users arises from fraud and identity theft. Reporting by The Information has indicated that fraudsters found ways to set up Polymarket accounts using stolen credit cards and hijacked identities, exploiting gaps between crypto-native systems and traditional payment and identity verification processes. Such activity not only harms the individuals whose identities and financial information are misused, but also exposes platforms to chargebacks, regulatory scrutiny, and reputational damage, which can in turn lead to stricter account controls and KYC requirements. In response, both Polymarket and Kalshi have reportedly taken steps to block fraud rings, tightening their defenses against such abuse and collaborating with partners to improve detection and prevention systems.

These developments help explain why Polymarket has moved toward mandatory KYC for active traders, even though earlier promotional materials emphasized no-KYC access for users outside the United States. The move toward stronger identity verification is consistent with broader trends in both centralized and decentralized finance, where regulators and service providers increasingly demand that platforms know who their users are, particularly in higher-risk domains like derivatives and event-based betting. For privacy-conscious users, these developments may be unwelcome, but for platforms seeking long-term viability in a tightening regulatory environment, KYC and enhanced fraud controls are becoming difficult to avoid.

Gambling Harm, Consumer Protection, And Public Perception

Beyond technical and legal risks, prediction markets like Polymarket face concerns about gambling harm and consumer protection, particularly when markets cover sports and other entertainment topics that resemble traditional betting. The Kentucky Attorney General’s lawsuits against Polymarket and Kalshi explicitly characterize them as illegal sportsbooks, arguing that their offerings allow users to place wagers on sports outcomes without the safeguards and responsible gambling measures required of licensed operators. The lawsuits further contend that Polymarket, Kalshi, and affiliated entities such as Coinbase, Robinhood, and Webull provide few or no resources to help users identify or seek assistance for gambling problems, in contrast to obligations imposed on licensed sportsbooks under Kentucky law. These claims reflect a view that prediction markets should be regulated as gambling platforms, especially where they feature sports-related markets and high-stakes trading.

From the platforms’ perspective, prediction markets can be defended as tools for price discovery and information aggregation, but the line between “research” and “gambling” is often blurred in practice. Users may approach Polymarket differently: some treat it as a venue for disciplined probabilistic trading and hedging, while others see it primarily as a way to bet on favorite teams, political outcomes, or sensational events. The presence of large, attention-grabbing wins and losses—such as million-dollar payouts on unlikely sports draws—can exacerbate concerns that prediction markets encourage risky behavior and speculative excess, particularly among inexperienced users who may be tempted to emulate high-stakes traders. For regulators, balancing these concerns against the potential informational benefits of prediction markets is a challenging task, and responses vary widely across jurisdictions.

One possible direction for the industry is the adoption of stronger responsible trading features, such as deposit limits, self-exclusion tools, and clearer risk disclosures, even where not strictly required by law. While these measures may not fully address regulators’ concerns, they can help demonstrate that platforms are taking user welfare seriously and may mitigate some of the most acute risks of problem gambling behavior. The extent to which Polymarket and similar platforms adopt such features will likely influence both their public perception and their regulatory treatment over time.

Competition, Integrations, And The Wider Ecosystem

Kalshi And Regulated U.S. Event Markets

Kalshi is often mentioned alongside Polymarket as a leading prediction market platform, but its strategy and regulatory posture differ markedly. Kalshi operates as a CFTC-regulated exchange for event contracts, positioning its products as derivatives rather than as gambling and emphasizing that it is an American company regulated domestically. In its public statements and legal filings, Kalshi has argued that event contracts traded on federally designated exchanges should be treated similarly to other derivatives, and that state-level attempts to impose targeted excise taxes or gambling classifications are preempted by federal law. This stance underlies Kalshi’s participation in the Coalition for Fair Markets, which is challenging Kentucky’s 14.25% excise tax on prediction market transaction fees as discriminatory and contrary to federal policy.

The Kentucky Attorney General, however, has not drawn a clear distinction between Kalshi and Polymarket in his lawsuits, instead lumping both together as illegal sportsbooks that facilitate unlicensed betting on sports outcomes and other events. This illustrates the regulatory ambiguity around event-based derivatives: even where a platform secures federal derivatives regulatory approval, states may still seek to regulate or restrict its activities under gambling laws, particularly where sports-related markets are involved. For Polymarket, which has not taken the same path toward CFTC designation, Kalshi’s experience both offers a potential template for more formal regulatory integration and highlights the challenges of navigating overlapping state and federal regimes.

Coinbase, Robinhood, Webull, And Brokerage Integrations

Centralized trading platforms such as Coinbase, Robinhood, and Webull play a significant role in the prediction markets ecosystem, even if they do not operate event markets directly in the same way as Polymarket. The Kentucky lawsuits allege that these companies, as affiliates of Kalshi and Polymarket, offer users few or no resources for managing gambling problems, suggesting that they serve as conduits for funds and user acquisition into prediction markets without adopting the same consumer protection standards required of licensed gambling operators. At the same time, Coinbase and Robinhood are mentioned alongside Polymarket and Kalshi in reporting about the broader sector of yes/no and event-based trading platforms, reflecting how their introduction of retail-accessible options, leveraged products, or sports-betting style products blurs boundaries between traditional brokerage and prediction markets.

For Polymarket, partnerships and integrations with centralized platforms can provide important on-ramps, enabling users to fund their prediction market accounts using fiat currencies or popular cryptocurrencies held at exchanges. However, such relationships also extend the regulatory surface area of prediction markets, as regulators and lawmakers scrutinize the entire chain of services that facilitate event-based trading, from wallet providers to exchanges and brokerage apps. The way Coinbase, Robinhood, and other intermediaries position their connections to prediction markets—whether as distinct product categories or as part of a broader menu of speculative instruments—will influence how regulators perceive and address the sector as a whole.

Wallets, Casinos, And Infrastructure: MetaMask And BC.GAME

Polymarket’s integration with MetaMask and BC.GAME illustrates how prediction markets can function not only as standalone websites but also as underlying infrastructure embedded within other applications. MetaMask’s dedicated prediction markets section allows users to explore and trade Polymarket contracts directly from their wallets, using any EVM-compatible token to fund a predictions account or trading with top tokens from their wallet, before routing settlement through Polymarket’s USDC-based contracts. This integration lowers the barrier to entry for users who are already comfortable with MetaMask and DeFi, exposing Polymarket to a broad audience of crypto-native users who may not have otherwise sought out prediction markets.

BC.GAME, a global online casino and gaming platform, has taken a different approach by integrating Polymarket as the backend for a new Prediction Center spanning sports, crypto, and real-world events. In this setup, BC.GAME users can access Polymarket-powered markets through a familiar casino interface, while the underlying pricing and liquidity are provided by Polymarket’s on-chain markets. This demonstrates how Polymarket can act as a liquidity and pricing provider for other platforms, much like how centralized exchanges provide order books for a variety of front-end applications, and suggests that prediction markets could become a modular component in a larger ecosystem of entertainment and financial products.

These integrations also raise regulatory and ethical questions. When Polymarket markets are accessed through a casino-like front end, it becomes more difficult to argue that the platform is purely an information or research tool, reinforcing gambling-related concerns. Conversely, embedding prediction markets within wallets and DeFi interfaces may accentuate their financial and analytical dimensions, aligning them more closely with derivatives and investment-oriented products. How these different front ends frame and regulate access to Polymarket’s markets will shape both user behavior and regulatory responses.

On-Chain Rivals And The Competitive Landscape

Polymarket is not alone in the on-chain prediction markets space. Other crypto-native platforms on networks such as Solana and Ethereum are experimenting with similar models, offering users the ability to trade on real-world events using tokenized contracts and decentralized governance structures. Some of these rivals emphasize deeper integration with decentralized finance primitives, such as automated market makers or governance tokens, while others focus on niche verticals like sports or politics. Although specific competitors vary over time, the overall trend is clear: prediction markets have become a recognized DeFi vertical, attracting both entrepreneurial experimentation and venture funding.

For Polymarket, this competition underscores the importance of liquidity, user experience, and regulatory positioning. Liquidity tends to be self-reinforcing: platforms with deeper markets attract more traders, which further improves liquidity and price discovery, making it harder for newer entrants to gain traction without offering compelling differentiators. At the same time, regulatory headwinds that hit one platform can spill over to others, either by prompting industry-wide KYC and compliance upgrades or by deterring users from engaging with prediction markets altogether. Polymarket’s ability to maintain its position as a leading prediction market may thus depend not only on its own choices, but also on the evolution of the broader ecosystem and how regulators choose to address it.

DraftKings launches proprietary prediction markets exchange DKeX as annualized consumer volume tops $3.4B, intensifying competition with Polymarket and Kalshi

$11.3B annualized trading volume off one DraftKings Predictions week puts sportsbook UX directly against Kalshi’s CFTC wrapper and Polymarket’s crypto-native CLOB. Sportsbooks already know how to acquire and retain retail at scale; crypto’s edge is composable settlement and open books, and that pitch gets shakier when Polymarket research is finding 1.95M reverted match-order txs and $1.78B at risk from off-chain match/on-chain settle gaps. If DKeX owns the fiat funnel while Kalshi owns regulatory precedent, Polymarket has to prove liquidity quality beats on-chain branding.

CFTC consent order, FBI raid on the CEO, Singapore access block, Senate push to ban election betting, and state AG scrutiny represent overlapping multi-jurisdictional legal exposure with no settled resolution.

UMA-based resolution is vulnerable to coordinated whale voting that can override media consensus, as demonstrated by the Zelenskyy suit market where $39M in open interest resolved against near-universal press coverage.

Freshly funded wallets winning $1M on Iran airstrike timing and $600K on ceasefire windows suggest that state-adjacent or insider-adjacent actors can systematically extract value from retail liquidity.

Polymarket runs on Polygon and relies on USDC as collateral; smart-contract risk is derivative of both Polygon network security and Circle's USDC redemption guarantees, neither of which is Polymarket-controlled.

Resolution authority is concentrated in UMA token holders, creating a single governance chokepoint where a sufficiently capitalized actor can manipulate outcomes without exploiting any on-chain bug.

- LiquidityLow

Presidential election markets exceeded $1B in volume and total bets threatened to flippen Polygon's TVL, indicating deep liquidity on high-salience events, though thin markets on niche questions remain arbitrage targets.

Using Polymarket In Practice: A Conceptual Walkthrough

For a typical user, engaging with Polymarket involves a series of decisions that intertwine financial, technical, and legal considerations. At the most basic level, a would-be trader must decide whether they are comfortable interacting with on-chain platforms and stablecoins, and whether their jurisdiction allows participation in such markets without violating local laws or exchange policies. Users must also consider the practicalities of funding an account with USDC on the Polygon network, which may involve acquiring USDC on a centralized exchange, bridging assets to Polygon, and connecting a compatible wallet such as MetaMask to the Polymarket interface or to an integrated front end like BC.GAME. For many crypto-savvy users, these steps are familiar, but for newcomers they can constitute a significant learning curve.

Once funded, users face the more conceptual challenge of interpreting and evaluating markets. Each Polymarket listing is accompanied by a description, resolution criteria, and sometimes external sources or definitions that outline what will count as a “Yes” outcome. Users must read these carefully, particularly where wording may be open to interpretation or where the underlying event is complex, as in diplomatic agreements or multi-stage corporate actions. They must then decide whether the current market price reflects a mispricing of probabilities relative to their own beliefs or information, and whether the expected value of a trade justifies the risk, taking into account both the potential payoff and the possibility of loss. Because contracts are binary, even small miscalculations in probability estimates can have large effects on expected returns, especially at extreme price levels.

Risk management is a critical but often underappreciated aspect of using Polymarket responsibly. Traders must decide how much of their portfolio to allocate to any single market, how to diversify across multiple events, and whether to use positions as hedges for other exposures rather than pure speculation. For example, a user worried about a geopolitical conflict impacting their broader investments might choose to buy “Yes” shares in a conflict-related Polymarket market as a hedge, so that if the adverse event occurs, gains on Polymarket partially offset losses elsewhere. Conversely, using Polymarket solely as a venue for high-stakes bets on sports or elections without diversification can amplify the risk of large, sudden losses, particularly if emotional factors or cognitive biases influence trading decisions.

Finally, users must remain aware of the evolving regulatory environment and platform policies. Changes in KYC requirements, country restrictions, or exchange policies—such as Bitbank’s willingness to suspend accounts for Polymarket-linked activity—can affect both access and the safety of funds. Traders should consider how they would respond if their access is curtailed or if regulatory actions impact the platform’s operations, as occurred when Polymarket agreed to wind down non-compliant markets under its CFTC settlement. In short, using Polymarket is not just a matter of clicking “Yes” or “No” on a screen; it involves navigating a complex interplay of probabilistic reasoning, financial risk, technical infrastructure, and regulatory risk.

Broader Significance: Information, Markets, And Policy

Polymarket and similar platforms occupy an increasingly prominent place in discussions about how societies aggregate information and make decisions under uncertainty. Academic research on prediction markets, including corporate experiments like Google’s Prophit platform, has shown that such markets can provide well-calibrated forecasts that improve over time as participants gain experience, often aligning closely with or even outperforming traditional forecasting methods. In Google’s case, internal markets were used to forecast product launches, sales, and other business outcomes, with results indicating that the collective wisdom of employees, expressed through trading, could produce accurate and timely probabilistic forecasts. These findings have fueled enthusiasm for prediction markets as tools that can complement surveys, expert panels, and quantitative models in both public and private decision-making contexts.

Polymarket extends this idea into the public, crypto-native domain, enabling anyone with sufficient technical and regulatory access to trade on real-world events and thereby contribute to a decentralized forecasting system. In principle, this open participation can harness a broader pool of information than closed corporate markets, capturing insights from diverse perspectives and geographies. At the same time, public prediction markets may be more susceptible to speculative frenzies, manipulation attempts, and herd behavior, particularly in high-profile political or sports markets where emotions run high. The net effect on forecast quality is an empirical question that remains under active study, but the Polymarket case demonstrates both the potential for large-scale information aggregation and the challenges of ensuring that incentives and rules produce robust rather than distorted signals.

For policymakers, Polymarket raises several difficult questions. One is whether and how to incorporate prediction market prices into official decision-making, such as using market-implied probabilities when evaluating policy options or contingency plans. Another is how to regulate platforms that provide these signals without stifling innovation or driving users toward opaque, unregulated alternatives. Efforts like Kentucky’s excise tax and lawsuits, or the CFTC’s enforcement actions, reflect the tension between seeing prediction markets as socially useful forecasting tools and as potentially harmful gambling or unlicensed derivatives. As mainstream financial institutions like Charles Schwab and Cboe enter the yes/no options space, the policy landscape may shift further, prompting calls for harmonized rules that apply consistently across on-chain and off-chain venues.

Polymarket also touches on broader debates about the role of crypto and DeFi in the global financial system. Its reliance on USDC and Polygon illustrates how stablecoins and layer-2 networks can support complex financial products without requiring centralized custodians or brokers, while integrations with wallets and gaming platforms demonstrate the composability of DeFi primitives. At the same time, the platform’s experience with KYC, regulatory enforcement, and state-level lawsuits shows that even highly decentralized architectures can be targeted through their visible operators, front ends, and service providers. The future of Polymarket, therefore, will likely be shaped not only by its own technical and product choices but also by broader societal decisions about how to integrate or constrain crypto-based financial experimentation.

Conclusion

Polymarket sits at the nexus of several powerful trends: the rise of prediction markets as tools for aggregating information, the maturation of crypto-based financial infrastructure built on stablecoins and layer-2 networks, and a global regulatory environment still grappling with how to categorize and control event-based trading. As a platform, it offers users the ability to trade on the outcomes of real-world events using binary yes/no contracts denominated in USDC, spanning topics from geopolitics and elections to sports, crypto, and cultural phenomena. Its design leverages on-chain settlement via the Polygon network, a nuanced fee structure with maker incentives, and integrations with wallets and gaming platforms to build liquidity and reach a wide audience. At the same time, its operations are constrained by evolving KYC policies, geographic restrictions, and the risk appetites of intermediaries like exchanges and wallet providers, which must interpret and comply with local laws and regulations.

The platform’s history and ongoing regulatory challenges illustrate the unsettled status of prediction markets in law and public policy. The CFTC’s 2022 enforcement action treated Polymarket’s event markets as off-exchange binary options, requiring a settlement, penalties, and the winding down of certain markets, while recent actions in Kentucky and Michigan frame the platform as an unlicensed sportsbook and gambling operator. Concurrently, Kentucky’s excise tax dispute and Kalshi’s efforts to defend federally regulated event markets highlight tensions between state-level gambling and tax regimes and federal derivatives regulation. Internationally, warnings from exchanges like Bitbank and Polymarket’s own KYC and country-blocking measures reflect a landscape in which prediction markets are increasingly seen as high-risk or legally ambiguous.

Yet despite—or perhaps because of—these challenges, Polymarket continues to demonstrate the distinctive capabilities of prediction markets. High-profile contracts like the U.S.–Iran permanent peace deal market have turned complex diplomatic developments into tradable probabilities, drawing hundreds of millions of dollars in volume and offering a real-time, crowd-sourced view of geopolitical risk. Sports markets have produced dramatic million-dollar swings on unexpected draws, while crypto and tech markets have captured sentiment on token launches, valuations, and macroeconomic events. These markets show how economic incentives can be harnessed to reveal collective beliefs, even as they raise questions about fairness, gambling harm, and the potential for confusion over resolution rules.

Ultimately, Polymarket’s significance extends beyond its own user base. It serves as a case study in how DeFi-native platforms can build and operate complex financial instruments at scale, and in how regulators are responding to those experiments. The convergence of traditional players like Charles Schwab and Cboe toward yes/no options, and of regulated platforms like Kalshi toward event contracts, suggests that prediction-like markets are unlikely to disappear; instead, the key question is what mix of on-chain and regulated models will prevail. Polymarket’s trajectory—its ability to adapt to regulatory demands, maintain user trust in its resolution processes, and balance entertainment with responsible trading—will shape not only its own future but also the broader evolution of prediction markets in the crypto era.

Outlook

Looking ahead, Polymarket and the wider prediction markets ecosystem face a bifurcated path. On one side lies integration with mainstream finance, as evidenced by Schwab and Cboe’s embrace of yes/no options and Kalshi’s bid to solidify event contracts within the U.S. derivatives framework, pointing toward a future where binary event trading is a standard, regulated financial product. On the other side lies the crypto-native vision embodied by Polymarket’s on-chain markets, with their global reach, composability, and rapid innovation, but also their exposure to fragmented regulation, KYC pressures, and platform-specific risks. The balance between these models will depend on how regulators choose to classify prediction markets—as gambling, derivatives, or a novel category—and on whether platforms can demonstrate robust consumer protection, fair resolution processes, and tangible informational value.

For a crypto news audience, Polymarket is likely to remain a key bellwether for the sector. Its growth, legal battles, and market innovations will offer early signals about where prediction markets are heading, how far DeFi-native platforms can push the envelope, and how quickly traditional finance adapts their core ideas into regulated products. Traders and observers alike should expect continued experimentation, periodic controversy, and a gradual convergence between on-chain and off-chain event markets, even as debates over risk, fairness, and regulation continue to shape the contours of this emerging asset class.

Latest Polymarket news

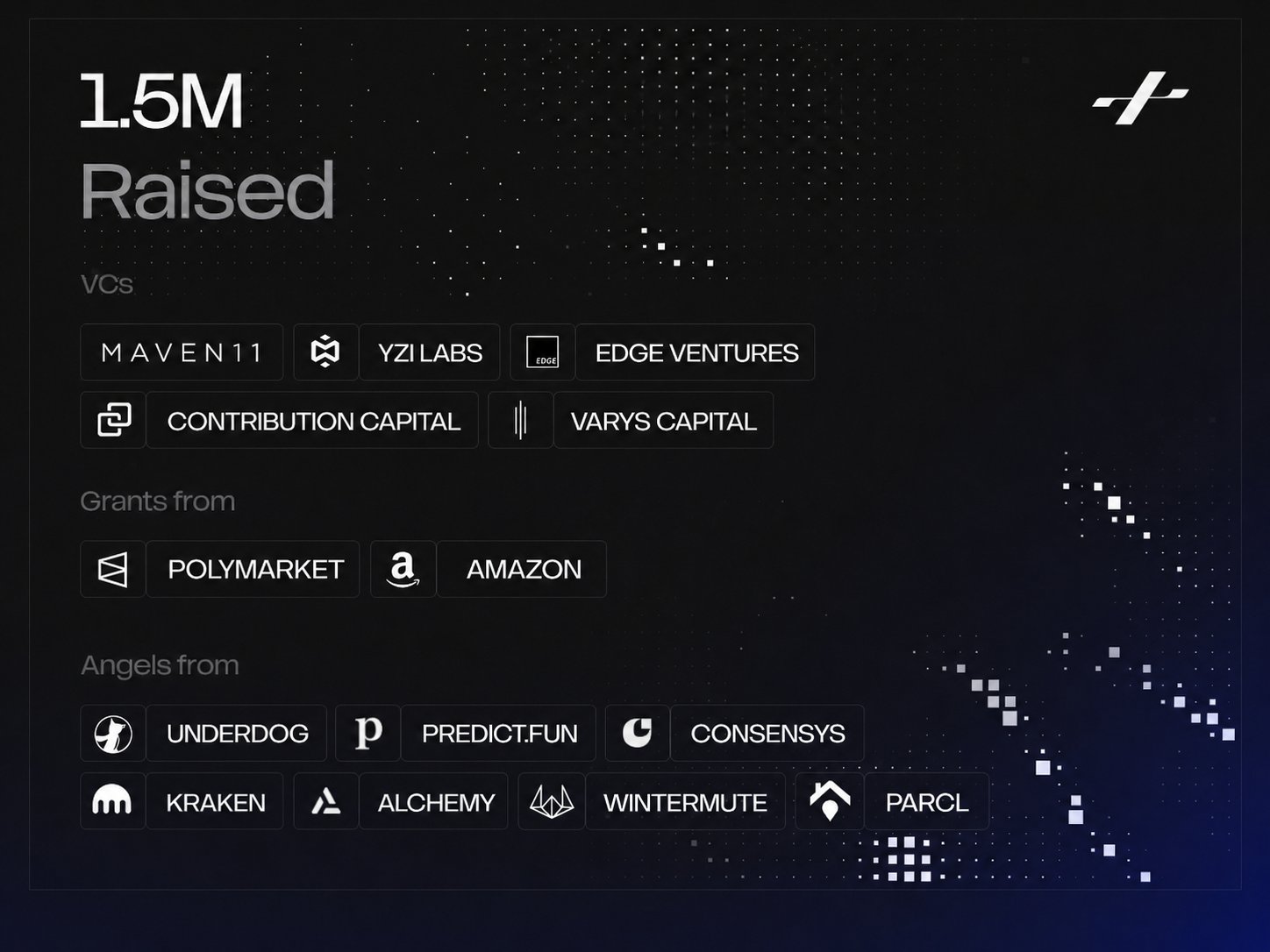

Polymarket paid creators to stage $900K in fake winning bets on cloned sites, courting American users it's banned from servingKalshi and Polymarket non-sports volume hits $3.6B in a week, up 18x since JulyDraftKings launches proprietary prediction markets exchange DKeX as annualized consumer volume tops $3.4B, intensifying competition with Polymarket and Kalshi AI analytics platform Polysights raises $1.5M pre-seed funding to combat insider trading in prediction markets. The raise was backed by YZi Labs S3, Maven 11 Capital, and angels from Kraken and Consensys, plus grants from Polymarket and AWS.

AI analytics platform Polysights raises $1.5M pre-seed funding to combat insider trading in prediction markets. The raise was backed by YZi Labs S3, Maven 11 Capital, and angels from Kraken and Consensys, plus grants from Polymarket and AWS. Meta reportedly builds points-based Arena prediction market app to rival Polymarket and Kalshi

Meta reportedly builds points-based Arena prediction market app to rival Polymarket and Kalshi WSJ finds Polymarket paid creators to stage fake trades in 1,100 videos courting U.S. users

WSJ finds Polymarket paid creators to stage fake trades in 1,100 videos courting U.S. usersSources

- https://polymarket.com

- https://help.polymarket.com/en/articles/13364518-how-are-prediction-markets-resolved

- https://www.cftc.gov/PressRoom/PressReleases/8478-22

- https://www.bloomberg.com/news/articles/2026-06-15/polymarket-traders-clash-over-345-million-iran-peace-market

- https://kentucky.gov/Pages/Activity-stream.aspx?n=AttorneyGeneral&prId=1944

- https://x.com/BLaw/status/2067341578302013487

- https://seekingalpha.com/news/4605279-charles-schwab-cboe-venturing-prediction-markets

- https://metamask.io/prediction-markets

- https://bitcoinfoundation.org/news/prediction-markets/polymarket-kyc/

- https://polymarket.com/event/us-x-iran-permanent-peace-deal-by