Comprehensive explainer on crypto “rates” covering Fed policy, T‑bill yields, DeFi lending APYs, stablecoin yield dynamics, perpetual funding, CeFi loans, security risk, oracles and AI agents, and how these interconnected rates drive liquidity and leverage across crypto.

- x.com19

- cnbc.com5

- coindesk.com3

- dlnews.com3

- leviathannews.substack.com3

- truthsocial.com2

- forum.makerdao.com2

+50 sources across the wider coverage universe

Smoothing crvUSD Borrow Rates2026-02

Smoothing crvUSD Borrow Rates2026-02 Inside crvUSD borrow rate.2025-12

Inside crvUSD borrow rate.2025-12 A LOOK INTO COINBASE:

Coinbase’s “brand refresh” is really a pivot into an everything exchange—AI agents, stocks, perps, prediction markets, regulated token sales, B2B stablecoins, SocialFi, and curated DeFi—all on crypto rails. Bull case: this makes Coinbase a global financial utility, pulls TradFi liquidity onchain, scales revenue, and accelerates mass adoption. Bear case: it dilutes altcoins, centralizes power, invites heavy regulation, and could kill degen culture as capital rotates from speculative tokens into real, cash-flow assets.2025-12

A LOOK INTO COINBASE:

Coinbase’s “brand refresh” is really a pivot into an everything exchange—AI agents, stocks, perps, prediction markets, regulated token sales, B2B stablecoins, SocialFi, and curated DeFi—all on crypto rails. Bull case: this makes Coinbase a global financial utility, pulls TradFi liquidity onchain, scales revenue, and accelerates mass adoption. Bear case: it dilutes altcoins, centralizes power, invites heavy regulation, and could kill degen culture as capital rotates from speculative tokens into real, cash-flow assets.2025-12 Federal Reserve cuts rates to three-year low after fractious meeting. Three top US central bankers object to move in biggest revolt since 2019. The benchmark rate was cut by a quarter point to between 3.5 to 3.75 per cent as widely anticipated by Wall Street. It marked the third reduction in borrowing costs in a row.2025-12

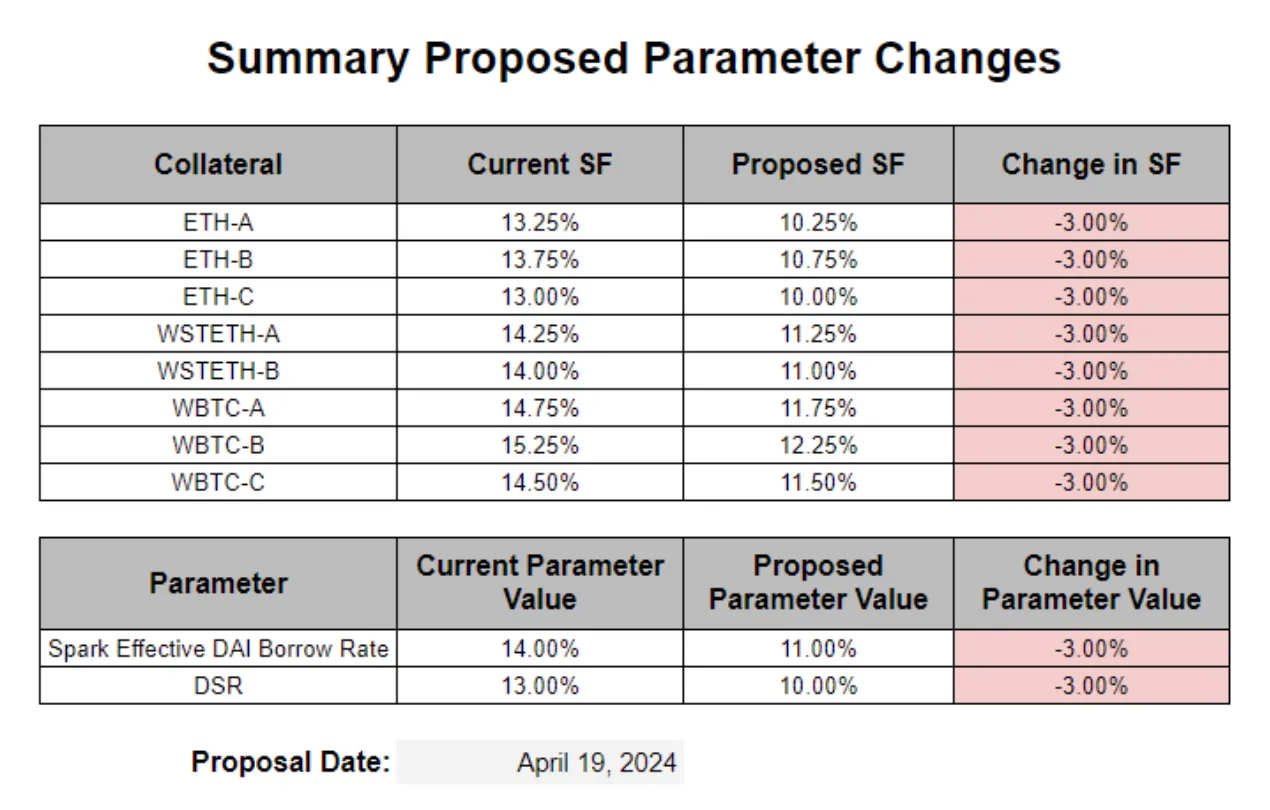

Federal Reserve cuts rates to three-year low after fractious meeting. Three top US central bankers object to move in biggest revolt since 2019. The benchmark rate was cut by a quarter point to between 3.5 to 3.75 per cent as widely anticipated by Wall Street. It marked the third reduction in borrowing costs in a row.2025-12 BA Labs recommends Maker DAO decrease rates 3%, which would drop the Dai Savings Rate to 10%2024-04

BA Labs recommends Maker DAO decrease rates 3%, which would drop the Dai Savings Rate to 10%2024-04 Liquity releases details on v2 BOLD stability pool opportunities: "Will behave similarly to money markets but with opposite spreads: depending on the utilization and integration of BOLD in the broader DeFi ecosystem, the Stability Pool will generally exceed the average borrow rates"2024-05

Liquity releases details on v2 BOLD stability pool opportunities: "Will behave similarly to money markets but with opposite spreads: depending on the utilization and integration of BOLD in the broader DeFi ecosystem, the Stability Pool will generally exceed the average borrow rates"2024-05

Rates In Crypto Markets: An Evergreen Explainer

Rates in crypto span far more than central bank interest decisions: they include on‑chain lending yields, perpetual futures funding, CeFi borrowing costs, and stablecoin or T‑bill–linked returns, all of which interact to shape liquidity, leverage, and price dynamics across digital asset markets. Understanding how these different rates are set, how they respond to macro policy, and how they compensate for risks such as smart‑contract exploits or depegs has become essential for anyone trading, building, or regulating in the crypto ecosystem.

What “Rates” Mean In And Around Crypto

The word rates is deceptively simple, but in crypto conversations it is shorthand for a dense web of prices on time, leverage, and risk. Traders might talk about funding rates on perpetual futures, DeFi participants focus on lending APYs for stablecoins, macro analysts track the Federal Reserve’s policy rate, while stablecoin issuers quietly earn yields on short‑term government bonds backing their tokens. All of these are manifestations of the same underlying concept: the interest rate is the price of moving money through time, shaped by supply and demand, credit risk, and the broader macroeconomic backdrop.

At the most basic level, an interest rate is the proportion of a principal amount charged or paid for its use per unit of time. In traditional finance this might be a bank paying 3% annually on a savings deposit, or a central bank setting an overnight policy rate. In crypto, similar concepts appear as an annualized percentage yield (APY) on stablecoin deposits in a lending protocol, or a periodic funding rate paid every few hours between long and short positions in a perpetual swap. These rates can be quoted as simple annual percentages or as compounded equivalents that assume reinvestment of interest over time. Although the underlying mathematics is universal, the mechanisms that produce rates in crypto—algorithms, smart contracts, and on‑chain auctions—differ markedly from the committee‑driven processes of central banks.

It is helpful to distinguish several broad categories of rates that are relevant to digital assets. First are policy rates, such as the federal funds rate in the United States or benchmark rates in Japan, which influence global liquidity and the opportunity cost of holding risk assets. Second are market interest rates in traditional instruments like Treasury bills and bank deposits, which provide a baseline against which crypto yields are measured; three‑month U.S. T‑bills, for example, have recently yielded around 3.8% annualized. Third are crypto‑native rates, including DeFi lending and borrowing rates, margin and VIP loan rates on centralized exchanges, perpetual futures funding rates, and staking or validator yields. Finally, there are implied rates, such as the yield on basis trades that combine spot and derivative positions, or the effective returns embedded in liquidity provision on automated market makers.

Within these categories, crypto discourse often toggles between APR and APY. APR, or annual percentage rate, is a simple annualized figure without compounding; APY assumes interest is periodically added to principal, so that returns grow at an exponential rate if interest is reinvested. On DeFi platforms, borrow rates are commonly quoted as APR while deposit returns are framed as APY, reflecting the compounding effect for depositors whose interest payments are continuously added to their balance by the protocol. For sophisticated analysis, nominal rates should be adjusted for inflation to obtain real rates, and for risk to obtain risk‑adjusted or Sharpe‑ratio‑like measures. Yet many crypto discussions still focus on headline APYs without carefully weighing the underlying risk exposures or the macro environment.

Across the ecosystem, these rates are not independent. A trader leveraging a long bitcoin position might borrow stablecoins from a DeFi protocol at a variable borrow rate, post them as margin on a centralized exchange, and hold a perpetual futures position that either pays or receives funding depending on the sign of the funding rate. A stablecoin issuer might invest reserves in T‑bills whose yields are influenced by both central bank policy and, as recent research suggests, by the scale of stablecoin demand itself. A DeFi protocol might design its interest rate model to remain competitive with off‑chain savings rates, aware that depositors can always exit into tokenized T‑bills or regulated custodial accounts. Understanding “rates” in crypto therefore requires following these linkages from base macro policy to on‑chain algorithms and back again.

This explainer traces that chain of causality. It begins with central bank policy rates and the macro backdrop, then moves through algorithmic DeFi lending, derivatives funding, stablecoins and safe assets, centralized lending markets, and the security risks that shape the required yield premium in DeFi. It closes by outlining how data infrastructure and autonomous agents are reshaping rate discovery, and how traders and builders can develop a coherent framework for interpreting rates across market cycles.

Smoothing crvUSD Borrow Rates

Readers click rates content not for yield-farming tutorials but for governance power plays: who sets the number, who benefits from the change, and whether a single whale or committee can reprice everyone else's position overnight.↗

Central Bank Rates And The Macro Backdrop

Although crypto is often framed as an alternative to legacy finance, its rate environment is anchored in the traditional monetary system. Central banks set short‑term policy rates that influence the entire yield curve of government bonds and bank funding costs, and these in turn shape investors’ appetite for risk assets, including bitcoin, ether, and DeFi governance tokens. When risk‑free rates are low, the opportunity cost of holding volatile assets is reduced and liquidity tends to chase higher returns; when policy rates are high, safe yields become more attractive and speculative activity can wane.

How The Federal Reserve Sets Policy Rates

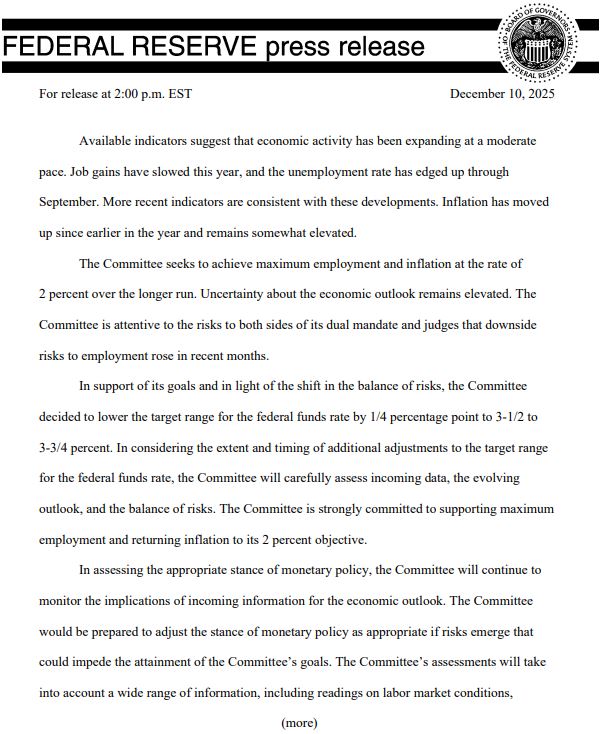

In the United States, the authority to set key interest rates is divided between the Board of Governors of the Federal Reserve and the Federal Open Market Committee (FOMC). The Board of Governors decides on changes in the discount rate—the rate at which banks can borrow directly from the Fed’s discount window—typically in response to recommendations from regional Federal Reserve Banks. The FOMC, which includes the Board and a rotating group of Reserve Bank presidents, determines the target range for the federal funds rate, the interest rate at which depository institutions lend balances to each other overnight.

The FOMC implements its policy stance primarily through open market operations, adjusting the supply of central bank reserves such that the effective federal funds rate trades within the desired target range. As of mid‑2026, the Fed has kept the federal funds target range unchanged at 3.50%–3.75% for several consecutive meetings, including a unanimous 12–0 vote to hold rates steady in June. Official commentary has emphasized that economic activity is expanding at a solid pace while inflation remains elevated relative to the 2% target, justifying a cautious approach that keeps policy restrictive but stable.

The FOMC’s decisions rely on a broad data dashboard. The Fed closely monitors real GDP growth, unemployment rates, and inflation metrics such as the Consumer Price Index (CPI), alongside financial conditions and global developments. When inflation runs hotter than desired, the committee is more inclined to raise rates to cool demand; when growth slows and unemployment rises, it may cut rates to stimulate economic activity. Geopolitical shocks, such as conflicts in the Middle East that drive oil price spikes, complicate this calculus by simultaneously pressuring inflation via energy and dampening growth, forcing trade‑offs in the path of policy rates.

For crypto markets, the federal funds rate serves both as a macro barometer and as a competitor. Bulletins from crypto research outlets frequently frame bitcoin rallies or corrections in relation to expectations for Fed cuts or hikes. Educational resources stress that lower interest rates tend to be favorable for crypto assets over the long run, because they increase liquidity in financial markets, making more capital available for riskier investments like cryptocurrencies. Empirically, Fed rate cuts are often followed by heightened volatility in bitcoin and other major tokens, with a tendency toward higher prices in the months after cuts begin, though causality is hard to disentangle from broader risk‑on sentiment.

Why Macro Rates Matter For Crypto

The transmission channel from policy rates to crypto is indirect but powerful. Higher risk‑free rates increase the yields available on instruments such as Treasury bills and insured bank deposits, raising the hurdle rate for crypto investments. An investor deciding whether to deposit USDC into a DeFi lending pool at 2% APY or to buy three‑month T‑bills yielding 3.8% will naturally gravitate toward the latter unless they perceive additional upside in DeFi, whether from token incentives, governance rights, or optionality on future rate spikes. Conversely, when T‑bill yields are near zero, DeFi yields of 4–8% appear very attractive even after accounting for smart‑contract risk.

Monetary policy also affects crypto through its impact on the dollar’s value and on leverage conditions in traditional markets. Higher U.S. rates tend to strengthen the dollar, tighten global financial conditions, and make it more expensive for traders to borrow dollars or dollar‑linked stablecoins to fund leveraged bets. Hedge funds engaged in basis trades between spot and futures may scale back activity when their dollar funding costs rise, reducing liquidity and compressing derivatives spreads. For retail traders, higher mortgage or credit card rates can crowd out speculative investments, as a larger share of income goes toward debt service rather than discretionary investment.

Yet the relationship is not mechanical. Crypto markets have periodically surged even in tightening cycles, particularly when narratives about technological adoption or digital gold properties take center stage. Bitcoin’s rally despite elevated policy rates has been interpreted as a sign that investors view it as a hedge against fiscal concerns or as a high‑beta asset to broader tech optimism. At the same time, episodes of policy uncertainty—such as surprise decisions to hold rates steady amid geopolitical turmoil—can trigger short‑term volatility in crypto as traders reassess the timing of future cuts or hikes.

Global Policy Divergence: Japan’s Rate Shift

The global dimension of rates adds another layer of complexity. Japan, long associated with ultra‑low or negative policy rates, has recently shifted course, with Japanese benchmark rates hitting their highest levels in roughly three decades. Crypto news coverage has emphasized that, despite this historically significant move in one of the world’s major economies, there has been no “meaningful disruption” to crypto markets. Bitcoin and other major tokens have continued to trade in line with global risk sentiment rather than responding sharply to yen‑denominated funding conditions.

This relative insulation reflects the dollar‑centric nature of crypto liquidity. Most trading pairs are quoted against USD or USD‑linked stablecoins rather than the yen, and the bulk of institutional leverage is funded in dollars. However, Japanese rates still matter at the margin, particularly for investors using yen‑funded carry trades to invest in crypto or for exchanges serving a large Japanese user base. Over time, convergence of global policy rates could narrow international funding differentials that some sophisticated traders exploit when moving capital between jurisdictions.

For the purposes of this explainer, the key takeaway is that macro policy rates—whether in the U.S., Japan, or elsewhere—provide the baseline against which crypto yields must compete. When three‑month U.S. Treasury bills offer around 3.8%, and short‑term policy rates sit in the 3.5–3.75% range, DeFi protocols and CeFi lenders cannot ignore that their users can exit into instruments that are not subject to smart‑contract exploits or exchange insolvencies. The rest of this article examines how crypto‑native rate markets have adapted—or in some cases failed to adapt—to this shifting baseline.

On‑Chain Interest Rates In DeFi Lending

Decentralized finance (DeFi) emerged in part by re‑imagining the basic bank function of maturity transformation and lending as a set of permissionless smart contracts. Protocols such as Aave, Compound, and newer designs like Morpho enable users to supply cryptoassets into shared liquidity pools and allow others to borrow against overcollateralized positions, all without a centralized intermediary deciding who gets a loan. In this system, interest rates are not set by committees but by algorithms that respond in real time to supply and demand.

Utilization‑Based Algorithmic Rate Models

Most major DeFi lending protocols use a simple but powerful framework: the utilization rate, defined as the ratio of borrowed funds to total supplied liquidity in a pool. Let \(L_t\) denote the total value supplied at time \(t\) and \(B_t\) the total value borrowed. By design, both quantities are non‑negative and borrowers cannot take more than has been supplied, so \(0 < B_t \leq L_t\). The utilization rate is then \(U_t = B_t / L_t\), which is bounded between 0 and 1. When utilization rises, indicating that liquidity is scarce relative to demand, the protocol raises borrow rates; when utilization falls, indicating ample idle capital, it lowers them.

The specific shape of the interest rate curve as a function of utilization varies by protocol, but a widely adopted model first introduced by Aave around 2020 is a non‑decreasing bilinear function with a “kink.” Below a target utilization level—say, 80%—the borrow rate increases gradually with utilization, encouraging borrowing while still keeping some liquidity available. Above the target, the rate steepens dramatically, imposing a kind of quadratic penalty on utilization levels that exceed the desired range. This mechanism is intended to discourage the pool from becoming fully utilized, which would make withdrawals difficult for depositors, and to compensate suppliers for the increased liquidity risk when most of the pool is lent out.

Deposit rates are derived from borrow rates after accounting for a reserve factor that accrues a share of interest to the protocol’s treasury or insurance fund. If the borrow APR is \(r_b(U_t)\) at a given utilization and a fraction \(k\) of interest is reserved, the supply APY for depositors depends on \(r_b(U_t)\), the utilization \(U_t\), and compounding frequency. In practice, DeFi front‑ends present both a variable borrow APR and a supply APY, updated block‑by‑block as utilization changes. Because loans in these protocols typically have no fixed maturity—borrowers can repay at any time and depositors can withdraw as long as liquidity is available—rates float continuously with market conditions.

Risk‑Aware Interest Rate Design

While early DeFi lending models focused primarily on balancing utilization and liquidity, more recent research has examined how to design risk‑aware interest rate functions that optimize not just utilization but also the risk‑adjusted profit and loss (P&L) of the liquidity pool. A 2025 agent‑based modeling study proposes treating the interest rate as a control variable chosen by the protocol in response to the state of the pool, represented by \(L_t\), \(B_t\), and derived metrics like utilization. The goal is to determine an interest rate policy that maximizes expected returns to liquidity providers subject to constraints on risk, such as bounds on drawdowns or probability of large losses.

When the responses of agents—borrowers and lenders—to interest rates are assumed to be linear, the optimal policy can be derived from a system of Riccati‑type ordinary differential equations (ODEs). In more realistic settings where behaviors are nonlinear—borrowers may only respond to large rate changes, or lenders may exit abruptly if yields fall below a threshold—the authors propose a Monte Carlo estimator coupled with deep learning techniques to approximate the optimal rate function. They calibrate their model using block‑by‑block on‑chain data from an actual DeFi protocol and compare the resulting optimal interest rate schedule with industry‑standard utilization curves such as Aave’s.

The study finds that traditional bilinear utilization‑based curves may not be optimal from a risk‑adjusted P&L perspective, especially in periods of volatile demand. The optimal risk‑aware rate function can differ significantly, sometimes setting higher rates at intermediate utilization levels to deter excessive pro‑cyclical borrowing, or adjusting more rapidly when volatility indicators spike. By introducing a quadratic penalty for utilization levels above a target, the model explicitly prices liquidity risk and can better protect depositors from episodes when nearly the entire pool is borrowed, which can coincide with sharp price swings. This line of research suggests that DeFi lending models may evolve toward more sophisticated, data‑driven rate policies rather than relying solely on static utilization curves.

Determinants Of Crypto Lending Rates

Empirical work on actual lending data helps clarify what drives DeFi rates in practice. A study of bitcoin lending markets on a decentralized finance platform uses a moderated mediation framework to examine how loan‑to‑value (LTV) ratios and bitcoin price dynamics influence interest rates. The authors find a strong positive relationship between the interest rate charged and the LTV ratio, consistent with traditional collateralized lending where loans with higher LTV—meaning less collateral cushion—command higher interest to compensate for greater default or liquidation risk.

They also find a significant link between interest rates and bitcoin price fluctuations, indicating a momentum effect in crypto lending. When bitcoin prices rise and volatility increases, borrowers are more inclined to seek additional funding to speculate further, and lenders demand higher rates to compensate for the heightened risk, resulting in pro‑cyclical behavior. However, the analysis reveals a moderation effect: when the aggregate amount lent surpasses a certain threshold, the overall impact of bitcoin prices on interest rates becomes negative, creating a “seesaw” dynamic. In other words, when there is already a large volume of outstanding loans, interest rates may not rise as much with prices, possibly because competition among lenders compresses spreads or because risk constraints cap further rate increases.

These findings support the view that cryptocurrency lending has option‑like features and fits within a risk‑debt model where collateral value, volatility, and aggregate leverage jointly determine interest rates. They also underscore that DeFi interest rates are not purely mechanical functions of utilization; behavioral factors and market structure shape the effective cost of borrowing. This helps explain why headline APYs can diverge significantly between protocols and assets even when utilization levels appear similar.

The Compression Of DeFi Yields

Against this structural background, one of the striking developments of the past few years has been the collapse of DeFi yields from the double‑digit levels seen during the 2020–2021 boom to levels that in many cases now sit below traditional savings or T‑bill rates. The CoinDesk Overnight Rate, a benchmark that tracks daily borrowing costs across major DeFi lending markets, spiked above 35% during the 2023 bull run, reflecting intense demand for leverage and limited supply of stablecoin liquidity. As speculative activity cooled and more capital flowed into DeFi, that benchmark has fallen sharply to roughly 3.5%.

Concrete examples illustrate the new reality. Aave, one of the largest DeFi lending protocols by total value locked, has recently offered an APY of around 2.61% on USDC deposits in a major pool. That sits below the roughly 3.14% paid on idle cash at Interactive Brokers, a popular traditional brokerage platform among crypto‑native investors. Aave’s largest USDT pool has yielded around 1.84%, and several other stablecoin pools sit below 2%. Across the broader stablecoin lending market, many yields have followed a similar path lower; for some pools, annualized yields are effectively near zero.

Crypto analytics reports note that median DeFi yields have fallen to multi‑year lows, with many lending vaults and stablecoin pairs yielding between 0% and 0.5%, levels that are below U.S. T‑bill yields around 3.8%. At the same time, there remain pockets of very high yields: certain Morpho vaults, for instance, have advertised APYs as high as 352% for the riskiest configurations, while others in the same protocol range from virtually zero. This stark dispersion highlights how undifferentiated lending in blue‑chip pools has seen yields converge toward risk‑free rates, while exotic or thinly traded pools still display outsized nominal returns to compensate, at least in theory, for much higher risk.

The table below summarizes this contrast in broad terms, using indicative figures from recent coverage:

| Market / Instrument | Indicative Yield (Annualized) | Notes |

|---|---|---|

| U.S. 3‑month T‑bills | ≈ 3.8% | Short‑term “risk‑free” benchmark. |

| Fed funds target range | 3.50%–3.75% | Policy rate set by FOMC. |

| CoinDesk Overnight DeFi Rate (current) | ≈ 3.5% | Down from >35% in 2023 bull run. |

| Aave USDC deposit APY | ≈ 2.61% | Major pool on Ethereum. |

| Aave USDT largest pool APY | ≈ 1.84% | Major pool on Ethereum. |

| Many stablecoin lending pairs (median) | ≈ 0–0.5% | Across DeFi, multi‑year lows. |

| Morpho riskiest vaults | Up to ≈ 352% | Highly risky, thinly traded strategies. |

This compression of organic DeFi yields reflects several forces. As macro risk‑free rates rose, DeFi yields had to compete with safer alternatives. Token incentive programs that had artificially boosted returns were scaled back under regulatory pressure or as treasuries dwindled. Security incidents and regulatory scrutiny raised the perceived risk of on‑chain lending, discouraging leveraged borrowing that previously sustained high rates. As one industry participant put it, many investors now feel that on‑chain yields need to be around 18% to justify the hassle and risk, a level that is rarely available in blue‑chip pools. The next sections explore where higher rates still exist—particularly in derivatives funding and risky stablecoin strategies—and how they relate to macro conditions.

- 01Protocol governance rate-setting↗

MakerDAO (DSR to 10%), Prisma's 15% proposal, and MagicInternet/CRV debates showed readers that DeFi rates are political decisions, not market outputs — triggering the highest engagement of any angle.

- 02Liquity v2 user-set rates

The promise of user-controlled interest rates on BOLD flipped the governance angle — readers were drawn to the idea that borrowers, not committees, could set their own terms.

- 03Macro rate spill into DeFi yields↗

Fed decisions, SNB cuts, and Circle's 99%-rate-dependent revenue model made readers track how TradFi rate cycles directly compress or inflate DeFi returns and RWA demand.

- 04Large-actor liquidity shocks↗

Justin Sun pulling $1.7B ETH from Aave and spiking borrow rates from 4.4% to 33.6% illustrated how one actor can unilaterally reprice an entire lending market.

- 05Rate arbitrage and carry trades↗

Elevated Bitcoin funding rates, MakerDAO EDSR vs borrow-rate spreads, and Gearbox leverage opportunities drew readers hunting concrete yield-gap trades.

- 06Stablecoin depeg via rate mechanics

The USD0++ depeg showed how abrupt redemption-rule changes interact with leveraged rate strategies, trapping farmers and cascading through Morpho and Pendle.

Perpetual Futures Funding Rates

Perpetual futures, or perpetual swaps, are among the most actively traded derivatives in crypto. These contracts track the price of an underlying asset, such as bitcoin, but unlike traditional futures they have no expiration date, allowing traders to hold positions indefinitely. The absence of expiry creates a challenge: without a natural convergence point, the perpetual contract’s price could drift significantly above or below the spot price. To prevent such divergence, exchanges employ a mechanism known as the funding rate.

Mechanism Of Funding In Perpetual Swaps

The funding rate is a periodic payment exchanged directly between traders who hold long and short positions in a perpetual futures contract. When the perpetual contract price trades above the spot price, indicating that longs are willing to pay a premium for leverage, the funding rate is typically positive. In this case, traders holding long positions pay a fee to traders holding short positions at each funding interval. Conversely, when the perpetual price trades below spot, the funding rate becomes negative and shorts pay longs. The goal is to incentivize traders to take the “cheaper” side of the market, thereby bringing the perpetual price back toward spot.

Exchanges generally determine the funding rate using a combination of an interest rate component and a premium index that measures the difference between the perpetual contract price and an index price derived from spot markets. A common formula is

\[ \text{Funding Rate} = \text{Premium Index} + \text{Interest Rate}, \]

where the interest rate is a small, fixed percentage set by the exchange and usually remains constant, while the premium index reflects the current deviation between perp and spot. For example, if the fixed interest rate is 0.01% and the premium index is 0.02%, the funding rate would be 0.03% for that period. On platforms like Coinbase, this rate is applied hourly, whereas on many other exchanges funding is exchanged every eight hours.

Funding rates are generally determined by market demand. When there is strong demand for long positions, heavy buying pushes the perpetual contract price above the spot price, leading to a positive premium index and thus a positive funding rate. Longs are then required to pay shorts at each funding interval, increasing the cost of maintaining a leveraged long position. If demand swings toward shorts, the perpetual price can fall below spot; the premium index turns negative, and shorts must pay funding to longs. This mechanism effectively embeds a floating interest rate into the derivative, aligning its price with the underlying asset over time.

Funding Rates As A Sentiment Indicator

Because funding rates directly reflect the balance of leverage between longs and shorts, they are widely used as a real‑time sentiment indicator. Analytics from bitcoin derivatives markets note that a negative funding rate typically means traders are predominantly taking short positions and are overall bearish, expecting the price to move lower. Persistent positive funding, by contrast, suggests that longs dominate and are willing to pay to maintain bullish exposure. These patterns can be interpreted in different ways: momentum traders may see positive funding as confirmation of an uptrend, while contrarians may view very high positive funding as a sign of froth and elevated liquidation risk.

Negative funding is particularly interesting in the context of rising spot prices. Market reports have highlighted episodes where bitcoin’s price has rallied toward new highs even as funding rates became deeply negative, indicating that short sellers were increasingly crowded. A mid‑April 2026 analysis from a major asset manager pointed to two historically bullish signals for bitcoin: negative funding rates and a clustered hash rate drawdown, all while volatility was cooling. The combination suggested that speculators were betting against the rally even as miners were under some pressure, a setup that in past cycles had sometimes preceded sharp squeezes higher. While such historical analogies are far from deterministic, they illustrate how funding rates can complement on‑chain metrics and volatility indicators in gauging market positioning.

For traders, the funding rate is both a cost and a signal. A long‑term bullish investor might be reluctant to hold a highly leveraged long perpetual if funding is persistently positive and high, as the cumulative funding payments could erode returns or even turn a profitable price move into a net loss. A market‑neutral trader, on the other hand, might deliberately construct a basis trade by buying spot bitcoin and shorting the perpetual contract when funding is significantly positive, capturing the funding payments as yield while remaining roughly hedged on price. In effect, this transforms the funding rate into an interest rate on capital deployed in a delta‑neutral strategy.

Basis Trades And The DeFi “Risk‑Free” Rate

The yields from such basis trades are often discussed alongside DeFi lending yields as part of crypto’s evolving notion of a “risk‑free” rate. Research from Galaxy Digital, for example, argues that DeFi’s risk‑free rate can be approximated by the returns on low‑risk strategies such as lending high‑quality stablecoins to overcollateralized borrowers or implementing delta‑neutral basis trades that harvest funding and term structure spreads. This rate, they note, cannot be too high without causing problems: if the effective risk‑free rate on DeFi platforms is elevated, borrowers—who represent capital demand—face sky‑high interest rates, making DeFi liquidity uncompetitive relative to broader capital markets.

Conversely, when macro risk‑free rates, such as T‑bill yields, rise, the ceiling for sustainable DeFi “risk‑free” yields also shifts upward. If safe yields outside crypto are 4% while on‑chain lending pools offer 2%, capital will likely flow out of DeFi until the remaining depositors are those either unable or unwilling to exit. In this environment, basis trade yields derived from funding rates become more important, because they can occasionally exceed both DeFi lending APYs and T‑bill yields when funding dislocations occur. Yet these apparent “free lunches” carry their own risks, including exchange counterparty risk, sudden shifts in funding, and basis instability during market stress.

Funding rates thus occupy a unique position in the crypto rate stack. They are truly crypto‑native, arising from the design of perpetual swaps, yet they are shaped by macro conditions and in turn influence on‑chain yields by affecting the demand for leverage and the attractiveness of basis trades. For a holistic view of rates in crypto, they must be considered alongside DeFi lending and stablecoin yields.

Inside crvUSD borrow rate.

TL;DR: crvUSD’s borrow rate has been very volatile because new mint markets (like YieldBasis) made Peg Stabilization Reserve (PSR) balances swing harder, causing sharp rate changes. Curve DAO just approved two key fixes: increasing TargetFraction to reduce sensitivity to PSR fluctuations and lowering rate0 to make borrowing cheaper. These changes should smooth volatility, stabilize the peg, and make Llamalend borrowing more predictable. More upgrades—like EMA smoothing—are coming next to further steady the system.

Stablecoins, Safe Assets, And Interest‑Bearing Tokens

Stablecoins sit at the heart of crypto liquidity, providing a relatively price‑stable medium of exchange and unit of account in an otherwise volatile ecosystem. Their design and reserve management decisions have profound implications for both crypto and traditional safe asset markets. As policy rates have risen, the yields earned on the reserves backing fiat‑pegged stablecoins have become a significant, if often opaque, revenue stream, and debates have intensified over whether and how that yield should be shared with users.

Stablecoins As Conduits To Real‑World Rates

Most major fiat‑backed stablecoins, such as USDC and similar tokens, maintain their peg by holding reserves in cash, bank deposits, and high‑quality short‑term government securities. As short‑term rates have increased, the income generated by these reserves has grown, turning some stablecoin issuers into large investors in Treasury bills and related instruments. A working paper from the Bank for International Settlements (BIS) analyzes this phenomenon and finds that stablecoin market capitalization has been on the rise since the second half of 2023, with notable increases in early and late 2024 and through 2025.

The BIS study shows that inflows into stablecoins can have measurable effects on safe asset prices, particularly at the short end of the yield curve. At the token‑blockchain pair level, the authors estimate that a 3.5 billion U.S. dollar inflow into stablecoins—roughly a two‑standard‑deviation shock—lowers three‑month Treasury bill yields by about 0.71 basis points on impact, and up to 4 basis points within 10 days. The trough effect of approximately 5 basis points is reached around day 13, and the impact remains around 3 to 4 basis points over horizons of 10 to 25 days. In other words, stablecoin demand appears to compress short‑term T‑bill yields, indicating that crypto markets are now large enough to influence safe asset pricing at the margin.

This feedback loop underscores that stablecoins are not simply passive wrappers around dollars; they are conduits through which crypto demand can affect and be affected by global interest rate conditions. When stablecoin issuance grows, issuers buy more T‑bills, nudging yields down. Lower T‑bill yields, in turn, may reduce the opportunity cost of holding stablecoins relative to direct T‑bill exposure, especially for investors who cannot easily access U.S. money markets. On the other hand, if stablecoin growth stalls or reverses during a crypto downturn, the unwind of T‑bill holdings could modestly push yields up.

The Debate Over Interest‑Bearing Stablecoins

As reserve yields have swelled, policymakers and market participants have debated whether stablecoins should pay interest directly to holders. A report from the Bank Policy Institute (BPI) examines the potential risks of allowing stablecoins to pay interest at competitive rates. The authors conclude that an expansion of interest‑bearing stablecoins could reduce traditional bank deposits by around 10% and increase banks’ cost of funds by roughly 24 basis points. Such a shift would effectively move a portion of the money creation and maturity transformation process outside the regulated banking system, raising concerns about financial stability and regulatory arbitrage.

Interest‑bearing stablecoins would also reshape rate competition within crypto. If a widely used fiat‑backed stablecoin began paying, say, 3–4% directly to holders simply for holding tokens in a wallet, many users might withdraw from DeFi lending protocols that offer similar or only slightly higher yields but carry additional smart‑contract risk. DeFi protocols might be forced to raise rates to attract deposits, which could in turn increase borrowing costs and reduce leverage, potentially dampening activity in on‑chain markets. Alternatively, they might pivot to serving as credit intermediaries for stablecoin issuers themselves, building structured products atop interest‑bearing stablecoins.

Regulators worry that if stablecoins compete head‑on with bank deposits on yield, they could accelerate digital bank runs in times of stress. The fact that stablecoins can be transferred instantly across borders and into DeFi protocols makes them powerful but also potentially destabilizing if not properly ring‑fenced and supervised. These concerns help explain why many major stablecoin issuers have so far opted not to share reserve yields directly with holders, instead monetizing the interest spread to cover costs, manage risks, or fund ecosystem development.

Stablecoin Yields, DeFi Savings, And Depeg Risk

Even without explicitly interest‑bearing stablecoins, the DeFi ecosystem effectively offers savings products by allowing users to deposit stablecoins into lending markets, liquidity pools, or structured yield vaults. As noted above, however, yields on many blue‑chip stablecoin lending pools have fallen below U.S. T‑bill rates, raising questions about whether they adequately compensate for depeg risk and smart‑contract vulnerabilities. A stablecoin is said to “depeg” when its market price deviates significantly from its intended value, often 1 U.S. dollar, due to concerns about reserve backing, regulatory actions, or sudden shifts in liquidity.

Crypto risk dashboards show that for a substantial share of stablecoin pairs, yields are now under 0.5% annualized, well below the approximately 3.8% available on T‑bills. For major lending protocols like Aave V3, many stablecoin vaults offer annualized yields starting at essentially zero. At the same time, there are still high individual liquidity pair yields on decentralized exchanges that compensate liquidity providers for risks such as impermanent loss or token “rug pulls.” For example, the Morpho protocol’s vault yields range from virtually zero to as much as 352% for the riskiest vaults, indicating that extremely high APYs are associated with niche, thinly traded, or structurally risky positions.

The security dimension is critical. Drift Protocol, for instance, reportedly offered yields of up to 16% before suffering an exploit that led to losses of roughly 280 million dollars, underscoring how smart‑contract and protocol risk can wipe out years of yield in a single incident. A separate report of a 285 million dollar crypto hack occurring in the context of falling DeFi rates further highlights that low yields do not necessarily equate to low risk; investors may be facing higher technological and governance risks while receiving lower compensation than in earlier cycles. Industry voices have remarked that, given these exposures, on‑chain yields may need to be around 18% to justify participation for many users, especially those with easy access to traditional savings instruments.

In this environment, stability and trust matter as much as headline APY. Stablecoin issuers must maintain robust reserves and transparent disclosures to minimize depeg risk, while DeFi protocols must invest in audits, bug bounties, and conservative oracle designs to reduce the probability and impact of exploits. Meanwhile, the macro rate environment sets the floor: when T‑bills yield 3.8%, a DeFi stablecoin vault offering 2% must explain what additional benefits—such as composability, flexibility, or upside optionality—it offers to compensate for the incremental risk of holding and using stablecoins on‑chain.

MakerDAO launches Enhanced DSR (EDSR) at 8% to attract DAI demand

- 2024-02governance

MakerDAO reduces EDSR from 8% to 5% after borrow-rate arbitrage drains collateral

- 2024-09launch

Liquity announces v2 with user-set interest rates and BOLD stablecoin

FOMC sets Fed funds rate to 4.25–4.5%, anchoring DeFi RWA benchmark yields

- 2025-01exploit

USD0++ depeg: Usual Money changes redemption rules, spiking Morpho and Pendle rates

Swiss National Bank cuts policy rate to zero, reviving negative-rate fears

BA Labs recommends MakerDAO cut rates 3%, targeting DAI Savings Rate of 10%

- 2025-05milestone

Circle S-1 filed for IPO, disclosing 99% of revenue tied to prevailing interest rates

CeFi And Exchange Lending Rates

Alongside DeFi, centralized finance (CeFi) platforms and exchanges have built their own lending and borrowing markets, often with structures that resemble traditional margin lending more than on‑chain money markets. These platforms control rate setting directly, sometimes in opaque ways, but their offerings influence and are influenced by DeFi rates as traders arbitrage between them.

Exchange Margin And VIP Lending Programs

Major exchanges offer margin borrowing facilities that allow users to borrow assets to trade with leverage, posting other assets as collateral. Some exchanges have launched dedicated institutional lending products with more sophisticated rate structures. Binance’s VIP Loan program is one example of an institutional‑level loan service that supports fixed and flexible interest rates and allows users to aggregate assets across accounts as collateral, enhancing capital efficiency. The flexible rate displayed to users is based on real‑time interest rates derived from market conditions, and the actual interest payable is accrued hourly and calculated based on the average real‑time rate from the previous hour.

In contrast, the program’s stable, or fixed, rate loans accrue interest daily, providing borrowers with more predictable costs at the expense of flexibility. Accrued interest is updated daily between midnight and 01:00 UTC, and there are no transaction fees for taking out VIP loans. However, borrowers remain responsible for loan interest and face a 2% liquidation fee if their collateral falls below margin requirements and positions are forcibly liquidated. Overdue loans incur triple the daily interest rate, creating a strong incentive for timely repayment.

These design choices highlight how CeFi platforms blend elements of traditional bank lending with crypto‑specific features. Hourly interest accrual and real‑time rate updates emulate the floating rates seen in DeFi but remain under centralized control, allowing the platform to adjust quickly to market stress or changes in balance sheet composition. Fixed‑rate options cater to institutions that require predictable financing costs for hedging or market‑making strategies, even if the platform must manage the residual interest rate risk internally.

CeFi Lenders Adjusting Rates Amid Volatility

Beyond exchanges, specialized CeFi lenders offer crypto‑backed loans to retail and institutional clients, often supporting dozens or hundreds of different collateral assets. These lenders adjust rates in response to volatility, liquidity conditions, and competitive pressures. Coverage of firms like CoinRabbit, which has reduced lending rates for XRP loans and more than 300 other assets, illustrates how CeFi platforms may cut borrowing costs to maintain market share or reflect lower perceived risk in certain assets, even as they warn about the potential for liquidation in volatile markets.

Such rate cuts can stimulate borrowing activity, increasing open interest in associated assets and potentially feeding into spot and derivatives trading volumes. When a lender reduces the interest rate for borrowing XRP while maintaining tight risk controls, traders who believe volatility will remain contained may be more inclined to open leveraged positions. On the other hand, if rates are cut primarily to attract volume in a highly volatile asset, borrowers may underestimate liquidation risk and become vulnerable to sharp corrections.

In this sense, CeFi lenders act as active intermediaries who translate their risk assessments and funding costs into headline borrowing rates. Unlike DeFi’s algorithmic models, these decisions can incorporate qualitative judgments, proprietary risk signals, or expectations about regulatory developments. However, this flexibility comes at the cost of transparency: users must trust that platforms maintain adequate reserves, match the term of their assets and liabilities, and will not change terms unexpectedly under stress.

Comparing CeFi And DeFi Rate Formation

The contrast between CeFi and DeFi rate formation is instructive. In DeFi, interest rates are generally determined by open, pre‑programmed formulas that react to observable on‑chain metrics like utilization. Anyone can inspect the code and see how rates will change with supply and demand, though understanding the full risk profile still requires analyzing smart‑contract logic, oracle dependencies, and governance structures. In CeFi, by contrast, rates are discretionary: risk committees may adjust them based on internal models of market risk, balance sheet constraints, or strategic considerations, and users must infer these drivers from published rate schedules and observed changes.

For sophisticated market participants, this creates arbitrage opportunities. A fund might borrow stablecoins cheaply on a CeFi platform where rates lag market conditions, then lend them at higher variable rates in DeFi, earning the spread while accepting counterparty and smart‑contract risk. Conversely, when DeFi rates fall below CeFi, traders might borrow on‑chain and lend off‑chain, if custodial limits and capital controls allow. These flows help equalize rates across venues but can also transmit stress: a security incident in a major DeFi protocol may lead CeFi platforms to tighten collateral haircuts or raise borrowing rates preemptively, while an exchange solvency scare can drive demand for on‑chain lending and push up DeFi yields.

Taken together, CeFi lending markets add another layer to the crypto rate stack, one that is closer in spirit to traditional banking but still deeply intertwined with on‑chain dynamics. For users, the key is to evaluate not only the headline interest rate but also the associated risks: custody, rehypothecation, regulatory uncertainty, and the alignment of incentives between platform and clients.

Security, Risk, And The Price Of Yield

The rate a market must offer to attract capital is inseparable from the risks that capital faces. In crypto, where code, governance, and regulatory regimes are all evolving, the risk side of the equation is unusually complex. As organic yields have declined, debate has intensified over what level of return justifies exposure to smart‑contract bugs, governance exploits, oracle failures, and regulatory shocks.

Smart‑Contract Risk And Required Yield

Crypto analysts and practitioners increasingly emphasize that DeFi yields must be evaluated on a risk‑adjusted basis. When DeFi lending rates were in the high single or low double digits while bank deposits and T‑bills yielded near zero, it was easier to argue that the spread compensated for technological and legal uncertainty. Today, with median DeFi yields on many stablecoin pools around 0–0.5% and flagship pools on Aave hovering near 2%, the comparison looks stark against roughly 3.8% on “risk‑free” T‑bills. In this context, some industry voices have suggested that on‑chain yields need to be around 18% to be compelling after accounting for risk, operational overhead, and the possibility of catastrophic loss.

Security incidents reinforce this caution. The Drift Protocol exploit, which resulted in approximately 280 million dollars in losses shortly after the platform had offered yields up to 16%, is now cited as a textbook case of how headline APYs can mask systemic vulnerabilities. Investors who chased those yields may have underestimated smart‑contract complexity, liquidity fragility, or adversarial behavior. Elsewhere, a 285 million dollar hack that rocked parts of the DeFi ecosystem amid falling yields served as another reminder that technological risks are not linearly related to APY levels; one can face high risk and low return simultaneously.

The challenge is that many DeFi protocols still set base interest rate models primarily as a function of utilization and collateral parameters, without dynamically incorporating security or governance risk signals. A protocol may continue to offer low single‑digit yields even as its governance becomes more centralized, its codebase ages, or its dependency graph grows more complex. Risk‑aware rate models like those discussed earlier offer one avenue for improvement, but they require credible risk metrics and consensus among stakeholders to be implemented. Until then, the market fills the gap with heuristics: high yields imply high risk, but low yields do not necessarily imply low risk.

Undifferentiated Lending And Rate Convergence

Another structural reason for yield compression is the undifferentiated nature of many DeFi lending markets. A widely cited analysis of DeFi yields notes that when every depositor shares the same collateral, the same parameters, and the same outcomes, there is limited room for specialization and returns naturally converge toward the broader risk‑free rate. In early DeFi, informational frictions and capacity constraints allowed some users to earn outsized yields simply by being early or technically savvy. As interfaces improved and capital poured in, these spreads narrowed.

The trajectory of the CoinDesk Overnight Rate encapsulates this convergence: from levels above 35% during the speculative frenzy of 2023 to around 3.5% in a more mature, capital‑rich market. Aave’s two largest stablecoin pools—USDT and USDC on Ethereum—jointly hold about 8.5 billion dollars in deposits yet yield just over 2%, numbers that would not look out of place in a traditional money market fund. However, unlike money market funds, these pools do not benefit from explicit government backstops, deposit insurance, or the legal clarity afforded to bank deposits or cash‑like instruments.

At the same time, the long tail of DeFi still offers eye‑popping APYs, particularly in illiquid altcoin pools or complex structured products. Platforms like Morpho can show yields ranging from near zero to more than 300% for different vaults. While some of these returns may be justified by idiosyncratic demand or temporary incentives, many rely on token emissions or leverage loops that are unlikely to be sustainable. The coexistence of near‑risk‑free yields in blue‑chip pools and extreme yields in niche markets suggests that DeFi is bifurcating into a quasi‑money‑market segment and a speculative frontier, with rates reflecting the risk profile of each.

Insurance, Risk Segmentation, And Protocol Design

One way DeFi is responding to this risk–return disconnect is through risk segmentation and on‑chain insurance. Protocols are experimenting with tranching mechanisms that divide deposits into senior and junior layers, where senior depositors accept lower yields in exchange for priority in recoveries, while junior depositors earn higher yields but absorb first losses. In principle, such structures allow rates to reflect differentiated risk classes more accurately than a single pooled APY. Similarly, some protocols offer isolated lending markets for specific assets, preventing contagion from one volatile collateral type to the entire system.

On‑chain insurance products, whether mutualized pools or parametric cover protocols, aim to reduce the tail risk faced by DeFi depositors. By paying a premium, users can insure against specific failure modes, such as smart‑contract bugs or oracle manipulation, effectively converting some of the risk into a known cost that can be priced into net yields. However, the capacity of DeFi insurance remains limited relative to total value locked, and claims processes can be contentious, highlighting the need for better risk modeling and governance.

Ultimately, the “price of yield” in DeFi will be determined not only by macro rates and leverage demand but also by the sector’s ability to credibly manage and signal risk. As long as large hacks and depegs remain frequent, investors will demand a premium to be on‑chain. When such events become rarer and risk management frameworks mature, the spread between DeFi yields and traditional benchmarks may narrow further, aligning with the idea that truly low‑risk on‑chain rates should not dramatically exceed those available in regulated markets.

A LOOK INTO COINBASE: Coinbase’s “brand refresh” is really a pivot into an everything exchange—AI agents, stocks, perps, prediction markets, regulated token sales, B2B stablecoins, SocialFi, and curated DeFi—all on crypto rails. Bull case: this makes Coinbase a global financial utility, pulls TradFi liquidity onchain, scales revenue, and accelerates mass adoption. Bear case: it dilutes altcoins, centralizes power, invites heavy regulation, and could kill degen culture as capital rotates from speculative tokens into real, cash-flow assets.

Utilization-based interest rate models can spike non-linearly under sudden liquidity withdrawal, as demonstrated when Aave borrow rates jumped from 4.4% to 33.6% following a single large ETH withdrawal.

Rate parameters in major lending protocols (MakerDAO DSR, Prisma mint fees) are set by small governance bodies or risk delegates such as BA Labs, giving concentrated actors outsized control over DeFi's effective benchmark rate.

Interest-bearing stablecoins face direct regulatory scrutiny — U.S. proposals would ban yield on stablecoins, which would eliminate the core revenue model that makes Circle's USDC 99% dependent on prevailing interest rates.

Sudden large withdrawals (Justin Sun's $570M USDT pull from Aave, $1.7B ETH exit) can collapse available liquidity and send deposit and borrow rates into extreme ranges within hours, trapping remaining participants.

DeFi-native yields and RWA demand move inversely with Fed rate cycles — a drop to near-zero rates would simultaneously compress tokenized Treasury yields (ONDO, sFRAX) and reduce stablecoin issuer revenue (Circle), repricing the entire risk-free-rate anchor for DeFi.

- Liquidation / leveraged rate riskHigh

Leveraged stability-pool and rate-farming positions (USD0++ depeg, Gearbox 10x stETH strategies) can cascade into forced liquidations when protocol redemption rules change mid-position, even without an oracle failure.

Data, Oracles, And Autonomous Rate Optimization

Behind every rate quoted in crypto, whether on‑chain or off‑chain, lies a growing infrastructure of data providers, oracles, and algorithmic agents. As this infrastructure evolves, it is reshaping how rates are discovered, transmitted, and arbitraged across the ecosystem.

Oracles And Dynamic Price Feeds For Rates

DeFi protocols rely on oracles to ingest external data—asset prices from centralized exchanges, FX rates, sometimes even off‑chain interest rates or volatility measures—and to feed that data into smart contracts that calculate collateral values, liquidation thresholds, and in some cases interest rates themselves. Oracle design has traditionally focused on price feeds for underlying tokens, but more recent proposals aim to integrate oracle‑driven rate data as a first‑class input.

For example, network upgrade proposals such as CIP‑0092 have introduced native dynamic price feeds that can supply not only token prices but also metrics relevant to rate setting, such as implied volatility or cross‑market basis spreads. In such a model, a lending protocol’s interest rate schedule might adjust automatically based on external indicators of market stress, raising rates when volatility spikes to compensate depositors or lowering them when demand collapses to maintain some activity. By automating these adjustments at the protocol level, networks hope to “boost the network economy” with more responsive, data‑driven rate mechanisms.

The integration of oracles with rate logic is not without risk. Oracle manipulation attacks, where adversaries push price feeds off‑market via thin liquidity on reference exchanges, can already trigger wrongful liquidations or allow undercollateralized borrowing. If interest rates themselves become a direct function of oracle outputs, such attacks could also distort borrowing costs, potentially enabling cheap leverage for attackers or causing sudden, cascading changes in yields. This makes oracle security and redundancy central to the integrity of crypto rate markets.

AI Copilots And Autonomous Agents Hunting Yields

Parallel to oracle innovation, a new generation of AI‑driven tools is emerging to monitor and act on rate data across chains and venues. Projects described as DeFi “copilots,” such as AIWayfinder and other on‑chain agents, are designed to transact autonomously across multiple blockchains, reallocating capital to optimize yield, funding, and risk exposure. These agents can scan DeFi lending rates, perpetual funding rates, and liquidity pool rewards in near real time, using on‑chain and off‑chain data to decide where to deploy capital.

Developers and retail traders alike are experimenting with AI‑assisted trading infrastructure that plugs into various market data APIs and middleware control planes (MCPs). Educational content shows how users can connect AI tools to financial datasets via APIs that offer institutional‑grade stock market infrastructure, and similar techniques are being applied to crypto data feeds. Internal prototypes, such as an intern‑built dashboard on the Orderly network that aggregates funding rates and auto‑trades the best spreads via the Orderly API, demonstrate that algorithmic strategies can systematically harvest rate differentials, producing attractive APYs by arbitraging differences in funding and lending across venues.

As more capital is managed by such autonomous agents, rate dislocations are likely to be arbitraged away faster, contributing to the convergence of yields across protocols and exchanges. However, these agents can also amplify systemic risk if many of them follow similar signals. In a stress event where funding rates spike or collateral values fall, AI‑driven strategies might all attempt to unwind positions or withdraw liquidity simultaneously, exacerbating slippage and triggering additional liquidations. Designing agents that incorporate not just short‑term rate optimization but also systemic risk awareness remains an open challenge.

Transparency, Composability, And Systemic Risk

One of DeFi’s defining features is composability: protocols can be stacked on top of one another, with one protocol’s tokens serving as collateral or yield‑bearing assets in another. This composability extends to rates. An increase in borrowing costs on a major lending protocol can cascade into higher funding rates on derivatives venues, as traders pass through funding costs to counterparties, and into higher yields demanded by liquidity providers on DEXs, who perceive greater price risk. Conversely, a drop in DeFi lending rates can reduce the cost of liquidity provision and arbitrage strategies, affecting spreads across markets.

The transparency of on‑chain data is a double‑edged sword in this context. On the one hand, researchers can analyze block‑by‑block flows to understand how rate changes propagate through the system, as in the risk‑aware interest rate modeling study that calibrates agent behavior using actual DeFi data. On the other hand, transparency can make herding easier: when every participant can see that a particular yield vault is attracting large flows or that funding rates are extremely skewed, they may rush to join or exit crowded trades, magnifying volatility.

Ultimately, robust rate markets in crypto will depend on a balance between automation and governance. Oracles and AI agents can improve efficiency and responsiveness, while human‑led governance can set guardrails, such as caps on maximum rates, throttles on capital inflows, or emergency circuit breakers that prevent abrupt regime shifts. As these systems mature, the lines between “rates” in DeFi, CeFi, and traditional finance may blur further, but the need for clear, risk‑aware rate design will only grow.

Putting It All Together: How Crypto Participants Should Think About Rates

With so many types of rates in play—policy rates, T‑bill yields, DeFi lending APYs, CeFi borrow rates, perpetual funding, stablecoin and basis yields—it is easy to lose the forest for the trees. A coherent framework can help market participants interpret the signal embedded in this complex rate environment.

A Conceptual Framework For Crypto Rates

One useful starting point is to view crypto rates as a stack built atop the traditional risk‑free rate. At the base is the short‑term government bond yield curve and central bank policy rates: the federal funds rate at 3.50%–3.75% and three‑month U.S. T‑bills around 3.8% currently represent the opportunity cost of holding any risky asset denominated in dollars. Above that lies a quasi‑risk‑free layer of crypto, comprising fully reserved stablecoins and tokenized T‑bill products, where the main risks are custodial and regulatory rather than market.

The next layer consists of low‑risk DeFi yields, such as lending blue‑chip stablecoins on major protocols to overcollateralized borrowers, or delta‑neutral basis trades that harvest funding or term spreads on liquid derivatives. These rates should, in principle, offer a modest premium over the traditional risk‑free rate to compensate for smart‑contract, oracle, and exchange risks. Above that are higher‑risk DeFi and CeFi yields, including altcoin lending, leveraged liquidity provision, and yield farming strategies with complex, path‑dependent dynamics. Here, double‑digit APYs may be justified only if investors understand that they are underwriting significantly higher probabilities of large losses.

Perpetual funding rates cut across these layers: at times they can be harvested as near‑risk‑free yield in basis trades, while at other times they represent a cost of speculative leverage that signals froth or panic. Stablecoin yields, whether explicit via interest‑bearing designs or implicit via DeFi lending, bridge the gap between fiat rates and on‑chain returns. In evaluating any specific rate, investors should ask three questions: how does it compare to the risk‑free rate, what incremental risks are being taken to earn it, and how might macro conditions or protocol design changes alter it over time.

Reading The Rate Environment Across Market Cycles

Rates are not static; they move with market cycles. In a high‑rate environment, like the current one where the Fed has held the funds rate at 3.50%–3.75% for multiple meetings and short‑term Treasuries yield close to 4%, it is natural for safer yields to crowd out marginal DeFi and CeFi opportunities. DeFi lending pools see reduced borrowing demand, pushing APYs down, while stablecoin issuers earn more on reserves. Crypto prices may still appreciate if driven by adoption or narrative, but the bar for leveraged speculation is higher.

As macro conditions change and central banks eventually pivot toward cutting rates—whether due to slowing growth, disinflation, or financial stability concerns—liquidity tends to return to risk assets, including crypto. Educational resources emphasize that interest rate cuts are often followed by increased volatility in crypto markets and, over the long run, can be favorable for assets like bitcoin by increasing the available liquidity for riskier investments. In those periods, DeFi borrowing demand may rise, funding rates may turn positive and elevated, and yields across the crypto rate stack may expand, at least temporarily.

Market cycles also shape the sign of certain rates. During exuberant bull markets, perpetual funding is commonly positive, reflecting net long leverage, and yields in DeFi lending are elevated as traders borrow stablecoins to chase returns. During bear markets or sideways consolidations, funding can turn persistently negative as hedgers and short‑biased traders dominate, and DeFi yields may compress toward or even below risk‑free benchmarks as borrowing demand dries up. Episodes where negative funding coincides with rising prices, as seen in some recent bitcoin rallies toward 76,000 dollars, can signal strong latent demand and risk of short squeezes.

Understanding where the market is in this cycle helps contextualize individual rate observations. A 10% APY in a world where T‑bills yield 0.5% is very different from the same 10% when T‑bills yield 4% and large hacks are frequent. Similarly, a slightly negative bitcoin funding rate might be benign during a slow grind higher but ominous if it reflects aggressive hedging by large holders ahead of known catalysts. Context is everything.

Implications For Stablecoins, DeFi Protocols, And Traders

For stablecoin issuers, the rate environment raises strategic questions about whether to share reserve yields with users, how to manage maturity and duration risk in reserve portfolios, and how to prepare for potential regulatory changes regarding interest‑bearing stablecoins. The BIS finding that stablecoin inflows compress T‑bill yields suggests that as stablecoins grow, they may become systemically important holders of safe assets, inviting closer scrutiny. BPI’s warning that interest‑bearing stablecoins could reduce bank deposits by 10% and raise bank funding costs by 24 basis points underscores the stakes.

DeFi protocols must design interest rate models that remain competitive yet sustainable. If base lending rates are too low compared with T‑bills and CeFi, capital will leak out of DeFi; if they are too high, borrowers may be discouraged and risk may be mispriced. Incorporating risk‑aware mechanisms that respond to volatility and liquidity metrics, rather than solely to utilization, can help align rates with actual risk exposures. Protocols also need to consider how their rate structures interact with governance token incentives, insurance pools, and composability with other protocols, lest they create hidden leverage loops.

For traders and investors, the practical advice is to treat all crypto rates as prices on specific bundles of risk. A DeFi stablecoin APY should be compared not just to nominal T‑bill yields but also adjusted for smart‑contract and depeg risk. A perpetual funding rate should be evaluated in light of basis stability, exchange solvency risk, and the likelihood of regime shifts. A CeFi loan rate must be weighed against counterparty risk and the possibility of withdrawal restrictions. In all cases, it is essential to distinguish sustainable, organic yields derived from genuine borrowing demand or structural spreads from transient, incentive‑driven yields that depend on token emissions or marketing budgets.

Conclusion

Rates are the connective tissue linking crypto markets to the broader financial system. From the Federal Reserve’s policy rate at 3.50%–3.75% and three‑month T‑bills around 3.8%, through stablecoin reserve yields and DeFi lending APYs, to perpetual funding rates and CeFi borrowing costs, each rate reflects a particular balance of time preference, risk, and liquidity. In recent years, rising macro rates and the maturation of DeFi have led to a dramatic compression of on‑chain yields in blue‑chip pools, even as isolated pockets of very high APY persist in riskier corners of the market. At the same time, security incidents and depegs have reminded investors that crypto rate markets still carry unique technological and governance risks that must be priced into any rational assessment of returns.

DeFi lending protocols primarily use utilization‑based, algorithmic interest rate models, but cutting‑edge research is pushing toward risk‑aware designs that optimize the risk‑adjusted P&L of liquidity pools. Empirical studies of bitcoin lending highlight how collateral ratios, price momentum, and aggregate loan volumes jointly determine interest rates, creating complex “seesaw” dynamics. Perpetual futures funding rates serve both as an anchoring mechanism for perpetual prices and as a real‑time sentiment indicator, with negative funding in rising markets often interpreted as a contrarian bullish signal. Stablecoins, by channeling demand into T‑bills, have begun to affect safe asset prices at the margin, while debates over interest‑bearing stablecoins raise important questions about the future of deposits and bank funding.

On the infrastructure side, oracle systems and AI‑driven agents are making rate markets more responsive and integrated, but also potentially more prone to rapid contagion when shocks occur. CeFi lending and margin products add a discretionary layer to rate setting that can complement or compete with algorithmic DeFi rates, opening arbitrage channels but also introducing counterparty risk. In this complex landscape, understanding rates is not a niche skill but a prerequisite for informed participation in crypto markets.

Outlook

Looking ahead, the evolution of rates in crypto will likely be shaped by three intertwined forces. First, the macro environment: as inflation and growth dynamics shift, central banks will adjust policy rates, influencing the baseline against which all crypto yields are measured. A sustained decline in traditional risk‑free rates would once again make on‑chain yields relatively more attractive, potentially reviving leverage demand and elevating DeFi borrow and funding rates. Second, regulatory developments around stablecoins and DeFi will determine how much of the traditional money market and credit intermediation stack migrates on‑chain and under what constraints. Rules governing interest‑bearing stablecoins, tokenized T‑bills, and DeFi lending platforms will directly affect who can offer which rates to whom.

Third, technological progress in smart‑contract security, oracle design, and AI‑assisted capital allocation will influence the risk side of the equation. If protocols can significantly reduce the frequency and severity of exploits and depegs, the risk premium embedded in DeFi rates may narrow, bringing them closer to traditional benchmarks and cementing DeFi’s role as a programmable money market layer. Conversely, if security incidents continue at scale, investors may demand persistently higher yields to remain on‑chain, or may retreat to tokenized representations of traditional instruments that offer clearer protections.

In all scenarios, rates will remain a central lens through which to view crypto’s integration with, and divergence from, legacy finance. For builders, regulators, and traders alike, staying attuned to the shifting landscape of policy rates, stablecoin yields, DeFi APYs, and derivatives funding will be essential to navigating the next phase of digital asset markets.

Latest Rates news

Smoothing crvUSD Borrow RatesInside crvUSD borrow rate.A LOOK INTO COINBASE:

Coinbase’s “brand refresh” is really a pivot into an everything exchange—AI agents, stocks, perps, prediction markets, regulated token sales, B2B stablecoins, SocialFi, and curated DeFi—all on crypto rails. Bull case: this makes Coinbase a global financial utility, pulls TradFi liquidity onchain, scales revenue, and accelerates mass adoption. Bear case: it dilutes altcoins, centralizes power, invites heavy regulation, and could kill degen culture as capital rotates from speculative tokens into real, cash-flow assets.Federal Reserve cuts rates to three-year low after fractious meeting. Three top US central bankers object to move in biggest revolt since 2019. The benchmark rate was cut by a quarter point to between 3.5 to 3.75 per cent as widely anticipated by Wall Street. It marked the third reduction in borrowing costs in a row. FedWatch shows a 69.4% rise in the probability of the Federal Reserve cutting interest rates by 25 basis points in December.

FedWatch shows a 69.4% rise in the probability of the Federal Reserve cutting interest rates by 25 basis points in December. Lista DAO flags mounting risks in MEVCapital’s USDT Vault and Re7Labs’ USD1 Vault as collateral faces soaring borrowing rates and no repayments, urging both projects to act immediately

Lista DAO flags mounting risks in MEVCapital’s USDT Vault and Re7Labs’ USD1 Vault as collateral faces soaring borrowing rates and no repayments, urging both projects to act immediatelySources

- https://tradingeconomics.com/united-states/interest-rate

- https://www.youtube.com/watch?v=UqNHwZkgXAk

- https://x.com/DecryptMedia/status/2066953516992610615

- https://arxiv.org/html/2502.19862v1

- https://www.vaneck.com/us/en/blogs/digital-assets/matthew-sigel-vaneck-mid-april-2026-bitcoin-chaincheck/

- https://www.galaxy.com/insights/research/defis-risk-free-rate

- https://www.bis.org/publ/work1270.pdf

- https://www.coinbase.com/learn/perpetual-futures/understanding-funding-rates-in-perpetual-futures

- https://www.bitcoinmagazinepro.com/charts/bitcoin-funding-rates/

- https://bpi.com/the-risks-from-allowing-stablecoins-to-pay-interest/

- https://wealthx.com/daily-news/a-285-million-crypto-hack-and-falling-rates-rock-defi-world

- https://www.binance.com/vip-loan

- https://x.com/top7ico/status/2062136843412312432

- https://www.sciencedirect.com/science/article/abs/pii/S0275531921000647

- https://coinledger.io/learn/how-do-interest-rates-impact-crypto-prices

- https://seekingalpha.com/article/4912352-time-to-start-diversifying-away-from-ai

- https://www.youtube.com/watch?v=dw4hZ4rLbso

- https://www.youtube.com/watch?v=kSqdrx6qcxE

- https://cryptorank.io/news/feed/03172-is-defi-yield-too-low-attract-on-chain-users

Community notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…