Explainer on how the U.S. Federal Reserve shapes crypto via interest rates, bank regulation, stablecoin rules, CBDC politics, and payment access, with analysis of Kraken, skinny master accounts, FedNow, and Bitcoin’s role in the evolving dollar system.

+12 sources across the wider coverage universe

Fed's reliance on third-party data highlights stablecoin oversight gaps2026-04

Fed's reliance on third-party data highlights stablecoin oversight gaps2026-04 U.S. Senate passes housing bill containing a four-year ban on a Federal Reserve CBDC, advancing efforts to formally block a digital dollar despite limited Fed development2026-06

U.S. Senate passes housing bill containing a four-year ban on a Federal Reserve CBDC, advancing efforts to formally block a digital dollar despite limited Fed development2026-06 Trump order pushes US regulators to streamline rules and expand Federal Reserve access so fintech and digital asset firms can integrate into traditional finance while preserving safeguards.2026-05

Trump order pushes US regulators to streamline rules and expand Federal Reserve access so fintech and digital asset firms can integrate into traditional finance while preserving safeguards.2026-05 Kraken becomes first crypto firm to win a Federal Reserve master account, gaining direct access to Fedwire interbank payments2026-03

Kraken becomes first crypto firm to win a Federal Reserve master account, gaining direct access to Fedwire interbank payments2026-03 A criminal investigation into Jerome H. Powell, Federal Reserve chair, has been opened by U.S. attorney’s office in the District of Columbia over the central bank’s renovation of its Washington headquarters and whether Mr. Powell lied to Congress about the scope of the project. Jerome H. Powell has posted this video in response2026-01

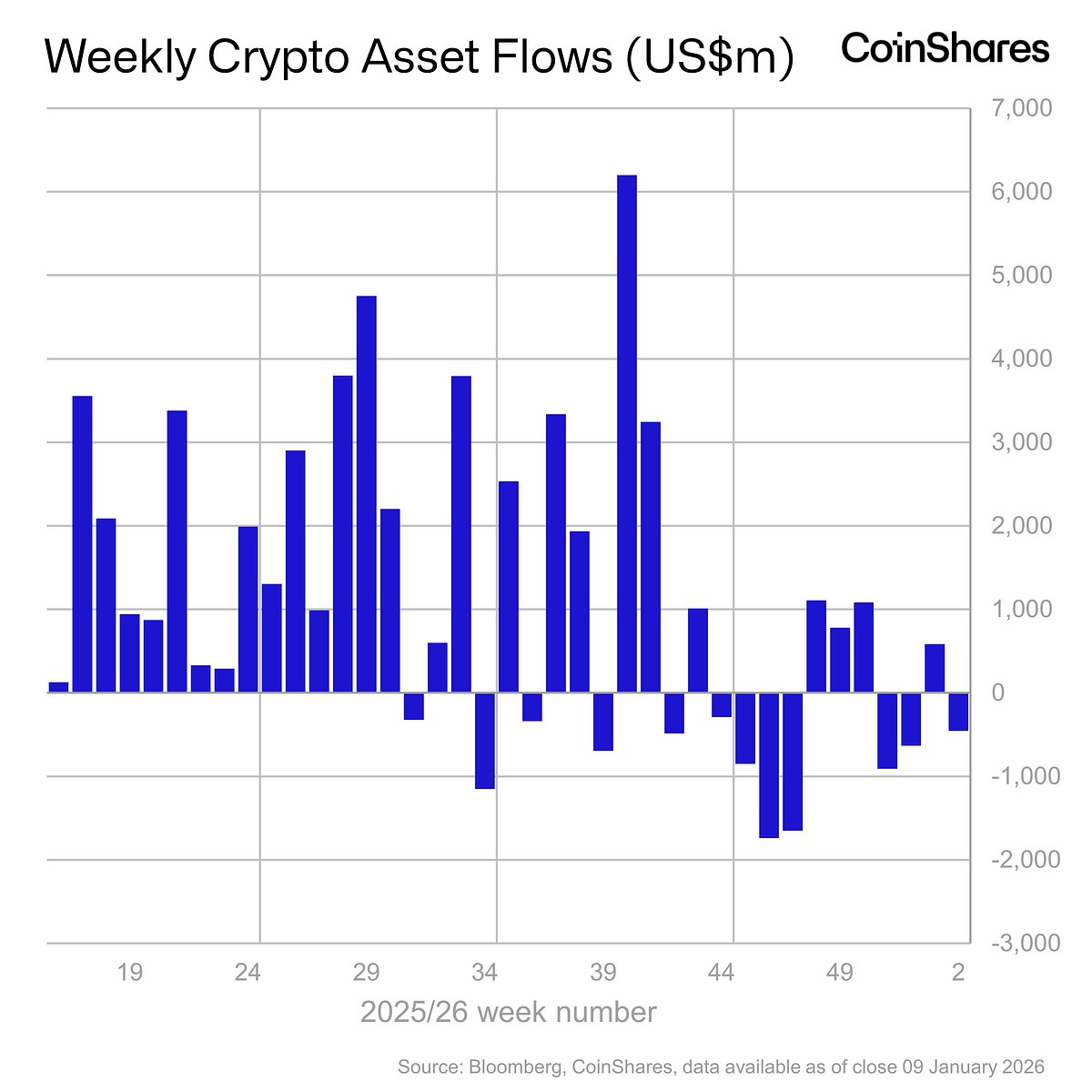

A criminal investigation into Jerome H. Powell, Federal Reserve chair, has been opened by U.S. attorney’s office in the District of Columbia over the central bank’s renovation of its Washington headquarters and whether Mr. Powell lied to Congress about the scope of the project. Jerome H. Powell has posted this video in response2026-01 Digital asset funds saw $454 million in weekly outflows, extending a four-day $1.3 billion withdrawal streak that nearly erased $1.5 billion in year-to-date inflows as expectations for a March Federal Reserve rate cut faded.2026-01

Digital asset funds saw $454 million in weekly outflows, extending a four-day $1.3 billion withdrawal streak that nearly erased $1.5 billion in year-to-date inflows as expectations for a March Federal Reserve rate cut faded.2026-01

The Federal Reserve, Crypto, And The Future Of U.S. Money

The United States’ central bank, known as the Federal Reserve or simply “the Fed,” is the institution that manages the dollar’s supply, steers interest rates, safeguards the banking system, and operates critical payment rails that underpin both traditional finance and the crypto on‑ and off‑ramps that connect to it. For anyone in crypto—whether building stablecoins, trading Bitcoin, or running a payments startup—the Fed’s decisions on rates, regulation, and payment access are now among the most important forces shaping the industry’s opportunities and constraints.

Understanding how the Fed is structured, what its legal mandate is, and how its tools work is essential context for making sense of crypto price cycles, bank‑issued stablecoins, master‑account fights like Kraken’s, and the long political battle over whether the United States should ever issue a central bank digital currency. The Fed is at once a creator of money, a prudential supervisor, a payments infrastructure operator, and a political lightning rod, and each of those roles now intersects with digital assets in different ways. Its monetary policy decisions on the federal funds rate influence liquidity conditions that can amplify or crush speculative booms in Bitcoin and DeFi, while its regulatory choices determine how banks can custody crypto, issue stablecoins, or provide access to Fed payment rails. Recent developments—from a congressional moratorium on a Fed CBDC to new proposals for “skinny” master accounts for payment innovators and draft rules that would force stablecoin issuers to run bank‑style customer identification programs—signal a shift from treating crypto as an external curiosity to integrating it into the core of the dollar system on the Fed’s terms. This explainer surveys the Fed’s mandate and tools, traces how they interact with crypto markets and regulation, and outlines what a crypto‑aware Fed means for builders, traders, and policymakers over the coming decade.

The Federal Reserve’s Mandate, Structure, And Core Functions

A dual mandate central bank at the heart of the dollar system

The Federal Reserve System is the central bank of the United States, created by Congress in 1913 to provide a more stable and secure monetary and financial system after repeated banking panics. It has a complex, quasi‑federal structure combining a Board of Governors in Washington, D.C., and twelve regional Federal Reserve Banks, reflecting an early political compromise between centralized federal control and regional banking interests. By statute, the Fed’s modern monetary policy mandate is to promote maximum employment, stable prices, and moderate long‑term interest rates, a formulation often described as its “dual mandate” of balancing employment and inflation objectives. In practice, this mandate gives the Federal Open Market Committee (FOMC) considerable discretion to decide how aggressively to fight inflation versus supporting growth, which makes its reading of economic data crucial for markets.

Beyond monetary policy, the Fed performs several additional functions that place it at the center of the U.S. financial system. It promotes the stability of the financial system and seeks to contain systemic risks through active monitoring of markets and institutions, and it directly supervises many banks and bank holding companies for safety and soundness. It fosters payment and settlement system safety and efficiency by operating services such as Fedwire, the automated clearing house (ACH) network, and, more recently, the FedNow instant payment service, all of which facilitate dollar transactions domestically and, indirectly via correspondent banking, internationally. The Fed also plays a consumer protection role, enforcing certain federal laws that aim to ensure fair treatment of consumers in credit and payment markets, though other agencies like the Consumer Financial Protection Bureau share that space. This combination of monetary policy, prudential supervision, and payments infrastructure means that even though the Fed does not directly regulate decentralized protocols, nearly every U.S. dollar touchpoint of the crypto economy is ultimately linked to the Federal Reserve System.

The Fed’s governance is deliberately insulated from day‑to‑day partisan politics, but it is not fully independent. Members of the Board of Governors, including the Chair, are nominated by the President and confirmed by the Senate, and Congress can alter the Fed’s mandate or authorities by statute. The FOMC, which sets short‑term interest rate targets and decides on asset purchases or sales, blends the Board with presidents of regional Reserve Banks, who themselves are appointed through a mix of regional and Board processes. This design aims to insulate technical decisions about interest rates and liquidity from political cycles, while still anchoring the institution in democratic oversight. For crypto, this governance structure means that today’s leadership—such as a chair whose financial disclosures now routinely include crypto and AI investments—can influence tone and priorities, but the underlying framework within which the Fed operates is set by law and evolves only slowly.

Monetary policy tools: rates, balance sheet, and guidance

Monetary policy is the area where markets feel the Fed’s influence most directly, and where crypto traders often focus first. The Fed’s primary monetary policy instrument is the target range for the federal funds rate, which is the interest rate banks charge one another for overnight borrowing of reserves held at the Fed. By setting a target range, currently 3.50 to 3.75 percent as of a March 2026 FOMC decision to hold rates steady, and using open market operations and administered rates to keep the effective fed funds rate within that band, the Fed influences broader financial conditions, including yields on Treasury securities, bank lending rates, and asset valuations. When the Fed wants to stimulate the economy, it typically lowers the target range, making borrowing cheaper and encouraging credit expansion; when it wants to cool inflation, it raises the target range, tightening financial conditions.

The mechanics of how the Fed moves the fed funds rate involve several interlocking tools. Open market operations—buying or selling U.S. government securities in the open market—alter the quantity of reserves in the banking system, influencing the supply and demand dynamics in the overnight funds market. The interest the Fed pays on reserve balances and the rate offered in its overnight reverse repurchase facility provide floor and ceiling constraints that help keep the effective federal funds rate within the target range. During extraordinary periods, such as the post‑2008 financial crisis or the early stages of the COVID‑19 pandemic, the Fed has also turned to large‑scale asset purchases, commonly referred to as quantitative easing, to inject additional liquidity into the economy and compress long‑term interest rates. Conversely, when it wants to normalize or tighten policy after such episodes, it can allow its balance sheet to run off by not reinvesting maturing securities, a process often called quantitative tightening.

Another important tool, particularly for expectations‑driven markets like crypto, is forward guidance. Forward guidance consists of the Fed’s descriptions of its likely future policy path, communicated through FOMC statements, economic projections, and speeches by policymakers. By signaling how long rates might stay high or low, or under what conditions they might change, the Fed shapes market expectations that feed into current asset prices. For example, when Federal Reserve Governor Christopher Waller delivered a hawkish speech backing removal of the Fed’s “easing bias” and emphasizing that future rate hikes could not be ruled out, market participants adjusted their expectations about the path of rates, affecting yields and risk asset valuations even though no immediate move occurred. For crypto, forward guidance can amplify or dampen cycles, as traders update their assumptions about dollar liquidity, leverage costs, and the opportunity cost of holding non‑yielding assets like Bitcoin.

Supervision, stability, and the Fed as bank regulator

In addition to steering the macroeconomy, the Fed is a prudential supervisor charged with promoting the safety and soundness of banks and the stability of the financial system more broadly. It supervises bank holding companies, certain state‑chartered banks that are members of the Federal Reserve System, and systemically important financial institutions, assessing their capital, liquidity, risk‑management practices, and governance. Through onsite exams, horizontal reviews, and rulemaking under statutes like the Bank Holding Company Act and the Bank Secrecy Act (in coordination with other agencies), the Fed can shape what kinds of assets banks hold, how they manage counterparty exposures, and how they engage with novel activities, including crypto assets.

This supervisory role gives the Fed substantial indirect influence over the crypto ecosystem. Banks are the key gateway for fiat inflows and outflows to exchanges, stablecoin issuers, and fintech platforms, and their access to central bank money and Fed payment services is conditioned on satisfying supervisory expectations. When the Fed signals heightened concern about crypto‑asset risks, banks may tighten relationships with exchanges or service providers; when it rescinds restrictive guidance, it can ease a perceived chill without necessarily embracing all activities. For example, the Fed’s 2025 decision to withdraw earlier supervisory letters that had required state member banks to provide advance notification of planned crypto‑asset activities signaled a shift toward monitoring such activities through the normal supervisory process rather than through bespoke pre‑clearance, even as underlying safety and soundness standards remained. This type of move can be read by the market as cautiously reopening space for innovation under the existing bank‑regulatory framework.

Financial stability is another lens through which the Fed views crypto. Even if the Fed does not regulate decentralized protocols, it monitors whether crypto‑related activities could propagate stress into the banking system or broader markets, for instance through leveraged exposures, stablecoin runs, or dependence on uninsured deposits. Concerns of this kind have motivated joint agency statements about the risks of holding or taking crypto collateral on bank balance sheets, as well as efforts to clarify how stablecoin arrangements intersect with bank‑like functions. As crypto integrates more deeply with traditional finance, especially via bank‑issued stablecoins and tokenized deposits, the Fed’s stability mandate will increasingly drive its stance toward digital asset intermediation.

The Fed as payment system operator and its relevance for crypto

Finally, the Fed is a major operator of payment and settlement systems. It runs Fedwire Funds and Fedwire Securities, which settle large‑value payments and government securities transactions in central bank money, as well as the ACH network for batch retail payments. In 2023, the Fed launched FedNow, a real‑time gross settlement service that allows participating financial institutions to send and receive instant payments 24 hours a day, seven days a week, with finality. FedNow differs from legacy systems like ACH and Fedwire by settling payments individually and irrevocably at any hour, rather than in batches or only during business hours, and it is aimed at enabling instant wage payments, bill payments, and business‑to‑business transfers in central bank money.

For crypto markets, the Fed’s role in payments matters because it defines the infrastructure through which fiat legs of crypto trades settle and through which stablecoin reserves are held and moved. Banks with master accounts at the Fed can settle U.S. dollar transactions directly on Fed rails such as Fedwire and FedNow, bypassing intermediary correspondent banks, which can lower costs and speed up fiat transfers to and from exchanges or stablecoin treasuries. The expansion of FedNow and the debate over whether non‑bank payment innovators and crypto‑focused institutions should have some form of direct access to Fed payment services go directly to competitive dynamics between blockchain‑based settlement and central bank‑operated instant payments. As later sections explore, the question of who can plug into the Fed’s pipes—via full master accounts, limited “payment accounts,” or not at all—is now a central regulatory battleground for crypto and fintech firms.

U.S. Senate passes housing bill containing a four-year ban on a Federal Reserve CBDC, advancing efforts to formally block a digital dollar despite limited Fed development

$314B of on-chain dollars already exists, led by USDT at $186B and USDC at $74.6B, so freezing a Fed CBDC mostly locks in the private-issuer model DeFi already runs on. The next fight is tokenized deposits: JPMorgan, BofA, Citi and Wells are lining up a 2027 bank-run network, and if that gets 24/7 settlement plus regulatory comfort while stablecoin yield gets squeezed, Circle/Tether keep crypto rails but banks keep the corporate balance sheets.

Readers aren't clicking the Fed for its rate-setting role — they're clicking for its power as crypto's banking gatekeeper: who gets a master account, who gets a cease-and-desist, and which firms are forced out of the US dollar settlement system entirely.↗

Monetary Policy, Interest Rates, And Crypto Markets

Why the federal funds rate matters for risk assets and Bitcoin

Crypto markets may be built on public blockchains, but they are tightly linked to the dollar funding environment that the Fed controls. The federal funds rate anchors the price of short‑term dollar funding; when that price rises, it increases the cost of leverage across the financial system and raises the yield on safe assets like Treasury bills, which in turn affects investors’ appetite for riskier exposures such as equities and digital assets. In periods when the Fed is cutting rates or holding them near zero, abundant liquidity and low opportunity costs can encourage speculative activity in assets like Bitcoin and Ether, contributing to bull markets. Conversely, when the Fed hikes rates aggressively to fight inflation, higher yields on cash and short‑term bonds can draw capital away from non‑yielding or highly volatile crypto assets.

The latest FOMC communications illustrate this dynamic. In March 2026, the Committee decided to maintain the target range for the federal funds rate at 3.50 to 3.75 percent, noting that economic activity had been expanding at a solid pace while inflation remained somewhat elevated relative to its 2 percent objective. The statement emphasized that uncertainty about the economic outlook remained high and that the Fed was attentive to risks on both sides of its dual mandate, signaling a cautious posture rather than a rapid pivot to easing. Around the same time, Governor Waller delivered a speech described as hawkish by market observers, arguing for removing explicit “easing bias” language and stressing that future rate hikes could not be ruled out if inflation proved persistent. For crypto traders, such signals mean that hopes for a quick return to ultra‑low rates—and thus to the kind of cheap leverage that fueled earlier bull cycles—should be tempered.

Crypto derivatives markets often embed these macro expectations. Perpetual swap funding rates, stablecoin borrowing costs in DeFi, and the term structure of implied volatility in options can all move as traders anticipate changes in the Fed’s stance. Although crypto is sometimes framed as “uncorrelated,” empirical behavior over the last several cycles has shown that Bitcoin and major altcoins tend to trade like high‑beta risk assets during periods of macro stress or monetary tightening. The Fed’s rate decisions and guidance thus function as a macro regime switch for digital asset markets, affecting both dollar liquidity available to buy coins and the risk premiums demanded by investors for holding them.

Inflation, liquidity cycles, and digital asset valuations

Inflation is the other key macro variable that connects the Fed’s decisions to crypto valuations. The Fed targets 2 percent inflation over the longer run and adjusts policy to try to keep actual inflation near that objective. When inflation runs well above target, as in the post‑pandemic period, the Fed typically tightens monetary policy by raising rates and shrinking its balance sheet, which can compress the valuations of long‑duration assets whose cash flows are far in the future, including growth stocks and many token projects promising future utility. When inflation is low or below target, the Fed can ease policy, lowering discount rates and supporting higher valuations.

Crypto adds an additional layer to this picture because Bitcoin, in particular, is often pitched as an inflation hedge or “digital gold” due to its capped supply and predictable issuance schedule. While some long‑term correlations between Bitcoin and measures of inflation expectations can be observed, the short‑to‑medium‑term relationship is more complicated. In practice, extreme inflation that forces the Fed into aggressive tightening can be negative for Bitcoin prices in dollar terms, because tighter policy hurts liquidity and risk appetite even if the long‑run narrative of fiat debasement becomes more salient. Conversely, when inflation has been brought closer to target and the Fed signals an eventual shift toward easing, narratives about renewed liquidity often dominate, fueling crypto rallies.

From a macro‑prudential standpoint, the Fed also cares about how leveraged crypto exposures could interact with broader liquidity cycles. Cheap funding conditions can encourage hedge funds and proprietary trading firms to lever up basis trades between spot and futures or to borrow against crypto collateral in both CeFi and DeFi structures. If a tightening cycle triggers sharp price corrections, these leveraged structures can unwind disorderly, potentially spilling back into the traditional financial system through prime brokerage relationships or bank exposures. Although this channel has been limited to date, its potential scale increases as institutional participation in crypto grows, which in turn feeds back into the Fed’s assessment of systemic risk.

Forward guidance, quantitative policy, and crypto narratives

Forward guidance and balance sheet policy can sometimes matter for crypto even more than small incremental changes in the policy rate. When the Fed communicates that rates will stay at a restrictive level “for longer,” markets may price a prolonged period of tighter financial conditions, affecting everything from venture funding for crypto startups to valuations of governance tokens whose future fee streams are highly uncertain. Conversely, hints of a future pivot to easing can catalyze narrative‑driven rallies long before the first cut actually occurs, as traders reprice path‑dependent outcomes and re‑enter risk assets.

Quantitative easing and tightening also shape the overall liquidity environment in which crypto operates. When the Fed buys large quantities of Treasuries and agency securities, expanding its balance sheet, it injects reserves into the banking system, increasing the availability of high‑quality collateral and pushing investors out along the risk curve. Some of that marginal risk‑seeking can flow into crypto, especially during periods when other asset classes look expensive. When the Fed lets assets roll off its balance sheet or sells them outright, the reverse occurs: reserves shrink, safe yields rise, and risk appetite tends to diminish. Crypto narratives often simplify these dynamics into slogans about “money printing” or “liquidity drains,” but the underlying mechanisms are more nuanced.

For crypto builders, understanding how the Fed uses its toolkit helps in planning capital raises and product launches. Launching a token in a period of aggressive tightening and hawkish forward guidance can be materially harder than doing so into a dovish or easing cycle, because investor risk tolerance and available liquidity differ. DeFi protocols whose business models depend on offering yields above prevailing risk‑free rates must calibrate their parameters to a moving benchmark set by Fed policy. In that sense, even though blockchains operate independently of any central bank, the economic conditions around them are still profoundly shaped by the Fed’s macro decisions.

The Fed’s Evolving Role In Digital Asset Regulation

Bank supervision, crypto activities, and the withdrawal of earlier guidance

Unlike securities or commodities regulators, the Fed does not regulate crypto assets directly. Its influence flows through the banks it supervises and through its control over access to central bank money and payment services. This indirect control has been salient in the way the Fed has handled banks’ crypto‑asset activities over the last several years. In 2022 and 2023, the Fed issued supervisory letters that, among other things, established an expectation that state member banks would provide advance notification of planned or current crypto‑asset activities and follow a supervisory non‑objection process for engaging in certain dollar‑token activities. These letters, combined with joint statements from the Fed, the Federal Deposit Insurance Corporation (FDIC), and the Office of the Comptroller of the Currency (OCC), were widely interpreted as signaling caution and imposing an additional procedural hurdle for banks exploring crypto services.

In April 2025, the Federal Reserve Board announced the withdrawal of this guidance. It rescinded its 2022 letter requiring advance notice for crypto‑asset activities and its 2023 letter outlining a supervisory non‑objection process for state member bank engagement in dollar‑token activities, and it joined the FDIC in withdrawing from two 2023 joint statements regarding banks’ crypto‑asset activities and exposures. The Board explained that these actions were intended to ensure that its expectations remained aligned with evolving risks and to further support innovation in the banking system, and it emphasized that banks’ crypto‑asset activities would now be monitored through the normal supervisory process rather than through bespoke notification or non‑objection mechanisms.

For crypto‑exposed banks and their partners, this shift has two sides. On the one hand, withdrawing the special notifications regime reduces legal uncertainty and the perception that crypto activities are singled out for exceptional treatment, which may encourage more banks to cautiously re‑enter digital asset custody, trading facilitation, and stablecoin‑related services. On the other hand, this does not mean a deregulatory free‑for‑all; banks remain subject to existing safety and soundness standards, anti‑money‑laundering (AML) obligations, and risk‑management expectations, and supervisors can still push back on crypto exposures they deem unsafe. Rather than codifying prescriptive rules for every crypto use case, the Fed appears to be reverting to a more principles‑based supervisory approach, in which examiners evaluate the adequacy of banks’ risk controls and compliance frameworks on a case‑by‑case basis.

The shift also reflects a broader policy context in which the executive branch and Congress have pressed regulators to support financial technology innovation while preserving core safeguards. A recent executive order on fintech innovation, for instance, directed agencies including the Fed to review their frameworks for payment access by non‑bank fintechs and digital asset firms and to identify unnecessary barriers to entry, while still maintaining safety and soundness. Senator Cynthia Lummis and other lawmakers have applauded these efforts as steps toward “equal access” to the payments system for law‑abiding innovators, even as critics warn of potential risks to financial stability and consumer protection. The Fed’s withdrawal of earlier crypto‑specific supervisory letters should be seen against this backdrop of political pressure to integrate digital asset activities into existing regulatory structures rather than ban them outright.

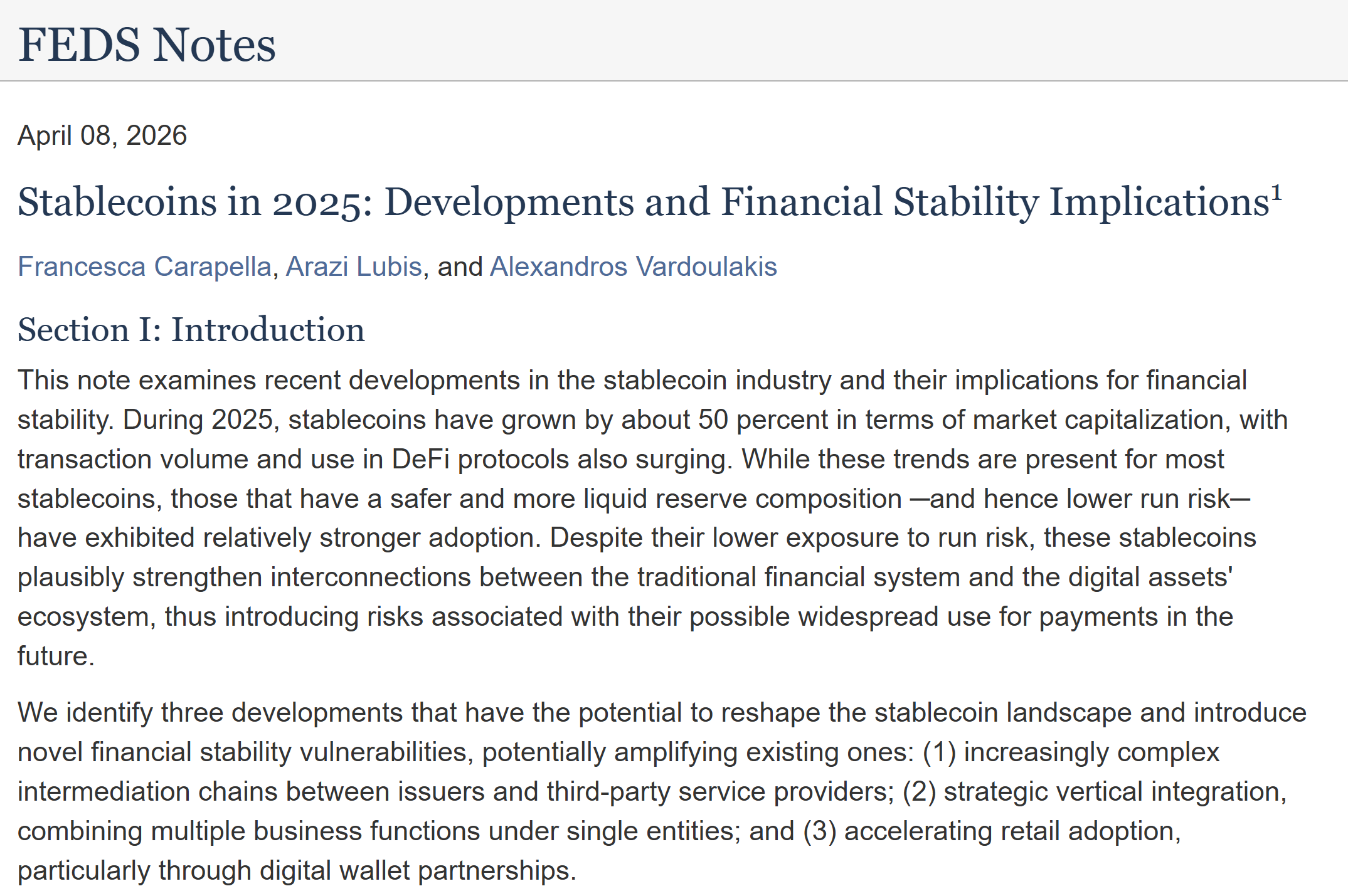

Stablecoin oversight, the GENIUS Act, and bank‑style customer identification programs

If Bitcoin is the ideological challenge to central banking, dollar‑denominated stablecoins are the practical one. Stablecoin arrangements allow users to move dollar‑pegged value across blockchains at internet speed, with potential implications for payments, capital markets, and monetary sovereignty. Policymakers have increasingly focused on bringing these arrangements within the perimeter of prudential and AML regulation. In the United States, one legislative pillar of this effort is the GENIUS Act, which directs that certain “permitted payment stablecoin issuers” be treated as financial institutions under the Bank Secrecy Act (BSA) and be required to maintain customer identification programs (CIPs). In June 2026, the Financial Crimes Enforcement Network (FinCEN) and several federal banking agencies, including the Fed, proposed a rule to implement this mandate, specifying how such issuers must identify and verify the identity of their customers.

In parallel, the Federal Reserve Board requested comment on a proposal to require certain payment stablecoin issuers subject to its oversight to maintain an effective customer identification program that is comparable to the CIP requirements for banks. The proposal would introduce requirements for these stablecoin issuers that mirror the customer identification program rules that banks must follow under the BSA, including collecting identifying information, verifying identities using risk‑based procedures, and maintaining records. Together, the GENIUS Act implementation and the Fed’s proposal signal a clear policy direction: if you are issuing dollar‑denominated tokens that function like money in payment systems, regulators will expect you to follow bank‑like AML and CIP standards.

The SEC has also weighed in with a comprehensive framework for stablecoin regulation, highlighting that stablecoin arrangements often rely on third‑party service providers and require robust oversight, including due diligence requirements for issuers and intermediaries. Among other things, the SEC framework emphasizes the need for comprehensive initial and ongoing due diligence on reserve assets, custodians, and key service providers, as well as clear disclosures about redemption rights and risks. While the SEC’s jurisdiction depends on whether particular stablecoins are deemed securities, its analysis influences broader regulatory expectations and underscores that stablecoins are not outside the reach of financial regulation.

From the perspective of crypto builders, these developments mean that the age of lightly regulated, offshore‑issued dollar tokens operating at global scale is likely to give way to a more stratified ecosystem. One layer will consist of regulated, bank‑ or bank‑like issuers in the United States and other major jurisdictions, running stablecoins with strict reserve, governance, and CIP/AML standards, potentially with direct or indirect access to central bank money. Another layer will consist of more permissive or experimental arrangements that avoid U.S. jurisdiction but face frictions when interacting with regulated institutions. The Fed’s role is not to regulate every stablecoin globally, but to set the baseline for what is acceptable when U.S. banks or Fed‑supervised entities are involved and when dollar stability and financial integrity are at stake.

CBDC debates and Congress’s temporary ban on a Fed digital dollar

Central bank digital currency (CBDC) has been one of the most contested issues at the intersection of the Fed and crypto. A CBDC is generally defined as a digital liability of the central bank that is widely accessible to the public, essentially a digital form of cash. Proponents argue that a Fed‑issued CBDC could provide safe, programmable digital money, enhance financial inclusion, and modernize payments infrastructure; critics worry about privacy, government surveillance, and disintermediation of banks. The Federal Reserve has studied CBDC design and implications and has made clear it would not issue a retail CBDC without congressional authorization, reflecting both legal and political constraints.

Congress has now moved to impose explicit limits. In a bipartisan housing bill, the U.S. Senate and House agreed on language that bans the Federal Reserve from issuing a CBDC through December 31, 2030, unless Congress acts again to change that prohibition. The bill defines a CBDC as a dollar‑denominated digital asset that is directly or indirectly issued by the Federal Reserve and intended for use by the general public, thereby capturing both direct retail designs and some intermediated models. This statutory moratorium not only prevents the Fed from launching a CBDC pilot or live system in the near term, but also reflects a broader skepticism among lawmakers about the risks of a government‑run digital dollar, especially in a political climate where control over money and data is deeply contested.

For crypto, the CBDC ban is a double‑edged sword. On one side, it removes the near‑term competitive threat that a Fed digital dollar could pose to privately issued stablecoins, giving bank‑backed and other regulated tokens more room to develop. On another, it keeps the United States on the sidelines as other jurisdictions experiment with CBDCs, which could shape the long‑term architecture of cross‑border payments and interchangeability between central bank money and tokenized assets. The Fed remains free to continue research and experimentation in a purely analytical sense, but it cannot issue or widely test a CBDC under current law. That means, for at least the rest of this decade, the primary interface between the Fed and the crypto ecosystem will be through bank supervision, payment access, and oversight of stablecoin issuers rather than via a directly issued digital dollar.

- 01Crypto bank enforcement crackdowns↗

Cease-and-desist orders against SoFi, Customers Bank, United Texas Bank, and Farmington demonstrated that the Fed could sever firms from the banking system through supervisory action alone, without legislation.

- 02Master account access fight↗

Custodia's multi-year legal battle and Kraken's eventual win crystallized whether crypto firms could ever gain direct access to Fed payment rails — a question with existential stakes for crypto-native banking.

- 03Rate decisions crashing crypto prices↗

Headlines linking Fed rate signals directly to BTC dropping below $90K on a single jobs report pulled readers tracking macro triggers for crypto volatility.

- 04Fed political leadership shakeup

Trump's firing of Lisa Cook, Barr's exit from the Vice Chair role, and Miran's narrow 48–47 confirmation signaled a possible ideological pivot toward crypto-friendlier Fed oversight.

- 05Tokenization and Fed experimentation↗

Project Agorá's 40-firm pilot, the NY Fed and BIS testing smart contracts for monetary policy, and the Fed's tokenization conference showed the central bank actively exploring digital asset infrastructure rather than merely policing it.

- 06Stablecoin regulatory gaps↗

Barr's public calls for stablecoin legislation and the Fed's acknowledged reliance on third-party data for stablecoin oversight drew readers watching whether the Fed could actually supervise a sector it didn't yet understand.

Master Accounts, Payment Access, And The ‘Skinny’ Account Debate

What a master account is and why it matters for crypto

At the heart of many recent crypto policy debates lies a seemingly technical concept: the Federal Reserve master account. A master account is the account that a depository institution holds at a Federal Reserve Bank, through which the institution can settle payments in central bank money, including via services like Fedwire, FedNow, and ACH. Holding a master account allows an institution to credit or debit balances in real time, access daylight overdrafts under certain conditions, and, for eligible institutions, earn interest on reserve balances and borrow from the discount window. In short, a master account is the key to direct participation in the core of the dollar payment system.

Traditionally, access to master accounts has been limited to banks and certain other depository institutions that meet statutory eligibility criteria and prudential standards. Non‑bank entities, including many fintech and crypto firms, must instead rely on correspondent relationships with banks that hold master accounts, adding layers of cost, complexity, and counterparty risk. As the crypto industry has grown, some firms have sought ways to gain more direct access, either by obtaining special‑purpose bank charters or by partnering with entities that can qualify. The question of who should be allowed a master account, under what conditions, has become a flashpoint in litigation and policy.

The American Action Forum’s analysis of the Kraken case illustrates these issues. Kraken’s Wyoming‑chartered special‑purpose depository institution obtained a limited scope master account that allows it to settle dollar transactions directly on Fed rails, strengthening its institutional offerings by removing some reliance on correspondent banks. However, this access is constrained: the institution does not have access to the discount window, does not earn interest on its balances, and operates under a narrow set of permissions, effectively serving as a test of a “skinny” master account concept under evolving Fed guidelines. This arrangement highlights both the potential benefits of giving crypto‑focused institutions direct payment access and the Fed’s concern with containing risks by limiting the privileges attached to such accounts.

Kraken, eligibility, and the boundaries of the banking system

Kraken’s experience underscores an unresolved question in U.S. financial law: should novel institutions that do not fit neatly into traditional categories be allowed direct access to central bank money and payment services, and if so, on what terms? Wyoming’s special‑purpose depository institution (SPDI) charter was designed in part to give digital asset firms a path to gaining Fed access by meeting certain prudential standards, without becoming full‑service commercial banks. The Fed has responded cautiously, developing frameworks for evaluating such applications that consider not only the legal eligibility of the institution but also the risks its business model could pose to the payment system and financial stability.

The limited master account granted to Kraken’s SPDI suggests that the Fed is willing to experiment but remains wary. By allowing access to payment rails while withholding other privileges like interest on balances and discount window borrowing, the Fed is effectively testing whether a narrower form of central bank account can accommodate payment innovators without fully integrating them into the safety net reserved for traditional banks. Critics argue that this creates a two‑tier system in which novel institutions face competitive disadvantages and regulatory uncertainty, while supporters counter that it appropriately recognizes differences in business models and regulatory oversight. For crypto markets, the outcome of these debates will determine whether exchanges, stablecoin issuers, and other digital asset intermediaries can ultimately plug into Fed infrastructure on more equal terms.

The broader policy challenge is to balance innovation and risk. Direct access to Fed payment services can reduce settlement risk, lower costs, and enable new business models, but it also brings the Fed closer to supervising entities that may engage in activities—such as custodying volatile digital assets or interfacing with lightly regulated offshore actors—that raise concerns about operational resilience, AML compliance, and reputational risk. The Fed’s evolving master account guidelines reflect this tension, and ongoing litigation and legislative proposals seek to clarify the criteria the central bank must apply. For crypto firms, this is not merely a legal curiosity; it is a determinant of whether they must always route dollar flows through intermediaries or can eventually operate closer to the core of the dollar system.

Governor Waller’s “payment account” proposal and Trump’s fintech executive order

One prominent attempt to bridge these competing objectives comes from Federal Reserve Governor Christopher Waller, who has proposed a concept he calls a “payment account” or “skinny” master account. In this framework, the Fed would offer a basic account that provides access to Fed payment rails for legally eligible institutions that currently conduct payment services primarily through third‑party banks. The payment account would be tailored to the needs of payment innovators that do not want or need all the features of a full master account, such as earning interest on reserves or using the discount window. Instead, it would offer limited functionality focused on payments, potentially with balance caps, no daylight overdraft privileges, and restrictions on access to certain services where the Reserve Banks cannot adequately control the risk of daylight overdrafts.

Governor Waller has explicitly referenced institutions specializing in digital assets as potential beneficiaries of such accounts, arguing that supporting those actively transforming the payment system is in the public interest so long as risks are appropriately managed. By decoupling payment access from full banking privileges, the payment account proposal aims to expand competition and innovation in the provision of payment services without undermining financial stability or extending the safety net to entities that are not subject to bank‑like supervision. For crypto firms, this could open a path to direct settlement on Fedwire or FedNow for fiat legs of crypto trades and stablecoin reserve movements, reducing dependence on a small number of crypto‑friendly banks.

The policy context for Waller’s proposal includes an executive order signed by President Donald Trump in May 2026, titled “Integrating Financial Technology Innovation into Regulatory Infrastructure.” That order directs the Federal Reserve and other regulators to evaluate their legal frameworks for Reserve Bank payment access by uninsured depository institutions and non‑bank entities, including fintech and digital asset firms, and to identify changes needed to provide appropriate, risk‑sensitive access. It also instructs agencies to streamline rules and remove unnecessary barriers to entry while preserving core safeguards around safety, soundness, and financial integrity. Senator Cynthia Lummis and other crypto‑friendly lawmakers applauded the order as putting the Fed “on notice” that it must provide equal access to the payments system for all lawful entities that meet statutory criteria, reinforcing the political pressure toward some form of payment account reform.

Together, Waller’s proposal and the executive order suggest that the U.S. is moving toward a more explicit framework for non‑traditional institutions to access Fed payment services, even if the details remain contested. For crypto and fintech firms, this represents both an opportunity and a regulatory challenge. Gaining direct access would likely come with new supervisory expectations, including robust AML/CFT controls, operational resilience standards, and possibly stablecoin‑specific requirements for those issuing tokens. The trajectory is away from ad hoc, case‑by‑case master account fights and toward a codified regime that defines who can connect to the Fed’s pipes and on what terms.

Politics, courts, and the future of Fed payment access

As with CBDCs, the question of payment access is not purely technocratic; it is political and legal as well. Congress can legislate criteria for access, as some proposed bills have sought to do, and courts can review the Fed’s decisions for consistency with statutes and administrative law principles. The Trump administration’s executive order accelerated these debates by explicitly pushing regulators to integrate fintech and digital asset firms into the traditional payments infrastructure, framing it as a competitiveness and innovation imperative. At the same time, skeptics in Congress and among public interest groups caution that widening access to Fed accounts could blur the line between banks and non‑banks, potentially undermining the effectiveness of prudential regulation and the stability of the payment system.

For the Fed, this puts a premium on designing access frameworks that are transparent, legally defensible, and clearly tied to risk‑based criteria rather than ad hoc discretion. The proposed payment account or skinny master account model is one attempt to thread this needle, but implementing it will require detailed rulemaking, supervisory coordination, and possibly statutory changes. From the perspective of crypto firms, engagement in these processes—through public comment, industry coalitions, and dialogue with policymakers—will be crucial. Whether Kraken’s limited master account remains a one‑off experiment or becomes the prototype for a broader class of regulated, crypto‑connected payment institutions will shape the architecture of the U.S. digital asset ecosystem for years to come.

Payments Innovation: FedNow, Stablecoins, And The 24/7 Settlement Race

How Fed payment rails work today

To understand how crypto and the Fed intersect on payments, it helps to distinguish between existing Fed payment rails and blockchain‑based systems. Fedwire Funds is a real‑time gross settlement system used primarily for large‑value, time‑critical payments between banks and other financial institutions, settling each transaction individually in central bank money during business hours. The ACH network, by contrast, is a batch system for lower‑value payments like payroll, bill payments, and many consumer transactions, where transfers are netted and settled at intervals. Both have been workhorses of the U.S. payment system for decades, but neither alone provides ubiquitous, 24/7 instant settlement for retail payments.

FedNow, launched in 2023, is meant to fill that gap. It is a real‑time gross settlement service that allows participating depository institutions to send and receive instant payments around the clock, every day of the year. Unlike ACH, FedNow settles each payment individually and immediately, with finality, rather than netting transactions. Unlike Fedwire, it operates at all hours, including nights, weekends, and holidays, and is designed to handle a broad range of use cases, from person‑to‑person transfers to business payments to bill settlements. Participation is voluntary, but the Fed’s role as operator and regulator of core payment infrastructure gives FedNow the potential to become a widely used platform for instant dollar transfers.

For institutions active in crypto, FedNow’s significance lies in its potential to enable near‑instant fiat settlement to and from exchanges, stablecoin issuers, and over‑the‑counter desks. If a bank serving a crypto exchange participates in FedNow, it can credit customers or counterparties with funds in real time once incoming transfers settle, reducing reliance on cut‑off times and batch processes. This could narrow one of the experiential advantages that stablecoins and crypto‑native payment systems have enjoyed: the ability to move value 24/7. At the same time, FedNow is an account‑based system limited to regulated institutions, and it is not programmable in the same way that smart‑contract platforms are, leaving room for complementary roles for blockchain‑based money.

Instant payments versus stablecoins for 24/7 finance

The Chicago Fed has explored how instant payment systems like FedNow and stablecoins might address settlement risk in exchange‑traded derivatives markets, particularly for weekend margin calls. One of the challenges in such markets is that price movements can occur outside of traditional banking hours, leaving exposures uncollateralized until payments can be processed. Instant payment systems operating 24/7 could reduce this gap by allowing margin to be posted at any time, while stablecoins and other tokenized forms of money could enable similar functionality on blockchain‑based settlement venues. Each approach has advantages and trade‑offs in terms of legal finality, counterparty risk, technological complexity, and integration with existing financial infrastructure.

Stablecoins excel at interoperability across platforms and jurisdictions, particularly when built on widely used public blockchains. They can be integrated directly into smart contracts, enabling automated settlement of trades, loans, and other financial arrangements. However, their stability depends on the quality and transparency of their reserves, their legal structure, and the robustness of their issuers and key service providers. Regulators worry about run risk, operational failures, and AML gaps, especially when stablecoins are issued by entities outside the traditional supervisory perimeter. Instant payment systems like FedNow, by contrast, settle in central bank money and are operated by a trusted public institution, but they lack native programmability and are limited to participants that meet depository institution criteria.

For crypto markets, the likely outcome is not a binary choice but a layered ecosystem. At the core, FedNow and similar systems will enable 24/7 settlement in sovereign money for regulated institutions, improving liquidity management for banks and large intermediaries. On top of that, bank‑issued stablecoins and tokenized deposits could bridge between these rails and public blockchains, allowing programmable, on‑chain representations of claims on central‑bank‑backed balances. Finally, public, non‑bank stablecoins will continue to operate in parallel, particularly in cross‑border and DeFi contexts, though their integration with the regulated financial system will depend on how they adapt to evolving CIP and prudential standards. The Fed’s stance will be central at each layer, from rules for FedNow participation to oversight of bank‑issued tokens and expectations for banks interacting with third‑party stablecoins.

Bank‑issued stablecoins, SoFi‑style projects, and direct Fed connectivity

One of the most significant developments at the intersection of the Fed and crypto is the emergence of bank‑issued stablecoins and tokenized deposits. In these models, a regulated U.S. bank issues a digital token that represents a redeemable claim on deposits held at the bank, which in turn are backed by reserves that may be held partly at the Fed. Recent launches, such as SoFiUSD by a regulated U.S. bank, illustrate this trend toward integrating stablecoin functionality with the traditional banking system. These bank‑issued tokens aim to combine the programmability and interoperability of blockchain‑based assets with the safety and regulatory oversight associated with insured depository institutions.

From the Fed’s perspective, bank‑issued stablecoins raise both familiar and novel questions. On one side, they may reduce certain risks associated with non‑bank stablecoins because the issuers are already subject to prudential supervision, FDIC insurance requirements for eligible deposits, and BSA/AML obligations. On another, they introduce new operational and systemic considerations, such as how large‑scale tokenization of deposits might affect the transmission of monetary policy, the stability of bank funding, and the functioning of payment systems. If tokens circulate widely on public or permissioned blockchains, they could also create new dependencies on smart‑contract infrastructure and raise questions about cybersecurity and governance.

The Fed’s proposed CIP requirements for certain payment stablecoin issuers signal that it intends to apply bank‑like standards to entities that effectively function as deposit substitutes, whether or not they are traditional banks. For banks issuing tokens, this may be relatively straightforward, as they can leverage existing AML and customer due diligence frameworks. For non‑bank issuers seeking payment access, the bar may be higher. The debate over skinny master accounts and payment accounts is especially salient here: a non‑bank stablecoin issuer that gains direct Fed payment access would occupy a hybrid position, combining features of a bank, a money services business, and a crypto protocol. Crafting appropriate oversight for such entities will be an ongoing challenge for the Fed and its fellow regulators.

- 2023-12regulatory

SoFi ceases crypto trading under Fed regulatory pressure, customers directed to Blockchain.com before Dec. 19

- 2024-12governance

Fed cuts rates to 3.5–3.75%; three governors dissent in biggest internal revolt since 2019

- 2025-01governance

Vice Chair Michael Barr announces departure, stalling prospects for crypto-friendly supervisory reform

Fed issues enforcement action (bcreg20250424) against crypto-adjacent bank

Federal Reserve monetary policy rate decision

Trump executive order directs regulators to streamline rules and expand Fed payment account access for fintech and digital asset firms

Federal Reserve issues new bank regulatory action (bcreg20260618)

Bitcoin, Competing Monies, And The Fed’s Strategic Position

Bitcoin as money, store of value, and speculative asset

Bitcoin was originally conceived as a peer‑to‑peer electronic cash system, intended to function as a form of money independent of central banks. The St. Louis Fed has analyzed whether Bitcoin functions as money and concluded that it has some characteristics that allow it to do so—such as relative ease of transfer, including across borders—but that other aspects make it less desirable for everyday transactions. Chief among these drawbacks are volatile price fluctuations and security problems in certain use contexts, which undermine its usefulness as a medium of exchange and a stable unit of account. Because money also serves as a store of value, the stability of that value is crucial, and Bitcoin’s dramatic price swings have led many users to treat it more as a speculative investment than as currency.

Former Federal Reserve Chair Janet Yellen has summarized this view by saying that Bitcoin is “not a stable source of store of value” and does not constitute legal tender, and she described it as a “highly speculative asset.” While some merchants and individuals do use Bitcoin for payments, especially in jurisdictions with weak local currencies or capital controls, its primary use in advanced economies remains as an investment or trading asset. This does not negate its monetary properties entirely; Bitcoin still functions as a kind of digital bearer asset with global liquidity. But it means that, for now, Bitcoin has not displaced the dollar or other fiat currencies as the primary medium of exchange in daily economic life.

For the Fed, Bitcoin’s rise has been both a challenge and a source of information. On one hand, Bitcoin embodies a critique of central banking, arguing that programmatic, capped supply and decentralized governance are superior to discretionary monetary policy. On another, its volatility and periodic boom‑bust cycles highlight the importance of lender‑of‑last‑resort functions and prudential oversight in maintaining financial stability. The Fed monitors Bitcoin and other crypto‑asset markets as part of its broader assessment of financial conditions, but it does not treat them as core monetary instruments. Instead, Bitcoin functions as an external, market‑based benchmark for some investors’ views on inflation, currency debasement, and geopolitical risk.

The Strategic Bitcoin Reserve proposal and potential Fed balance sheet impacts

The growing prominence of Bitcoin has nonetheless sparked proposals that would place it directly on public balance sheets. One such example is a Senate bill introduced as the “Strategic Bitcoin Reserve Act,” which would establish a Strategic Bitcoin Reserve and other programs to ensure transparent management of the federal government’s Bitcoin holdings. The bill contemplates offsetting the purchase requirements for building this reserve by utilizing certain resources of the Federal Reserve System, effectively envisioning a world in which Bitcoin becomes, at least at the margin, part of the broader public sector balance sheet landscape. While such proposals remain at the discussion stage and face significant political and technical hurdles, they illustrate how far the crypto conversation has moved from the fringes toward mainstream policy debate.

From a Fed perspective, holding Bitcoin on its balance sheet would be a dramatic departure from current practice, which limits holdings largely to U.S. government securities and certain other highly liquid, creditworthy assets aligned with its mandate. Introducing a volatile, non‑sovereign asset like Bitcoin would raise complex questions about monetary policy transmission, financial stability, and market functioning. For example, large‑scale official purchases could influence Bitcoin’s price and liquidity, potentially undermining market neutrality. The valuation volatility of Bitcoin holdings could in turn affect the Fed’s capital position and public perceptions of its financial strength, even though central banks are not profit‑maximizing entities in the same way as private firms.

Even if such a Strategic Bitcoin Reserve were established at the Treasury rather than the Fed, drawing on Fed resources to fund purchases would blur institutional boundaries. It would also implicitly recognize Bitcoin as a kind of strategic reserve asset, analogous to gold or foreign exchange reserves, a step that would have far‑reaching implications for how both markets and other central banks view digital assets. At present, there is no indication that the Fed itself is moving in this direction; the proposal reflects legislative experimentation rather than central bank policy. Nonetheless, crypto participants should pay attention to these debates, as they signal how the role of Bitcoin in the global financial system continues to evolve.

How Bitcoin challenges and complements the Fed’s role

Bitcoin’s existence as a non‑sovereign, programmable, and globally accessible form of value challenges some aspects of the traditional monetary system while complementing others. It challenges central banks conceptually by offering an alternative model of money creation and governance, one in which supply is fixed and policy cannot respond flexibly to economic shocks. It challenges them practically by enabling cross‑border value transfer that can bypass certain capital controls and by providing a parallel asset in which investors can park wealth outside of the fiat system. It also challenges the informational monopoly that central banks have historically enjoyed about money and payments by enabling transparent, on‑chain data about transactions and balances, even if identities remain pseudonymous.

At the same time, Bitcoin and the broader crypto ecosystem have highlighted unmet demands in the existing system—such as 24/7 settlement, programmable money, and global interoperability—that have spurred central banks, including the Fed, to accelerate innovation efforts like FedNow and explorations of CBDC. The presence of a credible outside option in the form of crypto may increase the incentive for central banks to maintain low and stable inflation and to modernize payment infrastructure, lest they cede ground to alternative systems. Moreover, Bitcoin’s volatility and the occasional failures of centralized intermediaries have reinforced the importance of prudential regulation, custody standards, and lender‑of‑last‑resort facilities, roles that the Fed continues to perform in the dollar system.

For crypto builders and investors, the key point is that Bitcoin and the Fed are likely to coexist rather than one simply replacing the other. The Fed will continue to manage the dollar, which remains the dominant unit of account and medium of exchange in the United States and much of the world, while Bitcoin and other digital assets provide alternative stores of value, speculative opportunities, and programmable financial primitives. The interaction between these spheres—through price correlations, regulatory decisions, and technological cross‑fertilization—will shape the future landscape of money and finance.

Governance, Personnel, And Conflicts Of Interest In A Crypto‑Aware Fed

How the Board and FOMC make decisions

The Fed’s governance structure is central to how it sets policy toward both the macroeconomy and emerging issues like crypto. The Board of Governors consists of up to seven members appointed by the President and confirmed by the Senate, each serving staggered 14‑year terms, with the Chair and Vice Chair serving renewable four‑year terms in those roles. The Federal Open Market Committee, which sets monetary policy, comprises the members of the Board plus five of the twelve Reserve Bank presidents, one of whom is always the president of the New York Fed, reflecting that bank’s role in implementing open market operations. Decisions are typically made by majority vote, and individual members may dissent, as when one FOMC participant recently preferred a quarter‑point rate cut while the majority opted to hold the target range steady.

This committee structure means that no single individual, not even the Chair, can unilaterally dictate policy. Nonetheless, the Chair sets the agenda, shapes consensus, and serves as the public face of the institution, including in testimony before Congress and communication with markets. The backgrounds, views, and personal portfolios of Board members and Reserve Bank presidents can thus subtly influence the Fed’s stance toward issues like crypto, AI, and fintech. For instance, when a chair nominee or sitting chair’s financial disclosure reveals early‑stage investments in crypto infrastructure or AI companies, it raises questions about potential conflicts of interest and about how personally familiar the leadership may be with the technology they are regulating.

Ethics rules and recusal requirements exist to mitigate conflicts. Fed officials are generally restricted in their trading and investment activities, particularly in assets that could be affected by their policy decisions, and they must periodically disclose holdings and transactions. Nonetheless, crypto is a relatively new asset class, and its intersection with other investments, such as venture funds that hold a mix of fintech, AI, and token projects, can complicate conflict assessments. As the Fed becomes more deeply engaged with crypto‑related regulatory issues, including stablecoin oversight and payment access for digital asset firms, managing real and perceived conflicts will be important for maintaining public trust and institutional legitimacy.

Leadership views on crypto, AI, and innovation

Beyond formal conflicts, the personal views of Fed leaders on innovation shape the tone and content of policy. Some governors and Reserve Bank presidents have expressed cautious openness to digital assets and fintech, emphasizing the need to harness potential efficiency gains while safeguarding stability and consumer protection. Others have been more skeptical, highlighting volatility, fraud, and risks to the banking system. Speeches by figures like Governor Waller illustrate this tension: he has been hawkish on inflation and wary of premature easing, while also advocating for payment account reforms to support innovators, including digital asset firms, that currently rely on intermediaries to access Fed services.

The Trump administration’s emphasis on integrating fintech innovation into regulatory infrastructure, as evidenced by its executive order directing the Fed and other agencies to evaluate payment access for non‑bank entities, has put leadership views under additional scrutiny. Supporters of the order argue that it pushes a historically cautious central bank to more fully engage with technological changes that are reshaping finance, from AI‑driven credit models to tokenized assets. Critics fear that political pressure to promote innovation could erode prudential standards or lead the Fed into roles better suited to the private sector. The balance struck by current and future chairs, governors, and Reserve Bank presidents between openness to innovation and adherence to traditional central banking conservatism will significantly influence the trajectory of crypto regulation and payment system modernization.

Transparency, data, and supervising decentralized technologies

Supervising decentralized technologies poses unique challenges for an institution designed around supervising centralized intermediaries. Stablecoins, for example, rely on complex arrangements involving issuers, custodians, governance bodies, and third‑party service providers, many of which may be located in different jurisdictions or structured as DAOs rather than corporations. The SEC’s stablecoin regulatory framework notes that these arrangements require robust oversight of third‑party service providers, including due diligence on their operations and risk management. Similarly, the Fed’s proposed CIP requirements for stablecoin issuers reflect a recognition that customer identification and transaction monitoring must adapt to token‑based, pseudonymous systems.

One recurring issue in this context is data. The Fed and other regulators have historically relied on standardized regulatory reporting from banks and other supervised institutions, supplemented by exam findings and market data, to monitor risks. In the stablecoin and DeFi space, much of the relevant data is on‑chain, publicly accessible but often fragmented, requiring specialized analytics to interpret. At the same time, critical off‑chain data—such as the composition of reserves backing stablecoins, the terms of service governing redemptions, and the operational resilience of key infrastructure providers—may be opaque or subject to limited disclosure. Recent commentary has highlighted the Fed’s reliance on third‑party data for assessing stablecoin risks, underscoring gaps that could impede effective oversight.

Closing these gaps will likely require a combination of regulatory reporting, technical capacity building, and collaboration with other agencies and the private sector. Regulators may require stablecoin issuers and other crypto intermediaries to provide standardized data on reserves, flows, and risk exposures, while also investing in their own on‑chain analytics capabilities. They may also need to clarify how existing frameworks like the Bank Secrecy Act apply to DeFi protocols and non‑custodial wallets, areas where the traditional distinction between “financial institution” and “technology provider” blurs. For the Fed, which is not the lead AML regulator but plays a major role in supervising banks’ compliance, aligning expectations across agencies like FinCEN and the SEC will be key.

The Fed has issued cease-and-desist orders against multiple crypto-adjacent banks and can effectively de-bank a digital asset firm through supervisory action without any new legislation.

Master account access to Fedwire is a single chokepoint controlled by the Fed; denial bars a firm from US dollar settlement, as Custodia's years-long legal fight over its application illustrates.

Fed rate signals directly move crypto prices — BTC dropped 7% below $90K on one stronger-than-expected jobs report, and $454 million in weekly digital asset fund outflows materialized when a March rate cut appeared unlikely.

- GovernanceMedium

Political turnover — Cook's firing, Barr's Vice Chair exit, and Miran's narrow confirmation — creates policy uncertainty precisely when the Fed is actively rewriting its crypto supervisory guidance.

- LiquidityMedium

Rate-path uncertainty translates directly into digital asset fund flow reversals, with a single shift in Fed cut expectations capable of wiping out months of year-to-date inflows in under a week.

The Fed's dependence on third-party data leaves stablecoin oversight structurally incomplete, while a congressional CBDC ban through 2030 has closed off the Fed's digital dollar path regardless of its own preferences.

What Crypto Participants Need To Know About The Fed In Practice

How Fed decisions filter into crypto prices and liquidity

For traders and investors, the most immediate way the Fed affects crypto is through its influence on dollar liquidity and risk sentiment. Changes in the federal funds target range, adjustments to balance sheet policy, and shifts in forward guidance all feed into borrowing costs, asset allocation decisions, and the pricing of risk. When the Fed signals a prolonged period of restrictive policy to bring inflation back to its 2 percent goal, markets tend to demand higher risk premiums on volatile assets, and leverage becomes more expensive. Crypto prices often fall in such environments, particularly for smaller tokens and highly leveraged strategies, even if Bitcoin sometimes benefits from long‑term narratives about fiat debasement.

Conversely, when the Fed approaches the end of a tightening cycle and begins to hint at future easing, liquidity expectations can improve, supporting rallies in risk assets that often include crypto. Traders should pay attention not only to headline rate decisions but also to the language in FOMC statements, the Summary of Economic Projections, and speeches by key policymakers like the Chair, the Vice Chair, and influential governors such as Waller. These communications shape the anticipated path of policy, which is what markets ultimately price. Reading Fed signals in conjunction with macro data releases—such as inflation, employment, and growth figures—can provide a framework for anticipating shifts in the macro regime that are likely to impact digital asset markets.

How Fed regulation shapes on‑ and off‑ramps, stablecoins, and DeFi

Beyond macro conditions, the Fed’s supervisory and regulatory activities shape the infrastructure through which crypto interacts with the dollar system. Banks’ willingness to provide accounts, payment services, and credit to exchanges, stablecoin issuers, and fintech platforms depends heavily on their assessment of regulatory expectations, including from the Fed. When guidance is perceived as hostile or uncertain, banks may “de‑risk” by exiting relationships, making it harder for crypto firms to maintain on‑ and off‑ramps. When the Fed clarifies that crypto activities can be pursued under normal supervisory processes, banks may feel more comfortable engaging, provided they implement robust risk controls.

Stablecoins are a particularly vivid example. The Fed’s coordination with FinCEN on implementing the GENIUS Act, and its own proposals to require payment stablecoin issuers to maintain effective CIPs, will determine how easily stablecoin arrangements can interface with regulated banks and payment systems. Issuers that accept bank‑like CIP and AML obligations may gain smoother access and legitimacy, while those that resist could find their tokens increasingly fenced off from the regulated perimeter. DeFi protocols that integrate regulated stablecoins may in turn become indirect subjects of supervisory expectations, as banks and stablecoin issuers seek assurances about how their tokens are used in on‑chain environments.

Payment access is the other critical dimension. As debates over master accounts, payment accounts, and skinny Fed access frameworks evolve, the set of institutions that can directly settle in central bank money may expand to include crypto‑specialized entities under certain conditions. If that happens, exchanges, custodians, and stablecoin issuers that secure such access could gain a competitive advantage in speed, cost, and reliability over those that remain reliant on correspondent banking. DeFi protocols themselves will remain outside the Fed’s direct reach, but their connective tissue—the fiat gateways, custodial bridges, and stablecoin issuers that link them to the dollar system—will increasingly be shaped by Fed‑influenced regulation.

How to read Fed communications as a crypto market participant

Given this multifaceted impact, crypto participants benefit from developing a disciplined approach to reading Fed communications. On the monetary policy side, FOMC statements and implementation notes provide the official record of decisions on the target range for the federal funds rate, balance sheet policy, and the Committee’s assessment of economic conditions. The Fed’s educational materials on monetary policy tools can help interpret these decisions in terms of how they influence the money supply, credit conditions, and inflation. Speeches by individual FOMC members, particularly those like Governor Waller whose remarks often move markets, offer insights into internal debates and potential shifts in consensus.

On the regulatory and supervisory side, Fed press releases announcing new proposals, such as the stablecoin CIP requirements, and policy changes, such as the withdrawal of earlier crypto‑specific supervisory letters, are equally important. These documents often open public comment periods, during which industry participants can provide input and raise concerns. For those building or investing in crypto infrastructure that interfaces with banks or payment systems, engaging with these processes, either directly or through trade associations, can influence the final shape of rules and expectations. Tracking related communications from FinCEN, the SEC, and other agencies is also crucial, given the overlapping jurisdictions and the Fed’s role in interagency coordination.

Finally, crypto participants should remember that Fed policy changes rarely occur in isolation. Congressional actions, such as the CBDC moratorium, and executive actions, such as Trump’s fintech innovation order, constrain and shape what the Fed can do. Market narratives often oversimplify this ecosystem into a single omnipotent actor, but in reality, the Fed operates within a web of political, legal, and institutional constraints. Understanding that web improves one’s ability to anticipate both the direction and the limits of future developments affecting crypto.

Conclusion

The Federal Reserve occupies a unique position in the U.S. and global financial system, combining roles as monetary authority, bank supervisor, payment system operator, and guardian of financial stability. For the crypto ecosystem, this means that the Fed is not just a background macro actor setting interest rates; it is an institution whose decisions on regulation, payment access, and innovation policy directly shape the environment in which digital assets develop. From the vantage point of a crypto news audience, understanding the Fed is no longer optional background knowledge but a core part of making sense of markets, regulation, and strategic opportunities.

On the macro side, the Fed’s management of the federal funds rate, its balance sheet, and its forward guidance influences dollar liquidity, risk appetite, and asset valuations, with clear spillovers into Bitcoin, stablecoins, and DeFi. Tightening cycles tend to pressure speculative crypto activity by raising funding costs and increasing competition from safe yields, while easing cycles can support rallies by lowering the opportunity cost of holding volatile assets. On the regulatory side, the Fed’s supervision of banks and its coordination with agencies like FinCEN and the SEC determine how crypto‑related activities can be integrated into the regulated financial system, particularly for stablecoins and payment services. Its decisions to withdraw earlier crypto‑specific supervisory letters, propose bank‑style CIP requirements for stablecoin issuers, and explore new payment account models for innovators all point toward a more systematic, risk‑based approach to digital assets.

Payment access and infrastructure form the third pillar of the Fed–crypto relationship. Through services like Fedwire, ACH, and FedNow, the Fed defines the rails on which dollar transactions move, and access to master accounts is the key to using those rails directly. Debates over who should have master accounts, whether skinny payment accounts should be created for non‑traditional institutions, and how bank‑issued stablecoins should be treated reflect deeper questions about the boundaries of the banking system and the role of non‑bank innovators. At the same time, Congress’s decision to ban a Fed‑issued CBDC through 2030 ensures that, for now, private stablecoins and tokenized deposits will remain the primary vehicles for blockchain‑based dollars, subject to increasing regulation.

Finally, Bitcoin and other non‑sovereign digital assets present both a conceptual challenge and a source of impetus for central bank innovation. The Fed’s own research acknowledges Bitcoin’s monetary properties while emphasizing its volatility and speculative character, and proposals like a Strategic Bitcoin Reserve underscore how deeply the asset has penetrated policy discussions. Yet the Fed’s core mandate remains focused on the dollar, and its engagement with crypto is framed by concerns about stability, integrity, and the efficient operation of payment systems. For crypto participants, the task is to navigate this evolving landscape, recognizing both the constraints and the opportunities that a crypto‑aware Fed creates.

Outlook

Looking ahead, the relationship between the Federal Reserve and the crypto ecosystem is likely to become more institutionalized and less ad hoc. On the monetary policy front, the Fed will continue to grapple with balancing inflation control and employment, with interest‑rate decisions and forward guidance driving cycles in dollar liquidity that will influence crypto prices and funding conditions. As digital assets become more integrated into portfolios and financial intermediaries, the Fed’s monitoring of crypto markets will likely deepen, not because it seeks to control them directly, but because they are increasingly relevant to financial conditions and stability assessments.

On the regulatory and infrastructure side, several paths seem probable. First, the Fed and its fellow agencies are poised to finalize rules that treat key stablecoin issuers as financial institutions subject to robust CIP and AML obligations, narrowing the regulatory gray zone in which many dollar tokens have operated. Second, some version of skinny payment accounts or expanded access to Fed payment rails for non‑traditional entities, including crypto‑specialized firms, is likely to emerge from the current policy process, although the details of eligibility, oversight, and privileges will be critical. Third, FedNow and other instant payment systems will continue to roll out, reshaping expectations around 24/7 dollar settlement and interacting in complex ways with stablecoins and tokenized deposits. Meanwhile, the congressional moratorium on a Fed CBDC through 2030 ensures that private and bank‑issued digital dollars will remain at the forefront of blockchain‑based payments in the United States, even as research on CBDC quietly continues.